Three YearAnnual Performance Plan

2016/17-2018/19

AbbreviationsAA - Accounting Authority

ADR - Alternative Dispute Resolution

CCMR - Consumer Credit Market Report

CEO - Chief Executive O�cer

CFO - Chief Financial O�cer

COTII - Council of Trade and Industry Institutions

DCEO - Deputy Chief Executive O�cer

dti - Department of Trade & Industry

DPSA - Department of Public Service Administration

EXCO - Executive Committee

FIN - Finance

HR - Human Resources

ICT - Information Communication Technology

MICT SETA - Media Information and Communication Technologies Sector Education

and Training Authority

NCA - National Credit Act

NCAA - National Credit Amendment Act

NCR - National Credit Regulator

NCT - National Consumer Tribunal

PDA - Payment Distribution Agents

NDP - National Development Plan

PFMA - Public Finance Management Act

SADC - Southern African Development Community

SCM - Supply Chain Management

SDIP - Service Delivery Improvement Plan

SLA - Service Level Agreement

W&RSETA - Wholesale and Retail Sector Education and Training Authority

De�nitions used to measure performanceE�ective - Successful in producing a desired or intended result

Enhance - Improve the quality of performance

Support - To give assistance

Facilitate - To make an action or process easier

Table of Contents1. NCR Organisational structure 3

2. O�cial sign-o� 4

3. Foreword by the Minister 5

4. Overview by the Accounting Authority 6

PART A: Strategic Overview 9

5. Vision 9

6. Mission 9

7. Values 9

8. Legislative and other Mandates including Constitutional Mandates 9

9. Strategic Outcome Oriented Goals 10

10. Strategic objectives 10

11. The dti key strategic focus areas 10

12. Recent Court Rulings 10

13. Situational analysis 12

State of the Credit Market 12

13.1 Performance Delivery Environment (external) 12

a) Uncertainty in the regulatory framework 12

b) Increasing complexity and sophistication 12

c) Stakeholder management 12

d) Challenges faced by the NCR 13

13.2 Organisational Delivery Environment (internal) 13

a) Processes, system and structure renewal 13

b) Human Capital 13

c) Knowledge intensity 13

13. 3 Strategic Alignment to the dti 13

14. Description of the Planning Process 14

15. Financial Plan 15

(i) Projections of revenue, expenditure and borrowings 15

(ii) Asset and Liability Management 15

(iii) Cash �ow projections 16

1

(iv) Capital expenditure projects 16

(v) Infrastructure plans 16

(vi) Dividend policies 16

PART B: Programme Performance 17

16. Programme 1: 17

17. Programme 2: 20

18. Programme 3: 23

19. Programme 4: 27

20. Programme 5: 29

PART C: Links to other plans 34

21. Asset Management Plan 34

22. Information Technology Plan 34

23. Risk Management and Fraud Prevention Plan 34

23.1 Risk Management Process 34

23.2 Risk Strategy (Risk Register) 36

24. Any subsidiary of statutory body reporting to the entity 38

25. Service delivery improvement Plan 38

Annexure: Indicator Pro�les 39

2

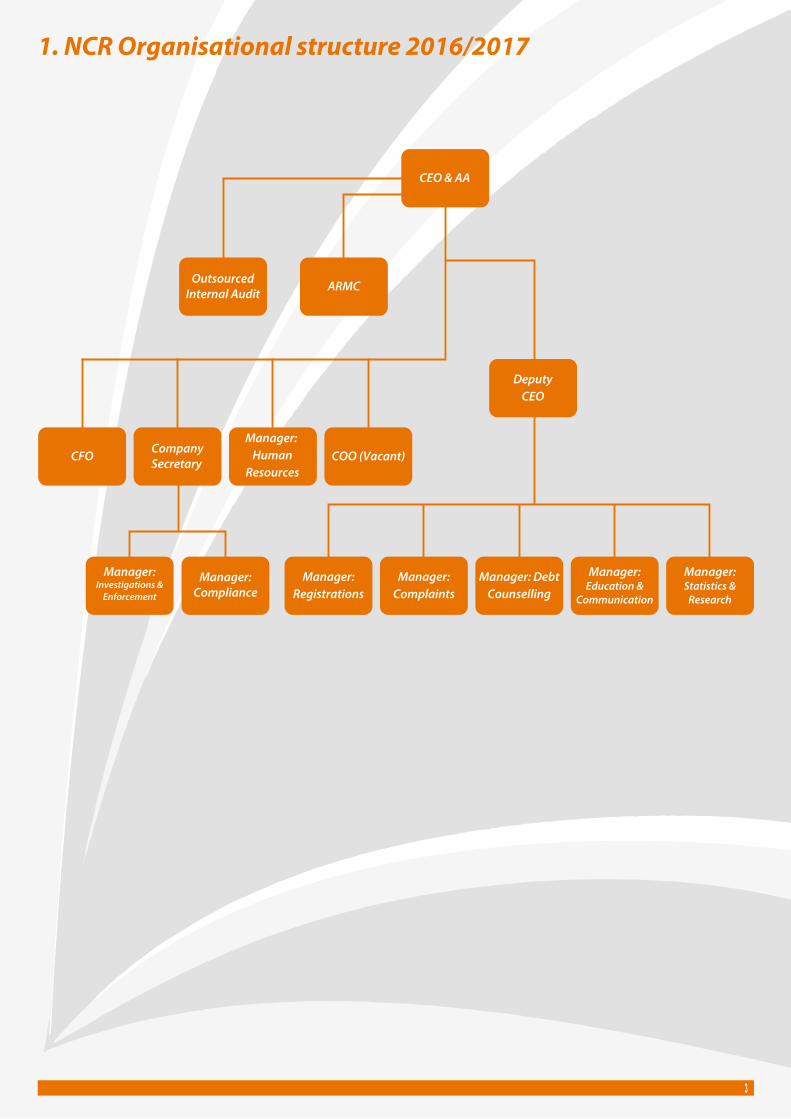

1. NCR Organisational structure 2016/2017

Manager:Compliance

Manager:Investigations &

Enforcement

Manager:Registrations

Manager:Complaints

Manager: DebtCounselling

Manager:Education &

Communication

Manager:Statistics &

Research

CEO & AA

ARMC

DeputyCEO

CompanySecretaryCFO

Manager: Human

ResourcesCOO (Vacant)

3

OutsourcedInternal Audit

4

2. O�cial sign-o�It is hereby certi�ed that this Annual Performance Plan:

Was developed by the management of the National Credit Regulator under the guidance of Ms Motshegare, who is the CEO and

Accounting Authority.

Takes into account all relevant policies, legislation and other mandates for which the National Credit Regulator is responsible.

Accurately re�ects the strategic outcome oriented goals and objectives which the National Credit Regulator will endeavour to

achieve over the period 2016/2017 – 2018/2019.

Signature:

Ms. Ayanda Mafuleka

Chief Financial O�cer

Signature:

Mr. Obed Tongoane

Deputy Chief Executive O�cer

Recommended for approval by

Signature:

Ms. Nomsa Motshegare

Chief Executive O�cer and Accounting Authority

5

3. Foreword by the MinisterThe National Credit Regulator (NCR) is established in terms of the National Credit Act No 34 of 2005 (the Act). It commenced operations in 2006. The Act was amended in 2014 (Act No.19 of 2014) and the Regulations pertaining to the Act as amended became e�ective in March 2015, except for the A�ordability Assessment Regulations which became enforceable in September 2015.

As a result of the above Regulations, the NCR is expected to focus on a number of key policy areas. These include monitoring compliance with: registration by new entrants, that is, small credit providers, payment distribution agents and alternative dispute resolution agents; Regulations relating to the collection and sale of prescribed debt; and the implementation of the A�ordability Assessment Regulations. In instances of contraventions, relevant enforcement action must be taken.

An additional key policy area the NCR must focus on, is to monitor the e�ect of the cost of credit and credit life insurance on consumers.

In the past year, the NCR embarked on various campaigns in an e�ort to raise consumer awareness and educate consumers in terms of their rights and obligations in terms of the Act as amended. This must continue, especially in predatory and deceptive advertisements where consumers are lured to take on credit with high interest rates. Consumers must also be made aware that they need to be honest in disclosing their �nancial obligations in full to credit providers for proper a�ordability assessments to be conducted.

The NCR’s achievements of its targets in the past years, and especially the last �nancial year are praiseworthy. In the 2014/15 �nancial year, the entity obtained an unquali�ed audit opinion with no matters of emphasis (clean audit).

For the three quarters up to 31 December 2015, the NCR achieved about 85% of its targets. Promoting public awareness on consumer credit matters with the aim of reaching across a broad range of consumers with varying needs, especially the vulnerable sectors of our communities is high on NCR’s agenda. Outreach programmes in the form of “Imbizos” were conducted in rural areas in the Free State, KwaZulu-Natal and Limpopo Provinces. The target audience were pensioners and self-employed people. In their proactive investigations, the NCR has mounted pressure on retailers to root out undesirable credit practices by selling unemployment insurance to consumers and levying unlawful fees that add to the indebtedness of consumers (for example, club fees).

