SM

Making Sense of Managed CareRegulation in CaliforniaNovember 2001

Making Sense ofManaged Care

Regulationin California

November 2001

Prepared for the California HealthCare Foundation

byDebra L. Roth

Deborah Reidy Kelch

476 Ninth Street Oakland, California 94607 Tel: (510) 238-1040 Fax:(510) 238-1388 www.chcf.org

Printed on recycled paper.

Acknowledgments

The authors thank the many individuals who participated in interviews and provided background for thisreport. In addition, the staffs at the Department of Managed Health Care and the Department of Insuranceprovided helpful comments and suggestions. Several people, including individuals from both departments,reviewed this report in draft form. Their feedback was valuable in the editing process. Maureen Sullivan pro-vided planning and research assistance for this project.

About the Authors

Debra L. Roth is an attorney and health care policy consultant with Ruderman & Roth in Sacramento. Herwork includes policy research and advocacy on a range of health care issues, including funding, managed care,and covering the uninsured. She has ten years of experience crafting health care legislation, including eightyears as a policy consultant to the California Legislature. During the 1997-98 session, Ms. Roth served asChief Consultant to the Assembly Health Committee.

Deborah Reidy Kelch, M.P.P.A., is an independent health researcher and president of Kelch AssociatesConsulting. Since 1995, Kelch Associates has published numerous health policy reports and articles, and pro-vides research, consulting, and strategic planning services to nonprofit organizations. Ms. Kelch served as poli-cy and fiscal consultant to the California Legislature for nearly ten years and assisted the Assembly HealthCommittee as policy consultant during staff transition periods in 1997 and 2001.

Copyright © 2001 California HealthCare Foundation

ISBN 1-929008-78-3

Additional copies of this and other publications can be obtained by calling the California HealthCareFoundation’s publications line at 1-888-430-2423 or visiting us online (www.chcf.org).

The California HealthCare Foundation (CHCF) is an independent philanthropy committed to improvingCalifornia’s health care delivery and financing systems. Our mission is to expand access to affordable, qualityhealth care for underserved individuals and communities and to promote fundamental improvements in thehealth status of the people of California.

C O N T E N T S

S e c t i o n 1 5Introduction

S e c t i o n 2 6History of the Knox-Keene Act

S e c t i o n 3 1 2Uncovering the Differences in Regulatory Frameworks

S e c t i o n 4 2 0Understanding the Products in the Health Coverage Marketplace

S e c t i o n 5 2 5Conclusion

Appendices 2 7

Notes 3 9

In California, regulation and oversight of healthinsurance is split between two state departments.The new Department of Managed Health Care(DMHC) primarily regulates health maintenanceorganizations (HMOs), while the CaliforniaDepartment of Insurance (CDI) has jurisdictionover traditional health insurance.

The 1999 legislation establishing the new DMHC(AB 78) transferred regulatory responsibility forHMOs from the Department of Corporations(DOC) to DMHC.1 AB 78 also requires DMHCto report to the Legislature by December 31, 2001on the feasibility of transferring regulatory jurisdic-tion of CDI-regulated health insurers to DMHC.

The two regulatory models, and their deficienciesand strengths, are the result of history, changingpolitical judgments and circumstances, andsweeping marketplace trends over a half-century.While the differences are rooted in distinct statu-tory frameworks and generally apply to discrete

product types, there have been many twists andturns along the way. Today, it can be difficult tounderstand why one regulator rather than anotherhas jurisdiction over a particular product orcompany.

This report considers the political history, currentstatutory and regulatory requirements, and thepredominant types of health insurance productsavailable in today’s market. The goal here is tocontribute to an informed discussion and debate aspolicymakers and stakeholders evaluate the optionswithin the context of the pending AB 78 report.

Research for this report included a review oflegislative history and relevant statutes, review ofmaterials provided by DMHC and CDI, review of other relevant research and reports, and keyinformant interviews with individuals who areparticularly knowledgeable regarding the evolutionand current status of health insurance regulation inCalifornia.

M a k i n g S e n s e o f M a n a g e d C a r e R e g u l a t i o n i n C a l i f o r n i a 5

Introduction 1

The Knox-Keene Health Care Service Plan Act of 1975, the current statutory framework underwhich HMOs and most managed care plansoperate in California, is very directly the result of the history and the times during which it hasevolved. This section provides a brief overview of that history and the evolution of prepaid healthcare and health insurance in California. A detailedchronology appears in Appendix A.

The story of health insurance in California is thestory of two systems developing in parallel: indem-nity health insurance, based on fee-for-serviceprovider payments and broad provider networks,alongside prepaid health plans, or HMOs, providingspecific services for a fixed monthly fee throughmore tightly organized and restrictive networks.2

Until the mid-1970s, Blue Cross, Blue Shield, andcommercial indemnity business, claimed the lion’sshare of the California market.3 Over time, costcontainment concerns yielded much of the marketto the HMOs with their relatively low-cost struc-tures and tighter management of service delivery.

Early Prepaid Health Care

One of the very first prepaid health plans wasestablished in 1929 when the Ross-Loos Clinic, a group practice of physicians, contracted toprovide care for workers in the Los Angeles waterdepartment.4

At about the same time, the Kaiser PermanenteProgram was emerging out of an effort in theMojave Desert to bring medical care to thousandsof workers laboring on the construction of the Los

Angeles Aqueduct. The physician who establishedthe on-site clinic approached Kaiser Industriesproposing to accept a prepaid fixed amount percovered worker to provide medical care for bothon-the-job and non-job related injuries. Theresulting Kaiser model was expanded to otherprojects in California and Washington and wasultimately made available to the public in 1945.

Blue Cross and Blue Shield

In the late 1930s, organized medicine and hospitalassociations around the country helped to establishBlue Cross (hospital coverage) and Blue Shield(coverage for physician services) plans. These plansaimed to shore up revenues dependent on theuncertainties of patient payments and, someobservers report, to block more radical changes in medical care delivery such as government healthinsurance.5

Historians dispute the first place in the countrywhere a Blue Cross plan developed, but many put the origins in Dallas, Texas. The first statutoryauthorization for a California Blue Cross plancame in 1937 legislation creating the new desig-nation of “nonprofit hospital service plan” subjectto regulation by the Insurance Commissioner. As a nonprofit hospital service plan, California BlueCross was exempt from paying the gross premiumstax applicable to other insurers.6

In 1939, the California Medical Association(CMA) founded the California Physicians Service(CPS), the nation’s first statewide, medical-society–controlled, prepaid plan, which would later becalled Blue Shield of California.

6 C a l i f o r n i a H e a l t h C a r e F o u n d a t i o n

2 History of the Knox-Keene Act

In the early 1940s, California’s Insurance Commis-sioner challenged Blue Shield’s contention that itwas not subject to the Insurance Code. In 1946,the California Supreme Court held that BlueShield (and prepaid health plans) are not in thebusiness of insurance and are not subject toregulation by the Insurance Code. The decisionrepresented the first distinction in California lawbetween the “promise to pay” (indemnity healthinsurance) and the “promise to deliver or arrangefor care” (prepaid health care).

According to key informants, Kaiser, Blue Cross,and Blue Shield resisted being regulated by CDI in the same way as commercial insurers for philo-sophical reasons, because they fundamentallybelieved that that they were not in the business of traditional insurance. Several key informantsalso suggested that these companies avoided CDIregulation because they were concerned about thepossibility of having to pay the gross premiums tax.

The Rise of Indemnity Health Insurance

The growth of health insurance (Blue Cross, BlueShield, and commercial indemnity coverage) wasdramatically fueled during World War II whenwages were frozen but benefits were not.7

Organized labor turned its bargaining strategy to benefits instead of wages.

By the early 1950s, health care became a routinebenefit of the workplace, with nearly eight out often workers in the private sector covered throughemployment by some type of voluntary, if limited,health care plan.8 In 1958, nearly two-thirds ofAmericans had coverage for hospital costs, then themost common type of health insurance coverage.

Knox-Mills Act

In 1965, concerned about the lack of any reg-ulatory framework for prepaid health plans inCalifornia, and the increasing potential that therewould be an effort to license them as insurers,Kaiser, Blue Shield, and Ross-Loos actively sup-ported passage of the Knox-Mills registrationprogram. Knox-Mills required “health care serviceplans” to “register” with the Attorney General.Much of the language in Knox-Mills continues in the present day Knox-Keene statute.

Knox-Mills was never considered to be a rigorouslicensing framework by either the plans or otherstakeholders. It was, however, the scandals thatemerged in the early Medi-Cal Prepaid HealthPlan (PHP) program that prompted the Legislatureto consider more substantive regulation of prepaidhealth plans.

