N O V E M B E R 2 0 0 7

D I S T R E S S E D D E B T T R A D I N G

ST

RI

CT

LY

P

RI

VA

TE

A

ND

C

ON

FI

DE

NT

IA

L

John Abate

Managing Director and Head of Distressed Trading & Loan Trading

John Abate has 19 years of distressed portfolio management experience. John began his career as a

High Yield analyst with PPM America and moved to Citibank in 1994 to become Head of Distressed

Research on the Loan Trading Desk. In 1996, John became Head of Distressed Trading at Citibank.

John moved to Lehman Brothers Distressed Trading business in 1998, before joining JPMorgan in

2000 as Head of Distressed Loan Trading. In 2005 John became Head of all Distressed Trading and

Distressed Loan Trading at JPMorgan, his current position. John is a CFA Charterholder and holds

an MBA from the University of Florida; and a BA from James Madison University. John is married

to Kimberly Toor Abate and has 3 children, Drew (11), Abby (9), and AJ (7)

DI

ST

RE

SS

ED

D

EB

T

TR

AD

IN

G

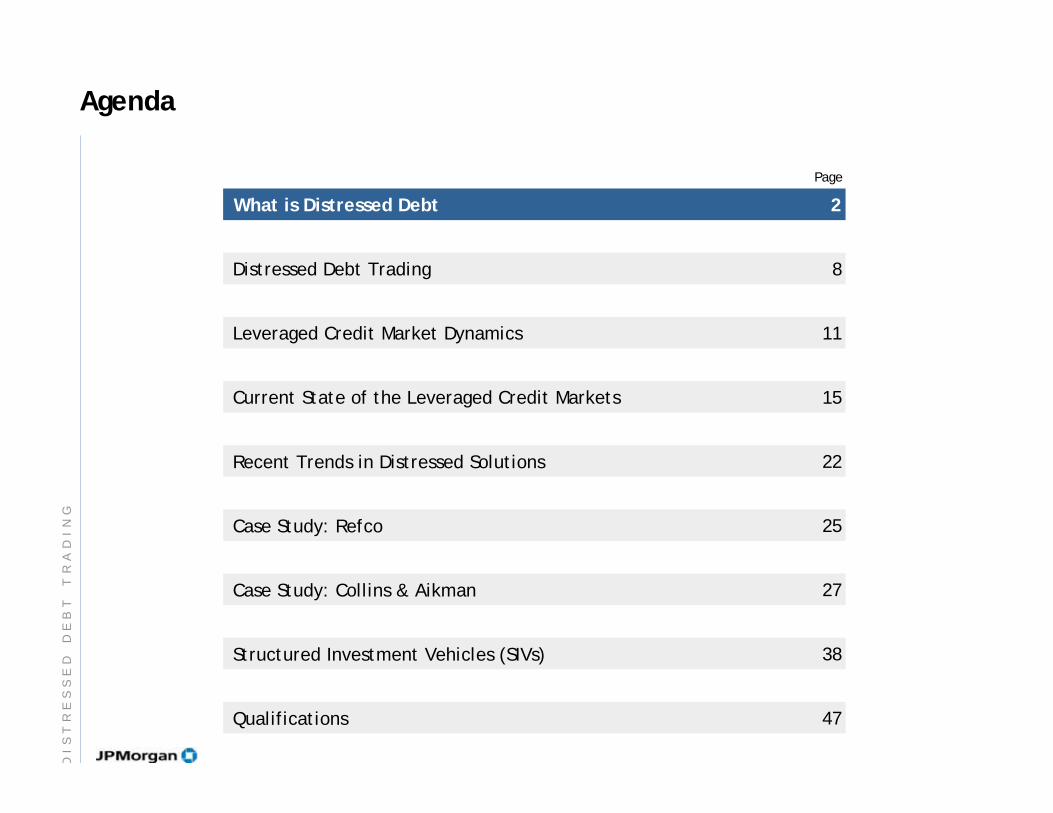

Agenda

Page

Qualifications

Structured Investment Vehicles (SIVs)

Case Study: Collins & Aikman

Case Study: Refco

Recent Trends in Distressed Solutions

Current State of the Leveraged Credit Markets

Leveraged Credit Market Dynamics

Distressed Debt Trading

What is Distressed Debt 2

8

11

15

22

25

27

38

47

DI

ST

RE

SS

ED

D

EB

T

TR

AD

IN

G

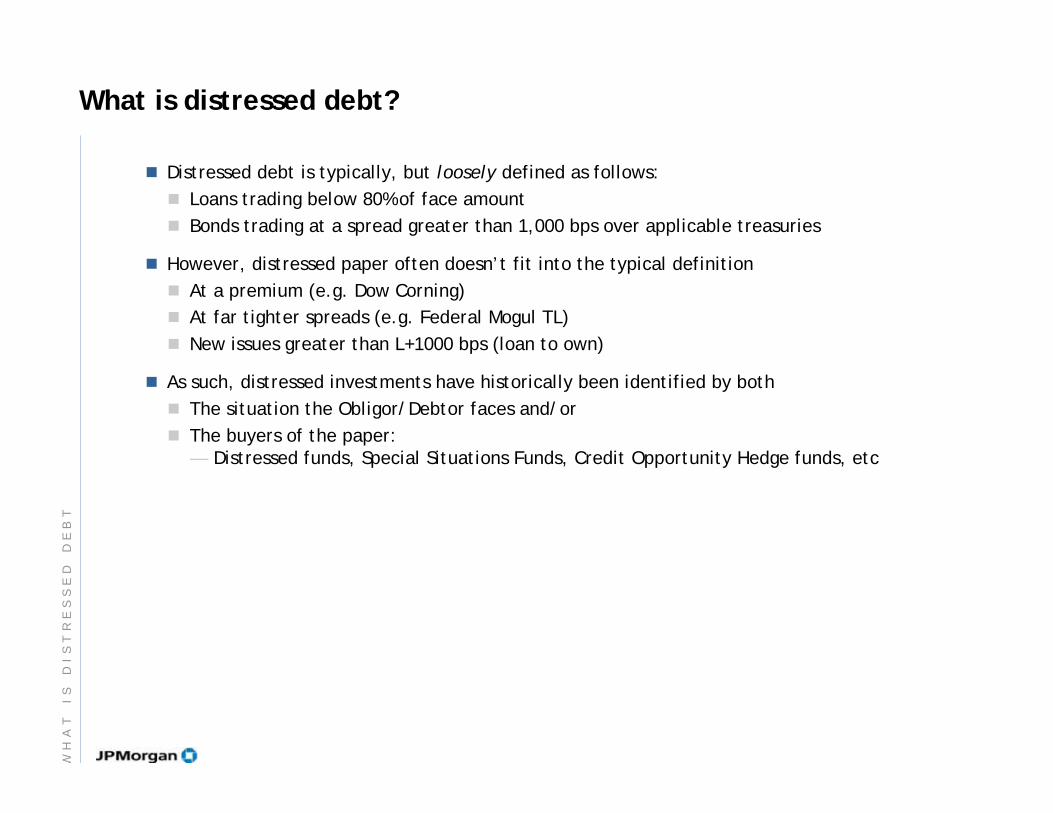

What is distressed debt?

Distressed debt is typically, but loosely defined as follows:

Loans trading below 80% of face amount

Bonds trading at a spread greater than 1,000 bps over applicable treasuries

However, distressed paper often doesn’t fit into the typical definition

At a premium (e.g. Dow Corning)

At far tighter spreads (e.g. Federal Mogul TL)

New issues greater than L+1000 bps (loan to own)

As such, distressed investments have historically been identified by both

The situation the Obligor/Debtor faces and/or

The buyers of the paper:— Distressed funds, Special Situations Funds, Credit Opportunity Hedge funds, etc

WH

AT

I

S

DI

ST

RE

SS

ED

D

EB

T

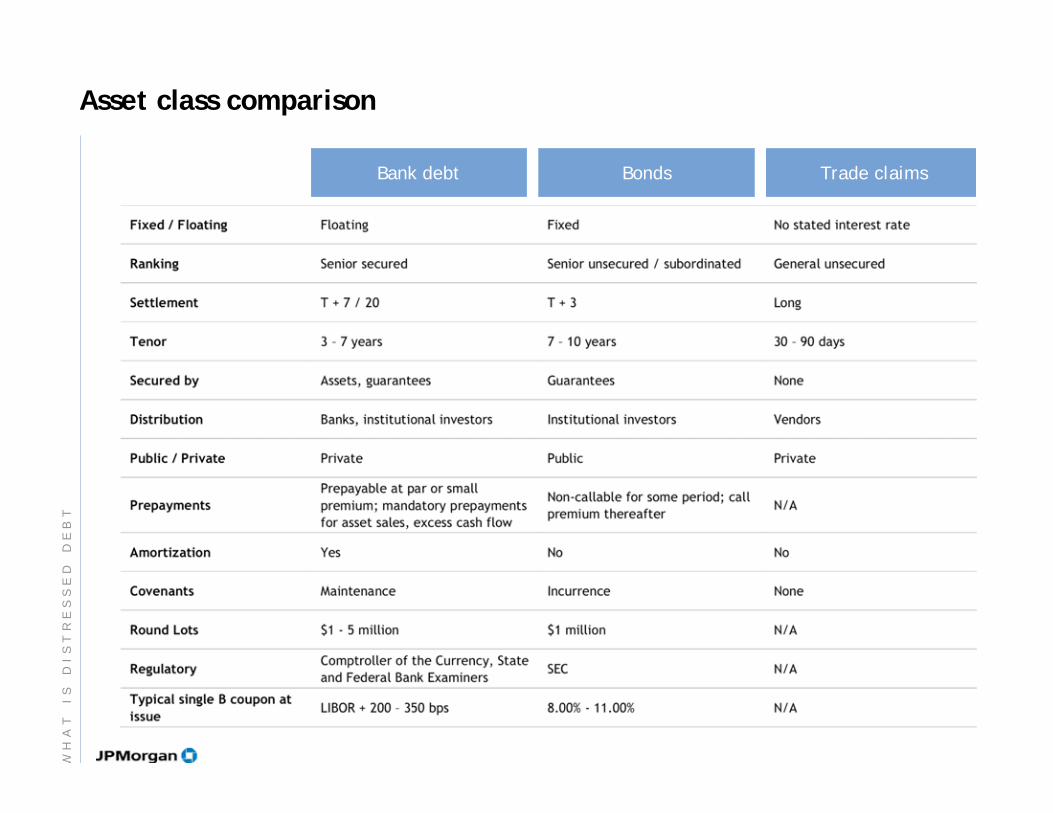

Asset class comparison

Bank debt Bonds Trade claims

WH

AT

I

S

DI

ST

RE

SS

ED

D

EB

T

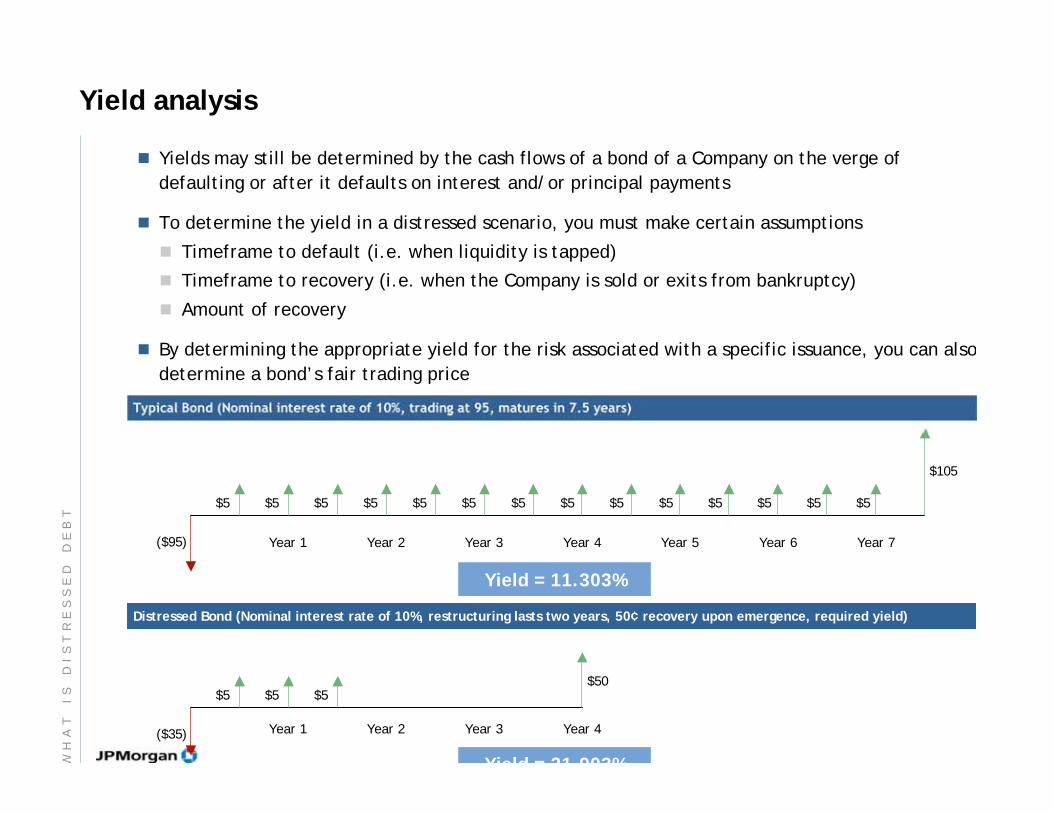

Yield analysis

Yields may still be determined by the cash flows of a bond of a Company on the verge of

defaulting or after it defaults on interest and/or principal payments

To determine the yield in a distressed scenario, you must make certain assumptions

Timeframe to default (i.e. when liquidity is tapped)

Timeframe to recovery (i.e. when the Company is sold or exits from bankruptcy)

Amount of recovery

By determining the appropriate yield for the risk associated with a specific issuance, you can also

determine a bond’s fair trading price

($95)

$5 $5 $5 $5 $5 $5 $5 $5 $5 $5 $5 $5 $5 $5

$105

Yield = 11.303%

($35)

$5 $5 $5$50

Typical Bond (Nominal interest rate of 10%, trading at 95, matures in 7.5 years)

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7

Year 1 Year 2 Year 3 Year 4

Distressed Bond (Nominal interest rate of 10%, restructuring lasts two years, 50¢ recovery upon emergence, required yield)

Yield = 21 903%WH

AT

I

S

DI

ST

RE

SS

ED

D

EB

T

0

10

20

30

40

50

60

70

80

90

100

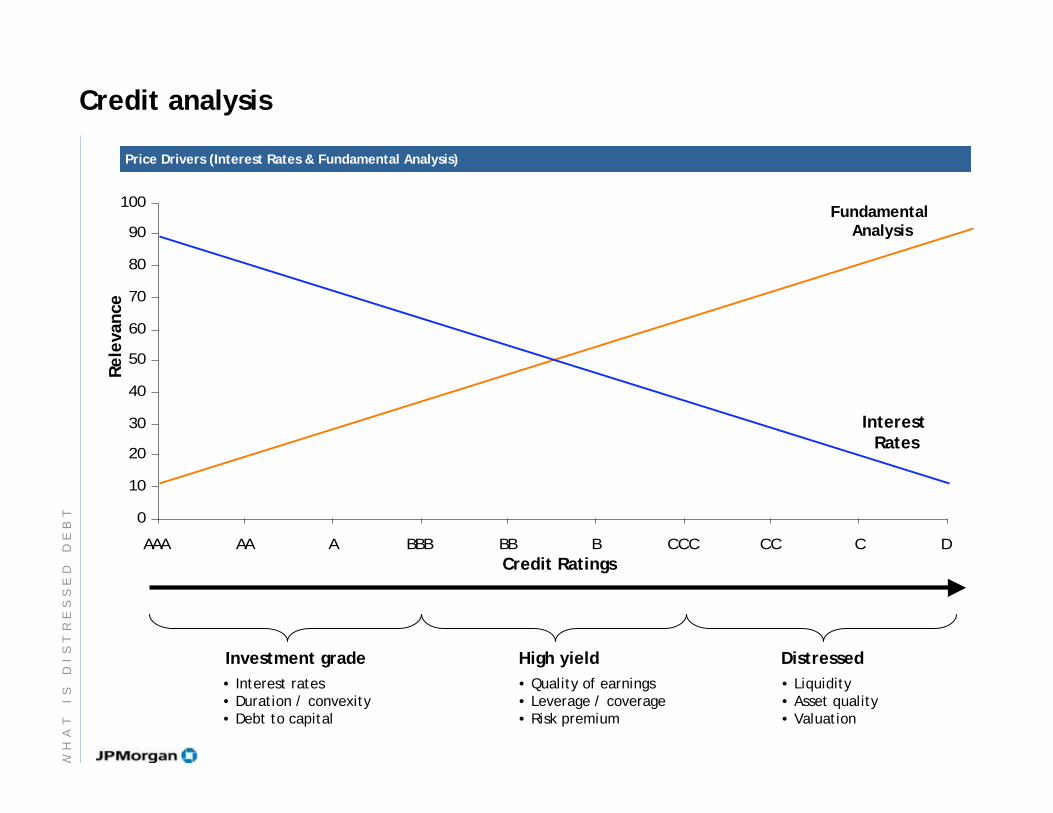

AAA AA A BBB BB B CCC CC C D

Interest Rates

Rele

vance

Credit Ratings

• Interest rates• Duration / convexity • Debt to capital

• Quality of earnings• Leverage / coverage• Risk premium

• Liquidity• Asset quality• Valuation

Investment grade High yield Distressed

Price Drivers (Interest Rates & Fundamental Analysis)

