Opportunities in the Indian Packaging Sector

May 2020

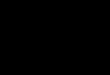

Major Pharma Clusters

States with more than5000 registered food processing units

States with two or more operational Mega Food Parks

Uttarakhand

Andhra Pradesh

Tamil Nadu

HyderabadMaharashtra

Baddi-Solan

Ahmedabad Madhya Pradesh

Sources: Federation of Indian Chambers of Commerce and Industry (FICCI), Center for Market Research & Social Development, Mordor Intelligence, Ministry of Food Processing Industries, Invest India

INDIAN PACKAGING SECTOR: OVERVIEW

4.3

20

42

India Taiwan Germany

Packaging Consumption Per Capita (in kilogram)

India and the World

CHF 75 billion Indian Packaging

Sector (2020)

CHF 205 billion Indian Packaging

Sector (2025 E)

22,000Registered Packaging Companies in India

85%Manufacturers in the small

and mid-size segment

Market Size Sector Hubs

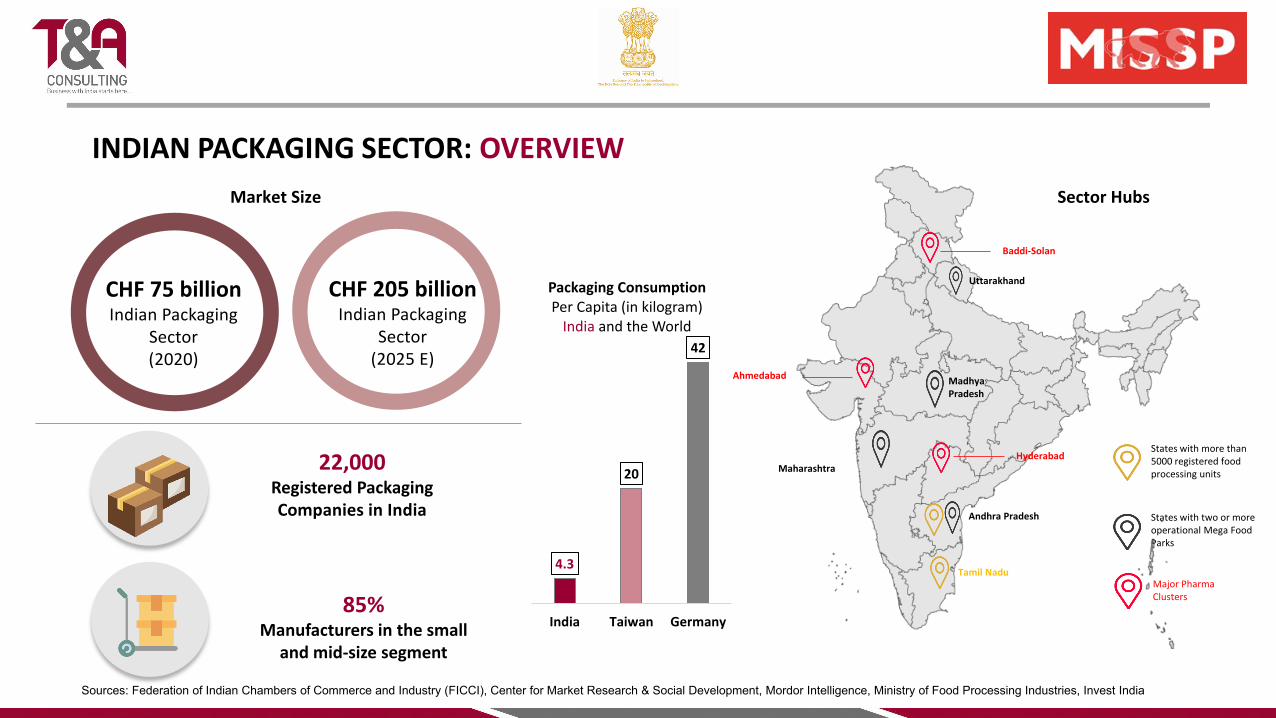

Sources: Euromonitor, Wisconsin Economic Development Corporation, Goldstein Research

38%

32%

7%

13%

10%

Beverages Packaging(Segments by material used)

Rigid Glass Metal cans Cartons Caps

Soft drinks sub-segment is expected to grow 13% till2023 from current 44 billion units in 2019. Whereas, teaand hot beverages packaging sub-segment will grow at6% rate from 2019 to 2023 riding on premium and eco-friendly product demand.

