Copyright 2016, Kinsale Trading LLC. All Rights Reserved. www.sevensreport.com

October 20, 2016

Equities

Market Recap

Stocks rallied for a second straight day thanks to higher

oil, although the gains were modest and stocks finished

off their best levels of the day. The S&P 500 rose 022%.

Stocks were flat initially Wednesday as Chinese econom-

ic data largely met expectations (which isn’t a negative,

but not exactly a positive, either, given current market

valuations). Earnings continued to roll in and there were

some more decent beats, especially from the banks, but

overall the results aren’t materially changing anyone’s

outlook on the markets (it’s still way too early).

Stocks opened slightly lower but then rebounded and

were flat heading into the weekly oil inventory data.

That data was bullish (more on that later) and combined

with jawboning from the Saudi Oil minster crude oil shot

higher and pulled stocks up with it. The S&P 500 rallied

immediately following the inventory release and then

took a short pause for the close in Europe before rallying

throughout the afternoon.

Energy was the sector pulling the market higher and that

continued through oil’s close despite the fact that oil hit

its intraday high earlier in the morning. But with oil

closed, stocks gave back about half the day’s gains and

closed quietly.

Trading Color

The major indices all traded generally in line with one

another, but beneath the surface Wednesday for a sec-

ond straight day the rotation out of safety and into cycli-

cals was back on. Specifically, of the nine SPDRs we track

only three—utilities, healthcare and consumer staples—

Pre 7:00 Look

Futures and int’l shares are flat to slightly higher as the last

Presidential Debate and some overnight Fed comments are

digested ahead of the ECB Announcement this morning.

Economically, British Retail Sales was the latest data point

to disappoint (0.0% vs. E: 0.2%), as Brexit woes continue.

Econ Today: ECB Press Conference (8:30 a.m.), Jobless

Claims (E: 250K), Philly Fed Survey (7.0), Existing Home

Sales (E: 5.350M). Fed Speak: Dudley (8:30 a.m. ET)

Earnings Today: AAL ($1.68), VZ ($0.99), MSFT ($$0.68), BK

($0.81), TRV ($2.37).

Regional Banks (KRE): Banks are closing in on 52 week

highs, and if banks can continue to rally that will help

support the broad market.

