Personal Lines Insurance:Overview & Outlook

Pillars of Profitability &Drivers of Revenue, Cost,

Profit & Competition

Insurance Information Institute

March 2006

Robert P. Hartwig, Ph.D., CPCU, Senior Vice President & Chief EconomistInsurance Information Institute 110 William Street New York, NY 10038

Tel: (212) 346-5520 Fax: (212) 732-1916 [email protected] www.iii.org

Presentation Outline

• P/C Profit Overview Auto & Home

• Public Perceptions of the P/C Insurance Industry• The Six Pillars of P/C Profitability

Underwriting Pricing Investments Expenses Leverage (Capacity) P/C Operating Environment: Tort Focus

• Catastrophe Loss Management• Auto Insurance: Drivers of Success• Homeowners Insurance: The Jury’s Still Out

Insurance-to-Value

P/C PROFIT OVERVIEW

2006 Outlook is Good

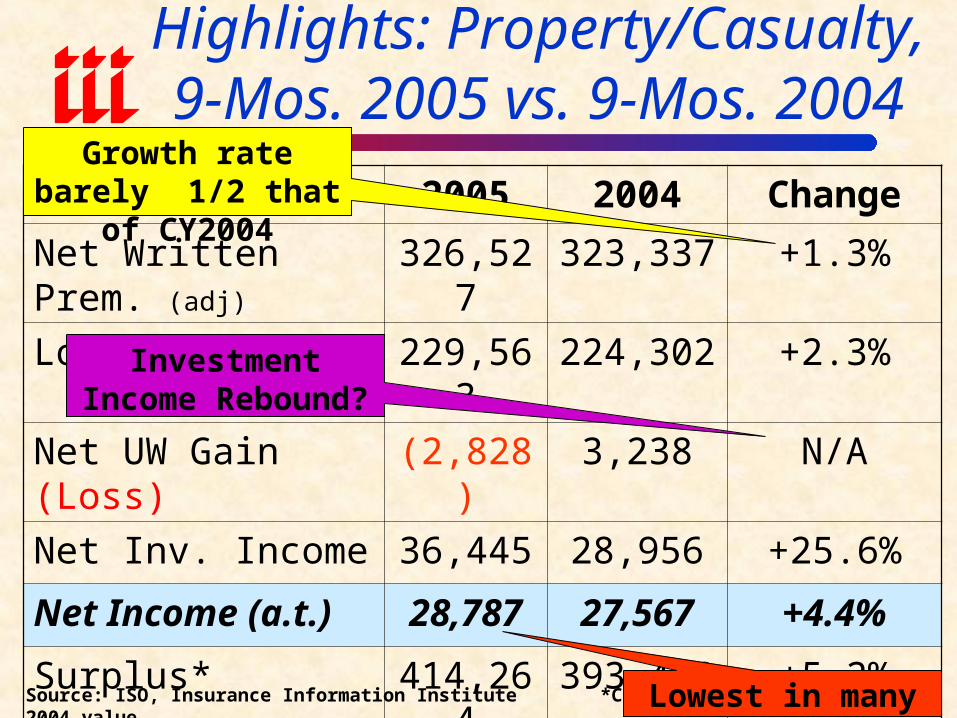

Highlights: Property/Casualty,9-Mos. 2005 vs. 9-Mos. 2004

2005 2004 Change

Net Written Prem. (adj) 326,527 323,337 +1.3%

Loss & LAE 229,563 224,302 +2.3%

Net UW Gain (Loss) (2,828) 3,238 N/A

Net Inv. Income 36,445 28,956 +25.6%

Net Income (a.t.) 28,787 27,567 +4.4%

Surplus* 414,264 393,488 +5.2%

Combined Ratio* 100.0 98.1 +1.9 pts.

Source: ISO, Insurance Information Institute *Comparison is with year-end 2004 value.

Growth rate barely 1/2 that of CY2004

Investment Income Rebound?

Lowest in many years

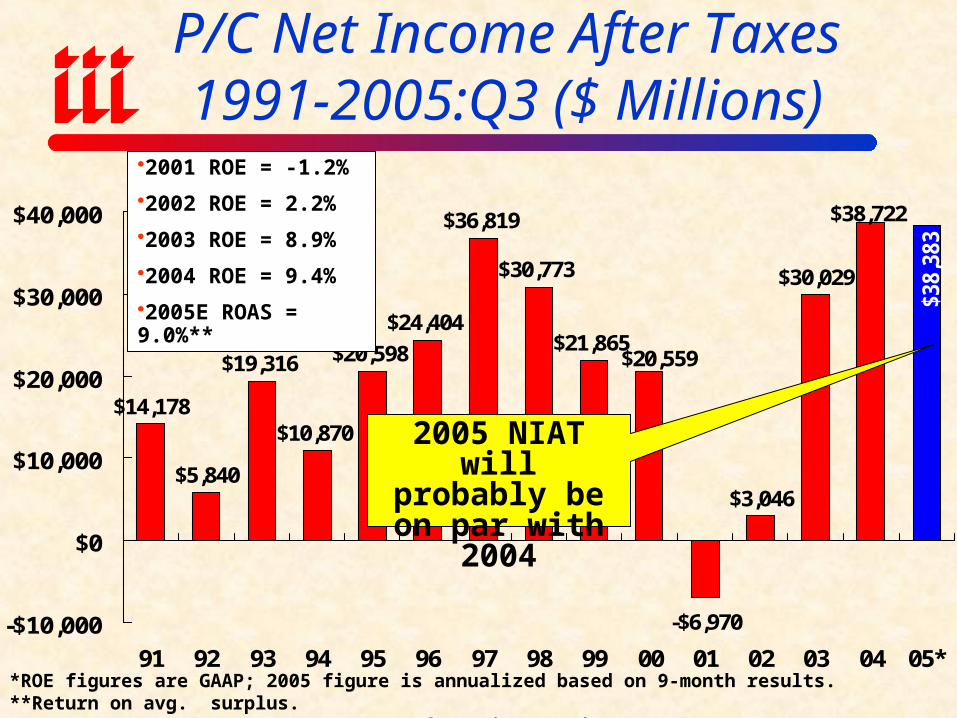

P/C Net Income After Taxes1991-2005:Q3 ($ Millions)

$14,178

$5,840

$19,316

$10,870

$20,598

$24,404

$36,819

$30,773

$21,865

-$6,970

$3,046

$30,029

$38,

383

$20,559

$38,722

-$10,000

$0

$10,000

$20,000

$30,000

$40,000

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05**ROE figures are GAAP; 2005 figure is annualized based on 9-month results. **Return on avg. surplus.Sources: A.M. Best, ISO, Insurance Information Institute.

2001 ROE = -1.2%

2002 ROE = 2.2%

2003 ROE = 8.9%

2004 ROE = 9.4%

2005E ROAS = 9.0%**

2005 NIAT will probably be on par with 2004

-10%

-5%

0%

5%

10%

15%

20%

25%

19

70

19

71

19

72

19

73

19

74

19

75

19

76

19

77

19

78

19

79

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

F2

00

7F

20

08

F2

00

9F

20

10

F

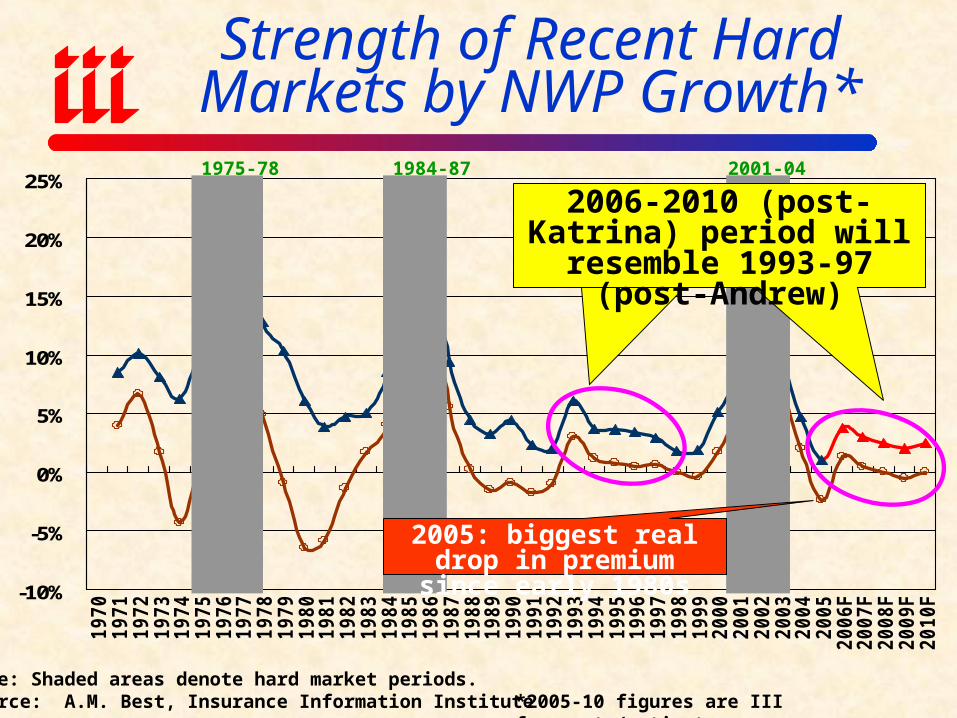

Note: Shaded areas denote hard market periods.Source: A.M. Best, Insurance Information Institute

Strength of Recent Hard Markets by NWP Growth*

1975-78 1984-87 2001-04

*2005-10 figures are III forecasts/estimates.

2006-2010 (post-Katrina) period will resemble 1993-97

(post-Andrew)

2005: biggest real drop in premium since early 1980s

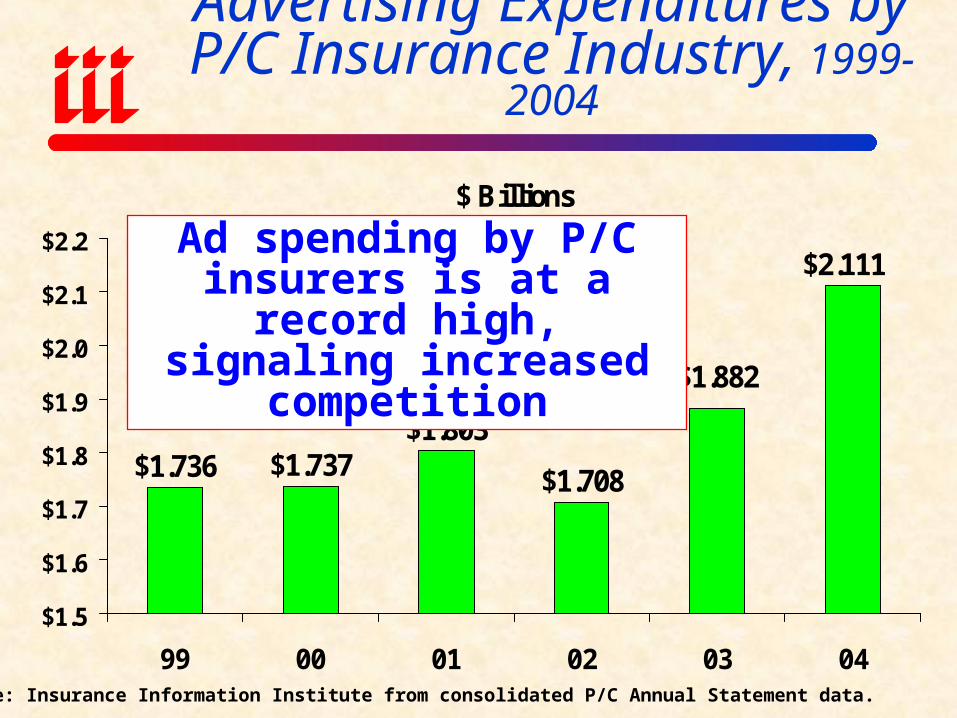

Advertising Expenditures by P/C Insurance Industry, 1999-2004

$ Billions

$1.736 $1.737$1.803

$1.708

$2.111

$1.882

$1.5

$1.6

$1.7

$1.8

$1.9

$2.0

$2.1

$2.2

99 00 01 02 03 04Source: Insurance Information Institute from consolidated P/C Annual Statement data.

Ad spending by P/C insurers is at a record high, signaling

increased competition

-5%

0%

5%

10%

15%

20%

87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04

05H

1

05E

06E

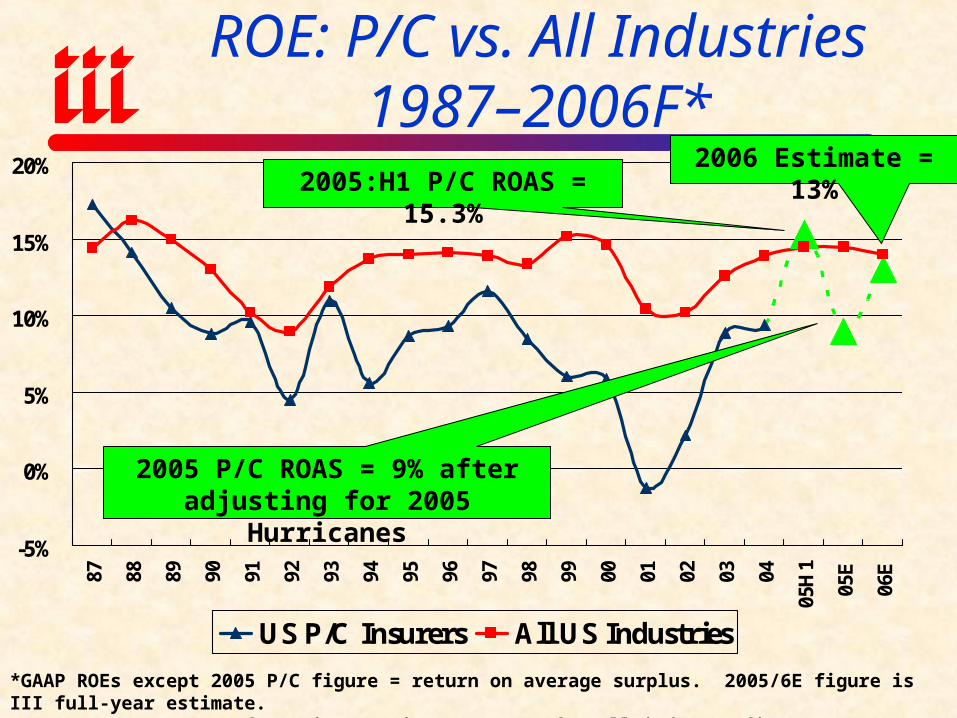

US P/C Insurers All US Industries

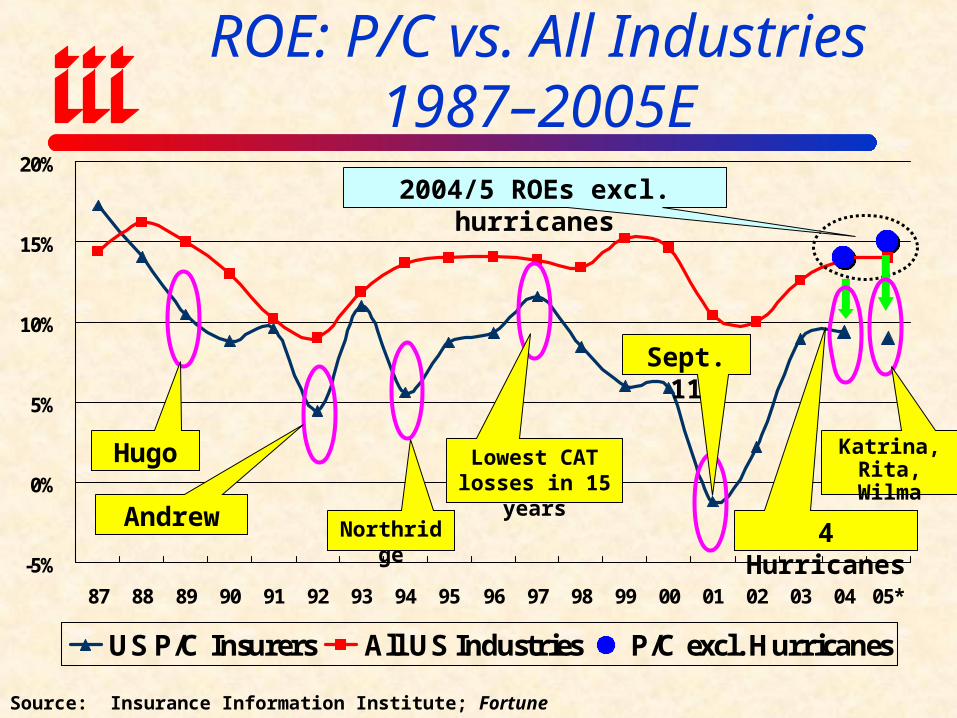

ROE: P/C vs. All Industries 1987–2006F*

*GAAP ROEs except 2005 P/C figure = return on average surplus. 2005/6E figure is III full-year estimate.Source: Insurance Information Institute; Fortune for all industry figures

2005 P/C ROAS = 9% after adjusting for 2005 Hurricanes

2005:H1 P/C ROAS = 15.3%2006 Estimate = 13%

-5%

0%

5%

10%

15%

20%

87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05*

US P/C Insurers All US Industries P/C excl. Hurricanes

ROE: P/C vs. All Industries 1987–2005E

Source: Insurance Information Institute; Fortune

Andrew Northridge

Hugo Lowest CAT losses in 15 years

Sept. 11

2004/5 ROEs excl. hurricanes

4 Hurricanes

Katrina, Rita, Wilma

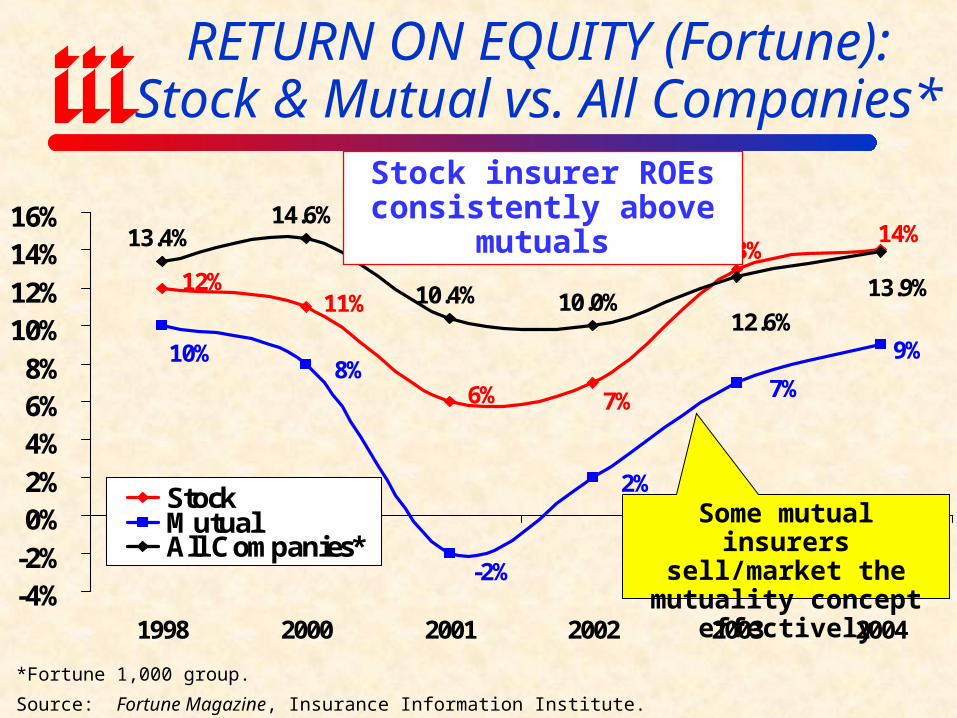

RETURN ON EQUITY (Fortune):Stock & Mutual vs. All Companies*

*Fortune 1,000 group.

Source: Fortune Magazine, Insurance Information Institute.

9%

13.4%14.6%

10.4% 10.0%

14%13%

7%6%

11%12%

-2%

8%7%

2%

10%

13.9%

12.6%

-4%-2%0%2%4%6%8%

10%12%14%16%

1998 2000 2001 2002 2003 2004

StockMutualAll Companies*

Stock insurer ROEs consistently above mutuals

Some mutual insurers sell/market the mutuality

concept effectively

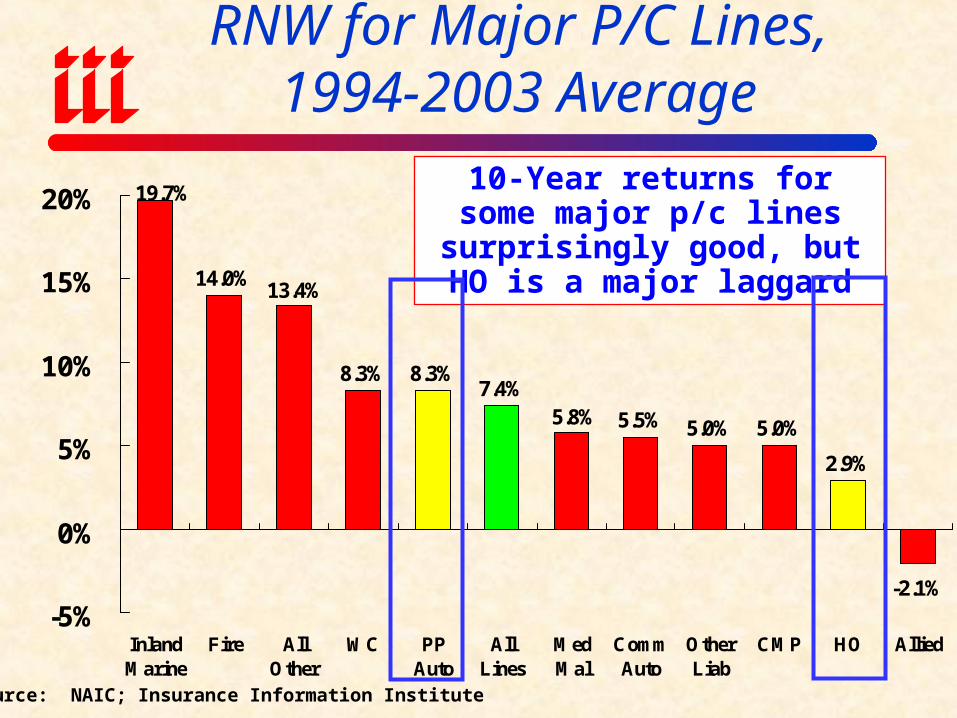

RNW for Major P/C Lines,1994-2003 Average

14.0%

8.3% 8.3%7.4%

5.5% 5.0% 5.0%

2.9%

-2.1%

19.7%

13.4%

5.8%

-5%

0%

5%

10%

15%

20%

InlandMarine

Fire AllOther

WC PPAuto

AllLines

MedMal

CommAuto

OtherLiab

CMP HO Allied

Source: NAIC; Insurance Information Institute

10-Year returns for some major p/c lines surprisingly good, but

HO is a major laggard

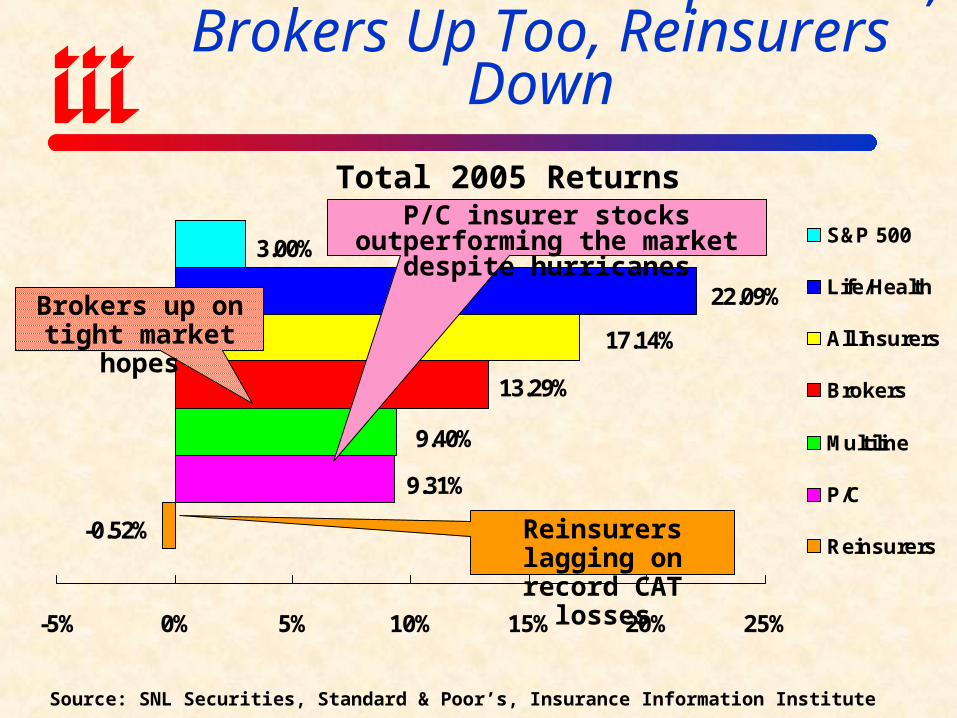

WALL STREET:

GENERALLY STRONG GAINS

P/C Insurers Stocks Up in 2005, Brokers Up Too, Reinsurers Down

-0.52%

9.31%

9.40%

13.29%

17.14%

22.09%

3.00%

-5% 0% 5% 10% 15% 20% 25%

S&P 500

Life/Health

All Insurers

Brokers

Multiline

P/C

Reinsurers

Source: SNL Securities, Standard & Poor’s, Insurance Information Institute

Total 2005 ReturnsP/C insurer stocks outperforming

the market despite hurricanes

Reinsurers lagging on record CAT losses

Brokers up on tight market hopes

4.2%

4.0% 4.5%

3.8%

2.2%

2.5% 3.

3%

2.7% 3.

9%

2.6% 3.2%

2.9%

4.9%

8.7% 9.3%

-4.0

%

-3.5

%

-2.7

%

-4.1

%

-5.3

%

-4.5

%

-5.7

%

-5.8

%

-6.0

%

-6.2

%

-5.3

%

-5.6

%

-5.6

%

-1.3

%

-0.5

%

-5.5

%

-6.4

% -4.8

%

-5.5

%

-0.6

%

1.9%

2.1% 3.

6% 4.8%

3.4%

2.2% 2.

8%

5.0%

7.0%

13.3

%

-10%

-5%

0%

5%

10%

15%

5-Aug

12-Aug

19-Aug

26-Aug

2-Sep

9-Sep

16-Sep

23-Sep

30-Sep

7-Oct

14-Oct

21-Oct

28-Oct

04-Nov

31-Dec

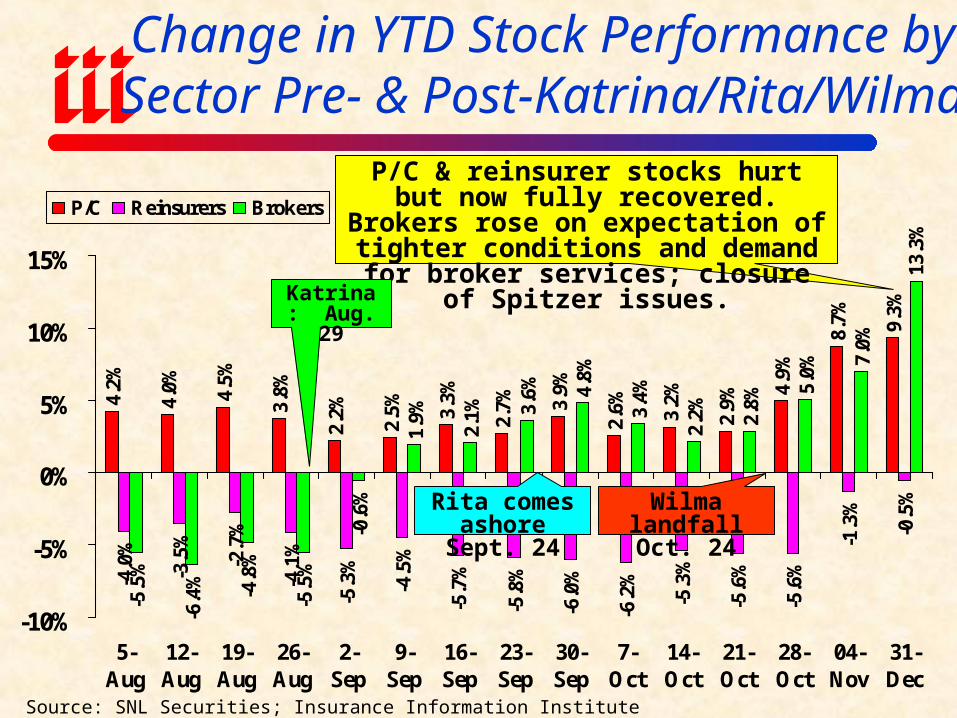

P/C Reinsurers Brokers

Source: SNL Securities; Insurance Information Institute

Change in YTD Stock Performance by Sector Pre- & Post-Katrina/Rita/Wilma

P/C & reinsurer stocks hurt but now fully recovered. Brokers rose on expectation of tighter conditions and demand for broker

services; closure of Spitzer issues.