45%

25%

10%

10%

10%

Packaging Materials and MachineryEnd Users (by share of volume)

Food Processing

Pharmaceutical

Personal andHomecareProducts

Hot Beverages

IndustrialProducts

Beauty and Personal Care Packaging(Trends)

Dispensing Systems

Airless Packaging

Smaller Pack Sizes

Home Care Packaging(Trends)

Stand-up Pouches

Refill Packaging

Innovation in Pack Formats

KEY SEGMENTS: END CONSUMERS

Sources: Federation of Indian Chambers of Commerce and Industry (FICCI), Export Import Data Bank, Department of Commerce, Interpack Alliance, Packaging Gateway

36%

64%

Packaging Sector Segments(by value)

Rigid Flexible

Segmentation by type of material

55%20%

10%

15%

Packaging Materials Segments (by revenue share in %)

Plastic

Paper andcardboardGlass

Other

Import Trend of Packaging Materials

4068

101

349

4780 75

272

0

50

100

150

200

250

300

350

Sacks and bagsof jute and

other textilematerials

Glass bottles,jars, and lids

Paper cartons,boxes, bags

includingwrapping paper

Plasticpackaging goods

Import of Packaging Materials in India (values in CHF million)

2018-19 2019-2020(Apr-Jan)

KEY SEGMENTS: TYPE OF MATERIALS

Sources: Avendus

40%60%

Automation in Corrugated Segment (Share in capacity)

Automatic lines

Semi automatic / manual line

KEY SEGMENTS: CORRUGATED BOXES

56% Corrugated

Polybag, others44%

Transit Packaging Material Segments (Share in Indian Market) CHF 660 billion

Market size of TransitPackaging for E-commercein India (2020)