Medi-Cal PHP Scandals

In 1971, Governor Ronald Reagan proposedsweeping reforms in the Medi-Cal program, whichincluded a strong emphasis on prepaid health plansas a means of reducing Medi-Cal costs.9

The problems began almost immediately. By mid-1972, the media was reporting misrepresentationsby health plan enrollers, poor quality of care, andfailure to provide promised transportation tomedical offices.10

Many newly organized PHPs were little more than schemes to funnel Medi-Cal dollars through a nonprofit shell to for-profit corporations ownedby the same providers. In some cases, the plansactually sold health plan “shares” to unscrupulousproviders who were hoping to reap huge profits inthe form of provider payments. Plan owners and

M a k i n g S e n s e o f M a n a g e d C a r e R e g u l a t i o n i n C a l i f o r n i a 7

partners siphoned off funds, leaving otherproviders without payment and the PHP shell in financial disarray.

In response to the complaints, the Legislaturepassed the Waxman-Duffy Act, which set regula-tory standards for Medi-Cal PHPs.11 Despite thenew requirements, problems grew.12

State and federal legislative investigations revealedthat California Department of Health Services(DHS) officials had shown favoritism to plansrepresented by former DHS staffers and hadrenewed licenses even where quality of care prob-lems had been documented.13 Investigators alsouncovered financial and/or political ties between a few legislators and plans, where legislators pres-sured DHS to approve new contracts or continueexisting ones despite evidence of potential abuses.A DHS deputy was even accused of impeding aninvestigation by the Los Angeles District Attorney’soffice.14 The written rules had changed, but theunwritten rules had not.

Federal HMO Act

The term “health maintenance organization” wascoined in 1973 with the enactment of the federalHMO Act, an attempt by federal policymakers tostem the “crisis” in health care cost inflation.15

The HMO Act established comprehensive benefits,community rating requirements, administrativeoversight procedures, requirements for financialreserves, annual open enrollments, prohibitions on pre-existing condition limitations, and otherrequirements. The Act recognized several differentmodels of plans and provided federal start-upgrants for nonprofit HMOs to encourage HMOexpansion and development.

Under the HMO Act, plans could choose to applyfor federal qualification and agree to meet therequirements of the Act. In return, HMOs wouldbe eligible for start-up grants and loans and couldmarket the HMO as meeting federal standards and requirements. In addition, the Act originallyrequired employers of more than 25 workers whoalready provided health benefits to offer as onechoice an available federally qualified HMO. Thisrequirement was phased out in the early 1990s. Inthe wake of the HMO Act, the number of HMOsgrew dramatically. By 1987, at least 16 new HMOshad appeared in California.16

The Time Is Right for Knox-Keene

In 1975, Governor Jerry Brown appointed thePrepaid Health Plan Advisory Committee toexamine the Medi-Cal PHP program. Amongother things, the Committee recommended that all Medi-Cal PHPs be required to meet the stan-dards in the federal HMO Act.

At the same time, there was increasing pressure to find a regulatory home for the expandingnonprofit Knox-Mills plans including Blue Shield,Kaiser, and Ross-Loos, which were subject to onlyminimal regulation under Knox-Mills.17

The Knox-Keene Health Care Service Plan Act of 1975 transferred regulatory authority from the Attorney General to the Department ofCorporations and established the basic frameworkfor regulation of health care service plans thatremains today. Knox-Keene was heavily influencedby the failures and inadequacies of the PHP pro-gram and also paralleled many provisions of thefederal HMO Act. The Act set rules for mandatorybasic services, financial stability, availability andaccessibility of providers, review of provider

8 C a l i f o r n i a H e a l t h C a r e F o u n d a t i o n

contracts, administrative organization, and con-sumer disclosure and grievance requirements.

According to key informants, the primary reasonsfor selection of DOC to regulate Knox-Keeneplans were: (1) Department of Health Services was universally viewed as incompetent in the wakeof the PHP scandals, and had a reputation as anunmanageable and unwieldy bureaucracy; (2)Legislative staff and other key stakeholders felt that the Department of Insurance was too friendlyto the interests of insurers; and (3) Stakeholdersbelieved that DOC could bring financial stabilityto the health plan industry, given DOC’s expertisein financial and investment regulation, while thedepartment could contract for or hire the requiredhealth care expertise.

The Act required all Knox-Mills plans to seekKnox-Keene licensure and, according to keyinformants, more than 100 plans applied for andreceived the new license.18 In addition, the new law required Blue Shield to become a Knox-Keeneplan but gave it and several specialized plans(dental and mental health) three years to reduce(but not eliminate) the portion of their businessthat “substantially indemnified subscribers.”19 BlueShield was essentially being told to look more likea prepaid health plan and less like an indemnitycarrier,20 although the company retained the abilityto offer products paying for services delivered bysome providers not under contract.21

Rising HMO Enrollment and the Development of PPOs

In 1982, faced with rising Medi-Cal costs, theLegislature enacted the selective hospital contract-ing program in Medi-Cal. Private insurers arguedthat hospitals would shift costs to the private sector

when their Medi-Cal revenues declined, promptingthe Legislature to repeal the Freedom of Choiceprovisions in the Insurance Code and authorizeinsurers to negotiate and enter into contracts withproviders at “alternative rates of payment.”22 Thestatute provides no further definition or detail onwhat that means. The Act also permitted carriers to limit claims payment to providers charging thealternative rates.

The resulting preferred provider organization(PPO) model of indemnity insurance—whereindividuals have reduced out-of-pocket costs ifthey use providers on the insurer’s preferred list—meant that indemnity carriers could move to bemore price competitive with Knox-Keene licensedHMOs. PPOs implemented utilization review andother cost containment strategies in an effort tocompete with the lower priced HMO plans. By1985, there were 60 PPO plans with nearly 4million covered lives in California.23

California’s health care market became intenselycompetitive. By 1990, there were more than 35HMOs in California with nearly 10 millionenrollees,24 all but six of which had been formedsince passage of the 1973 HMO Act.

HMOs Become Increasingly For-profit

In 1979, the federal HMO Act was amended topermit conversion of nonprofit plans to for-profitstatus. While Knox-Keene permitted both non-profit and for-profit plans since its inception, mostof the HMOs that were developing around thecountry, including in California, were nonprofit.This was primarily because of the availability offederal grants and loans for nonprofit HMOsunder the federal HMO Act. In the early 1980s,

M a k i n g S e n s e o f M a n a g e d C a r e R e g u l a t i o n i n C a l i f o r n i a 9

federal grants and loans were discontinued,prompting many HMOs to pursue for-profitconversions in the search for capital. As a result, awave of conversions of California HMOs occurredthrough the 1980s and into the 1990s.

Blue Cross Moves to Knox-Keene

Blue Cross of California (BCC) continued tooperate as a nonprofit hospital service plan underthe Insurance Code throughout the 1970s and1980s.25 In the early 1990s, a complex combina-tion of political and economic events promptedBCC to seek Knox-Keene licensure. One issue,according to key informants, was the concernamong insurers that BCC’s poor financial condi-tion at the time might result in BCC insolvencyand become a drain on the new health insuranceguarantee fund at CDI. This concern led to therequirement in the legislation establishing theHealth Insurance Guarantee Fund that BCC apply for Knox-Keene licensure by 1991.26

In 1993, BCC obtained multiple Knox-Keenelicenses for health, pharmacy, and dental business.BCC also submitted an initial proposal for“restructuring” of assets that included BCCownership of a large for-profit subsidiary,Wellpoint Health Networks, which in turn owned three nonprofit Knox-Keene licenses.

The ultimate restructuring of BCC was legally and technically complex, controversial, and heavilydebated in legal, legislative, and public forums.After a prolonged legislative and regulatorystruggle, BCC reached agreement with policy-makers and DOC (as its regulator) to dedicatemajor corporate assets to charitable purposes andto maintain a single license as a for-profit healthcare service plan.

BCC was granted specific statutory authorityunder Knox-Keene, similar to the originalauthority provided for Blue Shield, allowing BCC to continue offering PPO products.27

The New Department of Managed Health Care

As providers, consumers, and consumer advocateswitnessed the dramatic changes in health caredelivery precipitated by the growth in managedcare, they increasingly sought legislative andregulatory changes in how HMOs operate and are regulated. Throughout the 1990s, Knox-Keene(and to a large extent the Insurance Code) wasamended to include a series of additional benefitand provider mandates, new provider contractingand claims payment requirements, and changes tocoverage and contract requirements.

In 1997, the statutorily mandated Managed HealthCare Improvement Task Force put forward a seriesof reform recommendations. These included theneed for a new agency to regulate Knox-Keeneplans, and phased-in regulation of other entities,including other health insurance carriers andorganized medical groups.

In 1999, the Legislature passed a series of managedcare reforms, including AB 78, which created thenew Department of Managed (Health) Care. Inaddition, 20 other bills, referred to by consumeradvocates as the “Patient Bill of Rights,” wereenacted in 1999:

■ Guaranteed coverage for second opinions;

■ Time limits on utilization review and mandateddisclosure of the criteria health plans use indenying coverage;

10 C a l i f o r n i a H e a l t h C a r e F o u n d a t i o n

■ Independent external medical review to resolvedisputes related to denials, delays, or modifica-tions of coverage;

■ Improvements in the external review system forcoverage of experimental treatments;

■ Consumer right to sue an HMO for damagesrelated to denials or delays in care;

■ Standards to assure the solvency of medicalgroups under contract with health plans; and

■ Specific mandated benefits, such as mentalhealth parity, contraception, hospice, cancerscreening, and coverage for diabetes supplies.

