PovertyofvisionholdsbackAustralia

DavidLeitch,ITK,April2018

AboutITK

• DavidLeitch– PrincipalITK• ResearchanalystatUBS,JPMorganandpredecessorfirmsfor33years.David’svarious teams achievedNo1inGreenwichsurveyin3separatesectorsoverthattimeperiod.Consistenttop3inutilities2004-2016.

• Analysisofelectricity,gasanddecarbonisation.• Companyanalysis• Investmentsecondopinions• Marketreviews

• Someworkisdoneonvoluntarybasisandfoundatwww.reneweconomy.com.au.

2

Politics- Thepeopleareaheadofthepollies

3

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Vote Seats*

Shareofnationaltotal%

LowerhouseofParliamentdoesn'trepresentnationalopinion

Nationals+50%LibNationals Greens 0% 10% 20% 30% 40% 50% 60% 70%

Renewables+storage

Renewables+fossilfuels

Maintainstatusquo

HowshouldwepowerAustralia?

Source:ClimateInstitutesurvey2017

50%

60%

70%

80%

2012 2013 2014 2015 2016 2017

Australianswhoacceptclimatechange,includes64%ofLiberalvotersand54%ofNationalvoters

Source:ClimateInstitutesurvey2017

DespitehighpowerpricesthesittingpartyinVictoria,theALP,isregardedbyvotersasmorelikelythantheCoalitiontomaintainelectricitysupplyandkeeppowerpriceslower

Home ownersvotewiththeirwallets

• Basedon480,000 USApropertysales• Propertiesprojectedtobeexposedtosealevelrisesellat7%discountrelativetootherwisesimilarproperties• Thisdiscountisnotinrentsjustinsalesprice• Propertiesnotionallyexposedto1footofexpectedrisesellata22%discount• Therewasnodiscountin2007• Thepricediscountisconsistentwiththe“severe”sealevelriseforecastsofclimatechangemodels• Source:BernsteinGustafson&Lewis2017