USA and Canada

1,30012,000

India

Number of manufacturingunits of Corrugated boxes:A Comparison

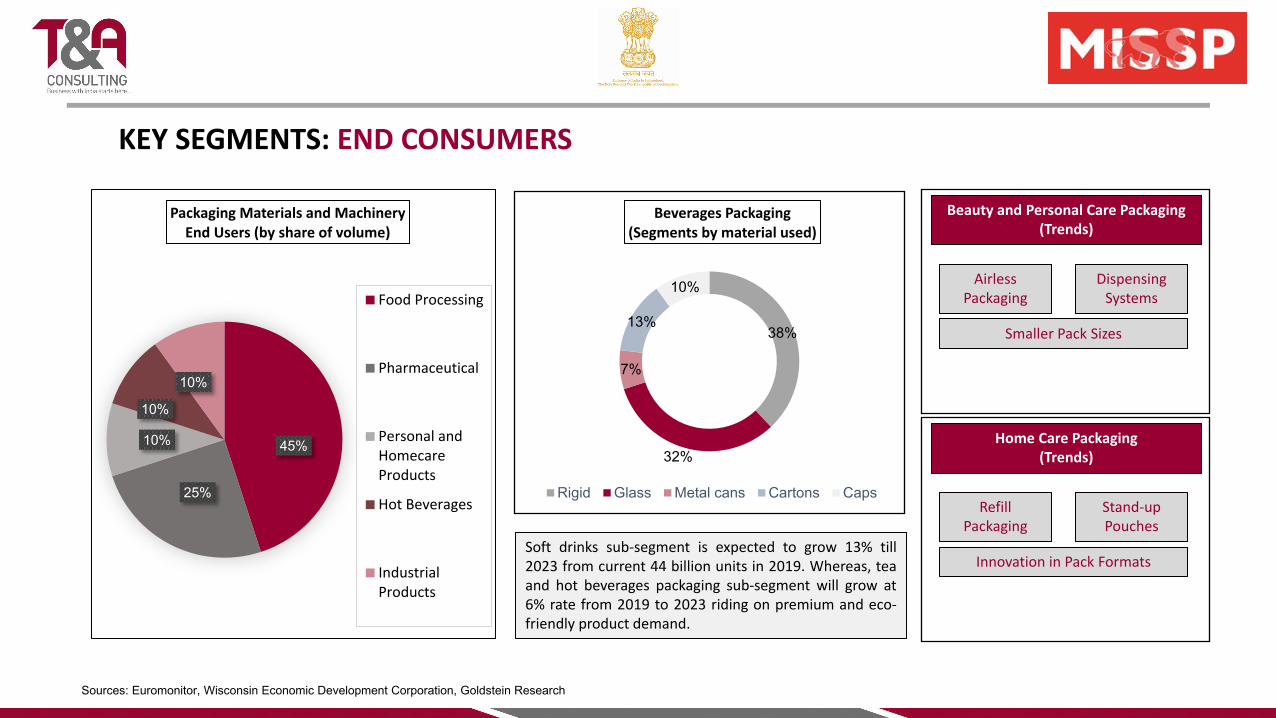

Import Trend of Packaging Machinery

251229

144

11

198 190

105

80

50

100

150

200

250

300

Filling, sealing andlabelling

Paper packaging Wrapping and heat-shrink

Container and bottlecleaning and drying

Import of Packaging Machinery in India (values in CHF million)

2018-19 2019-2020(Apr-Jan)

Sources: Export Import Data Bank, Department of Commerce, Icegate

Customs Duty on Packaging Machinery

Sl. No.

Equipment HS Code Effective Duty (in %)

1 Bottle cleaning and drying 842220 38.0

2 Filling, sealing, capsuling 842230 35.1

3 Wrapping including Heat-shrink wrapping machinery

842240 35.1

4 Paper packaging machinery 8441 27.7

5 Automatic labelling machinery

84798999 27.7

PACKAGING MACHINERY

Sources: India Retailing, Media releases

01

KEY TRENDS: IN PACKAGING TECHNOLOGY & MATERIALS

01

Growing shift towards

Bioplastics owing to

range of applications.

PLA (Polylactic acid) is

the most common

bioplastic in use in India.

02

Mono-material

packaging technology to

develop ‘Synthetic

Paper’ which results in a

recyclable packaging

product with better

longevity than paper.

03

Focus on functionality of

products to ensure

reusability and re-

closability to improve

product experience.

.

04

Equipment for product

pack design, labelling

especially for food

processing industry

where packaging is a key

differentiator.

05

Consumption of Paper

based packaging

material rising and Kraft

paper and cardboard

volumes are expected to

be 6.7 million tonnes by

2021.

PILLARS OF

GROWTH

• Compliance with Good Manufacturing Practices (GMP) have led the Pharmaceuticalindustry to upgrade packaging processes and systems

• Industry is more open to product safety and packaging standards are being adoptedgradually

Growth of Indian Pharmaceutical Industry

• Government’s plan to phase out single use plastics has sparked innovation• Lower tax rates for new manufacturing units among government’s strategies to make

India a global manufacturing hub

Government Initiatives

• Growing inclination of population towards Ready to Cook and Ready to Cook foodproducts

• Retail, Fast Moving Consumer Goods (FMCG) riding the digital India drivenconsumption wave

Evolving Consumer Behaviour

• Major organizations including Indian Railways, Air India, Zomato, Amazon India,Nestle planning to shun plastic for eco-friendly options

• Sustainable sourcing, packaging and labelling are emerging as key productdifferentiator

Sustainable Sourcing Altering Demand

Sources: Media releases

GROWTH DRIVERS

Sources: Packaging Industry Association of India (PIAI), Ministry of Food Processing Industries (MoFPI), Euromonitor

