NATIONAL BOARD OF ACCOUNTANTS AND

AUDITORSINTERNATIONAL STANDARDS ON AUDITING

ISAs - OVERVIEW

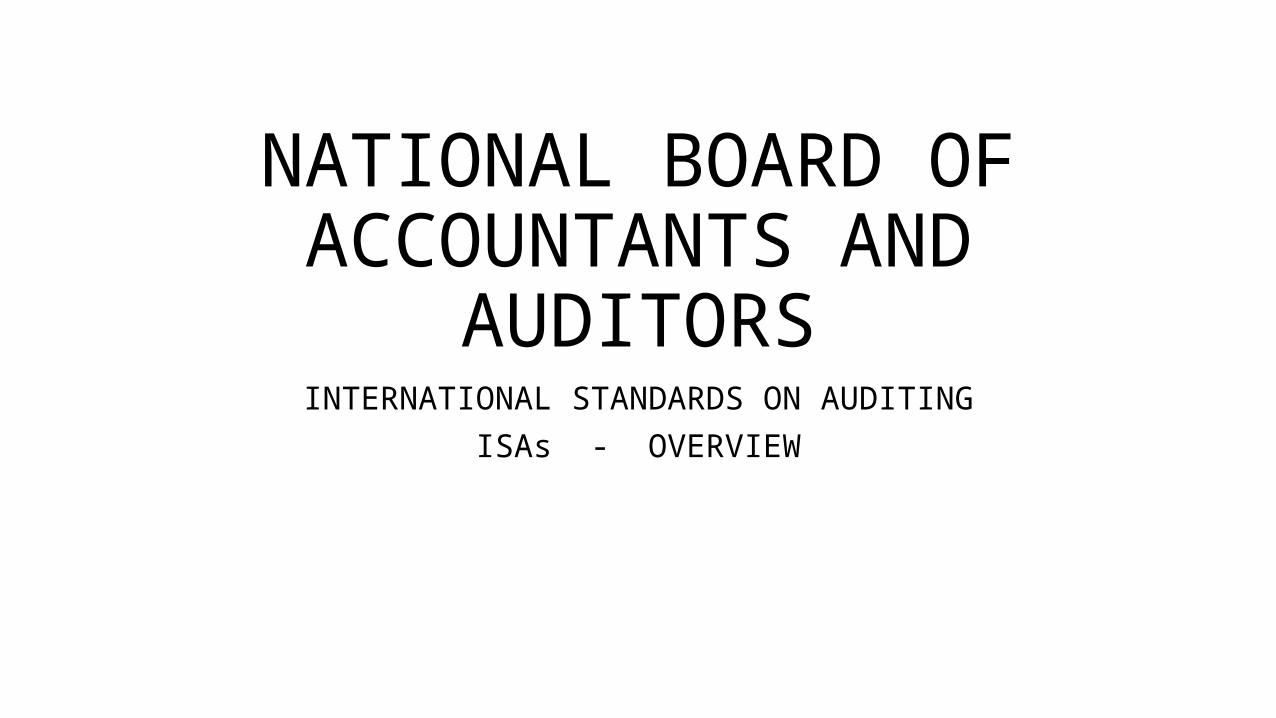

INTERNATIONAL STANDARDS ON AUDITINGISA 200: Overall Responsibilities when Conducting an Audit (a) Overall Objectives of the Auditor i) to obtain reasonable assurance ii) to report on the financial statements (b) Requirements = “ the auditor shall “ i) comply with ethical requirements ii) apply professional scepticism iii) exercise professional judgement iv) obtain sufficient appropriate audit evidence and assess audit risk v) conduct the audit in accordance with ISAs

