1

PILLAR 3 (BASEL III) DISCLOSURES AS ON 30.09.2019

CENTRAL BANK OF INDIA

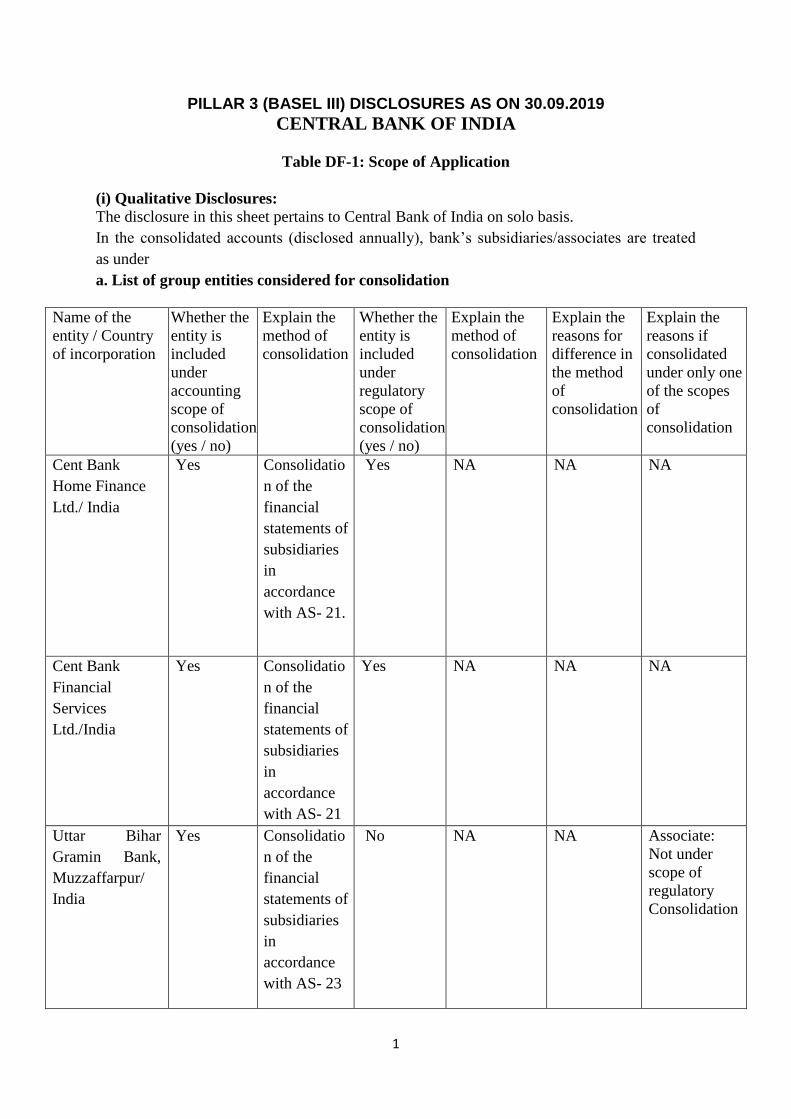

Table DF-1: Scope of Application

(i) Qualitative Disclosures:

The disclosure in this sheet pertains to Central Bank of India on solo basis.

In the consolidated accounts (disclosed annually), bank‟s subsidiaries/associates are treated

as under

a. List of group entities considered for consolidation

Name of the

entity / Country

of incorporation

Whether the

entity is

included

under

accounting

scope of

consolidation

(yes / no)

Explain the

method of

consolidation

Whether the

entity is

included

under

regulatory

scope of

consolidation

(yes / no)

Explain the

method of

consolidation

Explain the

reasons for

difference in

the method

of

consolidation

Explain the

reasons if

consolidated

under only one

of the scopes

of

consolidation

Cent Bank

Home Finance

Ltd./ India

Yes Consolidatio

n of the

financial

statements of

subsidiaries

in

accordance

with AS- 21.

Yes NA NA NA

Cent Bank

Financial

Services

Ltd./India

Yes Consolidatio

n of the

financial

statements of

subsidiaries

in

accordance

with AS- 21

Yes NA NA NA

Uttar Bihar

Gramin Bank,

Muzzaffarpur/

India

Yes Consolidatio

n of the

financial

statements of

subsidiaries

in

accordance

with AS- 23

No NA NA Associate:

Not under

scope of

regulatory

Consolidation

2

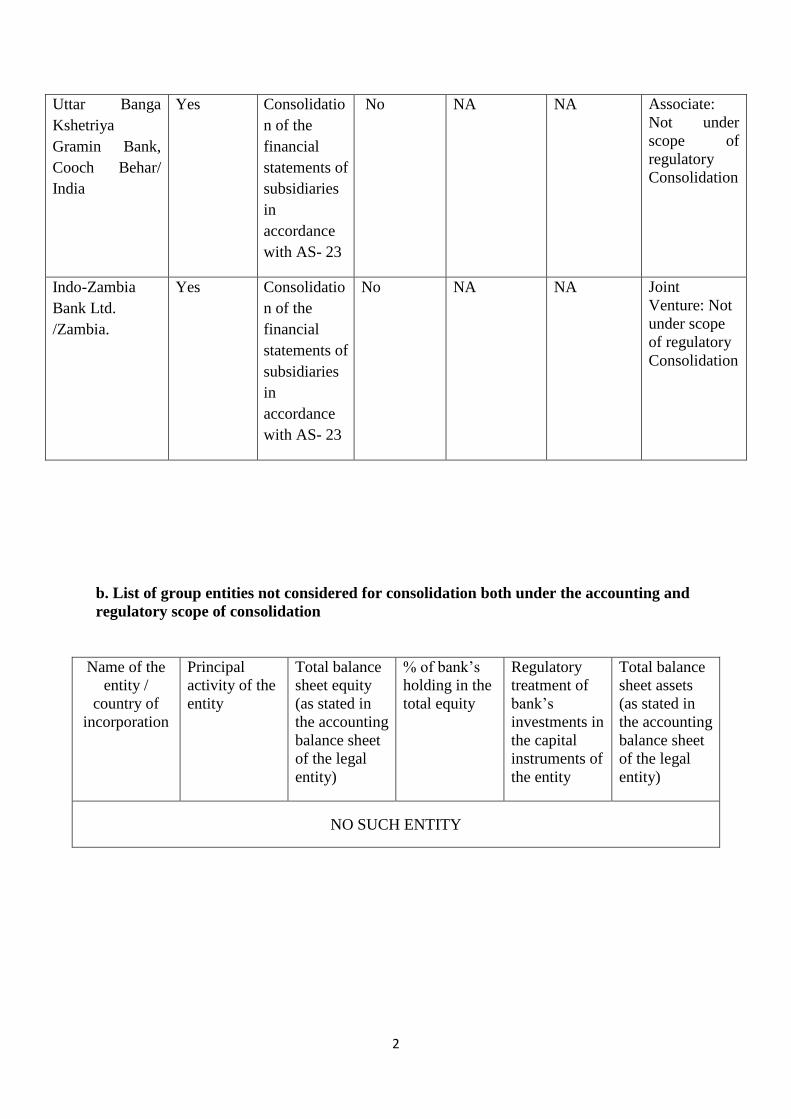

Uttar Banga

Kshetriya

Gramin Bank,

Cooch Behar/

India

Yes Consolidatio

n of the

financial

statements of

subsidiaries

in

accordance

with AS- 23

No NA NA Associate:

Not under

scope of

regulatory

Consolidation

Indo-Zambia

Bank Ltd.

/Zambia.

Yes Consolidatio

n of the

financial

statements of

subsidiaries

in

accordance

with AS- 23

No NA NA Joint

Venture: Not

under scope

of regulatory

Consolidation

b. List of group entities not considered for consolidation both under the accounting and

regulatory scope of consolidation

Name of the

entity /

country of

incorporation

Principal

activity of the

entity

Total balance

sheet equity

(as stated in

the accounting

balance sheet

of the legal

entity)

% of bank‟s

holding in the

total equity

Regulatory

treatment of

bank‟s

investments in

the capital

instruments of

the entity

Total balance

sheet assets

(as stated in

the accounting

balance sheet

of the legal

entity)

NO SUCH ENTITY

3

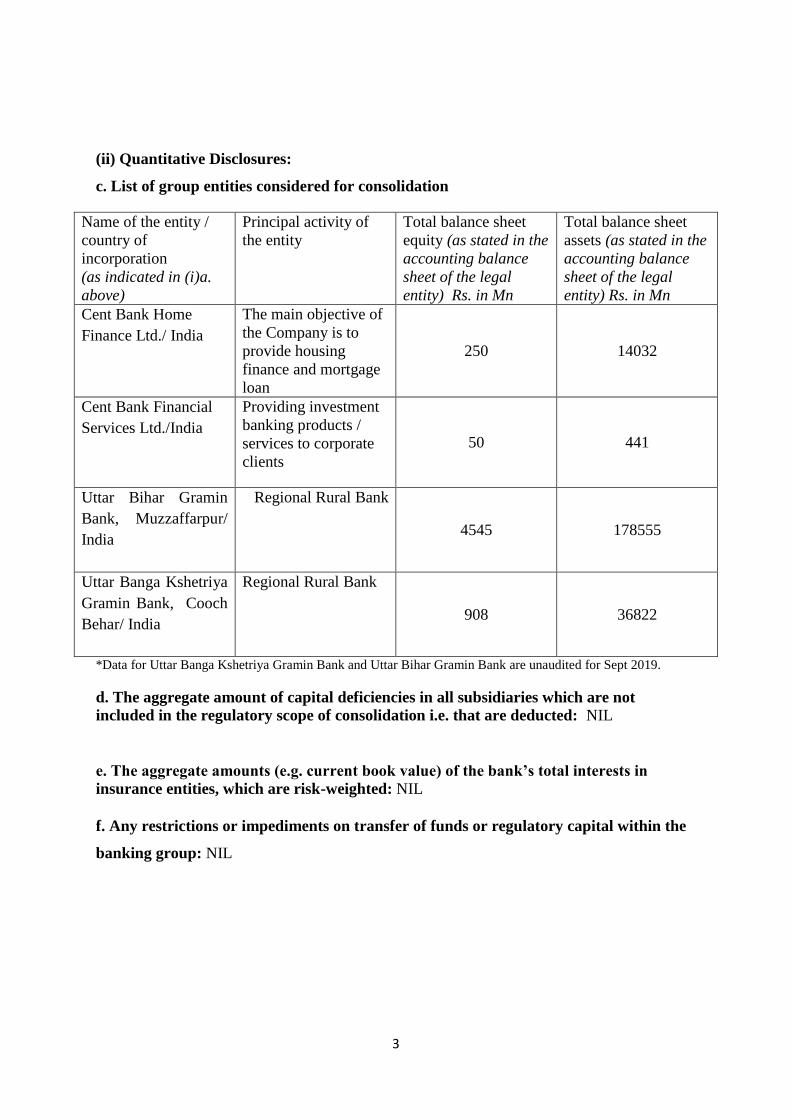

(ii) Quantitative Disclosures:

c. List of group entities considered for consolidation

Name of the entity /

country of

incorporation

(as indicated in (i)a.

above)

Principal activity of

the entity

Total balance sheet

equity (as stated in the

accounting balance

sheet of the legal

entity) Rs. in Mn

Total balance sheet

assets (as stated in the

accounting balance

sheet of the legal

entity) Rs. in Mn

Cent Bank Home

Finance Ltd./ India

The main objective of

the Company is to

provide housing

finance and mortgage

loan

250 14032

Cent Bank Financial

Services Ltd./India

Providing investment

banking products /

services to corporate

clients

50 441

Uttar Bihar Gramin

Bank, Muzzaffarpur/

India

Regional Rural Bank

4545 178555

Uttar Banga Kshetriya

Gramin Bank, Cooch

Behar/ India

Regional Rural Bank

908 36822

*Data for Uttar Banga Kshetriya Gramin Bank and Uttar Bihar Gramin Bank are unaudited for Sept 2019.

d. The aggregate amount of capital deficiencies in all subsidiaries which are not

included in the regulatory scope of consolidation i.e. that are deducted: NIL

e. The aggregate amounts (e.g. current book value) of the bank’s total interests in

insurance entities, which are risk-weighted: NIL

f. Any restrictions or impediments on transfer of funds or regulatory capital within the

banking group: NIL

4

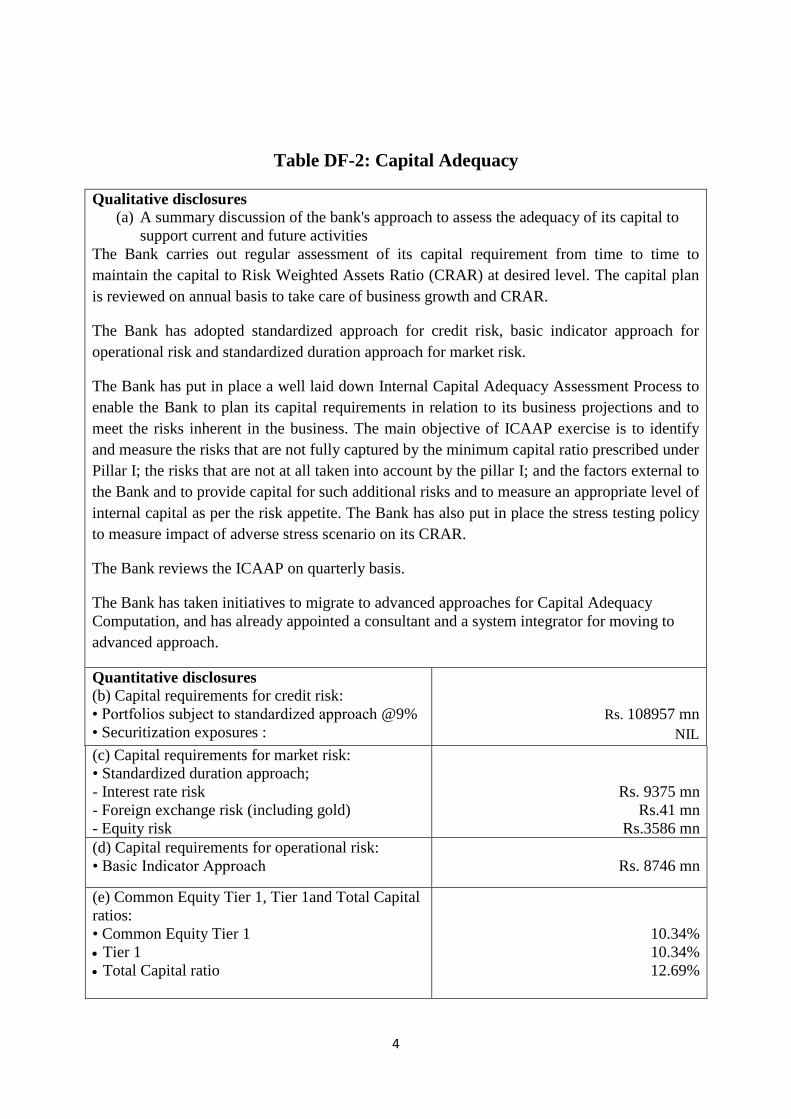

Table DF-2: Capital Adequacy

Qualitative disclosures (a) A summary discussion of the bank's approach to assess the adequacy of its capital to

support current and future activities

The Bank carries out regular assessment of its capital requirement from time to time to

maintain the capital to Risk Weighted Assets Ratio (CRAR) at desired level. The capital plan

is reviewed on annual basis to take care of business growth and CRAR.

The Bank has adopted standardized approach for credit risk, basic indicator approach for

operational risk and standardized duration approach for market risk.

The Bank has put in place a well laid down Internal Capital Adequacy Assessment Process to

enable the Bank to plan its capital requirements in relation to its business projections and to

meet the risks inherent in the business. The main objective of ICAAP exercise is to identify

and measure the risks that are not fully captured by the minimum capital ratio prescribed under

Pillar I; the risks that are not at all taken into account by the pillar I; and the factors external to

the Bank and to provide capital for such additional risks and to measure an appropriate level of

internal capital as per the risk appetite. The Bank has also put in place the stress testing policy

to measure impact of adverse stress scenario on its CRAR.

The Bank reviews the ICAAP on quarterly basis.

The Bank has taken initiatives to migrate to advanced approaches for Capital Adequacy

Computation, and has already appointed a consultant and a system integrator for moving to

advanced approach.

Quantitative disclosures (b) Capital requirements for credit risk:

• Portfolios subject to standardized approach @9%

• Securitization exposures :

Rs. 108957 mn

NIL

(c) Capital requirements for market risk:

• Standardized duration approach;

- Interest rate risk

- Foreign exchange risk (including gold)

- Equity risk

Rs. 9375 mn

Rs.41 mn

Rs.3586 mn

(d) Capital requirements for operational risk:

• Basic Indicator Approach

Rs. 8746 mn

(e) Common Equity Tier 1, Tier 1and Total Capital

ratios:

• Common Equity Tier 1

Tier 1

Total Capital ratio

10.34%

10.34%

12.69%

5

General qualitative disclosure requirement

A committee of Board of Directors regularly oversees the Bank‟s Risk Management

policies/practices under various risks viz. credit, operational, market, etc. The Bank also has

separate committees comprising of top executives of Bank, headed by Managing Director &

CEO and Executive Directors, such as Asset Liability Management, Credit Risk

Management, and Operational Risk Management. These committees meet at regular intervals

to assess and monitor the level of risk under various operations and initiate appropriate

mitigation measures wherever necessary.

The Risk Management Department at Central Office headed by the Chief Risk Officer

(General Manager) measures, controls and manages risk within the limits set by the Board

and enforces compliance with risk parameters set by the committees. The General Manager is

assisted by a team of Deputy General Managers, Assistant General Managers, Chief

Managers, Senior Managers and Managers.

Risk Managers are posted at all Zonal offices who act as extended arms of Risk Management

Department of Central Office. Risk Managers have also been identified at Regional Offices.

The Bank has in place detailed policies such as Credit Risk Policy, Credit Risk Mitigation

and Collateral Management Policy, Enterprise Risk Management Policy, Market Discipline

& Disclosure Policy, Operational Risk Management Policies, ALM Policy, Market Risk

Management Policy, etc.

Besides these, the Loan Policies prescribe the parameters governing loan sourcing, guidelines

on appraisal and evaluation of credit proposals, lending powers of delegated authorities,

exposure norms, prudential limits, and monitoring and supervising the credit portfolio.

Credit Monitoring Department headed by a General Manager monitors the loan portfolio,

identifies Special Mention Accounts and takes corrective measures. Loan Review Mechanism

is implemented by the department apart from managing of accounts under CDR mechanism.

The Bank has introduced rating models for different segments of borrowers including for

retail lending schemes which measure the risks associated with counterparties and helps in

making lending and pricing decisions. In case of large borrowers, credit risk assessment

models evaluate financial risk, Industry risk, management risk and business risk of the

counter party. Conduct of account is also factored in for arriving at an overall rating of the

counter party. Facility rating module is also available in the rating tool. Where parental

support as corporate guarantee is available, it is also factored in.

6

Table DF-3

Credit risk: General disclosures for all banks

Qualitative Disclosures

Credit risk

Impaired :

The Working Group to review the existing prudential guidelines on restructuring of advances

by banks/financial institutions in its report dated 20.07.2012 observed that as per

international accounting standards, accounts are generally treated as impaired on

restructuring and recommended that similar practice should be followed in India. Ind AS 109

contains guidance on the recognition, derecognition, classification and measurement of

financial instruments including impairment and hedge accounting

A Non-Performing Asset shall be a loan or an advance where-

(i) Interest and/or instalment of principal remain overdue for a period of more than

90 days in respect of a Term Loan;

(ii) The account remains out of order for 90 days

(iii) The bill remains overdue for a period of more than 90 days in the case of Bills

Purchased and Discounted

(iv) In case of advances granted for Agricultural purposes

a) The instalment of principal or interest thereon remains overdue for two crop

seasons for short duration crops

b) The instalment of principal or interest thereon remains overdue for one crop

season for long duration crops

(v) The amount of liquidity facility remains outstanding for more than 90 days, in

respect of a securitization transaction undertaken in terms of guidelines on

securitization dated February 1, 2006.

(vi) in respect of derivative transactions, the overdue receivables representing positive

mark to- market value of a derivative contract, if these remain unpaid for a period

of 90 days from the specified due date for payment.

Out of Order:

An account should be treated as “Out of Order” if the outstanding balance remains

continuously in excess of the sanctioned limit/drawing power, or in cases where the

outstanding balance in the principal operating account is less than the sanctioned

limit/drawing power, but there are no credits continuously for 90 days as on the date of

balance sheet or credits are not enough to cover the interest debited in the account during

the same period.

