CTC AND OTHER POINTS NEEDS TO BE KEPT

26th May, 2018,SaturdayMondeal Heights, Iscon Circle, Ahmedabad

CA Nitin PathakF.C.A ,CISA, CISM,CIA, CISSP(USA)DISA(ICAI) ,DIRM(ICAI) ,SAP(FICO) Certification course on International taxation( ICAI) Certification course on IFRS ( ICAI)

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

We are going to deliberate on CTC , what is simple tax option available, what needs to be taken while submitting the papers to CA/Tax consultant

New forms What is the importance of submitting the

details and consequences for not filing the same

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

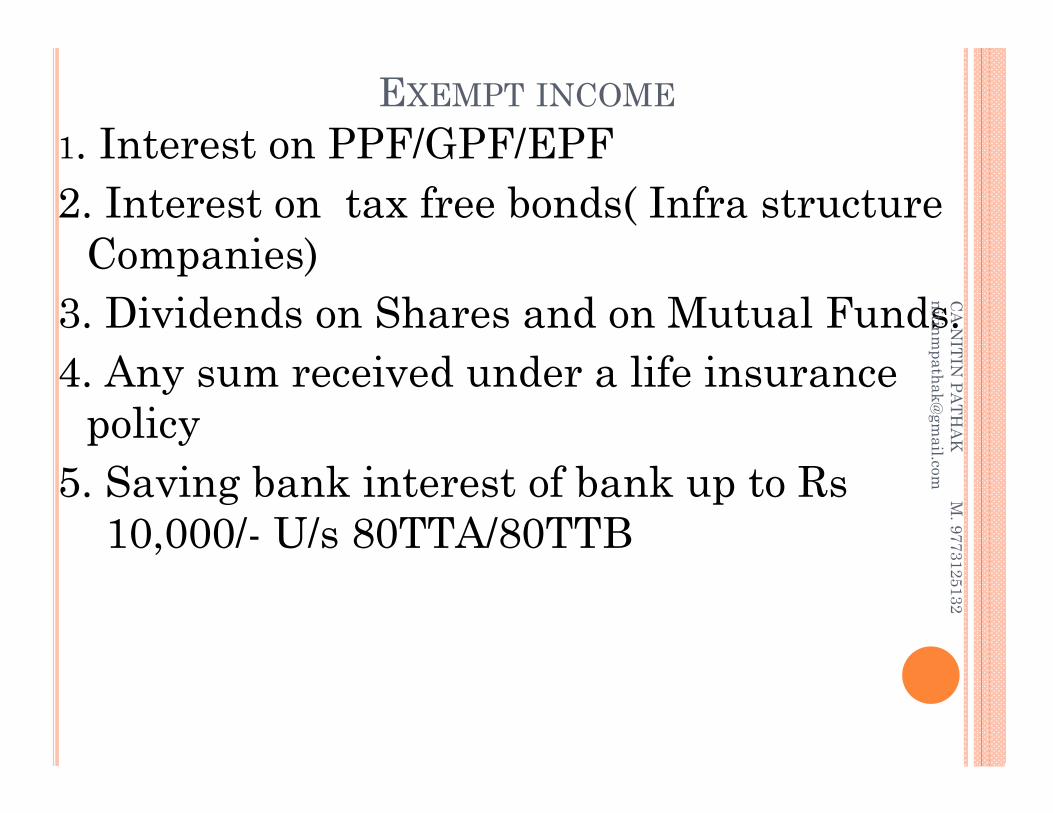

EXEMPT INCOME1. Interest on PPF/GPF/EPF2. Interest on tax free bonds( Infra structure

Companies)3. Dividends on Shares and on Mutual Funds.4. Any sum received under a life insurance

policy 5. Saving bank interest of bank up to Rs

10,000/- U/s 80TTA/80TTB

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

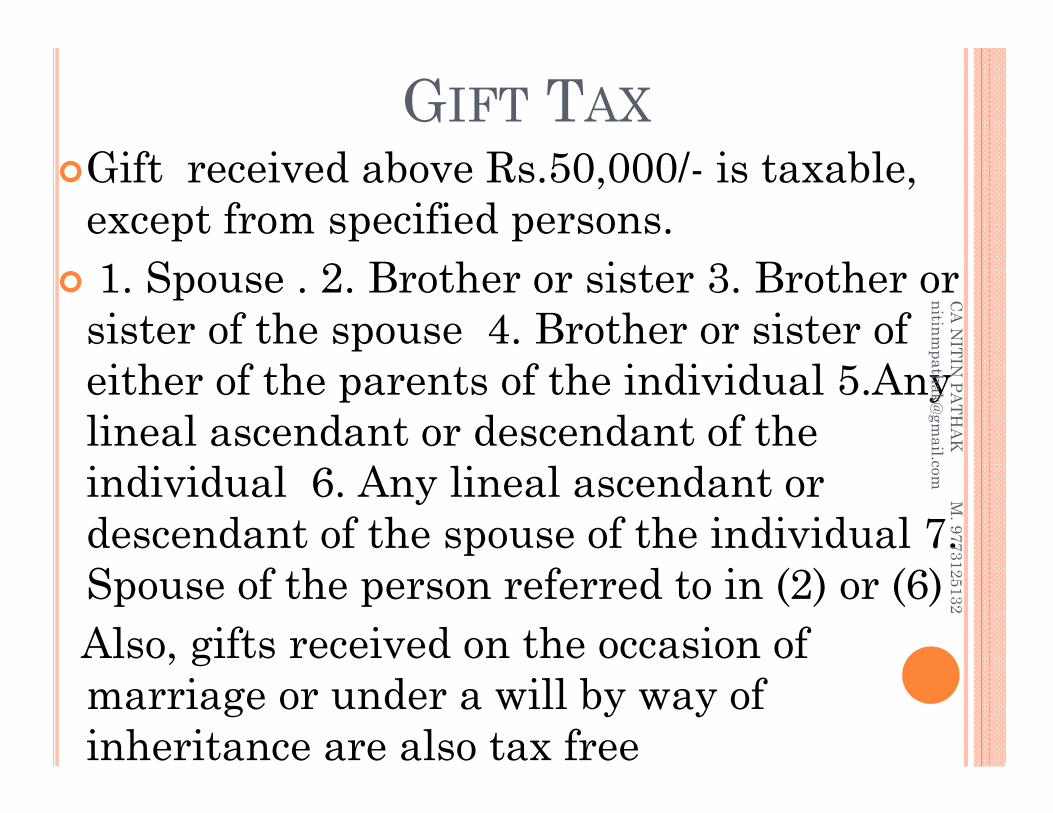

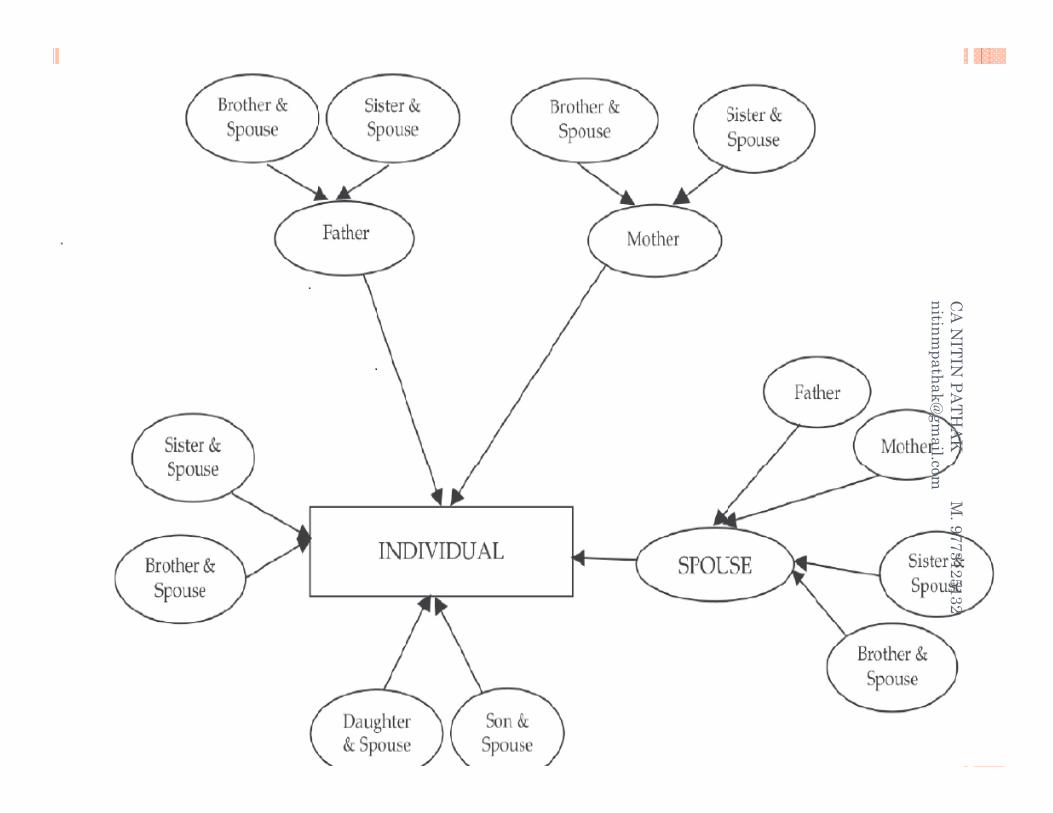

GIFT TAXGift received above Rs.50,000/- is taxable,

except from specified persons. 1. Spouse . 2. Brother or sister 3. Brother or

sister of the spouse 4. Brother or sister of either of the parents of the individual 5.Any lineal ascendant or descendant of the individual 6. Any lineal ascendant or descendant of the spouse of the individual 7. Spouse of the person referred to in (2) or (6) Also, gifts received on the occasion of marriage or under a will by way of inheritance are also tax free

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

Tax Planning

Filling income tax return of wife, sons, daughters, etc.Creating HUF/Company/Firm/LLPInvest Income flow in such a manner

that creates minimum tax liabilityTransferring the fund

directly/indirectly in the name of spouse, daughter-in-law or minor child will lead to deem income in the hand of transferor

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

NATIONAL PENSION SCHEME(NPS)NPS keep contributing till the age of 65 yearsDeduction to NPS Scheme for contribution by

individual u/s 80CCD(1) :Salaried employee 10% of his salary;Non salaried employee 20 % of his GTIDeduction towards NPS scheme for

contribution made by the employer u/s 80CCD(2)(No deduction in excess of 10% of salary)

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

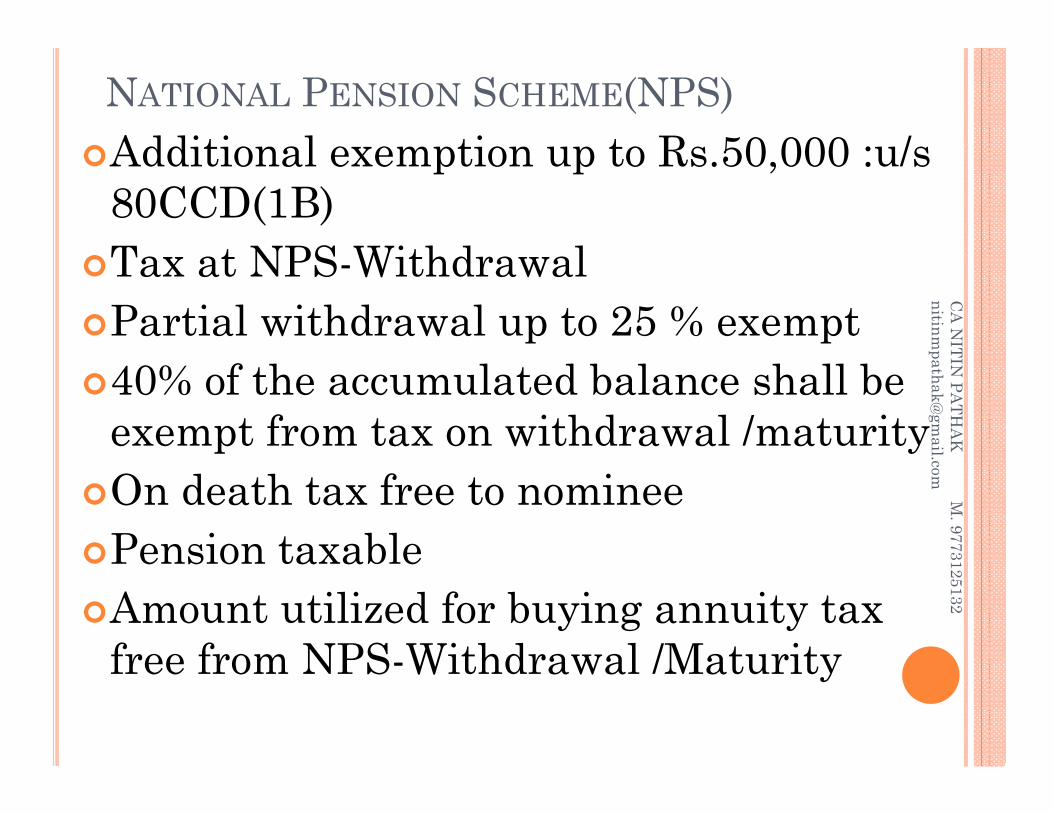

NATIONAL PENSION SCHEME(NPS)Additional exemption up to Rs.50,000 :u/s

80CCD(1B)Tax at NPS-WithdrawalPartial withdrawal up to 25 % exempt40% of the accumulated balance shall be

exempt from tax on withdrawal /maturityOn death tax free to nomineePension taxableAmount utilized for buying annuity tax

free from NPS-Withdrawal /Maturity

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

COMPUTATION OF GROSS TAXABLE INCOME

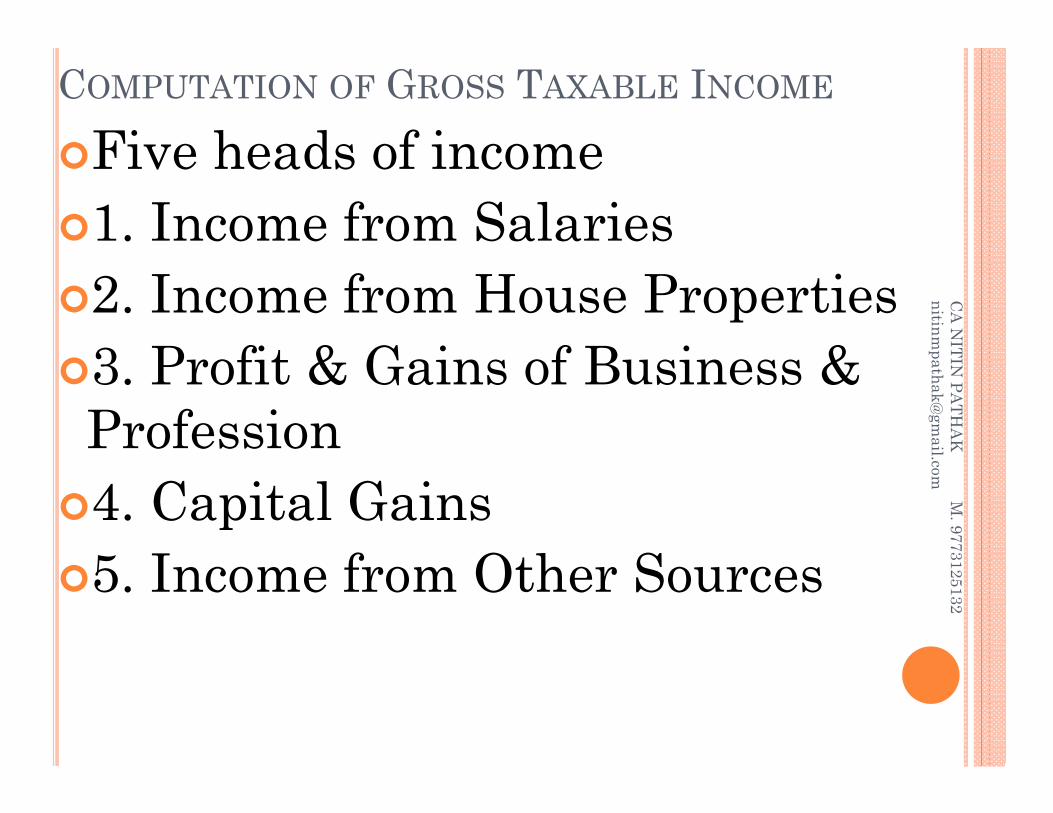

Five heads of income1. Income from Salaries2. Income from House Properties3. Profit & Gains of Business & Profession4. Capital Gains5. Income from Other Sources

