Opportunities for Optimism?A New Vision for Value in Asset Management

Featuring the findings of the 2015 State Street Asset Manager Survey

General

CORP-1518

General

CORP-1518

2

Opportunities for Optimism? A New Vision for Value in Asset Management

State Street research shows that asset managers are positive about growth opportunities.1 As AUMs continue to rise, opportunities are arising on many fronts, but they will be realized only through creating new kinds of value for clients.

Asset managers are revamping their investment strategies, upgrading their capabilities, targeting new markets and hunting for acquisitions that could extend their capabilities or reach to compete in a fast-changing industry.

Optimism must be tempered by an awareness of new risks. Our research reveals that costs are under scrutiny and investors want “more bang for their buck” – they are seeking value beyond beating traditional performance benchmarks. Competition is intensifying – including from tech-savvy challengers and the trend toward greater insourcing by asset owners.

The most enterprising asset managers are “bringing more value to the table.” They’re focusing on delivering more specific investment outcomes for clients. Many are forging closer partnerships with investors based on a transparent dialogue on risk and performance.

A new industry landscape is emerging, according to our research. Opportunities are there for the taking. But asset managers will need to demonstrate where and how they create enduring value for their customers if they are to translate today’s optimism into long-term success.

1. State Street 2015 Asset Manager Survey conducted by FT Remark. All data and opinions in this presentation originate from this survey unless otherwise noted. Conducted in April and May 2015, this survey canvassed the opinions of 400 senior executives in the asset management industry. Respondents from 23 countries participated, with the majority from Australia, Canada, China, Germany, Japan, Switzerland, the UK and US.

General

CORP-1518

3

New Sources of Value, New Forces for Change

A rising market creates opportunities on multiple fronts. Asset managers are racing to develop new offerings and invest in new capabilities to meet changing client demands.

Opportunity Threat

88 percent of asset managers predict a positive outlook for profitable growth

96 percent say they are under pressure to reduce costs

78 percent see growing demand for bespoke investment solutions built around their clients’ requirements

79 percent believe it is likely they will face direct competition from a non-traditional entrant to the asset management industry

95 percent see positive scope for acquisitions, with 46 percent evaluating acquisition targets today

81 percent of pension funds say they plan to increase the proportion of their portfolio that is managed in house2, causing asset managers to seek new ways to create value for these clients

Leading players will move fast to plug any capability gaps through acquisition and investment while increasing their penetration of the fastest-growing customer segments.

2. State Street 2014 Asset Owner Survey conducted by the Economist Intelligence Unit. Pension fund respondents only. The survey was conducted in August 2014. Respondents from 15 countries participated, with the majority coming from the US, UK, Australia and Canada.

General

CORP-1518

4

Opportunity Knocks − At Home and OverseasAcquisitions Are on the Horizon as Asset Managers T arget New Markets and Growth Around New Product Lines

What actions is your firm taking as a result of the opportunities you are seeing in the market?

Source: State Street 2015 Asset Manager Survey, conducted by FT Remark

44%

28%

48%

48%

45%

33%

52%

45%

36%

42%

42%

46%

Preparing to enter a new product category for thefirst time

Preparing to enter new markets

Accessing new distribution channels

Evaluating targets for acquisition

EMEA NA APAC

• 43% of asset managers evaluating targets for acquisition are preparing to enter new markets, compared to just 27% of others, highlighting a tendency toward strategic M&A that will extend the firm’s reach

• Those asset managers serving institutional investors are more likely than those serving retail investors to be targeting acquisitions – 58% vs 38%

• Far more asset managers serving the active end of the market (59%) are evaluating targets for acquisition than the managers on the passive side (36%)