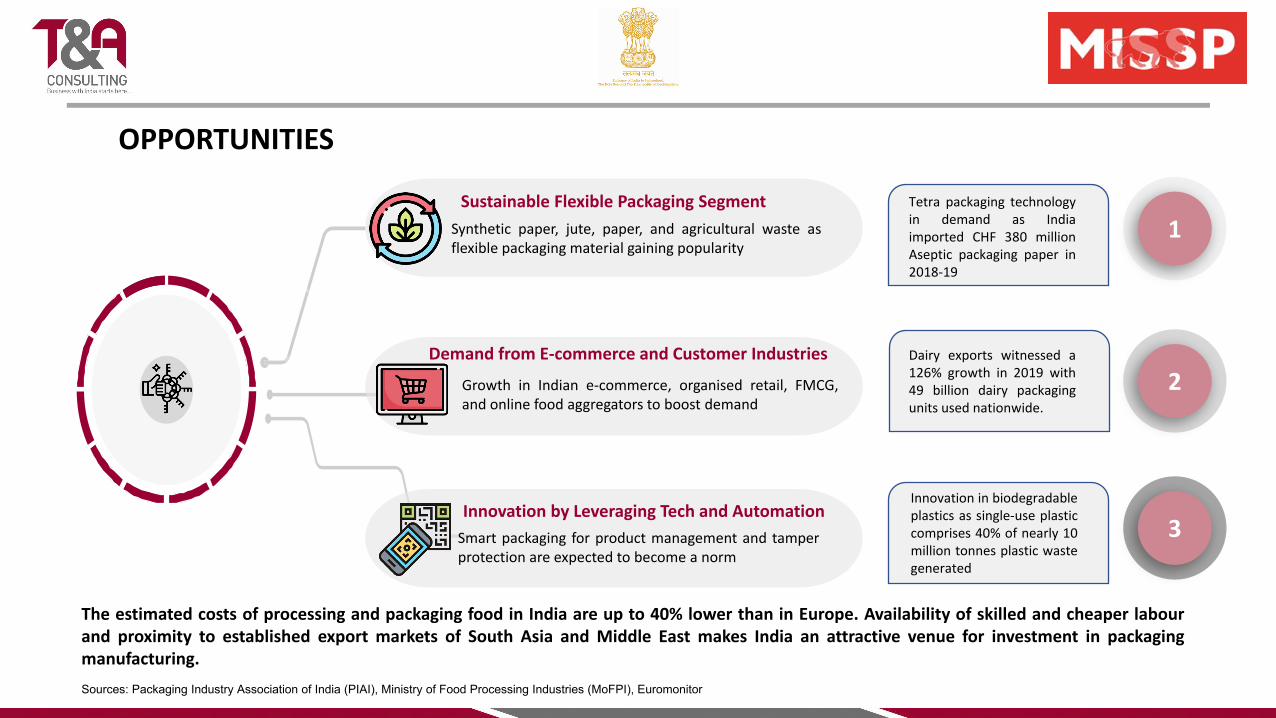

Synthetic paper, jute, paper, and agricultural waste asflexible packaging material gaining popularity

Growth in Indian e-commerce, organised retail, FMCG,and online food aggregators to boost demand

Smart packaging for product management and tamperprotection are expected to become a norm

A

C

Sustainable Flexible Packaging Segment

Demand from E-commerce and Customer Industries

Innovation by Leveraging Tech and Automation

The estimated costs of processing and packaging food in India are up to 40% lower than in Europe. Availability of skilled and cheaper labourand proximity to established export markets of South Asia and Middle East makes India an attractive venue for investment in packagingmanufacturing.

1

2

3

Tetra packaging technologyin demand as Indiaimported CHF 380 millionAseptic packaging paper in2018-19

Dairy exports witnessed a126% growth in 2019 with49 billion dairy packagingunits used nationwide.

Innovation in biodegradableplastics as single-use plasticcomprises 40% of nearly 10million tonnes plastic wastegenerated

OPPORTUNITIES

• Ministry ofConsumer Affairs hasmade it mandatoryfor package boxes ofstandard sizes

• Government of Indiaand Indian Instituteof Packagingdesigned thepackaging norms forproduct exports

Packaging Standards Food Safety (Packaging & Labelling) Regulations

• Guidelines defininglabelingrequirements for allpackaged food inIndia

• Mandatorycertification toensure materialquality and meetglobal packagingstandards

Profit-linked Tax Holiday

• Companies involvedin packagingactivities ofperishable foodproducts exemptedfrom paying tax on100% of profits andgains

• Step to encouragepackaging of fruits,vegetables, dairy andmeat products, andminimise waste

Sources: Food Safety and Standards Authority of India (FSSAI), Ministry of Consumer Affairs, Make In India, Export Import Data Bank, Department of Commerce, Icegate

Customs Duty on Packaging Material ImportsGovernment Policies

Sl. No.