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

INCOME FROM HOUSE PROPERTY

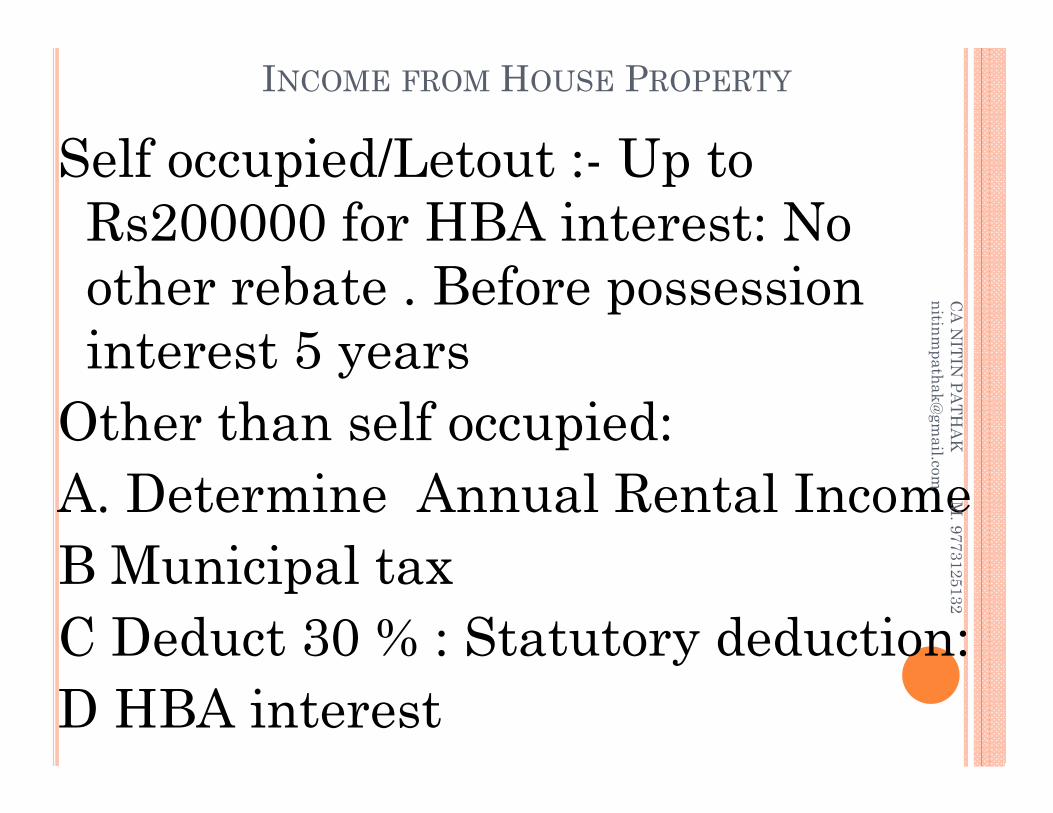

Self occupied/Letout :- Up to Rs200000 for HBA interest: No other rebate . Before possession interest 5 years

Other than self occupied:A. Determine Annual Rental IncomeB Municipal taxC Deduct 30 % : Statutory deduction:D HBA interest

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

PROFIT FROM BUSINESS / PROFESSION

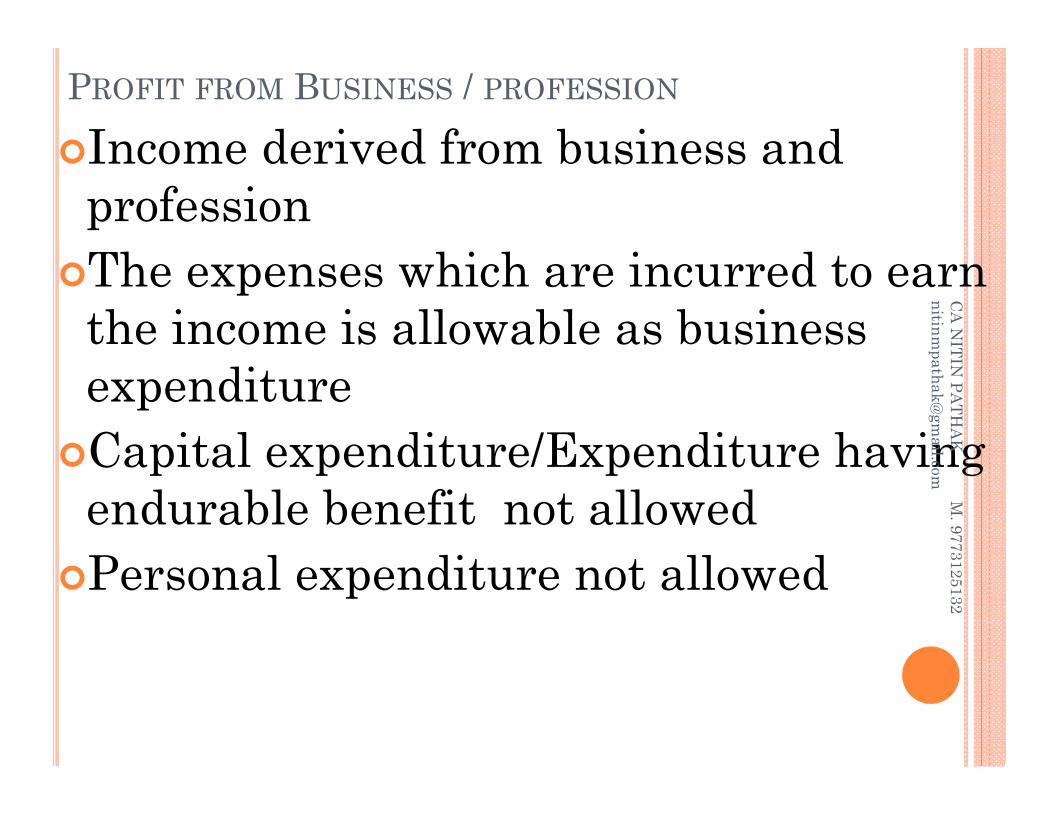

Income derived from business and professionThe expenses which are incurred to earn

the income is allowable as business expenditureCapital expenditure/Expenditure having

endurable benefit not allowedPersonal expenditure not allowed

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

INCOME FROM OTHER SOURCES

Interest Income:Company depositsDebentures/bondsSavings / Fixed deposits with banksPost office savings schemes like MIS, NSC, Time Deposit etc.Private loans given to relatives, friends or any other entity.Government securities.

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

15G AND 15H

The above form one can not submit if income of the assessee is higher than basic exemption limit.

If you still submit the form you are liable for penal action

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

CAPITAL GAINS

Any sale of a personal asset( Certain assets exempt), capital gain is taxable between sale price and purchase priceCapital gain tax is a levy on sale of

immovable property, FMV, Shares & Mutual funds, etc.Certain deduction is available to reduce

tax liability.Base Year of indexation for Immovable

property is change to 01/04/2001.

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

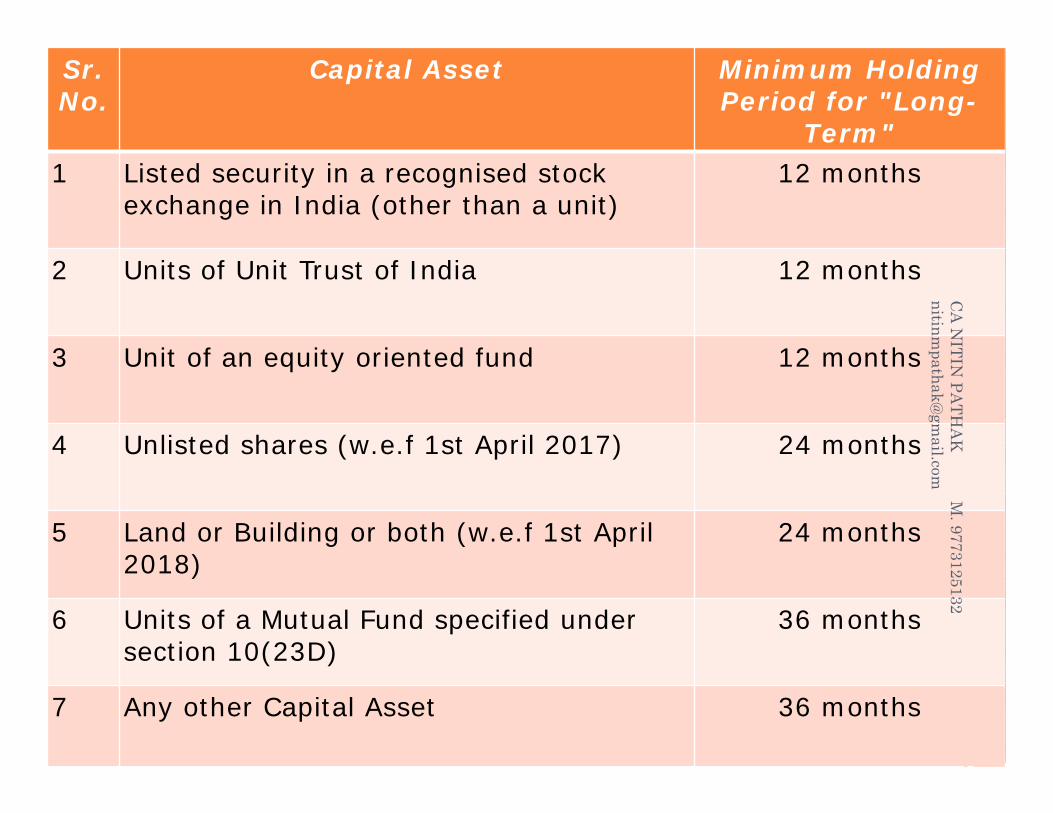

Sr. No.

Capital Asset Minimum Holding Period for "Long-

Term"1 Listed security in a recognised stock

exchange in India (other than a unit)12 months

2 Units of Unit Trust of India 12 months

3 Unit of an equity oriented fund 12 months

4 Unlisted shares (w.e.f 1st April 2017) 24 months

5 Land or Building or both (w.e.f 1st April 2018)

24 months

6 Units of a Mutual Fund specified under section 10(23D)

36 months

7 Any other Capital Asset 36 months

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

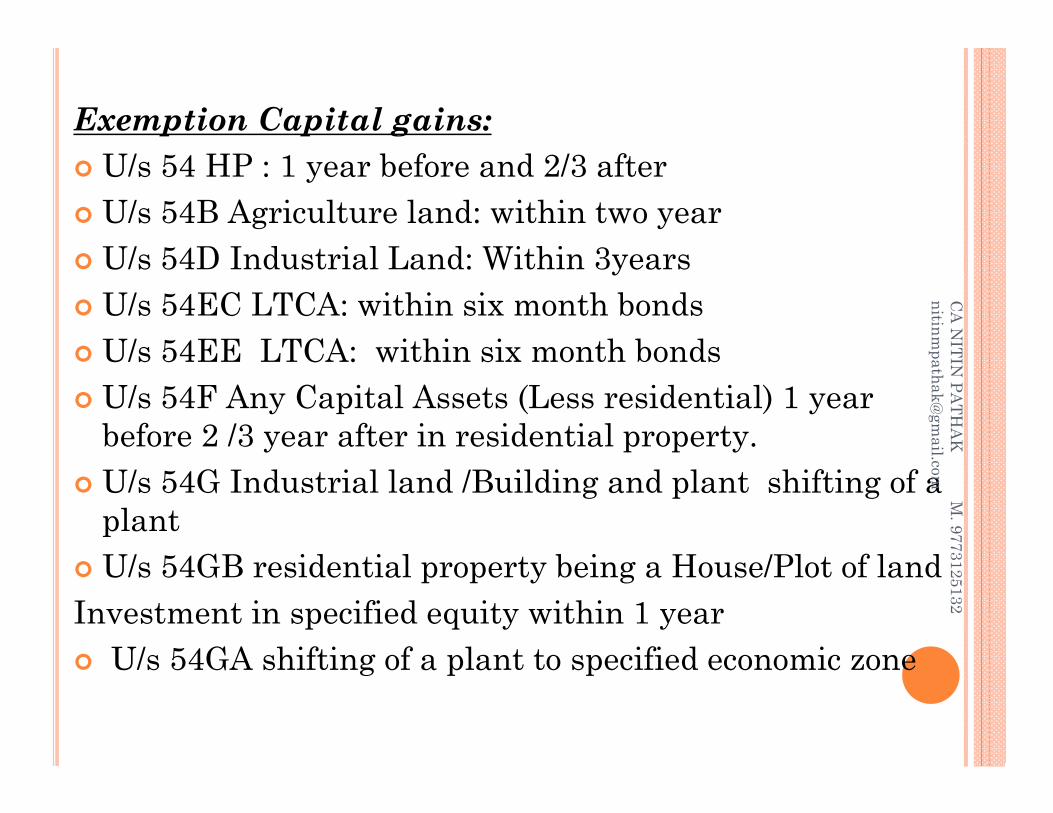

Exemption Capital gains: U/s 54 HP : 1 year before and 2/3 after U/s 54B Agriculture land: within two year U/s 54D Industrial Land: Within 3years U/s 54EC LTCA: within six month bonds U/s 54EE LTCA: within six month bonds U/s 54F Any Capital Assets (Less residential) 1 year

before 2 /3 year after in residential property. U/s 54G Industrial land /Building and plant shifting of a

plant U/s 54GB residential property being a House/Plot of land Investment in specified equity within 1 year U/s 54GA shifting of a plant to specified economic zone

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

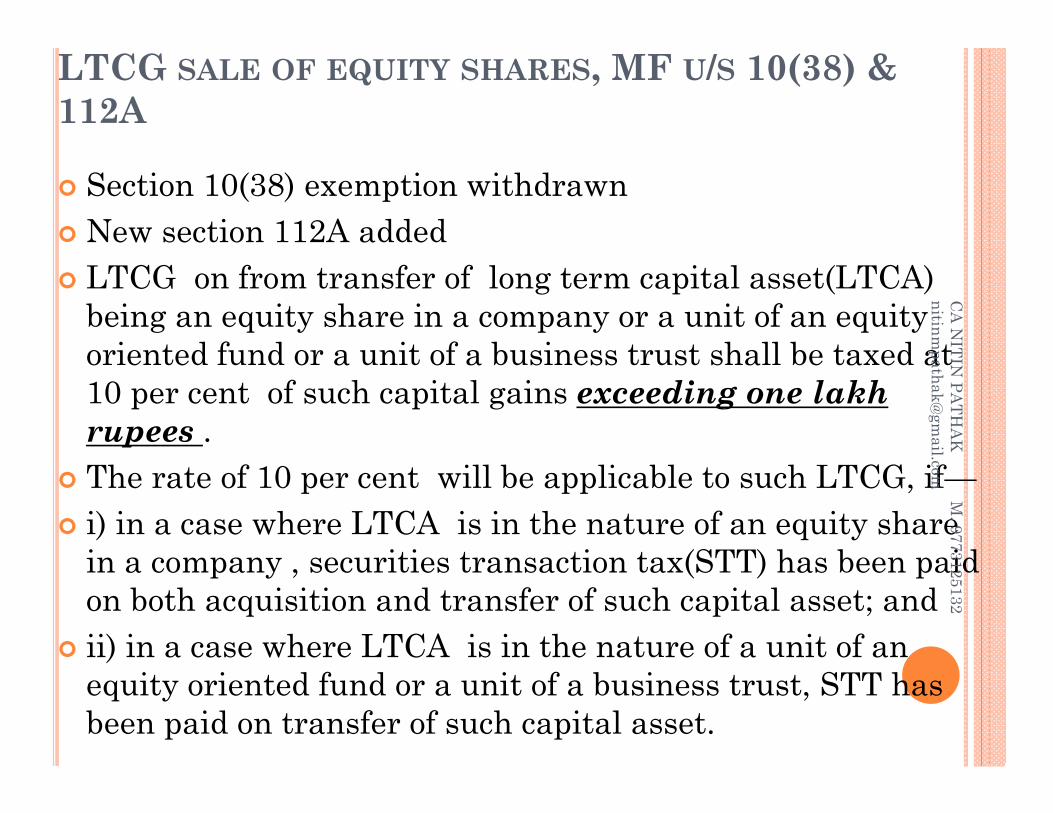

LTCG SALE OF EQUITY SHARES, MF U/S 10(38) & 112A

Section 10(38) exemption withdrawn New section 112A added LTCG on from transfer of long term capital asset(LTCA)

being an equity share in a company or a unit of an equity oriented fund or a unit of a business trust shall be taxed at 10 per cent of such capital gains exceeding one lakhrupees .

The rate of 10 per cent will be applicable to such LTCG, if— i) in a case where LTCA is in the nature of an equity share

in a company , securities transaction tax(STT) has been paid on both acquisition and transfer of such capital asset; and

ii) in a case where LTCA is in the nature of a unit of an equity oriented fund or a unit of a business trust, STT has been paid on transfer of such capital asset.

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

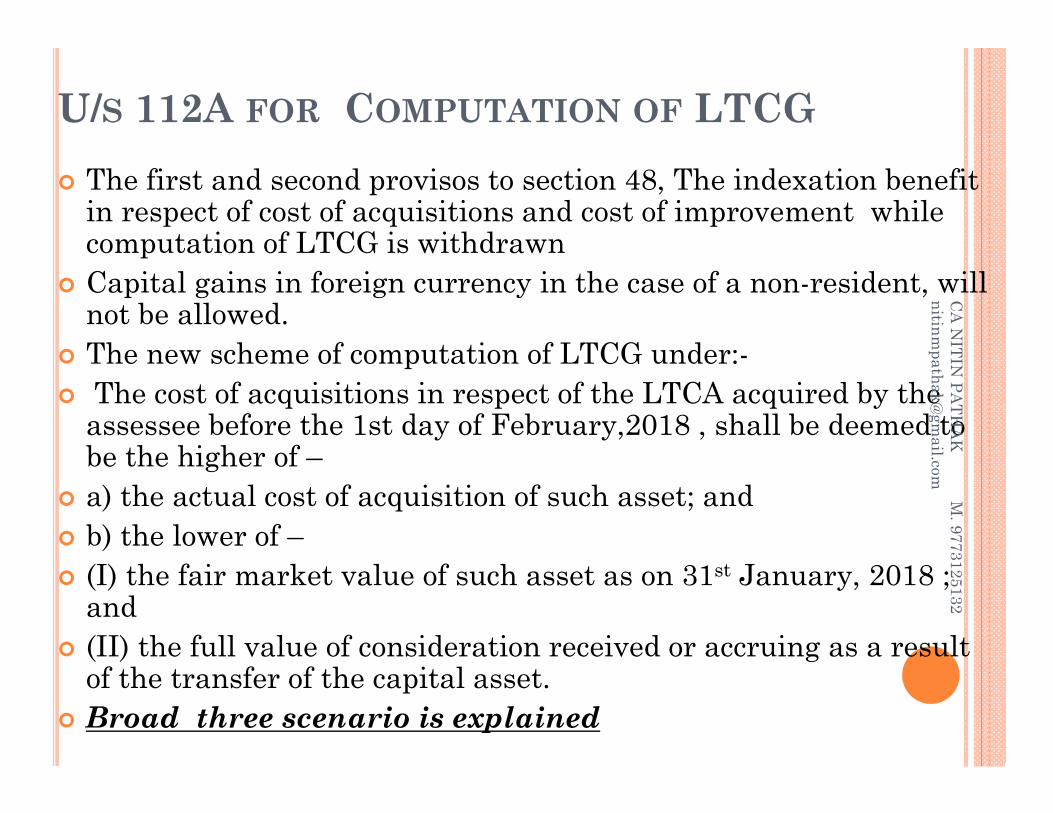

U/S 112A FOR COMPUTATION OF LTCG The first and second provisos to section 48, The indexation benefit

in respect of cost of acquisitions and cost of improvement while computation of LTCG is withdrawn

Capital gains in foreign currency in the case of a non-resident, will not be allowed.

