Operating leases and the assessment of

lease±debt substitutability

Vivien Beattie, Alan Goodacre *, Sarah Thomson

Department of Accounting, Finance and Law, University of Stirling, Stirling FK9 4LA, Scotland, UK

Received 22 December 1998; accepted 16 April 1999

Abstract

Operating leases are estimated in the current paper to be approximately thirteen

times larger than ®nance leases, on average. In recognition of this, the paper investigates

the degree of substitutability between leasing and non-lease debt using a comprehensive

measure of leasing, improving on the partial measures used in prior research. Operating

lease liabilities are estimated using the Ôconstructive capitalisationÕ approach suggested

by Imho�, Lipe and Wright (1991, Accounting Horizons 5, pp. 51±63), modi®ed to

incorporate company-speci®c and UK-relevant assumptions. The results imply that

leasing and debt are partial substitutes, with £1 of leasing displacing approximately

£0.23 of non-lease debt, on average, consistent with the argument that lessors bear some

risks which are not inherent in debt contracts. These ®ndings suggest that substitution

e�ects are not uniform across lease types. Ó 2000 Elsevier Science B.V. All rights re-

served.

JEL classi®cation: G32

Keywords: Operating leases; Capital structure; Lease±debt substitutability

Journal of Banking & Finance 24 (2000) 427±470

www.elsevier.com/locate/econbase

* Corresponding author. Tel.: +44-1786-467291; fax: +44-1786-467308.

E-mail address: [email protected] (A. Goodacre).

0378-4266/00/$ - see front matter Ó 2000 Elsevier Science B.V. All rights reserved.

PII: S 0 3 7 8 - 4 2 6 6 ( 9 9 ) 0 0 0 4 5 - X

1. Introduction

In recent years, signi®cant progress has been made in understanding thedeterminants of corporate capital structure with an increased emphasis on®nancial contracting theory (see, for example, Smith and Wakeman, 1985;Barclay and Smith, 1995; Sharpe and Nguyen, 1995; Mehran et al., 1997;Graham et al., 1998 and, for an international view, Rajan and Zingales,1995). This theory suggests that ®rm characteristics such as business risk andinvestment opportunity set a�ect contracting costs. In turn, these costs im-pact on the choice between alternative forms of ®nance such as debt andequity and between di�erent classes of ®xed-claim ®nance such as debt andleasing.

However, our understanding of the relationship between leasing and debtis far from complete and the degree of substitutability (or, indeed, comple-mentarity) between the two remains unresolved. Finance theory generallypredicts that leasing and debt are substitutes, to a greater or lesser extent. YetAng and Peterson (1984), in their seminal empirical study using ®nancialstatement data, failed to con®rm this prediction, instead ®nding a comple-mentary relationship. They referred to this result as the Ôleasing puzzleÕ. Al-though subsequent analytical work by Lewis and Schallheim (1992)demonstrated the theoretical possibility of complementarity, more recentempirical papers have supported substitutability (Marston and Harris, 1988;Adedeji and Stapleton, 1996) although the evidence in Mehran et al. (1997) ismixed.

A major obstacle to resolving this issue is the di�culty in measuring leaseliabilities from sources which are publicly available. This arises becausecompanies are currently required to include only ®nance (capital) leases ontheir balance sheets and not assets that have been ®nanced by operatingleases. Thus, explanatory models of the lease ratio su�er from major mea-surement error of the dependent variable. None of the previous studies hasfully considered the issue of how to incorporate operating leases in theirmeasure of leasing. Marston and Harris (1988) had to use a fairly crude as-sumption, while Sharpe and Nguyen (1995) and Mehran et al. (1997) used anapproximation based on the ratio of lease payments to an estimate of totalcapital costs in a given year. Other studies, including Ang and Peterson (1984)and Adedeji and Stapleton (1996) are partial analyses incorporating only®nance leases.

In the UK, the lease accounting standard, SSAP 21 (ASC, 1984), intro-duced the distinction between operating and ®nance leases. Since the stan-dard came into operation, company management have tended to switch thecontractual nature of their leases towards operating leases. Recent UK re-search (Beattie et al., 1998) has identi®ed that operating leases are now amajor source of long-term debt-type ®nancing and are considerably more

428 V. Beattie et al. / Journal of Banking & Finance 24 (2000) 427±470

important than ®nance leases; similar results have emerged from the US(Marston and Harris, 1988; Imho� et al., 1991; Graham et al., 1998). Thus, asubstantial contribution can be made to the lease±debt substitutability liter-ature by using a comprehensive measure of leasing which includes operatinglease ®nance.

The aim of the present study is to investigate the degree of substitutabilitybetween lease and non-lease debt ®nancing using comprehensive measures ofleasing and debt. 1 The primary focus is to explain the observed lease ratio fora cross-section of ®rms, following the methods of Ang and Peterson (1984), asamended by Adedeji and Stapleton (1996). Given the limited information onoperating lease liabilities disclosed in published ®nancial statements, we usean estimate of total operating lease liabilities based on the method of Ôcon-structive capitalisationÕ suggested by Imho� et al. (1991). This basic approachhas been modi®ed to incorporate company-speci®c and UK relevant as-sumptions using the procedures developed by Beattie et al. (1998).

The remainder of this paper is structured as follows. Section 2 provides abrief discussion of capital structure theories and the determinants of ®xed-claim ®nancing, to support the variables selected to model the lease±debtrelationship. Section 3 reviews the literature on lease±debt substitutabilityand presents the models tested in the present study. Methods, including adescription of the approach used to capitalise operating leases, are outlinedin Section 4. Results, based on both the partial and comprehensive leaseratios, are presented and compared in Section 5. Section 6 summarises andconcludes.

1 A basic premise of the paper is that operating leases can be, indeed should be, pooled with

®nance (capital) leases. This can be justi®ed on three grounds. First, lease contract terms lie on a

ÔcontinuumÕ. At one extreme is the contract in which it is clear that the lessor is essentially providing

®nance for the purchase of an asset by the lessee. At the other, the nature of the contract is that the

lessee is paying a rental for the use of the asset, usually over a short period with no commitment

other than the rental payment. However, the vast majority of contracts lie in the middle of the

continuum and do not ®t neatly into either category. The distinction between the two lease types

often does not relate to a fundamental di�erence in their characteristics. Rather, it relates to a desire

to meet the essentially ÔarbitraryÕ accounting classi®cation criteria in order to keep leased assets and

liabilities o� the balance sheet. Second, there is convincing empirical evidence that all leases are

viewed similarly by the market as giving rise to assets and liabilities, with Ely (1995) ®nding that her

results Ôsupport the treatment of operating leases as property rightsÕ. Third, the potentially

distinguishing feature of ÔcancellabilityÕ of operating leases is deceptive. The disclosure in published

®nancial statements is of non-cancellable operating leases; further, even cancellable leases often

carry a punitive termination penalty. We are grateful to an anonymous referee for suggesting the

inclusion of this justi®cation.

V. Beattie et al. / Journal of Banking & Finance 24 (2000) 427±470 429

2. Fixed-claim ®nancing

2.1. Capital structure theories

The traditional Static Trade-O� Theory can be characterised by the as-sumption that capital structure is optimised year by year with managementweighing up the relative advantage of the tax-shield bene®ts of debt against theincreased likelihood of incurring debt-related bankruptcy costs. However, inreality, managers do not appear to determine capital structure in this way butrather as part of a dynamic process. Consequently, at any particular time, a®rm may deviate from its optimal or target debt ratio.

Early recognition of this dynamic process was demonstrated by Donaldson(1961), in what he described as the Pecking-Order Theory of ®nancial choices.He observed that managers preferred to fund investment initially from retainedpro®ts rather than use outside funds. This preference led ®rms to adopt divi-dend policies that re¯ected their anticipated need for investment funds, policieswhich managers were reluctant to substantially change. If retained pro®ts ex-ceeded investment needs then debt would be repaid. If external ®nance wasrequired ®rms tended ®rst to issue the safest security, debt, and only issuedequity as a last resort.

Several possible theoretical explanations for this observed behaviour havebeen proposed. First, taxes and transaction costs favour the use of retainedearnings and favour debt over the issuing of new equity. Second, Myers andMajluf (1984) argue that, under asymmetric information, equity issues arerationally interpreted as Ôbad newsÕ on average, since managers are reluctantto issue stock when they believe the shares are undervalued. Empirical evi-dence con®rms that announcements of new issues are associated with declinesin stock price, which at least partly explains the relatively small number ofnew equity issues. This asymmetric information argument also extends to theuse of dividends as a signalling mechanism. Consequently, managers areaverse to reducing dividends, thereby limiting access to retained earningswhich, in certain periods, leads to the use of external funds to ®nance in-vestment.

The Stakeholder Theory suggests that the way in which a ®rm and its non-®nancial stakeholders (i.e., customers, suppliers, employees and the commu-nity at large) interact is an important additional determinant of the ®rmÕsoptimal capital structure (Grinblatt and Titman, 1998, ch. 16). This theoryargues that the indirect costs of ®nancial distress are higher for certain typesof ®rm than for others. They are especially costly for ®rms characterised byproducts whose quality is important yet unobservable, or by products thatrequire future servicing, or by stakeholders who require specialised capital ortraining. Such ®rms should have relatively less debt in their capital structure.On the other hand, ®nancial distress should be less costly for ®rms that sell

430 V. Beattie et al. / Journal of Banking & Finance 24 (2000) 427±470

non-durable goods and services, that are relatively less specialised and whosequality can easily be assessed. It is expected that these ®rms will have rela-tively higher debt levels. This theory helps to explain why some ®rms choosenot to borrow even when lenders are willing to provide ®nance on attractiveterms.