A number of these matters and others which relate to various contraventions of the Act have been referred to the National Consumer Tribunal.

I am optimistic about the positive role that the NCR will continue to play in e�ectively regulating the consumer credit industry and protecting consumers. NCR is well on course to improve its performance with appropriate strategies and e�ective implementation of the Act as amended.

I am therefore pleased to release the NCR’s 3-year Annual Performance Plan for 2016-2019 and the 5-year Strategic Plan for 2016-2021 which set out in detail how objectives will be met with the continued support of the dti.

Dr Rob Davies, MPMinister of Trade and Industry

6

4. Overview by the Accounting AuthorityAs we recognise the challenging current economic climate in

the country, the National Credit Regulator (NCR) has made

tremendous inroads in making a di�erence in the lives of

South African citizens, especially the vulnerable sector of

society by e�ectively regulating the consumer credit industry.

The priorities of the NCR are aligned with the Key Policy Areas

of the Department of Trade and Industry (dti). These focus

areas re�ect the NCR’s vision of promoting a South African

consumer credit market which is fair, transparent, accessible

and contributing to South Africa’s socio-economic

development.

The NCR operates under the ambit of the National Credit Act

No 34 of 2005 (the Act). The Act was amended in 2014 (Act No.

19 of 2014) and most of the Regulations pertaining to the Act

as amended became e�ective in March 2015, with the

exception of the A�ordability Assessment Regulations which

came into force in September 2015.

A high level situational analysis conducted identi�ed trends in

the developments that are likely to in�uence the consumer

credit industry and impact the NCR over a period of time. The

factors impacting on the regulatory environment include the

following:

The state of the credit market: - The following were some of the

most signi�cant trends in terms of credit granted for the

quarter ended September 2015: the value of new mortgage

loans granted increased by R2.50 billion (6.77%) year-on-year;

secured credit, which is dominated by vehicle �nance,

increased by R2.80 billion (7.68%) year-on-year; and unsecured

credit increased by R2.42 billion (13.28%) year-on year.

The total outstanding consumer credit balances (gross

debtor’s book) as at September 2015 was R1.63 trillion, an

increase of 4.09% year-on-year.

About 23.45 million credit-active consumers were recorded on

the credit bureau records for the quarter ended September

2015. This is an increase of 4.2% when compared to the 22.50

million in September 2014. Consumers classi�ed in good

standing increased by 1.08 million year-on-year, to 13.53

million consumers in September 2015. As a percentage of the

total number of credit-active consumers at 57.7%, this re�ects

an increase of 2.4% year-on-year.

The number of consumers with impaired records has

decreased by 138 000 year-on-year, from 10.05 million in

September 2014, to 9.91 million in September 2015. The

number of accounts increased from 81.18 million in

September 2014 to 80.60 million for the quarter ended

September 2015. The number of impaired accounts decreased

from 21.64 million to 20.24 million when compared to

September 2014, a decrease of 1.40 million year-on-year.

Stakeholder management-: the NCR established a Credit

Industry Forum to address challenges relating to the

implementation of the Act. The forum meets quarterly and is

chaired by the NCR. Representation on the forum includes the

Banking Association of South Africa, the Micro Finance South

Africa, Debt Counselling Associations, Payment Distribution

Association of South Africa, Credit Bureau Association and

Consumer representatives. Regular meetings are also held

with large credit providers individually to discuss regulatory

issues.

The NCR also engages on a regular basis with other local

regulators such as the South African Reserve Bank and the

Financial Services Board to cooperate on regulatory matters

and to share information in respect of investigations relating to

entities that are regulated by these regulators.

The NCR participates in quarterly regulatory cluster meetings

of the Council of Trade and Industry Institutions (COTII) which

facilitate sharing of information and pulling resources to work

together as regulators. These meetings are chaired by the dti.

The members of the COTII are regulators and consumer

tribunals that report to the dti.

We continue to host regulators from the Southern African

Development Community (SADC) region to share information

on the work of the NCR. The countries from the region that

have visited the NCR to date include Swaziland, Namibia,

Botswana, Uganda and Tanzania.

Consumer Education:- In terms of consumer education and

communication, the main activities that stand out include the

involvement of the NCR in a project initiated by the

Department of Public Service and Administration (DPSA) to

develop and implement a debt relief programme to relieve

government employees of high indebtedness levels. This

relationship is to be formalised in a form of a Memorandum of

Understanding.

The NCR also conducted the “Know your credit status”

campaigns jointly with credit bureaus at shopping centres,

7

o�ces of the dti and the South African Revenue Services.

The NCR working jointly with local Tribal Authorities in rural

areas of the Free State, Limpopo, and KwaZulu-Natal Provinces,

conducted outreach programmes (“Imbizos”) aimed at mainly

pensioners and self employed people to create awareness

relating to undesirable practices of credit providers, especially

retailers.

Investigations:- During its investigations, the NCR discovered

that some of the retailers sold retrenchment and occupational

disability covers to pensioners and consumers receiving

government social grants such as old age, disability, foster care

and child support grants; and charged most of these

consumers a club fee which is not permitted in terms of the

Act.

The sale of retrenchment and occupational disability covers to

pensioners and consumers receiving government social grants

is unreasonable and imposes an unreasonable cost to such

consumers because they cannot claim bene�ts under these

covers.

The NCR also found that in some instances consumers

receiving disability grants from the government on account of

their permanent disability were sold occupational disability

cover at a time when they were already certi�ed permanently

disabled.

Entities found to have engaged in the abovementioned

practices were referred to the National Consumer Tribunal

(NCT) for appropriate sanctions.

Nineteen (19) matters involving credit providers (retailers,

banks, and other credit providers) were referred to the NCT

between April 2015 and September 2015. Contraventions

uncovered include over-charging of credit life insurance,

reckless lending, obtaining judgments in incorrect

jurisdictions, overcharging of fees, misleading advertisements

and others.

The enforcement of the Act is one of the key functions of the

NCR. In carrying out enforcement, the NCR conducts reactive

and proactive investigations. Reactive investigations are

informed by complaints from consumers, trends identi�ed in

the media, referrals from other institutions and on-site

compliance visits while proactive investigations target speci�c

areas following extensive information gathering.

Clean Audit Opinion: - As a result of the prudent �nancial

management and corporate governance practiced, the NCR

obtained an unquali�ed Audit Opinion without matters of

emphasis (Clean Audit) for the �nancial year 2014/15. There

were no �ndings on compliance, supply chain management

and performance information.

We recognise the �nancial challenges encountered to

implement the planned strategic activities. To achieve the

long-term goals, we will need to harness the experience and

expertise accumulated over the years.

The NCR has continuously been focusing on measures to cut

operational costs to deal with funding challenges. For

example, some of the work that was outsourced has been

internalised by providing extensive training to sta�. At the

same time, measures to supplement income have also been

identi�ed. These include proposals to increase registration fees

which have been submitted to the dti. The fee regulations have

been published by the dti.

The NCR is committed to good governance practices. The

responsibilities of the Accounting Authority vest in the Chief

Executive O�cer. An Audit and Risk Management Committee

(ARMC) is constituted in terms of the PFMA and Treasury

Regulations. The Internal Audit function is outsourced and

reports to the ARMC. The ARMC meets at least four times a

year.

The actions of the NCR have been e�ective in dealing with the

challenges as we see them today, but more work needs to be

done and �exibility coupled with creativity is going to become

crucial. The organisation has been working smartly to achieve

most of the objectives it set out to meet. By the end of

September 2015, about 85% of the targets had been either

achieved or exceeded.

For the 2016/17 �nancial year and as a result of the

Amendments and Regulations, key policy areas that the NCR

would focus on are the following: Monitoring compliance with

registration requirements - registration by new entrants, that

is, small credit providers, payment distribution agents, and

alternative dispute resolution agents; Regulations relating to

the collection and sale of prescribed debt; and

Implementation of the A�ordability Assessment Regulations.

In instances of contraventions, relevant enforcement action

will be taken.

8

The NCR will also focus on monitoring the e�ect of the cost of

credit and credit life insurance on consumers.

We have aligned the key performance areas with the strategic

objectives and core themes of the dti. The vision and mission

are articulated through strategic goals. Measurable

performance indicators as well as an analysis of external and

internal factors that could a�ect the ability to achieve our goals

are indicated. Strategic risks, which we could be exposed to, as

well as possible mitigating controls, are also identi�ed. The

strategic thrusts driving the plan include: - To promote

responsible credit granting, To protect consumers from abuse

and unfair practices in the consumer credit market and

address over indebtedness; To enhance the quality and

accuracy of credit bureau information; To monitor and improve

NCR’s operational e�ectiveness; and ensure e�ective

implementation of the National Credit Act as amended.

