Page 1

Update on recent developmentsUpdate on recent developments

September 2008

Page 2

June 2007

September 2007

June 2008

August 2008

April 2008

January 2008

October 2007

Official disclosure of ultimate

beneficiaries

Capital injection of $95 mn. by

shareholders

New Management Team joined the

Bank

Repayment of syndicated loan -

$135 mn.

Moody’s confirmed recent Bank’s ratings

Eurobonds repayment - $150

mn.

Repayment of syndicated loan -

$133 mn.

Another capital injection of $53.8 mn.

by shareholders

Provisions increased by $50 mn.

Attraction of new funding from Kazyna

and SME Fund

Nurbank Nurbank HighlightsHighlights

Page 3

Nurbank Recent DevelopmentsNurbank Recent Developments

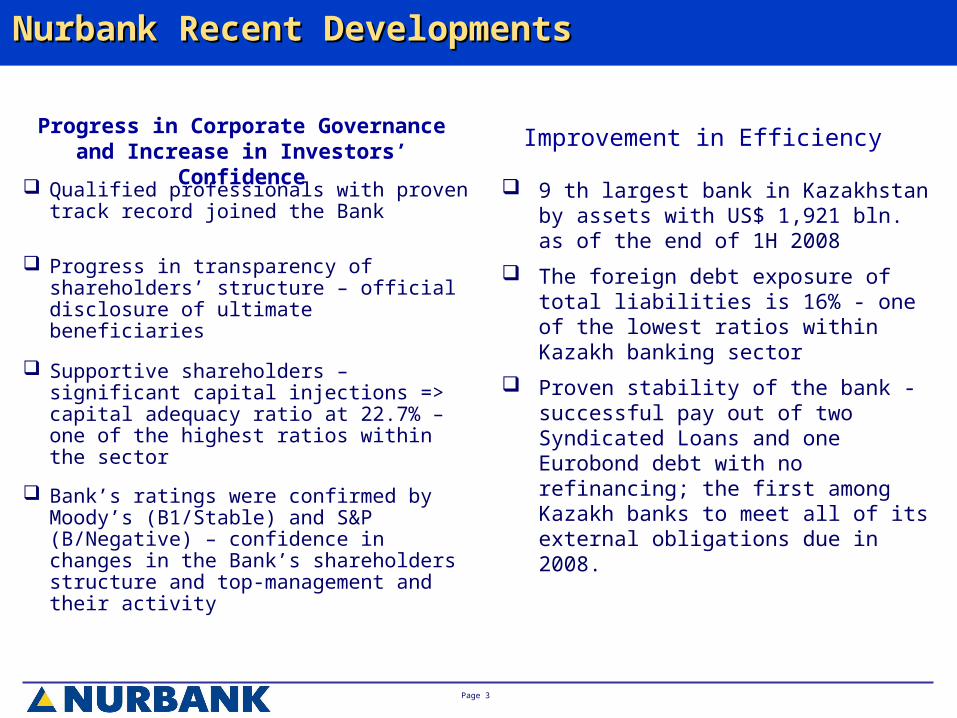

Qualified professionals with proven track record joined the Bank

Progress in transparency of shareholders’ structure – official disclosure of ultimate beneficiaries

Supportive shareholders – significant capital injections => capital adequacy ratio at 22.7% – one of the highest ratios within the sector

Bank’s ratings were confirmed by Moody’s (B1/Stable) and S&P (B/Negative) – confidence in changes in the Bank’s shareholders structure and top-management and their activity

9 th largest bank in Kazakhstan by assets with US$ 1,921 bln. as of the end of 1H 2008

The foreign debt exposure of total liabilities is 16% - one of the lowest ratios within Kazakh banking sector

Proven stability of the bank - successful pay out of two Syndicated Loans and one Eurobond debt with no refinancing; the first among Kazakh banks to meet all of its external obligations due in 2008.