Katrina: Aug. 29

Rita comes ashore Sept. 24

Wilma landfall Oct. 24

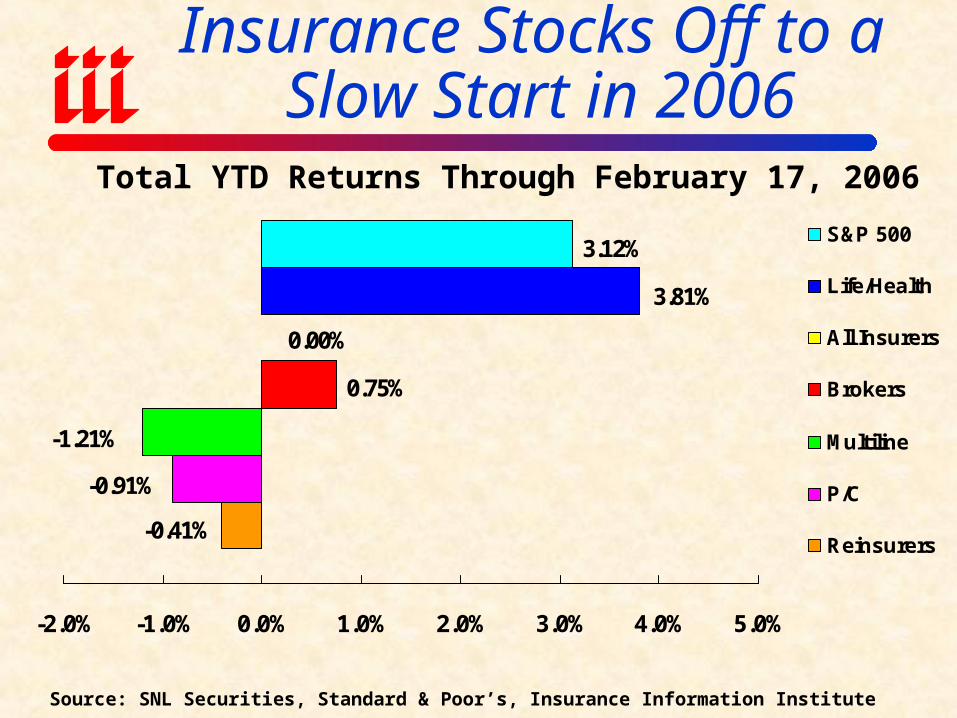

Insurance Stocks Off to a Slow Start in 2006

-0.41%

-0.91%

-1.21%

0.75%

0.00%

3.81%

3.12%

-2.0% -1.0% 0.0% 1.0% 2.0% 3.0% 4.0% 5.0%

S&P 500

Life/Health

All Insurers

Brokers

Multiline

P/C

Reinsurers

Source: SNL Securities, Standard & Poor’s, Insurance Information Institute

Total YTD Returns Through February 17, 2006

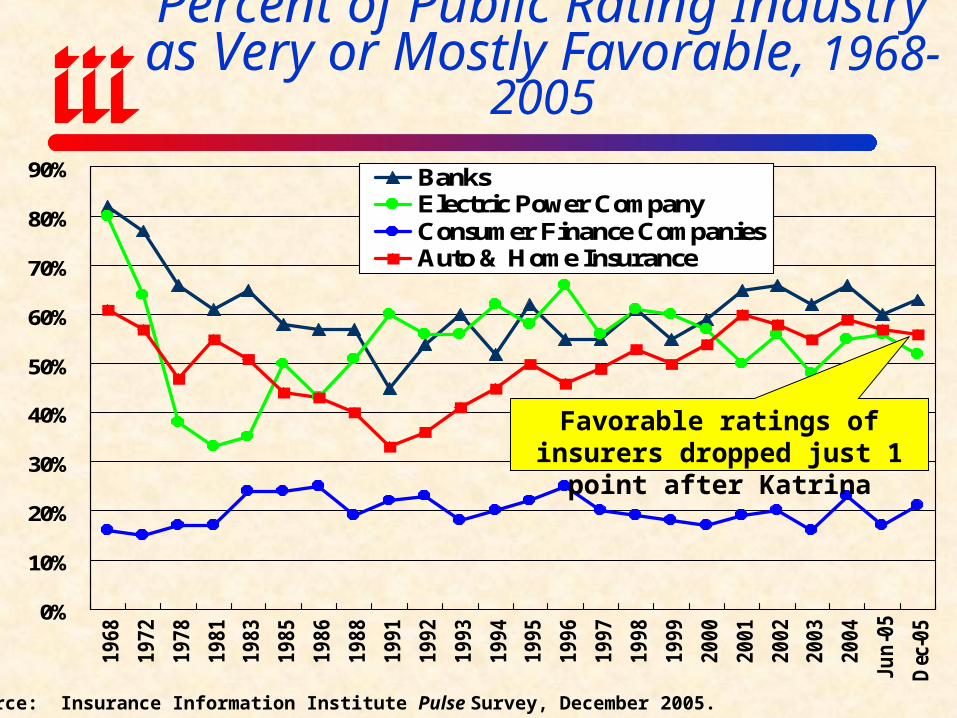

PUBLIC PERCEPTIONS OF INSURANCE

INDUSTRYHave Public Perceptions of the

Industry Been Affected by Mega-Disasters and Scandals

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

1968

1972

1978

1981

1983

1985

1986

1988

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

Ju

n-0

5

Dec

-05

BanksElectric Power CompanyConsumer Finance CompaniesAuto & Home Insurance

Source: Insurance Information Institute Pulse Survey, December 2005.

Percent of Public Rating Industry as Very or Mostly Favorable, 1968-2005

Favorable ratings of insurers dropped just 1 point after Katrina

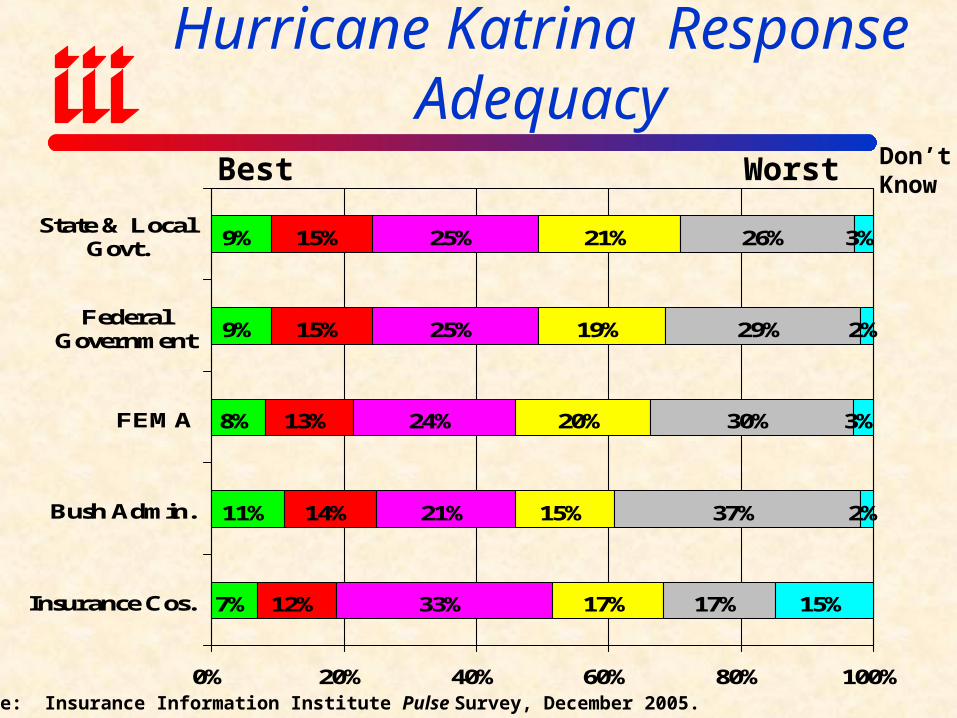

7%

11%

8%

9%

9%

12%

14%

13%

15%

15%

33%

21%

24%

25%

25%

17%

15%

20%

19%

21%

17%

37%

30%

29%

26%

15%

2%

3%

2%

3%

0% 20% 40% 60% 80% 100%

Insurance Cos.

Bush Admin.

FEMA

FederalGovernment

State & LocalGovt.

Source: Insurance Information Institute Pulse Survey, December 2005.

Public Perceptions of Hurricane Katrina Response AdequacyBest Worst Don’t

Know

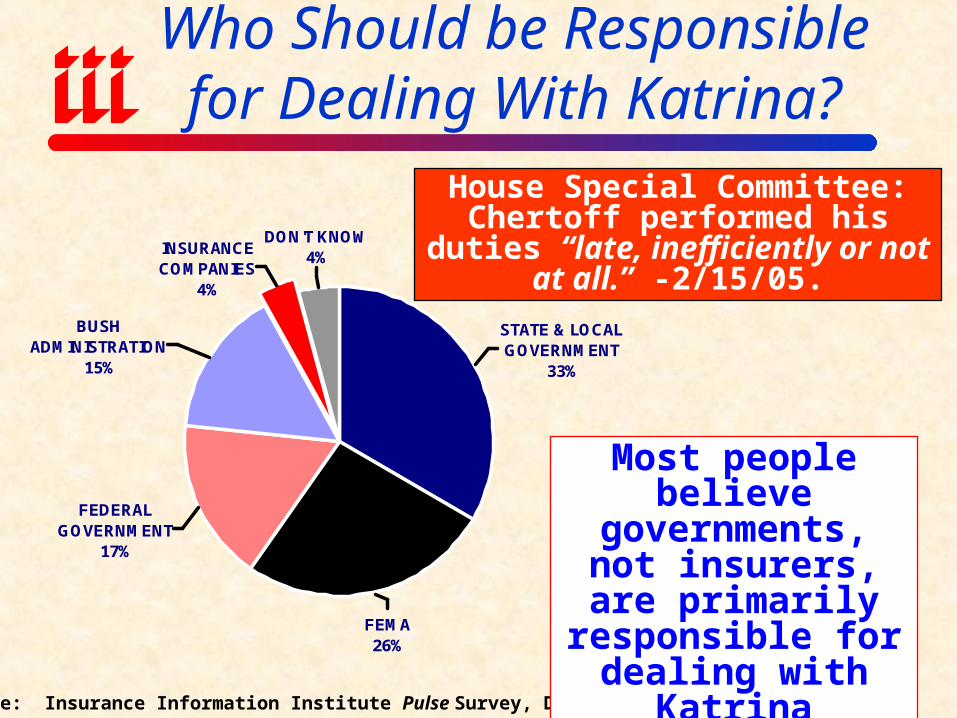

Who Should be Responsible for Dealing With Katrina?

STATE & LOCAL GOVERNMENT

33%

FEMA26%

FEDERAL GOVERNMENT

17%

BUSH ADMINISTRATION

15%

INSURANCE COMPANIES

4%

DON'T KNOW4%

Source: Insurance Information Institute Pulse Survey, December 2005.

Most people believe governments, not

insurers, are primarily responsible

for dealing with Katrina

House Special Committee: Chertoff performed his duties “late,

inefficiently or not at all.” -2/15/05.

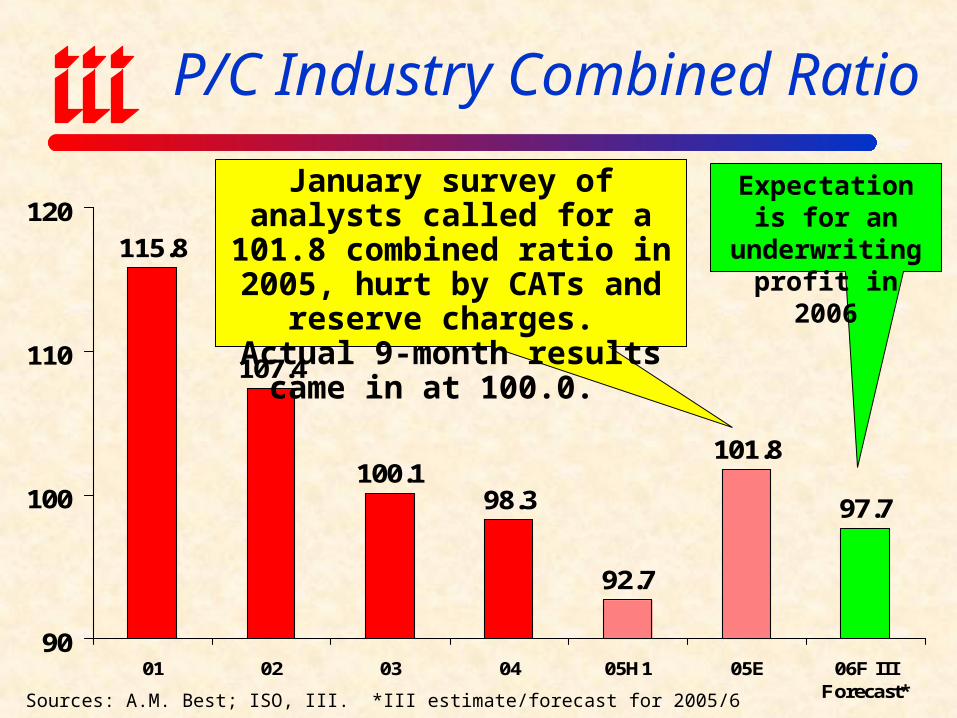

Profit Pillar #1UNDERWRITING

Surprisingly Strong in 2005, Stage is Set for a

Good 2006

115.8

107.4

100.198.3

92.7

101.8

97.7

90

100

110

120

01 02 03 04 05H1 05E 06F IIIForecast*

P/C Industry Combined Ratio

Sources: A.M. Best; ISO, III. *III estimate/forecast for 2005/6

January survey of analysts called for a 101.8 combined ratio

in 2005, hurt by CATs and reserve charges. Actual 9-month

results came in at 100.0.

Expectation is for an underwriting

profit in 2006

103.

9

104.

5

103.

5

104.

9

99.8 10

2.7

104.

5

109.

9

110.

9

105.

3

98.4

94.3

100.

0

95.9

85

90

95

100

105

110

115

93 94 95 96 97 98 99 00 01 02 03 04 05E 06F

Personal LinesCombined Ratio, 1993-2006E

Source: A.M. Best; Insurance Information Institute. 2006 forecast from Fitch Ratings as of 12/7/05.

A very strong 2006 is expected in personal lines assuming “normal”

catastrophe loss activity

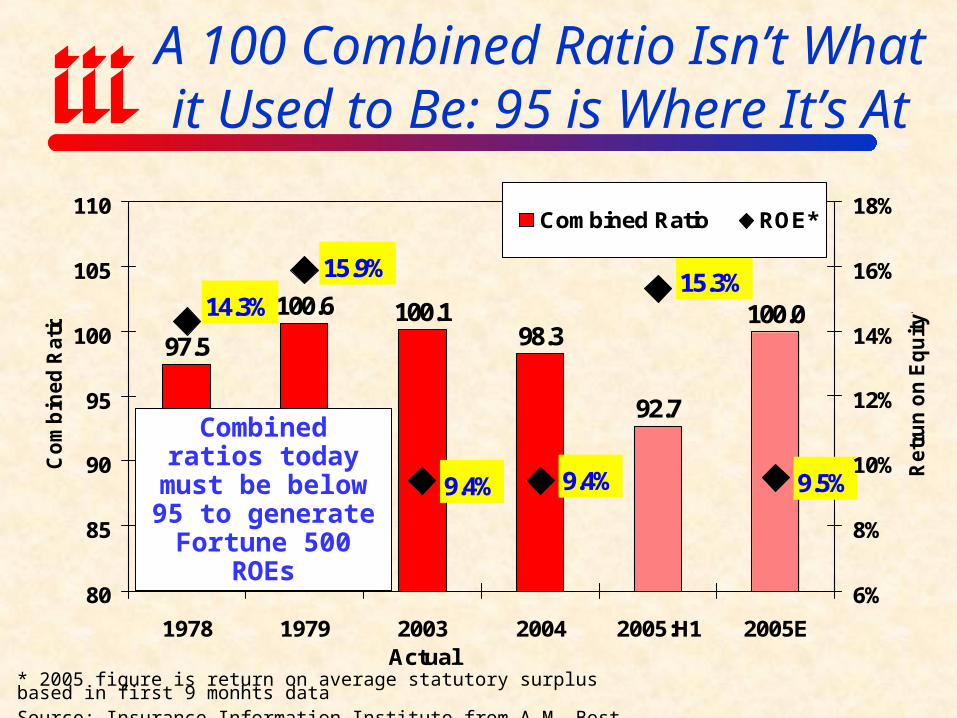

97.5

100.6 100.198.3

92.7

100.0

9.4% 9.5%

15.3%14.3%

15.9%

9.4%

80

85

90

95

100

105

110

1978 1979 2003Actual

2004 2005:H1 2005E

Co

mb

ined

Ratio

6%

8%

10%

12%

14%

16%

18%

Retr

un

on

Eq

uity*

Combined Ratio ROE*

* 2005 figure is return on average statutory surplus based in first 9 monhts dataSource: Insurance Information Institute from A.M. Best and ISO data.

A 100 Combined Ratio Isn’t What it Used to Be: 95 is Where It’s At

Combined ratios today must be below

95 to generate Fortune 500 ROEs

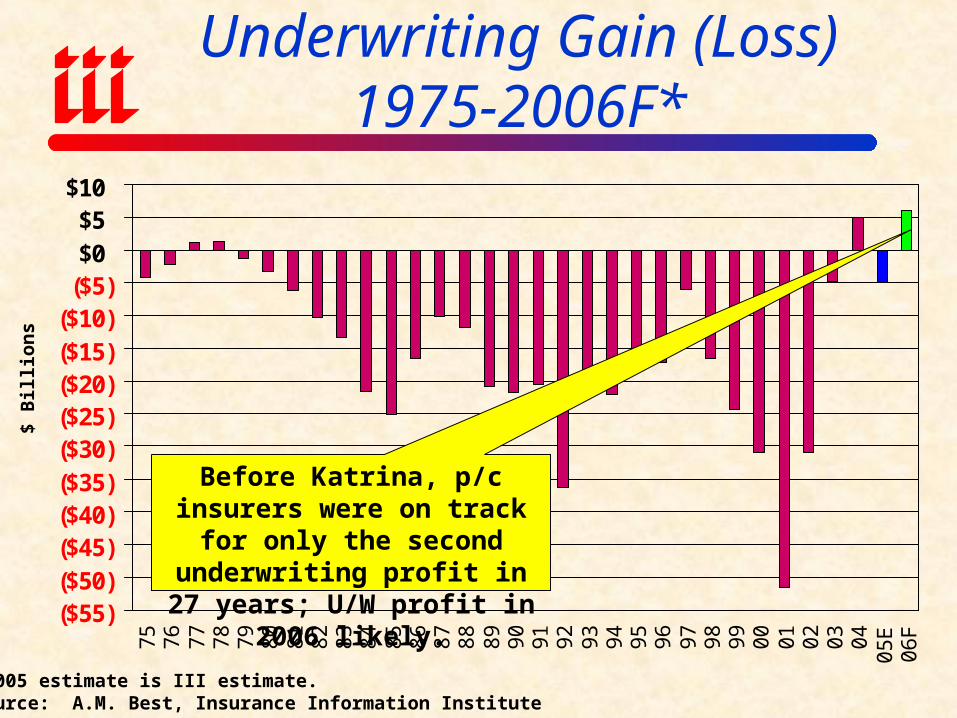

($55)($50)($45)($40)($35)($30)($25)($20)($15)($10)($5)$0$5

$10

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

00

01

02

03

04

05

E0

6F

Underwriting Gain (Loss)1975-2006F*

*2005 estimate is III estimate. Source: A.M. Best, Insurance Information Institute

$ B

illi

ons

Before Katrina, p/c insurers were on track for only the

second underwriting profit in 27 years; U/W profit in 2006 likely.

110

.5

10

5.0 11

3.6 11

9.2

10

4.8

10

0.8

10

0.5

114

.3

10

6.5

12

5.8

111

.0

12

4.6

12

4.1

10

8.8 11

5.8

10

6.9

10

8.5

10

6.7

10

6.0

10

1.9

10

5.9

10

8.0

110

.1 115

.8

10

7.4

10

0.1

98

.3 10

1.8

16

2.4

12

6.5

90

100

110

120

130

140

150

160

170

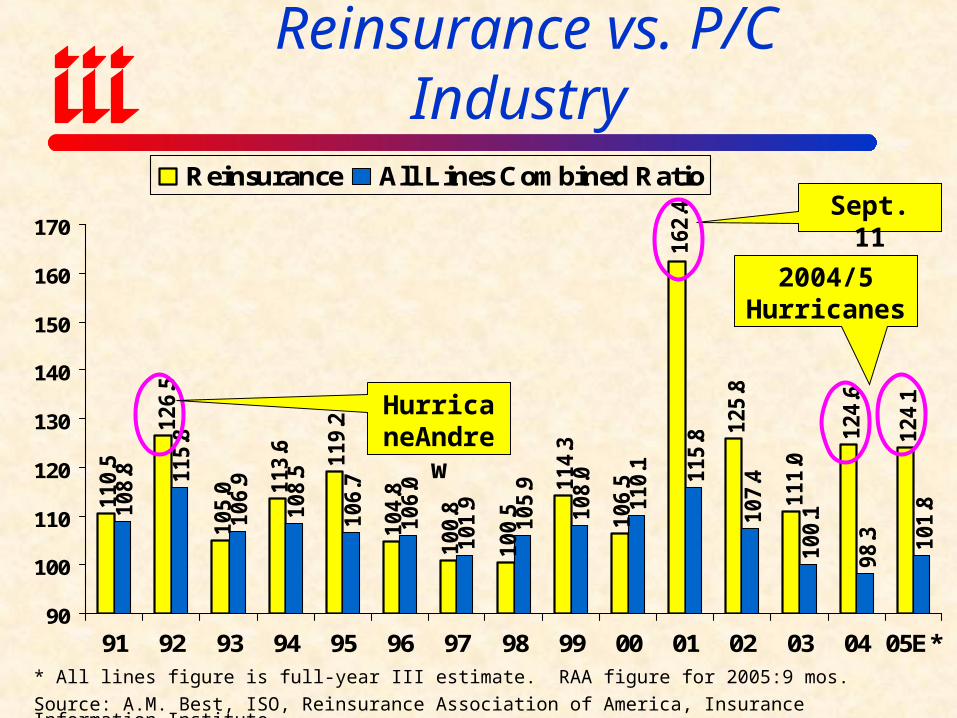

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05E*

Reinsurance All Lines Combined Ratio

Combined Ratio: Reinsurance vs. P/C Industry

* All lines figure is full-year III estimate. RAA figure for 2005:9 mos.

Source: A.M. Best, ISO, Reinsurance Association of America, Insurance Information Institute

HurricaneAndrew

Sept. 11

2004/5 Hurricanes

UNDERWRITING AFFECTS FINANCIAL

STRENGTH

Is There Causefor Concern?

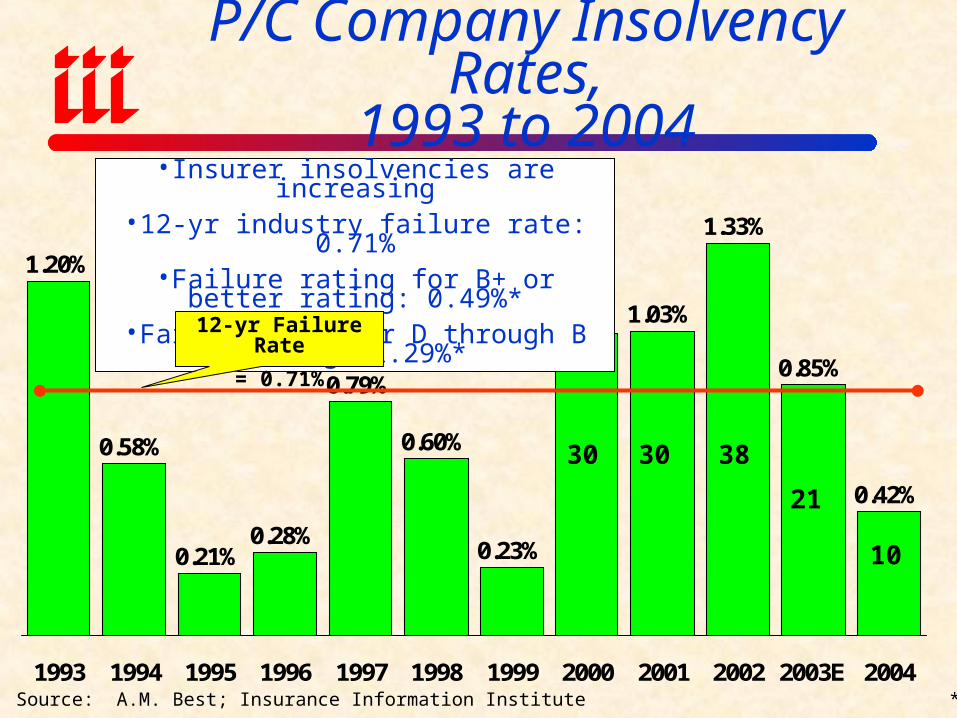

P/C Company Insolvency Rates,1993 to 2004

Source: A.M. Best; Insurance Information Institute *1993-2003

1.20%

0.58%

0.21%0.28%

0.79%

0.60%

0.23%

1.02% 1.03%

1.33%

0.85%

0.42%

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003E 2004

•Insurer insolvencies are increasing•12-yr industry failure rate: 0.71%

•Failure rating for B+ or better rating: 0.49%*•Failure rate for D through B rating: 1.29%*

383030

12-yr Failure Rate

= 0.71%

21

10

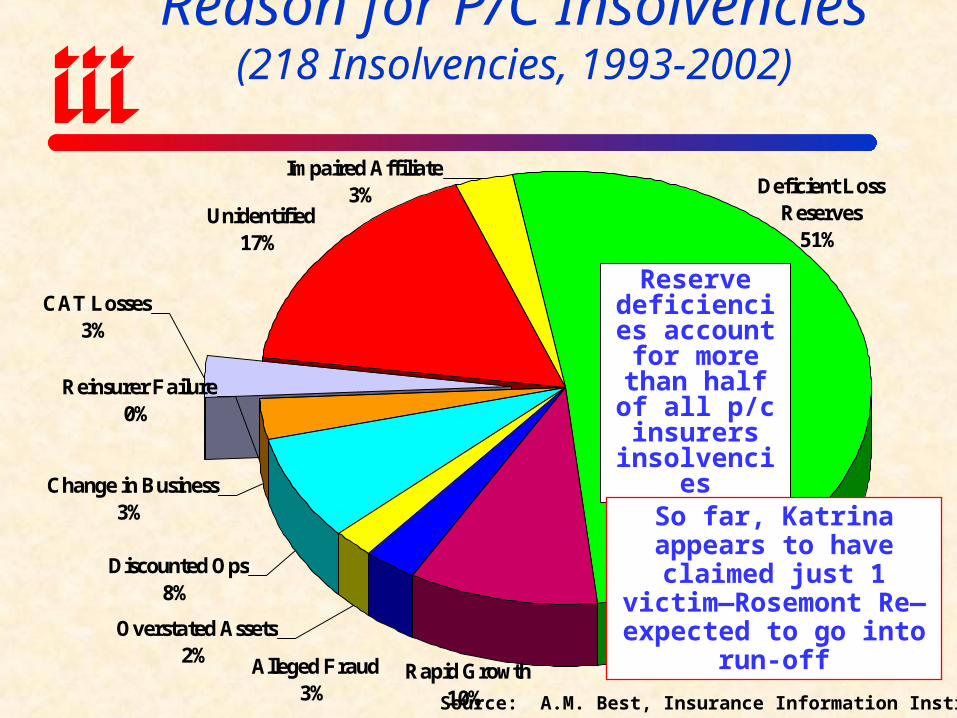

Reason for P/C Insolvencies(218 Insolvencies, 1993-2002)

Unidentified17%

Impaired Affiliate3%

Overstated Assets2%

Change in Business3%

CAT Losses3%

Reinsurer Failure0%

Rapid Growth10%

Discounted Ops8%

Alleged Fraud3%

Deficient Loss Reserves

51%

Source: A.M. Best, Insurance Information Institute

Reserve deficiencies account for

more than half of all p/c insurers

insolvencies

So far, Katrina appears to have claimed just 1 victim—Rosemont Re—expected

to go into run-off

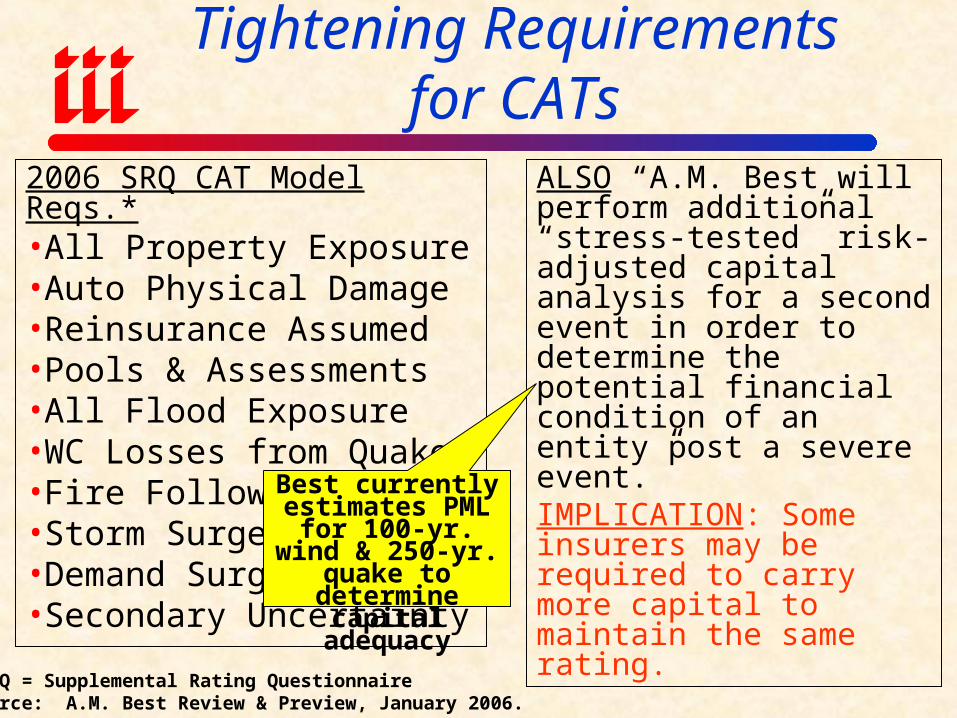

Ratings Agencies Tightening Requirements for CATs

2006 SRQ CAT Model Reqs.*•All Property Exposure•Auto Physical Damage•Reinsurance Assumed•Pools & Assessments•All Flood Exposure•WC Losses from Quake•Fire Following•Storm Surge•Demand Surge•Secondary Uncertainty

ALSO “A.M. Best will perform additional “stress-tested” risk-adjusted capital analysis for a second event in order to determine the potential financial condition of an entity post a severe event.”IMPLICATION: Some insurers may be required to carry more capital to maintain the same rating.