In July 2000, the new Department of ManagedHealth Care (DMHC) opened its doors. DMHCis currently divided into teams: the HMO Help

Center, Enforcement, Legal Services, Health PlanOversight, Administrative Efficiency, Technologyand Innovation, and Staff Leadership.28

Three boards advise DMHC: the AdvisoryCommittee on Managed Care, the ClinicalAdvisory Panel, and the Financial SolvencyStandards Board. The meetings of these boards and their subcommittees are open to the public.

The Advisory Committee on Managed Care iscurrently considering the regulation of health plansand indemnity insurers in response to the AB 78requirement that DMHC study the feasibility oftransferring the regulation of health insurance from CDI to DMHC. The report is due to theLegislature in December 2001.

M a k i n g S e n s e o f M a n a g e d C a r e R e g u l a t i o n i n C a l i f o r n i a 11

Although both departments regulate carriersproviding health coverage, DMHC and CDIapproach regulation very differently, primarilybecause the various carriers they regulate, and the statutory authority under which they regulate,are very different. At the heart of the distinctionbetween “disability insurers”29 and “health careservice plans”30 is the “promise to pay” versus the“promise to deliver care.”

Under Knox-Keene, health care service plans(commonly referred to as HMOs) actually arrangefor and organize the delivery of health care andservices through contracted or owned providersand facilities. Disability insurers protect against(indemnify) the expenses or charges (losses)associated with illness or injury. A disabilityinsurance policy, or indemnity policy, providescoverage for defined benefits related to the insuredevent—accident, illness, or other covered healthcondition or situation. This is the traditionalconcept of indemnity insurance, and appliesgenerally to all forms of insurance, including ahome destroyed by fire or an automobile destroyedin a collision.

Another inherent difference between a health careservice plan and a disability insurer is the nature of the protection afforded consumers under eachcoverage type. Knox-Keene HMOs assume the riskand pay for all medically necessary covered servicesfor one monthly, prepaid payment; insurers paymedical expenses or a portion of medical expensesaccording to the specific coverage under the con-tract. In effect, under Knox-Keene, consumers arenot financially affected by variations in either costor utilization, outside of specified copayments or

other contract cost-sharing provisions. This isbecause the health plan provides (or contracts for)the services, rather than making payments to covera specific dollar loss (charges), or percentage of theloss, as in indemnity insurance.

Providers may look to their patients with indem-nity coverage to pay costs or charges regardless of whether or how much the insurer indemnifies(reimburses the patient) for the services. However,contracts between Knox-Keene HMOs and pro-viders must specifically prevent the providers fromseeking payment directly from enrollees for coveredservices if the health plan fails to pay.

Marketplace Changes Blur the Distinctions

Over time, the differences between these twomodels of health coverage have been obscured orblurred for many observers and stakeholders. Thereare two primary reasons for this.

First, there have been two significant exceptionsmade in law and regulation in the types of carriersregulated as Knox-Keene plans. Through thehistorical and statutory authorizations describedabove, both Blue Cross and Blue Shield arelicensed as health care service plans, but along with several specialized plans are able to also offerPPO contracts, a type of contract otherwise subjectto CDI licensure and more commonly associatedwith indemnity insurance.31

Second, over the past several decades, theLegislature has authorized both health plans andinsurers to offer new types of policies and contracts

12 C a l i f o r n i a H e a l t h C a r e F o u n d a t i o n

3 Uncovering the Differences in Regulatory Frameworks

that appear more similar than different. Insurershave increasingly offered PPO policies with whatlook like delivery systems, where a published list of “preferred” providers offer their services atdiscounted rates, reducing out-of-pocket costs forconsumers who use the PPO network to obtainhealth care. Health care service plans (HMOs) arenow able to offer point-of-service (POS) contracts,allowing enrollees to receive some services outsideof the network of contracted or employed provid-ers, if they are willing to pay increased out-of-pocket costs for these choices.

Moreover, virtually all health coverage today(whether health plan or disability insurance carrier)has some elements of “managed care” including,for example, prior authorization, coverage limitedto medically necessary care, and utilization review.These hybrid products have in some respectsblurred the distinctions between health plans andinsurers for consumers, policymakers, and otherkey stakeholders.

Key Informant Impressions

Key informants interviewed for this project offeredthe following opinions and observations about thetwo models of health coverage and the respectiveregulation by each department. Appendix E liststhe key informants who were interviewed.

Current System Is Confusing to ConsumersSince the department of jurisdiction for differenthealth insurance products is based in part onhistory and legal technicalities, the differences areinvisible or too complex for consumers to recog-nize. As a result, the dual regulatory system isdifficult for consumers to navigate when they have problems with their health care.

Key informants agreed that DMHC, in existencefor little more than one year, is seen as moreconsumer oriented than the entity that previouslyregulated health plans, the Department ofCorporations. Some key informants also felt that CDI was potentially less consumer friendlybecause CDI’s consumer complaint system isgenerally more limited than DMHC’s system. This is because DMHC has a statutory mandate toreview and resolve complaints related to the qualityof health care services while CDI does not.

Departments Have Different Strengths and WeaknessesEach department regulates in a fundamentallydifferent way. Consequently, key informantsviewed DMHC’s emphasis on insuring quality ofcare as generally more burdensome for health plansin the regulation of adequacy of in-network care,benefit design, consumer complaints, and qualityreview. Virtually all key informants viewed CDI as stricter in the application of financial and claimspayment standards and a more rigorous enforcer offinancial solvency and reserve requirements.

Consumer Recourse Is DifferentThe two types of coverage result in very differentrelationships between consumers and carriers andbetween consumers and providers.

An individual covered by an insurance productindependently selects and deals directly with theprovider, is generally responsible for payment and, if not satisfied, can exercise the option tochange providers. An insured can register com-plaints with CDI, but CDI does not have thestatutory authority to become directly involved in resolving consumer complaints about medicalservices or providers. CDI does enforce laws andregulations related to claims, underwriting, andrating practices. According to CDI, by enforcing

M a k i n g S e n s e o f M a n a g e d C a r e R e g u l a t i o n i n C a l i f o r n i a 13

these requirements, the department is able toensure that consumers are paid for the medicalservices necessary for their treatment.

In contrast, a person covered by an HMO contracthas less flexibility in changing providers, is subjectto greater plan involvement in the delivery ofservices, but can seek assistance from the plan inresolving issues relating to a provider or the qualityof care. Consumers are required to use the healthplan grievance system but can go to DMHC if theplan does not resolve the issue or act in a timelymanner.

Products and Companies Are DifferentCompanies operating health care service plans, as a general rule, have a business focus on healthcoverage. However, for many companies offeringdisability insurance, health is just one smallportion of their overall business, which typicallyalso includes life insurance and may includemultiple other forms of individual and corporateinsurance. Large indemnity insurers with multiplelines of insurance have a different corporate culturethat reflects the business of insurance, not healthcare.

Traditional indemnity health insurance regulatedunder CDI represents a decreasing portion of theoverall health coverage market, with key infor-mants estimating that indemnity represents only 5to 10 percent of the total health coverage market.32

Comparing Statutes and Regulations

This section includes an overview of the statutoryand regulatory differences between disabilityinsurers and health care service plans. Table 1summarizes the differences, which are discussed

more fully below. Appendix B contains a detailedstatutory comparison.

Initial LicensureHealth care service plans apply for and obtain aKnox-Keene license prior to operating in Califor-nia. Disability insurers obtain a certificate ofauthority from the Insurance Commissioner forthe specific line(s) of business they intend to offerprior to conducting insurance business in the state.

In applying for licensure, a health care service plan must submit for review and approval all of the types of plan contracts (policies) it will offer,standard provider contracts and payment methods,proposed advertising and marketing materials,audited financial statements, administrative struc-ture, projections of financial viability, actuarialanalyses, and specific proposed service areas.

The CDI certificate of authority review processinvolves a detailed operational and financial review.The application process includes review of thecompany’s financial stability, available capital andassets, competency and integrity of ownership andmanagement, claims payment procedures, actuarialcertifications, and financial projections. Insurerssubmit their policy forms for review and aresubject to specific “market conduct” (claimshandling) requirements and procedures oftenreferenced as the Fair Claims Practices rules.

While both health care service plans and insurersare required to demonstrate administrative capacityand financial solvency, a health care service planmust also provide a detailed outline of the pro-posed delivery system for in-network care anddemonstrate network adequacy. There is generallylittle or no specific review of the adequacy ofnetworks for insurers, regardless of the type of plan or product they are offering.