Improvement in Efficiency Progress in Corporate Governance and Increase in Investors’ Confidence

Page 4

Shareholders’ StructureShareholders’ Structure

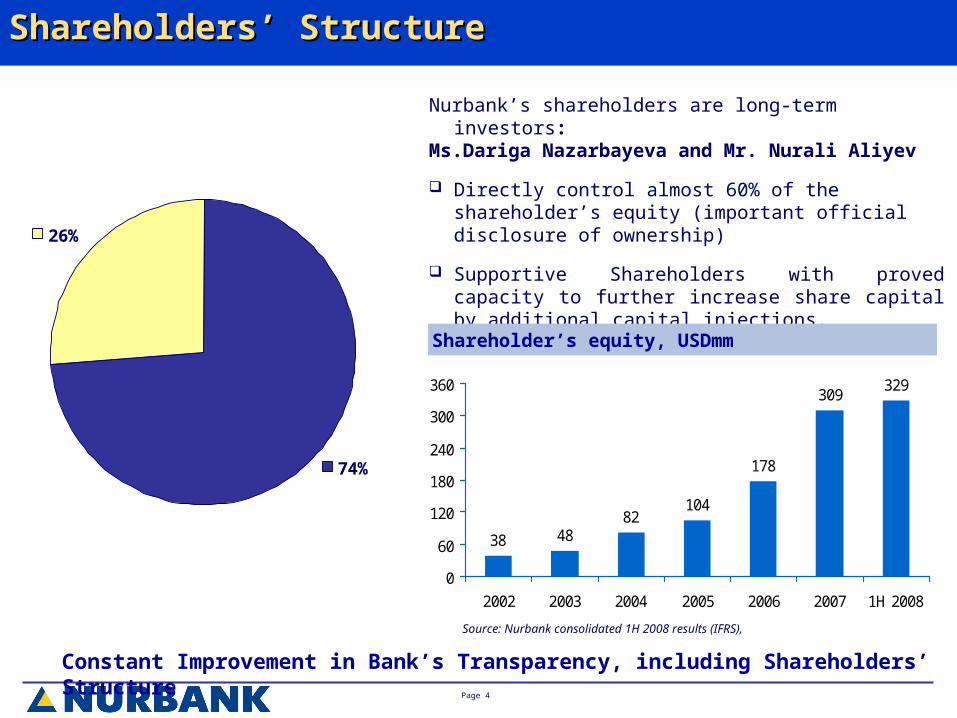

74%

26%

Nazarbayeva D.Aliev N.

Minorities

Constant Improvement in Bank’s Transparency, including Shareholders’ Structure

Nurbank’s shareholders are long-term investors:Ms.Dariga Nazarbayeva and Mr. Nurali Aliyev

Directly control almost 60% of the shareholder’s equity (important official disclosure of ownership)

Supportive Shareholders with proved capacity to further increase share capital by additional capital injections.

Shareholder’s equity, USDmm

38 4882

104

178

309329

0

60

120

180

240

300

360

2002 2003 2004 2005 2006 2007 1H 2008

Source: Nurbank consolidated 1H 2008 results (IFRS),

Page 5

Management Board Management Board

Organizational structure revised according to the best international practice with Focus on Client Orientation

Chairman of the Management Board (CEO)