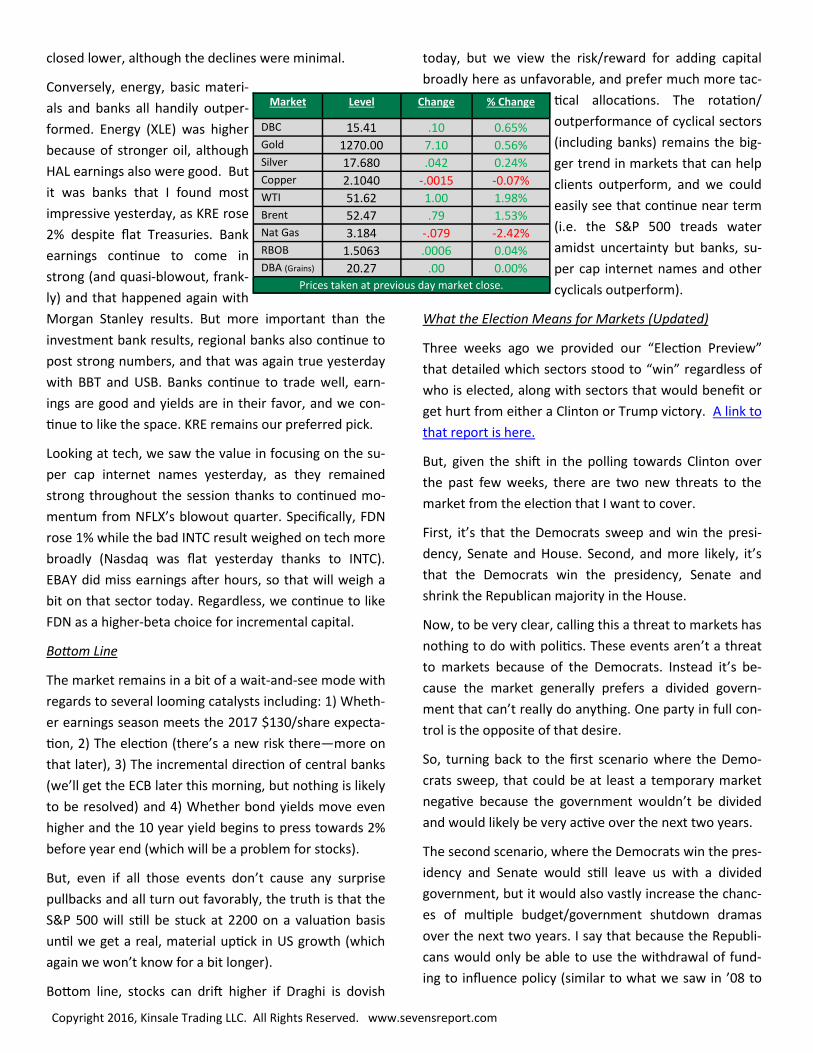

Market Level Change % Change

S&P 500 Futures 2140.25 2.25 0.11%

U.S. Dollar (DXY) 98.005 .065 0.07%

Gold 1270.80 .90 0.07%

WTI 51.28 -.54 -1.04%

10 Year 1.752 .003 0.17%

Market Level Change % Change

Dow 18,202.62 40.68 0.22% TSX 14,840.49 88.24 0.60% Stoxx 50 3,065.34 9.40 0.31% FTSE 7,015.54 -6.38 -0.09% Nikkei 17,235.50 236.59 1.39% Hang Seng 23,374.40 69.43 0.30% ASX 5,442.14 6.78 0.12%

Prices taken at previous day market close.

Copyright 2016, Kinsale Trading LLC. All Rights Reserved. www.sevensreport.com

closed lower, although the declines were minimal.

Conversely, energy, basic materi-

als and banks all handily outper-

formed. Energy (XLE) was higher

because of stronger oil, although

HAL earnings also were good. But

it was banks that I found most

impressive yesterday, as KRE rose

2% despite flat Treasuries. Bank

earnings continue to come in

strong (and quasi-blowout, frank-

ly) and that happened again with

Morgan Stanley results. But more important than the

investment bank results, regional banks also continue to

post strong numbers, and that was again true yesterday

with BBT and USB. Banks continue to trade well, earn-

ings are good and yields are in their favor, and we con-

tinue to like the space. KRE remains our preferred pick.

Looking at tech, we saw the value in focusing on the su-

per cap internet names yesterday, as they remained

strong throughout the session thanks to continued mo-

mentum from NFLX’s blowout quarter. Specifically, FDN

rose 1% while the bad INTC result weighed on tech more

broadly (Nasdaq was flat yesterday thanks to INTC).

EBAY did miss earnings after hours, so that will weigh a

bit on that sector today. Regardless, we continue to like

FDN as a higher-beta choice for incremental capital.

Bottom Line

The market remains in a bit of a wait-and-see mode with

regards to several looming catalysts including: 1) Wheth-

er earnings season meets the 2017 $130/share expecta-

tion, 2) The election (there’s a new risk there—more on

that later), 3) The incremental direction of central banks

(we’ll get the ECB later this morning, but nothing is likely

to be resolved) and 4) Whether bond yields move even

higher and the 10 year yield begins to press towards 2%

before year end (which will be a problem for stocks).

But, even if all those events don’t cause any surprise

pullbacks and all turn out favorably, the truth is that the

S&P 500 will still be stuck at 2200 on a valuation basis

until we get a real, material uptick in US growth (which

again we won’t know for a bit longer).

Bottom line, stocks can drift higher if Draghi is dovish

today, but we view the risk/reward for adding capital

broadly here as unfavorable, and prefer much more tac-

tical allocations. The rotation/

outperformance of cyclical sectors

(including banks) remains the big-

ger trend in markets that can help

clients outperform, and we could

easily see that continue near term

(i.e. the S&P 500 treads water

amidst uncertainty but banks, su-

per cap internet names and other

cyclicals outperform).

What the Election Means for Markets (Updated)

Three weeks ago we provided our “Election Preview”

that detailed which sectors stood to “win” regardless of

who is elected, along with sectors that would benefit or

get hurt from either a Clinton or Trump victory. A link to

that report is here.

But, given the shift in the polling towards Clinton over

the past few weeks, there are two new threats to the

market from the election that I want to cover.