4

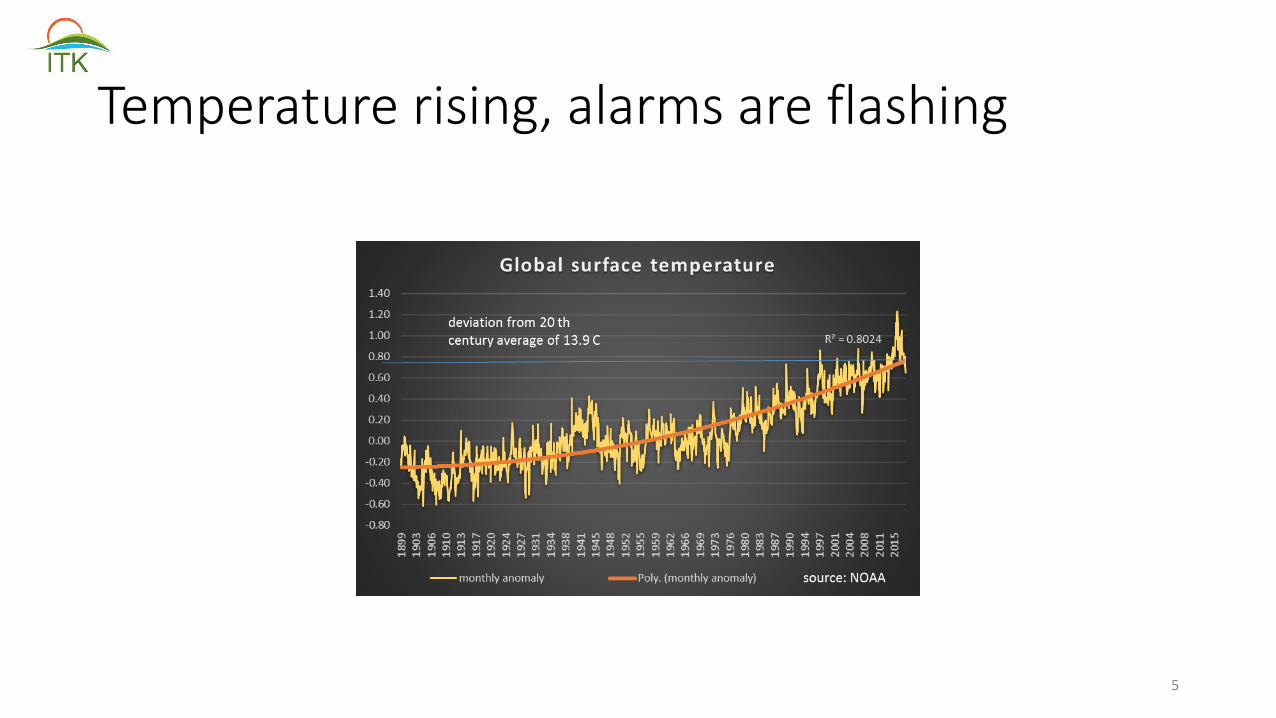

Temperaturerising,alarmsareflashing

5

World viewin30seconds

6

0

20

40

60

80

100

120

GW

Globalnewgeneration2017

Source:UN Environment,BNEF

5

10

15

20

2011 2012 2013 2014 2015 2016 2017 2018

%

Globalrenewableshare

Power EnergySource:UN Environment,NEF

0

200

400

600

2013 2013 2014 2015 2016 2017

GW

Globalcumulativeinstalledwind&PV

wind PVSource:GWEC,GSC

LCOEbasedongloballearningrate

Growth Years Annual LCOE

Peryear Todouble Reduction in2022

A$MWh

Wind 8% 9 2.5% 49

PV 30% 2.5 8.5% 47

PolicyforahighVREgrid

RenewablesmuchmoresensitivetoWACCrequirement

PV GasCapacity MW 200 200Capex $M 330 278LCOEfor6.5%projectIRR* $MWh 66 82.5LCOEfor7.5%projectIRR* $MWh 72 84.8Change % 9% 3%*$8GJgas

7

• ReducerisktoVREinvestorstokeepWACClow• Reduceconnectioncostsbybuildingtransmissiontonewrenewablezones• Minimiseamountofdispatchablegenerationrequired,butstartbuildingitnow.• Continuetosupportbehindthemeterforsystemresilience

MorethanhalfofNSWcoalfleettocloseby2035– morelikelytobeearlierthanlater?• 4/5NSWcoalgeneratorstocloseinnext14years• NSWcoalcostsarerising• GladstoneinQLDandYallourn inVictoriaalsolikelytocloseby2032orthereabouts

8

Dependingonmixabout20GWnewpowerneededinNSW

9

0200400600800100012001400160018002000

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

ANNUAL

MWNEW

VRE

REQ

UIRED

ReplacingcoalinNSW

Liddell ValesPoint Eraring Bayswater MtPiper

NSWneedsd20GWpowerby2035Closure Years Annualnewbuild AnnualMWPowerat TotalpowerComment

TWh Date toclose TWh @32%capfactor GWLiddell 8.2 2022 4 2.1 732 2.9AnnouncedValesPoint 8.1 2029 11 0.7 262 2.9Eraring 17.8 2032 14 1.3 454 6.4AnnouncedBayswater 16.2 2035 17 1.0 339 5.8AnnouncedMtPiper 7.3 2043 25 0.3 105 2.6Total 57.6NSWdemand 70.8 5.31 1893 21

• Moreifbatteries,pumpedhydrohavetoberecharged• MoreforEVs• Buthowmuchdispatchable power?• Whatpolicywillminimisepriceandreliabilityuncertaintyfacingthisdemand?