Nurmukhamed Bektemissov

SME Business

Assain K. Baikhanov

Managing Director

Retail Business

Tatyana I. Belozerceva

Managing Director

Corporate Business

Zhanbolat U. Nadyrov

Managing Director Investment Banking

Daniyar Zh. Nurskenov

Managing Director

CIO

Andrey A. Chuchelov

CFO

Orsolya Ekler

COO

Irina I. Bogatkina

Page 6

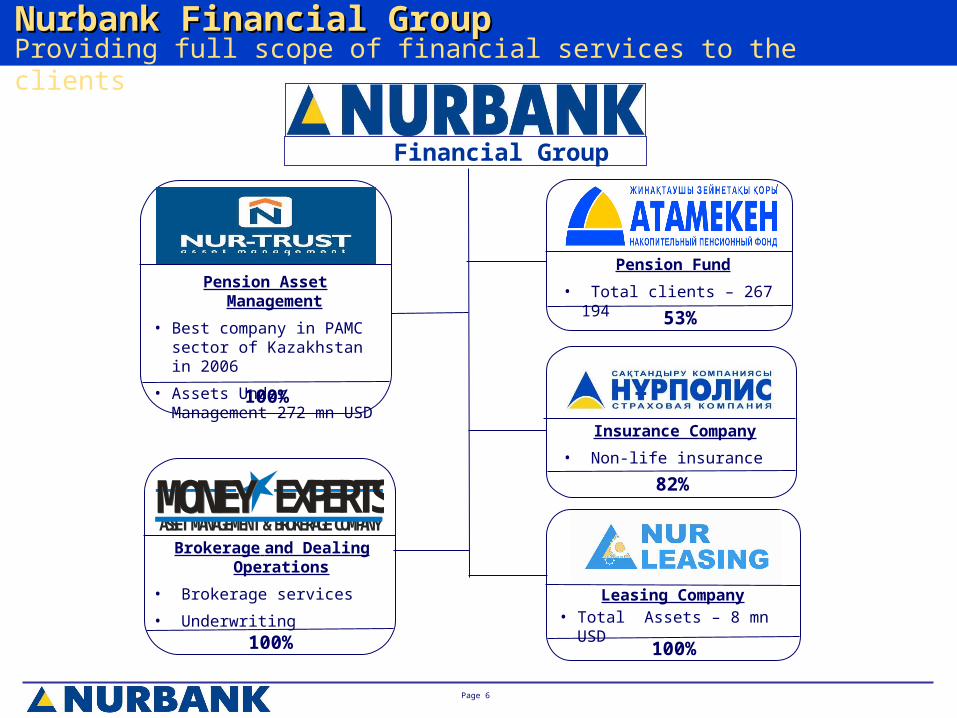

Nurbank Financial GroupNurbank Financial GroupProviding full scope of financial services to the clients