14 C a l i f o r n i a H e a l t h C a r e F o u n d a t i o n

M a k i n g S e n s e o f M a n a g e d C a r e R e g u l a t i o n i n C a l i f o r n i a 15

Table 1: Comparing the Functions of CDI and DMHC

Area of Oversight CDI Requirements DMHC Requirements

Primary Focus Ability to pay claims. Ability to deliver care.

Benefits Specific mandated benefits but nominimum benefit package.

Specific mandated benefits plus “basichealth care services.”

Quality No oversight of medical care.

Disclosure and standards for utilizationreview and utilization management.

On-site medical surveys, including on-siteprovider reviews, and mandatory internalquality assurance system.

Disclosure and standards for utilizationreview and utilization management.

ProviderAccessibility

No accessibility standards enforced. Providers must be “readily available andaccessible,” subject to DMHC review.

ProviderPayments

Provider payments limited to fee-for-service and negotiated discount rates.

In addition to fee-for-service and discountrate options, plans may share risk withproviders (e.g., capitation).

ConsumerProtection

Same as those applicable to all lines ofinsurance: consumer disclosure, FairClaims Practices Act (market conduct).Complaints can be filed with CDI.

Independent Medical Review for denials of care.

Consumer disclosure requirements,complaints handled through internal plan grievance system with DMHCintervention if necessary.

Independent Medical Review for denials of care.

FinancialReserves

Reserves based on the greater of: $5million statutory minimum capital or 200 percent of the Risk-Based Capitalstandards developed by the NationalAssociation of Insurance Commissioners.Generally higher than reserverequirements for Knox-Keene plans.

Insurers required to join GuaranteeAssociation. Association will assessmember insurers to pay the claims of an insolvent insurer.

Reserves (tangible net equity) calculatedbased on the greatest of: 2 percent ofpremium revenues; minimum of $1million; or specified percent ofexpenditures.

DMHC can require other plans in an area to assume care of an insolvent plan’senrollees.

Fee and TaxStructures

Licensing fees and other filing fees.

Gross premiums tax (in lieu of othercorporate taxes): 2.35 percent of totalpremiums annually, regardless of profit.

Annual “per enrollee” assessments.

No gross premiums tax. Subject toapplicable corporate taxes.

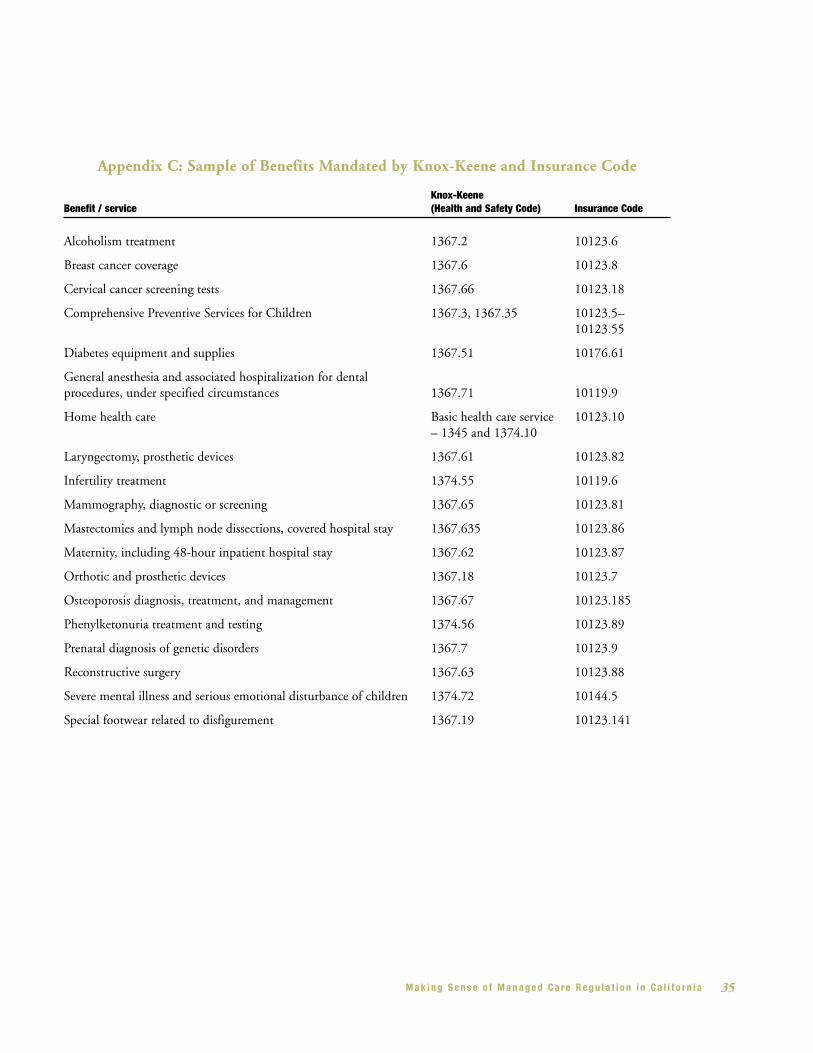

BenefitsAll health care service plans, including PPOsregulated by DMHC, must offer basic health careservices: physician services, inpatient and outpa-tient hospital services, diagnostic lab and radiology,therapeutic radiology, home health, preventivehealth services, emergency services, and hospicecare. In contrast to Knox-Keene requirements forhealth care service plans, there are no minimum or basic benefits required in the Insurance Code.However, both the Insurance Code and Knox-Keene contain numerous mandatory benefit orcoverage provisions requiring that carriers offer orprovide specific services and/or specific providers.Examples are listed in Appendix C.

Knox-Keene basic health care services can besubject to copayments and deductibles, butDMHC has regulatory authority to review cost-sharing arrangements and other limitations toensure that the contract requirements are “fair,reasonable, and consistent with the objectives ofthe chapter” and are not held to be objectionableby the director.33

By contrast, disability insurers have enormousflexibility to develop alternative benefit packages,with variations on covered services, copaymentsand deductibles, and annual and lifetime maxi-mums. Policies can be written to cover limitedmedical expenses, exclude specific services notmandated in statute, cover primarily catastrophicexpenses, or include significant consumer cost-sharing requirements not subject to regulatoryoversight. In addition, disability insurers are able to develop specialized and supplemental policiessuch as disease-specific coverage, short-term healthinsurance, and coverage for copayments anddeductibles from another policy. These types ofsupplemental policies would not meet Knox-Keenebasic benefit requirements.34

Key informants reported that the flexibility inbenefit design under the Insurance Code is one of the primary reasons that many Knox-Keenelicensed plans also maintain a disability insurancecertificate of authority. Reportedly, the insurancecertificate allows them to respond to purchaser andmarketplace demands for different products, suchas low-cost high-deductible plans, greater choice of out-of-network providers, or lower-cost benefitplans that do not include all of the basic benefitsunder Knox-Keene and are not subject to otherKnox-Keene Act provisions.

For example, instead of offering their point-of-service products35 entirely under their Knox-Keenelicense, some Knox-Keene HMOs offer the equiv-alent of a point-of-service through a combinationof an HMO contract for in-network services and aCDI indemnity “wraparound” for out-of-networkservices.36

Quality Assurance and Quality MonitoringHealth care service plans are required to haveinternal quality assurance and utilization reviewprograms, directed by providers, to document andimprove the quality of care. The regulations requirea written plan, regular meetings of the qualityassurance committee(s), and supervision by a planmedical director. DMHC is required to conducton-site medical surveys of all licensed health plans,including review of patient medical records, at leastevery three years.

Insurers are not subject to comparable qualityassurance requirements. CDI does conduct on-sitereview and regulatory examination of claims,financial records, and rating and underwritingpractices of all licensed insurers.

16 C a l i f o r n i a H e a l t h C a r e F o u n d a t i o n

Utilization Review and Utilization ManagementBoth disability insurers and health care serviceplans are subject to similar statutory requirementsapplicable to their utilization review process.Carriers must have written policies, develop criteriausing health professionals consistent with clinicalprinciples, make decisions within specified time-frames, and disclose the criteria being used. Therequirements apply to approvals, modifications,delays, or denials of services prior to, after, or atthe time of services being rendered.

Health care service plans must designate or employa medical director to set the policies and overseethe decisions, and their programs and policies aresubject to review during the on-site medical survey.Disability insurers must have a medical directoronly if the number of California insureds is 50percent or more of their total national health carebusiness. Violations by either carrier type aresubject to fines and penalties.

Provider AccessibilityHealth care service plans must ensure that servicesare “readily available and accessible to enrollees.”Except for contracts specifically allowing for someout-of-network providers (PPOs, EPOs, and POS),all participating providers must be under contractor employed by the health plan. Regulatory guide-lines include specific physician-enrollee ratios anddistance standards for the location of providers toenrollee residences and workplaces.

