E-books Market in India

February 2015

2 E-BOOKS MARKET IN INDIA 2015.PPT

Executive Summary

Market Overview

E-book has been a known phenomenon in the global platform for quite some years and is posting a healthy growth

E-books market in India is still in its nascent stage but is slated to see good growth in the coming 1-2 years

E-books can be categorized into academic, trade and graphic novels

Drivers & Challenges

Competitive Landscape

Drivers: Growth in education Increase in internet users Demographical alterations Increase of internet enabled

computing devices Improvised content Publishers save costs in this format

Challenges:

Negative consumer perspective related to cyber security & piracy

High prices of e-book readers

Majority focus on academic text books

Lack of touch and feel element

Major Players

Company A Company B Company C

Company D Company E Company F

Application approval from Apple Retail chain offering e-book reading

application Drive to convert books into digital formats Foreign giant setting stores in India

Trends

Technological add-ons Digital rights management Sports category emerges as a thriving option

3 E-BOOKS MARKET IN INDIA 2015.PPT

•Macro Economic Indicators

•Introduction

•Market Overview

•Benefits

•Formats & Software

•Drivers & Challenges

•Government Regulations

•Trends

•Competitive Landscape

•Strategic Recommendation

•Appendix

4

Economic Indicators (-/-)

GDP at Factor Cost: Quarterly

Inflation Rate: Monthly

11

12

13

14

15

INR tn

Q4

c4

d2 c2

b2 a2

Q1

d1 b4

a4

Q3

c3

b3

a3

Q2

c1

b1

a1

2013-14 2012-13 2011-12 2010-11

0.0

0.5

1.0

1.5

2.0

%

Oct 2013 - Nov 2013

t

Sep 2013 - Oct 2013

s

Aug 2013 - Sep 2013

r

Jul 2013 - Aug 2013

q

Jun 2013 - Jul 2013

p

E-BOOKS MARKET IN INDIA 2015.PPT

5

SAMPLE

E-BOOKS MARKET IN INDIA 2015.PPT

Evolution of e-books

1991 2008 2007

• X

2012

• X

1995

• X

2001-

2006 2003

• X

• X

• X

X

X

X

• X

6

SAMPLE

E-BOOKS MARKET IN INDIA 2015.PPT

Though nascent, the market is slated to usher in a positive change in the coming 1-2 years

• Indian e-Book market is currently witnessing a positive growth and is expected to gain further momentum in the next 2-3 years

Basically, the huge presence of tech savvy youth and working class population is driving the demand for e-books in India

Additionally, educational institutions in an attempt to bring about innovation are incorporating the use of e-books in the curriculum

By the end of 2013, India had an estimated population of close to x mn e-book readers in India as compared to y mn as on Feb 2012

Although, the market accounts for merely x% of the total publishing market in the nation, nevertheless the sheer amount of the population is driving the market

E-books – Indian Market Overview

E-books – Market Segmentation (2013) E-books – Market Size & Growth

C

B

A

0

x4

2015e

x3

2014*

x2

2013

x1

INR bn

X

2018e

x6

2017e

x5

2016e Y

X

Y

X

Note: Others include ‘Trade’ and ‘Graphic Novels’ * Data corresponds to the month of Oct, 2014

7

SAMPLE

E-BOOKS MARKET IN INDIA 2015.PPT

The comparative study throws light on the pros and cons of using e-books over print books

X

• X

• X

Advantages

Print Books E-books

XX

Disadvantages

X

• X

• X

Advantages

Disadvantages

Print Book v/s E-book

8

SAMPLE

E-BOOKS MARKET IN INDIA 2015.PPT

• Under the agency pricing model, retailers act as agents and take a% while leave the remaining b% to the publisher

• The comparative analysis shows that even though retail price of e-books cost lesser than their printed counterparts, the payments made to different heads are also less which makes the end revenues generated by the publisher is more than the physical books

Print Book v/s E-book

E-book

Print Book

Retail Price per book

Paid to retailer Royalty

payment to author

INR X INR X

INR X

INR X

INR X INR X

INR X

INR X

The publisher receives ~ INR X per

unit sold

The publisher receives ~ INR X per

unit sold

Others

XX

9

SAMPLE

E-BOOKS MARKET IN INDIA 2015.PPT

• X

• X

• X

• X

• X

• X

Format and Software XX

Format and Software XX

• X

• X

• X

Format and Software XX

E-book – Formats & Software (-/-)

10

SAMPLE

E-BOOKS MARKET IN INDIA 2015.PPT

E-books will penetrate proportionately with the rise in internet penetration and its users