Financial Group

Pension Asset Management

• Best company in PAMC sector of Kazakhstan in 2006

• Assets Under Management 272 mn USD100%

Leasing Company• Total Assets – 8 mn USD

100%

Pension Fund

• Total clients – 267 194

53%

Brokerage and Dealing Operations

• Brokerage services

• Underwriting100%

Insurance Company

• Non-life insurance

82%

ASSET MANAGEMENT & BROKERAGE COMPANY EXPERTSMONEY EXPERTSMONEY

Page 7

RUSSIA

MO

NG

OL

IA

CHINA

KYRGYZSTAN

UZBEKISTAN

TURKMENISTAN

AZERBAIJAN

Kyzyl-Orda

Shymkent

Taraz

Almaty

Taldy-Korgan

Ust-Kamenogorsk

Pavlodar

ASTANA

Aktobe

Uralsk

Atyrau

Aktau

Kokshetau

Petropavlovsk

Kostanay

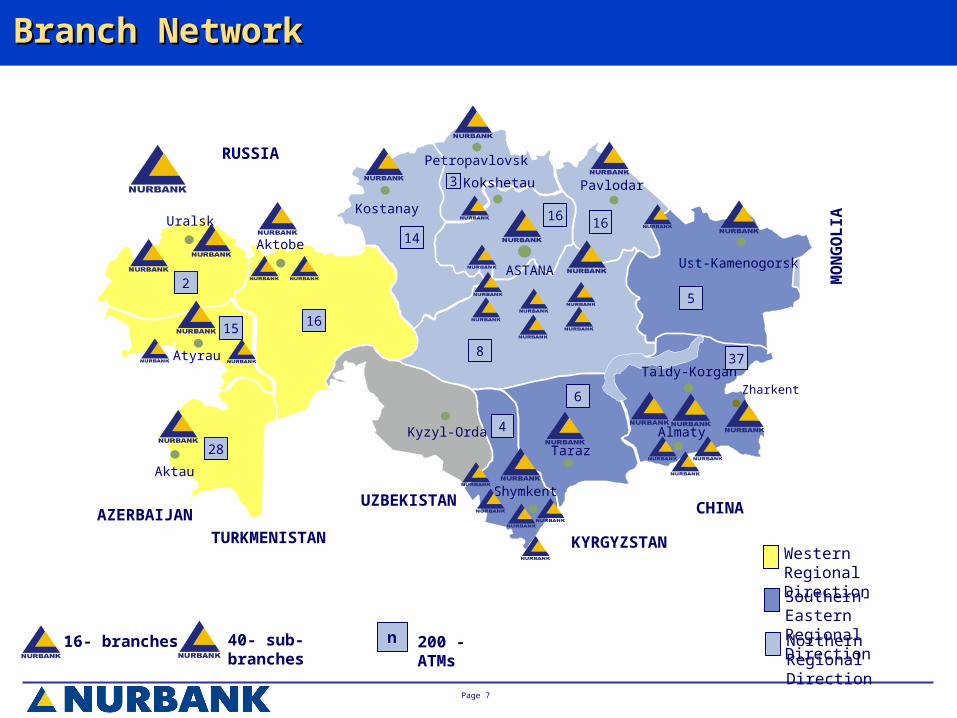

16- branches 40- sub-branches

Zharkent

28

2

15

200 - ATMs

16

16

14

37

16

5

6

4

3

8

n Northern Regional Direction

Southern-Eastern Regional Direction

Western Regional Direction

Branch NetworkBranch Network

Page 8

Nurbank’s Position vs. Kazakh PeersNurbank’s Position vs. Kazakh Peers

Stable Position Among Second-Tier Banks with Strong CapitalizationAs of 01.08.08

Source: AFN data as of 01.08.08, unaudited, unconsolidated data; Exchange rate KZT/USD = 120.18

Rank Bank (US$ million) Equity

1 BTA 3 505

2 KKB 2 278

3 Halyk 1 436

4 Alliance 1 399

5 ATF 861

6 BCC 632

7 Temir 475

8 NURBANK 315

9 Sberbank 283

10 Caspian 261

11 Eurasian 206

Rank Bank (US$ million) Assets

1 BTA 24 720

2 KKB 21 347

3 Halyk 14 613

4 Alliance 8 846

5 ATF 8 737

6 BCC 7 503

7 Temir 2 656

8 Caspian 2 084

9 NURBANK 1 840

10 Eurasian 1 791

11 ABN AMRO 1 343

Page 9

Key FinancialsKey Financials

Source: Nurbank Audited report 2007; Nurbank consolidated 1H 2008 results (IFRS), *Bank only **k2 ratio for the Bank ***overdue more than 90 days

US$ mm or % 2006 2007 07/06

YoY % growth

1H 2008

Total Assets 1 596 1 652 3.5% 1 921

Total Loans, net 1 133 1 279 13.0% 1266

Total deposits 589 498 -15.0% 1 072

Shareholder’s Equity 178 309 74.0% 329

Net Interest Income (before provisions)* 43 85 98.0% 38

Net Income 11 25 127.0% (22)