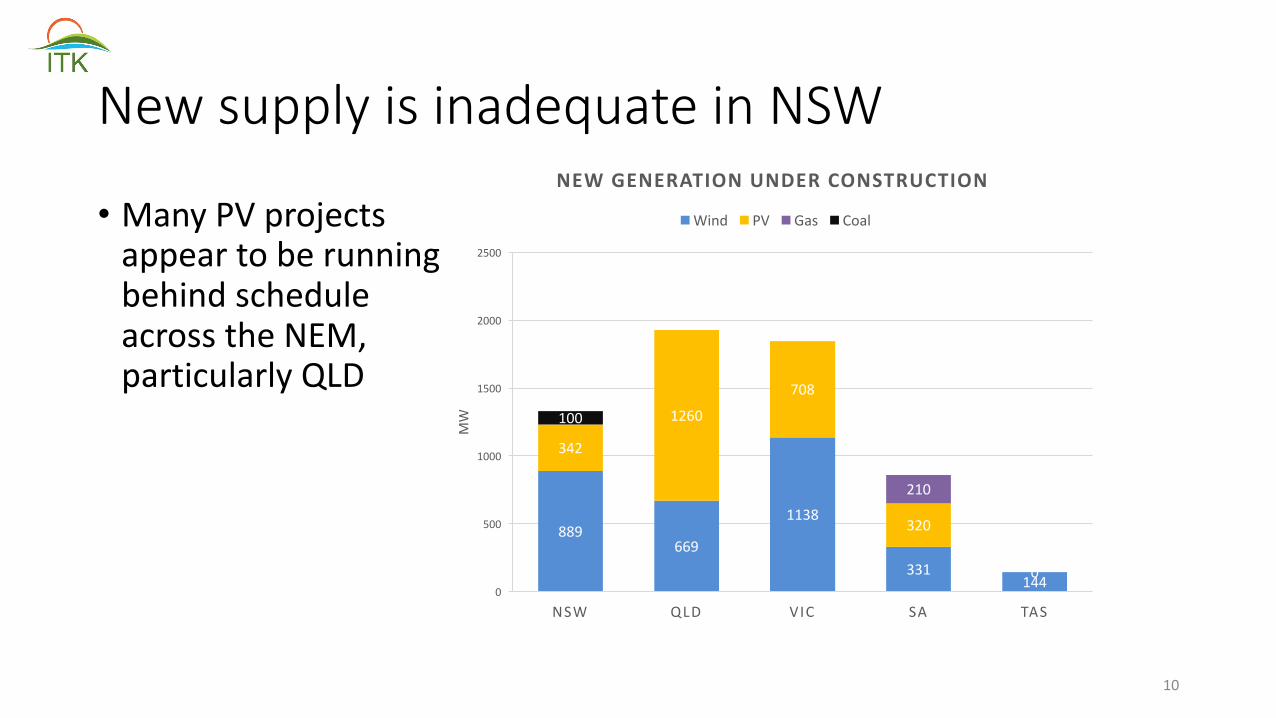

NewsupplyisinadequateinNSW

• ManyPVprojectsappeartoberunningbehindscheduleacrosstheNEM,particularlyQLD

10

889669

1138

331144

342

1260

708

320

0

210

100

0

500

1000

1500

2000

2500

NSW QLD VIC SA TAS

MW

NEWGENERATIONUNDERCONSTRUCTION

Wind PV Gas Coal

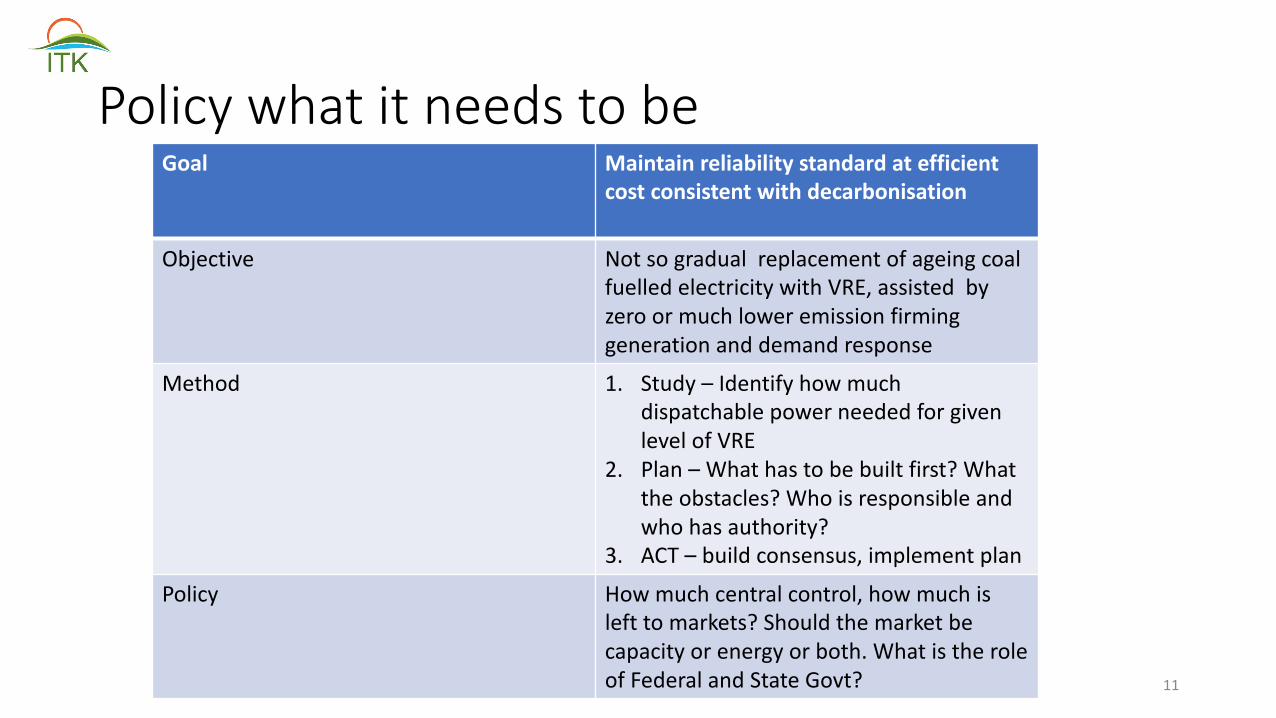

PolicywhatitneedstobeGoal Maintainreliabilitystandardatefficient

costconsistentwithdecarbonisation

Objective Notsogradual replacementofageingcoalfuelledelectricitywithVRE,assistedbyzeroormuchloweremissionfirminggenerationanddemandresponse

Method 1. Study– IdentifyhowmuchdispatchablepowerneededforgivenlevelofVRE

2. Plan– What hastobebuiltfirst?Whattheobstacles?Whoisresponsibleandwhohasauthority?

3. ACT– buildconsensus, implementplan

Policy Howmuchcentral control,howmuchislefttomarkets?Shouldthemarketbecapacityorenergyorboth.WhatistheroleofFederalandStateGovt? 11

Isthereanarchitectinthehouse?

• Energymarketswill likelyleadtoperiodsofundersupplyinthefirstinstanceleadstohighpricesandreliabilityissues• CurrentnewsupplyisarguablymostlyresultofLGCschemeratherthanresponsetoNEMpricesignals

• Someformofplanningisneededfornewtransmissionanyway.So• Capacityauctions,orGovtPPAswiththeobjectiveofincentivisingnewsupplybeforeitsneeded.• Govtbearscost,passedtoconsumers• Potentiallyahighercost,butlowerriskthanwaitingforologopolistic energymarkettosolveblackoutproblem• Essentiallythereisasystemarchitect,isitsobad?

12

Therulemakingprocesshasnovisionorgoal

13

CostVariableElecrticity

Balancingcost

Costofelectricity

Balancetechnologiesexpensivebuthowmuchisneeded?• Demandmanagement• Battery• Pumpedhydro• Concentratingthermal• Biomass• Hydrogen• Gas• Remainingcoal