Increase in internet users Impact

• Xx

• Xx

• Xx

• Xx

• Xx

• Xx

• xx

Total Internet Subscribers – India Number of Broadband Subscribers – India

F

E

D

C

B

A

0

mn

Apr - Jun 2014 e

x4

Jan - Mar 2014e

x3

Oct - Dec 2013 e

x2

Jul - Sep 2013

x1

A

0

C

D

B

y4

Jan - Mar 2014e

y3

Oct - Dec 2013 e

y2

Jul - Sep 2013

y1

mn

Apr - Jun 2014 e

11

SAMPLE

E-BOOKS MARKET IN INDIA 2015.PPT

As Indians open up to newer innovations, e-books evolve as an addition to online shopping list

Demographical alterations Impact

• Xx

• Xx

• Xx

• Xx

• Xx

• Xx

C

B

A E

D

E

D

C

B

A

aa

C

B

A

0

X1

55+ years

X5

45-54 years

X4

35-44 years

X3

25-34 years

X2

15-24 years

bn minutes

Internet Users – Age-wise Distribution (2014) Average Time Spent on Internet – Age-wise

12

SAMPLE

E-BOOKS MARKET IN INDIA 2015.PPT

High prices of e-book readers acts as serious impediments for a rapid off-take of e-books

High prices of e-book readers Impact

• X

• X

• X

• X

• X

• X

• X

• X

13

SAMPLE

E-BOOKS MARKET IN INDIA 2015.PPT

This bill details on the copyright mechanism especially when digital copy gets imported

The Copyright (Amendment) Bill, 2010

• A • B • C • D

• A • B • C

• X • Y • Z

14

SAMPLE

E-BOOKS MARKET IN INDIA 2015.PPT

Approval from majors open gates for device manufacturers to feature e-books on their devices

• Xx • Xx • Xx • Xx

Application approval from Apple

• x

• x

• x

xx

xx

xx

xx

xx

xx

Features

T R E N D

15

SAMPLE

E-BOOKS MARKET IN INDIA 2015.PPT

Trends reveal that foreign giants are setting up stores in the country and introducing cheap product offerings

• Xx • Xx

Point A

• Xx • Xx

Point C

• Xx • Xx

Point B

• Xx • Xx

Point D

This initiative spells a positive trend as majors focus on this emerging market

Foreign giant setting stores in India

• xx • xx

16

SAMPLE

E-BOOKS MARKET IN INDIA 2015.PPT

Porter’s Five Forces Analysis

Competitive Rivalry

• X

Bargaining Power of Suppliers

• X

Bargaining Power of Buyers

• X

Threat of Substitutes

• X

Threat of New Entrants

• X

Impact X

Impact X

Impact X

Impact X

Impact X

17

SAMPLE Key Ratios of Top 3 Companies – Operational Basis (FY 2013) (-/-)

Competitive Benchmarking (-/-)

-20

-10

0

10

20

Company B

x2 x1

Company A

x2 x1

%

Company D

x2 x1

Company C

x2 x1

Operating Margin Net Margin

• XX

• XX

• XX

E-BOOKS MARKET IN INDIA 2015.PPT

18

SAMPLE

E-BOOKS MARKET IN INDIA 2015.PPT

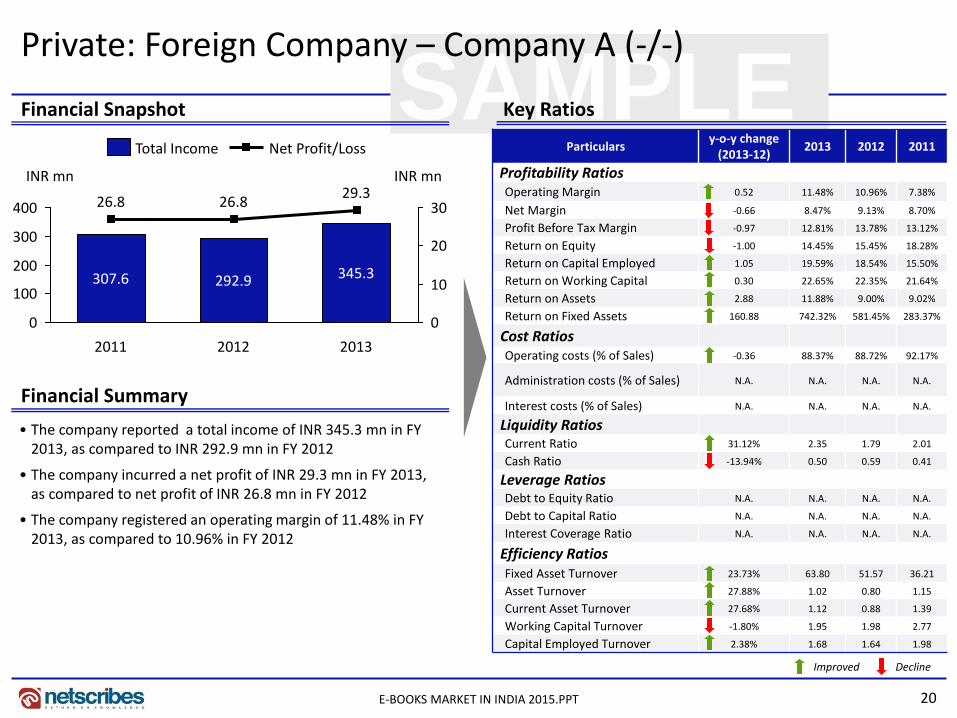

Private: Foreign Company – Company A (-/-)

Key People

Products and Services

Company Information Offices and Centres – India

Corporate Address XX

Tel No. XX

Website XX

Year of Incorporation XX

Category Products/Services

XX

Name Designation

XX XX

XX XX

XX XX

XX XX

Note: The list of products and services is not exhaustive

New Delhi

Head Office

19

SAMPLE Name No. of Shares held

Cengage Learning Holdings BV 1,832,268

Cengage Learning Hong Kong Ltd.