Product HS Code Effective Duty (in %)

1 Jute packaging 6305 50.5

2 Plastic packaging 3923 31.0

3 Glass packaging 7010 31.0

4 Paper packaging 4819 24.5

5 Wooden packaging 4415 24.3

GOVERNMENT POLICIES: AND REGULATORY LANDSCAPES

Acrobat Pro DCAcrobat Pro DC

Sources: T&A Analysis, Media releases

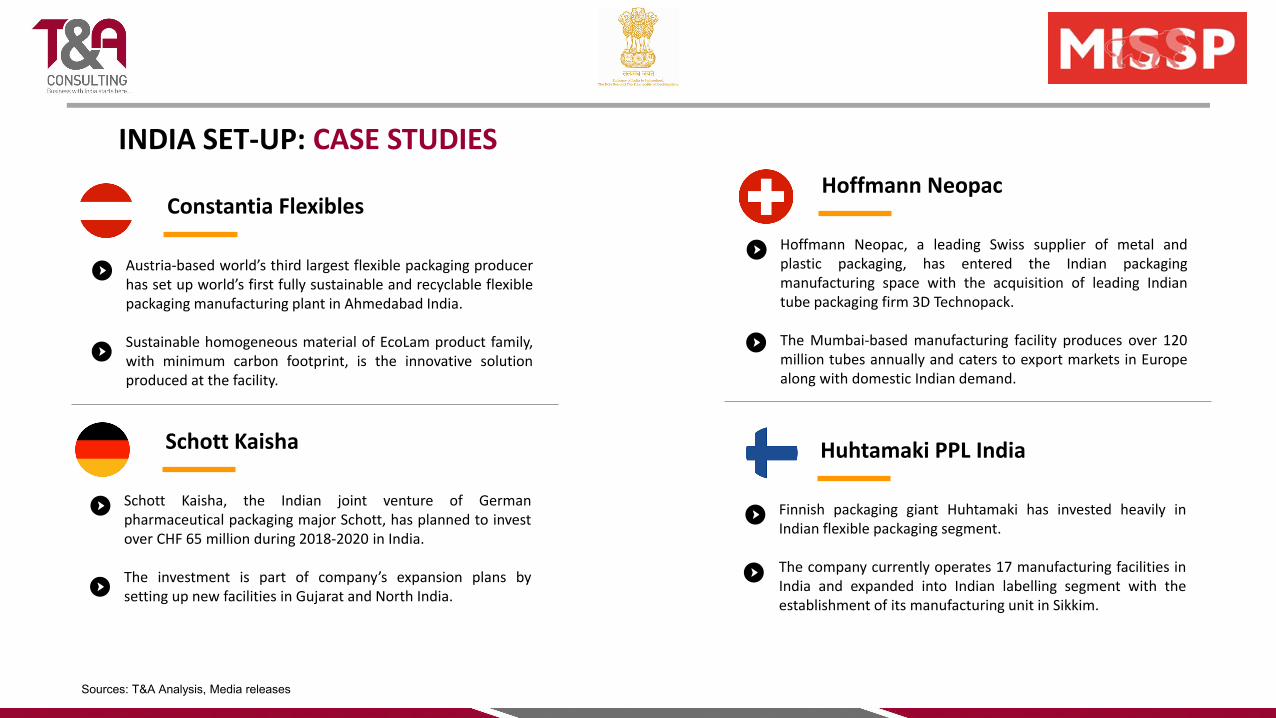

INDIA SET-UP: CASE STUDIES

Constantia Flexibles

Austria-based world’s third largest flexible packaging producerhas set up world’s first fully sustainable and recyclable flexiblepackaging manufacturing plant in Ahmedabad India.

Sustainable homogeneous material of EcoLam product family,with minimum carbon footprint, is the innovative solutionproduced at the facility.

Schott Kaisha

Schott Kaisha, the Indian joint venture of Germanpharmaceutical packaging major Schott, has planned to investover CHF 65 million during 2018-2020 in India.

The investment is part of company’s expansion plans bysetting up new facilities in Gujarat and North India.

Hoffmann Neopac

Hoffmann Neopac, a leading Swiss supplier of metal andplastic packaging, has entered the Indian packagingmanufacturing space with the acquisition of leading Indiantube packaging firm 3D Technopack.

The Mumbai-based manufacturing facility produces over 120million tubes annually and caters to export markets in Europealong with domestic Indian demand.

Huhtamaki PPL India

Finnish packaging giant Huhtamaki has invested heavily inIndian flexible packaging segment.

