11PB 1

NOTICE

STATE BANK OF BIKANER & JAIPURHead Office, Tilak Marg, 'C' Scheme,

JAIPUR - 302005

NOTICE OF ANNUAL GENERAL METTING AND BOOK CLOSURE FOR DIVIDEND

lwpuk

LVsV cSad vkWiQ chdkusj ,.M t;iqjiz/ku dk;kZy;] fryd ekxZ] lh&Ldhe] t;iqj&302005

okf"kZd lk/kj.k lHkk ,oa ykHkka'k gsrq jftLVj can dh lwpuk

Place: Jaipur

Date: 29th April, 2016

By ORDER OF THE BOARD

(Jyoti Ghosh)Managing Director

,rn~okjk lwpuk nh tkrh gS fd LVsV cSad vkWiQ chdkusj ,.M t;iqj ds va'k/kjdksa dh 55oha okf"kZd lk/kj.k lHkk] egkjk.kk çrki vkWfMVksfj;e] Hkkjrh; fo|k Hkou] ds-,e-eqa'kh ekxZ] vks-Vh-,l- ds lkeus] t;iqj esa eaxyokj] fnukad 7 twu] 2016 dks çkr% 11-30 cts (Hkkjrh; ekud le;) vk;ksftr dh tk;sxh] ftlesa 1 vçsy 2015 ls 31 ekpZ] 2016 rd dh vof/ ds rqyu&i=k ,oa ykHk vkSj gkfu [kkrk] blh vof/ esa cSad ds dk;Zdj.k ,oa fØ;kdykiksa ij funs'kd e.My ds çfrosnu rFkk rqyu&i=k o ys[kksa ds lEcU/ esa laijh{kdksa ds çfrosnu ij fopkj dj ikfjr fd;k tk;sxkA

cSad ds va'k/kjdksa dk jftLVj 'kfuokj] fnukad 7 ebZ 2016 ls cq/okj] fnukad 11 ebZ 2016 rd (nksuks fnu feykdj)] 31 ekpZ] 2016 dks lekIr foÙkh; o"kZ ds ykHkka'k gsrq va'k/kfj;ks dh ik=krk lqfuf'pr djus gsrq cUn jgsxkA

e.My ds vkns'kkuqlkj

(T;ksfr ?kks"k)izcU/ funs'kd

LFkku% t;iqjfnukad% 29 vizSy] 2016

NOTICE is hereby given that the Fifty- fifth Annual General Meeting of the Shareholders of State Bank of Bikaner and Jaipur will be held at the Maharana Pratap Auditorium, Bharatiya Vidya Bhavan, K. M. Munshi Marg, Opp. O.T.S., Jaipur - 302015 on Tuesday, the 7th June, 2016 at 11.30 a.m. (Indian Standard Time) to discuss and adopt the Balance Sheet and Profit & Loss Account of the Bank, the report of the Board of Directors on the working and activities of the Bank and the Auditors' Report on the Balance Sheet and Accounts for the period 1st April, 2015 to 31st March, 2016.

The register of shareholders of the Bank shall remain closed from 7th May, 2016 (Saturday) to 11th May, 2016 (Wednesday) both the days inclusive , in order to ascertain the entitlement of share holders for the dividend for financial year 2015-16.

222 3

mUufr dk ,d n'kd 2007&2016A Decade of Progress 2007-2016

(` djksM+ esa)(` in Crore)

ladsrdIndicators

iwath ,oa vkjf{kfr;ka Capital & Reserves

dqy O;olk;Total

Business

ifjpkyu ykHk

OperatingProfit

fuoy ykHkNet

Profit

'kk[kkvksadh la[;kNo. of

Branches

izfr deZpkjhvkSlr O;olk;

Average Business per

Employee

izfr deZpkjhfuoy ykHk(` yk[k esa)Net Profit

perEmployee (` in lakh)

ekpZ March 2007 1653.71 49246 679.20@ 305.80 844 3.56 2.57

ekpZ March 2008 1713.21 59427 661.18@ 315.00 850 4.45 2.73

ekpZ March 2009 2046.47 69312 892.84@ 403.45 860 5.55 3.55

ekpZ March 2010 2417.40 81622 903.73@ 455.16 861 6.28 3.96

ekpZ March 2011 2850.81 95596 1140.25@ 550.88 902 7.51 4.84

ekpZ March 2012 4164.88 111558 1489.61@ 652.03 950 8.27 5.42

ekpZ March 2013 6764.13 130590 1712.87@ 730.24 1037 9.00 5.91

ekpZ March 2014 5355.92 139208 1694.66@ 731.69 1148 9.77 5.62

ekpZ March 2015 6012.68 155392 2104.11@ 776.87 1261 11.00 6.02

ekpZ March 2016 6742.80 168748 2305.03@ 850.60 1316 12.15 6.60

@ fuos'kksa ds ewY;kadu ds fy, Hkkjrh; fjt+oZ cSad }kjk tkjh iqujhf{kr fn'kkfunsZ'kksa dks n`f"Vxr djrs gq,AKeeping in view revised RBI guidelines on valuation of investments.

fo"k; & lwph CONTENTS

mYys[kuh; rF; 03Highlights 03funs'kd e.My 04Board of Directors 04funs'kd e.My dk izfrosnu 08Directors' Report 09dkWjiksjsV vfHk'kklu 44Corporate Governance 45cklsy&III izdVhdj.k 74Basel-III Disclosures 75Lok;Ÿk ys[kk ijh{kdksa dk izfrosnu 146Independent Auditors' Report 147rqyu&i= 150Balance Sheet 151ykHk&gkfu [kkrk 152Profit & Loss Account 152rqyu&i= ,oa ykHk gkfu [kkrs dh vuqlwfp;ka 154Schedules of Balance Sheet and Profit & Loss Account 154egRoiw.kZ ys[kk uhfr;ka 166Principal Accounting Policies 167[kkrksa ij fVIif.k;ka 184Notes on Accounts 185

332 3

mYys[kuh; rF;

HIGHLIGHTS(` djksM+ esa) (` in Crore)

2014-15 2015-16

dqy O;olk; vUrj cSad tekvksa lfgr Total Business including inter-bank deposits 155392 168748

tekjkf'k;k¡ Deposits 84239 94005

dqy vfxze Total Advances 71153 74743

vfxze (fuoy) Advances (Net) 69548 72927

fuos'k (fuoy) Investments (Net) 22465 24782

fuoy ykHk Net Profit 776.87 850.60

tekvksa dh ykxr Cost of Deposits 7.01% 6.76%

vfxzeksa ij vk; Yield on Advances 10.98% 10.70%

fuoy C;kt vUrj Net Interest Margin 3.37% 3.47%

iznRr iwath ,oa vkjf{kfr;ka Paid-up Capital & Reserves 6012.68 6742.80

izfr va'k vk; (` esa) Earning per Share (in `) 110.98 121.51

izfr va'k iqLrd ewY; (` esa) Book Value per Share (in `) 858.95 963.26

iwath i;kZIrrk vuqikr Capital Adequacy Ratiocklsy&II ds vuqlkj As per Basel - II 11.69% 11.33%

cklsy&III ds vuqlkj As per Basel - III 11.57% 11.06%

ykHkka'k nj Dividend Rate 143% 143%

ldy xSj&fu"ikfnr vkfLr;ka Gross Non Performing Assets 2945.14 3602.76

ldy xSj&fu"ikfnr vkfLr;ka izfr'kr Gross NPA% 4.14% 4.82%

fuoy xSj&fu"ikfnr vkfLr;ka izfr'kr Net NPA% 2.54% 2.75%

izkFkfedrk izkIr {ks=k dks vfxze Advances to Priority Sectors 27844 29677

Ñf"k {ks=k dks vfxze Advances to Agriculture 11927 13399

lw{e ,oa y?kq m|eksa dks vfxze Advances to Micro and Small Enterprises 10838 11632

fu;kZr foRr Export Finance 2544 2438

'kk[kkvksa dh dqy la[;k Total Number of branches 1261 1316

deZpkfj;ksa dh la[;k Number of Employees 13238 13529

izfr deZpkjh vkSlr O;olk; Average Business per Employee 11.00 12.15

izfr deZpkjh fuoy ykHk (` yk[kksa esa) Net Profit per Employee (` in lakh) 6.02 6.60

444 5

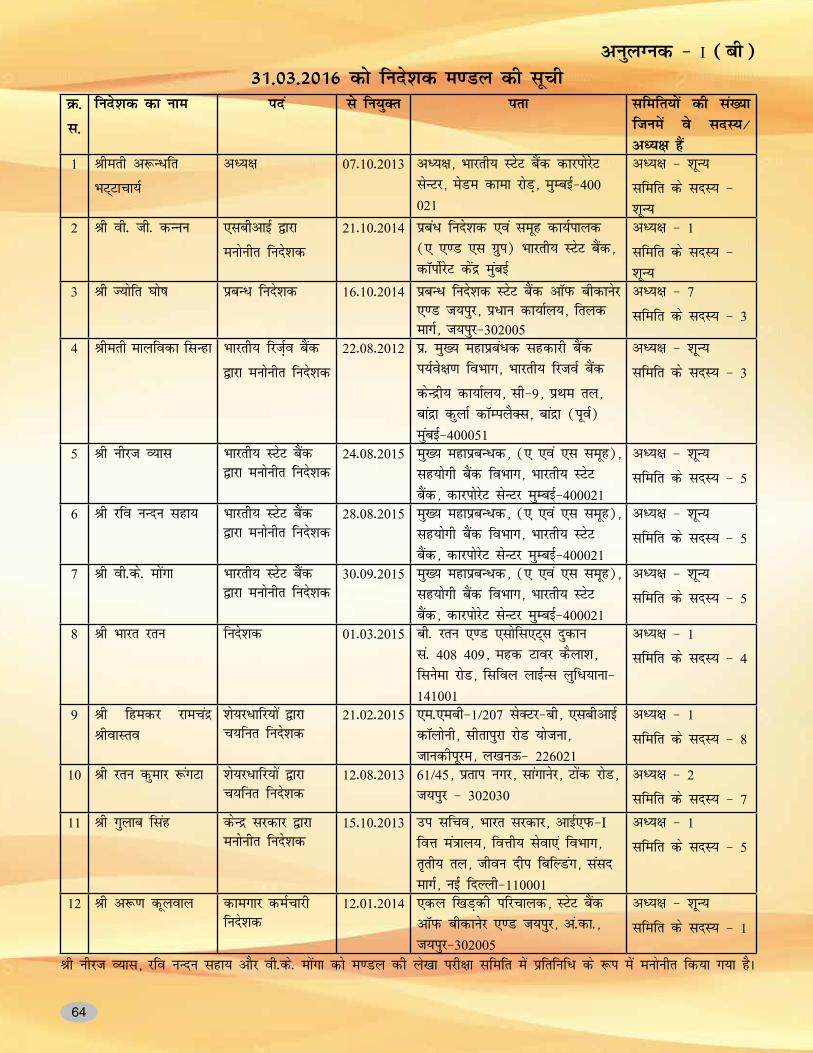

Jherh v:U/kfr HkV~Vkpk;Zv/;{k]Hkkjrh; LVsV cSad] dkjiksjsV lsUVj] esMe dkek jksM] eqEcbZ & 400 021

Jh T;ksfr ?kks"kizcU/k funs'kd]LVsV cSad vkWQ chdkusj ,.M t;iqj] iz/kku dk;kZy;] fryd ekxZ] t;iqj 302005

Jherh ekyfodk fLkUgkiz- eq[; egkizcU/kd] lgdkjh cSad i;Zos{k.k foHkkx] Hkkjrh; fjtoZ cSad] lsUV™y vkWfQl lh&9] izFke ry] ckUnzk dqykZ dkWEiySDl] ckUnzk (bZ)eqEcbZ&400051

Jh oh- th- dUuuizca/k funs'kd ,oa l-dk- (l- ,oa v-)Hkkjrh; LVsV cSad] dkjiksjsV lsUVj]eqEcbZ & 400 021

Jh uhjt O;kleq[; egkizcU/kd] (l-,oa v-)]Hkkjrh; LVsV cSad] dkjiksjsV lsUVj]eqEcbZ & 400 021

Jh jfo uUnu lgk;eq[; egkizcU/kd] (l-,oa v-)]Hkkjrh; LVsV cSad] dkjiksjsV lsUVj]eqEcbZ & 400 021

Jh oh-ds- eksaxkegkizcU/kd] (l-,oa v-)]lg;ksxh cSad foHkkxHkkjrh; LVsV cSad] dkjiksjsV lsUVj]eqEcbZ & 400 021

Jh jru dqekj #axVk61@45] izrki uxjlkaxkusj] Vksad jksMt;iqj & 302030

Jh fgedj jkepanz JhokLro,e-,e-ch- 1@207] lSDVj&ch] ,l-ch-vkbZ- dkWyksuh] lhrkiqj jksM+ ;kstuk]tkudhiqje] y[ku≈&226021

Jh Hkkjr jruch- jru ,.M ,lksfLk;sV~l]nqdku la- 408&409] egd Vkoj]dSyk'k fLkusek jksM+ fLkfoy ykbal]yqf/k;kuk & 141001

Jh xqykc fLkagmi lfpo] Hkkjr ljdkj] vkbZ,Q&Ifor ea=ky;] foŸkh; lsok,a foHkkx](cSafdax izHkkx) rrh; ry] thou nhi fcfYMax] laln ekxZ] ubZ fnYyh&110001

Jh v:.k dwyoky,dy f[kM+dh ifjpkydLVsV cSad vkWQ chdkusj ,.M t;iqjva-dk-] t;iqj&302001