I would like to warmly thank the NCR Executive Team,

Management and Personnel for their contribution in building a

sustainable consumer credit market and the development of

South Africa. The important lessons captured each year

prepare us to take on new challenges in the years to come. The

organisational performance ultimately depends on the

continued dedication and hard work of our employees, to

whom I personally express appreciation for their enthusiasm

while encouraging sustained service with integrity, dedication

and professionalism.

Furthermore, it is important to continue collaboration with our

key stakeholders, and in particular the dti, in spearheading

socio-economic development. As we proceed on this journey,

the unwavering and continued support of the Honourable

Minister, the dti and Parliament will be of importance to assist

us to build on our strength through our ability to adapt and

respond quickly to changes and developing trends in the

consumer credit market.

The NCR will strive to improve its e�ectiveness in the

implementation of the Act and protection of consumers. I am

grateful to the Honourable Members of the Portfolio

Committee on Trade & Industry, Honourable Members of the

Select Committee on Trade and International Relations, the

Honourable Minister of Trade and Industry, Dr Rob Davies,

Director-General, Mr Lionel October, the Group Chief

Operations O�cer, Ms Jodi Scholtz, Deputy Director-General,

Ms Zodwa Ntuli and the Acting Deputy Director-General, Mr

MacDonald Netshitenzhe for their continued support and

guidance in terms of regulating the consumer credit industry.

I would also like to extend my sincere appreciation to the

Members of the Audit & Risk Management Committee for their

support and guidance.

Ms Nomsa Motshegare

Chief Executive O�cer and Accounting Authority

PART A: Strategic Overview

5. Vision

The vision of the NCR is:

To promote a South African consumer credit market that is fair, transparent, accessible and dynamic.

6. Mission

The mission of the NCR is:

To support the social and economic advancement of South Africa, by:– • regulating for a fair and non-discriminatory market for access to consumer credit; and • promoting responsible credit granting, use and effective redress.

7. Values

The values of the NCR are:

Service Excellence We strive for service excellence that exceeds the expectations of all stakeholders.

Integrity We are committed to honesty and integrity without compromise.

Empowerment We strive for empowerment in the consumer credit market and we are also committed to employee empowerment.

Good Corporate Governance We strive to be a model of good corporate governance at all times.

9

8. Legislative and other mandates including constitutional mandates

The legislative mandate of the NCR is as follows:

• To promote a fair and non-discriminatory marketplace for access to consumer credit and for that purpose to provide for the general regulation of consumer credit improved standards for consumer information; • To prohibit certain unfair credit and credit market practices; • To promote responsible credit granting and use and for that purpose to prohibit reckless credit granting; • To provide for debt re-organisation in cases of over-indebtedness; • To regulate credit information; and • To promote a consistent enforcement framework relating to consumer credit.

9. Strategic Outcome Orientated Goals

The NCR has six strategic outcome orientated goals. These are aligned to its �ve strategic objectives.

10. Strategic Objectives

The strategic objectives the NCR pursues are as follows:

1. To promote responsible credit granting. 2. To protect consumers from abuse and unfair practices in the consumer credit market and address over-indebtedness. 3. To enhance the quality and accuracy of credit bureau information. 4. To monitor and improve NCR’s operational e�ectiveness. 5. To ensure e�ective implementation of the National Credit Amendment Act (NCAA).

10

11. The dti key strategic focus areas

• To facilitate broad-based economic participation through targeted interventions to achieve more inclusive growth;• To create a fair regulatory environment that enables investment, trade and enterprise development in an equitable and socially responsible manner; and • To promote a professional, ethical, dynamic, competitive and customer-focused work environment that ensures e�ective and e�cient service delivery.

12. Recent Court Rulings

A brief summary of recent court cases and rulings are provided below:

Van Zyl vs NCR KwaZulu-Natal High Court: Case AR620/13.

Section 148

Bridge vs NCR North Gauteng High CourtCase No: 87768/14

Sections 55 and 57

The Applicant has applied to the High Court in order to declare sections 55 and 57 of the NCA unconstitutional. The NCR has �led its opposing papers. The matter was withdrawn.

Blue Chip vsCedric DeanRyneveldt

Supreme Court of AppealCase No: A233/14

Sections 129 and 130

The appeal was heard on 2 March 2015. The court had to rule on whether or not s129 is part of the cause of action. The High Court ruled in the a�rmitive. Blue Chip sought leave to appeal to the Supreme Court of Appeals. The set down date is being awaited.

The Appellant appealed against the decision by the Tribunal in terms of which he was �ned a R100 000 for his failure to conduct his debt counselling business in line with the provisions of the Act. The Appellant has since withdrawn the appeal resulting in the Tribunal order becoming e�ective. The Appellant has been requested to pay the �ne and NCR’s legal costs. The NCR needs to make a determination on whether it is viable to collect as the DC does not have assets.

Name Court & Case Noor Reference No

NCA Status

11

Name Court & Case Noor Reference No

NCA Status

M & S Funeralsvs NCR andothers

North Gauteng High CourtCase No: 83374/14

N/A The Applicant has applied to the High court to declare the search warrant that was used by the NCR to search and seize ID Books and cash that was kept by the Applicant in the course of its business as a credit provider as unlawful. The application was brought on an urgent basis and the High Court dismissed the application. The Applicant has since �led papers to bring the application on a normal basis. The matter was heard in the North Gauteng High Court on 26 October 2015 and the application was dismissed. The matter has been referred to the NCT for the de-registration of the registrant. The date of hearing is being awaited.

North Gauteng High CourtCase No: A440/14NCT Case No: NCT9152/2013/140(1)

NCR vs Capitec Section 90; Section 92(2) read with Regulation 29(1) and Form 20.1; Regulation 42(1)(b); Section 81(2)

The NCR has appealed to the High Court against the whole of the judgment and order of the NCT. The appeal will be heard in March 2016.

North Gauteng High CourtCase No: 75195/2015

De Noon vs NCR

N/A De Noon intends appealing the decision to cancel its registration as a credit provider. The NCR has �led an application to oppose the notice to appeal. The set down date is being awaited.

North Gauteng High Court Case No: 82869/2014

Bayport vs Minister of Justice and NCR

Section 90(2)(k)(vi)(bb)

Bayport brought an application to declare consent to foreign jurisdiction as legitimate. The NCR has �led its opposing papers. The case has been set down for 03 May 2016.

Western Cape High Court

NCR vs Bank on Assets

Section 90 NCR has made an application to declare the Bank on Asset’s business model unlawful. The set down date is being awaited. The entity is under liquidation.

Regional Court for Regional Division of Gauteng: Randburg

Koshava O�ce Solutions CC vs NCR

N/A Koshava (a service provider) is suing the NCR for outstanding rental fees and the return of leased equipment. The NCR opposes the matter which is being heard in February 2016.

North Gauteng High CourtCase No: 73338/15

Developmentn-omics vs NCR

N/A Developmentnomics (a service provider) is suing the NCR for non-payment of services allegedly rendered. The NCR has �led a notice of intention to defend and refuses to pay because Developmentnomics failed to deliver in terms of the SLA. The matter is at the pleading stage.

13. Situational Analysis

A high-level assessment was undertaken to identify the most signi�cant developments in the external and internal environment that are likely to in�uence or impact the NCR over the next several years. First, a brief synopsis of the state of the credit market is provided and thereafter, the analysis of the internal and external factors impacting on the NCR.

State of the Credit Market

The total value of credit granted for the twelve months ending September 2015 amounted to R461.42 billion compared to R441.64 billion for the same period in 2014. The value of the outstanding debtors’ book increased by R64.19 billion (4.09%) for the quarter ended September 2015, when compared to the quarter ended September 2014. The value of the debtors book at the end of September 2015 was R1.63 trillion consisting of 41.29 million accounts. For the quarter ended September 2015, the total Rand value of new credit granted was R123.93 billion, with mortgages comprising R39.39 billion (31.78%). Unsecured Credit increased by 13.28% from R18.23 billion for the quarter ended September 2014 to R20.66 billion for the quarter ended September 2015.

Applications for registration of credit providers have stabilised. A total of 4 885 credit providers with 49 941 branches, 14 Credit Bureaus and 2314 debt counsellors are now registered with the NCR.

As at September 2015, about 740 500 consumers applied to be under debt review and an estimated 408 976 cases remain under “active” debt review. The total PDA distributions to credit providers from April 2015 to December 2015 was R4.9 billion. These are funds collected by PDAs from consumers under debt review.

13.1 Performance Delivery Environment (external)

The following external developments were identi�ed as the key trends or issues that are likely to a�ect the work of the NCR:

a) Uncertainty in the regulatory framework

Regulatory uncertainty creates inconsistent application of the legislation resulting in undesirable outcomes that have a negative impact on the credit market. It also leads to interpretation problems which impede regulatory certainty.