First, it’s that the Democrats sweep and win the presi-

dency, Senate and House. Second, and more likely, it’s

that the Democrats win the presidency, Senate and

shrink the Republican majority in the House.

Now, to be very clear, calling this a threat to markets has

nothing to do with politics. These events aren’t a threat

to markets because of the Democrats. Instead it’s be-

cause the market generally prefers a divided govern-

ment that can’t really do anything. One party in full con-

trol is the opposite of that desire.

So, turning back to the first scenario where the Demo-

crats sweep, that could be at least a temporary market

negative because the government wouldn’t be divided

and would likely be very active over the next two years.

The second scenario, where the Democrats win the pres-

idency and Senate would still leave us with a divided

government, but it would also vastly increase the chanc-

es of multiple budget/government shutdown dramas

over the next two years. I say that because the Republi-

cans would only be able to use the withdrawal of fund-

ing to influence policy (similar to what we saw in ’08 to

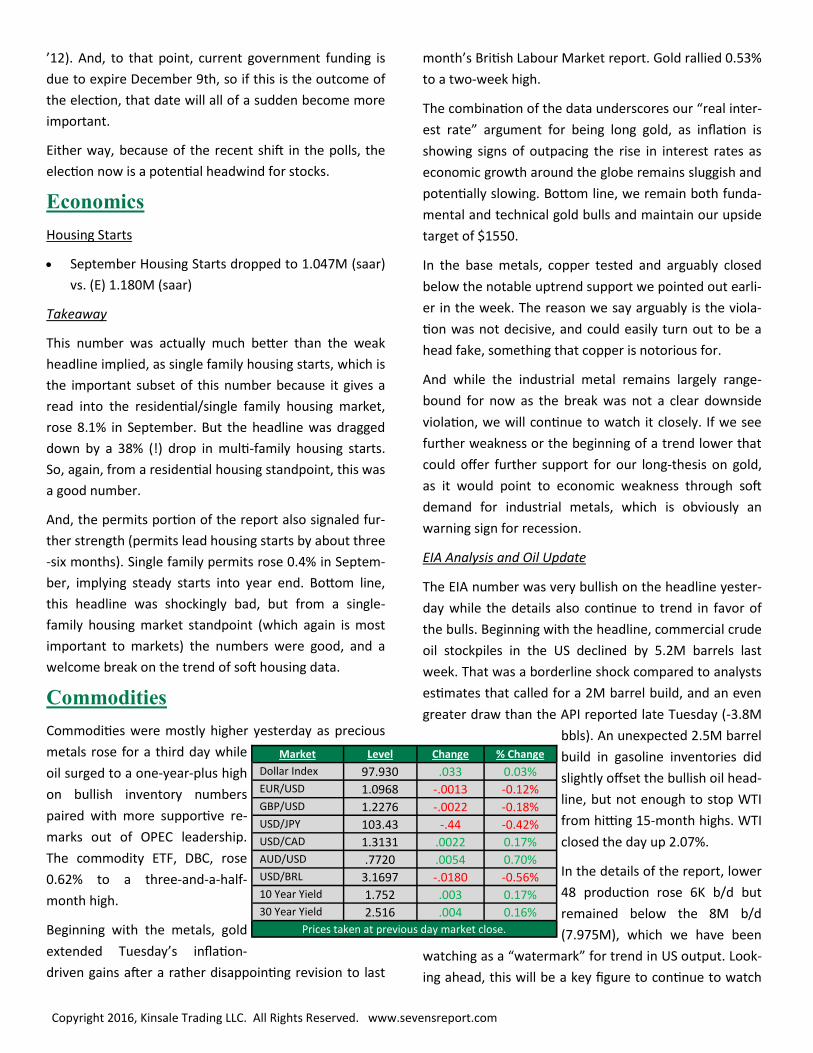

Market Level Change % Change

DBC 15.41 .10 0.65% Gold 1270.00 7.10 0.56% Silver 17.680 .042 0.24%

Copper 2.1040 -.0015 -0.07% WTI 51.62 1.00 1.98% Brent 52.47 .79 1.53% Nat Gas 3.184 -.079 -2.42% RBOB 1.5063 .0006 0.04% DBA (Grains) 20.27 .00 0.00%

Prices taken at previous day market close.

Copyright 2016, Kinsale Trading LLC. All Rights Reserved. www.sevensreport.com

’12). And, to that point, current government funding is

due to expire December 9th, so if this is the outcome of

the election, that date will all of a sudden become more

important.

