Please refer to Disclosures and Disclaimers at the end of the Research Report.

Metals Monthly wrap up

PhillipCapital (India) Pvt. Ltd.

Weak demand and increasing supply has seen pressure in the domestic flat steel prices however the Long products has shown resilience with low inventory and stable demand. The domestic industry is awaiting SC order on Orissa iron ore case which could significantly disrupt the supply in the event of mining restrictions. Global steel prices were mixed with higher steel prices in the developing economies and developed nations showing flat to marginal weakness in the prices. The current month also stood bad for the raw material prices with both iron ore and coking coal (contract) showing strong declines during the month. Non Ferrous metals gained during the month with zinc leading the pack. Key Highlights Ferrous • Flat product prices have corrected by 1‐2% across India in Apr 2014 post gaining 3‐7% since start of the calendar year. Long products prices increased by 1‐5% across India. Improved demand, higher semi product prices and low inventory led to another hike of Rs 500‐1,000 per tonne in May 2014.

• Flat products prices in China and CIS have seen 2‐4% gain in April 2014 while it has corrected in US and Europe. Long products prices stood flat in CIS and Europe while improved in US and China.

• Global iron ore prices of 62% Fe grade fell by 9.8% to US$ 105 per tonnes during the month as Chinese banking regulator has urged local authorities and banks to step up investigation into iron ore financing deals to minimize default risks. This overhang could drive down the prices further in near future. Indian iron ore miners have kept their prices unchanged while NMDC has reduced lumps prices by Rs 200 per tonne after keeping it constant for five months. Domestic pellet prices increased by Rs 300/tn to Rs 6,650/tn in Apr 2014.

• Scrap prices increased across geographies with domestic market leading the pack (up 4.0% mom).

• Spot coking coal prices increased by US$ 5/tn to US$ 112/tn. Contract prices for Q2CY14 were down 16% to US$ 120. Thermal coal prices fell across regions (except South Africa) with highest fall reported in Indonesia.

• Global steel inventory excluding EU fell by 6.2% (~2.2mn tonnes) in Apr 2014 on falling inventory in China. Iron ore inventory at ports in China stands at 105.2mn tonnes, up 1.4% mom.

Non Ferrous • All base metal prices gained during the month with Zinc leading the pack. Prices of aluminium/ zinc/ lead/ copper moved +2.3%/ +3.6%/ +2.0%/ +0.1% respectively. Base metal prices in Shanghai increased by 1‐6% with copper leading the pack.

• Aluminium regional premiums have increased significantly post UK court has scrapped plan of changes in warehousing rules to be implemented from 1st April, 2014. Premium in Japan/ Europe/ China increased by US$ 112/ 20/ 33 to US$ 367/ 375/ 363 respectively. Premium for zinc in Singapore improved by 12.1% while premium for lead decreased by 12.5% in Apr 2014.

• Alumina price as a % of LME decreased to 17.8% in Apr 2014 against 18.5% in Mar 2014.

• LME inventory have fell across base metals with highest fall reported by copper. LME inventory of aluminium/ zinc/ lead/ copper fell by 0.5%/ 0.3%/ 3.3%/ 12.0% respectively.

Valuations FY15E (x) P/E P/BV EV/EBITDAJSW Steel 9.3 1.1 5.8Tata Steel 11.1 1.0 11.1SAIL 14.6 0.7 9.4JSPL 9.9 2.1 6.6Hindalco 12.5 0.7 8.0Nalco 11.7 0.8 3.7Hindustan Zinc 7.7 1.2 3.3Sesa Sterlite 6.9 1.5 4.4 Regional Performance (rebased)

60708090

100110120130140 India Brazil

Australia London

Indices (rebased)

60708090

100110120130140

BSE Ssnsex

BSE Metal Index

Absolute Performance Change (table)

1M 3M 6MAluminium 2.3 6.4 (3.5)Zinc 3.6 3.9 6.3Copper 0.1 (6.2) (8.0)Lead 2.0 (0.6) (3.7)HRC (1.0) (0.5) 1.0TMT 5.4 3.4 12.8Iron Ore (9.8) (14.0) (20.1)Coking Coal 4.3 (10.6) (23.2)Thermal Coal (0.4) (8.9) (9.7)

Source: Company, PhillipCapital India Research Dhawal Doshi (+ 9122 6667 9769) [email protected] Dharmesh Shah (+ 9122 6667 9974) [email protected]

– 2 of 33 –

12 May 2014 / INDIA EQUITY RESEARCH / METALS – MONTHLY WRAP UP

INDEX Ferrous ‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐ 3

Steel Prices ‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐ 3

Raw Material Prices (Iron ore, Scrap, Coal) ‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐ 6

Ferro Alloy Prices ‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐ 9

Steel Profitability & Cost Index ‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐ 10

Production & Inventory ‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐ 11

Trade Data ‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐ 13

Non Ferrous ‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐ 15

Aluminium, Alumina & Bauxite ‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐ 15

Zinc ‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐ 20

Lead ‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐ 22

Copper ‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐ 24

Trade Data ‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐ 27

– Aluminium ‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐ 27

– Zinc & Lead ‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐ 28

– Copper ‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐ 29

LME Cancelled Warrant ‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐ 30

Open Interest – LME ‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐ 31

– 3 of 33 –

12 May 2014 / INDIA EQUITY RESEARCH / METALS – MONTHLY WRAP UP

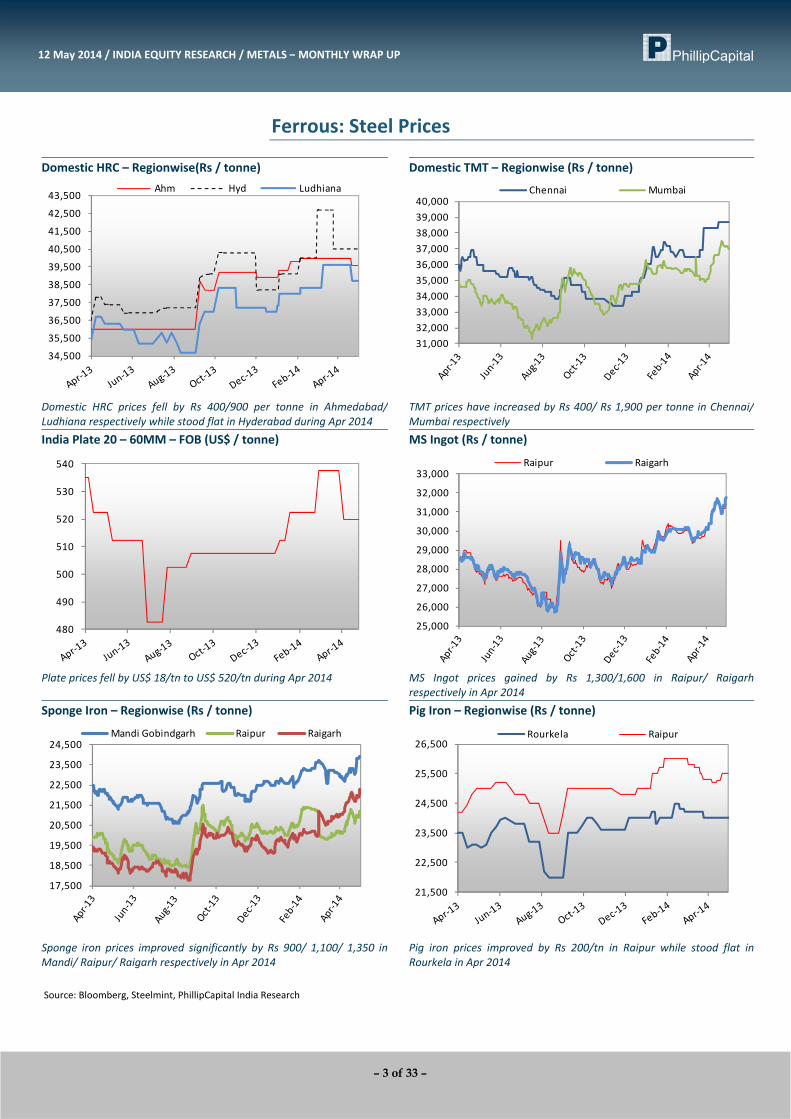

Ferrous: Steel Prices

Domestic HRC – Regionwise(Rs / tonne) Domestic TMT – Regionwise (Rs / tonne)

34,500

35,500

36,500

37,500

38,500

39,500

40,500

41,500

42,500

43,500 Ahm Hyd Ludhiana

31,000 32,000 33,000 34,000 35,000 36,000 37,000 38,000 39,000 40,000

Chennai Mumbai

Domestic HRC prices fell by Rs 400/900 per tonne in Ahmedabad/Ludhiana respectively while stood flat in Hyderabad during Apr 2014

TMT prices have increased by Rs 400/ Rs 1,900 per tonne in Chennai/ Mumbai respectively

India Plate 20 – 60MM – FOB (US$ / tonne) MS Ingot (Rs / tonne)

480

490

500

510

520

530

540

25,000

26,000

27,000

28,000

29,000

30,000

31,000

32,000

33,000 Raipur Raigarh

Plate prices fell by US$ 18/tn to US$ 520/tn during Apr 2014

MS Ingot prices gained by Rs 1,300/1,600 in Raipur/ Raigarh respectively in Apr 2014

Sponge Iron – Regionwise (Rs / tonne) Pig Iron – Regionwise (Rs / tonne)

17,500

18,500

19,500

20,500

21,500

22,500

23,500

24,500 Mandi Gobindgarh Raipur Raigarh

21,500

22,500

23,500

24,500

25,500

26,500 Rourkela Raipur

Sponge iron prices improved significantly by Rs 900/ 1,100/ 1,350 inMandi/ Raipur/ Raigarh respectively in Apr 2014

Pig iron prices improved by Rs 200/tn in Raipur while stood flat in Rourkela in Apr 2014

Source: Bloomberg, Steelmint, PhillipCapital India Research

– 4 of 33 –

12 May 2014 / INDIA EQUITY RESEARCH / METALS – MONTHLY WRAP UP

China Export HRC (US$ / tonne) China Export Rebar (US$ / tonne)

490

500

510

520

530

540

550

560

570

580

470

480

490

500

510

520

530

540

550

HRC prices fell by US$ 10/tn to US$ 525/tn in Apr 2014

Rebar prices gained by US$ 8/tn to US$ 485/tn in Apr 2014

China Domestic HRC (Yuan / tonne) China Domestic Rebar (Yuan / tonne)

3,250

3,350

3,450

3,550

3,650

3,750

3,850

3,950

3200

3300

3400

3500

3600

3700

Unlike export HRC, China domestic HRC prices gained 2.9% mom in April 2014

Rebar prices gained by 60 Yuan/tn (1.8% mom) in Apr 2014

CIS Export HRC – (US$ / tonne) CIS Export Rebar – (US$ / tonne)

500

510

520

530

540

550

560

570

520

530

540

550

560

570

580

590

600

CIS HRC prices more than recovered its loss during Mar 2014. Pricesincreased by US$ 22.5/ tn (4.4% mom) in Apr 2014

