New York State Tax Update

Mark S. Klein, Esq.Hodgson Russ LLP

140 Pearl StreetBuffalo, New York 14202

[email protected]: (716) 848-1411

Fax: (716) 819-4624

Copyright © 2016

2016-17 BUDGET BILL

Income tax rates reduced (ish)

NY charitable giving won’t affect domicile

Business credits extended

E-filing mandate continues

2

CORPORATE TAX REFORM

$1,000,000 NY sales threshold

Market-based sourcing

Exempt investment income limited to stocks held over one year

8% limitation on investment income exemption

Special rules for pre-2015 NOLs

Mandatory combined reporting (50% ownership test)

Special NYC rules

3

ESTATE TAX CHANGES

Rates Exclusion phase-out Gift “tax” GST gone No portability New calculation for nonresidents Trust changes

4

WHAT DIDN’T PASS

Expand sales tax collection requirements to marketplace vendors

Disregard SMLLCs for sales tax purchases Disallow related party leases Eliminate the sales tax exemption for contributions of

property to new ventures Reduce the tax liability threshold to $5,000 to suspend

a taxpayer’s driver’s license Like-kind exchanges under IRC § 1031 – still the best

loophole in New York! Limited sales tax liability for LLC owners

5

COMPLIANCE AND ENFORCEMENT

Whistleblowers

New compliance measures

New reporting obligations

New York wants a “CISS”

Increased criminal investigations

CARP

6

“FISH IN A BARREL”

Hot Buttons for 2016-17• Corp v. sales tax revenue• Art Gallery sales and use• NYC residents with Sch. C income (BOD members, too!)• “No” Box• Visiting executives• Cash/credit ratio seems off• Used automobile registration • Facebook

Return preparer penalties - $1K/return – no reasonable belief$5K/return – reckless disregard

Voluntary Disclosure

Offers in compromise

7

PERSONAL INCOME TAX TAKE-AWAYS

Move out of NYC before the closing.

Avoid permanent place of abode (PPA) rules with brokerage agreement.

Does statutory residence trump domicile?

Keep an eye on Wynne

8

RESIDENCY

Why do we care?

• Income tax• 17 states still impose an estate or inheritance tax

Domicile or by statute

“Leave and Land”

When did you “move” or “change” your domicile?

Explain the “change”

Who proves what?

9

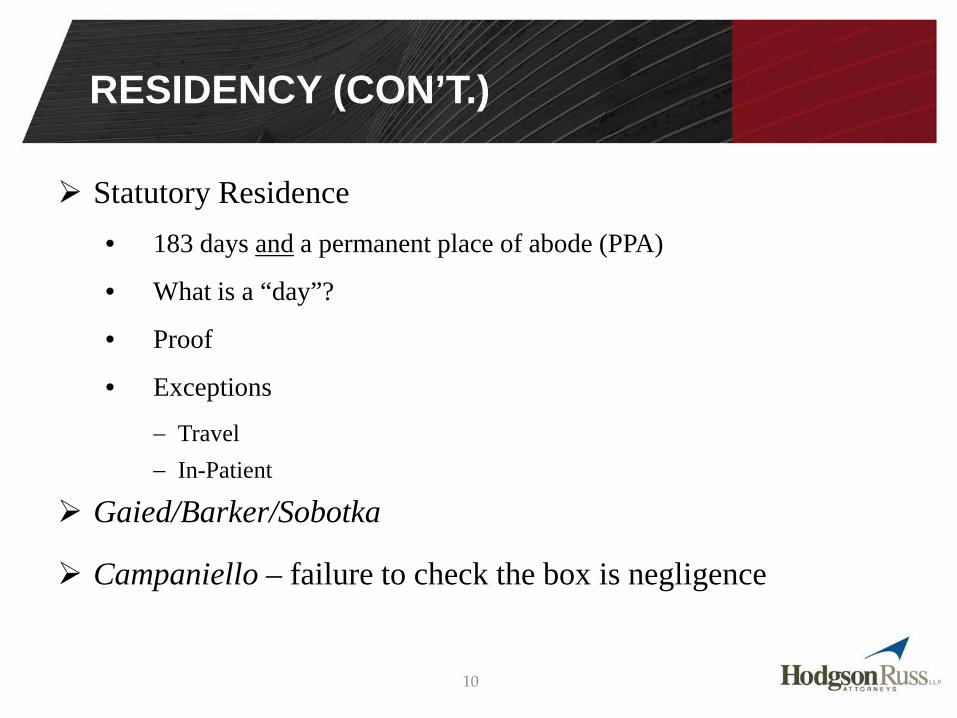

RESIDENCY (CON’T.)

Statutory Residence• 183 days and a permanent place of abode (PPA)

• What is a “day”?