*SRQ = Supplemental Rating QuestionnaireSource: A.M. Best Review & Preview, January 2006.

Best currently estimates PML for

100-yr. wind & 250-yr. quake to determine capital

adequacy

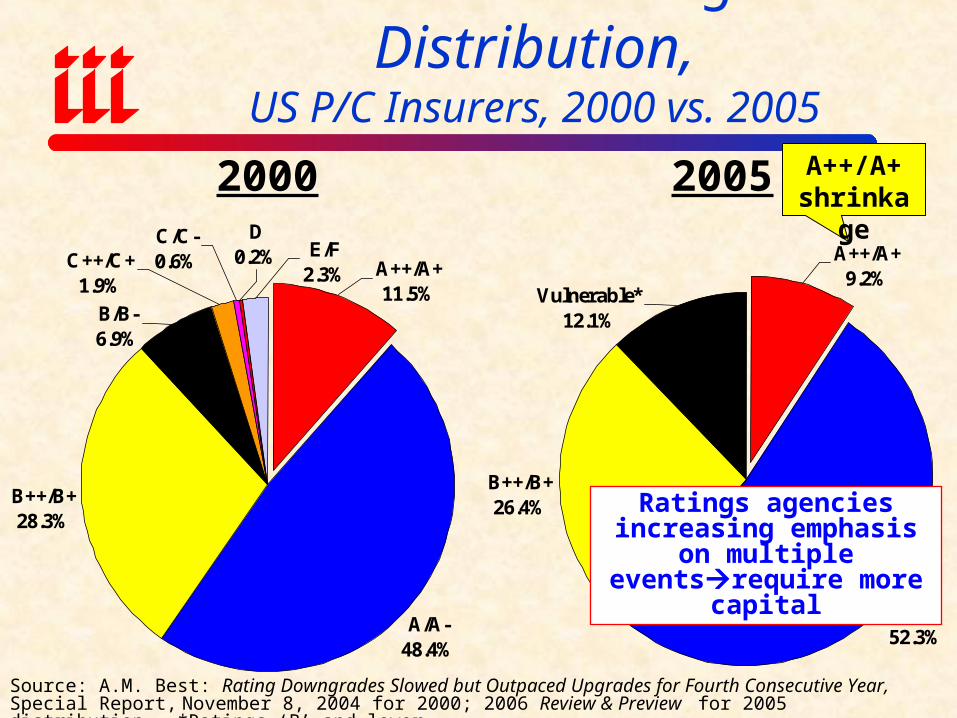

Historical Ratings Distribution,US P/C Insurers, 2000 vs. 2005

A/A-52.3%

A++/A+9.2%

B++/B+26.4%

Vulnerable*12.1%

Source: A.M. Best: Rating Downgrades Slowed but Outpaced Upgrades for Fourth Consecutive Year, Special Report, November 8, 2004 for 2000; 2006 Review & Preview for 2005 distribution. *Ratings ‘B’ and lower.

A/A-48.4%

D0.2%C++/C+

1.9%

E/F2.3% A++/A+

11.5%

C/C-0.6%

B++/B+28.3%

B/B-6.9%

2000 2005 A++/A+ shrinkage

Ratings agencies increasing emphasis on multiple

eventsrequire more capital

P/C Insurers Maintaining Rating of A+ or Better Rating for 50+ Years

P/C Company1. AIU Insurance Co.2. Alfa Mutual Ins. Co.3. Amica Mutual Ins. Co.4. Church Mutual Ins. Co.5. Federal Insurance Co.6. General Reinsurance Corp.

7. Great Northern Ins. Co.8. Lititz Mutual Ins. Co.9. Nationwide Mutual Fire Co.10. Otsego Mutual Fire11. Quincy Mutual Fire Ins. Co.12. State Automobile Mutual Ins. Co.13. State Farm Mutual Automobile Ins. Co.14. Vigilant Insurance Co.

Group Affiliation1. American International Group2. Alfa Insurance Group3. Amica Mutual Group4. None5. Chubb Group of Ins Cos.6. Berkshire Hathaway Ins. Group7. Chubb Group of Ins Cos.8. Lititz Mutual Group9. Nationwide Mutual Group10. None11. Quincy Mutual Group12. State Auto Ins. Group13. State Farm Group14. Chubb Group of Ins Cos.

Source: Best’s Review, January 1, 2004.

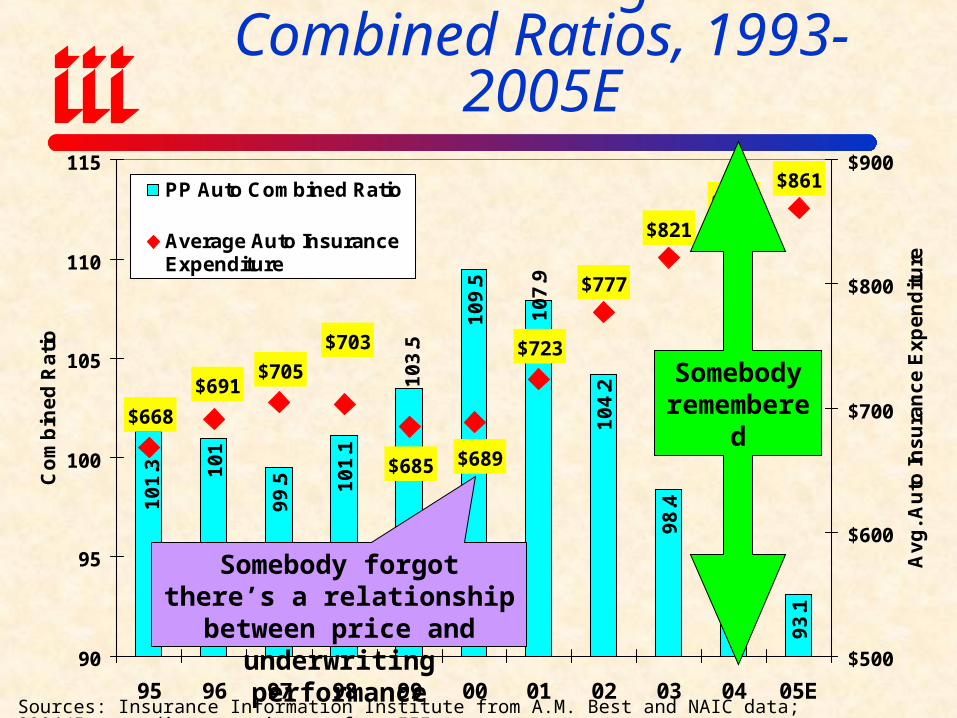

Underwriting Matters Because Pricing is Often Undisciplined

99

.5 10

1.1

10

9.5

10

4.2

98

.4

94

.0

93

.1

10

7.9

10

3.5

10

1.3 10

1

$777

$821

$844$861

$689$685

$705

$703 $723

$691

$668

90

95

100

105

110

115

95 96 97 98 99 00 01 02 03 04 05E

Co

mb

ine

d R

ati

o

$500

$600

$700

$800

$900

Av

g. A

uto

Ins

ura

nc

e E

xp

en

dit

ure

PP Auto Combined Ratio

Average Auto InsuranceExpenditure

Private Passenger AutoCombined Ratios, 1993-2005E

Sources: Insurance Information Institute from A.M. Best and NAIC data; 2004/5 expenditure estimates from III.

Somebody forgot there’s a relationship between price and

underwriting performance

Somebody remembered

CATASTROPHE LOSS

MANAGEMENT

Failure to Adequately Manage this Risk Has Been Devastating

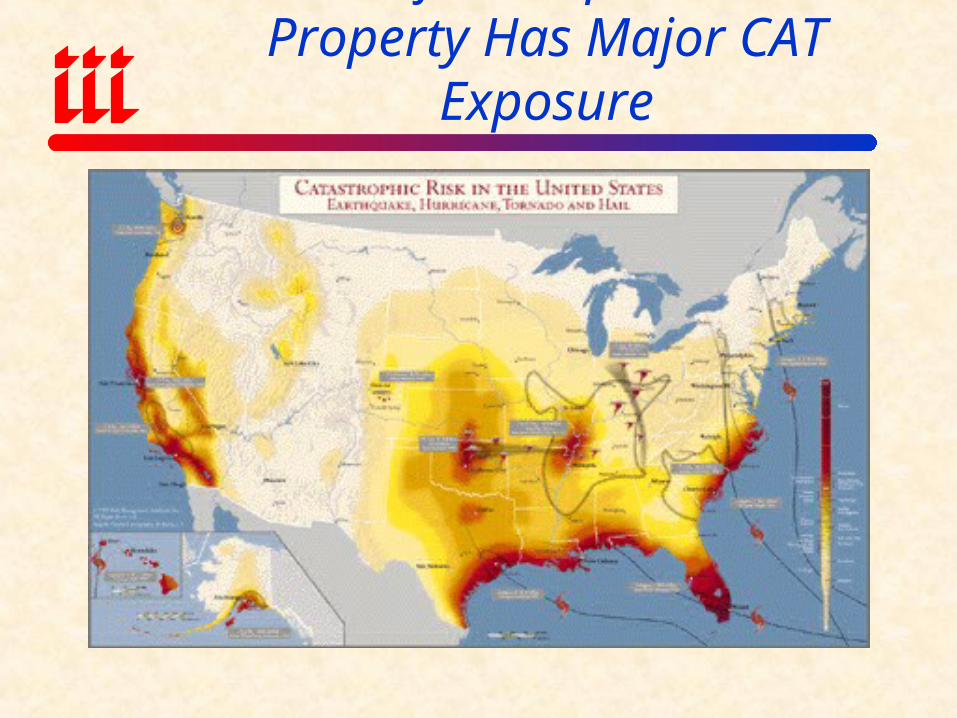

Most of US Population & Property Has Major CAT Exposure

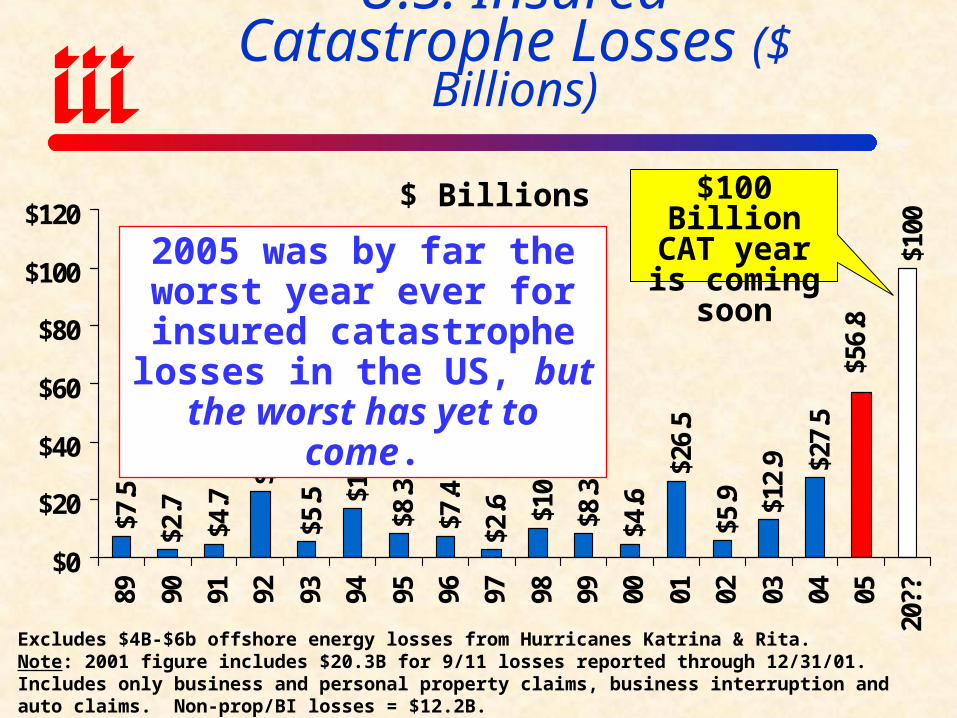

U.S. InsuredCatastrophe Losses ($ Billions)

$7.5

$2.7

$4.7

$22.

9

$5.5 $1

6.9

$8.3

$7.4

$2.6 $1

0.1

$8.3

$4.6

$26.

5

$5.9 $1

2.9 $2

7.5

$56.

8

$100

$0

$20

$40

$60

$80

$100

$120

89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05

20??

Excludes $4B-$6b offshore energy losses from Hurricanes Katrina & Rita.Note: 2001 figure includes $20.3B for 9/11 losses reported through 12/31/01. Includes only business and personal property claims, business interruption and auto claims. Non-prop/BI losses = $12.2B.Source: Property Claims Service/ISO; Insurance Information Institute

$ Billions

2005 was by far the worst year ever for insured

catastrophe losses in the US, but the worst has yet to come.

$100 Billion CAT year is coming soon

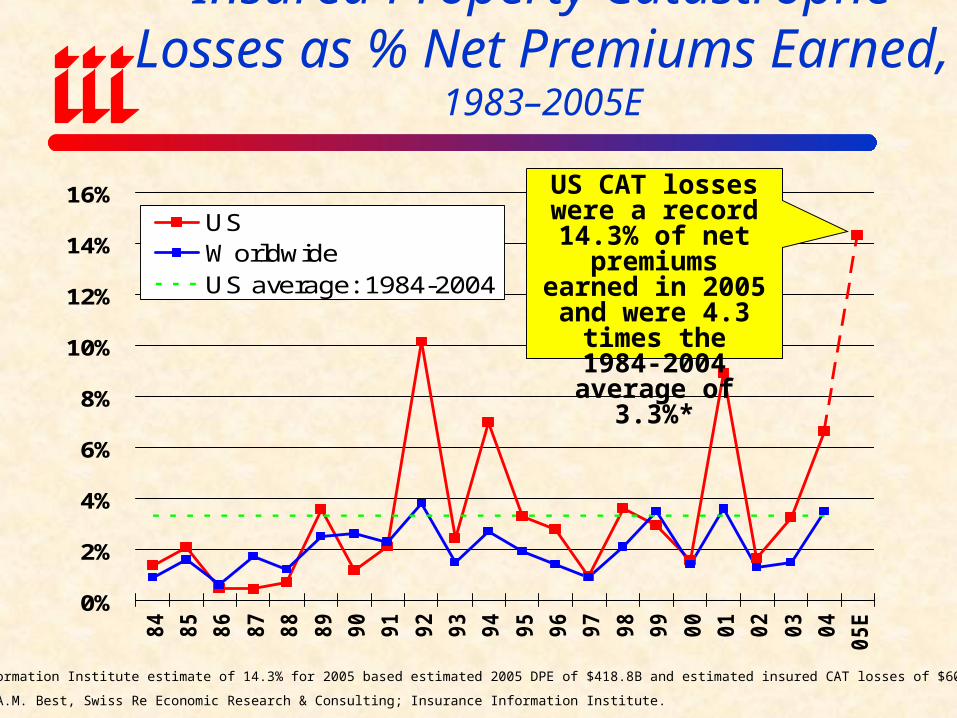

Insured Property Catastrophe Losses as % Net Premiums Earned, 1983–2005E

0%

2%

4%

6%

8%

10%

12%

14%

16%

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

00

01

02

03

04

05E

USWorldwideUS average: 1984-2004

*Insurance Information Institute estimate of 14.3% for 2005 based estimated 2005 DPE of $418.8B and estimated insured CAT losses of $60B.

Sources: ISO, A.M. Best, Swiss Re Economic Research & Consulting; Insurance Information Institute.

US CAT losses were a record 14.3% of

net premiums earned in 2005 and were 4.3 times the 1984-2004 average

of 3.3%*

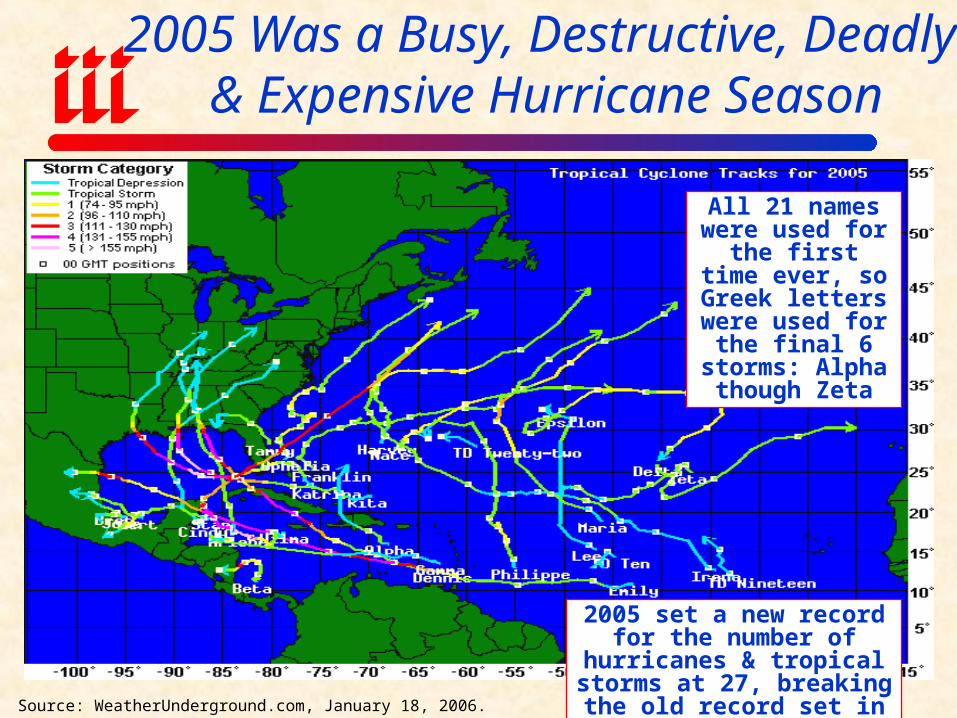

2005 Was a Busy, Destructive, Deadly & Expensive Hurricane Season

Source: WeatherUnderground.com, January 18, 2006.

All 21 names were used for the first

time ever, so Greek letters were used for the final 6

storms: Alpha though Zeta

2005 set a new record for the number of hurricanes &

tropical storms at 27, breaking the old record set in 1933.

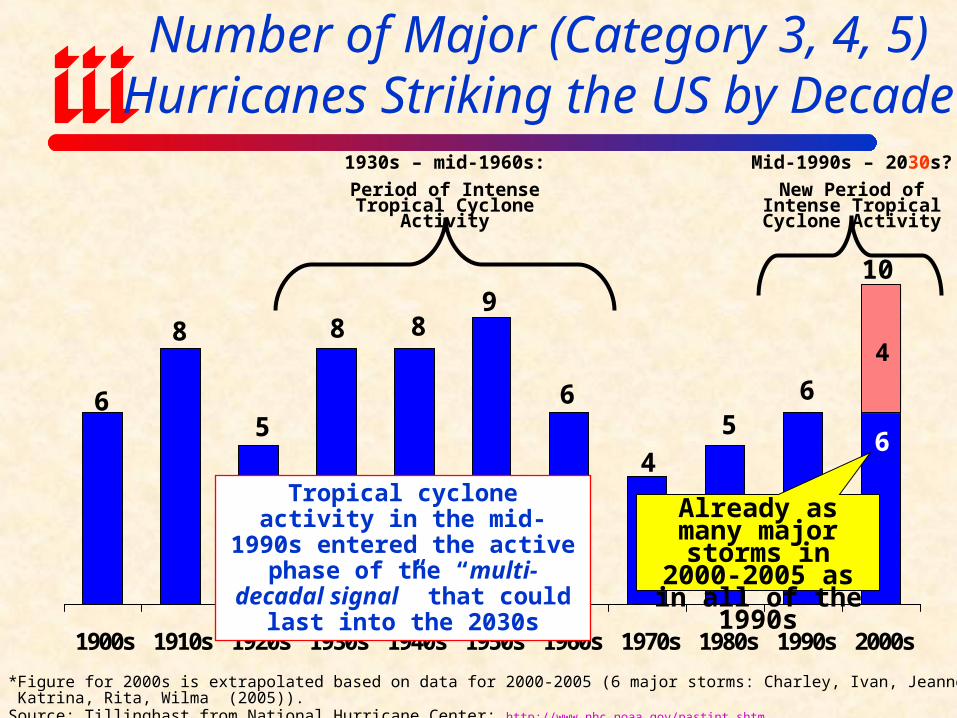

Number of Major (Category 3, 4, 5) Hurricanes Striking the US by Decade

4

6

65

4

6

88

5

8

6

9

1900s 1910s 1920s 1930s 1940s 1950s 1960s 1970s 1980s 1990s 2000s

*Figure for 2000s is extrapolated based on data for 2000-2005 (6 major storms: Charley, Ivan, Jeanne (2004) & Katrina, Rita, Wilma (2005)).Source: Tillinghast from National Hurricane Center: http://www.nhc.noaa.gov/pastint.shtm.

10

1930s – mid-1960s:

Period of Intense Tropical Cyclone Activity

Mid-1990s – 2030s?

New Period of Intense Tropical Cyclone Activity

Tropical cyclone activity in the mid-1990s entered the active

phase of the “multi-decadal signal” that could last into the 2030s

Already as many major storms in

2000-2005 as in all of the 1990s

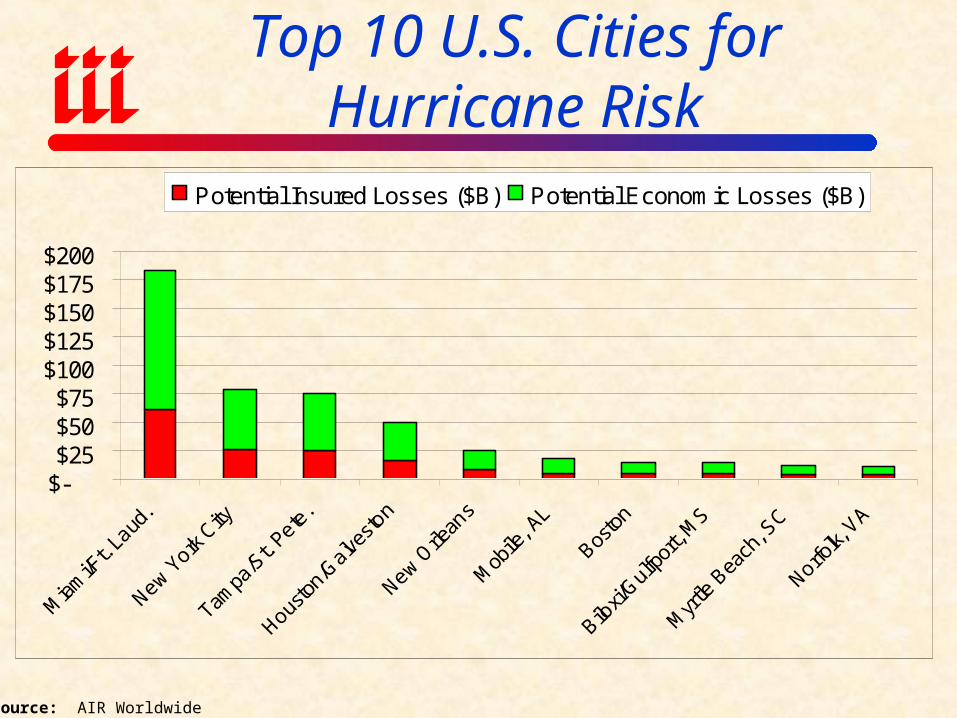

Top 10 U.S. Cities for Hurricane Risk

$-$25$50$75

$100$125$150$175$200

Potential Insured Losses ($B) Potential Economic Losses ($B)

Source: AIR Worldwide

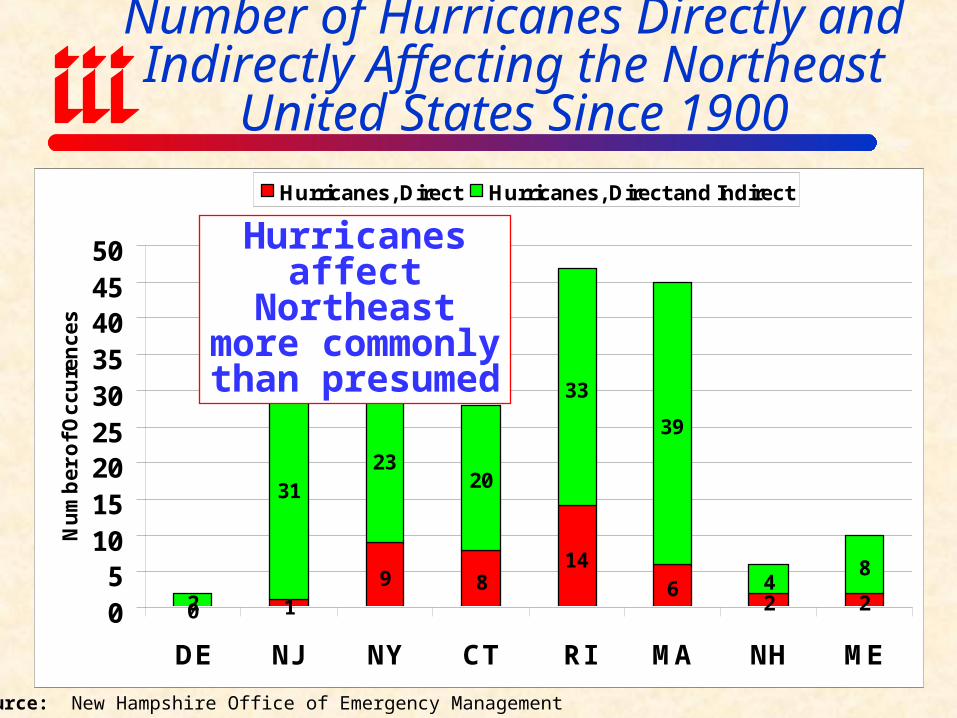

Number of Hurricanes Directly and Indirectly Affecting the Northeast

United States Since 1900

0 19 8

146

2 22

3123

20

33

39

48

05

101520253035404550

DE NJ NY CT RI MA NH ME

Nu

mb

er

of

Oc

cu

ren

ce

s

Hurricanes, Direct Hurricanes, Direct and Indirect

Source: New Hampshire Office of Emergency Management

Hurricanes affect Northeast more commonly than

presumed

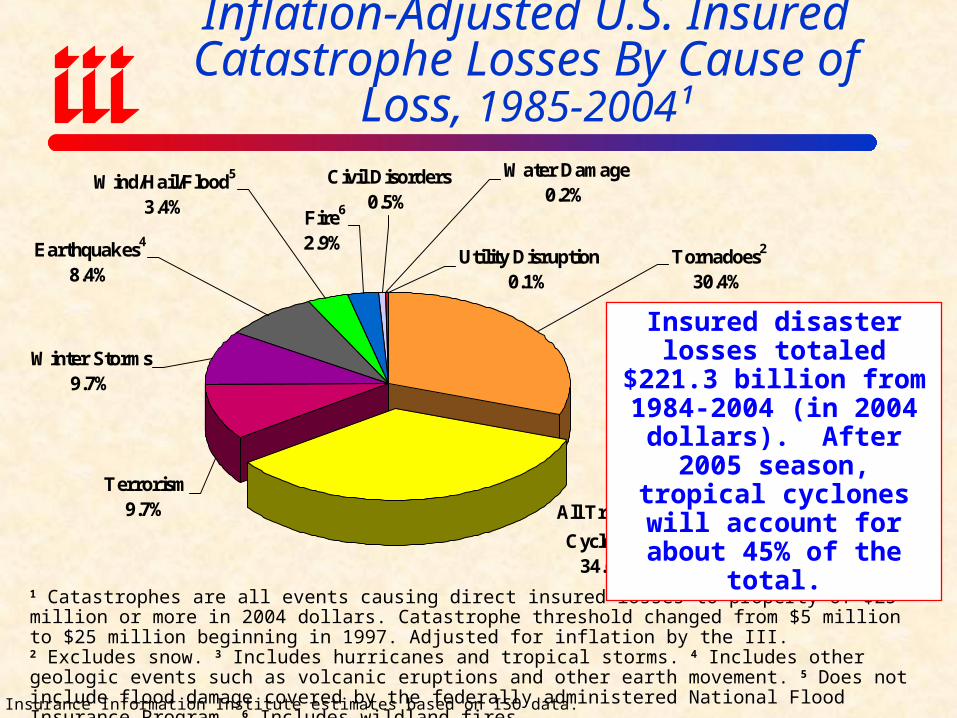

Inflation-Adjusted U.S. Insured Catastrophe Losses By Cause of Loss,

1985-2004¹

Utility Disruption0.1%

Terrorism9.7% All Tropical

Cyclones3

34.6%

Tornadoes2

30.4%

Water Damage0.2%

Civil Disorders0.5%

Fire6

2.9%

Wind/Hail/Flood5

3.4%

Earthquakes4

8.4%

Winter Storms9.7%

Source: Insurance Information Institute estimates based on ISO data.