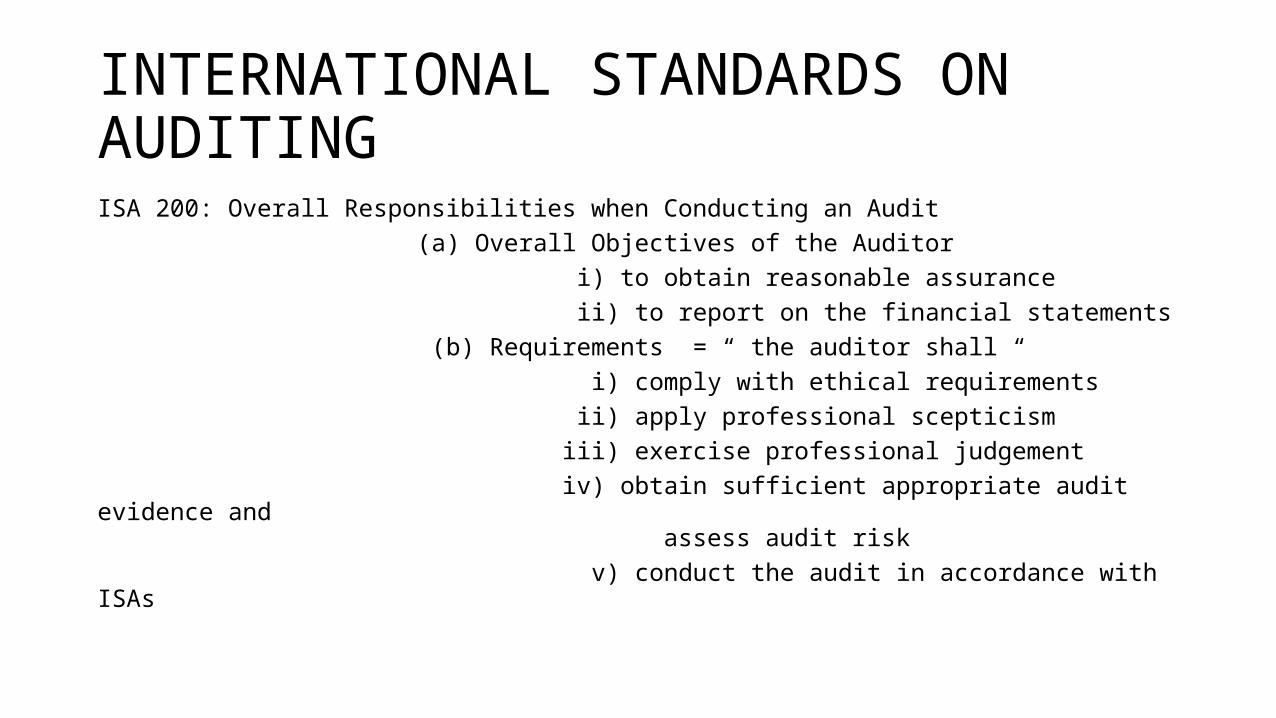

INTERNATIONAL STANDARDS ON AUDITINGISA 210: Agreeing Terms of the Audit Engagement (a) Objective = to accept an audit after i) establishing the preconditions ii) confirming that there is a common understanding (b) Requirements = the auditor shall i) establish preconditions for the audit ii) obtain an agreement of the terms of the audit iii) review the situation for recurring audits iv) ensure acceptance of change in the terms v) consider additional considerations, if any.

INTERNATIONAL STANDARDS ON AUDITINGISA 220: Quality Control for an Audit (a) Objective = to implement quality control procedures to ensure i) that the audit complies professional standards and legal and regulatory requirements ii) that the auditor’s report is appropriate (b) Requirements = the engagement partner shall i) take leadership responsibility for quality ii) comply with relevant ethical requirements iii) complete the procedures for acceptance and continuance of client relationships iv) assign an appropriate engagement team v) review engagement performance vi) monitor the engagement vii) ensure appropriate documentation for the audit

INTERNATIONAL STANDARDS ON AUDITINGISA 230: Audit Documentation (a) Objective = to prepare audit documentation that provides i) sufficient and appropriate record of the basis for the auditor’s report ii) evidence that the audit was planned and performed in accordance with ISAs and legal and regulatory requirements (b) Requirements = the auditor shall i) ensure timely preparation of audit documentation ii) ensure that audit procedures performed and audit evidence obtained are documented iii) assemble the final audit file

ISA 230: Important points to note

1. ISA 230 says: the audit documentation should enable an experienced auditor to understand i) the nature, timing and extent of the audit procedures ii) the results and evidence obtained and iii) how significant matters have been dealt with

2. The audit file must stand on its own3. When documenting the nature, timing and extent of audit procedures,

one has to record the identifying characteristics of the specific items tested, who performed the audit work, date completed, who reviewed the audit work and the date and extent of the review.

INTERNATIONAL STANDARDS ON AUDITINGISA 300: Planning an Audit of Financial Statements (a) Objective = to plan the audit so that it will be performed in an effective manner (b) Requirements = the auditor shall i) involve key engagement team members ii) carry out preliminary engagement activities iii) complete planning activities iv) ensure proper documentation v) attend to additional considerations in the case of initial audit engagements, e.g. acceptance procedures, communication with previous auditors