• Proof

• Exceptions

− Travel− In-Patient

Gaied/Barker/Sobotka

Campaniello – failure to check the box is negligence

10

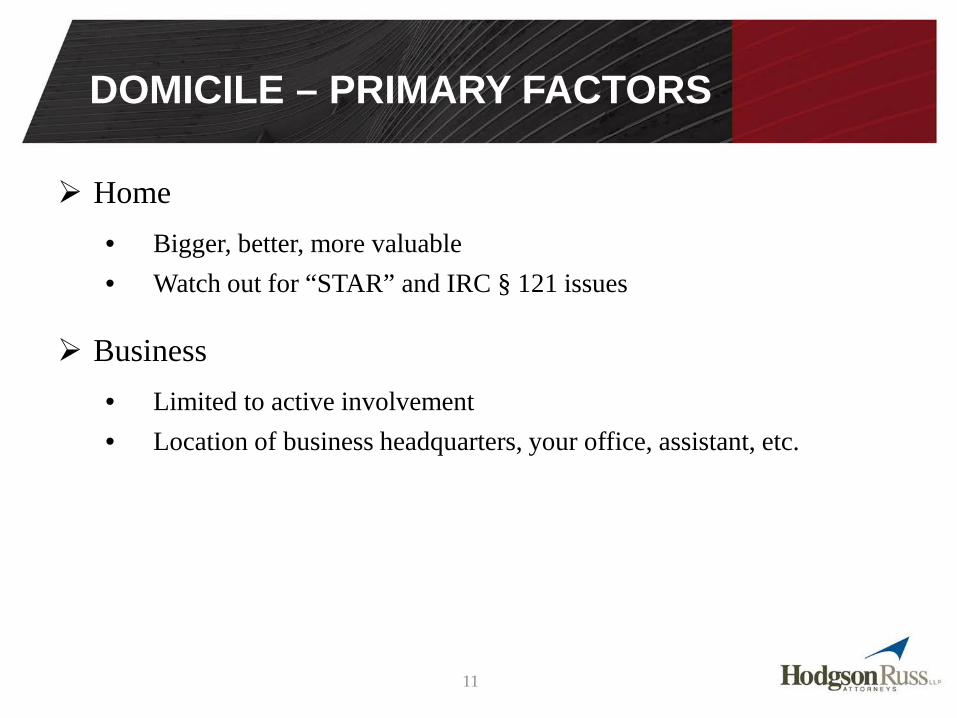

DOMICILE – PRIMARY FACTORS

Home• Bigger, better, more valuable• Watch out for “STAR” and IRC § 121 issues

Business• Limited to active involvement• Location of business headquarters, your office, assistant, etc.

11

DOMICILE – PRIMARY FACTORS (CON’T.)

Time

• Not 183-day rule!• Domicile day count

Near and Dear

• Where is your teddy bear,• Safe deposit box,• And insured and other “valuables”?• Moving vans v. storage

12

DOMICILE

Family Factor• Most spouses share their domicile• Minor children can be critical

Other Factors• Checklist items – nice but not determinative• Parking tax exemption