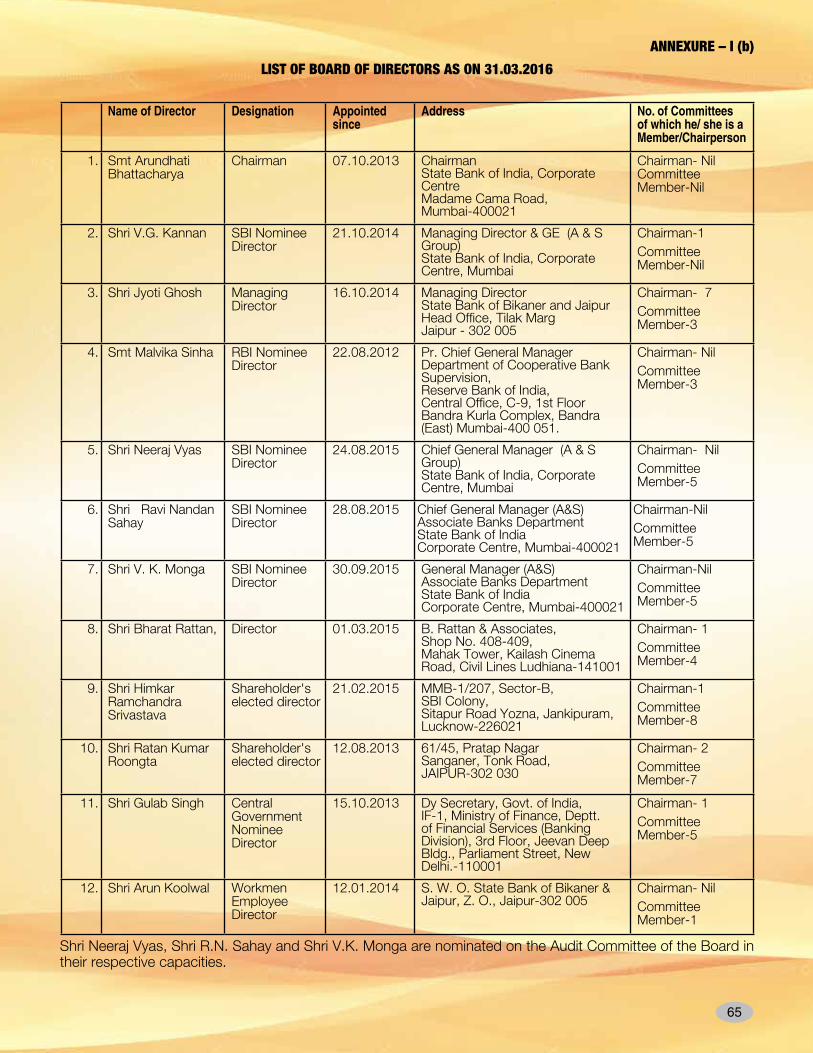

Smt. Arundhati BhattacharyaChairman,State Bank of India, Corporate Centre, Madame Cama Road, Mumbai-400021

Shri Jyoti GhoshManaging Director,State Bank of Bikaner and Jaipur Head Office, Tilak Marg, Jaipur - 302 005

Smt. Malvika SinhaPr. Chief General Manager,Department of Cooperative Bank Supervision, Reserve Bank of India, Central Office, C-9, 1st FloorBandra Kurla Complex, Bandra (E)Mumbai- 400051

Shri V.G. KannanMD & GE (A&S)State Bank of India, Corporate Centre, Mumbai-400021

Shri Neeraj VyasChief General Manager (A&S)State Bank of India, Corporate Centre, Mumbai-400021

Shri Ravi Nandan SahayChief General Manager (A&S)State Bank of India, Corporate Centre, Mumbai-400021

Shri V.K. MongaGeneral Manager (A&S)Associate Banks DepartmentState Bank of India, Corporate Centre, Mumbai-400021

Shri Ratan Kumar Roongta61/45, Pratap NagarSanganer Tonk RoadJaipur-302030

Shri Himkar Ramchandra SrivastavaMMB-1/207, Sector-B, SBI Colony,Sitapur Road Yojna, Jankipuram, Lucknow-226021

Shri Bharat RattanB. Rattan & Associates,Shop No. 408-409,Mahak Tower, Kailash Cinema Road, Civil Lines Ludhiana-141001

Shri Gulab SinghDy. Secretary Govt. of India, IF-I Ministry of Finance Department of Financial Services (Banking Divison) IIIrd Floor, Jeevan Deep Building, Parliament street, New Delhi-110001

Shri Arun KoolwalS.W.O. State Bank of Bikaner &Jaipur, Z.O. Jaipur - 302001

Chairman, ex-officio under clause (a) of sub-section (1) of section 25 of the State Bank of India (Subsidiary Banks) Act, 1959.

Nominated under clause (aa) of sub-section (1) of section 25 of the Act.

Nominated by the Reserve Bank of India under clause (b) of sub-section (1) of section 25 of the Act.

Nominated by the State Bank of India under clause (c) of sub-section (1) of section 25 of the Act.

Nominated by the State Bank of India under clause (c) of sub-section (1) of section 25 of the Act.

Nominated by the State Bank of India under clause (c) of sub-section (1) of section 25 of the Act.

Nominated by the State Bank of India under clause (c) of sub-section (1) of section 25 of the Act.

Elected director under clause (d) of sub-section (1) of section 25 of the Act.

Elected director under clause (d) of sub-section (1) of section 25 of the Act.

Nominated by the State Bank of India under clause (d) of sub-section (1) of section 25 of the Act.

Nominated by the Central Government under clause (e) of sub-section (1) of section 25 of the Act.

Nominated by the Central Government under clause (ca) of sub-section (1) of section 25 read with sub-section (2A) of section 26 of the Act.

Hkkjrh; LVsV cSad (leuq"kaxh cSad) vf/kfu;e 1959 dh /kkjk 25 dh mi/kkjk (1) ds [k.M (,) ds v/khu insu v/;{k

vf/kfu;e dh /kkjk 25 dh mi/kkjk (1) ds [k.M (,,) ds v/khu euksuhr

vf/kfu;e dh /kkjk 25 dh mi/kkjk (1) ds [k.M (ch) ds v/khu Hkkjrh; fjt+oZ cSad }kjk euksuhr

vf/kfu;e dh /kkjk 25 dh mi/kkjk (1) ds [k.M (lh) ds v/khu Hkkjrh; LVsV cSad }kjk euksuhr

vf/kfu;e dh /kkjk 25 dh mi/kkjk (1) ds [k.M (lh) ds v/khu Hkkjrh; LVsV cSad }kjk euksuhr

vf/kfu;e dh /kkjk 25 dh mi/kkjk (1) ds [k.M (lh) ds v/khu Hkkjrh; LVsV cSad }kjk euksuhr

vf/kfu;e dh /kkjk 25 dh mi/kkjk (1) ds [k.M (lh) ds v/khu Hkkjrh; LVsV cSad }kjk euksuhr

vf/kfu;e dh /kkjk 25 dh mi/kkjk (1) ds [k.M (Mh) ds v/khu p;fur funs'kd

vf/kfu;e dh /kkjk 25 dh mi/kkjk (1) ds [k.M (Mh) ds v/khu p;fur funs'kd

vf/kfu;e dh /kkjk 25 dh mi/kkjk (1) ds [k.M (Mh) ds v/khu Hkkjrh; LVsV cSad }kjk euksuhr

vf/kfu;e dh /kkjk 25 dh mi/kkjk (1) ds [k.M (bZ) ds v/khu dsUnzh; ljdkj }kjk euksuhr

vf/kfu;e dh /kkjk 26 dh mi/kkjk (2,) ds lkFk ifBr /kkjk 25 dh mi/kkjk (1) ds [k.M (lh,) ds v/khu dsUnzh; ljdkj }kjk euksuhr

funs'kd e.My (31 ekpZ] 2016 dks) BOARD OF DIRECTORS (AS ON 31ST MARCH, 2016)

554 5

funs'kd e.My (31 ekpZ] 2016 dks)BOARD OF DIRECTORS (AS ON 31st March, 2016)

Jherh v:U/fr HkV~Vkpk;Zvè;{k

Smt. Arundhati Bhattacharya Chairman

Jh uhjt O;klShri Neeraj Vyas

Jherh ekyfodk flUgkSmt. Malvika Sinha

Jh Hkkjr jruShri Bharat Rattan

Jh oh-th- dUuuizcU/ funs'kd ,oa l-dk- (l-,oa-v-)

Shri V. G. KannanManaging Director & GE (A&S)

Jh jfo uUnu lgk;Shri Ravi Nandan Sahay

Jh jru dqekj :axVkShri Ratan Kumar Roongta

Jh oh-ds- eksaxkShri V.K. Monga

Jh T;ksfr ?kks"kizcU/ funs'kd

Shri Jyoti GhoshManaging Director

Jh xqykc flagShri Gulab Singh

Jh fgedj jkepUnz JhokLroShri Himkar Ramchandra Srivastava

Jh v:.k dwyokyShri Arun Koolwal

666 7

fofo/k % cSad ds vk;kstu o miyfC/;ka A kaleidoscope of the Bank’s events and accomplishments

776 7

iqjLdkj ,oa lEeku 2015&16 (AWARDS AND ACCOLADES 2015-16)

nyky LVªhV tuZy }kjk 2016 esa fuos'k gsrq fpfUgr 250 feMdSi LVkWDl esa 5oka loZJs"BA

Identified by Dalal Street Journal as the 5th best among the 250 identified Mid Cap Stocks for investing in 2016.

Hkkjrh; 'kh"kZ 500 daifu;ksa 2015 esa mYys[kA Featured in India’s Top 500 Companies 2015.

fctusl VqMs }kjk ¶loZJs"B feMlkbt Hkkjrh; cSadksa¸ varxZr 5oka LFkkuA Ranked 5th in “Best MID Size Indian Banks” by “Business Today”.

,lkspSe }kjk ¶loZJs"B lkekftd cSad&eè;e cSad oxZ¸ varxZr mifotsrk iqjLdkj ls Jh t;ar flUgk dsaæh; foÙk jkT;ea=kh] Hkkjr ljdkj] }kjk iqjLd`rA

Runner Up as “Best Social Bank” under Medium Bank Class category by ASSOCHAM, awarded by Shri Jayant Sinha, MoS for Finance, Govt. of India.

Hkkjrh; lw{e y?kq ,oa eè;e bdkbZ pSacj (CIMSME) }kjk ¶mHkjrs cSadksa gsrq loZJs"B ,e,l,ebZ cSad vokMZ¸ varxZr mifotsrk iqjLdkj ls Jh ih;w"k xks;y] dsaæh; ÅtkZ] dks;yk] uohu o uohdj.kh; ÅtkZ jkT;ea=kh] Hkkjr ljdkj }kjk iqjLd`rA

Runner Up under “Best MSME Bank Award for Emerging Bank” by Chamber of Indian Micro, Small & Medium Enterprises {CIMSME}, awarded by Shri Piyush Goyal, MoS for Power, Coal, New and Renewable Energy, Govt. of India.

ih,iQvkjMh, }kjk vVy isa'ku ;kstuk f}rh; pj.k ds dk;kZUo;u esa loZJs"B çn'kZu (lkoZtfud {ks=k cSadksa esa r`rh; LFkku) iqjLdkjA

Best Performance Award (3rd prize amongst all PSBs) conferred by PFRDA for implementation of Atal Pension Yojna Phase-II.

8 98 98 9

LVsV cSad vkWiQ chdkusj ,.M t;iqj ds funs'kd eaMy dks cSad ds 31 ekpZ 2016 dks lekIr foÙk o"kZ dk okf"kZd çfrosnu o lkFk gh vadsf{kr rqyu i=k ,oa ykHk gkfu [kkrksa dks çLrqr djrs gq, çlUurk gSA

çca/u fopkj foe'kZ vkSj fo'ys"k.k

vkfFkZd ifjn`';

oSf'od vFkZO;oLFkk

2015 esa oSf'od vkfFkZd xfrfof/ ean cuh jghA oSf'od n`f"Vdks.k eq[;r% phu dh vkfFkZd xfrfof/ esa iquZlarqyu cukus o /heh xfr ls mrkj] ÅtkZ o vU; mRiknksa ds ewY;ksa esa deh rFkk la;qDr jkT; vesfjdk dh ekSfæd uhfr esa /heh xfr ls ykbZ tk jgh dlkoV ls çHkkfor jgk] tcfd vU; dbZ fodflr vFkZO;oLFkkvksa ds dsUæh; cSad fujarj :i ls viuh ekSfæd uhfr dks yphyk cukrs jgsA

varjkZ"Vªh; eqæk dks"k vuqlkj oSf'od o`f¼] tks fd orZeku esa 2015 esa 3-1% vuqekfur gS] 2016 esa 3-4% rFkk 2017 esa 3-6% ç{ksfir gSA oSf'od xfrfof/ esa mBku dh xfr] fo'ks"kdj mHkjrs gq, cktkjksa o fodkl'khy vFkZO;oLFkkvksa esa] /heh gh jguh ç{ksfir gSA fodflr vFkZO;oLFkkvksa esa] mRiknu varj ds vkSj vf/d ladqpu ls ,d ekewyh rFkk vfu;fer lq/kj cus jgus dh vk'kk gSA

mDr ?kVuk,¡ o lekukUrj :i ls phuh vFkZO;oLFkk ds Hkkoh dk;Zfu"iknu dks ysdj cktkj esa O;kIr fparkvksa dk O;kikj lsrqvksa ds ekè;e ls vU; vFkZO;oLFkkvksa ij detksj gks jgs mRikn ewY;ksa] vkfFkZd vkRefo'okl esa fxjkoV o foÙkh; cktkjksa esa O;kid mrkj&p<+ko ds lesfdr :i esa çHkko ifjyf{kr gks jgk gSA

oSf'od Lrj ij fuekZ.k xfrfof/ o O;kikj detksj cus jgs] tks fd oSf'od ekax rFkk fuos'k esa eanh dks n'kkZrs gSaA blds vfrfjDr] vkfFkZd ladV ls tw>rs dbZ mHkjrs gq, ckt+kjkss o fodkl'khy vFkZO;oLFkkvksa esa vk;kr esa fxjkoV oSf'od O;kikj ij cgqr T;knk gkoh cuh gqbZ gSA mHkjrs gq, cktkj rFkk fodkl'khy vFkZO;oLFkkvksa esa o`f¼ 2015 ds 4%] tks fd 2008&09 ds foÙkh; ladV ds ckn ls vc rd dk U;wure Lrj jgk gS] ls c<+dj 2016 esa 4-3% o 2017 esa 4-7% ç{ksfir gSA rFkkfi] fodflr vFkZO;oLFkkvksa esa o`f¼ 2-1% ç{ksfir gS o 2017 esa fLFkj cus jguk laHkkfor gSA

Hkkjrh; vFkZO;oLFkk

ldy ?kjsyw mRikn (thMhih) ds vk/kj o"kZ dh x.kuk gsrq 2004&05 ls 2011&12 esa la'kks/u mijkar Hkkjr ds ldy ?kjsyw mRikn o`f¼ nj] tks vc rd 5% ls Hkh

de cuh jgh Fkh] rsth ls mNy dj 7% ls vf/d (2015&16 dh rhljh frekgh esa 7-3%] tks phu ds 6-8% ls csgrj Fkh) igq¡p x;h o Hkkjrh; vFkZO;oLFkk fo'o dh lokZf/d rsth ls c<+ jgh vFkZO;oLFkk cu x;hA ;|fi orZeku foÙkh; o"kZ esa Hkkjrh; vFkZO;oLFkk dh o`f¼ nj ç{ksfir 7-6% ds lkis{k 7-4% vuqekfur gS] rFkkfi ljdkj us vk'kk O;Dr dh gS fd foÙkh; o"kZ 2015&16 esa ldy ?kjsyw mRikn o`f¼ nj 7-6% gksxhA

fo'o cSad dh Hkfo";okf.k;ksa vuqlkj vkxkeh nks o"kksaZ esa fodkl'khy ns'kksa ds çfr uSjk';iw.kZ n`f"Vdks.k ds chp Hkkjr ,d vk'kkoku o ÅtkZ ls vksrçksr dsaæ jgsxk rFkk 2018 esa bldh o`f¼ nj c<+dj 7-9% gksus dh laHkkouk O;Dr dh gSA cká [krjksa esa deh] ,d lqn`<+ gksrk ?kjsyw O;olk; pØ rFkk ,d lg;ksxiw.kZ] leFkZu;qDr uhfr okrkoj.k ds vkyksd esa Hkkjr dks fu'p; gh ykHk gksxkA

Hkkjrh; LVsV cSad (leuq"kaxh cSad) vf/fu;e]1959 dh /kjk 43(1) ds fuca/uksa ds rgr Hkkjrh; LVsV cSad] Hkkjrh; fjtoZ cSad ,oa Hkkjr ljdkj dks funs'kd eaMy dk çfrosnu

çfrosnu dh vof/ % 01 vçSy] 2015 ls 31 ekpZ] 2016

iz/kuea=kh jkgr dks"k dks lgk;rk Donation to the Prime Minister’s Relief Fund

8 98 98 9

The Board of Directors of State Bank of Bikaner and Jaipur have pleasure in presenting this Annual Report together with the audited Balance Sheet and Profit and Loss Account of the Bank for the year ended 31st March 2016.