1 Catastrophes are all events causing direct insured losses to property of $25 million or more in 2004 dollars. Catastrophe threshold changed from $5 million to $25 million beginning in 1997. Adjusted for inflation by the III.2 Excludes snow. 3 Includes hurricanes and tropical storms. 4 Includes other geologic events such as volcanic eruptions and other earth movement. 5 Does not include flood damage covered by the federally administered National Flood Insurance Program. 6 Includes wildland fires.

Insured disaster losses totaled $221.3 billion from

1984-2004 (in 2004 dollars). After 2005 season, tropical

cyclones will account for about 45% of the total.

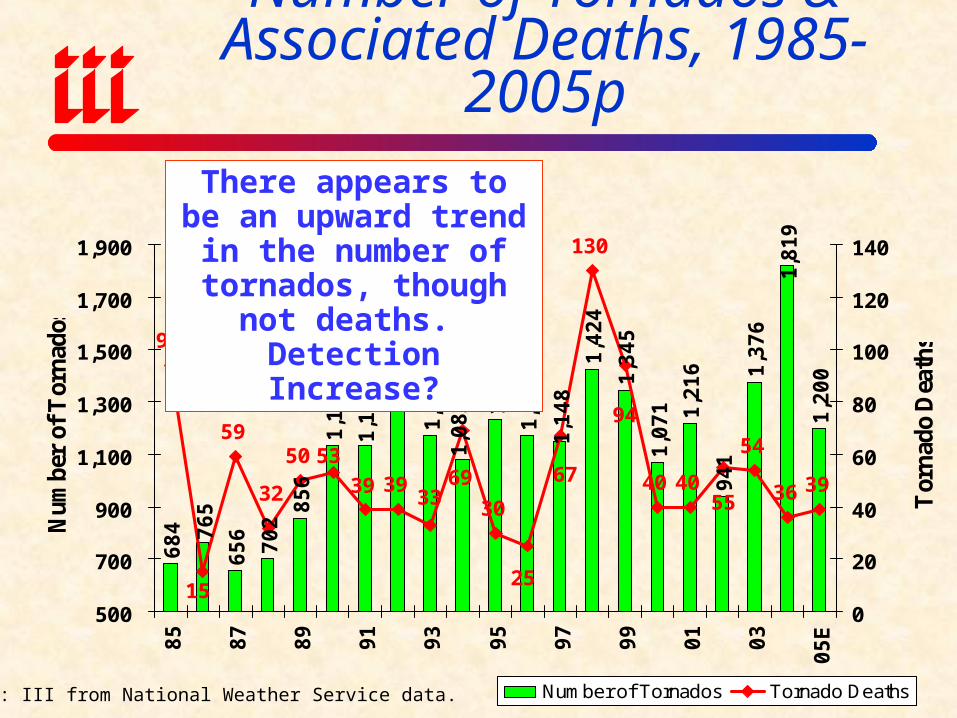

Number of Tornados & Associated Deaths, 1985-2005p

68

4

65

6

70

2

85

6

1,1

33 1,2

97

1,1

73

1,2

34

1,1

73

1,4

24

1,3

45

1,0

71 1,2

16

94

1

1,3

76

1,8

19

1,2

00

76

5

1,1

32

1,1

48

1,0

82

94

5950

3930

130

40 40

54

36 3953

15

69 67

94

5532 3933

25

500

700

900

1,100

1,300

1,500

1,700

1,900

85

87

89

91

93

95

97

99

01

03

05

E

Nu

mb

er o

f T

orn

ados

0

20

40

60

80

100

120

140

Tor

nad

o D

eath

s

Number of Tornados Tornado DeathsSource: III from National Weather Service data.

There appears to be an upward trend in the number of tornados, though not deaths. Detection Increase?

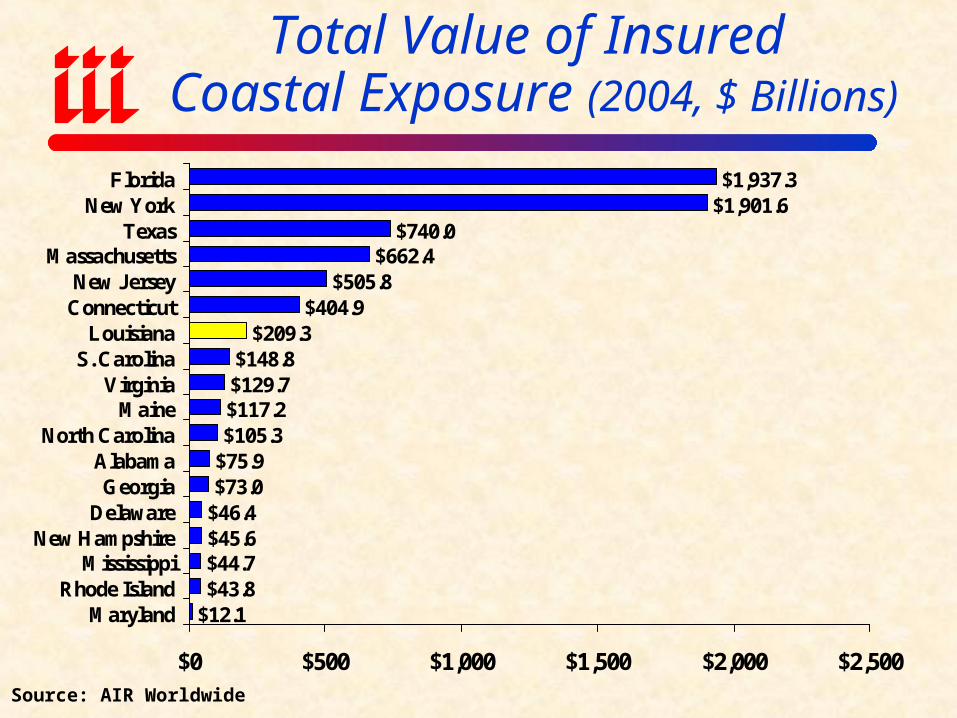

Total Value of Insured Coastal Exposure (2004, $ Billions)

$1,901.6$740.0

$662.4$505.8

$404.9$209.3

$148.8$129.7$117.2$105.3

$75.9$73.0

$46.4$45.6$44.7$43.8

$12.1

$1,937.3

$0 $500 $1,000 $1,500 $2,000 $2,500

FloridaNew York

TexasMassachusetts

New JerseyConnecticut

LouisianaS. Carolina

VirginiaMaine

North CarolinaAlabamaGeorgia

DelawareNew Hampshire

MississippiRhode Island

Maryland

Source: AIR Worldwide

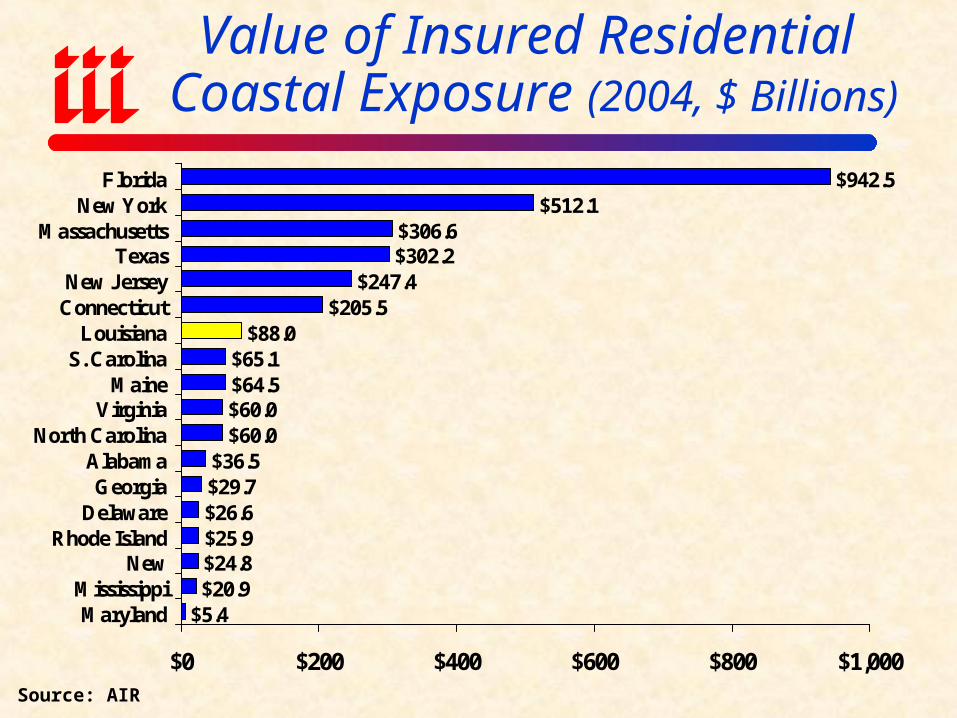

Value of Insured Residential Coastal Exposure (2004, $ Billions)

$512.1$306.6$302.2

$247.4$205.5

$88.0$65.1$64.5$60.0$60.0

$36.5$29.7$26.6$25.9$24.8$20.9

$5.4

$942.5

$0 $200 $400 $600 $800 $1,000

FloridaNew York

MassachusettsTexas

New JerseyConnecticut

LouisianaS. Carolina

MaineVirginia

North CarolinaAlabamaGeorgia

DelawareRhode Island

NewMississippiMaryland

Source: AIR

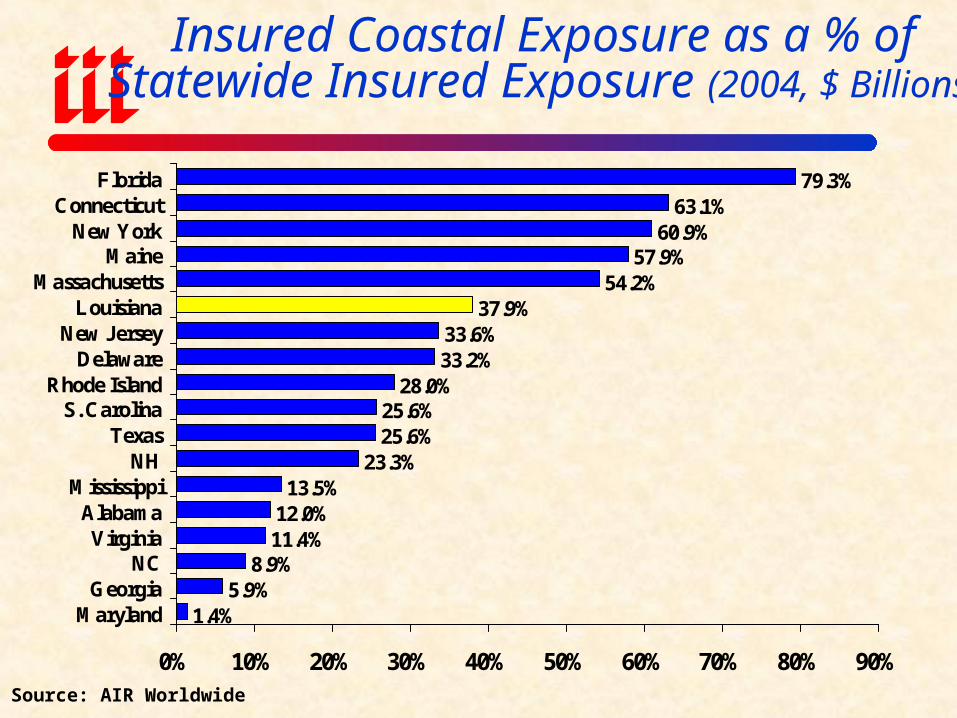

Insured Coastal Exposure as a % of Statewide Insured Exposure (2004, $ Billions)

63.1%60.9%

57.9%54.2%

37.9%33.6%33.2%

28.0%25.6%25.6%

23.3%13.5%

12.0%11.4%

8.9%5.9%

1.4%

79.3%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

FloridaConnecticut

New YorkMaine

MassachusettsLouisiana

New JerseyDelaware

Rhode IslandS. Carolina

TexasNH

MississippiAlabamaVirginia

NCGeorgia

Maryland

Source: AIR Worldwide

The 2006 Hurricane Season:

Preview to Disaster?

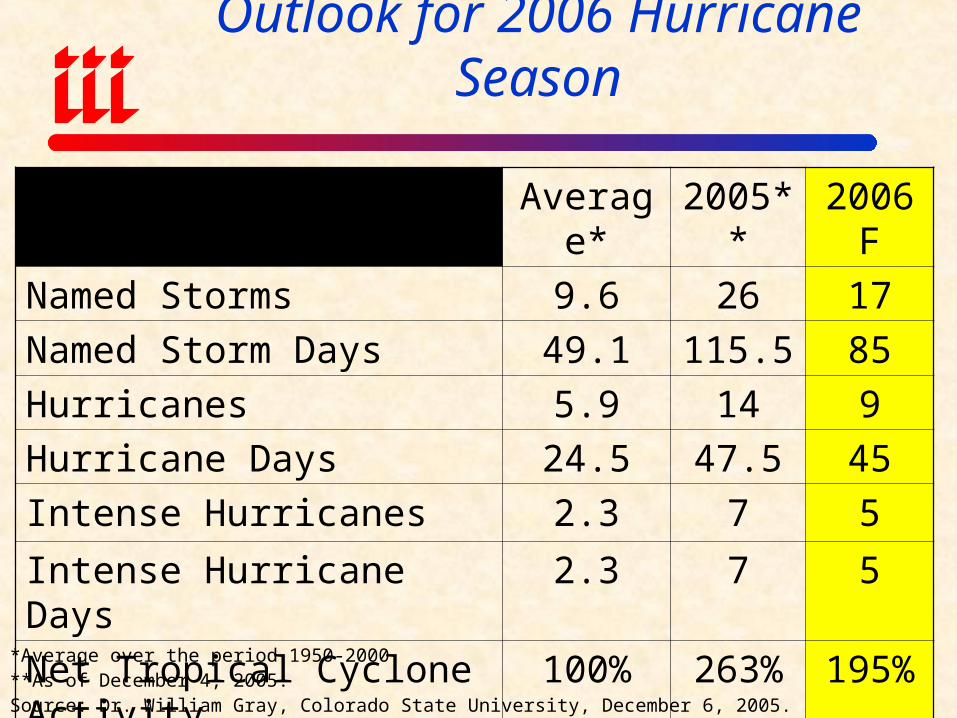

Outlook for 2006 Hurricane Season

Average* 2005** 2006F

Named Storms 9.6 26 17

Named Storm Days 49.1 115.5 85

Hurricanes 5.9 14 9

Hurricane Days 24.5 47.5 45

Intense Hurricanes 2.3 7 5

Intense Hurricane Days 2.3 7 5

Net Tropical Cyclone Activity 100% 263% 195%

*Average over the period 1950-2000.**As of December 4, 2005.Source: Dr. William Gray, Colorado State University, December 6, 2005.

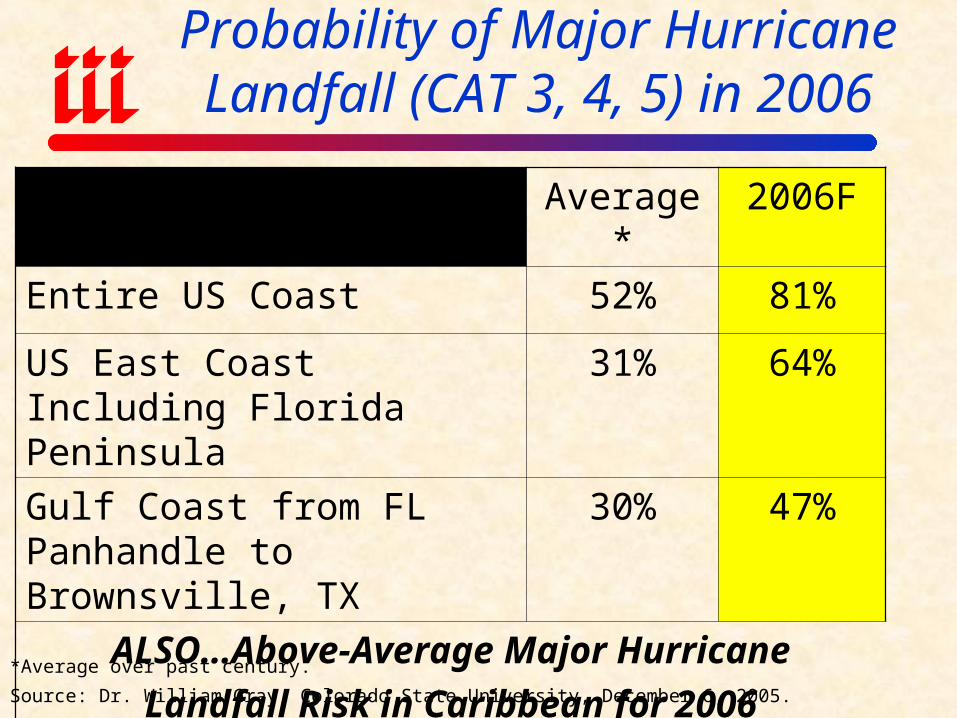

Probability of Major Hurricane Landfall (CAT 3, 4, 5) in 2006

Average* 2006F

Entire US Coast 52% 81%

US East Coast Including Florida Peninsula

31% 64%

Gulf Coast from FL Panhandle to Brownsville, TX

30% 47%

ALSO…Above-Average Major Hurricane

Landfall Risk in Caribbean for 2006

*Average over past century.

Source: Dr. William Gray, Colorado State University, December 6, 2005.

Hurricanes Katrina, Rita & Wilma:

Their Place in History

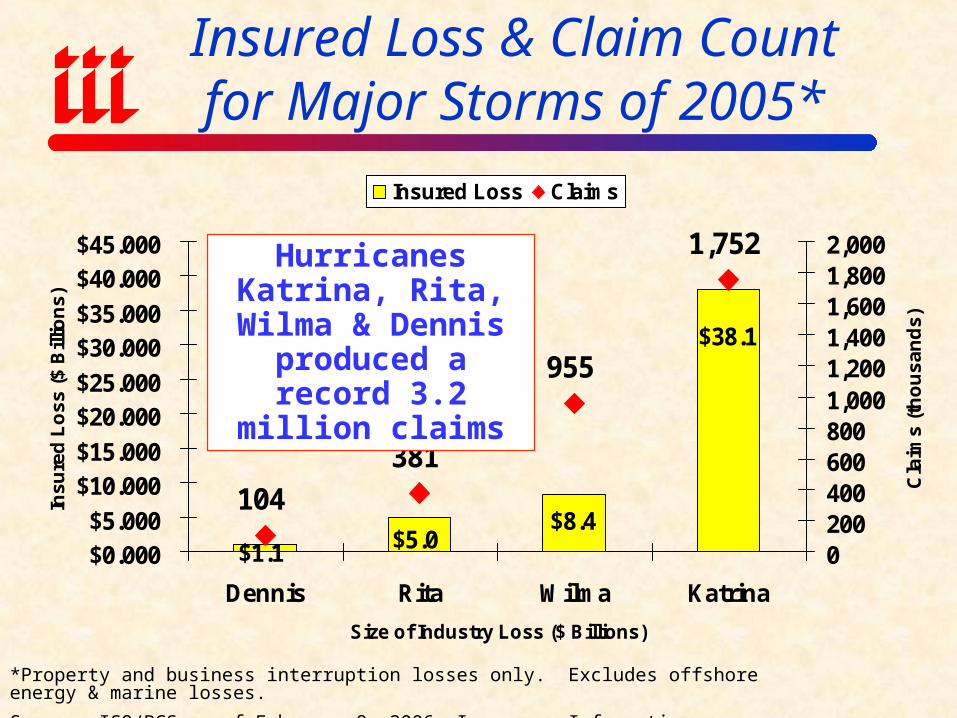

Insured Loss & Claim Count for Major Storms of 2005*

$1.1

$38.1

$8.4$5.0

104

381

955

1,752

$0.000$5.000

$10.000$15.000

$20.000$25.000

$30.000$35.000

$40.000$45.000

Dennis Rita Wilma Katrina

Size of Industry Loss ($ Billions)

Ins

ure

d L

os

s (

$ B

illio

ns

)

02004006008001,0001,2001,4001,6001,8002,000

Cla

ims

(th

ou

sa

nd

s)

Insured Loss Claims

*Property and business interruption losses only. Excludes offshore energy & marine losses.

Source: ISO/PCS as of February 8, 2006; Insurance Information Institute.

Hurricanes Katrina, Rita, Wilma & Dennis produced a record 3.2

million claims

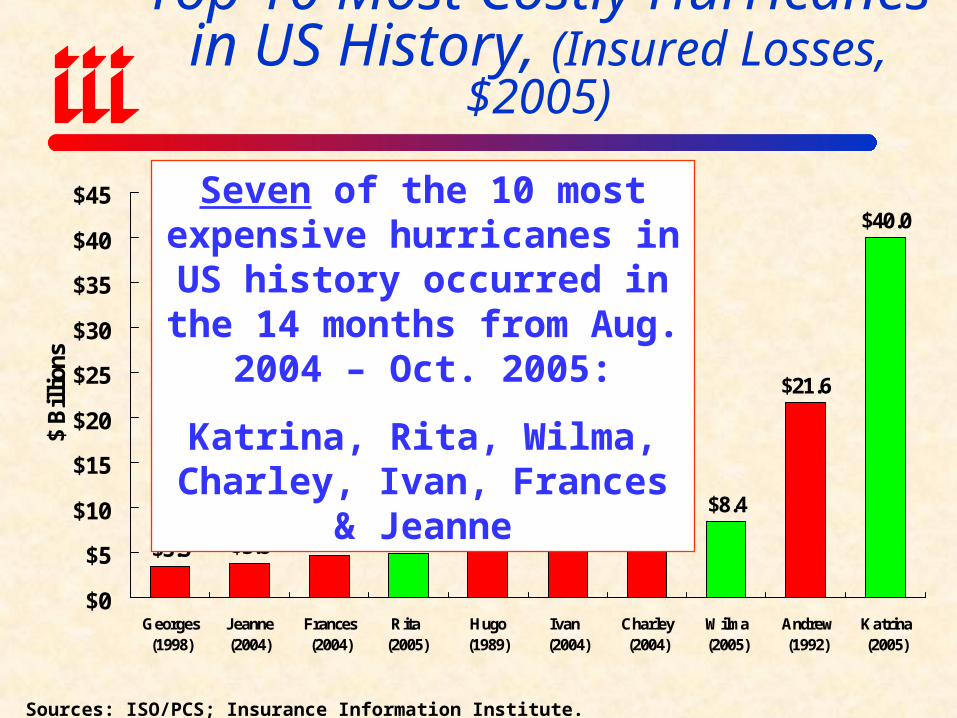

Top 10 Most Costly Hurricanes in US History, (Insured Losses, $2005)

$3.5 $3.8 $4.8 $5.0$6.6 $7.4 $7.7 $8.4

$21.6

$40.0

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

Georges(1998)

Jeanne(2004)

Frances(2004)

Rita (2005)

Hugo(1989)

Ivan (2004)

Charley(2004)

Wilma(2005)

Andrew(1992)

Katrina(2005)

$ B

illi

ons

Sources: ISO/PCS; Insurance Information Institute.

Seven of the 10 most expensive hurricanes in US history

occurred in the 14 months from Aug. 2004 – Oct. 2005:

Katrina, Rita, Wilma, Charley, Ivan, Frances & Jeanne

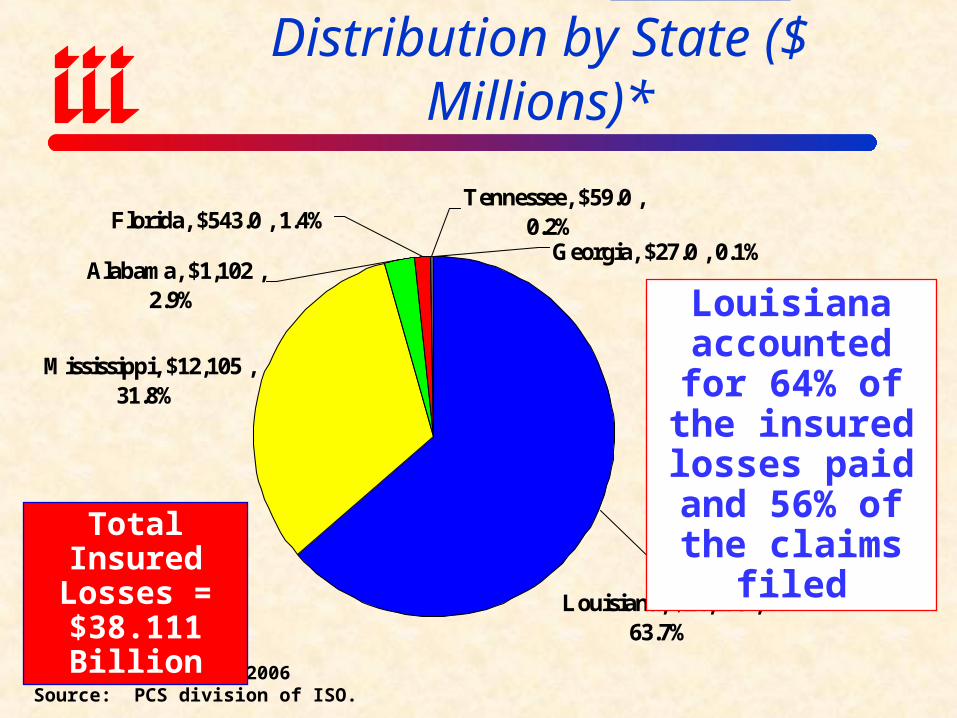

Hurricane Katrina Insured Loss Distribution by State ($ Millions)*

Mississippi, $12,105 , 31.8%

Louisiana, $24,275 , 63.7%

Tennessee, $59.0 , 0.2%Florida, $543.0 , 1.4%

Georgia, $27.0 , 0.1%Alabama, $1,102 ,

2.9%

*As of February 8, 2006Source: PCS division of ISO.