General

CORP-1518

5

Opportunity Makers: Four Drivers of Value

Limited Access6

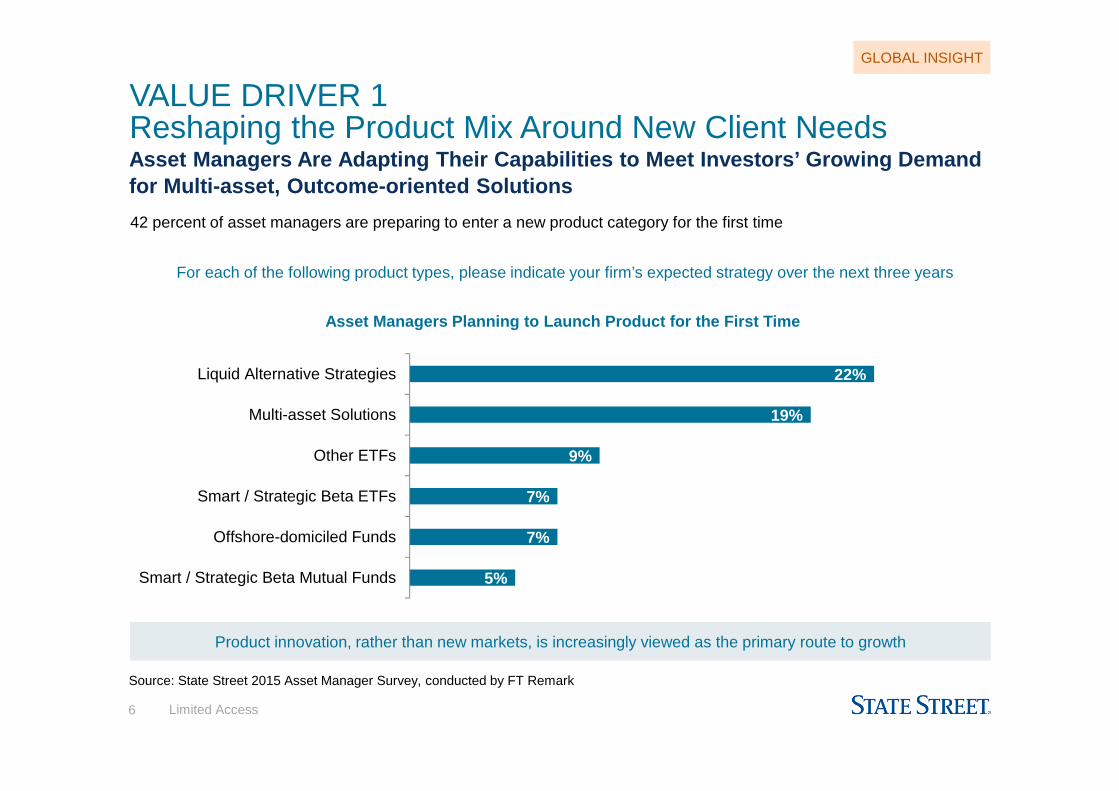

VALUE DRIVER 1Reshaping the Product Mix Around New Client NeedsAsset Managers Are Adapting Their Capabilities to M eet Investors’ Growing Demand for Multi-asset, Outcome-oriented Solutions

Product innovation, rather than new markets, is increasingly viewed as the primary route to growth

Source: State Street 2015 Asset Manager Survey, conducted by FT Remark

GLOBAL INSIGHT

5%

7%

7%

9%

19%

22%

Smart / Strategic Beta Mutual Funds

Offshore-domiciled Funds

Smart / Strategic Beta ETFs

Other ETFs

Multi-asset Solutions

Liquid Alternative Strategies

For each of the following product types, please indicate your firm’s expected strategy over the next three years

42 percent of asset managers are preparing to enter a new product category for the first time

Asset Managers Planning to Launch Product for the F irst Time

General

CORP-1518

7

CORP-1518

�

�

�

�

�

VALUE DRIVER 1

Articulate and communicate a clearly defined and focused proposition, from serving a specific market niche to active management capability.

Focus on the client objectives, rather than delivering relative performance through generic, manufactured investment products.

Plug gaps in capabilities, both in terms of product and the wider service proposition, using acquisitions, partnerships or outsourcing to augment your platform.

Master the multi-asset challenge by building the systems and talent pool required to manage risk and performance across today’s complex portfolios.

Prepare to innovate as clients get more demanding and new entrants intensify competition, fostering the entrepreneurial culture required for growth.

How to Compete as a Solutions Maker

GLOBAL INSIGHT

General

CORP-1518

8

VALUE DRIVER 2Client Services Become More Personalized and Transparent• Leading asset managers are ready to be more transparent about all aspects of investment performance and risk. They

are learning to work in closer partnerships with their institutional clients

– 79 percent of asset managers say client demands for increased transparency on how their money is managed are impacting business strategy

– 77 percent now offer their clients more transparency on risk and return

– Only 36 percent are highly confident in their ability to use advanced analytics to segment clients according to their characteristics and needs

Percent Indicating “Significant Impact”

For each of the following investor trends, please indicate the extent to which it is impacting your firm’s business strategy, in terms of shaping your products and how you deliver them

24%

31%

31%

32%

34%

36%

44%Investor demand for more transparency

into the investment processInvestor demand for multi-asset,

outcome-oriented investment strategies

Investor adoption of factor-based allocation models

Investor demand for impact investing strategies

Investor demand for liability-driven investing strategies

Investor demand for increased customization

Investor demand for passive investment strategies

Source: State Street 2015 Asset Manager Survey, conducted by FT Remark

GLOBAL INSIGHT

General

CORP-1518

9

CORP-1518

VALUE DRIVER 2

Provide investors with more granular detail about the performance and risk profile of their holdings. Meet the need for a variety of different formats and respond to bespoke requests.

Recognize that transparency is a two-way street. Develop new channels for investor feedback and use analytics to better understand clients’ needs.

Develop approaches to the increasing demand for information from regulators and investors. Prioritize specialist data units.

Invest in the consultative skills and intellectual capital that will enable you to deliver uniquely valuable insights to your clients.

Deliver personalization at scale. Build strategic asset allocation models that can be adjusted to accommodate client-specific overlays.

