1Copyright © 2012 Tata Consultancy Services Limited

Customer Keynote: GDF Suez

Olivier Vandelaer

M & IS IS Service Center Manager, GDF Suez

#TCSARDay

2TCS Confidential 2

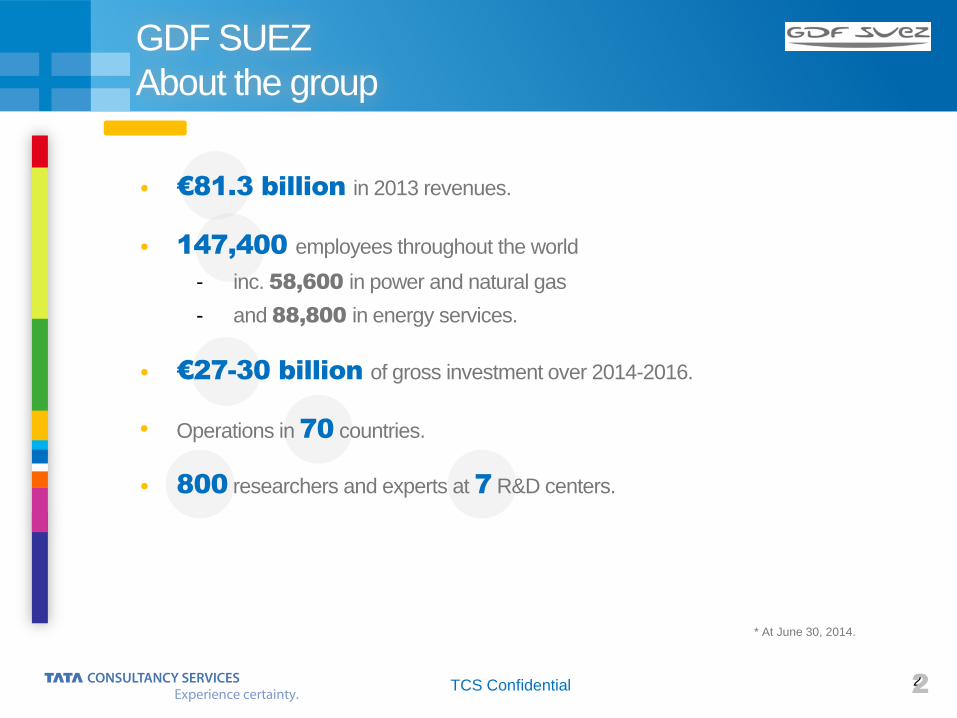

• €81.3 billion in 2013 revenues.

• 147,400 employees throughout the world

- inc. 58,600 in power and natural gas

- and 88,800 in energy services.

• €27-30 billion of gross investment over 2014-2016.

• Operations in 70 countries.

• 800 researchers and experts at 7 R&D centers.

* At June 30, 2014.

GDF SUEZ

About the group

3TCS Confidential 3

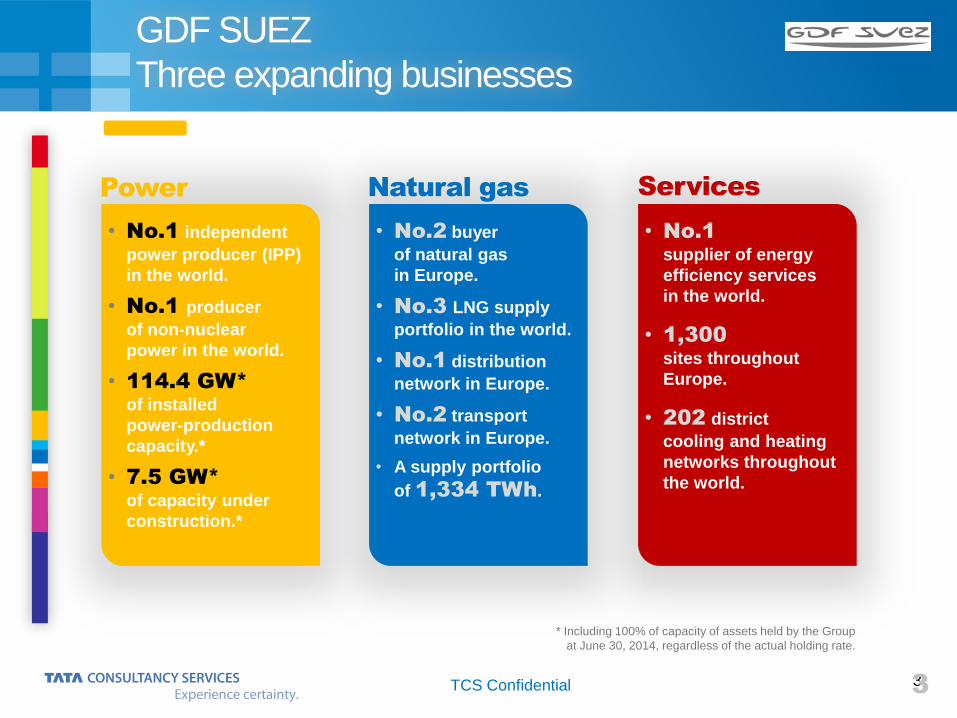

• No.1

supplier of energy

efficiency services

in the world.