ROAE 7.3% 10.2% - (13.4)%

ROAA 0.9% 1.5% - (2.3)%

Capital Adequacy (k2)** 16.0% 20.9% - 22.7%

Net Interest Margin (before provisions)* 4.3% 6.2% - 5.4%

Cost/Income Ratio** 54.2% 45.0% - 57.2%

NPL*** 1.56% 3.5% - 4.1%

Page 10

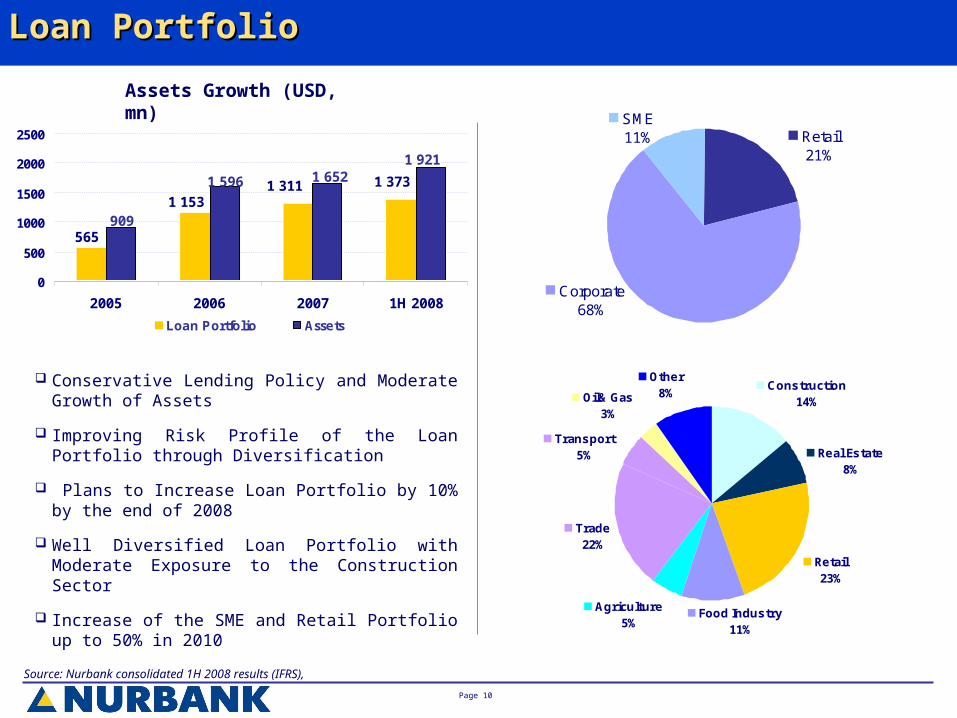

Conservative Lending Policy and Moderate Growth of Assets

Improving Risk Profile of the Loan Portfolio through Diversification

Plans to Increase Loan Portfolio by 10% by the end of 2008

Well Diversified Loan Portfolio with Moderate Exposure to the Construction Sector

Increase of the SME and Retail Portfolio up to 50% in 2010

SME11% Retail

21%

Corporate68%

Agriculture5%

Transport5%

Trade22%

Real Estate8%

Retail23%

Construction14%Oil& Gas

3%

Food Industry11%

Other 8%

Loan Portfolio Loan Portfolio

565

1 1531 311 1 373

1 9211 6521 596

909

0

500

1000

1500

2000

2500

2005 2006 2007 1H 2008

Loan Portfolio Assets

Assets Growth (USD, mn)

Source: Nurbank consolidated 1H 2008 results (IFRS),

Page 11

Corporate BusinessCorporate Business

Priority to Key Corporate Clients with Retail Exposure to Cross-Sell Retail Banking

Focus on Trade Finance to Decrease Funding Costs to the Clients

Investment Banking Solutions for the Large Customers

Corporate Loan Portfolio (USD, mn)

643,0

858,0933,4

0,0

200,0

400,0

600,0

800,0

1000,0

1200,0

2006 2007 1H 2008

Source: Nurbank unconsolidated 1H 2008 results (IFRS)

Corporate deposits (USD, mn)

33,9

292,8

73,2

606,8

-

200,0

400,0

600,0

800,0

Current Accounts Time Deposits

2007 1H 2008

Page 12

SME BusinessSME Business

SME Loan Portfolio (USD, mn)

299,6

170,3 151,0

0,0

100,0

200,0

300,0

400,0

2006 2007 1H 2008

Source: unconsolidated 1H 2008 results (IFRS)

SME is the Key Area for the Bank’s Growth

Decrease in the Loan Portfolio is Related to Reclassification of

the Loan Portfolio to Identify “pure” SME clients so that to Serve

Them Faster and Better

Plans to Increase SME Loan Portfolio up to USD265mm by the end 2008

SME Deposits (USD, mn)

12,6

71,5

183,5

77,3

-

50,0

100,0

150,0

200,0

250,0

Current Accounts Time Deposits

2007 1H 2008

Page 13

Retail BusinessRetail Business

Retail Loan Portfolio (USD, mn)

210,5

283,1 288,3

0,0

50,0

100,0

150,0

200,0

250,0

300,0

350,0

2006 2007 1H 2008

Source: unconsolidated 1H 2008 results (IFRS)

Improving Confidence of Individuals in the

Bank translates into Increase of the Retail

Deposit Base

Healthy Risk Profile of Retail Loan

Portfolio - No Unsecured Consumer

Finance

Retail Deposits (USD, mn)