Credit analysis

Fundamental Analysis

WH

AT

I

S

DI

ST

RE

SS

ED

D

EB

T

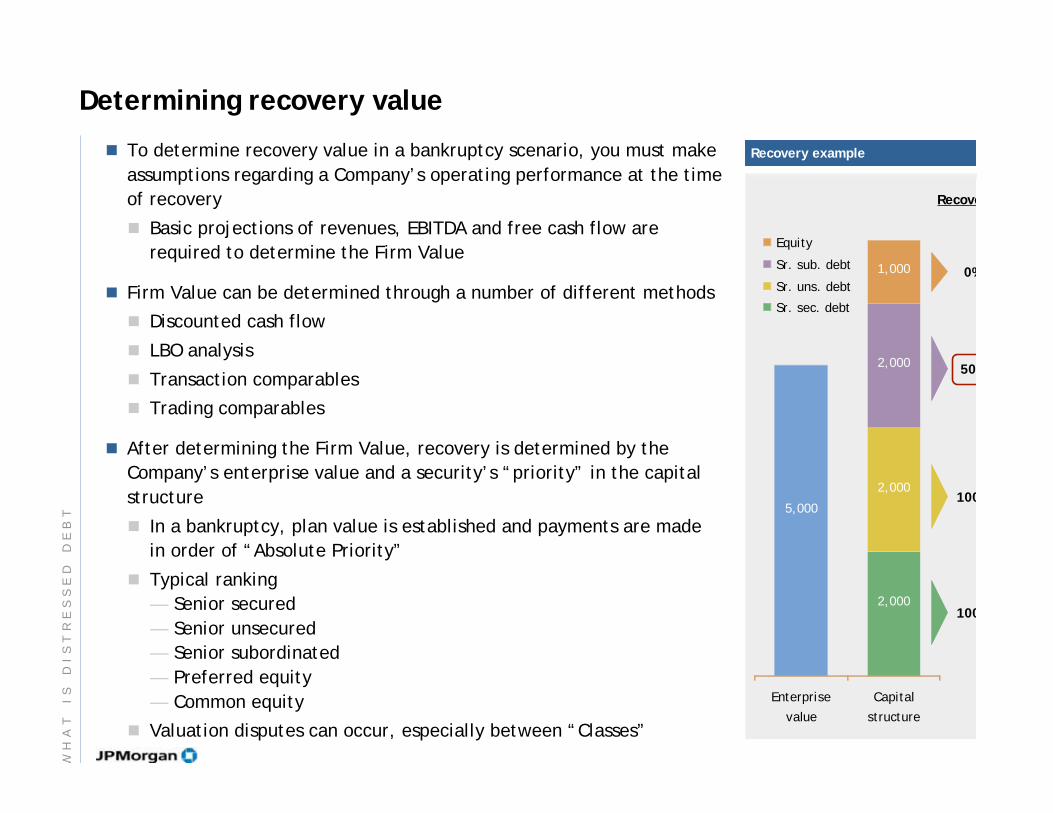

Determining recovery value

To determine recovery value in a bankruptcy scenario, you must make

assumptions regarding a Company’s operating performance at the time

of recovery

Basic projections of revenues, EBITDA and free cash flow are

required to determine the Firm Value

Firm Value can be determined through a number of different methods

Discounted cash flow

LBO analysis

Transaction comparables

Trading comparables

After determining the Firm Value, recovery is determined by the

Company’s enterprise value and a security’s “priority” in the capital

structure

In a bankruptcy, plan value is established and payments are made

in order of “Absolute Priority”

Typical ranking

— Senior secured

— Senior unsecured

— Senior subordinated

— Preferred equity

— Common equity

Valuation disputes can occur, especially between “Classes”

5,000

2,000

2,000

2,000

1,000

Enterprise

value

Capital

structure

Equity

Sr. sub. debt

Sr. uns. debt

Sr. sec. debt

Recove

100

100

50

0%

Recovery example

WH

AT

I

S

DI

ST

RE

SS

ED

D

EB

T

Agenda

Page

Qualifications

Structured Investment Vehicles (SIVs)

Case Study: Collins & Aikman

Case Study: Refco

Recent Trends in Distressed Solutions

Current State of the Leveraged Credit Markets

Leveraged Credit Market Dynamics

Distressed Debt Trading

What is Distressed Debt 2

8

11

15

22

25

27

38

47

DI

ST

RE

SS

ED

D

EB

T

TR

AD

IN

G

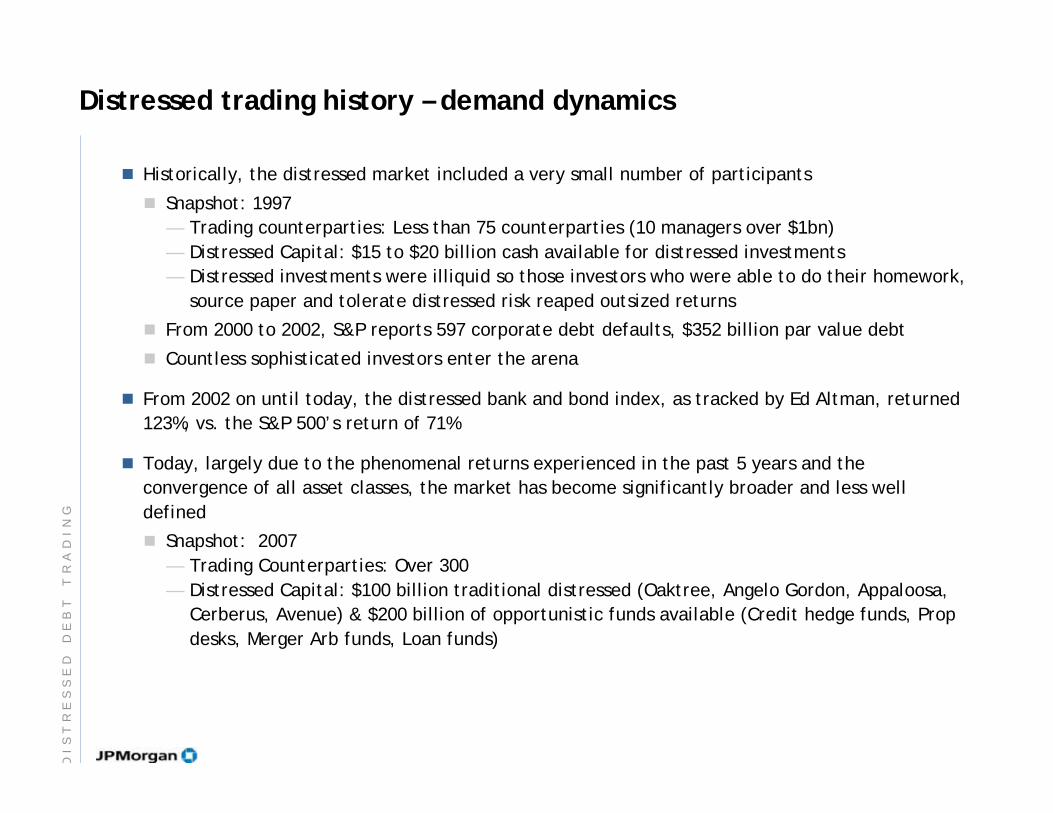

Distressed trading history – demand dynamics

Historically, the distressed market included a very small number of participants

Snapshot: 1997

— Trading counterparties: Less than 75 counterparties (10 managers over $1bn)

— Distressed Capital: $15 to $20 billion cash available for distressed investments

— Distressed investments were illiquid so those investors who were able to do their homework,

source paper and tolerate distressed risk reaped outsized returns

From 2000 to 2002, S&P reports 597 corporate debt defaults, $352 billion par value debt

Countless sophisticated investors enter the arena

From 2002 on until today, the distressed bank and bond index, as tracked by Ed Altman, returned

123%, vs. the S&P 500’s return of 71%

Today, largely due to the phenomenal returns experienced in the past 5 years and the

convergence of all asset classes, the market has become significantly broader and less well

defined

Snapshot: 2007

— Trading Counterparties: Over 300

— Distressed Capital: $100 billion traditional distressed (Oaktree, Angelo Gordon, Appaloosa,

Cerberus, Avenue) & $200 billion of opportunistic funds available (Credit hedge funds, Prop

desks, Merger Arb funds, Loan funds)

DI

ST

RE

SS

ED

D

EB

T

TR

AD

IN

G

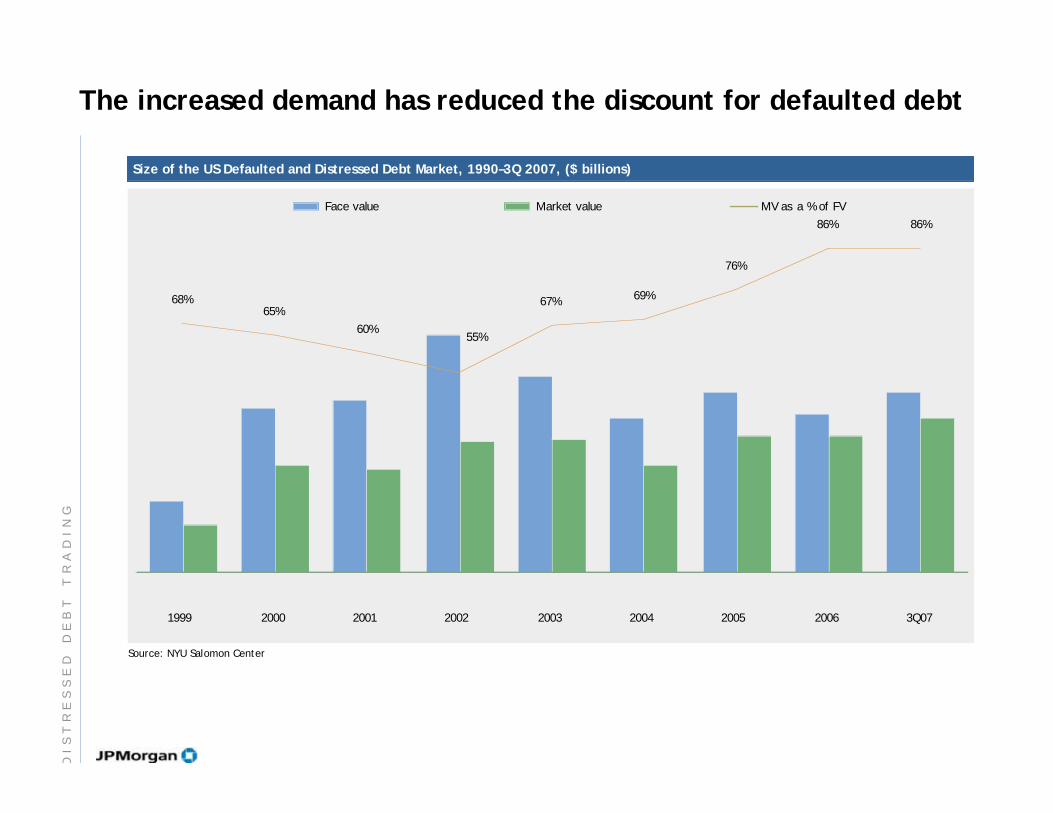

Source: NYU Salomon Center

Size of the US Defaulted and Distressed Debt Market, 1990–3Q 2007, ($ billions)

The increased demand has reduced the discount for defaulted debt

68%65%

60%

67%69%

76%

86% 86%

55%

1999 2000 2001 2002 2003 2004 2005 2006 3Q07

Face value Market value MV as a % of FV

DI

ST

RE

SS

ED

D

EB

T

TR

AD

IN

G

Agenda

Page

Qualifications

Structured Investment Vehicles (SIVs)

Case Study: Collins & Aikman

Case Study: Refco

Recent Trends in Distressed Solutions

Current State of the Leveraged Credit Markets

Leveraged Credit Market Dynamics

Distressed Debt Trading

What is Distressed Debt 2

8

11

15

22

25

27

38

47

DI

ST

RE

SS

ED

D

EB

T

TR

AD

IN

G

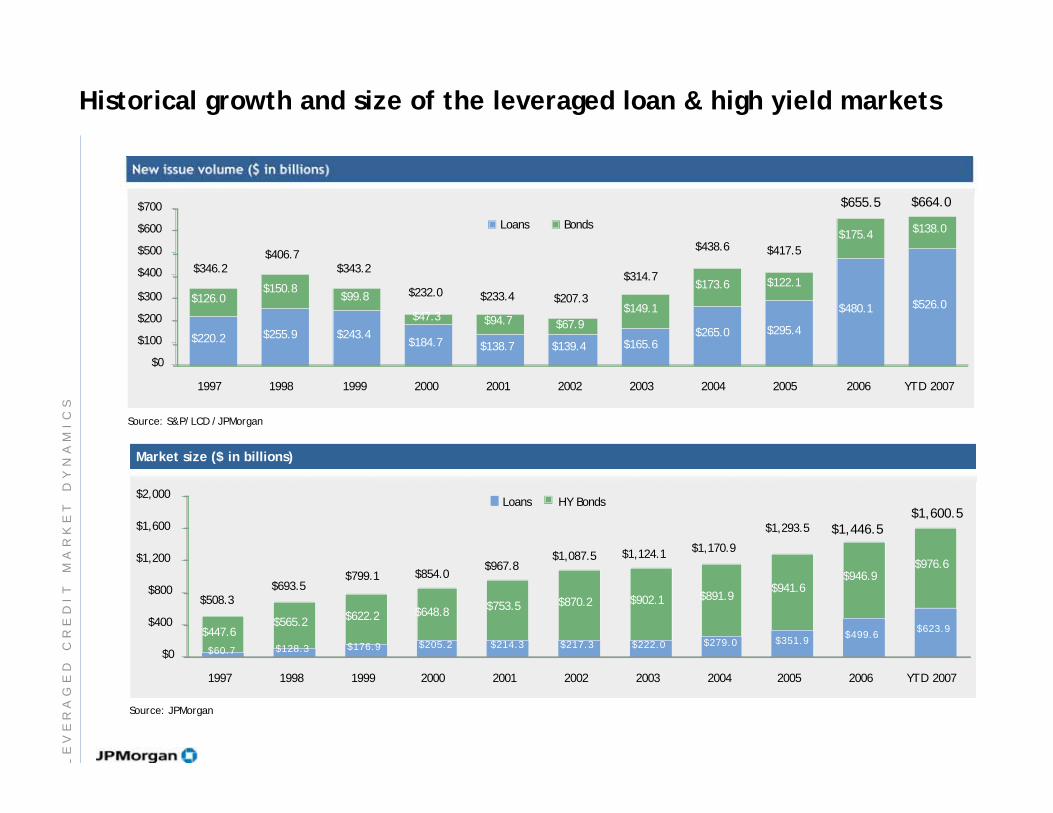

Historical growth and size of the leveraged loan & high yield markets

New issue volume ($ in billions)

