INTRODUCTIONTO BEHAVIORALPOLICYMAKING MODULE 1

1

1

Acknowledgments

MODULE 1: INTRODUCTION TO BEHAVIORAL POLICYMAKING

This deck was researched and prepared by Rafe Mazer and Alexandra Fiorillo (GRID Impact). The authors would like to thank our colleagues at CGAP. Specifically, the authors would like to thank Silvia Baur and Greg Chen (CGAP), Katherine McKee (World Bank), and Stanislaw Zmitrowicz (Central Bank of Brazil).

This is a culmination of more than five years of work by CGAP to pioneer behavioral research methods for consumer protection in emerging markets. This includes technical assistance with consumer protection policy makers in more than 10 jurisdictions and training of hundreds of policy makers on behavioral research and design methods. Please visit cgap.org's publications page for even more on this topic.

This work is available under the Creative Commons Attribution 3.0 IGO license (CC BY 3.0 IGO)https://creativecommons.org/licenses/by/3.0/igo/. By using the content of this publication, youagree to be bound by the terms of this license.

All queries on rights and licenses should be addressed to CGAP Publications, 1818 H Street, NW,MSN IS7-700, Washington, DC 20433 USA; e-mail: [email protected]; CGAP.org.Consultative Group to Assist the Poor/World Bank Group

Behavioral Research

Behavioral research seeks to understand the predictable but often unintuitive ways people make decisions, form

intentions, and decide whether to follow through with them.

MODULE 1: INTRODUCTION TO BEHAVIORAL POLICYMAKING

This course will help policy makers and those whosupport policy makers build better consumer

protection policies that reflect how consumersand financial institutions really behave.

MODULE 1: INTRODUCTION TO BEHAVIORAL POLICYMAKING

“The Big Three” Behaviors That Matter in Financial Consumer Protection

1. People have inconsistent preferences.

2. People have inconsistent behaviors.

3. Factors that are non-economic, small, and often overlooked can play a

large role in our behavior.

How do these behaviors affect the decisions we make in our daily lives?

MODULE 1: INTRODUCTION TO BEHAVIORAL POLICYMAKING

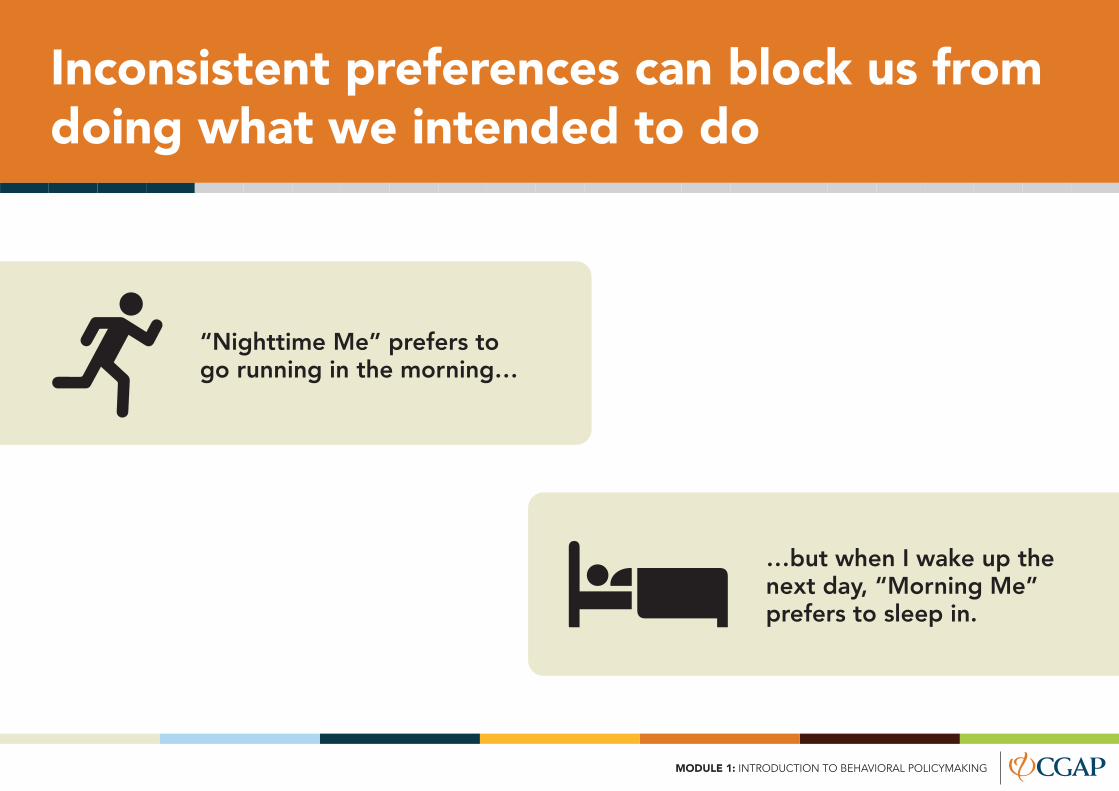

Inconsistent preferences can block us fromdoing what we intended to do

“Nighttime Me” prefers to go running in the morning…

…but when I wake up thenext day, “Morning Me”prefers to sleep in.