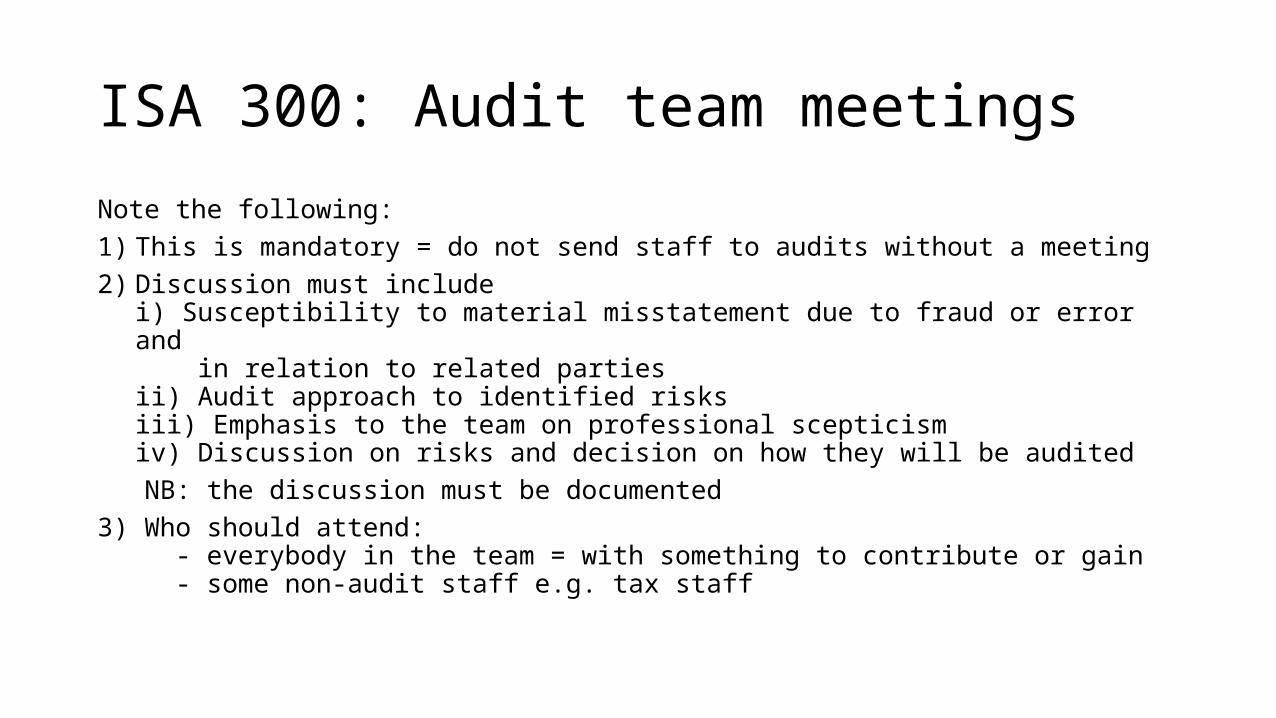

ISA 300: Audit team meetings

Note the following:1) This is mandatory = do not send staff to audits without a meeting2) Discussion must include

i) Susceptibility to material misstatement due to fraud or error and in relation to related partiesii) Audit approach to identified risksiii) Emphasis to the team on professional scepticismiv) Discussion on risks and decision on how they will be audited

NB: the discussion must be documented3) Who should attend: - everybody in the team = with something to contribute or gain - some non-audit staff e.g. tax staff

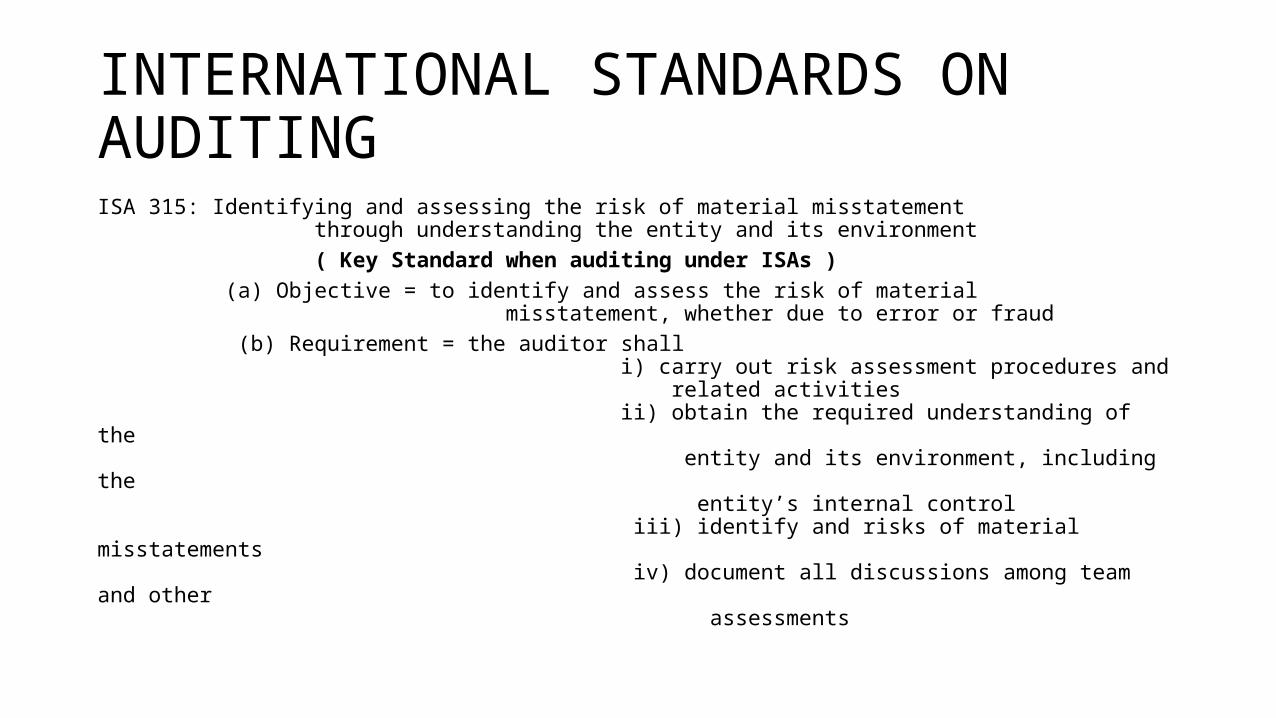

INTERNATIONAL STANDARDS ON AUDITINGISA 315: Identifying and assessing the risk of material misstatement through understanding the entity and its environment ( Key Standard when auditing under ISAs ) (a) Objective = to identify and assess the risk of material misstatement, whether due to error or fraud (b) Requirement = the auditor shall i) carry out risk assessment procedures and related activities ii) obtain the required understanding of the entity and its environment, including the entity’s internal control iii) identify and risks of material misstatements iv) document all discussions among team and other assessments