Decisions of the courts and National Consumer Tribunal have also created uncertainty in the regulatory framework when interpreting the National Credit Act. Some of the decisions for example are inconsistent with the overall purpose of the legislation.

The NCR has worked closely with the dti to close the gaps that exist currently in the legislation through the National Credit Amendment Act No.19 of 2014 and its regulations such as, A�ordability Assessment, Credit Life Insurance and Interest Rate Caps.

In addition, the NCR is empowered to issue guidelines to the industry to provide guidance on the interpretation and application of the Act as amended.

b) Increasing complexity and sophistication

The evolution of the credit market has come with innovation by the industry. This has increased the levels of complexity and sophistication in the market.

The emergence of on-line and social lending in South Africa has brought new regulatory challenges for the NCR. As a regulator, the NCR must be adept to the new challenges to ensure consumer protection.

The NCR is also closely monitoring the introduction of the new credit products and the advertising methods of credit providers in order to curb the luring of consumers into debt traps. This in turn requires improved product knowledge and understanding by the NCR to be able to monitor their compliance with legislation e�ectively.

c) Stakeholder management

The approach of the NCR towards stakeholder management is to facilitate open discussion and engagement with the industry and other stakeholders. E�orts are being made to achieve this objective while avoiding regulatory capture by the industry.

The NCR has established the Credit Industry Forum which serves as a platform for the NCR and industry to engage and reach agreement on industry issues. The forum represents all industry players and consumers. It plays an important role in resolving operational problems on the implementation of the legislation.

12

13

The NCR is a member of the African Consumer Protection Dialogue which is facilitated by the Federal Trade Commission of the United States. This forum brings together regulators from all over the African continent to discuss consumer protection issues and share information. A formal structure for information sharing and collaboration is being explored in this forum.

The NCR also holds regular meetings with industry associations, registrants and magistrates. On-going meetings are also held with local and foreign investors as well as local �nancial institutions and other regulators including the Reserve Bank of South Africa.

The NCR has also established networks with other regulators in the SADC region, North America and the United Kingdom. More relationships will be established with other regulators across the globe.

d) Challenges faced by the NCR

The main challenge of the NCR is funding. The NCR requires additional funding for new premises to accommodate its growing sta� complement and increase sta� capacity. In addition, funding is required for compliance monitoring, consumer education, conducting workshops and enforcement.

The NCR continues to �nd creative ways to augment its budget in order to be able to execute its legislative mandate. These include, but not limited to, requesting the dti to issue regulations increasing registration fees.

13.2 Organisational Delivery Environment (internal)

The following internal developments were identi�ed as the key issues that are likely to a�ect the work of the NCR:

a) Processes, system and structure renewal

A new human resource management system and a performance management system have been introduced.

b) Human Capital

The NCR is focusing on sta� issues and ensures that sta� morale remains high.

There is a learneship programme in which �fteen (15) graduates were recruited and trained with the hope of providing additional capacity to the NCR. This is a joint project between the NCR, the WRSETA and MICSETA. The NCR has been running the learnership programme since 2011.

c) Knowledge intensity

The NCR is expected to provide guidance to stakeholders on the developments and trends in the credit market. This is achieved through measures such as issuing public notices, capacity building workshops, media statements, radio and TV interviews, outreach programmes (Imbizos) and others. In addition, the NCR also publishes statistics on a quarterly basis on the level and nature of consumer indebtedness.

13.3 Strategic Alignment to the dti

In addition to the external and internal environmental trends and issues, the need to ensure strategic alignment to priorities of government was taken into account in formulating the strategic priorities of the NCR. Government has committed itself to achieving twelve (12) outcomes.

The dti, as the NCR’s line ministry, plays a pivotal role in ensuring the achievement of Outcome 4 – Decent Employment through Inclusive Growth. A stable and e�cient �nancial sector, of which the consumer credit market is a critical component, is vital for ensuring inclusive growth and employment creation. Thus, the activities of the NCR are most closely associated with contributing to Outcome 4.

14

The alignment between the outcomes that the NCR seeks to achieve, and the strategic objectives of the dti, is set out below

The dti strategic objectives and NCR outcomes:

Facilitate broad-based economic participation through targeted interventions to achieve more inclusive growth:-

• To promote responsible credit granting.• To enhance the quality and accuracy of credit bureau information.

• Reduced levels of over-indebtedness.• Affordable levels of credit promoted.• Improved consumer credit information.

Create a fair regulatory environment that enables investment, trade and enterprise development in an equitable and socially responsible manner:-

• To protect consumers from abuse and unfair practices in the consumer credit market and address over-indebtedness.• To ensure effective implementation of the National Credit Amendment Act (NCAA).

• Decreased levels of reckless lending practices.• Improved compliance with regulations and consumer protection.• Improved and effective regulation.

Promote a professional, ethical, dynamic, competitive and customer-focused work environment that ensures e�ective and e�cient service delivery:-

• To monitor and improve NCR’s operational e�ectiveness.

E�cient service delivery.

14. Description of the Planning Process

The �rst stage begins with the Executive Committee initiating the planning process with the aim of creating the organisational strategic direction. Workshops are then held between executive members and the management team to develop the departmen-tal operational objectives. Management engages with their respective team members to develop operational objectives which are in line with the business plan of the organisation. Upon approval of the strategic and operational objectives, all employees including executive management conclude performance contracts with their respective team members.

dti Objectives NCR Objectives NCR Outcomes

15. Financial Plan

(ii) Asset and Liability Management

In terms of section 51(1)(c) of the PFMA, the Accounting Authority is responsible for the management, including the safeguarding, of the assets and the management of the revenue, expenditure and liabilities of the public entity. Within the NCR, the Asset Management Policy provides for the acquisition of assets when the need arises. Procurement processes are in line with legislative requirements as well as the NCR’s supply chain management policy. In addition, assets are e�ectively maintained and when required, disposed of in line with the requirements of the PFMA.

Financial planning and discipline are a key success factor for the NCR. With the limited �nancial resources, and the need to regulate the credit industry and enforce the NCA, it is imperative for the NCR to optimise the available funding.

This section provides an overview of the projected revenue, expenditure and cash �ow requirements over the three year period. In addition, the NCR’s assets and management strategy is provided, as well as the capital expenditure projections.

(i) Projections of revenue, expenditure, borrowings and capex

The following table provides a summary of the NCR’s projected �nancial plan for the three year period:

The NCR’s projected capital expenditure programme for the next three years focuses on the computer equipment and IT systems upgrade. The capex programme is outlined below:

Operational expenditure

Personnel costs

Administration costs

Professional/Programme costs

Total operational expenditure

Capital expenditure

Fixed assets

ICT operational system

Total capital expenditure

TOTAL EXPENDITURE

Income

Fees from registrants

Transfers from DTI

Interest

Other income

Additional Funding from DTI

TOTAL INCOME

78,988,539

18,745,941

23,545,823

121,280,303

3,903,303

2,000,000

5,903,303

127,183,606

55,106,606

69,577,000

1,500,000

1,000,000

-

127,183,606

82,924,000

18,521,113

23,752,198

125,197,310

4,020,402

1,500,000

5,520,402

130,717,712

55,161,712

73,056,000

1,500,000

1,000,000

-

130,717,712

87,070,200

18,876,746

24,437,404

130,384,350

4,141,014

1,500,000

5,641,014

136,025,364

56,816,564

76,708,800

1,500,000

1,000,000

-

136,025,364

Year 2016-2017 Year 2017-2018 Year 2018-2019

O�ce Equipment

Computer Equipment

Furniture

Software/licences

ICT operating system

Total

275,282

908,803

207,018

2,512,200

2,000,000

5,903,303

291,799

846,232

219,439

2,662,932

1,500,000

5,520,402

300,553

871,618

226,022

2,742,820

1,500,000

5,641,014

Year 2016-2017 Year 2017-2018 Year 2018-2019

15

275,282

908,803

207,018

2,512,200

2,000,000

5,903,303

291,799

846,232

219,439

2,662,932

1,500,000

5,520,402

300,553

871,618

226,022

2,742,820

1,500,000

5,641,014

Year 2016-2017 Year 2017-2018 Year 2018-2019

16

O�ce Equipment

Computer Equipment

Furniture

Software/licences

ICT operating system

Total

(iii) Cash �ow projections

Cash �ow from operating activities

Cash receipts from applicants and registered entities

Cash paid to suppliers

Cash paid to employees

Cash absorbed by operations before transfers received

Transfer received

Cash �ow absorbed by operations

Finance income

Net cash in�ows from operations activities

Cash �ows from investing activities

Additions to property, plan and equipment

New ICT system Developments, etc

Net cash out�ows from investing activities

Cash �ows from �nancing activities

Net cash in�ows from �nancing activities

Net decrease/increase in cash and cash equivalent

Year 2016-2017 Year 2017-2018 Year 2018-2019Budget

56,106,606

( 42,291,765 )

( 78,988,539 )

( 65,173,697 )

69,577,000

4,403,303

1,500,000

5,903,303

( 3,903,303 )

( 2,000,000 )

( 5,903,303 )

-

-

Budget

56,161,712

( 42,273,310 )

( 82,924,000 )

( 69,035,599 )

73,056,000

4,020,401

1,500,000

5,520,401

( 4,020,402 )

( 1,500,000 )

( 5,520,402 )

-

-

Budget

57,816,564

( 43,314,150 )

( 87,070,200)

( 72,567,786 )

76,708,800

4,141,014

1,500,000

5,641,014

( 4,141,014 )

( 1,500,000 )

( 5,641,014 )

-

-

(iv) Capital expenditure programmes

(v) Infrastructure Plans

The NCR does not have planned infrastructure projects and therefore does not have an infrastructure plan.