MODULE 1: INTRODUCTION TO BEHAVIORAL POLICYMAKING

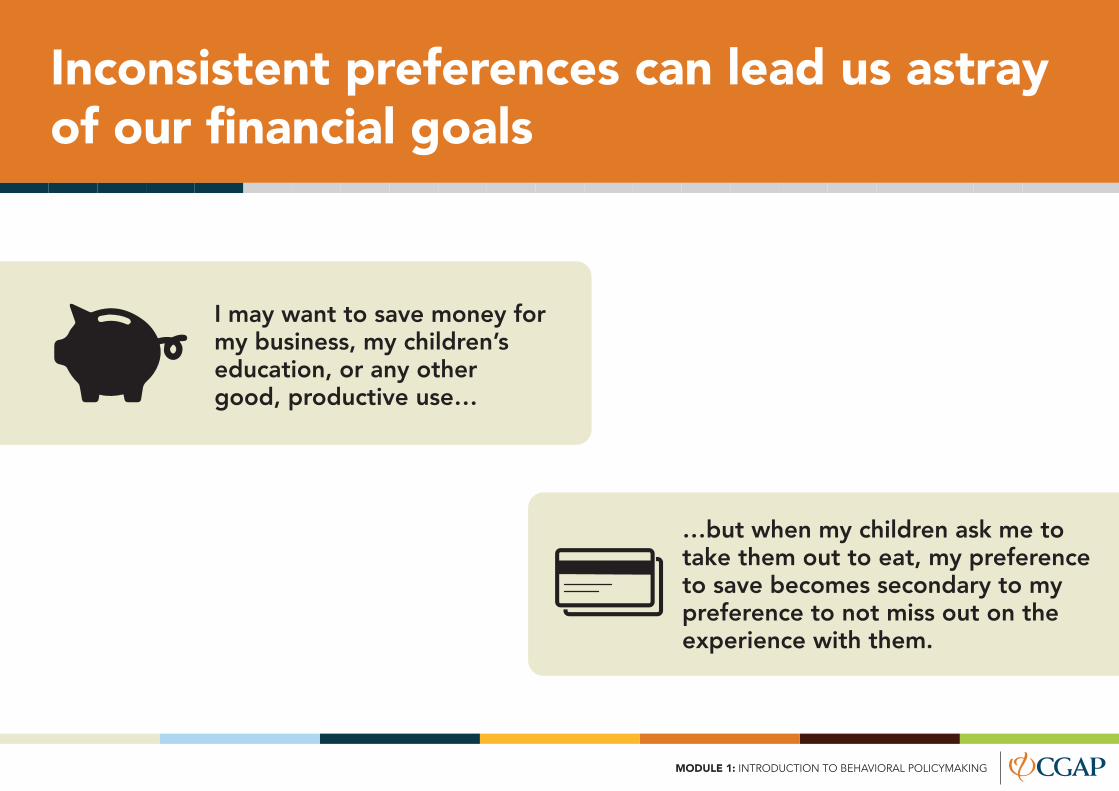

1Inconsistent preferences can lead us astrayof our financial goals

MODULE 1: INTRODUCTION TO BEHAVIORAL POLICYMAKING

I may want to save money for my business, my children’s education, or any othergood, productive use…

…but when my children ask me to take them out to eat, my preference to save becomes secondary to my preference to not miss out on the experience with them.

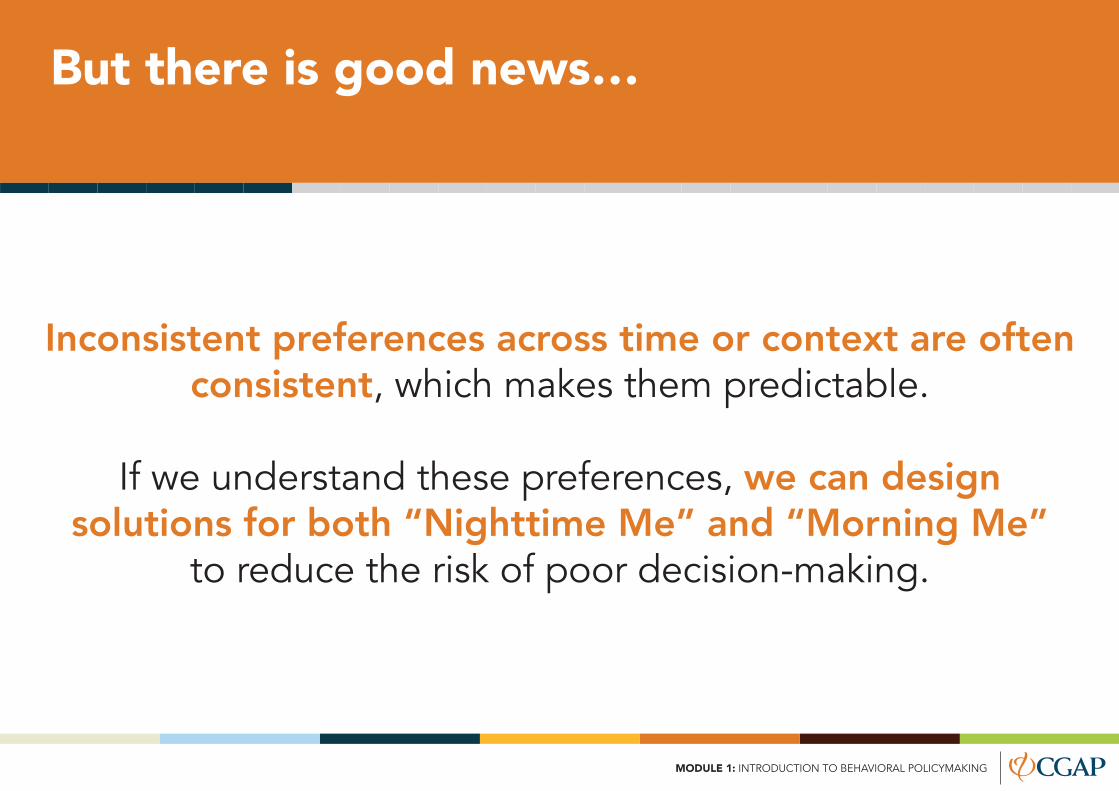

But there is good news…

Inconsistent preferences across time or context are often consistent, which makes them predictable.