MANAGEMENT DISCUSSION AND ANALYSIS ECONOMIC SCENARIOGLOBAL ECONOMY

In 2015, global economic activity remained subdued. Global outlook was mostly influenced by gradual slowdown & rebalancing of economic activity in China, lower prices for energy and other commodities and gradual tightening in monetary policy in the United States, as several other major advanced economies' central banks continued to ease monetary policy.

According to International Monetary Fund (IMF),Global growth, currently estimated at 3.1% in 2015, is projected at 3.4% in 2016 and 3.6% in 2017. The pickup in global activity is projected to be gradual, especially in emerging market and developing economies. In advanced economies, a modest and uneven recovery is expected to continue, with a gradual further narrowing of output gaps.

These developments, together with market concerns about the future performance of the Chinese economy, are having spillovers to other economies through

REPORT OF THE BOARD OF DIRECTORS TO THE STATE BANK OF INDIA, THE RESERVE BANK OF INDIA AND THE GOVERNMENT OF INDIA IN TERMS OF SECTION 43(1) OF THE STATE BANK OF INDIA

(SUBSIDIARY BANKS) ACT 1959

PERIOD COVERED BY REPORT : 1st APRIL, 2015 TO 31st MARCH, 2016

trade channels and weaker commodity prices, as well as through diminishing confidence and increasing volatility in financial markets.

Manufacturing activity and trade remained weak globally, reflecting a subdued global demand and investment. In addition, the decline in imports in a number of emerging markets and developing economies in economic distress is also weighing heavily on global trade. Growth in emerging markets and developing economies is projected to increase from 4% in 2015, the lowest since the 2008-09 financial crisis, to 4.3% in 2016 and 4.7% in 2017, while, the growth in advanced economies is projected to rise to 2.1% and hold steady in 2017.

INDIAN ECONOMY

After revision in base year GDP calculation from 2004-05 to 2011-12, India's GDP jumped from sub 5% growth to 7% plus to become world's fastest growing economy (7.3% in Q3 2015-16, better than China’s 6.8%). The Indian economy in the current fiscal is expected to grow at 7.4%, slightly lower than 7.6% projected. However, government has forecasted that GDP for the fiscal year 2015-16 would grow by 7.6%.

Forecasts from the World Bank showed that India will be a bright spot amid a gloomy outlook for developing countries in the next two years and predicts it will grow

at 7.9% by 2018. India would benefit on the backdrop of a reduction in external vulnerabilities, a strengthening domestic business cycle and a supportive policy environment.

Indian currency saw weakness due to global economic slowdown, weak commodity prices, falling of crude oil prices, contraction of India’s exports and large amount of selling by FIIs in stock market. The year 2015 saw FIIs being net sellers with total pull out amounting to `32985 crore till Feb’16 from equity bringing Sensex down to 17 month low of 22494.61 from its record high of 30000. India’s forex reserves, however, were of some respite as it stood at its all time high range of above $350 bn.

On the inflation front, WPI stayed in the negative for fifteen straight months till Jan’16, though, it is showing an upward movement from all time low of (-) 5.06% in Aug’15 to (-) 0.73% in Jan’16. Combined CPI also, after witnessing an all time low of 3.69% in July’15 increased to 5.69% in Jan’16, due to persistent services inflation, but was comfortably below RBI’s CPI inflation target of 6%.

BANKING INDUSTRY

2015-16 was the continuous second year witnessing low credit offtake and increasing stressed assets for the banks.

One of the main reasons for the muted advances growth was

10 1110 1110 11

oSf'od vkfFkZd eanh] detksj mRikn ewY;ksa] dPps rsy dh dherksa esa fxjkoV] Hkkjr ds fu;kZrksa esa ladqpu rFkk fons'kh laLFkkxr fuos'kdksa }kjk Hkkjh ek=k esa dh x;h fcdokyh ds dkj.k Hkkjrh; eqæk esa Hkh detksjh ns[kh x;hA 2015 us fons'kh laLFkkxr fuos'kdksa dks fuoy foØsrk ds :i esa LFkkfir fd;k ftUgksus iwath ls iQjojh*16 rd `32985 djksM+ dh dqy fcdokyh dj lsalsDl dks mlds 30000 ds fjdkWMZ Lrj ls 17 ekg ds 22494-61 ds fupys Lrj ij yk fn;kA rFkkfi] Hkkjr ds fons'kh eqæk HkaMkj ds 350 vjc MkWyj ls Hkh vf/d ds vius vc rd ds loksZPp Lrj ij LFkk;h cus jgus ls dqN jkgr jghA

eqækLiQhfr ds ekspsZ ij ;|fi Fkksd ewY; lwpdkad yxkrkj 15 ekg tuojh*16 rd ½.kkRed (negative) cuk jgk] rFkkfi vxLr*15 ds (&)5-06% ds vius lcls U;wure Lrj ls Åij dh vksj c<+rs gq, ;g tuojh*16 esa (&)0-73% gks x;kA ;|fi yxkrkj lsok,a eqækLiQhfr ds vkyksd esa lesfdr miHkksDrk ewY; lwpdkad (CPI) Hkh tqykbZ*15 ds 3-69% ds vius vc rd ds U;wure Lrj ls c<+dj tuojh*16 esa 5-69% gks x;k] rFkkfi ;g Hkkjrh; fjtoZ cSad ds tuojh*16 ds CPI eqækLiQhfr y{; 6% ls de jgrs gq, larks"kçn fLFkfr esa FkkA

cSafdax m|ksx

cSadksa ds fy, 2015&16 lk[k dh detksj ekax@ miHkksx o nckoxzLr vkfLr;ksa esa fujarj o`f¼ n'kkZrk yxkrkj nwljk o"kZ jgkA

lk[k dh eançk; o`f¼ dk ,d çeq[k dkj.k fu;kZr oLrqvksa dh ean oSf'od ekax o ifj.kkeLo:i de miHkksx rFkk mRiknu lhek dk de bLrseky gksuk jgkA ean lk[k ifjn`'; dk ,d dkj.k dkiksZjsV bdkb;ksa }kjk okf.kfT;d lk[k i=k cktkj o fons'kh L=kksrksa dks] ftudh njsa Hkkjrh; cSadksa dh vk/kj nj ls de gSa] iwath

vkiwfrZ ds fodYi ds :i es pquuk ekuk tk ldrk gSA dkiksZjsV txr esa pkSrjiQk ncko ds ekStwnk nkSj esa Hkh {ks=kokj lk[k fu{ksi.k vuqlkj fjVsy lk[k esa 15% ls vf/d dh o`f¼ o vis{kkd`r de ,uih, Lrj us cSadksa dks larks"kçn fLFkfr esa cuk, j[kkA

vuqlwfpr okf.kfT;d cSadksa (SCBs) dh ldy tekvksa esa fiNys o"kZ dh 10-7% dh o`f¼ ds lkis{k orZeku o"kZ esa 11-3% dh o`f¼ ns[kh x;h] tcfd vfxzeksa esa ;g o`f¼ xr o"kZ ds 9-6% ds lkis{k 11-5% jghA

pkSrjiQk O;kikj o ekax esa eanh ds dkj.k vkfLr xq.koÙkk dks ysdj fpark,¡ yxkrkj c<+us yxhaA fnlacj*15 dh foÙkh; LFkkf;Ro fjiksVZ (FSR) vuqlkj vf/lwfpr okf.kfT;d cSadksa (SCBs) dh ldy xSj fu"ikfnr vkfLr;ka (Gross NPAs) ekpZ*15 esa 4-6% ls c<+dj flracj*15 esa 5-1% gks x,A nckoxzLr vkfLr;ka (stressed assets) ekpZ*15 ds 11-1% ds Lrj ls c<+dj flracj*15 esa 11-3% gks xbZa] tcfd lkoZtfud {ks=k cSadksa (PSBs) dh nckoxzLr vkfLr;ka flracj*15 esa 14-1% ij igq¡p xbZaA

vkfLr xq.koÙkk ds ekspsZ ij ;g o"kZ vR;f/d pqukSrhiw.kZ cuk jgkA Hkkjrh; fjtoZ cSad }kjk dh x;h vkfLr xq.koÙkk leh{kk (Asset Quality Review)] ftlds vuqlkj cSadksa dks vfxzeksa dks iquoZxhZd`r djus rFkk nckoxzLr vkfLr;ksa ds lkis{k iwath ds vf/d çko/ku fd, tkus gsrq funsZf'kr fd;k x;k gS] ds vkyksd esa xSj fu"ikfnr vkfLr;ksa o çko/kuksa esa c<+ksrjh ns[kh xbZ gSA vxyk o"kZ 2016&17 Hkh] ftlesa Hkkjrh; fjtoZ cSad us cSadksa ls mudh leLr nckoxzLr vkfLr;ksa dks fpfUgr fd, tkus o rnuqlkj muds lkis{k çko/ku fd, tkus dh vis{kk dh gS] cSafdax m|ksx ds fy, bruk gh pqukSrhiw.kZ jgsxkA

n`f"Vdks.k

ekStwnk foÙkh; o"kZ esa Hkkjrh; fjtoZ cSad us eq[; njksa esa dVkSrh djrs gq, vFkZO;oLFkk dks 75 vk/kj vadksa (bps) dh jkgr çnku dhA rFkkfi] dsUæh; cSad }kjk xr ,d o"kZ esa dqy 125 vk/kj vadksa (bps)dh dVkSrh nsus ds mijkar Hkh Hkkjrh; cSadksa us muds ladqfpr gksrs tk jgs ykHk ekftZuks ds vkyksd esa viuh vk/kj njksa (base rate) esa vkSlru 70 vk/kj vadksa (bps) dh gh dVkSrh mrjksÙkj çlkfjr dhA lkekU; ekulwu] ldkjkRed O;kikj ladsrdksa] ?kjsyw vk; esa lq/kj rFkk bdkb;ksa dh vknku ykxrksa esa deh ds vkyksd esa Hkkjrh; fjtoZ cSad us o`f¼ ds Øfed l'kfDrdj.k dh vk'kk O;Dr djrs gq, ldy ?kjsyw mRikn o`f¼ nj 2016&17 esa 7-6% ç{ksfir dh gSA

ekStwnk ljdkj }kjk foÙkh; lesdhdj.k dh fn'kk esa mBk, x, dneksa ds vkyksd esa cktkj 2016&17 ds çkjEHk esa 25 ls 50 vk/kj vadksa (bps) rd dh njksa esa dVkSrh dh vk'kk dj jgk gSA orZeku ctV esa ljdkj us 2016&17 gsrq foÙkh; ?kkVs dks 3-5% j[krs gq, Hkkjrh; fjtoZ cSad dks viuh vkxkeh f}ekfldh esa njksa esa dVkSrh djus gsrq i;kZIr xqatkb'k ns nh gSA

ljdkj }kjk baizQkLVªDpj esa vf/d fuos'k fd, tkus rFkk vc rd BIi@LFkfxr jgh ifj;kstukvksa dks Rofjr Lohd`fr ds mrjksÙkj çHkko ds vkyksd esa orZeku o"kZ esa lk[k dh ekax ds dqN iquthZfor gksus dh laHkkouk gS A

volj o pqukSfr;k¡

Hkkjrh; vFkZO;oLFkk fo'o dh lokZf/d rsth ls c<+rh gqbZ vFkZO;oLFkk gSA rFkkfi] ekStwnk o`f¼ vHkh Hkh jkstxkj ds vf/dkf/d volj l`ftr djus@lq/kjus o lkekftd LFkkf;Ro çnku djus ds jk"Vªh; mís';@ekud ls dkiQh uhps gSA

10 1110 1110 11

subdued global demand for the export goods resulting in low consumption and lower capacity utilization. The low credit growth scenario may also be attributed to the corporates opting for fund raising through the commercial paper market and overseas sources, where rates are lower than base rate of Indian banks. Even in this period of corporate stress, retail credit growth as per sectoral deployment of credit kept the banks at comfortable position with a growth of over 15% and relatively low NPAs.

Aggregate deposits of the SCBs showed growth of 11.3% in the current fiscal as against previous year growth of 10.7%, while advances growth stood at 11.5% against 9.6% previous fiscal.

The asset quality concerns continued to build up, because of the overall trade and demand slowdown bottleneck. As per FSR of Dec’15, the Gross NPAs of the SCBs increased from 4.6% in Mar’15 to 5.1% in Sept’15. The stressed assets touched another high of 11.3% in Sept’15 up from 11.1% in Mar’15, while PSBs stressed assets stood high at 14.1% in Sept’15.

The year had been very challenging on the asset quality front. There has been a surge in bad loans and provisions after RBIs Asset Quality Review directing the Banks to reclassify loans and set aside more money against stressed assets. The next year 2016-17, by which time RBI expects banks to recognize all stressed assets & make provisions to cover them will be equally challenging for the industry.

OUTLOOK

In the current fiscal, RBI gave the economy a respite of 75 basis points in the form of key rate cuts. However, out of the total 125 bps cut given by the Central Bank in the last one year, Indian banks could bring down the average Base rate cut by 70 bps due to squeezing profit margin. For FY 2016-17, RBI expects the growth to strengthen gradually on the backdrop of normal monsoon, positive terms of trade gains, improving household incomes and lower input costs of firms and projected the GDP growth at 7.6%.

At the beginning of FY 2016-17, market is expecting a rate cut of 25 to 50 bps on the backdrop of fiscal consolidation measures of the current government. In the current budget, government has kept the fiscal deficit for 2016-17 at 3.5% giving RBI headroom to cut key rates.