CIS rebar prices stood flat at US$ 527.5/tn in Apr 2014

Source: Bloomberg, PhillipCapital India Research

– 5 of 33 –

12 May 2014 / INDIA EQUITY RESEARCH / METALS – MONTHLY WRAP UP

EU Domestic HRC (Euro / tonne) EU Domestic Rebar (Euro / tonne)

425435445455465475485495505515

Northern Southern

440450460470480490500510520530

Northern Southern

Price in Northern Europe stood flat at 447.5 euros while it fell by 5 euros in Southern Europe to 430 euros in Apr 2014

Price in Northern Europe stood flat at 490 euros while it gained by 7.5 euros in Southern Europe to 455 euros in Apr 2014

US Import HRC – (US$ / tonne) US Import Rebar (US$ / tonne)

560

570

580

590

600

610

620

550

560

570

580

590

600

610

US import HRC fell by US$ 5/tn to US$ 590/tn in Apr 2014

US import Rebar price stood flat at US$ 605/tn in Apr 2014

US Domestic Carbon Steel Plate (US$ / tonne)

680

700

720

740

760

780

800

820

840

Plate prices marginally gained by US$ 2/tn to US$ 818/tn in Apr 2014

Source: Bloomberg, PhillipCapital India Research

– 6 of 33 –

12 May 2014 / INDIA EQUITY RESEARCH / METALS – MONTHLY WRAP UP

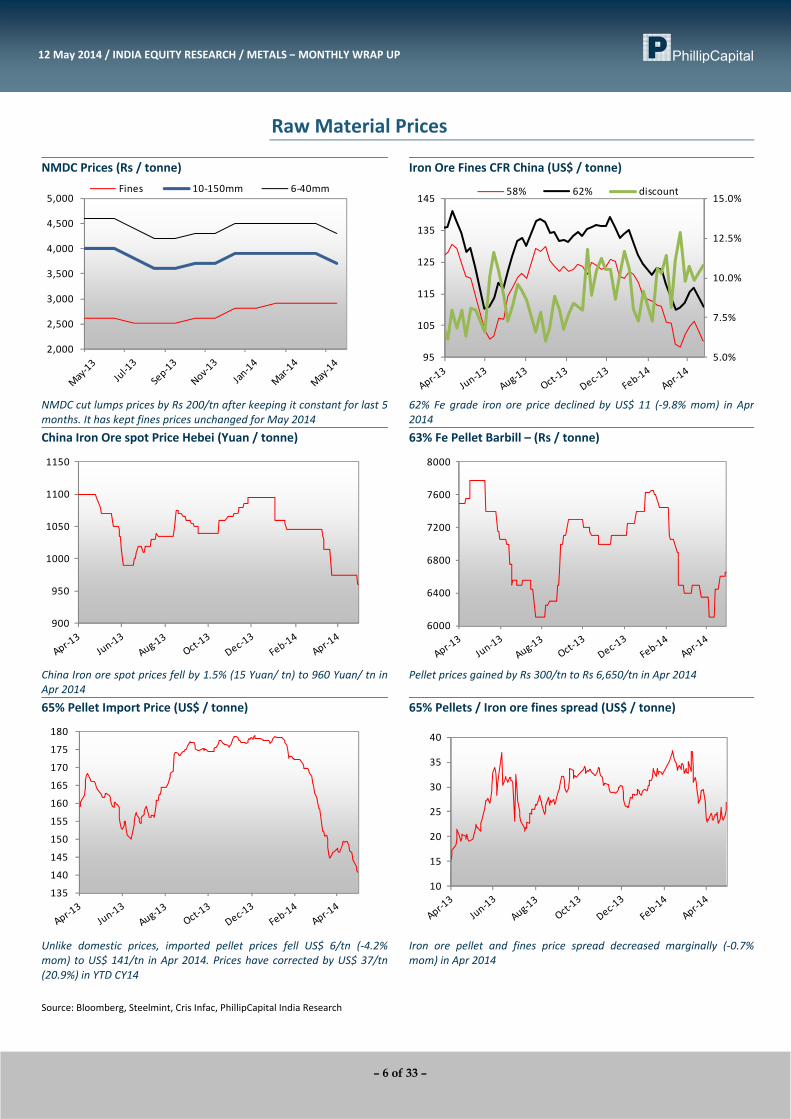

Raw Material Prices

NMDC Prices (Rs / tonne) Iron Ore Fines CFR China (US$ / tonne)

2,000

2,500

3,000

3,500

4,000

4,500

5,000 Fines 10‐150mm 6‐40mm

5.0%

7.5%

10.0%

12.5%

15.0%

95

105

115

125

135

14558% 62% discount

NMDC cut lumps prices by Rs 200/tn after keeping it constant for last 5months. It has kept fines prices unchanged for May 2014

62% Fe grade iron ore price declined by US$ 11 (‐9.8% mom) in Apr 2014

China Iron Ore spot Price Hebei (Yuan / tonne) 63% Fe Pellet Barbill – (Rs / tonne)

900

950

1000

1050

1100

1150

6000

6400

6800

7200

7600

8000

China Iron ore spot prices fell by 1.5% (15 Yuan/ tn) to 960 Yuan/ tn in Apr 2014

Pellet prices gained by Rs 300/tn to Rs 6,650/tn in Apr 2014

65% Pellet Import Price (US$ / tonne) 65% Pellets / Iron ore fines spread (US$ / tonne)

135

140

145

150

155

160

165

170

175

180

10

15

20

25

30

35

40

Unlike domestic prices, imported pellet prices fell US$ 6/tn (‐4.2% mom) to US$ 141/tn in Apr 2014. Prices have corrected by US$ 37/tn (20.9%) in YTD CY14

Iron ore pellet and fines price spread decreased marginally (‐0.7% mom) in Apr 2014

Source: Bloomberg, Steelmint, Cris Infac, PhillipCapital India Research

– 7 of 33 –

12 May 2014 / INDIA EQUITY RESEARCH / METALS – MONTHLY WRAP UP

Domestic Scrap (Rs / tonne) US Heavy Melting Scrap (US$ / tonne)

21,000 21,500 22,000 22,500 23,000 23,500 24,000 24,500 25,000 25,500 26,000 26,500

Raipur Mumbai

310

320

330

340

350

360

370

380

390

400

Scrap prices in Raipur/ Mumbai gained by Rs 1,000 (+4.2%) / 1,100 (+4.4%) per tonne in Apr 2014

China Heavy Steel Scrap over 8MM (Yuan / tonne) Germany Scrap Price (Euro / tonne)

2,200

2,300

2,400

2,500

2,600

2,700

2,800

230

240

250

260

270

280

Scrap prices gained by 20 Yuan/tn (+0.9% mom) to 2,300 Yuan/tn in Apr 2014

Scrap prices fell by 11 Euros (‐4.4%) to 239 euros sequentially in Mar2014

Hard Coking Coal (US$ / tonne) China Coking Coal (Yuan / tonne)

95

105

115

125

135

145

155

165

800

900

1000

1100

1200

1300Pindingshan Yinchuan

Coking coal prices increased by US$ 5/tn (+4.3%) to US$ 112 in Apr2014

China coking coal price in Yinchuan stood flat at 900 Yuan/tn since mid Oct 2013 while it fell 40 Yuan/tn (‐4.0%) sequentially in Pindingshan in Apr 2014

Source: Bloomberg, Steelmint, PhillipCapital India Research

– 8 of 33 –

12 May 2014 / INDIA EQUITY RESEARCH / METALS – MONTHLY WRAP UP

Coking Coal Contract price ($ / tonne) China 1st Grade Coke (Yuan / tonne)

100125150175200225250275300325350

1100

1200

1300

1400

1500

1600

Q2CY14 coking coal contract settled at US$ 120/tn, down US$ 23/tn qoq

Coke prices fell by 40 Yuan/ tn (‐3.4%) sequentially in Apr 2014

NCDEX Thermal Coal (Rs / tonne) McCloskey Newcastle Coal 6700Kcal Australia (US$ / tonne)

3500

3600

3700

3800

3900

4000

4100

4200

4300

70

75

80

85

90

Domestic coal prices stood flat at Rs 3,840/tn since first week of Oct2013

Coal prices declined marginally by 0.4% in Apr 2014 to US$ 73/tn. This is the lowest price reported post Oct 2009

Richards Bay South African Coal 6000 Kcal (US$ / tonne) Indonesian Coal (US$ / tonne)

70

75

80

85

90

40

45

50

55

60

65

70

75Indonesian Melawan Coal ‐5400 KcalIndonesian Eco Coal ‐4200 KcalIndonesian Envirocoal ‐5000 Kcal

South African coal price gained by US$ 3.5/tn (+4.7% mom) in Apr 2014to US$ 76/tn

Prices in Indonesia decreased by ~2.5% sequentially in Apr 2014. This is the lowest price reported since Dec 2009

Source: Bloomberg, PhillipCapital India Research

– 9 of 33 –

12 May 2014 / INDIA EQUITY RESEARCH / METALS – MONTHLY WRAP UP

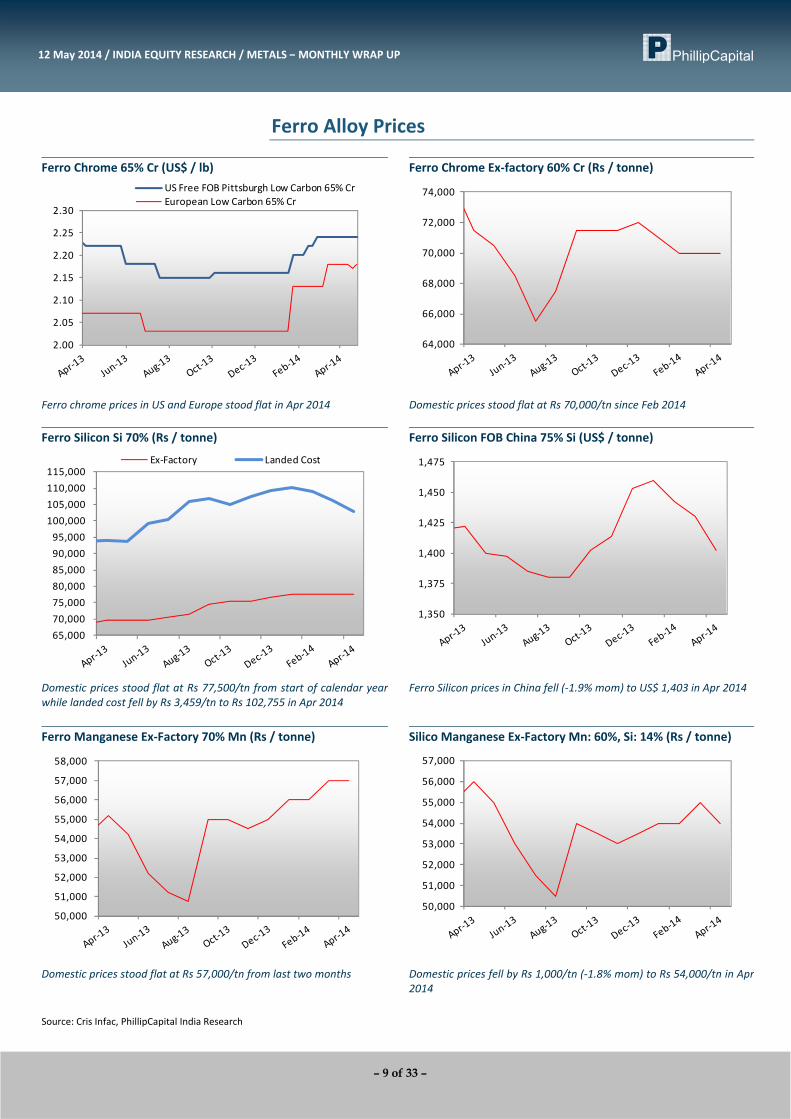

Ferro Alloy Prices

Ferro Chrome 65% Cr (US$ / lb) Ferro Chrome Ex‐factory 60% Cr (Rs / tonne)

