Performance Budgeting

United Kingdom Experience

11th Annual OECD Asian Senior Budget Officials Meeting

Bangkok, 17 December 2015

Julian Kelly

Director-General, Public Spending and Finance

Contents

1. Spending Review

2. Performance frameworks

3. Costing

2

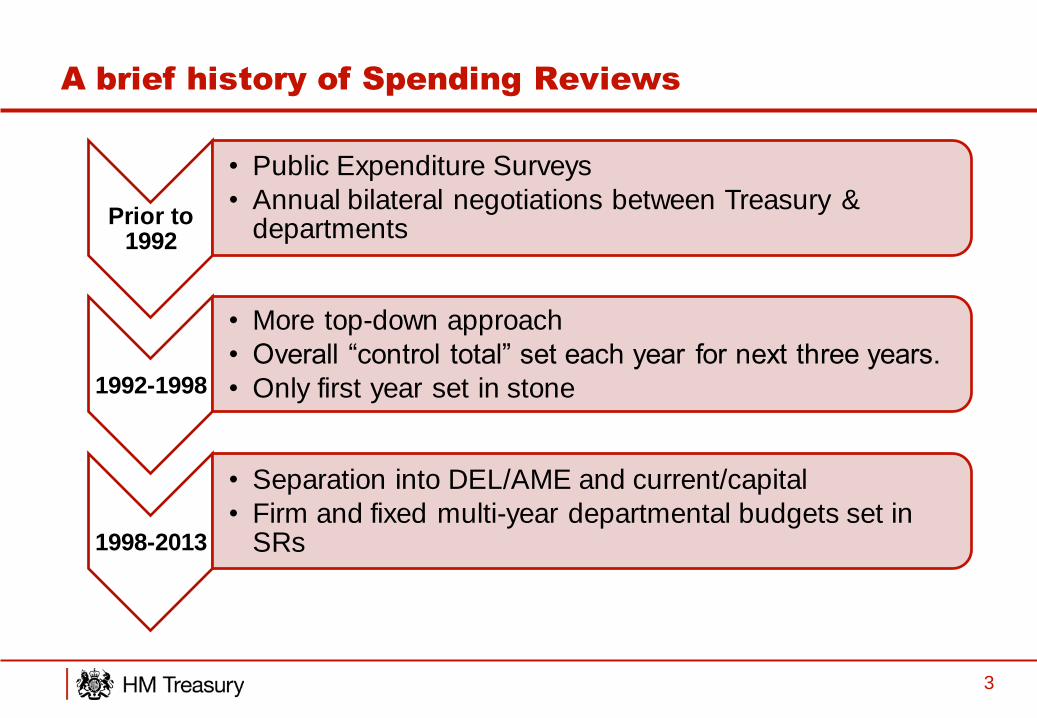

A brief history of Spending Reviews

Prior to 1992

• Public Expenditure Surveys

• Annual bilateral negotiations between Treasury & departments

1992-1998

• More top-down approach

• Overall “control total” set each year for next three years.