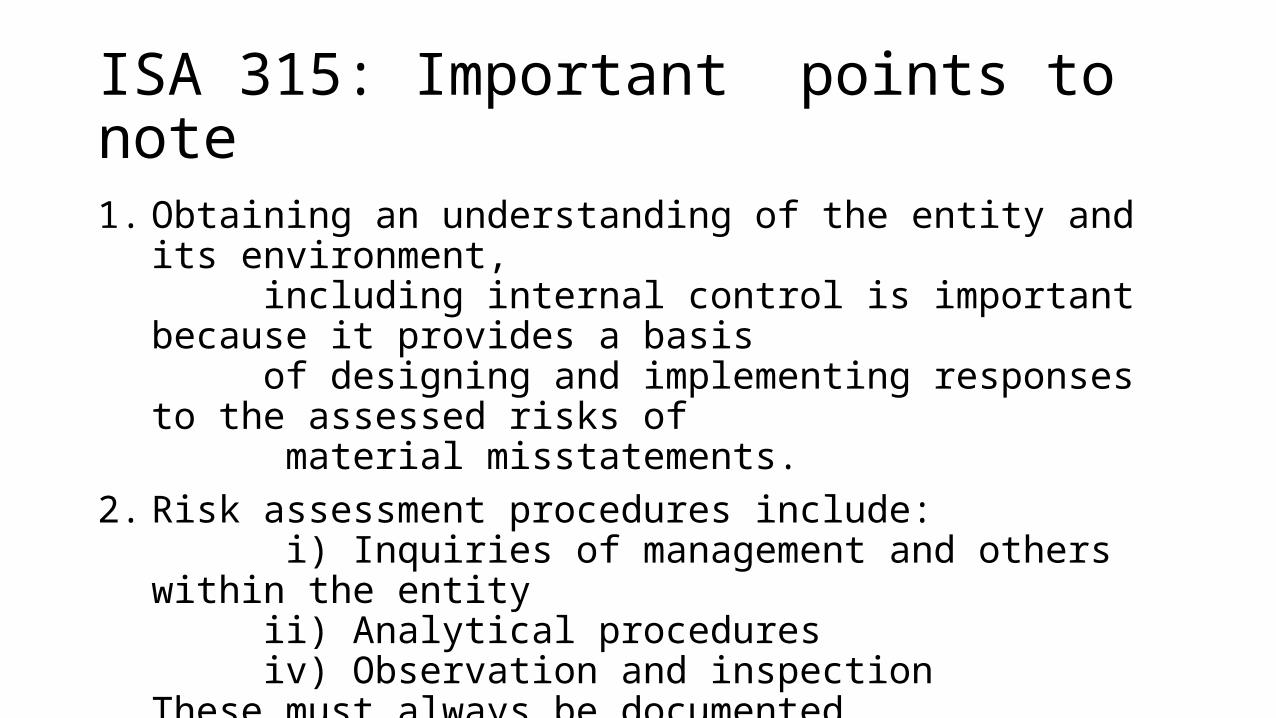

ISA 315: Important points to note

1. Obtaining an understanding of the entity and its environment, including internal control is important because it provides a basis

of designing and implementing responses to the assessed risks of

material misstatements.2. Risk assessment procedures include:

i) Inquiries of management and others within the entity ii) Analytical procedures iv) Observation and inspectionThese must always be documented

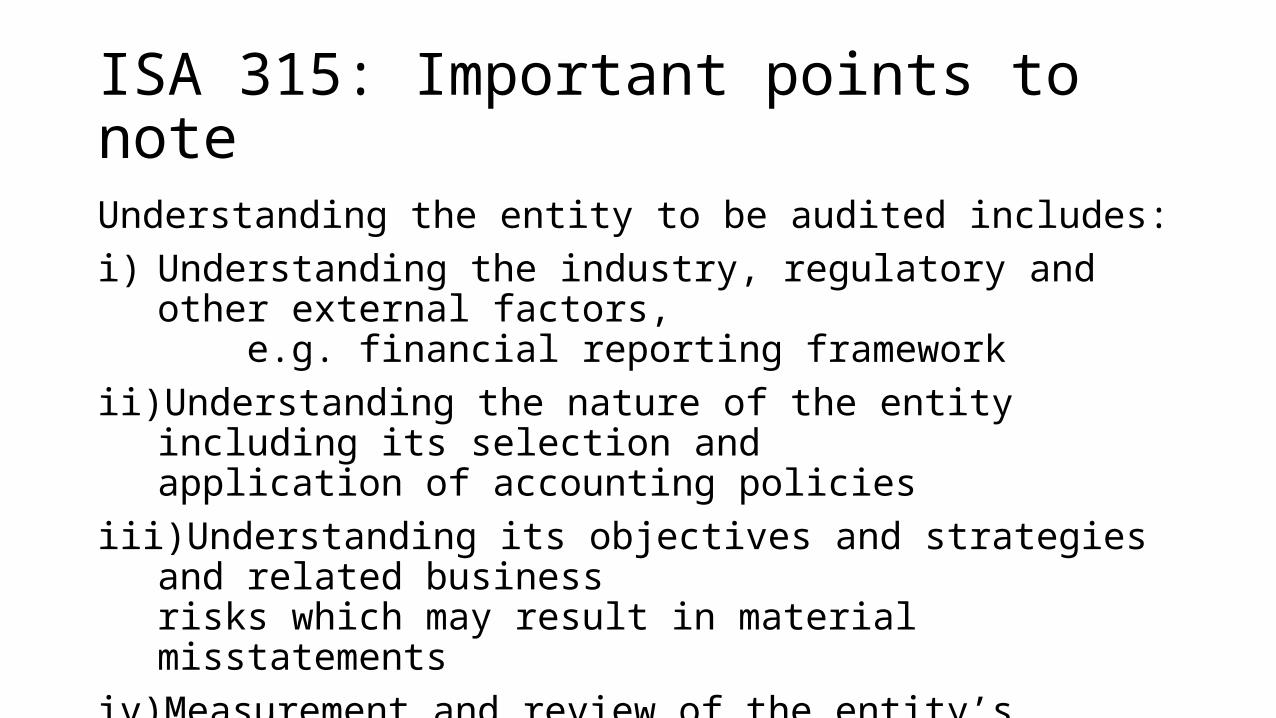

ISA 315: Important points to note

Understanding the entity to be audited includes:i) Understanding the industry, regulatory and other external factors,