2.00

2.05

2.10

2.15

2.20

2.25

2.30

US Free FOB Pittsburgh Low Carbon 65% CrEuropean Low Carbon 65% Cr

64,000

66,000

68,000

70,000

72,000

74,000

Ferro chrome prices in US and Europe stood flat in Apr 2014

Domestic prices stood flat at Rs 70,000/tn since Feb 2014

Ferro Silicon Si 70% (Rs / tonne) Ferro Silicon FOB China 75% Si (US$ / tonne)

65,000 70,000 75,000 80,000 85,000 90,000 95,000

100,000 105,000 110,000 115,000

Ex‐Factory Landed Cost

1,350

1,375

1,400

1,425

1,450

1,475

Domestic prices stood flat at Rs 77,500/tn from start of calendar yearwhile landed cost fell by Rs 3,459/tn to Rs 102,755 in Apr 2014

Ferro Silicon prices in China fell (‐1.9% mom) to US$ 1,403 in Apr 2014

Ferro Manganese Ex‐Factory 70% Mn (Rs / tonne) Silico Manganese Ex‐Factory Mn: 60%, Si: 14% (Rs / tonne)

50,000

51,000

52,000

53,000

54,000

55,000

56,000

57,000

58,000

50,000

51,000

52,000

53,000

54,000

55,000

56,000

57,000

Domestic prices stood flat at Rs 57,000/tn from last two months Domestic prices fell by Rs 1,000/tn (‐1.8% mom) to Rs 54,000/tn in Apr

2014 Source: Cris Infac, PhillipCapital India Research

– 10 of 33 –

12 May 2014 / INDIA EQUITY RESEARCH / METALS – MONTHLY WRAP UP

Steel Profitability & Cost Index

BOF Steel Profitability Index – North America (US$ / tonne) EAF Steel Profitability Index – Europe (Euro / tonne)

0

25

50

75

100

125

150

175

200

‐20

‐10

0

10

20

30

40

50

60

Profitability index gained by US$ 40/tn to US$ 190 in Apr 2014

Profitability index fell by 4 euros to 25 euros in Apr 2014

EAF Steel Cost Index – North America (US$ / tonne) EAF Steel Cost Index – Europe (Euro / tonne)

375

400

425

450

475

500

525

550

380

400

420

440

460

480

500

Source: Bloomberg, PhillipCapital India Research

– 11 of 33 –

12 May 2014 / INDIA EQUITY RESEARCH / METALS – MONTHLY WRAP UP

Production & Inventory

World Steel Production (mn tonnes) Regionwise Steel Production (mn tonnes)

124

126

128

130

132

134

136

138

140

142

5.0

15.0

25.0

35.0

45.0

55.0

65.0

75.0

China EU North AmericaAsia ex China CIS Others

World crude steel production for Mar 2014 stands at 141mn tonnes, up2.7% yoy and 13.1% sequentially

Except CIS, all regions have reported growth in steel production on yoy basis in Mar 2014

China Daily Steel Production (mn tonnes) India Steel Production (mn tonnes)

1.95

2.00

2.05

2.10

2.15

2.20

2.25

2.30

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

10.0

China daily crude steel production for 2nd 10 days of Apr 2014 stood at 2.28mn tonnes, up 7.8% yoy and 6.1% sequentially

Steel production for Apr 2014 stood at 7mn tonnes, up 8.9% yoy anddown 8.8% sequentially

China Iron Ore Production (mn tonnes) Iron Ore Production‐ Australia & Brazil (mn tonnes)

110

114

118

122

126

130

134

138

142

150

200

250

300

350

400

450

500

550Australia Brazil

China produced 120.9mn tonnes of iron ore in Mar 2014, up 7.8% yoy Iron ore production in Australia/ Brazil for CY13 stood at 530/ 398mntonnes, up 1.0%/ 6.1% on yoy basis respectively

Source: Bloomberg, JPC, WSA, CISA, PhillipCapital India Research

– 12 of 33 –

12 May 2014 / INDIA EQUITY RESEARCH / METALS – MONTHLY WRAP UP

Global Steel Inventory excl EU (mn tonnes) China Steel Inventory (mn tonnes)

29 30 31 32 33 34 35 36 37 38 39 40

500600700800900

100011001200130014001500

Longs Flats

World steel inventory fell by 6.2% (~2.2mn tonnes) sequentially to 33.9mn tonnes in Apr 2014 led by fall in inventory in China

Flat/ Long inventory fell by 9.8%/ 13.7% sequentially in Apr 2014

US Service Centre Inventory Canada Service Centre Inventory (mn tonnes)

2

2.2

2.4

2.6

2.8

3

3.2

3.4

3.6

5

5.5

6

6.5

7

7.5

8

8.5

9

US Steel products inventory (mn tonnes)US Steel products months of inventory

1,200 1,250 1,300 1,350 1,400 1,450 1,500 1,550 1,600 1,650 1,700 1,750 1,800

US steel products inventory fell to 2.3 months in Mar 2014 from 2.5months

Canada service centre inventory fell (‐1.1% mom) in Feb 2014 aftergaining from past 3 months

Japan Steel Inventory (mn tonnes) China Iron Ore Inventory at Ports (mn tonnes)

7.9

8.0

8.1

8.2

8.3

8.4

8.5

65707580859095

100105110

Japan steel inventory gained 2.7% sequentially to 8.4mn tonnes in Jan 2014

Iron ore inventory at port stands at 105.2mn tonnes, up 1.4% mom.This is the highest inventory ever reported by China

Source: Bloomberg, PhillipCapital India Research

– 13 of 33 –

12 May 2014 / INDIA EQUITY RESEARCH / METALS – MONTHLY WRAP UP

Trade Data

India Steel Consumption (mn tonnes) India Steel: Imports – Exports (000 tonnes)

5.0

6.0

7.0

8.0

9.0

10.0

11.0 Apparent Real

250

350

450

550

650

750

850 Import Export

Apparent/ Real consumption for Apr 2014 stood at 6.9/ 5.8mn tonnes,up 11.4%/ 4.0% yoy and down 9.1%/ 12.6% sequentially

Import/ Export for Apr 2014 stood at 494/ 461kt, moved by +41.1%/+1.3% yoy and +11.0%/ ‐15.4% sequentially

China Net Steel Exports (mn tonnes) EU Apparent Steel Consumption (mn tonnes)

3.33.53.84.04.34.54.85.05.35.55.8

10.5

11.0

11.5

12.0

12.5

13.0

13.5

14.0

14.5

Net steel exports from China in Mar 2014 stood at 5.51mn tonnes, up35.9% yoy and 44.1% sequentially

Apparent steel consumption in EU for Mar 2014 stood at 14.3mntonnes, up 7.6% and 11.4% on yoy and mom basis respectively

Europe Flat Products Net Imports/(Exports) (000 tonnes) Europe Long Products Net Exports (000 tonnes)

(700)(600)(500)(400)(300)(200)(100)

‐100 200

450500550600650700750800850900

Flat steel net exports from Europe stood at 384KT in Nov 2013 against 634KT in Nov 2012

Net steel exports of long products stood at 487KT in Nov 2013, down36.1% and 13.0% on yoy and mom basis respectively

Source: Bloomberg, JPC, PhillipCapital India Research

– 14 of 33 –

12 May 2014 / INDIA EQUITY RESEARCH / METALS – MONTHLY WRAP UP

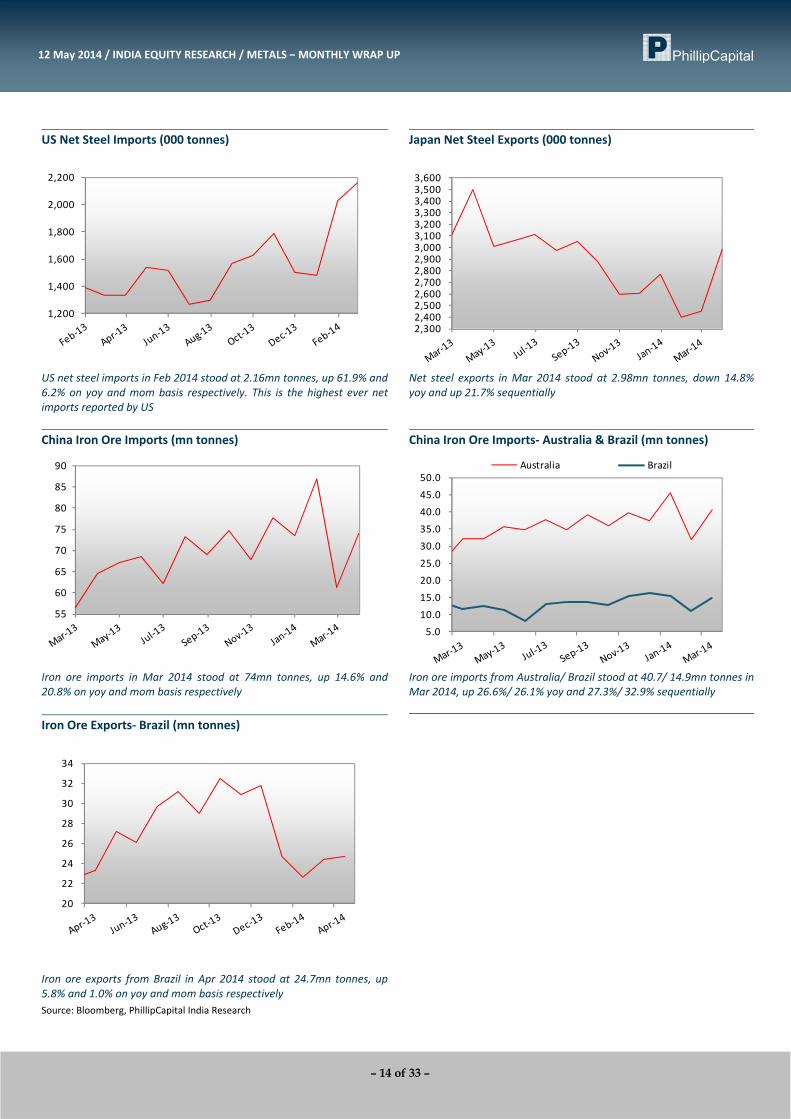

US Net Steel Imports (000 tonnes) Japan Net Steel Exports (000 tonnes)