• 1,300

sites throughout

Europe.

• 202 district

cooling and heating

networks throughout

the world.

• No.2 buyer

of natural gas

in Europe.

• No.3 LNG supply

portfolio in the world.

• No.1 distribution

network in Europe.

• No.2 transport

network in Europe.

• A supply portfolio

of 1,334 TWh.

• No.1 independent

power producer (IPP)

in the world.

• No.1 producer

of non-nuclear

power in the world.

• 114.4 GW*

of installed

power-production

capacity.*

• 7.5 GW*

of capacity under

construction.*

Power Services

* Including 100% of capacity of assets held by the Group

at June 30, 2014, regardless of the actual holding rate.

Natural gas

GDF SUEZ

Three expanding businesses

4TCS Confidential 4

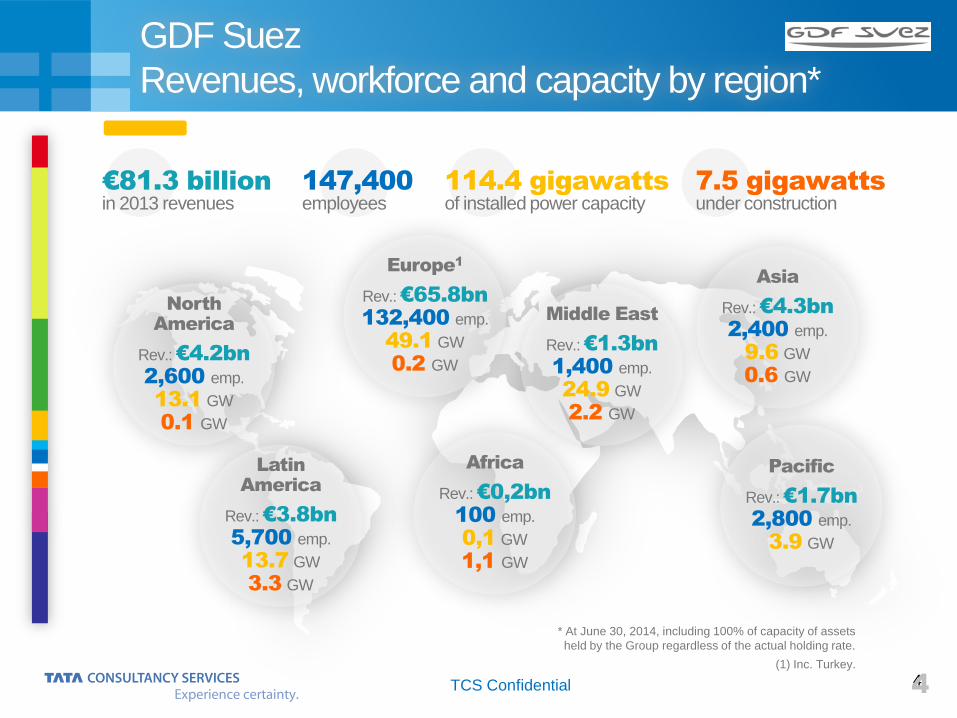

GDF Suez

Revenues, workforce and capacity by region*

* At June 30, 2014, including 100% of capacity of assets

held by the Group regardless of the actual holding rate.

(1) Inc. Turkey.

€81.3 billion

in 2013 revenues147,400

employees7.5 gigawatts

under construction114.4 gigawatts

of installed power capacity

Latin

America

Rev.:€3.8bn

5,700 emp.

13.7 GW

3.3 GW

North

America

Rev.:€4.2bn

2,600 emp.

13.1 GW

0.1 GW

Europe1

Rev.:€65.8bn

132,400 emp.

49.1 GW

0.2 GW

Africa

Rev.:€0,2bn

100 emp.

0,1 GW

1,1 GW

Middle East

Rev.:€1.3bn

1,400 emp.

24.9 GW

2.2 GW

Asia

Rev.:€4.3bn

2,400 emp.

9.6 GW

0.6 GW

Pacific

Rev.:€1.7bn

2,800 emp.