e.g. financial reporting frameworkii) Understanding the nature of the entity including its selection and

application of accounting policiesiii) Understanding its objectives and strategies and related business

risks which may result in material misstatementsiv) Measurement and review of the entity’s financial performancev) Assessing the entity’s Internal Controls

ISA 315: Important points to note

Internal Controls: ISA requires you to=i) Obtain an understanding of internal controls relevant to the auditii) Evaluate the design of those controls and determine whether they

have been implementedInternal Controls: Why controls are needed = in order to ensure thatiii) All transactions are recorded, i.e. Records are complete and therefore

reflected in the financial statementsiv) Erroneous transactions are not includedv) Transactions are recorded accurately

ISA 315: Important points to note

ISA 315 also requires the auditor to identify and assess risks of materialmisstatements at (a) the financial statement level and (b) assertion levelin order to provide a basis for designing and performing further audit procedures. For this purpose, the auditor does the following:i) identifies risks throughout the process of obtaining an understanding of the entity and its environmentii) relates the identified risks to what can go wrong at assertion leveliii) considers whether the risks are of a magnitude that could result into material misstatements of the financial statements

ISA 315: Important points to note

Preliminary Analytical Analysis: Why do it?1) Assists in assessing the risk of material misstatement2) Assists to determine nature, timing and extent of further audit

procedures3) Assists to identify abnormal transactions, balances and ratios

meriting further inquiry4) Highlights new transactions, balances or areas of importance5) Indicates whether extensive analytical procedures or control

reliance might be appropriate6) Identifies areas where minimal or no audit work is necessary

ISA 315: Important points to note

Preliminary Analytical Analysis: What is to be done1) Put the comparative figures and comments on the variances

and ratios2) Draw conclusions on

i) matters requiring further investigation ii) risk areas identified iii) confirmations

INTERNATIONAL STANDARDS ON AUDITINGISA 320: Materiality in planning and performing an audit (a) Objective = to apply the concept of materiality appropriately in planning and performing the audit (b) Requirements = the auditor shall: i) determine materiality and performance materiality when planning the audit ii) revise materiality as the audit progresses, when necessary iii) ensure proper documentation

ISA 320: Important points to note Other Planning Issues(a) MaterialityOne must consider the following:i) For Overall materiality, use the most appropriate benchmarksii) For Section-specific materiality, consider users of the accountsiii) For Performance materiality, take into account potential for errorsiv) Trivial amounts should be determined at planning stage

ISA 320: Important points to note Other planning issues(b) Fraud Risk ( ISA 240 )One needs to do the following in relation to fraud1) Maintain an attitude of professional scepticism throughout2) Audit team members must discuss possibilities for fraud3) Discuss fraud risks with management4) Consider fraud risk factors5) Document your discussions and conclusions

INTERNATIONAL STANDARDS ON AUDITINGISA 330: The auditors responses to assessed risks (a) Objective = to obtain sufficient appropriate audit evidence regarding the assessed risks through designing and implementing appropriate responses to these risks (b) Requirements = The auditor shall i) design overall responses to assessed risks of material misstatements at financial statement level ii) design audit procedures responsive to the assessed risks of material misstatements at assertion level iii) ensure adequate presentation and disclosure iv) evaluate the sufficiency and appropriateness of the audit evidence v) ensure proper documentation