The current year may witness some revival in credit demand on the backdrop of trickledown effect of clearance of stalled projects and increased investment in infrastructure by the government.

OPPORTUNITIES & THREATS

Indian economy is the fastest growing economy in the world.However, the current growth is still short of the mark required by the nation to improve job creation and social stability.

A sluggish rural economy is being considered as one of the important reasons for subdued growth in the economy. Any improvement in rural demand, middle class consumption pattern and increased investment is expected to witness recovery in the economy. Improvement in credit growth is mostly bolstered by the increased focus on retail segment by the banks. Of late, the agriculture sector has emerged

jktLFkku eq[;ea=kh jkgr dks"k dks lgk;rk Donation to the Rajasthan Chief Minister’s Relief Fund

12 1312 1312 13

xzkeh.k vFkZO;oLFkk esa f'kfFkyrk vFkZO;oLFkk dh ean o`f¼ dk ,d çeq[k dkj.k gSA xzkeh.k ekax] eè;e oxZ miHkksx lajpuk esa dksbZ Hkh lq/kj rFkk fuos'k esa c<+ksrjh ls vFkZO;oLFkk esa lq/kj gksus dh vk'kk gSA ÅtkZoku tula[;k oxZ] vkokl o vU; lkekftd lqfo/kvksa dks ysdj c<+rh gqbZ vkdka{kkvksa ls ifjiw.kZ ,d fujarj c<+rk gqvk eè;e oxZ o lkFk gh vk; vtZu dks"Bd esa vf/dkf/d yksxksa dk lekos'ku] ;s lHkh lexz :i ls cSadksa ds fy, ,d ,slh foiqy O;olk; laHkkouk ds :i esa :ikarfjr gks jgs gSa ftUgsa cSad vc viuk y{; cuk jgs gSaA lk[k o`f¼ esa lq/kj dks eq[; :i ls cSadksa }kjk fjVsy [kaM ij vf/dkf/d è;ku dsfUær fd, tkus ls cy fey jgk gSA gky esa d`f"k {ks=k us Hkh vius vk; Lrj esa c<+ksrjh ns[kh gS rFkk c<+s gq, d`f"k e'khuhdj.k&mUur midj.kksa ds ç;ksx o d`f"k mRiknksa rFkk lkFk gh Hkwfe vf/xzg.k ds çfriQyLo:i fn;s tk jgs csgrj ykHkdkjh ewY;ksa eqvkotk jkf'k ds dkj.k] ,d cM+s miHkksDrk oxZ ds :i esa mHkjk gSA

ns'k esa baizQkLVªDpj ifj;kstukvksa esa rsth o vc rd BIi@LFkfxr ifj;kstukvksa dks eatwjh@Lohd`fr dk vFkZO;oLFkk esa laiw.kZ O;olk; o`f¼ esa pØh; çHkko gksus ds dkj.k buesa o`f¼ pØ dks vkSj xfr çnku djus dh {kerk fufgr gSA ljdkj }kjk ^^esd bu bafM;k**] ^^LVSaM&vi bafM;k ** o vU; lekukUrj uoksUes"kh ç;klksa@vfHk;kuksa ds vkØked çpkj@çlkj rFkk orZeku ctV esa baizQkLVªDpj esa fuos'k dks vf/d çksRlkgu ls vkSj vf/d ?kjsyw o fons'kh fuos'k vkus dh laHkkouk,a çcy gSaA

;|fi cSadksa] fo'ks"kdj lkoZtfud {ks=k ds cSadks] ds fy, dbZ volj gS] rFkkfi ykHkçnrk ij ncko] vkfLr xq.koÙkk esa fxjkoV rFkk c<+rh gqbZ çfrLi/kZ ds :i esa varfuZfgr pqukSfr;k¡ Hkh gS tks fd ekftZu de dj jgh gSaA cSadksa dks u dsoy miyC/

lalk/kuksa dk loZJs"B mi;ksx djrs gq, bu pqukSfr;ksa dk MV dj eqdkcyk djus ds fy, rS;kj gksuk gksxk] vfirq lkFk gh vkxs cus jgus ds fy, lrr o fuckZ/ :i ls uoksUes"ku] uoç;ksx o uofparu djrs jguk gksxkA

y?kq cSadksa (Small Bank) rFkk Hkqxrku cSadksa (Payment Bank) oxZ esa u, cSad Hkh foÙkh; o"kZ 2016&17 esa viuk ifjpkyu çkjEHk dj nsaxsA ;|fi ;s cSafdax lsokvksa dks vkSj vf/d foLrkfjr djus esa lgk;d gksaxs] rFkkfi ;s orZeku fo|eku cSadksa ls Hkh Li/kZ djsaxsA ncko ds ekStwnk nkSj esa] ;s cSad viuk ifjpkyu ,d lkiQ lqFkjs rqyu i=k ij çkjEHk djsaxs vkSj bl çdkj vU; cSadksa] ftUgsa O;olk; ds lkFk&lkFk vkfLr xq.koÙkk] olwyh vkfn ij è;ku dsfUær djuk gS] dh vis{kk O;olk; o`f¼ ij è;ku dsfUær djsaxsA

ncko o fuokj.k

cSafdax {ks=k ds fy, 2015&16 ncko ls ifjiw.kZ ,d vkSj o"kZ FkkA xSj fu"ikfnr vkfLr;ka (,uih,) c<+dj `4 yk[k djksM+ gks x,] tcfd cSadksa dh nckoxzLr vkfLr;ka `8 yk[k djksM+ dks ikj dj xbZA Hkkjrh; fjtoZ cSad }kjk 2017 rd cSadksa ds rqyui=kksa ij cus gq, ncko dks iw.kZr;k nwj djus ds earO; dks O;Dr djrh ?kks"k.kkvksa o blds mijkar vkfLr xq.koÙkk leh{kk (AQR) lwph us cSadksa ij ncko vkSj c<+k fn;kA foÙkh; o"kZ 2015&16 esa cSafdax m|ksx us lokZf/d nckoxzLr vfxze vuqikr ntZ fd;kA m|ksx ds ik¡p çeq[k mi&{ks=kksa ;Fkk [kuu] ykSg ,oa bLikr] oL=k] baizQkLVªDpj o foekuu] ftudk fd lesfdr :i ls vuqlwfpr okf.kfT;d cSadksa (SCBs) ds dqy vfxzeksa esa 24-2% dk va'knku Fkk] us dqy nckoxzLr vfxzeksa esa 53% dk ;ksxnku fn;kA d`f"k [kaM esa Hkh dbZ jkT;ksa esa lw[ks rFkk vksyko`f"V dh fLFkfr ds dkj.k foxr nks o"kksaZ ls yxkrkj nckoxzLr ifjn`'; cuk gqvk gSA bldk d`"kdksa dh iquZHkqxrku {kerk ij] fo'ks"kdj çHkkfor jkT;ksa esa] çfrdwy çHkko iM+k gS ftlds

ifj.kkeLo:i bl {ks=k esa ncko c<+ x;k gSA

rFkkfi] dsaæ ljdkj us baizQkLVªDpj xfrjks/ksa] BIi iM+h@#dh gqbZ ifj;kstukvksa dh Rofjr Lohd`fr rFkk fuekZ.k m|ksxksa vkfn dks çksRlkgu nsus dh fn'kk esa dbZ dne mBk,¡ gSaA ljdkj }kjk mBk, x, bu dneksa@uoksUes"kh ç;klksa esa lkoZtfud {ks=k cSadksa dh uolTtk@ o uon`f"Vdks.k dks dsfUær djrh gqbZ lkr lw=kh; ;kstuk ^^baæ/uq"k** lfEefyr gS] ftldk y{; Hkh cSafdax ncko dks de djuk] vkfLr xq.koÙkk ds lq/kj gsrq fopkj cukuk] dsaæ lapkfyr cSadksa esa iwath çnÙk djus rFkk cSadksa dks ekStwnk o Hkkoh dfBukbZ;ksa vkfn ds fy, rS;kj djuk gSA bu ljdkjh ç;klksa ls u dsoy cSadksa dks lacy o lg;ksx feyus cfYd lkFk gh m|ksxksa dks ladV ls ckgj fudyus vkSj Hkkoh fodkl dk jksMeSi rS;kj fd, tkus dh vk'kk cuh gS tks fd mrjksÙkj ns'k dks vf/d o`f¼ nj çkIr djus esa lgk;d gksaxsA cSad l?ku olwyh ç;klksa] O;kolkf;d n`f"V ls mikns;@ ykHkçn o rdZlaxr ifj;kstukvksa dks foÙkh; lg;ksx çnku djus o nckoxzLr vkfLr;ksa ds laca/ esa gj ekeys ds xq.koÙkkiw.kZ foospu@leh{kk mijkar mi;qDr ik;s tkus dh n'kk esa mls vkfLr iquZlajpuk daifu;ksa (ARCs) dks csps tkus tSls lesfdr o lexz dneksa }kjk ncko Lrj dks de fd, tkus dh fn'kk esa lrr ç;kljr gSaA blds vfrfjDr cSad m|ksxksa ds fodkl o o`f¼ ls tqM+h ljdkjh ;kstukvksa o ç;klksa dks iw.kZ lg;ksx o leFkZu çnku dj jgs gSaA

jktLFkku vFkZO;oLFkk

jktLFkku {ks=kiQy dh n`f"V ls Hkkjr dk lcls cM+k jkT; gS tgka tSfod rFkk lafonk [ksrh ds {ks=kksa esa o lkFk gh d`f"k ls tqM+h ifj;kstukvksa ds laca/ esa foiqy volj miyC/ gSaA jktLFkku çkd`frd

12 1312 1312 13

as a big consumer class, owing to increased farm mechanisation and better remunerative prices for agricultural produce as also compensation in lieu of land acquisition.

The rise in the infrastructure projects and clearance of stalled projects in the country has the ability to spur the growth cycle by way of multiplier effect on overall business growth in the economy. The “Make in India” campaign, “Stand-up India” and other similar initiatives being aggressively pursued by the Government and increased investment in infrastructure in the current budget is likely to bring in further domestic and overseas investment in this sector.

While there are many opportunities for the banks, especially the public sector ones in the form of latest government initiatives, there are some inherent threats as well in the form of pressure on profitability, decline in asset quality and increasing competition, which is driving down the margins. The banks have not only to get themselves out of the current situation and try to make the best out of the available resources, but also to consistently improvise, invent and innovate for staying ahead of their peers.

The new banks in the Small Bank & Payment Bank category will also start their operation in FY-2016-17. Though they will help further deepen the banking services, they will also give competition to the already existing banks. In the time of stress, these banks will start their operations on a clean balance sheet and would, thus, be focusing on business growth as compared to others who have to focus on

maintaining asset quality, recovery etc along with business.

STRESS AND MITIGATION

The year 2015-16 was another year of stress for banking sector. The NPAs increased to `4 lakh crore, while the stressed assets of the banks crossed `8 lakh crore. The announcements of RBI intending to clearing the stress on balance sheet of the banks by 2017 and the consequent AQR list further increased the pressure on the banks. In the fiscal 2015-16, banking industry continued to record the highest stressed advances ratio. The five main sub-sectors of the industry viz, mining, iron & steel, textiles, infrastructure and aviation, which together constituted 24.2% of the total advances of SCBs contributed to 53% of the total stressed advances. Agriculture segment is also witnessing stressed scenario continuously for last two years due to drought and hailstorm situation in many of the states. This has adversely affected the repayment capacity of the farmers resulting in stress in this sector, particularly in the affected states.

However, various measures have been taken by the Central Government towards removing of infrastructure bottlenecks, clearing of stalled projects, giving boost to the manufacturing industries etc. Many of the initiatives of the Government like, “Indradhanush”, the seven pronged plan to revamp Public Sector Banks, also aims at reducing the banking stress, forming opinion on improving asset quality, infusing capital in the state run banks, preparing the banks to face the ongoing as well as future problems etc. These government

initiatives are expected to not only support the banks but also pull the industries out of the distress and provide a road map for further development helping the nation achieve a high growth rate scenario. Banks are also working profusely towards reducing stress level by strong recovery efforts, providing support for genuine projects and by selling of stressed assets to ARCs on the case to case basis. Besides this, the banks are giving full support to the government schemes and initiatives for growth of the industry.

RAJASTHAN ECONOMY

Rajasthan is the largest state in India in terms of area having tremendous opportunities in the areas of organic and contract farming as well as infrastructure developments related to agriculture. Rajasthan is richly endowed with natural resources, making it an attractive investment destination for extraction activities, as well as mineral-based manufacturing such as cement, ceramics and glass. Rajasthan accounts for 17.5% of the total cement grade limestone reserves in India and is the largest cement producer with 21 major cement plants. Rajasthan is the leading producer of limestone, silver, marble, sandstone and lignite. It is also second largest producer of the milk in India.