(vi) Dividend policies

The NCR is a schedule 3A public entity receiving a transfer payment from the dti. Hence the NCR does not declare dividends.

The NCR’s projected capital expenditure programme for the next three years focuses on the computer equipment and IT systems upgrade. The capex programme is outlined below:

17

Part

B: P

rogr

amm

e Pe

rfor

man

ce

16. P

rogr

amm

e 1:

To

prom

ote

resp

onsi

ble

cred

it g

rant

ing.

16

.1 P

urpo

se o

f the

pro

gram

me

Th

e pu

rpos

e of

this

pro

gram

me

is to

redu

ce le

vels

of c

onsu

mer

ove

r-in

debt

edne

ss b

y:

(

a) E

duca

ting

cred

it pr

ovid

ers

and

mon

itorin

g th

eir c

ompl

ianc

e w

ith th

e re

gula

tions

; and

(

b) E

nfor

cing

com

plia

nce

with

the

regu

latio

ns.

16

.2 D

escr

iptio

n of

the

prog

ram

me

Wor

ksho

ps a

nd c

ompl

ianc

e m

onito

ring

visi

ts w

ill b

e co

nduc

ted

in o

rder

to a

ssis

t cre

dit p

rovi

ders

to c

ompl

y w

ith a

�ord

abili

ty a

sses

smen

t reg

ulat

ions

and

cos

t of c

redi

t.

16

.3 P

erfo

rman

ce in

dica

tors

and

per

form

ance

targ

ets p

er p

rogr

amm

e.

Num

ber o

f

prov

ince

s vi

site

d to

mon

itor c

ompl

ianc

e

and

appr

opria

te

enfo

rcem

ent a

ctio

n

take

n w

here

nece

ssar

y.

App

rove

d

rese

arch

by

Boar

d.

Repo

rts o

n

Impl

emen

tatio

n

of re

com

men

datio

ns.

1 w

orks

hop

cond

ucte

d on

a�or

dabi

lity

asse

ssm

ent

regu

latio

ns.

*7 p

rovi

nces

visi

ted

to m

onito

r

cred

it pr

ovid

er

com

plia

nce

and

appr

opria

te

enfo

rcem

ent

actio

n ta

ken

on

non-

com

plia

nt

cred

it pr

ovid

ers

whe

re n

eces

sary

.

9 pr

ovin

ces

visi

ted

to m

onito

r cre

dit

prov

ider

com

plia

nce

and

appr

opria

te

enfo

rcem

ent

actio

n ta

ken

on

non-

com

plia

nt

cred

it pr

ovid

ers.

9 pr

ovin

ces

visi

ted

to

mon

itor c

redi

t

prov

ider

com

plia

nce

and

appr

opria

te

enfo

rcem

ent

actio

n ta

ken

on

non-

com

plia

nt

cred

it pr

ovid

ers

whe

re n

eces

sary

.

9 pr

ovin

ces

visi

ted

to

mon

itor c

redi

t

prov

ider

com

plia

nce

and

appr

opria

te

enfo

rcem

ent

actio

n ta

ken

on

non-

com

plia

nt

cred

it pr

ovid

ers

whe

re n

eces

sary

.

Redu

ced

leve

ls o

f

over

-inde

bted

ness

.

Goa

l/O

utco

me

Impr

ove

com

plia

nce

with

a�or

dabi

lity

asse

ssm

ent

regu

latio

ns.

Out

put

Perf

orm

ance

Indi

cato

r/m

easu

re

Aud

ited

Act

ual P

erfo

rman

ce

2013

/14

2014

/15

Esti

mat

edPe

rfor

man

ceM

ediu

m T

erm

Tar

gets

2015

/16

2016

/17

2017

/18

2018

/19

2012

/13

18

--

--

Goa

l/O

utco

me

Out

put

Perf

orm

ance

Indi

cato

r/m

easu

re

Aud

ited

Act

ual P

erfo

rman

ce

2012

/13

2013

/14

2014

/15

Esti

mat

edPe

rfor

man

ceM

ediu

m T

erm

Tar

gets

2015

/16

2016

/17

2017

/18

2018

/19

R25m

R17.

2mR5

.6m

R6.7

mR6

.8m

R7.5

m

*7

wor

ksho

ps

cond

ucte

d on

a�or

dabi

lity

asse

ssm

ent

regu

latio

ns

R6.5

mN

umbe

r of

inve

stig

atio

ns

cond

ucte

d to

enfo

rce

regu

latio

ns

and

appr

opria

te

enfo

rcem

ent a

ctio

n

take

n w

here

nece

ssar

y.

Num

ber o

f

Wor

ksho

ps

cond

ucte

d on

a�or

dabi

lity

asse

ssm

ent

regu

latio

ns a

nd

appr

opria

te

enfo

rcem

ent a

ctio

n

take

n w

here

nece

ssar

y

--

-

Dra

ft B

usin

ess

plan

app

rove

d by

Boar

d.

Fina

l fun

ctio

nal

spec

i�ca

tion

docu

men

t of t

he

NRC

A d

atab

ase

man

agem

ent

syst

em p

rodu

ced.

Esta

blis

hmen

t of

the

NCR

A s

teer

ing

com

mitt

ee.

-D

evel

op p

ropo

sal

on a

�ord

abili

ty

asse

ssm

ent

guid

elin

es.

---

--

-

Stud

y co

nduc

ted

to re

view

the

curr

ent l

evel

s of

the

cost

of c

redi

t

and

mak

e

reco

mm

enda

tions

to th

e dt

i.

R9.5

m

*15

inve

stig

atio

ns

cond

ucte

d an

d

appr

opria

te

enfo

rcem

ent

actio

n ta

ken

whe

re n

eces

sary

.

R10.

4m

Cond

uct 4

0

inve

stig

atio

ns a

nd

appr

opria

te

enfo

rcem

ent

actio

n ta

ken

whe

re n

eces

sary

.

R11m

Cond

uct 5

0

inve

stig

atio

ns a

nd

appr

opria

te

enfo

rcem

ent a

ctio

n

take

n w

here

nece

ssar

y.

Cond

uct a

revi

ew o

f

the

leve

ls o

f the

cost

of c

redi

t and

mak

e

reco

mm

enda

tions

to th

e dt

i.

R11.

2m

Cond

uct 6

0

inve

stig

atio

ns

and

appr

opria

te

enfo

rcem

ent

actio

n ta

ken

whe

re n

eces

sary

.

R11.

4m

A�o

rdab

le le

vels

of

cred

it pr

omot

ed.

Incr

ease

com

plia

nce

with

prov

isio

ns

pert

aini

ng to

the

tota

l cos

t of

cred

it.