Renewableguarantee

FederalGovtbasedonParisminimum

Retailerrenewableobligation

Reliabilityguarantee

ESBbasedonAEMOforecast

Somenewdispatchablegenerationprocurementmethod

14

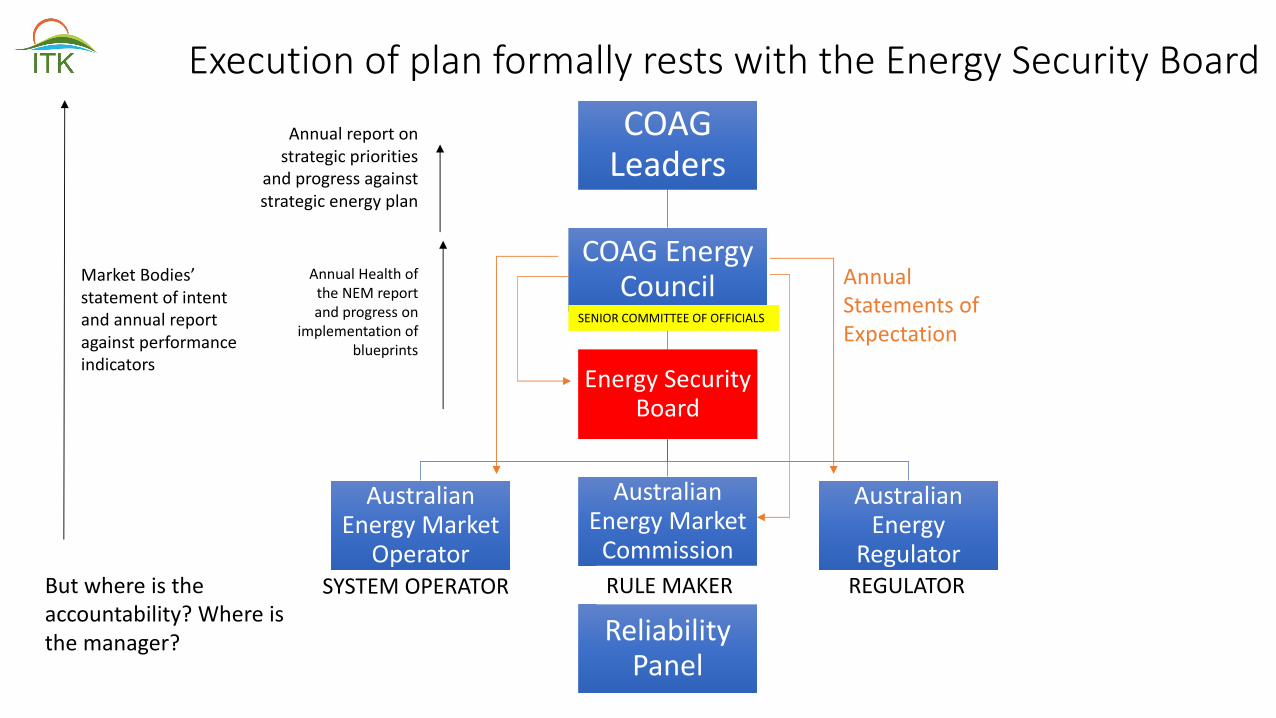

Aplanisrequired“By mid-2018, the COAG Energy Council should develop and maintain a strategic energy plan informed by the Panel’s blueprint to guide the operation and evolution of the National Electricity Market.” Finkel recommendation 7.1

ExecutionofplanformallyrestswiththeEnergySecurityBoardCOAGLeaders

COAGEnergyCouncil

EnergySecurityBoard

AustralianEnergyMarket

Operator

AustralianEnergyMarketCommission

ReliabilityPanel

AustralianEnergy

RegulatorSYSTEMOPERATOR REGULATORRULEMAKER

SENIORCOMMITTEEOFOFFICIALS

AnnualStatementsofExpectation

MarketBodies’statementofintentandannualreportagainstperformanceindicators

Annualreportonstrategicpriorities

andprogressagainststrategicenergyplan

AnnualHealthoftheNEMreportandprogresson

implementationofblueprints

Butwhereistheaccountability?Whereisthemanager?

Investorconsiderations

• Incumbentsincentivised towait• Benefitfromkeepingsupplytight• Expectnewbuildcoststofall,leaveittothelastminute• Butrisklosingmarketshareifnewentrantsgoearly• Riskregulation,orGovtpenaltyifseentobetooobviouslygouging

• Newentrants• Encouragedtotakeriskbyspotprice• Butneedtoprotectinvestmentlongerterm• Needlowbarrierstoentry• Easierwithaccesstoendusermarkets

16

17

AEMOhas thebeginningsofaplan

• TheplanwillleadtolotsofrelativelylowcostVRE• Butdoesnotyetincorporatefirming• Doesnotincorporateoverallsystemtargets• It’snotauniversallyacceptedplan