• Only first year set in stone

1998-2013

• Separation into DEL/AME and current/capital

• Firm and fixed multi-year departmental budgets set in SRs

3

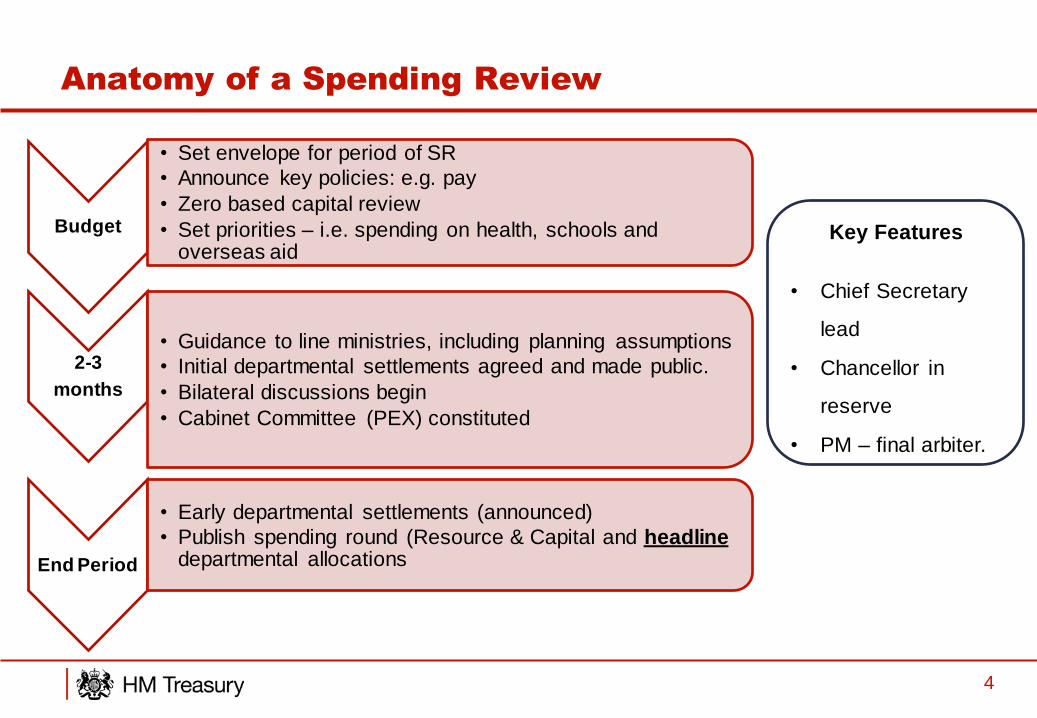

Anatomy of a Spending Review

4

Budget

• Set envelope for period of SR

• Announce key policies: e.g. pay

• Zero based capital review

• Set priorities – i.e. spending on health, schools and overseas aid

2-3

months

• Guidance to line ministries, including planning assumptions

• Initial departmental settlements agreed and made public.

• Bilateral discussions begin

• Cabinet Committee (PEX) constituted

End Period

• Early departmental settlements (announced)

• Publish spending round (Resource & Capital and headline departmental allocations

Key Features

• Chief Secretary

lead

• Chancellor in

reserve

• PM – final arbiter.

Key Reflections

• In the UK, the Finance Ministry runs the timetable/process and provides

guidance on the spending review framework

• Setting the key parameters and providing clear guidance at the start

manages expectations and provides certainty for departments and markets

• Success of zero based review for allocating capital investment

• Engagement with a broad range of stakeholders

• Planning ahead: start work early on the next review

5

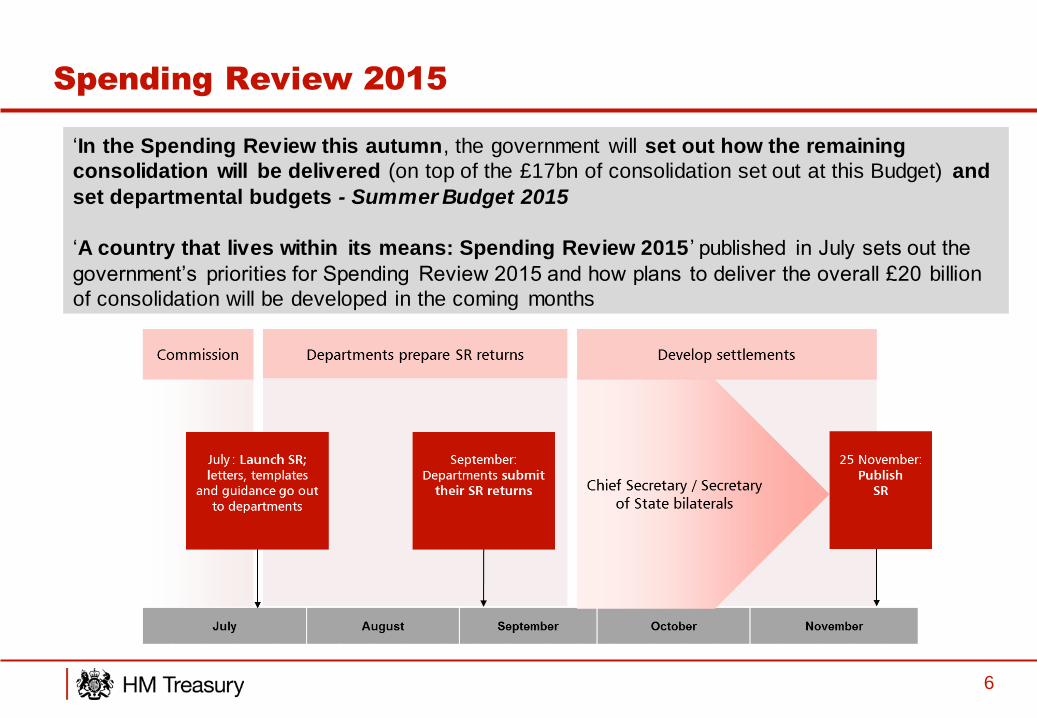

Spending Review 2015

6

‘In the Spending Review this autumn, the government will set out how the remaining