How to Get Closer to Your Clients

Source: State Street 2015 Asset Manager Survey, conducted by FT Remark

GLOBAL INSIGHT

�

�

�

�

�

General

CORP-1518

10

VALUE DRIVER 3New Ideas Around Risk Will Shape the Dialogue With Investors

Risk issues are at the heart of the conversation between asset managers and their clients, according to our research. Asset managers with the analytics tools to support new levels of risk insight may gain a competitive edge

Leading asset managers will need more robust methods to understand risks across complex multi-asset portfolios. This entails being able to integrate their risk analytics across multiple asset classes. The leaders are also designing more advanced risk models that can be customized to their clients’ needs

72 percent of asset managers say their conversations with clients have evolved to focus more heavily on risk

61 percent say clients are demanding a more personalized approach to help them understand their risks

75 percent say they are spending more time and resources on educating the boards of their institutional clients on risk issues

Source: State Street 2015 Asset Manager Survey, conducted by FT Remark

GLOBAL INSIGHT

Limited Access11

�

�

�

�

�

VALUE DRIVER 3

Recognize that investors are placing as much emphasis on risk management as they are on high performance. Allocate the right level of resources to meet this need.

Be prepared to educate investors on risk, developing more effective methods of communicating risk exposures to clients.

Ensure your data infrastructure supports the need for improved risk analysis across multi-asset portfolios. Make it an important competitive weapon in winning new clients.

Invest in new risk tools and more sophisticated risk models that give clients a more granular understanding of their exposures, both individually and consolidated across their portfolios.

Recognize that investors now consider a greater range of risks — including the operational risks that their asset managers may be exposed to.

How to Compete in the Risk Arena

GLOBAL INSIGHT

General

CORP-1518

12

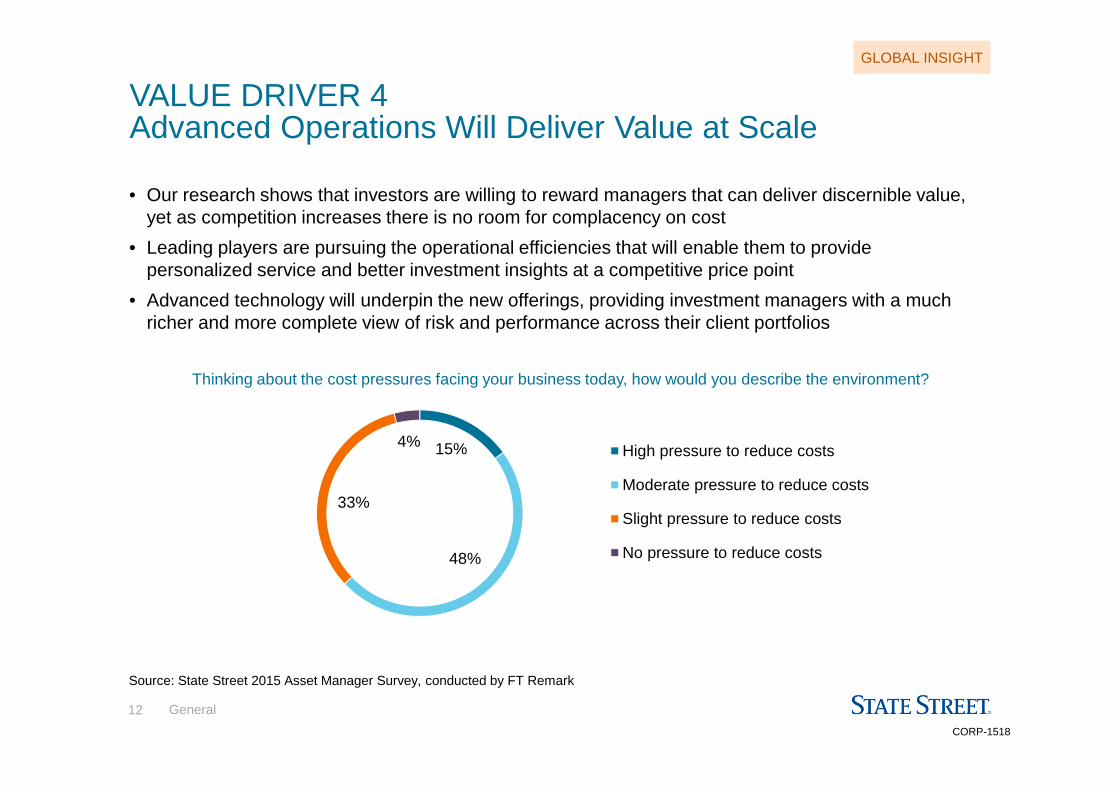

VALUE DRIVER 4Advanced Operations Will Deliver Value at Scale

• Our research shows that investors are willing to reward managers that can deliver discernible value, yet as competition increases there is no room for complacency on cost

• Leading players are pursuing the operational efficiencies that will enable them to provide personalized service and better investment insights at a competitive price point

• Advanced technology will underpin the new offerings, providing investment managers with a much richer and more complete view of risk and performance across their client portfolios

15%

48%

33%

4%High pressure to reduce costs

Moderate pressure to reduce costs

Slight pressure to reduce costs

No pressure to reduce costs

Thinking about the cost pressures facing your business today, how would you describe the environment?