As a general rule, disability insurers are not subjectto similar accessibility standards. There are stateinsurance regulations applicable to exclusiveprovider organizations (EPOs)—where payment is limited to providers who have agreed to acceptdiscounted rates—that require consumer disclosureof available providers and contain availability and accessibility standards nearly identical to

Knox-Keene. According to CDI, the regulations donot require that EPOs submit provider contracts oradequacy and accessibility information. Accordingto CDI, the department will inquire into adequacyof provider networks and will “ensure that thepolicy is not inconsistent with standards of goodhealth care.” CDI is not required to and does nottrack the number of EPO policies but concurs withkey informants that there are very few currently inthe marketplace.

Provider PaymentsDisability insurers are limited to paying fee-for-service claims and to negotiating discounted ratesof payment as in a PPO arrangement. Health careservice plans may pay fee-for-service or discountedfee-for-service, and in addition, may executeprovider contracts that pay providers either acapitation payment—a monthly flat rate perenrollee—or some other arrangement where theprovider shares in the risks related to costs andutilization of health services.

While the rates paid to providers contracting with Knox-Keene plans are not subject to DMHCreview and approval, health plans must submit thepayment method. In the case of capitation arrange-ments, plans retain legal responsibility for ensuringthat the provider has the administrative and finan-cial capacity to handle the contract. In addition,the plans must have “a mechanism to detect andcorrect under-service” by providers assumingfinancial risk in treating the plan’s members. In the wake of several highly visible medical groupbankruptcies, DMHC is currently implementingnew provider financial reporting requirements.

Consumer ProtectionHealth care service plans are required to maintainan internal plan grievance system to respond toconsumer complaints. DMHC established the

M a k i n g S e n s e o f M a n a g e d C a r e R e g u l a t i o n i n C a l i f o r n i a 17

“HMO Help Center” (continuing the toll-freeconsumer complaint hotline originally establishedat the Department of Corporations in 1995) andexpanded the hotline hours to 24 hours per day, 7 days per week. After normal business hours, anexternal contractor trained by DMHC responds to hotline calls. The contractor answers basicquestions and is able to send out information,including complaint forms. Help center staff havethe ability to page DMHC staff nurses or consult-ing nurses or physicians, 24 hours per day, forassistance with medical care issues.

There is no similar requirement that insurersmaintain an internal grievance or complaintsystem. CDI also operates a consumer hotline thatpredates the DOC hotline (for all lines of insur-ance, not just health insurance), which is available10 hours per day, 8:00 a.m. to 6:00 p.m. CDI hasvoice mail and email systems allowing consumersto register complaints after hours. CDI staff thenrespond to those complaints during regularbusiness hours.

Both departments are legislatively mandated todevelop an independent medical review (IMR)system where doctors and other professionalsoutside of the health plan or insurer reviewcoverage and medical care decisions made by thecarriers. DMHC contracted with the Center forDispute Resolution to conduct the reviews andCDI agreed to use the same organization forconsistency and clarity across programs.

Financial Reserve RequirementsBoth health care service plans and disabilityinsurers are subjected to financial reportingrequirements, review, and monitoring of theirfinancial capabilities, including on-site reviews, andmust meet specific financial reserve requirements.

Disability insurers are required to maintain reservelevels at the greater of either: (1) a minimum of $5 million or (2) 200 percent of the Risk-BasedCapital standards developed by the NationalAssociation of Insurance Commissioners.Insurance industry representatives report thatreserves under this formula are 50 to 100 percenthigher than the reserves required of Knox-Keenelicensees.

In addition, the Insurance Code requires all lifeand disability insurers to belong to the CaliforniaLife and Health Insurance Guarantee Association.The Guarantee Association is structured so that all insurers share the risk in the event of a carrier’sfinancial insolvency. Assessments on all carriersthen cover the losses (expenses) of people insuredby the insolvent carrier. This system is designed to protect the ability to pay claims.

Under Knox-Keene, health plans are required to maintain financial reserve levels, referred to as tangible net equity (TNE), at the greatest of: (1) a minimum of $1 million; (2) 2 percent ofpremium revenues; or (3) specified percentages of expenditures. In addition, PPO and point-of-service plans are subject to higher TNE require-ments in light of their increased liability fromout-of-network services.

In the event of an insolvent health plan, DMHChas the authority to proportionately assign themembers of the insolvent plan to other Knox-Keene plans in the service area. The neighboringplans are required to assume responsibility fordelivering health care to the assigned members.Under Knox-Keene contracts, providers are notstatutorily protected from the risk of lost paymentsin the event of plan insolvency.

18 C a l i f o r n i a H e a l t h C a r e F o u n d a t i o n

Fee and Tax StructuresHealth care service plans pay an annual assessment,as specified in statute. The amount of the assess-ment is based on the size of the health plan and the specific number of health plan members(enrollees). Health plan assessments support theregulatory and enforcement program at DMHC.By contrast, insurance fees are assessed for eachtype of filing or regulatory request and are not inany way based on the number of people an insurercovers. CDI fees support CDI operations. CDIdoes not track or require insurers to report thenumber of covered lives or insureds.

Knox-Keene plans are subject to all taxes applicableto the particular corporate and tax status of theplan. Insurers pay a gross premiums tax based onthe total dollar amount of premiums sold, regard-less of profit, in lieu of other state or local taxes.

It is difficult to compare and contrast the verydifferent types of assessments and reserve formulasapplicable to each carrier type since they are basedon distinct formulas and requirements. The relativeburden and protection afforded by the reserverequirements, fees, and tax structures betweenhealth care service plans and disability insurers maywarrant further review.

M a k i n g S e n s e o f M a n a g e d C a r e R e g u l a t i o n i n C a l i f o r n i a 19

Much of the confusion about the two differentdepartments and their jurisdictions—and thedriver behind recent interest in possibly combiningor overhauling jurisdictions and regulatory respon-sibilities in some way—results from the overlapand similarities between the products under eachdepartment’s jurisdiction.

Specifically, as indemnity insurers have developednetworks of providers at discounted rates, and ashealth care service plans have developed someproducts where consumers can go out-of-network,it increasingly appears as though both departmentsare regulating the same types of carriers andproducts. One way to begin to organize andanalyze the products in today’s market is to under-stand the prevalence of similar products and theregulatory jurisdiction applicable to these products.

Identifying Products and Regulators

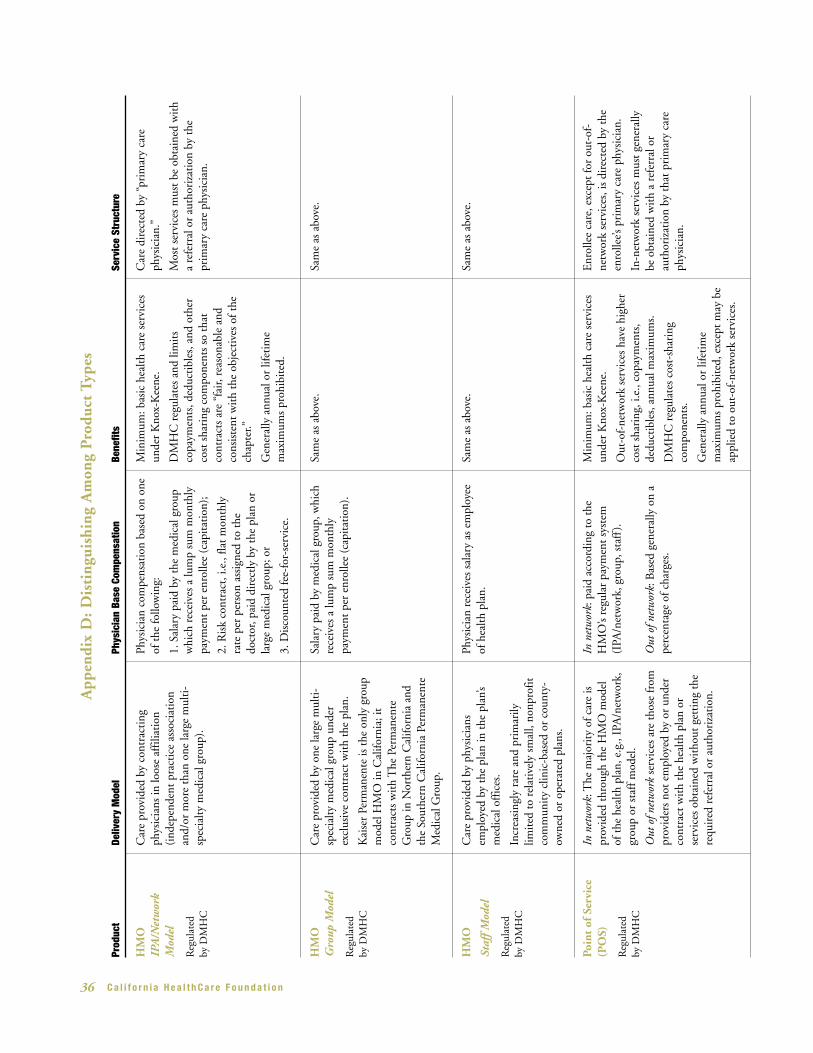

HMOs under Knox-KeeneAs stated earlier, HMOs under Knox-Keeneprovide all services through plan operated orcontracted providers (except for point-of-serviceproducts as discussed below).