The new scheme of computation of LTCG under:- The cost of acquisitions in respect of the LTCA acquired by the

assessee before the 1st day of February,2018 , shall be deemed to be the higher of –

a) the actual cost of acquisition of such asset; and b) the lower of – (I) the fair market value of such asset as on 31st January, 2018 ;

and (II) the full value of consideration received or accruing as a result

of the transfer of the capital asset. Broad three scenario is explained

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

FMV : FAIR MARKET VALUE(SHARES/UNITS OF MF)

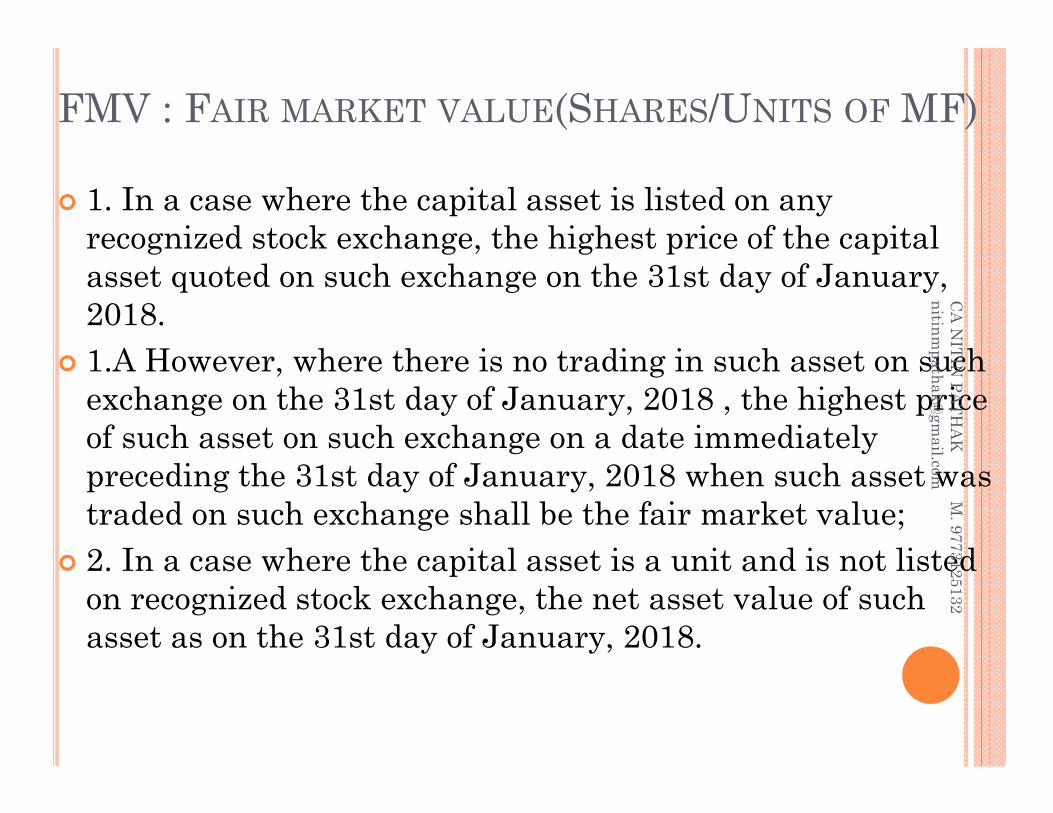

1. In a case where the capital asset is listed on any recognized stock exchange, the highest price of the capital asset quoted on such exchange on the 31st day of January, 2018.

1.A However, where there is no trading in such asset on such exchange on the 31st day of January, 2018 , the highest price of such asset on such exchange on a date immediately preceding the 31st day of January, 2018 when such asset was traded on such exchange shall be the fair market value;

2. In a case where the capital asset is a unit and is not listed on recognized stock exchange, the net asset value of such asset as on the 31st day of January, 2018.

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

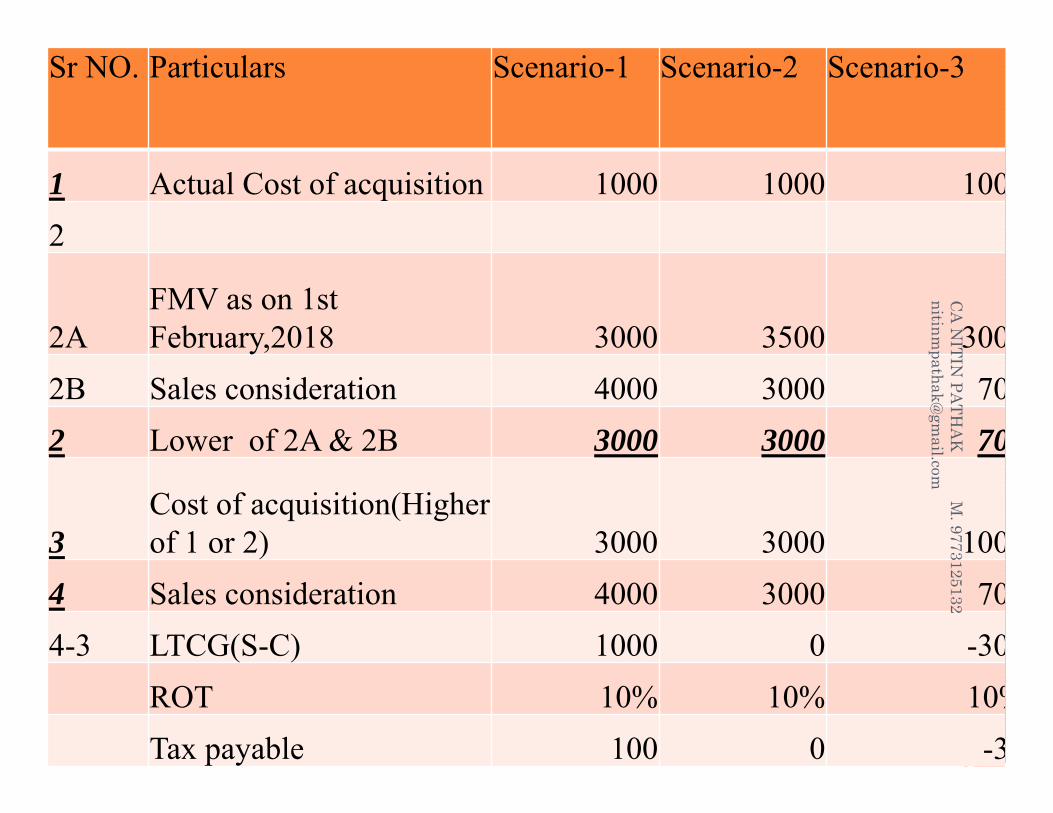

Sr NO. Particulars Scenario-1 Scenario-2 Scenario-3

1 Actual Cost of acquisition 1000 1000 1002

2AFMV as on 1st February,2018 3000 3500 300

2B Sales consideration 4000 3000 702 Lower of 2A & 2B 3000 3000 70

3Cost of acquisition(Higher of 1 or 2) 3000 3000 100

4 Sales consideration 4000 3000 704-3 LTCG(S-C) 1000 0 -30

ROT 10% 10% 10%Tax payable 100 0 -3

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

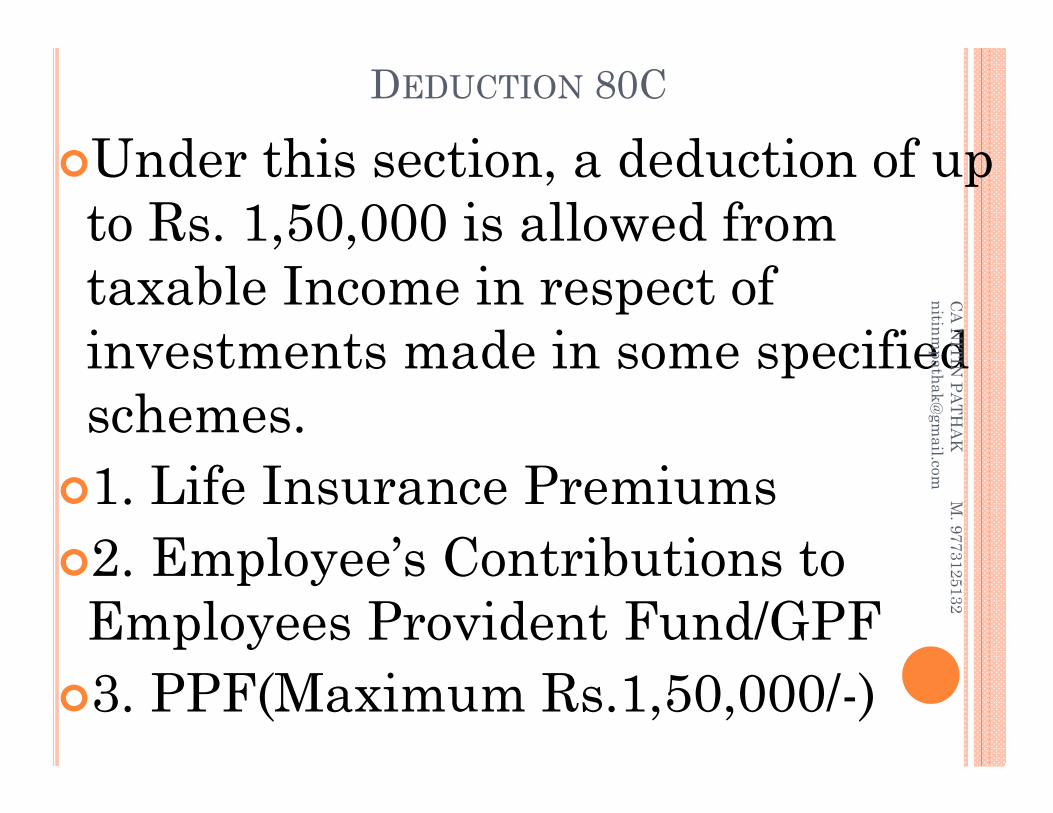

DEDUCTION 80C

Under this section, a deduction of up to Rs. 1,50,000 is allowed from taxable Income in respect of investments made in some specified schemes.1. Life Insurance Premiums2. Employee’s Contributions to Employees Provident Fund/GPF3. PPF(Maximum Rs.1,50,000/-)

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

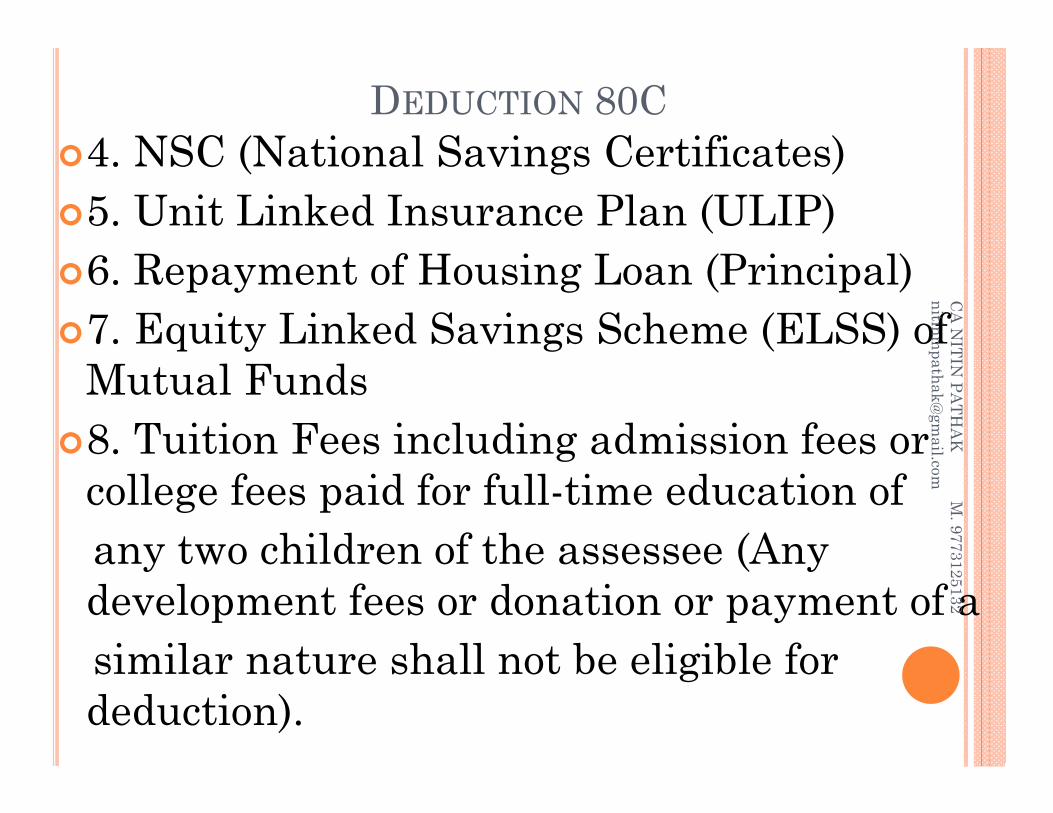

DEDUCTION 80C4. NSC (National Savings Certificates)5. Unit Linked Insurance Plan (ULIP)6. Repayment of Housing Loan (Principal)7. Equity Linked Savings Scheme (ELSS) of

Mutual Funds8. Tuition Fees including admission fees or

college fees paid for full-time education ofany two children of the assessee (Any development fees or donation or payment of asimilar nature shall not be eligible for deduction).

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

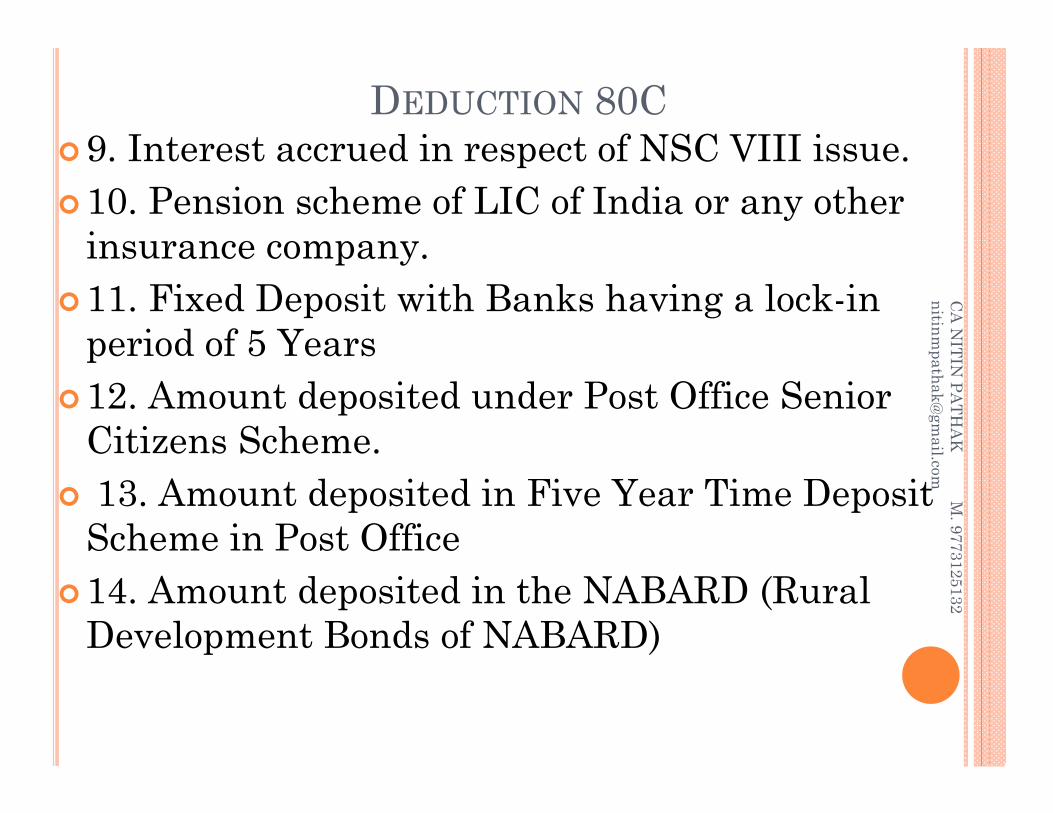

DEDUCTION 80C9. Interest accrued in respect of NSC VIII issue.10. Pension scheme of LIC of India or any other

insurance company.11. Fixed Deposit with Banks having a lock-in

period of 5 Years12. Amount deposited under Post Office Senior

Citizens Scheme. 13. Amount deposited in Five Year Time Deposit

Scheme in Post Office14. Amount deposited in the NABARD (Rural

Development Bonds of NABARD)