If we understand these preferences, we can designsolutions for both “Nighttime Me” and “Morning Me”

to reduce the risk of poor decision-making.

1

MODULE 1: INTRODUCTION TO BEHAVIORAL POLICYMAKING

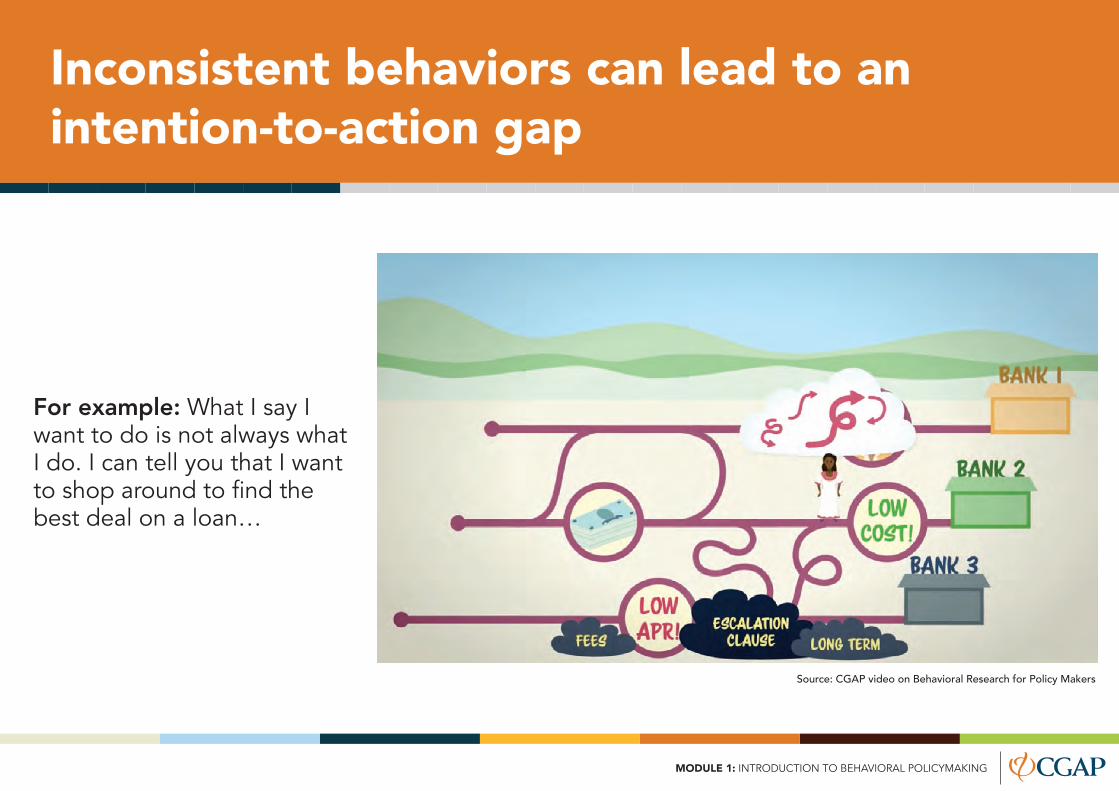

Inconsistent behaviors can lead to anintention-to-action gap

For example: What I say I want to do is not always what I do. I can tell you that I want to shop around to find the best deal on a loan…

Source: CGAP video on Behavioral Research for Policy Makers

MODULE 1: INTRODUCTION TO BEHAVIORAL POLICYMAKING

…but then I go to the bank closest to work because it is convenient, and I decide not to check other banks’ offers.

MODULE 1: INTRODUCTION TO BEHAVIORAL POLICYMAKING

MODULE 1: INTRODUCTION TO BEHAVIORAL POLICYMAKING

But there is good news here, too…

Inconsistent behaviors are often consistent acrossindividuals, which makes them predictable, meaningwe can design new tools—like an app that compares bank products available in a certain location—to help consumers achieve their stated goal of shopping

around for a savings account.

Non-economic factors can play a big rolein our economic decisions

In consumer finance, we may expose ourselves to greater financial risk because of decisions we make that have

very little to do with finance.