Source: State Street 2015 Asset Manager Survey, conducted by FT Remark

GLOBAL INSIGHT

Limited Access13

�

�

�

�

�

How to Deliver More Client Value Through Smarter Operations

Recognize investors’ growing concerns about fee levels. Be ready to demonstrate your added value.

Develop new fee structures that match the shifting focus from relative performance to a more outcome-focused approach.

Investigate whether new partnerships can help deliver more value to clients at lower cost. Build links with areas such as the fintech sector.

Automate manual processes to free up resources for more added-value tasks, ensuring operational efficiency helps protect margins in a climate of flat or falling fees.

Invest in the in-house technology infrastructure required to deliver value at scale and transform cost efficiency. Utilize alternative approaches such as outsourcing.

GLOBAL INSIGHT

General

CORP-1518

14

Moving Up the Value ChainOur Research Sheds Light on Several Important Consi derations for Asset Managers as They Adapt to the New Landscape

What is your unique value proposition today?

Asset managers will need a more focused proposition about the value they can deliver to investors, whether it’s providing the full spectrum of solutions, or carving out a particular specialism. This may mean scaling up, or deepening niche expertise.

How can you raise the bar in client interactions?

Investors are demanding more effective, detailed communication about complex areas of performance and risk. Servicing this need will mean devoting greater resource to investor engagement and strengthening advisory capabilities.

How will you meet demand for more outcome-based solutions?

To meet more specific investor needs on risk management and longer-term income requirements, asset managers must support multi-asset strategies, and use clients’ desired outcomes as a starting point for building their solutions.

How will you service new requirements on risk management and transparency of risk reporting?

With the popularity of multi-asset solutions, asset managers need to deliver granular risk analysis customized to individual investor demands. Those who can devise smarter risk models and apply sophisticated analytics tools will be highly sought after.

How will you respond to the threat of digital disruption?

Investors want easy access to their investments with the ability to manage their portfolios at the click of a button. Technology firms are a threat, but established asset managers can use data and analytics to find their own competitive edge, or look at partnering with start-ups, such as in the fintech sector, to innovate in this area.

What is the most effective way to reach new investors?

Central to asset managers’ growth ambitions is the ability to reach new investors and achieve more direct interaction with the end clients. Expanding the distribution network and taking ownership of distribution platforms will be important.

General

CORP-1518

15

Appendix: Regional Insights

General

CORP-1518

16

North America

General

CORP-1518

17

VALUE DRIVER 1Reshaping the Product Mix Around New Client NeedsAsset Managers are Adapting Their Capabilities to M eet Investors’ Growing Demand for Factor-Based Allocation and Custom-Tailored Sol utions

For each of the following investor trends, please indicate the extent to which it is impacting your firm’s overall business strategy, in terms of shaping your products and how you deliver them? (North America respondents)

41%

34%

37%

39%

42%

41%

21%

31%

29%

27%

29%

31%

Investor demand for passive investment strategies

Investor demand for liability driven investing strategies

Investor demand for multi-asset outcome-orientedinvestment strategies solutions

Investor demand for impact investing strategies

Investor demand for increased customization

Investor adoption of factor-based allocation models

Moderate impact Significant impact

More than a third (35 percent) of US-based asset managers say that demand for outcome-oriented solutions is significantly impacting business strategy, while 44 percent of Canadian asset managers think investor adoption of factor-based allocation models will have a similar level of impact