3.9 GW

5TCS Confidential

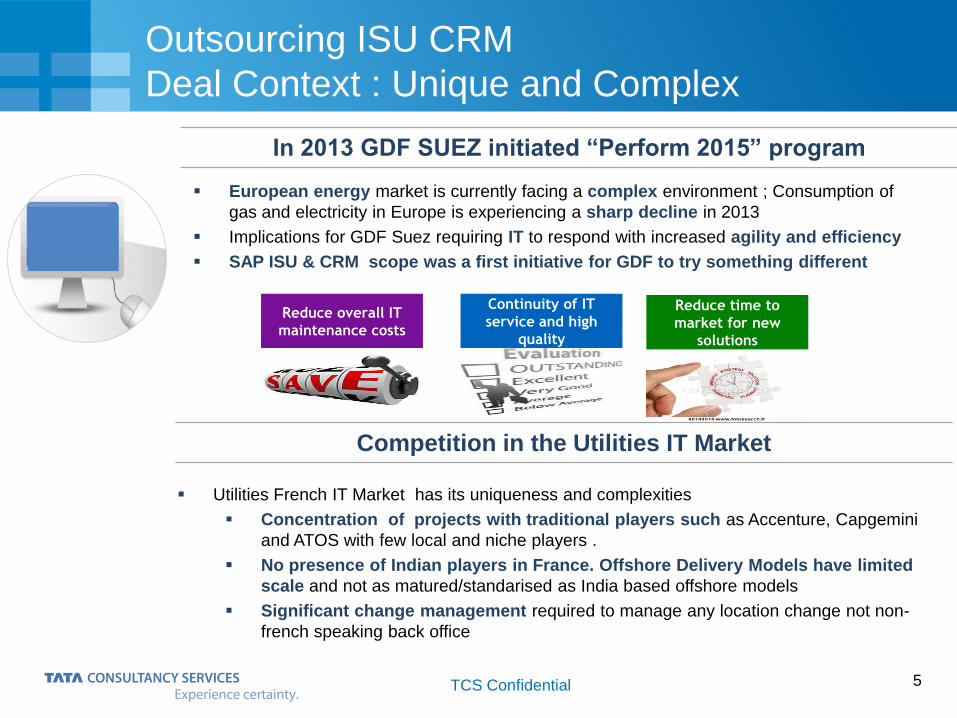

Outsourcing ISU CRM

Deal Context : Unique and Complex

In 2013 GDF SUEZ initiated “Perform 2015” program

European energy market is currently facing a complex environment ; Consumption of

gas and electricity in Europe is experiencing a sharp decline in 2013

Implications for GDF Suez requiring IT to respond with increased agility and efficiency

SAP ISU & CRM scope was a first initiative for GDF to try something different

Reduce overall IT

maintenance costs

Continuity of IT

service and high

quality

Reduce time to

market for new

solutions

Competition in the Utilities IT Market

Utilities French IT Market has its uniqueness and complexities

Concentration of projects with traditional players such as Accenture, Capgemini

and ATOS with few local and niche players .

No presence of Indian players in France. Offshore Delivery Models have limited

scale and not as matured/standarised as India based offshore models

Significant change management required to manage any location change not non-

french speaking back office

6TCS Confidential

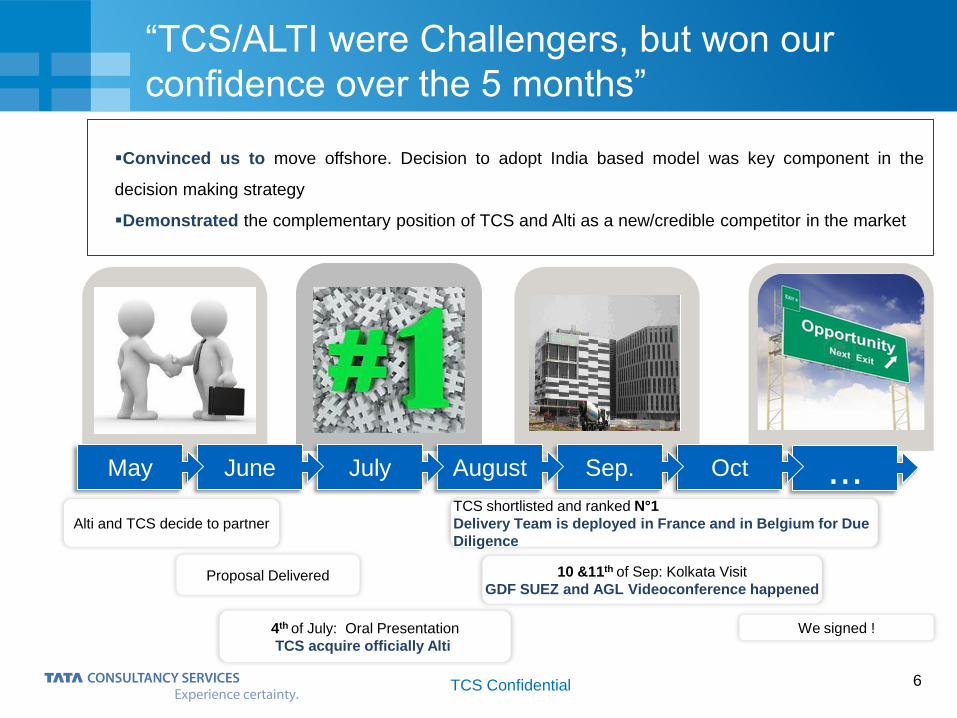

...Oct

Alti and TCS decide to partner

4th of July: Oral Presentation

TCS acquire officially Alti

Sep.AugustJulyJuneMay

Proposal Delivered 10 &11th of Sep: Kolkata Visit

GDF SUEZ and AGL Videoconference happened

TCS shortlisted and ranked N°1

Delivery Team is deployed in France and in Belgium for Due

Diligence

We signed !