MODULE 1: INTRODUCTION TO BEHAVIORAL POLICYMAKING

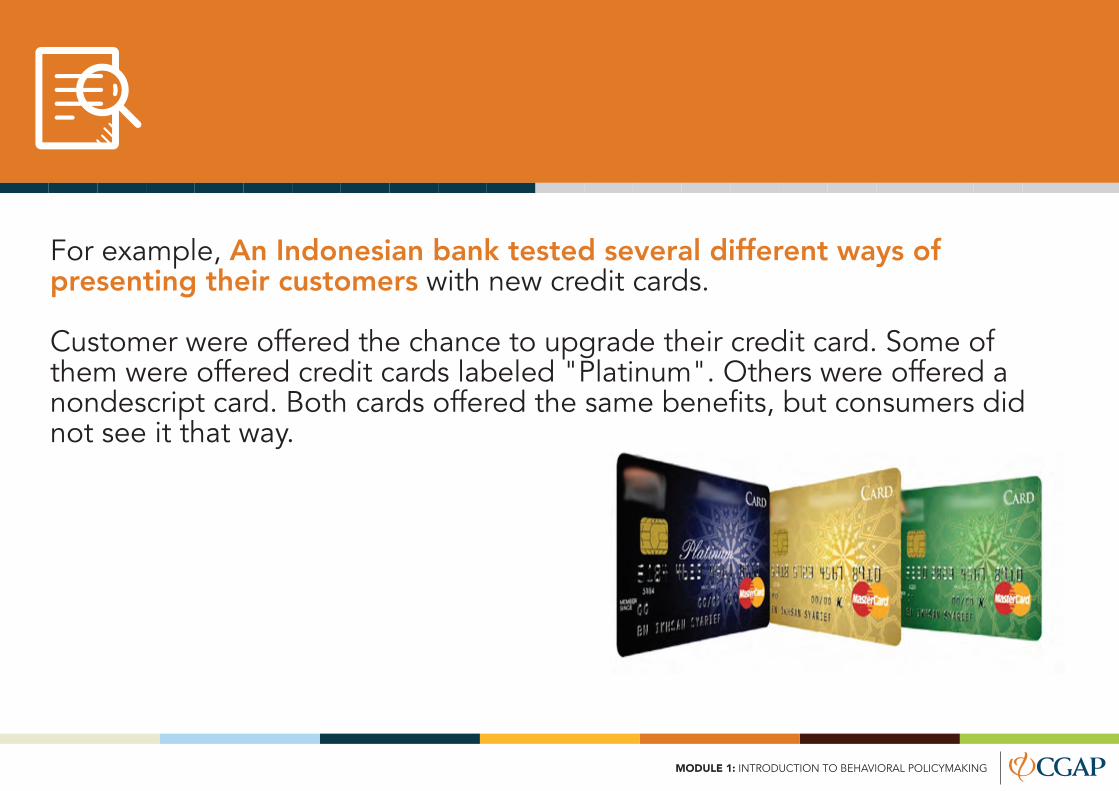

For example, An Indonesian bank tested several different ways of presenting their customers with new credit cards.

Customer were offered the chance to upgrade their credit card. Some of them were offered credit cards labeled "Platinum". Others were offered a nondescript card. Both cards offered the same benefits, but consumers did not see it that way.

MODULE 1: INTRODUCTION TO BEHAVIORAL POLICYMAKING

21% of customers who were offered the Platinum card accepted the offer.

14% of those who were offered the nondescript card accepted the offer.

Lower-income consumers showed more interested in the Platinum card than did higher-income customers.

Platinum cards were more likely to be used in social settings (bars, restaurants, etc.) than were the nondescript cards — consumers may have wanted to signal their Platinum status to their peers.

MODULE 1: INTRODUCTION TO BEHAVIORAL POLICYMAKING

How financial products are framed and positioned can greatly influencecustomer behavior.

Can a simple change in how disclosures are made helpconsumers avoid debt traps? Here’s a real-life consumer

protection design from the payday lending industryin the United States…

Behavioral research can identifychallenges — and it can solve them, too.

MODULE 1: INTRODUCTION TO BEHAVIORAL POLICYMAKING

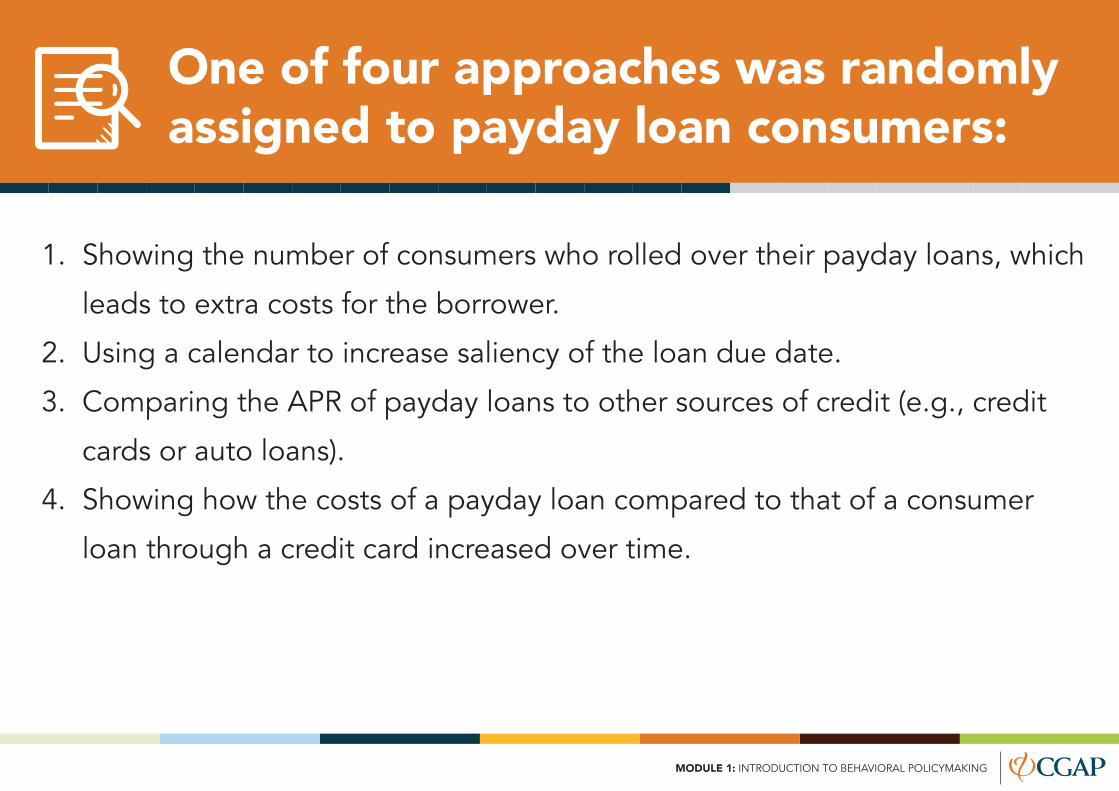

A payday lender in the United States worked withresearchers to test different types of disclosures of payday

loan costs and repayment obligations to see how theyaffected borrower behavior.