There are three models of HMOs: group model,staff model, and independent practice association(IPA) or “network” model plans. In California,Kaiser Permanente is the only group model plan,where one group provides, on an exclusive basis,virtually all of the medical care for plan membersin an area. Staff model plans, where the planemploys the providers, are increasingly rare andprimarily limited to relatively small, nonprofit

community clinic-based or county owned oroperated plans. Most of the HMOs in Californiaare IPA/network model plans, or what the Cali-fornia Association of Health Plans calls “mixedmodel” plans that provide coverage through acombination of large multi-specialty medicalgroups and more loosely organized IPAs—privatephysicians in their own offices who belong to anassociation for contracting purposes.

Unlike insurers, HMOs under Knox-Keene arepermitted to execute provider contracts that shiftsome of the risk to the providers while the healthplan retains legal responsibility to ensure that theproviders have the ability to manage and assumethe risk.

According to the California Association of HealthPlans (CAHP), in 1999 some 73 percent of Knox-Keene plans paid primary care providers by groupor individual capitation, while 19 percent paid

20 C a l i f o r n i a H e a l t h C a r e F o u n d a t i o n

4 Understanding the Products in the Health Coverage Marketplace

Figure 1: PCP Payment ArrangementsAmong Knox-Keene Plans in 1999

Source: California Association of Health Plans 2000 AnnualReport and Profile.

Group orindividualcapitation

73%

Salary3%

Other5%

Fee-for-service or

discountedfee-for-service19%

fee-for-service or discounted fee-for-service, 3 percent salary, and 5 percent other.37 Amongspecialists, 40 percent are paid by capitation and47 percent by fee-for-service. According to keyinformants, in the past two years there has been a gradual erosion of plans paying providers by wayof capitation arrangements.

PPOs and EPOs under Knox-KeeneThe PPO model of health coverage, where thecarrier offers a list of providers who have agreed to accept reduced payment, and the EPO model,where payment is limited to providers on the list,are generally not allowable under or subject to theKnox-Keene Act. However, as discussed, twosignificant exceptions continue to complicateanalysis of the regulatory framework for healthcoverage—Blue Shield and Blue Cross.

According to the California Association of Health Plans, in 2000, approximately 4.6 millionCalifornians, or 20 percent of those enrolled inKnox-Keene plans, were in PPOs, 73 percent inHMOs, and approximately 5 percent in point-of-service plans.38

Both Blue Cross and Blue Shield plans have aspecific statutory or historical exemption from the requirement that all services be delivered by participating providers. Both companies areotherwise subject to the provisions of Knox-Keene,including the requirement to provide all basichealth care services, to establish internal qualitymonitoring systems, to meet availability andaccessibility standards for in-network providers,and to submit plan contracts, advertising, andmarketing materials for prior approval to DMHC.

Historically, DOC, and now DMHC, haveallowed for considerable flexibility in PPOdesign—copayments, deductibles, annual

maximums—so that the Blue Cross and BlueShield PPO products more closely resemble otherPPO products in the marketplace. In addition,out-of-network providers and services, with nodirect affiliation to the plans, are not subject to thesame quality assurance requirements as in-networkproviders. The statutory authorization applicable to the Blue Cross and Blue Shield plans allowsthem to have some portion of their business that“substantially indemnifies subscribers” and bothcompanies also offer limited EPO contracts underthe Knox-Keene license.

Point-of-Service Contracts under Knox-KeeneIn 1992, legislation authorized Knox-Keene healthcare service plans to begin offering plan contractsthat include both an HMO delivery system andthe option for enrollees to choose providers outsideof the plan’s network, for some services. POScontracts are subject to all Knox-Keene standards,except for the providers and services delivered out-of-network. There are statutory limits on thecopayments and deductibles that can be chargedfor out-of-network services, restrictions on theamount of out-of-network care that a health plancan experience, and increased financial reserverequirements. As of 2001, DMHC reports thateight Knox-Keene plans offer point-of-servicecontracts under the POS provisions of Knox-Keene.

Based in part on the statutory constraints applica-ble to Knox-Keene POS contracts, several Knox-Keene plans offer purchasers a POS equivalent thatis regulated under both departments—the previ-ously mentioned HMO contract for in-networkcare, with a disability insurance “wrap-around” forout-of-network care.

M a k i n g S e n s e o f M a n a g e d C a r e R e g u l a t i o n i n C a l i f o r n i a 21

PPOs under the Insurance CodeThe 1982 selective contracting legislation (au-thorizing disability insurers, for the first time, tonegotiate with providers for “alternative rates ofpayment”) was a significant departure for indem-nity health coverage because the Insurance Codehad since 1937 protected the right of an insured to choose any licensed health care provider.

This “alternative payment” language is the basis fordevelopment of what became known as insurancePPOs.39 Key informants in this project consistentlyreported that virtually all of the current indemnitypolicies for full coverage health insurance in Cali-fornia include a PPO network through whichconsumers can access services at reduced cost.

Key informants indicated that many insurers “leaseor rent” PPO networks from corporations that arein the business of organizing the networks, negoti-ating rates, and executing provider contracts. Thesecompanies also make their PPO networks availableto large, self-insured employers. The contractedPPO may also perform other functions such asprior authorization or utilization review foremployers and insurers. The PPO networks and companies themselves are not subject to anylicensing or regulation under California law. PPOnetwork companies are regulated in some otherstates, complicating state-to-state comparisons of how “PPO products” are regulated.

EPOs under the Insurance CodeThe Insurance Code also allows insurers to limitpayment to providers agreeing to alternative rates.Exclusive provider organizations require individualsto receive all services from providers who agree toaccept reduced payments from the insurer.

These products are subject to increased consumerdisclosure regulations monitored through CDI

scrutiny of policy forms. CDI does not track thenumber of EPO policies it approves, but CDIagrees with key informants that there are very fewEPO plans being offered by disability insurers.

Traditional Indemnity Insurance under the Insurance CodeInsurance companies that offer health insuranceunder the Insurance Code may offer an open panelproduct allowing insureds to seek services fromlicensed providers with no network limitation ordiscounted network offering. These products aresubject to statute and regulations applicable todisability insurers generally.

These “traditional” indemnity policies typicallyhave annual deductibles and pay for services whena bill is received. The policies generally coverphysician and hospital services and medical tests.They may cover prescription drugs but are typi-cally limited in coverage of preventive care services.The insurer generally pays a specified percentage of the “usual and customary fees” (often 80percent) while the insured pays the remainingamount, known as “coinsurance.”

Key informants consistently reported that there arevery few “pure” indemnity products remaining intoday’s market. CDI does not track information onthe extent of availability of any product type underits jurisdiction, including traditional indemnitycoverage.

What Is a Health Insurance Product?

Individuals can obtain protection from the costs of health care services through multiple productstrategies, not just traditional health insuranceproducts. The traditional health insurance

22 C a l i f o r n i a H e a l t h C a r e F o u n d a t i o n

products discussed in this report, regulated byDMHC or CDI, constitute a subset of the differ-ent strategies available. Strategies include:

Full coverage health insurance, which generallycovers hospital, medical, and surgical services andmay include coverage for ancillary services. Knox-Keene plans, both HMOs and PPOs, will cover atleast the basic health care services and distinguishproducts primarily by the different levels of patientcost sharing. Among disability insurers, the typesof services covered, including the extent to whichthey cover preventive care, and variation in patientcost-sharing levels, may distinguish products.

Catastrophic or high-deductible health insurance,which covers health care costs above a relatively high fixed-dollar amount and may also includepolicies that cover only high-cost items such asmajor medical or hospitalization. In today’s marketthese policies may be sold in combination with aMedical Savings Account (MSA), a savings accountdedicated for health care expenses and organizedunder federal tax laws establishing MSAs as a tax-deductible option. Both Knox-Keene plans (pri-marily the PPOs) and disability insurers havedeveloped these types of products.

Cash benefit plan, which provides lump sum orperiodic cash payments related to specific eventssuch as hospitalization, accident, defined disability,catastrophic illness, or illness out of the country.These plans do not reimburse for health servicesbut pay cash payments when the insured eventoccurs. The payments can be used to pay for health care or for other expenses. These products

are exclusively offered by disability insurers and are not permissible under Knox-Keene.

Elements of a Health Insurance ProductEach full coverage health insurance product can be viewed as a combination of four key elements:(1) the benefit design—what is covered or insured;(2) the service delivery approach, if any—how andfrom whom the consumer must obtain services toreceive benefits under the contract; (3) the methodof provider payment—how the carrier pays pro-viders; and (4) the specific company or carrier type offering the coverage. Benefit design, whichcontains several elements that are not mutuallyexclusive, is the area of most variability product toproduct. Figure 2 provides an illustration of healthcoverage product components.

