The Collaborative

Economy:

A Response to a Digitally

Disrupted World

Frank Farrall

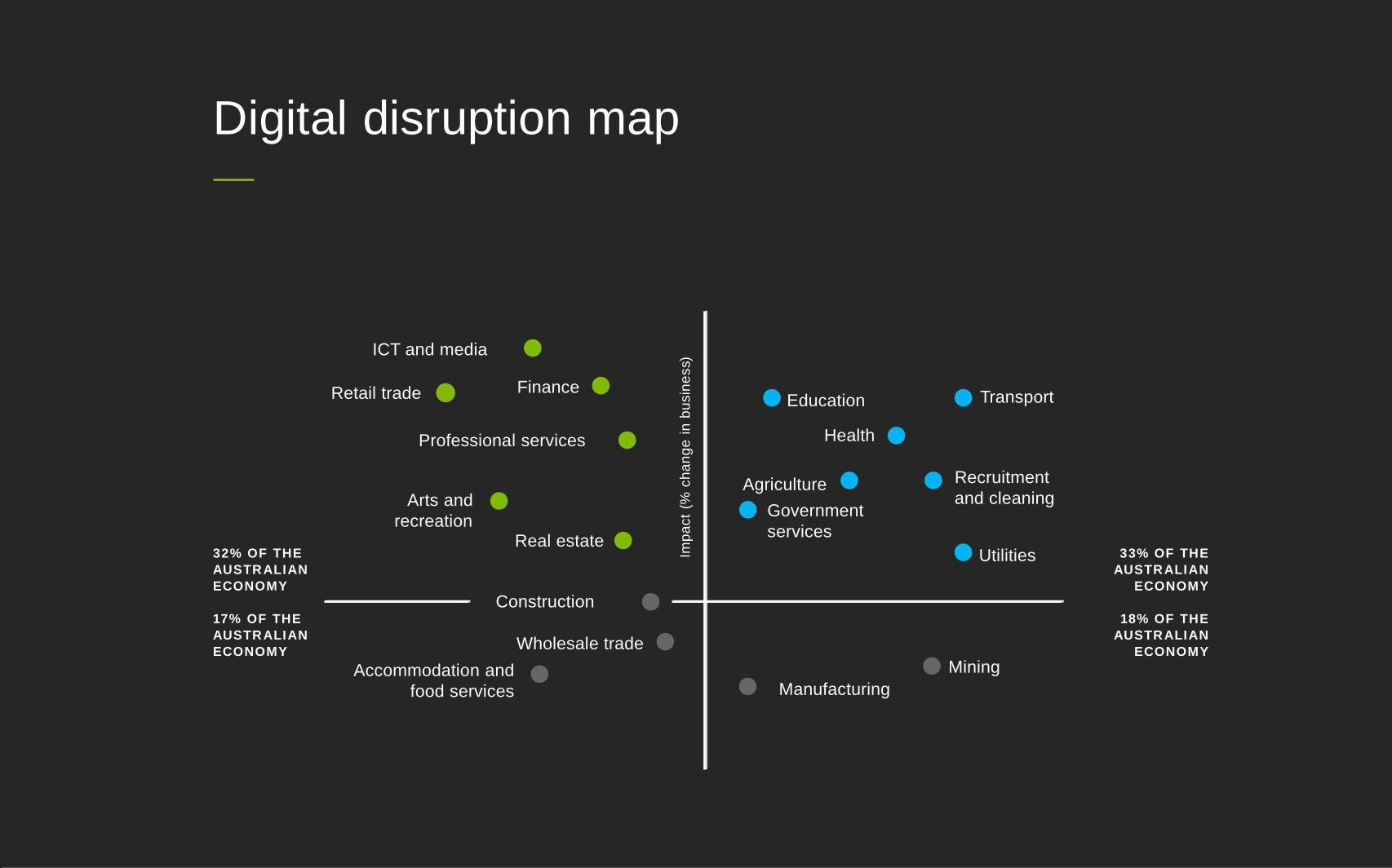

ICT and media

Finance

Professional services

Retail trade

Arts and

recreationReal estate

Construction

Wholesale trade

Manufacturing

Mining

Utilities

Agriculture

Government

services

Education

Health

Transport

Recruitment

and cleaning

Accommodation and

food services

32% OF THE

AUSTRALIAN

ECONOMY

17% OF THE

AUSTRALIAN

ECONOMY

18% OF THE

AUSTRALIAN

ECONOMY

33% OF THE

AUSTRALIAN

ECONOMY

Imp

act

(%ch

an

ge

inb

usin

ess)