MODULE 1: INTRODUCTION TO BEHAVIORAL POLICYMAKING

1. Showing the number of consumers who rolled over their payday loans, which

leads to extra costs for the borrower.

2. Using a calendar to increase saliency of the loan due date.

3. Comparing the APR of payday loans to other sources of credit (e.g., credit

cards or auto loans).

4. Showing how the costs of a payday loan compared to that of a consumer

loan through a credit card increased over time.

One of four approaches was randomlyassigned to payday loan consumers:

MODULE 1: INTRODUCTION TO BEHAVIORAL POLICYMAKING

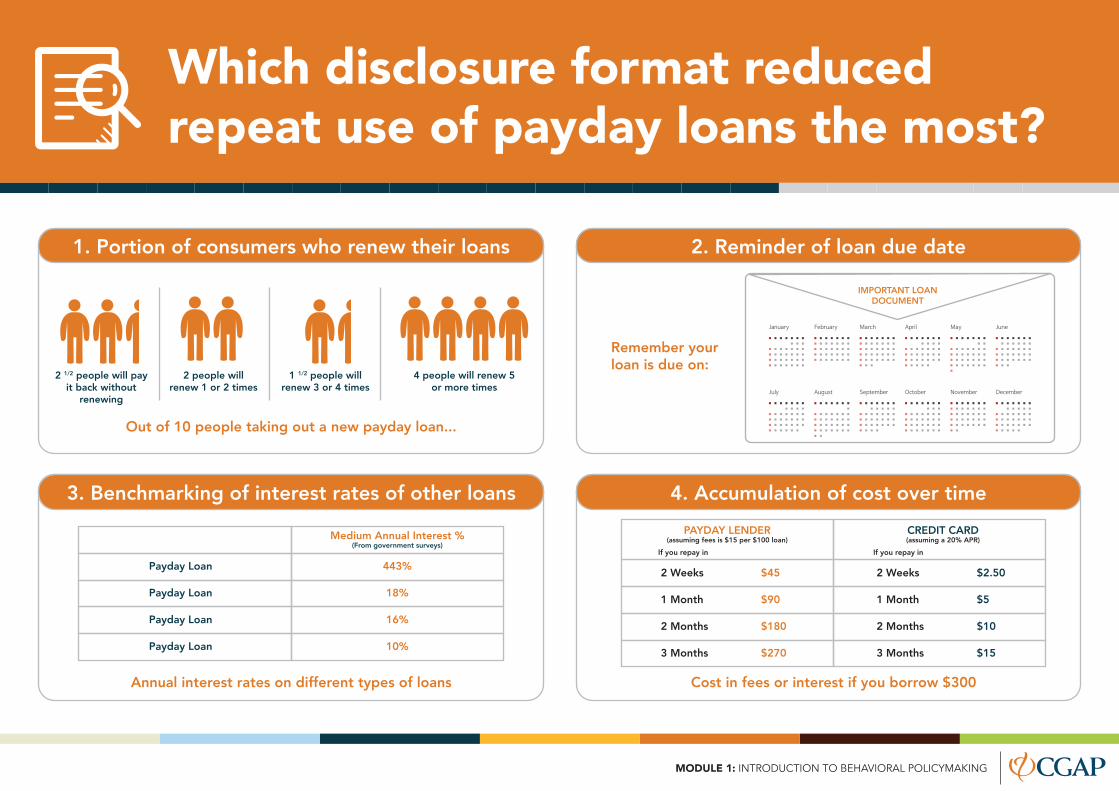

Which disclosure format reducedrepeat use of payday loans the most?

Out of 10 people taking out a new payday loan...

Remember yourloan is due on:

2 1/2 people will pay it back without

renewing

2 people willrenew 1 or 2 times

1 1/2 people willrenew 3 or 4 times

4 people will renew 5 or more times

1. Portion of consumers who renew their loans 2. Reminder of loan due date

Annual interest rates on different types of loans

3. Benchmarking of interest rates of other loans 4. Accumulation of cost over time

IMPORTANT LOANDOCUMENT

Payday Loan

Payday Loan

Payday Loan

Payday Loan

443%

18%

16%

10%

Medium Annual Interest %(From government surveys)

Cost in fees or interest if you borrow $300

2 Weeks $45

1 Month $90

2 Months $180

3 Months $270

2 Weeks $2.50

1 Month $5

2 Months $10

3 Months $15

CREDIT CARD(assuming a 20% APR)

PAYDAY LENDER(assuming fees is $15 per $100 loan)