548- and 30-day rules

13

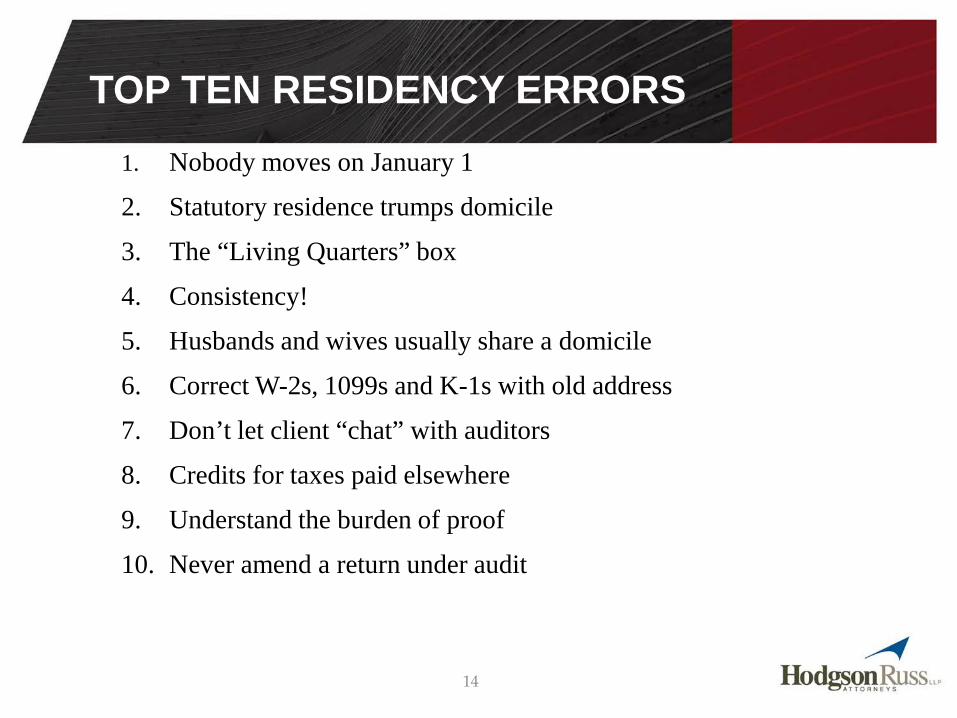

TOP TEN RESIDENCY ERRORS1. Nobody moves on January 1

2. Statutory residence trumps domicile

3. The “Living Quarters” box

4. Consistency!

5. Husbands and wives usually share a domicile

6. Correct W-2s, 1099s and K-1s with old address

7. Don’t let client “chat” with auditors

8. Credits for taxes paid elsewhere

9. Understand the burden of proof

10. Never amend a return under audit

14

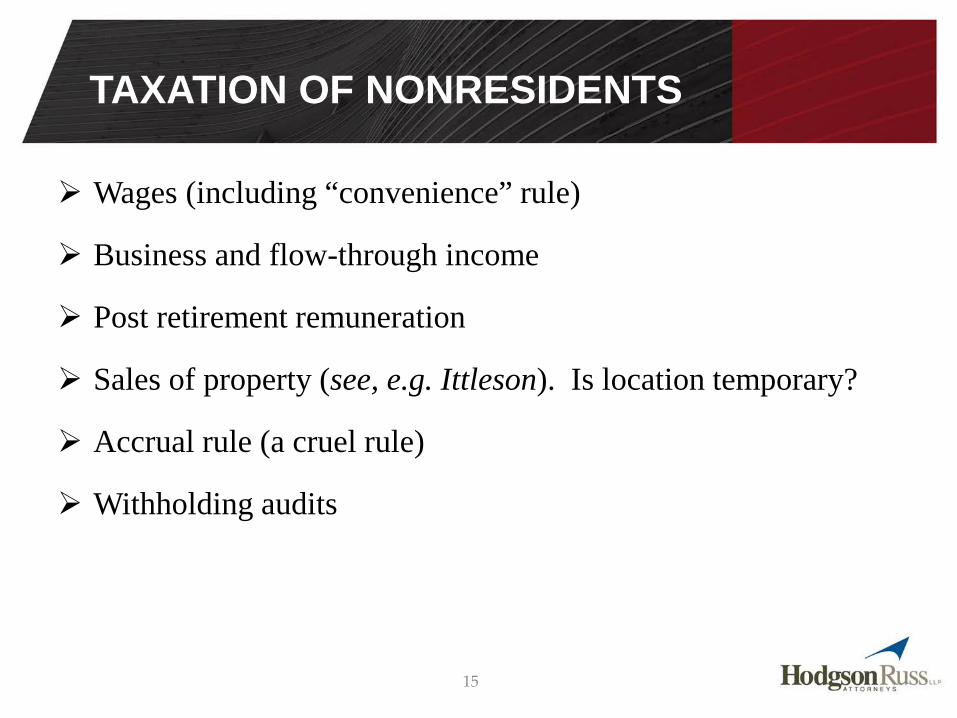

TAXATION OF NONRESIDENTS

Wages (including “convenience” rule)

Business and flow-through income

Post retirement remuneration

Sales of property (see, e.g. Ittleson). Is location temporary?

Accrual rule (a cruel rule)

Withholding audits

15

NUTS AND BOLTS OF A SALES TAX AUDIT

Expenses – recurring test or stat sample

Sales – guest checks - test?

• Reconcile to corporate return and bank deposits

Capital – usually in detail

• Reconcile to depreciation schedule

16

AUDIT QUESTIONS

Where to hold audit

Responsible officer questionnaire (special statute of limitations)

Access to information

Consent to extend

Statute of Limitations

Consent to test period

Penalties

Exemption certificate issues

FOIL!!

17

TOP TEN SALES TAX AUDIT ISSUES

1. Cloud computing

• Is it a license of software?• Is it a an information service? – RetailData and

Wegmans• Is it the electronic delivery of other tangible property?• Remember allocation and overlapping audit rules.

2. Cheeseboard consultants

3. Catering rules

4. Bulk sales rules (derivative liability)

18

5. Contractors

6. Sales to residents – use tax

7. Substitute of assets in a Trust

8. Art Galleries

9. Cash businesses

10. Boats

TOP TEN SALES TAX AUDIT ISSUES (CON’T.)

19

ADMINISTRATIVE UPDATE

BCMS

• 7,000 cases

• 75% agreement

• 67% resolved within six months

• 88% consent rate

ALJ

• 11-month backlog TAT

Article 78

20

THANK YOU

Mark S. Klein, Esq.Hodgson Russ LLP

140 Pearl StreetBuffalo, New York 14202

Phone: (716) 848-1411Fax: (716) 819-4624

Recommended