Digital disruption map

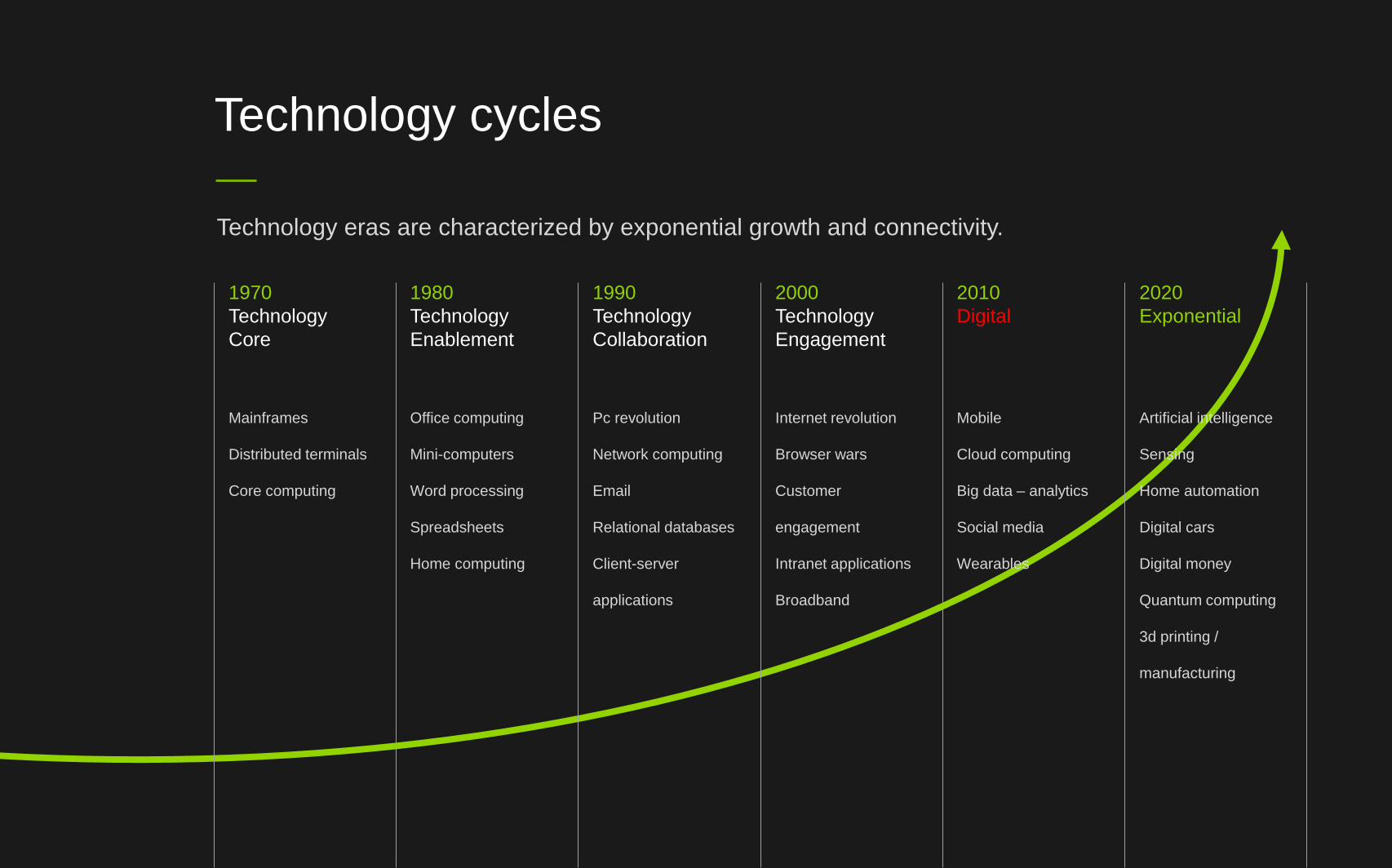

1970

Technology

Core

1980

Technology

Enablement

1990

Technology

Collaboration

2000

Technology

Engagement

2010

Digital

2020

Exponential

Technology cycles

Technology eras are characterized by exponential growth and connectivity.