The company currently operates 17 manufacturing facilities inIndia and expanded into Indian labelling segment with theestablishment of its manufacturing unit in Sikkim.

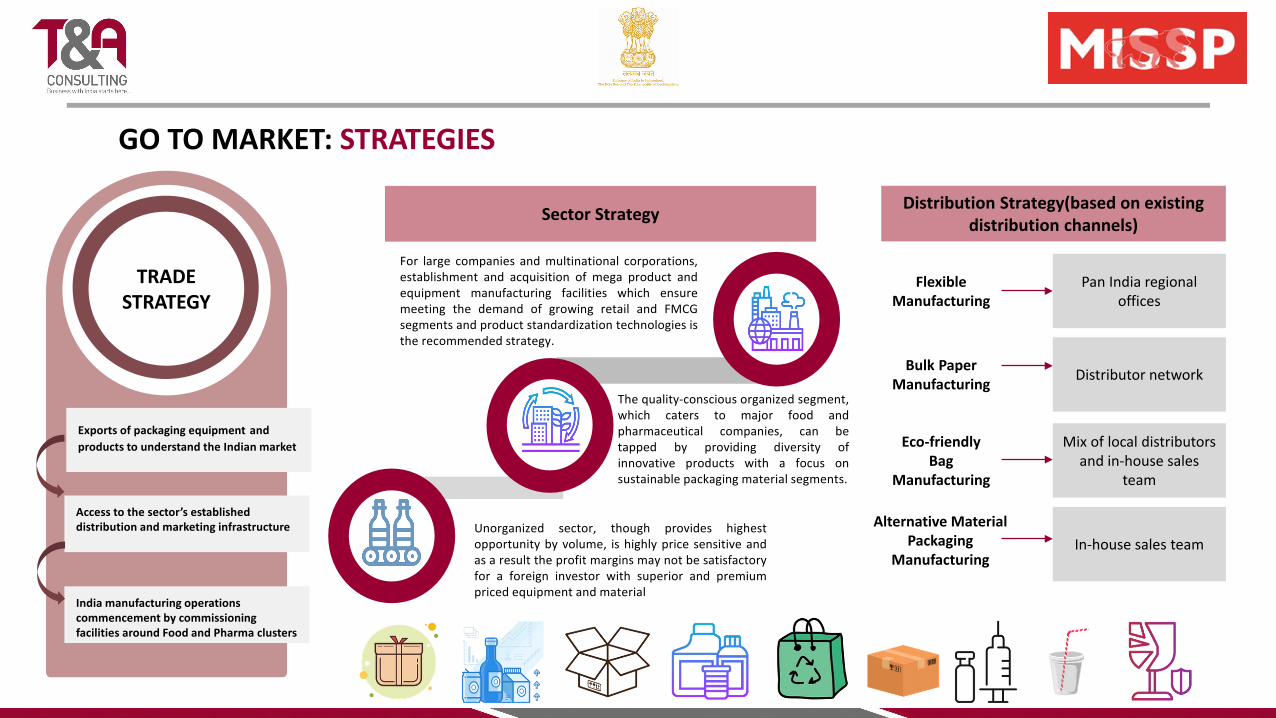

Distribution Strategy(based on existing distribution channels)

Flexible Manufacturing

Pan India regional offices

Bulk Paper Manufacturing Distributor network

Eco-friendly Bag

Manufacturing

Mix of local distributors and in-house sales

team

Alternative MaterialPackaging

ManufacturingIn-house sales team

The quality-conscious organized segment,which caters to major food andpharmaceutical companies, can betapped by providing diversity ofinnovative products with a focus onsustainable packaging material segments.

For large companies and multinational corporations,establishment and acquisition of mega product andequipment manufacturing facilities which ensuremeeting the demand of growing retail and FMCGsegments and product standardization technologies isthe recommended strategy.

Unorganized sector, though provides highestopportunity by volume, is highly price sensitive andas a result the profit margins may not be satisfactoryfor a foreign investor with superior and premiumpriced equipment and material

Sector Strategy

GO TO MARKET: STRATEGIES

TRADE STRATEGY

Exports of packaging equipment and products to understand the Indian market

Access to the sector’s established distribution and marketing infrastructure

India manufacturing operations commencement by commissioning facilities around Food and Pharma clusters

THANK YOU

Recommended