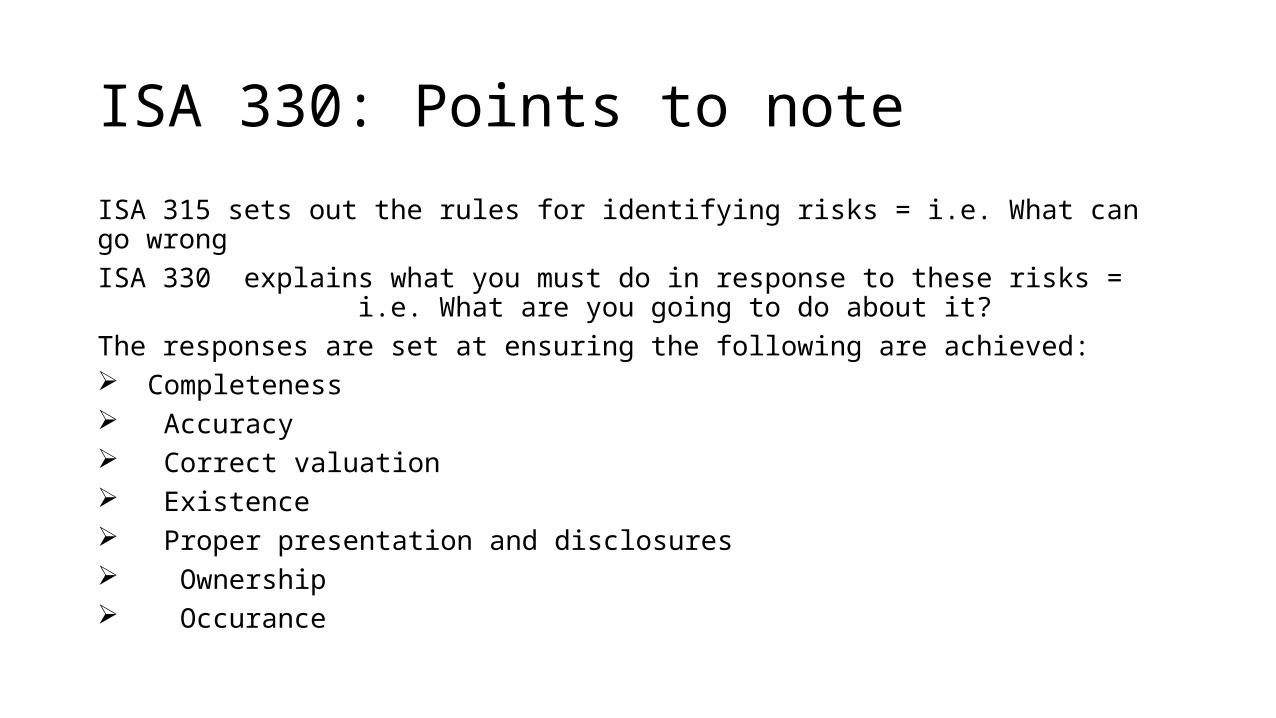

ISA 330: Points to note

ISA 315 sets out the rules for identifying risks = i.e. What can go wrongISA 330 explains what you must do in response to these risks = i.e. What are you going to do about it?The responses are set at ensuring the following are achieved: Completeness Accuracy Correct valuation Existence Proper presentation and disclosures Ownership Occurance

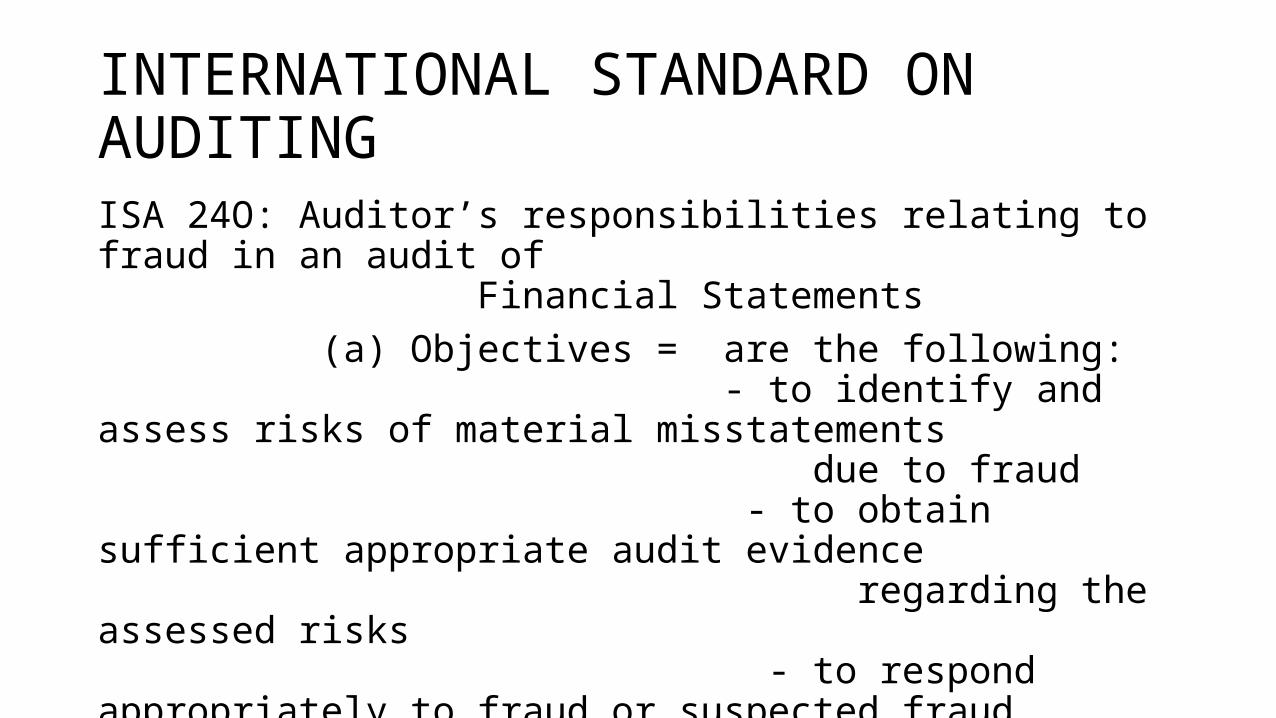

INTERNATIONAL STANDARD ON AUDITINGISA 24O: Auditor’s responsibilities relating to fraud in an audit of Financial Statements (a) Objectives = are the following: - to identify and assess risks of material misstatements due to fraud - to obtain sufficient appropriate audit evidence regarding the assessed risks - to respond appropriately to fraud or suspected fraud during the audit