7

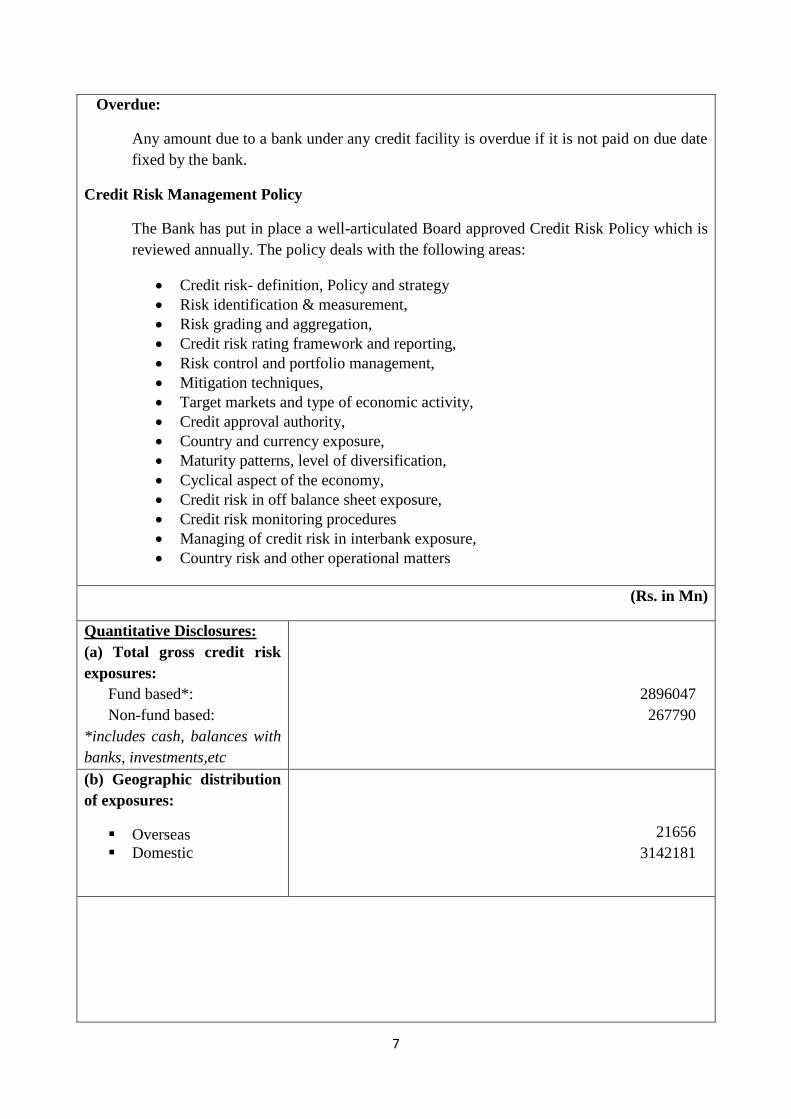

Overdue:

Any amount due to a bank under any credit facility is overdue if it is not paid on due date

fixed by the bank.

Credit Risk Management Policy

The Bank has put in place a well-articulated Board approved Credit Risk Policy which is

reviewed annually. The policy deals with the following areas:

Credit risk- definition, Policy and strategy

Risk identification & measurement,

Risk grading and aggregation,

Credit risk rating framework and reporting,

Risk control and portfolio management,

Mitigation techniques,

Target markets and type of economic activity,

Credit approval authority,

Country and currency exposure,

Maturity patterns, level of diversification,

Cyclical aspect of the economy,

Credit risk in off balance sheet exposure,

Credit risk monitoring procedures

Managing of credit risk in interbank exposure,

Country risk and other operational matters

(Rs. in Mn)

Quantitative Disclosures:

(a) Total gross credit risk

exposures:

Fund based*:

Non-fund based:

*includes cash, balances with

banks, investments,etc

2896047

267790

(b) Geographic distribution

of exposures:

Overseas

Domestic

21656

3142181

8

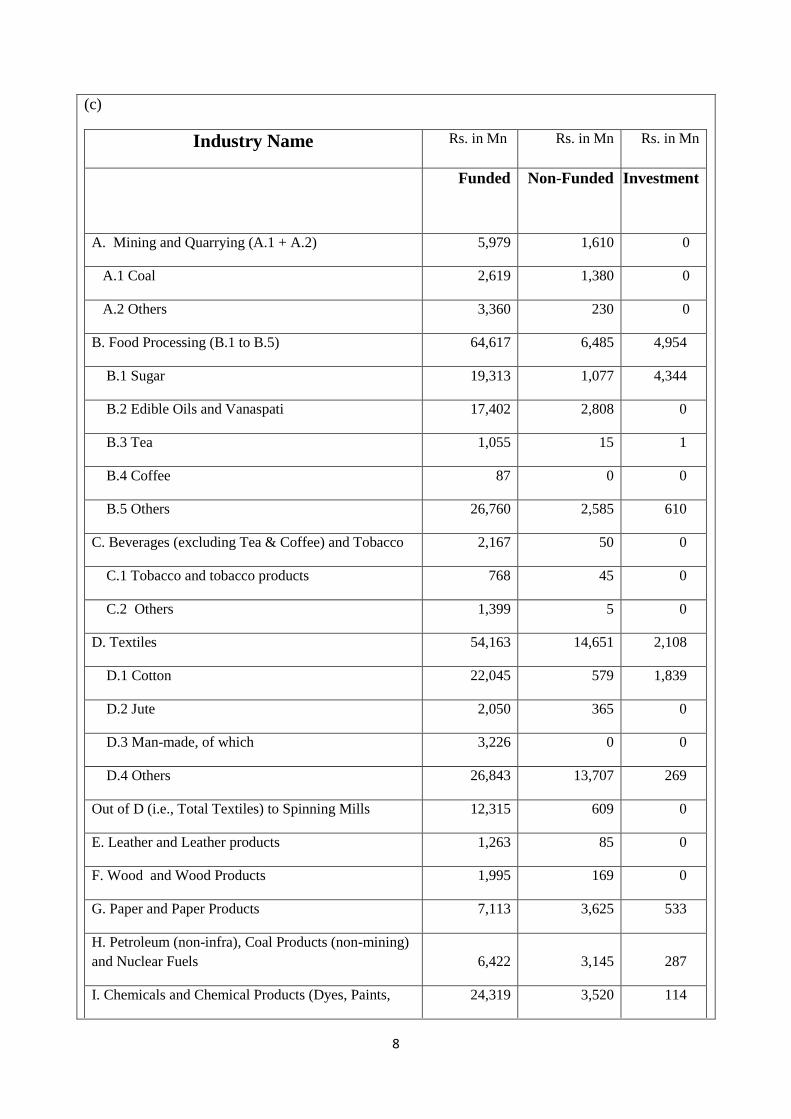

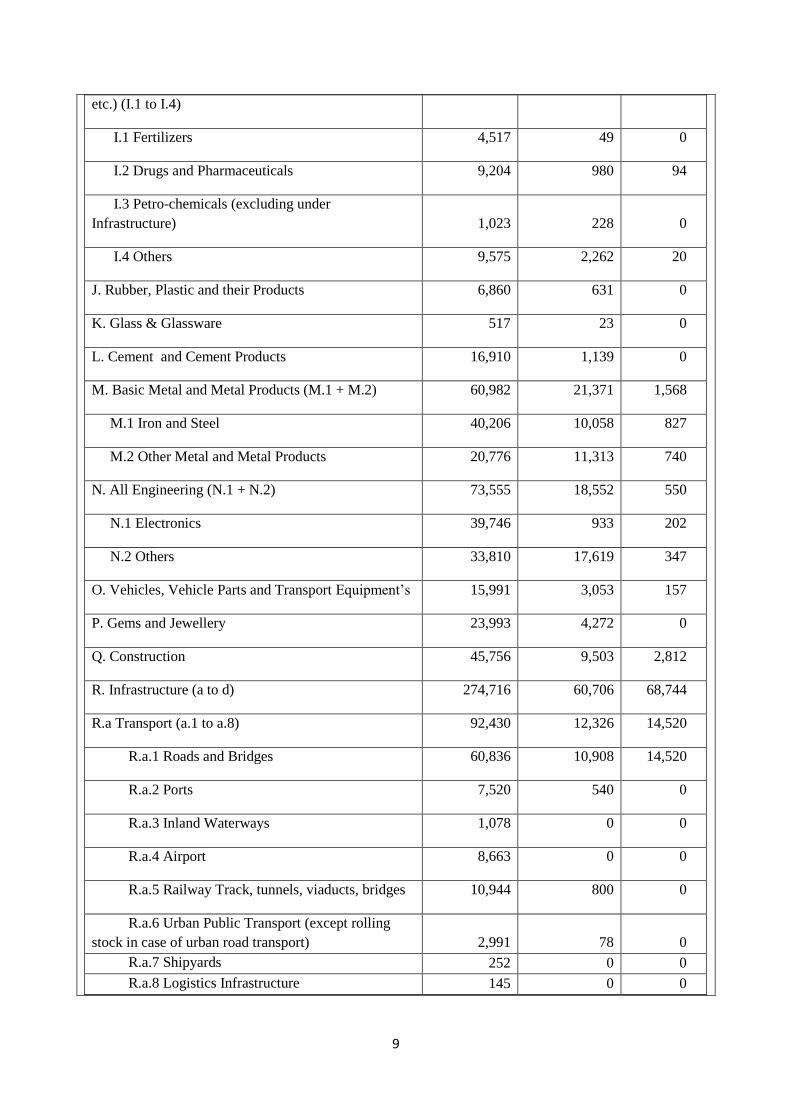

(c)

Industry Name Rs. in Mn Rs. in Mn Rs. in Mn

Funded Non-Funded Investment

A. Mining and Quarrying (A.1 + A.2) 5,979 1,610 0

A.1 Coal 2,619 1,380 0

A.2 Others 3,360 230 0

B. Food Processing (B.1 to B.5) 64,617 6,485 4,954

B.1 Sugar 19,313 1,077 4,344

B.2 Edible Oils and Vanaspati 17,402 2,808 0

B.3 Tea 1,055 15 1

B.4 Coffee 87 0 0

B.5 Others 26,760 2,585 610

C. Beverages (excluding Tea & Coffee) and Tobacco 2,167 50 0

C.1 Tobacco and tobacco products 768 45 0

C.2 Others 1,399 5 0

D. Textiles 54,163 14,651 2,108

D.1 Cotton 22,045 579 1,839

D.2 Jute 2,050 365 0

D.3 Man-made, of which 3,226 0 0

D.4 Others 26,843 13,707 269

Out of D (i.e., Total Textiles) to Spinning Mills 12,315 609 0

E. Leather and Leather products 1,263 85 0

F. Wood and Wood Products 1,995 169 0

G. Paper and Paper Products 7,113 3,625 533

H. Petroleum (non-infra), Coal Products (non-mining)

and Nuclear Fuels 6,422 3,145 287

I. Chemicals and Chemical Products (Dyes, Paints, 24,319 3,520 114

9

etc.) (I.1 to I.4)

I.1 Fertilizers 4,517 49 0

I.2 Drugs and Pharmaceuticals 9,204 980 94

I.3 Petro-chemicals (excluding under

Infrastructure) 1,023 228 0

I.4 Others 9,575 2,262 20

J. Rubber, Plastic and their Products 6,860 631 0

K. Glass & Glassware 517 23 0

L. Cement and Cement Products 16,910 1,139 0

M. Basic Metal and Metal Products (M.1 + M.2) 60,982 21,371 1,568

M.1 Iron and Steel 40,206 10,058 827

M.2 Other Metal and Metal Products 20,776 11,313 740

N. All Engineering (N.1 + N.2) 73,555 18,552 550

N.1 Electronics 39,746 933 202

N.2 Others 33,810 17,619 347

O. Vehicles, Vehicle Parts and Transport Equipment‟s 15,991 3,053 157

P. Gems and Jewellery 23,993 4,272 0

Q. Construction 45,756 9,503 2,812

R. Infrastructure (a to d) 274,716 60,706 68,744

R.a Transport (a.1 to a.8) 92,430 12,326 14,520

R.a.1 Roads and Bridges 60,836 10,908 14,520

R.a.2 Ports 7,520 540 0

R.a.3 Inland Waterways 1,078 0 0

R.a.4 Airport 8,663 0 0

R.a.5 Railway Track, tunnels, viaducts, bridges 10,944 800 0

R.a.6 Urban Public Transport (except rolling

stock in case of urban road transport) 2,991 78 0

R.a.7 Shipyards 252 0 0

R.a.8 Logistics Infrastructure 145 0 0

10

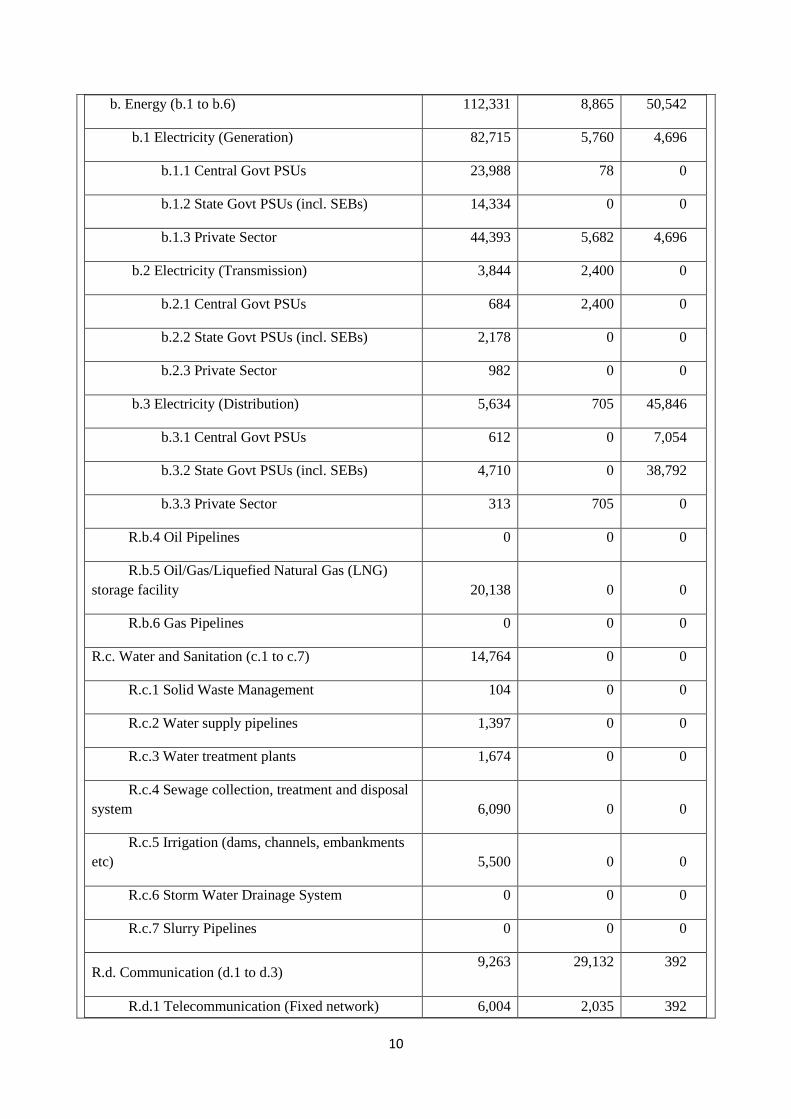

b. Energy (b.1 to b.6) 112,331 8,865 50,542

b.1 Electricity (Generation) 82,715 5,760 4,696

b.1.1 Central Govt PSUs 23,988 78 0

b.1.2 State Govt PSUs (incl. SEBs) 14,334 0 0

b.1.3 Private Sector 44,393 5,682 4,696

b.2 Electricity (Transmission) 3,844 2,400 0

b.2.1 Central Govt PSUs 684 2,400 0

b.2.2 State Govt PSUs (incl. SEBs) 2,178 0 0

b.2.3 Private Sector 982 0 0

b.3 Electricity (Distribution) 5,634 705 45,846

b.3.1 Central Govt PSUs 612 0 7,054

b.3.2 State Govt PSUs (incl. SEBs) 4,710 0 38,792

b.3.3 Private Sector 313 705 0

R.b.4 Oil Pipelines 0 0 0

R.b.5 Oil/Gas/Liquefied Natural Gas (LNG)

storage facility 20,138 0 0

R.b.6 Gas Pipelines 0 0 0

R.c. Water and Sanitation (c.1 to c.7) 14,764 0 0

R.c.1 Solid Waste Management 104 0 0

R.c.2 Water supply pipelines 1,397 0 0

R.c.3 Water treatment plants 1,674 0 0

R.c.4 Sewage collection, treatment and disposal

system 6,090 0 0

R.c.5 Irrigation (dams, channels, embankments

etc) 5,500 0 0

R.c.6 Storm Water Drainage System 0 0 0

R.c.7 Slurry Pipelines 0 0 0

R.d. Communication (d.1 to d.3) 9,263 29,132 392

R.d.1 Telecommunication (Fixed network) 6,004 2,035 392

11

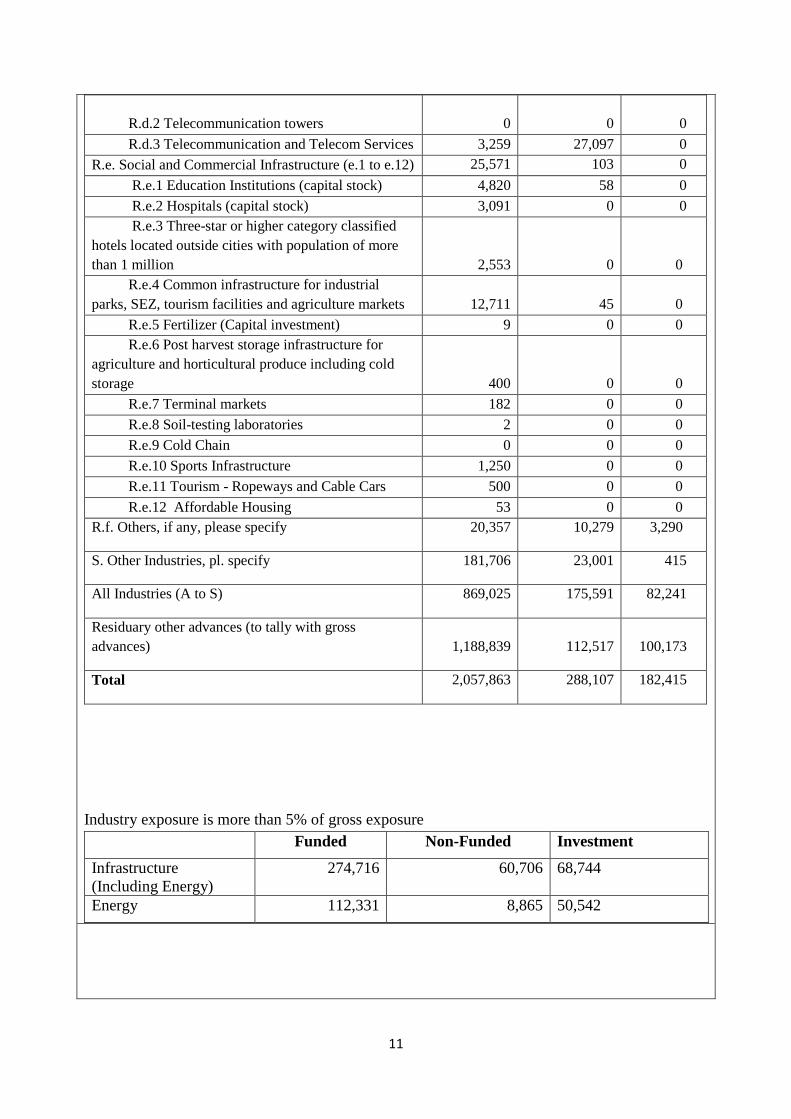

R.d.2 Telecommunication towers 0 0 0

R.d.3 Telecommunication and Telecom Services 3,259 27,097 0

R.e. Social and Commercial Infrastructure (e.1 to e.12) 25,571 103 0

R.e.1 Education Institutions (capital stock) 4,820 58 0

R.e.2 Hospitals (capital stock) 3,091 0 0

R.e.3 Three-star or higher category classified

hotels located outside cities with population of more

than 1 million 2,553 0 0

R.e.4 Common infrastructure for industrial

parks, SEZ, tourism facilities and agriculture markets 12,711 45 0

R.e.5 Fertilizer (Capital investment) 9 0 0

R.e.6 Post harvest storage infrastructure for

agriculture and horticultural produce including cold

storage 400 0 0

R.e.7 Terminal markets 182 0 0

R.e.8 Soil-testing laboratories 2 0 0

R.e.9 Cold Chain 0 0 0

R.e.10 Sports Infrastructure 1,250 0 0

R.e.11 Tourism - Ropeways and Cable Cars 500 0 0

R.e.12 Affordable Housing 53 0 0

R.f. Others, if any, please specify 20,357 10,279 3,290

S. Other Industries, pl. specify 181,706 23,001 415

All Industries (A to S) 869,025 175,591 82,241

Residuary other advances (to tally with gross

advances) 1,188,839 112,517 100,173

Total 2,057,863 288,107 182,415

Industry exposure is more than 5% of gross exposure

Funded Non-Funded Investment

Infrastructure

(Including Energy)