If you repay in If you repay in

MODULE 1: INTRODUCTION TO BEHAVIORAL POLICYMAKING

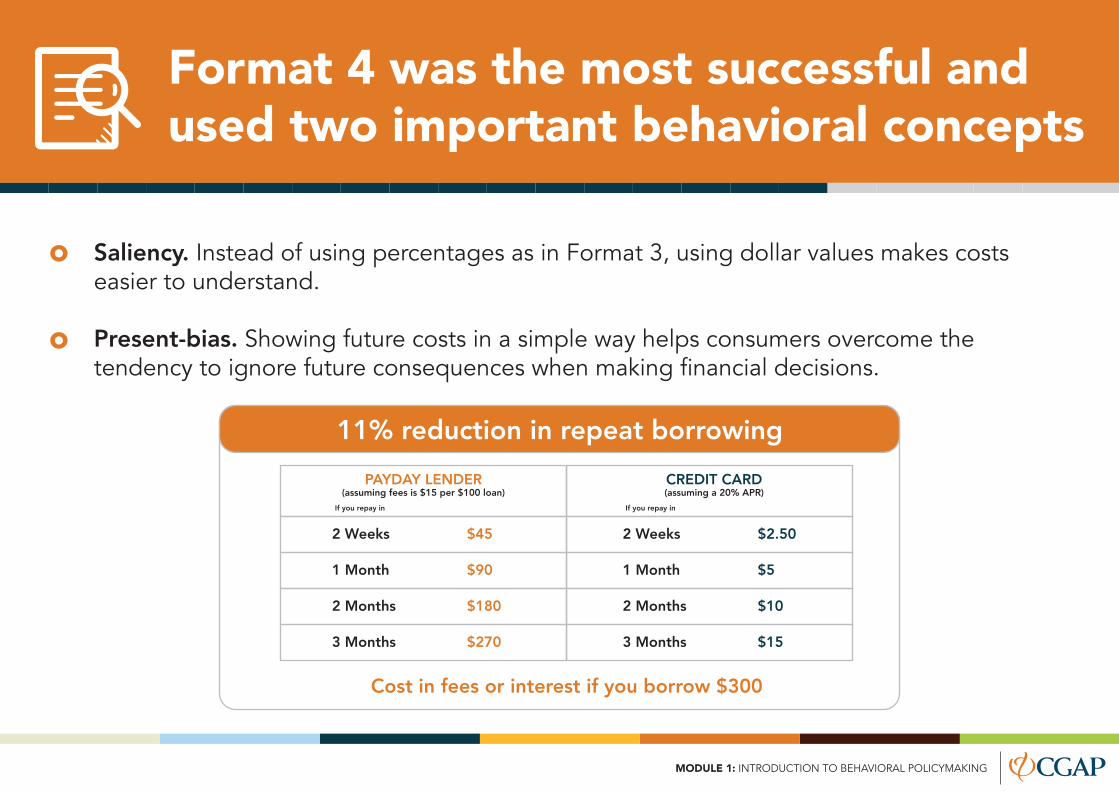

Saliency. Instead of using percentages as in Format 3, using dollar values makes costs easier to understand.

Present-bias. Showing future costs in a simple way helps consumers overcome the tendency to ignore future consequences when making financial decisions.

Format 4 was the most successful andused two important behavioral concepts

11% reduction in repeat borrowing

Cost in fees or interest if you borrow $300

2 Weeks $45

1 Month $90

2 Months $180

3 Months $270

2 Weeks $2.50

1 Month $5

2 Months $10

3 Months $15

CREDIT CARD(assuming a 20% APR)

PAYDAY LENDER(assuming fees is $15 per $100 loan)

If you repay in If you repay in

MODULE 1: INTRODUCTION TO BEHAVIORAL POLICYMAKING

Behavioral research sheds light on the choices and behavior of consumers

and providers. It helps policy makers test new policies and rigorously

measure how they impact consumer and provider behavior.

The next four slides describe the most relevant behavioral biases for

consumer protection. You can use these key insights to improve your

consumer protection policies.

Common Behavioral Biases inConsumer Protection Policy

MODULE 1: INTRODUCTION TO BEHAVIORAL POLICYMAKING

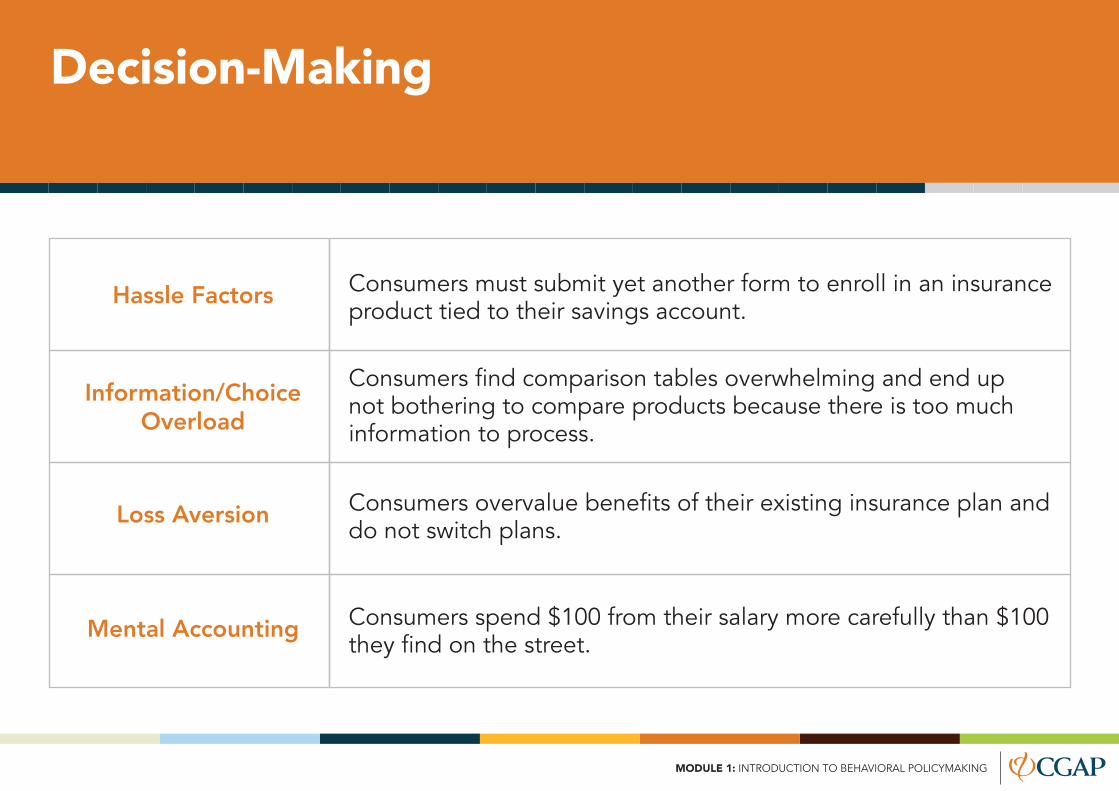

Decision-Making

Consumers must submit yet another form to enroll in an insurance product tied to their savings account.