Mainframes

Distributed terminals

Core computing

Office computing

Mini-computers

Word processing

Spreadsheets

Home computing

Pc revolution

Network computing

Relational databases

Client-server

applications

Internet revolution

Browser wars

Customer

engagement

Intranet applications

Broadband

Mobile

Cloud computing

Big data – analytics

Social media

Wearables

Artificial intelligence

Sensing

Home automation

Digital cars

Digital money

Quantum computing

3d printing /

manufacturing

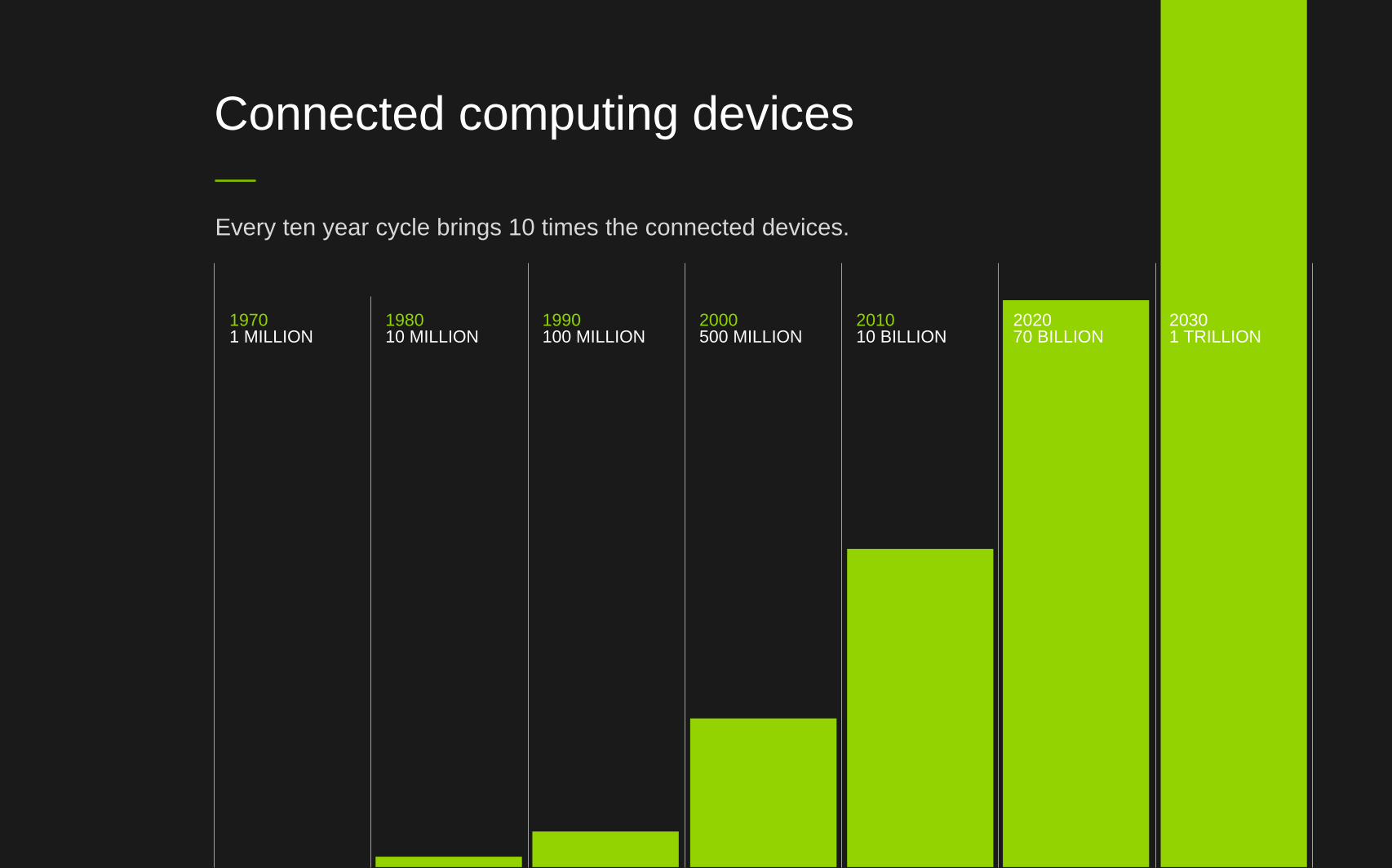

Connected computing devices

Every ten year cycle brings 10 times the connected devices.