274,716 60,706 68,744

Energy 112,331 8,865 50,542

12

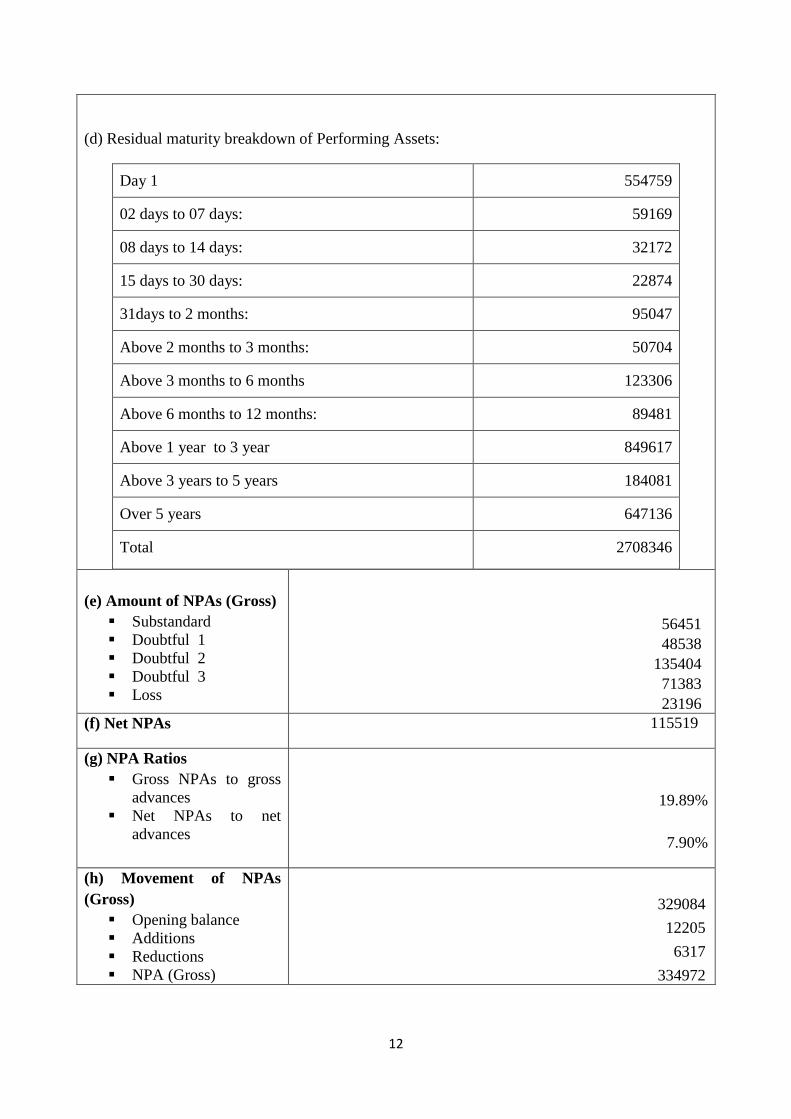

(d) Residual maturity breakdown of Performing Assets:

Day 1 554759

02 days to 07 days: 59169

08 days to 14 days: 32172

15 days to 30 days: 22874

31days to 2 months: 95047

Above 2 months to 3 months: 50704

Above 3 months to 6 months 123306

Above 6 months to 12 months: 89481

Above 1 year to 3 year 849617

Above 3 years to 5 years 184081

Over 5 years 647136

Total 2708346

(e) Amount of NPAs (Gross)

Substandard

Doubtful 1

Doubtful 2

Doubtful 3

Loss

56451

48538

135404

71383

23196

(f) Net NPAs 115519

(g) NPA Ratios

Gross NPAs to gross

advances

Net NPAs to net

advances

19.89%

7.90%

(h) Movement of NPAs

(Gross)

Opening balance

Additions

Reductions

NPA (Gross)

329084

12205

6317

334972

13

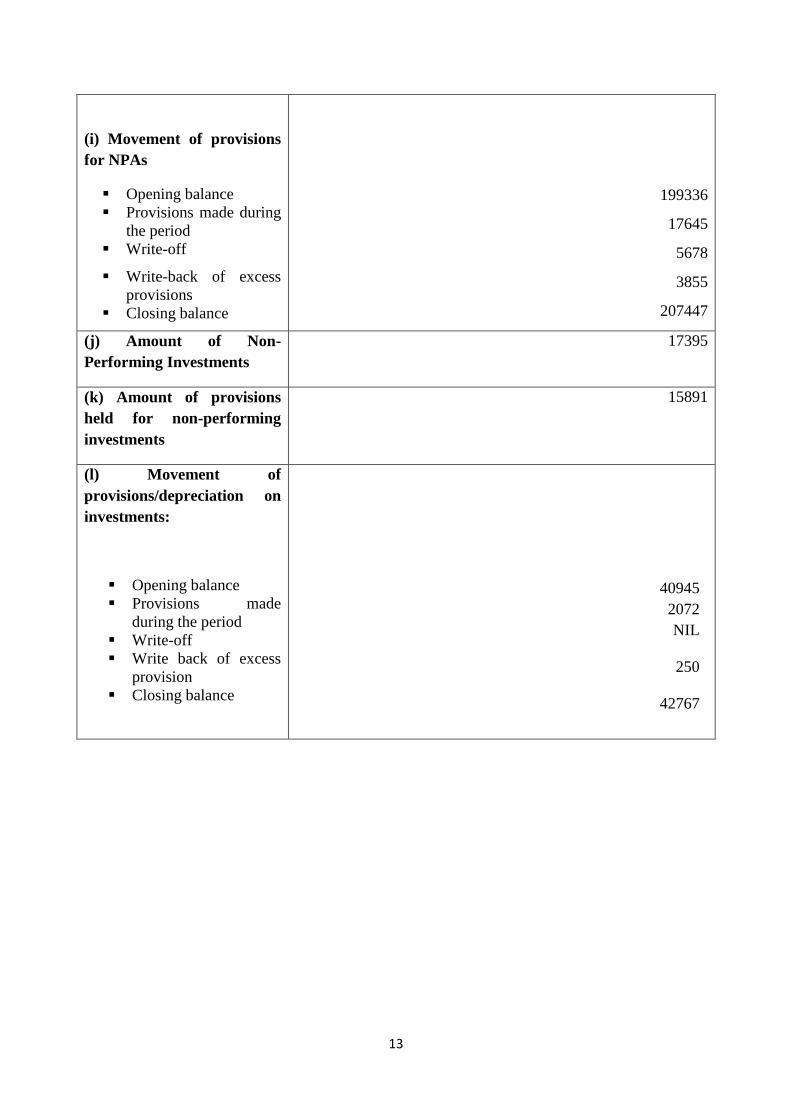

(i) Movement of provisions

for NPAs

Opening balance

Provisions made during

the period

Write-off

Write-back of excess

provisions

Closing balance

199336

17645

5678

3855

207447

(j) Amount of Non-

Performing Investments

17395

(k) Amount of provisions

held for non-performing

investments

15891

(l) Movement of

provisions/depreciation on

investments:

Opening balance

Provisions made

during the period

Write-off

Write back of excess

provision

Closing balance

40945

2072

NIL

250

42767

14

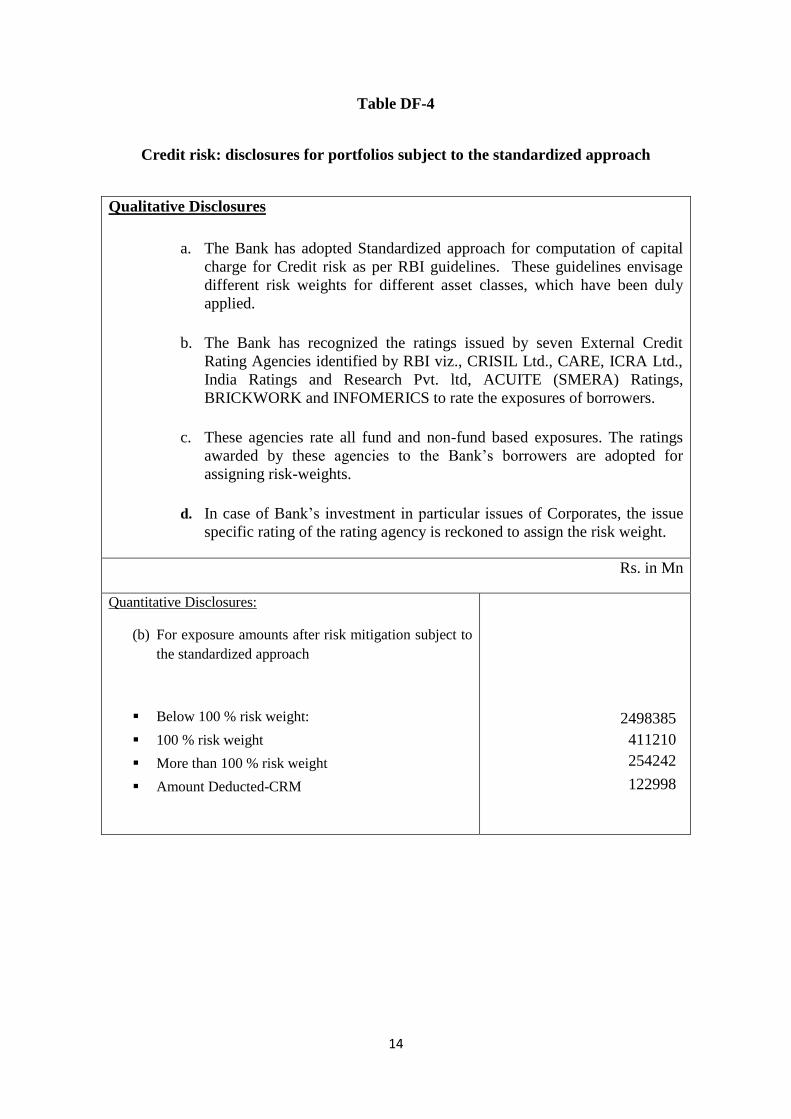

Table DF-4

Credit risk: disclosures for portfolios subject to the standardized approach

Qualitative Disclosures

a. The Bank has adopted Standardized approach for computation of capital

charge for Credit risk as per RBI guidelines. These guidelines envisage

different risk weights for different asset classes, which have been duly

applied.

b. The Bank has recognized the ratings issued by seven External Credit

Rating Agencies identified by RBI viz., CRISIL Ltd., CARE, ICRA Ltd.,

India Ratings and Research Pvt. ltd, ACUITE (SMERA) Ratings,

BRICKWORK and INFOMERICS to rate the exposures of borrowers.

c. These agencies rate all fund and non-fund based exposures. The ratings

awarded by these agencies to the Bank‟s borrowers are adopted for

assigning risk-weights.

d. In case of Bank‟s investment in particular issues of Corporates, the issue

specific rating of the rating agency is reckoned to assign the risk weight.

Rs. in Mn

Quantitative Disclosures:

(b) For exposure amounts after risk mitigation subject to

the standardized approach

Below 100 % risk weight:

100 % risk weight

More than 100 % risk weight

Amount Deducted-CRM

2498385

411210

254242

122998

15

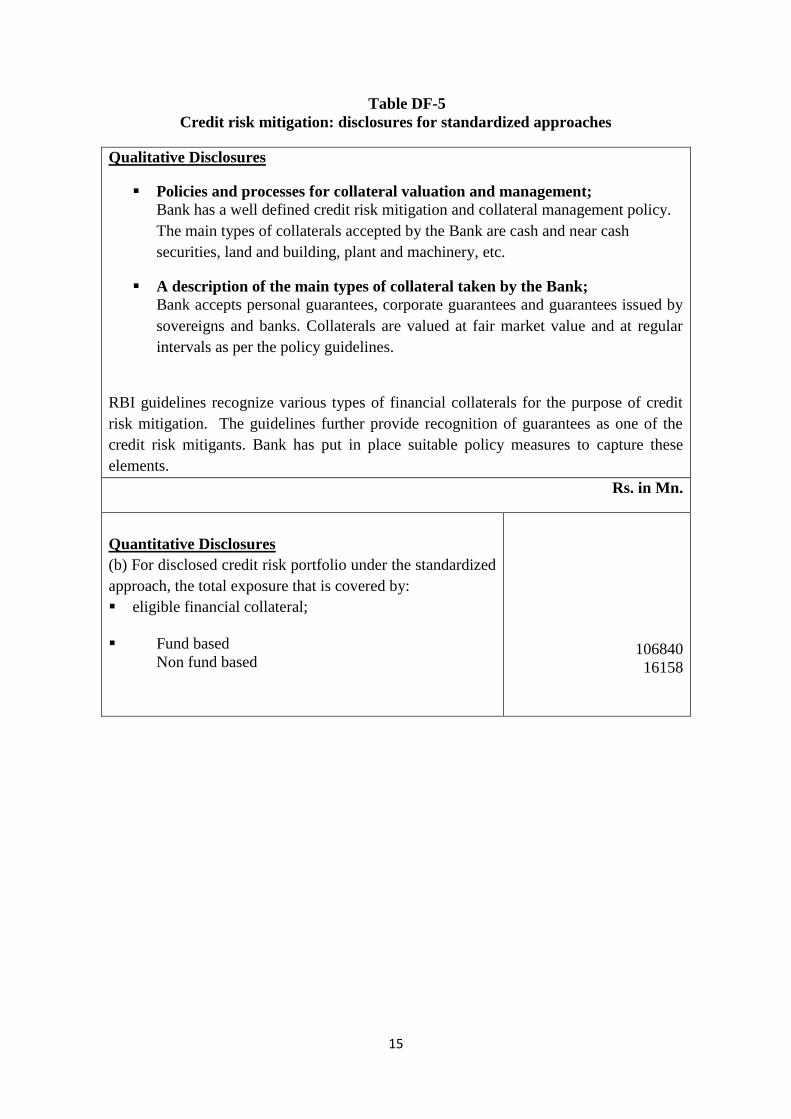

Table DF-5

Credit risk mitigation: disclosures for standardized approaches

Qualitative Disclosures

Policies and processes for collateral valuation and management;

Bank has a well defined credit risk mitigation and collateral management policy.

The main types of collaterals accepted by the Bank are cash and near cash

securities, land and building, plant and machinery, etc.

A description of the main types of collateral taken by the Bank;

Bank accepts personal guarantees, corporate guarantees and guarantees issued by

sovereigns and banks. Collaterals are valued at fair market value and at regular

intervals as per the policy guidelines.

RBI guidelines recognize various types of financial collaterals for the purpose of credit

risk mitigation. The guidelines further provide recognition of guarantees as one of the

credit risk mitigants. Bank has put in place suitable policy measures to capture these

elements.

Rs. in Mn.

Quantitative Disclosures

(b) For disclosed credit risk portfolio under the standardized

approach, the total exposure that is covered by:

eligible financial collateral;

Fund based

Non fund based

106840

16158

16

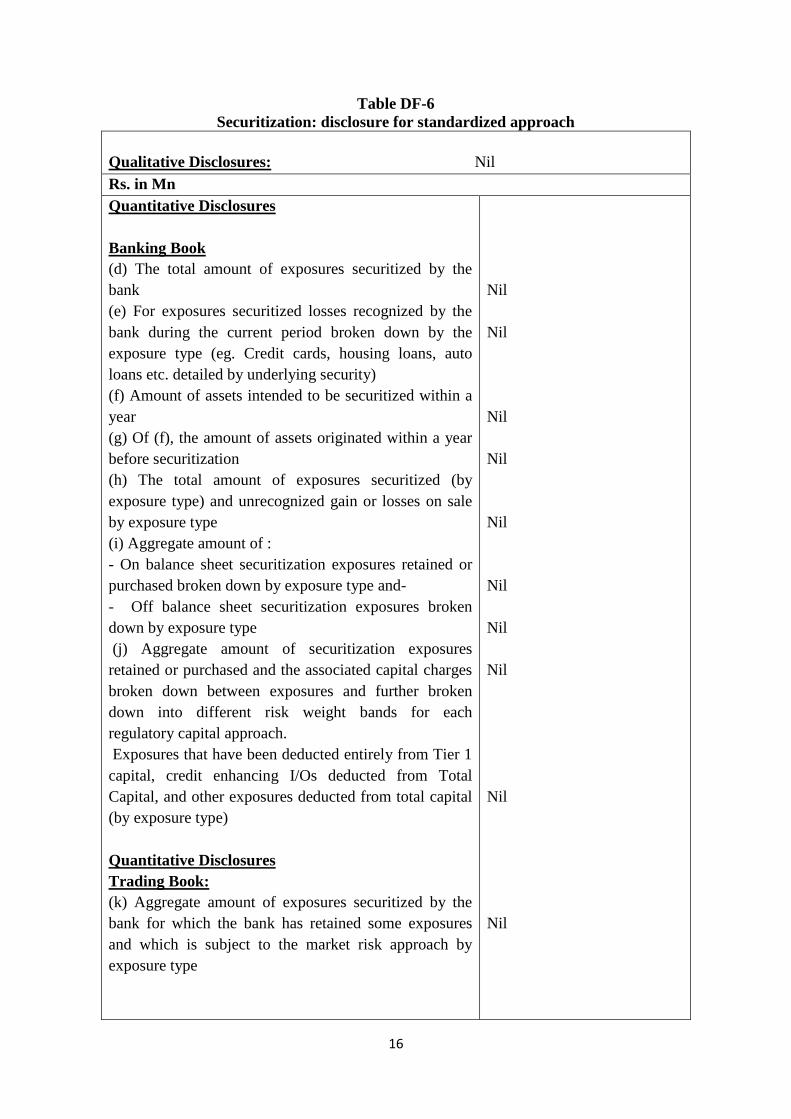

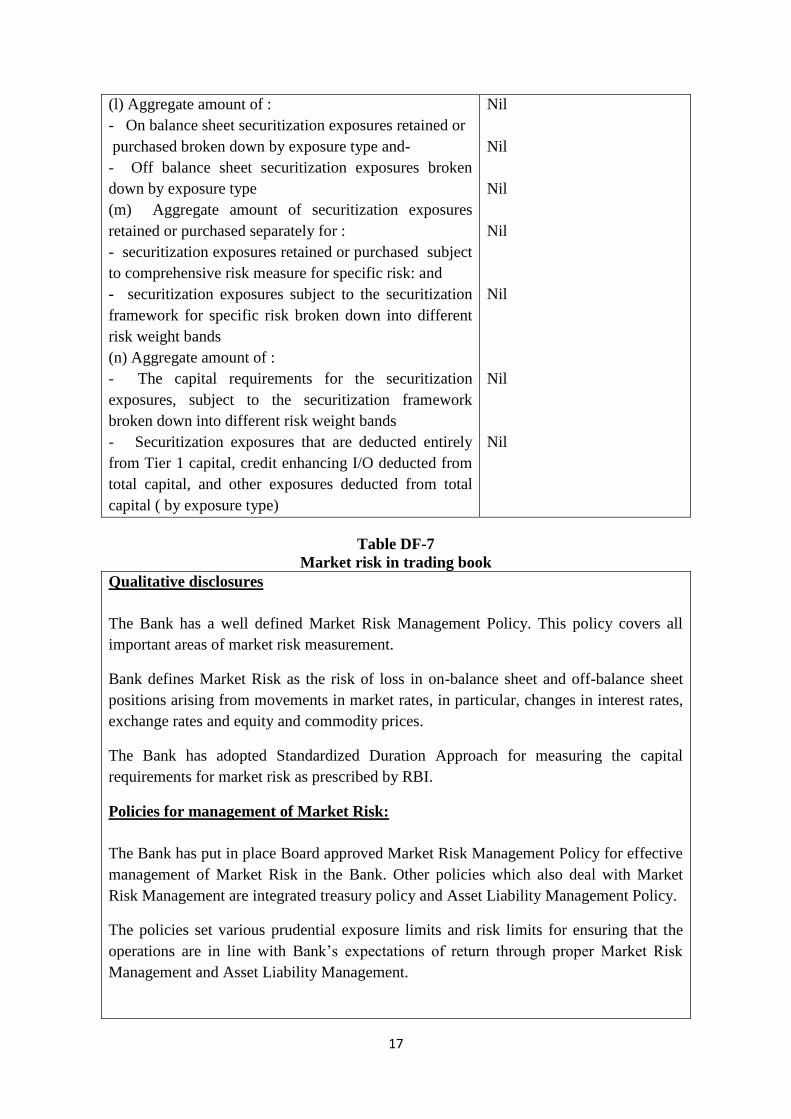

Table DF-6

Securitization: disclosure for standardized approach

Qualitative Disclosures: Nil

Rs. in Mn

Quantitative Disclosures

Banking Book

(d) The total amount of exposures securitized by the

bank

(e) For exposures securitized losses recognized by the

bank during the current period broken down by the

exposure type (eg. Credit cards, housing loans, auto

loans etc. detailed by underlying security)

(f) Amount of assets intended to be securitized within a

year

(g) Of (f), the amount of assets originated within a year

before securitization

(h) The total amount of exposures securitized (by

exposure type) and unrecognized gain or losses on sale

by exposure type

(i) Aggregate amount of :

- On balance sheet securitization exposures retained or

purchased broken down by exposure type and-

- Off balance sheet securitization exposures broken

down by exposure type

(j) Aggregate amount of securitization exposures

retained or purchased and the associated capital charges

broken down between exposures and further broken

down into different risk weight bands for each

regulatory capital approach.