Rajasthan has emerged as an investment destination with 23% of the NCR area and 39% of Delhi-Mumbai Industrial Corridor falling in the state. With the area of industrial zone increasing and more industries being established in the areas like, Neemrana, Gheelot, Khushkhera etc, the state is on the road to become major industrial

14 1514 1514 15

lalk/uks ds laca/ esa vR;f/d laiUu gS] tks fd bls [kuu vk/kfjr xfrfof/;ksa o lkFk gh [kfut vk/kfjr fuekZ.k ;Fkk lhesaV] fljsfed o Xykl ds laca/ esa ,d vkd"kZd fuos'k xarO; ds :i esa ifjHkkf"kr djrs gSaA jktLFkku dk Hkkjr ds dqy lhesaV oxZ pwukiRFkj HkaMkjksa esa 17-5% dk va'knku gS rFkk 21 çeq[k lhesaV la;a=kks ds lkFk ns'k dk lcls cM+k lhesaV mRiknd gSA jktLFkku pwukiRFkj] pkanh] laxejej] ckyw rFkk fyXukbZV dk çeq[k mRiknd gSA ;g Hkkjr dk nwljk lcls cM+k nqX/ mRiknd jkT; Hkh gSA

jk"Vªh; jkt/kkuh {ks=k (,ulhvkj) dk 23% {ks=k rFkk fnYyh&eqacbZ vkS|ksfxd dksfjMksj ds 39% {ks=k dk jkT; esa vkus@iM+us ds dkj.k jktLFkku ,d fuos'k dsaæ ds :i esa mHkj pqdk gSA vkS|ksfxd t+ksuksa ds {ks=k esa foLrkj ls rFkk uhejkuk] ?khyksr] [kq'k[ksjk vkfn {ks=kksa esa vf/dkf/d m|ksxksa dh LFkkiuk fd, tkus ds iQyLo:i jkT; ns'k dk ,d çeq[k vkS|ksfxd gc cuus ds iFk ij vxzlj gSA jktLFkku lkFk gh vFkZO;oLFkk esa LVkVZvIl (startups) ds egRo o Hkwfedk dks çeq[krk ls n'kkZrh@çfrikfnr djrh ,d LVkVZvi uhfr dh ?kks"k.kk djus okyk ik¡pok¡ jkT; cu x;k gSA jktLFkku LVkVZvi uhfr 2015 fnukad 09 vDrwcj 2015 ls çHkko esa vkbZ gS rFkk uoksUes"kh LVkVZvIl dks dsfUær dj bUgsa leFkZu o mn~Hkou çnku djrs gq, ik¡p o"kZ rd çHkkoh jgsxh A

jktLFkku dk ldy jkT; ?kjsyw mRikn (GSDP) 2004&05 ds lkis{k 2014&15 esa 12-8% dh pØh; okf"kZd o`f¼ nj (CAGR) ls c<+k gSA 2014&15 ds orZeku ewY;ksa ij jktLFkku dh GSDP dk Lrj 11% gSA jkT; esa iou ÅtkZ o uohdj.kh; ÅtkZ L=kksrksa }kjk fo|qr mRiknu dh foiqy laHkkouk,a gSaA jktLFkku uohdj.kh; ÅtkZ fuxe fyfeVsM us lkSj ÅtkZ rFkk tSoHkkj (biomass) ifj;kstukvks dks lfØ; :i ls çksRlkfgr fd;k gSA

tuojh 2016 ds var esa jktLFkku ds ikl dqy 17784 esxkokV fo|qr mRiknu laLFkkfir {kerk FkhA jktLFkku us xSj ikjaifjd ÅtkZ L=kksrksa] fo'ks"kdj lkSj ÅtkZ] ds fodkl dks c<+kok nsus o rnuqlkj ikjaifjd ÅtkZ L=kksrksa ij fuHkZjrk de djus ds mís'; ls lkSj ÅtkZ uhfr Hkh ykxw dh gSA

gky gh esa jktLFkku ljdkj us fo'ks"k fuos'k vapyksa dh ekLVj o fodkl ;kstuk,¡ cuk dj vkS|ksfxd fuos'k dks rnuqlkj xfr çnku djus gsrq ,d vè;kns'k vuqeksfnr fd;k gSA ljdkj }kjk fd, x, fofo/ ç;kl ;Fkk LVkVZvi uhfr] ^^esd bu bafM;k** ;kstuk] y?kq o eè;e m|ksxksa ds fy, ,e,l,ebZ uhfr] çeq[k {ks=kksa dh daifu;ksa ds lkFk vk;ksftr fjltsaZV jktLFkku lEesyu@ laxks"Bh us jkT; ds laiw.kZ fuos'k o vkfFkZd ifjn`'; dks vkSj Å¡pkbZ;k¡ çnku dh gSaA

fuxfer ifjpkyu

O;olk; fu"iknu

cSad dk lexz O;olk; (tek,¡ ,oa ldy vfxze) ekpZ] 2015 ds `155392 djksM+ ds Lrj esa `13356 djksM+ (8-59%) dh o`f¼ n'kkZrs gq, ekpZ] 2016 dh lekfIr ij `168748 djksM+ ds Lrj ij igqap x;kA ekpZ] 2016 dks lekIr vof/ ds nkSjku dqy tek,¡ `9766 djksM+ (11-59%) dh o`f¼ ntZ djrs gq, `94005 djksM+ ds Lrj ij igq¡p xbZa tcfd ldy vfxze `3590 djksM+ (5-05%) dh o`f¼ ntZ djrs gq, 74743 djksM+ ds Lrj ij igqap x,A tgka cSad ds tekvksa dh ykxr 2014&15 ds 7-01% ls ?kVdj 2015&16 esa 6-76% gks xbZ] ogha vfxzeksa ij çfriQy Hkh 10-98% ls ?kVdj 10-70% gks x;kA pkyw o cpr [kkrk (dklk) tekvksa us 11-17% dh o`f¼ ntZ dh fdUrq dklk vuqikr ekpZ*15 ds 38-85% ds lkis{k 38-70% jgkA

dks"k o fuos'k

Hkkjrh; fjtoZ cSad us foÙkh; o"kZ 2015&16 dh vius ekSfæd uhfr n`f"Vdks.k esa eqækLiQhfr ds fu;a=k.k ij è;ku dsafær fd;k] tks fd ç{ksi.k ds vuq:i jghA foÙkh; o"kZ 2015&16 esa foÙkh; ?kkVk dks 3-9% ij lhfer j[kk x;kA miHkksDrk ewY; lwpdkad dks fu;a=k.k esa j[krs gq, Hkkjrh; fjtoZ cSad us uhfrxr jsiks nj] tks o"kZ ds çkjEHk esa 8% Fkh] esa pj.kc¼ :i ls o iwjs o"kZ ds nkSjku dqy 125 vk/kj vadksa dh lexz dVkSrh djrs gq, bls o"kZ ds var rd 6-75% dj fn;kA ,slk fd, tkus ls fnlacj 2015 esa vesfjdh iQsMjy njksa esa 25 vk/kj vadksa dh o`f¼ ds mijkar Hkh ?kjsyw C;kt njksa dks fu;a=k.k esa j[kus esa enn feyhA

Hkkjrh; ckWUM] bfDoVh vkSj fons'kh eqæk cktkj] ?kjsyw vkfFkZd fLFkfr ds foijhr] oSf'od dkj.kksa ls vf/d çHkkfor jgkA ;wjksfi;u ;wfu;u dh enn ls vkfFkZd ladV ls ckgj fudkys tkus ls iwoZ xzhl dk varjZk"Vªh; eqæk dks"k ds ½.k pqdkSrh esa pwd] dPps rsy dh dherksa esa fujarj fxjkoV vkSj phuh vFkZO;oLFkk esa vkbZ eanh us oSf'od eanh dks bafxr fd;kA Hkkjr esa] laçHkq 10 o"khZ; ckWUM nj] tks o"kZ ds çkjEHk esa 7-74% Fkh] o"kZ ds lekiu rd 7-46% ij vk x;h tcfd phuh vFkZO;oLFkk esa vkbZ eanh ds vkyksd esa bfDoVh cktkj esa o"kZ ds nkSjku çeq[k lwpdkadksa ;Fkk ch,lbZ lsalsDl esa 9-35% vkSj ,u,lbZ ds fuÝVh50 esa 8-87% rd Hkkjh fxjkoV ns[kh x;hA

cSad us ckWUM vkSj 'ks;j cktkj esa Ø;&foØ; esa lrdZ #[k viuk;k vkSj 31 ekpZ 2016 dks cSad dk fuos'k iksVZiQksfy;ks `2643-75 djksM+ (11-94%) dh o`f¼ n'kkZrs gq, `24782-37 djksM+ gks x;kA tgk¡ fuos'k ls dqy vk; 10-52% dh o`f¼ n'kkZrs gq, `2186-41 djksM+ gks xbZ] ogha fuos'k dh fcØh@ fofue; ls ykHk `54-01 djksM+ (35-06%) dh o`f¼ n'kkZrs

14 1514 1514 15

hub in the country. Rajasthan has also become the fifth state to unveil a Startup Policy, highlighting the importance and role of start ups in the economy. The Rajasthan Startup Policy 2015 came into force w.e.f. 09th Oct’15 and will remain in operation for a period of five years targeting innovative startups to grow in the state through support and incubation.

The gross state domestic product (GSDP) of Rajasthan expanded at a compound annual growth rate (CAGR) of 12.8% over 2004-05 to 2014-15. At current prices 2014-15, GSDP of Rajasthan stands at 11%. The state has immense potential for electricity generation through renewable energy sources and wind power. As of January 2016, Rajasthan had a total installed power generation capacity of 17,784 megawatt (MW). Rajasthan has also introduced Solar Energy Policy to reduce dependence on conventional sources of energy by promoting the development of non-conventional energy sources, especially solar power.

Recently, Rajasthan Government approved a bill to accelerate industrial investment by preparing master and development plans in special investment regions. Government initiatives like implementing Startup Policy, Make in India Scheme, MSME Policy for small and medium industries, Resurgent Rajasthan Conclave has uplifted the overall investment and economic scenario of the state.

CORPORATE OPERATIONSBUSINESS PERFORMANCE

The overall business of the Bank (deposits plus gross advances) reached a level of `168748 crore

as at end-March 2016 as against `155392 crore as at end March 2015, recording a growth of 13356 crore (8.59%). The total deposits increased by `9766 crore (11.59%) to reach a level of `94005 crore while gross advances increased by `3590 crore (5.05%) to reach a level of `74743 crore by end-March 2016. The cost of deposits of the Bank decreased from 7.01% in 2014-15 to 6.76% in 2015-16, while the yield on advances also decreased from 10.98% to 10.70%. CASA deposits recorded a growth of 11.17% but the CASA ratio was at 38.70% as compared to 38.85% as at Mar’15.

TREASURY AND INVESTMENTS

In its monetary policy stance for the financial year 2015-16, Reserve Bank of India had focused in containing the inflation which remained in line with the projections. Fiscal deficit was contained at 3.9% for FY2015-16. With CPI under control, Reserve Bank of India cut the policy repo rate in phases from 8% at the beginning of the year to 6.75% by the year-end, a reduction of 125 bps during the year. This helped in keeping the domestic interest rates under control despite a 25 basis points hike in US Federal rates in December 2015.

More than the domestic economic

conditions, Indian bond, equity and forex markets were influenced by global considerations. While Greece economic crisis saw it defaulting in debt repayment to IMF before being bailed out by European Union, continuous fall in crude prices and slowdown in Chinese economy all pointed out to recessionary trends globally. In India, sovereign 10-year bond which was at 7.74% in the beginning of the year ended at 7.46% by the year end but the equity market was hit badly with fall in major indices, BSE Sensex by 9.35% and NSE Nifty50 by 8.87% during the year.

The Bank adopted a cautious approach in trading in bond and equity market and as at 31st March 2016, Bank’s investment portfolio rose by `2643.75 crore to `24782.37 crore reflecting a growth of 11.94 %. While the total income from investments grew by 10.52% to `2186.41 crore, profit from trading/sale of investment rose by `54.01 crore to `208.03 crore, registering an increase of 35.06%. The yield on investments stood at 7.71 % and after including trading profit, total return on investments stood at 8.53% for the year.

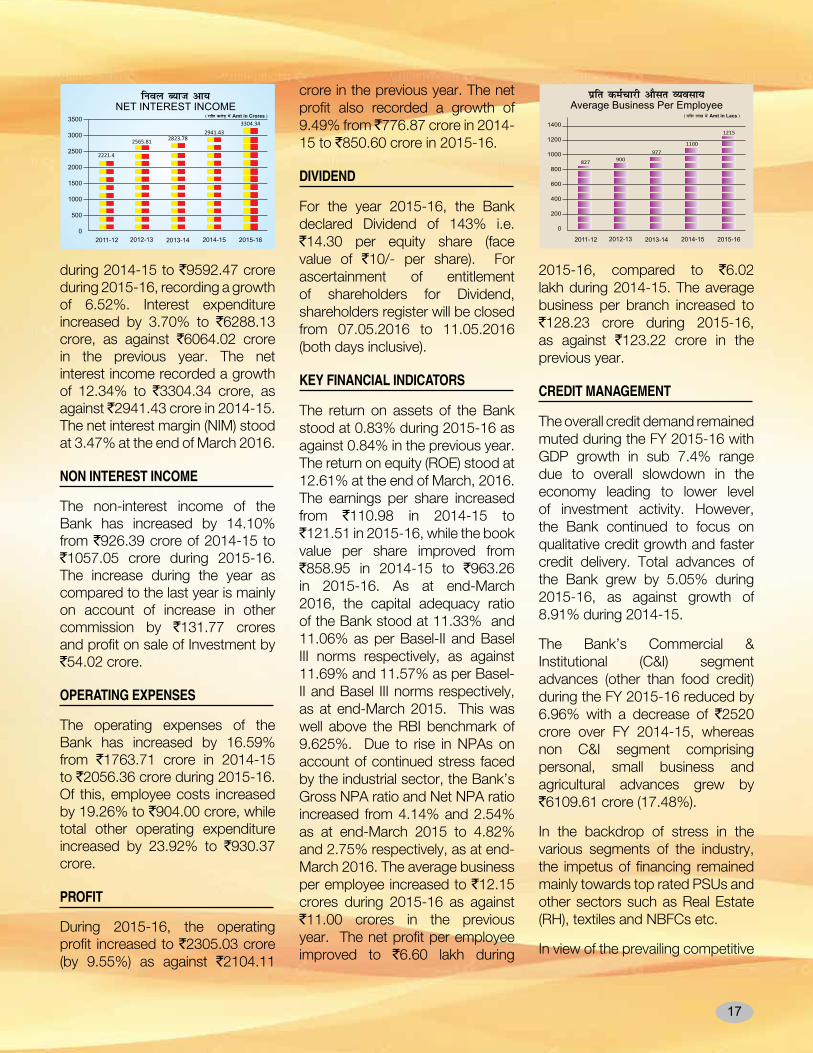

FINANCIAL HIGHLIGHTSNET INTEREST INCOME

The Bank’s total interest income increased from `9005.45 crore

16 1716 1716 17

gq, `208-03 djksM+ gks x;kA fuos'k ij çfriQy 7-71% jgk rFkk Ø;&foØ; ykHk dks lekfgr djrs gq, o"kZ ds nkSjku fuos'k ij dqy çfriQy 8-53% jgkA

fof'k"V foÙkh; rF;

fuoy C;kt vk;

cSad dh dqy C;kt vk; o"kZ 2014&15 ds `9005-45 djksM+ ls c<dj o 6-52% dh o`f¼ ntZ djrs gq, o"kZ 2015&16 esa `9592-47 djksM+ gks xbZA C;kt O;; xr o"kZ ds 6064-02 djksM+ ds lkis{k 3-70% c<dj `6288-13 djksM+ gks x;kA fuoy C;kt vk; o"kZ 2014&15 ds `2941-43 djksM+ esa 12-34% dh o`f¼ ntZ djrs gq, `3304-34 djksM+ gks xbZA fuoy C;kt ekftZu (NIM) ekpZ 2016 ds var esa 3-47% jgkA

xSj C;kt vk;

cSad dh xSj C;kt vk; 14-10% dh o`f¼ ntZ djrs gq, 2014&15 ds `926-39 djksM+ ls c<+dj 2015&16 esa `1057-05 djksM+ gks x;hA xr o"kZ dh rqyuk esa orZeku o"kZ esa o`f¼ dk çeq[k dkj.k vU; deh'ku esa `131-77 djksM+ dh o`f¼ rFkk fuos'k ds foØ; ij vftZr ykHk esa `54-02 djksM+ dh o`f¼ jgh gSA

ifjpkyu O;;

ifjpkyu O;; 2014&15 ds `1763-71 djksM+ esa 16-59% dh o`f¼ ntZ djrs gq, 2015&16 esa `2056-36 djksM+ gks x,A buesa ls tgka deZpkjh O;; 19-26% c<+dj `904-00 djksM+ gks x, ogha vU;

ifjpkyu O;; 23-92% c<+dj `930-37 djksM+ gks x,A

ykHk

2015&16 ds nkSjku ifjpkyu ykHk xr o"kZ ds `2104-11 djksM+ esa 9-55% dh o`f¼ n'kkZrs gq, `2305-03 djksM+ gks x;kA fuoy ykHk Hkh 9-49% dh o`f¼ n'kkZrs gq, 2014&15 ds `776-87 djksM+ ls c<dj 2015&16 esa `850-60 djksM+ gks x;kA

ykHkka'k

cSad }kjk o"kZ 2015&16 esa 143% dk ykHkka'k vFkkZr `14-30 çfr bZfDoVh 'ks;j ('ks;j dk vafdr ewY; `10 çfr 'ks;j) ?kksf"kr fd;k x;kA 'ks;j /kjdksa dh ykHkka'k ik=krk Kkr djus gsrq] va'kèkkjdksa dk jftLVj fnukad 07-05-2016 ls 11-05-2016 (nksuksa fnu lfEefyr) cUn jgsxkA

eq[; foÙkh; ladsrd

vkfLr;ksa ij vftZr çfriQy xr o"kZ ds 0-84% ds fo:¼ 2015&16 esa 0-83% gks x;kA ekpZ 2016 ds var esa bfDoVh ij çfriQy 12-61% jgkA çfr va'k vk; o"kZ 2014&15 ds `110-98 ls c<dj 2015&16 es `121-51 gks x;h] tcfd çfr va'k iqLrd ewY; o"kZ 2014&15 ds `858-95 ls c<dj 2015&16 esa 963-26 gks x;kA ekpZ 2016 dks lekIr vof/ ds nkSjku cSad dk cklsy&AA o cklsy&AAA ekunaMks ds vuqlkj iwath i;kZIrrk vuqikr