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

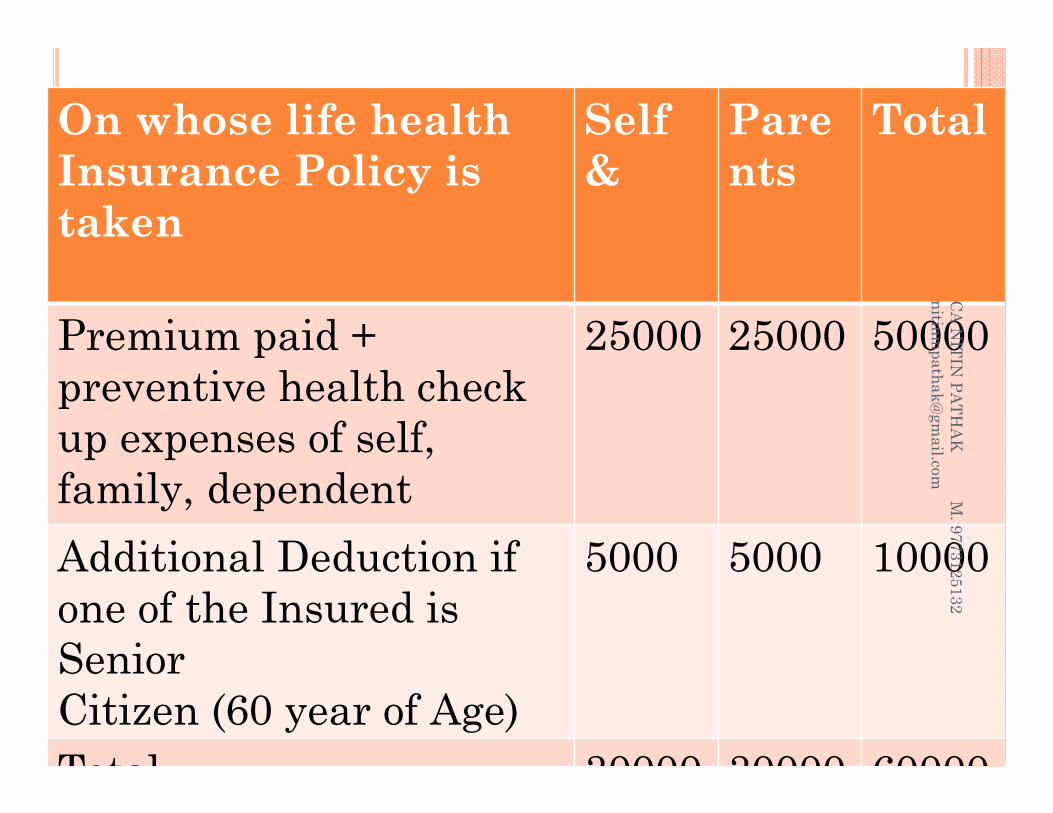

80DOn whose life healthInsurance Policy is taken

Self &

Parents

Total

Premium paid + preventive health check up expenses of self, family, dependent

25000 25000 50000

Additional Deduction if one of the Insured is SeniorCitizen (60 year of Age)

5000 5000 10000

Total 30000 30000 60000

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

U/S 15/17 SALARY INCOME. Salary is chargeable to tax on “due” or “receipt” basis whichever is earlier and includes wages, annuity or pension, gratuity, fees, commission, perquisites or profits in lieu of salary, advance salary, leave encashment, etc.

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

SECTION 17(3)/ PROFITS IN LIEUOF SALARYAny compensation from employer or former employer on termination or modification of the terms of employment.

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

SECTION 17(3)/ PROFITS IN LIEUOF SALARYAny receipt from Employer/former employer or from provident/other fund (other than gratuity, commuted pension, retrenchment compensation, house rent allowance, provident fund or such other funds) to extent not consisting of contributions by assessee/ interest on such contributions.

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

SECTION 17(3)/ PROFITS IN LIEUOF SALARYAny sum received under a Keyman insurance policy including the sum allocated by way of bonus on such policy.Any sum received before his joining any employment or after cessation of his employment.

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

PENSION [SECTION 10(10A)] Pension is taxable as salary Commuted value of pension is exempt: For Government employees, fully exempt For other employees, following is exempt —If employee has received gratuity then commuted value of 1/3rd of the pension which he is entitled to receive, andIn any other case, commuted value of 1/2 of the pension which he is entitled to receive.

Any payment in commutation of pension received from fund set up by LIC is exempt under section 10(23AAB)

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

GRATUITY [SECTION 10(10)] Death-cum-retirement gratuity received by the Government

employees or employees under Civil Services — wholly exempt from tax.

Employees covered by Payment of Gratuity Act.Amount received on termination, after continuous service of not less than five years qualifies for exemption.Exemption is least of the following: (aggregate maximum from any number of employers) 15 days salary (denominator taken as 26 in case of

monthly salary) for every completed year/ part thereof in excess of 6 months, or

₹10,00,000/- Gratuity actually received whichever is less.

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

GRATUITY [SECTION 10(10)]Other employees — Amount received on

retirement, incapacitation, death or termination — Exemption is least of the following : (aggregate maximum from any number of employments)₹10,00,000/-.

Half month’s salary for each completed year of service; (based on last ten months’ average salary), or

Gratuity actually received.Definition of salary: Salary includes dearness

allowance, if terms of payment allows but excludes all other allowances and perquisites

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

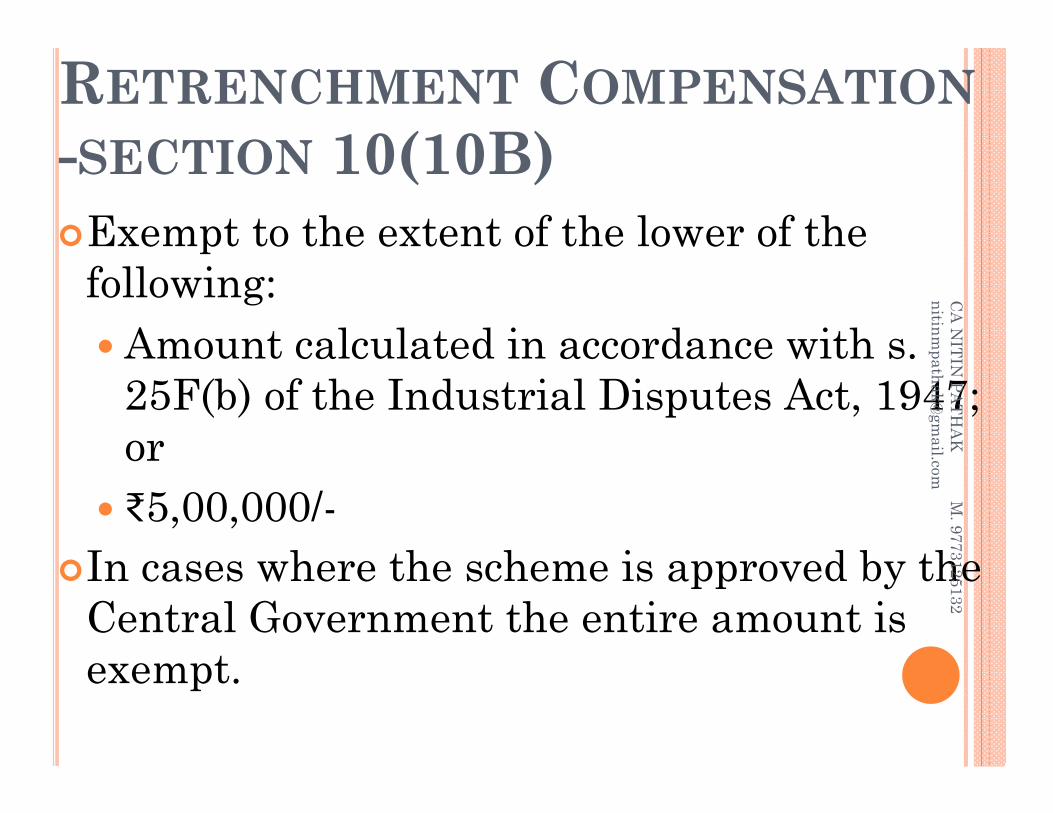

RETRENCHMENT COMPENSATION-SECTION 10(10B)Exempt to the extent of the lower of the

following: Amount calculated in accordance with s.

25F(b) of the Industrial Disputes Act, 1947; or

₹5,00,000/-In cases where the scheme is approved by the

Central Government the entire amount is exempt.

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

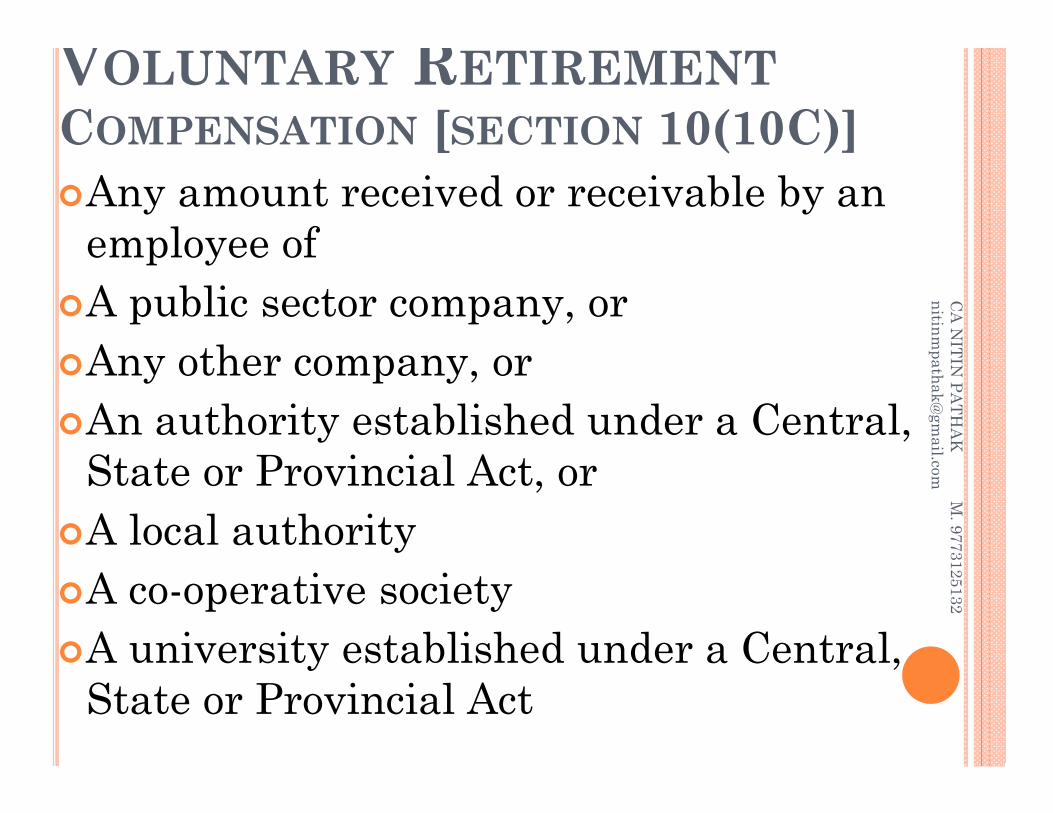

VOLUNTARY RETIREMENTCOMPENSATION [SECTION 10(10C)]Any amount received or receivable by an

employee ofA public sector company, orAny other company, orAn authority established under a Central,

State or Provincial Act, orA local authorityA co-operative societyA university established under a Central,

State or Provincial Act

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

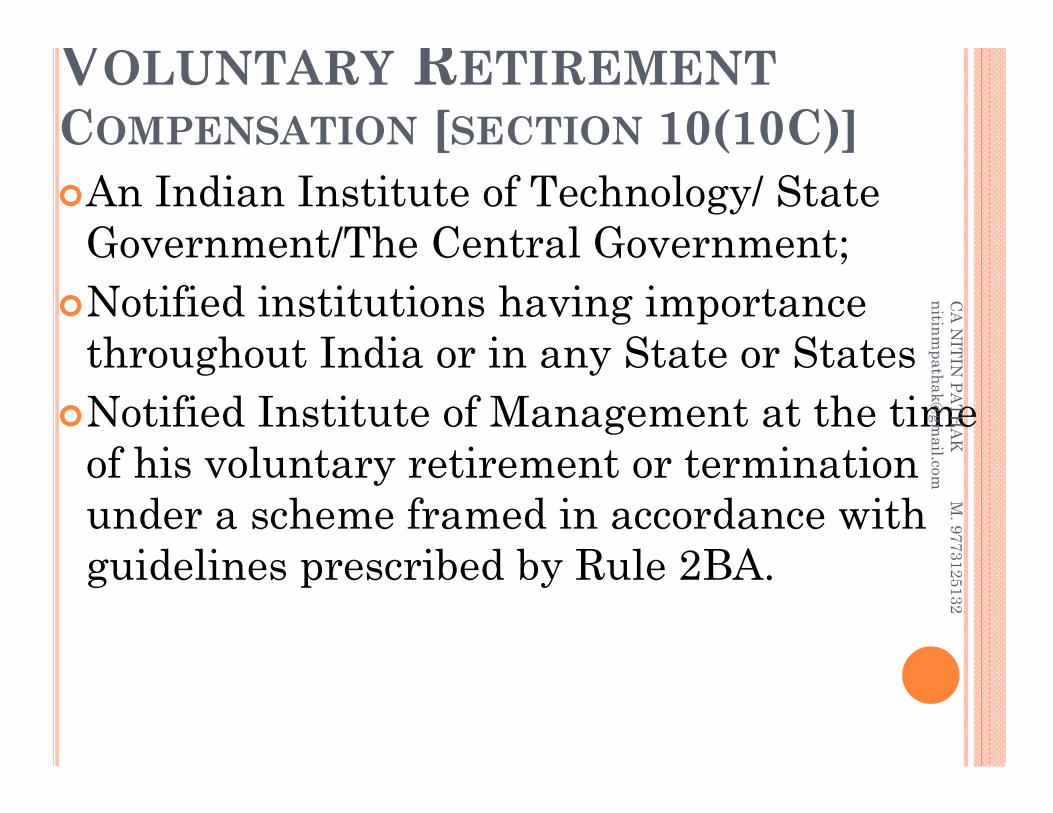

VOLUNTARY RETIREMENTCOMPENSATION [SECTION 10(10C)]An Indian Institute of Technology/ State

Government/The Central Government;Notified institutions having importance

throughout India or in any State or StatesNotified Institute of Management at the time

of his voluntary retirement or termination under a scheme framed in accordance with guidelines prescribed by Rule 2BA.

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

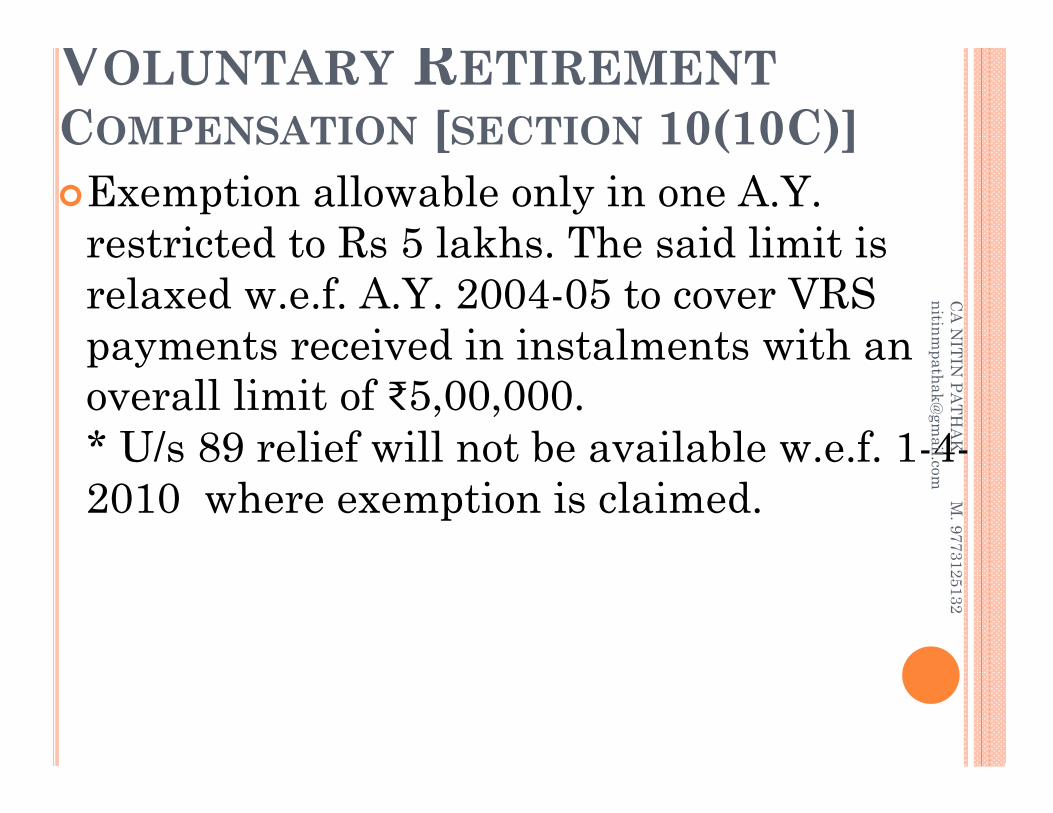

VOLUNTARY RETIREMENTCOMPENSATION [SECTION 10(10C)]Exemption allowable only in one A.Y.

restricted to Rs 5 lakhs. The said limit is relaxed w.e.f. A.Y. 2004-05 to cover VRS payments received in instalments with an overall limit of ₹5,00,000.* U/s 89 relief will not be available w.e.f. 1-4-2010 where exemption is claimed.

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

HOUSE RENT ALLOWANCE

50% of salary (Mumbai, Kolkata, Delhi or Chennai) and 40% of salary where residential house is situated at any other place; HRA paid Actual rent paid over 10% of salary

Where Salary = B+A+B+C

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

LEAVE ENCASHMENTEncashment of earned leave while in

service will be treated as incomeExempt at the time of retirement:10 months salary * last 10 months

average salary orRs.3,00,000/- whichever is less

Entitlement to earned leave not to exceed 30 days for every year of actual service.Limits aggregate n of employers.