Exposures that have been deducted entirely from Tier 1

capital, credit enhancing I/Os deducted from Total

Capital, and other exposures deducted from total capital

(by exposure type)

Quantitative Disclosures

Trading Book:

(k) Aggregate amount of exposures securitized by the

bank for which the bank has retained some exposures

and which is subject to the market risk approach by

exposure type

Nil

Nil

Nil

Nil

Nil

Nil

Nil

Nil

Nil

Nil

17

(l) Aggregate amount of :

- On balance sheet securitization exposures retained or

purchased broken down by exposure type and-

- Off balance sheet securitization exposures broken

down by exposure type

(m) Aggregate amount of securitization exposures

retained or purchased separately for :

- securitization exposures retained or purchased subject

to comprehensive risk measure for specific risk: and

- securitization exposures subject to the securitization

framework for specific risk broken down into different

risk weight bands

(n) Aggregate amount of :

- The capital requirements for the securitization

exposures, subject to the securitization framework

broken down into different risk weight bands

- Securitization exposures that are deducted entirely

from Tier 1 capital, credit enhancing I/O deducted from

total capital, and other exposures deducted from total

capital ( by exposure type)

Nil

Nil

Nil

Nil

Nil

Nil

Nil

Table DF-7

Market risk in trading book

Qualitative disclosures

The Bank has a well defined Market Risk Management Policy. This policy covers all

important areas of market risk measurement.

Bank defines Market Risk as the risk of loss in on-balance sheet and off-balance sheet

positions arising from movements in market rates, in particular, changes in interest rates,

exchange rates and equity and commodity prices.

The Bank has adopted Standardized Duration Approach for measuring the capital

requirements for market risk as prescribed by RBI.

Policies for management of Market Risk:

The Bank has put in place Board approved Market Risk Management Policy for effective

management of Market Risk in the Bank. Other policies which also deal with Market

Risk Management are integrated treasury policy and Asset Liability Management Policy.

The policies set various prudential exposure limits and risk limits for ensuring that the

operations are in line with Bank‟s expectations of return through proper Market Risk

Management and Asset Liability Management.

18

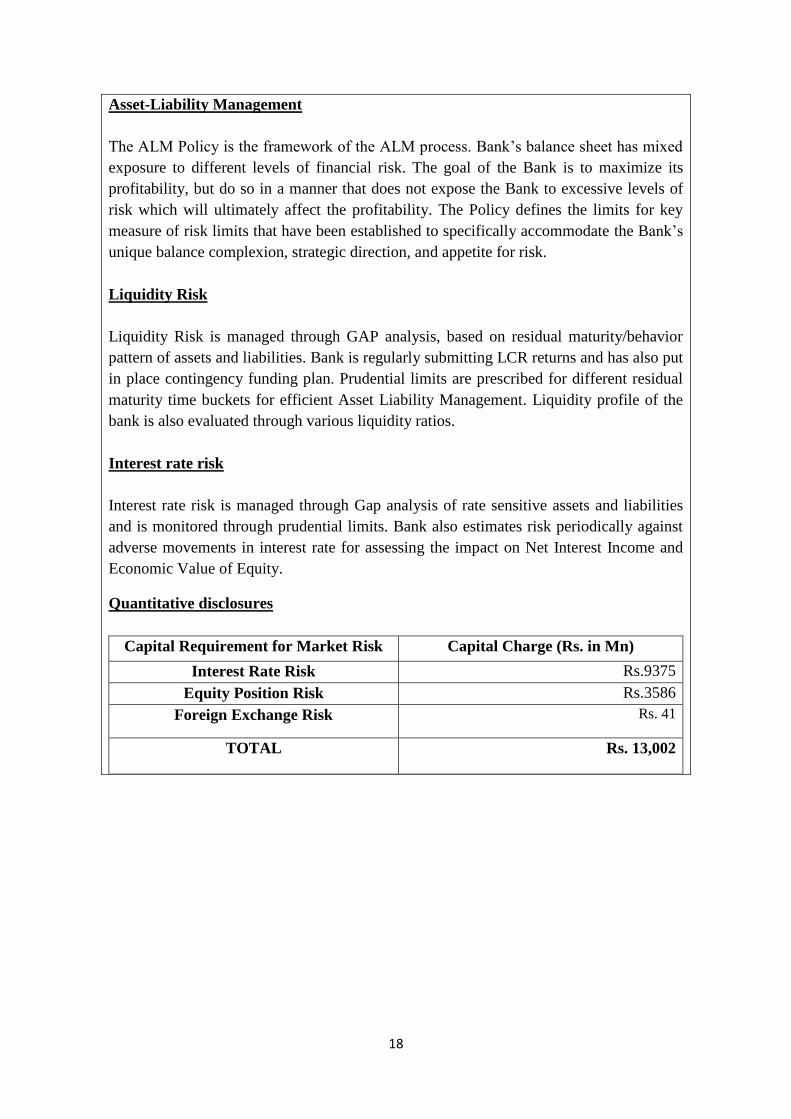

Asset-Liability Management

The ALM Policy is the framework of the ALM process. Bank‟s balance sheet has mixed

exposure to different levels of financial risk. The goal of the Bank is to maximize its

profitability, but do so in a manner that does not expose the Bank to excessive levels of

risk which will ultimately affect the profitability. The Policy defines the limits for key

measure of risk limits that have been established to specifically accommodate the Bank‟s

unique balance complexion, strategic direction, and appetite for risk.

Liquidity Risk

Liquidity Risk is managed through GAP analysis, based on residual maturity/behavior

pattern of assets and liabilities. Bank is regularly submitting LCR returns and has also put

in place contingency funding plan. Prudential limits are prescribed for different residual

maturity time buckets for efficient Asset Liability Management. Liquidity profile of the

bank is also evaluated through various liquidity ratios.

Interest rate risk

Interest rate risk is managed through Gap analysis of rate sensitive assets and liabilities

and is monitored through prudential limits. Bank also estimates risk periodically against

adverse movements in interest rate for assessing the impact on Net Interest Income and

Economic Value of Equity.

Quantitative disclosures

Capital Requirement for Market Risk Capital Charge (Rs. in Mn)

Interest Rate Risk Rs.9375

Equity Position Risk Rs.3586

Foreign Exchange Risk Rs. 41

TOTAL Rs. 13,002

19

Table DF-8

Operational risk

Qualitative disclosures

Operational Risk is the risk of losses resulting from inadequate or failed internal

processes, people and systems or from external events. Operational Risk includes legal

risk but excludes strategic and reputation risks. Operational Risk Management in the

Bank is guided by a well-defined Operational Risk Management Policy which is

reviewed every year. The Bank has initiated pro-active steps to equip itself to migrate to

advanced approaches under Operational Risk and has started collation of data pertaining

to Operational Risk loss events through Loss Data Management, Risk & Control Self-

Assessment (RCSA), Key Risk Indicators (KRI) & Scenario Analysis. Bank is also a

member of loss data consortium „CORDEx‟ for external loss data base.

The Bank has appointed consultant and system integrator for moving to Advanced

Measurement Approach.

The Bank has provided capital for operational risk as per Basic Indicator Approach.

Accordingly the capital requirement for operational risk as on 30.09.2019 is Rs. 8746 mn.

20

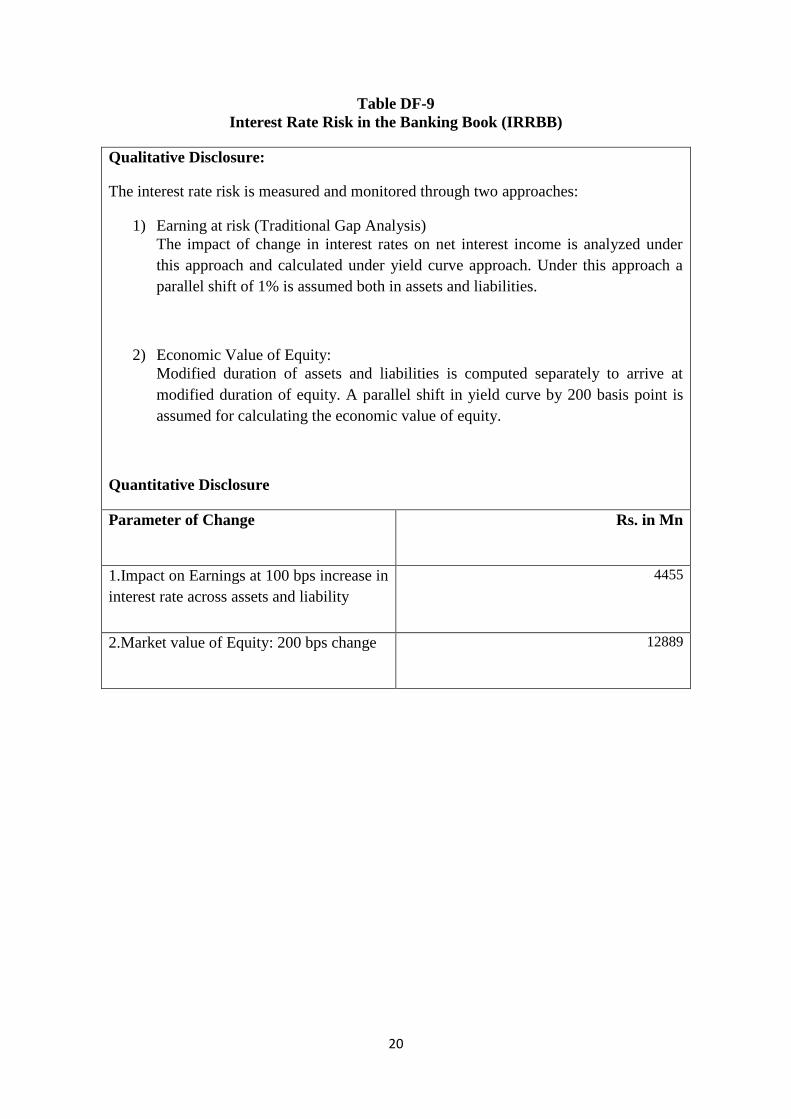

Table DF-9

Interest Rate Risk in the Banking Book (IRRBB)

Qualitative Disclosure:

The interest rate risk is measured and monitored through two approaches:

1) Earning at risk (Traditional Gap Analysis)

The impact of change in interest rates on net interest income is analyzed under

this approach and calculated under yield curve approach. Under this approach a

parallel shift of 1% is assumed both in assets and liabilities.

2) Economic Value of Equity:

Modified duration of assets and liabilities is computed separately to arrive at

modified duration of equity. A parallel shift in yield curve by 200 basis point is

assumed for calculating the economic value of equity.

Quantitative Disclosure

Parameter of Change Rs. in Mn

1.Impact on Earnings at 100 bps increase in

interest rate across assets and liability

4455

2.Market value of Equity: 200 bps change 12889

21

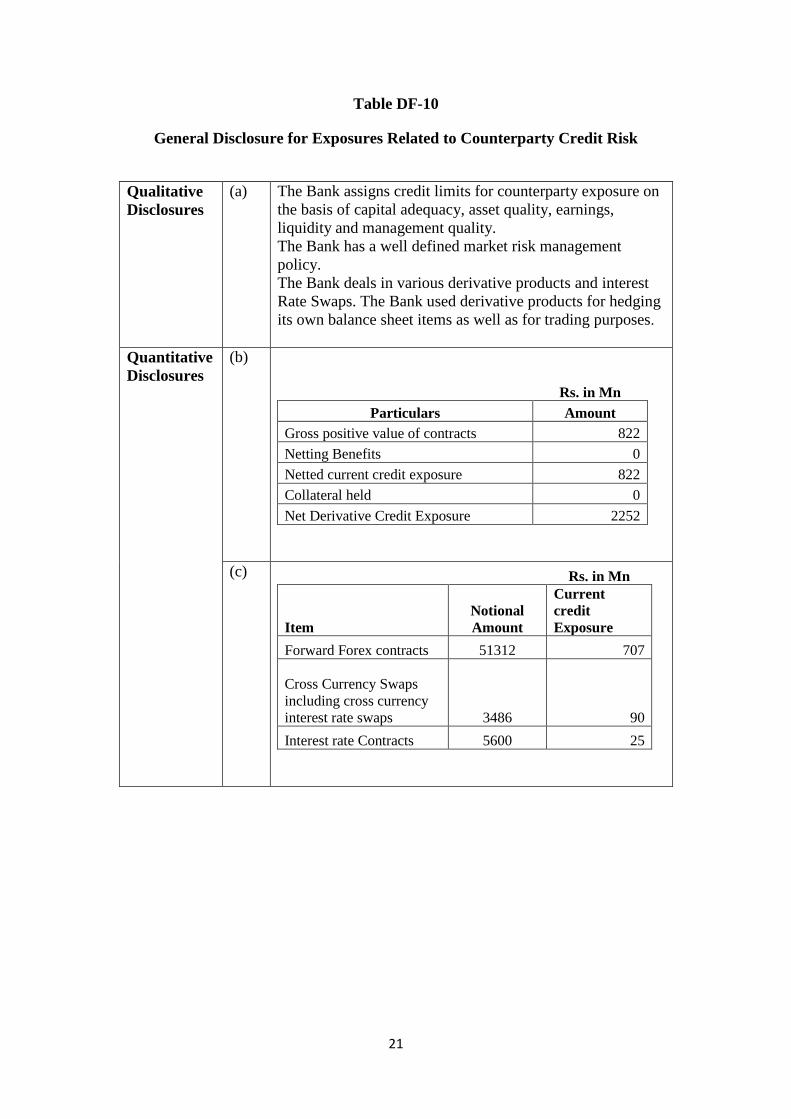

Table DF-10

General Disclosure for Exposures Related to Counterparty Credit Risk

Qualitative

Disclosures

(a) The Bank assigns credit limits for counterparty exposure on

the basis of capital adequacy, asset quality, earnings,

liquidity and management quality.

The Bank has a well defined market risk management

policy. The Bank deals in various derivative products and interest

Rate Swaps. The Bank used derivative products for hedging

its own balance sheet items as well as for trading purposes.

Quantitative

Disclosures

(b)

Rs. in Mn

Particulars Amount

Gross positive value of contracts 822

Netting Benefits 0

Netted current credit exposure 822

Collateral held 0

Net Derivative Credit Exposure 2252

(c)

Rs. in Mn

Item

Notional

Amount

Current

credit

Exposure

Forward Forex contracts 51312 707

Cross Currency Swaps

including cross currency

interest rate swaps 3486 90

Interest rate Contracts 5600 25

22

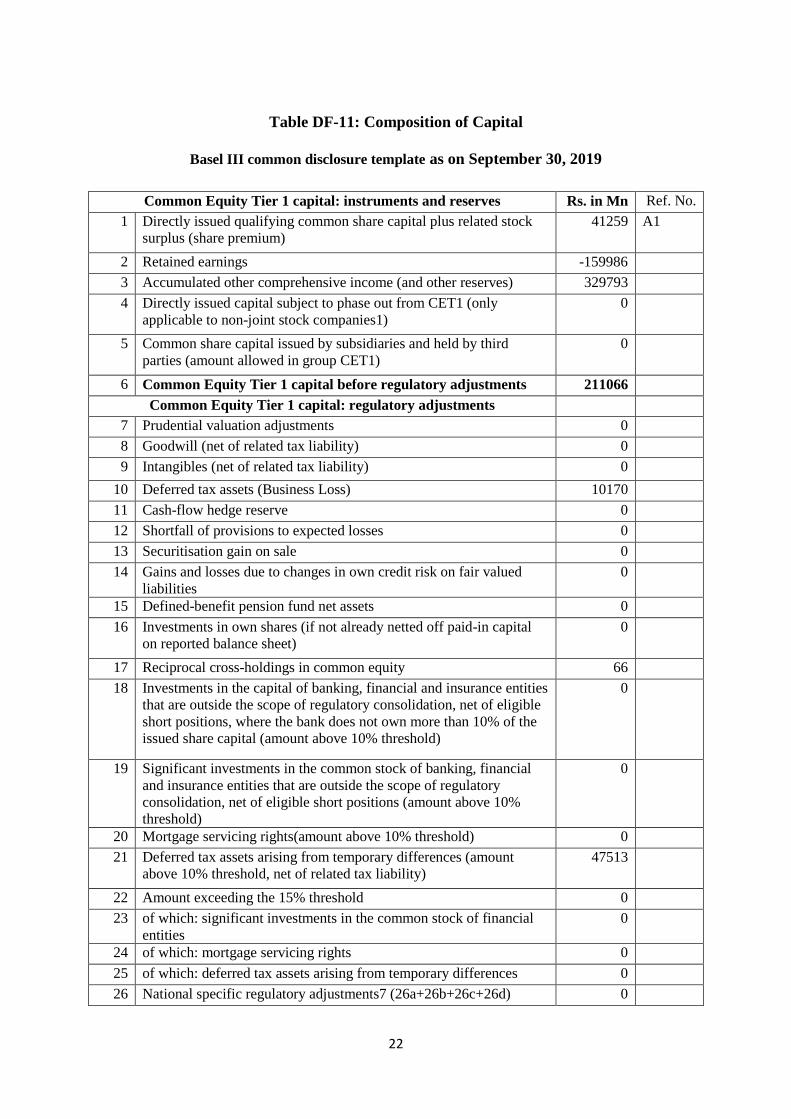

Table DF-11: Composition of Capital

Basel III common disclosure template as on September 30, 2019

Common Equity Tier 1 capital: instruments and reserves Rs. in Mn Ref. No.

