This white paper was produced by Cascade Asia exclusively for informational reasons. While every effort has been

made to ensure the accuracy of the information and data contained herein, Cascade Asia bears no responsibility for

any errors or omissions. The information herein is given in good faith but without legal responsibility.

August 2016

Manufacturing in Indonesia New Options, Opportunities & Challenges

1

1

Executive Summary

Though it has yet fully regained its former dynamism,

Indonesia is increasingly being recognized for its

manufacturing competitiveness. The combination of relatively

low labor costs, favorable demographics, economic stability

and growth, natural resource endowments and market

expansion present a viable alternative for manufacturers

looking to shift production capacity away from China.

This white paper provides a snapshot of Indonesia’s

manufacturing sector and identifies the fastest growing sectors

and cost effective locations. By examining the size, growth

trajectory, supporting infrastructure developments and the

government’s targets and strategies within manufacturing this

paper touches on both the challenges and opportunities facing

the industry at present.

2

Introduction

Businesses looking for low-cost export platforms in Asia would do well to consider Indonesia one of the

top global manufacturing countries in the world. The country’s demographic landscape presents not only

a massive labor force of some 127 million but also a rapidly expanding middle class that is forecasted to

reach 140 million by 2020, almost doubling in size from 2012 (when it was estimated at 74 million

people). This relatively young and emerging consumer class will continue to drive domestic consumption

for the foreseeable future.

President Joko Widodo, known locally as Jokowi, is aggressively pursuing foreign direct investment and

targeting ambitious business environment improvements. Among these initiatives includes a massive

push for infrastructure upgrades across the country to ease notoriously high logistics costs across the

archipelagic nation, not just on Java and Sumatra islands as has been the focus of previous

administrations. He has set a target to improve Indonesia's ease of doing business ranking from 109th out

of 189 countries to 40th. During his 21 months in office he has also embarked on a sorely needed push to

dismantle a maze of overlapping regulations and removing red-tape by reducing bureaucratic approvals.

Indonesia is also one of the most politically and economically stable countries in Asia; a remarkable

achievement for the 18 year old democratic nation. Still, the country is not without challenges. Despite

the various improvements that Jokowi has introduced, transportation limitations and productivity issues

among other challenges remain.

3

Manufacturing and Indonesia’s Economy

Following oil price volatility in the late 1970s and 1980s, then oil-rich Indonesia diversified its economy

away from agriculture and commodities and towards manufacturing. Manufacturing remained a key

driver of Indonesia’s economy through the early and mid-1990s when non-oil and gas manufacturing

growth reached 12% per year and contributed to one-third of overall GDP growth. But in 1997 the Asian

financial crisis devastated Indonesia’s economy and lead to the toppling of Suharto, the country’s long-

serving president, a year later.

Combined, the economic and political shocks caused lower domestic demand and an overall deterioration

of the business environment. The industry was further stunted by a range of factors including rising

commodity prices, losing market share to Asian competitors and inflexible domestic labor laws.

Sources: BPS, Bappenas, World Bank

Since 2001, Indonesia’s manufacturing sector has grown at an average annual rate of 5.5% and has yet to

recapture its former dynamism. Non-oil and gas manufacturing now accounts for 18.1% of GDP (2015),

or approximately US$156 billion.

4

Source: BPS

When he assumed office in October 2014, President Jokowi pledged to make Indonesia’s manufacturing

industry more competitive and envisioned a revitalized manufacturing sector as a key part of bolstering

the country’s broader economic growth and absorbing the 2.3 million new workers that join the labor

force each year. Particularly since shaking up his cabinet in August 2015, the tenor and pace of the

government’s business climate improvements have intensified.

In May 2016 the newly revised Negative Investment List was released which outlined the Government of

Indonesia’s latest ruling on which sectors foreign investment is prohibited or restricted. Under this

revision, sectors like manufacturing of raw pharmaceutical materials is now 100% open (previously 85%

open). In essence, through liberalized market access, improving factor conditions like labor regulations

and land and infrastructure and through trade promotion efforts, the current administration is pursuing a

path which it hopes will eventually expand manufacturing’s share of GDP to 30% by 2035.

Recent evidence suggests Jokowi’s reforms may be having an impact. The Nikkei Indonesia

Manufacturing PMI exceeded 501 for the first time in President Joko Widodo’s presidency in March 2016

(50.6) and it has remained above 50 since. The industry has been trending toward a recovery since

January 2016. These changes have only further been complemented by the launch of a one-stop shop to

help expedite investment approvals, providing export incentives and import benefits for input materials

and dramatically ramping up trade promotion efforts.