Either way, because of the recent shift in the polls, the

election now is a potential headwind for stocks.

Economics

Housing Starts

September Housing Starts dropped to 1.047M (saar)

vs. (E) 1.180M (saar)

Takeaway

This number was actually much better than the weak

headline implied, as single family housing starts, which is

the important subset of this number because it gives a

read into the residential/single family housing market,

rose 8.1% in September. But the headline was dragged

down by a 38% (!) drop in multi-family housing starts.

So, again, from a residential housing standpoint, this was

a good number.

And, the permits portion of the report also signaled fur-

ther strength (permits lead housing starts by about three

-six months). Single family permits rose 0.4% in Septem-

ber, implying steady starts into year end. Bottom line,

this headline was shockingly bad, but from a single-

family housing market standpoint (which again is most

important to markets) the numbers were good, and a

welcome break on the trend of soft housing data.

Commodities

Commodities were mostly higher yesterday as precious

metals rose for a third day while

oil surged to a one-year-plus high

on bullish inventory numbers

paired with more supportive re-

marks out of OPEC leadership.

The commodity ETF, DBC, rose

0.62% to a three-and-a-half-

month high.

Beginning with the metals, gold

extended Tuesday’s inflation-

driven gains after a rather disappointing revision to last

month’s British Labour Market report. Gold rallied 0.53%

to a two-week high.

The combination of the data underscores our “real inter-

est rate” argument for being long gold, as inflation is

showing signs of outpacing the rise in interest rates as

economic growth around the globe remains sluggish and

potentially slowing. Bottom line, we remain both funda-

mental and technical gold bulls and maintain our upside

target of $1550.

In the base metals, copper tested and arguably closed

below the notable uptrend support we pointed out earli-

er in the week. The reason we say arguably is the viola-

tion was not decisive, and could easily turn out to be a

head fake, something that copper is notorious for.

And while the industrial metal remains largely range-

bound for now as the break was not a clear downside

violation, we will continue to watch it closely. If we see

further weakness or the beginning of a trend lower that

could offer further support for our long-thesis on gold,

as it would point to economic weakness through soft

demand for industrial metals, which is obviously an

warning sign for recession.

EIA Analysis and Oil Update

The EIA number was very bullish on the headline yester-

day while the details also continue to trend in favor of

the bulls. Beginning with the headline, commercial crude

oil stockpiles in the US declined by 5.2M barrels last

week. That was a borderline shock compared to analysts

estimates that called for a 2M barrel build, and an even

greater draw than the API reported late Tuesday (-3.8M

bbls). An unexpected 2.5M barrel

build in gasoline inventories did

slightly offset the bullish oil head-

line, but not enough to stop WTI

from hitting 15-month highs. WTI

closed the day up 2.07%.

In the details of the report, lower

48 production rose 6K b/d but

remained below the 8M b/d

(7.975M), which we have been

watching as a “watermark” for trend in US output. Look-

ing ahead, this will be a key figure to continue to watch

Market Level Change % Change

Dollar Index 97.930 .033 0.03% EUR/USD 1.0968 -.0013 -0.12%

GBP/USD 1.2276 -.0022 -0.18% USD/JPY 103.43 -.44 -0.42% USD/CAD 1.3131 .0022 0.17% AUD/USD .7720 .0054 0.70% USD/BRL 3.1697 -.0180 -0.56% 10 Year Yield 1.752 .003 0.17% 30 Year Yield 2.516 .004 0.16%

Prices taken at previous day market close.

Copyright 2016, Kinsale Trading LLC. All Rights Reserved. www.sevensreport.com

as further declines could support a further move higher

in prices while a reversal back above 8M barrels a day

would have an equal and opposite effect.

Outside the data, Saudi Oil Minister Khalid al-Falih con-

tinued to jawbone support for the recent speculative

rally, as he said he believes that markets have seen the

worst of the price plunge of recent years and that funda-

mentals were improving as supply and demand were

rebalancing. And while the renewed decline in US pro-

duction is mildly supportive of prices, the fact that the

rest of the world is pumping at full throttle and the only

policy to prevent global producers from producing more

in the coming months is an “understanding to agree”

that came from last month’s meeting in Algiers.