What has made the dialogue about health coverageproducts and companies so complicated, and oftenconfusing, is that in the marketplace, products aretypically referred to more by the service deliverytype—HMO, PPO, and POS—than by any otherelement of the product design. And yet there canbe substantial variation among these products and,as the comparison of the two licensing schemesreveals, very different regulatory requirementsdepending on the carrier offering the product.

This section shows that breaking down the com-ponents of any product helps to identify the regu-latory framework and specific requirements thatgovern that product. Appendix D contains anoverview of the different products licensed andregulated in California, which serves to illustratethe complexities inherent in regulation.

M a k i n g S e n s e o f M a n a g e d C a r e R e g u l a t i o n i n C a l i f o r n i a 23

Figure 2: Elements of a Health Insurance Product

These four elements combine to form a health coverage product as sold to purchasers. Consumers may not always befamiliar with or aware of all the elements that make up a health coverage product.

BENEFIT DESIGN

What is covered orinsured by the product

List of services orevents covered

AND

Limits andtimeframes

One visit per year,number of hospitaldays per year, etc.

AND

Copayments,deductibles,co-insurance

SERVICE DELIVERY

How and from whomconsumers need toobtain services

HMO

Closed panel – planowned or contractproviders

OR

PPO

Choose preferred listor any provider

OR

Point-of-Service

Mostly in-network,some out of network

OR

Open panel/TraditionalIndemnity Insurance

Choose any licensedprovider

ABC-XYZ Health Plan Inc.

Subscriber Name: Maria SmithSubscriber ID: 123456789Plan Code: 99Z Copays: $15/$10

PROVIDER PAYMENTMETHOD

How the carrier pays foror reimburses providers

Capitation and risk-pools

Knox-Keene plansonly

OR

Salary

Knox-Keene HMOsonly

OR

Fee-for-service ordiscounted fee-forservice

Knox-Keene HMOs,PPOs, disabilityinsurers, self-insuredplans

BENEFIT PLAN

Covered services andhow much patient paysout-of-pocket

TYPE OF PLAN

Rules and requirementsfor using participatingproviders and/or non-participating providers

PROVIDER INCENTIVES

Applies to primary care,specialists, hospitals,and any other contract-ing provider

CARRIER

Who offers the plan orcoverage

Knox-Keene licensedhealth care serviceplan

OR

Disability insurer

OR

Self-insuredemployer/Trust

APPLICABLE STATUTE AND REGULATIONS

Legal requirements,including consumerprotections

24 C a l i f o r n i a H e a l t h C a r e F o u n d a t i o n

HEALTH COVERAGE PRODUCT AS

SOLD TO PUBLIC

The intent of this report has been to providethe reader with a contextual framework throughwhich to examine the difficult issue of whether theregulation of health coverage in California shouldbe altered or consolidated.

What this report reveals is that public policychoices and shifting political inclinations overmore than a half-century have resulted in two verydifferent statutory and regulatory frameworks. Theexisting differences between the two departments,and their respective regulatory personalities, arefirmly rooted in both history and statute. Thesechoices have also had profound effects on thehealth coverage market in California.

The report also suggests that as long as there are two different departments regulating healthcoverage, and two distinct statutory frameworks,there will be important differences in how carriersare regulated, distinct departmental cultures, anddisparate views of their respective roles and respon-sibilities toward consumers, providers, and carriers.

When properly channeled, and when there is effective collaboration and communicationbetween departments, the differences can serve as learning tools, presenting an opportunity tobuild on success. Many key informants interviewedreported that the information exchange resultingfrom the AB 78 review of the respective depart-ments and frameworks has resulted in many suchdesirable effects. At the same time, it is alsopossible, under dual regulation, for the twodepartments to become competitors vying forrecognition and acknowledgement of the sound-ness of their regulatory performance.

Dual regulation also invites carriers to designproducts to fit within the regulatory structure mostconducive to their business and marketplace needs.Allowing carriers discretion as they develop andlicense products may have the desirable conse-quence of greater flexibility in product design butalso the potentially undesirable consequence ofavoidance of some types of oversight.

Finally, among consumers, stakeholders, andpolicymakers, dual regulation means that there will always be the potential for confusion, mis-understanding, and misinformation.

This project has led the authors to conclude thatany policy change in this area necessitates clearlyarticulated goals and objectives along with opendiscussion of both intended and unintendedconsequences. This means carefully analyzing how statute, regulation, and department styles and strategies may combine such that the actualimpact of various policy choices may ultimatelydiffer from the original intent.

The following questions offer just two examples of possible proposed changes and consequences:

■ If all health coverage were moved to DMHC and made subject to Knox-Keene basic benefitsrequirements, would that reduce or eliminateaffordable options for some consumers?

■ Would consolidating consumer complaint func-tions result in lower levels of expertise or com-petence by complaint handlers who might notunderstand specific statutory and real world dif-ferences among carriers and licensing require-ments? How could that be avoided or mitigated?

M a k i n g S e n s e o f M a n a g e d C a r e R e g u l a t i o n i n C a l i f o r n i a 25

Conclusion 5

A deliberate process has been put in place to studythe ramifications of change, giving policymakersand stakeholders the opportunity to carefullyinvestigate all options before making changes tothe current statutory and regulatory environment.The complexities of the regulatory environment as outlined in this report warrant that level ofthoughtful scrutiny.

Simpler and more understandable regulatoryrequirements, combined with consistent enforce-ment, increase the likelihood that the system willfunction to bring consumers affordable, high-quality care. Given the high number of uninsuredCalifornians, and increasing consumer anxiety overhealth care quality, high-quality care at affordableprices should be the ultimate objective of policychange.

26 C a l i f o r n i a H e a l t h C a r e F o u n d a t i o n

M a k i n g S e n s e o f M a n a g e d C a r e R e g u l a t i o n i n C a l i f o r n i a 27

Appendices

Appendix A: History of the Knox-Keene Health Care Service Plan Act of 1975

1929 Ross-Loos Clinic opens in Los Angeles. First prepaid contract with a group practice of physicians providesmedical care for workers in the city’s water department.

1937 Chapter 11A of the Insurance Code enacted, authorizing first Blue Cross hospital insurance in California as anonprofit hospital service plan subject to the Insurance Code. (Chapter 881, Statutes of 1937)

1938 California Medical Association votes to create California Physicians Service (CPS) (later Blue Shield). CPSprovides coverage for medical and surgical services to employee groups who receive care from “professional[physician] members” of CPS “on a periodic budgeting basis.” CPS does not seek state licensure.

1941 Blue Shield registers as a health service plan under Civil Code Section 593a (legislation sponsored by BlueShield), requiring a service plan to obtain a certificate from the Board of Medical Examiners. Generalsupervision placed with the Attorney General but funds are not budgeted for implementation.

1945 Permanente Health Plan (later Kaiser Permanente) opens public enrollment in the nonprofit prepaid healthplan originally developed for employees of Kaiser Industries. Kaiser Permanente is a group practice modelHMO where a Permanente Medical Group provides services on an exclusive basis to Kaiser enrollees in anarea. The health plan also has an exclusive contract with Kaiser Foundation Hospitals for hospital services.

1946 CPS v. Garrison. California Supreme Court rules that CPS (Blue Shield) (and other prepaid health plans) isnot in the business of insurance and is not subject to the jurisdiction of the Insurance Commissioner.

1954 The local medical society establishes the Foundation for Medical Care in the Stockton/San Joaquin Valleyarea. FMC is an early prototype of the IPA-model HMO, providing health care services through non-exclusive contracts with community physicians, who are paid discounted fees for the services provided.

1959 Congress passes the Federal Employees’ Health Benefits Act, which establishes health coverage as a benefit forfederal employees.

1961 The Family Health Plan (later FHP, Inc.) opens in Southern California as a nonprofit staff-model HMO.Salaried physicians provide health services to enrolled members. FHP owns and operates its own hospitals,pharmacies, and laboratory facilities.

1965 Knox-Mills Health Plan Act requires health care service plans to register with the California Attorney Gene-ral. (Chapter 880, Statutes of 1965) Ultimately more than one hundred plans registered, including specializedplans such as dental and mental health plans, including Kaiser, Ross-Loos, Blue Shield, and FHP.

Kaiser Health Plan enrollment reaches 1 million members.

28 C a l i f o r n i a H e a l t h C a r e F o u n d a t i o n

1972 Innovative Health Systems of Los Angeles signs first non-pilot PHP contract. By December 1972, some 22PHP contracts with 132,668 Medi-Cal enrollees are in effect, mostly in Los Angeles County.

Within months, the public press, most notably the Los Angeles Times, reports serious PHP abuses. The Timesreports enrollment fraud and abuse, substandard care, and lack of physicians available during business hours.

PHP enrollers indicted in Los Angeles for forging the names of Medi-Cal recipients on PHP enrollmentforms. Los Angeles District Attorney initiates criminal investigation into Los Angeles-based PHPs.