1,200

1,400

1,600

1,800

2,000

2,200

2,300 2,400 2,500 2,600 2,700 2,800 2,900 3,000 3,100 3,200 3,300 3,400 3,500 3,600

US net steel imports in Feb 2014 stood at 2.16mn tonnes, up 61.9% and 6.2% on yoy and mom basis respectively. This is the highest ever netimports reported by US

Net steel exports in Mar 2014 stood at 2.98mn tonnes, down 14.8% yoy and up 21.7% sequentially

China Iron Ore Imports (mn tonnes) China Iron Ore Imports‐ Australia & Brazil (mn tonnes)

55

60

65

70

75

80

85

90

5.0 10.0

15.0

20.0 25.0

30.0 35.0

40.0 45.0

50.0 Australia Brazil

Iron ore imports in Mar 2014 stood at 74mn tonnes, up 14.6% and20.8% on yoy and mom basis respectively

Iron ore imports from Australia/ Brazil stood at 40.7/ 14.9mn tonnes in Mar 2014, up 26.6%/ 26.1% yoy and 27.3%/ 32.9% sequentially

Iron Ore Exports‐ Brazil (mn tonnes)

20

22

24

26

28

30

32

34

Iron ore exports from Brazil in Apr 2014 stood at 24.7mn tonnes, up 5.8% and 1.0% on yoy and mom basis respectively Source: Bloomberg, PhillipCapital India Research

– 15 of 33 –

12 May 2014 / INDIA EQUITY RESEARCH / METALS – MONTHLY WRAP UP

Non Ferrous: Aluminium

LME Aluminium (US$ / tonne) Shanghai Aluminium (Yuan / tonne)

1,600

1,650

1,700

1,750

1,800

1,850

1,900

1,950

2,000

12000

12500

13000

13500

14000

14500

15000

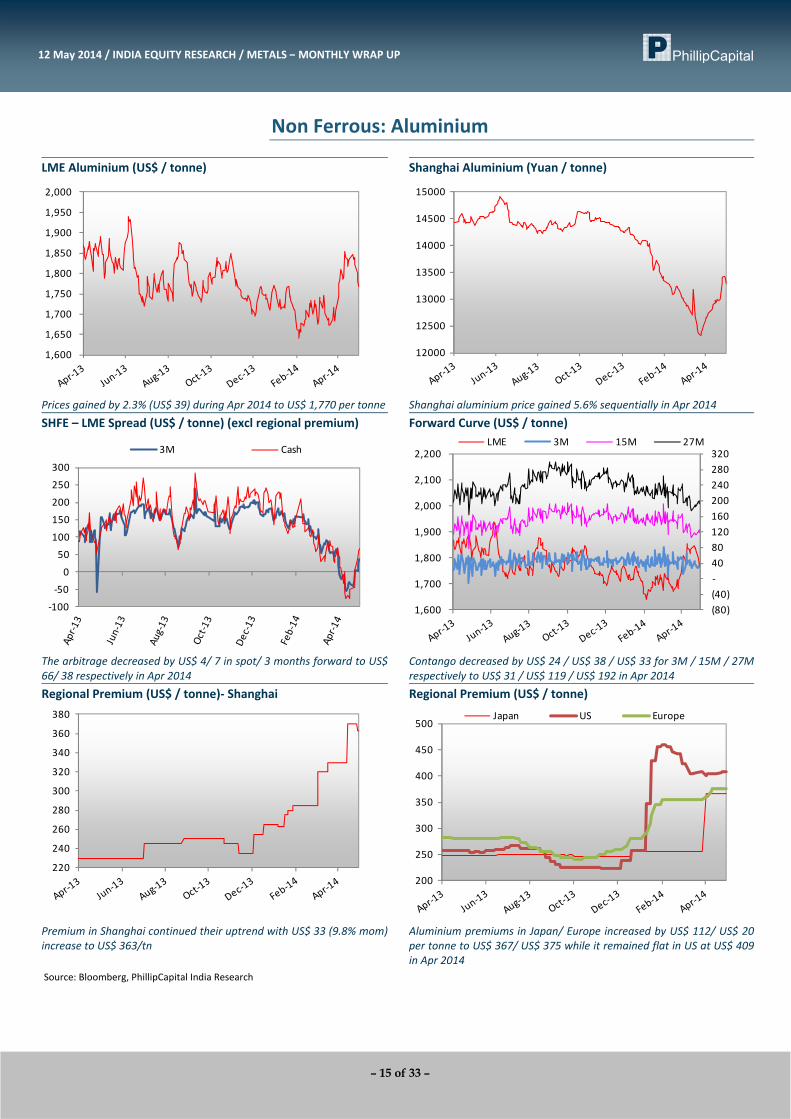

Prices gained by 2.3% (US$ 39) during Apr 2014 to US$ 1,770 per tonne Shanghai aluminium price gained 5.6% sequentially in Apr 2014 SHFE – LME Spread (US$ / tonne) (excl regional premium) Forward Curve (US$ / tonne)

‐100

‐50

0

50

100

150

200

250

300

3M Cash

(80)(40)‐40 80 120 160 200 240 280 320

1,600

1,700

1,800

1,900

2,000

2,100

2,200 LME 3M 15M 27M

The arbitrage decreased by US$ 4/ 7 in spot/ 3 months forward to US$66/ 38 respectively in Apr 2014

Contango decreased by US$ 24 / US$ 38 / US$ 33 for 3M / 15M / 27M respectively to US$ 31 / US$ 119 / US$ 192 in Apr 2014

Regional Premium (US$ / tonne)‐ Shanghai Regional Premium (US$ / tonne)

220

240

260

280

300

320

340

360

380

200

250

300

350

400

450

500Japan US Europe

Premium in Shanghai continued their uptrend with US$ 33 (9.8% mom)increase to US$ 363/tn

Aluminium premiums in Japan/ Europe increased by US$ 112/ US$ 20 per tonne to US$ 367/ US$ 375 while it remained flat in US at US$ 409 in Apr 2014

Source: Bloomberg, PhillipCapital India Research

– 16 of 33 –

12 May 2014 / INDIA EQUITY RESEARCH / METALS – MONTHLY WRAP UP

Warehousing Profit / Loss (US$ / tonne) LME / Used Beverages Cans spread – N America (US$ / tonne)

(60)

(40)

(20)

‐

20

40

60

80

100

27M 15M

‐

50

100

150

200

250

300

350

1,450

1,550

1,650

1,750

1,850

1,950

2,050 LME aluminium UBC Spread (RHS)

Profit in financing deals for 15M/ 27M moved by US$ +3/‐6 per tonneto US$ 35/14 per tonne in Apr 2014

LME Aluminium / UBC spread further decreased by US$ 17 (‐32.0% mom) to US$ 36/tn in Feb 2014

Scrap – North America (US$ / tonne) Aluminium Scrap – Italy (Euro / tonne)

64

66

68

70

72

74

76

78

80

Used Beverage Cans Mixed low copper clipsOld Sheet Old CastTurnings (Clean and dry)

1,160 1,180 1,200 1,220 1,240 1,260 1,280 1,300 1,320 1,340 1,360 1,380

Scrap prices in North America increased across products between 2.0% to 5.0% sequentially in Feb 2014

Aluminium scrap prices recovered its last month loss with prices increasing by 15 euros (+1.2% mom) to 1,210 euros in Apr 2014

Aluminium Scrap – US Foundry Ingot (US$ / lb) Aluminium Scrap – UK Foundary Ingot (GBP / tonne)

1.01

1.02

1.03

1.04

1.05

1.06

1.07

1.08

875 900 925 950 975

1,000 1,025 1,050 1,075 1,100 1,125 1,150

Aluminium scrap prices fell marginally (‐0.9% mom) in Apr 2014 Aluminium scrap prices gained 20 GBP/ tn (+2.2% mom) sequentially in Apr 2014

Source: Bloomberg, USGS, PhillipCapital India Research

– 17 of 33 –

12 May 2014 / INDIA EQUITY RESEARCH / METALS – MONTHLY WRAP UP

Alumina Prices: Australia FOB (US$ / tonne) Alumina Prices: China CFR (US$ / tonne)

310

315

320

325

330

335

340

365

375

385

395

405

415

425

435

Alumina FOB price stood at US$ 325/tn, up 2.4% mom. It is in line withjump in LME aluminium price

China alumina prices fell marginally by 0.8% to US$ 375/tn in Apr 2014

Alumina as a % of LME Caustic Soda – India (Rs / tonne)

16.5%

17.0%

17.5%

18.0%

18.5%

19.0%

19.5%

20.0%

20.5%

28,500

30,500

32,500

34,500

36,500

38,500

40,500

Alumina price as a % of LME decreased to 17.8% in Apr 2014 against18.5% in Mar 2014

Caustic soda price is down 1.0% sequentially to Rs 39,100/tn in Apr2014

Caustic Soda – US (US$ / tonne)

630

635

640

645

650

655

660

665

Caustic Soda prices stayed flat at US$ 639/tn since Sep 2013

Source: Bloomberg, PhillipCapital India Research

– 18 of 33 –

12 May 2014 / INDIA EQUITY RESEARCH / METALS – MONTHLY WRAP UP

Aluminium Production‐ World (000 tonnes) Regionwise Aluminium Production (000 tonnes)

3,900 3,950 4,000 4,050 4,100 4,150 4,200 4,250 4,300 4,350

‐200 400 600 800

1,000 1,200 1,400 1,600 1,800 2,000

China AmericaEurope Asia excl ChinaAfrica & Oceania Others

World aluminium production for Mar 2014 stood at 4.33mn tonnes, up5.0% and 9.2% on yoy and mom basis respectively

Excluding China, yoy production growth is down by 1.8% yoy and up 10.0% sequentially. Proudction in China for Mar 2014 stood at 1.98mn tonnes, up 14.4% and 8.2% on yoy and mom basis respectively

Companywise Aluminium Production (tonnes) Aluminium Consumption‐ World (000 tonnes)

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000 Hindalco Nalco Balco VAL

3650

3700

3750

3800

3850

3900

3950

4000

4050

4100

World consumption in Feb 2014 stood at 3.97mn tonnes, up 6.5% yoy and down 3.0% mom

Regionwise Aluminium Consumption (000 tonnes) Alumina Production (000 tonnes)

0500

1,0001,5002,0002,5003,0003,5004,0004,500

World USA Europe China Others

‐

1,000

2,000

3,000

4,000

5,000

East & Central Europe ChinaSouth America EuropeOthers

Except USA (+7.6% mom), all other regions have reported fall inconsumption sequentially in Feb 2014. All regions have reportedgrowth in aluminium consumption (led by Europe) on yoy basis