Modelling the lease±debt relationship ®rst requires some understanding ofthe determinants of ®xed-claim ®nancing. The above theoretical argumentslead to predictions about the factors that determine the level of ®xed-claim®nancing within a ®rm; discussion of these predictions and the empiricalsupport for them is presented below.

2.2. Determinants of ®xed-claim ®nancing

2.2.1. Pro®tThe static theory suggests that debt ratios ought to be positively correlated

with pro®tability. More pro®table ®rms have more income to shelter, are morelikely to have high marginal tax rates and are less susceptible to bankruptcy.However, this result has not been observed empirically (e.g. Titman andWessels, 1988), in fact, those ®rms with the highest taxable earnings tend tohave the lowest debt ratios. This is consistent with the pecking-order theoryand the observed relative infrequency of new equity issues.

2.2.2. Asset structureAgency arguments suggest that shareholders of leveraged ®rms have an

incentive to invest sub-optimally to expropriate wealth from the providers ofdebt. Further, the asymmetric information model implies that issuing debt in asituation where a ®rmÕs managers have better information than the debt pro-vider may increase the cost of such debt. Issuing debt secured on property withknown values avoids such costs and also reduces the underinvestment problem.Thus, ®rms with assets that can be used as collateral are likely to issue moredebt.

2.2.3. Investment opportunity setTitman and Wessels (1988) note that growth opportunities are capital assets

that increase ®rm value, but these are not re¯ected in the book value of assetsor in current pro®ts. Thus, the assets cannot be used as collateral for debt anddo not increase the pro®t available to absorb tax-shielding interest. Both ar-guments suggest a negative relationship between growth opportunities anddebt levels. Further, the costs associated with underinvestment, as a result ofthe agency relationship referred to in the previous section, are likely to behigher for ®rms in growing industries as there is greater ¯exibility in futureinvestment choice. This also implies that debt levels will be negatively corre-lated with expected future growth. However, Myers (1977) notes that this

V. Beattie et al. / Journal of Banking & Finance 24 (2000) 427±470 431

agency problem is reduced if the ®rm issues short-term rather than long-termdebt. Overall, these arguments suggest that long-term debt will be negativelyrelated to growth rates but that short-term debt will be positively related togrowth rates. The net e�ect on total debt will depend on the relative use oflong- and short-term debt by growing ®rms.

2.2.4. SizeA number of authors have suggested that debt ratios may be related to ®rm

size. Large ®rms tend to be relatively more diversi®ed and, therefore, less liableto su�er ®nancial distress. Also, the costs of issuing new long-term debt andequity securities tend to include a large ®xed element which militates againstsmall ®rms using such ®nance. Both arguments suggest that long-term debtratios should be positively related to ®rm size. In contrast, small ®rms tend toborrow short-term (through bank loans) because of the lower associated costs(see Marsh, 1982).

2.3. Determinants of leasing

Much of the above discussion relating to debt ®nance relates equally toleasing. However, the collateralised nature of leasing leads to four di�erencesthat a�ect managersÕ ®nancing choice. First, the characteristics of a ®rmÕscurrent and future assets, and in particular asset speci®city, can in¯uence ®-nancing. Stulz and Johnson (1985) show that high-priority claims, such asleasing, can mitigate the underinvestment problem relative to other forms ofdebt, because the senior claims on the new project assets limit the transfer ofwealth from shareholders to existing debt-providers. Following this line, Bar-clay and Smith (1995) argue that, for a given amount of ®xed-claim ®nancing,®rms with more growth opportunities might be expected to rely more heavilyon lease ®nancing than on lower priority forms of debt. Smith and Wakeman(1985) suggest that ®rms are more likely to buy, than lease, assets which arehighly speci®c to the ®rm. This results from con¯icts and agency costs betweenlessor and lessee which arise in the bilateral monopoly that is created when thelease is negotiated. Consequently, they suggest that ®rms are more likely tolease general facilities (such as o�ces) than ®rm-speci®c production or researchfacilities. Similarly, Williamson (1988) argues that assets which are more easilyredeployable, such as aircraft or trucks, are better suited for leasing and for useas collateral in debt contracts. In combination, these arguments suggest that,for a given level of ®xed-claim ®nancing, ®rms that have a high proportion ofgrowth opportunities, and/or whose assets are not ®rm-speci®c, are likely toemploy more leasing.

Second, ®rm size may have a di�erential in¯uence on leasing relative toother forms of debt-type ®nance. Grinblatt and Titman (1998) argue that thedebt holder±equity holder con¯ict may be worse for small ®rms. Smaller ®rms

432 V. Beattie et al. / Journal of Banking & Finance 24 (2000) 427±470

may be more ¯exible and thus better able to increase the risk of their invest-ment projects. The potentially higher return from accepting this risk accrues toshareholders only, while the increased risk is shared by debt-providers; this willreduce the willingness of lenders to provide debt ®nance. Moreover, topmanagers of small ®rms are more likely to be major shareholders and may,therefore, prefer the lower personal risk associated with low debt levels. Thesearguments reinforce the view that small ®rms will have lower debt ratios.However, they also suggest small companies may favour leasing over debt, ascreditors obtain more security and a manager with a large ownership interestmay prefer leasing to reduce personal exposure to obsolescence or other asset-speci®c risks.

Third, tax considerations may be important in the choice between debt andleasing. Leasing provides the option of ÔsellingÕ tax allowances to a lessor, inexchange for lower rental payments. Most empirical work has failed to provideevidence consistent with theory, until the recent study by Graham et al. (1998).The authors suggest that this failure re¯ects the fact that corporate tax status isendogenous to ®nancing decisions. Using a forward-looking estimate of before-®nancing corporate marginal tax rates, they document a negative relation be-tween operating leases and tax rates, and a positive relation between debt levelsand tax rates. They argue that their results provide unambiguous evidencesupporting the hypothesis that low tax rate ®rms lease more and have lowerdebt levels, than high tax rate ®rms.

Finally, poor liquidity and cash ¯ow problems have been found to be animportant in¯uence in the decision to lease (Drury and Braund 1990; Ad-edeji and Stapleton, 1996), the collateral of the asset increases the avail-ability of lease ®nance in situations where unsecured debt would be toorisky.

3. Lease±debt substitutability

3.1. Theories

Prevailing ®nance theory generally suggests that leases and non-lease debtare substitutes. Thus, an increase in one should lead to a compensating decreasein the other. There are three variants of this theory, which imply di�erentmagnitudes for the substitution coe�cient. Traditional ®nance theory treatscash ¯ows from lease obligations as equivalent to debt cash ¯ows, thus thetrade-o� between debt and leases is one-to-one. Some theorists argue thatdi�erences between the nature and terms of lease and debt contracts lead to alease using less debt capacity than an equivalent amount of non-lease debt (i.e.,the substitution coe�cient is less than 1). Finally, others argue that since leasedassets may be ®rm-speci®c, the risk of moral hazard may be great, resulting in a

V. Beattie et al. / Journal of Banking & Finance 24 (2000) 427±470 433

substitution coe�cient of more than one (see Ang and Peterson (1984) andreferences therein).

In contrast to this accepted wisdom, Lewis and Schallheim (1992) demon-strate analytically that debt and leasing can be complements. They argue thatleasing is a mechanism for selling excess tax deductions that can motivate lessee®rms to increase the proportion of debt in their capital structure. They alsoshow that lessee ®rms can derive a bene®t from leasing even with an as-sumption that the marginal tax rate is the same for lessor and lessee. Thiscontrasts with most existing models where the only situation in which leasingprovides an advantage is when the marginal tax rates di�er.

The following equation captures these opposing views and their variants:

DRNL � DRL � a LRL; �1�where DR is the debt ratio, LR is the lease ratio, NL is a company which doesnot lease, L is a company which does lease, and a is the lease±debt substitutioncoe�cient.

The above substitution arguments correspond to a values of exactly 1, of0 < a < 1 and of a > 1, respectively; all three share the view that leases are ex-pected to reduce debt capacity (i.e., a > 0). Complementarity between leasesand debt corresponds to a negative a.

3.2. Empirical evidence

There are three possible approaches to investigating the relationship be-tween leasing and debt: ®rst, by using historical ®nancial statement data,second, by invoking an experimental design with ®rm managers or ®nance-providers as subjects 2 and third, by directly obtaining the views of managersand providers using a survey method. 3 The focus of the current paper isstudies adopting the ®rst of these approaches. In this, it must be assumed eitherthat ®rms are operating at (or near) their optimal capital structure, on average,or that the model must somehow accommodate deviations from the optimalstructure. The approach must also include adequate control for the di�erences

2 For example, an experimental approach was used by Wilkins and Zimmer (1983a,b) and

Wilkins (1984) to explore the e�ect of alternative accounting methods for leases (capitalisation

versus footnote-only disclosure) using Singapore-based bank loan o�cers and investment analysts

as subjects. They found that the decisions of loan o�cers were a�ected by levels of leverage but not

by either the method of accounting for ®nancial leases or whether the ®nancing was by loan or

lease, implying that debt and leases were viewed as substitutes.3 For example, survey evidence concerning UK company managersÕ perceptions of leasing

(Drury and Braund, 1990) found that the majority of ®rms considered that leasing reduces

borrowing capacity by a smaller amount than an equivalent loan (implying a substitution

coe�cient, a < 1).