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

LEAVE TRAVEL CONCESSIONFor himself/spouse/children/dependent

parents/siblingsAmount actually spent for travellingIn India onlyTwice in a block of four calendar years. (Block

year 2014-17)Two surviving childRoad travel on vehicle, second class train fairAir fare of a economy class/Air condition first

class rail fare/1st class or deluxe class public transport fare

For C/f entitlement one is allowed

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

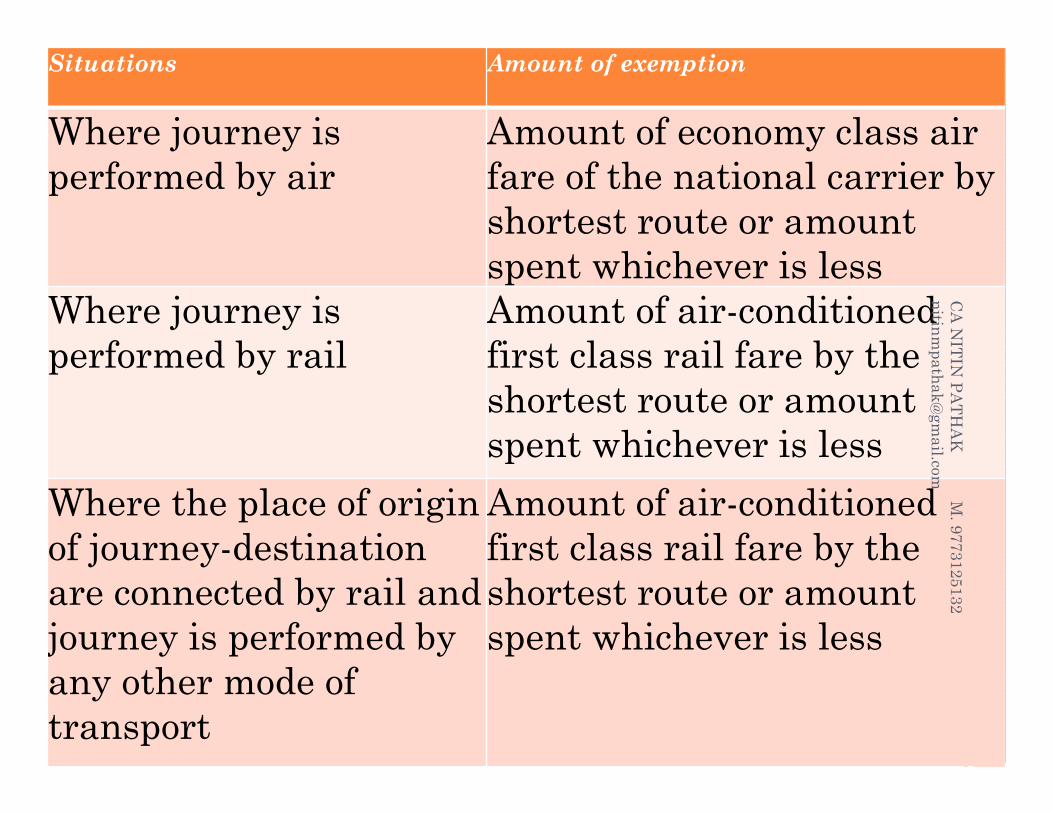

Situations Amount of exemption

Where journey is performed by air

Amount of economy class air fare of the national carrier by shortest route or amount spent whichever is less

Where journey is performed by rail

Amount of air-conditioned first class rail fare by the shortest route or amount spent whichever is less

Where the place of origin of journey-destination are connected by rail and journey is performed by any other mode of transport

Amount of air-conditioned first class rail fare by the shortest route or amount spent whichever is less

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

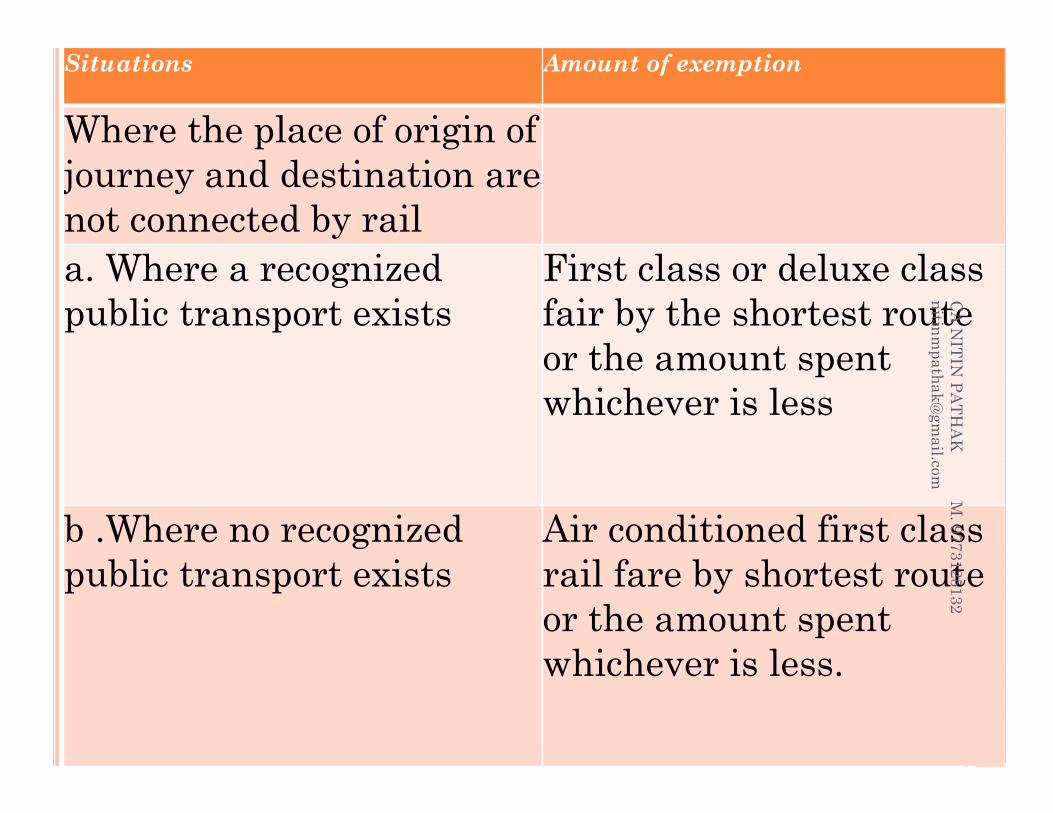

Situations Amount of exemption

Where the place of origin of journey and destination are not connected by raila. Where a recognized public transport exists

First class or deluxe class fair by the shortest route or the amount spent whichever is less

b .Where no recognized public transport exists

Air conditioned first class rail fare by shortest route or the amount spent whichever is less.

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

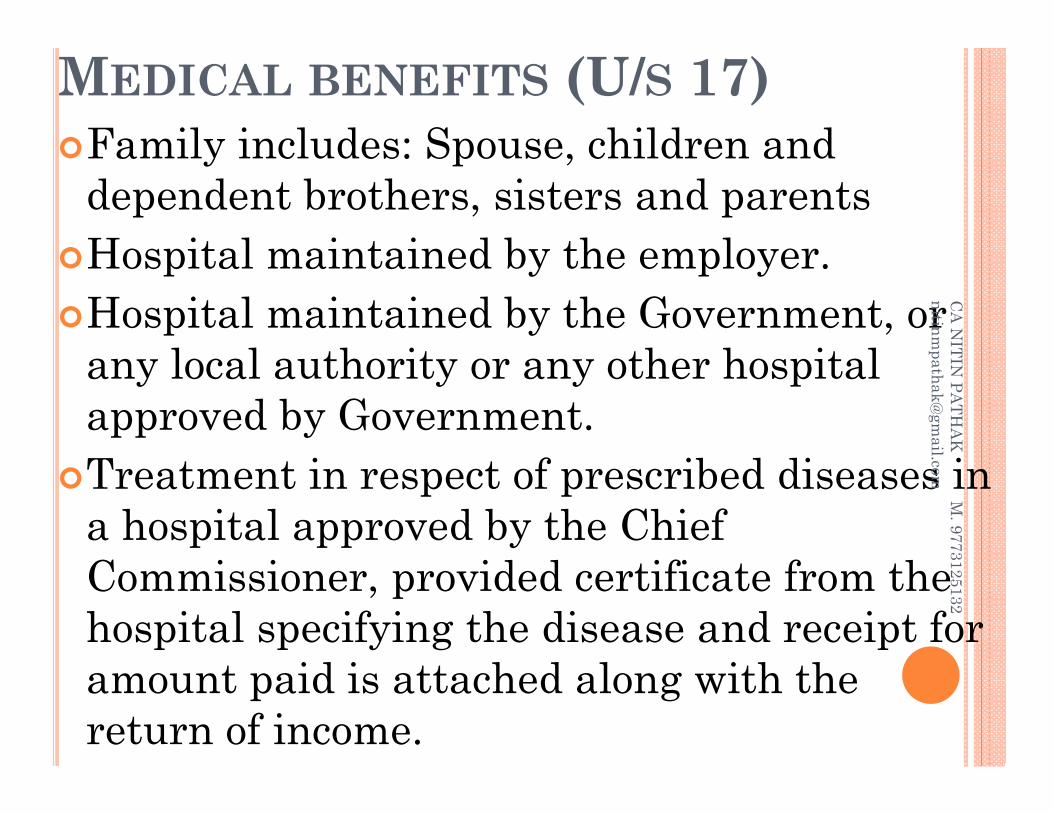

MEDICAL BENEFITS (U/S 17)Family includes: Spouse, children and

dependent brothers, sisters and parentsHospital maintained by the employer.Hospital maintained by the Government, or

any local authority or any other hospital approved by Government.

Treatment in respect of prescribed diseases in a hospital approved by the Chief Commissioner, provided certificate from the hospital specifying the disease and receipt for amount paid is attached along with the return of income.

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

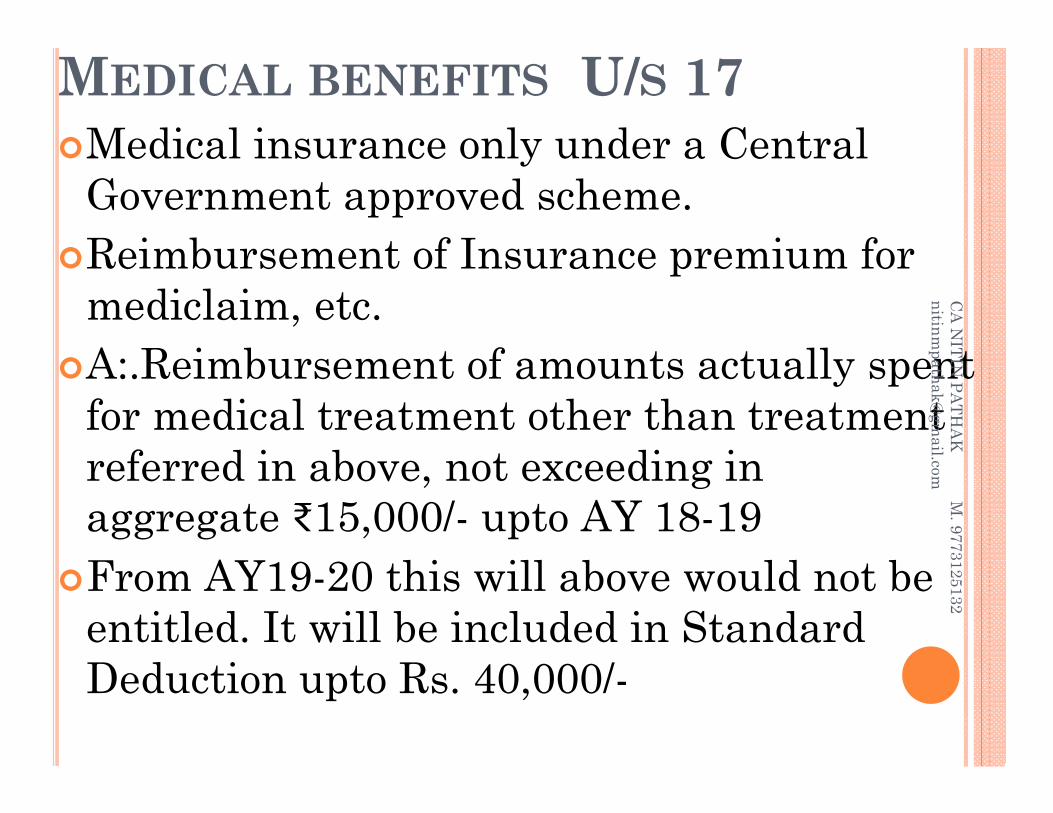

MEDICAL BENEFITS U/S 17Medical insurance only under a Central

Government approved scheme.Reimbursement of Insurance premium for

mediclaim, etc.A:.Reimbursement of amounts actually spent

for medical treatment other than treatment referred in above, not exceeding in aggregate ₹15,000/- upto AY 18-19

From AY19-20 this will above would not be entitled. It will be included in Standard Deduction upto Rs. 40,000/-

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

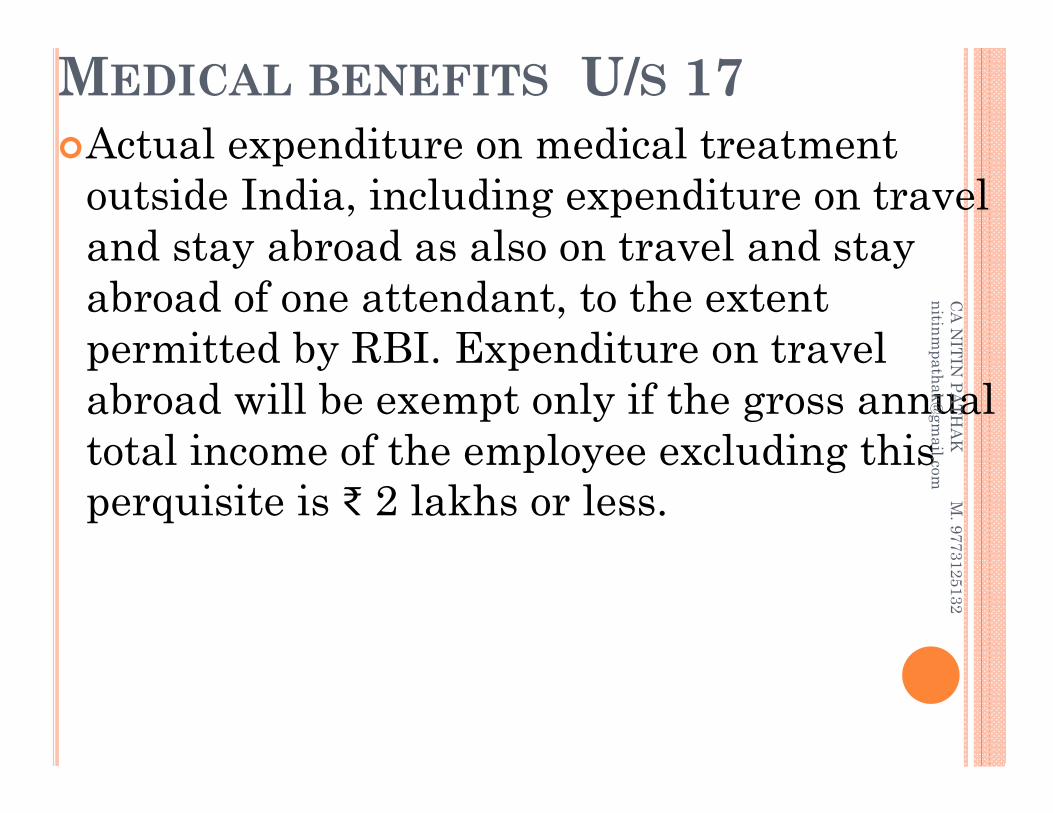

MEDICAL BENEFITS U/S 17Actual expenditure on medical treatment

outside India, including expenditure on travel and stay abroad as also on travel and stay abroad of one attendant, to the extent permitted by RBI. Expenditure on travel abroad will be exempt only if the gross annual total income of the employee excluding this perquisite is ₹ 2 lakhs or less.

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

SPECIAL ALLOWANCES EXEMPTAny allowance, not in the nature of

perquisite, granted to meet expenses wholly, necessarily and exclusively incurred in the performance of duties, to the extent to which actually incurred.Allowance granted to meet personal

expense at the place where duties of his office are ordinarily performed or at the place where he ordinarily resides or to compensate for increased cost of living as may be prescribed in Rule 2BB.

