Narrow-scope amendments to Section

3856 Financial Instruments

June 7, 2017

The views expressed in this presentation are those of the presenter, not necessarily those of the Accounting Standards Board.

Background

• November 2014 – the AcSB launched a Post-implementation Review (PIR) of Section 3856 Financial Instruments

• The PIR was designed to allow the AcSB to assess:

– if the Section provides useful information;

– whether there are unexpected costs of applying the

Section; and

– whether there are areas of the Section that should be

changed.

Background - continued

• During the PIR, the AcSB talked to:

– 86 practitioners

– 21 financial statement users

– 2 financial statement preparers; and

– 1 academic

• A copy of the AcSB’s feedback statement on the

PIR is available here.

Background - continued

• The Board reviewed topics identified by respondents to the PIR and assessed whether they had merit of being added to its project plan

• As part of this process, the Board:

– Prioritized some narrow-scope issues and included

them in this project;

– Identified other larger projects that will be

considered in the context of its broader agenda.

Topics included in this project

• The following topics have been included in this

project:

– initial recognition of related party financial instruments;

– measurement of related party compound financial

instruments;

– classification of impairment and forgiveness of related party

loans;

– scope of accounting for modifications and extinguishments of

related party financial liabilities; and

– financial instrument disclosure (excluded from this

discussion)

The Board’s current thinking

• The Board is reviewing and evaluating different

alternatives to address the topics included in this

project

• The proposed alternatives included in this

presentation are preliminary and may change as

the result of additional outreach or the AcSB’s

due process activities

Purpose of this meeting

Obtain feedback regarding some of the alternatives being explored by the AcSB to address the narrow-scope issues included in this project, including:

– Any comments you may have on the alternatives discussed; and

– Your views on the effects of the alternatives being explored.

Topic #1 – Scope of accounting for

related party financial instruments

What we heard from respondents:

Confused as to whether related party financial instruments are in the scope of Section 3856 or Section 3840 after initial recognition

8

Topic #1 – Scope of accounting for related

party financial instruments (cont’d)

The AcSB heard the following from additional practitioner outreach:

This issue is more than just a navigation issue

- Entities struggle to apply the concepts in Section

3840 (carrying amount and exchange amount) to

financial instruments

Why?

The theoretical starting point for the standards is in

conflict

9

Topic #1 – Scope of accounting for related

party financial instruments (cont’d)

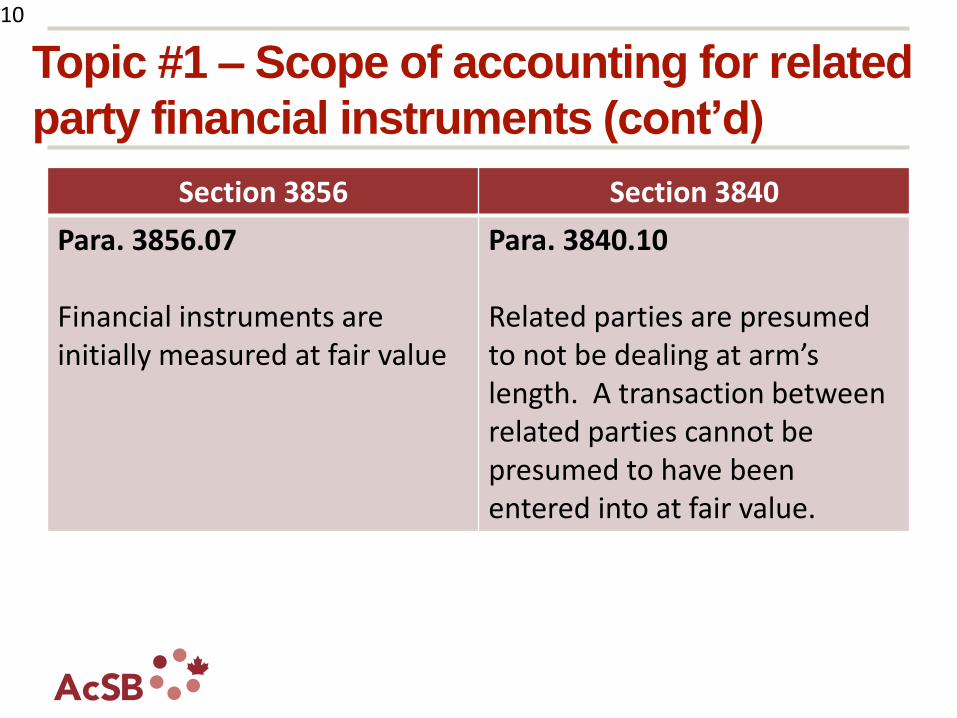

Section 3856 Section 3840

Para. 3856.07

Financial instruments are initially measured at fair value

Para. 3840.10

Related parties are presumed to not be dealing at arm’s length. A transaction between related parties cannot be presumed to have been entered into at fair value.