Øe'k% 11-33% rFkk 11-06% jgk tks fd ekpZ 2015 dks lekIr vof/ ds nkSjku cklsy&AA o cklsy&AAA ds vuqlkj Øe'k% 11-69% rFkk 11-57% FkkA ;g Hkkjrh; fjtoZ cSad }kjk fu/kZfjr 9-625% ds ekunaM ls vf/d gSA vkS|ksfxd {ks=k esa fujarj ncko ds iQyLo:i xSj fu"ikfnr vkfLr;ksa es o`f¼ ds dkj.k cSad dk ldy xSj fu"ikfnr vkfLr (,uih,) vuqikr ,oa fuoy xSj fu"ikfnr vkfLr (,uih,) vuqikr ekpZ 2015 ds Øe'k% 4-14% o 2-54% ls c<dj ekpZ 2016 ds var esa Øe'k% 4-82% o 2-75% gks x;kA çfr deZpkjh vkSlr O;olk; xr o"kZ ds `11-00 djksM+ ls c<+dj o"kZ 2015&16 ds nkSjku `12-15 djksM+ gks x;kA çfr deZpkjh fuoy ykHk o"kZ 2014&15 ds `6-02 yk[k ls c<+dj o"kZ 2015&16 esa `6-60 yk[k gks x;kA çfr 'kk[kk vkSlr O;olk; fiNys o"kZ ds 123-22 djksM+ ls c<dj o"kZ 2015&16 esa `128-23 djksM+ gks x;kA

lk[k çca/u

vFkZO;oLFkk esa lexz f'kfFkyrk o rnuqlkj fuos'k xfrfof/ ds Lrj esa deh o ldy ?kjsyw mRikn (thMhih) o`f¼ ifjf/ 7-4% ls uhps cus jgus ds dkj.k foÙkh; o"kZ 2015&16 ds nkSjku lexz lk[k ekax ean cuh jghA rFkkfi cSad us xq.koÙkkiw.kZ lk[k o`f¼ vkSj nzqr xfr ls lk[k iznku djus ij viuk è;ku dsfUær j[kkA 2014&15 esa 8-91% dh o`f¼ ds fo#¼ cSad ds dqy vfxzeksa es 2015&16 ds nkSjku 5-05% dh o`f¼ jghA

foÙkh; o"kZ 2015&16 ds nkSjku cSad ds okf.kfT;d ,oa laLFkkxr (lh ,aM vkbZ) [k.M ds vfxze ([kk| lk[k ds vfrfjDr) 6-96% dh fxjkoV ntZ djrs gq, foÙkh; o"kZ 2014&15 ds fo#¼ `2520 djksM+ ?kVs] ogha xSj&okf.kfT;d ,oa laLFkkxr [k.M ftlesa oS;fDrd] y?kq O;olk; rFkk d`f"k

16 1716 1716 17

during 2014-15 to `9592.47 crore during 2015-16, recording a growth of 6.52%. Interest expenditure increased by 3.70% to `6288.13 crore, as against `6064.02 crore in the previous year. The net interest income recorded a growth of 12.34% to `3304.34 crore, as against 2941.43 crore in 2014-15. The net interest margin (NIM) stood at 3.47% at the end of March 2016.

NON INTEREST INCOME

The non-interest income of the Bank has increased by 14.10% from `926.39 crore of 2014-15 to `1057.05 crore during 2015-16. The increase during the year as compared to the last year is mainly on account of increase in other commission by `131.77 crores and profit on sale of Investment by `54.02 crore.

OPERATING EXPENSES

The operating expenses of the Bank has increased by 16.59% from `1763.71 crore in 2014-15 to `2056.36 crore during 2015-16. Of this, employee costs increased by 19.26% to `904.00 crore, while total other operating expenditure increased by 23.92% to `930.37 crore.

PROFIT

During 2015-16, the operating profit increased to `2305.03 crore (by 9.55%) as against `2104.11

crore in the previous year. The net profit also recorded a growth of 9.49% from 776.87 crore in 2014-15 to `850.60 crore in 2015-16.

DIVIDEND

For the year 2015-16, the Bank declared Dividend of 143% i.e. `14.30 per equity share (face value of `10/- per share). For ascertainment of entitlement of shareholders for Dividend, shareholders register will be closed from 07.05.2016 to 11.05.2016 (both days inclusive).

KEY FINANCIAL INDICATORS

The return on assets of the Bank stood at 0.83% during 2015-16 as against 0.84% in the previous year. The return on equity (ROE) stood at 12.61% at the end of March, 2016. The earnings per share increased from `110.98 in 2014-15 to `121.51 in 2015-16, while the book value per share improved from `858.95 in 2014-15 to `963.26 in 2015-16. As at end-March 2016, the capital adequacy ratio of the Bank stood at 11.33% and 11.06% as per Basel-II and Basel III norms respectively, as against 11.69% and 11.57% as per Basel-II and Basel III norms respectively, as at end-March 2015. This was well above the RBI benchmark of 9.625%. Due to rise in NPAs on account of continued stress faced by the industrial sector, the Bank’s Gross NPA ratio and Net NPA ratio increased from 4.14% and 2.54% as at end-March 2015 to 4.82% and 2.75% respectively, as at end-March 2016. The average business per employee increased to `12.15 crores during 2015-16 as against `11.00 crores in the previous year. The net profit per employee improved to `6.60 lakh during

2015-16, compared to `6.02 lakh during 2014-15. The average business per branch increased to `128.23 crore during 2015-16, as against `123.22 crore in the previous year.

CREDIT MANAGEMENT

The overall credit demand remained muted during the FY 2015-16 with GDP growth in sub 7.4% range due to overall slowdown in the economy leading to lower level of investment activity. However, the Bank continued to focus on qualitative credit growth and faster credit delivery. Total advances of the Bank grew by 5.05% during 2015-16, as against growth of 8.91% during 2014-15.

The Bank’s Commercial & Institutional (C&I) segment advances (other than food credit) during the FY 2015-16 reduced by 6.96% with a decrease of `2520 crore over FY 2014-15, whereas non C&I segment comprising personal, small business and agricultural advances grew by `6109.61 crore (17.48%).

In the backdrop of stress in the various segments of the industry, the impetus of financing remained mainly towards top rated PSUs and other sectors such as Real Estate (RH), textiles and NBFCs etc.

In view of the prevailing competitive

18 1918 1918 19

[k.M 'kkfey gS] esa `6109-61 djksM+ (17-48%) dh o`f¼ gqbZA

m|ksx ds fofHkUu [kaMksa esa O;kIr ncko ds eísutj] foÙk iks"k.k gsrq mPp nj fu/kZfjr lkoZtfud {ks=k dh bdkb;ksa ;Fkk fj;y LVsV (RH)] VsDlVkbYl rFkk xSj&cSafdax okf.kfT;d bdkb;ksa (NBFCs) vkfn ij vf/d cy jgkA

orZeku çfrLi/kZRed rFkk nckoxzLr cktkj ifjn`'; ds vkyksd esa 'kh"kZ çca/u }kjk vfr egRoiw.kZ xzkgdksa ds lkFk ns'k ds çeq[k dsUæksa ij fd, x, xgu laokn o fu;fer laidZ ds iQyLo:i dbZ vPNs xq.koÙkkiw.kZ vfxze çLrko çkIr djus esa liQyrk feyhA

oS;fDrd cSafdax

oS;fDrd cSafdax [k.M foÙkh; o"kZ 2016 ds nkSjku cSad dk fo'ks"k dsUæ fcUnq cuk jgkA cSad us vkfLr o lkFk gh ns;rkvksa i{k ij fo'ks"k è;ku nsrs gq, o lkFk gh xzkgd larqf"V esa lq/kj ykrs gq, vius fjVsy iksVZiQksfy;ks dks vkSj lqn`<+ fd;kA ns;rkvksa i{k varxZr fjVsy dklk (CASA) esa vf/dkf/d O;olk; va'k

vftZr djus ij fo'ks"k è;ku dsfUær jgkA cSad }kjk vius orZeku xzkgdksa ls lEcU/ksa dks u dsoy lqn`<+ vfirq vkSj ÅtkZoku cukus o mrjksÙkj dklk tekvksa dks lq/kjus dh fn'kk esa o"kZ ds nkSjku dbZ u, ç;ksx@ ç;kl fd, x,A o"kZ 2015&16 esa cSad us vius fjVsy O;olk; ifjpkyu eas vR;ar l'kDr o`f¼ ntZ dh gSA

u, xzkgd tksM+us ij fo'ks"k è;ku fn;k tkrk jgk ftlds ifj.kkeLo:i o"kZ ds nkSjku 30-01 yk[k u, dklk [kkrs [kksys x, o rnuqlkj xzkgd vk/kj esa o`f¼ gqbZA

oS;fDrd [kaM vfxze varxZr cSad us cktkj dh vis{kkvksa ds vuq:i vius mRiknksa rFkk lsok dks vkSj vf/d Rofjr o vkd"kZd cuk, j[kus esa çfrc¼rk cuk, j[khA vius ½.k i{k dks vkSj vf/d larqfyr cuk, j[kus ds mís'; ls cSad us fjVsy O;olk; ij vf/d è;ku dsfUær fd;kA bl mís'; dh iwfrZ o vius mRiknksa dks vf/d vkd"kZd cukus gsrq cSad us fo'ks"k ç;kl o fofo/ ç;ksx fd,A vkokl ½.k varxZr ubZ ;kstuk,a ;Fkk ogu;ksX; vkokl ½.k (affordable housing loans) vkSj SBBJ Trust ykbZ xbZA is'kau ½.k vkSj f'k{kk ½.k

;kstukvksa esa vkSj lq/kj ykrs gq, bUgsa nksckjk çkjEHk fd;k x;kA ,lchchts lksyj ½.k ;kstuk] ,lchchts x`gvyadkj o ,lchchts bZth dkj ½.k ;kstuk foÙkh; o"kZ 2015&16 ds nkSjku çkjEHk dh x;h vU; ½.k ;kstuk,a jghaA

d`f"k

d`f"k {ks=k dks vfxze cSad dh çeq[k çkFkfedrkvksa esa ls ,d cuk jgk gSA d`f"k vfxzeksa dk Lrj ekpZ 2015 ds `11927 djksM+ esa 12-34% dh o`f¼ n'kkZrs gq, ekpZ 2016 ds var esa `13399 djksM+ gks x;kA

dqy Ñf"k vfxzeksa esa izR;{k Ñf"k ½.kksa dk fgLlk 83-34% gSA okf"kZd y{; `13748 djksM+ ds fo:¼ leh{kk o"kZ ds nkSjku d`f"k lk[k çokg `12432 djksM+ jgk gS] tks fd 90-42% miyfC/ gSA Hkkjrh; fjtoZ cSad ds 18% ekunaM ds lkis{k gekjs cSad ds d`f"k ½.k lek;ksftr fuoy cSad lk[k (ANBC) dk 22-51% gSA

cSad }kjk leh{kk o"kZ ds nkSjku 102791 fdlku ØsfMV dkMZ (dslhlh) `2651 djksM+ dh Lohd`r lk[k lhek ds lkFk tkjh fd;s x,A ekpZ 2016 ds var esa fdlku ØsfMV dkMZ (dslhlh) dh dqy la[;k 6,00,887 Fkh A

lw{e] y?kq ,oa eè;e m|e (,e,l,ebZ)lw{e] y?kq ,oa eè;e m|e (,e,l,ebZ) {ks=k 5-77 djksM+ bdkb;ksa ds vius o`gn usVodZ] tks fd 8 djksM+ ls vf/d O;fDr;ksa ds fy, jkstxkj l`ftr dj jgk gS] 6000 ls vf/d mRikn fufeZr dj jgk gS ftldk fofuekZ.k mRiknks esa 45% dk rFkk fu;kZr esa yxHkx 40% dk ;ksxnku gS] Hkkjrh; vFkZO;oLFkk dh o`f¼ esa egRo`iw.kZ ;ksxnku ns jgk gSA

cSad vFkZO;oLFkk ds bl çeq[k ?kVd ds fodkl o o`f¼ dks çkFkfedrk ns jgk gSA 31 ekpZ 2016 dks cSad dk lw{e y?kq ,oa eè;e m|e (,e,l,ebZ) {ks=k dks çnÙk dqy vfxze `13178 djksM+ Fkk tks fd

Hkkjrh; lw{e] y?kq ,oa eè;e bdkbZ pSacj (lhvkbZ,e,l,ebZ) }kjk ^^mHkjrs cSadks gsrq loZJs"B ,e,l,ebZ cSad vokMZ** varxZr mifotsrk iqjLdkj

Runner –Up under the “Best MSME Bank Award for Emerging Bank” by Chamber of Indian Micro, Small

and Medium Enterprises (CIMSME)

18 1918 1918 19

and stretched market scenario, closer interaction and regular meetings by the Top Management with high value customers were held at major centers in the country which resulted in booking several good advances.