Looking out on the horizon, President Jokowi has also expressed interest in joining the Trans-Pacific

Partnership (TPP) as a means of making Indonesia’s economy more competitive regionally and globally.

Some economists estimate that Indonesia’s exports would increase by some $2.9 billion and would ensure

that Indonesia remains competitive with Vietnam, one of the country’s toughest competitors. The move

1 Readings above 50 indicate an expansion in the manufacturing sector while readings below 50 indicate a

contraction.

5

would take two to three years and would require significant political wrangling but is a viable path

forward.

Manufactured Goods in Indonesia

Indonesia’s abundant natural resources provides a broad base for a diverse manufacturing industry and

rising personal incomes of its consumer class offers a strong growth driver. This is particularly true in the

food and beverage sector which is the largest manufacturing sub-sector in Indonesia. There are relatively

few manufacturers in Indonesia who have an international focus but local food and beverage

manufacturers are especially ambitious, several of whom successfully sell globally.

Source: Ministry of Industry

With manufacturing accounting for nearly a quarter of the country’s GDP, sluggish external demand on

the back of slowing global economic recovery since the 2007-2009 financial crisis has dampened

manufacturing growth. Since 2013, rising domestic wage growth rates are also cited by manufacturers as

an increasing concern. In the recent past (2012-2015), non-minerals and gas industry growth was mainly

driven by non-tech manufacturing like food and beverages, footwear and leather goods and jewelry.

During the first quarter of 2016, industries like automotive/machinery and electronics registered strong

growth that, if continued for the rest of the year, will mark their strongest performance in years.

6

Growth performance of Indonesia’s Manufactured Exports

Source: BPS, Ministry of Industry, Cascade Asia analysis

Cost and quality are among the most important factors manufacturers consider when deciding on where to

produce their goods. Cost considerations encompass factors such as wages, utility costs, real estate prices,

logistics costs, taxes and financial and fiscal incentives. While quality considers the broader ecosystem

which enables the manufacturing operations inclusive of labor, business environment and infrastructure.

Industries where Indonesia is cost competitive include automotive & components, chemicals and food &

beverage. Indonesia’s manufacturing labor costs are roughly one-third of those in China and, adjusting for

inflation, have remained comparatively flat. The average factory worker in China earns $29.70 per day,

compared with $10.40 in Indonesia. The industries that Indonesia is quality competitive include food &

beverage, tobacco, furniture, apparel and footwear.

Indonesia’s relative manufacturing strength has traditionally been in light manufacturing where it has

been competitive for years although the government is currently searching for way to graduate to

producing higher value goods. Specifically, the government is working on a policy to develop 10 priority,

higher value-added industries, including:

Food

Pharmaceutical, cosmetics and medical equipment

Textile, leather and footwear

Transportation equipment

Electronics, telecommunication and ICT

Power plant and energy generation

7

Capital goods, components and auxiliary materials

Upstream agriculture

Basic materials and non-metal mining materials

Oil, gas and coal

Indonesia’s Manufacturing Centers

Industry clustering is present in Indonesia’s manufacturing industry with most activities concentrating in

major urban centers like Jakarta, Bandung and Surabaya (all on Java island). Java and Sumatra are the

most populous and developed islands in Indonesia and are the preferred locations for manufacturing as

this is where skilled labor and access to good infrastructure is readily available.

Source: Tempo, Antara, Inilah

However, new clusters are forming outside of these areas due to high labor costs and infrastructure

bottlenecks. These include locations like Central Java and East Java where wages are roughly 40-50%

lower than in Jakarta, where new industrial zones are being installed and that are connected to the high-

speed train line that will eventually link Jakarta to Surabaya.