*Bas

ed o

n th

e es

timat

ed a

nnua

l per

form

ance

targ

ets

for 2

015/

16 �

nanc

ial y

ear

*Bas

ed o

n th

e es

timat

ed a

nnua

l per

form

ance

targ

ets

for 2

015/

16 �

nanc

ial y

ear

16

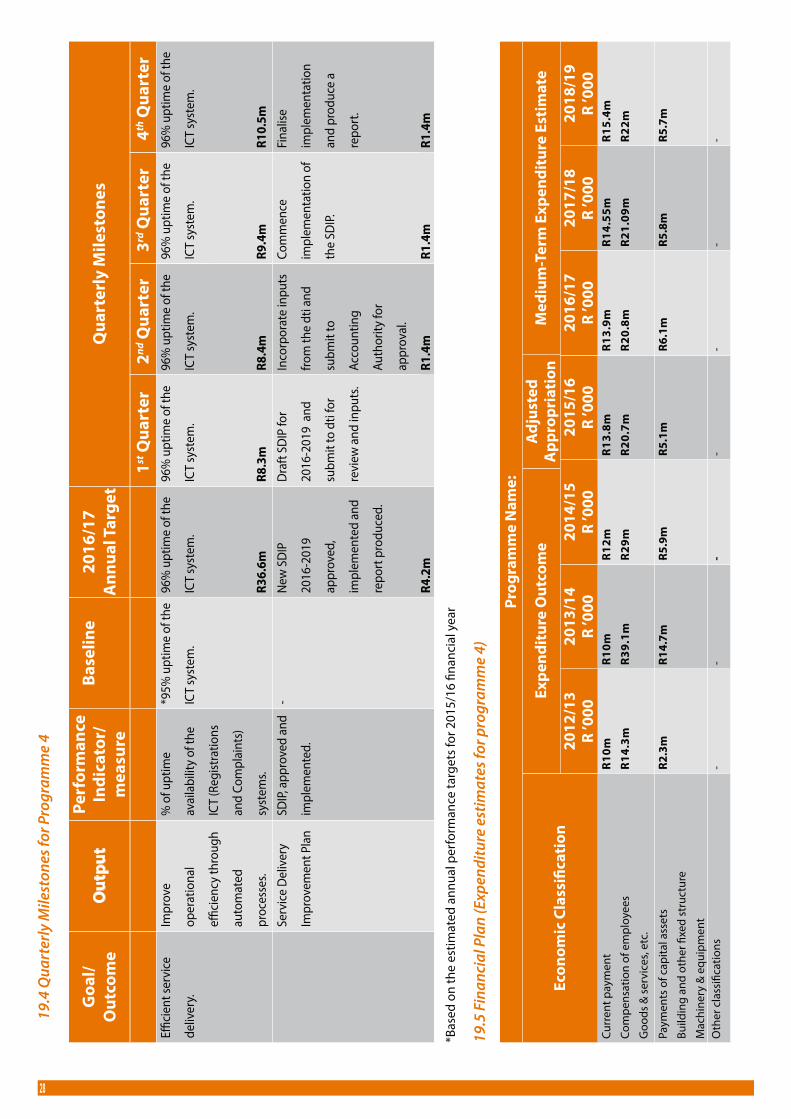

.4 Q

uart

erly

Mile

ston

es fo

r Pro

gram

me

1

Redu

ced

leve

ls of

over

-inde

bted

ness

.

Impr

ove

com

plia

nce

with

a�or

dabi

lity

asse

ssm

ent

regu

latio

ns.

Num

ber o

f

prov

ince

s visi

ted

to m

onito

r

com

plia

nce

and

appr

opria

te

enfo

rcem

ent

actio

n ta

ken

whe

re n

eces

sary

.

*7 p

rovi

nces

visit

ed to

mon

itor

cred

it pr

ovid

er

com

plia

nce

and

appr

opria

te

enfo

rcem

ent

actio

n ta

ken

on

non-

com

plia

nt

cred

it pr

ovid

ers.

9 pr

ovin

ces v

isite

d

to m

onito

r cre

dit

prov

ider

com

plia

nce

and

appr

opria

te

enfo

rcem

ent

actio

n ta

ken

on

non-

com

plia

nt

cred

it pr

ovid

ers.

R6.7

m

1 R0.8

m

3 R1.9

m

3 R2.5

m

2 R1.5

mA�

orda

ble

leve

ls

of c

redi

t

prom

oted

.

Incr

ease

com

plia

nce

with

regu

latio

ns

pert

aini

ng to

the

tota

l cos

t of c

redi

t.

Num

ber o

f

inve

stig

atio

ns

cond

ucte

d to

enfo

rce

regu

latio

ns a

nd

appr

opria

te

enfo

rcem

ent

actio

n ta

ken

*15

inve

stig

atio

ns

cond

ucte

d an

d

appr

opria

te

enfo

rcem

ent

actio

n ta

ken

whe

re n

eces

sary

.

Cond

uct 4

0

inve

stig

atio

ns a

nd

appr

opria

te

enfo

rcem

ent

actio

n ta

ken

whe

re n

eces

sary

.

R11m

8 R2.4

m

12 R3.1

m

12 R3.1

m

8 R2.4

m

Goa

l/O

utco

me

Out

put

Perf

orm

ance

Indi

cato

r/m

easu

re

Base

line

2016

/17

Ann

ual T

arge

tQ

uart

erly

Mile

ston

es

1st Q

uart

er2nd

Qua

rter

3rd Q

uart

er4th

Qua

rter

19

20

Curr

ent p

aym

ent

Com

pens

atio

n of

em

ploy

ees

Goo

ds &

ser

vice

s, et

c.

R11m

R8m

R12m

R6.6

m

R4m

R13m

R8.6

m

R8.3

m

R9m

R8.7

m

R9.1

m

R8.9

m

R9.6

m

R9.3

m

--

--

--

-Pa

ymen

ts o

f cap

ital a

sset

s

Build

ing

and

othe

r �xe

d st

ruct

ures

Mac

hine

ry a

nd e

quip

men

t

Oth

er c

lass

i�ca

tions

--

--

--

-

Econ

omic

Cla

ssi�

cati

on

Prog

ram

me

Nam

e:

2012

/13

R ’0

00

Expe

ndit

ure

Out

com

e

2013

/14

R ’0

0020

14/1

5R

’000

2015

/16

R ’0

00

Adj

uste

dA

ppro

pria

tion

2016

/17

R ’0

0020

17/1

8R

’000

2018

/19

R ’0

00

Med

ium

-Ter

m E

xpen

ditu

re E

stim

ate

16.5

Fin

anci

al P

lan

(Exp

endi

ture

est

imat

es fo

r pro

gram

me

1)

17. P

rogr

amm

e 2:

To

prot

ect c

onsu

mer

s fr

om a

buse

and

unf

air p

ract

ices

in th

e co

nsum

er c

redi

t mar

ket a

nd

a

ddre

ss o

ver-

inde

btne

ss.

17

.1 P

urpo

se o

f the

pro

gram

me

Th

e pu

rpos

e of

this

pro

gram

me

is to

dec

reas

e th

e pr

actic

e of

reck

less

lend

ing

by c

redi

t pro

vide

rs. T

his

will

be

impl

emen

ted

by c

ondu

ctin

g in

vest

igat

ions

and

taki

ng e

nfor

cem

ent

a

ctio

n on

non

-com

plia

nt c

redi

t pro

vide

rs.

17

.2 D

escr

iptio

n of

the

prog

ram

me

In

vest

igat

ions

will

be

cond

ucte

d pr

oact

ivel

y by

the

NCR

. Com

plai

nts

repo

rts

that

are

lodg

ed b

y co

nsum

ers

and

repo

rts

of n

on-c

ompl

ianc

e re

port

ed b

y Ac

coun

ting

O�

cers

and

au

dito

rs w

ill b

e in

vest

igat

ed th

roug

h re

activ

e m

echa

nism

s. A

ppro

pria

te e

nfor

cem

ent a

ctio

n w

ill b

e ta

ken

whe

re n

eces

sary

.

Num

ber o

f cre

dit

prov

ider

s

inve

stig

ated

and

appr

opria

te

enfo

rcem

ent a

ctio

n

take

n w

here

nece

ssar

y.

- R30m

- R39.

2m

15 c

ompl

ianc

e

notic

es/

com

plia

nce

cert

i�ca

tes

whe

re n

eces

sary

.

R35m

*40

cred

it

prov

ider

s

inve

stig

ated

and

appr

opria

te

enfo

rcem

ent

actio

n w

here

nece

ssar

y.

R28.

3m

60 c

redi

t

prov

ider

s

inve

stig

ated

and

appr

opria

te

enfo

rcem

ent

actio

n w

here

nece

ssar

y.

28.5

m

70 c

redi

t

prov

ider

s

inve

stig

ated

and

appr

opria

te

enfo

rcem

ent

actio

n w

here

nece

ssar

y.

29.2

m

80 c

redi

t

prov

ider

s

inve

stig

ated

and

appr

opria

te

enfo

rcem

ent

actio

n w

here

nece

ssar

y.

30.1

m

Dec

reas

ed le

vels

of

reck

less

lend

ing

prac

tices

.

Goa

l/O

utco

me

Cond

uct r

eckl

ess

lend

ing

inve

stig

atio

ns

and

appr

opria

te

enfo

rcem

ent

actio

n w

here

nece

ssar

y.

Num

ber o

f

mul

timed

ia

awar

enes

s

cam

paig

ns

(radi

o/TV

/inte

rvie

ws/

new

s prin

t)

cond

ucte

d

misl

eadi

ng o

n

adve

rtise

men

ts.

--

--

30 o

f any

of t

he

follo

win

g:

-Rad

io

-TV

-inte

rvie

ws

-New

s pr

int o

n

mis

lead

ing

adve

rtis

emen

ts.

R1.1

m

35 o

f any

of t

he

follo

win

g:

-Rad

io

-TV

-inte

rvie

ws

-New

s pr

int o

n

mis

lead

ing

adve

rtis

emen

ts.

R1.2

m

40 o

f any

of t

he

follo

win

g:

-Rad

io

-TV

-inte

rvie

ws

-New

s pr

int o

n

mis

lead

ing

adve

rtis

emen

ts.