Louisiana accounted for

64% of the insured losses

paid and 56% of the claims filed

Total Insured Losses =

$38.111 Billion

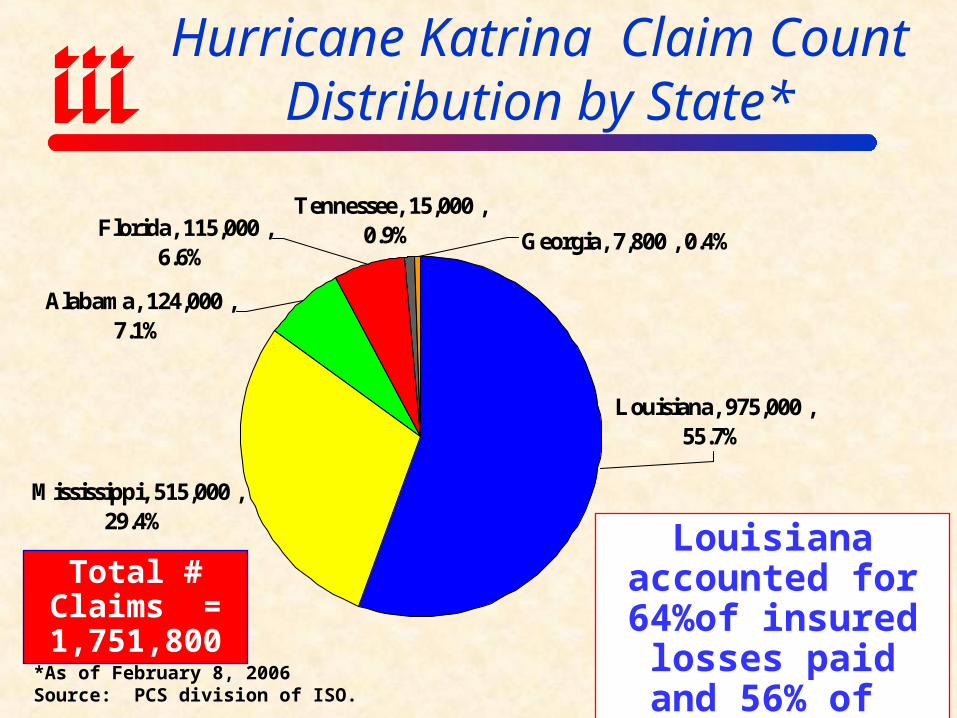

Hurricane Katrina Claim Count Distribution by State*

Mississippi, 515,000 , 29.4%

Tennessee, 15,000 , 0.9%

Louisiana, 975,000 , 55.7%

Florida, 115,000 , 6.6%

Georgia, 7,800 , 0.4%

Alabama, 124,000 , 7.1%

*As of February 8, 2006Source: PCS division of ISO.

Louisiana accounted for 64%of insured

losses paid and 56% of claims filed

Total # Claims = 1,751,800

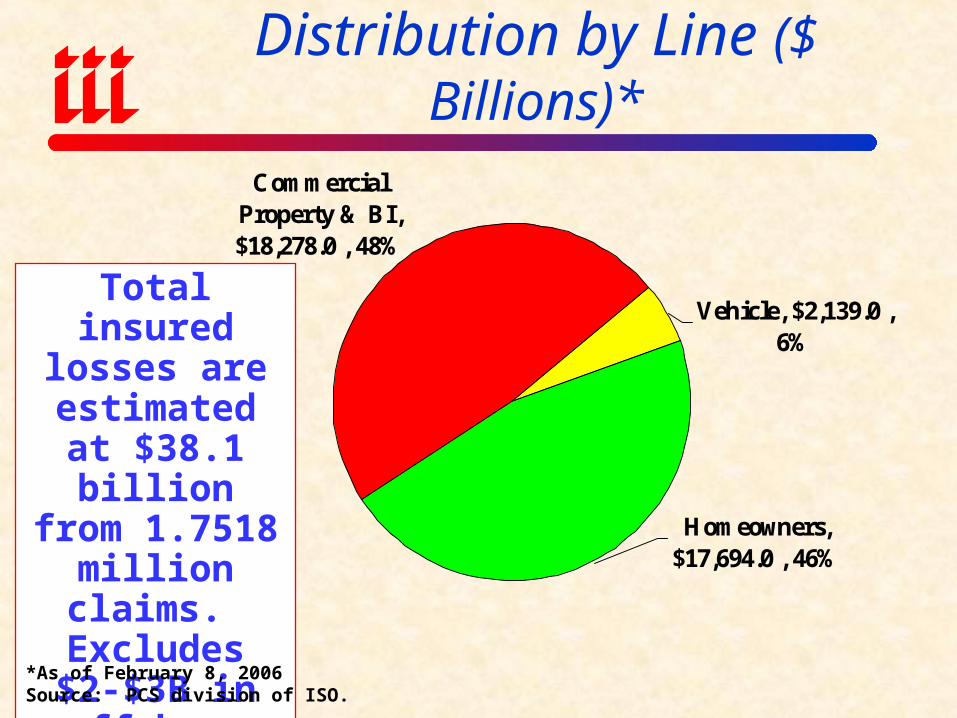

Hurricane Katrina Loss Distribution by Line ($ Billions)*

Homeowners, $17,694.0 , 46%

Commercial Property & BI, $18,278.0 , 48%

Vehicle, $2,139.0 , 6%

Total insured losses are

estimated at $38.1 billion from 1.7518

million claims. Excludes $2-

$3B in offshore energy losses

*As of February 8, 2006Source: PCS division of ISO.

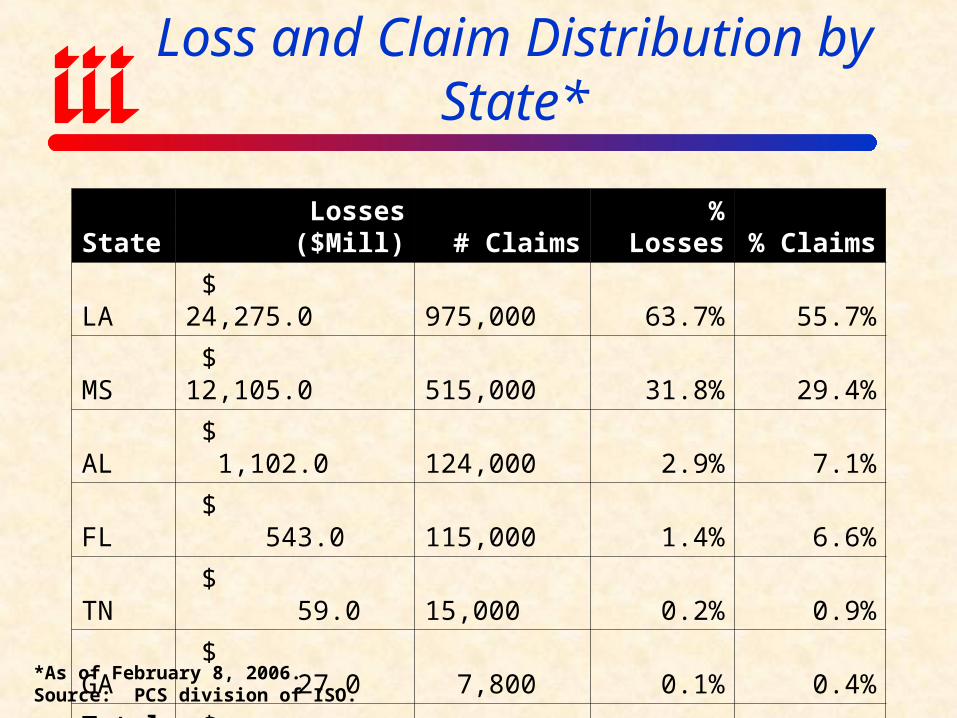

Hurricane Katrina Insured Loss and Claim Distribution by State*

State Losses ($Mill) # Claims % Losses % Claims

LA $ 24,275.0 975,000 63.7% 55.7%

MS $ 12,105.0 515,000 31.8% 29.4%

AL $ 1,102.0 124,000 2.9% 7.1%

FL $ 543.0 115,000 1.4% 6.6%

TN $ 59.0 15,000 0.2% 0.9%

GA $ 27.0 7,800 0.1% 0.4%

Totals $ 38,111.0 1,751,800 100.0% 100.0%

*As of February 8, 2006.Source: PCS division of ISO.

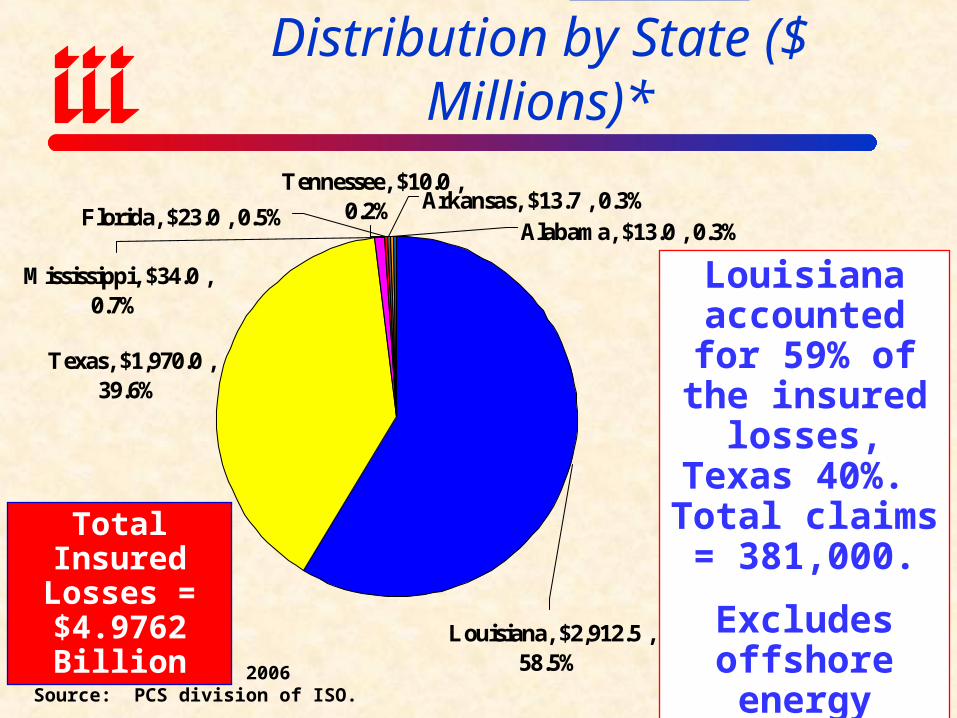

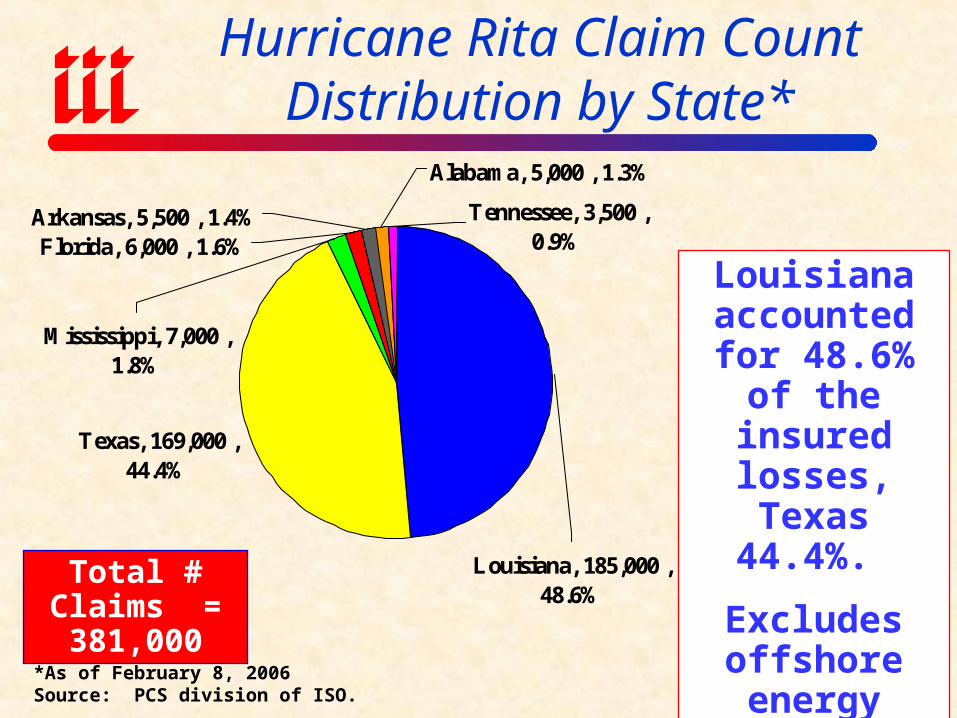

Hurricane Rita Insured Loss Distribution by State ($ Millions)*

Texas, $1,970.0 , 39.6%

Tennessee, $10.0 , 0.2%

Louisiana, $2,912.5 , 58.5%

Arkansas, $13.7 , 0.3%Florida, $23.0 , 0.5%

Alabama, $13.0 , 0.3%

Mississippi, $34.0 , 0.7%

*As of February 8, 2006Source: PCS division of ISO.

Louisiana accounted for

59% of the insured losses, Texas 40%.

Total claims = 381,000.

Excludes offshore energy losses of $2-3B

Total Insured Losses =

$4.9762 Billion

Hurricane Rita Claim Count Distribution by State*

Texas, 169,000 , 44.4%

Tennessee, 3,500 , 0.9%

Louisiana, 185,000 , 48.6%

Arkansas, 5,500 , 1.4%Florida, 6,000 , 1.6%

Alabama, 5,000 , 1.3%

Mississippi, 7,000 , 1.8%

*As of February 8, 2006Source: PCS division of ISO.

Louisiana accounted for 48.6% of the

insured losses, Texas 44.4%.

Excludes offshore energy losses of $2-3BTotal # Claims

= 381,000

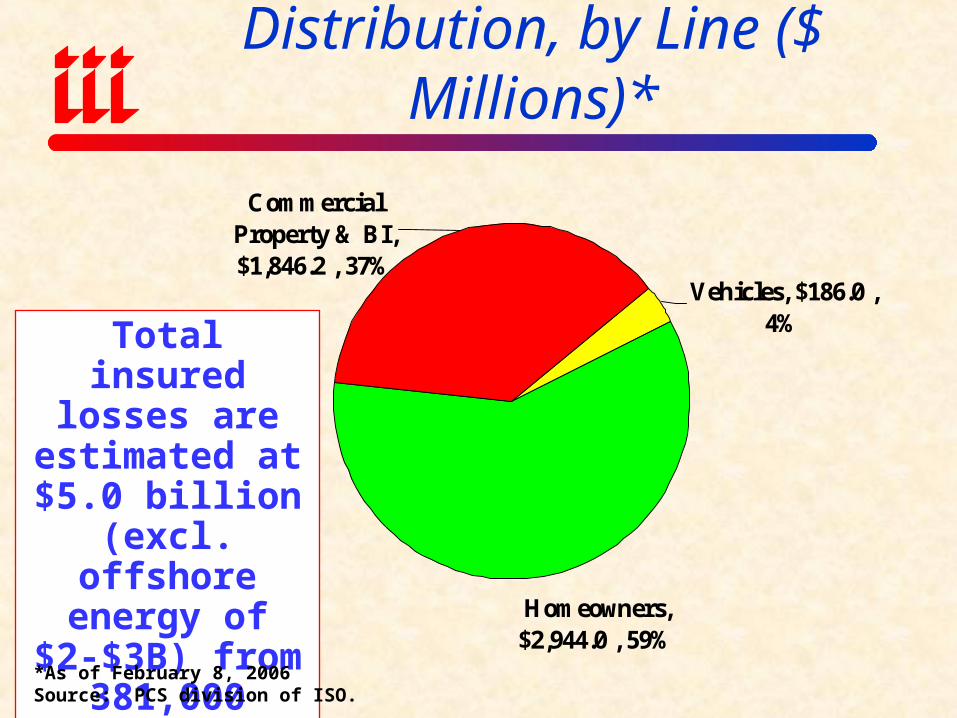

Hurricane Rita Loss Distribution, by Line ($ Millions)*

Homeowners, $2,944.0 , 59%

Commercial Property & BI, $1,846.2 , 37%

Vehicles, $186.0 , 4%Total insured

losses are estimated at $5.0

billion (excl. offshore energy of $2-$3B) from 381,000 claims.

*As of February 8, 2006Source: PCS division of ISO.

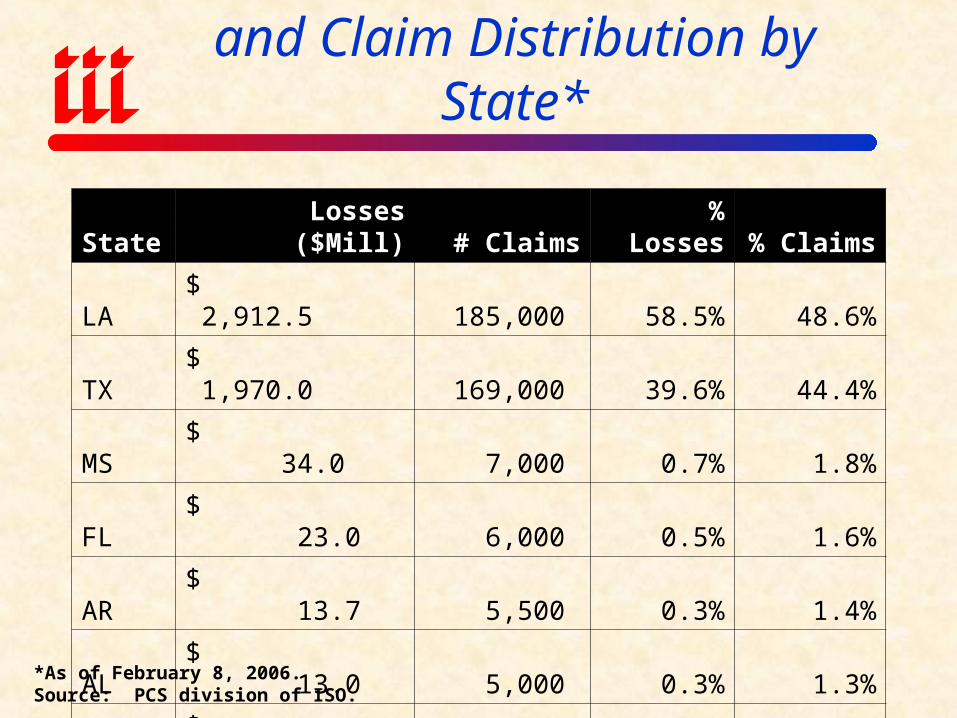

Hurricane Rita Insured Loss and Claim Distribution by State*

State Losses ($Mill) # Claims % Losses % Claims

LA $ 2,912.5 185,000 58.5% 48.6%

TX $ 1,970.0 169,000 39.6% 44.4%

MS $ 34.0 7,000 0.7% 1.8%

FL $ 23.0 6,000 0.5% 1.6%

AR $ 13.7 5,500 0.3% 1.4%

AL $ 13.0 5,000 0.3% 1.3%

TN $ 10.0 3,500 0.2% 0.9%

Totals $ 4,976.2 381,000 100.0% 100.0%

*As of February 8, 2006.Source: PCS division of ISO.

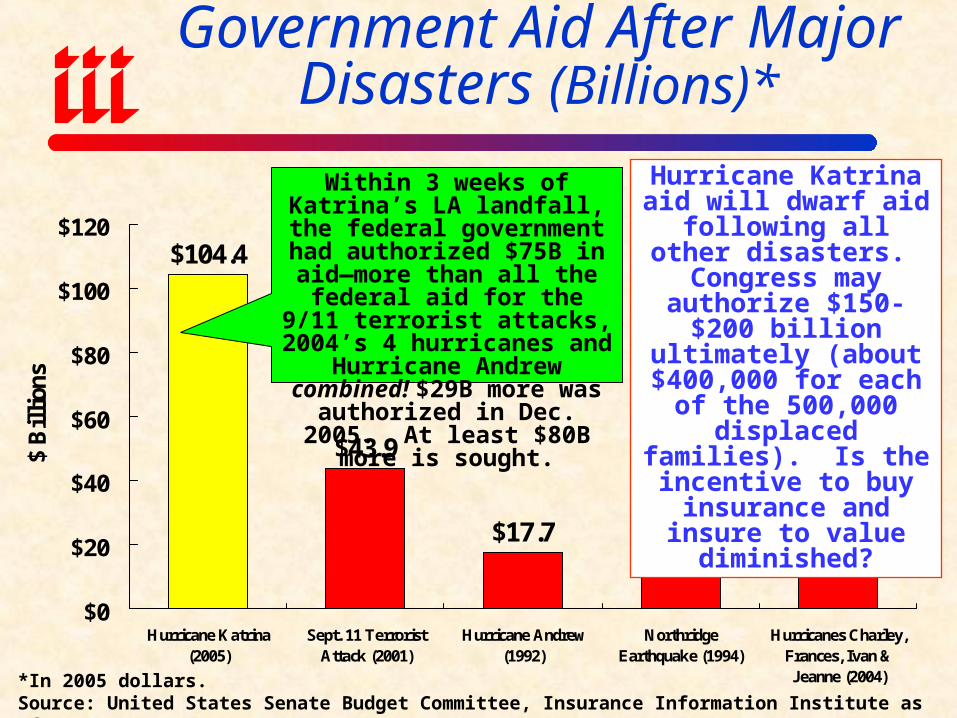

Government Aid After Major Disasters (Billions)*

$104.4

$43.9

$17.7 $15.5 $15.0

$0

$20

$40

$60

$80

$100

$120

Hurricane Katrina(2005)

Sept. 11 TerroristAttack (2001)

Hurricane Andrew(1992)

NorthridgeEarthquake (1994)

Hurricanes Charley,Frances, Ivan &Jeanne (2004)

$ B

illi

ons

*In 2005 dollars.Source: United States Senate Budget Committee, Insurance Information Institute as of 12/31/05.

Hurricane Katrina aid will dwarf aid following

all other disasters. Congress may authorize

$150-$200 billion ultimately (about

$400,000 for each of the 500,000 displaced

families). Is the incentive to buy insurance and

insure to value diminished?

Within 3 weeks of Katrina’s LA landfall, the federal government

had authorized $75B in aid—more than all the federal aid for the 9/11 terrorist attacks, 2004’s

4 hurricanes and Hurricane Andrew combined! $29B more

was authorized in Dec. 2005. At least $80B more is sought.

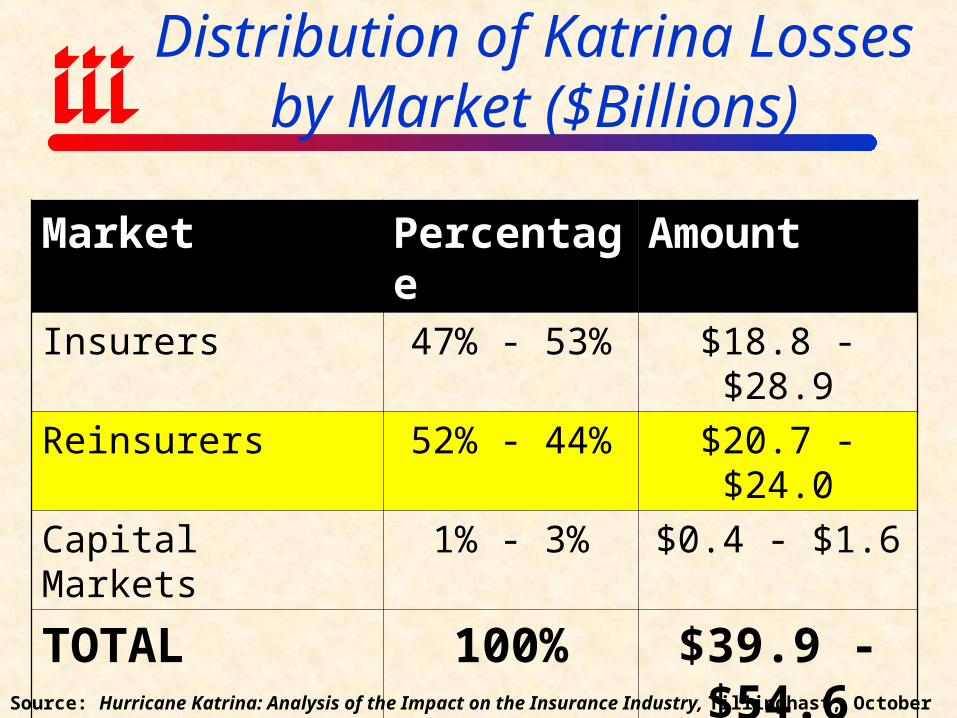

Distribution of Katrina Losses by Market ($Billions)

Market Percentage Amount

Insurers 47% - 53% $18.8 - $28.9

Reinsurers 52% - 44% $20.7 - $24.0

Capital Markets 1% - 3% $0.4 - $1.6

TOTAL 100% $39.9 - $54.6

Source: Hurricane Katrina: Analysis of the Impact on the Insurance Industry, Tillinghast, October 2005.

Overview of Plans for a National

Catastrophe Insurance Plan

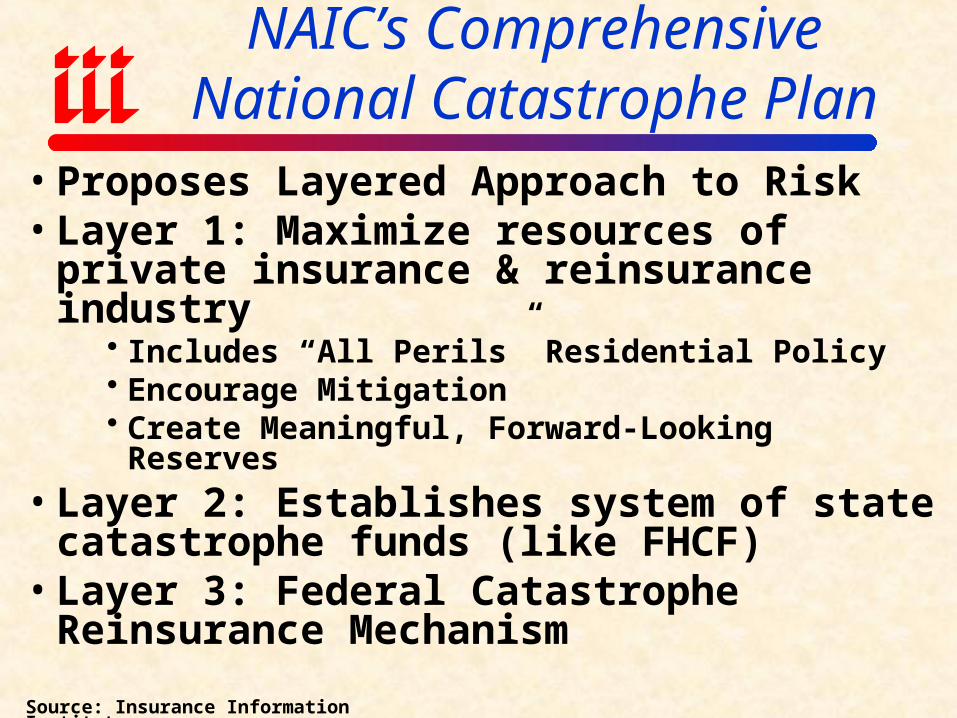

NAIC’s Comprehensive National Catastrophe Plan

• Proposes Layered Approach to Risk• Layer 1: Maximize resources of private

insurance & reinsurance industry Includes “All Perils” Residential Policy Encourage Mitigation Create Meaningful, Forward-Looking Reserves

• Layer 2: Establishes system of state catastrophe funds (like FHCF)

• Layer 3: Federal Catastrophe Reinsurance Mechanism

Source: Insurance Information Institute

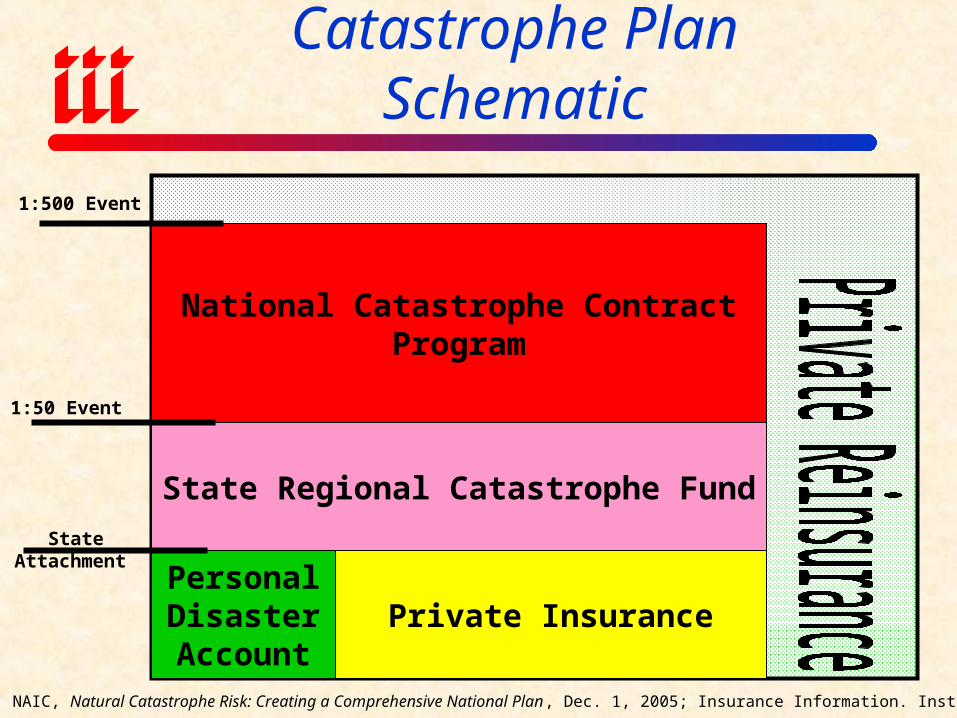

Comprehensive National Catastrophe Plan Schematic

Personal Disaster Account

Private Insurance

State Regional Catastrophe Fund

National Catastrophe Contract Program

Source: NAIC, Natural Catastrophe Risk: Creating a Comprehensive National Plan, Dec. 1, 2005; Insurance Information. Inst.