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

SPECIAL ALLOWANCES EXEMPTTravel expenses on tour or transfer,Ordinary daily charges on account of

absence from normal place of duty on tour or journey in connection with transferFor conveyance in performance of

duties where it is not providedFor expenditure on helper engaged for

performance of office duties

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

SPECIAL ALLOWANCES EXEMPT

For encouraging academic, research and training pursuits in educational and research institutionsFor purchase or maintenance of uniform,Special Compensatory Allowance in specified areas to extent specified

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

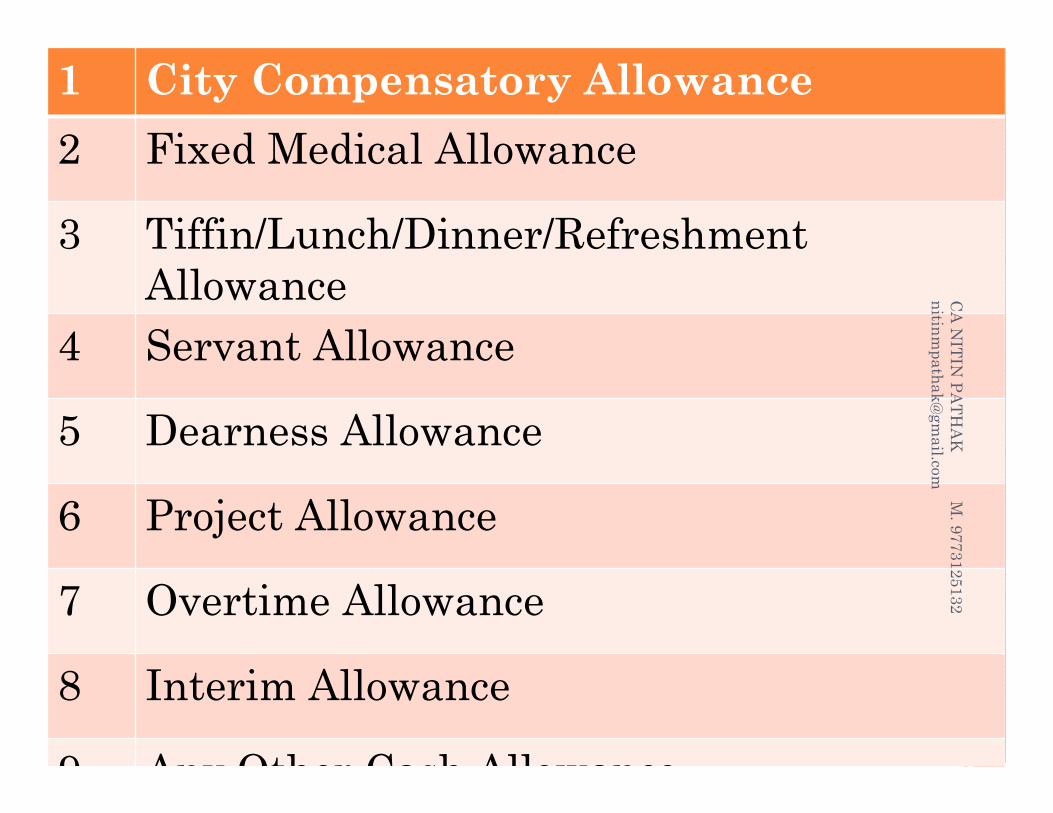

1 City Compensatory Allowance 2 Fixed Medical Allowance

3 Tiffin/Lunch/Dinner/Refreshment Allowance

4 Servant Allowance

5 Dearness Allowance

6 Project Allowance

7 Overtime Allowance

8 Interim Allowance

9 Any Other Cash Allowance

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

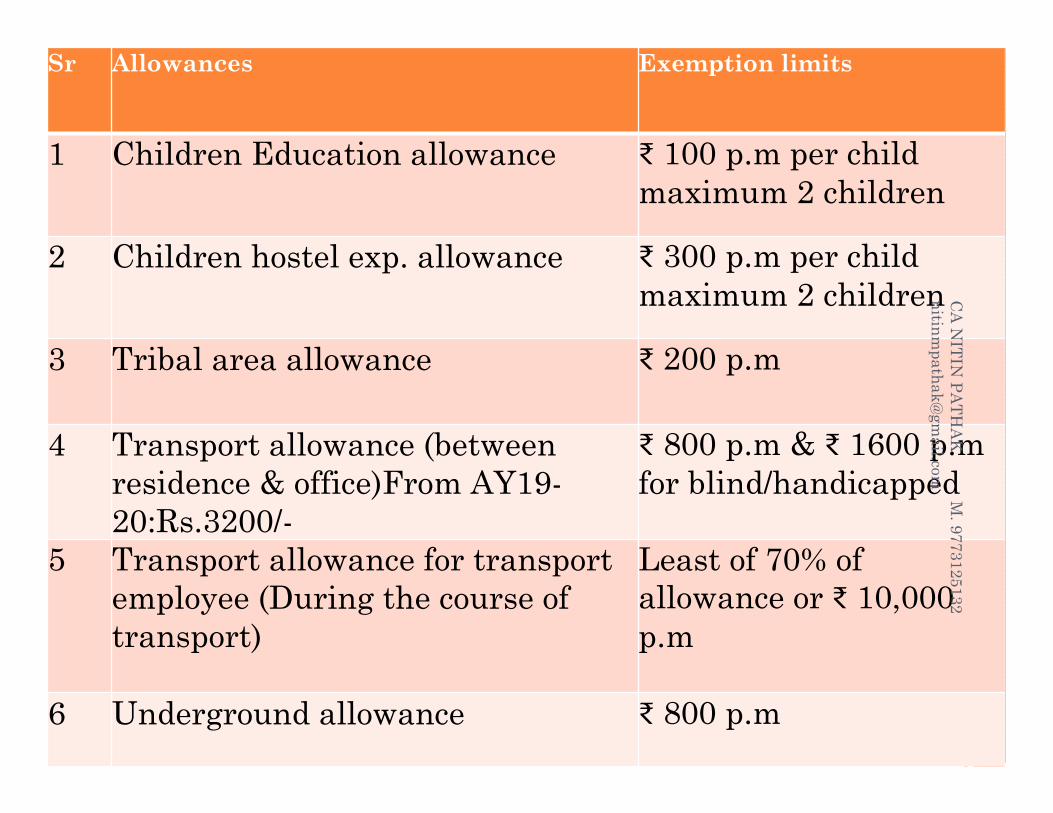

Sr Allowances Exemption limits

1 Children Education allowance ₹ 100 p.m per child maximum 2 children

2 Children hostel exp. allowance ₹ 300 p.m per child maximum 2 children

3 Tribal area allowance ₹ 200 p.m

4 Transport allowance (between residence & office)From AY19-20:Rs.3200/-

₹ 800 p.m & ₹ 1600 p.m for blind/handicapped

5 Transport allowance for transport employee (During the course of transport)

Least of 70% of allowance or ₹ 10,000 p.m

6 Underground allowance ₹ 800 p.m

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

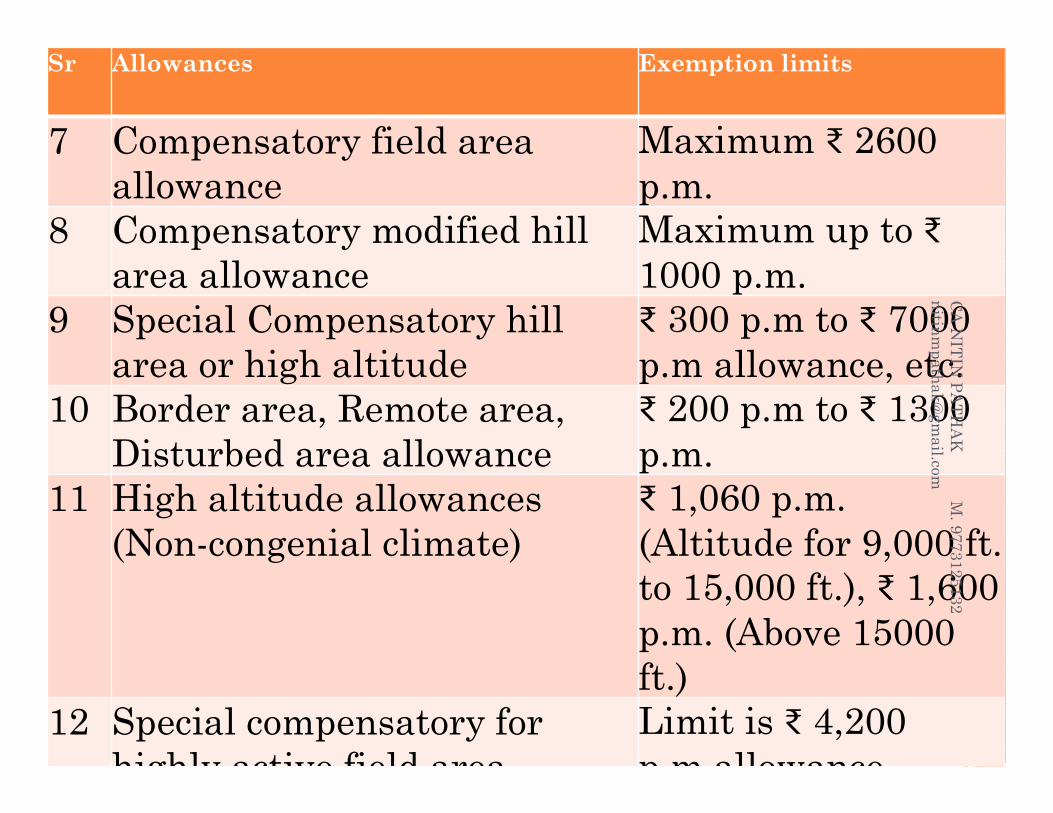

Sr Allowances Exemption limits

7 Compensatory field area allowance

Maximum ₹ 2600 p.m.

8 Compensatory modified hill area allowance

Maximum up to ₹1000 p.m.

9 Special Compensatory hill area or high altitude

₹ 300 p.m to ₹ 7000 p.m allowance, etc.

10 Border area, Remote area, Disturbed area allowance

₹ 200 p.m to ₹ 1300 p.m.

11 High altitude allowances (Non-congenial climate)

₹ 1,060 p.m. (Altitude for 9,000 ft. to 15,000 ft.), ₹ 1,600 p.m. (Above 15000 ft.)

12 Special compensatory for highly active field area

Limit is ₹ 4,200 p m allowance

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

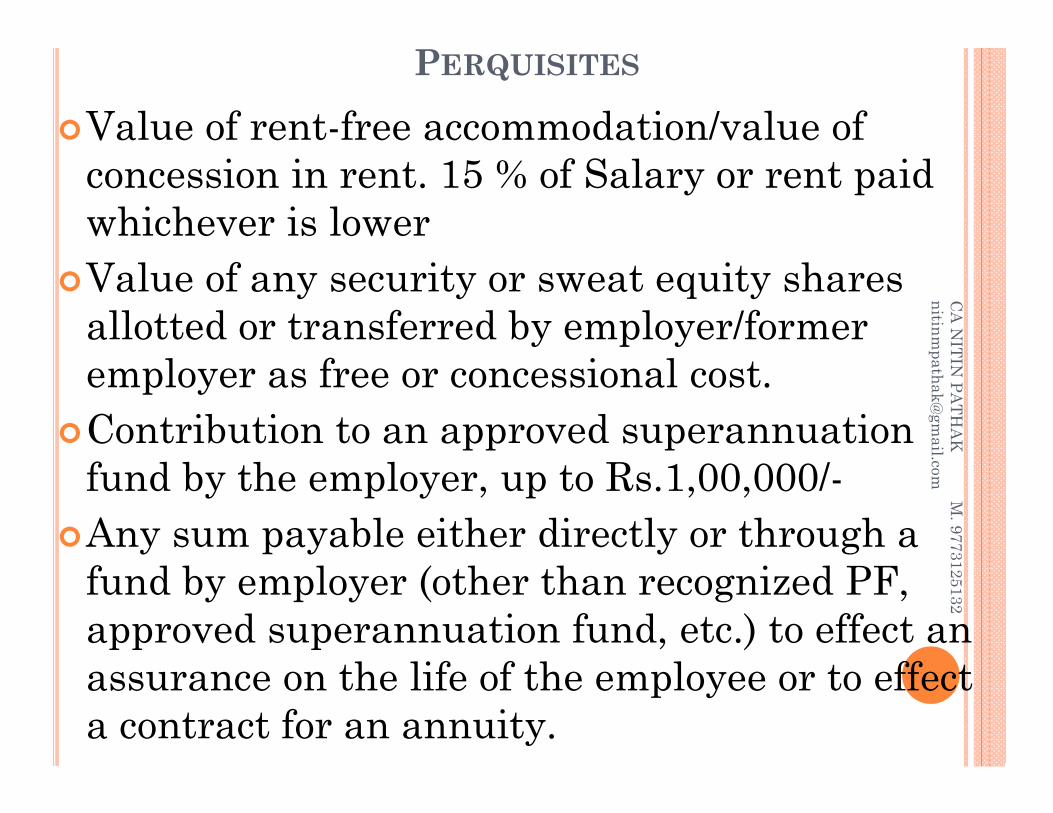

PERQUISITES

Value of rent-free accommodation/value of concession in rent. 15 % of Salary or rent paid whichever is lower

Value of any security or sweat equity shares allotted or transferred by employer/former employer as free or concessional cost.

Contribution to an approved superannuation fund by the employer, up to Rs.1,00,000/-

Any sum payable either directly or through a fund by employer (other than recognized PF, approved superannuation fund, etc.) to effect an assurance on the life of the employee or to effect a contract for an annuity.

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

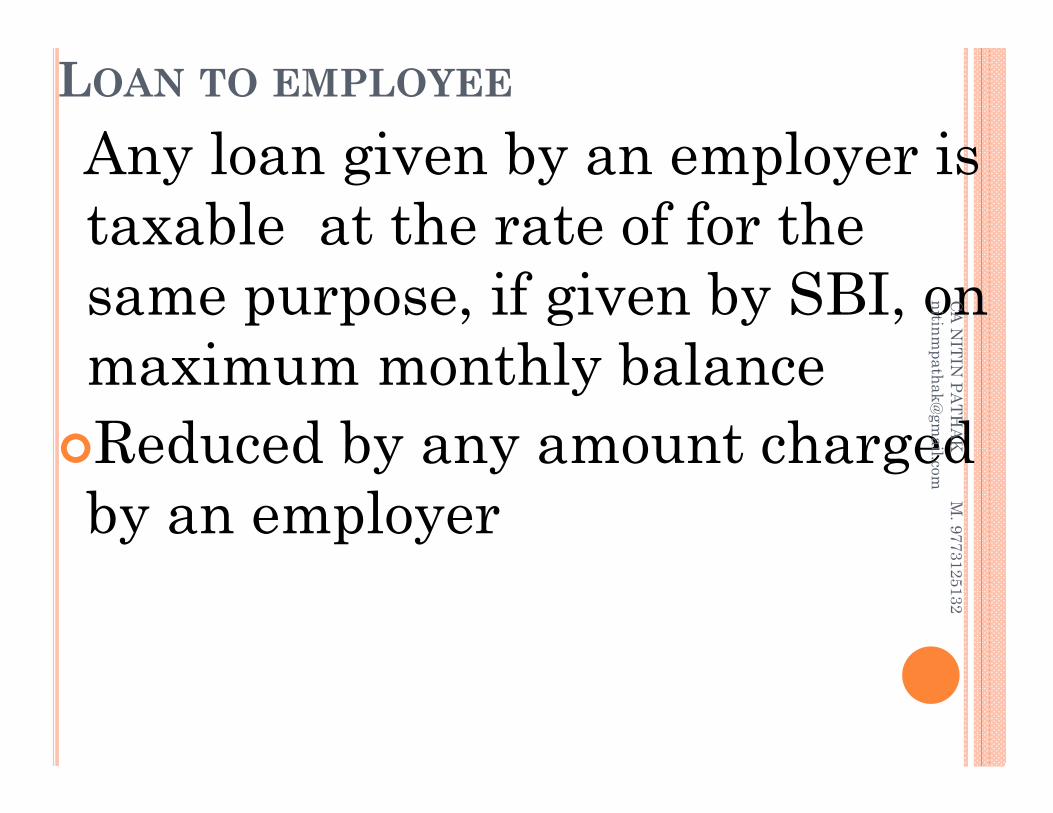

LOAN TO EMPLOYEE

Any loan given by an employer is taxable at the rate of for the same purpose, if given by SBI, on maximum monthly balanceReduced by any amount charged by an employer

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

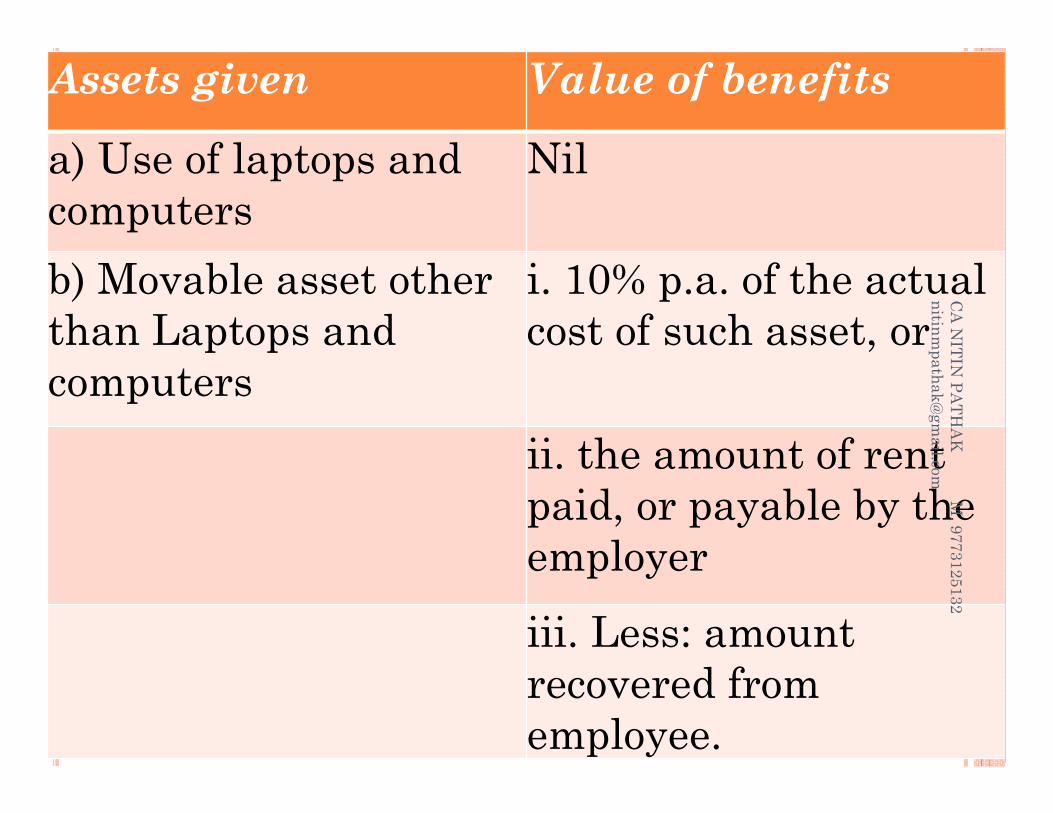

Assets given Value of benefits

a) Use of laptops and computers

Nil

b) Movable asset other than Laptops and computers

i. 10% p.a. of the actual cost of such asset, or

ii. the amount of rent paid, or payable by the employeriii. Less: amount recovered from employee.