434 V. Beattie et al. / Journal of Banking & Finance 24 (2000) 427±470

in debt capacity across ®rms. Otherwise, observed lease ratios and debt ratioswill re¯ect di�erences in debt capacity, or usage of debt capacity, as well asdebt displacement.

Ang and Peterson (1984) (AP) adopted the ®rst approach and used Tobitanalysis on ®nancial statement data drawn from 600 US ®rms between 1976±81.They concluded that, contrary to much accepted theory, leases and debt arecomplements rather than substitutes; lessee ®rms used more long-term debtthan did non-leasing ®rms (i.e., a < 0). They attempted to control for di�erencesin debt capacity by including six additional ®nancial variables in the regressionmodel, operating leverage, sales variability, pro®tability, expected growth, sizeand liquidity. Only operating leverage and pro®tability were found to be sig-ni®cant negative explanatory factors for the level of leasing. This latter result isconsistent with Kare and HerbstÕs (1990) survey evidence that more pro®table®rms, having easier access to low cost debt, prefer debt to leasing. The tax ratesof leasing ®rms were found by AP to be consistently higher than non-leasing®rms, suggesting that tax asymmetries between lessors and lessees are not asigni®cant cause of leasing activity. Smith and Wakeman (1985) suggested thefollowing partial explanation for APÕs ÔcomplementsÕ result: Ôalthough leasesand debt are substitutes for a given ®rm, looking across ®rms, characteristics. . . which provide high debt capacity also tend to provide more pro®tableleasing opportunitiesÕ (p. 907).

Bayless and Diltz (1986) criticised the AP method on the grounds of itsfundamental assumptions, in particular, of the di�culty in satisfactorily con-trolling for cross-sectional di�erences in debt capacity. Instead, they adoptedthe second approach and used an experimental design to control for variationin ®rmsÕ debt capacity, ®nding that lending o�cers reduced their willingness tolend when a ®rm took on lease obligations. Consequently, they estimated avery close substitutability between debt and leasing with capital lease obliga-tions displacing between 10% and 26% more debt capacity than debt ®nance(i.e., a > 1). Whilst the experimental approach avoids the problem of control-ling for debt capacity, it has its own limitations. In particular, achieving reli-able subject response in the arti®cial experimental situation is di�cult andgeneralisation to other groups not speci®cally included as experimental subjectsis hazardous.

Marston and Harris (1988) tried to reconcile these two studiesÕ con¯ictingresults using ®nancial statement data. They used an OLS regression approachbased on changes (rather than levels) of lease and debt ®nance and also usedcomprehensive measures of leasing (capitalised plus non-capitalised) and debt(short-term and long-term). The changes were measured relative to a policy ofmaintaining a constant proportion of assets ®nanced by leasing and by debt,with the proportion measured as the average over a pre-study 3-year period.Their model also allowed for changes in debt levels independent of any leasechanges. The results were consistent with the ®ndings of AP (1984), viz. the use

V. Beattie et al. / Journal of Banking & Finance 24 (2000) 427±470 435

of leasing tends to be associated with the use of non-lease debt. However, theyalso found support for Smith and WakemanÕs observation that certain ®rmcharacteristics simultaneously provide for use of both leasing and non-leasedebt. In combination, these ®ndings suggest strongly that APÕs results re¯ectdi�erences in debt capacity rather than complementarity. Importantly, theestimated coe�cient of substitution between leasing and non-lease debt wassigni®cantly positive, demonstrating that, at the margin, use of lease ®nancingsubstitutes for other forms of both short-term and long-term debt. On average,®rms reduced non-lease debt when leasing increased but did so on less than adollar-for-dollar basis, with $1 of leases substituting for about $0.6 of non-lease debt (i.e., 0 < a < 1). This may be value creating if ®rms are able to expandtheir debt capacity or it may re¯ect a di�erence in the risk characteristics of thetwo instruments. They also estimated that non-capitalised leases accounted forabout 65% of total leasing in 1982 (i.e., post-SFAS 13), thus arguing that it isimportant for empirical studies to use a comprehensive measure of leases.

Adedeji and Stapleton (1996) (A&S) replicate the AP (1984) study in theUK. They de®ne lease and debt ratios with total assets as the denominatorrather than the book value of equity used by AP, since the latter introduces abias in favour of a positive relationship between lease and debt ratios. Thecontrol variables used were price earnings ratio, liquidity, size and tax rate.These di�er from those used by AP in that operating leverage, sales variabilityand pro®tability were omitted but tax rate was included. Operating leases wereexcluded from the lease ratio measure due to data unavailability. In the light ofevidence regarding the importance of operating leases in corporate ®nancingfrom both the UK (Beattie et al., 1998) and the US (Marston and Harris, 1988;Graham et al., 1998), this omission is a serious limitation.

To serve as a benchmark, A&S replicate the AP study using a Tobit re-gression of the full sample in which 44% of companies had no ®nance leases.Consistent with AP, they ®nd that the lease ratio had a generally positive, butinsigni®cant, relationship with the debt ratio, which implies a complementaryrelationship. The only signi®cant control variable was liquidity (a negativerelationship, as predicted). A&S investigate whether the positive relationshipbetween lease and debt ratios is attributable to poor control for the di�erencesbetween the debt capacities of leasing and non-leasing ®rms, by re-estimatingthe regression model on the sub-sample of ®rms which undertook leasing. TheOLS method is used as the dependent variable is no longer truncated.

In contrast with the Tobit results, OLS regression showed the lease ratio tobe signi®cantly negatively related to the debt ratio in each of the 3 years of thestudy. A&S concluded that debt and ®nance leases are indeed substitutes with,on average, £1 of ®nance lease displacing approximately £0.55 of debt over theperiod studied. In addition, the lease ratio was signi®cantly negatively relatedto liquidity and tax rate for each of the 3 years and to the price earnings ratiofor two out of 3 years.

436 V. Beattie et al. / Journal of Banking & Finance 24 (2000) 427±470

A&SÕs results appear to support suggestions that liquidity has a negativee�ect on leasing (Hull and Hubbard, 1980; Drury and Braund, 1990) and thatexpected growth (measured by A&S as the price earnings ratio) is a negativedebt determinant (Myers, 1977). A&S did not ®nd size to be a signi®cant ex-planatory variable, in contrast with previous studies of UK debt ®nancing(Marsh, 1982). Arguments presented earlier suggest that a negative relationshipbetween size and debt is expected but that leasing may be attractive to small®rms, implying a positive relationship between size and leasing. Thus, the lackof signi®cance for the size variable may be attributable to o�setting in¯uences.Alternatively, it may be due to the particular size proxy used; Sharpe andNguyen (1995) argue that total assets could be inappropriate, due to its lack ofindependence from the leasing choice.

A further aspect of the lease decision examined by A&S was industry in-¯uence. Several studies on the use of debt have concluded that industry clas-si®cation has a signi®cant in¯uence (see, for example, Scott, 1972; Remmers etal., 1975; Ferri and Jones, 1979; Bradley et al., 1984). To investigate whetherthis in¯uence extended to the use of leasing, A&S modi®ed their model toinclude industry dummy variables. However, these variables were found to begenerally insigni®cant.

The impact of a ®rmÕs ownership structure on the decision to lease assets hasrecently been examined using historical ®nancial statement data by Mehran etal. (1997). Consistent with theoretical arguments, they ®nd that Chief Execu-tive O�cer share ownership is positively related to leasing activity. Their re-sults also provide mixed evidence on the relationship between debt and leasing,with OLS estimates suggesting a complementary relationship between debt andcapitalised leases but a logit analysis suggesting that the two forms of ®nancingare substitutes. They found no evidence of an interaction between debt andoperating leases.

In summary, there is considerable diversity of evidence regarding lease±debtsubstitutability. This may result from the use of small samples, failure toproperly account for di�erences in ®rmsÕ debt capacity and/or failure to use acomprehensive measure of leasing (i.e., one which includes operating leases).

4. Methods

4.1. Lease±debt substitutability models

The estimation model to determine lease-debt substitutability is derivedfrom the de®nition of the debt-to-lease displacement ratio a (Eq. (1) above).Assuming that the debt ratio of a non-leasing ®rm (DRNL) is a function of anumber of control variables which re¯ect the characteristics that determine a®rmÕs debt ratio, then Eq. (1) can be rewritten as

V. Beattie et al. / Journal of Banking & Finance 24 (2000) 427±470 437

C �Control variables� � DRL � a LRL: �2�Rearranging the above, it follows that the lease ratio of a ®rm is

LRL � ÿ1=a DRL � 1=a C �Control variables� �3�with the resulting equation to be estimated:

LR � b0 � b1�DR� � bi�1 �Control variablei�: �4�If lease and debt ®nance are substitutes, irrespective of the degree, a willbe greater than zero and consequently b

1, the debt ratio coe�cient, will be

negative. 4

Throughout this study, Eq. (4) was estimated in two ways. Tobit regressionwas applied to the full sample to accommodate the truncated dependentvariable and OLS regression was applied to the restricted sub-sample ofcompanies with positive leasing.