State Attachment

1:50 Event

1:500 Event

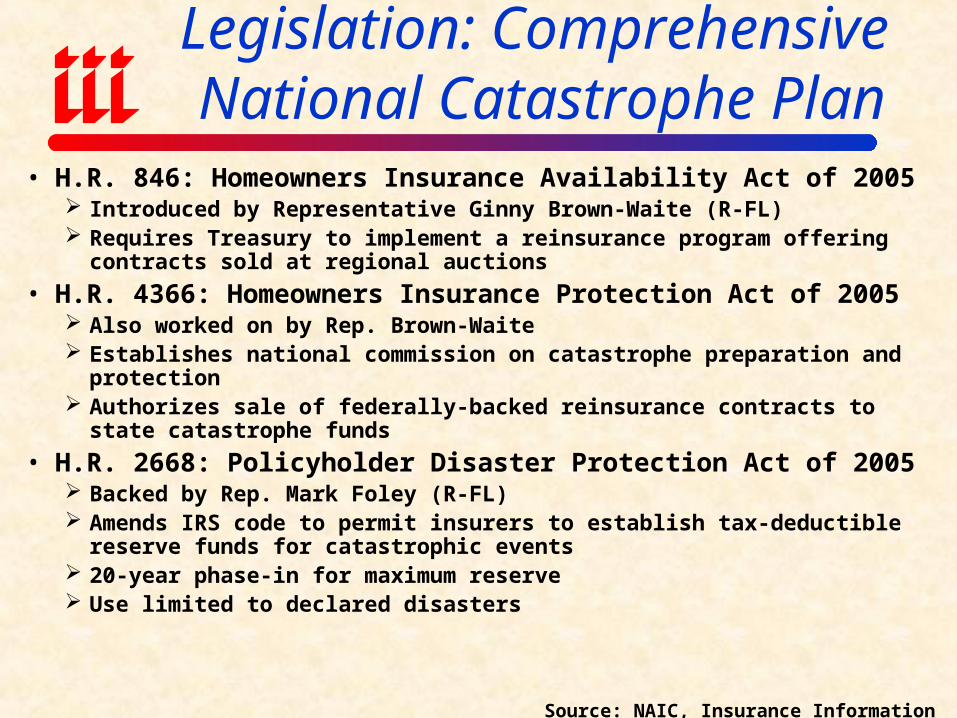

Legislation: Comprehensive National Catastrophe Plan

• H.R. 846: Homeowners Insurance Availability Act of 2005 Introduced by Representative Ginny Brown-Waite (R-FL) Requires Treasury to implement a reinsurance program offering contracts

sold at regional auctions

• H.R. 4366: Homeowners Insurance Protection Act of 2005 Also worked on by Rep. Brown-Waite Establishes national commission on catastrophe preparation and protection Authorizes sale of federally-backed reinsurance contracts to state catastrophe

funds

• H.R. 2668: Policyholder Disaster Protection Act of 2005 Backed by Rep. Mark Foley (R-FL) Amends IRS code to permit insurers to establish tax-deductible reserve funds

for catastrophic events 20-year phase-in for maximum reserve Use limited to declared disasters

Source: NAIC, Insurance Information Institute

Profit Pillar #2PRICING

Can Discipline be Maintained?

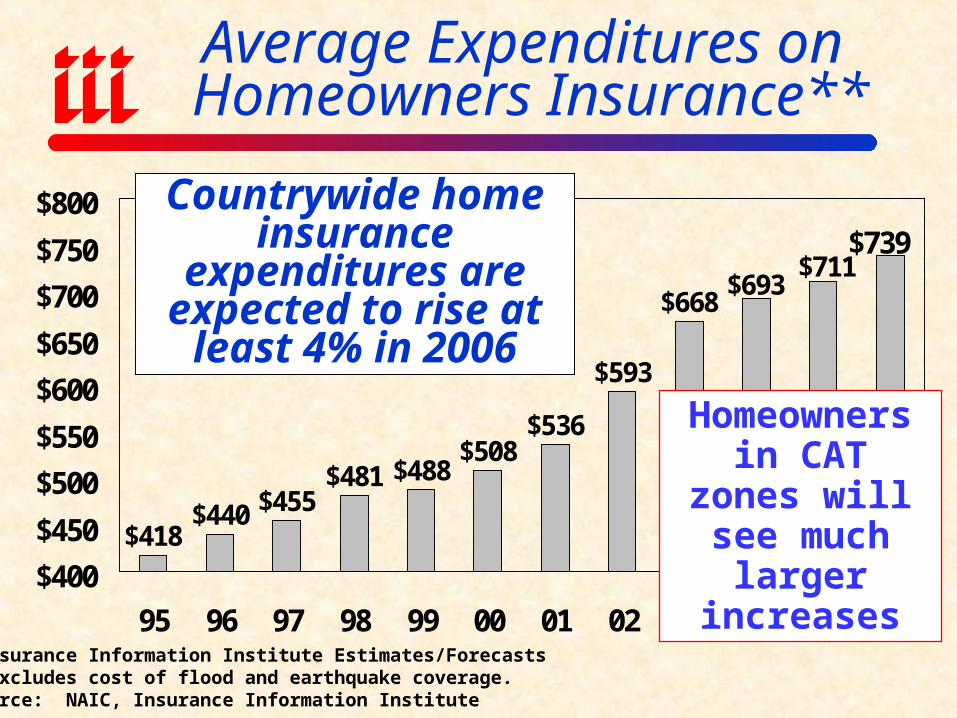

$418$440 $455

$481 $488$508

$536

$593

$668$693

$711$739

$400

$450

$500

$550

$600

$650

$700

$750

$800

95 96 97 98 99 00 01 02 03 04* 05* 06*

Average Expenditures on Homeowners Insurance**

*Insurance Information Institute Estimates/Forecasts**Excludes cost of flood and earthquake coverage.Source: NAIC, Insurance Information Institute

Countrywide home insurance expenditures are expected to rise at

least 4% in 2006

Homeowners in CAT zones will see much larger

increases

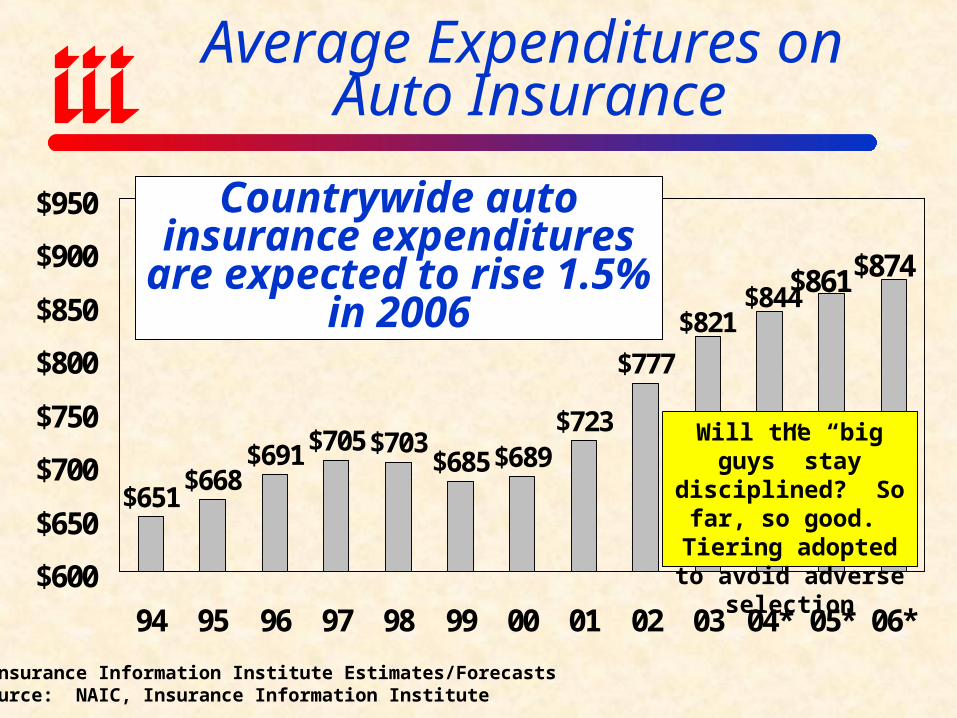

$651$668

$691 $705 $703$685 $689

$723

$777

$821

$874$844

$861

$600

$650

$700

$750

$800

$850

$900

$950

94 95 96 97 98 99 00 01 02 03 04* 05* 06*

Average Expenditures on Auto Insurance

*Insurance Information Institute Estimates/ForecastsSource: NAIC, Insurance Information Institute

Countrywide auto insurance expenditures are expected to

rise 1.5% in 2006

Will the “big guys” stay disciplined? So far, so good. Tiering

adopted to avoid adverse selection

Profit Pillar #3INVESTMENTS

Does Investment Performance Affect

Discipline?

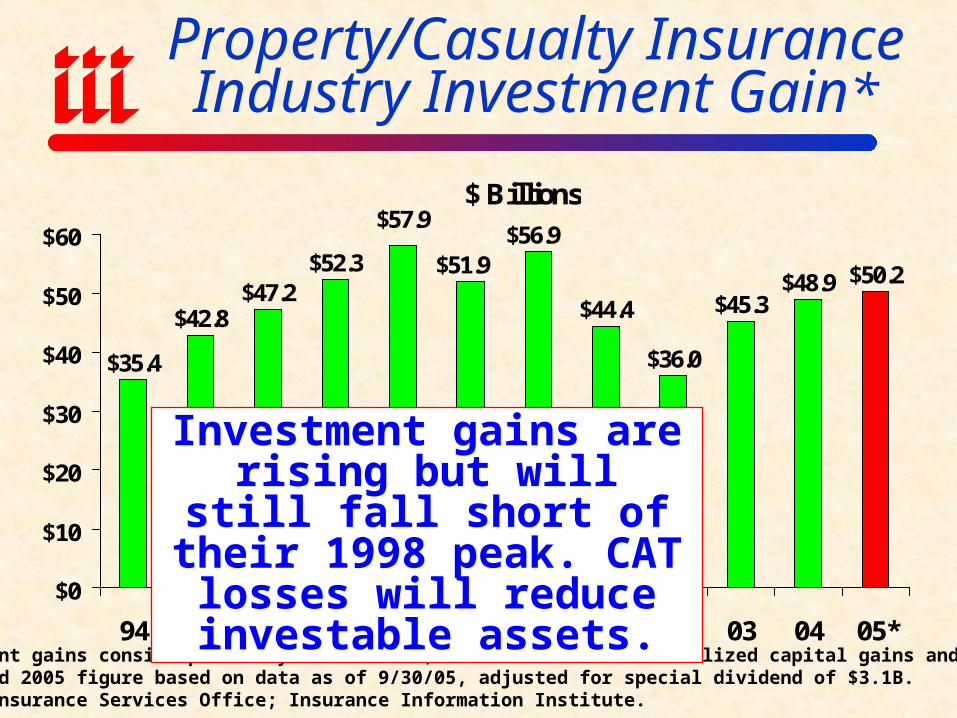

Property/Casualty Insurance Industry Investment Gain*

$ Billions

$35.4

$42.8$47.2

$52.3

$44.4

$36.0

$45.3$48.9 $50.2

$56.9$51.9

$57.9

$0

$10

$20

$30

$40

$50

$60

94 95 96 97 98 99 00 01 02 03 04 05**Investment gains consist primarily of interest, stock dividends and realized capital gains and losses.Annualized 2005 figure based on data as of 9/30/05, adjusted for special dividend of $3.1B.Source: Insurance Services Office; Insurance Information Institute.

Investment gains are rising but will still fall short of

their 1998 peak. CAT losses will reduce investable assets.

Profit Pillar #4EXPENSES

Will Expense Ratio Rise as Premium Growth Slows?

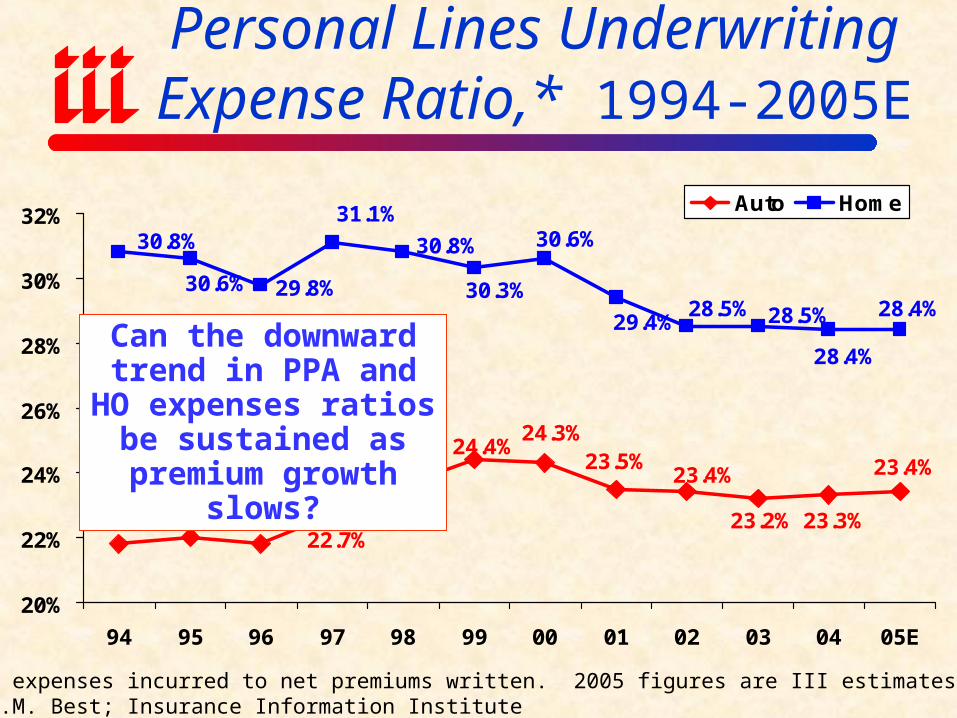

Personal Lines Underwriting Expense Ratio,* 1994-2005E

21.8% 22.0% 21.8%

23.5%

29.8%

24.3%24.4%

23.6%

23.4%

22.7%23.2% 23.3%

23.4%

28.4%

28.4%

28.5%28.5%

30.8%

31.1%30.8%

30.6% 30.3%

30.6%

29.4%

20%

22%

24%

26%

28%

30%

32%

94 95 96 97 98 99 00 01 02 03 04 05E

Auto Home

*Ratio of expenses incurred to net premiums written. 2005 figures are III estimates.Source: A.M. Best; Insurance Information Institute

Can the downward trend in PPA and HO expenses

ratios be sustained as premium growth slows?

Profit Pillar #5LEVERAGE

Can the Industry Efficiently Employ Its Increasing Capital?

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

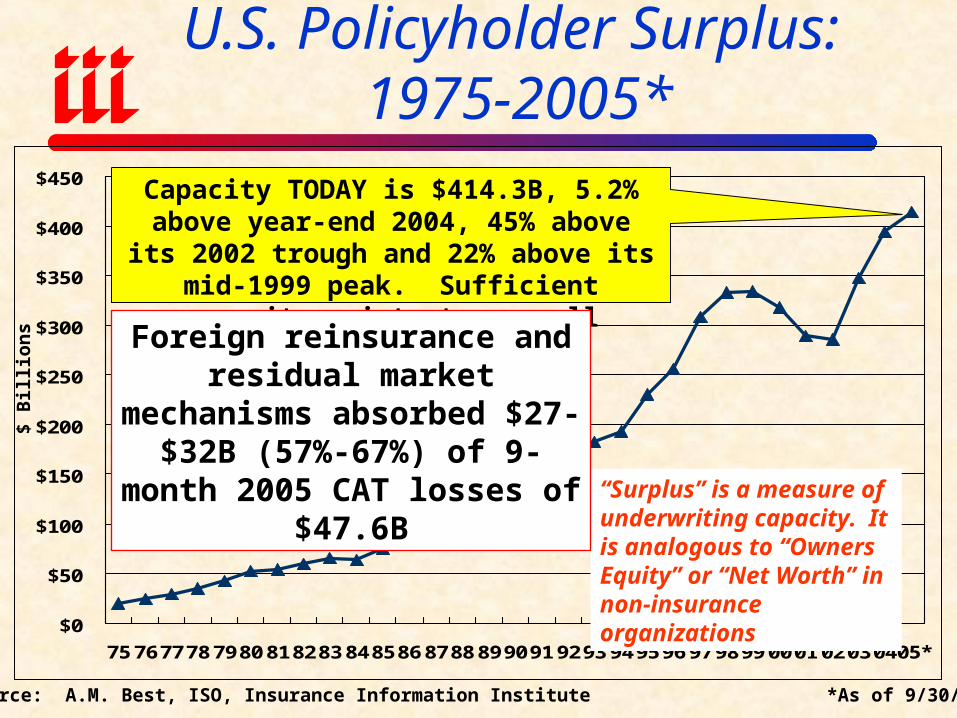

75 767778 7980 818283 848586 8788 899091 9293 949596 979899 0001 02030405*

U.S. Policyholder Surplus: 1975-2005*

Source: A.M. Best, ISO, Insurance Information Institute *As of 9/30/05.

$ B

illi

ons

“Surplus” is a measure of underwriting capacity. It is analogous to “Owners Equity” or “Net Worth” in non-insurance organizations

Capacity TODAY is $414.3B, 5.2% above year-end 2004, 45% above its 2002 trough and

22% above its mid-1999 peak. Sufficient capacity exists to pay all hurricane claims.

Foreign reinsurance and residual market mechanisms absorbed

$27-$32B (57%-67%) of 9-month 2005 CAT losses of $47.6B

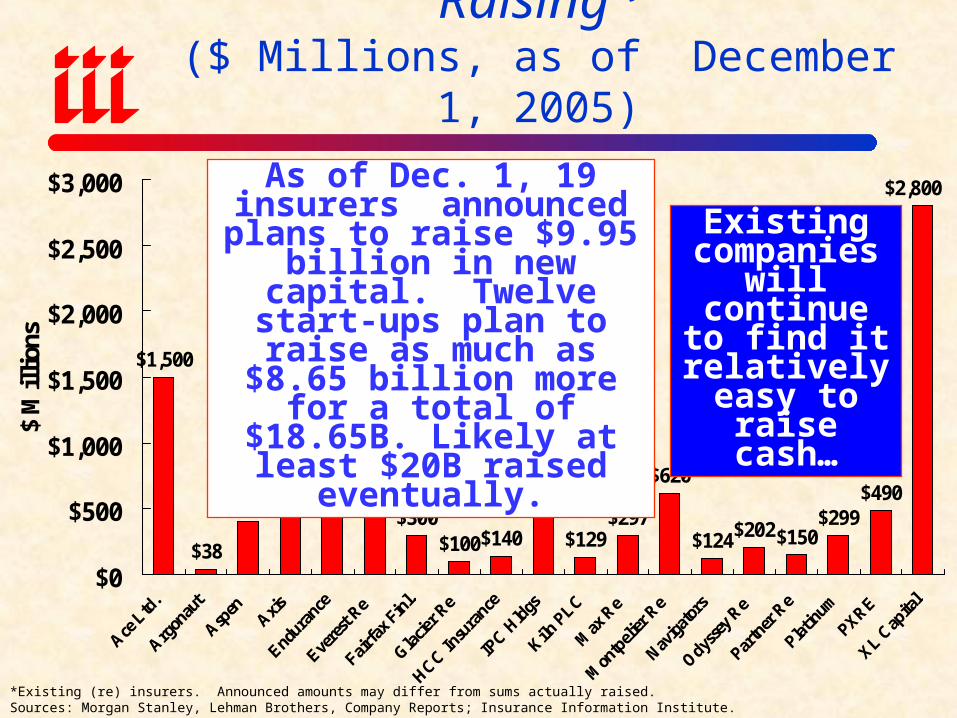

Announced Insurer Capital Raising*($ Millions, as of December 1, 2005)

$1,500

$38

$400$450$600

$710

$300$100$140

$600

$129$297

$620

$124$202$150$299

$490

$2,800

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$ M

illi

ons

*Existing (re) insurers. Announced amounts may differ from sums actually raised. Sources: Morgan Stanley, Lehman Brothers, Company Reports; Insurance Information Institute.

As of Dec. 1, 19 insurers announced plans to raise

$9.95 billion in new capital. Twelve start-ups plan to raise as much as $8.65

billion more for a total of $18.65B. Likely at least $20B

raised eventually.

Existing companies

will continue to find it

relatively easy to raise cash…

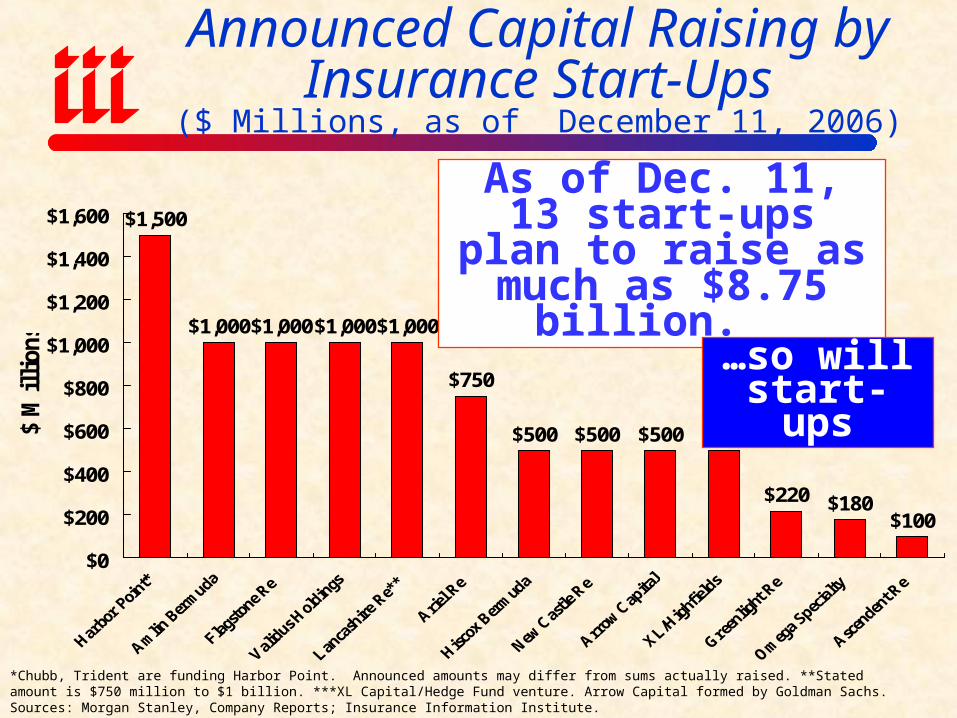

Announced Capital Raising by Insurance Start-Ups

($ Millions, as of December 11, 2006)

$1,500

$1,000$1,000$1,000$1,000

$750

$500 $500 $500 $500

$220 $180$100

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$ M

illi

ons

*Chubb, Trident are funding Harbor Point. Announced amounts may differ from sums actually raised. **Stated amount is $750 million to $1 billion. ***XL Capital/Hedge Fund venture. Arrow Capital formed by Goldman Sachs.Sources: Morgan Stanley, Company Reports; Insurance Information Institute.

As of Dec. 11, 13 start-ups plan to raise as

much as $8.75 billion.

…so will start-ups

Profit Pillar #6P/C OPERATING ENVIRONMENT

Have Things Changed for the Better?

TORT SYSTEM

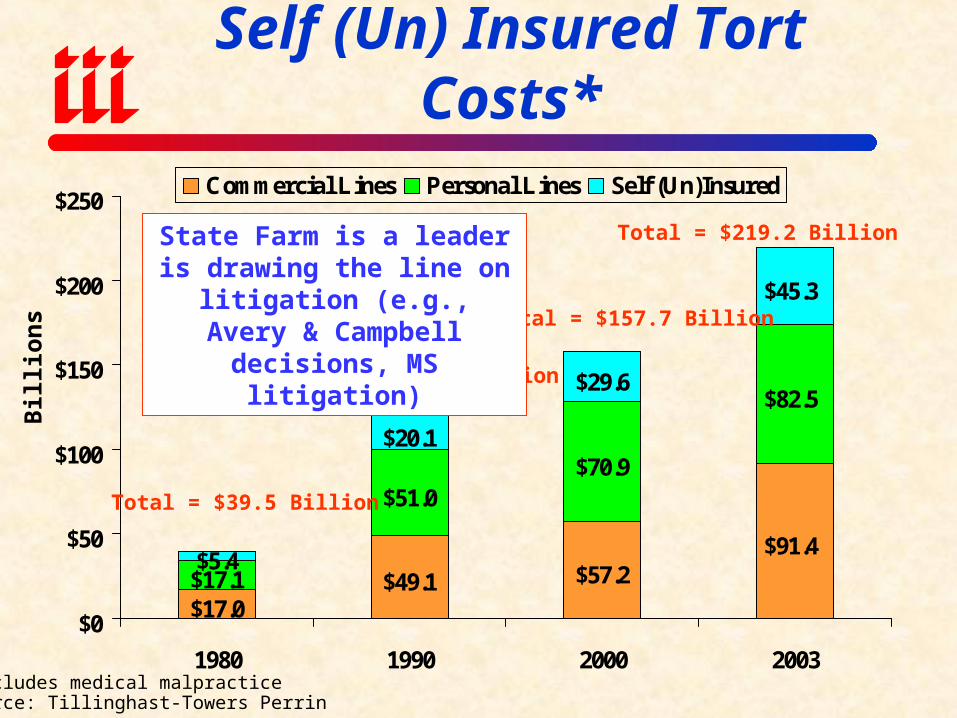

Personal, Commercial & Self (Un) Insured Tort Costs*

$17.0$49.1 $57.2

$91.4

$17.1

$51.0$70.9

$82.5

$5.4

$20.1

$29.6

$45.3

$0

$50

$100

$150

$200

$250

1980 1990 2000 2003

Commercial Lines Personal Lines Self (Un)Insured

Bil

lion

s

Total = $39.5 Billion

*Excludes medical malpracticeSource: Tillinghast-Towers Perrin

Total = $120.2 Billion

Total = $157.7 Billion

Total = $219.2 BillionState Farm is a leader is drawing the line on litigation

(e.g., Avery & Campbell decisions, MS litigation)

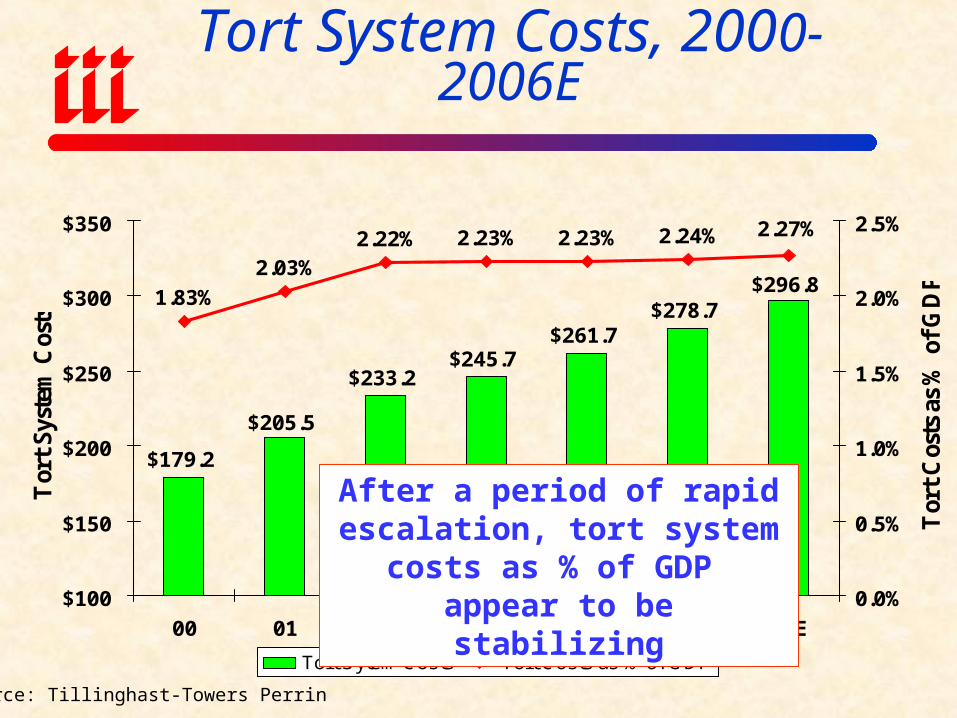

Tort System Costs, 2000-2006E

$179.2

$233.2$245.7

$261.7$278.7

$296.8

$205.5

1.83%

2.03%2.22% 2.23% 2.24% 2.27%2.23%

$100

$150

$200

$250

$300

$350

00 01 02 03 04E 05E 06E

Tor

t S

yste

m C

osts

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

Tor

t C

osts

as

% o

f G

DP

Tort Sytem Costs Tort Costs as % of GDP

Source: Tillinghast-Towers Perrin

After a period of rapid escalation, tort system costs as % of GDP appear to be stabilizing

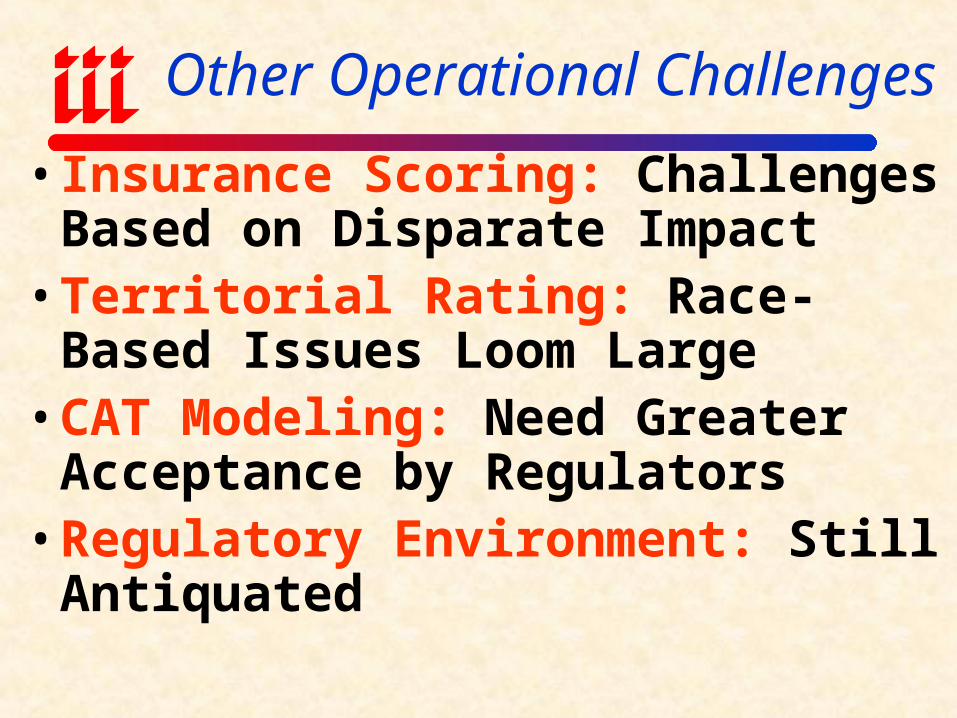

Other Operational Challenges

• Insurance Scoring: Challenges Based on Disparate Impact

• Territorial Rating: Race-Based Issues Loom Large

• CAT Modeling: Need Greater Acceptance by Regulators

• Regulatory Environment: Still Antiquated

AUTO & HOME:

A SUCCESSFUL SHIFT TO THE UNDERWRITING

CULTURE?