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

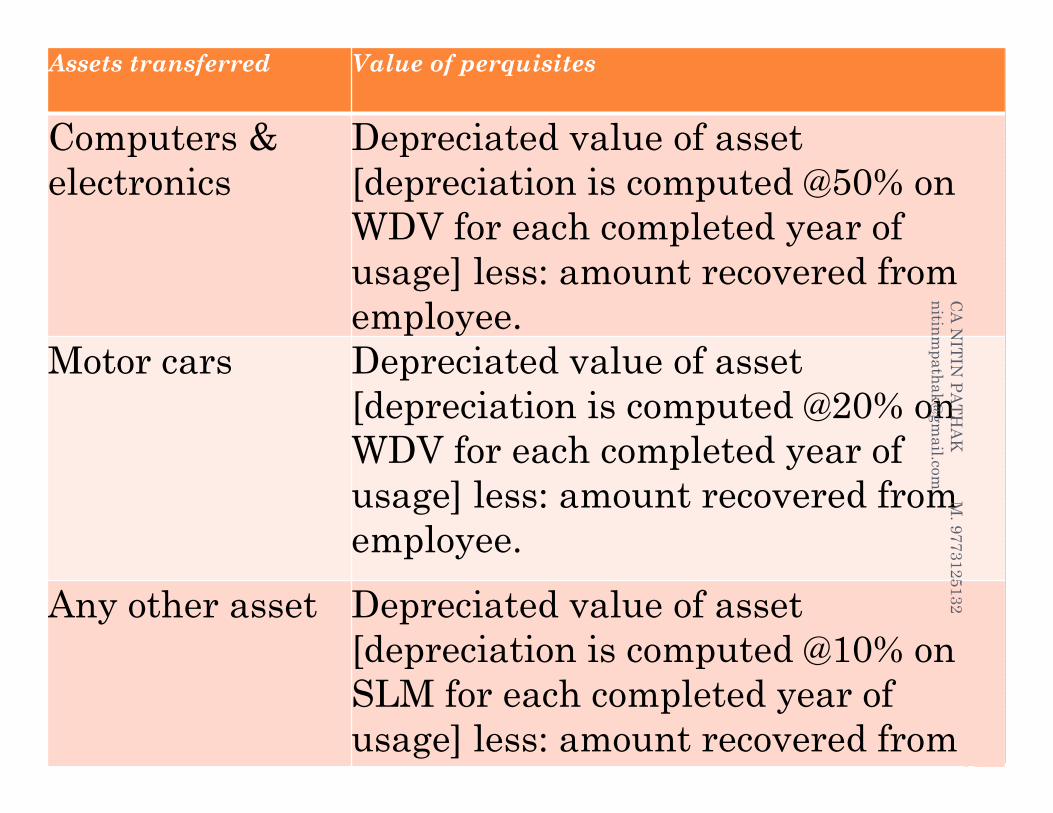

Assets transferred Value of perquisites

Computers & electronics

Depreciated value of asset [depreciation is computed @50% on WDV for each completed year of usage] less: amount recovered from employee.

Motor cars Depreciated value of asset [depreciation is computed @20% on WDV for each completed year of usage] less: amount recovered from employee.

Any other asset Depreciated value of asset [depreciation is computed @10% on SLM for each completed year of usage] less: amount recovered from

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

MISCELLANEOUS

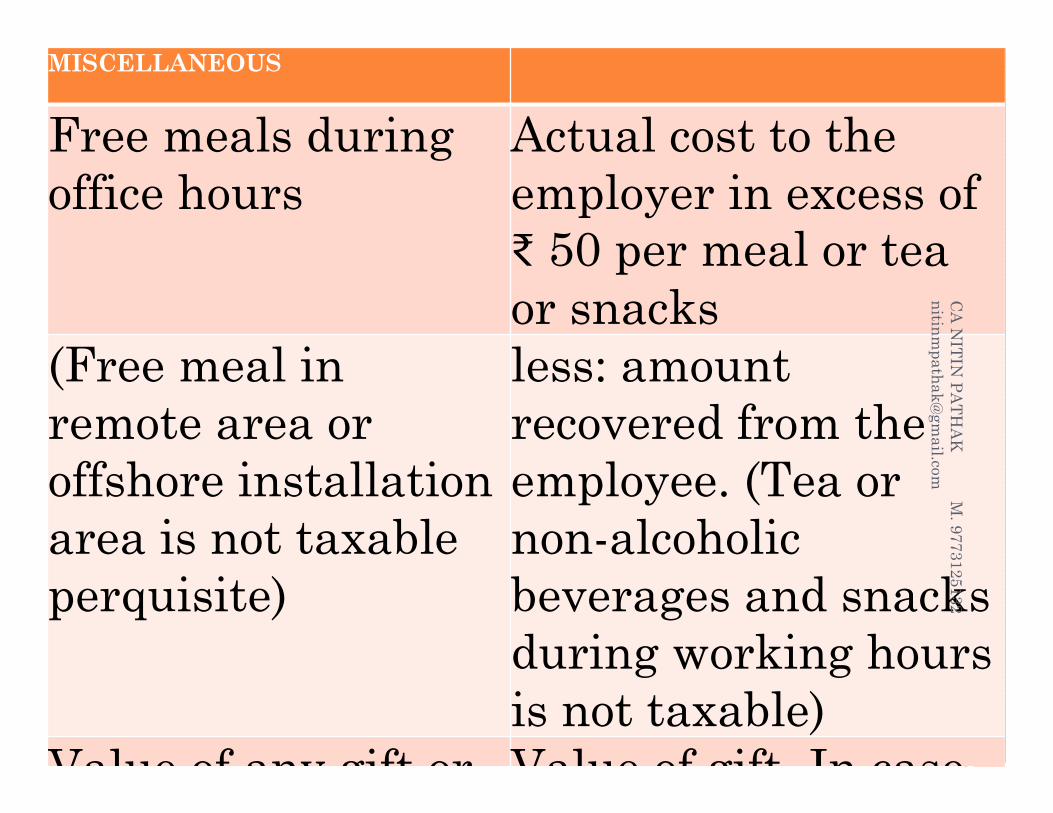

Free meals during office hours

Actual cost to the employer in excess of ₹ 50 per meal or tea or snacks

(Free meal in remote area or offshore installation area is not taxable perquisite)

less: amount recovered from the employee. (Tea or non-alcoholic beverages and snacks during working hours is not taxable)

Value of any gift or Value of gift In case

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

MISCELLANEOUS

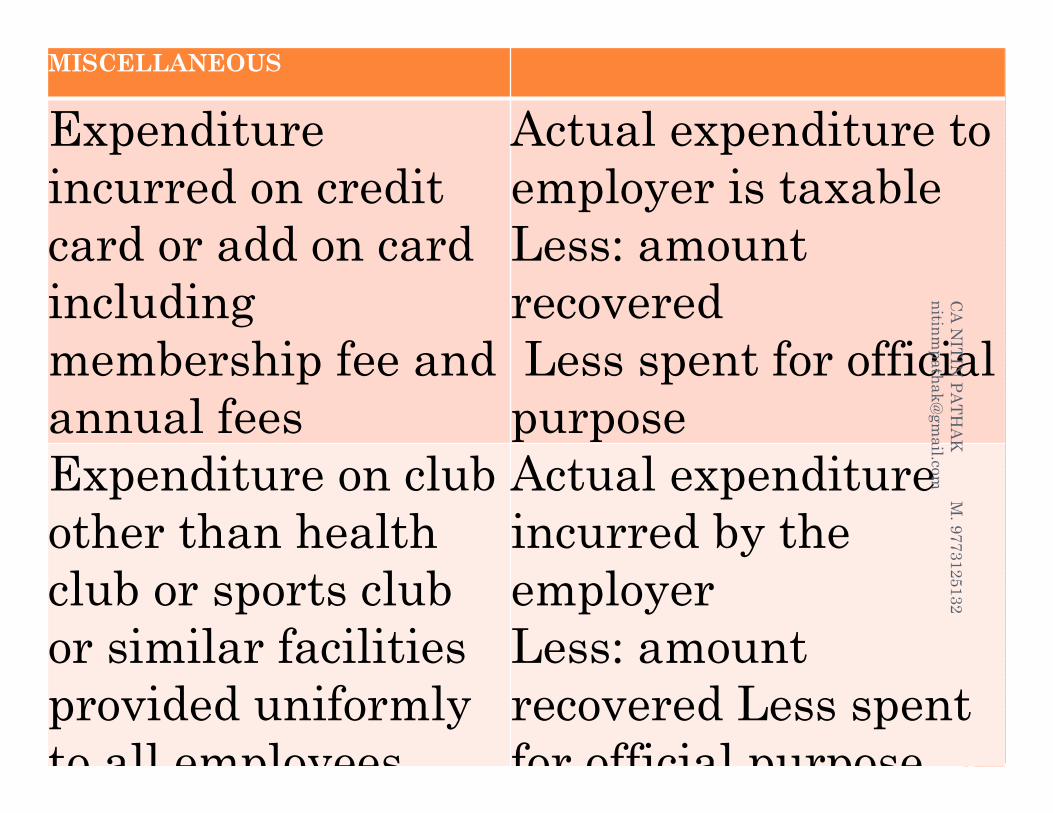

Expenditure incurred on credit card or add on card including membership fee and annual fees

Actual expenditure to employer is taxableLess: amount recoveredLess spent for official

purposeExpenditure on club other than health club or sports club or similar facilities provided uniformly to all employees

Actual expenditure incurred by the employerLess: amount recovered Less spent for official purpose

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

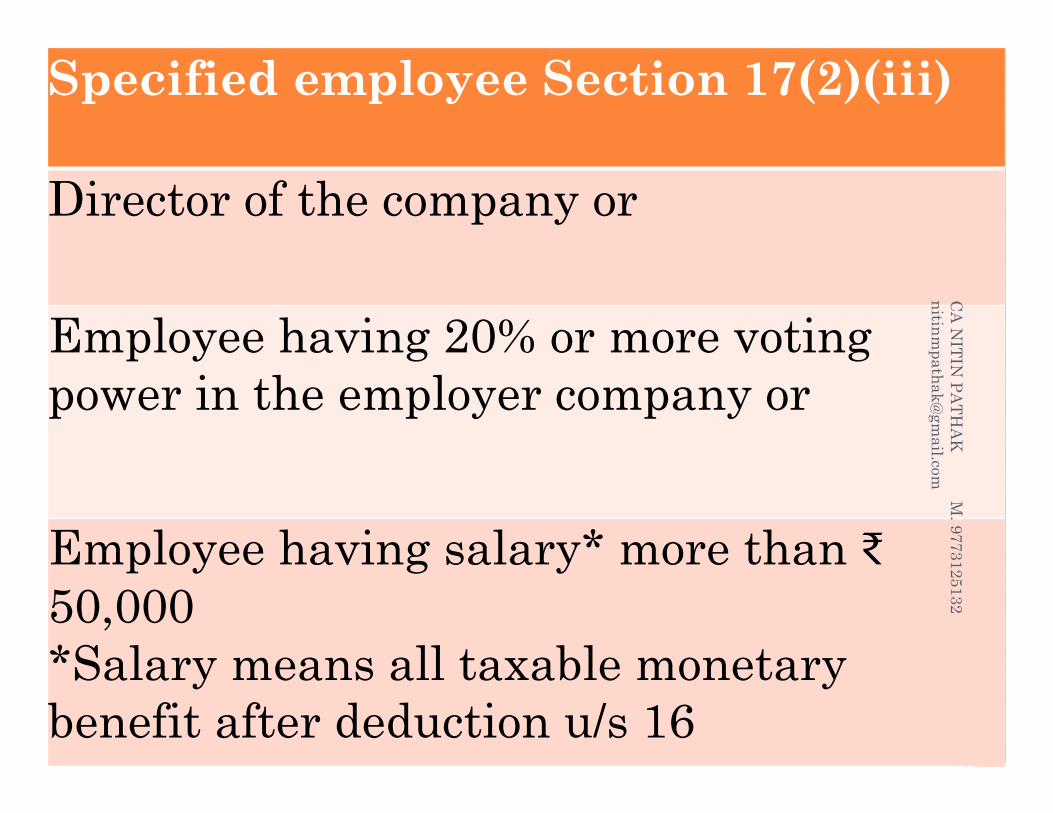

Specified employee Section 17(2)(iii)

Director of the company or

Employee having 20% or more voting power in the employer company or

Employee having salary* more than ₹50,000*Salary means all taxable monetary benefit after deduction u/s 16

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

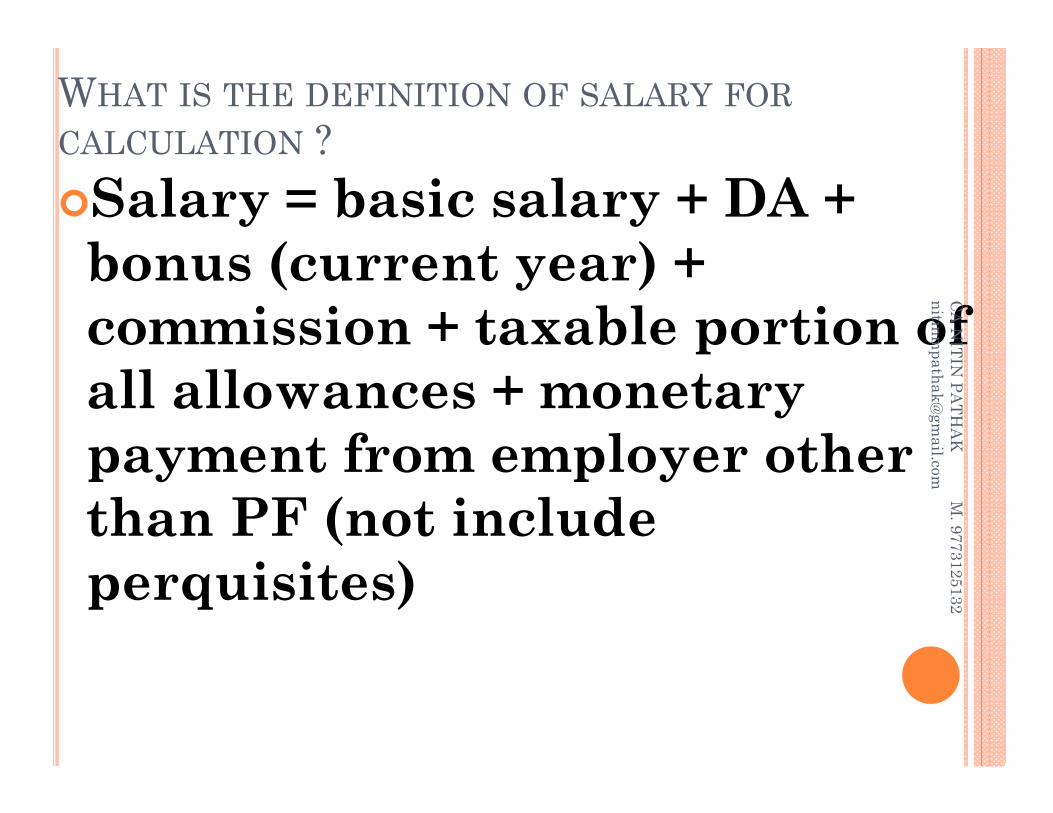

WHAT IS THE DEFINITION OF SALARY FORCALCULATION ?Salary = basic salary + DA + bonus (current year) + commission + taxable portion of all allowances + monetary payment from employer other than PF (not include perquisites)