consolidation will be delivered (on top of the £17bn of consolidation set out at this Budget) and

set departmental budgets - Summer Budget 2015

‘A country that lives within its means: Spending Review 2015 ’ published in July sets out the

government’s priorities for Spending Review 2015 and how plans to deliver the overall £20 billion

of consolidation will be developed in the coming months

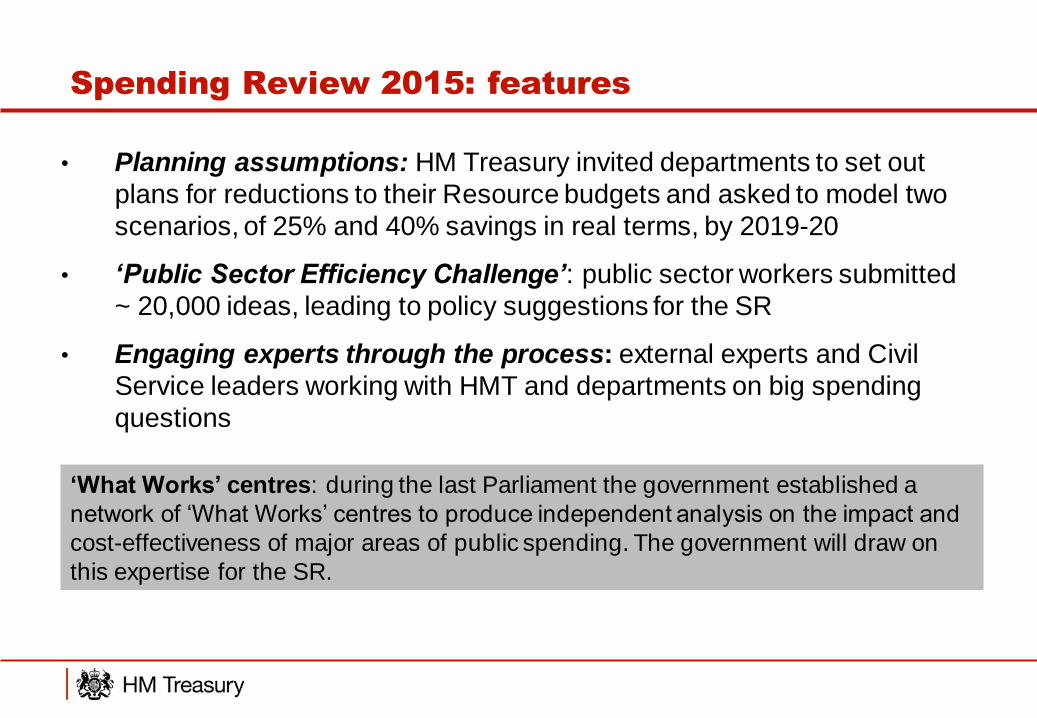

• Planning assumptions: HM Treasury invited departments to set out

plans for reductions to their Resource budgets and asked to model two

scenarios, of 25% and 40% savings in real terms, by 2019-20

• ‘Public Sector Efficiency Challenge’: public sector workers submitted

~ 20,000 ideas, leading to policy suggestions for the SR

• Engaging experts through the process: external experts and Civil

Service leaders working with HMT and departments on big spending

questions

Spending Review 2015: features

‘What Works’ centres: during the last Parliament the government established a

network of ‘What Works’ centres to produce independent analysis on the impact and

cost-effectiveness of major areas of public spending. The government will draw on

this expertise for the SR.