1 Directly issued qualifying common share capital plus related stock

surplus (share premium)

41259 A1

2 Retained earnings -159986

3 Accumulated other comprehensive income (and other reserves) 329793

4 Directly issued capital subject to phase out from CET1 (only

applicable to non-joint stock companies1)

0

5 Common share capital issued by subsidiaries and held by third

parties (amount allowed in group CET1)

0

6 Common Equity Tier 1 capital before regulatory adjustments 211066

Common Equity Tier 1 capital: regulatory adjustments

7 Prudential valuation adjustments 0

8 Goodwill (net of related tax liability) 0

9 Intangibles (net of related tax liability) 0

10 Deferred tax assets (Business Loss) 10170

11 Cash-flow hedge reserve 0

12 Shortfall of provisions to expected losses 0

13 Securitisation gain on sale 0

14 Gains and losses due to changes in own credit risk on fair valued

liabilities

0

15 Defined-benefit pension fund net assets 0

16 Investments in own shares (if not already netted off paid-in capital

on reported balance sheet)

0

17 Reciprocal cross-holdings in common equity 66

18 Investments in the capital of banking, financial and insurance entities

that are outside the scope of regulatory consolidation, net of eligible

short positions, where the bank does not own more than 10% of the

issued share capital (amount above 10% threshold)

0

19 Significant investments in the common stock of banking, financial

and insurance entities that are outside the scope of regulatory

consolidation, net of eligible short positions (amount above 10%

threshold)

0

20 Mortgage servicing rights(amount above 10% threshold) 0

21 Deferred tax assets arising from temporary differences (amount

above 10% threshold, net of related tax liability)

47513

22 Amount exceeding the 15% threshold 0

23 of which: significant investments in the common stock of financial

entities

0

24 of which: mortgage servicing rights 0

25 of which: deferred tax assets arising from temporary differences 0

26 National specific regulatory adjustments7 (26a+26b+26c+26d) 0

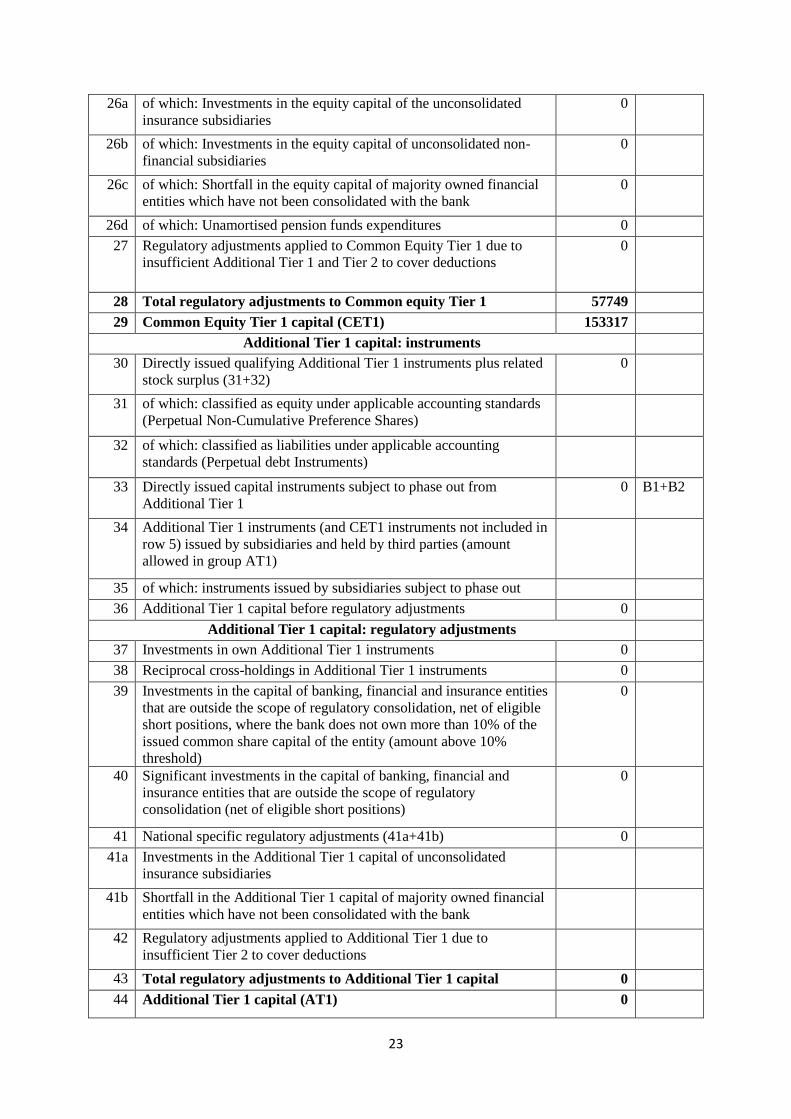

23

26a of which: Investments in the equity capital of the unconsolidated

insurance subsidiaries

0

26b of which: Investments in the equity capital of unconsolidated non-

financial subsidiaries

0

26c of which: Shortfall in the equity capital of majority owned financial

entities which have not been consolidated with the bank

0

26d of which: Unamortised pension funds expenditures 0

27 Regulatory adjustments applied to Common Equity Tier 1 due to

insufficient Additional Tier 1 and Tier 2 to cover deductions

0

28 Total regulatory adjustments to Common equity Tier 1 57749

29 Common Equity Tier 1 capital (CET1) 153317

Additional Tier 1 capital: instruments

30 Directly issued qualifying Additional Tier 1 instruments plus related

stock surplus (31+32)

0

31 of which: classified as equity under applicable accounting standards

(Perpetual Non-Cumulative Preference Shares)

32 of which: classified as liabilities under applicable accounting

standards (Perpetual debt Instruments)

33 Directly issued capital instruments subject to phase out from

Additional Tier 1

0 B1+B2

34 Additional Tier 1 instruments (and CET1 instruments not included in

row 5) issued by subsidiaries and held by third parties (amount

allowed in group AT1)

35 of which: instruments issued by subsidiaries subject to phase out

36 Additional Tier 1 capital before regulatory adjustments 0

Additional Tier 1 capital: regulatory adjustments

37 Investments in own Additional Tier 1 instruments 0

38 Reciprocal cross-holdings in Additional Tier 1 instruments 0

39 Investments in the capital of banking, financial and insurance entities

that are outside the scope of regulatory consolidation, net of eligible

short positions, where the bank does not own more than 10% of the

issued common share capital of the entity (amount above 10%

threshold)

0

40 Significant investments in the capital of banking, financial and

insurance entities that are outside the scope of regulatory

consolidation (net of eligible short positions)

0

41 National specific regulatory adjustments (41a+41b) 0

41a Investments in the Additional Tier 1 capital of unconsolidated

insurance subsidiaries

41b Shortfall in the Additional Tier 1 capital of majority owned financial

entities which have not been consolidated with the bank

42 Regulatory adjustments applied to Additional Tier 1 due to

insufficient Tier 2 to cover deductions

43 Total regulatory adjustments to Additional Tier 1 capital 0

44 Additional Tier 1 capital (AT1) 0

24

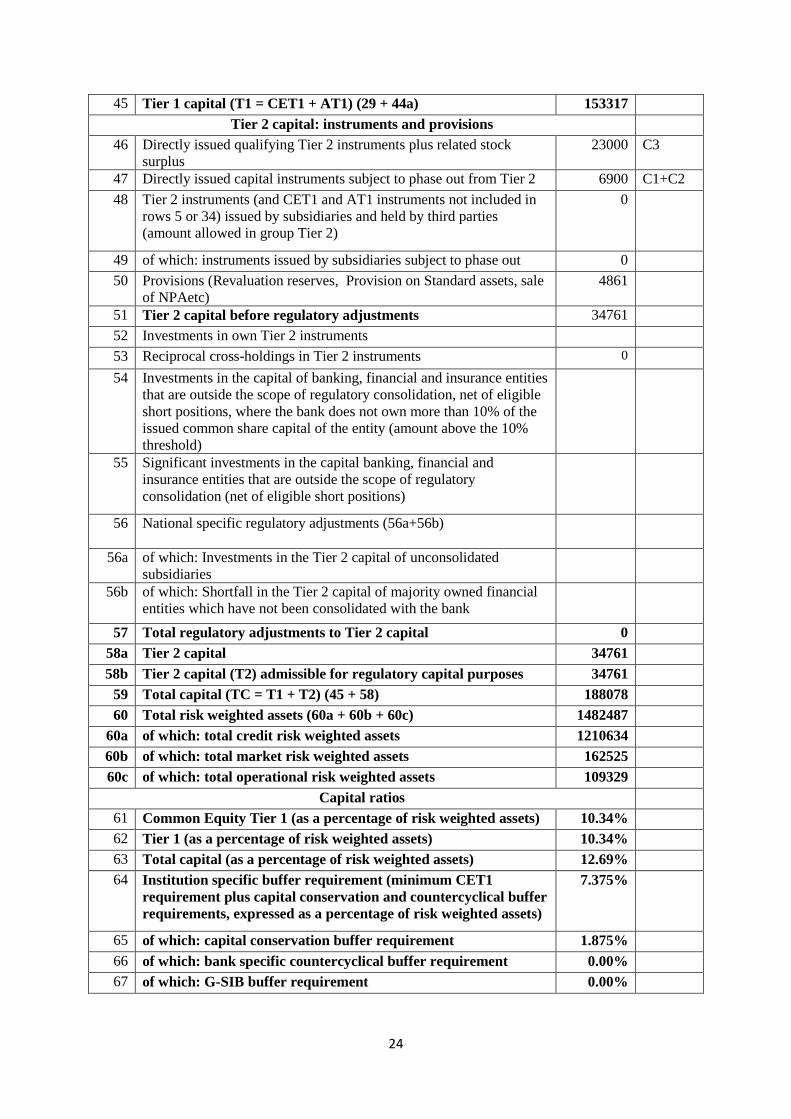

45 Tier 1 capital (T1 = CET1 + AT1) (29 + 44a) 153317

Tier 2 capital: instruments and provisions

46 Directly issued qualifying Tier 2 instruments plus related stock

surplus

23000 C3

47 Directly issued capital instruments subject to phase out from Tier 2 6900 C1+C2

48 Tier 2 instruments (and CET1 and AT1 instruments not included in

rows 5 or 34) issued by subsidiaries and held by third parties

(amount allowed in group Tier 2)

0

49 of which: instruments issued by subsidiaries subject to phase out 0

50 Provisions (Revaluation reserves, Provision on Standard assets, sale

of NPAetc)

4861

51 Tier 2 capital before regulatory adjustments 34761

52 Investments in own Tier 2 instruments

53 Reciprocal cross-holdings in Tier 2 instruments 0

54 Investments in the capital of banking, financial and insurance entities

that are outside the scope of regulatory consolidation, net of eligible

short positions, where the bank does not own more than 10% of the

issued common share capital of the entity (amount above the 10%

threshold)

55 Significant investments in the capital banking, financial and

insurance entities that are outside the scope of regulatory

consolidation (net of eligible short positions)

56 National specific regulatory adjustments (56a+56b)

56a of which: Investments in the Tier 2 capital of unconsolidated

subsidiaries

56b of which: Shortfall in the Tier 2 capital of majority owned financial

entities which have not been consolidated with the bank

57 Total regulatory adjustments to Tier 2 capital 0

58a Tier 2 capital 34761

58b Tier 2 capital (T2) admissible for regulatory capital purposes 34761

59 Total capital (TC = T1 + T2) (45 + 58) 188078

60 Total risk weighted assets (60a + 60b + 60c) 1482487

60a of which: total credit risk weighted assets 1210634

60b of which: total market risk weighted assets 162525

60c of which: total operational risk weighted assets 109329

Capital ratios

61 Common Equity Tier 1 (as a percentage of risk weighted assets) 10.34%

62 Tier 1 (as a percentage of risk weighted assets) 10.34%

63 Total capital (as a percentage of risk weighted assets) 12.69%

64 Institution specific buffer requirement (minimum CET1

requirement plus capital conservation and countercyclical buffer

requirements, expressed as a percentage of risk weighted assets)

7.375%

65 of which: capital conservation buffer requirement 1.875%

66 of which: bank specific countercyclical buffer requirement 0.00%

67 of which: G-SIB buffer requirement 0.00%

25

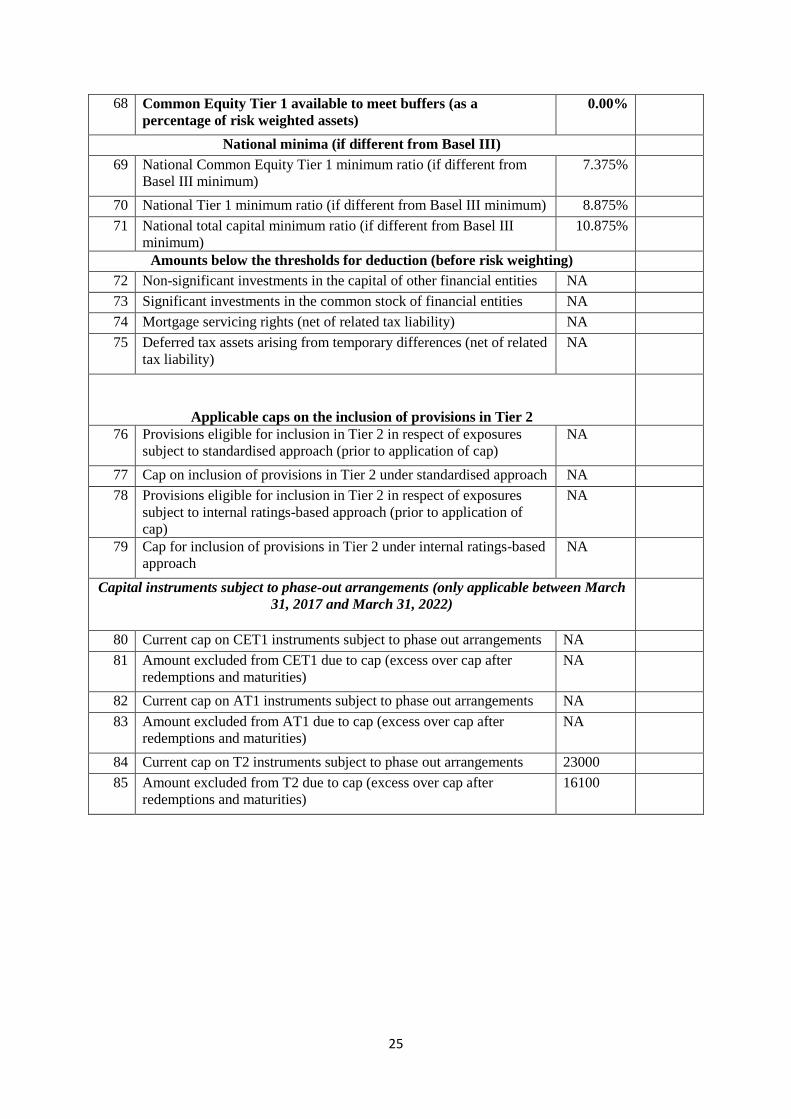

68 Common Equity Tier 1 available to meet buffers (as a

percentage of risk weighted assets)

0.00%

National minima (if different from Basel III)

69 National Common Equity Tier 1 minimum ratio (if different from

Basel III minimum)

7.375%

70 National Tier 1 minimum ratio (if different from Basel III minimum) 8.875%

71 National total capital minimum ratio (if different from Basel III

minimum)

10.875%

Amounts below the thresholds for deduction (before risk weighting)

72 Non-significant investments in the capital of other financial entities NA

73 Significant investments in the common stock of financial entities NA

74 Mortgage servicing rights (net of related tax liability) NA

75 Deferred tax assets arising from temporary differences (net of related

tax liability)

NA

Applicable caps on the inclusion of provisions in Tier 2

76 Provisions eligible for inclusion in Tier 2 in respect of exposures

subject to standardised approach (prior to application of cap)

NA

77 Cap on inclusion of provisions in Tier 2 under standardised approach NA

78 Provisions eligible for inclusion in Tier 2 in respect of exposures

subject to internal ratings-based approach (prior to application of

cap)

NA

79 Cap for inclusion of provisions in Tier 2 under internal ratings-based

approach

NA

Capital instruments subject to phase-out arrangements (only applicable between March

31, 2017 and March 31, 2022)

80 Current cap on CET1 instruments subject to phase out arrangements NA

81 Amount excluded from CET1 due to cap (excess over cap after

redemptions and maturities)

NA

82 Current cap on AT1 instruments subject to phase out arrangements NA

83 Amount excluded from AT1 due to cap (excess over cap after

redemptions and maturities)

NA

84 Current cap on T2 instruments subject to phase out arrangements 23000

85 Amount excluded from T2 due to cap (excess over cap after

redemptions and maturities)

16100

26

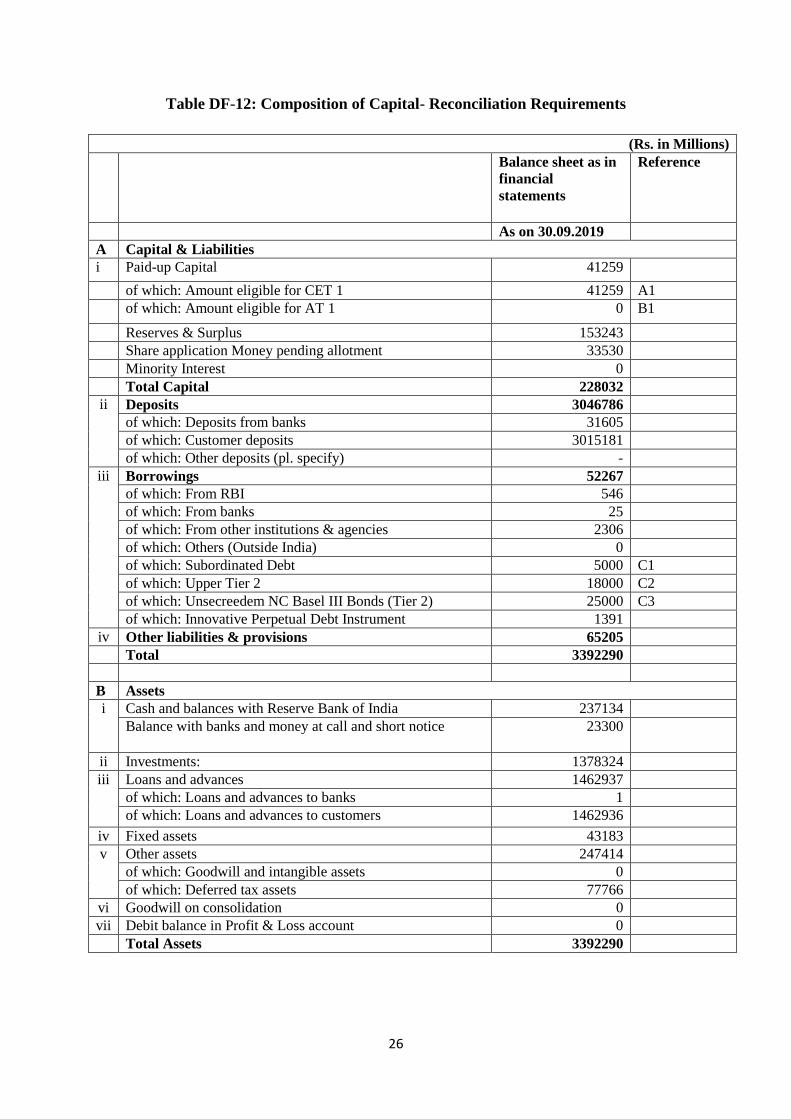

Table DF-12: Composition of Capital- Reconciliation Requirements

(Rs. in Millions)

Balance sheet as in

financial

statements

Reference

As on 30.09.2019

A Capital & Liabilities

i Paid-up Capital 41259

of which: Amount eligible for CET 1 41259 A1

of which: Amount eligible for AT 1 0 B1

Reserves & Surplus 153243

Share application Money pending allotment 33530

Minority Interest 0

Total Capital 228032

ii Deposits 3046786

of which: Deposits from banks 31605

of which: Customer deposits 3015181

of which: Other deposits (pl. specify) -

iii Borrowings 52267

of which: From RBI 546

of which: From banks 25

of which: From other institutions & agencies 2306

of which: Others (Outside India) 0

of which: Subordinated Debt 5000 C1

of which: Upper Tier 2 18000 C2

of which: Unsecreedem NC Basel III Bonds (Tier 2) 25000 C3

of which: Innovative Perpetual Debt Instrument 1391

iv Other liabilities & provisions 65205

Total 3392290

B Assets

i Cash and balances with Reserve Bank of India 237134

Balance with banks and money at call and short notice 23300

ii Investments: 1378324

iii Loans and advances 1462937

of which: Loans and advances to banks 1

of which: Loans and advances to customers 1462936

iv Fixed assets 43183

v Other assets 247414

of which: Goodwill and intangible assets 0

of which: Deferred tax assets 77766

vi Goodwill on consolidation 0

vii Debit balance in Profit & Loss account 0

Total Assets 3392290

27

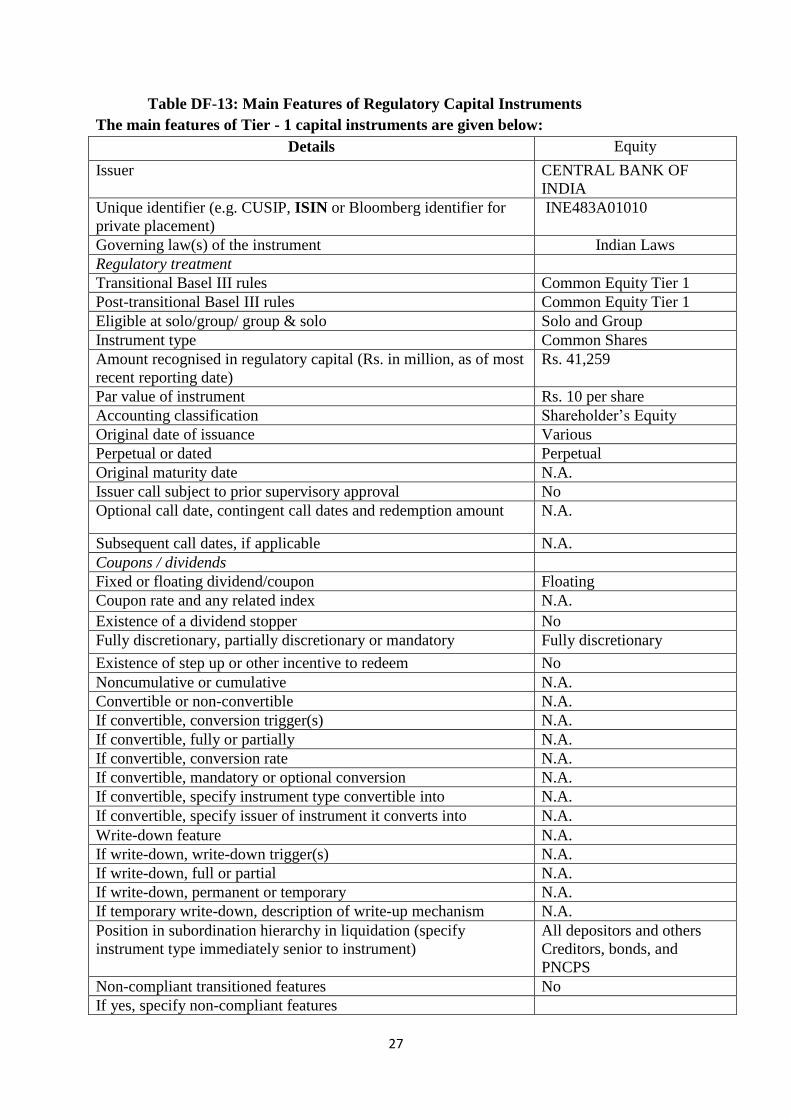

Table DF-13: Main Features of Regulatory Capital Instruments

The main features of Tier - 1 capital instruments are given below:

Details Equity

Issuer CENTRAL BANK OF

INDIA

Unique identifier (e.g. CUSIP, ISIN or Bloomberg identifier for

private placement)

INE483A01010

Governing law(s) of the instrument Indian Laws

Regulatory treatment

Transitional Basel III rules Common Equity Tier 1

Post-transitional Basel III rules Common Equity Tier 1

Eligible at solo/group/ group & solo Solo and Group

Instrument type Common Shares

Amount recognised in regulatory capital (Rs. in million, as of most

recent reporting date)

Rs. 41,259

Par value of instrument Rs. 10 per share

Accounting classification Shareholder‟s Equity

Original date of issuance Various

Perpetual or dated Perpetual

Original maturity date N.A.