8

Comparison of key factors of production across Java

Key Factors Jakarta and

Surrounding Area Serang Bandung Central Java Surabaya

Labour Supply Available Easily Available Available Easily Available Easily Available

Minimum Wage

(2016)2

$233 $134 $169 $143 $228

Land Availability Available Easily Available Available Easily Available Easily Available

Land Cost Highest Medium to High Relatively High Low Relatively High

Time to Port of

Tanjung Priok

(hours)

1-2

2

(Merak Port also

an option)

3-4

(Patimban Port

will be

completed in

2017)

Roughly 4 days

(Tanjung Emas

Port also an

option)

Roughly 3 days

(Many products

shipped out from

Tanjung Perak)

Major

Manufacturing

Clusters

Full spectrum Marginal Textile and

garments

Textile and

garment,

furniture, and

automotive

Full spectrum

Source: Ministry of Human Rights, Ministry of Industry, HKTDC, Infopublik, Cascade Asia

The government aims to increase the proportion of manufacturers operating outside of Java from roughly

30% to 40% by 2025 and is in the process of establishing 36 new industrial hubs over the next 15 years

on islands other than Java. To date, Indonesia has 74 industrial zones, of which 67% are located on Java.

2 1 US$ = 13,298 rupiah exchange rate

9

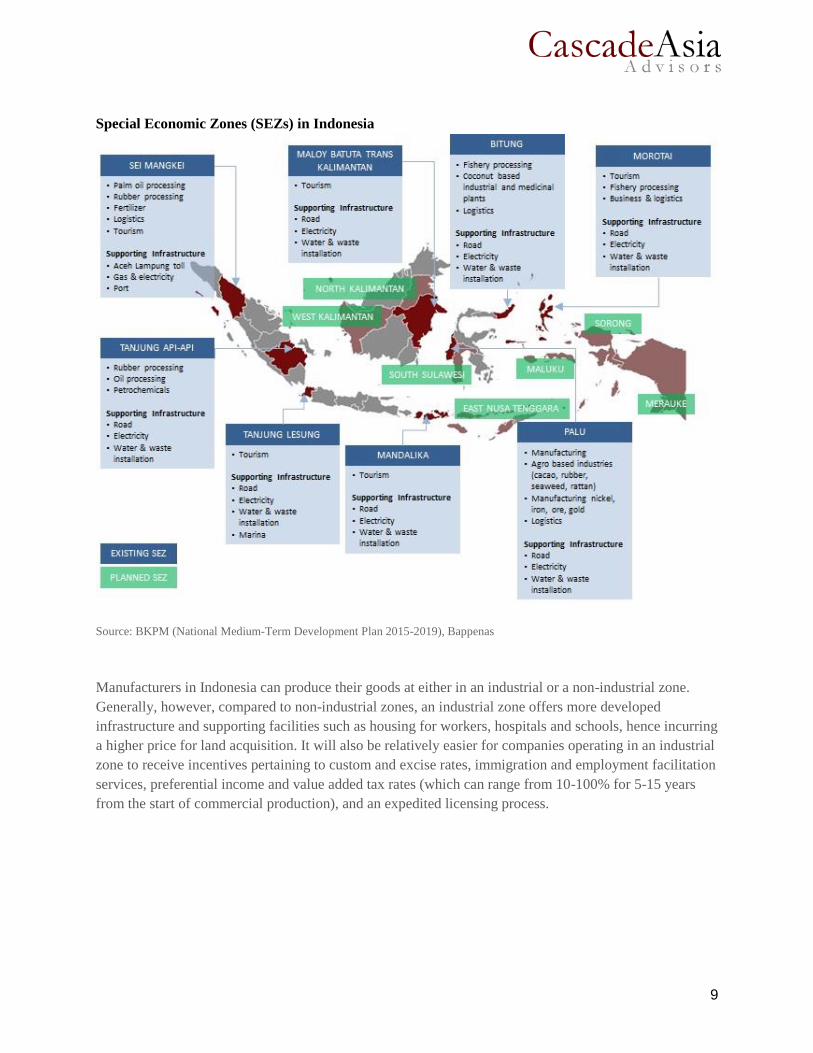

Special Economic Zones (SEZs) in Indonesia

Source: BKPM (National Medium-Term Development Plan 2015-2019), Bappenas

Manufacturers in Indonesia can produce their goods at either in an industrial or a non-industrial zone.

Generally, however, compared to non-industrial zones, an industrial zone offers more developed

infrastructure and supporting facilities such as housing for workers, hospitals and schools, hence incurring

a higher price for land acquisition. It will also be relatively easier for companies operating in an industrial

zone to receive incentives pertaining to custom and excise rates, immigration and employment facilitation

services, preferential income and value added tax rates (which can range from 10-100% for 5-15 years

from the start of commercial production), and an expedited licensing process.