Source: State Street 2015 Asset Manager Survey, conducted by FT Remark

Regional: North America

General

CORP-1518

18

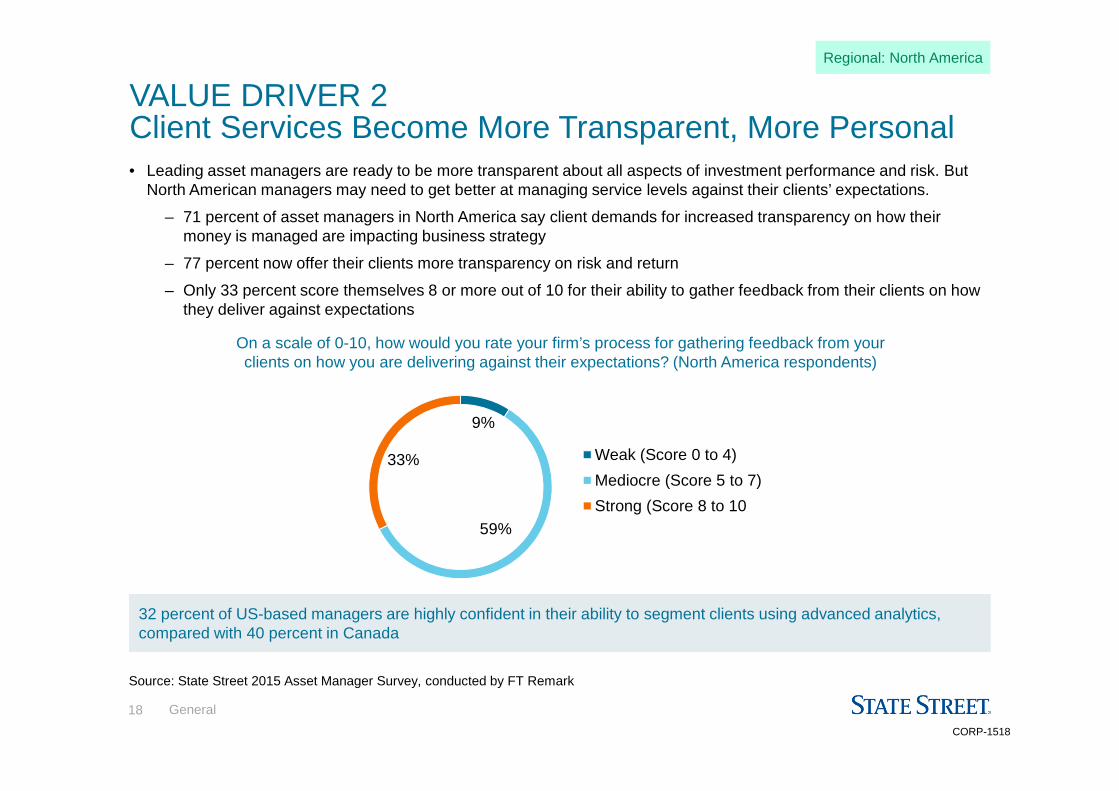

VALUE DRIVER 2Client Services Become More Transparent, More Personal• Leading asset managers are ready to be more transparent about all aspects of investment performance and risk. But

North American managers may need to get better at managing service levels against their clients’ expectations.

– 71 percent of asset managers in North America say client demands for increased transparency on how their money is managed are impacting business strategy

– 77 percent now offer their clients more transparency on risk and return

– Only 33 percent score themselves 8 or more out of 10 for their ability to gather feedback from their clients on how they deliver against expectations

On a scale of 0-10, how would you rate your firm’s process for gathering feedback from your clients on how you are delivering against their expectations? (North America respondents)

Source: State Street 2015 Asset Manager Survey, conducted by FT Remark

32 percent of US-based managers are highly confident in their ability to segment clients using advanced analytics, compared with 40 percent in Canada

9%

59%

33% Weak (Score 0 to 4)

Mediocre (Score 5 to 7)

Strong (Score 8 to 10

Regional: North America

General

CORP-1518

19

VALUE DRIVER 3Risk Goes to the Heart of the Conversation

Risk issues are at the heart of the conversation between asset managers and their clients, according to our research. Asset managers with the analytics tools to support new levels of risk insight may gain a competitive edge over their rivals

North America’s leading asset managers will need more robust methods to understand risks across complex multi-asset portfolios. This entails being able to integrate their risk analytics across multiple asset classes. The leaders are also designing more advanced risk models that can be customized to their clients’ needs

72 percent of asset managers in North America say their conversations with clients have evolved to focus more heavily on risk

75 percent of them are spending more time and resources on educating the boards of their institutional clients on risk issues

66 percent say that heightened risk and compliance demands threaten to divert resources from critical business areas

Source: State Street 2015 Asset Manager Survey, conducted by FT Remark

Regional: North America

General

CORP-1518

20

VALUE DRIVER 4Advanced Operations Can Deliver Value at Scale• Our research shows that investors are willing to reward managers that can deliver discernible value, yet as

competition increases there is no room for complacency on cost.

• Leading players are pursuing the operational efficiencies that will enable them to deliver a more personalized service and better investment insights at a competitive price point.

• Advanced technology will underpin the new offerings, providing investment managers with a much richer and more complete view of risk and performance across their client portfolios.

Thinking about the cost pressures facing your business today, how would you describe the environment? (All North America respondents)

11%

40%42%

6%

High pressure to reduce costs

Moderate pressure to reduce costs

Slight pressure to reduce costs

No pressure to reduce costs

• 47 percent of asset managers based in the US say they face moderate to significant pressure to reduce costs

• Only 35 percent of North America-based managers are highly confident their current operating infrastructure can accommodate future distribution strategy

Source: State Street 2015 Asset Manager Survey, conducted by FT Remark

Regional: North America

General

CORP-1518

21

EMEA

General

CORP-1518

22

VALUE DRIVER 1Reshaping the Product Mix Around New Client NeedsAsset Managers are Adapting Their Capabilities to M eet Investors’ Growing Demand for Customized and Outcome-Oriented Solutions