Source: S&P/LCD /JPMorgan

$220.2 $255.9 $243.4$184.7 $138.7 $139.4 $165.6

$265.0 $295.4

$480.1 $526.0$126.0

$150.8$99.8

$47.3 $94.7 $67.9

$149.1

$173.6 $122.1

$175.4$138.0

$417.5

$346.2

$406.7

$343.2

$232.0 $233.4 $207.3

$314.7

$438.6

$0

$100

$200

$300

$400

$500

$600

$700

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 YTD 2007

Loans Bonds

$655.5 $664.0

$60.7 $128.3 $176.9 $205.2 $214.3 $217.3 $222.0 $279.0 $351.9$499.6

$623.9$447.6$565.2

$622.2 $648.8$753.5 $870.2 $902.1 $891.9

$941.6$946.9

$976.6

$1,293.5

$1,124.1$1,087.5$967.8

$1,170.9

$854.0$799.1$693.5

$508.3

$0

$400

$800

$1,200

$1,600

$2,000

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 YTD 2007

Loans HY Bonds

Market size ($ in billions)

Source: JPMorgan

$1,446.5$1,600.5

LE

VE

RA

GE

D

CR

ED

IT

M

AR

KE

T

DY

NA

MI

CS

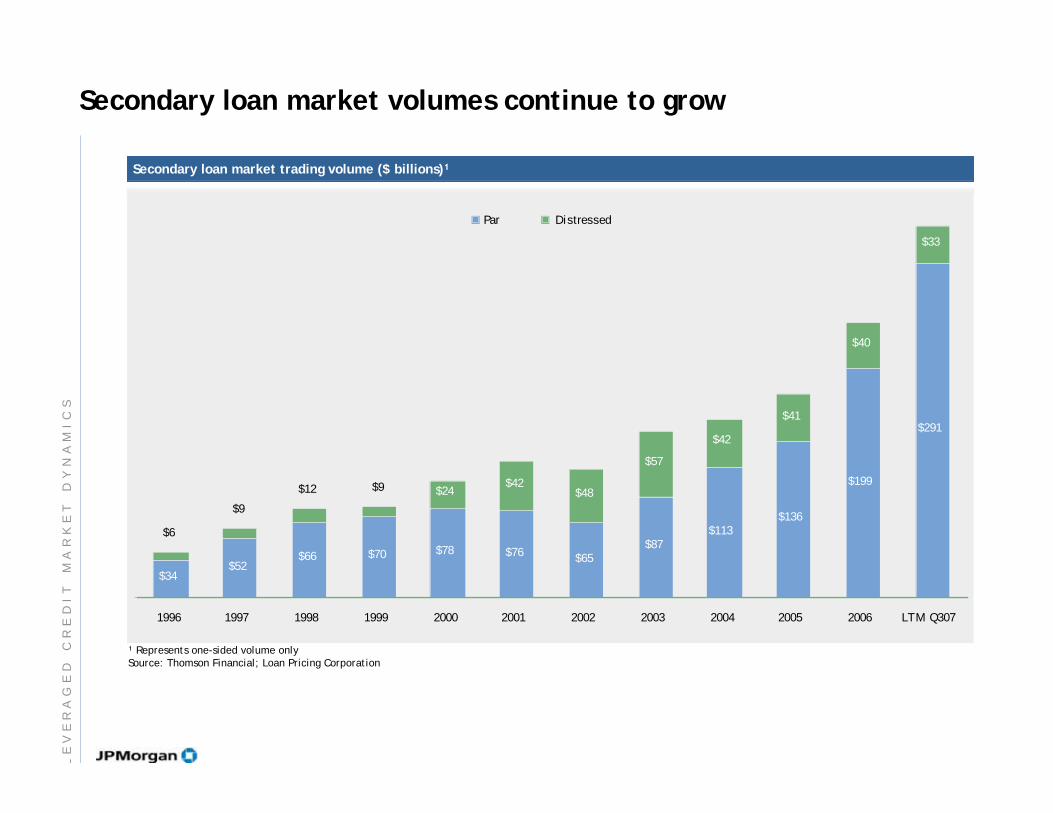

$34$52

$66 $70 $78 $76$65

$87$113

$136

$199

$291

$24$42

$48

$57

$42

$41

$40

$33

$9$12

$9

$6

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 LTM Q307

Par Distressed

Secondary loan market trading volume ($ billions)

Represents one-sided volume onlySource: Thomson Financial; Loan Pricing Corporation

Secondary loan market volumes continue to grow

LE

VE

RA

GE

D

CR

ED

IT

M

AR

KE

T

DY

NA

MI

CS

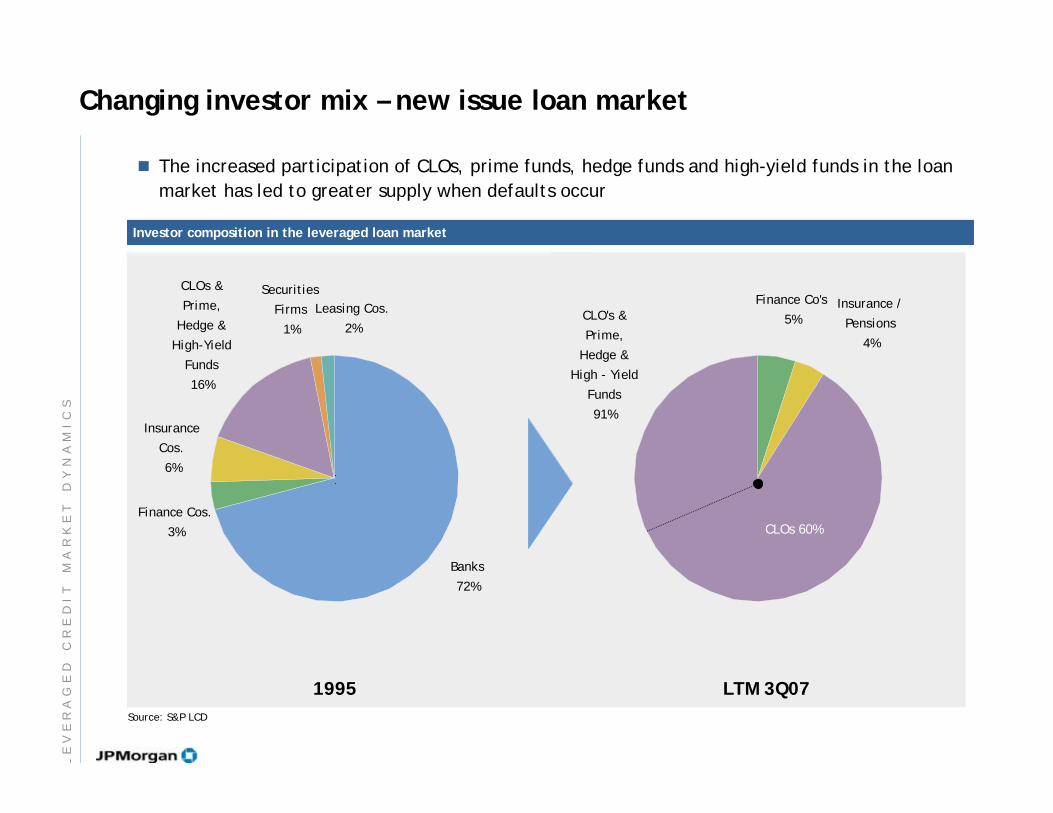

Insurance

Cos.

6%

Banks

72%

CLOs &

Prime,

Hedge &

High-Yield

Funds

16%

Securities

Firms

1%

Leasing Cos.

2%

Finance Cos.

3%

Source: S&P LCD

Investor composition in the leveraged loan market

1995

Changing investor mix – new issue loan market

The increased participation of CLOs, prime funds, hedge funds and high-yield funds in the loan

market has led to greater supply when defaults occur

Finance Co's

5%CLO's &

Prime,

Hedge &

High - Yield

Funds

91%

Insurance /

Pensions

4%

LTM 3Q07

CLOs 60%

LE

VE

RA

GE

D

CR

ED

IT

M

AR

KE

T

DY

NA

MI

CS

Agenda

Page

Qualifications

Structured Investment Vehicles (SIVs)

Case Study: Collins & Aikman

Case Study: Refco

Recent Trends in Distressed Solutions

Current State of the Leveraged Credit Markets

Leveraged Credit Market Dynamics

Distressed Debt Trading

What is Distressed Debt 2

8

11

15

22

25

27

38

47

DI

ST

RE

SS

ED

D

EB

T

TR

AD

IN

G

CU

RR

EN

T

ST

AT

E

OF

T

HE

L

EV

ER

AG

ED

C

RE

DI

T

MA

RK

ET

S

Confluence of recent events has distressed investors excited

Unprecedented new issue volumes over past 2 years, especially lower-rated new issuance

Supply and demand imbalance

Demand for leveraged loans diminished in the absence of CLO originations

Hung Bridge Loans

Cancellation of Warehouse Lines / TRS Programs

Opportunistic distressed funds expected to fill the void

Consumer led recession

Declining home prices and tightening lending standards

Deteriorating consumer sentiment

Stock market volatility

Structured Credit in the headlines

Overhang from subprime, ABCP, SIVs and structured credit continues to weigh on investorsentiment and risk appetites

Troubled industries in the headlines

Homebuilding, Mortgage Originators & Insurance Providers

CU

RR

EN

T

ST

AT

E

OF

T

HE

L

EV

ER

AG

ED

C

RE

DI

T

MA

RK

ET

S

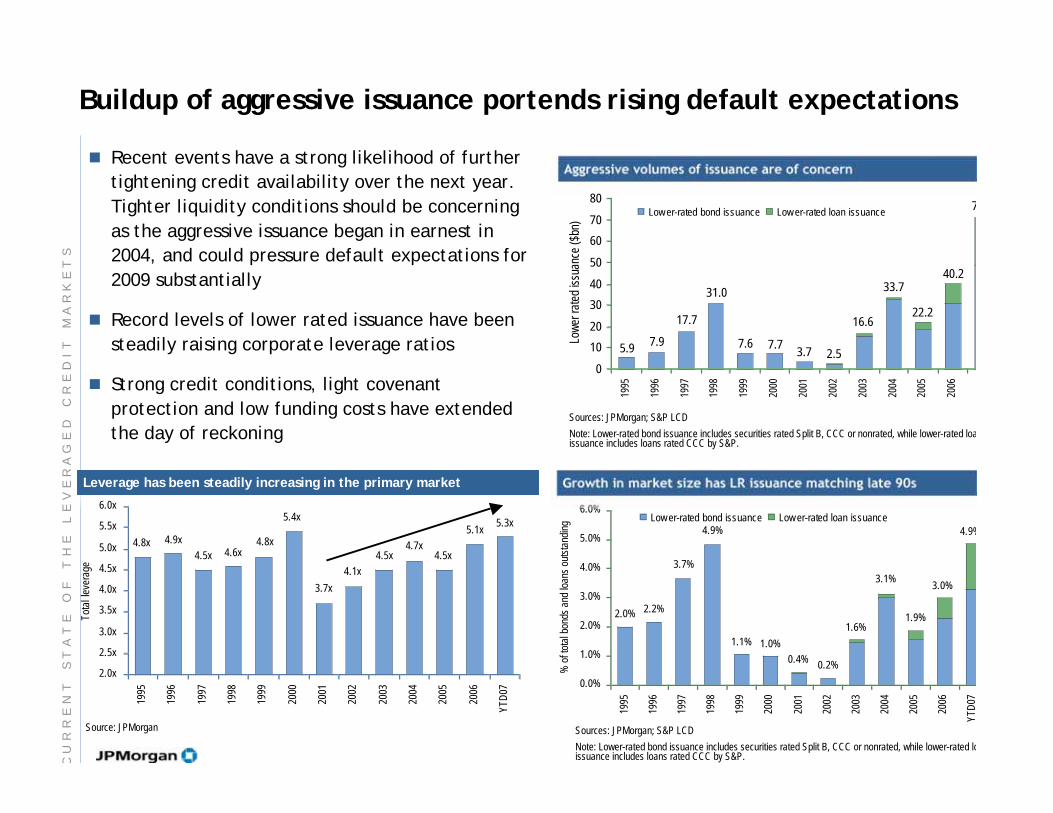

Buildup of aggressive issuance portends rising default expectations

Aggressive volumes of issuance are of concernRecent events have a strong likelihood of further

tightening credit availability over the next year.

Tighter liquidity conditions should be concerning

as the aggressive issuance began in earnest in

2004, and could pressure default expectations for

2009 substantially

Record levels of lower rated issuance have been

steadily raising corporate leverage ratios

Strong credit conditions, light covenant

protection and low funding costs have extended

the day of reckoning

4.9%

3.0%

1.9%

3.1%

1.6%

0.2%0.4%

1.0%1.1%

4.9%

3.7%

2.2%2.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

YT

D07

% o

f tot

al b

onds

and

loan

s ou

tsta

ndin

g Low er-rated bond issuance Low er-rated loan issuance

Growth in market size has LR issuance matching late 90s

Sources: JPMorgan; S&P LCD

Note: Lower-rated bond issuance includes securities rated Split B, CCC or nonrated, while lower-rated loissuance includes loans rated CCC by S&P.

Leverage has been steadily increasing in the primary market

Source: JPMorgan

5.3x5.1x

4.5x4.7x

4.5x

4.1x

3.7x

5.4x

4.8x4.6x4.5x

4.9x4.8x

2.0x

2.5x

3.0x

3.5x

4.0x

4.5x

5.0x

5.5x

6.0x

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

YT

D07

Tot

al l

ever

age

Sources: JPMorgan; S&P LCD

Note: Lower-rated bond issuance includes securities rated Split B, CCC or nonrated, while lower-rated loaissuance includes loans rated CCC by S&P.