10

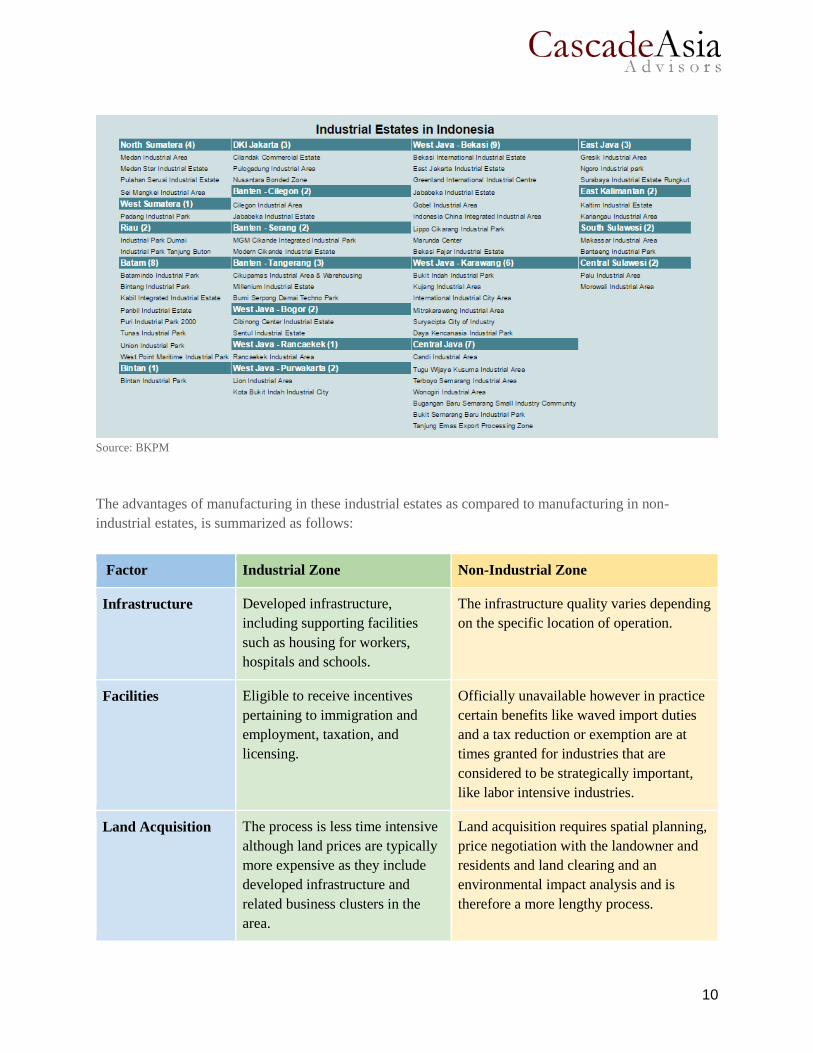

Source: BKPM

The advantages of manufacturing in these industrial estates as compared to manufacturing in non-

industrial estates, is summarized as follows:

Factor Industrial Zone Non-Industrial Zone

Infrastructure Developed infrastructure,

including supporting facilities

such as housing for workers,

hospitals and schools.

The infrastructure quality varies depending

on the specific location of operation.

Facilities Eligible to receive incentives

pertaining to immigration and

employment, taxation, and

licensing.

Officially unavailable however in practice

certain benefits like waved import duties

and a tax reduction or exemption are at

times granted for industries that are

considered to be strategically important,

like labor intensive industries.

Land Acquisition The process is less time intensive

although land prices are typically

more expensive as they include

developed infrastructure and

related business clusters in the

area.

Land acquisition requires spatial planning,

price negotiation with the landowner and

residents and land clearing and an

environmental impact analysis and is

therefore a more lengthy process.

11

Licensing Licenses are relatively easy to

obtain as the permitting process is

more streamlined. For instance, a

nuisance permit and an

environmental impact analysis are

not needed for investments in

industrial zones.

Investors will deal with local government

offices which are notorious for red tape.

Typical time to process these permits are

as follows:

1. Nuisance permit (10 working days)

2. Construction permit (15 working days)

3. Environmental impact analysis (75

working days)

Source: Ministry of Industry, BKPM

Indonesia’s Labor Market

With a workforce of approximately 127 million workers, few countries can match the size of Indonesia’s

working population. Indonesia’s labor costs are also relatively low when compared with other

manufacturing hubs in Asia.