Waxman-Duffy Prepaid Health Plan Act sets standards for Medi-Cal PHPs, under the oversight of DHS,including minimum patient-physician ratios, conflict of interest limitations, and onsite reviews. (AB 1496,Chapter 1366, Statutes of 1972)

1973 California Auditor General’s follow-up report documents serious failures in oversight by DHS and violationsof law by some participating PHPs.

Office of the Legislative Analyst issues scathing report on the administration of the PHP program by DHS.Report details financial schemes where “nonprofit” health plans channel Medi-Cal payments into for-profitsubsidiary provider corporations.

Congress passes the Federal Health Maintenance Organization Act of 1973. (42 U.S.C. 300 et seq.) TheHMO Act establishes comprehensive benefits, community rating requirements, administrative procedures,financial reserves, annual open enrollments, prohibitions on pre-existing condition limitations, and otherrequirements, and provides federal grants for start-up of nonprofit HMOs seeking federal qualification. Thephrase “health maintenance organization” is coined for the first time. The Act also requires employers of morethan 25 workers who are already providing health benefits to offer as one choice an available federallyqualified HMO (later repealed).

Assembly Health Committee holds a series of investigatory hearings on PHP abuses. Topics includeenrollment, marketing procedures, and quality of care.

Chapter 11A of the Insurance Code (nonprofit hospital service plans) is amended to allow for developmentand regulation of nonprofit HMOs, and their licensure as nonprofit hospital service plans. Health Net andTake Care are licensed as nonprofit hospital service plan HMOs, originally as subsidiaries of Blue Cross.

1974 Third Auditor General Report reveals that among 15 PHPs investigated (14 in Los Angeles), only 48 percentof funds paid to the plans over a two-year period went for services to Medi-Cal recipients. The remainingfunds went to administrative costs and profits to contractors and subcontractors.

California Attorney General Younger repudiates Knox-Mills, refuses to administer the Act, and urges theLegislature to enact tougher regulation of health plans.

Appendix A: History of the Knox-Keene Health Care Service Plan Act of 1975 (continued)

1971 AB 949, put forward by then Governor Ronald Reagan, enacts significant Medi-Cal reforms, includingauthorizing “prepaid health plans” to serve Medi-Cal beneficiaries, on a capitated basis, under contract withthe Department of Health Services (DHS).

M a k i n g S e n s e o f M a n a g e d C a r e R e g u l a t i o n i n C a l i f o r n i a 29

1975 U.S. Senator Henry Jackson convenes congressional oversight hearings on the California PHP program.Hearings on Prepaid Health Plans before the Permanent Subcommittee on Investigations of the Senate Committeeon Government Operations, 94th Congress.

Knox-Keene Health Care Service Plan Act of 1975 transfers regulation of health care service plans from theAttorney General to the Commissioner of Corporations. (Assembly Bill 138, Chapter 941, Statutes of 1975)Enacts standards related to basic health care services, administrative and financial systems, marketing andadvertising, forms for plan contracts issued, etc. The bill requires the transfer of Blue Shield from Knox-Millsto Knox-Keene licensure, giving them three years to reduce (but not completely eliminate) their indemnitymodel business.

1979 Congress amends Federal HMO Act to permit for-profit plans to seek federal qualification.

1982 California Legislature passes selective contracting for disability insurers. Insurers authorized to negotiate andenter into contracts with providers at alternative rates of payment and permitted to limit claims payment toservices received from providers charging alternative rates. (AB 3480, Ch. 329 of 1982) Paves the way forPPO products to be offered by carriers licensed as disability carriers under Department of Insurance.

1983 Legislation transfers from the Attorney General to the Department of Corporations authority for admin-istering conversions of health care service plans. Federal HMO Act start-up grants and loans for nonprofitHMOs discontinued.

1984 California Legislature adopts a renewed emphasis on PHP contracts in the Medi-Cal program but continuesto require Knox-Keene licensure or licensure as a nonprofit hospital service plan as a pre-condition for a PHPcontract.

1990 Legislation establishes the Health Insurance Guarantee Fund for disability insurers and requires Blue Cross of California to seek Knox-Keene licensure within one year. Includes statutory authority for BCC to continuesome portion of business as indemnity model coverage. (SB 785, Chapter 1043, Statutes of 1990)

Appendix A: History of the Knox-Keene Health Care Service Plan Act of 1975 (continued)

1992 Small employer group access legislation reforms the market for small employer health coverage. Similarprovisions apply to Knox-Keene and disability insurers. (AB 1672, Chapter 1128, Statutes of 1992)

Legislature eliminates door-to-door marketing for Medi-Cal Prepaid Health Plans, effective January 1994.(AB 3463, Ch. 1056 of 1992)

Legislature expands DHS authority to enter into contracts for Medi-Cal managed care resulting inimplementation of the Medi-Cal Two-Plan Model. Limits PHP contracts to Knox-Keene licensees, withcertain limited exceptions. (SB 485, Ch. 722 of 1992)

Congress enacts the Employee Retirement Income Security Act of 1974 (ERISA). ERISA supersedes orpreempts all state laws related to employee health benefits provided by self-insured employers.

1974

30 C a l i f o r n i a H e a l t h C a r e F o u n d a t i o n

Appendix A: History of the Knox-Keene Health Care Service Plan Act of 1975 (continued)

1998 Managed Care Improvement Task Force releases final report. Recommends the creation of a new statedepartment for regulation of health care service plans and phasing in regulation of medical groups and otherprovider entities that bear substantial risk for health care services.

1999 California Legislature passes Patient Bill of Rights. The 21-bill package sponsored and supported byconsumer advocacy groups becomes law. AB 78 creates the new Department of Managed Care and transfersauthority for health care service plans to the new agency.

2000 New Department of Managed Health Care opens for business July 1, 2000. The DMHC constitutes a newAdvisory Committee on Managed Care, a Clinical Advisory Panel, and a Financial Solvency Standards Board,consistent with requirements of AB 78 of 1999.

2001 DMHC contracts with independent consultant for a feasibility study regarding transferring the regulation ofhealth insurance from the California Department of Insurance (CDI) to the new DMHC. Report due to theLegislature December 2001.

1993 Legislature authorizes Knox-Keene plans to develop point-of-service plan contracts. SB 1221, Ch. 987 of1993, allows plans to offer contracts where subscribers can go outside of the plan network for specifiedservices, while incurring higher out-of-pocket costs.

Blue Cross of California licenses four health care service plans, including dental and pharmacy plans, andproposes a controversial corporate restructuring plan.

1995 Consumer hotline enacted. Legislation requires DOC to establish a toll-free number to receive consumercomplaints and inquiries. (SB 689, Ch.789 of 1995)

Blue Cross of California reaches agreement with DOC and the Legislature to dedicate substantial assets tocharity and move forward as a for-profit health care service plan.

1996 Legislature repeals the nonprofit hospital service plan law since there are no remaining licensees. (SB 1866,Ch. 484 of 1996)

Legislation requires DOC to establish HMO Ombudsperson to resolve and respond to consumer complaintsand problems with their health plan. (SB 1936, Ch. 1095 of 1996)

Legislature creates the Managed Health Care Improvement Task Force to report on the status of health carecoverage and the extent to which health care service plans are meeting the goals of cost containment, quality,and access, and to make recommendations on the appropriate role of government in oversight and regulationof managed care. (AB 2343, Ch. 815 of 1996)

M a k i n g S e n s e o f M a n a g e d C a r e R e g u l a t i o n i n C a l i f o r n i a 31

Spec

ializ

ed P

lans

Sec.

740

(a)

Car

rier

s co

veri

ng t

he s

ame

type

s of

serv

ices

are

sub

ject

to

Insu

ranc

ere

gula

tion

but

the

re is

no

spec

ial

cate

gory

of i

nsur

er.

Sec.

134

5(o)

Lice

nses

and

reg

ulat

es s

peci

aliz

edhe

alth

car

e se

rvic

e pl

ans,

tha

t is

,co

ntra

cts

for

heal

th s

ervi

ces

in a

sing

le s

peci

aliz

ed a

rea

such

as

dent

al,

men

tal h

ealth

, or

visi

on.

Oth

er E

ntit

ies

Sec.

742

.20-

742.

44M

ulti

ple

empl

oyer

wel

fare

arra

ngem

ents

(M

EW

As)

mus

t ob

tain

a ce

rtifi

cate

of a

utho

rity

.

1345

, 134

9.1

CC

R §

130

0.43

-130

0.43

.15

Adm

inis

ters

oth

er v

ery

narr

ow a

nd/o

rob

sole

te e

xem

ptio

ns fr

om li

cens

ure

inst

atut

e an

d re

gula

tion

.

App

endi

x B

: Com

pari

son

of S

tatu

tory

and

Reg

ulat

ory

Req

uire

men

tsD

epar

tmen

t of

Man

aged

Hea

lth

Car

e an

d C

alif

orni

a D

epar

tmen

t of

Ins

uran