Contents

1. Spending Review

2. Performance frameworks

3. Costing

2

Context: our current performance framework is facing

a number of challenges

• In 2010, the government reformed performance management

o Abolished PSAs, replacing them with Departmental Business Plans

• The context/ environment has changed significantly in the last 5-10 years. The

financial environment is more constrained, the ‘low fruit’ been picked, and performance frameworks need to be adapted accordingly to ensure that money is spent in the most

effective way

• A number of challenges have arisen since 2010:

o BPs are not an effective performance management tool o Not linked to spend, and do not track VfM

• The current environment is a good opportunity to reassess & reform performance

management

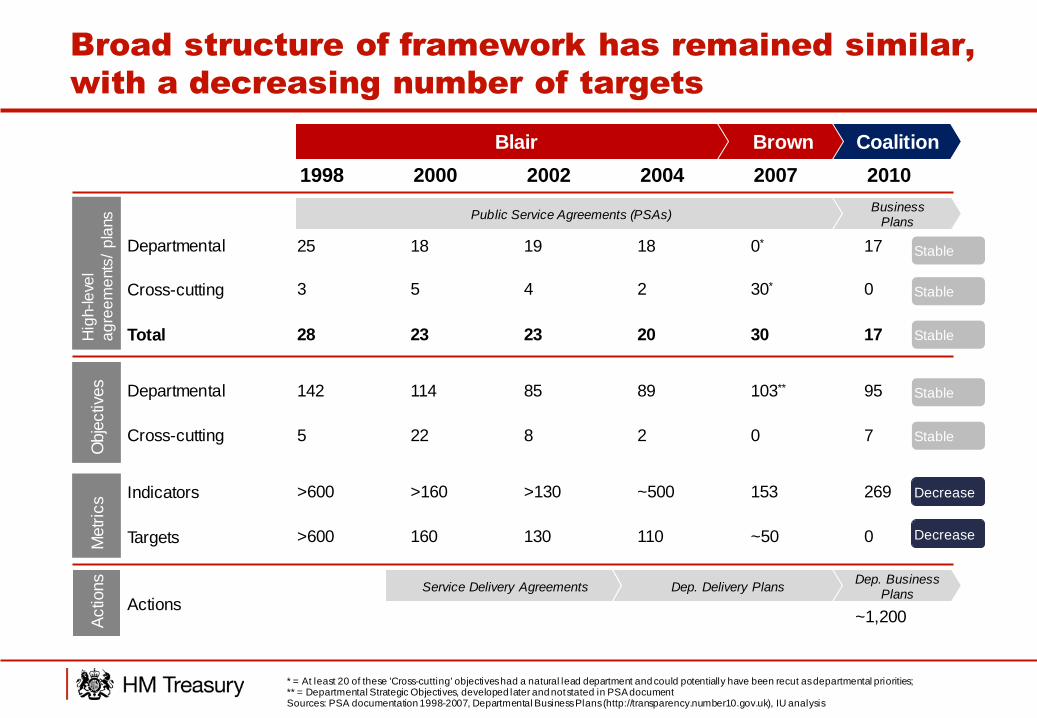

Broad structure of framework has remained similar,

with a decreasing number of targets

1998 2000 2002 2004 2007 2010

Blair Brown Coalition

Public Service Agreements (PSAs) Business

Plans

Departmental

Cross-cutting

Total Hig

h-le

vel

ag

ree

me

nts

/ p

lans

Service Delivery Agreements Dep. Delivery Plans Dep. Business

Plans

25 18 19 18 0* 17

3 5 4 2 30* 0

28 23 23 20 30 17

Obje

ctiv

es

Departmental 89 103** 95

Cross-cutting 2 0 7

85

8

114

22

142

5

Indicators

Targets

>600 >160 >130 ~500 153 269

>600 160 130 110 ~50 0 Metr

ics

Actions ~1,200 A

ctio

ns

* = At least 20 of these 'Cross-cutting' objectives had a natural lead department and could potentially have been recut as departmental priorities; ** = Departmental Strategic Objectives, developed later and not stated in PSA document Sources: PSA documentation 1998-2007, Departmental Business Plans (http://transparency.number10.gov.uk), IU analysis