Bottom line, oil is still solidly trending higher and anyone

who knows technical analysis will tell you not to fight the

trend. And while the sizeable supply draws of recent;

declining imports, and slipping output in the US all seem

supportive, the long-term outlook for oil is not overly

bullish considering there is still no firm policy in place to

control global production. Moreover, output is hovering

at or near record highs outside of the US, and at some

point high enough prices will bring US producers back

into the market as they tap into their DUC (drilled but

uncompleted) wells. Unless OPEC actually agrees, that

means more supply out of the US, and that would be a

bearish development as it would delay rebalancing the

supply/demand imbalance.

Bottom Line

The several notable developments in the commodities

market of recent; rallying oil prices, signs of weakness in

the copper market, and a bullish uptrend developing in

gold are collectively not very optimistic signals for the

global economy or risk assets in general. Oil potentially

breaking back towards $60/barrel will have an inflation-

ary impact while copper breaking down flashes a warn-

ing sign of global recession.

And while there are a ton of takeaways for other asset

classes, those two developments are both supportive of

the rally in gold over the medium term, as they support

the argument that inflation will likely outpace a rise in

interest rates.

Currencies & Bonds

It was another quiet day in the currency and bond mar-

kets as there was no market-moving economic data and

everyone was looking ahead to the ECB meeting this

morning. The Dollar Index was basically unchanged.

The only real mover in the currency markets yesterday

was the Aussie, which rallied 0.70% on the in-line Chi-

nese economic data, which caused further short cover-

ing. But while the rally was decent and the Aussie is back

up towards the upper end of the mid-to-high .70s trad-

ing range, the bottom line is that the near-term direction

policy for the Reserve Bank of Australia is lower, and we

may see that in November if the September inflation

reading, released in a few weeks, misses expectations.

I’d rather be a seller of Aussie with a stop at the recent

high (.7818) than a buyer.

Elsewhere in currencies it was quiet. As mentioned, the

Dollar Index was flat as there wasn’t any important Fed

speak, and Housing Starts didn’t move markets. The eu-

ro also was flat, as expected, ahead of the ECB. Looking

at the euro, watch 1.0976 and 1.0947. Those are the two

recent low ticks, and if they are broken on Draghi being

surprisingly dovish then we could see an acceleration

lower in the euro (which will push the Dollar Index

through 98, and that could be a headwind on stocks).

The pound, yen and loonie were all little changed (there

was a Bank of Canada rate announcement, but no

change was made, as expected).

Turning to bonds, the 30-year Treasury closed yesterday

unchanged and the 10-year yield didn’t even move one

basis point, as global bond markets were on hold ahead

of the ECB meeting today. The 10-year yield remains

comfortably in the middle of the 1.70% - 1.80% trading

range, and unless we get a dovish or hawkish shock from

the ECB, things will stay that way near term.

Have a good day,

Tom

Copyright 2016, Kinsale Trading LLC. All Rights Reserved. www.sevensreport.com

Technical Perspectives

(Updated 10/16/16)

S&P 500

Technical View: The S&P 500 is currently range bound and has been since mid-July.

Dow Theory: Remains bearish (since week of August 17, 2015) but Dow Transports

are threatening to break out to a new high. Watch for a weekly close above 8086.

Key Resistance Levels: 2150, 2164, 2186

Key Support Levels: 2120, 2102, 2070

WTI Crude Oil

Technical View: WTI crude oil futures are in a well-defined uptrend dating back to

the mid-February lows.

Proprietary Model: Bullish (since week of September 26, 2016)

Key Resistance Levels: $50.86, $51.45, $52.85

Key Support Levels: $49.57, $47.30, $46.10

Gold

Technical View: Gold is currently pulling back in an otherwise upward trending mar-

ket; however, support in the mid-$1200s is critical to the health of the uptrend.

Proprietary Model: Bullish (since week of April 4, 2016)

Key Resistance Levels: $1270, $1311, $1341

Key Support Levels: $1250, $1246, $1217.50

30-Year T-Bond Futures

Technical View: Long-bond futures have been trending lower since hitting all-time

highs in the wake of the surprise Brexit decision.

Proprietary Model: Bearish (since week of August 15, 2016)

Key Resistance Levels: 165’07 166’12, 168’09

Key Support Levels: 162’28, 161’07, 160’04

Dollar Index Futures

Technical View: The Dollar Index recently broke out through longstanding, down-

trend resistance and is now in a near-term uptrend.