19701 MILLION

198010 MILLION

1990100 MILLION

2000500 MILLION

201010 BILLION

202070 BILLION

20301 TRILLION

The Super Disruptors Of 2010

Enabling the Digital Era

MOBILE ANALYTICS CLOUD SOCIAL

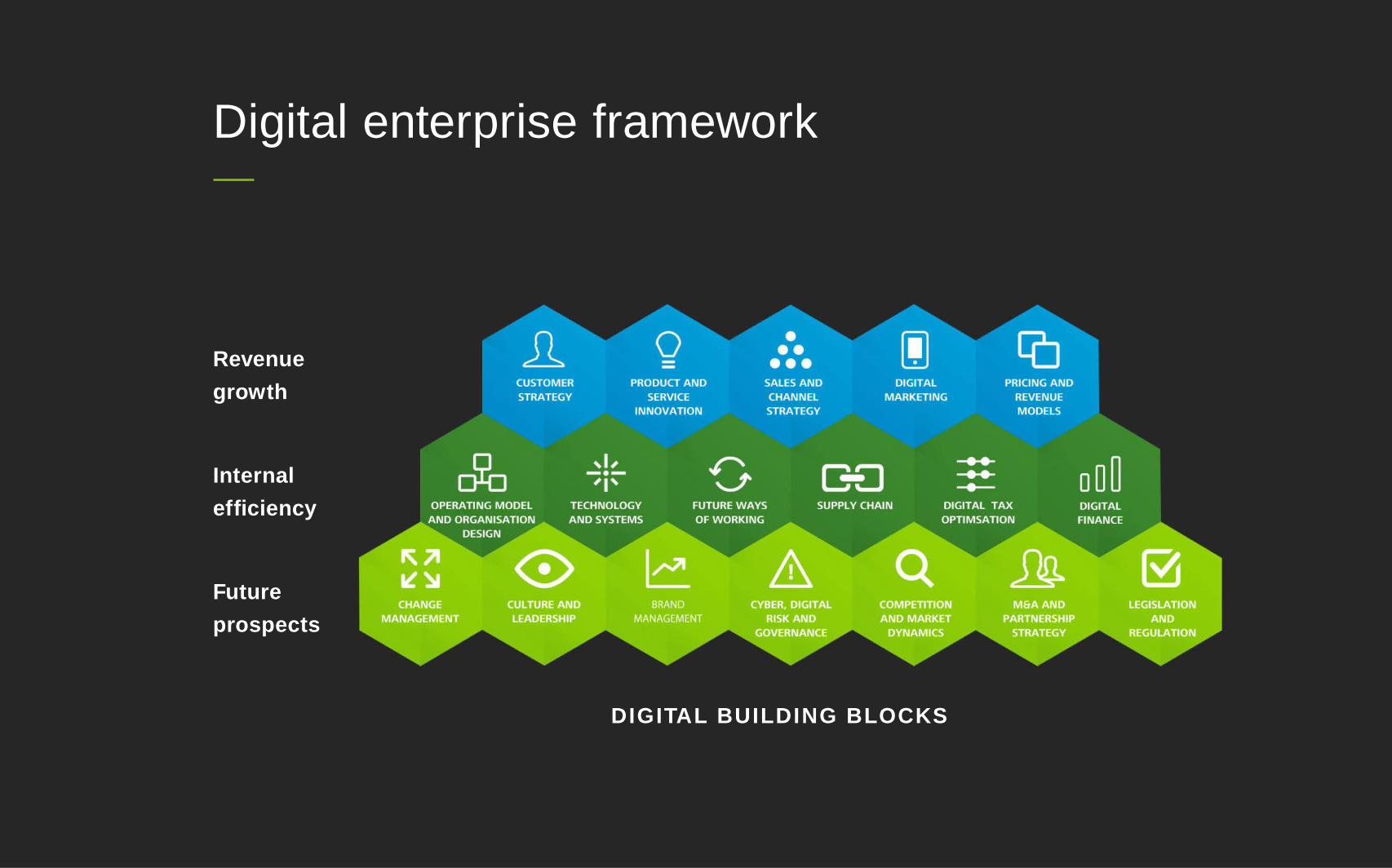

Digital enterprise framework

Revenue

growth

Internal

efficiency