Source: World Economic Forum, Wall Street Journal, FDRA

However, since the Asian financial crisis, Indonesia has struggled to make strides towards converging

with global productivity norms. Productivity in the country’s manufacturing sector is more than double

the productivity of the broader economy. Still, employers have argued that minimum wage increases need

to be tied to productivity gains though the government has not yet been willing to adopt such a wage

setting mechanism.

As part of President Widodo’s fourth economic stimulus package in October 2015, the government

announced the end to the failed tripartite mechanism for negotiating annual adjustments of wages on a

regional basis. In its place, the president signed Government Regulation on Wages (No. 78/2015)

ultimately opted for formula that accounts the current year’s inflation (at the provincial level) plus the

12

GDP growth rate. Though the new system is more centralized and transparent than its predecessor, the

government abandoned the most attractive component of the formula that appeared in an earlier draft,

namely the inclusion of productivity gains, though it is possible this could be included in a future

revision.

The Ministry of Manpower is the government agency responsible for planning strategic policies,

including among others, industrial relationships, employment supervision and all related employment

practices. The Manpower Law (No. 13/2003) and various implementing regulations set the legal basis for

employment in Indonesia. Labor disputes are directed to a labor court for resolution.

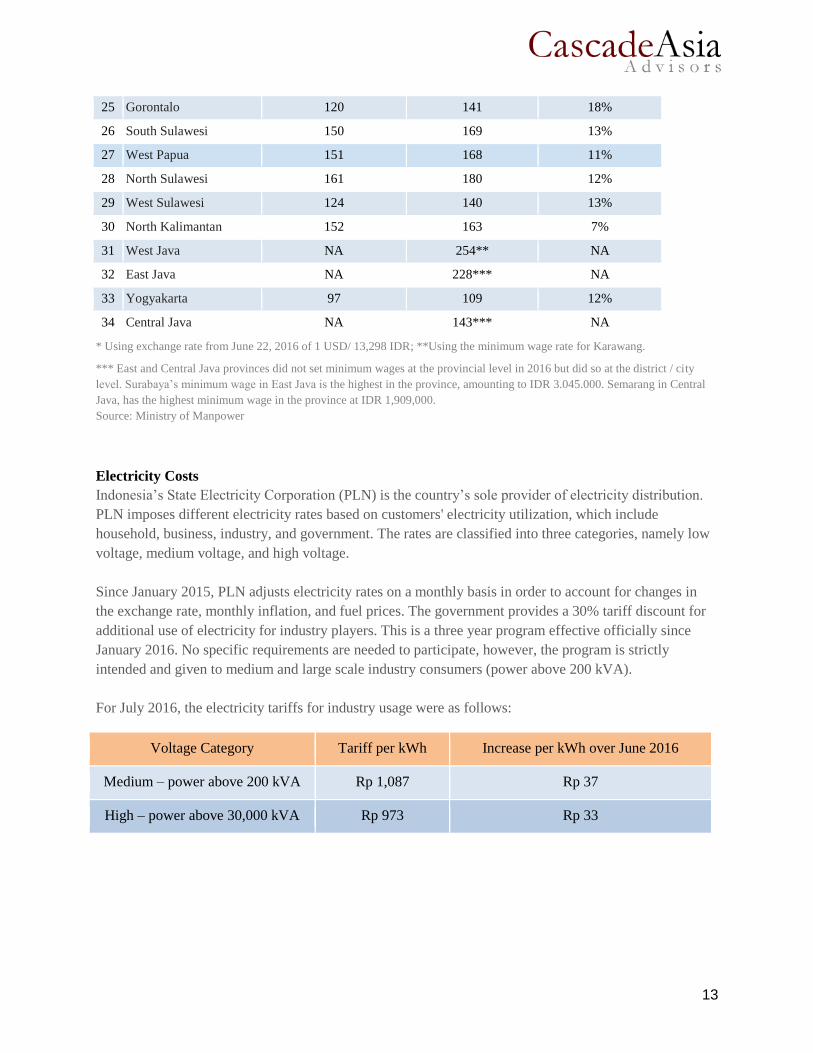

INDONESIA 2016 MINIMUM WAGES BY PROVINCE

Province

Monthly Minimum Wage (USD*) Growth (yoy, %)