Issuer call subject to prior supervisory approval No

Optional call date, contingent call dates and redemption amount N.A.

Subsequent call dates, if applicable N.A.

Coupons / dividends

Fixed or floating dividend/coupon Floating

Coupon rate and any related index N.A.

Existence of a dividend stopper No

Fully discretionary, partially discretionary or mandatory Fully discretionary

Existence of step up or other incentive to redeem No

Noncumulative or cumulative N.A.

Convertible or non-convertible N.A.

If convertible, conversion trigger(s) N.A.

If convertible, fully or partially N.A.

If convertible, conversion rate N.A.

If convertible, mandatory or optional conversion N.A.

If convertible, specify instrument type convertible into N.A.

If convertible, specify issuer of instrument it converts into N.A.

Write-down feature N.A.

If write-down, write-down trigger(s) N.A.

If write-down, full or partial N.A.

If write-down, permanent or temporary N.A.

If temporary write-down, description of write-up mechanism N.A.

Position in subordination hierarchy in liquidation (specify

instrument type immediately senior to instrument)

All depositors and others

Creditors, bonds, and

PNCPS

Non-compliant transitioned features No

If yes, specify non-compliant features

28

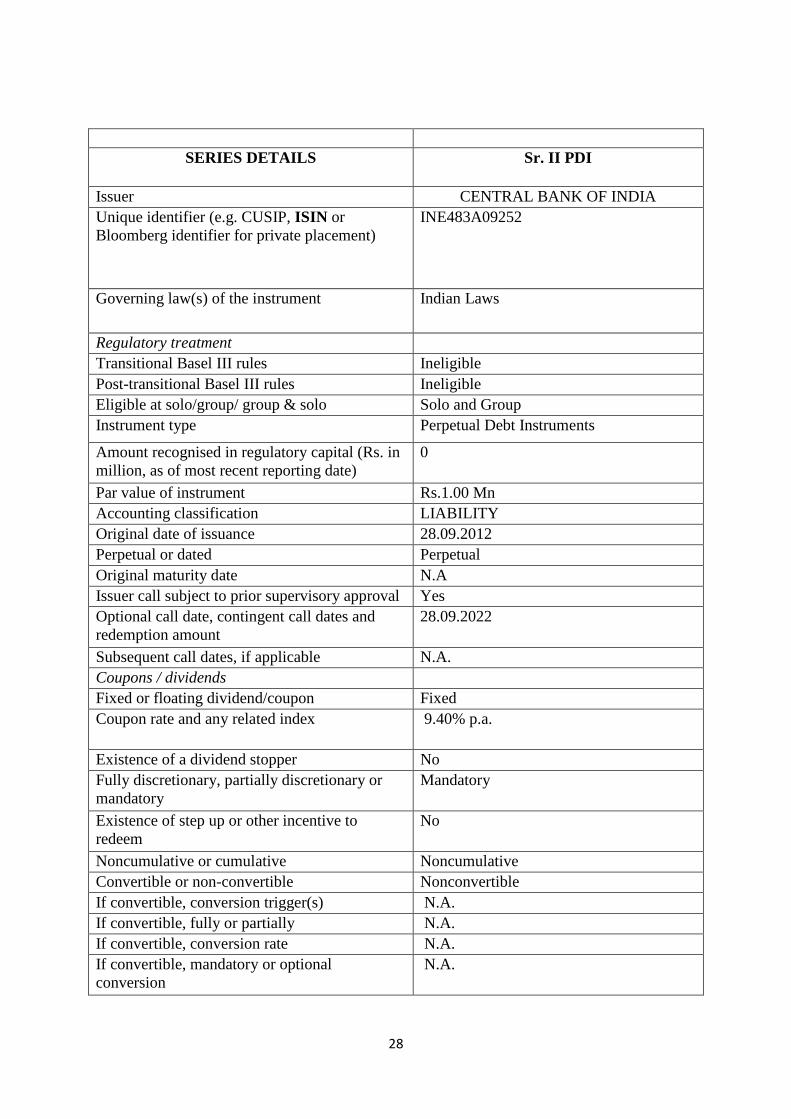

SERIES DETAILS Sr. II PDI

Issuer CENTRAL BANK OF INDIA

Unique identifier (e.g. CUSIP, ISIN or

Bloomberg identifier for private placement)

INE483A09252

Governing law(s) of the instrument Indian Laws

Regulatory treatment

Transitional Basel III rules Ineligible

Post-transitional Basel III rules Ineligible

Eligible at solo/group/ group & solo Solo and Group

Instrument type Perpetual Debt Instruments

Amount recognised in regulatory capital (Rs. in

million, as of most recent reporting date)

0

Par value of instrument Rs.1.00 Mn

Accounting classification LIABILITY

Original date of issuance 28.09.2012

Perpetual or dated Perpetual

Original maturity date N.A

Issuer call subject to prior supervisory approval Yes

Optional call date, contingent call dates and

redemption amount

28.09.2022

Subsequent call dates, if applicable N.A.

Coupons / dividends

Fixed or floating dividend/coupon Fixed

Coupon rate and any related index 9.40% p.a.

Existence of a dividend stopper No

Fully discretionary, partially discretionary or

mandatory

Mandatory

Existence of step up or other incentive to

redeem

No

Noncumulative or cumulative Noncumulative

Convertible or non-convertible Nonconvertible

If convertible, conversion trigger(s) N.A.

If convertible, fully or partially N.A.

If convertible, conversion rate N.A.

If convertible, mandatory or optional

conversion

N.A.

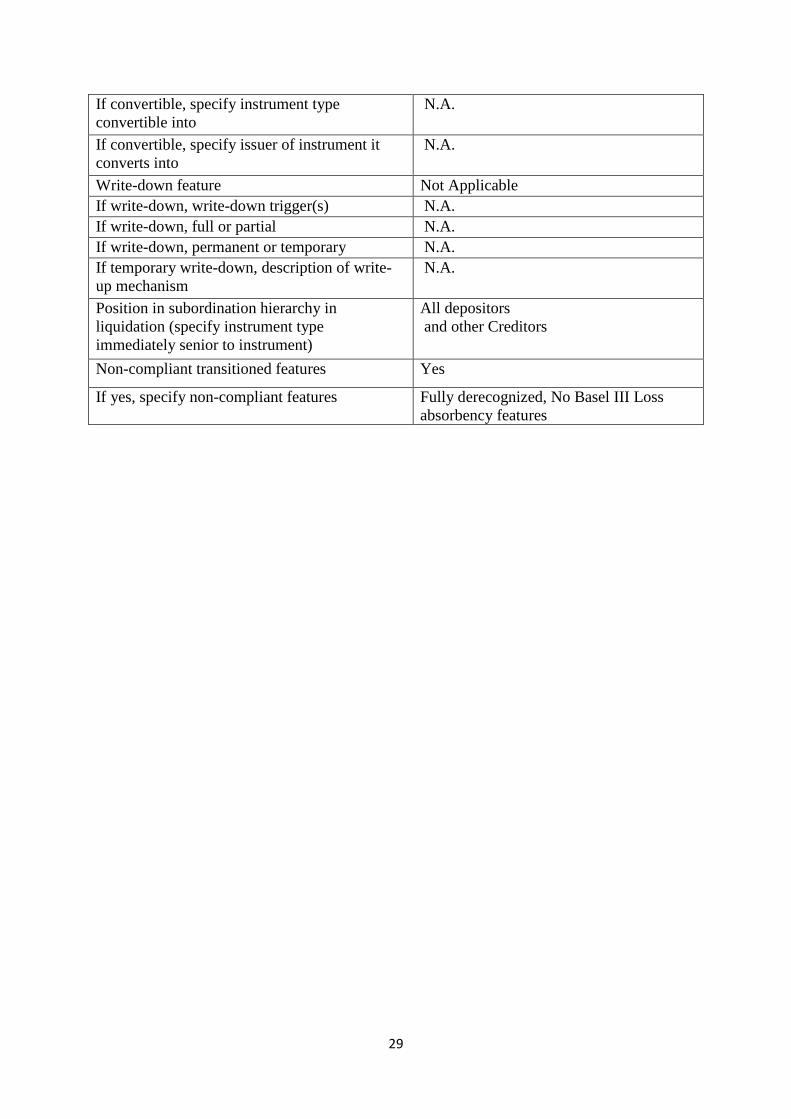

29

If convertible, specify instrument type

convertible into

N.A.

If convertible, specify issuer of instrument it

converts into

N.A.

Write-down feature Not Applicable

If write-down, write-down trigger(s) N.A.

If write-down, full or partial N.A.

If write-down, permanent or temporary N.A.

If temporary write-down, description of write-

up mechanism

N.A.

Position in subordination hierarchy in

liquidation (specify instrument type

immediately senior to instrument)

All depositors

and other Creditors

Non-compliant transitioned features Yes

If yes, specify non-compliant features Fully derecognized, No Basel III Loss

absorbency features

30

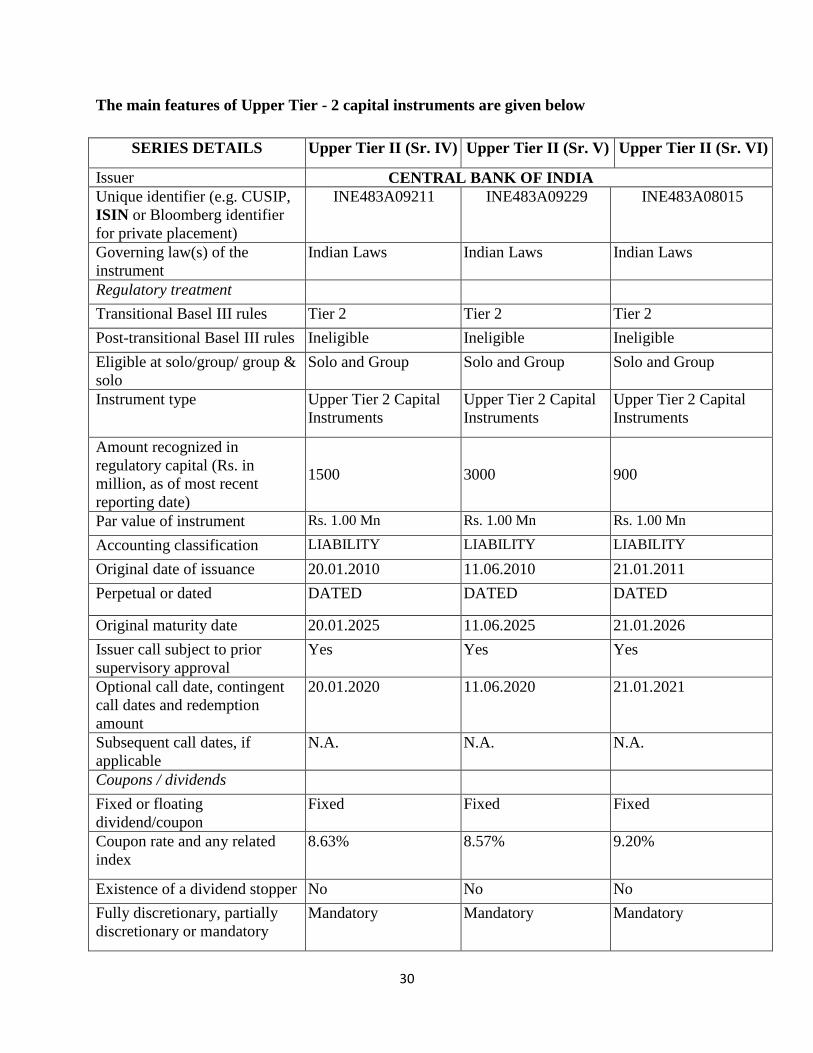

The main features of Upper Tier - 2 capital instruments are given below

SERIES DETAILS Upper Tier II (Sr. IV) Upper Tier II (Sr. V) Upper Tier II (Sr. VI)

Issuer CENTRAL BANK OF INDIA

Unique identifier (e.g. CUSIP,

ISIN or Bloomberg identifier

for private placement)

INE483A09211 INE483A09229 INE483A08015

Governing law(s) of the

instrument

Indian Laws Indian Laws Indian Laws

Regulatory treatment

Transitional Basel III rules Tier 2 Tier 2 Tier 2

Post-transitional Basel III rules Ineligible Ineligible Ineligible

Eligible at solo/group/ group &

solo

Solo and Group Solo and Group Solo and Group

Instrument type Upper Tier 2 Capital

Instruments

Upper Tier 2 Capital

Instruments

Upper Tier 2 Capital

Instruments

Amount recognized in

regulatory capital (Rs. in

million, as of most recent

reporting date)

1500 3000 900

Par value of instrument Rs. 1.00 Mn Rs. 1.00 Mn Rs. 1.00 Mn

Accounting classification LIABILITY LIABILITY LIABILITY

Original date of issuance 20.01.2010 11.06.2010 21.01.2011

Perpetual or dated DATED DATED DATED

Original maturity date 20.01.2025 11.06.2025 21.01.2026

Issuer call subject to prior

supervisory approval

Yes Yes Yes

Optional call date, contingent

call dates and redemption

amount

20.01.2020 11.06.2020 21.01.2021

Subsequent call dates, if

applicable

N.A. N.A. N.A.

Coupons / dividends

Fixed or floating

dividend/coupon

Fixed Fixed Fixed

Coupon rate and any related

index

8.63% 8.57% 9.20%

Existence of a dividend stopper No No No

Fully discretionary, partially

discretionary or mandatory

Mandatory Mandatory Mandatory

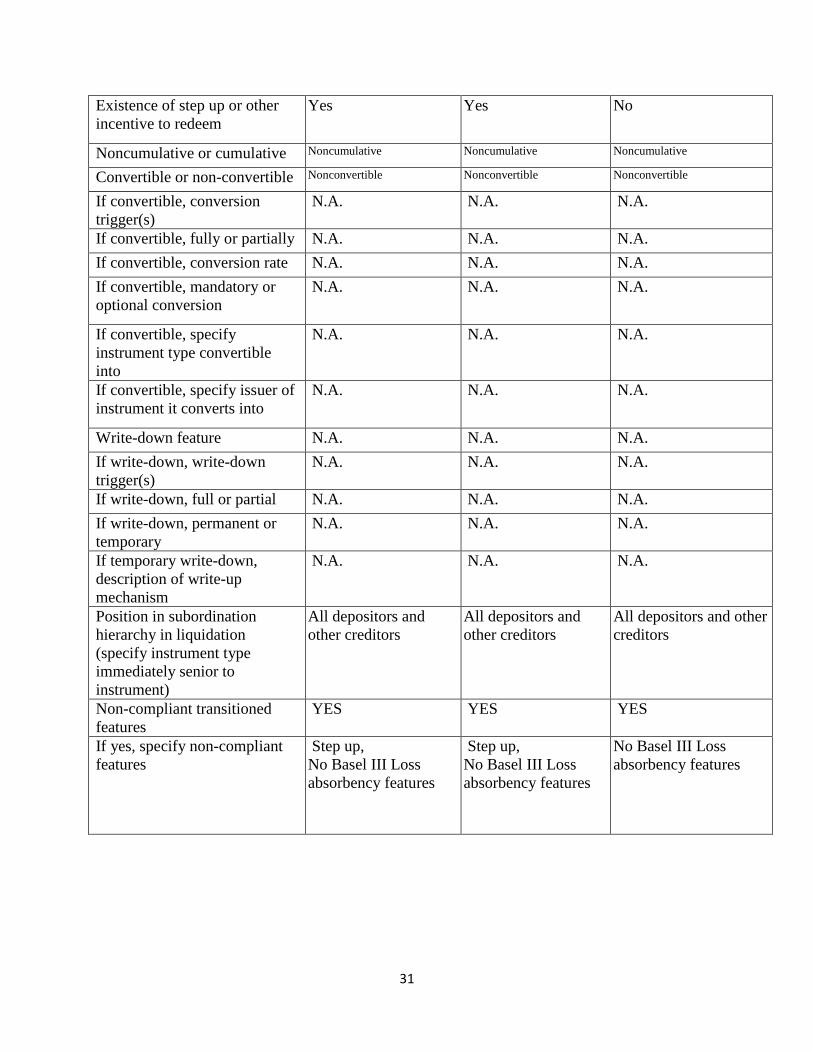

31

Existence of step up or other

incentive to redeem

Yes Yes No

Noncumulative or cumulative Noncumulative Noncumulative Noncumulative

Convertible or non-convertible Nonconvertible Nonconvertible Nonconvertible

If convertible, conversion

trigger(s)

N.A. N.A. N.A.

If convertible, fully or partially N.A. N.A. N.A.

If convertible, conversion rate N.A. N.A. N.A.

If convertible, mandatory or

optional conversion

N.A. N.A. N.A.

If convertible, specify

instrument type convertible

into

N.A. N.A. N.A.

If convertible, specify issuer of

instrument it converts into

N.A. N.A. N.A.

Write-down feature N.A. N.A. N.A.

If write-down, write-down

trigger(s)

N.A. N.A. N.A.

If write-down, full or partial N.A. N.A. N.A.

If write-down, permanent or

temporary

N.A. N.A. N.A.

If temporary write-down,

description of write-up

mechanism

N.A. N.A. N.A.