10

Topic #1 – Scope of accounting for related

party financial instruments (cont’d)

Potential alternative being considered

• Include initial measurement guidance for related party

financial instruments in Section 3856

• Related party financial instruments would be initially

measured at the:

– undiscounted cash flow(s) of the instrument (excluding interest and

dividend payments);

– cost of the instrument (if it does not have contractual cash flows); or

11

Topic #1 – Scope of accounting for related

party financial instruments (cont’d)

Potential alternative being considered (cont’d)

– fair value (if the entity is required or intends to re-

measure the instrument at fair value after initial

recognition)

12

Topic #1 – Scope of accounting for related

party financial instruments (cont’d)

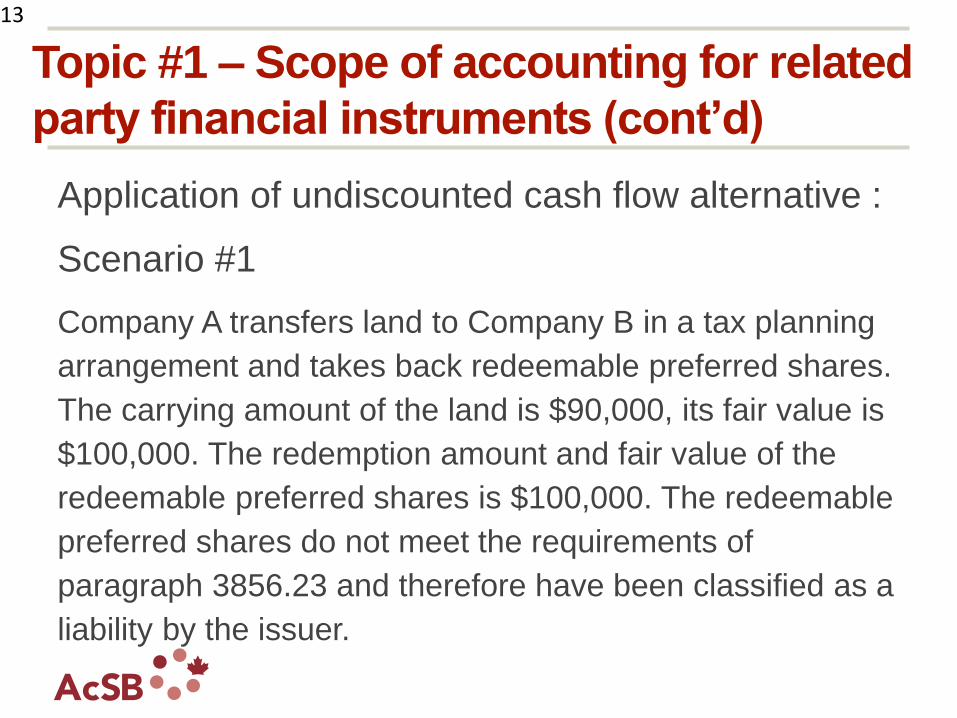

Application of undiscounted cash flow alternative :

Scenario #1

Company A transfers land to Company B in a tax planning

arrangement and takes back redeemable preferred shares.

The carrying amount of the land is $90,000, its fair value is

$100,000. The redemption amount and fair value of the

redeemable preferred shares is $100,000. The redeemable

preferred shares do not meet the requirements of

paragraph 3856.23 and therefore have been classified as a

liability by the issuer.