Decrease

Stable

Stable

Stable

Stable

Stable

Decrease

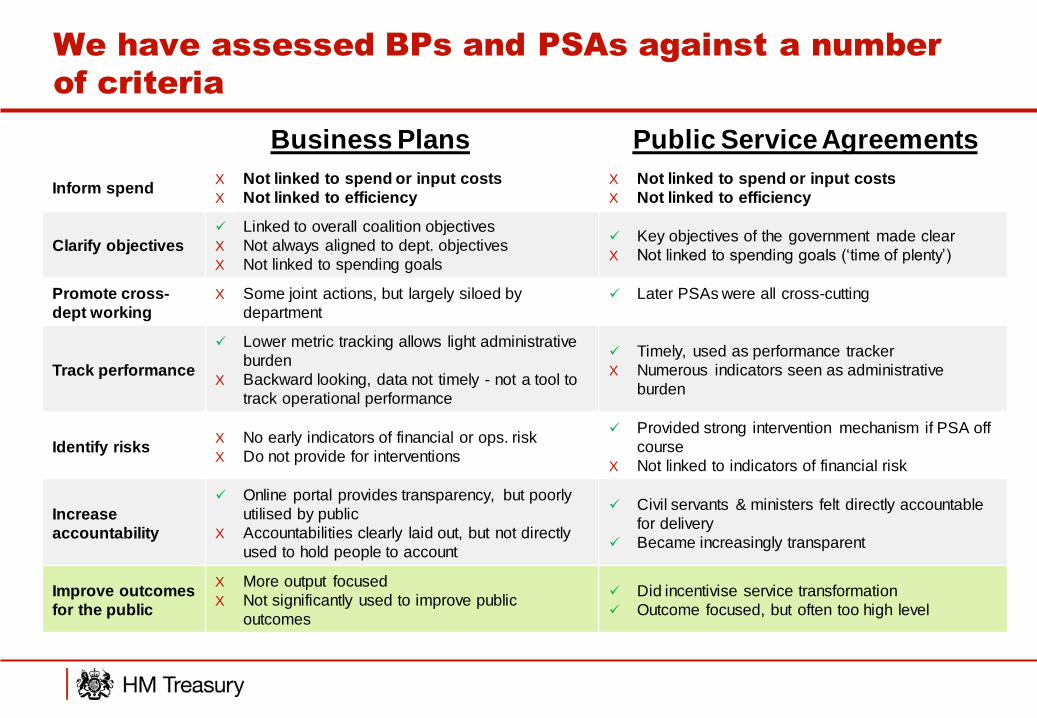

We have assessed BPs and PSAs against a number

of criteria

Inform spend X Not linked to spend or input costs

X Not linked to efficiency

X Not linked to spend or input costs

X Not linked to efficiency

Clarify objectives

Linked to overall coalition objectives

X Not always aligned to dept. objectives

X Not linked to spending goals

Key objectives of the government made clear

X Not linked to spending goals (‘time of plenty’)