Position in subordination

hierarchy in liquidation

(specify instrument type

immediately senior to

instrument)

All depositors and

other creditors

All depositors and

other creditors

All depositors and other

creditors

Non-compliant transitioned

features

YES YES YES

If yes, specify non-compliant

features

Step up,

No Basel III Loss

absorbency features

Step up,

No Basel III Loss

absorbency features

No Basel III Loss

absorbency features

32

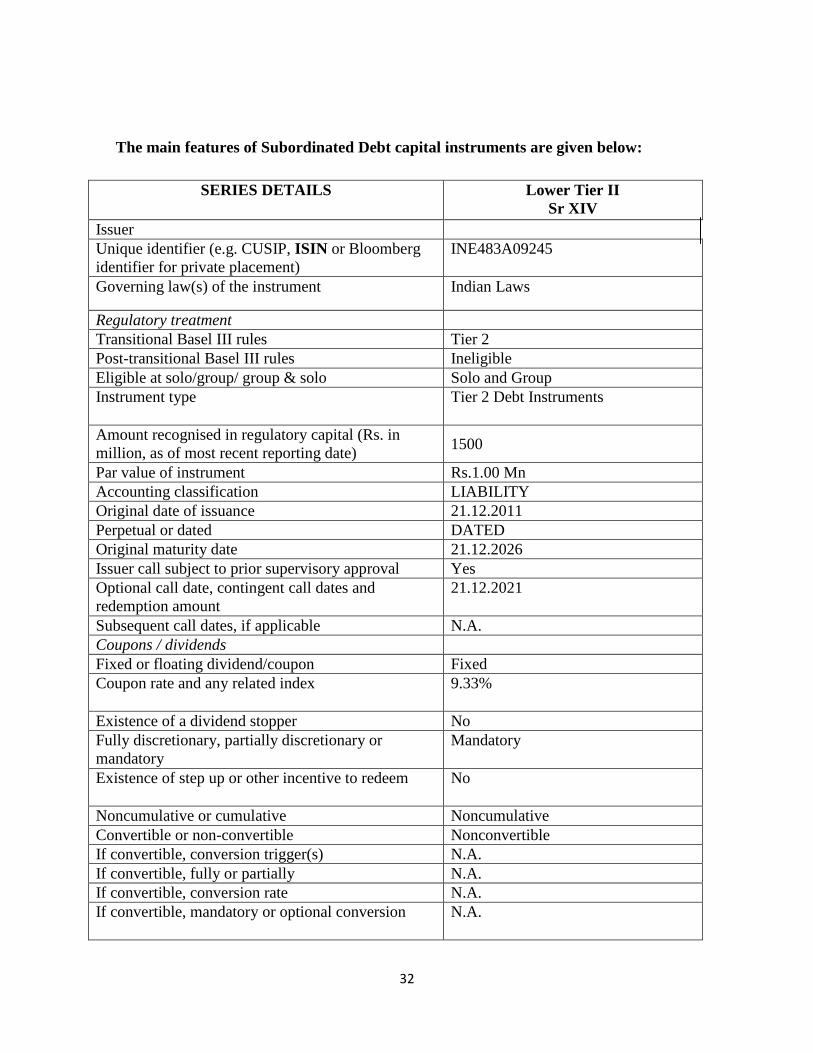

The main features of Subordinated Debt capital instruments are given below:

SERIES DETAILS Lower Tier II

Sr XIV

Issuer

Unique identifier (e.g. CUSIP, ISIN or Bloomberg

identifier for private placement)

INE483A09245

Governing law(s) of the instrument Indian Laws

Regulatory treatment

Transitional Basel III rules Tier 2

Post-transitional Basel III rules Ineligible

Eligible at solo/group/ group & solo Solo and Group

Instrument type Tier 2 Debt Instruments

Amount recognised in regulatory capital (Rs. in

million, as of most recent reporting date) 1500

Par value of instrument Rs.1.00 Mn

Accounting classification LIABILITY

Original date of issuance 21.12.2011

Perpetual or dated DATED

Original maturity date 21.12.2026

Issuer call subject to prior supervisory approval Yes

Optional call date, contingent call dates and

redemption amount

21.12.2021

Subsequent call dates, if applicable N.A.

Coupons / dividends

Fixed or floating dividend/coupon Fixed

Coupon rate and any related index 9.33%

Existence of a dividend stopper No

Fully discretionary, partially discretionary or

mandatory

Mandatory

Existence of step up or other incentive to redeem No

Noncumulative or cumulative Noncumulative

Convertible or non-convertible Nonconvertible

If convertible, conversion trigger(s) N.A.

If convertible, fully or partially N.A.

If convertible, conversion rate N.A.

If convertible, mandatory or optional conversion N.A.

33

If convertible, specify instrument type convertible

into

N.A.

If convertible, specify issuer of instrument it

converts into

N.A.

Write-down feature Not Applicable

If write-down, write-down trigger(s) N.A.

If write-down, full or partial N.A.

If write-down, permanent or temporary N.A.

If temporary write-down, description of write-up

mechanism

N.A.

Position in subordination hierarchy in liquidation

(specify instrument type immediately senior to

instrument)

All depositors and other creditors

Non-compliant transitioned features YES

If yes, specify non-compliant features No Basel III Loss absorbency features

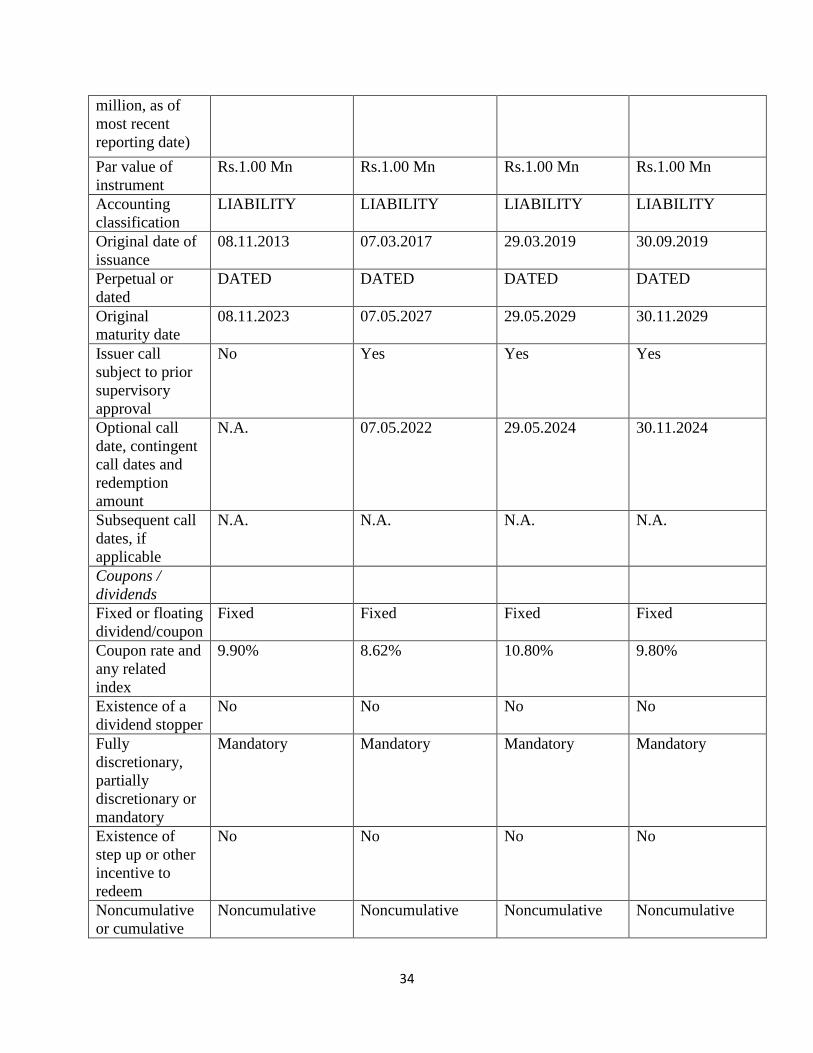

The main features of BASEL III compliant Tier 2 Bonds are given below:

BASEL III COMPLIANT TIER II BONDS

SR I SR II SR III SR IV

Issuer

Unique

identifier (e.g.

CUSIP, ISIN or

Bloomberg

identifier for

private

placement)

INE483A09260 INE483A09278 INE483A09286 INE483A08023

Governing

law(s) of the

instrument

Indian Laws Indian Laws Indian Laws Indian Laws

Regulatory

treatment

Transitional

Basel III rules

Tier 2 Tier 2 Tier 2 Tier 2

Post-transitional

Basel III rules

ELIGIBLE ELIGIBLE ELIGIBLE ELIGIBLE

Eligible at

solo/group/

group & solo

Solo and Group Solo and Group Solo and Group Solo and Group

Instrument type Tier 2 Debt

Instruments

Tier 2 Debt

Instruments

Tier 2 Debt

Instruments

Tier 2 Debt

Instruments

Amount

recognised in

regulatory

capital (Rs. in

8000 5000 5000 5000

34

million, as of

most recent

reporting date)

Par value of

instrument

Rs.1.00 Mn Rs.1.00 Mn Rs.1.00 Mn Rs.1.00 Mn

Accounting

classification

LIABILITY LIABILITY LIABILITY LIABILITY

Original date of

issuance

08.11.2013 07.03.2017 29.03.2019 30.09.2019

Perpetual or

dated

DATED DATED DATED DATED

Original

maturity date

08.11.2023 07.05.2027 29.05.2029 30.11.2029

Issuer call

subject to prior

supervisory

approval

No Yes

Yes

Yes

Optional call

date, contingent

call dates and

redemption

amount

N.A. 07.05.2022 29.05.2024 30.11.2024

Subsequent call

dates, if

applicable

N.A. N.A. N.A. N.A.

Coupons /

dividends

Fixed or floating

dividend/coupon

Fixed Fixed Fixed Fixed

Coupon rate and

any related

index

9.90% 8.62% 10.80% 9.80%

Existence of a

dividend stopper

No No No No

Fully

discretionary,

partially

discretionary or

mandatory

Mandatory Mandatory Mandatory Mandatory

Existence of

step up or other

incentive to

redeem

No No No No

Noncumulative

or cumulative

Noncumulative Noncumulative Noncumulative Noncumulative

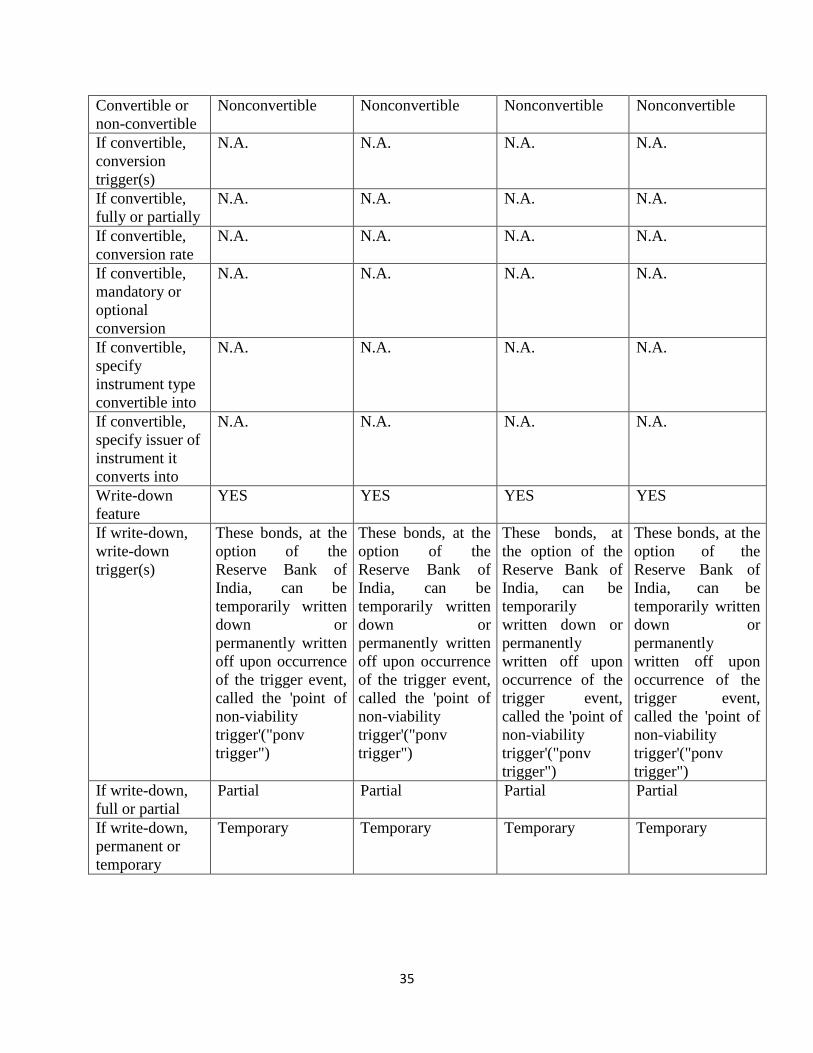

35

Convertible or

non-convertible

Nonconvertible Nonconvertible Nonconvertible Nonconvertible

If convertible,

conversion

trigger(s)

N.A. N.A. N.A. N.A.

If convertible,

fully or partially

N.A. N.A. N.A. N.A.

If convertible,

conversion rate

N.A. N.A. N.A. N.A.

If convertible,

mandatory or

optional

conversion

N.A. N.A. N.A. N.A.

If convertible,

specify

instrument type

convertible into

N.A. N.A. N.A. N.A.

If convertible,

specify issuer of

instrument it

converts into

N.A. N.A. N.A. N.A.

Write-down

feature

YES YES YES YES

If write-down,

write-down

trigger(s)

These bonds, at the

option of the

Reserve Bank of

India, can be

temporarily written

down or

permanently written

off upon occurrence

of the trigger event,

called the 'point of

non-viability

trigger'("ponv

trigger")

These bonds, at the

option of the

Reserve Bank of

India, can be

temporarily written

down or

permanently written

off upon occurrence

of the trigger event,

called the 'point of

non-viability

trigger'("ponv

trigger")

These bonds, at

the option of the

Reserve Bank of

India, can be

temporarily

written down or

permanently

written off upon

occurrence of the

trigger event,

called the 'point of

non-viability

trigger'("ponv

trigger")

These bonds, at the

option of the

Reserve Bank of

India, can be

temporarily written

down or

permanently

written off upon

occurrence of the

trigger event,

called the 'point of

non-viability

trigger'("ponv

trigger")

If write-down,

full or partial

Partial Partial Partial Partial

If write-down,

permanent or

temporary

Temporary Temporary Temporary Temporary

36

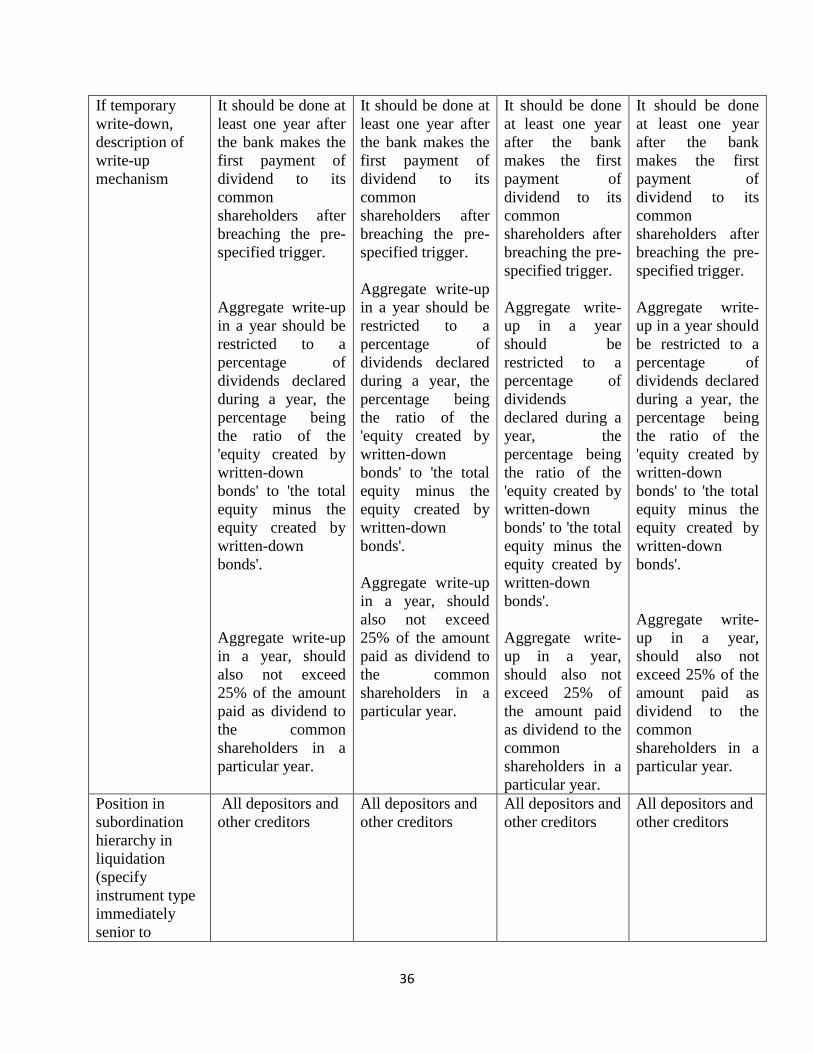

If temporary

write-down,

description of

write-up

mechanism

It should be done at

least one year after

the bank makes the

first payment of

dividend to its

common

shareholders after

breaching the pre-

specified trigger.

Aggregate write-up

in a year should be

restricted to a

percentage of

dividends declared

during a year, the

percentage being

the ratio of the

'equity created by

written-down

bonds' to 'the total

equity minus the

equity created by

written-down

bonds'.

Aggregate write-up

in a year, should

also not exceed

25% of the amount

paid as dividend to

the common

shareholders in a

particular year.

It should be done at

least one year after

the bank makes the

first payment of

dividend to its

common

shareholders after

breaching the pre-

specified trigger.

Aggregate write-up

in a year should be

restricted to a

percentage of

dividends declared

during a year, the

percentage being

the ratio of the

'equity created by

written-down

bonds' to 'the total

equity minus the

equity created by

written-down

bonds'.

Aggregate write-up

in a year, should

also not exceed

25% of the amount

paid as dividend to

the common

shareholders in a

particular year.

It should be done

at least one year

after the bank

makes the first

payment of

dividend to its

common

shareholders after

breaching the pre-

specified trigger.

Aggregate write-

up in a year

should be

restricted to a

percentage of

dividends

declared during a

year, the

percentage being

the ratio of the

'equity created by

written-down

bonds' to 'the total

equity minus the

equity created by

written-down

bonds'.

Aggregate write-

up in a year,

should also not

exceed 25% of

the amount paid

as dividend to the

common

shareholders in a

particular year.

It should be done

at least one year

after the bank

makes the first

payment of

dividend to its

common

shareholders after

breaching the pre-

specified trigger.

Aggregate write-

up in a year should

be restricted to a

percentage of

dividends declared

during a year, the

percentage being

the ratio of the

'equity created by

written-down

bonds' to 'the total

equity minus the

equity created by

written-down

bonds'.

Aggregate write-

up in a year,

should also not

exceed 25% of the

amount paid as

dividend to the

common

shareholders in a

particular year.

Position in

subordination

hierarchy in

liquidation

(specify

instrument type

immediately

senior to

All depositors and

other creditors

All depositors and

other creditors

All depositors and

other creditors

All depositors and

other creditors

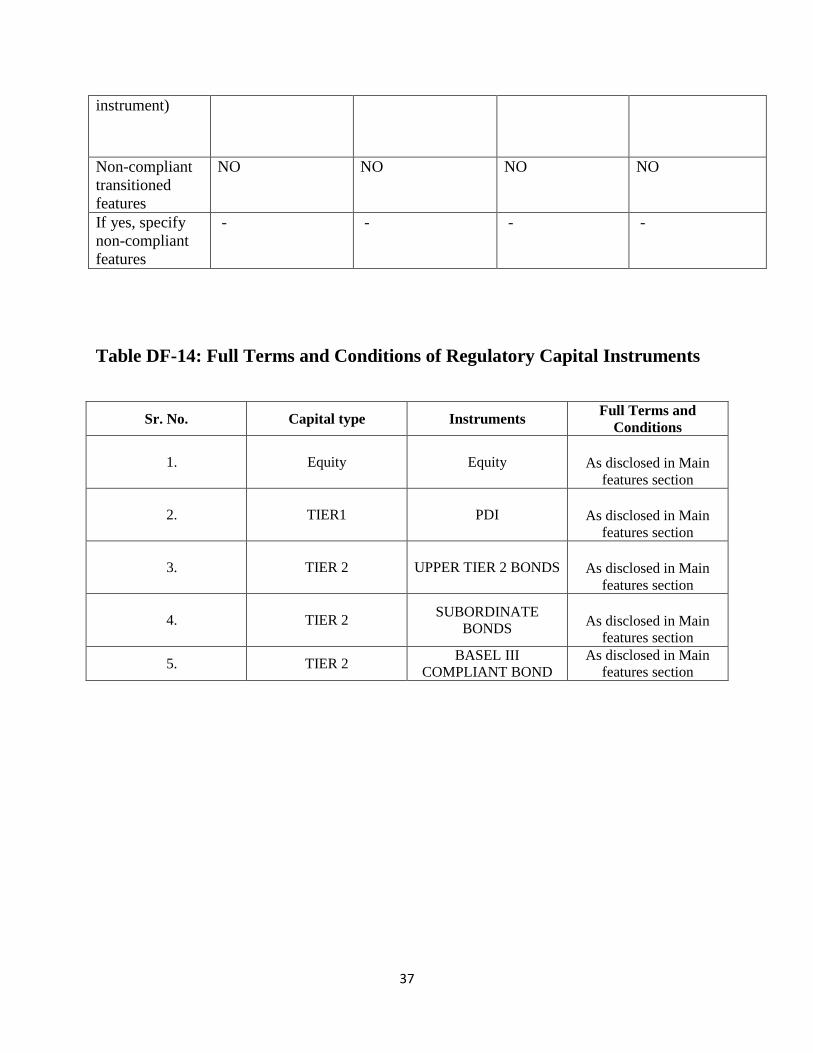

37

instrument)