Hassle Factors

Consumers overvalue benefits of their existing insurance plan and do not switch plans.

Loss Aversion

Consumers spend $100 from their salary more carefully than $100 they find on the street.

Mental Accounting

Consumers find comparison tables overwhelming and end up not bothering to compare products because there is too much information to process.

Information/ChoiceOverload

MODULE 1: INTRODUCTION TO BEHAVIORAL POLICYMAKING

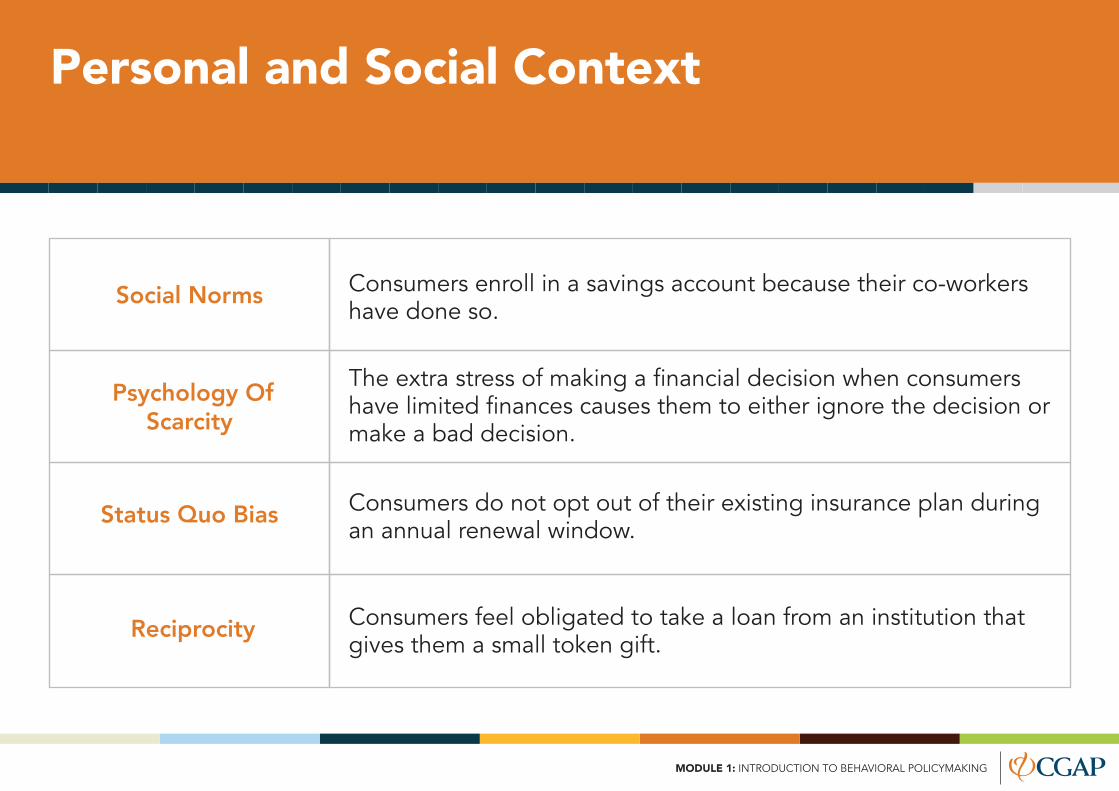

Personal and Social Context

Consumers enroll in a savings account because their co-workers have done so.

Social Norms

Consumers do not opt out of their existing insurance plan during an annual renewal window.

Status Quo Bias

Consumers feel obligated to take a loan from an institution that gives them a small token gift.

Reciprocity

The extra stress of making a financial decision when consumers have limited finances causes them to either ignore the decision or make a bad decision.