PERSONAL BANKING

Personal Banking Segment continued to be the thrust area of the Bank in FY’16. Bank strengthened its retail portfolio by placing special emphasis both on asset as well as on the liability side and also improved customer satisfaction. On the liability side focus was placed on garnering higher share of retail CASA. A number of initiatives were undertaken during the year for strengthening and reviving the relationship with existing customers for improving CASA deposits. The Bank’s retail operations have recorded a robust growth during the year 2015-16.

Acquisition of new customers continued to remain one of the focus area consequently resulting in increase of customer base with opening of 30.01 lacs new CASA accounts during the year.

In Personal Segment lending, Bank was committed to fine tune the products and service delivery to the market expectations. Bank placed added thrust on retail business to make its loan-book more balanced. To achieve this, Bank introduced special measures to increase the attractiveness of its products. Under Home Loans, new schemes were introduced such as Affordable Housing loans and SBBJ Trust. Pension Loan and Education Loan were re-launched with improvements. SBBJ Solar loan scheme, SBBJ Grih Alankar

and SBBJ Easy Car loan are the other loan schemes introduced during the FY’16.

AGRICULTURE

Lending to agriculture remains one of the major thrust areas of the bank. The outstanding level of agriculture advances increased from `11927 crore as at the end of March 2015 to `13399 crores as at the end of March, 2016 and registered a growth of 12.34%.

Our bank’s total direct agriculture lending is 83.34% of total agriculture advances. The flow of credit in agriculture stood at `12432 crores against the annual target of 13748 crores, i.e. an achievement of 90.42% for the financial year 2015-16. Agriculture advances constitute 22.51% of the (ANBC), against RBI benchmark of 18%.

The bank has issued 102791 Kisan Credit Cards (KCC’s) with sanctioned limit of `2651 crores during the period under review. The total number of KCC’s stood at

6,00,887 as at end of March, 2016.

MICRO, SMALL AND MEDIUM ENTERPRISES (MSMEs)

The Micro, Small and Medium Enterprises (MSME) Sector contributes in a big way to the growth of Indian Economy with a vast network of 5.77 crore units, creating employment for more than 8 crore people, manufacturing more than 6000 products, contributing about 45% of manufacturing output and about 40% of exports.

The Bank gives due importance for the growth of this vital segment of the economy. As on 31st March 2016, Bank's total exposure to Micro, Small and Medium Enterprises (MSME) sector is `13178 crore in more than 171000 MSME units. MSME Segment is one of the key growth areas identified by the Bank, which constitutes more than 17.63% of Bank’s total advances. During the year, Bank has sanctioned credit facilities to more than 64900 new MSME units amounting to `3323

,lkspSe }kjk ^^loZJs"B lkekftd cSad** eè;e cSad

oxZ varxZr mifotsrk iqjLdkj

Runner-Up in the “Best Social Bank” category under Medium Bank Class by ASSOCHAM

20 2120 2120 21

171000 ls vf/d ,e,l,ebZ bdkb;ksa dks çnÙk fd;k gqvk gSA lw{e] y?kq ,oa eè;e m|ksx (,e,l,ebZ) [k.M cSad }kjk fpfUgr lexz o`f¼ dk ,d çeq[k {ks=k gS rFkk bldk cSad ds dqy vfxze esa 17-63% ls vf/d dk va'knku gSA leh{kk o"kZ ds nkSjku cSad us 64900 ls vf/d ubZ ,e,l,ebZ bdkb;ksa dks 3323 djksM+ jkf'k dh lk[k lqfo/k çnÙk djokbZ] ftlesa ls ,e,lbZ bdkb;ksa dks çnÙk `10 yk[k rd ds ½.k dh jkf'k `1553 djksM+ FkhA

cSad lhthVh,e,lbZ dh ½.k xkjaVh ;kstuk varxZr ,e,lbZ {ks=k dks `1 djksM rd ds leikf'oZd çfrHkwfr eqDr ½.k miyC/ djok jgk gSA bl xkjaVh ;kstuk varxZr ik=k ,e,lbZ [kkrksa esa `100 yk[k rd dh lk[k lhek ij 50 ls 85% xkjaVh doj çnku fd;k tkrk gSA cSad us lhthVh,e,lbZ varxZr foÙkh; o"kZ 2015&16 esa `238 djksM+ ds 7802 [kkrksa dks doj fd;k gSA

çkFkfedrk {ks=k vfxze

Hkkjrh; fjtoZ cSad }kjk fu/kZfjr 40% ds ekun.M ds fo#¼ 31 ekpZ 2016 ds var esa cSad ds çkFkfedrk {ks=k vfxze lek;ksftr fuoy cSad lk[k (ANBC) dk 41-52% FksA vkadM+ksa ds ifjçs{; esa çkFkfedrk {ks=k vfxze ekpZ 2015 dh lekfIr ij `27844 djksM ds fo#¼ `29677 djksM+ FksA Hkkjrh; fjtoZ cSad@ Hkkjr ljdkj ds funsZ'kksa@ uhfr;ksa ds vuq#i vFkZO;oLFkk ds misf{kr {ks=k ds lkfE;d ,oa lrr vkfFkZd fodkl ds fy, çkFkfedrk {ks=k dks vfxze cSad dk çeq[k fparu gSA bl {ks=k dh fof'k"V vko';drkvksa dh iwfrZ gsrq cSad ifjpkyu çkf/dkfj;ksa dks le; le; ij d`f"k] ,e,lbZ] vkokl] f'k{kk fu;kZr lk[k vkfn ij fo'ks"k è;ku fn;s tkus gsrq vfHkçsfjr dj jgk gSA

foÙkh; lekos'ku ;kstuk (FI Plan 2013&16) varxZr çxfr

Hkkjrh; fjtoZ cSad dh foÙkh; lekos'ku

;kstuk (2013&16) vuqlkj cSad }kjk 31-03-2016 rd 2000 ls de dh tula[;k okys 7348 xk¡o doj fd, tkus Fks rFkk bu lHkh xkaoksa dks chlh@'kk[kkvksa }kjk doj dj fy;k x;k gSA fnukad 31-03-2016 rd 490 xzkeh.k 'kk[kk,¡ [kksyus ds y{; ds lkis{k cSad us 508 xzkeh.k 'kk[kk,¡ [kksyh gSaA chlh pSuy ds ekè;e ls 7]50]000 [kkrs [kksyus ds lkis{k 18]47]754 [kkrs [kksys tk pqds gSaA

ç/kuea=kh tu&/u ;kstuk (PMJDY)varxZr çxfr

cSad us ekuuh; ç/kuea=kh }kjk ?kksf"kr ç/kuea=kh tu&/u ;kstuk dks vaxhdkj djrs gq, 35-30 yk[k [kkrs [kksy fn;s gSa] ftuesa ls 17-85 yk[k [kkrs xzkeh.k {ks=kksa esa vkSj 17-45 yk[k [kkrs 'kgjh {ks=kksa esa gSaA bl ;kstuk varxZr 31-03-2016 rd `892-16 djksM+ dk tek laxzg.k gks pqdk gS ,oa 31-36 yk[k #is MsfcV dkMZ tkjh fd, tk pqds gSaA 'kwU; 'ks"k okys [kkrksa dh la[;k 26-95% gSA

cSad }kjk fnukad 31-03-2016 rd 1754 tu&/u [kkrksa esa `54-25 yk[k dk vf/fod"kZ Lohd`r fd;k tk pqdk gS ftldh vf/dre lhek #i;s 5000@& gSA

#is MsfcV dkMZ] tks fd ekLVj dkMZ ;k ohlk MsfcV dkMZ dk Hkkjrh; :ikUrj.k gS o ftlesa `1-00 yk[k dk vkdfLed nq?kZVuk chek varfuZfgr (inbuilt) gS] [kkrk/kjdksa dks miyC/ gSA

ç/kuea=kh lqj{kk chek ;kstuk (PMSBY)@ ç/kuea=kh thou T;ksfr chek ;kstuk (PMJJBY)@ vVy isa'ku ;kstuk (APY) varxZr çxfr

foÙkh; o"kZ ds nkSjku ekuuh; ç/kuea=kh }kjk rhu lkekftd lqj{kk ;kstukvksa ;Fkk ç/kuea=kh lqj{kk chek ;kstuk (PMSBY)] ç/kuea=kh thou T;ksfr chek ;kstuk (PMJJBY) o vVy isa'ku ;kstuk (APY) dk 'kqHkkjaHk fd;k x;kA ,lchchts us PMSBY, PMJJBY o APY varxZr Øe'k% 561362] 168216 ,oa 27414

vkosnu iathd`r fd, gSA 'kk[kkvksa }kjk bu ;kstukvksa esa vf/dre vkosnu iathd`r djus ds fy, fu;fer dSai ,oa ykWfxu fnol dk vk;kstu fd;k x;k gSA PMSBY ,oa PMJJBY esa çkIr nkoksa dk le; ij fuiVku fd;k tkrk gSA fnukad 31-03-2016 rd ,lchchts }kjk PMSBY esa 54 ,oa PMJJBY esa 275 nkoksa dk fuiVku fd;k tk pqdk gSA foÙkh; o"kZ esa ih,iQvkjMh, }kjk vVy isa'ku ;kstuk ds f}rh; pj.k dk;kZUo;u esa ,lchchts dks loZJs"B çn'kZu (lkoZtfud {ks=k cSadksa esa r`rh; LFkku) iqjLdkj çnku fd;k x;k gSA

mi lsok {ks=k (SSA) dojst dh fLFkfr

gekjs cSad dks jktLFkku esa gekjs lsok {ks=k ,oa vU; jkT;ksa esa 1948 mi lsok {ks=k (SSA) vkoafVr fd, x, gSaA bues ls 1935 mi lsok {ks=k (SSA) jktLFkku esa gSaA cSad }kjk lHkh mi lsok {ks=kksa (SSA) dks 'kk[kk,¡ [kksydj vFkok dkWiksZjsV @O;fDrxr ch-lh- yxkdj doj dj fy;k x;k gSA

foÙkh; lk{kjrk

,lchchts ds vxz.kh ftyks eas 9 foÙkh; lk{kjrk o lk[k ijke'kZ dsaæ (FLCC) gS ,oa 31-03-2016 rd 701 ijke'kZ dSaiksa dk vk;kstu fd;k x;k gS ftuesa 63418 O;fDr;ksa dks ijke'kZ fn;k x;k gSA buesa ls 20816 O;fDr cSafdax ç.kkyh ls tqM+ pqds gSa vkSj 11249 O;fDr lk[k lgc¼rk ls ykHkkfUor gq, gSaA gekjh xzkeh.k 'kk[kk,¡ fu;fer :i ls xzkeh.kksa ls feydj foÙkh; lk{kjrk dSai vk;ksftr dj jgh gSaA lHkh ;kstukvksa dk O;kid çpkj@çlkj lqfuf'pr fd;k tkrk gS rFkk bues foÙkh; lk{kjrk lkexzh forfjr dh tkrh gSA

çR;{k ykHk varj.k (DBT / DBTL)

gekjh lHkh 'kk[kk,¡ [kkrksa esa vk/kj lhfMax dk dk;Z ,dy ,oa lkewfgd (bulk) :i ls djus esa leFkZ gSaA çR;{k ykHk varj.k (DBT) ds fy, gekjh ukfer uksMy 'kk[kk

20 2120 2120 21

crore, out of which loans up to `10 lacs given to MSE units are `1553 crore.

Bank is extending collateral free loans up to `1.00 crore to MSE sector under CGTMSE Scheme of Credit Guarantee Trust, which provides 50% to 85% guarantee cover on eligible MSE. Bank has covered 7802 accounts amounting to `238 crore during the FY 2015-16 under CGTMSE.

PRIORITY SECTOR LENDING (PSL)

The Priority Sector Advances of Bank is 41.52% of the Adjusted Net Bank Credit (ANBC) as at the end of 31st March 2016, as against the RBI stipulation of 40%. In value terms priority sector advances stood at `29677 crore as against `27844 crore as at the end of March 2015. In line with RBI /GOI directives/policies, lending to Priority Sector Advances is Bank’s prime concern for equitable and sustainable economic development of the neglected sectors of the economy. To meet the specific need of this sector, Bank is sensitizing the operating functionaries from time to time to give special attention to Agriculture, MSE, Education, Housing, Export Credit etc.

PROGRESS UNDER FI PLAN (2013-16)

As per RBI FIP Plan (2013-16), the Bank was required to cover 7348 villages of population less than 2000 up to 31.03.2016 and all these villages have been covered by BC/ Branches. As against the target of opening of 490 rural branches up to 31.03.2016, the Bank has opened 508 rural branches. 18,47,754 accounts have been opened through BC channel against the

target of 7,50,000.

PROGRESS UNDER PMJDY

The bank took the PMJDY Scheme announced by the Hon'ble Prime Minister in true spirit and 35.30 lac accounts have been opened under PMJDY, out of which 17.85 lac accounts are in rural areas and 17.45 lac accounts are in urban areas. Deposits of `892.16 crore have been mobilised and 31.36 lac RuPay cards have been issued under PMJDY up to 31.03.2016. Percentage of zero balance accounts is 26.95%.

As on 31.03.2016, `54.25 lac in 1754 accounts has been extended by SBBJ to the Jan Dhan account holders in the form of overdraft with maximum limit of `5000/-.

RuPay debit card, the Indian version of Mastercard or Visa debit cards, having inbuilt accidental insurance cover of `1.00 lac is available to account holders.

PROGRESS UNDER PMSBY/PMJJBY/APY

Three social security schemes namely PMSBY, PMJJBY & APY were launched by the Hon'ble Prime Minister during the financial year. SBBJ has registered 5,61,362, 1,68,216 & 27,414 applications in PMSBY, PMJJBY & APY respectively. Branches have organised regular camps & login day to source maximum applications of these schemes. The claims received in PMSBY & PMJJBY are settled timely. Till 31.03.2016, 54 claims in PMSBY & 275 claims in PMJJBY have been settled by SBBJ. During the FY 2015-16, PFRDA has awarded SBBJ as 3rd best performing bank in the PSBs category under APY Phase-II.

STATUS OF SSA COVERAGE

The Bank has been allotted 1948 SSAs (Sub Service Area) in our Service Area in Rajasthan & in other States. Out of this, 1935 SSAs are in Rajasthan. The Bank covered all these SSAs either by opening of Branches or by engagement of Corporate/ Individual BCs.

FINANCIAL LITERACY

The Bank has 9 FLCCs in its Lead District and during the financial year, up to 31.03.2016, 701 counseling camps have been organised and 63,418 people counseled in such programs. Out of these, 20,816 people are linked to banking system and 11,249 people have benefited with credit linkage. Our rural branches regularly meet the villagers and hold financial literacy camps. Wide publicity is ensured and financial literacy material is distributed in those camps.