4.2. Variable measurement

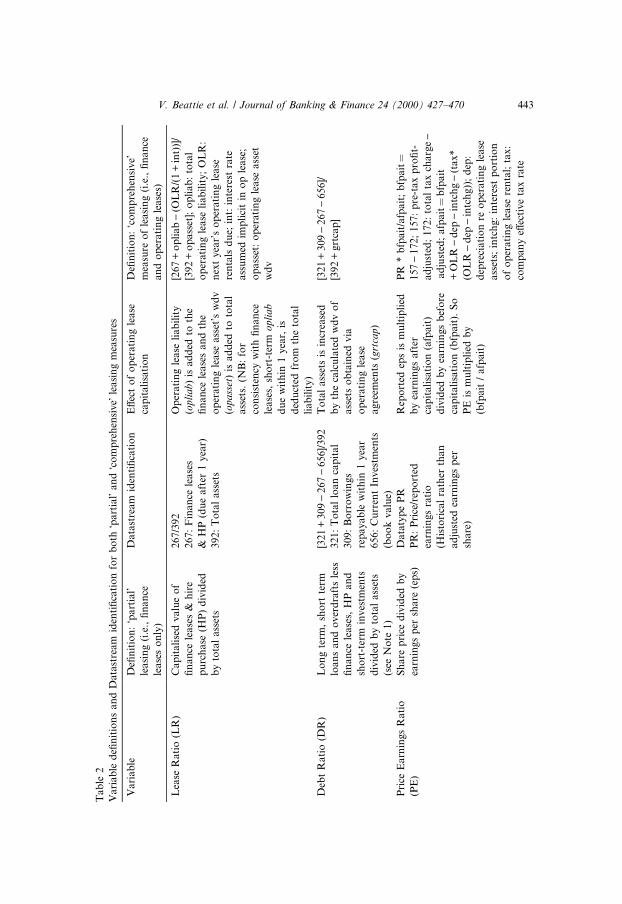

The experimental variables under consideration are measures of leasing andnon-leasing debt.

Leasing. Two ratios were used. The ®rst, which we call the partial lease ratio(LRP), represents long-term ®nance (capital) leases as a proportion of totalassets. The second, which we call the comprehensive lease ratio (LRC), is theratio of total long-term leases, including the estimated long-term operatinglease liability, to total assets.

Debt. The debt ratio was measured as the ratio of (the book value of) long-term and short-term debt, net of ®nance leases, to total assets.

To control for di�erences in debt capacity and its usage across ®rms, severalexplanatory variables which are likely to in¯uence the debt ratio of a non-leasing ®rm are chosen, consistent with the arguments presented earlier.

Pro®tability. Firms with higher pro®tability will generally be able to makegreater use of the tax-shielding e�ect of debt and will also have a lower risk ofbankruptcy, so would be expected to have higher debt levels. The measure ofpro®tability adopted here was return on capital employed (PROF).

4 The value of b1, however, is a measure of the lease-to-debt displacement ratio rather than the

debt-to-lease displacement ratio, a. Alpha cannot be determined by simply taking the inverse of b1

due to the presence of the constant and other independent variables in the regression model.

However, should a substitutability relationship arise, A&S proposed that a can easily be

determined by swapping the lease ratio and debt ratio in the above equation to treat the debt ratio

as the dependent variable.

438 V. Beattie et al. / Journal of Banking & Finance 24 (2000) 427±470

Asset structure. Firms with assets that can be used as security may be likelyto issue more debt. A simple proxy for the relative collateral value in a ®rmÕsassets structure is the proportion of ®xed assets to total assets (FAPROP).

Growth opportunities. Two proxies for potential growth opportunities wereadopted. The ®rst was a historical measures of the average percentage change,over the past 4 years, in total assets (TAGROW). 5 The second indicator ofgrowth was the price earnings ratio (PE). The advantage of this measure is thatit represents the stock marketÕs forward looking assessment of growth pros-pects. However, it is determined in part by the ®rmÕs leverage and is thereforesubject to some bias due to reverse causality (Titman and Wessels, 1988).

Size. Consistent with many previous studies, size was measured as thenatural log of total assets (LNSZ). An alternative speci®cation which allowsfor non-linearities was also adopted by including both size (SZ), measured astotal assets, and its square (SZSQ) in the model.

Industry classi®cation. In our model, a dummy variable for the industrialclassi®cation of the ®rm was adopted as a proxy for the nature of the ®rmÕsassets and its stakeholder relationships. Industries were split between thosewhere the number of sample constituents might be su�ciently large to captureany speci®c industry e�ects, and the rest. Five industries contain, on average,14 or more companies and were classed as large. Firms within these ®ve in-dustry groups were identi®ed with separate dummies (building, retail, engi-neering, electrical and leisure), taking the value of 1 if the ®rm is within thesector and zero otherwise. The remaining Ôcontrol groupÕ ®rms were accom-modated within the intercept term. Thus, the industry dummy coe�cientshould be viewed as an impact relative to the average control group ®rm. Thenon-speci®c nature of assets employed in retailing and leisure (e.g., shop space)suggests that these industries will use more leasing (positive coe�cients). Bycontrast, the likely ®rm-speci®c assets in the engineering and electrical indus-tries imply negative coe�cients; assets in the building sector are more variedand the expected sign is uncertain.

Tax. The tax-paying status of the ®rm was proxied by calculating the ef-fective tax rate, measured as the current year reported tax charge divided bypro®t before tax (TR). 6

Liquidity. This variable (LQ) was measured as the ®rmÕs current ratio (i.e.,current assets/current liabilities).

5 Another historical proxy was used. This measured the average percentage change, over the past

four years, in total sales (SALEGROW). There was a strong positive association (correlation

coe�cient of 0.75) between this and the TAGROW variable so to reduce potential multicollinearity

problems only TAGROW was included in the modelling stage.6 A second tax rate variable (TRAVE), the average of the TR measure over the last three years,

was also investigated. Results for the separate models incorporating TR and TRAVE were almost

identical so only results using TR are presented.

V. Beattie et al. / Journal of Banking & Finance 24 (2000) 427±470 439

When the comprehensive lease ratio (LRC) was used as the dependent vari-able, the explanatory variables were adjusted for the e�ect of operating leasecapitalisation. 7

4.3. Sample selection

A randomly selected sample of 300 listed industrial and commercial com-panies was originally selected for analysis and steps were taken to minimisesurvivorship bias. 8 Financial companies were excluded as our analysis of theExtel Company Analysis database showed this sector to employ minimalleasing. This original sample of 300 companies comprised 53 ÔdeadÕ companies,122 ÔnewÕ companies, and 125 companies which had existed from 1981 to 1994.Over the 1990±94 period of our study this gave between 217 (1990) and 232(1994) companies in existence in each particular year. The data requirements ofthe models, especially for variables such as growth proxies measured overseveral years, reduced the sample size for the models presented here. 9

Panel A of Table 1 gives details of the sample composition over the studyperiod, while Panel B provides an analysis of sample companies by industry for

7 Two variables were not adjusted, namely FAPROP and TAGROW. Adjustment to FAPROP

requires the addition of the total operating lease asset to the ®xed assets numerator of the variable

and also to the total assets denominator. The lease ratio dependent variable (LRP) requires a very

similar ÔadjustmentÕ as it is measured as ®nance lease liability plus operating lease liability/total

assets (including operating lease asset). The operating lease asset and liability are of similar size,

di�ering only in the cumulative net pro®t e�ect on equity, and are both of relatively large

magnitude, on average. The adjustment introduces a signi®cant positive bias in the correlation

between FAPROP and (LRP). Similar arguments apply to the TAGROW variable.8 The UKQI list current in 1995 (the year in which the sampling was undertaken) was used as the

initial sampling frame. This Datastream listing of approximately 1300 companies contains all of the

UK industrial and commercial companies for which Datastream has accounting information. A

particular methodological problem in studies concerning performance is survivorship bias, which

refers to the use of samples which are biased towards long-surviving companies (see, for example,

Brown et al. (1992) for a review of this problem). This is also important in a leasing context, as

previous research ®ndings suggest that leasing may be the only option in acquiring the use of assets

for unpro®table, or high growth, companies which have exhausted all alternative sources of ®nance.

To overcome this problem, the 1995 UKQI list was augmented by a group of approximately 250

ÔdeadÕ companies (failed, taken over, or gone private), identi®ed from a comparison of the Times

1000 1981/82 top UK companies (no historic UKQI list being available) with the 1995 UKQI list.

The year 1981 was selected for comparison purposes because it is the year in which ED 29 was

published, and some of our analysis therefore covers the 14-year period 1981 to 1994. Sample

representativeness checks were performed, based on total assets (item 392) and share capital and

reserves (item 307). This showed that the company size distribution and industry sector distribution

of the sample approximated closely to that of the population.9 Models were also estimated on the full sample set by excluding such multi-year variables. The

results (not presented here) were almost identical, con®rming that bias resulting from data needs is

not a signi®cant issue.