7

40.2

22.2

33.7

16.6

2.53.77.77.6

31.0

17.7

7.95.9

0

10

20

30

40

50

60

70

80

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Low

er ra

ted

issu

ance

($bn

)

Low er-rated bond issuance Low er-rated loan issuance

CU

RR

EN

T

ST

AT

E

OF

T

HE

L

EV

ER

AG

ED

C

RE

DI

T

MA

RK

ET

S

$97

$53

$25

< $75

> $120

2004 2005 2006 1/07

Estimate

10/07

Estimate

2008

Estimate

Supply and demand imbalance

CLO Activity ($Bn)

Primary Investors for Institutional Term Loans

Since the start of Labor Day, arrangers have

syndicated roughly $87Bn of leveraged finance

paper

In July, the peak of the leveraged finance

calendar was at $356Bn

CLO investor demand has declined since the end of

June as new CLO issuance slowed dramatically

Many suppliers of warehouse capacity now have

prohibitions on covenant-lite loans

CLO warehouse lines have been unwound or are

in the process of being unwound

The market is anticipating that several well-proven

CLO managers will begin structuring new vehicles

the latter part of this year but demand will fall

well short of the estimates from the start of the

year

Demand in the recent month has come from cross-

over investors, whom have been raising funds for

investment in the product

Source: S&P LCD

9M’07

Actual

9M’07

Actual TBD

11/9/2

Leveraged Finance – Forward and In-Market calendar

$180 $160$192

$232$255

$139 $132

$185 $198

$386$350

$308$280

$250

Jan-07 Apr-07 Jul-07 Aug-07 Sep-07 Oct-07 Nov-07

Loans Bonds

CU

RR

EN

T

ST

AT

E

OF

T

HE

L

EV

ER

AG

ED

C

RE

DI

T

MA

RK

ET

S

7.50%

8.00%

8.50%

9.00%

9.50%

May Jun Jul Aug Sep Oct

2

30

3

40

4

50

Average yields and spreads have stabilized since June/July’sleakage

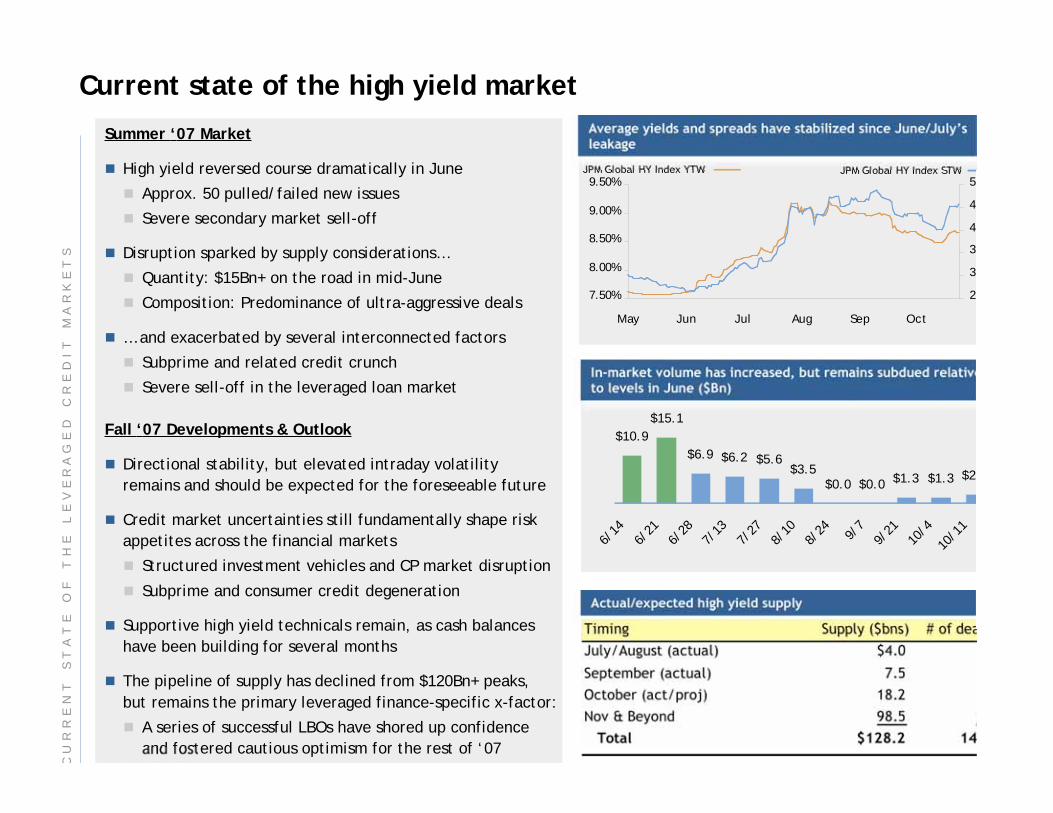

Current state of the high yield market

Summer ‘07 Market

High yield reversed course dramatically in June

Approx. 50 pulled/failed new issues

Severe secondary market sell-off

Disruption sparked by supply considerations…

Quantity: $15Bn+ on the road in mid-June

Composition: Predominance of ultra-aggressive deals

… and exacerbated by several interconnected factors

Subprime and related credit crunch

Severe sell-off in the leveraged loan market

Fall ‘07 Developments & Outlook

Directional stability, but elevated intraday volatility

remains and should be expected for the foreseeable future

Credit market uncertainties still fundamentally shape risk

appetites across the financial markets

Structured investment vehicles and CP market disruption

Subprime and consumer credit degeneration

Supportive high yield technicals remain, as cash balances

have been building for several months

The pipeline of supply has declined from $120Bn+ peaks,

but remains the primary leveraged finance-specific x-factor:

A series of successful LBOs have shored up confidence

and fostered cautious optimism for the rest of ‘07

$10.9

$15.1

$6.9 $6.2 $5.6$3.5

$0.0 $0.0$1.3 $1.3 $2

6/14

6/21

6/28

7/13

7/27

8/10

8/24 9/7

9/21

10/4

10/1

1

In-market volume has increased, but remains subdued relativeto levels in June ($Bn)

JPM Global HY Index YTW JPM Global HY Index STW

Actual/expected high yield supply

CU

RR

EN

T

ST

AT

E

OF

T

HE

L

EV

ER

AG

ED

C

RE

DI

T

MA

RK

ET

S

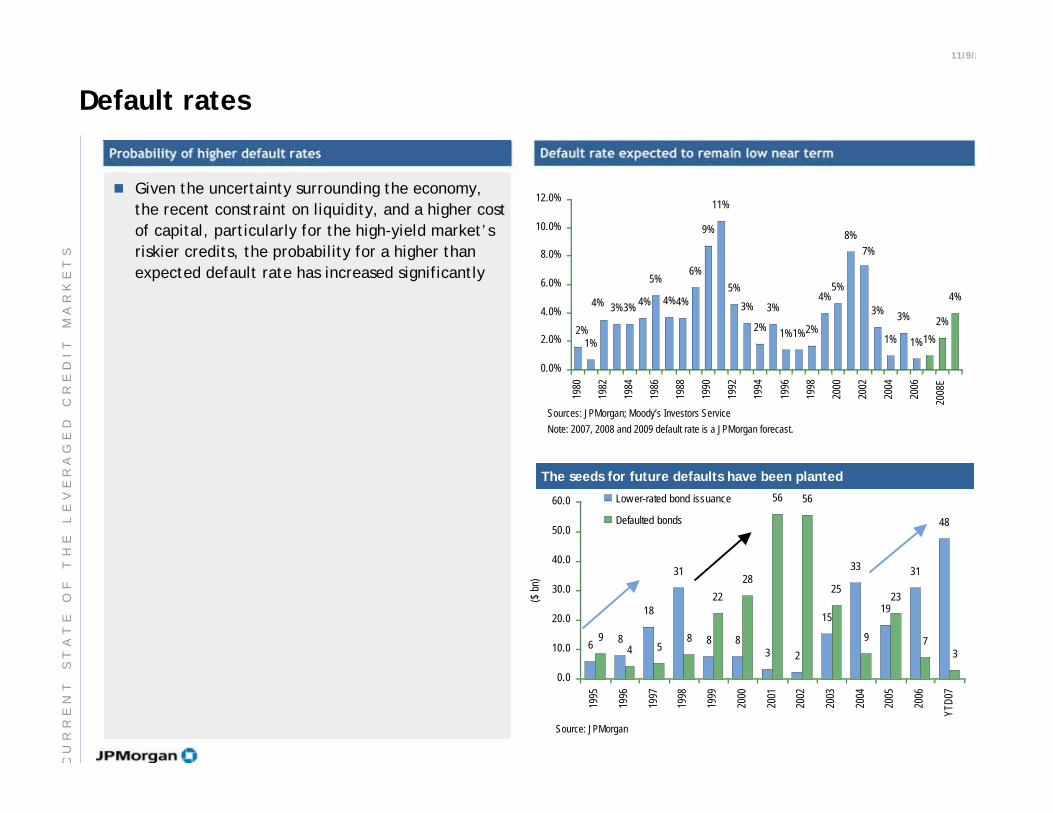

Default rates

Probability of higher default rates

Given the uncertainty surrounding the economy,

the recent constraint on liquidity, and a higher cost

of capital, particularly for the high-yield market’s

riskier credits, the probability for a higher than

expected default rate has increased significantly

11/9/2

Default rate expected to remain low near term

1%

3%3%

5%

4%4%

6%

9%

11%

5%

3%

2%

3%

1%1%2%

4%5%

8%

3%

1%

3%

1%1%

2%

4%

7%

4%4%

2%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008E

Sources: JPMorgan; Moody’s Investors Service

Note: 2007, 2008 and 2009 default rate is a JPMorgan forecast.

The seeds for future defaults have been planted

Source: JPMorgan

68

18

31

8 83 2

15

33

19

31

48

94 5

8

22

28

56 56

25

9

23

73

0.0

10.0

20.0

30.0

40.0

50.0

60.0

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

YTD

07

($ b

n)

Low er-rated bond issuance

Defaulted bonds

CU

RR

EN

T

ST

AT

E

OF

T

HE

L

EV

ER

AG

ED

C

RE

DI

T

MA

RK

ET

S

Agenda

Page

Qualifications

Structured Investment Vehicles (SIVs)

Case Study: Collins & Aikman

Case Study: Refco

Recent Trends in Distressed Solutions

Current State of the Leveraged Credit Markets

Leveraged Credit Market Dynamics

Distressed Debt Trading

What is Distressed Debt 2

8

11

15

22

25

27

38

47

DI

ST

RE

SS

ED

D

EB

T

TR

AD

IN

G

Backstopped rights offerings have become increasingly popular amon

companies exiting bankruptcy

A backstopped rights offering at exit provides creditors with choice and certainty

Choice: An anti-dilution mechanism providing the right to purchase equity at a given price at exit (right of first ref

Certainty with respect to the reduction in pro forma leverage and increase in pro forma liquidity at exit

Rationale

Marketed backstopped equity rights offerings

JPMorgan served as the sole-bookrunner on a

$2,187 million commitment to backstop Owens-

Corning’s equity rights offering to unsecured

creditors upon its emergence from Chapter 11

JPMorgan served as the sole-bookrunner on a $750

million equity commitment for Northwest Airlines

Recent rights offerings

February 2006

$1,800 million

October 2006

$2,200 million

February 2007

$750 million

(Announced)

$3,400 million

RE

CE

NT

T

RE

ND

S

IN

D

IS

TR

ES

SE

D

SO

LU

TI

ON

S

Trade execution Settlement process upon a credit event

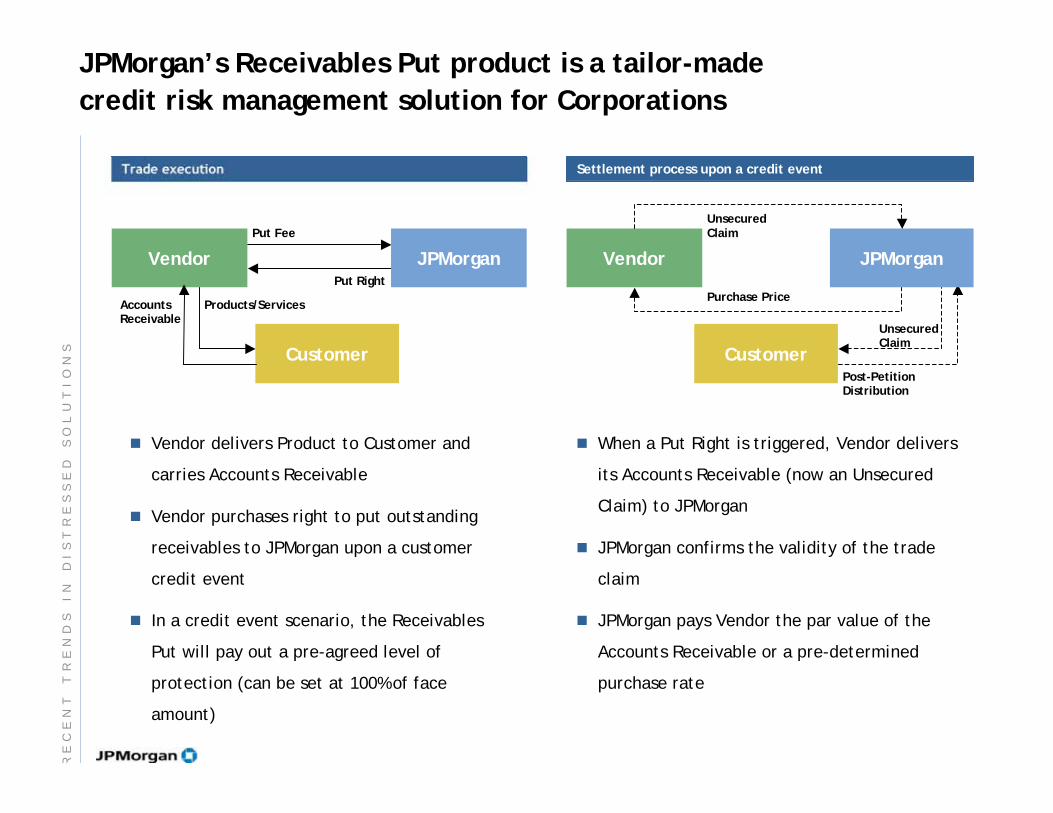

JPMorgan’s Receivables Put product is a tailor-made

credit risk management solution for Corporations

Vendor delivers Product to Customer and

carries Accounts Receivable

Vendor purchases right to put outstanding

receivables to JPMorgan upon a customer

credit event

In a credit event scenario, the Receivables

Put will pay out a pre-agreed level of

protection (can be set at 100% of face

amount)

When a Put Right is triggered, Vendor delivers

its Accounts Receivable (now an Unsecured

Claim) to JPMorgan

JPMorgan confirms the validity of the trade

claim

JPMorgan pays Vendor the par value of the

Accounts Receivable or a pre-determined

purchase rate

Customer

AccountsReceivable

Put Right

Put Fee

Vendor JPMorgan

Products/Services

UnsecuredClaim

Post-PetitionDistribution

Purchase Price

Vendor JPMorgan

Customer

UnsecuredClaim

RE

CE

NT

T

RE

ND

S

IN

D

IS

TR

ES

SE

D

SO

LU

TI

ON

S

Agenda

Page

Qualifications

Structured Investment Vehicles (SIVs)

Case Study: Collins & Aikman

Case Study: Refco

Recent Trends in Distressed Solutions

Current State of the Leveraged Credit Markets

Leveraged Credit Market Dynamics

Distressed Debt Trading

What is Distressed Debt 2

8

11

15

22

25

27

38

47

DI

ST

RE

SS

ED

D

EB

T

TR

AD

IN

G

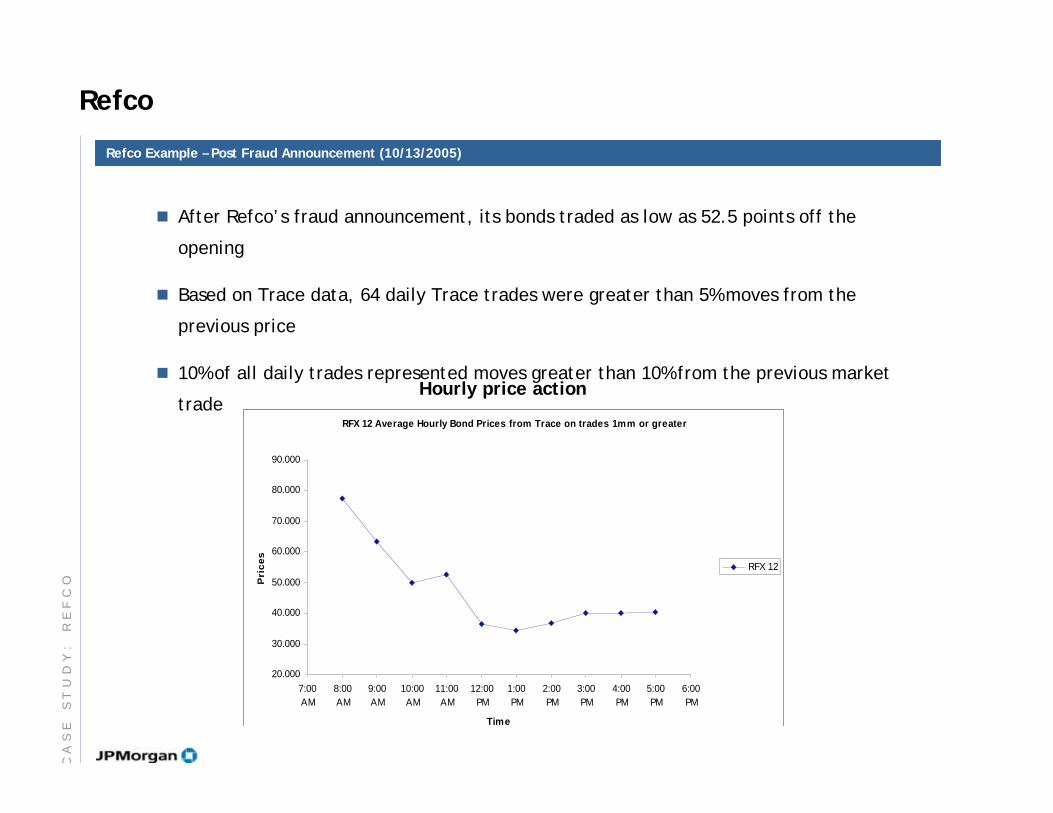

After Refco’s fraud announcement, its bonds traded as low as 52.5 points off the

opening

Based on Trace data, 64 daily Trace trades were greater than 5% moves from the

previous price

10% of all daily trades represented moves greater than 10% from the previous market

trade

Refco Example – Post Fraud Announcement (10/13/2005)