Promote cross-

dept working

X Some joint actions, but largely siloed by

department

Later PSAs were all cross-cutting

Track performance

Lower metric tracking allows light administrative

burden

X Backward looking, data not timely - not a tool to

track operational performance

Timely, used as performance tracker

X Numerous indicators seen as administrative

burden

Identify risks X No early indicators of financial or ops. risk

X Do not provide for interventions

Provided strong intervention mechanism if PSA off

course

X Not linked to indicators of financial risk

Increase

accountability

Online portal provides transparency, but poorly

utilised by public

X Accountabilities clearly laid out, but not directly

used to hold people to account

Civil servants & ministers felt directly accountable

for delivery

Became increasingly transparent

Improve outcomes

for the public

X More output focused

X Not significantly used to improve public

outcomes

Did incentivise service transformation

Outcome focused, but often too high level

Business Plans Public Service Agreements

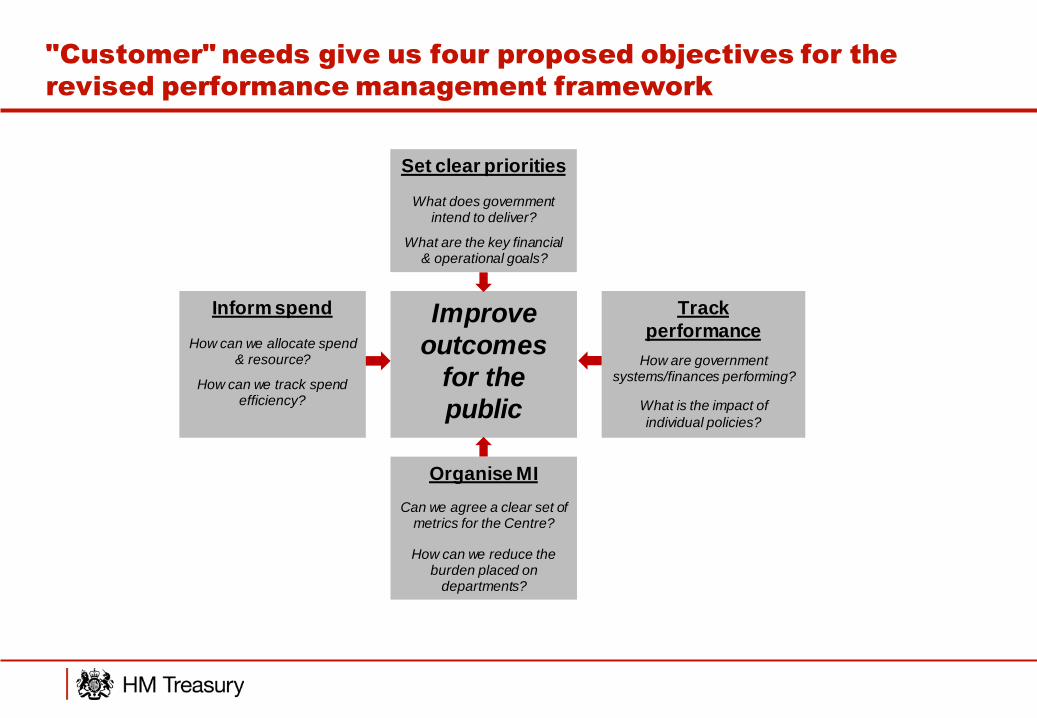

"Customer" needs give us four proposed objectives for the

revised performance management framework

Improve

outcomes

for the

public

Organise MI

Can we agree a clear set of metrics for the Centre?

How can we reduce the burden placed on

departments?

Track

performance

How are government systems/finances performing?

What is the impact of

individual policies?

Inform spend

How can we allocate spend & resource?

How can we track spend efficiency?

Set clear priorities

What does government intend to deliver?

What are the key financial & operational goals?

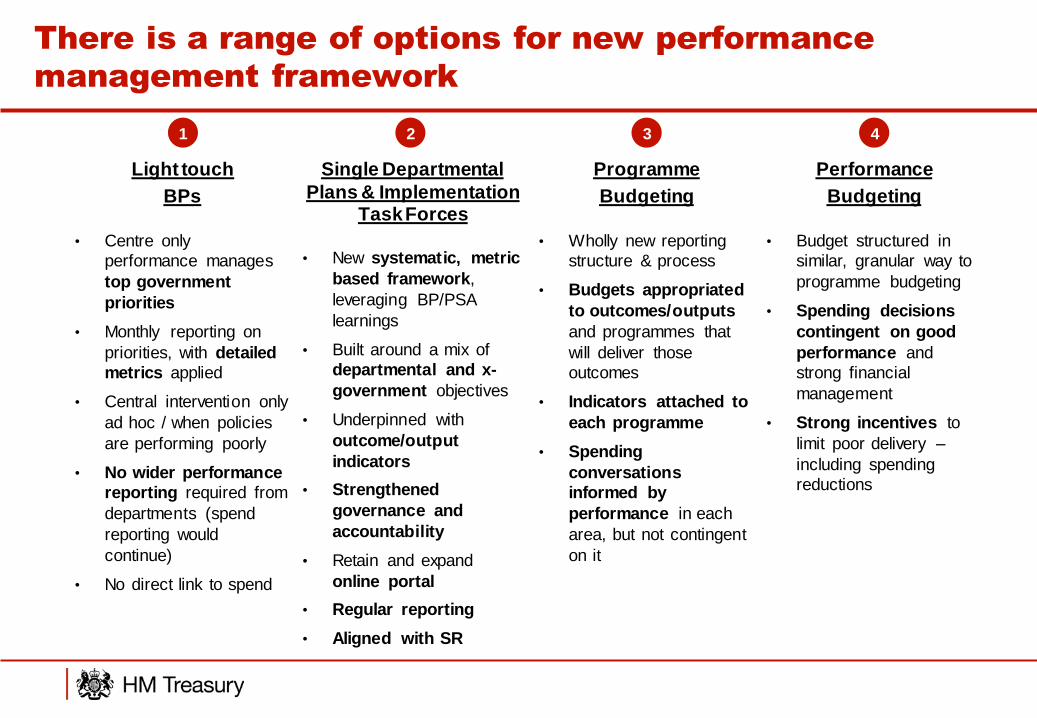

There is a range of options for new performance

management framework

Light touch

BPs

• Centre only

performance manages

top government

priorities

• Monthly reporting on

priorities, with detailed

metrics applied

• Central intervention only

ad hoc / when policies

are performing poorly

• No wider performance

reporting required from

departments (spend

reporting would

continue)