For each of the following investor trends, please indicate the extent to which it is impacting your firm’s overall business strategy, in terms of shaping your products and how you deliver them? (EMEA respondents)

44%

30%

42%

36%

37%

50%

16%

39%

27%

32%

33%

30%

Investor demand for passive investmentstrategies

Investor demand for multi-asset outcome-oriented investment strategies solutions

Investor demand for liability driven investingstrategies

Investor adoption of factor-based allocationmodels

Investor demand for impact investingstrategies

Investor demand for increased customization

Moderate impact Significant impact

53 percent of Switzerland-based asset managers say that multi-asset strategies will significantly impact business strategy, while 1 in 2 German managers say that investor demand for more transparency into the investment process is having a similar level of impact on their strategy

Source: State Street 2015 Asset Manager Survey, conducted by FT Remark

Regional: EMEA

General

CORP-1518

23

VALUE DRIVER 2Client Services Become More Transparent, More Personal• Leading asset managers are ready to be more transparent about all aspects of investment performance and risk. But

EMEA managers may need to get better at managing service levels against their clients’ expectations.

– 83 percent of asset managers in EMEA say client demands for increased transparency on how their money is managed are impacting business strategy

– 78 percent now offer their clients more transparency on risk and return

– Only 23 percent score themselves 8 or more out of 10 for their ability to gather feedback from their clients on how they deliver against expectations

On a scale of 0-10, how would you rate your firm’s process for gathering feedback from your clients on how you are delivering against their expectations? (EMEA respondents)

Source: State Street 2015 Asset Manager Survey, conducted by FT Remark

Half of German-based managers are highly confident in their ability to segment clients using advanced analytics, compared with 37 percent in Switzerland and 36 percent in the UK

14%

62%

23%Weak (Score 0 to 4)

Mediocre (Score 5 to 7)

Strong (Score 8 to 10

Regional: EMEA

General

CORP-1518

24

VALUE DRIVER 3Risk Goes to the Heart of the Conversation

Risk issues are at the heart of the conversation between asset managers and their clients, according to our research. Asset managers with the analytics tools to support new levels of risk insight may gain a competitive edge

EMEA’s leading asset managers will need more robust methods to understand risks across complex multi-asset portfolios. This entails being able to integrate their risk analytics across multiple asset classes. The leaders are also designing more advanced risk models that can be customized to their clients’ needs

72 percent of asset managers in EMEA say their conversations with clients have evolved to focus more heavily on risk

82 percent of them are spending more time and resources on educating the boards of their institutional clients on risk issues

60 percent say that heightened risk and compliance demands threaten to divert resources from critical business areas