RFX 12 Average Hourly Bond Prices from Trace on trades 1mm or greater

20.000

30.000

40.000

50.000

60.000

70.000

80.000

90.000

7:00

AM

8:00

AM

9:00

AM

10:00

AM

11:00

AM

12:00

PM

1:00

PM

2:00

PM

3:00

PM

4:00

PM

5:00

PM

6:00

PM

Time

Pri

ce

s

RFX 12

Hourly price action

Refco

CA

SE

S

TU

DY

:

RE

FC

O

Agenda

Page

Qualifications

Structured Investment Vehicles (SIVs)

Case Study: Collins & Aikman

Case Study: Refco

Recent Trends in Distressed Solutions

Current State of the Leveraged Credit Markets

Leveraged Credit Market Dynamics

Distressed Debt Trading

What is Distressed Debt 2

8

11

15

22

25

27

38

47

DI

ST

RE

SS

ED

D

EB

T

TR

AD

IN

G

Executive Summary

Collins & Aikman Corp (“C&A”, “The Company”, or “The Debtors”) was one of the largest domestic

auto parts suppliers, with 25 - 40% market share in each of its business lines

Headquartered in Troy, Michigan, roughly 80% of C&A’s sales were to the Big 3 domestic auto

makers. The Company’s North American workforce totaled 17,898 at its peak, with a network of

55 plants located in the U.S., Canada and Mexico

In FY 2003, C&A’s Sales and EBITDA were $4.0bn and $325mm respectively

C&A’s legacy business was the Carpet & Acoustics business (aka “Soft Trim”). The Company’s Soft

Trim plants were efficient, well-managed and profitable

In recent years C&A made a series of acquisitions in the Plastics product line, designed to create a

one-stop provider for hard-trim and soft-trim interior components

While the Plastics division doubled the size of the company’s top line, the products were viewed

by customers as commodities, and therefore, were low-margin businesses

In addition, C&A never integrated the acquired businesses into its global operations, and as a

result, the Plastics division was highly inefficient, which further cut into profitability

On May 17, 2005 C&A filed for bankruptcy as a result of intense pricing pressure, increasing raw

materials pricing, and declining unit volumes at the Big 3

In the years leading up to C&A’s bankruptcy, relations with the Big 3 became strained. In order

to maintain existing business and compete for new program awards, the company was forced to

implement pricing discounts, which the company was unable to offset

CA

SE

S

TU

DY

:

CO

LL

IN

S

&

AI

KM

AN

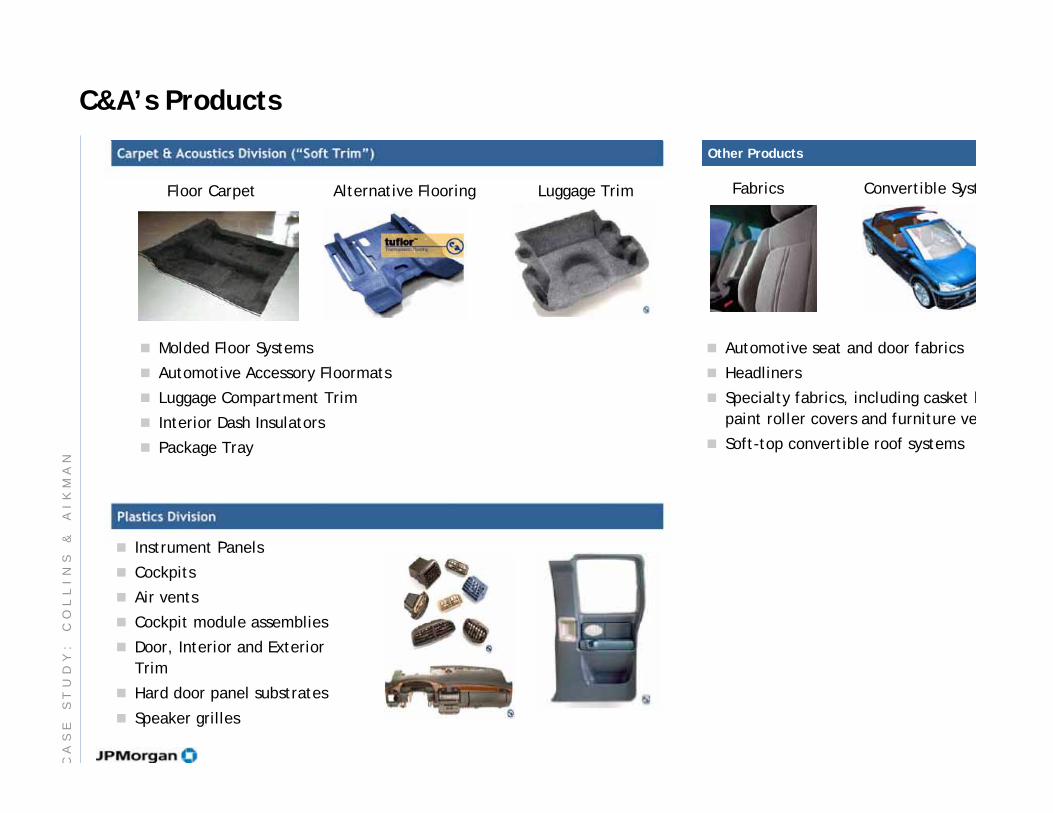

C&A’s Products

Plastics Division

Instrument Panels

Cockpits

Air vents

Cockpit module assemblies

Door, Interior and Exterior

Trim

Hard door panel substrates

Speaker grilles

Carpet & Acoustics Division (“Soft Trim”)

Floor Carpet Alternative Flooring Luggage Trim

Other Products

Fabrics Convertible Syst

Automotive seat and door fabrics

Headliners

Specialty fabrics, including casket l

paint roller covers and furniture ve

Soft-top convertible roof systems

Molded Floor Systems

Automotive Accessory Floormats

Luggage Compartment Trim

Interior Dash Insulators

Package Tray

CA

SE

S

TU

DY

:

CO

LL

IN

S

&

AI

KM

AN

Failed Restructuring Attempts

While in bankruptcy, the Company’s restructuring advisors made several attempts to restructure

the business as a going concern

The turnaround plan centered around the advisors’ beliefs that the Plastics division could return to

profitability by eliminating its high fixed cost structure and becoming a low-cost operator, while

Soft Trim maintained its leading competitive position and EBITDA margins

Despite several attempts, in October 2006, C&A’s stakeholders agreed that fixing the problems in

Plastics was impossible given the timeframe and funding requirements

On October 26, 2006, C&A reported to the bankruptcy court that it was unable to reach an

agreement to enable a Plan of Reorganization. As a result, the Debtors began liquidating the

business by actively marketing the individual segments to potential purchasers

Ultimately C&A’s Soft Trim business was sold to IAC North America, LLC (“IAC”), a company run by

Wilbur Ross, which is now comprised of the former Soft Trim assets of both Lear and C&A

C&A’s pre-petition lenders were given the right to purchase up to 25% of the equity of IAC

After a failed attempt to sell the Plastics business to Cadence Innovation, most of the Plastics

plants and other C&A assets were shut down in July 2007. Some plants and remaining assets

were sold piecemeal or are in process of being sold for de minimus value

CA

SE

S

TU

DY

:

CO

LL

IN

S

&

AI

KM

AN

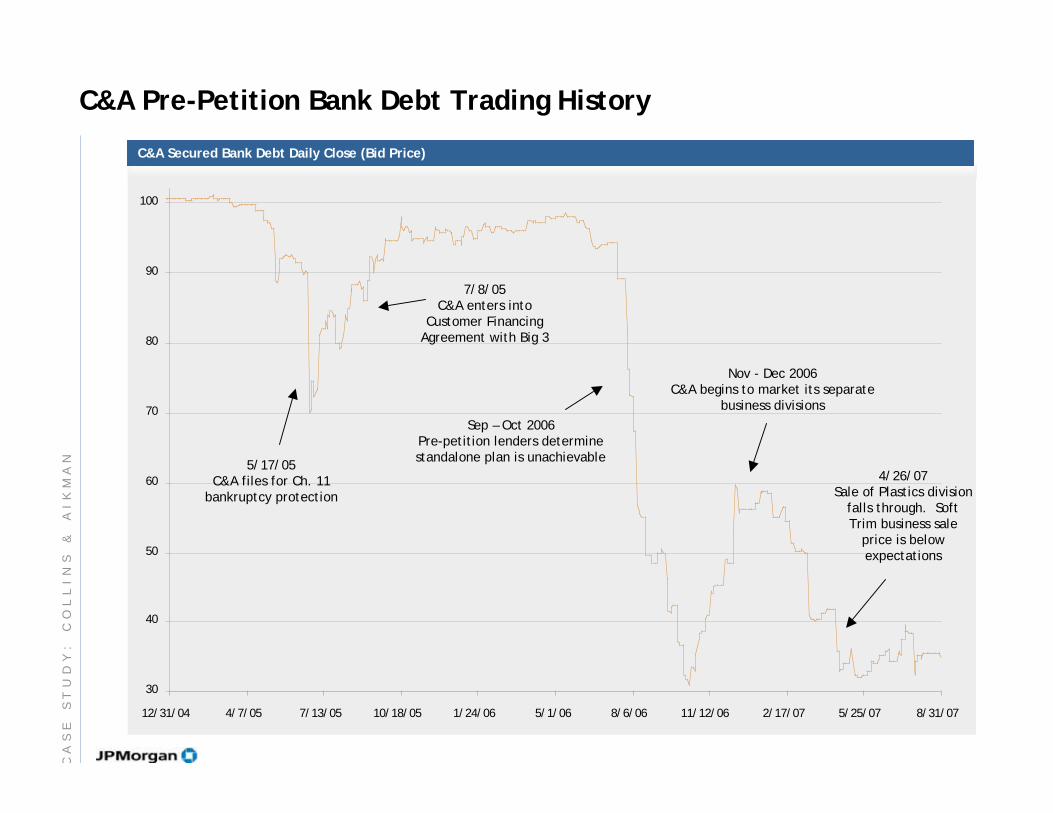

30

40

50

60

70

80

90

100

12/31/04 4/7/05 7/13/05 10/18/05 1/24/06 5/1/06 8/6/06 11/12/06 2/17/07 5/25/07 8/31/07

C&A Secured Bank Debt Daily Close (Bid Price)

C&A Pre-Petition Bank Debt Trading History

5/17/05C&A files for Ch. 11

bankruptcy protection

Sep – Oct 2006Pre-petition lenders determinestandalone plan is unachievable

Nov - Dec 2006C&A begins to market its separate

business divisions

4/26/07Sale of Plastics division

falls through. SoftTrim business sale

price is belowexpectations

7/8/05C&A enters into

Customer FinancingAgreement with Big 3

CA

SE

S

TU

DY

:

CO

LL

IN

S

&

AI

KM

AN

Key Events Timeline

5/17/05: Concurrent with its bankruptcy filing, C&A obtains $150mm of Debtor-in-Possession (“DIP

financing, with $150mm to be loaned thereafter, subject to certain terms

6/11/05: 3 weeks after the filing date, the Debtors had consumed the entire initial $150mm DIP

loan, and the DIP lenders refuse to loan the additional $150mm due to insufficient collateral

7/8/05: C&A enters into agreements with its Big 3 Customers, whereby the Big 3 provided $165mm

of financing to C&A through retroactive price increases on existing contracts and a junior DIP loan.

The Big 3 also agrees not to resource production away from C&A until Sept 2005

Dec 2005: Though the Company’s budget calls for EBITDA of $265mm, Capstone (pre-petition

lenders’ financial advisor) urges a sale of the company, arguing sustainable EBITDA is below $265m

June 2006: After two failed rights offering attempts by C&A bondholders, IAC offers to purchase

C&A at a price equal to 80% for pre-petition lenders. The offer includes contingencies that make a

sale unsuitable to the lenders. The lenders consider the offer illusory, and pursue a plan to conve

their debt into equity of a reorganized C&A

Oct 2006: After further analysis reveals continued deterioration in the Plastics division, the pre-

petition lenders determine a standalone plan is no longer achievable

Dec 2006 – Mar 2007: The pre-petition lenders and the company begin marketing the company’s

individual business segments to potential buyers. Capstone estimates that the sale of the Soft Trim

and Plastics businesses will yield proceeds of approximately $400mm, which would equate to a 45-

61% recovery for pre-petition lenders

CA

SE

S

TU

DY

:

CO

LL

IN

S

&

AI

KM

AN

Key Events Timeline (cont)

4/26/07: Capstone holds a meeting of pre-petition senior lenders, and distributes an updated

recovery analysis, reflecting value to pre-petition lenders of 24-40% – well below its original 45-61%

estimate

The sale of Plastics to Cadence Innovation had fallen apart in April, and the sale price of Soft Tr

to IAC is below expectations

As part of the sale of Soft Trim, pre-petition lenders are given rights to purchase 25% of IAC

9/26/07: Capstone delivers presentation to lender group estimating remaining asset sale recoverie

to be higher than its April analysis

Net recoveries from claims receivable as well as higher than anticipated Europe and Canadian

proceeds are the primary drivers

CA

SE

S

TU

DY

:

CO

LL

IN

S

&

AI

KM

AN

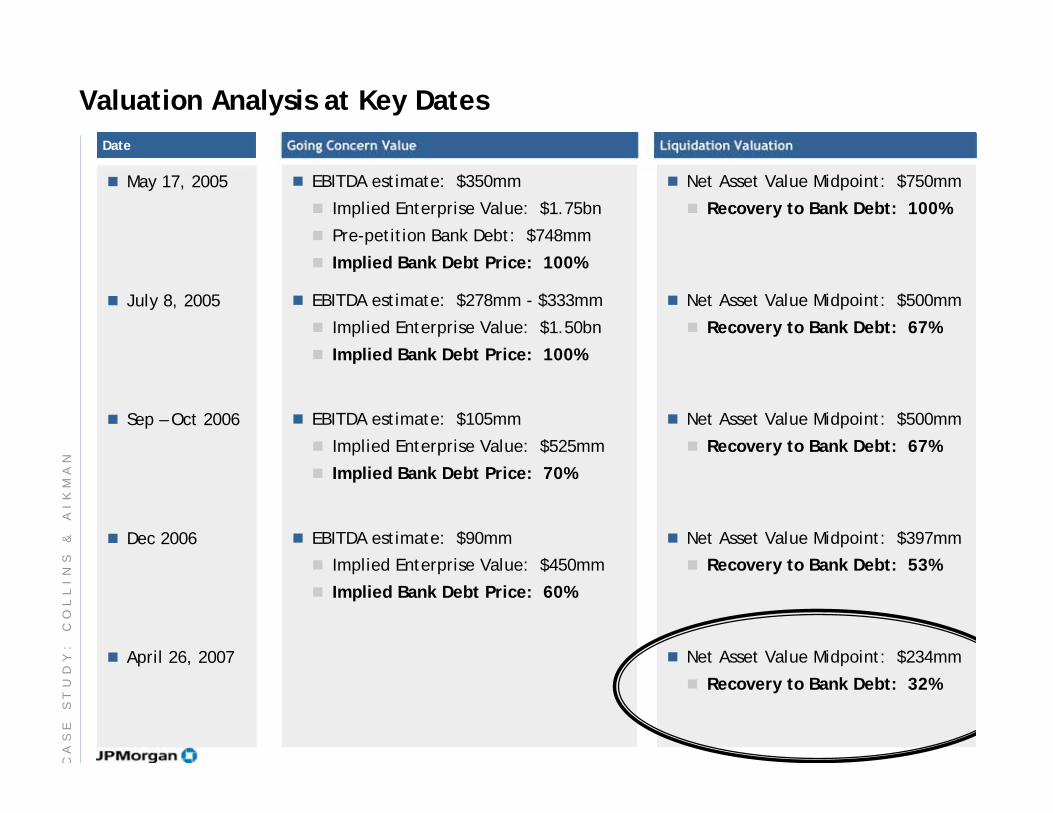

Valuation Analysis at Key Dates

Going Concern Value Liquidation Valuation

May 17, 2005

July 8, 2005

Sep – Oct 2006

Dec 2006

April 26, 2007

Date

EBITDA estimate: $350mm

Implied Enterprise Value: $1.75bn

Pre-petition Bank Debt: $748mm

Implied Bank Debt Price: 100%

EBITDA estimate: $278mm - $333mm

Implied Enterprise Value: $1.50bn

Implied Bank Debt Price: 100%

EBITDA estimate: $105mm

Implied Enterprise Value: $525mm

Implied Bank Debt Price: 70%

EBITDA estimate: $90mm

Implied Enterprise Value: $450mm

Implied Bank Debt Price: 60%

Net Asset Value Midpoint: $750mm

Recovery to Bank Debt: 100%

Net Asset Value Midpoint: $500mm

Recovery to Bank Debt: 67%

Net Asset Value Midpoint: $500mm

Recovery to Bank Debt: 67%

Net Asset Value Midpoint: $397mm

Recovery to Bank Debt: 53%

Net Asset Value Midpoint: $234mm

Recovery to Bank Debt: 32%

CA

SE

S

TU

DY

:

CO

LL

IN

S

&

AI

KM

AN

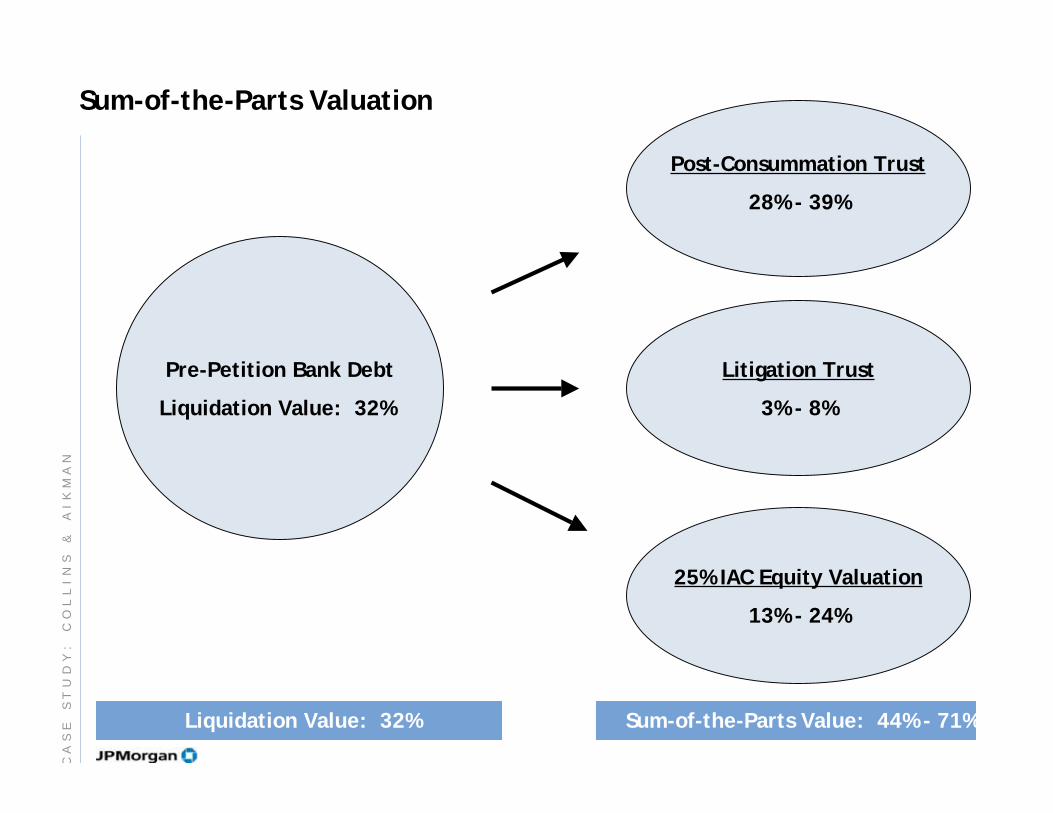

Sum-of-the-Parts Valuation

Pre-Petition Bank Debt

Liquidation Value: 32%

Post-Consummation Trust

28% - 39%

Litigation Trust

3% - 8%

25% IAC Equity Valuation

13% - 24%

Sum-of-the-Parts Value: 44% - 71%Liquidation Value: 32%

CA

SE

S

TU

DY

:

CO

LL

IN

S

&

AI

KM

AN

30

35

40

45

50

55

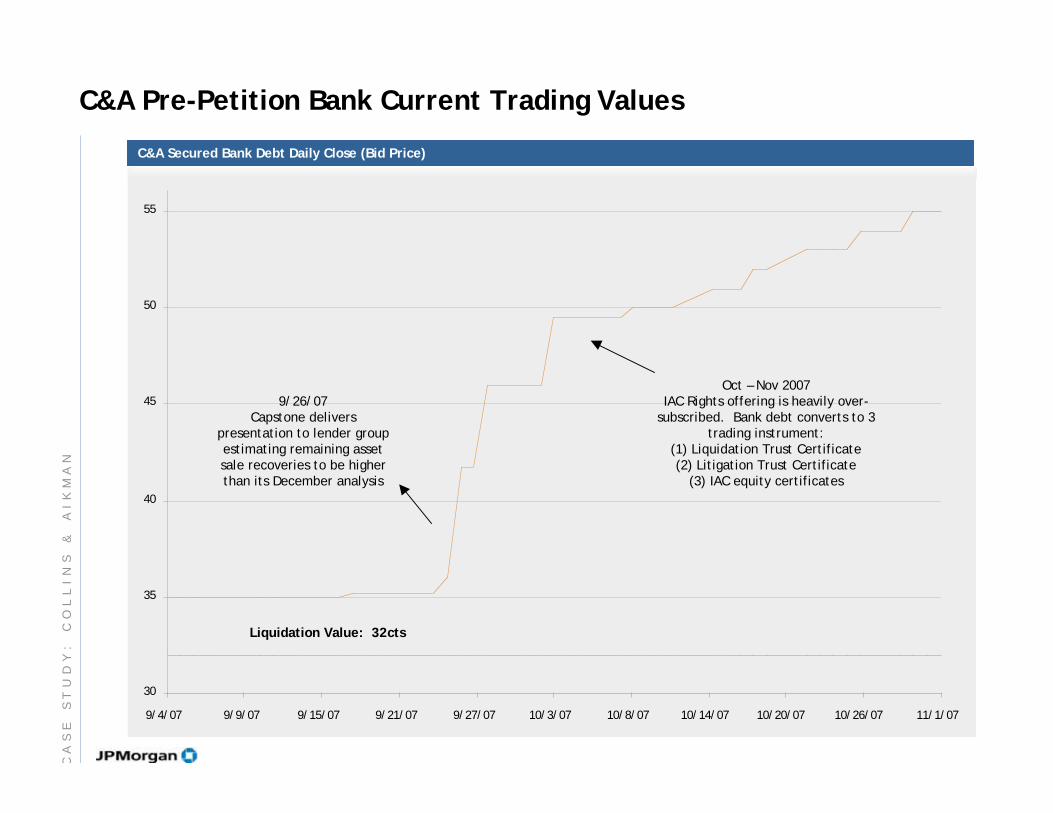

9/4/07 9/9/07 9/15/07 9/21/07 9/27/07 10/3/07 10/8/07 10/14/07 10/20/07 10/26/07 11/1/07

C&A Secured Bank Debt Daily Close (Bid Price)

C&A Pre-Petition Bank Current Trading Values

9/26/07Capstone delivers

presentation to lender groupestimating remaining assetsale recoveries to be higherthan its December analysis

Liquidation Value: 32cts

Oct – Nov 2007IAC Rights offering is heavily over-

subscribed. Bank debt converts to 3trading instrument:

(1) Liquidation Trust Certificate(2) Litigation Trust Certificate

(3) IAC equity certificates

CA

SE

S

TU

DY

:

CO

LL

IN

S

&

AI

KM

AN

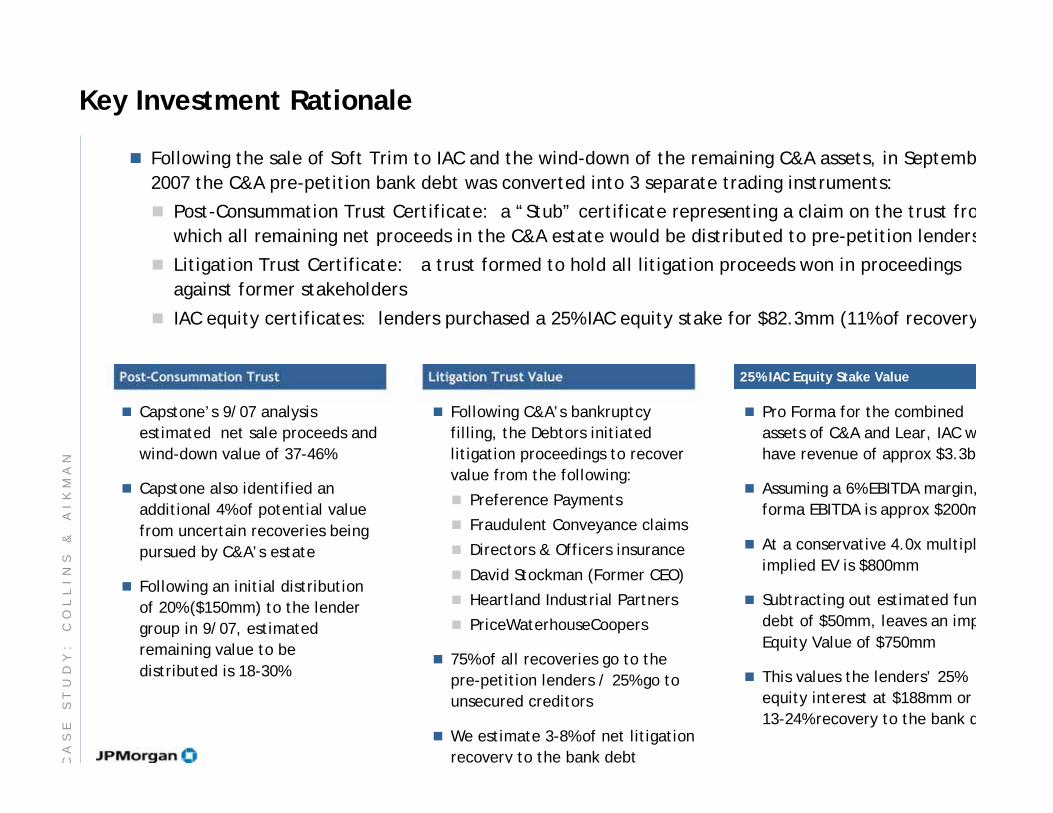

Key Investment Rationale

Following the sale of Soft Trim to IAC and the wind-down of the remaining C&A assets, in Septemb

2007 the C&A pre-petition bank debt was converted into 3 separate trading instruments:

Post-Consummation Trust Certificate: a “Stub” certificate representing a claim on the trust fro

which all remaining net proceeds in the C&A estate would be distributed to pre-petition lenders

Litigation Trust Certificate: a trust formed to hold all litigation proceeds won in proceedings

against former stakeholders

IAC equity certificates: lenders purchased a 25% IAC equity stake for $82.3mm (11% of recovery

Capstone’s 9/07 analysis

estimated net sale proceeds and

wind-down value of 37-46%

Capstone also identified an

additional 4% of potential value

from uncertain recoveries being

pursued by C&A’s estate

Following an initial distribution

of 20% ($150mm) to the lender

group in 9/07, estimated

remaining value to be

distributed is 18-30%

Following C&A’s bankruptcy

filling, the Debtors initiated

litigation proceedings to recover

value from the following:

Preference Payments

Fraudulent Conveyance claims

Directors & Officers insurance

David Stockman (Former CEO)

Heartland Industrial Partners

PriceWaterhouseCoopers

75% of all recoveries go to the

pre-petition lenders / 25% go to

unsecured creditors

We estimate 3-8% of net litigation

recovery to the bank debt

Pro Forma for the combined

assets of C&A and Lear, IAC w

have revenue of approx $3.3b

Assuming a 6% EBITDA margin,

forma EBITDA is approx $200m

At a conservative 4.0x multipl

implied EV is $800mm

Subtracting out estimated fun

debt of $50mm, leaves an imp

Equity Value of $750mm

This values the lenders’ 25%

equity interest at $188mm or

13-24% recovery to the bank d

Post-Consummation Trust Litigation Trust Value 25% IAC Equity Stake Value

CA

SE

S

TU

DY

:

CO

LL

IN

S

&

AI

KM

AN

Agenda

Page

Qualifications

Structured Investment Vehicles (SIVs)

Case Study: Collins & Aikman

Case Study: Refco

Recent Trends in Distressed Solutions

Current State of the Leveraged Credit Markets

Leveraged Credit Market Dynamics

Distressed Debt Trading

What is Distressed Debt 2

8

11

15

22

25

27

38

47

DI

ST

RE

SS

ED

D

EB

T

TR

AD

IN

G

1452,115

12,096

18,23320,875

11,45

18,51

11,67

18,669

-16,01-15,83-13,026-14,10

-10,684

-13,93

-9,391-11,86

-14,23-14,230

-11,54-11,26-9,804

-11,67

-9,030-9,613

-6,314-7,214

Jan-07 Feb-07 Mar-07 Apr-07 May-07 Jun-07 Jul-07 Aug-07 Sep-07 Oct-07 Nov-07 Dec-07 Jan-08 Feb-08 Mar-08 Apr-08 May-08 Jun-08

Issuance Redemptions

MTN issuance and redemptions by outstandings ($ millions)