65,6

22,1

108,6

19,9

0,0

20,0

40,0

60,0

80,0

100,0

120,0

Current Accounts Time Deposits

2007 1H 2008

Page 14

Source: Nurbank unconsolidated 1H 2008 results

Deposit base growth (USD mn)

Deposit BaseDeposit Base

Monthly deposit base growth(USD mn)

Deposit base growth - growing investors’ confidence due to new shareholders’ structure

and top-management strengthening

61% growth during the second half of 2007 and 115% growth during first half of 2008

289

498

1 069

0

200

400

600

800

1 000

1 200

1H 2007 2007 1H 2008

(US

$m

n)

289

310 365

350 43

3

486

431 49

8 557 70

6 858

721 80

0

1069

149%177%

270%

7% 26%21%50%

68%49%

72%93%

144%

197%

0

200

400

600

800

1 000

1 200

01

.06

.07

01

.07

.07

01

.08

.07

01

.09

.07

01

.10

.07

01

.11

.07

01

.12

.07

01

.01

.08

01

.02

.08

01

.03

.08

01

.04

.08

01

.05

.08

01

.06

.08

01

.07

.08

(US

$m

)

0%

50%

100%

150%

200%

250%

300%

%

deposit base growrth from beg. 2H 2007

Page 15

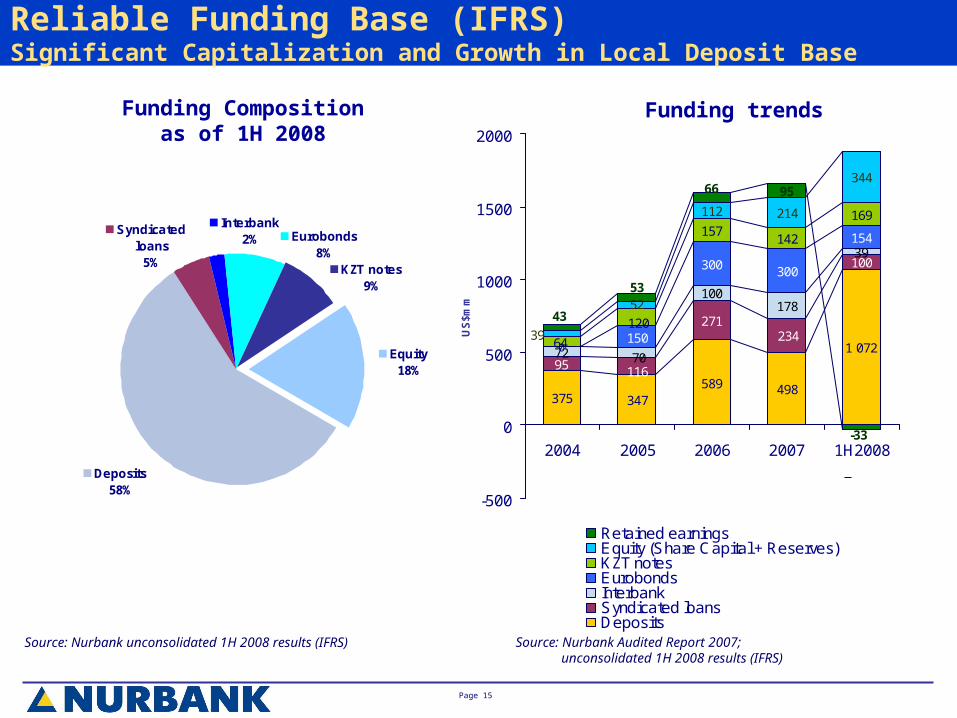

Syndicated loans

5%

Deposits 58%

KZT notes 9%

Interbank2%

Equity18%

Eurobonds 8%

Reliable Funding Base (IFRS)Significant Capitalization and Growth in Local Deposit Base

375 347589 498

95

271

72

100178

39

150

300

154157

34495

1 072

100

234

11670

0

300

169

142

120

64

52

39

112 214

-33

66

53

43

-500

0

500

1000

1500

2000

2004 2005 2006 2007 1H2008U

S$m

m

Retained earningsEquity (Share Capital + Reserves)KZT notesEurobondsInterbankSyndicated loansDeposits