Source: State Street 2015 Asset Manager Survey, conducted by FT Remark

Regional: EMEA

General

CORP-1518

25

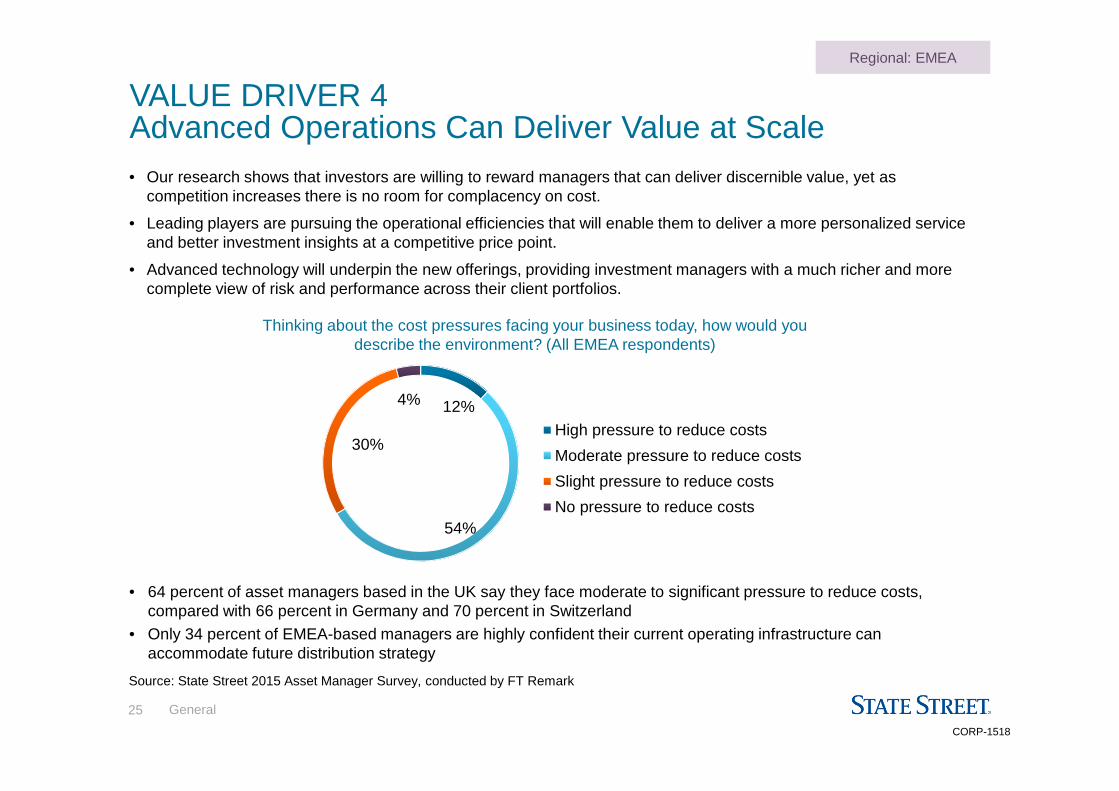

VALUE DRIVER 4Advanced Operations Can Deliver Value at Scale• Our research shows that investors are willing to reward managers that can deliver discernible value, yet as

competition increases there is no room for complacency on cost.

• Leading players are pursuing the operational efficiencies that will enable them to deliver a more personalized service and better investment insights at a competitive price point.

• Advanced technology will underpin the new offerings, providing investment managers with a much richer and more complete view of risk and performance across their client portfolios.

Thinking about the cost pressures facing your business today, how would you describe the environment? (All EMEA respondents)

12%

54%

30%

4%

High pressure to reduce costs

Moderate pressure to reduce costs

Slight pressure to reduce costs

No pressure to reduce costs

• 64 percent of asset managers based in the UK say they face moderate to significant pressure to reduce costs, compared with 66 percent in Germany and 70 percent in Switzerland

• Only 34 percent of EMEA-based managers are highly confident their current operating infrastructure can accommodate future distribution strategy

Source: State Street 2015 Asset Manager Survey, conducted by FT Remark

Regional: EMEA

General

CORP-1518

26

Asia-Pacific

General

CORP-1518

27

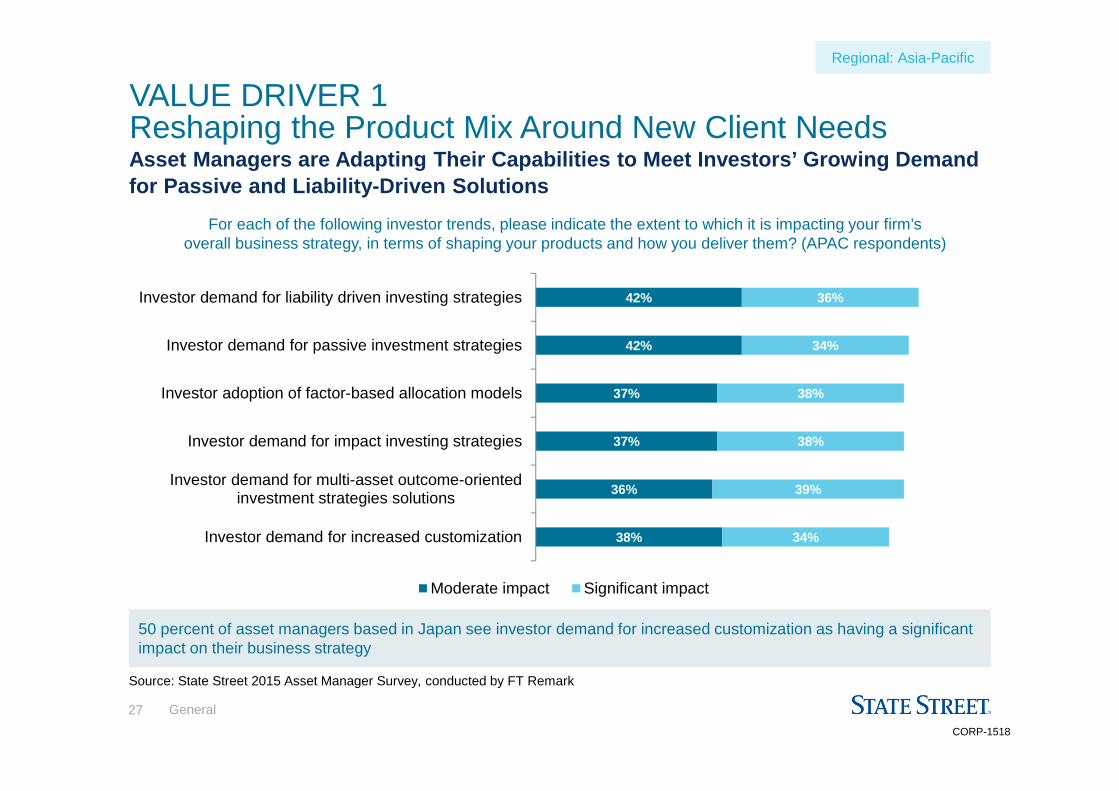

50 percent of asset managers based in Japan see investor demand for increased customization as having a significant impact on their business strategy