83%decrease in

August

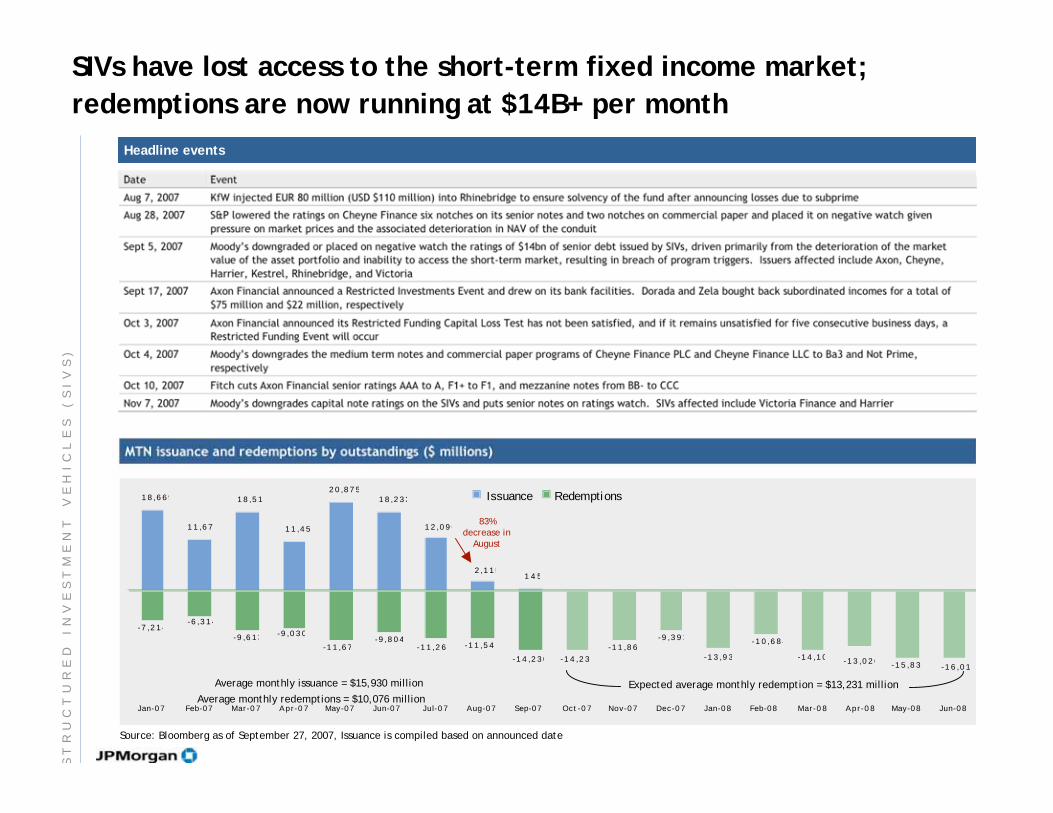

SIVs have lost access to the short-term fixed income market;

redemptions are now running at $14B+ per month

Average monthly issuance = $15,930 million

Average monthly redemptions = $10,076 million

Source: Bloomberg as of September 27, 2007, Issuance is compiled based on announced date

Expected average monthly redemption = $13,231 million

Headline events

ST

RU

CT

UR

ED

I

NV

ES

TM

EN

T

VE

HI

CL

ES

(

SI

VS

)

34,487

75,275

11,87 12,685

50,441

106,14

19,59615,486

66,419

164,287

25,44329,520

69,975

211,95

32,127

USCP USMTN ECP EMTN

2004 2005 2006 2007

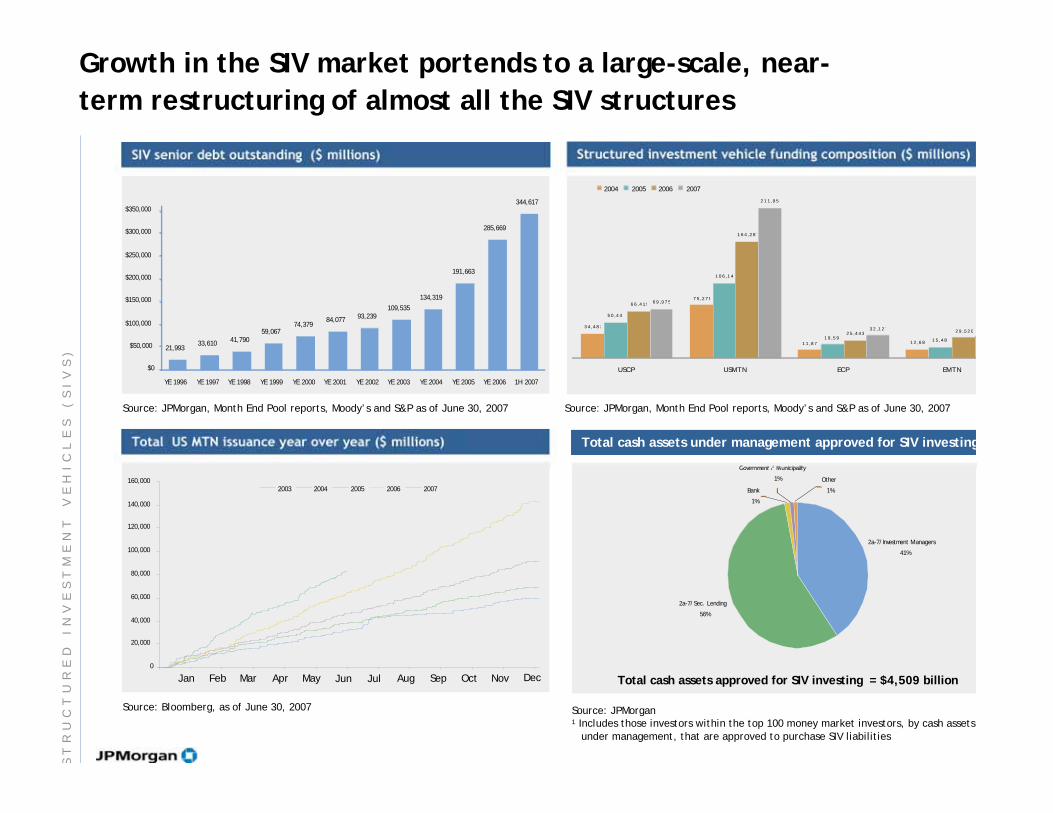

Growth in the SIV market portends to a large-scale, near-

term restructuring of almost all the SIV structures

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

2003 2004 2005 2006 2007

SIV senior debt outstanding ($ millions)

Source: JPMorgan1 Includes those investors within the top 100 money market investors, by cash assets

under management, that are approved to purchase SIV liabilities

Total US MTN issuance year over year ($ millions)

Source: Bloomberg, as of June 30, 2007

Structured investment vehicle funding composition ($ millions)

Jan Feb AprMar May Jun AugJul Sep Oct DecNov

2a-7/Investment Managers

41%

2a-7/Sec. Lending

56%

Bank

1%

Government / Municipality

1% Other

1%

Total cash assets under management approved for SIV investing

Total cash assets approved for SIV investing = $4,509 billion

21,99333,610

41,79059,067

74,37984,077

93,239109,535

191,663

285,669

134,319

344,617

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

YE 1996 YE 1997 YE 1998 YE 1999 YE 2000 YE 2001 YE 2002 YE 2003 YE 2004 YE 2005 YE 2006 1H 2007

Source: JPMorgan, Month End Pool reports, Moody’s and S&P as of June 30, 2007 Source: JPMorgan, Month End Pool reports, Moody’s and S&P as of June 30, 2007

ST

RU

CT

UR

ED

I

NV

ES

TM

EN

T

VE

HI

CL

ES

(

SI

VS

)

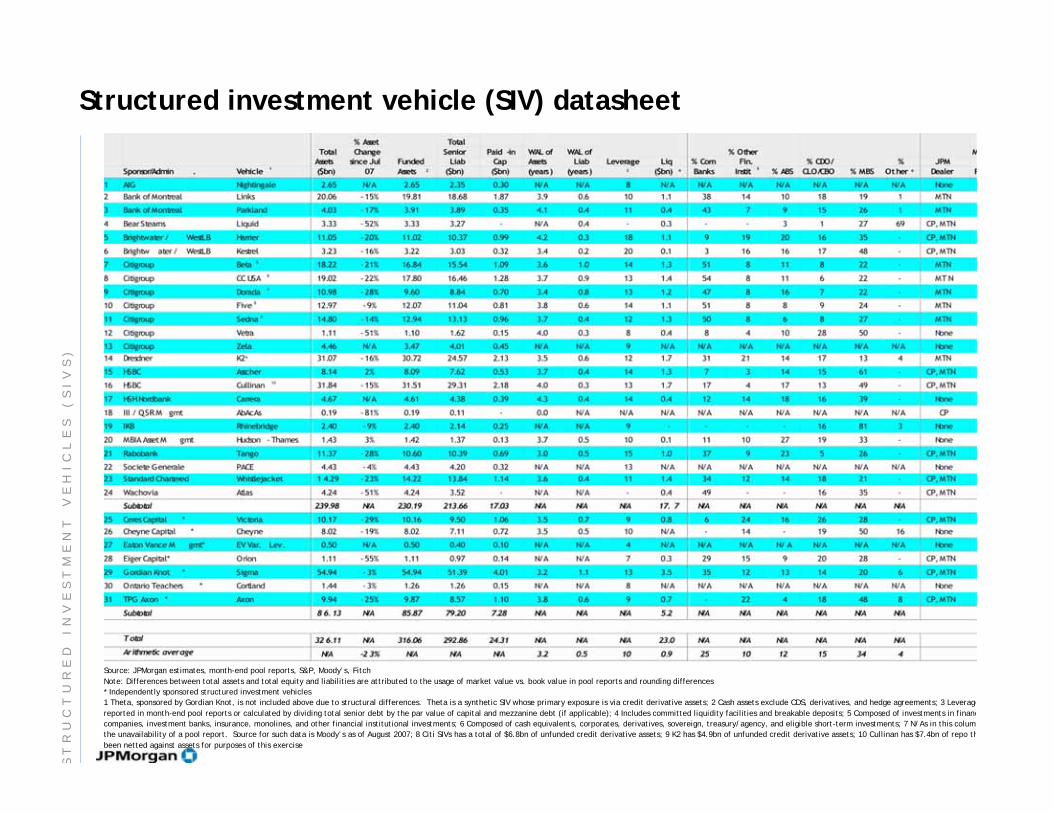

Structured investment vehicle (SIV) datasheet

Source: JPMorgan estimates, month-end pool reports, S&P, Moody’s, Fitch

Note: Differences between total assets and total equity and liabilities are attributed to the usage of market value vs. book value in pool reports and rounding differences

* Independently sponsored structured investment vehicles

1 Theta, sponsored by Gordian Knot, is not included above due to structural differences. Theta is a synthetic SIV whose primary exposure is via credit derivative assets; 2 Cash assets exclude CDS, derivatives, and hedge agreements; 3 Leverage

reported in month-end pool reports or calculated by dividing total senior debt by the par value of capital and mezzanine debt (if applicable); 4 Includes committed liquidity facilities and breakable deposits; 5 Composed of investments in financ

companies, investment banks, insurance, monolines, and other financial institutional investments; 6 Composed of cash equivalents, corporates, derivatives, sovereign, treasury/agency, and eligible short-term investments; 7 N/As in this colum

the unavailability of a pool report. Source for such data is Moody’s as of August 2007; 8 Citi SIVs has a total of $6.8bn of unfunded credit derivative assets; 9 K2 has $4.9bn of unfunded credit derivative assets; 10 Cullinan has $7.4bn of repo th

been netted against assets for purposes of this exercise

ST

RU

CT

UR

ED

I

NV

ES

TM

EN

T

VE

HI

CL

ES

(

SI

VS

)

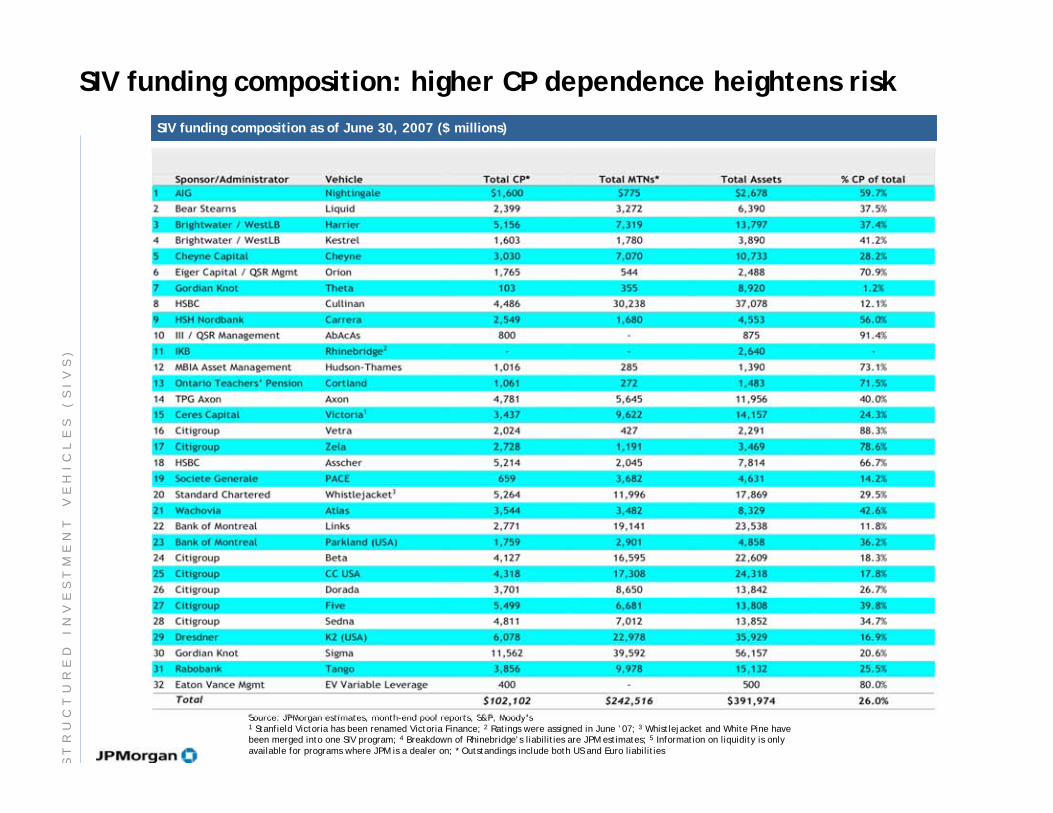

SIV funding composition: higher CP dependence heightens risk

Source: JPMorgan estimates, month-end pool reports, S&P, Moody’s1 Stanfield Victoria has been renamed Victoria Finance; 2 Ratings were assigned in June ’07; 3 Whistlejacket and White Pine havebeen merged into one SIV program; 4 Breakdown of Rhinebridge’s liabilities are JPM estimates; 5 Information on liquidity is onlyavailable for programs where JPM is a dealer on; * Outstandings include both US and Euro liabilities

SIV funding composition as of June 30, 2007 ($ millions)

ST

RU

CT

UR

ED

I

NV

ES

TM

EN

T

VE

HI

CL

ES

(

SI

VS

)

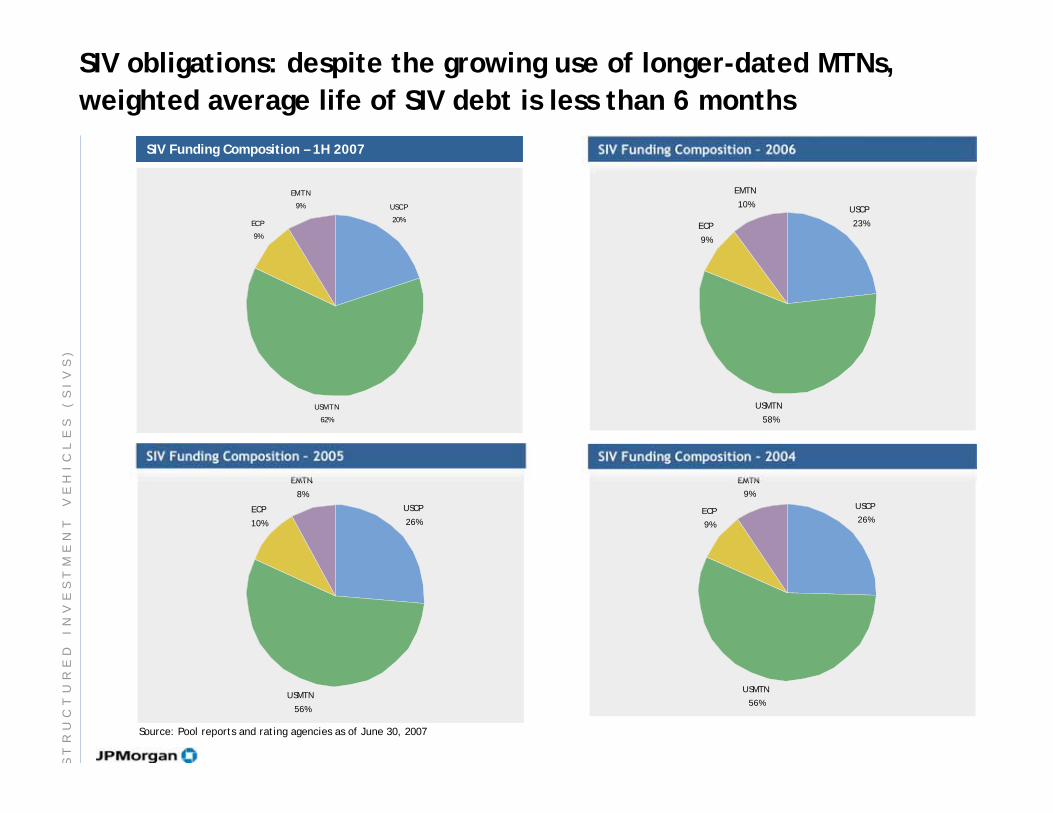

SIV obligations: despite the growing use of longer-dated MTNs,

weighted average life of SIV debt is less than 6 months

USCP

26%

ECP

9%

EMTN

9%

USMTN

56%

SIV Funding Composition - 2004

USCP

23%ECP

9%

EMTN

10%

USMTN

58%

SIV Funding Composition – 2006

USCP

26%

ECP

10%

EMTN

8%

USMTN

56%

SIV Funding Composition – 2005

Source: Pool reports and rating agencies as of June 30, 2007

SIV Funding Composition – 1H 2007

USCP

20%

USMTN

62%

ECP

9%

EMTN

9%

ST

RU

CT

UR

ED

I

NV

ES

TM

EN

T

VE

HI

CL

ES

(

SI

VS

)