440 V. Beattie et al. / Journal of Banking & Finance 24 (2000) 427±470

Table 1

Composition of sample for 1990 through 1994

Number of companies with Total

Finance

leases

Operating

leases (only)

Any leases No leases

Panel A: Analysis of leasing by year

1990 95 60 155 24 179

1991 97 68 165 24 189

1992 97 72 169 24 193

1993 101 75 176 21 197

1994 105 83 188 18 206

Panel B: Analysis of leasing by industry for 1994a

Five largest industry groups (incorporated as dummy variables)

Building 11 12 23 3 26

Retail 10 12 22 1 23

Electrical/tronic 6 11 17 1 18

Engineering 11 6 17 0 17

Leisure 9 4 13 1 14

Sub-total A 47 45 92 6 98

Smaller industry groups (treated as control group)

Motor 8 0 8 3 11

Textiles 5 4 9 2 11

Breweries 2 5 7 3 10

Household goods 5 3 8 2 10

Utilities 5 4 9 0 9

Business support 4 2 6 1 7

Food manufacturing 5 2 7 0 7

Publishing & Printing 6 1 7 0 7

Chemicals 2 2 4 1 5

Computer services 5 0 5 0 5

Diversi®ed industrials 2 3 5 0 5

Distribution 2 2 4 0 4

Health 2 2 4 0 4

Media and agencies 2 1 3 0 3

Oil 0 3 3 0 3

Paper & Packaging 1 2 3 0 3

Metals 1 0 1 0 1

Mining 0 1 1 0 1

Transport 0 1 1 0 1

Waste control 1 0 1 0 1

Sub-total B 58 38 96 12 108

Total (A + B) 105 83 188 18 206

a The pattern across industries was very similar for 1990 to 1993 and, therefore, details are not

reported here.

V. Beattie et al. / Journal of Banking & Finance 24 (2000) 427±470 441

1994. Panel A shows that between 179 and 206 companies each year possessedall the relevant data. It also indicates the number of companies which used just®nance leases and those which used operating and/or ®nance leases. For ex-ample, in 1994, 105 companies (51%) used ®nance leases but this increased to188 (91%) once operating leases were considered. This suggests that mostcompanies adopt some form of leasing to ®nance the use of assets.

4.4. Data collection

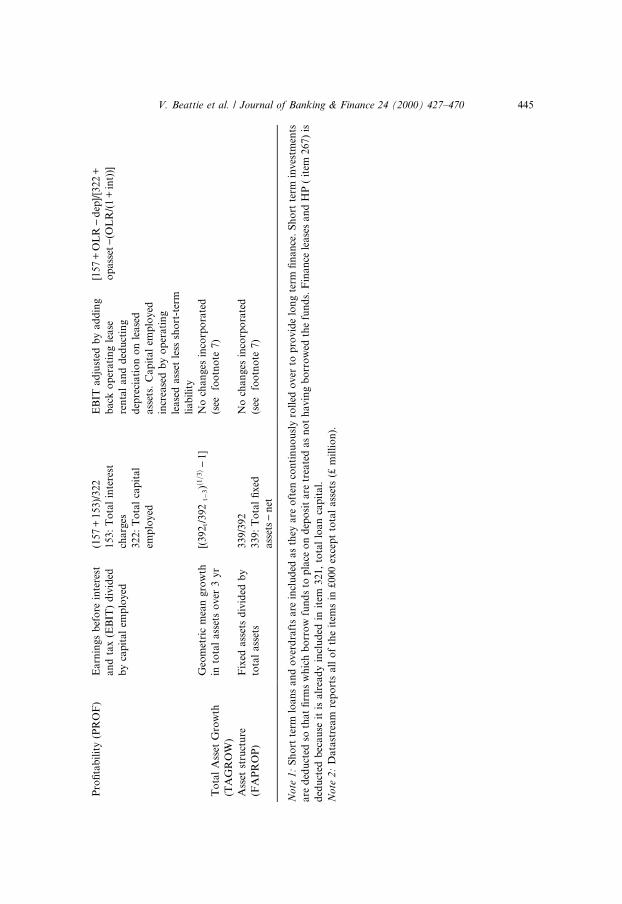

Eleven pro®t and loss and balance sheet items and industry group mem-bership were extracted from Datastream (see Table 2, column 3) to calculatethe regression variables. Leasing data to support the operating lease capitali-sation procedure is contained in the notes to the accounts (not available inDatastream) and was extracted manually from company ®nancial statementson micro®ches. Detailed speci®cation of variables is presented in Table 2.

4.5. Operating lease capitalisation procedure

The basis of the procedure developed by Imho� et al. (1991) for Ôcon-structive capitalisationÕ of operating leases is the schedule of minimum totalfuture operating lease payments disclosed by US companies in a note to the®nancial statements. The total commitment is analysed by time period(amounts payable in each of the next 5 years and after 5 years). Estimation ofthe present value of the unrecorded lease liability requires assumptions to bemade regarding the appropriate interest rate and the average remaining leaselife of leases whose remaining lease life exceeds 5 years. Estimation of thepresent value of the unrecorded lease asset requires further assumptions to bemade regarding the weighted average total lease life and the depreciationmethod which would be used. Finally, the impact of capitalisation on deferredtax, and hence balance sheet measures, requires an assumption to be maderegarding the appropriate tax rate.

The operating lease information disclosed by UK companies in a note to the®nancial statements is a schedule of next year's operating lease payments(compared to the minimum total future payments disclosed by US companies).This ®gure is analysed by asset category (i.e. Ôland and buildingsÕ and ÔotherÕ)and by lease expiry date (i.e., leases expiring within 1 year, between one and5 years and after 5 years). Although generally less complete than US disclo-sures, UK disclosures do have the advantage of giving a more reliable pictureof the companyÕs pattern of remaining lease lives.

In the present study, the Ôconstructive capitalisationÕ procedure was adaptedto take into account the di�erent operating lease disclosure requirements in theUK. In addition, preliminary analysis based on a set of six common assump-tions similar to those of Imho� et al., failed to produce reasonable and

442 V. Beattie et al. / Journal of Banking & Finance 24 (2000) 427±470

Tab

le2

Va

ria

ble

de®

nit

ion

sa

nd

Da

tast

ream

iden

ti®

cati

on

for

bo

thÔp

art

ialÕ

an

dÔc

om

pre

hen

siveÕ

leasi

ng

mea

sure

s

Va

ria

ble

De®

nit

ion

:`p

art

ial'

lea

sin

g(i

.e.,

®n

an

ce

lea

ses

on

ly)

Data

stre

am

iden

ti®

cati

on

E�

ect

of

op

erati

ng

lease

cap

itali

sati

on

De®

nit

ion

:`c

om

pre

hen

sive'

mea

sure

of

leasi

ng

(i.e

.,®

nan

ce

an

do

per

ati

ng

lease

s)

Lea

seR

ati

o(L

R)

Ca

pit

ali

sed

va

lue

of

®n

an

cele

ase

s&

hir

e

pu

rch

ase

(HP

)d

ivid

ed

by

tota

la

sset

s

267/3

92

Op

erati

ng

lease

liab

ilit

y

(opli

ab)

isad

ded

toth

e

®n

an

cele

ase

san

dth

e

op

erati

ng

lease

ass

et's

wd

v

(opass

et)

isad

ded

toto

tal

ass

ets.

(NB

:fo

r

con

sist

ency

wit

h®

nan

ce

lease

s,sh

ort

-ter

mopli

ab

du

ew

ith

in1

yea

r,is

ded

uct

edfr

om

the

tota

l

liab

ilit

y)

[267

+o

pli

ab

)(O

LR

/(1

+in

t))]

/

[392

+o

pass

et];

op

liab

:to

tal

op

erati

ng

lease

liab

ilit

y;

OL

R:

nex

tyea

r's

op

erati

ng

lease

ren

tals

du

e;in

t:in

tere

stra

te

ass

um

edim

pli

cit

ino

ple

ase

;

op

ass

et:

op

erati

ng

lease

ass

et

wd

v

267:

Fin

an

cele

ase

s

&H

P(d

ue

aft

er1

yea

r)

392:

To

tal

ass

ets

Deb

tR

ati

o(D

R)

Lo

ng

term

,sh

ort

term

loa

ns

an

do

ver

dra

fts

less

®n

an

cele

ase

s,H

Pa

nd

sho

rt-t

erm

inv

estm

ents

div

ided

by

tota

la

sset

s

(see

No

te1

)

[321

+309)

267)

656]/

392

To

tal

ass

ets

isin

crea

sed

by

the

calc

ula

ted

wd

vo

f

ass

ets

ob

tain

edvia

op

erati

ng

lease

agre

emen

ts(g

rtca

p)

[321

+309)

267)

656]/

[392

+grt

cap

]321:

To

tal

loan

cap

ital

309:

Bo

rro

win

gs

rep

ayab

lew

ith

in1

yea

r

656:

Cu

rren

tIn

ves

tmen

ts

(bo

ok

valu

e)

Pri

ceE

arn

ing

sR

ati

o

(PE

)

Sh

are

pri

ced

ivid

edb

y

earn

ing

sp

ersh

are

(ep

s)

Data

typ

eP

RR

epo

rted

eps

ism

ult

ipli

ed

by

earn

ings

aft

er

cap

itali

sati

on

(afp

ait

)

div

ided

by

earn

ings

bef

ore

cap

itali

sati

on

(bfp

ait

).S

o

PE

ism

ult

ipli

edb

y

(bfp

ait

/afp

ait

)

PR

*b

fpait

/afp

ait

;b

fpait�

157)

172;