13

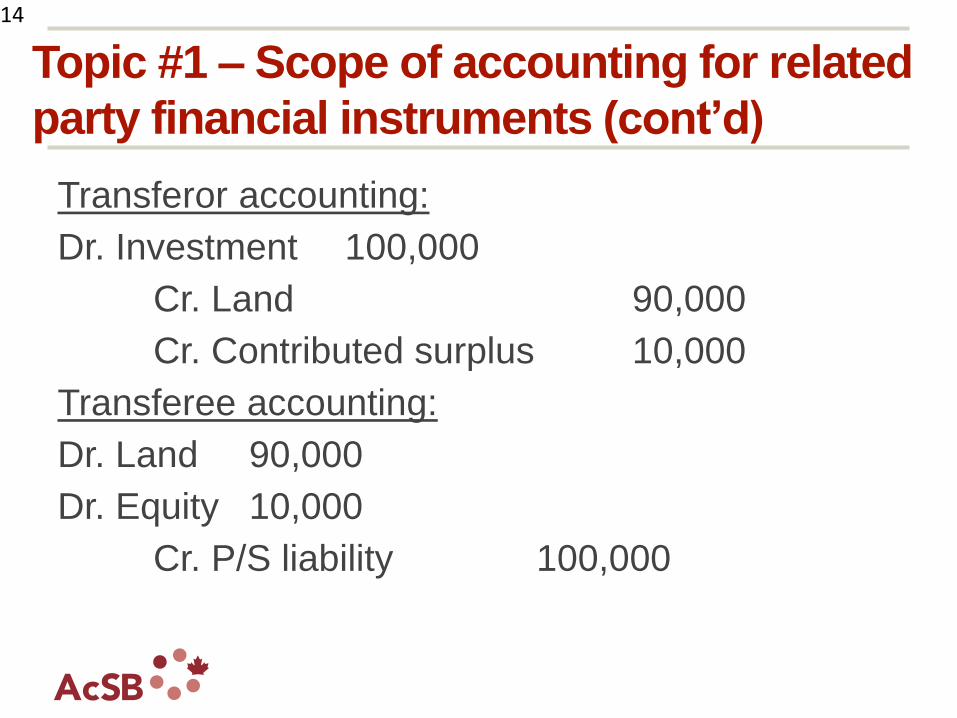

Topic #1 – Scope of accounting for related

party financial instruments (cont’d)

Transferor accounting:

Dr. Investment 100,000

Cr. Land 90,000

Cr. Contributed surplus 10,000

Transferee accounting:

Dr. Land 90,000

Dr. Equity 10,000

Cr. P/S liability 100,000

14

Topic #1 – Scope of accounting for related

party financial instruments (cont’d)

Application of cost alternative:

Scenario #2

Company A transfers land to Company B and

takes back common shares (Company B is not

publicly traded). The carrying amount of the land

is $90,000, its fair value is $100,000.

15

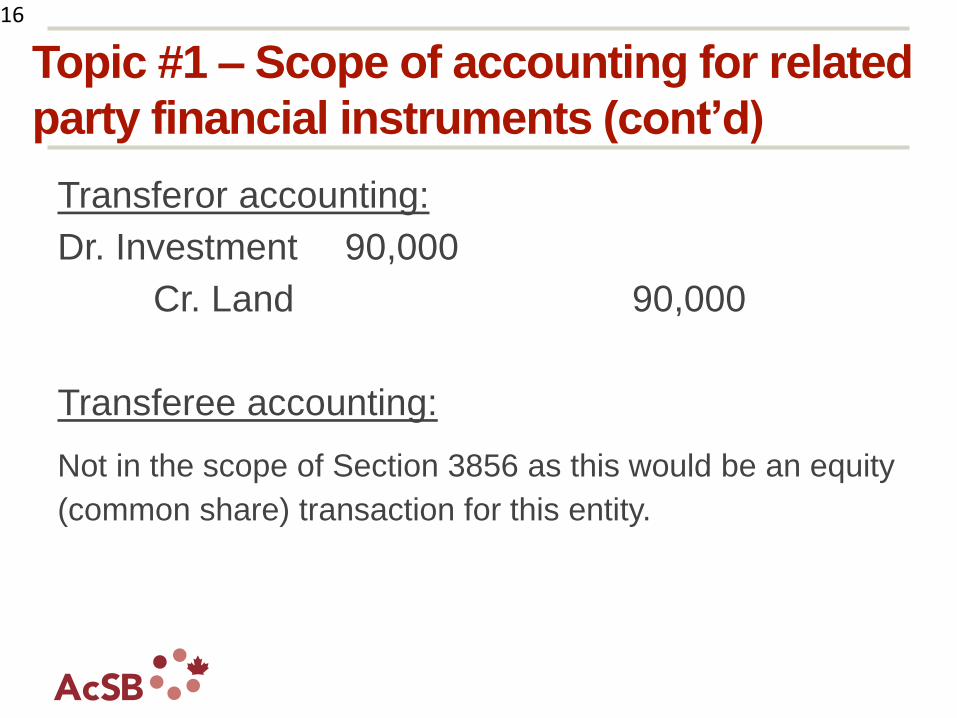

Topic #1 – Scope of accounting for related

party financial instruments (cont’d)

Transferor accounting:

Dr. Investment 90,000

Cr. Land 90,000

Transferee accounting:

Not in the scope of Section 3856 as this would be an equity

(common share) transaction for this entity.