Source: Nurbank unconsolidated 1H 2008 results (IFRS)

Funding Compositionas of 1H 2008

Source: Nurbank Audited Report 2007; unconsolidated 1H 2008 results (IFRS)

Funding trends

Page 16

Foreign Debt RepaymentForeign Debt Repayment

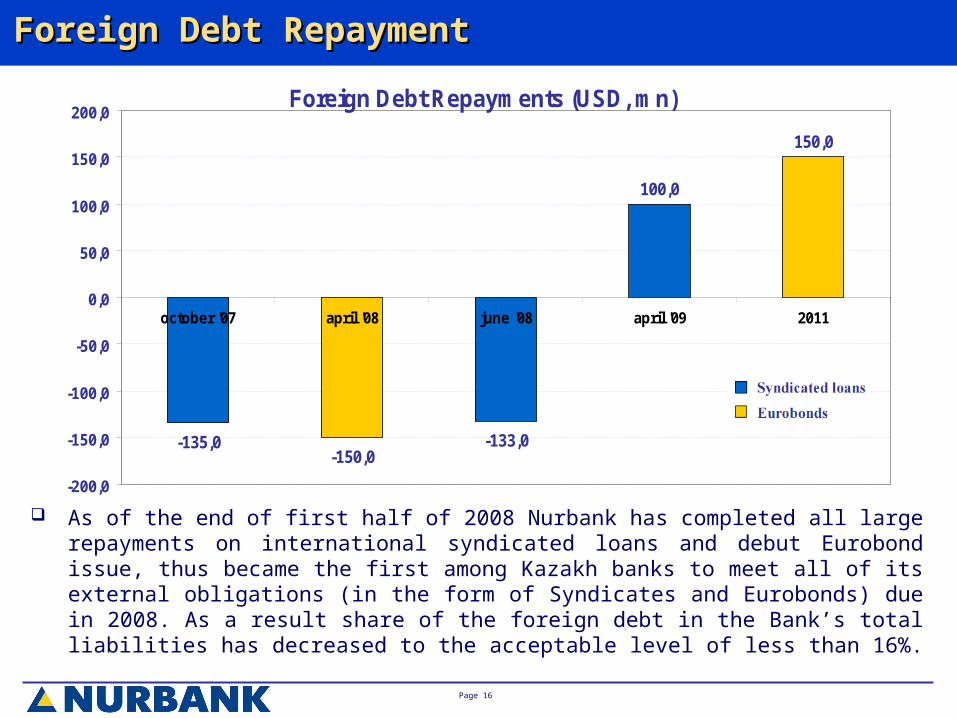

Foreign Debt Repayments (USD, mn)

-135,0-150,0

-133,0

100,0

150,0

-200,0

-150,0

-100,0

-50,0

0,0

50,0

100,0

150,0

200,0

october '07 april '08 june '08 april '09 2011

As of the end of first half of 2008 Nurbank has completed all large repayments on international syndicated loans and debut Eurobond issue, thus became the first among Kazakh banks to meet all of its external obligations (in the form of Syndicates and Eurobonds) due in 2008. As a result share of the foreign debt in the Bank’s total liabilities has decreased to the acceptable level of less than 16%.

Page 17

StrategyStrategy

► Enhance cross sales and create investment banking products for corporate clients

► Strengthen risk manage-ment and improve operating efficiency

► Penetrate retail and SME businesses through selective expansion into designated regions and improved servicing of the clients

► Strengthen local funding through increasing retail and corporate deposit base.

► Increase the volumes of trade finance to provide clients with low-cost funding

► Expand current exposure to

the local capital markets

Expanding SME and Retail

Business with Focus

on Local Funding

Page 18

ContactsContacts

• Mrs. Sholpan Sakhvaliyeva

• Executive Director

• International Department

• Tel. 007 (7272) 599 - 710 ext. 5330

• E-mail: [email protected]

• Mr. Daniyar Nurskenov

• Managing Director

• Capital Markets and Investor Relations

• Tel. 007 (7272) 599 - 711

• E-mail: [email protected]

Recommended