World alumina production for Mar 2014 stands at 9.34mn tonnes, up 6.4% and 9.1% on yoy and mom basis respectively

Source: Bloomberg, IAI, Ministry of Mines, PhillipCapital India Research

– 19 of 33 –

12 May 2014 / INDIA EQUITY RESEARCH / METALS – MONTHLY WRAP UP

World‐ Bauxite Production (mn tonnes) Regionwise‐ Bauxite Production (mn tonnes)

20.0 20.5 21.0 21.5 22.0 22.5 23.0 23.5 24.0 24.5

‐1.0 2.0 3.0 4.0 5.0 6.0 7.0 8.0

China Indonesia AustraliaBrazil India Others

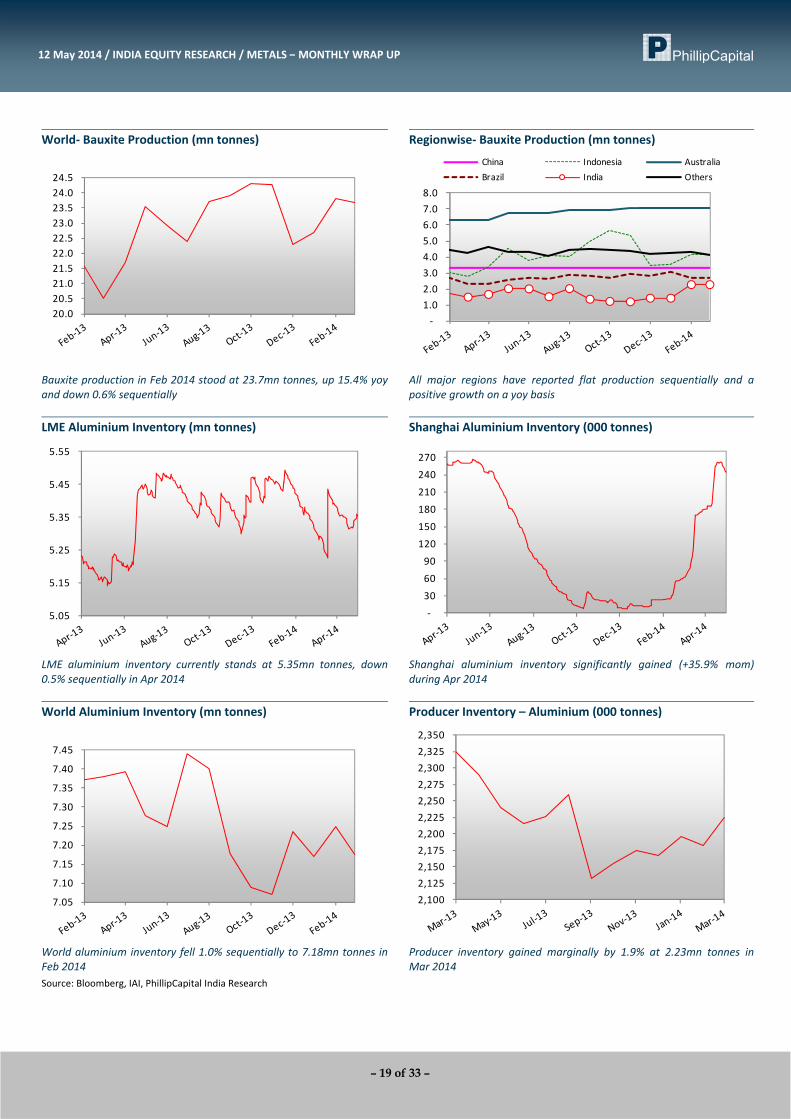

Bauxite production in Feb 2014 stood at 23.7mn tonnes, up 15.4% yoy and down 0.6% sequentially

All major regions have reported flat production sequentially and a positive growth on a yoy basis

LME Aluminium Inventory (mn tonnes) Shanghai Aluminium Inventory (000 tonnes)

5.05

5.15

5.25

5.35

5.45

5.55

‐

30

60

90

120

150

180

210

240

270

LME aluminium inventory currently stands at 5.35mn tonnes, down 0.5% sequentially in Apr 2014

Shanghai aluminium inventory significantly gained (+35.9% mom)during Apr 2014

World Aluminium Inventory (mn tonnes) Producer Inventory – Aluminium (000 tonnes)

7.05

7.10

7.15

7.20

7.25

7.30

7.35

7.40

7.45

2,100 2,125 2,150 2,175 2,200 2,225 2,250 2,275 2,300 2,325 2,350

World aluminium inventory fell 1.0% sequentially to 7.18mn tonnes inFeb 2014

Producer inventory gained marginally by 1.9% at 2.23mn tonnes in Mar 2014

Source: Bloomberg, IAI, PhillipCapital India Research

– 20 of 33 –

12 May 2014 / INDIA EQUITY RESEARCH / METALS – MONTHLY WRAP UP

Zinc

LME Zinc (US$ / tonne) Shanghai Zinc (Yuan / tonne)

1750

1800

1850

1900

1950

2000

2050

2100

2150

2200

14600

14800

15000

15200

15400

15600

15800

16000

Zinc prices reported highest gain across base metals with 3.6% (US$ 70)jump during Apr 2014 to US$ 2,040 per tonne

Shanghai Zinc prices gain 3.0% mom in Apr 2014

SHFE – LME Spread (US$ / tonne) (excl regional premium) Forward Curve (US$ / tonne)

0

50

100

150

200

250

3003M Cash

‐60‐300306090120150180210

1750180018501900195020002050210021502200

LME 3M 15M 27M

The arbitrage decreased by US$ 20/ 37 in spot/ 3 months forward toUS$ 50/ 68 respectively in Apr 2014

Zinc prices for 3M moved back into a backwardation of US$ 0.25 while contango for 15M / 27M fell by US$ 38.5/ US$ 59.5 and stood at US$ 26/ US$ 35 respectively

Regional Premium (US$ / tonne)

100

120

140

160

180

200

220Shanghai Singapore

Premium in Singapore/ Shanghai increased by US$ 20/2.5 per tonne toUS$ 185/152.5 in Apr 2014

Source: Bloomberg, PhillipCapital India Research

– 21 of 33 –

12 May 2014 / INDIA EQUITY RESEARCH / METALS – MONTHLY WRAP UP

Zinc Production (000 tonnes) Company wise production – India (tonnes)

950

1,000

1,050

1,100

1,150

1,200

1,250 Metal production Mine production

500 750 1,000 1,250 1,500 1,750 2,000 2,250 2,500 2,750 3,000

50,000

55,000

60,000

65,000

70,000

75,000

80,000

85,000

90,000 Hindustan Zinc Binani (RHS)

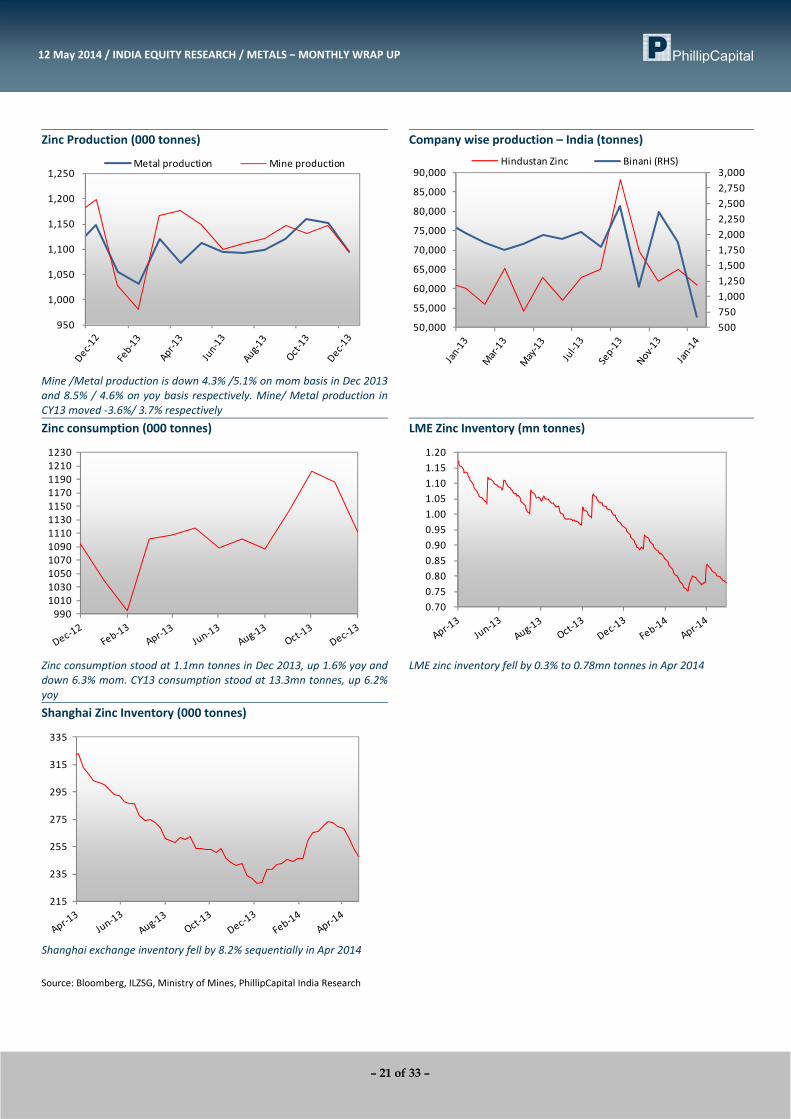

Mine /Metal production is down 4.3% /5.1% on mom basis in Dec 2013 and 8.5% / 4.6% on yoy basis respectively. Mine/ Metal production inCY13 moved ‐3.6%/ 3.7% respectively

Zinc consumption (000 tonnes) LME Zinc Inventory (mn tonnes)

990101010301050107010901110113011501170119012101230

0.70 0.75 0.80 0.85 0.90 0.95 1.00 1.05 1.10 1.15 1.20

Zinc consumption stood at 1.1mn tonnes in Dec 2013, up 1.6% yoy and down 6.3% mom. CY13 consumption stood at 13.3mn tonnes, up 6.2%yoy

LME zinc inventory fell by 0.3% to 0.78mn tonnes in Apr 2014

Shanghai Zinc Inventory (000 tonnes)

215

235

255

275

295

315

335

Shanghai exchange inventory fell by 8.2% sequentially in Apr 2014 Source: Bloomberg, ILZSG, Ministry of Mines, PhillipCapital India Research

– 22 of 33 –

12 May 2014 / INDIA EQUITY RESEARCH / METALS – MONTHLY WRAP UP

Lead

LME Lead (US$ / tonne) Shanghai Lead (Yuan / tonne)