R1.3

m

Impr

ove

awar

enes

s on

mis

lead

ing

adve

rtis

emen

ts

and

hone

st

disc

losu

res

by

cons

umer

s on

a�or

dabi

lity

test

s.

Out

put

Perf

orm

ance

Indi

cato

r/m

easu

re

Aud

ited

Act

ual P

erfo

rman

ce

2012

/13

2013

/14

2014

/15

Esti

mat

edPe

rfor

man

ceM

ediu

m T

erm

Tar

gets

2015

/16

2016

/17

2017

/18

2018

/19

*Bas

ed o

n th

e es

timat

ed a

nnua

l per

form

ance

targ

ets

for 2

015/

16 �

nanc

ial y

ear

17

.3 P

erfo

rman

ce in

dica

tors

and

per

form

ance

targ

ets p

er p

rogr

amm

e.

21

*Bas

ed o

n th

e es

timat

ed a

nnua

l per

form

ance

targ

ets

for 2

015/

16 �

nanc

ial y

ear

17

.4 Q

uart

erly

Mile

ston

es fo

r Pro

gram

me

2

Dec

reas

ed le

vels

of re

ckle

ss le

ndin

g

prac

tices

.

Cond

uct r

eckl

ess

lend

ing

inve

stig

atio

ns a

nd

appr

opria

te

enfo

rcem

ent

actio

n w

here

nece

ssar

y.

Num

ber o

f cre

dit

prov

ider

s

inve

stig

ated

and

appr

opria

te

enfo

rcem

ent

actio

n ta

ken

whe

re n

eces

sary

.

*40

cred

it

prov

ider

s’

inve

stig

atio

ns

cond

ucte

d an

d

appr

opria

te

enfo

rcem

ent

actio

n ta

ken

whe

re n

eces

sary

.

60 c

redi

t pro

vide

rs

inve

stig

ated

and

appr

opria

te

enfo

rcem

ent

actio

n ta

ken

whe

re n

eces

sary

.

R28.

5m

15 R7.3

m

16 R7.5

m

13 R6m

2 R1.5

mIm

prov

e

awar

enes

s on

misl

eadi

ng

adve

rtise

men

ts

and

hone

st

disc

losu

res b

y

cons

umer

s on

a�or

dabi

lity

test

s.

Num

ber o

f

mul

timed

ia

awar

enes

s

cam

paig

ns

(radi

o/TV

/

inte

rvi w

s/ne

ws

prin

t) co

nduc

ted

on m

isle

adin

g

adve

rtis

emen

ts.

-30

of a

ny o

f the

follo

win

g:

-Rad

io

-TV

-inte

rvie

ws

-New

s prin

t on

mis

lead

ing

adve

rtis

emen

ts.

R1.1

m

6 R0.2

m

10 R0.4

m

6 R0.2

m

8 R0.3

m

Goa

l/O

utco

me

Out

put

Perf

orm

ance

Indi

cato

r/m

easu

re

Base

line

2016

/17

Ann

ual T

arge

tQ

uart

erly

Mile

ston

es

1st Q

uart

er2nd

Qua

rter

3rd Q

uart

er4th

Qua

rter

22

23

Curr

ent p

aym

ent

Com

pens

atio

n of

em

ploy

ees

Goo

ds &

ser

vice

s, et

c.

R12m

R27.

2m

R14m

R21m

R16m

R13m

R15.

6m

R12.

7m

R16.

2m

R13.

4m

R16.

7m

R13.

m

R17.

4m

R14m

Oth

er c

lass

i�ca

tions

--

---

--

-

Econ

omic

Cla

ssi�

cati

on

Prog

ram

me

Nam

e:

2012

/13

R ’0

00

Expe

ndit

ure

Out

com

e

2013

/14

R ’0

0020

14/1

5R

’000

2015

/16

R ’0

00

Adj

uste

dA

ppro

pria

tion

2016

/17

R ’0

0020

17/1

8R

’000

2018

/19

R ’0

00

Med

ium

-Ter

m E

xpen

ditu

re E

stim

ate

17.5

Fin

anci

al P

lan

(Exp

endi

ture

est

imat

es fo

r pro

gram

me

2)

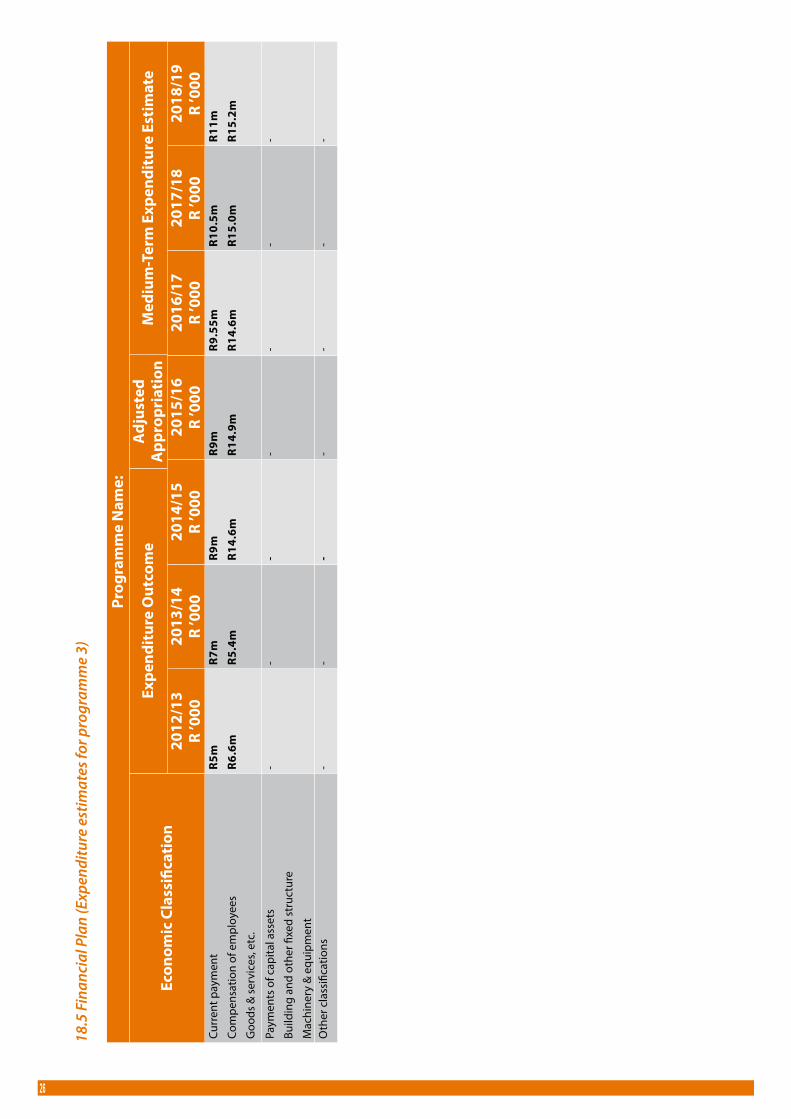

18.

Prog

ram

me

3: T

o en

hanc

e th

e qu

alit

y an

d ac

cura

cy o

f cre

dit b

urea

u in

form

atio

n.

18

.1 P

urpo

se o

f the

pro

gram

me

Th

e pu

rpos

e of

this

pro

gram

me

is to

incr

ease

com

plia

nce

by c

redi

t bur

eaus

thro

ugh

com

plia

nce

mon

itorin

g an

d in

vest

igat

ions

and

by

taki

ng a

ppro

pria

te e

nfor

cem

ent a

ctio

n

w

here

nec

essa

ry.

18

.2 D

escr

iptio

n of

the

prog

ram

me

In

vest

igat

ions

and

com

plia

nce

mon

itorin

g w

ill b

e co

nduc

ted

proa

ctiv

ely

by th

e N

CR. C

ompl

aint

s th

at a

re lo

dged

by

cons

umer

s w

ill b

e in

vest

igat

ed th

roug

h re

activ

e

m

echa

nism

s. Ba

sed

on th

e ou

tcom

e of

the

inve

stig

atio

ns, a

ppro

pria

te e

nfor

cem

ent a

ctio

n w

ill b

e ta

ken

whe

re n

eces

sary

.

--

--

--

-Pa

ymen

ts o

f cap

ital a

sset

s

Build

ing

and

othe

r �xe

d st

ruct

ures

Mac

hine

ry a

nd e

quip

men

t

Num

ber o

f cre

dit

bure

aus

inve

stig

ated

and

appr

opria

te

enfo

rcem

ent a

ctio

n

take

n w

here

nece

ssar

y.

2 cr

edit

bure

aus

inve

stig

atio

ns

cond

ucte

d &

enfo

rcem

ent

actio

n ta

ken

in

term

s of

sec

tions

43,7

0,71

,72

and

regu

latio

ns 1

7 to

20 o

f the

NCA

.