Private Passenger Auto

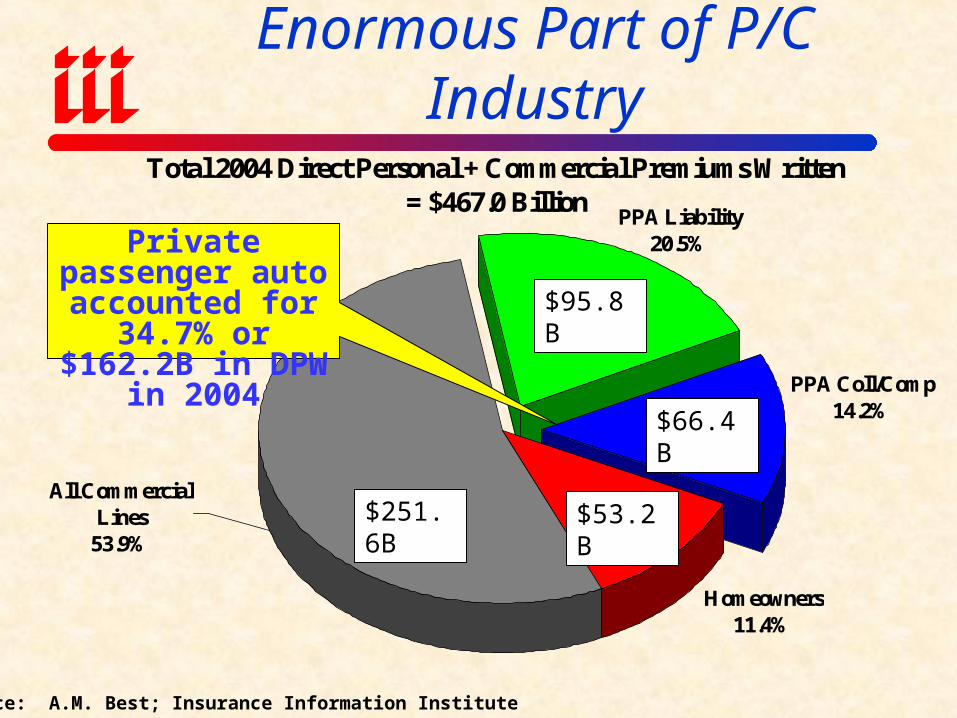

Private Passenger Auto is Enormous Part of P/C Industry

Total 2004 Direct Personal + Commercial Premiums Written = $467.0 Billion

All Commercial Lines

53.9%

PPA Coll/Comp14.2%

Homeowners11.4%

PPA Liability20.5%

Source: A.M. Best; Insurance Information Institute

Private passenger auto accounted for 34.7% or $162.2B in DPW in 2004

$251.6B $53.2B

$95.8B

$66.4B

Auto Insurance:Direct Premiums Written

$61.3 $64.7 $67.8 $70.0 $72.3 $71.6 $70.7 $70.6 $75.9 $84.0 $91.7

$34.4 $36.0 $38.2 $40.6 $43.8 $47.3 $49.9 $51.6$56.2

$61.2$64.9

$66.4

$95.8

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

93 94 95 96 97 98 99 00 01 02 03 04

PP Auto Liability PP Auto Phys Damage

Bil

lion

s

$95.7B

Source: A.M. Best; Insurance Information Institute

$100.7B+5.2%

$106.0B+5.3%

$110.5B+4.3%

$116.1B+5.0%

$118.9B+2.4%

$120.6B

+1.4%

$122.2B

+1.3%

$132.1B+8.1%

$145.1B+9.8%

$162.2B+11.9%

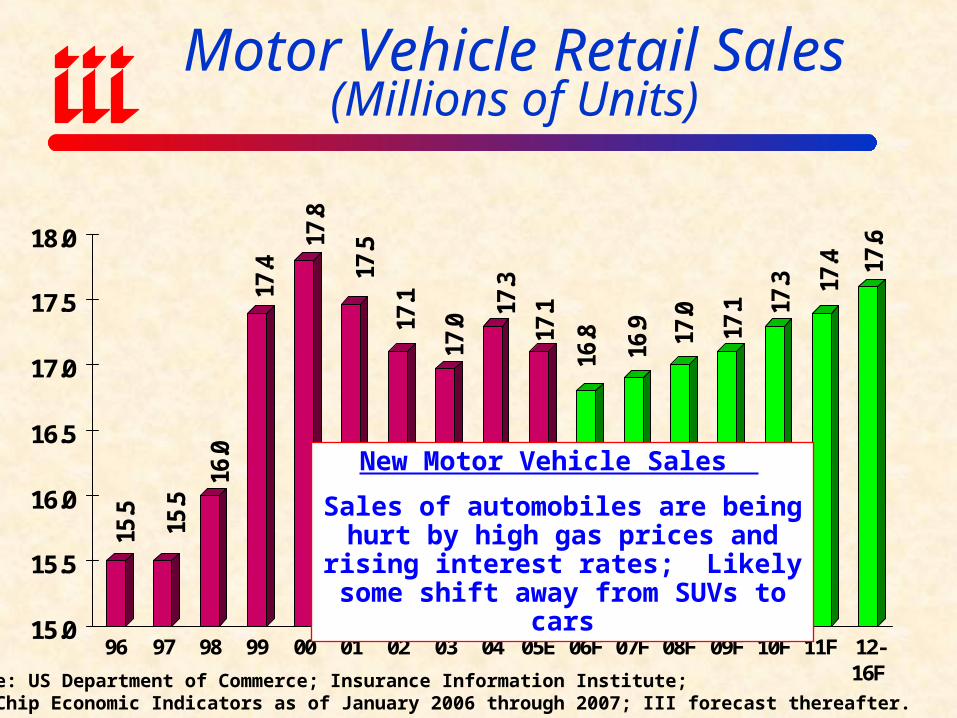

Motor Vehicle Retail Sales (Millions of Units)

15.5

15.5

16.0

17.4

17.8

17.5

17.1

17.0

17.3

17.1

16.8

16.9 17

.0

17.1 17

.3 17.4 17

.6

15.0

15.5

16.0

16.5

17.0

17.5

18.0

96 97 98 99 00 01 02 03 04 05E 06F 07F 08F 09F 10F 11F 12-16F

Source: US Department of Commerce; Insurance Information Institute;Blue Chip Economic Indicators as of January 2006 through 2007; III forecast thereafter.

New Motor Vehicle Sales

Sales of automobiles are being hurt by high gas prices and rising interest rates;

Likely some shift away from SUVs to cars

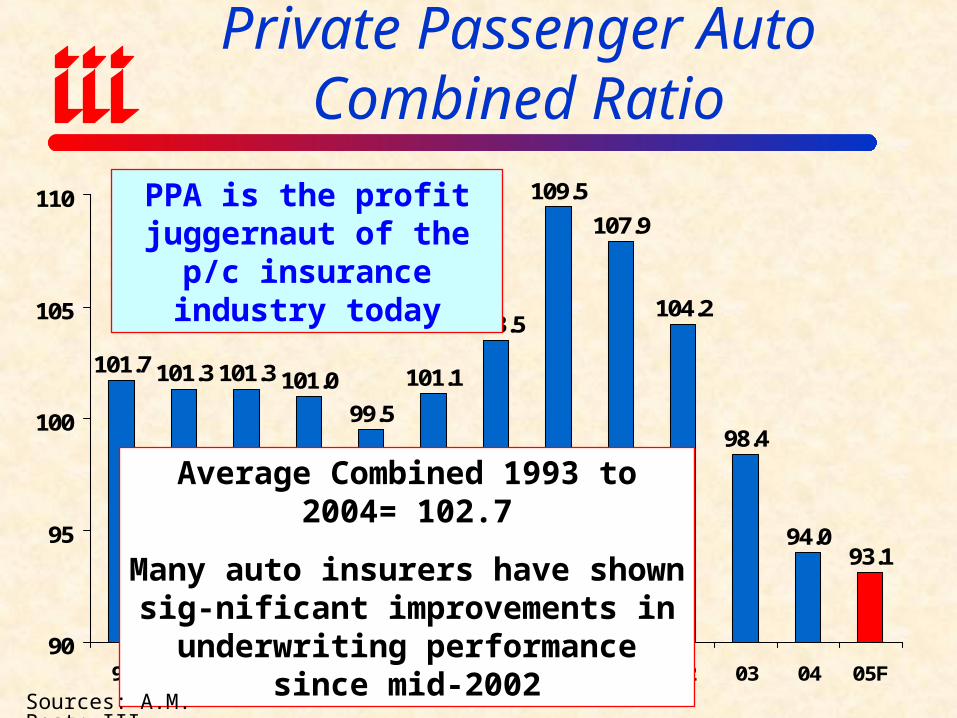

101.7 101.3 101.3 101.0

99.5

101.1

103.5

109.5

107.9

104.2

98.4

94.093.1

90

95

100

105

110

93 94 95 96 97 98 99 00 01 02 03 04 05F

Private Passenger Auto Combined Ratio

Average Combined 1993 to 2004= 102.7

Many auto insurers have shown sig-nificant improvements in underwriting

performance since mid-2002

Sources: A.M. Best; III

PPA is the profit juggernaut of the p/c

insurance industry today

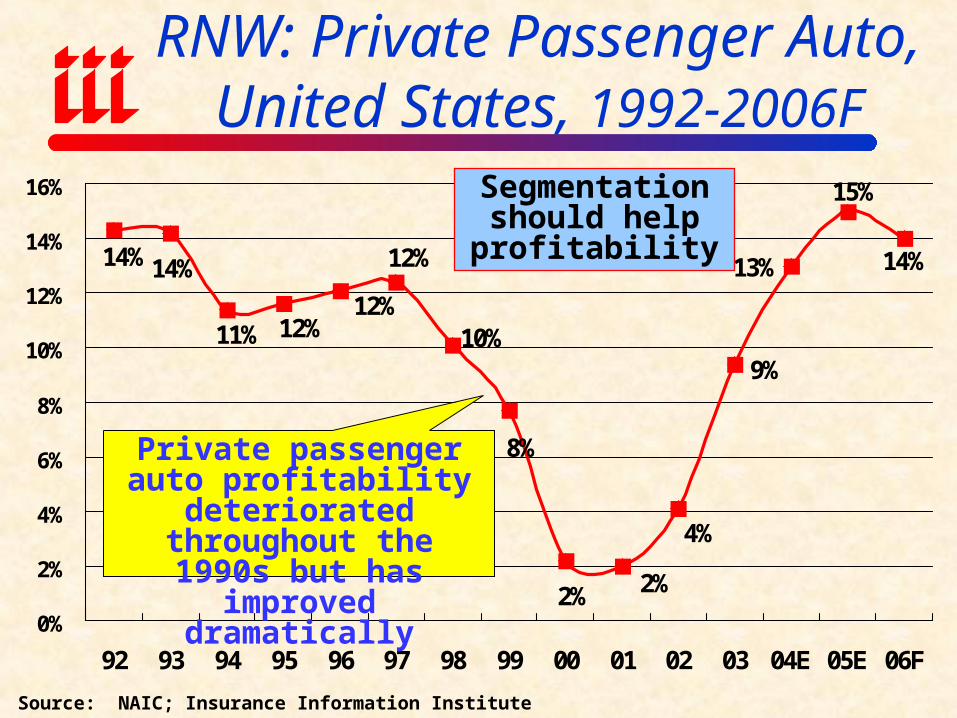

9%

14%13%

15%

12%14%14%

11% 12%12%

10%

8%

2% 2%

4%

0%

2%

4%

6%

8%

10%

12%

14%

16%

92 93 94 95 96 97 98 99 00 01 02 03 04E 05E 06F

RNW: Private Passenger Auto, United States, 1992-2006F

Source: NAIC; Insurance Information Institute

Private passenger auto profitability deteriorated throughout the 1990s but

has improved dramatically

Segmentation should help profitability

50%

60%

70%

80%

90%

100%

110%

99:Q

1

99:Q

2

99:Q

3

99:Q

4

00:Q

1

00:Q

2

00:Q

3

00:Q

4

01:Q

1

01:Q

2

01:Q

3

01:Q

4

02:Q

1

02:Q

2

02:Q

3

02:Q

4

03:Q

1

03:Q

2

03:Q

3

03:Q

4

04:Q

1

04:Q

2

04:Q

3

04:Q

4

05:Q

1

05:Q

2

05:Q

3

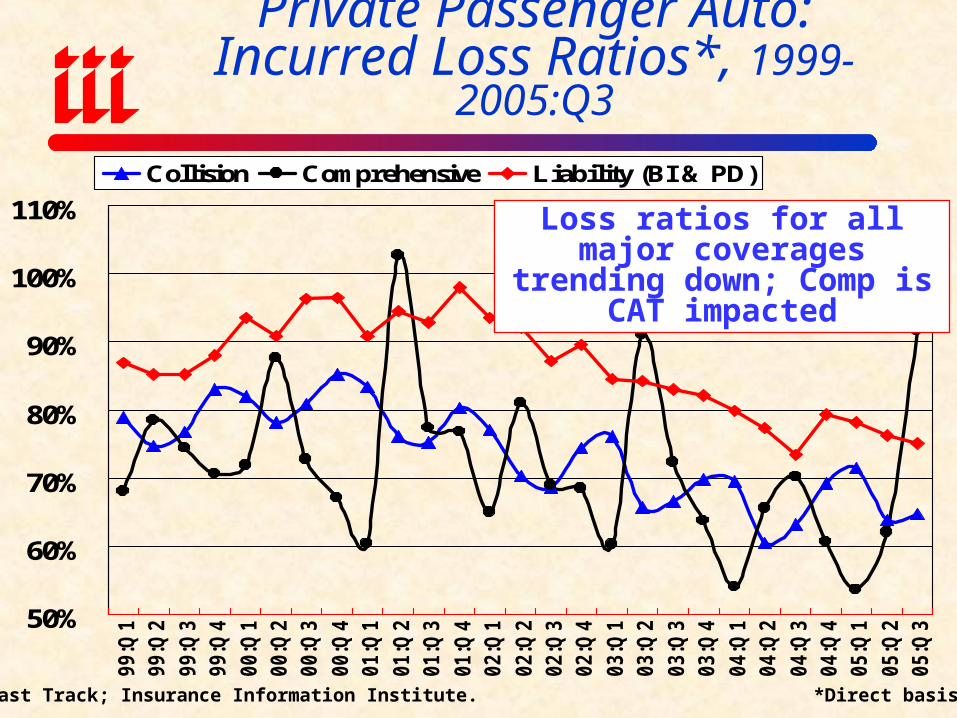

Collision Comprehensive Liability (BI & PD)

Source: ISO Fast Track; Insurance Information Institute. *Direct basis

Private Passenger Auto:Incurred Loss Ratios*, 1999-2005:Q3

Loss ratios for all major coverages trending down; Comp is CAT impacted

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

00

:Q1

00

:Q3

01

:Q1

01

:Q3

02

:Q1

02

:Q3

03

:Q1

03

:Q3

04

:Q1

04

:Q3

05

:Q1

05

:Q3

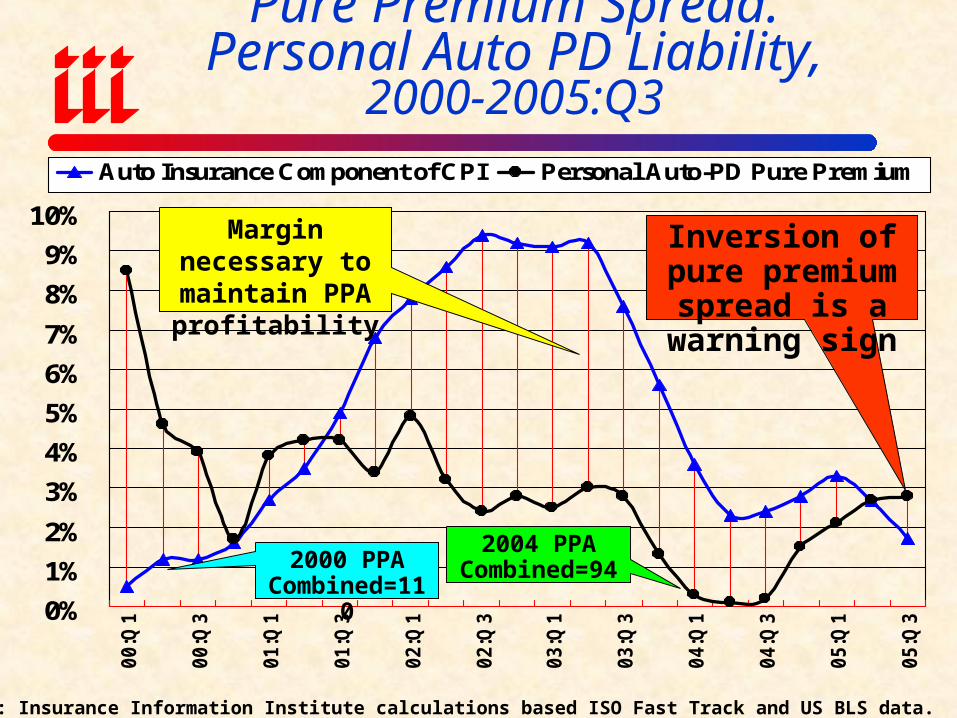

Auto Insurance Component of CPI Personal Auto-PD Pure Premium

Source: Insurance Information Institute calculations based ISO Fast Track and US BLS data.

Pure Premium Spread: Personal Auto PD Liability, 2000-2005:Q3

Margin necessary to maintain PPA

profitability

2000 PPA Combined=110

2004 PPA Combined=94

Inversion of pure premium spread is a warning sign

-2.2%

-5.3%

-4.0%-3.4%

-0.9%

-2.6%

-5.3%

3.0%3.6% 3.9%

3.4% 3.4%

-0.3%

4.7%

-6%

-4%

-2%

0%

2%

4%

6%

99 00 01 02 03 04 05*

Frequency Severity

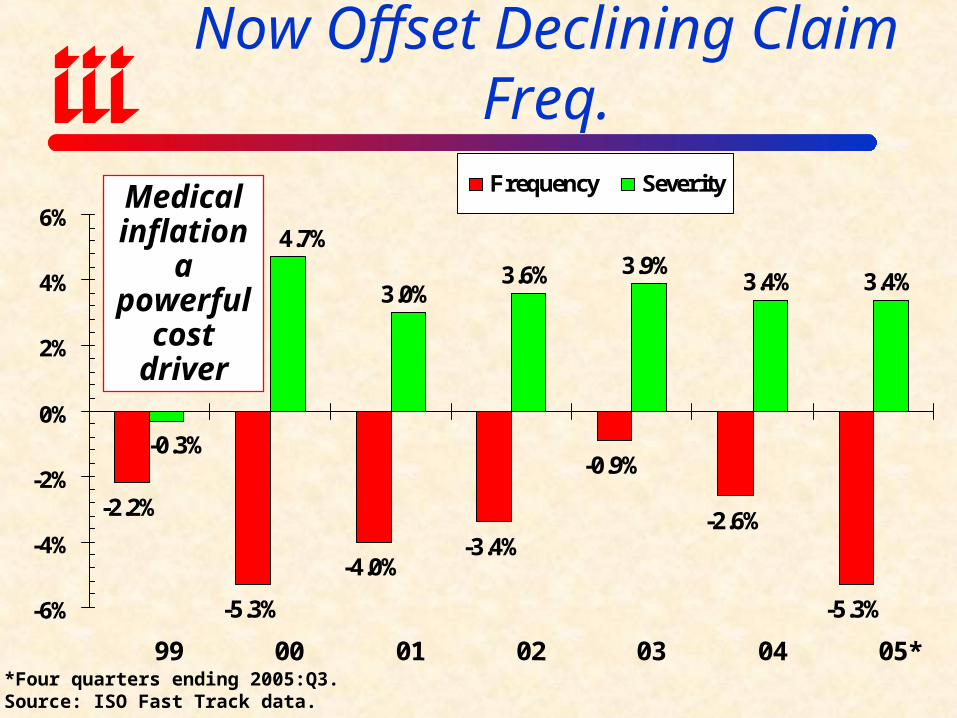

Bodily Injury: Severity Trends Now Offset Declining Claim Freq.

*Four quarters ending 2005:Q3.Source: ISO Fast Track data.

Medical inflation a powerful

cost driver

0.8%

-1.5%

0.3%

-1.8%-2.6% -2.4%

-1.6%

3.9%3.3%

2.4%

0.5%

2.3%

4.3%

6.2%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

99 00 01 02 03 04 05*

Frequency Severity

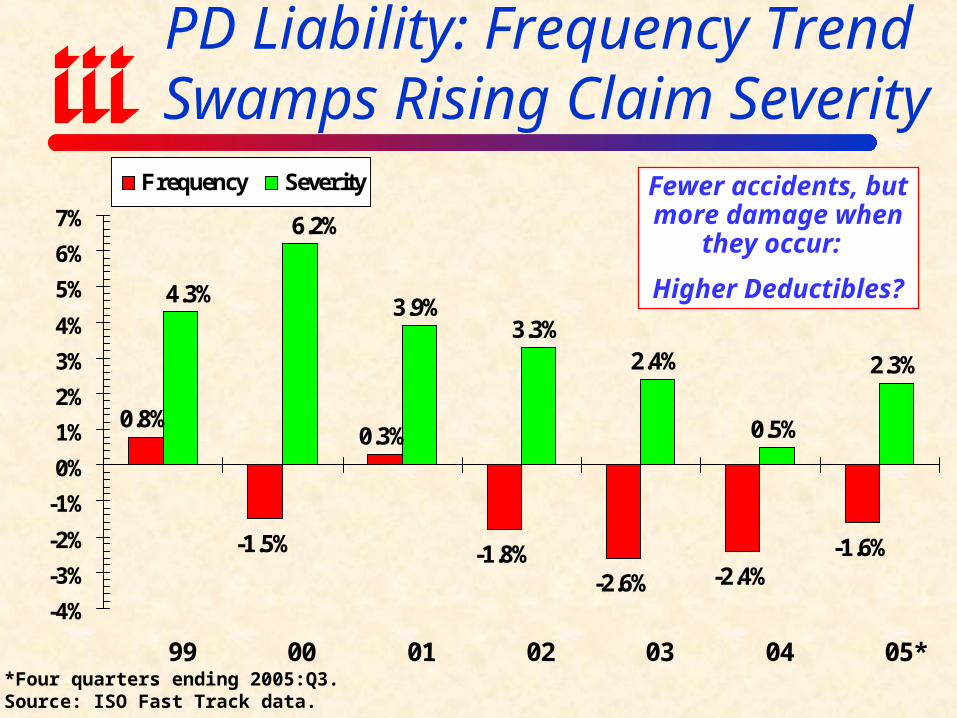

PD Liability: Frequency Trend Swamps Rising Claim Severity

Fewer accidents, but more damage when

they occur:

Higher Deductibles?

*Four quarters ending 2005:Q3.Source: ISO Fast Track data.

-1.6%

1.1%

-1.1%

0.0%

-0.6%

-7.2%-5.9%

3.2%

6.5%

-3.9%

0.5%

4.5%6.3%

16.1%

-10%

-5%

0%

5%

10%

15%

20%

99 00 01 02 03 04 05*

Frequency Severity

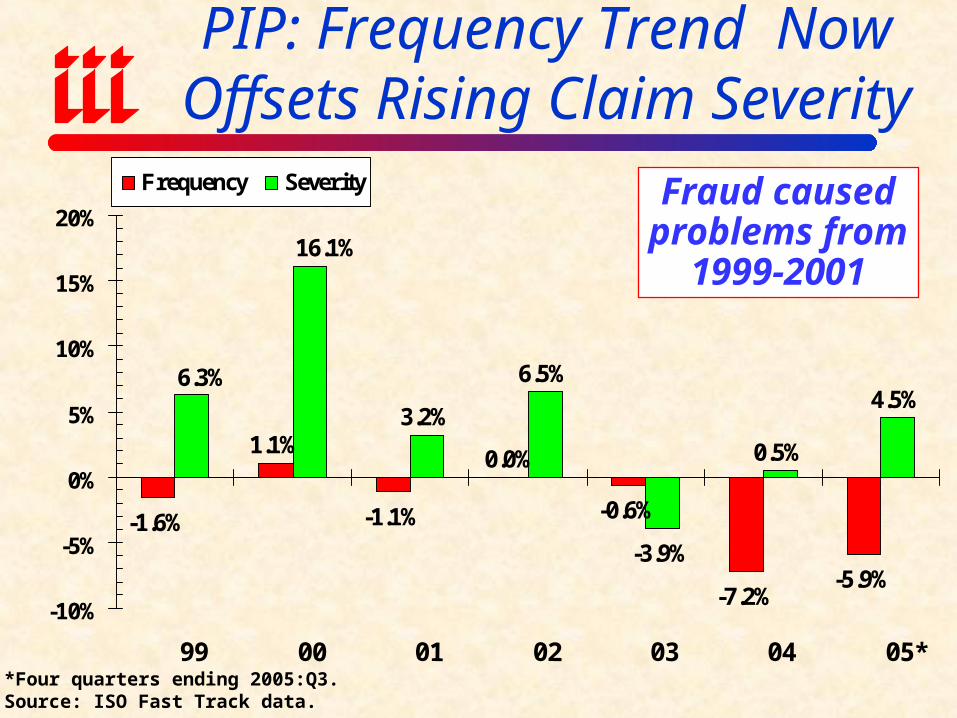

PIP: Frequency Trend Now Offsets Rising Claim Severity

Fraud caused problems from

1999-2001

*Four quarters ending 2005:Q3.Source: ISO Fast Track data.