Psychology OfScarcity

MODULE 1: INTRODUCTION TO BEHAVIORAL POLICYMAKING

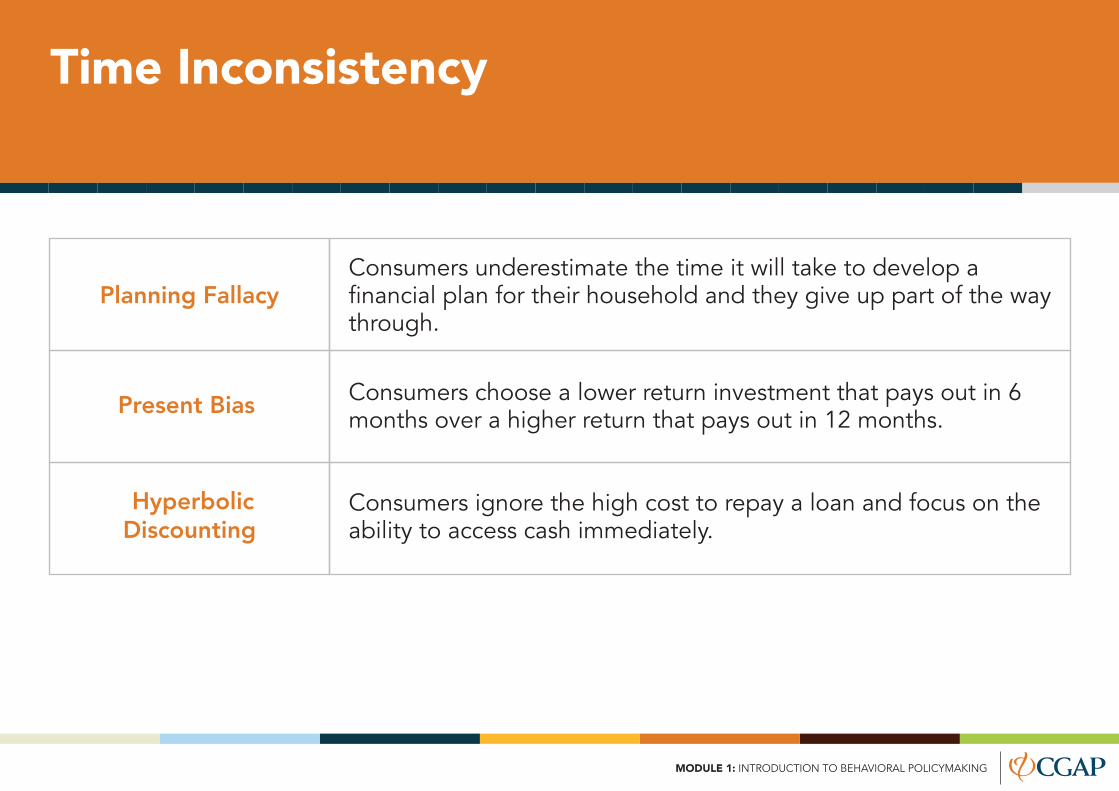

Time Inconsistency

Consumers underestimate the time it will take to develop a financial plan for their household and they give up part of the way through.

Planning Fallacy

Consumers ignore the high cost to repay a loan and focus on the ability to access cash immediately.

HyperbolicDiscounting

Consumers choose a lower return investment that pays out in 6 months over a higher return that pays out in 12 months.

Present Bias

MODULE 1: INTRODUCTION TO BEHAVIORAL POLICYMAKING

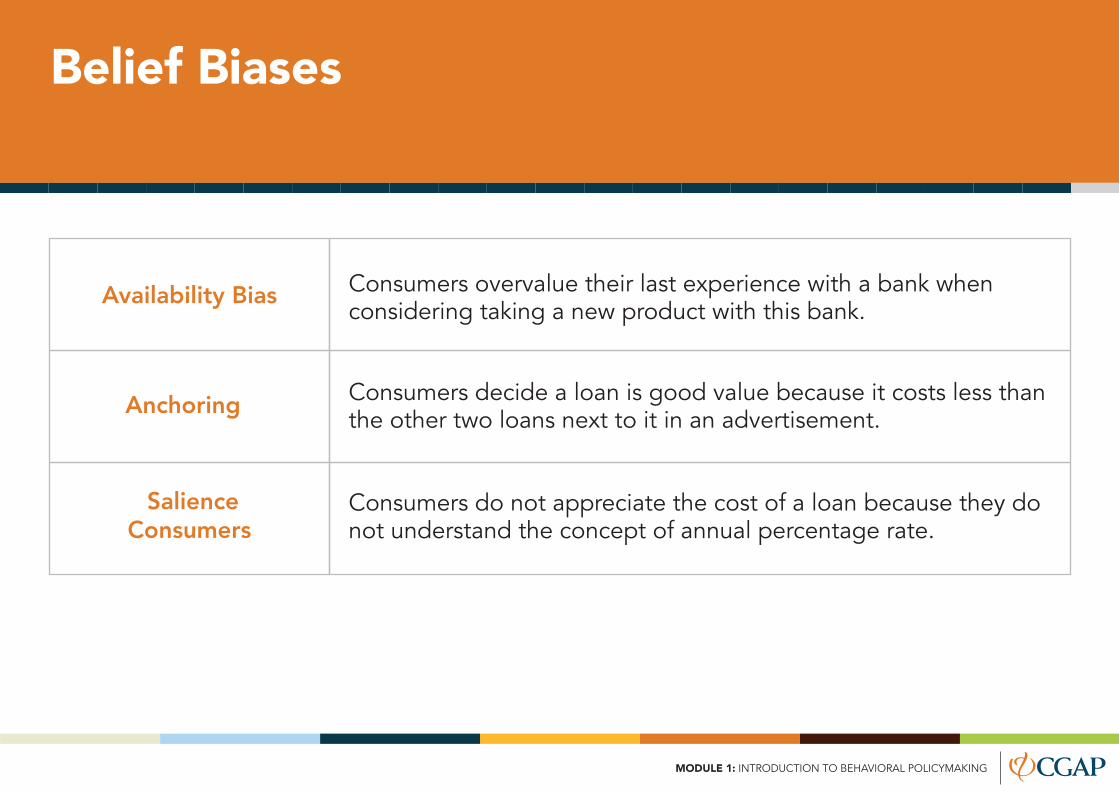

Belief Biases

Consumers overvalue their last experience with a bank whenconsidering taking a new product with this bank.

Availability Bias

Consumers do not appreciate the cost of a loan because they do not understand the concept of annual percentage rate.

SalienceConsumers

Consumers decide a loan is good value because it costs less than the other two loans next to it in an advertisement.

Anchoring

MODULE 1: INTRODUCTION TO BEHAVIORAL POLICYMAKING

This course comprises four short learning modules that connect behavioral concepts to consumer protection priorities policy makers face and share use cases from policy makers across the globe:

Disclosure and transparency

Fair treatment and sales practices

Recourse and complaints handling

Financial capability

Summary

MODULE 1: INTRODUCTION TO BEHAVIORAL POLICYMAKING

Learn how behavioral research helps you address four key consumerprotection policy challenges, click on one of these Learning Modules:

Transparencyand

disclosure

Salespracticesand fair

treatment

Recourseand

complaintshandling

Financialcapability

MODULE 1: INTRODUCTION TO BEHAVIORAL POLICYMAKING

Let’s get started!

Recommended