R11.

4m

2 cr

edit

bure

aus

inve

stig

atio

ns

cond

ucte

d &

enfo

rcem

ent

actio

n ta

ken

in

term

s of

sec

tions

43,7

0,71

,72

and

regu

latio

ns 1

7 to

20 o

f the

NCA

.

R6.2

m

2 cr

edit

bure

aus

inve

stig

ated

and

appr

opria

te

enfo

rcem

ent

actio

n ta

ken

whe

re n

eces

sary

.

R14m

*2 c

redi

t bur

eaus

inve

stig

ated

and

appr

opria

te

enfo

rcem

ent

actio

n ta

ken

whe

re n

eces

sary

.

R14.

9m

3 cr

edit

bure

aus

inve

stig

ated

and

appr

opria

te

enfo

rcem

ent

actio

n ta

ken

whe

re n

eces

sary

.

R14.

15m

4 cr

edit

bure

aus

inve

stig

ated

and

appr

opria

te

enfo

rcem

ent

actio

n ta

ken

whe

re n

eces

sary

.

R15m

5 cr

edit

bure

aus

inve

stig

ated

and

appr

opria

te

enfo

rcem

ent

actio

n ta

ken

whe

re n

eces

sary

.

R15.

4

Impr

oved

cons

umer

cre

dit

info

rmat

ion.

Goa

l/O

utco

me

Incr

ease

com

plia

nce

by c

redi

t bur

eaus

in re

spec

t of

cons

umer

cre

dit

info

rmat

ion.

Num

ber o

f cre

dit

bure

aus

audi

ted

repo

rts

revi

ewed

and

appr

opria

te

corr

ectiv

e ac

tion

take

n w

here

nece

ssar

y.

--

- R6.2

m

14 c

redi

t bur

eaus

audi

ted

repo

rts

revi

ewed

and

corr

ectiv

e ac

tion

take

n w

here

nece

ssar

y.

R9.6

m

All

regi

ster

ed

cred

it bu

reau

s

audi

ted

repo

rts

revi

ewed

and

appr

opria

te

corr

ectiv

e ac

tion

take

n w

here

nece

ssar

y.

R10m

All

regi

ster

ed

cred

it bu

reau

s

audi

ted

repo

rts

revi

ewed

and

appr

opria

te

corr

ectiv

e ac

tion

take

n w

here

nece

ssar

y.

R10.

5m

All

regi

ster

ed

cred

it bu

reau

s

audi

ted

repo

rts

revi

ewed

and

appr

opria

te

corr

ectiv

e ac

tion

take

n w

here

nece

ssar

y.

R10.

8m

Out

put

Perf

orm

ance

Indi

cato

r/m

easu

re

Aud

ited

Act

ual P

erfo

rman

ce

2012

/13

2013

/14

2014

/15

Esti

mat

edPe

rfor

man

ceM

ediu

m T

erm

Tar

gets

2015

/16

2016

/17

2017

/18

2018

/19

*Bas

ed o

n th

e es

timat

ed a

nnua

l per

form

ance

targ

ets

for 2

015/

16 �

nanc

ial y

ear

18

.3 P

erfo

rman

ce in

dica

tors

and

per

form

ance

targ

ets p

er p

rogr

amm

e.

24

25

*Bas

ed o

n th

e es

timat

ed a

nnua

l per

form

ance

targ

ets

for 2

015/

16 �

nanc

ial y

ear

18

.4 Q

uart

erly

Mile

ston

es fo

r Pro

gram

me

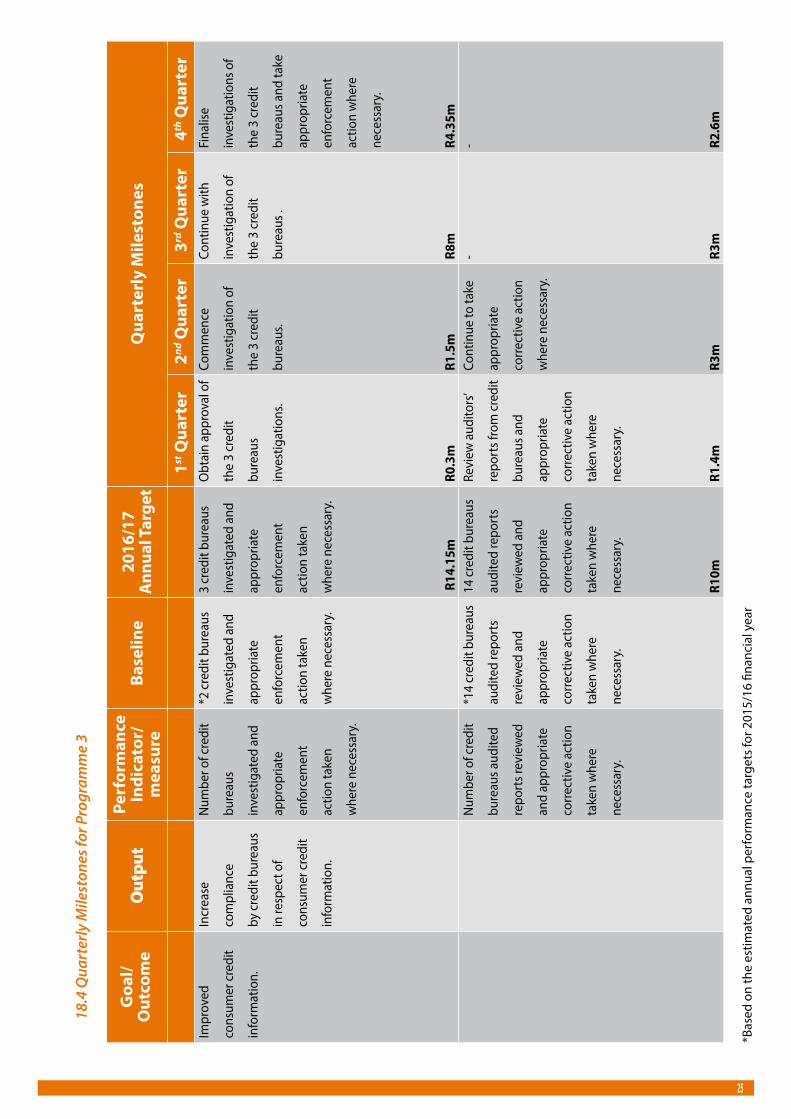

3

Impr

oved

cons

umer

cre

dit

info

rmat

ion.

Incr

ease

com

plia

nce

by c

redi

t bur

eaus

in re

spec

t of

cons

umer

cre

dit

info

rmat

ion.

Num

ber o

f cre

dit

bure

aus

inve

stig

ated

and

appr

opria

te

enfo

rcem

ent

actio

n ta

ken

whe

re n

eces

sary

.

*2 c

redi

t bur

eaus

inve

stig

ated

and

appr

opria

te

enfo

rcem

ent

actio

n ta

ken

whe

re n

eces

sary

.

3 cr

edit

bure

aus

inve

stig

ated

and

appr

opria

te

enfo

rcem

ent

actio

n ta

ken

whe

re n

eces

sary

.

R14

.15m

Obt

ain

appr

oval

of

the

3 cr

edit

bure

aus

inve

stig

atio

ns.

R0.3

m

Com

men

ce

inve

stig

atio

n of

the

3 cr

edit

bure

aus.

R1.5

m

Cont

inue

with

inve

stig

atio

n of

the

3 cr

edit

bure

aus .

R8m

Fina

lise

inve

stig

atio

ns o

f

the

3 cr

edit

bure

aus a

nd ta

ke

appr

opria

te

enfo

rcem

ent

actio

n w

here

nece

ssar

y.

R4.3

5mN

umbe

r of c

redi

t

bure

aus a

udite

d

repo

rts r

evie

wed

and

appr

opria

te

corr

ectiv

e ac

tion

take

n w

here

nece

ssar

y.

*14

cred

it bu

reau

s

audi

ted

repo

rts

revi

ewed

and

appr

opria

te

corr

ectiv

e ac

tion

take

n w

here

nece

ssar

y.

14 c

redi

t bur

eaus

audi

ted

repo

rts

revi

ewed

and

appr

opria

te

corr

ectiv

e ac

tion

take

n w

here

nece

ssar

y.

R10m

Revi

ew a

udito

rs’

repo

rts f

rom

cre

dit

bure

aus a

nd

appr

opria

te

corr

ectiv

e ac

tion

take

n w

here

nece

ssar

y.

R1.4

m

Cont

inue

to ta

ke

appr

opria

te

corr

ectiv

e ac

tion

whe

re n

eces

sary

.

R3m

- R3m

- R2.6

m

Goa

l/O

utco

me

Out

put

Perf

orm

ance

Indi

cato

r/m

easu

reBa

selin

e20

16/1

7A

nnua

l Tar

get

Qua

rter

ly M

ilest

ones