1900

1950

2000

2050

2100

2150

2200

2250

2300

13500

13750

14000

14250

14500

14750

15000

15250

15500

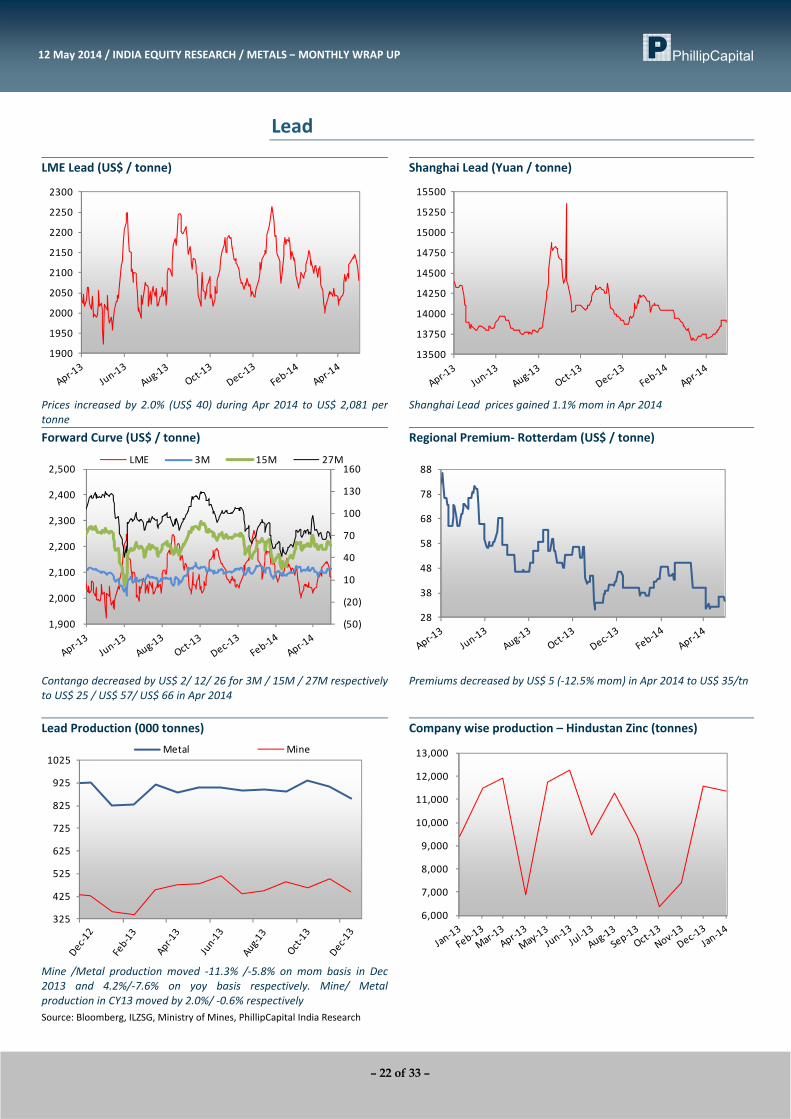

Prices increased by 2.0% (US$ 40) during Apr 2014 to US$ 2,081 per tonne

Shanghai Lead prices gained 1.1% mom in Apr 2014

Forward Curve (US$ / tonne) Regional Premium‐ Rotterdam (US$ / tonne)

(50)

(20)

10

40

70

100

130

160

1,900

2,000

2,100

2,200

2,300

2,400

2,500 LME 3M 15M 27M

28

38

48

58

68

78

88

Contango decreased by US$ 2/ 12/ 26 for 3M / 15M / 27M respectivelyto US$ 25 / US$ 57/ US$ 66 in Apr 2014

Premiums decreased by US$ 5 (‐12.5% mom) in Apr 2014 to US$ 35/tn

Lead Production (000 tonnes) Company wise production – Hindustan Zinc (tonnes)

325

425

525

625

725

825

925

1025Metal Mine

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

Mine /Metal production moved ‐11.3% /‐5.8% on mom basis in Dec2013 and 4.2%/‐7.6% on yoy basis respectively. Mine/ Metalproduction in CY13 moved by 2.0%/ ‐0.6% respectively

Source: Bloomberg, ILZSG, Ministry of Mines, PhillipCapital India Research

– 23 of 33 –

12 May 2014 / INDIA EQUITY RESEARCH / METALS – MONTHLY WRAP UP

Lead Consumption (000 tonnes) LME Lead Inventory (000 tonnes)

800

825

850

875

900

925

950

175

195

215

235

255

275

Lead consumption stood at 0.84mn tonnes in Dec 2013, down 10.3%and 5.9% on yoy and mom basis respectively. CY13 consumption stoodat 10.7mn tonnes, flat yoy

LME lead inventory fell by 3.3% sequentially in Apr 2014 to 0.194mntonnes

Shanghai Lead Inventory (000 tonnes)

65

75

85

95

105

115

125

135

145

Shanghai lead inventory fell by 4.6% sequentially in Apr 2014

Source: Bloomberg, ILZSG, PhillipCapital India Research

– 24 of 33 –

12 May 2014 / INDIA EQUITY RESEARCH / METALS – MONTHLY WRAP UP

Copper

LME Copper (US$ / tonne) Shanghai Copper (Yuan / tonne)

6300

6500

6700

6900

7100

7300

7500

7700

44,000

46,000

48,000

50,000

52,000

54,000

56,000

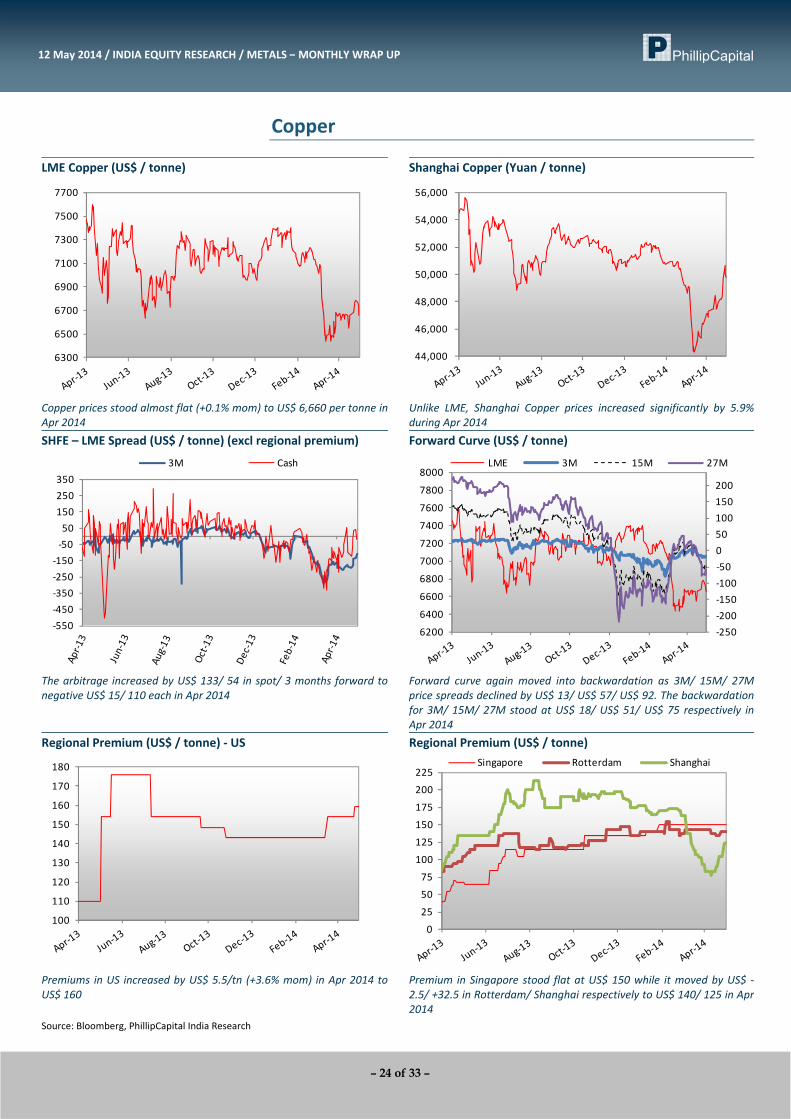

Copper prices stood almost flat (+0.1% mom) to US$ 6,660 per tonne in Apr 2014

Unlike LME, Shanghai Copper prices increased significantly by 5.9% during Apr 2014

SHFE – LME Spread (US$ / tonne) (excl regional premium) Forward Curve (US$ / tonne)

‐550‐450‐350‐250‐150‐5050

150250350

3M Cash

‐250‐200‐150‐100‐50050100150200

6200

6400

6600

6800

7000

7200

7400

7600

7800

8000LME 3M 15M 27M

The arbitrage increased by US$ 133/ 54 in spot/ 3 months forward to negative US$ 15/ 110 each in Apr 2014

Forward curve again moved into backwardation as 3M/ 15M/ 27M price spreads declined by US$ 13/ US$ 57/ US$ 92. The backwardation for 3M/ 15M/ 27M stood at US$ 18/ US$ 51/ US$ 75 respectively in Apr 2014

Regional Premium (US$ / tonne) ‐ US Regional Premium (US$ / tonne)

100

110

120

130

140

150

160

170

180

0

25

50

75

100

125

150

175

200

225Singapore Rotterdam Shanghai

Premiums in US increased by US$ 5.5/tn (+3.6% mom) in Apr 2014 toUS$ 160

Premium in Singapore stood flat at US$ 150 while it moved by US$ ‐2.5/ +32.5 in Rotterdam/ Shanghai respectively to US$ 140/ 125 in Apr2014

Source: Bloomberg, PhillipCapital India Research

– 25 of 33 –

12 May 2014 / INDIA EQUITY RESEARCH / METALS – MONTHLY WRAP UP

Copper Scrap (Euro / tonne)‐ France Copper Scrap China (US$ / tonne)

4,200

4,400

4,600

4,800

5,000

5,200

5,400

5,600

3,000

3,050

3,100

3,150

3,200

3,250

3,300

3,350

Copper scrap prices in France gained 3.2% mom to 4,515 euros in Apr2014

Scrap prices in China increased marginally (+0.5% mom) to US$ 3,202/tn in Mar 2014

Copper Scrap Prices – Germany (Euro / tonne) Copper Mine Production (000 tonnes)

4,500

4,700

4,900

5,100

5,300

5,500

5,700

5,900

1,300

1,350

1,400

1,450

1,500

1,550

1,600

1,650

Copper scrap prices in Germany gained 2.4% mom to US$ 4,770/tn during Apr 2014

World mine production stood at 1.54mn tonnes, up 5.0% yoy and down5.2% sequentially

Copper Refined Production (000 tonnes) Companywise Production – India (tonnes)

200

450

700

950

1,200

1,450

1,700

1,950

Primary Secondary Total

‐

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000 Hindalco Sterlite Hindustan Copper

Refined production stood at 1.81mn tonnes, up 1.9% yoy and down1.8% sequentially

Source: Bloomberg, ICSG, PhillipCapital India Research

– 26 of 33 –

12 May 2014 / INDIA EQUITY RESEARCH / METALS – MONTHLY WRAP UP

Copper Consumption (000 tonnes) LME Copper Inventory (000 tonnes)