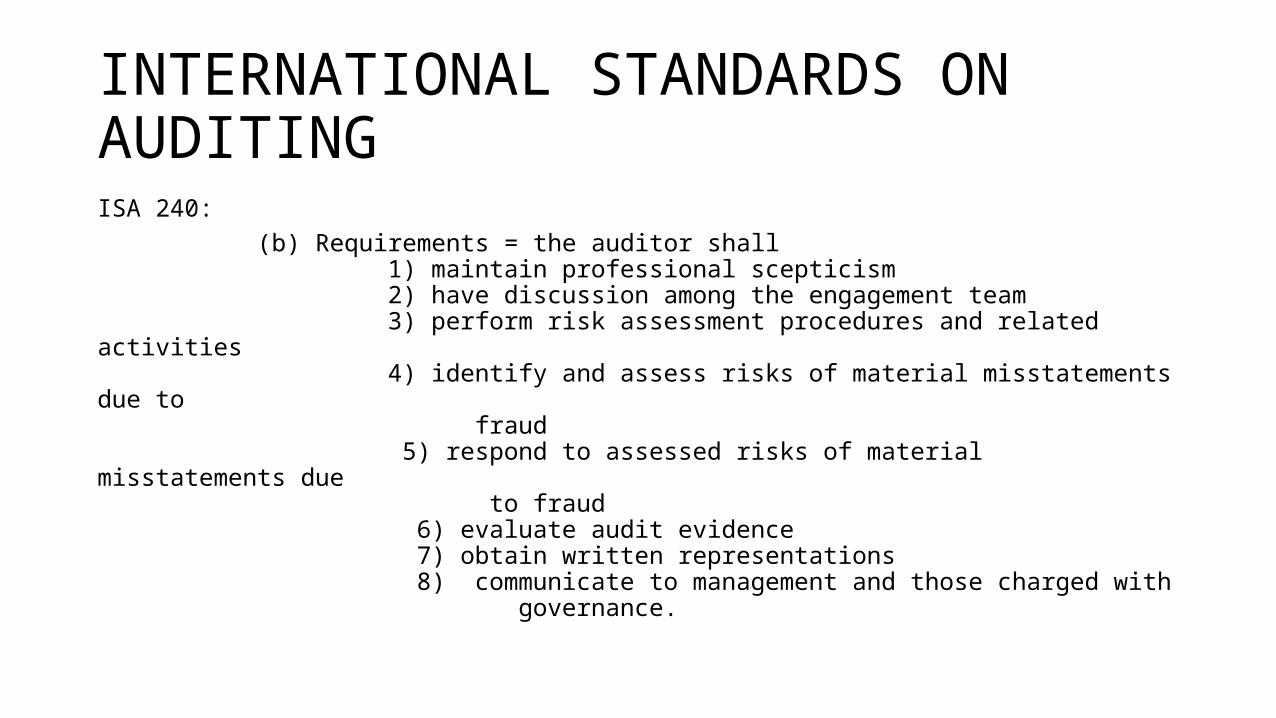

INTERNATIONAL STANDARDS ON AUDITINGISA 240: (b) Requirements = the auditor shall 1) maintain professional scepticism 2) have discussion among the engagement team 3) perform risk assessment procedures and related activities 4) identify and assess risks of material misstatements due to fraud 5) respond to assessed risks of material misstatements due to fraud 6) evaluate audit evidence 7) obtain written representations 8) communicate to management and those charged with governance.