Future

prospects

DIGITAL BUILDING BLOCKS

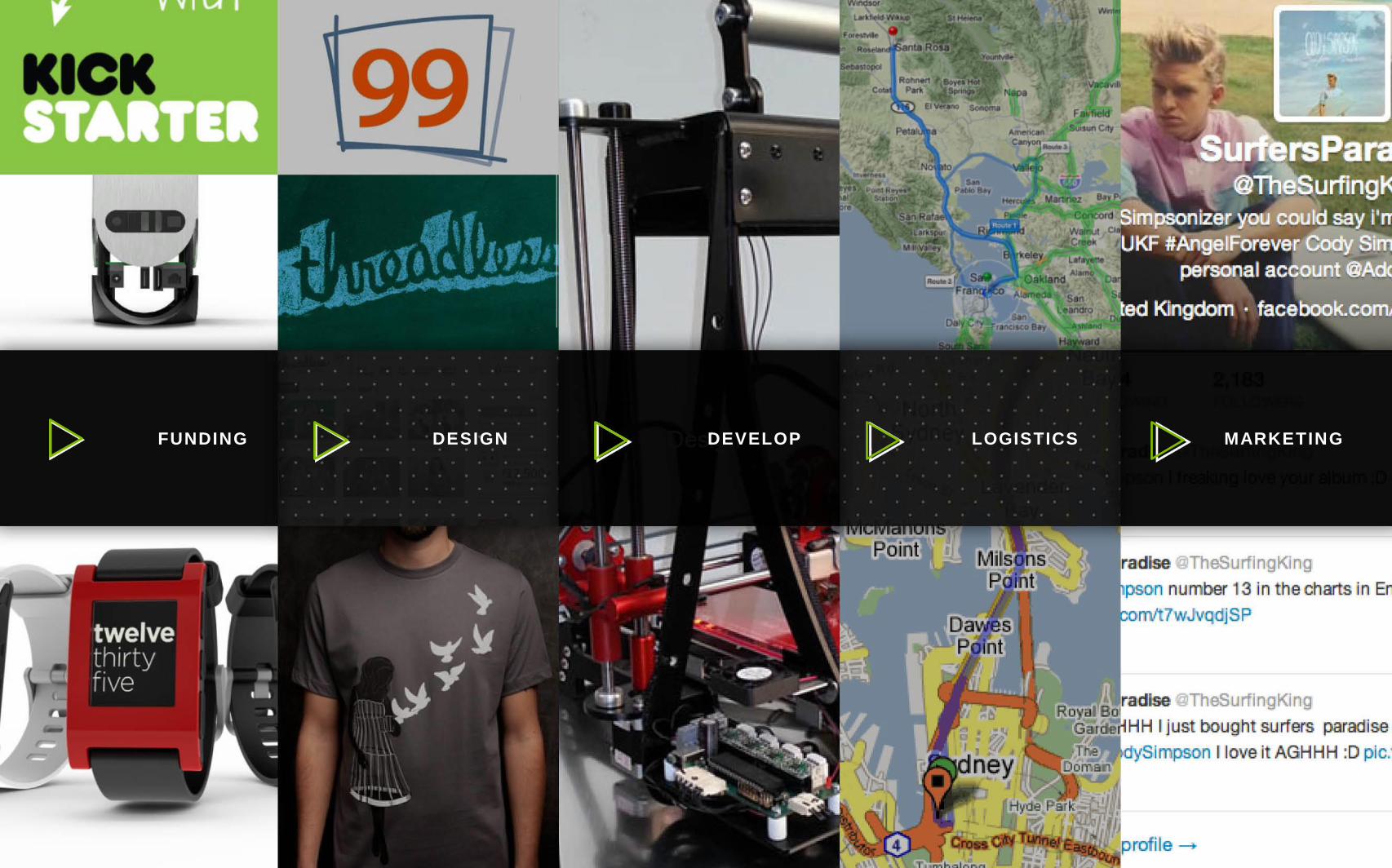

FUNDING DEVELOP MARKETINGLOGISTICSDESIGN

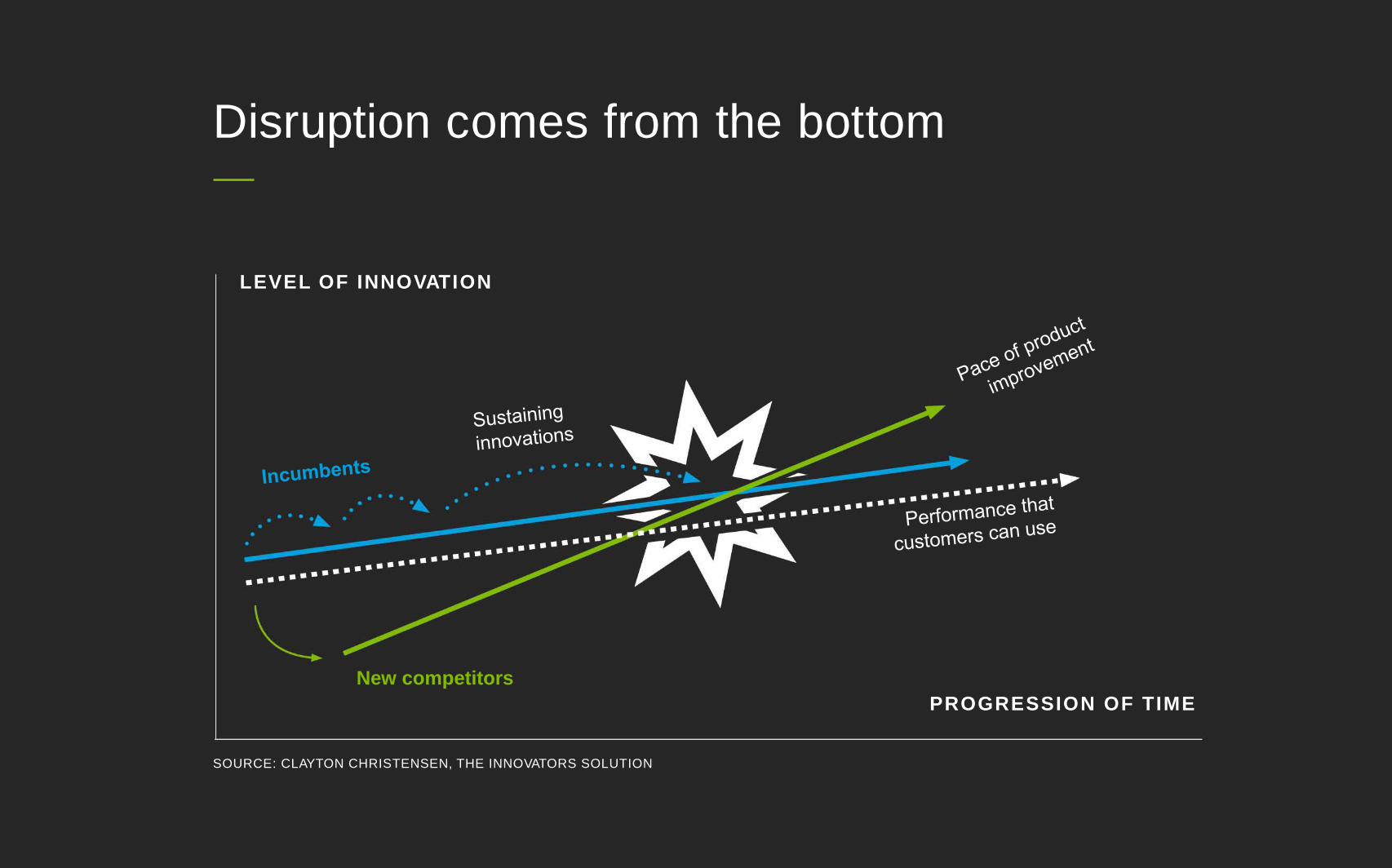

LEVEL OF INNOVATION

New competitors

PROGRESSION OF TIME

SOURCE: CLAYTON CHRISTENSEN, THE INNOVATORS SOLUTION

Disruption comes from the bottom