1,550

1,600

1,650

1,700

1,750

1,800

1,850

1,900

1,950

2,000

200250300350400450500550600650700

World copper consumption for Jan 2014 stands at 1.87mn tonnes, up9.6% on yoy and mom basis respectively each

LME copper inventory has seen highest fall across base metals with12% decline to 0.233mn tonnes in Apr 2014. It has corrected by 61.9% since July 2013

Shanghai Copper Inventory (000 tonnes) World Refined Copper Stocks (mn tonnes)

0

10

20

30

40

50

60

70

80

0.8

0.9

1.0

1.1

1.2

1.3

1.4

Like LME, Shanghai copper inventory has seen highest fall across basemetals with 84.8% fall to 6KT in Apr 2014

World refined copper stocks currently stands at 0.88mn tonnes, up 0.9% sequentially in Feb 2014

Source: Bloomberg, ICSG, PhillipCapital India Research

– 27 of 33 –

12 May 2014 / INDIA EQUITY RESEARCH / METALS – MONTHLY WRAP UP

Trade data ‐ Aluminium

China Aluminium Net Exports (000 tonnes) China Alumina Net Imports (000 tonnes)

100

125

150

175

200

225

250

275

300

50

150

250

350

450

550

650

Net Aluminium exports from China in Mar 2014 stood at 0.279mn tonnes, up 35.1% and 157% on yoy and mom basis respectively

Net alumina imports in China stood at 0.37mn tonnes in Mar 2014, up 87.2% yoy and down 19.3% sequentially

Australia Alumina Exports (mn tonnes) China Bauxite imports (mn tonnes)

1.25

1.35

1.45

1.55

1.65

1.75

1.85

1.95

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

Alumina exports from Australia in Dec 2013 stood at 1.83mn tonnes, down 3.9% yoy and up 22.5% sequentially. CY13 alumina exports stoodat 18.53mn tonnes, up 1.4% yoy

China bauxite imports in Mar 2014 stood at 1.83mn tonnes, down 59.9% and 43.3% on yoy and mom basis respectively. Bauxite export ban in Indonesia led to significant decrease in bauxite imports of China

Indonesia Bauxite Exports (mn tonnes) Australia Bauxite Exports (mn tonnes)

1.0

2.0

3.0

4.0

5.0

6.0

7.0

0.75 0.85 0.95 1.05 1.15 1.25 1.35 1.45 1.55 1.65 1.75

Bauxite exports from Indonesia in Nov 2013 stood at 4.1mn tonnes, up80.6% and 2.1% on yoy and mom basis respectively

Bauxite exports from Australia in Dec 2013 stood at 1.34mn tonnes, up 44.5% and 12.9% on yoy and mom basis respectively

Source: Bloomberg, PhillipCapital India Research

– 28 of 33 –

12 May 2014 / INDIA EQUITY RESEARCH / METALS – MONTHLY WRAP UP

Trade data ‐ Zinc & Lead

China Refined Zinc Net Imports (000 tonnes) China Zinc Ore & Concentrates Imports (000 tonnes)

15

25

35

45

55

65

75

85

95

70

90

110

130

150

170

190

210

230

China refined zinc net imports for Feb 2014 stood at 38,766 tonnes, up92.2% yoy and down 57.0% sequentially

China’s imports of zinc ore & concentrates in Mar 2014 stood at 0.154mn tonnes, up 107.9% yoy and down 11.2% sequentially

China Refined Lead Net Exports/ (Imports)‐ (tonnes) China Lead Ore & Concentrates Imports‐ (000 tonnes)

‐

500

1,000

1,500

2,000

2,500

3,000

3,500

75

95

115

135

155

175

195

215

Lead ore & concentrate imports in China stood at 157KT in Mar 2014,up 54.6% and 78.9% on yoy and mom basis respectively

Source: Bloomberg, PhillipCapital India Research

– 29 of 33 –

12 May 2014 / INDIA EQUITY RESEARCH / METALS – MONTHLY WRAP UP

Trade data ‐ Copper

China Refined Copper Net Imports (000 tonnes) China Copper Scrap Imports (000 tonnes)

125150175200225250275300325350375

225

250

275

300

325

350

375

400

425

450

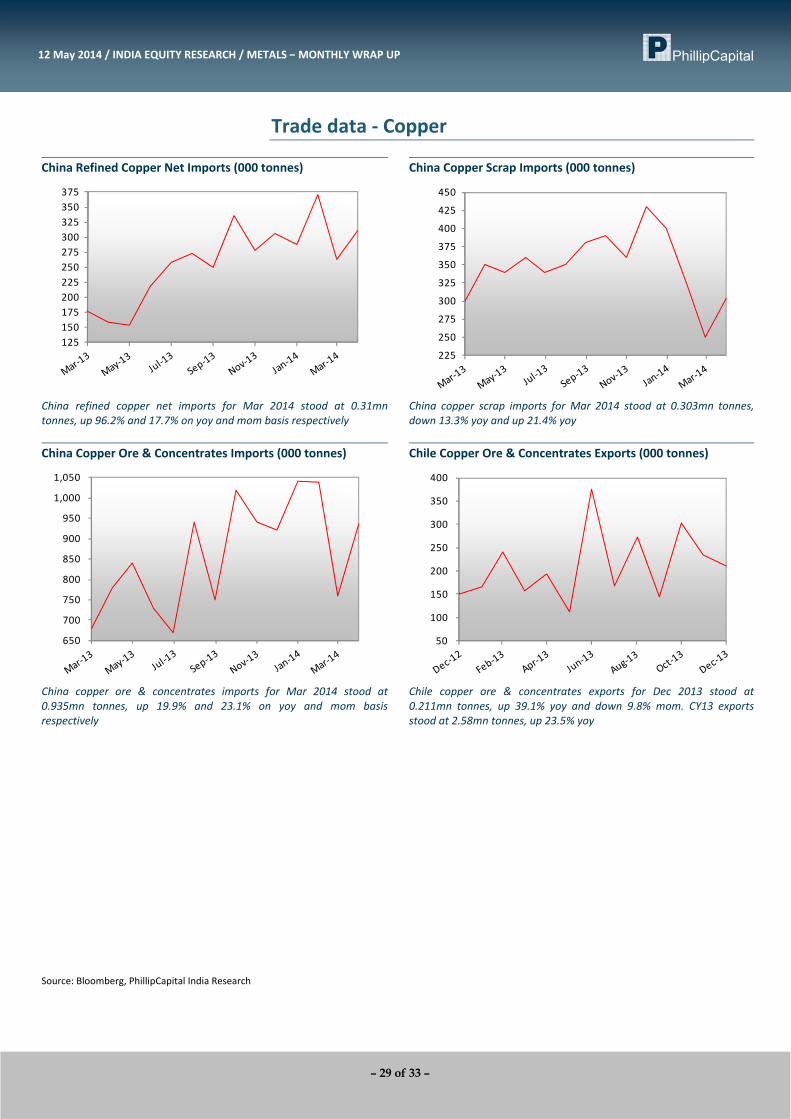

China refined copper net imports for Mar 2014 stood at 0.31mn tonnes, up 96.2% and 17.7% on yoy and mom basis respectively

China copper scrap imports for Mar 2014 stood at 0.303mn tonnes,down 13.3% yoy and up 21.4% yoy

China Copper Ore & Concentrates Imports (000 tonnes) Chile Copper Ore & Concentrates Exports (000 tonnes)

650

700

750

800

850

900

950

1,000

1,050

50

100

150

200

250

300

350

400

China copper ore & concentrates imports for Mar 2014 stood at 0.935mn tonnes, up 19.9% and 23.1% on yoy and mom basisrespectively

Chile copper ore & concentrates exports for Dec 2013 stood at 0.211mn tonnes, up 39.1% yoy and down 9.8% mom. CY13 exports stood at 2.58mn tonnes, up 23.5% yoy

Source: Bloomberg, PhillipCapital India Research

– 30 of 33 –

12 May 2014 / INDIA EQUITY RESEARCH / METALS – MONTHLY WRAP UP

LME Cancelled Warrants

LME Aluminium Cancelled Warrants (mn tonnes) LME Zinc Cancelled Warrants (000 tonnes)

1.8

2.0

2.2

2.4

2.6

2.8

3.0

3.2

100

200

300

400

500

600

700

800

LME Aluminium cancelled warrant currently stands at 2.92mn tonnes, up 12.7% mom

LME zinc cancelled warrant currently stands at 0.14mn tonnes, down17.7% mom

LME Lead Cancelled Warrants (000 tonnes) LME Copper Cancelled Warrants (000 tonnes)

10

30

50

70

90

110

130

150

170

190

‐

50

100

150

200

250

300

350

400

LME lead cancelled warrant declined by 30.5% mom to 21,125 tonnesin Apr 2014

LME copper cancelled warrant currently stands at 0.106mn tonnes, down 9.7% mom

Source: Bloomberg, PhillipCapital India Research

– 31 of 33 –

12 May 2014 / INDIA EQUITY RESEARCH / METALS – MONTHLY WRAP UP

Open Interest ‐ LME

Aluminium (000 contracts) Zinc (000 contracts)

675

725

775

825

875

925

245

255

265

275

285

295

305

315

325

Open interest in Aluminium LME contracts gained 4.7% in Apr 2014 Open interest in Zinc LME contracts gained by 4.9% sequentially in Apr2014

Lead (000 contracts) Copper (000 contracts)

100105110115120125130135140145150

245

255

265

275

285

295

305

315

Open interest in Lead LME contracts fell by 3.7% in Apr 2014 Open interest in Copper LME contracts increased by 5.8% sequentiallyin Apr 2014

Source: Bloomberg, PhillipCapital India Research

– 32 of 33 –

12 May 2014 / INDIA EQUITY RESEARCH / METALS – MONTHLY WRAP UP

Management

(91 22) 2300 2999(91 22) 6667 9735

Research Pharma

Deepak Jain (9122) 6667 9758 Anjali Verma (9122) 6667 9969 Surya Patra (9122) 6667 9768Priya Ranjan (9122) 6667 9965

Engineering, Capital Goods Retail, Real EstateAnkur Sharma (9122) 6667 9759 Abhishek Ranganathan, CFA (9122) 6667 9952

Manish Agarwalla (9122) 6667 9962 Aditya Bahety (9122) 6667 9986 Neha Garg (9122) 6667 9996Sachit Motwani, CFA, FRM (9122) 6667 9953Paresh Jain (9122) 6667 9948 Infrastructure & IT Services Technicals

Vibhor Singhal (9122) 6667 9949 Subodh Gupta, CMT (9122) 6667 9762Varun Vijayan (9122) 6667 9992

Naveen Kulkarni, CFA, FRM (9122) 6667 9947 Production ManagerVivekanand Subbaraman (9122) 6667 9766 Metals Ganesh Deorukhkar (9122) 6667 9966Manish Pushkar, CFA (9122) 6667 9764 Dhawal Doshi (9122) 6667 9769