Non-compliant

transitioned

features

NO NO NO NO

If yes, specify

non-compliant

features

- - - -

Table DF-14: Full Terms and Conditions of Regulatory Capital Instruments

Sr. No. Capital type Instruments Full Terms and

Conditions

1. Equity Equity

As disclosed in Main

features section

2. TIER1 PDI

As disclosed in Main

features section

3. TIER 2 UPPER TIER 2 BONDS

As disclosed in Main

features section

4. TIER 2 SUBORDINATE

BONDS

As disclosed in Main

features section

5. TIER 2 BASEL III

COMPLIANT BOND

As disclosed in Main

features section

38

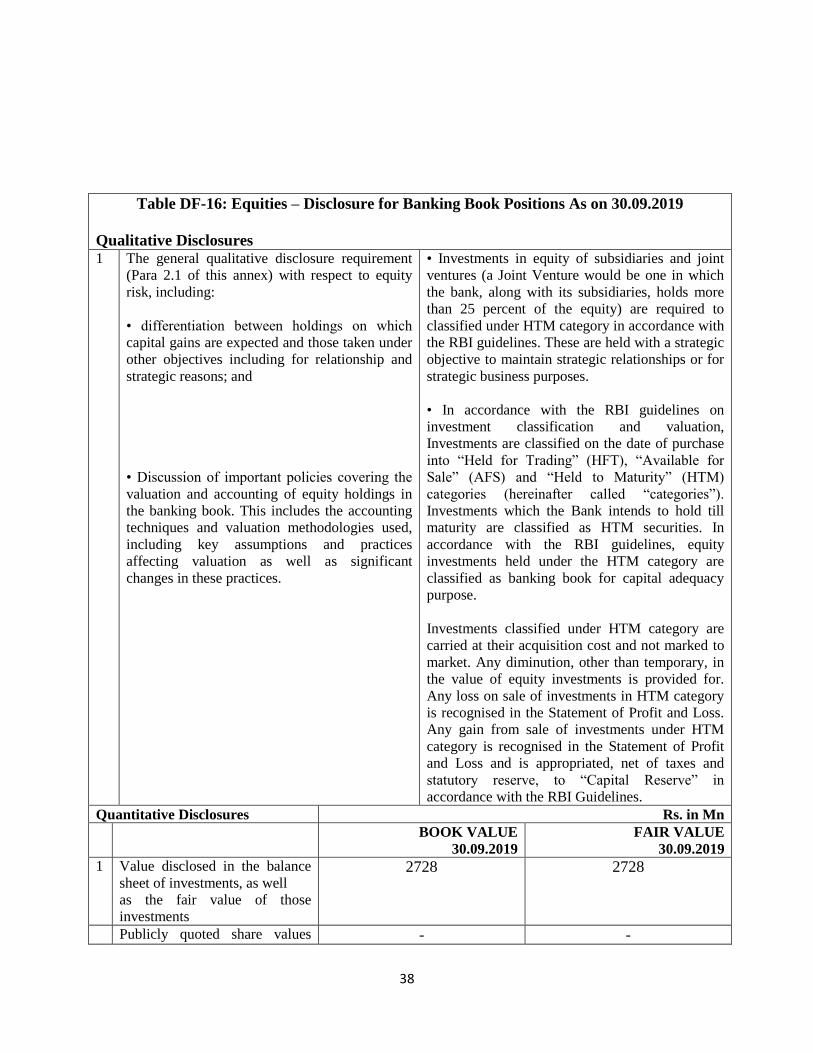

Table DF-16: Equities – Disclosure for Banking Book Positions As on 30.09.2019

Qualitative Disclosures

1 The general qualitative disclosure requirement

(Para 2.1 of this annex) with respect to equity

risk, including:

• differentiation between holdings on which

capital gains are expected and those taken under

other objectives including for relationship and

strategic reasons; and

• Discussion of important policies covering the

valuation and accounting of equity holdings in

the banking book. This includes the accounting

techniques and valuation methodologies used,

including key assumptions and practices

affecting valuation as well as significant

changes in these practices.

• Investments in equity of subsidiaries and joint

ventures (a Joint Venture would be one in which

the bank, along with its subsidiaries, holds more

than 25 percent of the equity) are required to

classified under HTM category in accordance with

the RBI guidelines. These are held with a strategic

objective to maintain strategic relationships or for

strategic business purposes.

• In accordance with the RBI guidelines on

investment classification and valuation,

Investments are classified on the date of purchase

into “Held for Trading” (HFT), “Available for

Sale” (AFS) and “Held to Maturity” (HTM)

categories (hereinafter called “categories”).

Investments which the Bank intends to hold till

maturity are classified as HTM securities. In

accordance with the RBI guidelines, equity

investments held under the HTM category are

classified as banking book for capital adequacy

purpose.

Investments classified under HTM category are

carried at their acquisition cost and not marked to

market. Any diminution, other than temporary, in

the value of equity investments is provided for.

Any loss on sale of investments in HTM category

is recognised in the Statement of Profit and Loss.

Any gain from sale of investments under HTM

category is recognised in the Statement of Profit

and Loss and is appropriated, net of taxes and

statutory reserve, to “Capital Reserve” in

accordance with the RBI Guidelines.

Quantitative Disclosures Rs. in Mn

BOOK VALUE

30.09.2019

FAIR VALUE

30.09.2019

1 Value disclosed in the balance

sheet of investments, as well

as the fair value of those

investments

2728 2728

Publicly quoted share values - -

39

where the share price is

materially different from fair

value

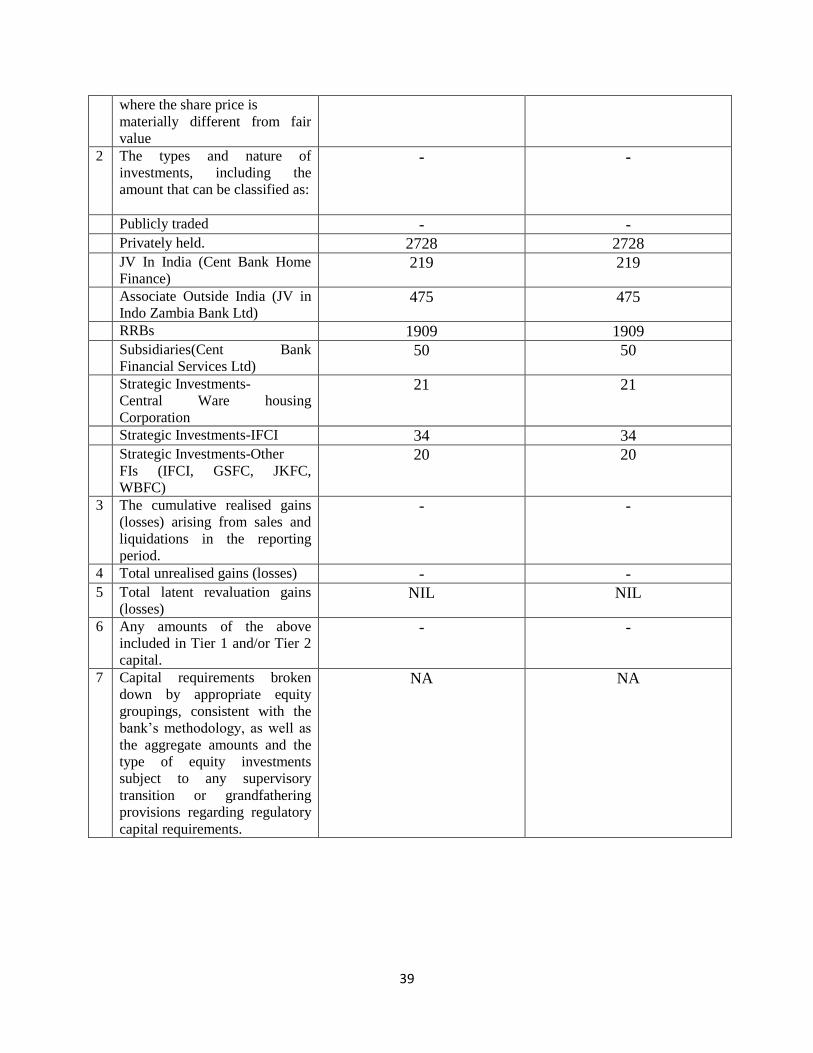

2 The types and nature of

investments, including the

amount that can be classified as:

- -

Publicly traded - - Privately held. 2728 2728 JV In India (Cent Bank Home

Finance) 219 219

Associate Outside India (JV in

Indo Zambia Bank Ltd) 475 475

RRBs 1909 1909 Subsidiaries(Cent Bank

Financial Services Ltd) 50 50

Strategic Investments-

Central Ware housing

Corporation

21 21

Strategic Investments-IFCI 34 34 Strategic Investments-Other

FIs (IFCI, GSFC, JKFC,

WBFC)

20 20

3 The cumulative realised gains

(losses) arising from sales and

liquidations in the reporting

period.

- -

4 Total unrealised gains (losses) - - 5 Total latent revaluation gains

(losses) NIL NIL

6 Any amounts of the above

included in Tier 1 and/or Tier 2

capital.

- -

7 Capital requirements broken

down by appropriate equity

groupings, consistent with the

bank‟s methodology, as well as

the aggregate amounts and the

type of equity investments

subject to any supervisory

transition or grandfathering

provisions regarding regulatory

capital requirements.

NA NA

40

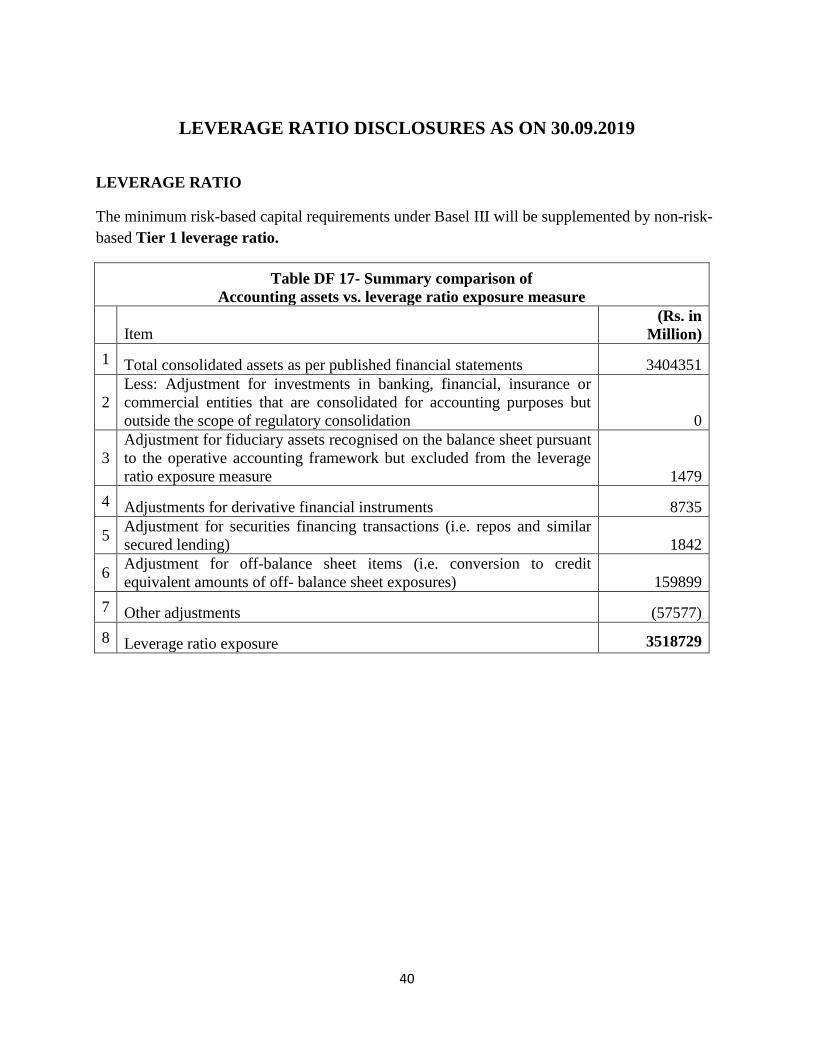

LEVERAGE RATIO DISCLOSURES AS ON 30.09.2019

LEVERAGE RATIO

The minimum risk-based capital requirements under Basel III will be supplemented by non-risk-

based Tier 1 leverage ratio.

Table DF 17- Summary comparison of

Accounting assets vs. leverage ratio exposure measure

Item (Rs. in

Million)

1 Total consolidated assets as per published financial statements 3404351

2

Less: Adjustment for investments in banking, financial, insurance or

commercial entities that are consolidated for accounting purposes but

outside the scope of regulatory consolidation 0

3

Adjustment for fiduciary assets recognised on the balance sheet pursuant

to the operative accounting framework but excluded from the leverage

ratio exposure measure 1479

4 Adjustments for derivative financial instruments 8735

5 Adjustment for securities financing transactions (i.e. repos and similar

secured lending) 1842

6 Adjustment for off-balance sheet items (i.e. conversion to credit

equivalent amounts of off- balance sheet exposures) 159899

7 Other adjustments (57577)

8 Leverage ratio exposure 3518729

41

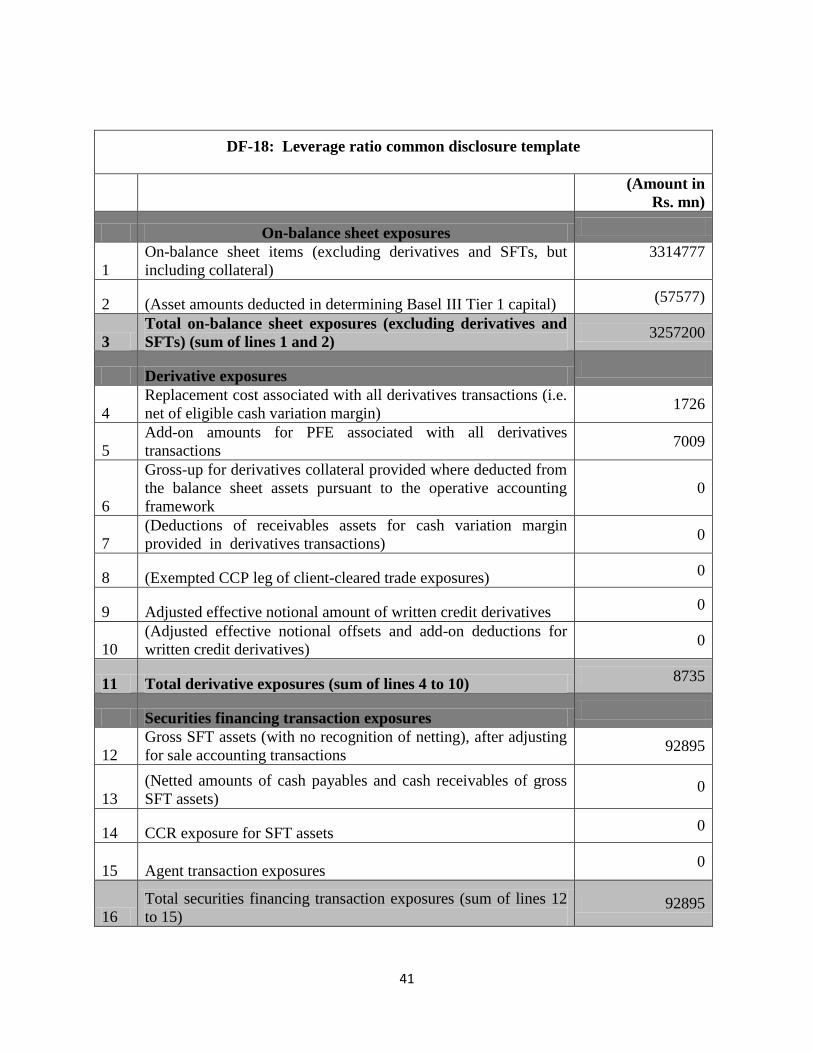

DF-18: Leverage ratio common disclosure template

(Amount in

Rs. mn)

On-balance sheet exposures

1

On-balance sheet items (excluding derivatives and SFTs, but

including collateral)

3314777

2 (Asset amounts deducted in determining Basel III Tier 1 capital) (57577)

3

Total on-balance sheet exposures (excluding derivatives and

SFTs) (sum of lines 1 and 2) 3257200

Derivative exposures

4

Replacement cost associated with all derivatives transactions (i.e.

net of eligible cash variation margin) 1726

5

Add-on amounts for PFE associated with all derivatives

transactions 7009

6

Gross-up for derivatives collateral provided where deducted from

the balance sheet assets pursuant to the operative accounting

framework

0

7

(Deductions of receivables assets for cash variation margin

provided in derivatives transactions) 0

8 (Exempted CCP leg of client-cleared trade exposures) 0

9 Adjusted effective notional amount of written credit derivatives 0

10

(Adjusted effective notional offsets and add-on deductions for

written credit derivatives) 0

11 Total derivative exposures (sum of lines 4 to 10) 8735

Securities financing transaction exposures

12

Gross SFT assets (with no recognition of netting), after adjusting

for sale accounting transactions 92895

13

(Netted amounts of cash payables and cash receivables of gross

SFT assets) 0

14 CCR exposure for SFT assets 0

15 Agent transaction exposures 0

16

Total securities financing transaction exposures (sum of lines 12

to 15) 92895

42

Other off-balance sheet exposures

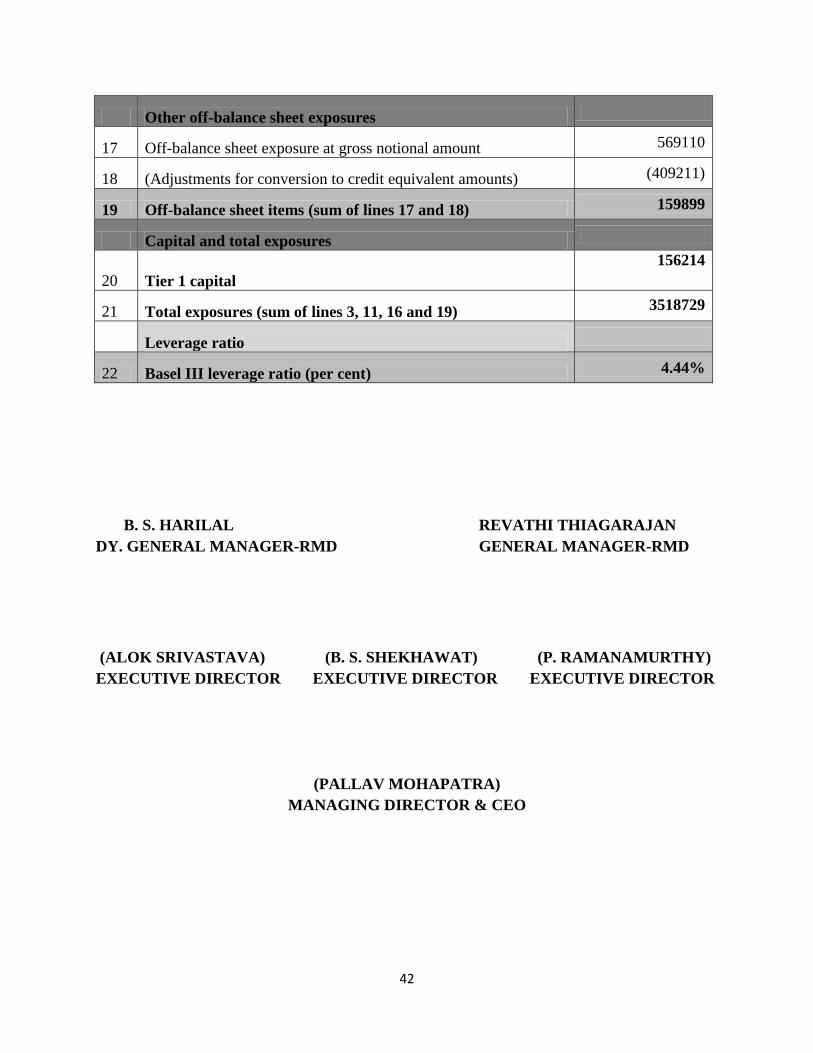

17 Off-balance sheet exposure at gross notional amount 569110

18 (Adjustments for conversion to credit equivalent amounts) (409211)

19 Off-balance sheet items (sum of lines 17 and 18) 159899

Capital and total exposures

20 Tier 1 capital

156214

21 Total exposures (sum of lines 3, 11, 16 and 19) 3518729

Leverage ratio

22 Basel III leverage ratio (per cent) 4.44%

B. S. HARILAL REVATHI THIAGARAJAN

DY. GENERAL MANAGER-RMD GENERAL MANAGER-RMD

(ALOK SRIVASTAVA) (B. S. SHEKHAWAT) (P. RAMANAMURTHY)

EXECUTIVE DIRECTOR EXECUTIVE DIRECTOR EXECUTIVE DIRECTOR

(PALLAV MOHAPATRA)

MANAGING DIRECTOR & CEO

Recommended