DIRECT BENEFIT TRANSFER (DBT/DBTL)

All our branches are enabled for individual & bulk seeding of Aadhaar numbers in accounts. Our nodal branch for DBT is uploading the seeded data on NPCI mapper on daily basis. Till 31.03.2016, a total number of 48,23,473 Aadhaar have been seeded. Out of total 35,30,374 PMJDY accounts, Aadhaar have been seeded in 19,80,098 accounts.

Till 31.03.2016, a total number of 2,49,79,124 DBT/DBTL records have been received, out of which 2,45,98,445 records have been processed.

LEAD BANK SCHEME

As per directions of RBI, our Bank

22 2322 2322 23

NPCI eSij nSfud vk/kj ij lhMsM MkVk dks viyksM dj jgh gSA fnukad 31-03-2016 rd 48]23]743 [kkrksa esa vk/kj uacj tksM+us dk dk;Z fd;k tk pqdk gSA dqy 35]30]374 PMJDY [kkrksa esa ls 19]80]098 [kkrksa esa vk/kj uacj tksM+s tk pqds gSaA fnukad 31-03-2016 rd dqy 2]49]79]124 DBT/DBTL fjdkWMZ çkIr gq;s gSa ftuesa ls 2]45]98]445 fjdkWMZ çlaLd`r fd, tk pqds gSaA

ekxZn'khZ cSad ;kstuk

Hkkjrh; fjtoZ cSad ds funsZ'kksa dh vuqikyuk esa gekjk cSad jktLFkku ds 9 ftyksa ;Fkk chdkusj] ckM+esj] guqekux<] tSlyesj] tkyksj] ikyh] fljksgh] jktleUn ,oa mn;iqj esa ekxZn'khZ cSad ds mÙkjnkf;Ro dk fuokZg dj jgk gSA cSad okf"kZd lk[k ;kstuk dh rFkk Hkkjr ljdkj] jktLFkku ljdkj o ukckMZ }kjk ykxw dh x;h fofo/ fodklksUeq[kh ,oa xjhch mUewyu ;kstukvksa ds dk;kZUo;u o fuxjkuh@leh{kk esa dk;Zjr gSA 2015&16 dh okf"kZd lk[k ;kstuk varxZr 9 ekxZn'khZ ftyksa dks vkoafVr `6382-58 djksM+ ds y{; ds lkis{k geus okf"kZd y{;ksa dk 107% çkIr djrs gq, `6831-98 djksM+ forfjr fd, gSaA

lw{e foÙk (Lo;a lgk;rk lewg)

ekpZ 2016 ds var rd cSad us 45965 Lo;a lgk;rk lewgksa dks `209-36 djksM+ dh lk[k lhek,a Lohd`r djrs gq, lk[k lgcí fd;k gS] ftuesa ls 37426 [kkrs efgyk ykHkkfFkZ;ksa ds gSa ftUgsa `175-62 djksM+ dh lk[k lhek Lohd`r dh x;h gSA fnukad 09 ekpZ] 2016 dks ukckMZ t;iqj }kjk vk;ksftr jkT; Lrjh; lEeku lekjksg esa "Status of Micro Finance" vuqlkj gekjs cSad dks okf.kfT;d cSafdax laoxZ varxZr Lo;a lgk;rk lewg esa mRd`"V çn'kZu ds fy, çFke iqjLdkj çnku fd;k x;k gSA

xzkeh.k Lojkstxkj çf'k{k.k laLFkku (vkjlsVh)

xzkeh.k csjkstxkj ;qokvksa dks Lojkstxkj lapkyu lEcU/h dkS'ky çnku djus gsrq gekjs cSad us chdkusj] guqekux<+] ckMesj] tSlyesj] tkykSj] ikyh] fljksgh ,oa ukFk}kjk (ftyk&jktleUn) esa vkB xzkeh.k Lojkstxkj çf'k{k.k laLFkku (vkjlsVh% RSETI) LFkkfir fd, gSa A

ekpZ] 2016 ds var rd bu laLFkkuksa }kjk 46152 mEehnokjksa dks LFkkuh; ekax o vko';drkuqlkj fofHkUu dk;ksaZ lEcU/h çf'k{k.k çnku fd;k x;k gS rFkk dkS'ky laca/h çf'k{k.k çnÙk djk;s tkus ds mijkar 5231 çf'kf{kr mEehnokj fofHkUu jkstxkjksa ls tqM+ x, gSa rFkk 16673 mEehnokjksa us viuk Lo;a dk m|e çkjEHk dj fn;k gS A 11519 O;fDr;ksa dks 7635-30 yk[k dh lk[k lgc¼rk çnku dh gSA

gekjh leLr vkB (8) vkjlsVh dks o"kZ ds nkSjku ^^AA** xzsfMax çkIr gqbZ gSA

vkjlsVh chdkusj dks xzkeh.k fodkl ea=kky;] Hkkjr ljdkj] }kjk fnukad 15-07-2015 dks vkjlsVh fnol ds volj ij vk;ksftr lekjksg esa mRd`"V dk;Zfu"iknu gsrq r`rh; iqjLdkj çnku fd;k x;kA

ljdkj }kjk çk;ksftr ;kstuk,a

ljdkj }kjk çk;ksftr ;kstukvksa varxZr m|fe;ksa dks foÙkiksf"kr djus esa cSad lnk ls gh egRoiw.kZ Hkwfedk fuHkkrk vk jgk gSA jk"Vªh; xzkeh.k vkthfodk fe'ku (NULM) varxZr cSad us 765 ykHkkfFkZ;ksa dks 569-69 yk[k dh jkf'k LohÑr dh gSA blh çdkj çèkkuea=kh jkstxkj l`tu dk;ZØe (PMEGP) varxZr 553 ykHkkfFkZ;ksa dks `2814 yk[k LohÑr fd, x,] ihvksih (PoP) ds vUrZxr 3484 ykHkkfFkZ;ksa dks `1216 yk[k LohÑr fd, x, rFkk jk"Vªh; xzkeh.k vkthfodk fe'ku

(NRLM)ds varxZr 330 ykHkkfFkZ;ksa dks `345-88 yk[k LohÑr fd, x,A

{ks=kh; xzkeh.k cSad

,lchchts }kjk çk;ksftr rRdkyhu e:/jk xzkeh.k cSad (MGB) rFkk vkbZlhvkbZlhvkbZ cSad }kjk çk;ksftr esokM vkapfyd xzkeh.k cSad (MAGB) ds foy; mijkar fnukad 01-04-2014 dks jktLFkku e:/jk xzkeh.k cSad (RMGB) vfLrRo es vk;k] ftldk ç/ku dk;kZy; tks/iqj esa fLFkr gSA cSad blds 15 ftyksa dh vFkZO;oLFkk es çkFkfedrk rFkk xSj& çkFkfedrk çkIr nksuksa gh {ks=kks esa foÙkh; lgk;rk çnku djrs gq, çeq[k Hkwfedk fuHkk jgk gSA

,lchchts vkj,ethch (RMGB) dks çcU/dh; lg;ksx rFkk iqufoZÙk ds ekè;e ls foÙkh; lgk;rk çnku djrk jgk gSA vkj,ethch dh leLr 'kk[kk,¡ lhch,l IysViQkeZ ij dk;Z djrs gq, bysDVªksfud dks"k vUrj.k dh lqfo/k çnku dj jgh gSA vkj,ethch us 5 vkulkbZV ,Vh,e o xzkgdksa dks muds }kj ij cSafdax lqfo/k ds fy, ,d eksckbZy ,Vh,e LFkkfir fd;k gSA ekpZ 2016 ds var esa vkj,ethch dh `7290-26 djksM dh tek,¡ o `5507-52 djksM+ ds vfxze FksA

ljdkjh O;olk;

cSad viuh 306 vf/d`r 'kk[kkvksa ds ekè;e ls jkT;@dsaæ ljdkj ds fy, ljdkjh O;olk; dk dk;Z djrh gSA vk;dj] mRikn 'kqYd] lsokdj] ewY; laof/Zr dj (oSV) vkfn dk HkkSfrd pkyku }kjk ,oa bysDVªksfud rjhds ls laxzg.k fd;k tkrk gSA cSad }kjk dsaæh;Ñr isa'ku çlaLdj.k dsaæ (lhihihlh) dh LFkkiuk dh x;h gS tks fd isa'ku dh x.kuk djus ds lkFk&lkFk lHkh 'kk[kkvks esa isa'kulZ ds [kkrksa esa tek Hkh djrh gSA jktLFkku ljdkj ds deZpkfj;ksa dks jkT; ljdkj }kjk vkWu ykbu osru Hkqxrku djus ds mís'; ls vkWu ykbu Vªstjh 'kk[kk

22 2322 2322 23

has Lead Bank responsibility in nine districts in the State of Rajasthan viz. Bikaner, Barmer, Hanumangarh, Jaisalmer, Jalore, Pali, Sirohi, Rajsamand and Udaipur. The Bank has been implementing and monitoring the Annual Credit Plan and other developmental and poverty eradication schemes launched by the Govt. of India, Govt. of Rajasthan and NABARD. Targets allotted in 9 Lead Districts for Annual Credit Plan to our Bank for the year 2015-16 was 6382.58 crore, against which achievement of our Bank in these lead districts up to March, 2016 is `6831.98 crore, achieving 107% of the annual targets.

MICRO CREDIT (SHGs)

Up to the end of March, 2016 the Bank has credit linked a total of 45965 Self Help Groups with limit sanctioning amount of `209.36 crore, out of which 37426 accounts are of women beneficiaries with limit sanctioning amount of `175.62 crore. Our Bank has been awarded First Prize in Commercial Banking Category for excellent performance in SHG, as per “Status of Micro Finance” by NABARD, Jaipur during the State Level Felicitation Programme held on 9th March, 2016.

RURAL SELF EMPLOYMENT TRAINING INSTITUTES (RSETI)

In order to impart job- oriented skills to rural unemployed youth, the Bank has set-up eight RSETIs at Bikaner, Hanumangarh, Barmer Jaisalmer, Jalore, Pali, Sirohi and Nathdwara (Distt. Rajsamand).

By the end of March, 2016, 46152 candidates have been imparted training for various local demand

jobs in these institutions and 5231 trained candidates have been engaged in various jobs and 16673 trained candidates have started their own ventures. 11519 trained candidates have been credit linked amounting to `7635.30 lac.

Our all eight (8) RSETIs got “AA” grading, conducted during the year.

RSETI Bikaner was awarded Third Prize by the MoRD, GoI, New Delhi for excellent performance on the occasion of RSETI Diwas at New Delhi held on 15.07.2015.

GOVERNMENT SPONSORED SCHEMES

Laying utmost emphasis on Government sponsored schemes, the Bank continued to play a pioneering role in financing entrepreneurs under various government sponsored schemes. Under National Urban Livelihood Mission (NULM scheme), the bank sanctioned amount of `569.69 lacs to 765 beneficiaries. Similarly, under Prime Minister Employment Generation Programme (PMEGP) an amount of `2814 lacs was sanctioned to 553 beneficiaries, under POP amount of `1216 lacs to 3484 beneficiaries and `345.88 lacs to 330 beneficiaries under National Rural Livelihood Mission (NRLM scheme).

REGIONAL RURAL BANK

Rajasthan Marudhara Gramin Bank (RMGB) has come into existence on 01.04.2014 with the amalgamation of the erstwhile Marudhara Gramin Bank (MGB), sponsored by SBBJ and Mewar Anchalik Gramin Bank (MAGB), sponsored by ICICI Bank. The Head Office of the Bank is at Jodhpur. The Bank is playing vital

role in the economy of 15 districts of their area of operation by extending financial assistance to both priority and non priority sectors.

SBBJ provides managerial support and financial assistance by way of refinance etc. to RMGB. All branches of RMGB are on CBS platform and provide Electronic Fund Transfer facility. RMGB has installed its five on site ATMs and one mobile ATM for providing door step banking facility to its customers. RMGB has deposits of `7290.26 crores and advances of `5507.52 crores as on March, 2016.

GOVERNMENT BUSINESS

The Bank conducts Government Business on behalf of State/Central Government departments through 306 Authorized Branches. Income Tax, Central Excise, Service Tax, Value Added Tax (VAT) etc. are collected through physical challans and also through the electronic mode. The Bank has established a Centralized Pension Processing Centre (CPPC) which calculates as well as credits pension to the accounts of pensioners across all the Branches. We also have an Online Treasury Branch for online payment of salary of Rajasthan Govt. employees on behalf of the State Govt. Presently, our Online Treasury Branch is processing 35.71 lacs State Govt. transactions received through 23175 digitally signed files in a month. During 2015-16, the commission income from Government business was `99.51 crore.

INTERNATIONAL BANKING

The Bank provides Foreign Exchange related services to

24 2524 2524 25

Hkh gSA orZeku esa vkWu ykbu Vªstjh 'kk[kk 35-71 yk[k jkT; ljdkj laca/h ysunsu 23175 fMftVy gLrk{kj;qDr iQkbyksa ds ekè;e ls çfrekg fu"iknu dj jgh gSA o"kZ 2015&16 esa jktdh; O;olk; ls `99-51 djksM+ dh deh'ku vk; gqbZA

varjkZ"Vªh; cSafdax

cSad viuh fons'kh fofue; O;olk; gsrq ^ch* Js.kh esa vf/d`r 61 ,oa lHkh ^lh* Js.kh esa vf/d`r 'kk[kkvksa rFkk 4 O;kikj foÙk dsUæh; lalk/u dsUæksa ds usVodZ ds ekè;e ls fu;kZrdksa@vk;krdksa vU; fuoklh ,oa vfuoklh xzkgdksa dks fons'kh fofue; lEcU/h lsok,¡ çnku djrk gSA

gekjk eqEcbZ esa fLFkr fons'kh fofue; ysunsu dsUæ ,oa lHkh ^ch* Js.kh esa vf/d`r 'kk[kk,¡ vk/qfud rduhdh o æqrxkeh lapkj O;oLFkk ls lqlfTtr gSa rFkk fLoÝV }kjk vkil esa ,oa lEiw.kZ fo'o esa fLFkr 750 ls vf/d fons'kh cSadksa ds dk;kZy;ksa ls tqMs+ gq, gSaA cSad ds fo'o dh lHkh çeq[k eqækvksa esa 20 uksLVªks [kkrs gSa ,oa fo'o ds vU; lHkh çeq[k cSafdax lewgksa ls Hkh [kkrk jfgr lEcU/ gSaA vfuoklh Hkkjrh; xzkgdksa gsrq /u&çs"k.k ds fy, fLoÝV] vkWu ykbu çs"k.k lqfo/k o [kkMh ns'kksa esa fLFkr 4 fofue; x`gksa ds lkFk #i;ksa esa Rofjr /u&çs"k.k gsrq xBcU/u gSaA gekjh 231 'kk[kk,a ^osLVuZ ;wfu;u /u çs"k.k* ds Hkqxrku gsrq vf/d`r gSaA