2015 2016

1 Central Kalimantan 142 154 8%

2 West Kalimantan 117 130 11%

3 Jambi 128 143 12%

4 Southeast Sulawesi 124 139 12%

5 West Sumatra 121 135 12%

6 Bangka Belitung 157 176 12%

7 Papua 164 184 12%

8 Bengkulu 112 120 7%

9 Nusa Tenggara B. 100 111 11%

10 Nusa Tenggara T. 94 107 14%

11 Banten 120 134 12%

12 South Kalimantan 140 156 11%

13 DKI Jakarta 203 233 15%

14 Riau 141 157 11%

15 Riau Islands 146 163 12%

16 Bali 121 135 12%

17 North Sumatra 122 136 11%

18 East Kalimantan 152 162 7%

19 Aceh 142 159 12%

20 Lampung 118 132 12%

21 Central Sulawesi 112 125 12%

22 Moluccas 124 133 7%

23 North Moluccas 118 126 7%

24 South Sumatra 148 165 11%

13

25 Gorontalo 120 141 18%

26 South Sulawesi 150 169 13%

27 West Papua 151 168 11%

28 North Sulawesi 161 180 12%

29 West Sulawesi 124 140 13%

30 North Kalimantan 152 163 7%

31 West Java NA 254** NA

32 East Java NA 228*** NA

33 Yogyakarta 97 109 12%

34 Central Java NA 143*** NA

* Using exchange rate from June 22, 2016 of 1 USD/ 13,298 IDR; **Using the minimum wage rate for Karawang.

*** East and Central Java provinces did not set minimum wages at the provincial level in 2016 but did so at the district / city

level. Surabaya’s minimum wage in East Java is the highest in the province, amounting to IDR 3.045.000. Semarang in Central

Java, has the highest minimum wage in the province at IDR 1,909,000.

Source: Ministry of Manpower

Electricity Costs

Indonesia’s State Electricity Corporation (PLN) is the country’s sole provider of electricity distribution.

PLN imposes different electricity rates based on customers' electricity utilization, which include

household, business, industry, and government. The rates are classified into three categories, namely low

voltage, medium voltage, and high voltage.

Since January 2015, PLN adjusts electricity rates on a monthly basis in order to account for changes in

the exchange rate, monthly inflation, and fuel prices. The government provides a 30% tariff discount for

additional use of electricity for industry players. This is a three year program effective officially since

January 2016. No specific requirements are needed to participate, however, the program is strictly

intended and given to medium and large scale industry consumers (power above 200 kVA).

For July 2016, the electricity tariffs for industry usage were as follows:

Voltage Category Tariff per kWh Increase per kWh over June 2016

Medium – power above 200 kVA Rp 1,087 Rp 37

High – power above 30,000 kVA Rp 973 Rp 33

14

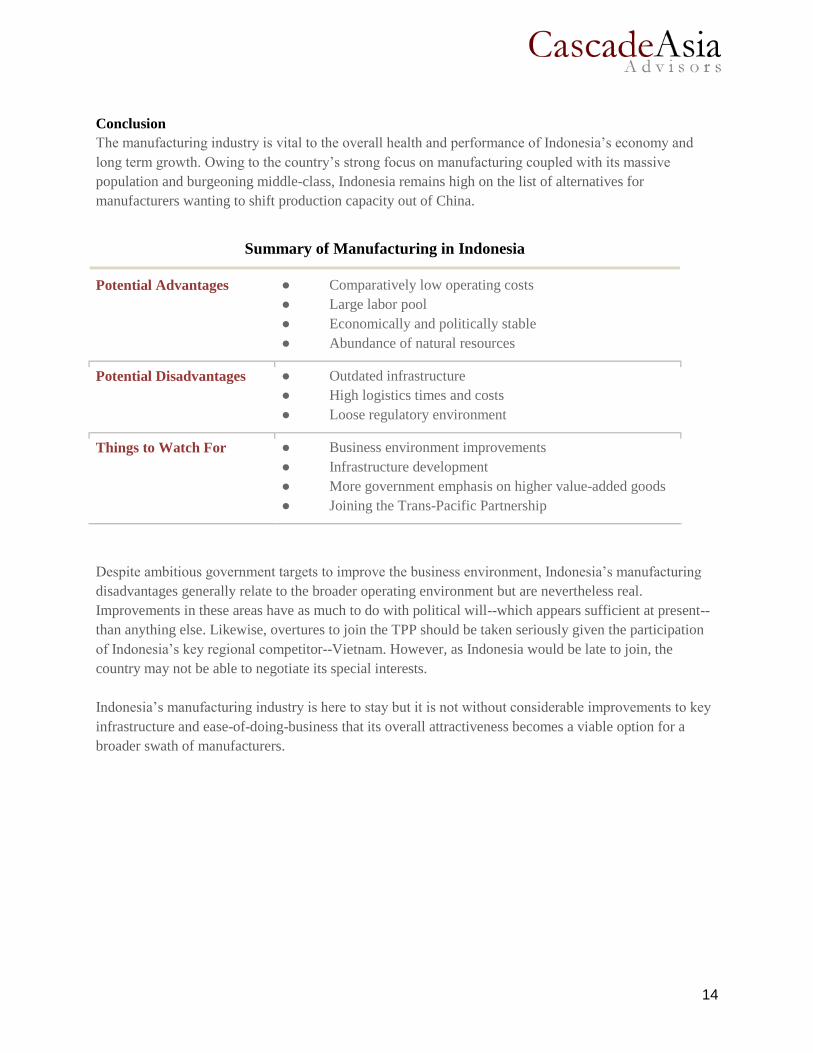

Conclusion

The manufacturing industry is vital to the overall health and performance of Indonesia’s economy and

long term growth. Owing to the country’s strong focus on manufacturing coupled with its massive

population and burgeoning middle-class, Indonesia remains high on the list of alternatives for

manufacturers wanting to shift production capacity out of China.

Summary of Manufacturing in Indonesia

Potential Advantages ● Comparatively low operating costs

● Large labor pool

● Economically and politically stable

● Abundance of natural resources

Potential Disadvantages ● Outdated infrastructure

● High logistics times and costs

● Loose regulatory environment

Things to Watch For ● Business environment improvements

● Infrastructure development

● More government emphasis on higher value-added goods

● Joining the Trans-Pacific Partnership

Despite ambitious government targets to improve the business environment, Indonesia’s manufacturing

disadvantages generally relate to the broader operating environment but are nevertheless real.

Improvements in these areas have as much to do with political will--which appears sufficient at present--

than anything else. Likewise, overtures to join the TPP should be taken seriously given the participation

of Indonesia’s key regional competitor--Vietnam. However, as Indonesia would be late to join, the

country may not be able to negotiate its special interests.

Indonesia’s manufacturing industry is here to stay but it is not without considerable improvements to key

infrastructure and ease-of-doing-business that its overall attractiveness becomes a viable option for a

broader swath of manufacturers.

15

Relevant Cascade Asia Publications

Indonesia Policy Monitor

Indonesia presents a host of challenges that can impede the ability

of foreign business players from operating at full stride. Among

these challenges, the multiple and often overlapping layers of

policy making and regulations makes for a complicated operating

environment. Cascade Asia developed the Indonesia Policy Monitor

as a complementary service to foreign players to help monitor

newly passed and pending legislation and regulations. Subscribe

Asia Light Manufacturing Outlook

The Asia Light Manufacturing Outlook is an executive-ready risk

assessment and outlook by our in-country analysts. Countries of

coverage include Cambodia, China, Indonesia and Vietnam. The

monthly outlook includes issues and events on the horizon,

inclusive of wage and currency forecasts. Customization is

available. Subscribe

Footwear Sourcing in Indonesia and Cambodia: Opportunities and

Risks

The analysis is designed to help footwear sourcing managers better

understand the socio-economic, regulatory, and political dynamics

in these countries as they look at alternative sourcing countries

outside China.

Footwear Sourcing Weekly

A multi-language media monitoring report across 11 key sourcing

countries tracking developments that impact operations and

reputations.

16

About the Authors

Adhiascha Iznandra Soemitro is an associate in the Jakarta office of Cascade Asia Advisors where he

focuses on due diligence and market research engagements. You may contacts him by email at

Garnadi Walanda Dharmaputra serves as a director in the firm’s Jakarta office. You may contact him

About Cascade Asia

Cascade Asia Advisors is a business intelligence advisory firm focused on Southeast Asia. We help

businesses anticipate risk and make informed decisions using forward-looking, on-the-ground business

intelligence. Please visit www.cascadeasia.com for more information.

Our Services

Vendor Screening

Commercial Due Diligence

Reputational Due Diligence

Business Intelligence

Market Entry Support

Policy & Regulatory Assessment

Government Relations

Stakeholder Mapping

Our Locations

Recommended