Dharmesh Shah (9122) 6667 9974 Database ManagerCement Vishal Randive (9122) 6667 9944Vaibhav Agarwal (9122) 6667 9967 Oil&Gas, Agri Inputs

Gauri Anand (9122) 6667 9943 Sr. Manager – Equities SupportDeepak Pareek (9122) 6667 9950 Rosie Ferns (9122) 6667 9971

Sales & Distribution Kinshuk Tiwari (9122) 6667 9946 Sales Trader ExecutionAshvin Patil (9122) 6667 9991 Dilesh Doshi (9122) 6667 9747 Mayur Shah (9122) 6667 9945Shubhangi Agrawal (9122) 6667 9964 Suniil Pandit (9122) 6667 9745Kishor Binwal (9122) 6667 9989Sidharth Agrawal (9122) 6667 9934Dipesh Sohani (9122) 6667 9756

Economics

Consumer, Media, Telecom

Vineet Bhatnagar (Managing Director)Jignesh Shah (Head – Equity Derivatives)

Automobiles

Banking, NBFCs

Contact Information (Regional Member Companies)

SINGAPORE

Phillip Securities Pte Ltd 250 North Bridge Road, #06‐00 Raffles City Tower,

Singapore 179101 Tel : (65) 6533 6001 Fax: (65) 6535 3834

www.phillip.com.sg

MALAYSIA Phillip Capital Management Sdn Bhd B‐3‐6 Block B Level 3, Megan Avenue II,

No. 12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel (60) 3 2162 8841 Fax (60) 3 2166 5099

www.poems.com.my

HONG KONG Phillip Securities (HK) Ltd

11/F United Centre 95 Queensway Hong Kong Tel (852) 2277 6600 Fax: (852) 2868 5307

www.phillip.com.hk

JAPAN Phillip Securities Japan, Ltd

4‐2 Nihonbashi Kabutocho, Chuo‐ku Tokyo 103‐0026

Tel: (81) 3 3666 2101 Fax: (81) 3 3664 0141 www.phillip.co.jp

INDONESIA PT Phillip Securities Indonesia

ANZ Tower Level 23B, Jl Jend Sudirman Kav 33A, Jakarta 10220, Indonesia

Tel (62) 21 5790 0800 Fax: (62) 21 5790 0809 www.phillip.co.id

CHINA Phillip Financial Advisory (Shanghai) Co. Ltd.

No 550 Yan An East Road, Ocean Tower Unit 2318 Shanghai 200 001

Tel (86) 21 5169 9200 Fax: (86) 21 6351 2940 www.phillip.com.cn

THAILAND Phillip Securities (Thailand) Public Co. Ltd.

15th Floor, Vorawat Building, 849 Silom Road, Silom, Bangrak, Bangkok 10500 Thailand

Tel (66) 2 2268 0999 Fax: (66) 2 2268 0921 www.phillip.co.th

FRANCE King & Shaxson Capital Ltd.

3rd Floor, 35 Rue de la Bienfaisance 75008 Paris France

Tel (33) 1 4563 3100 Fax : (33) 1 4563 6017 www.kingandshaxson.com

UNITED KINGDOM King & Shaxson Ltd.

6th Floor, Candlewick House, 120 Cannon Street London, EC4N 6AS

Tel (44) 20 7929 5300 Fax: (44) 20 7283 6835 www.kingandshaxson.com

UNITED STATES Phillip Futures Inc.

141 W Jackson Blvd Ste 3050 The Chicago Board of Trade Building

Chicago, IL 60604 USA Tel (1) 312 356 9000 Fax: (1) 312 356 9005

AUSTRALIA PhillipCapital Australia

Level 37, 530 Collins Street Melbourne, Victoria 3000, Australia

Tel: (61) 3 9629 8380 Fax: (61) 3 9614 8309 www.phillipcapital.com.au

SRI LANKA Asha Phillip Securities Limited

Level 4, Millennium House, 46/58 Navam Mawatha, Colombo 2, Sri Lanka

Tel: (94) 11 2429 100 Fax: (94) 11 2429 199 www.ashaphillip.net/home.htm

INDIA PhillipCapital (India) Private Limited

No. 1, C‐Block, 2nd Floor, Modern Center , Jacob Circle, K. K. Marg, Mahalaxmi Mumbai 400011 Tel: (9122) 2300 2999 Fax: (9122) 6667 9955 www.phillipcapital.in

– 33 of 33 –

12 May 2014 / INDIA EQUITY RESEARCH / METALS – MONTHLY WRAP UP

Disclosures and Disclaimers PhillipCapital (India) Pvt. Ltd. has three independent equity research groups: Institutional Equities, Institutional Equity Derivatives and Private Client Group. This report has been prepared by Institutional Equities Group. The views and opinions expressed in this document may or may not match or may be contrary at times with the views, estimates, rating, target price of the other equity research groups of PhillipCapital (India) Pvt. Ltd. This report is issued by PhillipCapital (India) Pvt. Ltd. which is regulated by SEBI. PhillipCapital (India) Pvt. Ltd. is a subsidiary of Phillip (Mauritius) Pvt. Ltd. References to "PCIPL" in this report shall mean PhillipCapital (India) Pvt. Ltd unless otherwise stated. This report is prepared and distributed by PCIPL for information purposes only and neither the information contained herein nor any opinion expressed should be construed or deemed to be construed as solicitation or as offering advice for the purposes of the purchase or sale of any security, investment or derivatives. The information and opinions contained in the Report were considered by PCIPL to be valid when published. The report also contains information provided to PCIPL by third parties. The source of such information will usually be disclosed in the report. Whilst PCIPL has taken all reasonable steps to ensure that this information is correct, PCIPL does not offer any warranty as to the accuracy or completeness of such information. Any person placing reliance on the report to undertake trading does so entirely at his or her own risk and PCIPL does not accept any liability as a result. Securities and Derivatives markets may be subject to rapid and unexpected price movements and past performance is not necessarily an indication to future performance. This report does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. Investors must undertake independent analysis with their own legal, tax and financial advisors and reach their own regarding the appropriateness of investing in any securities or investment strategies discussed or recommended in this report and should understand that statements regarding future prospects may not be realized. In no circumstances it be used or considered as an offer to sell or a solicitation of any offer to buy or sell the Securities mentioned in it. The information contained in the research reports may have been taken from trade and statistical services and other sources, which we believe are reliable. PhillipCapital (India) Pvt. Ltd. or any of its group/associate/affiliate companies do not guarantee that such information is accurate or complete and it should not be relied upon as such. Any opinions expressed reflect judgments at this date and are subject to change without notice Important: These disclosures and disclaimers must be read in conjunction with the research report of which it forms part. Receipt and use of the research report is subject to all aspects of these disclosures and disclaimers. Additional information about the issuers and securities discussed in this research report is available on request. Certifications: The research analyst(s) who prepared this research report hereby certifies that the views expressed in this research report accurately reflect the research analyst’s personal views about all of the subject issuers and/or securities, that the analyst have no known conflict of interest and no part of the research analyst’s compensation was, is or will be, directly or indirectly, related to the specific views or recommendations contained in this research report. The Research Analyst certifies that he /she or his / her family members does not own the stock(s) covered in this research report. Independence/Conflict: PhillipCapital (India) Pvt. Ltd. has not had an investment banking relationship with, and has not received any compensation for investment banking services from, the subject issuers in the past twelve (12) months, and PhillipCapital (India) Pvt. Ltd does not anticipate receiving or intend to seek compensation for investment banking services from the subject issuers in the next three (3) months. PhillipCapital (India) Pvt. Ltd is not a market maker in the securities mentioned in this research report, although it or its employees, directors, or affiliates may hold either long or short positions in such securities. PhillipCapital (India) Pvt. Ltd may not hold more than 1% of the shares of the company(ies) covered in this report. Suitability and Risks: This research report is for informational purposes only and is not tailored to the specific investment objectives, financial situation or particular requirements of any individual recipient hereof. Certain securities may give rise to substantial risks and may not be suitable for certain investors. Each investor must make its own determination as to the appropriateness of any securities referred to in this research report based upon the legal, tax and accounting considerations applicable to such investor and its own investment objectives or strategy, its financial situation and its investing experience. The value of any security may be positively or adversely affected by changes in foreign exchange or interest rates, as well as by other financial, economic or political factors. Past performance is not necessarily indicative of future performance or results. Sources, Completeness and Accuracy: The material herein is based upon information obtained from sources that PCIPL and the research analyst believe to be reliable, but neither PCIPL nor the research analyst represents or guarantees that the information contained herein is accurate or complete and it should not be relied upon as such. Opinions expressed herein are current opinions as of the date appearing on this material and are subject to change without notice. Furthermore, PCIPL is under no obligation to update or keep the information current. Copyright: The copyright in this research report belongs exclusively to PCIPL. All rights are reserved. Any unauthorized use or disclosure is prohibited. No reprinting or reproduction, in whole or in part, is permitted without the PCIPL’s prior consent, except that a recipient may reprint it for internal circulation only and only if it is reprinted in its entirety. Caution: Risk of loss in trading in can be substantial. You should carefully consider whether trading is appropriate for you in light of your experience, objectives, financial resources and other relevant circumstances. For U.S. persons only: This research report is a product of PhillipCapital (India) Pvt Ltd. which is the employer of the research analyst(s) who has prepared the research report. The research analyst(s) preparing the research report is/are resident outside the United States (U.S.) and are not associated persons of any U.S. regulated broker‐dealer and therefore the analyst(s) is/are not subject to supervision by a U.S. broker‐dealer, and is/are not required to satisfy the regulatory licensing requirements of FINRA or required to otherwise comply with U.S. rules or regulations regarding, among other things, communications with a subject company, public appearances and trading securities held by a research analyst account. This report is intended for distribution by PhillipCapital (India) Pvt Ltd. only to "Major Institutional Investors" as defined by Rule 15a‐6(b)(4) of the U.S. Securities andExchange Act, 1934 (the Exchange Act) and interpretations thereof by U.S. Securities and Exchange Commission (SEC) in reliance on Rule 15a 6(a)(2). If the recipient of this report is not a Major Institutional Investor as specified above, then it should not act upon this report and return the same to the sender. Further, this report may not be copied, duplicated and/or transmitted onward to any U.S. person, which is not the Major Institutional Investor. In reliance on the exemption from registration provided by Rule 15a‐6 of the Exchange Act and interpretations thereof by the SEC in order to conduct certain business with Major Institutional Investors, PhillipCapital (India) Pvt Ltd. has entered into an agreement with a U.S. registered broker‐dealer, Marco Polo Securities Inc. ("Marco Polo").Transactions in securities discussed in this research report should be effected through Marco Polo or another U.S. registered broker dealer. PhillipCapital (India) Pvt. Ltd. Registered office: 2nd Floor, C‐Block, Modern Centre, Mahalaxmi, Mumbai – 400011

Recommended