15

7:

pre

-tax

pro

®t-

ad

just

ed;

172:

tota

lta

xch

arg

e)

ad

just

ed;

afp

ait�

bfp

ait

+O

LR

)d

ep)

intc

hg)

(tax*

(OL

R)

dep

)in

tch

g))

;d

ep:

dep

reci

ati

on

reo

per

ati

ng

lease

ass

ets;

intc

hg

:in

tere

stp

ort

ion

of

op

erati

ng

lease

ren

tal;

tax:

com

pan

ye�

ecti

ve

tax

rate

PR

:P

rice

/rep

ort

ed

earn

ings

rati

o

(His

tori

cal

rath

erth

an

ad

just

edea

rnin

gs

per

share

)

V. Beattie et al. / Journal of Banking & Finance 24 (2000) 427±470 443

Ta

ble

2(C

on

tin

ued

)

Va

ria

ble

De®

nit

ion

:`p

art

ial'

lea

sin

g(i

.e.,

®n

an

ce

lea

ses

on

ly)

Data

stre

am

iden

ti®

cati

on

E�

ect

of

op

erati

ng

lease

cap

itali

sati

on

De®

nit

ion

:`c

om

pre

hen

sive'

mea

sure

of

leasi

ng

(i.e

.,

®n

an

cean

do

per

ati

ng

lease

s)

Liq

uid

ity

(LQ

)C

urr

ent

ass

ets

div

ided

by

curr

ent

lia

bil

itie

s

741�

376/3

89

Cu

rren

tli

ab

ilit

ies

are

incr

ease

db

yth

ep

rese

nt

valu

eo

fn

ext

yea

r's

op

erati

ng

lease

ren

tal

ob

ligati

on

s

376/[

389

+(O

LR

/(1

+in

t))]

376:

To

tal

curr

ent

ass

ets

389:

To

tal

curr

ent

liab

ilit

ies

Siz

e(S

Z)

To

tal

ass

ets

392

(see

No

te2)

To

tal

ass

ets

are

incr

ease

d

by

op

erati

ng

lease

ass

et's

wd

v

(392

+o

pass

et)/

1000

Ta

xR

ate

(TR

)T

ax

cha

rge

div

ided

by

pro

®t

bef

ore

tax

172/1

57

To

tal

tax

charg

eis

ad

just

edb

yth

eaft

er-t

ax

chan

ge

inp

ro®

td

ue

to

op

erati

ng

lease

cap

itali

sa-

tio

n.

Ch

an

ge

inp

ro®

t

resu

lts

fro

mad

din

gb

ack

op

erati

ng

lease

ren

tal

an

d

ded

uct

ing

dep

reci

ati

on

an

d

inte

rest

charg

efo

r

lease

dass

ets

[172

+(t

ax*(O

LR

)d

ep)

intc

hg))

]/[1

57

+O

LR

)d

ep)

intc

hg]

157:

Pre

-tax

pro

®t-

ad

just

ed

172:

To

tal

tax

charg

e-ad

just

ed

444 V. Beattie et al. / Journal of Banking & Finance 24 (2000) 427±470

Pro

®ta

bil

ity

(PR

OF

)E

arn

ing

sb

efo

rein

tere

st

an

dta

x(E

BIT

)d

ivid

ed

by

cap

ita

lem

plo

yed

(157

+153)/

322

EB

ITad

just

edb

yad

din

g

back

op

erati

ng

lease

ren

tal

an

dd

edu

ctin

g

dep

reci

ati

on

on

lease

d

ass

ets.

Cap

ital

emp

loyed

incr

ease

db

yo

per

ati

ng

lease

dass

etle

sssh

ort

-ter

m

liab

ilit

y

[157

+O

LR

)d

ep]/

[322

+

op

ass

et)

(OL

R/(

1+

int)

)]153:

To

tal

inte

rest

charg

es

322:

To

tal

cap

ital

emp

loyed

To

tal

Ass

etG

row

th

(TA

GR

OW

)

Geo

met

ric

mea

ngro

wth

into

tal

ass

ets

ov

er3

yr

[(392

t/392

tÿ3)�

1=3� )

1]

No

chan

ges

inco

rpo

rate

d

(see

foo

tno

te7)

Ass

etst

ruct

ure

(FA

PR

OP

)

Fix

eda

sset

sd

ivid

edb

y

tota

la

sset

s

339/3

92

No

chan

ges

inco

rpo

rate

d

(see

foo

tno

te7)

339:

To

tal

®xed

ass

ets)

net

No

te1

:S

ho

rtte

rmlo

an

sa

nd

ov

erd

raft

sa

rein

clu

ded

as

they

are

oft

enco

nti

nu

ou

sly

roll

edo

ver

top

rovid

elo

ng

term

®n

an

ce.

Sh

ort

term

inves

tmen

ts

are

ded

uct

edso

tha

t®

rms

wh

ich

bo

rro

wfu

nd

sto

pla

ceo

nd

epo

sit

are

trea

ted

as

no

th

avin

gb

orr

ow

edth

efu

nd

s.F

inan

cele

ase

san

dH

P(

item

267)

is

ded

uct

edb

eca

use

itis

alr

ead

yin

clu

ded

init

em3

21

,to

tal

loan

cap

ital.

No

te2

:D

ata

stre

am

rep

ort

sall

of

the

item

sin

£000

exce

pt

tota

lass

ets

(£m

illi

on

).

V. Beattie et al. / Journal of Banking & Finance 24 (2000) 427±470 445

consistent results, due to the considerable variation in leasing patterns withinour sample companies. 10 We therefore developed the method to incorporatecompany-speci®c assumptions in respect of the remaining lease life, the assetproportion, and the e�ective tax rate. We also distinguish in our analysis be-tween asset categories and lease expiry categories, performing separate calcu-lations of remaining lease life and asset proportion for each. Further details ofour capitalisation procedure, and an illustration of its application to a par-ticular company, are given in Appendices 1 and 2.

Company ®nancial statements will be a�ected in several ways by thecapitalisation of operating leases. The e�ect on the variables in this study issummarised in Table 2 (columns 4 and 5). On the balance sheet, ®xed assetswill increase by the capitalised leased asset and liabilities will increase by theliability to make future lease payments, split between the current portion duewithin 1 year (current liability) and the longer-term portion. ShareholdersÕequity (retained pro®t) will be changed by the cumulative pro®t and losse�ect of capitalisation and deferred tax will also be a�ected. In the pro®t andloss account the full operating lease rental (OLR) payments are chargedagainst operating pro®t as a tax-deductible expense. On capitalisation of theleased asset, depreciation will be charged against operating pro®t and theinterest element of the OLR will be included under interest charges. Theimpact is that operating pro®t is likely to be higher (depreciation < OLR).Pro®t before tax will be lower in the early years of a lease, or lease portfolio,(depreciation + interest > OLR) and higher in the later years as the interestelement of OLR declines (depreciation + interest < OLR). Under current taxrules, the amount of tax paid will be unchanged, but the tax charged in thepro®t and loss account will be lower in the early years of the lease portfolioand higher in the later years. This was accommodated by adjustments todeferred tax.

10 The pattern of operating lease commitments over the period 1985 through 1994 was analyzed

for a small sub-sample of companies. This identi®ed some companies with commitments

predominantly in the Ô>5 yearsÕ category, some predominantly spread over the two Ô<5 yearsÕcategories, and some spread over all three expiry categories. Thus, some companies take on only

short- to medium-term leases, some mainly long-term leases, and some the whole range of lease

durations. Imho� et al.Õs assumption of uniform total and remaining lease lives is unable to capture

such diversity. In particular, calculation of the impact of capitalisation on the pro®t and loss

account (not discussed by the authors until their later paper Imho� et al., 1997) would be severely

distorted. For example, imagine a company which takes on only medium-term leases of, say, ®ve

years. In a steady state, the average remaining life for the company's leases would be approximately

3 years. Imho� et al. suggested a uniform assumption of 15 year remaining lease life. If this were

applied to such a company, the depreciation charge in the P&L account upon capitalisation of the

operating leases would be one-®fteenth of the asset value (assuming straight-line method) rather

than one-third and would give a large understatement of the e�ect on operating and pre-tax pro®t.

446 V. Beattie et al. / Journal of Banking & Finance 24 (2000) 427±470

5. Results

5.1. Descriptive statistics

The Ôconstructive capitalisationÕ process outlined above and in the Appen-dices allows the relative size of ®nance leases and operating leases to be as-sessed. For example, in 1994, the mean total liability in respect of ®nance leaseswas £3.8 million and for operating leases £50.8 million, of which £8.3 millionwould be categorised as short-term (<1 year) and £42.5 million long-term (>1year). This suggests that, on average, the operating leased liability is approx-imately 13 times larger than the liability in respect of ®nance leased assets. Thisreinforces the need for lease±debt substitutability research to incorporate op-erating leases.