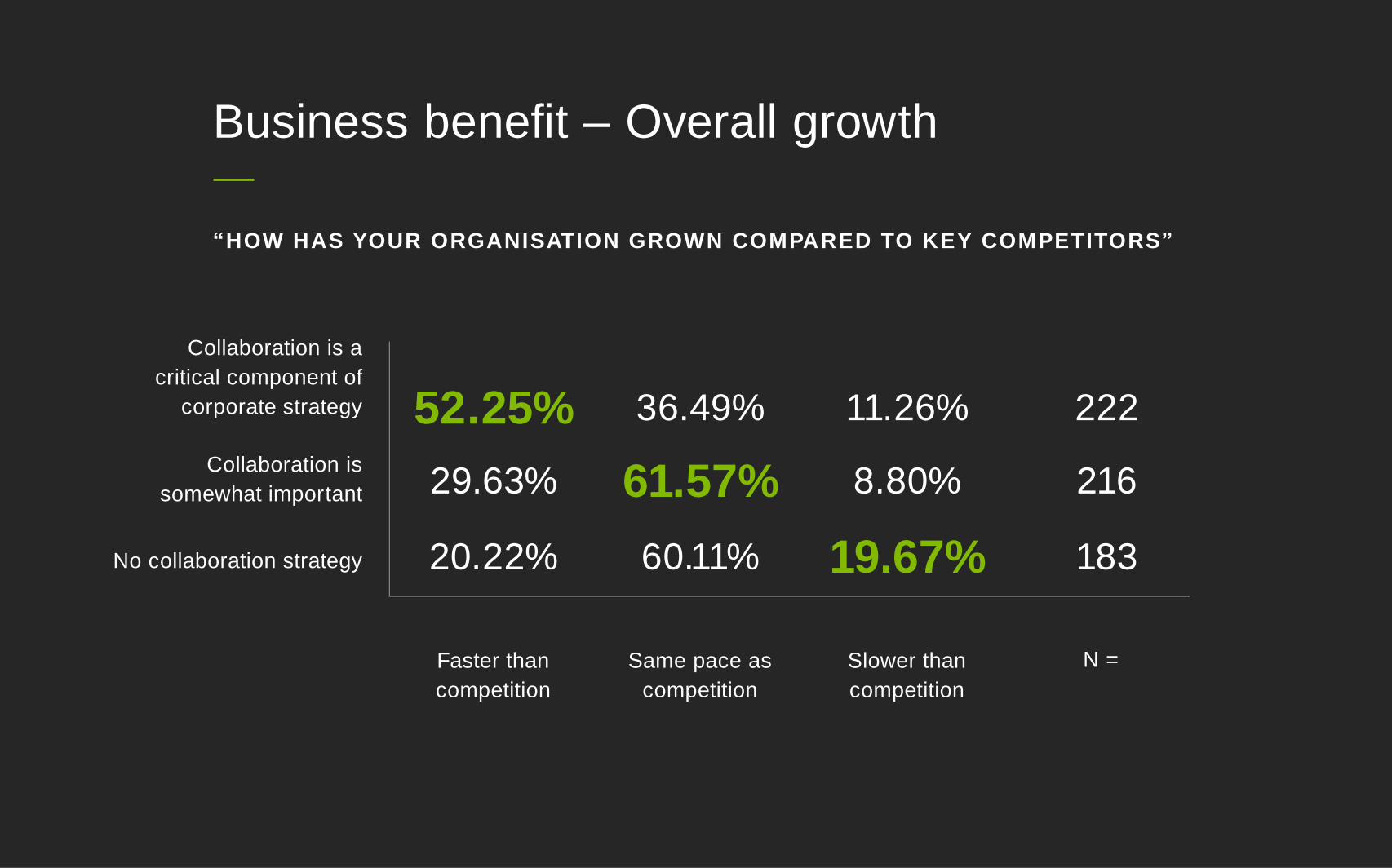

Collaboration is a

critical component of

corporate strategy

Collaboration is

somewhat important

No collaboration strategy

Faster than

competition

Same pace as

competition

52.25% 36.49% 11.26% 222

29.63% 61.57% 8.80% 216

20.22% 60.11% 19.67% 183

Slower than