16

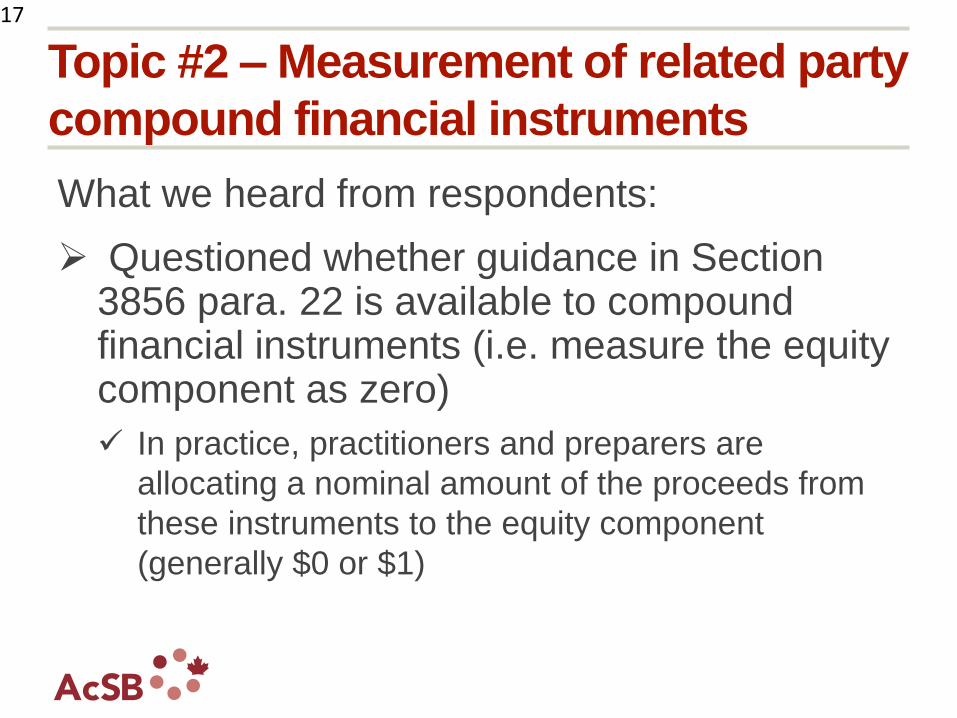

Topic #2 – Measurement of related party

compound financial instruments

What we heard from respondents:

Questioned whether guidance in Section 3856 para. 22 is available to compound financial instruments (i.e. measure the equity component as zero)

In practice, practitioners and preparers are

allocating a nominal amount of the proceeds from

these instruments to the equity component

(generally $0 or $1)