Table 3 provides summary statistics for the variables, subscripted C to de-note their relevance to the comprehensive leasing measure, i.e., after they hadbeen adjusted to take account of the capitalisation of operating leases. 11

Statistics for variables based on the partial lease measure are also provided forcomparison (subscripted P). The mean value of the adjusted lease ratio LRC isapproximately 9.5% of total assets on average over the 5 years, compared to0.7% when considering only the use of ®nance leases. 12 This is consistent withthe above multiplier of approximately 13. The maximum value of LRC for anysingle company is 75% (in 1992), compared to a maximum of 18% (in 1991) forLRP, when only ®nance leases are considered. A similar pattern for debt ratiosDRC and DRP is observed with a decreasing trend in the mean DRC from apeak of 17.3% in 1991 down to 14.2% in 1994. The DRC values remain higherthan LRC, but are slightly lower than DRP, when ®nance leases alone wereconsidered. This occurs because capitalisation of operating leased assets leadsto an increase in total assets and a commensurate reduction in the debt ratio(debt to total assets).

Adjusted PEC ratios have slightly higher mean values than before. Thisimplies that earnings per share is reduced on average, due to the depreciationplus interest (after capitalisation) being a greater charge against pro®t than theoperating lease rental (before capitalisation). Adjusted LQC ratios have lower

11 The 1990-94 study period included a recession during which some companies reported losses

or very small pro®ts. This situation can distort relationships and two variables, in particular,

required adjustment to minimise the impact. Negative PE ratios were set to 100 for consistency

with companies experiencing low pro®ts (which explains the relatively high mean PE ratios

reported in Table 3) and PE ratios greater than 100 were set equal to 100. Companies reporting a

negative tax charge (i.e. repayment) associated with negative earnings gives a positive e�ective tax

rate. Such companies need to be recognised as ÔlowÕ tax payers so TR was set equal to 0. For

companies with a negative e�ective tax rate, TR was also set to 0, and high TR values in excess of 1

were set equal to 1.12 A&S report a ®nance LR of 0.9% of total assets in their sample.

V. Beattie et al. / Journal of Banking & Finance 24 (2000) 427±470 447

Table 3

Summary descriptive statistics for variables after and before adjustment for the capitalisation of

operating leases for the period 1990 through 1994a

1990 1991 1992 1993 1994

Number of companies 179 189 193 197 206

Lease Ratio (LR)

LRC Mean 8.34% 9.50% 10.05% 9.92% 9.59%

Standard deviation 11.98% 13.21% 14.11% 13.37% 13.24%

LRP Mean 0.65% 0.64% 0.60% 0.71% 0.67%

Standard deviation 1.44% 1.79% 1.56% 1.73% 1.51%

Debt Ratio (DR)

DRC Mean 16.86% 17.32% 15.77% 14.96% 14.19%

Standard deviation 13.75% 13.38% 13.16% 13.31% 11.03%

DRP Mean 18.19% 18.96% 17.25% 16.25% 15.54%

Standard deviation 14.37% 14.21% 13.97% 14.13% 12.02%

Expected Growth (PE)

PEC Mean 16.51 19.36 32.35 39.11 41.35

Standard deviation 22.39 25.12 34.80 34.79 36.24

PEP Mean 15.78 18.16 30.98 39.14 40.95

Standard deviation 21.51 23.68 33.89 34.99 36.18

Liquidity (LQ)

LQC Mean 1.476 1.439 1.510 1.466 1.440

Standard deviation 1.045 1.189 1.220 0.956 0.792

LQP Mean 1.539 1.510 1.603 1.559 1.529

Standard deviation 1.047 1.193 1.230 0.964 0.811

Size (SZ)

SZC Mean 612.1 654.2 663.3 684.3 728.1

Standard deviation 1889.7 2090.2 2230.4 2254.7 2270.2

SZP Mean 578.0 616.7 623.1 642.0 684.2

Standard deviation 1860.4 2058.0 2188.0 2209.8 2222.8

Tax Rate (TR)

TRC Mean 31.8% 28.2% 26.0% 28.2% 29.3%

Standard deviation 11.9% 14.4% 15.5% 17.3% 13.2%

TRP Mean 31.5% 28.4% 26.6% 28.8% 29.4%

Standard deviation 11.7% 14.3% 16.1% 17.9% 13.1%

Pro®tability (PROF)

PROFC Mean 20.1% 15.7% 13.8% 14.9% 14.3%

Standard deviation 13.7% 14.4% 15.9% 14.1% 19.5%

PROFP Mean 20.8% 14.9% 13.3% 14.8% 14.4%

Standard deviation 16.7% 22.8% 18.7% 15.4% 22.1%

Total Asset Growth (TAGROW)

TAGROW Mean 24.3% 16.5% 6.2% 3.5% 5.9%

Standard deviation 25.8% 24.0% 15.7% 14.9% 17.4%

Fixed Asset Proportion (FAPROP)

FAPROP Mean 37.0% 38.8% 38.3% 38.5% 37.7%

Standard deviation 21.7% 21.9% 21.9% 21.8% 22.0%

a Subscript C denotes the use of the comprehensive leasing measure (i.e., after capitalisation).

Subscript P denotes the use of the partial leasing measure (i.e., ®nance leases only) Fixed asset

proportion (FAPROP) and total asset growth (TAGROW) variables were not adjusted for capi-

talisation of operating leases in modelling (see footnote 7 in main text).

448 V. Beattie et al. / Journal of Banking & Finance 24 (2000) 427±470

mean values due to the increase in current liabilities caused by the short termelement of operating lease commitments. The average company size increasesby about 6% on average on adjustment for operating leased assets. The meanadjusted TRC does not signi®cantly change but, on average, the tax charge isslightly lower in line with a corresponding reduction in earnings. The observedtrends in pro®tability (PROF) and total asset growth (TAGROW) variablesre¯ect the impact of the recession during the study period. 13

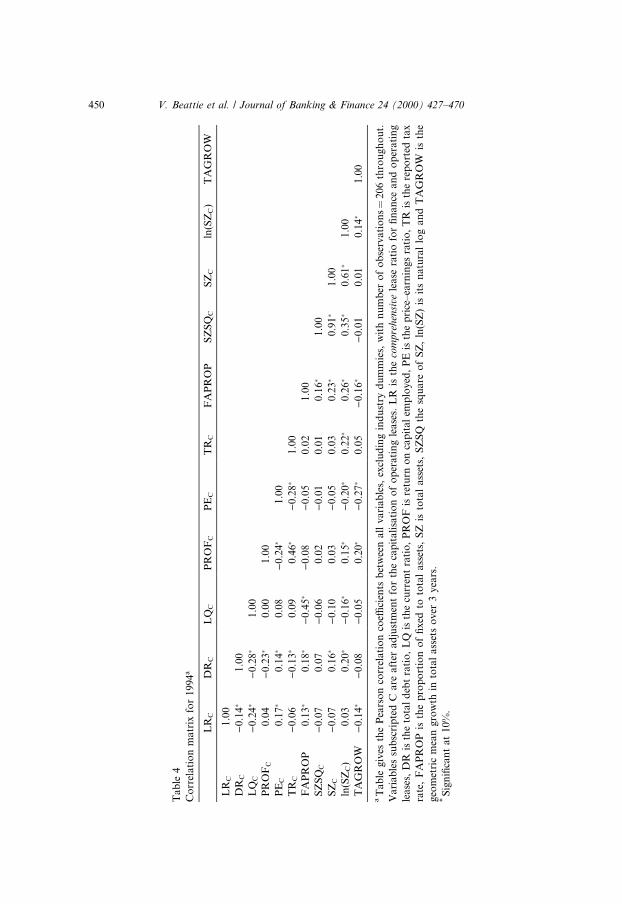

5.2. Correlation analysis for capitalisation-adjusted variables

Table 4 provides details of the correlations between the variables after ad-justment for operating lease capitalisation; these are generally as predicted.First, consider the control variables, seven of which are signi®cantly correlatedwith the debt ratio. The debt ratio is negatively related to pro®tability(PROFC) and to tax rate (TRC), contrary to the static trade-o� theory butconsistent with the pecking order theory. The positive association with FA-PROP suggests an increased use of debt by ®rms with assets which can be usedas collateral for loans. The proxies for growth give mixed signals; the weaknegative association with historical measure TAGROW is consistent with thepredicted lower use of debt by growth ®rms. However, the positive correlationbetween debt and PE ratio suggests that PEC may be capturing a di�erentcharacteristic to the other growth variables; indeed, the correlations betweenPEC and these are signi®cantly negative. Size (SZC) is expected to be positivelyrelated to long-term and inversely related to short-term debt. Our DRC mea-sure includes both short-term and long-term debt so the expected association isuncertain. The observed relationship is positive and signi®cant. Splitting thedebt ratio between short- and long-term reveals that the expected relationshipsdo hold, with a signi®cant correlation of 0.28 between size and long-term debt,and an insigni®cant correlation of )0.10 between size and short-term debt.Marsh (1982) also cites similar evidence that large companies tend to use morelong-term debt and small companies more short-term debt.

Second, consider the lease ratio (LRC) variable. It has a signi®cant nega-tive relationship with the debt ratio (DRC), indicating substitutability. The

13 We also carried out tests to see if there were any signi®cant di�erences between variables for

the three groups of ®rms (i.e., ÔdeadÕ, ÔnewÕ and ÔcontinuingÕ) in our sample. For each of the 5 years,

the lease ratio and the debt ratio were tested for both partial and comprehensive measures.