VALUE DRIVER 1Reshaping the Product Mix Around New Client NeedsAsset Managers are Adapting Their Capabilities to M eet Investors’ Growing Demand for Passive and Liability-Driven Solutions

For each of the following investor trends, please indicate the extent to which it is impacting your firm’s overall business strategy, in terms of shaping your products and how you deliver them? (APAC respondents)

38%

36%

37%

37%

42%

42%

34%

39%

38%

38%

34%

36%

Investor demand for increased customization

Investor demand for multi-asset outcome-orientedinvestment strategies solutions

Investor demand for impact investing strategies

Investor adoption of factor-based allocation models

Investor demand for passive investment strategies

Investor demand for liability driven investing strategies

Moderate impact Significant impact

Source: State Street 2015 Asset Manager Survey, conducted by FT Remark

Regional: Asia-Pacific

General

CORP-1518

28

VALUE DRIVER 2Client Services Become More Transparent, More Personal• Leading asset managers are ready to be more transparent about all aspects of investment performance and risk. But

APAC managers may need to get better at managing service levels against their clients’ expectations.

– 84 percent of asset managers in APAC say client demands for increased transparency on how their money is managed are impacting business strategy

– 78 percent now offer their clients more transparency on risk and return

– Only 16 percent score themselves 8 or more out of 10 for their ability to gather feedback from their clients on how they deliver against expectations

On a scale of 0-10, how would you rate your firm’s process for gathering feedback from your clients on how you are delivering against their expectations? (APAC respondents)

Source: State Street 2015 Asset Manager Survey, conducted by FT Remark

37 percent of China/HK-based managers are highly confident in their ability to segment clients using advanced analytics, compared with 33 percent in Australia, 30 percent in Japan and 25 percent in SE Asia

18%

66%

16%

Weak (Score 0 to 4)

Mediocre (Score 5 to 7)

Strong (Score 8 to 10

Regional: Asia-Pacific

General

CORP-1518

29

VALUE DRIVER 3Risk Goes to the Heart of the Conversation

Risk issues are at the heart of the conversation between asset managers and their clients, according to our research. Asset managers with the analytics tools to support new levels of risk insight may gain a competitive edge

APAC’s leading asset managers will need more robust methods to understand risks across complex multi-asset portfolios. This entails being able to integrate their risk analytics across multiple asset classes. The leaders are also designing more advanced risk models that can be customized to their clients’ needs

72 percent of asset managers in APAC say their conversations with clients have evolved to focus more heavily on risk

67 percent of them are spending more time and resources on educating the boards of their institutional clients on risk issues

63 percent say that heightened risk and compliance demands threaten to divert resources from critical business areas

Source: State Street 2015 Asset Manager Survey, conducted by FT Remark

Regional: Asia-Pacific

General

CORP-1518

30

VALUE DRIVER 4Advanced Operations Can Deliver Value at Scale• Our research shows that investors are willing to reward managers that can deliver discernible value, yet as

competition increases there is no room for complacency on cost.

• Leading players are pursuing the operational efficiencies that will enable them to deliver a more personalized service and better investment insights at a competitive price point.

• Advanced technology will underpin the new offerings, providing investment managers with a much richer and more complete view of risk and performance across their client portfolios.

Thinking about the cost pressures facing your business today, how would you describe the environment? (All APAC respondents)

• 83 percent of asset managers based in Japan say they face moderate to significant pressure to reduce costs, compared with 69 percent in Australia

• Only 28 percent of APAC-based managers are highly confident their current operating infrastructure can accommodate future distribution strategy

23%

50%

25%

2%

High pressure to reduce costs

Moderate pressure to reduce costs

Slight pressure to reduce costs

No pressure to reduce costs

Source: State Street 2015 Asset Manager Survey, conducted by FT Remark

Regional: Asia-Pacific

General

CORP-1518

31

Disclaimer

The information in this document is accurate as of July 20, 2015.

This document is for marketing and/or informational purposes only, it does not take into account any investor's particular investment objectives, strategies or tax and legal status, nor does it purport to be comprehensive or intended to replace the exercise of a clients own careful independent review regarding any corresponding investment decision or review of our products and services prior to making any decision regarding their utilization.

This does not constitute investment, legal, or tax advice and is not a solicitation to for products or services or intended to constitute any binding contractual arrangement or commitment by State Street and/or any subsidiary referenced herein to provide securities services. State Street hereby disclaims all liability, whether arising in contract, tort or otherwise, forany losses, liabilities, damages, expenses or costs arising, either direct or consequential, from or in connection with the use of this document and/or the information herein.

This document contains certain statements that may be deemed forward-looking statements, which are based on certain assumptions and analyses made in light of experience and perception of historical trends, current conditions, expected future developments and other factors believed appropriate in the circumstances.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without State Street express written consent.

© 2015 State Street Corporation. All Rights Reserved

CORP-1518

Expiration Date: 07/31/2016

Recommended