17

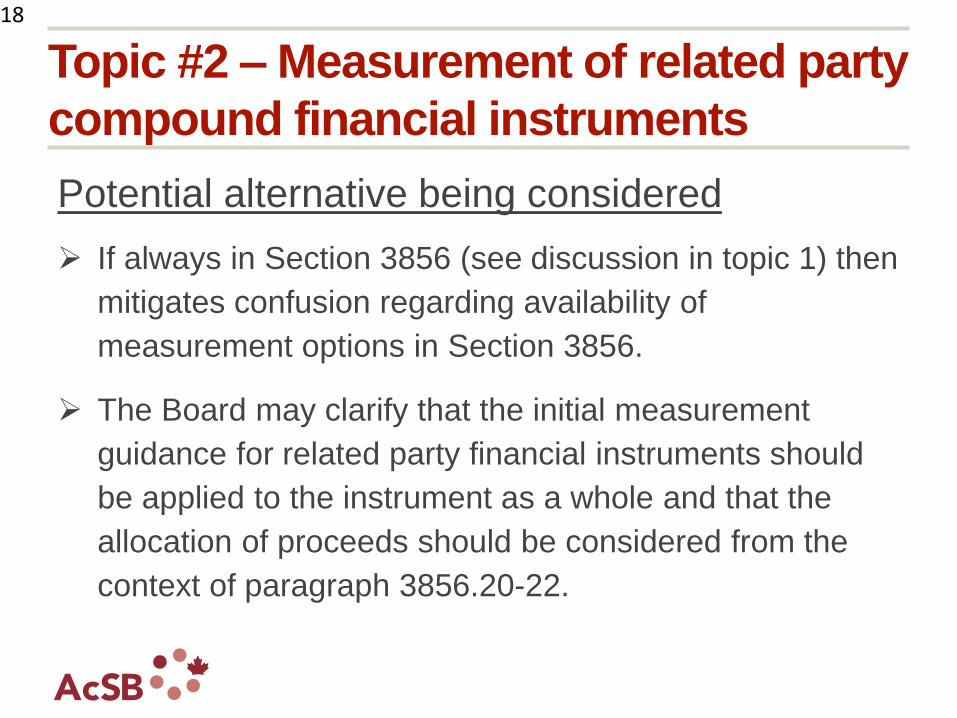

Topic #2 – Measurement of related party

compound financial instruments

Potential alternative being considered

If always in Section 3856 (see discussion in topic 1) then

mitigates confusion regarding availability of

measurement options in Section 3856.

The Board may clarify that the initial measurement

guidance for related party financial instruments should

be applied to the instrument as a whole and that the

allocation of proceeds should be considered from the

context of paragraph 3856.20-22.

18

Topic #3 – Classification of impairment

and forgiveness of related party loans

What the AcSB heard from respondents:

Accounting for the impairment and / or forgiveness of a related party loan is unclear

Should the impairment of a related party loan be

recorded in equity?

Should both the impairment and subsequent

forgiveness be accounted for together through

income or through equity?

Topic #3 – Classification of impairment

and forgiveness of related party loans

Key observations from lender users consulted:

Primarily concerned with “leakage”

Once the money has left the entity, the related party

loan has no value unless it is secured;

Generally have protective rights that would restrict

management from removing capital or assets from

the entity.

Users were less concerned with the nature of the

relationship (i.e. management or shareholder) and

more concerned with the original transaction.

20

Topic #3 – Classification of impairment

and forgiveness of related party loans

Key observations from lender users consulted (cont’d):

If the original transaction was in the normal course

of operations the impairment and forgiveness

should be recognized through profit or loss;

If not, it should be recognized through equity.

21

Topic #3 – Classification of impairment

and forgiveness of related party loans

Key observations from practitioners consulted:

In practice related party accounts often include a

mixture of transactions (normal course and not

normal course) and that it would be impracticable to

determine the nature of cash flows within these

accounts.

22

Topic #3 – Classification of impairment

and forgiveness of related party loans

Potential alternatives being considered

a) Clarify that the impairment indicators in para.

3856.A15 are not exclusive to third party financial

assets;

b) Clarify that impairments, are recognized in income

as indicators arise;

23

Topic #3 – Classification of impairment

and forgiveness of related party loans

c) Add guidance that the forgiveness of related party

financial assets should be recognized in:

• Income, if the original transaction that brought rise to

the asset was in the normal course of operations; or

• Equity if:

– The original transaction that brought rise to the asset was

not in the normal course of operations; or

– It is impracticable to determine whether the amount

forgiven originated in the normal or non-normal course of

operations.

24

Topic #3 – Classification of impairment

and forgiveness of related party loans

Forgiveness of loans with an individual that is acting solely in capacity of senior management (i.e. is not also a shareholder) is compensation and should be recognized in income.

25

Topic #4 – Scope of accounting for modifications

and extinguishments of related party loans

Key observations from practitioners consulted:

ASPE preparers struggle to apply the 10% test (for both

related and third party modifications)

Modification of related party loans is often done for tax

purposes (similar to forgiveness);

Para. 3856.28 requires the difference between the

carrying amount of the FL and consideration paid to be

recognized in accordance with Section 3840.

26

Topic #4 – Scope of accounting for modifications

and extinguishments of related party loans

Potential alternative being considered

• All modifications or related party financial liabilities

are accounted for as an extinguishment with the

new instrument measured in accordance with the

initial measurement guidance alternative explored in

Topic #1.

27

For more information, visit www.frascanada.ca

Contacts

Andrew White, CPA, CA Kelly Khalilieh, CPA, CA

Principal, AcSB Senior Principal, AcSB

Phone: +1 (416) 204-3487 +1 (416) 204-3453

Email: [email protected] [email protected]

June 7, 2017

Recommended

![[3856] – 105 - unipune.ac.in · [3856] – 105 First Year B.Pharm ... Neat diagrams must be drawn wherever necessary. SECTION – I 1. Attempt any one: 10 ... Hammer Mill e) Define](https://img.pdfslide.us/doc/110x75/5b1d3d5e7f8b9a8e158b4823/3856-105-3856-105-first-year-bpharm-neat-diagrams-must-be.jpg)