Proprietary Model: Bullish (since week of October 10, 2016)

Key Resistance Levels: 98.215, 98.635, 99.335

Key Support Levels: 97.50, 96.50, 96.01

Copyright 2016, Kinsale Trading LLC. All Rights Reserved. www.sevensreport.com

Disclaimer: The 7:00’s Report is protected by federal and international copyright laws. Kinsale Trading, LLC is the publisher of the newsletter and owner of all

rights therein, and retains property rights to the newsletter. The Newsletter may not be forwarded, copied, downloaded, stored in a retrieval system or oth-

erwise reproduced or used in any form or by any means without express written permission from Kinsale Trading LLC. The information contained in the

7:00’s Report is not necessarily complete and its accuracy is not guaranteed. Neither the information contained in The 7:00’s Report or any opinion expressed

in The 7:00’s Report constitutes a solicitation for the purchase of any future or security referred to in the Newsletter. The Newsletter is strictly an informa-

tional publication and does not provide individual, customized investment or trading advice to its subscribers. SUBSCRIBERS SHOULD VERIFY ALL CLAIMS

AND COMPLETE THEIR OWN RESEARCH AND CONSULT A REGISTERED FINANCIAL PROFESSIONAL BEFORE INVESTING IN ANY INVESTMENTS MENTIONED IN

THE PUBLICATION. INVESTING IN SECURITIES, OPTIONS AND FUTURES IS SPECULATIVE AND CARRIES A HIGH DEGREE OF RISK, AND SUBSCRIBERS MAY LOSE

MONEY TRADING AND INVESTING IN SUCH INVESTMENTS.

Fundamental Market View (Updated 10/16/16)

Near-Term General US Stock Market Outlook

This is designed to provide a snapshot of our near-term (1 month) outlook for stocks. For general equity market ex-posure, we use a mix of SPHB (S&P 500 High Beta) and SPLV (S&P 500 Low Volatility) to create an aggressive, neu-

tral or defensive stance on general equity market exposure.

Near Term Stock Market

Outlook:

Defensive SPHB: 25% SPLV: 75%

Stocks dropped 1% last week as soft Chinese economic data combined with a

strong US dollar to pressure markets. Going forward, higher bond yields and a

higher dollar will continue to create a headwind on stocks, and we remain cautious

on markets broadly given a lack of any real, positive near-term catalysts.

Tactical Allocation Ideas:

What’s Outperforming: Defensive Sectors (XLU/XLP, FXG), Short Duration TIPS ETF (VTIP), Super Cap Internet/Social Media Stocks (AMZN, FB, GOOGL, LNKD, FDN is a good internet ETF). Top Contrarian Idea (if you are a bull: Banks KRE).

What’s Underperforming: Europe (HEDJ/VGK), Retail (XRT), Tech (AAPL related supply chain), Healthcare (especially special-ty pharma and biotech stocks), Small Caps.

Long Term Fundamental Outlook for Other Asset Classes

Fundamental

Outlook Market Intelligence

Commodities Neutral

Commodities continued to rally last week, driven higher by energy. Notably, commodities rallied de-

spite the stronger US dollar, although if the dollar continues to surge towards par that will become a

headwind. Bigger picture, in the near term, worries about supply are helping push energy commodi-

ties higher. Longer term, the supply/demand outlook is not particularly favorable. Gold, meanwhile,

sits near multi-month lows; however, inflation is firm and that will support gold prices.

US Dollar Neutral

The Dollar Index rose to an eight-month high last week as markets continue to price in the reality of

marginally more hawkish policy from the Fed. The dollar rally came despite any real dollar positive

events or catalysts, and instead is just markets acknowledging the massive (and widening) gulf be-

tween incremental Fed policy (tighter) and other central banks (stable to easier).

Treasuries Bearish

Treasury yields were little changed last week, but that’s notable in so much as Treasuries didn’t rise/

yields fall despite the drop in stocks. That again reinforces our opinion that the near-term trend for

bonds is lower. Rising yields are a steady and growing headwind on stocks, and if the 10-year yield

moves through 1.80% and towards 2.00% that will begin to pressure equities.

This page is meant to provide a general outlook for the path of each major asset class and is updated at the start of each week.

Recommended