2.6%

-0.4%

1.9%

-3.8%

-5.1%-4.6%

-2.5%

3.7% 3.6%

1.6%

3.6%3.0%

4.1%

6.8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

99 00 01 02 03 04 05*

Frequency Severity

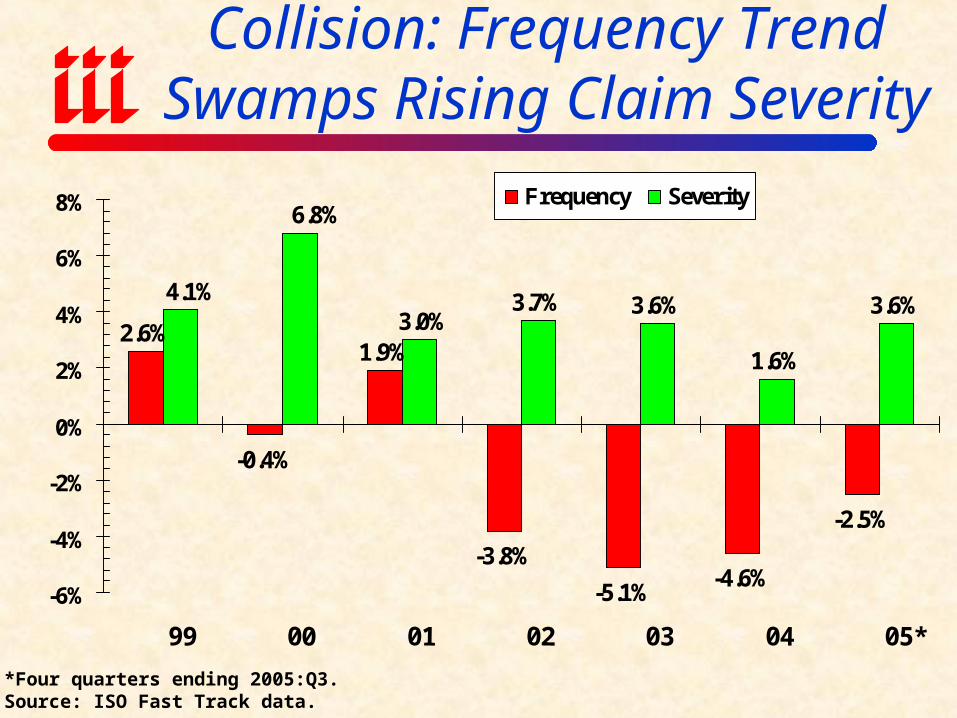

Collision: Frequency Trend Swamps Rising Claim Severity

*Four quarters ending 2005:Q3.Source: ISO Fast Track data.

-1.7%-2.6%

3.3%

-5.6%

-2.1%

-8.1%

-5.0%

-7.0%

-4.0%

2.7%

-2.7%

3.3%

-4.7%

8.9%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

99 00 01 02 03 04 05*

Frequency Severity

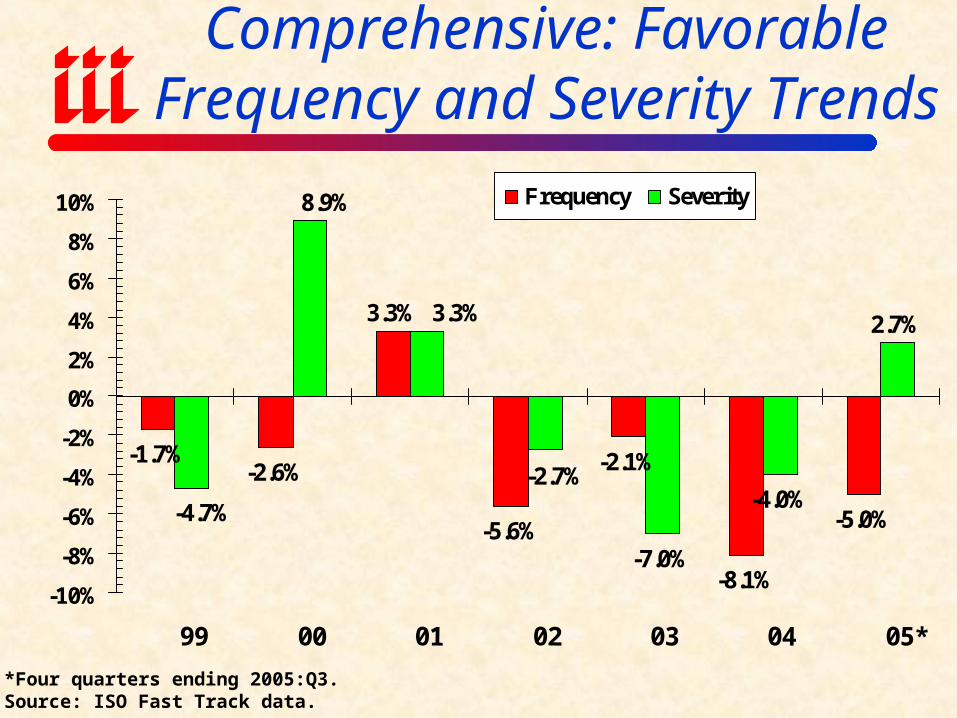

Comprehensive: Favorable Frequency and Severity Trends

*Four quarters ending 2005:Q3.Source: ISO Fast Track data.

Homeowners

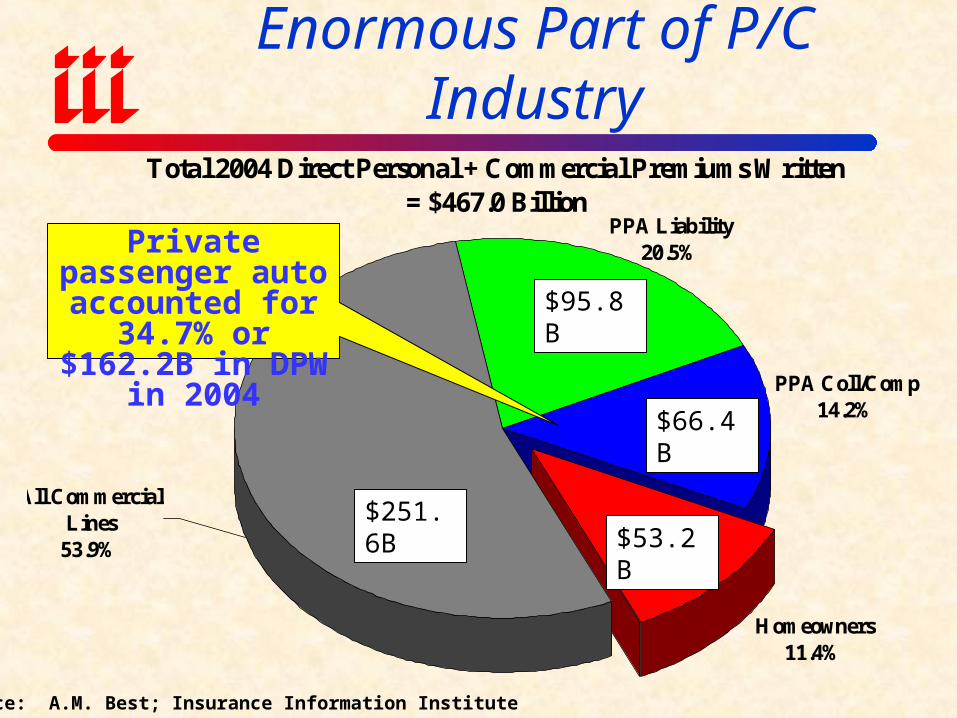

Private Passenger Auto is Enormous Part of P/C Industry

Total 2004 Direct Personal + Commercial Premiums Written = $467.0 Billion

All Commercial Lines

53.9%

PPA Coll/Comp14.2%

Homeowners11.4%

PPA Liability20.5%

Source: A.M. Best; Insurance Information Institute

Private passenger auto accounted for 34.7% or $162.2B in DPW in 2004

$251.6B$53.2B

$95.8B

$66.4B

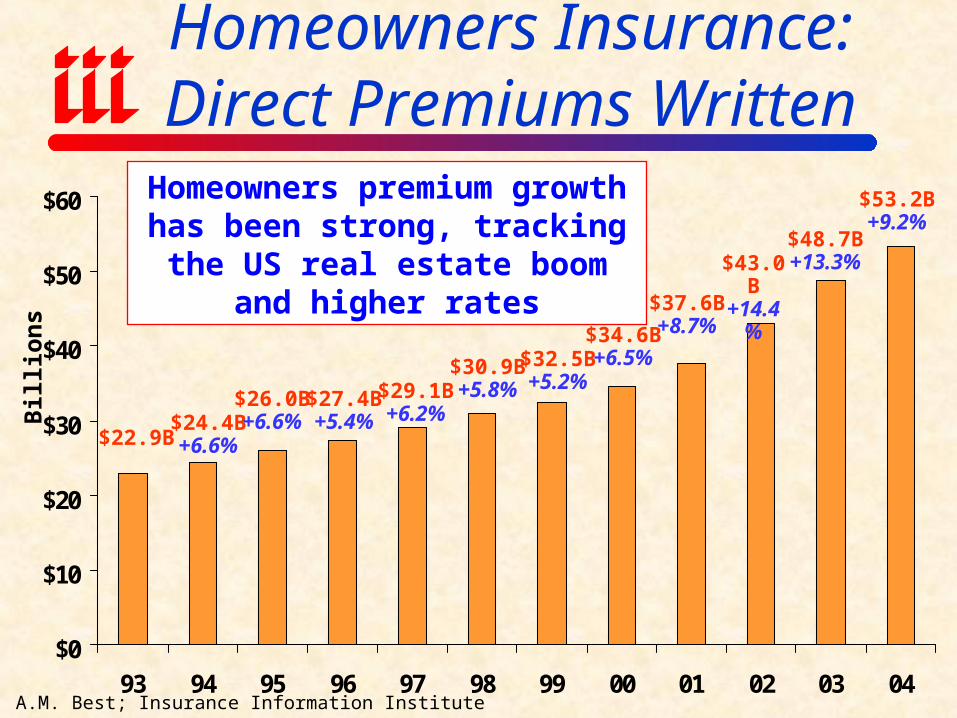

Homeowners Insurance:Direct Premiums Written

$0

$10

$20

$30

$40

$50

$60

93 94 95 96 97 98 99 00 01 02 03 04

Bil

lion

s

$22.9B

Source: A.M. Best; Insurance Information Institute

$24.4B+6.6%

$26.0B+6.6%

$27.4B+5.4%

$29.1B+6.2%

$30.9B+5.8%

$32.5B+5.2%

$34.6B+6.5%

$37.6B+8.7%

$43.0B+14.4

%

$48.7B+13.3%

$53.2B+9.2%

Homeowners premium growth has been strong, tracking the US real

estate boom and higher rates

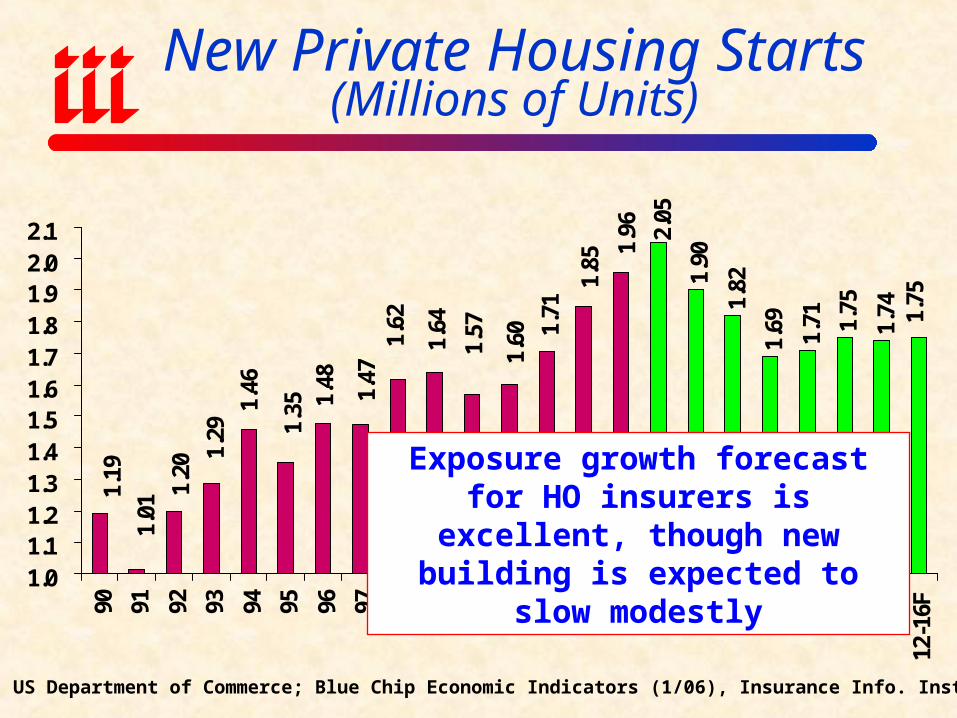

New Private Housing Starts(Millions of Units)

2.05

1.90

1.82

1.69 1.71 1.

75

1.74 1.

75

1.48

1.351.

46

1.29

1.20

1.01

1.19

1.47

1.62

1.64

1.57

1.60 1.

71

1.85

1.96

1.01.11.21.31.41.51.61.71.81.92.02.1

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04

05E

06F

07F

08F

09F

10F

11F

12-1

6F

Source: US Department of Commerce; Blue Chip Economic Indicators (1/06), Insurance Info. Institute

Exposure growth forecast for HO insurers is excellent, though new

building is expected to slow modestly

117.7

158.4

113.6118.4

112.7

121.7

101.0

108.2111.4

121.7

109.3

98.295.1

110113.0

109.4

90

100

110

120

130

140

150

160

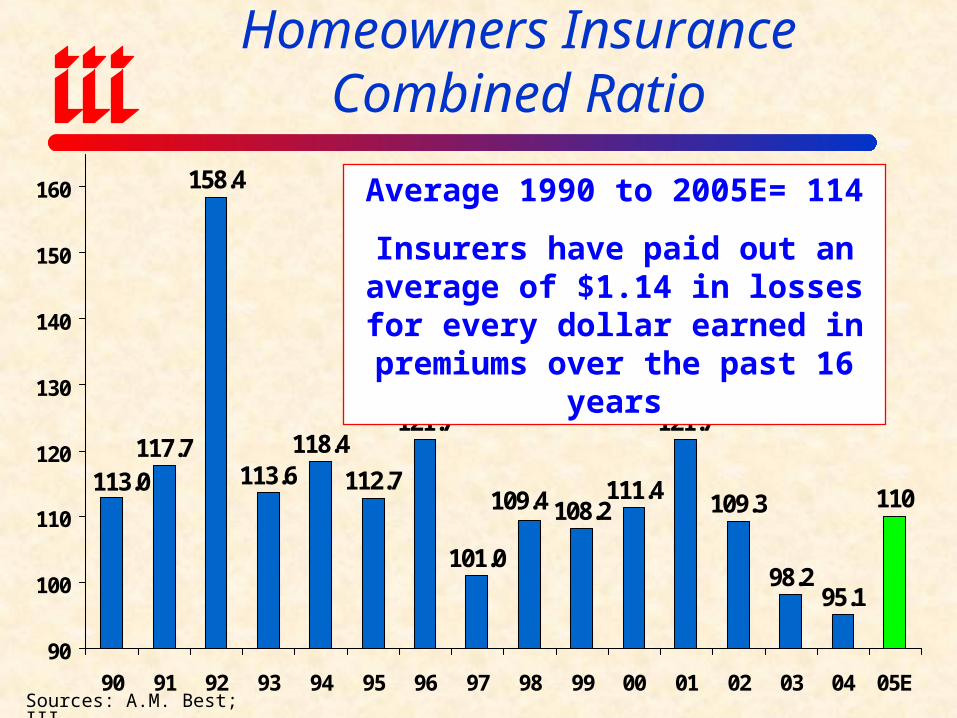

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05E

Homeowners Insurance Combined Ratio

Average 1990 to 2005E= 114

Insurers have paid out an average of $1.14 in losses for every dollar earned

in premiums over the past 16 years

Sources: A.M. Best; III

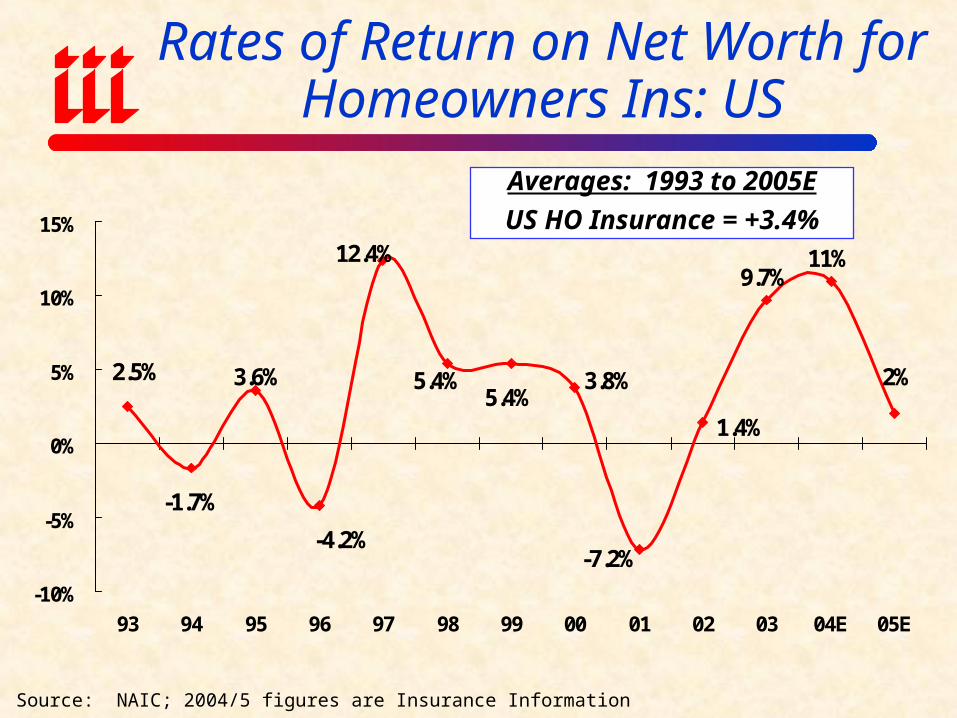

Rates of Return on Net Worth for Homeowners Ins: US

Source: NAIC; 2004/5 figures are Insurance Information Institute estimates.

9.7%11%

2%

-1.7%

-4.2%

3.6%

12.4%

5.4%2.5% 5.4% 3.8%

1.4%

-7.2%

-10%

-5%

0%

5%

10%

15%

93 94 95 96 97 98 99 00 01 02 03 04E 05E

Averages: 1993 to 2005E

US HO Insurance = +3.4%

INSURANCE-TO-VALUE:

Ending the Blame Game is aWin-Win Situation Deal

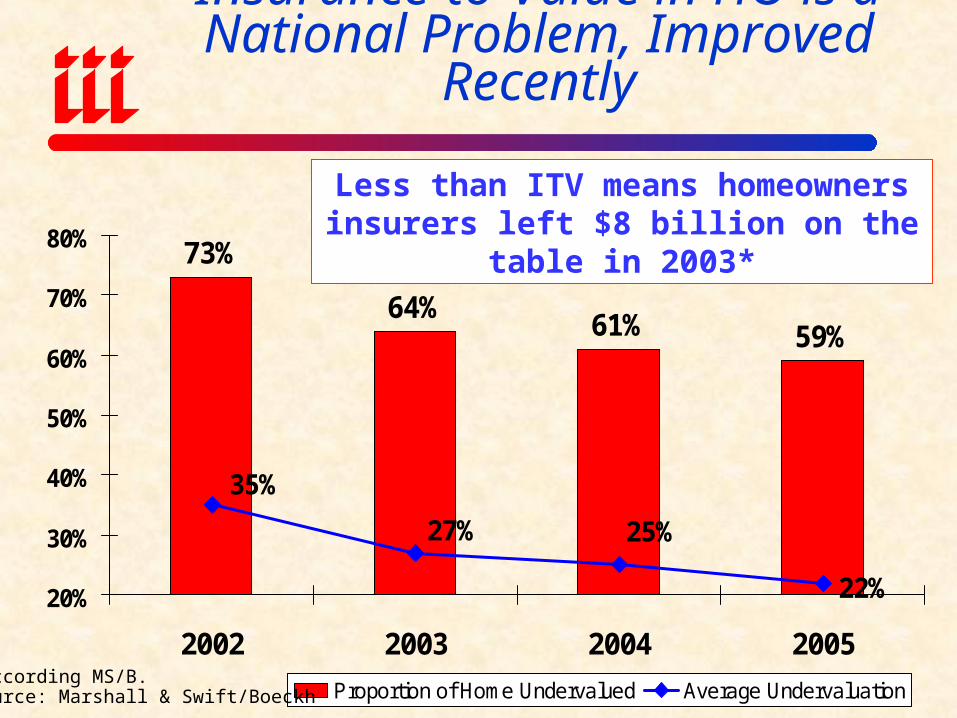

Insurance-to-Value in HO is a National Problem, Improved Recently

73%

64%61% 59%

22%

25%27%

35%

20%

30%

40%

50%

60%

70%

80%

2002 2003 2004 2005

Proportion of Home Undervalued Average Undervaluation*According MS/B.Source: Marshall & Swift/Boeckh

Less than ITV means homeowners insurers left $8 billion on the table in 2003*

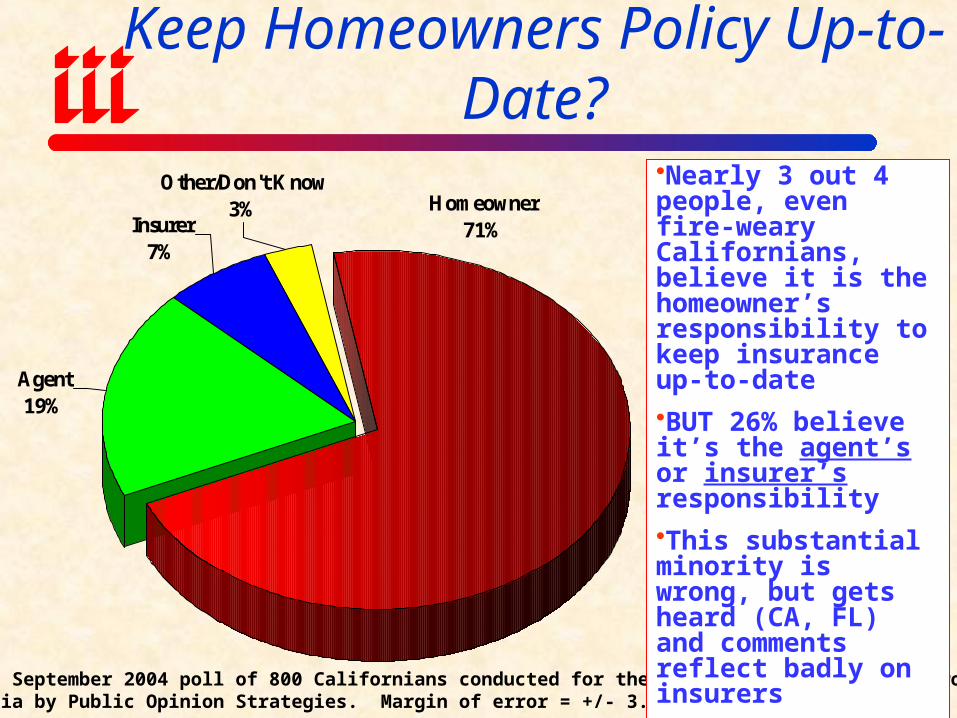

Who’s Responsibility Is It to Keep Homeowners Policy Up-to-Date?

Other/Don't Know3%

Agent19%

Insurer7%

Homeowner71%

Source: September 2004 poll of 800 Californians conducted for the Insurance Information Network ofCalifornia by Public Opinion Strategies. Margin of error = +/- 3.46%.

Nearly 3 out 4 people, even fire-weary Californians, believe it is the homeowner’s responsibility to keep insurance up-to-date

BUT 26% believe it’s the agent’s or insurer’s responsibility

This substantial minority is wrong, but gets heard (CA, FL) and comments reflect badly on insurers

Media, regulators and legislators join fray

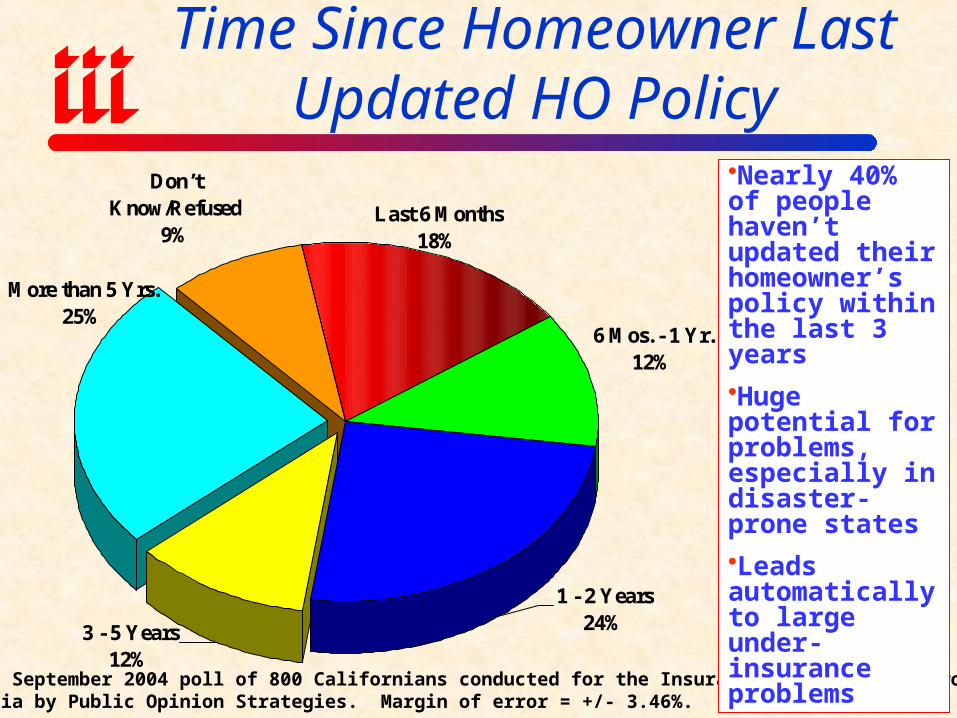

Time Since Homeowner Last Updated HO Policy

3 - 5 Years12%

Don’t Know/Refused

9%

6 Mos. - 1 Yr.12%

More than 5 Yrs.25%

1 - 2 Years24%

Last 6 Months18%

Source: September 2004 poll of 800 Californians conducted for the Insurance Information Network ofCalifornia by Public Opinion Strategies. Margin of error = +/- 3.46%.

Nearly 40% of people haven’t updated their homeowner’s policy within the last 3 years

Huge potential for problems, especially in disaster-prone states

Leads automatically to large under-insurance problems

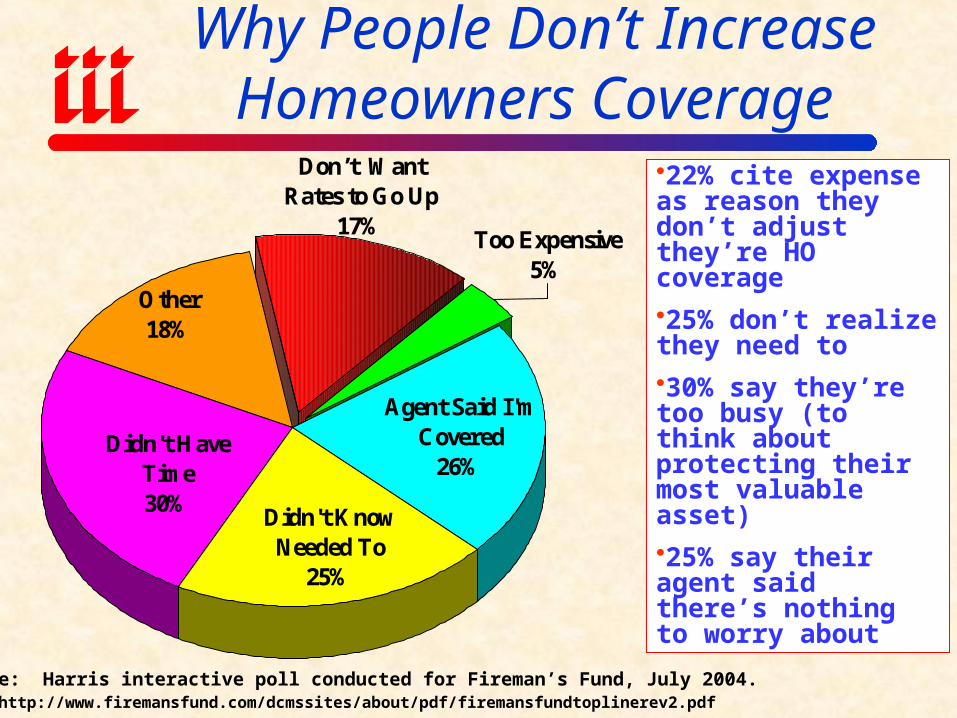

Why People Don’t Increase Homeowners Coverage

Didn't Know Needed To

25%

Other18%

Too Expensive5%

Didn't Have Time30%

Agent Said I'm Covered

26%

Don’t Want Rates to Go Up

17%

22% cite expense as reason they don’t adjust they’re HO coverage

25% don’t realize they need to

30% say they’re too busy (to think about protecting their most valuable asset)

25% say their agent said there’s nothing to worry about

Source: Harris interactive poll conducted for Fireman’s Fund, July 2004.See: http://www.firemansfund.com/dcmssites/about/pdf/firemansfundtoplinerev2.pdf

Summary• Home/Auto picture is bright for 2006, assuming “normal” CAT loss

activity

• Concern about pricing discipline, esp. if freq/severity trends turn adverse

• Rising investment returns insufficient to support deep soft market in terms of price, terms & conditions

• Clear need to be more underwriting focused

• Major Challenges:

Maintaining price/underwriting discipline

Managing variability/volatility of results

Insurance Information Institute On-Line

If you would like a copy of this presentation, please give me your business card with e-mail address

Recommended