• No direct link to spend

Single Departmental

Plans & Implementation Task Forces

• New systematic, metric

based framework,

leveraging BP/PSA

learnings

• Built around a mix of

departmental and x-

government objectives

• Underpinned with

outcome/output

indicators

• Strengthened

governance and

accountability

• Retain and expand

online portal

• Regular reporting

• Aligned with SR

Programme

Budgeting

• Wholly new reporting

structure & process

• Budgets appropriated

to outcomes/outputs

and programmes that

will deliver those

outcomes

• Indicators attached to

each programme

• Spending

conversations

informed by

performance in each

area, but not contingent

on it

1 2 3

Performance

Budgeting

• Budget structured in

similar, granular way to

programme budgeting

• Spending decisions

contingent on good

performance and

strong financial

management

• Strong incentives to

limit poor delivery –

including spending

reductions

4

Contents

1. Spending Review

2. Performance frameworks

3. Costing

2

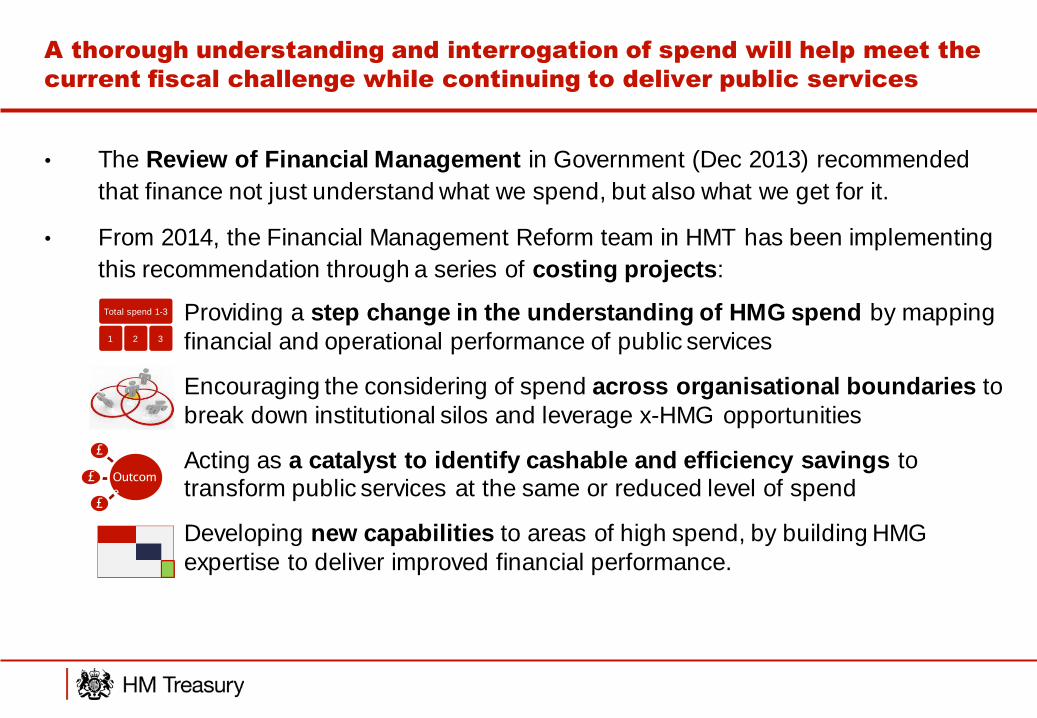

A thorough understanding and interrogation of spend will help meet the

current fiscal challenge while continuing to deliver public services

• Providing a step change in the understanding of HMG spend by mapping

financial and operational performance of public services

• Encouraging the considering of spend across organisational boundaries to

break down institutional silos and leverage x-HMG opportunities

• Acting as a catalyst to identify cashable and efficiency savings to transform public services at the same or reduced level of spend

• Developing new capabilities to areas of high spend, by building HMG

expertise to deliver improved financial performance.

Total spend 1-3

1 2 3

£

£

£

Outcom

e

• The Review of Financial Management in Government (Dec 2013) recommended

that finance not just understand what we spend, but also what we get for it.

• From 2014, the Financial Management Reform team in HMT has been implementing

this recommendation through a series of costing projects:

Questions?

Recommended