“TCS/ALTI were Challengers, but won our

confidence over the 5 months”

Convinced us to move offshore. Decision to adopt India based model was key component in the

decision making strategy

Demonstrated the complementary position of TCS and Alti as a new/credible competitor in the market

7TCS Confidential

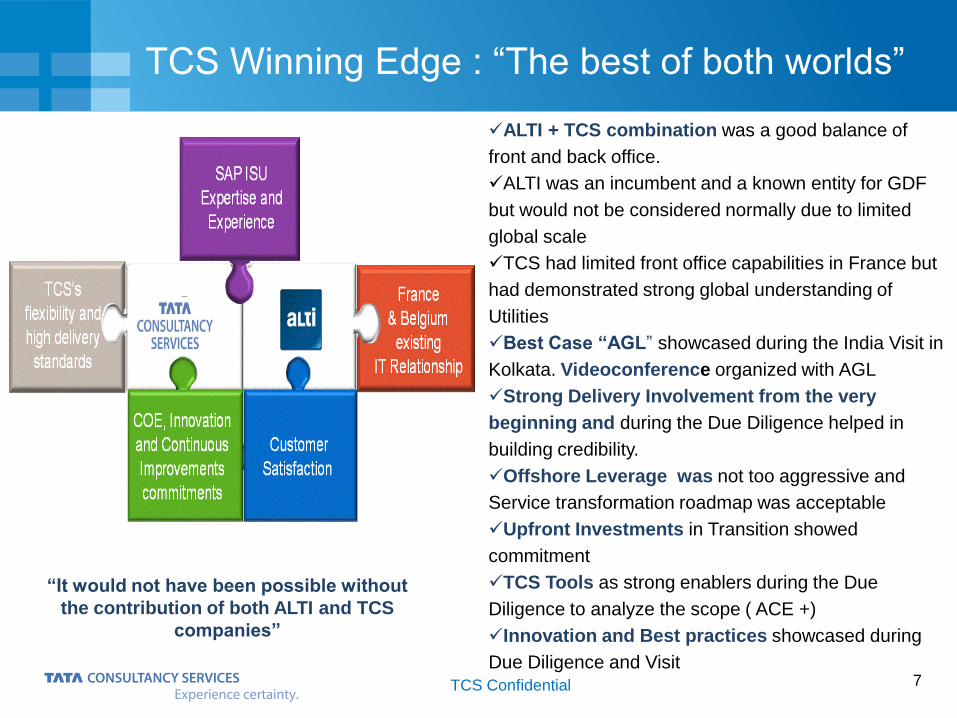

TCS Winning Edge : “The best of both worlds”

ALTI + TCS combination was a good balance of

front and back office.

ALTI was an incumbent and a known entity for GDF

but would not be considered normally due to limited

global scale

TCS had limited front office capabilities in France but

had demonstrated strong global understanding of

Utilities

Best Case “AGL” showcased during the India Visit in

Kolkata. Videoconference organized with AGL

Strong Delivery Involvement from the very

beginning and during the Due Diligence helped in

building credibility.

Offshore Leverage was not too aggressive and

Service transformation roadmap was acceptable

Upfront Investments in Transition showed

commitment

TCS Tools as strong enablers during the Due

Diligence to analyze the scope ( ACE +)

Innovation and Best practices showcased during

Due Diligence and Visit

“It would not have been possible without

the contribution of both ALTI and TCS

companies”

8TCS Confidential

12 months later….

Transition of all 5 applications completed and TCS are

delivering the services since April 2013. Over 100

associates from TCS are assigned to this contract in

France, Belgium and India

Several major and minor releases have been delivered

both as evolutions and projects

Governance of this programme across France, Belgium

and India is now global. The second strategic committee

was held out of India with GDF Suez and TCS teams

travelling together to discuss opportunities for further

collaboration

We have now moved into year 2 of operations and

looking to further industrialise and bring in best practices

into the relationship

A continuous improvement initiative has in place for

some with TCS and GDF Suez proposing joint initiatives to

improve service and value to the end user community

Copyright © 2012 Tata Consultancy Services Limited

Thank You

Recommended