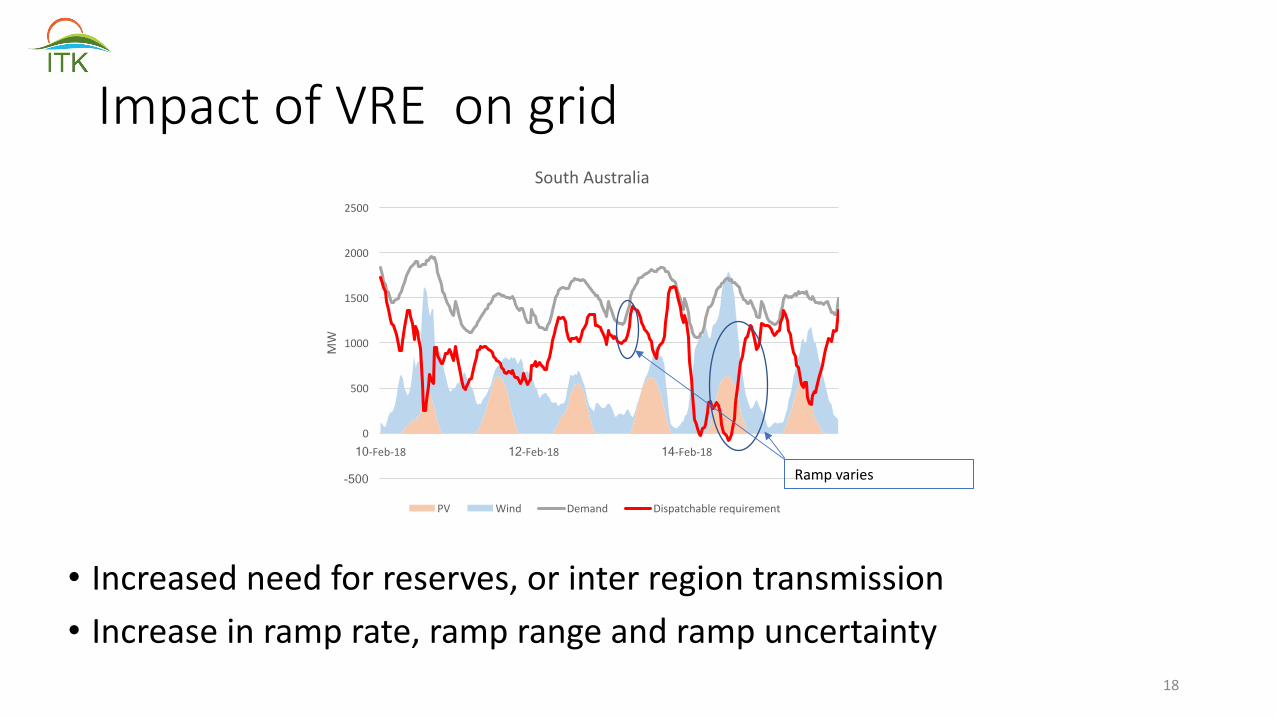

ImpactofVRE ongrid

• Increasedneedforreserves,orinterregiontransmission• Increaseinramprate,ramprangeandrampuncertainty

18

-500

0

500

1000

1500

2000

2500

10-Feb-18 12-Feb-18 14-Feb-18

MW

SouthAustralia

PV Wind Demand Dispatchablerequirement

Rampvaries

ImpactofVREonVREgenerators

• Morechanceofcurtailment• Curtailmentlowersvalue• ThenextunitofVREisworthlesstothesystemthantheunitthatcamebefore

• Lowerprice expectations

19

Costofindividuallyfirmedrenewables

20

$-

$50

$100

$150

$200

$250

$300

$350

Windnostore PVnostore Wind/PHES UtilityPV/PHES Biomass+AD Wind/Batt Conc.Solar UtilityPV/Batt Wind/H2 UtilityPV/H2 RooftopPV/Batt DryBiomass$2.5/GJ

Levelised

Costo

fEne

rgy($/M

Wh)

LCOEcontributions- 4hoursstorage2020estimates

collection initialconversion storage finalconversion

Source:ARENAstudyforthcoming

Lowercostswhenasystemviewistaken100%renewables

Power Energy LCOEGW TWh $MWh

PV 30 49Wind 43 159Total 73 208 50Spillagecost 6

HoursFirming 17 26 13Transmission 6Total 75SourceBlakersFeb2017

21

• Firminginvestmentmayneedcentralplanning• Transmission• Environment• Location• Quantity

• Blakers studyarguablyalreadyleadstoSnowy2.0

Carbatterypricesarefalling,butdata isanecdotal

22

0

20

40

60

80

100

120

140

160

180

200

ChevvyBolt TeslaModel3 Audi Teslatruck

2015 2016 2017 2017

US/KW

H

Electriccarbattterypackprices

Residentialbatteries cost3X-6Xcarbatteries

23

0 200 400 600 800 1000 1200 1400 1600

TeslaPowerwall2GCLE-KwBe5.6

SunGrowSBP4K8Ampetus"Super"LithiumBYDB-BoxLVResidential

SolaXPowerStationSoltaro

Alpha-ESSECOS5AmpetusEnergyPod

LGAquionAspen48S-2.2

OpalStoragePylontechUS2000B

DCSPV5.0DCSPV5.0DCSPV10.0TrinabessPowercube

RedflowZcellArvioSiriusCapacitorModule

Hybrid"Home"PlusDeltaHybridE5

Simpliphi

$KWH

Residentialbatteriescheapest50%of35brands

Source:Solarquotes

Recommended