Unfortunately, there were insu�cient numbers of ÔdeadÕ ®rms in each yearÕs sample for reliable

estimation of variable means. No signi®cant di�erences between ÔnewÕ and ÔcontinuingÕ ®rms were

found for the mean partial lease ratio (LRP) or for either of the debt ratios (DRP, DRC). However,

the mean comprehensive lease ratio (LRC) was signi®cantly higher (at the 5% level) for ÔnewÕ ®rms

than for ÔcontinuingÕ ®rms, in each of the 5 years. This is consistent with the growth of the UK

services sector, which contains high users of operating leases. This growth is re¯ected our sample.

We are grateful to an anonymous referee for suggesting this additional analysis.

V. Beattie et al. / Journal of Banking & Finance 24 (2000) 427±470 449

Tab

le4

Co

rrel

ati

on

matr

ixfo

r1

99

4a

LR

CD

RC

LQ

CP

RO

FC

PE

CT

RC

FA

PR

OP

SZ

SQ

CS

ZC

ln(S

ZC

)T

AG

RO

W

LR

C1

.00

DR

C)

0.1

4�

1.0

0

LQ

C)

0.2

4�

)0

.28�

1.0

0

PR

OF

C0

.04

)0

.23�

0.0

01

.00

PE

C0

.17�

0.1

4�

0.0

8)

0.2

4�

1.0

0

TR

C)

0.0

6)

0.1

3�

0.0

90

.46�

)0.2

8�

1.0

0

FA

PR

OP

0.1

3�

0.1

8�

)0

.45�

)0.0

8)

0.0

50.0

21.0

0

SZ

SQ

C)

0.0

70

.07

)0

.06

0.0

2)

0.0

10.0

10.1

6�

1.0

0

SZ

C)

0.0

70

.16�

)0

.10

0.0

3)

0.0

50.0

30.2

3�

0.9

1�

1.0

0

ln(S

ZC

)0

.03

0.2

0�

)0

.16�

0.1

5�

)0.2

0�

0.2

2�

0.2

6�

0.3

5�

0.6

1�

1.0

0

TA

GR

OW

)0

.14�

)0

.08

)0

.05

0.2

0�

)0.2

7�

0.0

5)

0.1

6�

)0.0

10.0

10.1

4�

1.0

0

aT

ab

legiv

esth

eP

ears

on

corr

elati

on

coe�

cien

tsb

etw

een

all

vari

ab

les,

excl

ud

ing

ind

ust

ryd

um

mie

s,w

ith

nu

mb

ero

fo

bse

rvati

on

s�

206

thro

ugh

ou

t.

Va

ria

ble

ssu

bsc

rip

ted

Ca

rea

fter

ad

just

men

tfo

rth

eca

pit

ali

sati

on

of

op

erati

ng

lease

s.L

Ris

the

com

pre

hen

sive

lease

rati

ofo

r®

nan

cean

do

per

ati

ng

lea

ses,

DR

isth

eto

tal

deb

tra

tio

,L

Qis

the

curr

ent

rati

o,

PR

OF

isre

turn

on

cap

ital

emp

loyed

,P

Eis

the

pri

ce±ea

rnin

gs

rati

o,

TR

isth

ere

po

rted

tax

rate

,F

AP

RO

Pis

the

pro

po

rtio

no

f®

xed

toto

tal

ass

ets,

SZ

isto

tal

ass

ets,

SZ

SQ

the

squ

are

of

SZ

,ln

(SZ

)is

its

natu

ral

log

an

dT

AG

RO

Wis

the

geo

met

ric

mea

ng

row

thin

tota

la

sset

so

ver

3y

ears

.*

Sig

ni®

can

ta

t1

0%

.

450 V. Beattie et al. / Journal of Banking & Finance 24 (2000) 427±470

signi®cant negative coe�cient with liquidity (LQC) is as expected with poorliquidity ®rms engaging in more leasing. The positive coe�cient with PEC

suggests that growth ®rms undertake more leasing, but the historical growthmeasures give opposite indications. The positive association with the assetstructure variable (FAPROP) supports the Smith and Wakeman (1985) con-tention that ®rms with certain types of assets will ®nd it easier to engage in bothleasing and debt ®nance. The size e�ect is weakly negative, but is consistentwith smaller ®rms using more leasing, on average.

Two separate models were estimated: First, with size proxied using LNSZand, second, to accommodate potential non-linearities, including both SZ andSZSQ. As almost identical results were obtained, only the model with theLNSZ proxy is presented here.

5.3. Regression estimates based on partial lease ratio

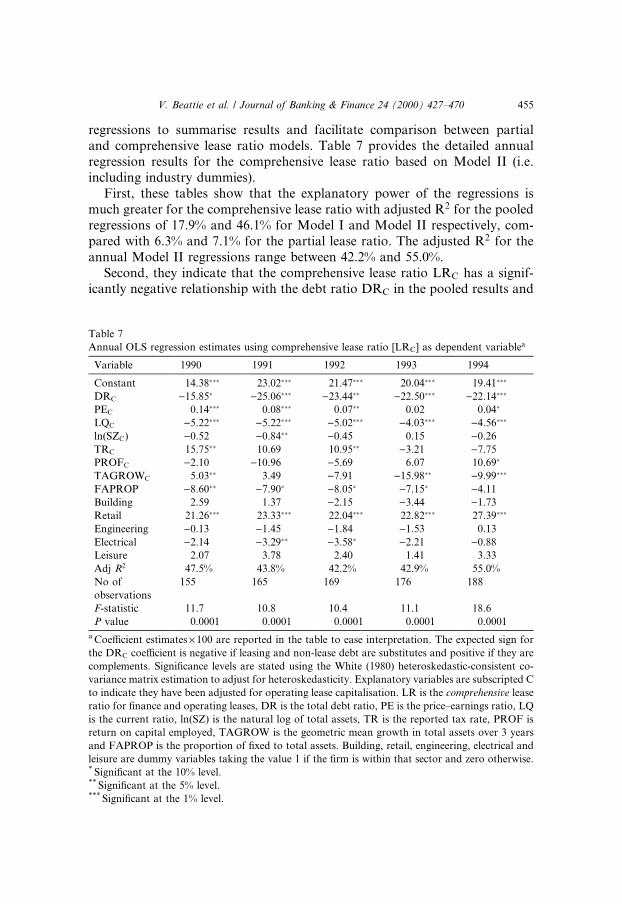

Initially, to give a benchmark for later comparisons, we replicate the A&Sstudy which considered a partial measure of leases only (i.e., ®nance leases) butwe include three additional control variables (PROF, TAGROW and FA-PROP). For comparison with the A&S results, Eq. (4) was ®rst estimated ex-cluding industry dummies (Model I) and then including them (Model II). Tobitregression was used for the full sample and OLS regression for only thosecompanies which used ®nance leases. Cross-sectional regressions were carriedout separately for each of the 5 years 1990 through 1994 and pooled over theentire 5 years. The pooled regressions provide a useful means of summarisingthe results and are reported in Table 5. The signi®cance levels from these re-gressions are subject to bias and are likely to be overstated; they should,therefore, be viewed with caution. To aid interpretation of signi®cance, thenumber of times, out of ®ve, in which the variable appeared as signi®cant (atthe 10% level) in the annual regressions is also reported.

The explanatory power of the annual regressions was low (mean adj. R2 ofapproximately 3%), and did not greatly improve in the pooled regressions. Inboth the Tobit and OLS regression models, the debt ratio coe�cient wasgenerally positive, consistent with complementarity, but was not signi®cant.Only the liquidity variable, LQ (in the Tobit regressions) and the asset struc-ture variable, FAPROP (in the OLS regressions) were generally signi®cant withthe expected sign. Thus, there is weak evidence that companies with poor li-quidity and those with assets which can be used as collateral, take on relativelymore ®nance leases.

The coe�cients on the industry dummies are generally insigni®cant in theannual regressions, though signi®cantly negative for retail in the pooled re-gression. This provides weak evidence that the retail sector employs relativelyless ®nance leases than most sectors. Given the general, rather than ®rm-speci®c, nature of assets within the retail sector, this result is counter-intuitive.

V. Beattie et al. / Journal of Banking & Finance 24 (2000) 427±470 451

Ta

ble

5

Po

ole

dcr

oss

-sec

tio

nal

To

bit

an

dO

LS

regre

ssio

nes

tim

ate

su

sin

gp

art

ial

lease

rati

o[L

RP]

as

dep

end

ent

vari

ab

lea

Vari

ab

leT

ob

ites

tim

ate

sO

LS

esti

mate

sE

xp

ecte

d

Sig

nM

od

elI

No

Sig

Mo

del

IIN

oS

igM

od

elI

No

Sig

Mo

del

IIN

oS

ig

Co

nst

an

t0.5

42

00.6

13

00.9

30�

00

.937�

0

DR

P1.0

95

00.8

23

00.1

48

0)

0.0

05

0U

nce

rtain

PE

P0.0

02

00.0

03

00.0

01

00

.001

0U

nce

rtain

LQ

P)

0.5

83���

4)

0.5

97���

4)

0.1

63

0)

0.1

71

0N

egati

ve

ln(S

ZP)

)0.2

01���

2)

0.1

75���

1)

0.1

17��

0)

0.0

91�

0U

nce

rtain

TR

P0.5

08

00.3

76

00.0

26

0)

0.1

81

0N

egati

ve

PR

OF

P)

0.7

01

0)

0.7

42

0)

0.0

30

0)

0.0

18

0U

nce

rtain

TA

GR

OW

P1.4

08���

21.3

27���

20.2

31

00

.187

0N

egati