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

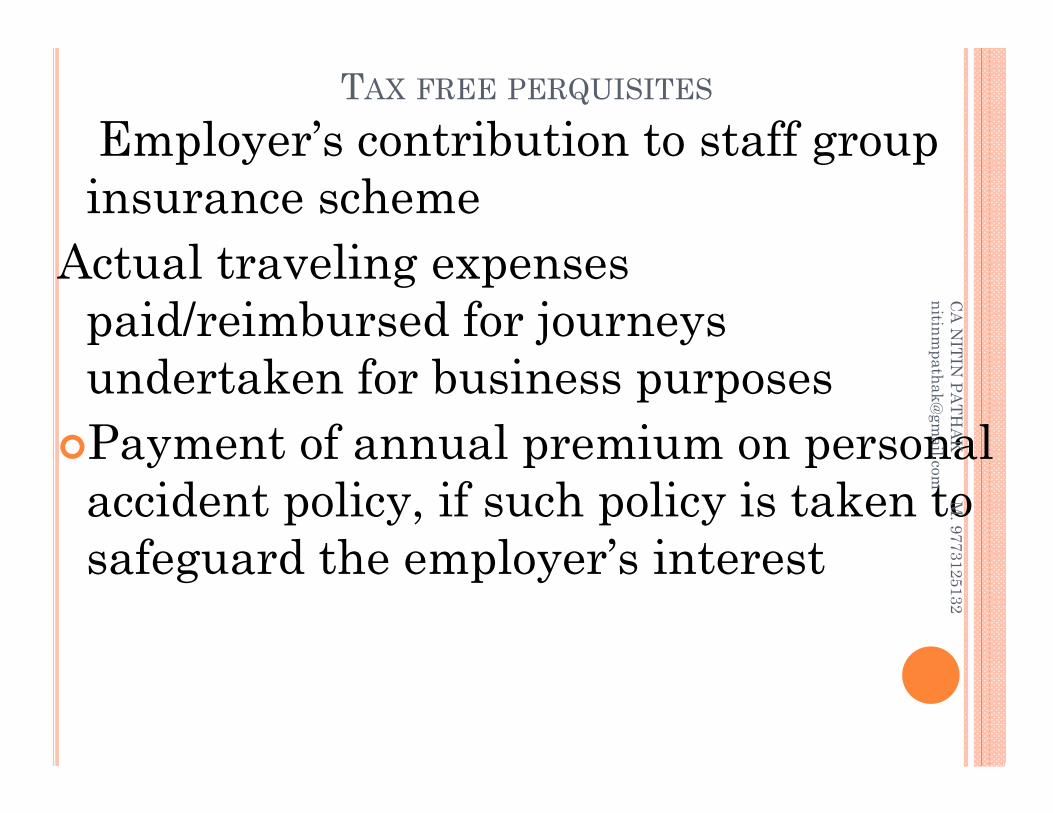

TAX FREE PERQUISITES

Employer’s contribution to staff group insurance scheme

Actual traveling expenses paid/reimbursed for journeys undertaken for business purposesPayment of annual premium on personal

accident policy, if such policy is taken to safeguard the employer’s interest

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

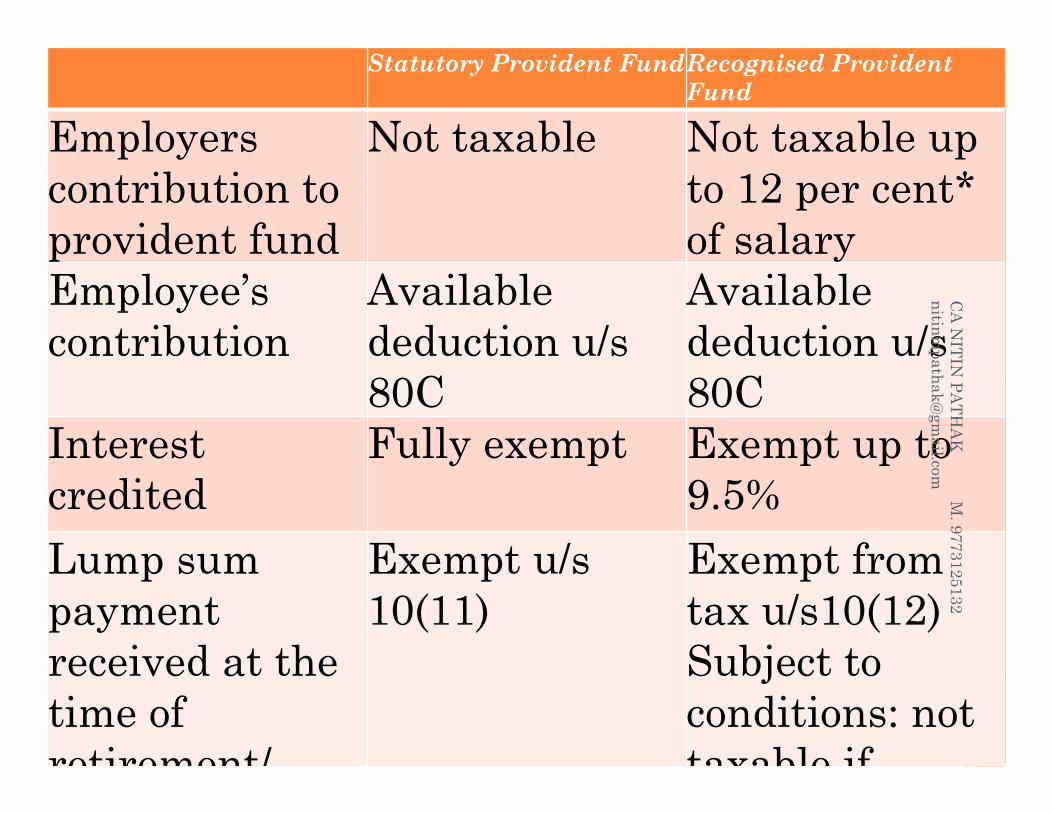

Statutory Provident FundRecognised Provident Fund

Employers contribution to provident fund

Not taxable Not taxable up to 12 per cent* of salary

Employee’s contribution

Available deduction u/s 80C

Available deduction u/s 80C

Interest credited

Fully exempt Exempt up to 9.5%

Lump sum payment received at the time of retirement/

Exempt u/s 10(11)

Exempt from tax u/s10(12)Subject to conditions: not taxable if

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

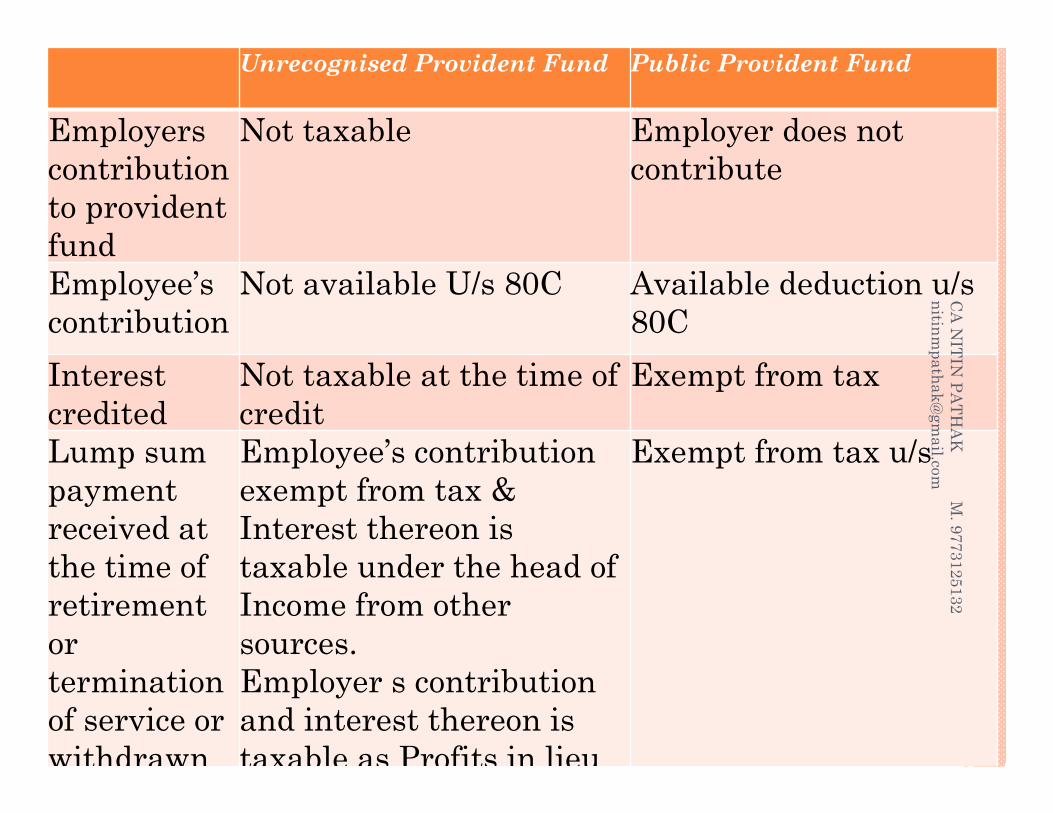

Unrecognised Provident Fund Public Provident Fund

Employers contribution to provident fund

Not taxable Employer does not contribute

Employee’s contribution

Not available U/s 80C Available deduction u/s 80C

Interest credited

Not taxable at the time of credit

Exempt from tax

Lump sum payment received at the time of retirement or termination of service or withdrawn

Employee’s contribution exempt from tax & Interest thereon is taxable under the head of Income from other sources.Employer s contribution and interest thereon is taxable as Profits in lieu

Exempt from tax u/s

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

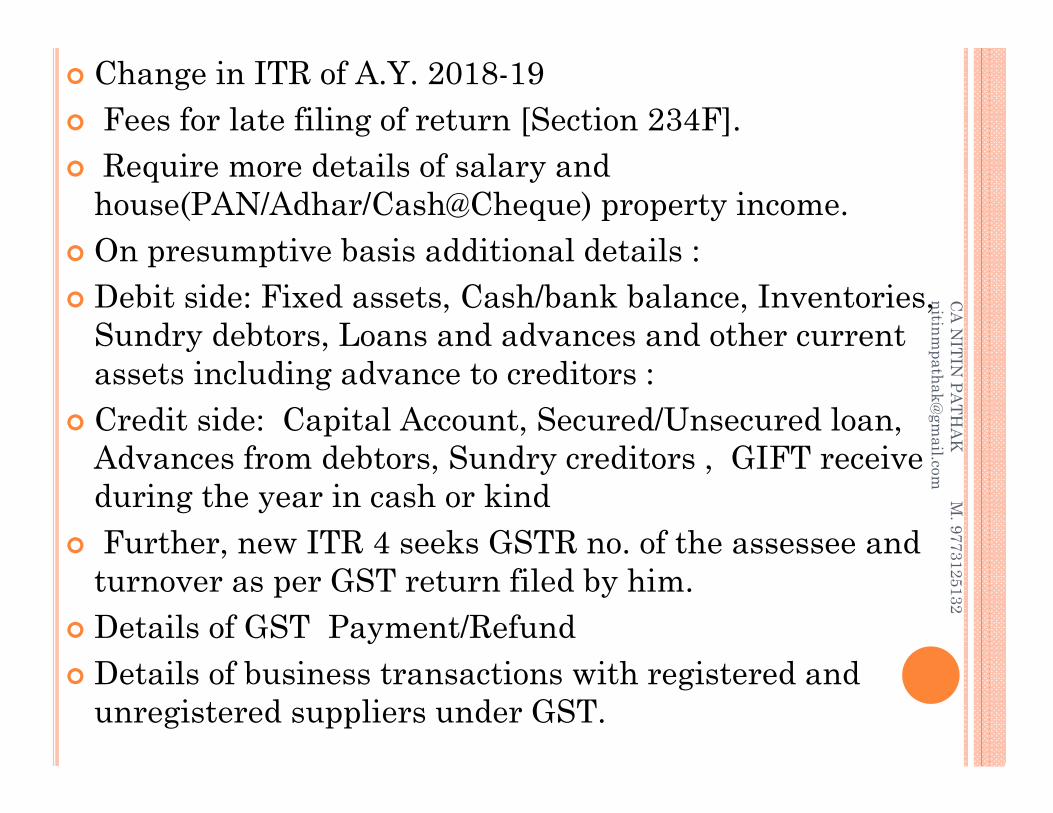

Change in ITR of A.Y. 2018-19 Fees for late filing of return [Section 234F]. Require more details of salary and

house(PAN/Adhar/Cash@Cheque) property income. On presumptive basis additional details : Debit side: Fixed assets, Cash/bank balance, Inventories,

Sundry debtors, Loans and advances and other current assets including advance to creditors :

Credit side: Capital Account, Secured/Unsecured loan, Advances from debtors, Sundry creditors , GIFT receive during the year in cash or kind

Further, new ITR 4 seeks GSTR no. of the assessee and turnover as per GST return filed by him.

Details of GST Payment/Refund Details of business transactions with registered and

unregistered suppliers under GST.

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

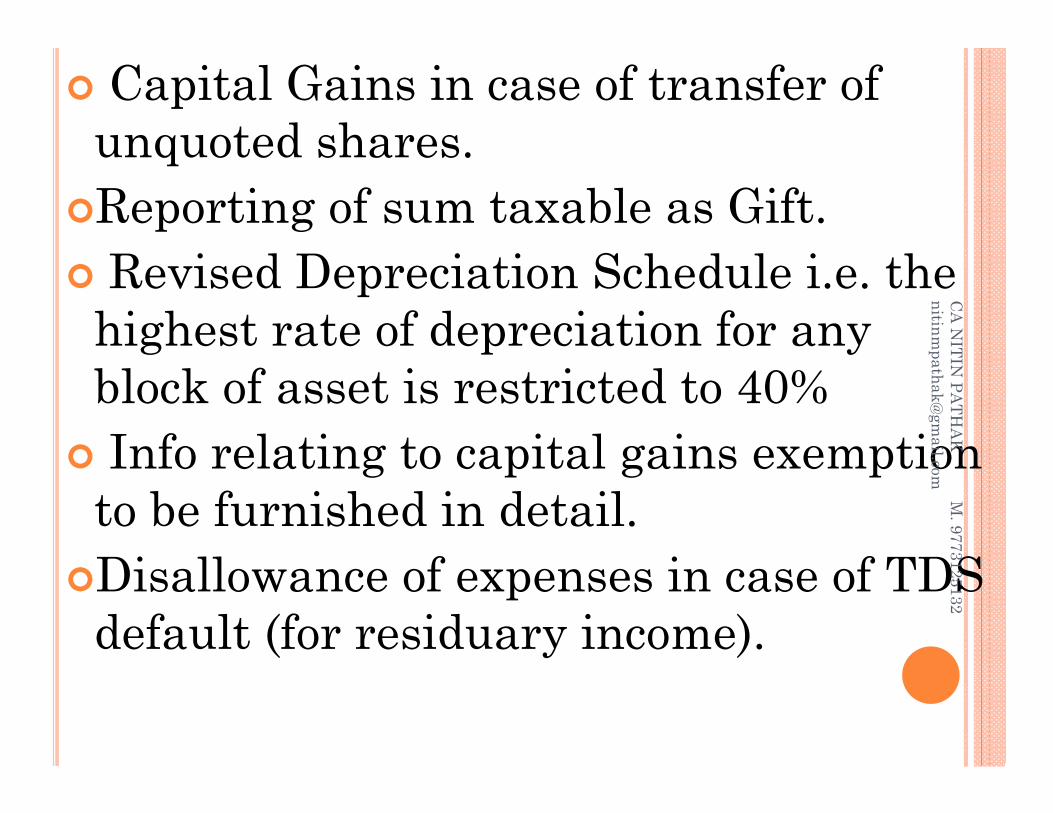

Capital Gains in case of transfer of unquoted shares.Reporting of sum taxable as Gift. Revised Depreciation Schedule i.e. the

highest rate of depreciation for any block of asset is restricted to 40% Info relating to capital gains exemption

to be furnished in detail.Disallowance of expenses in case of TDS

default (for residuary income).

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

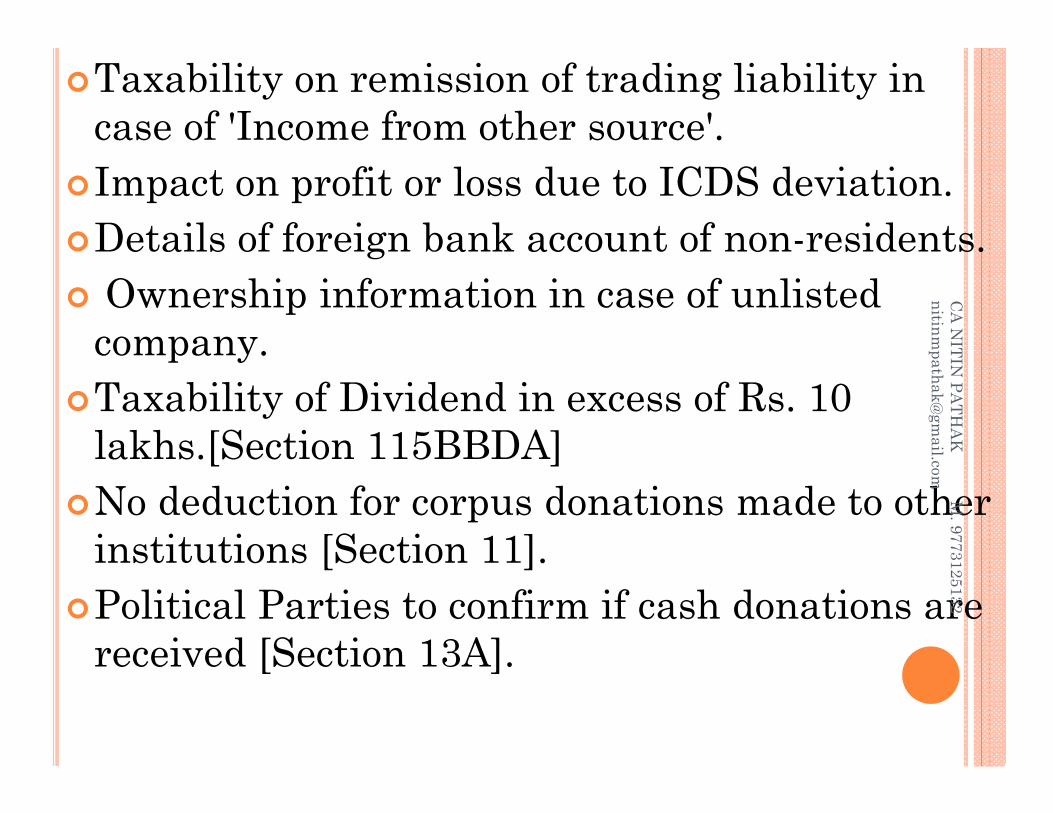

Taxability on remission of trading liability in case of 'Income from other source'.

Impact on profit or loss due to ICDS deviation.Details of foreign bank account of non-residents. Ownership information in case of unlisted

company.Taxability of Dividend in excess of Rs. 10

lakhs.[Section 115BBDA]No deduction for corpus donations made to other

institutions [Section 11].Political Parties to confirm if cash donations are

received [Section 13A].

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

THINKS COVERED IN ONE LINE

WILLAnnual ReturnRTIRights of consumerRights of a citizenRecord of books, vouchers and

documentsReverse MortgageGST

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

PrayerOh god give me a courage,To change the things, which I can,Oh God give me a serenity to accept the things,

which I cannot change,Give me a wisdom to know,what I can change and what I can’t change.

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

Thanks you all for being with meC

A N

ITIN PA

THA

K M

. 9773125132 nitinm

pathak@gm

ail.com

QUESTIONS IF ANY?

E-MAIL:[email protected]

M. 9825804094BLOG: CANITINMPATHAK.BLOGSPOT.IN

CA

NITIN

PATH

AK

M. 9773125132

nitinmpathak@

gmail.com

Recommended