competition

N =

“HOW HAS YOUR ORGANISATION GROWN COMPARED TO KEY COMPETITORS”

Business benefit – Overall growth

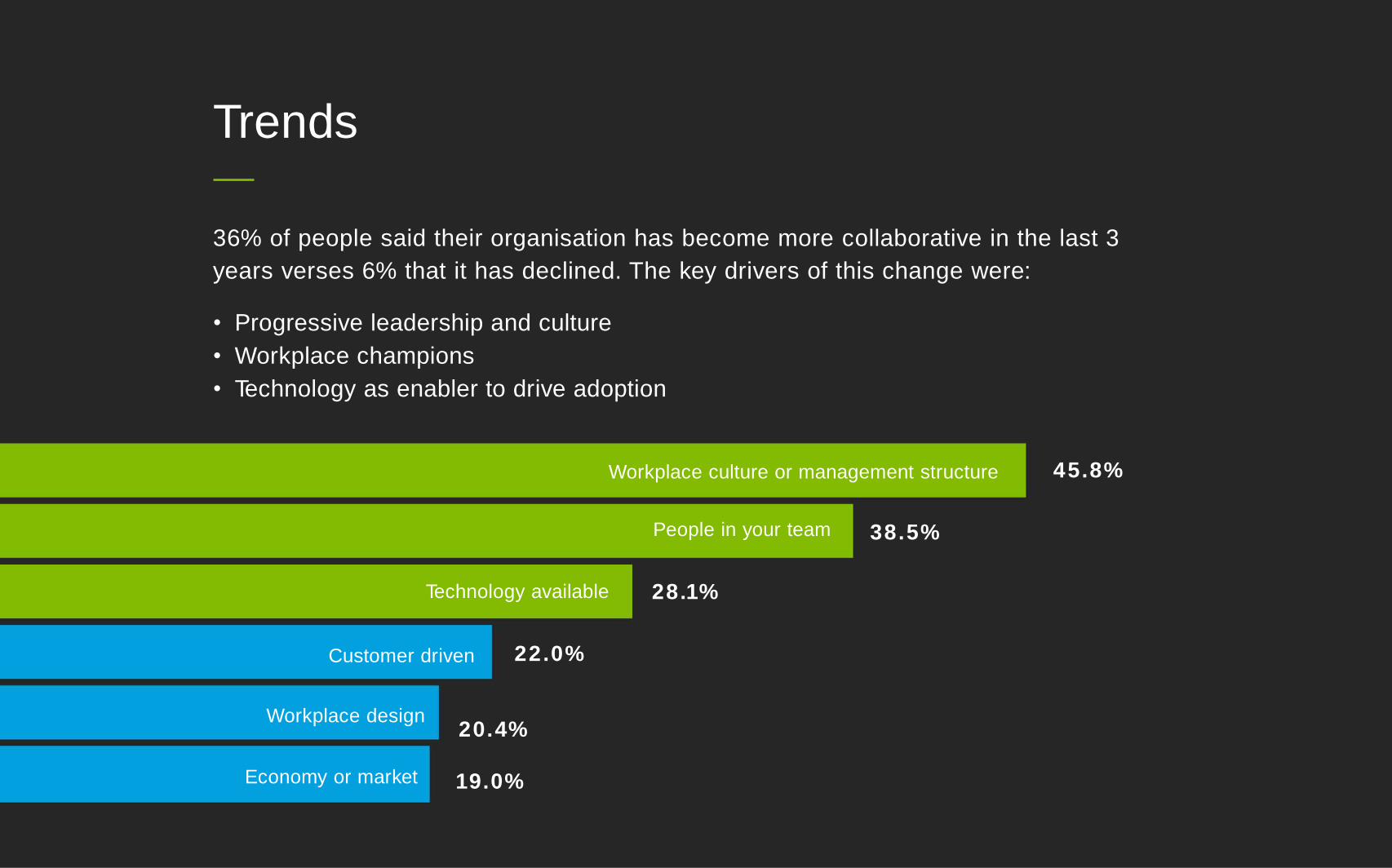

36% of people said their organisation has become more collaborative in the last 3

years verses 6% that it has declined. The key drivers of this change were:

• Progressive leadership and culture

• Workplace champions

• Technology as enabler to drive adoption

45.8%Workplace culture or management structure

People in your team

Technology available

Customer driven

Workplace design

Economy or market

38.5%

28.1%

22.0%

20.4%

19.0%

Trends

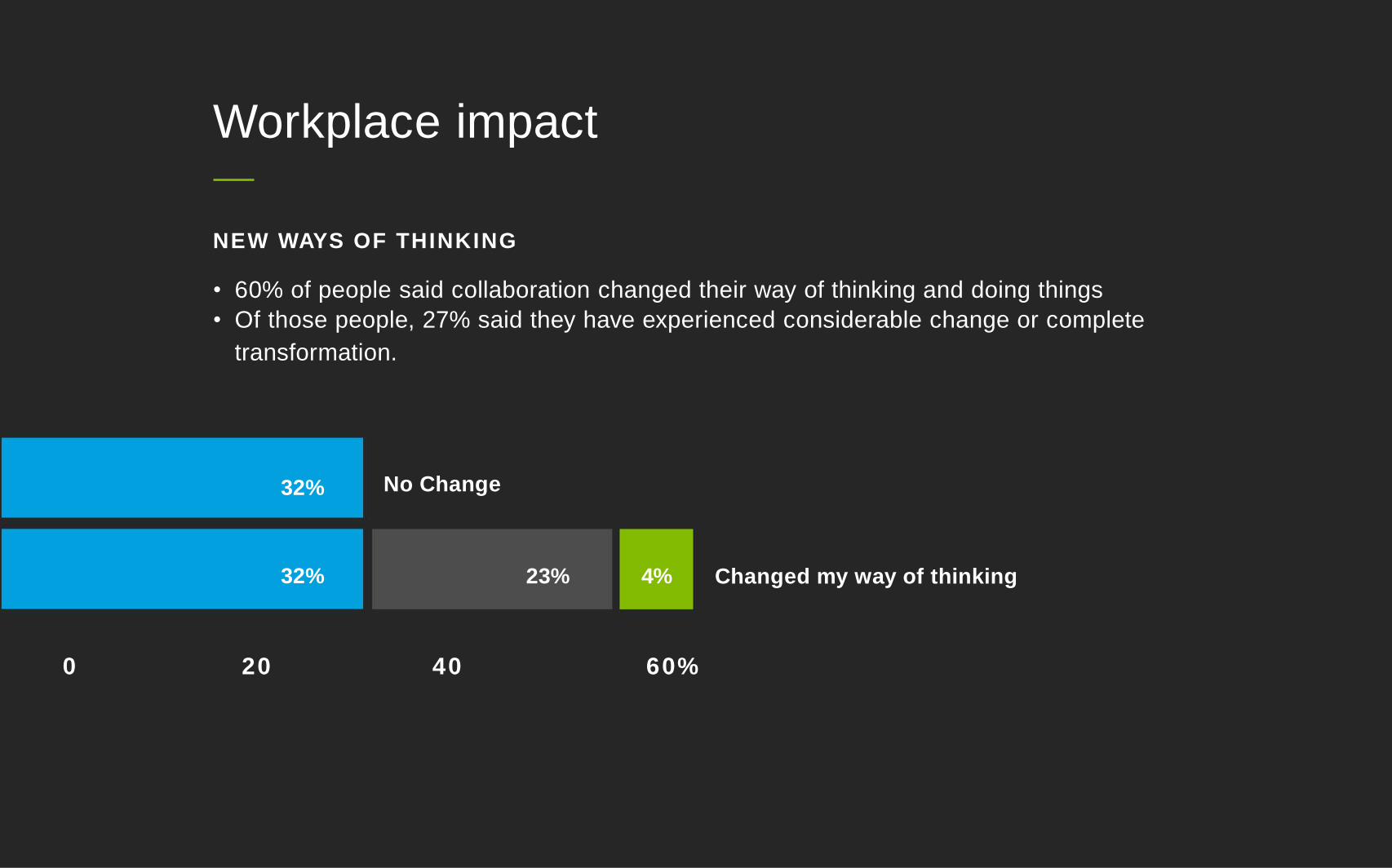

No Change

20 40 60%0

Changed my way of thinking

32%

32% 23% 4%

NEW WAYS OF THINKING

• 60% of people said collaboration changed their way of thinking and doing things

• Of those people, 27% said they have experienced considerable change or complete

transformation.

Workplace impact

Know your

customer

01

Invest in

mobile, social,

data and cloud

02

Enable a

digital culture

03

Drive

continuous

improvement

04

Next steps for businesses

Recommended