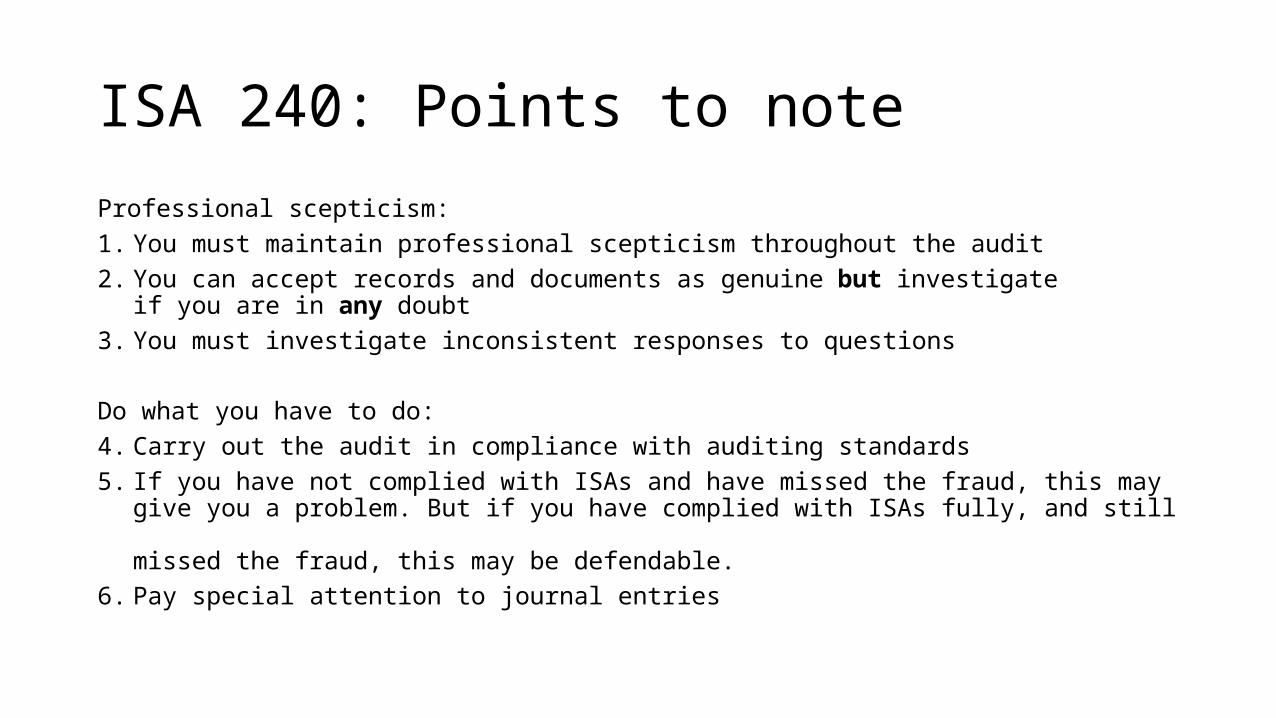

ISA 240: Points to note

Professional scepticism:1. You must maintain professional scepticism throughout the audit2. You can accept records and documents as genuine but investigate

if you are in any doubt3. You must investigate inconsistent responses to questions

Do what you have to do:4. Carry out the audit in compliance with auditing standards5. If you have not complied with ISAs and have missed the fraud, this may

give you a problem. But if you have complied with ISAs fully, and still missed the fraud, this may be defendable.

6. Pay special attention to journal entries

INTERNATIONAL STANDARDS ON AUDITINGISA 500: Audit Evidence (a) Objective = To design and perform audit procedures in such a

way as to enable the auditor to obtain sufficient appropriate audit evidence to be able to draw reasonable conclusions on which to base the auditor’s opinion

(b) Requirements = the auditor shall i) Obtain sufficient appropriate audit evidence ii) Obtain information to be used as audit evidence iii) Select items for testing to obtain audit evidence iv) Identify inconsistencies in or doubts over reliability of audit evidence

INTERNATIONAL STANDARDS ON AUDITINGISA 501: Audit Evidence – Specific considerations for selected items (a) Objective = to obtain sufficient appropriate audit evidence on

- existence and condition of inventory - completeness of litigation and claims involving the entity - presentation and disclosure of segment information

(b) Requirements = the auditor shall 1) Inventory obtain sufficient appropriate audit evidence regarding the existence and condition of inventory i) by attendance at physical inventory counting ii) by performing audit procedures over the final inventory records of the entity

INTERNATIONAL STANDARDS ON AUDITINGISA 501 Cont. (b) Requirements:

2) Litigation and claims design and perform audit procedures to identify

litigation and claims which may give rise to a risk of material misstatement

3) Segment information obtain sufficient appropriate audit evidence regarding the presentation and disclosure of segment information in accordance with the applicable financial reporting framework

INTERNATIONAL STANDARDS ON AUDITINGISA 505: External confirmations (a) Objective = to design and perform such procedures as to

obtain relevant and reliable audit evidence (b) Requirements = the auditor shall

- maintain control over external confirmation requests - follow appropriate procedures if management refuse to allow the auditor to send confirmation requests - follow appropriate results of external confirmation procedures - follow appropriate procedures in case of negative confirmations - evaluate the evidence obtained

INTERNATIONAL STANDARDS ON AUDITINGISA 580: Written Representation (a) Objectives =

i) To obtain written representations from management/ those with governance ii) To support other audit evidence relevant to the Financial Statements iii) To respond appropriately if management do not provide written representations requested

(b) Requirements = the auditor shall i) identify management from whom written representations are requested

INTERNATIONAL STANDARDS ON AUDITINGISA 580: Written Representations (b) Requirements ( cont. ) = the auditor shall

ii) specify written representations about management’s responsibilities

iii) specify other written representations iv) specify date and period covered

v) specify form of written representation vi) clear any doubt as to the reliability of the written representations and requested written representations not provided

AUDIT PROGRAMME COMPLETION

AUDIT FILE:Each Audit File will containFile IndexFile sections for respective working papersFile Sections will contain

- Audit programs - Summary sheet - Sample selection forms ( if used ) -Supporting working papers

NB: Audit programs must be completed and supported by working papers as audit evidence. Working papers must be signed and dated for work done and reviews done

AUDIT COMPLETION

Audit completion will comprise of the following activities:1) Preparation of final completion memorandum ( Matters for

Attention of Partners )2) Completion of Auditing Standards checklist3) Completion of File Completion checklist 4) Review of the Financial Statements ( for errors etc. )5) Preparation of Audit Highlights6) Preparation of Unadjusted Errors report7) Preparation of Justification of Audit report

INTERNATIONAL STANDARDS ON AUDITINGOTHER IMPORTANT ISAsISAs not discussed but need to draw your attention on:ISA 250 = Consideration of Laws and Regulations in an AuditISA 260/265 = Communication with those charged with GovernanceISA 450 = Evaluation of Misstatements Identified During the AuditISA 520 = Analytical ProceduresISA 530 = Audit SamplingISA 560 = Subsequent EventsISA 570 = Going ConcernISA 700 = Forming an Opinion and Reporting on Financial Statements

INTERNATIONAL STANDARDS ON AUDITING

PLEASE DO WHAT YOU HAVE TO DO

THANK YOU

Recommended