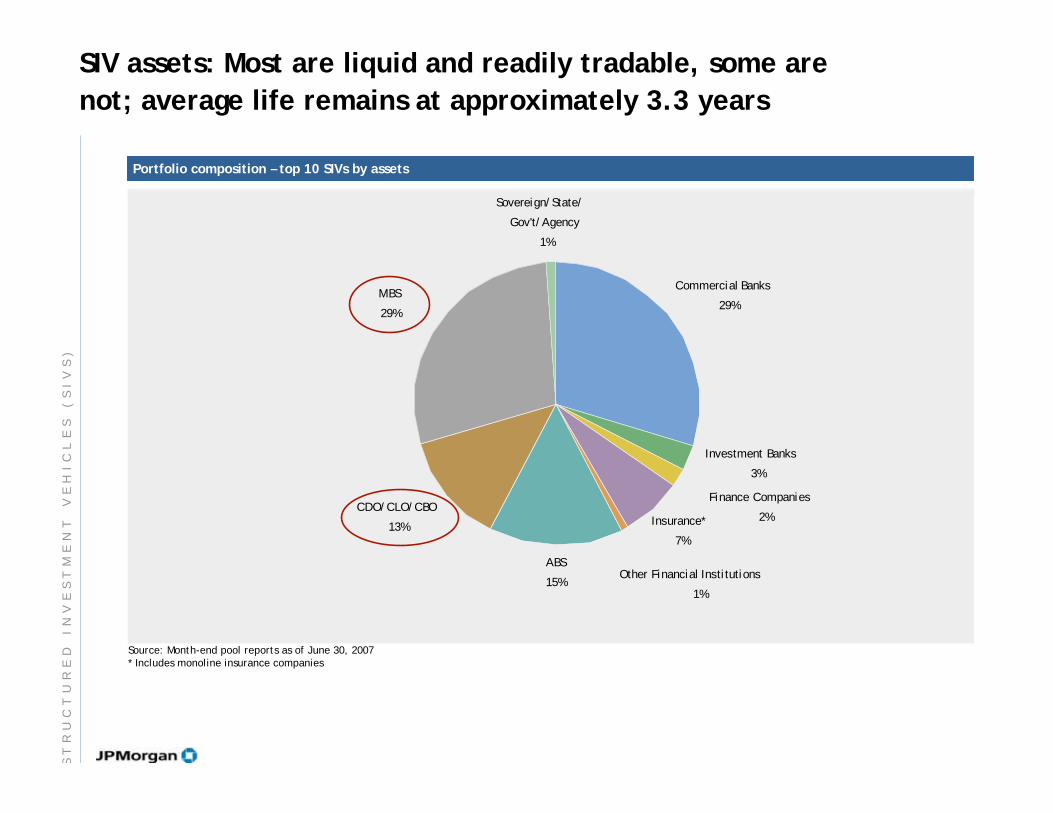

Commercial Banks

29%

ABS

15%

CDO/CLO/CBO

13%

MBS

29%

Finance Companies

2%Insurance*

7%

Other Financial Institutions

1%

Investment Banks

3%

Sovereign/State/

Gov't/Agency

1%

Portfolio composition – top 10 SIVs by assets

Source: Month-end pool reports as of June 30, 2007* Includes monoline insurance companies

SIV assets: Most are liquid and readily tradable, some are

not; average life remains at approximately 3.3 years

ST

RU

CT

UR

ED

I

NV

ES

TM

EN

T

VE

HI

CL

ES

(

SI

VS

)

Consortium-led solution for SIV funding crisis

October 2007: Bank consortium led by Citibank, Bank of America and JPMorgan

Chase announces the creation of a “super conduit” (called MLEC) to purchase

troubled assets in exchange for new short term debt.

Size of fund: $80 - $100 billion

Duration of fund: 12 – 18 months

Timing of implementation: Originally expected by year end, though that remains

in question given lack of substantive information since MLEC announcement.

Fund will pay market prices for SIV assets in an effort to prevent “dumping” of

assets

Biggest questions: what assets will the MLEC buy and what will “market” price be?

Any market price lower than book will crystallize losses and could trigger

covenants and/or rating agency downgrades

MLEC will not solve the SIV crisis nor will it fix the SIV model

MLEC, if implemented by year end, may minimize asset “fire sales”

Most observers, including many SIV managers, see SIV model as broken

Will MLEC favor bank sponsored vehicles over non-bank sponsored vehicles ?

If MLEC duration is a year or less, SIVs’ survival remains dependent on the

recovery of US MBS and CDO squared markets

Objections to the MLEC structure as a “bailout” highlights the commercial and

political sensitivities of the proposed fund.

ST

RU

CT

UR

ED

I

NV

ES

TM

EN

T

VE

HI

CL

ES

(

SI

VS

)

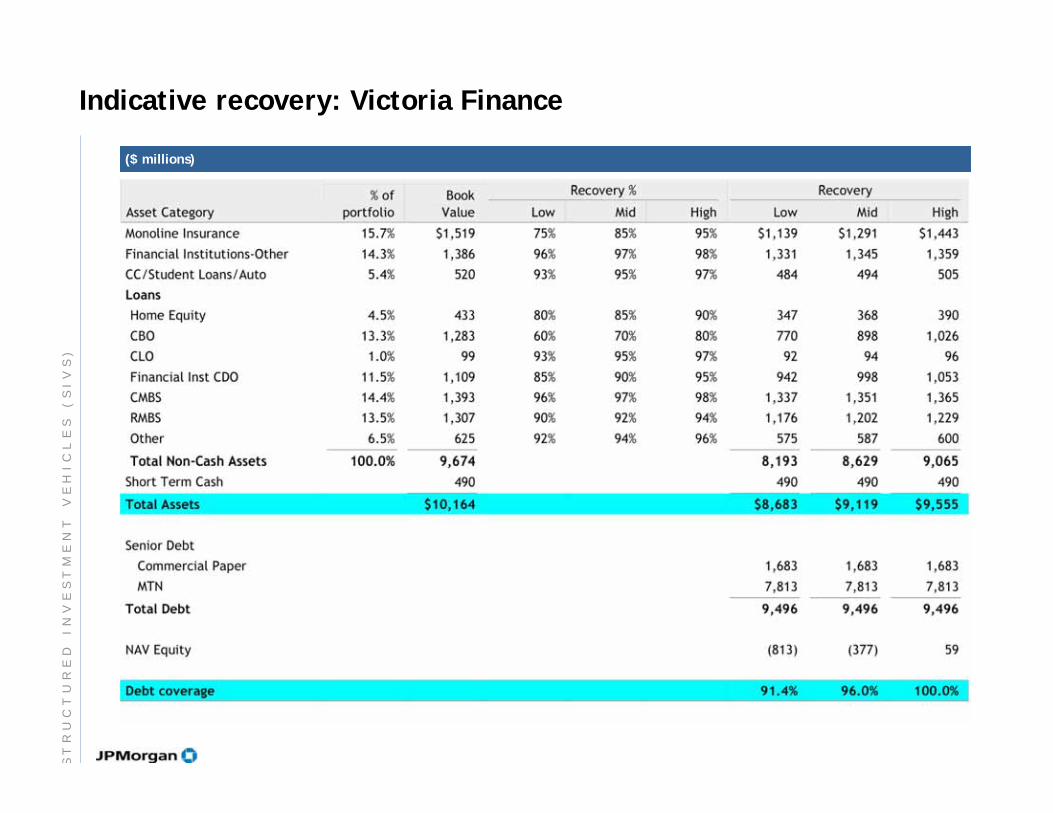

Indicative recovery: Victoria Finance

($ millions)

ST

RU

CT

UR

ED

I

NV

ES

TM

EN

T

VE

HI

CL

ES

(

SI

VS

)

Agenda

Page

Qualifications

Structured Investment Vehicles (SIVs)

Case Study: Collins & Aikman

Case Study: Refco

Recent Trends in Distressed Solutions

Current State of the Leveraged Credit Markets

Leveraged Credit Market Dynamics

Distressed Debt Trading

What is Distressed Debt 2

8

11

15

22

25

27

38

47

DI

ST

RE

SS

ED

D

EB

T

TR

AD

IN

G

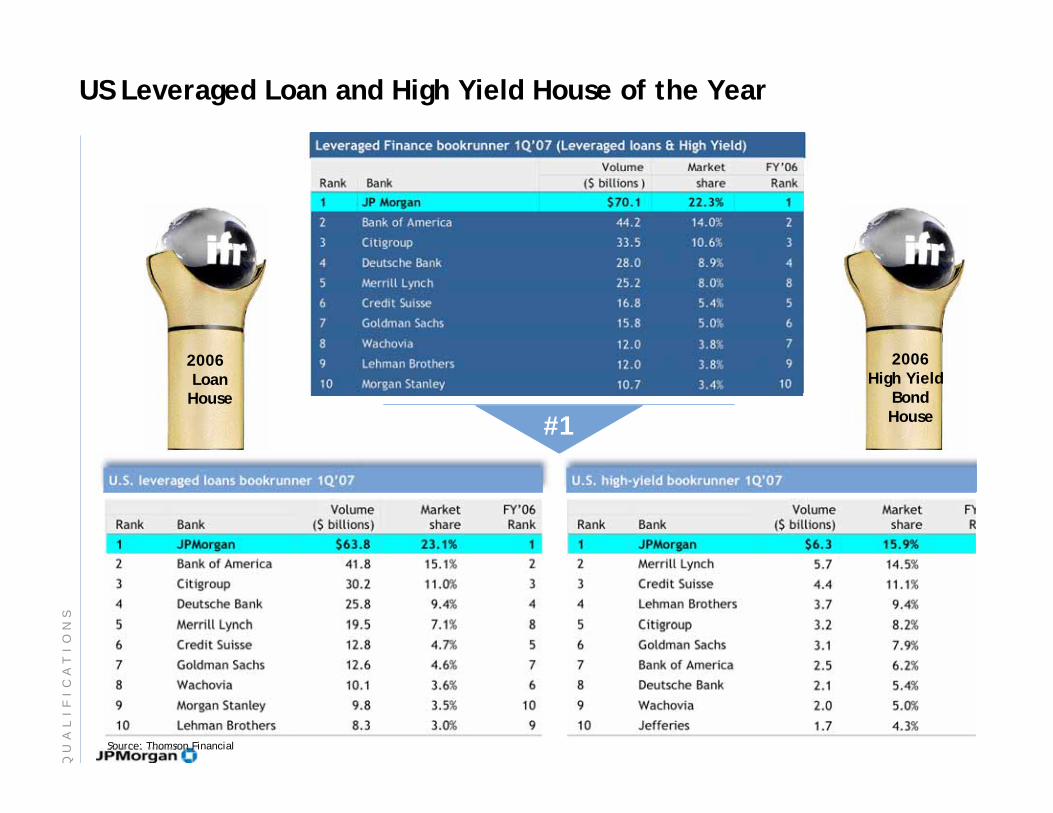

US Leveraged Loan and High Yield House of the Year

Leveraged Finance bookrunner 1Q’07 (Leveraged loans & High Yield)

Source: Thomson Financial

#1

U.S. leveraged loans bookrunner 1Q’07 U.S. high-yield bookrunner 1Q’07

2006LoanHouse

2006High Yield

BondHouse

QU

AL

IF

IC

AT

IO

NS

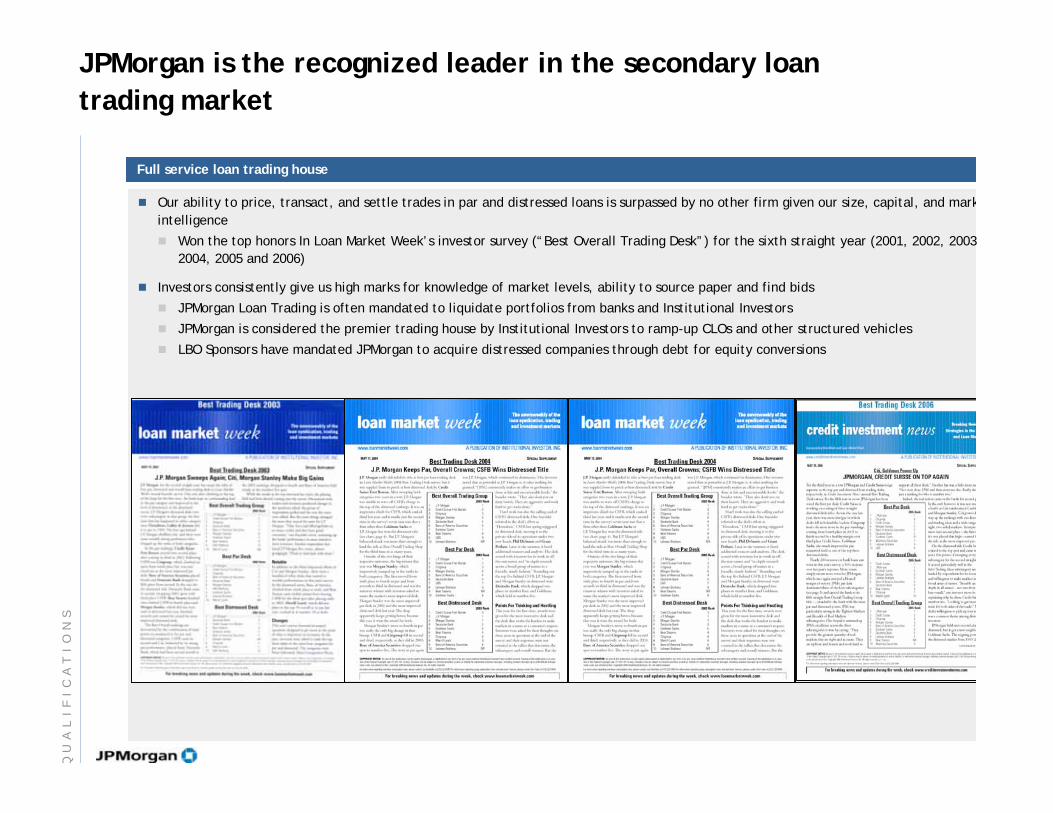

Full service loan trading house

Our ability to price, transact, and settle trades in par and distressed loans is surpassed by no other firm given our size, capital, and mark

intelligence

Won the top honors In Loan Market Week’s investor survey (“Best Overall Trading Desk”) for the sixth straight year (2001, 2002, 2003

2004, 2005 and 2006)

Investors consistently give us high marks for knowledge of market levels, ability to source paper and find bids

JPMorgan Loan Trading is often mandated to liquidate portfolios from banks and Institutional Investors

JPMorgan is considered the premier trading house by Institutional Investors to ramp-up CLOs and other structured vehicles

LBO Sponsors have mandated JPMorgan to acquire distressed companies through debt for equity conversions

JPMorgan is the recognized leader in the secondary loan

trading market

QU

AL

IF

IC

AT

IO

NS

Recommended