1

Total 1,832,269 100.00%

Foreign Holdings

Note: Shareholding pattern as on AGM dated 26th Sep 2014

Private: Foreign Company – Company A (-/-)

Shareholders of the Company Ownership Structure

E-BOOKS MARKET IN INDIA 2015.PPT

20

SAMPLE

E-BOOKS MARKET IN INDIA 2015.PPT

Financial Snapshot Key Ratios

Financial Summary

• The company reported a total income of INR 345.3 mn in FY 2013, as compared to INR 292.9 mn in FY 2012

• The company incurred a net profit of INR 29.3 mn in FY 2013, as compared to net profit of INR 26.8 mn in FY 2012

• The company registered an operating margin of 11.48% in FY 2013, as compared to 10.96% in FY 2012

Improved Decline

Particulars y-o-y change

(2013-12) 2013 2012 2011

Profitability Ratios

Operating Margin 0.52 11.48% 10.96% 7.38%

Net Margin -0.66 8.47% 9.13% 8.70%

Profit Before Tax Margin -0.97 12.81% 13.78% 13.12%

Return on Equity -1.00 14.45% 15.45% 18.28%

Return on Capital Employed 1.05 19.59% 18.54% 15.50%

Return on Working Capital 0.30 22.65% 22.35% 21.64%

Return on Assets 2.88 11.88% 9.00% 9.02%

Return on Fixed Assets 160.88 742.32% 581.45% 283.37%

Cost Ratios

Operating costs (% of Sales) -0.36 88.37% 88.72% 92.17%

Administration costs (% of Sales) N.A. N.A. N.A. N.A.

Interest costs (% of Sales) N.A. N.A. N.A. N.A.

Liquidity Ratios

Current Ratio 31.12% 2.35 1.79 2.01

Cash Ratio -13.94% 0.50 0.59 0.41

Leverage Ratios

Debt to Equity Ratio N.A. N.A. N.A. N.A.

Debt to Capital Ratio N.A. N.A. N.A. N.A.

Interest Coverage Ratio N.A. N.A. N.A. N.A.

Efficiency Ratios

Fixed Asset Turnover 23.73% 63.80 51.57 36.21

Asset Turnover 27.88% 1.02 0.80 1.15

Current Asset Turnover 27.68% 1.12 0.88 1.39

Working Capital Turnover -1.80% 1.95 1.98 2.77

Capital Employed Turnover 2.38% 1.68 1.64 1.98

30

20

10

0

400

300

200

100

0

29.3

345.3

2012

26.8

292.9

2011

26.8

307.6

INR mn INR mn

2013

Net Profit/Loss Total Income

Private: Foreign Company – Company A (-/-)

21

SAMPLE

E-BOOKS MARKET IN INDIA 2015.PPT

Business Highlights

Description News

Overview XX

E-books XX

Private: Foreign Company – Company A (-/-)

22

SAMPLE

XX XX

XX XX

T O

W S

Private: Foreign Company – Company A (-/-)

Strength Weakness

Opportunity Threat

E-BOOKS MARKET IN INDIA 2015.PPT

23

SAMPLE

E-BOOKS MARKET IN INDIA 2015.PPT

Strategic Recommendations (-/-)

Point A

• X

• X

• X

• X

• X

Point B

• X

• X

• X

• X

• X

• X

24 E-BOOKS MARKET IN INDIA 2015.PPT

Thank you for the attention

About Netscribes, Inc. Netscribes, Inc. is a knowledge-consulting and solutions firm with clientele across the globe. The company’s expertise spans areas of investment & business research, business & corporate intelligence, content-management services, and knowledge-software services. At its core lies a true value proposition that draws upon a vast knowledge base. Netscribes Inc. is a one-stop shop designed to fulfil clients’ profitability and growth objectives.

Disclaimer: This report is published for general information only. Although high standards have been used in the preparation, “Netscribes” is not responsible for any loss or damage arising from use of this document. This document is the sole property of Netscribes and prior permission is required for guidelines on reproduction.

The E-books Market – India 2015 report is a part of Netscribes, Inc.’s Information Technology Industry Series. For more detailed information or customized research requirements please contact:

Phone: +91 22 4098 7600 E-Mail: [email protected]

Recommended