© PA Knowledge Limited 2013 1

© PA Knowledge Limited 2013

LOS ANGELES DEPARTMENT OF WATER AND POWER REVENUE REQUIREMENT EVALUATION

Prepared for Board of Water and

Power Commissioners

May 19, 2015

© PA Knowledge Limited 2013 2

Discussion Topics

• Objectives of Our Assignment

• Major Recent LADWP Initiatives

• Current Industry Trends

• Revenue Requirement Analysis

– Water System

– Power System

• Industry Rate Trends

• Summary

© PA Knowledge Limited 2013 3

Objectives of Our Assignment PA’s Role

PA is providing LADWP independent evaluation and assistance on a wide variety of

tasks associated with development of the revenue requirement and proposed new

rates to help the Department plan for the future.

Water and Power Cost of Service Studies

Benchmarking

Revenue Requirement Analysis

Rate Design Alternatives

Rate Action Reports

Industry Rate Trends

© PA Knowledge Limited 2013 4

Objectives of Our Assignment Development and Analysis of Revenue Requirement

PA is assisting LADWP with the development of its new revenue requirements and

rates for water and power services for FY 2015-16 through FY 2019-20. As part of

this effort, we have reviewed the revenue requirements to validate:

Financial plans reflect budget and financial metric requirements, so resulting

rates will both recover adequate revenues and minimize customer bill impacts

Regulatory mandated obligations are met

Infrastructure investments are designed to move towards industry standards for

asset replacement and plant age

Cost of service studies meet industry standards

Guiding legal principles are followed

Board approved financial metrics are maintained

© PA Knowledge Limited 2013 5

© PA Knowledge Limited 2013

MAJOR RECENT LADWP INITIATIVES

© PA Knowledge Limited 2013 6

Major Recent LADWP Initiatives

Similar to other utilities, LADWP has undertaken many initiatives designed to meet

Council recommendations, improve operations and financial performance, and

increase accountability.

Significant cost reduction

plan savings

A new labor agreement

Working with the

Ratepayer Advocate

Business planning to avoid

unnecessary rate increases

Establishment of corporate

performance unit

System-

Wide

Renewable energy supply,

reduction of GHG emission

Local solar

programs

Energy

efficiency

Transitioning off

coal

Electric vehicle

programs

Power System Reliability

Program (PSRP)

Power

Eastern Sierra

commitments Seismic retrofits

Infrastructure improvements:

mainlines, regulator stations, etc.

Meeting water quality

compliance regulations Water conservation

Water

Increasing local water

supply

Once-Through Cooling /

Repowering

© PA Knowledge Limited 2013 7

Major Recent LADWP Initiatives Response to Council Recommendations

In response to the 2012 Council recommendations, LADWP has taken actions that

contribute to cost efficiencies, accountability and benchmarking.

All of the recommendations have been addressed; however, programs implemented for some of the

recommendations require recurring efforts.

Recommendation Status Recommendation Status

Negotiate with labor to increase flexibility for

contracting out and to bring salaries and

benefits closer to utility market rates

Complete

Reevaluate surcharge-based restructuring

approach with fully restructured, permanent

rates, if legally permissible

Complete

Conduct benchmarking assessment to

review cost per project and to ensure cost

reasonableness

Initial study

completed /

On-going

Conduct new cost of service studies in

preparation for new rate restructuring Complete

Submit a semi-annual report to Mayor and

City Council on status of Renewable

Portfolio Standards

Several reports

submitted / On-

going

Establish plan for energy efficiency that

maintains expenditures at cost effective

levels

Complete

Identify opportunities to contract out and

explore potential savings On-going

Review overtime expense allocations and

contractual requirements that have an

impact on overtime

On-going

Seek Departmental efficiencies by pursuing

process improvements On-going

Review the Department’s hedging plan to

lock in low fuel prices Complete

© PA Knowledge Limited 2013 8

Major Recent LADWP Initiatives Cost Reduction Plan

LADWP has saved $467 million from the initial cost reduction plan exceeding the

original $459 million three-year target. Major cost reduction initiatives included:

• Negotiation and implementation of new labor

agreement

• Reduced overtime, vacancies, and attrition-

based labor savings

• Increased vigilance over hiring

• Refinancing, state grants and low interest

loans

• Reduce new computer purchases - stretch out

life to 5 year cycle

• Suspend office remodels and furniture

purchases

Source February 2011 – June

2014 Savings ($M)

Labor $230.0

Non-Labor $142.8

Capital $94.1

Total $466.9

Castaic

power plant

improvements

Electronic

WQ report

Power Water

Solar facilities

on LADWP

property

Shade balls Pipe material

evaluations

City

coordination

Capital

project

controls

Capital

prioritization

LADWP has also been pursuing other cost reduction efforts.

© PA Knowledge Limited 2013 9

Major Recent LADWP Initiatives New Labor Agreement

LADWP’s new labor agreement will provide $456 million in savings over FYs 2013-14

through FY 2016-17 and an estimated $5 billion in savings over thirty years.

Key Components of the MOU Four-Year Savings

Estimate ($M)

Defer Cost of Living Adjustment from 10/1/13 to 10/1/16 $385.0

Entry Level Salary Reduction for 34 Common Classes $15.0

Sick Time Medical Certification Requirement $12.0

Contracting Out Overtime Restriction - Reduction from 10% to 5% $3.0

Retirement Plan Tier 2 For All New Hires $41.0

Total $456.0

© PA Knowledge Limited 2013 10

Major Recent LADWP Initiatives Benchmarking – Water System

LADWP has begun a comprehensive benchmarking program to identify areas with

strong performance and areas for further cost and operational improvements.

Considerations:

• High reliance on walk in payment centers compared to electronic based solutions

• Infrastructure age; upgrades should reduce maintenance costs over long term

• Higher relative cost of living in California

• Allocation process between water and power for Customer service costs

= LADWP position

Note: Large Utility Companies: AWWA benchmarks comprised of 7 survey participants (water operations only, >500,000 customers)

Western Region : 1) AZ, CO, ID, MT, NV, NM, UT, WY, AK, CA, HI, OR, WA (16 survey participants (water operations only, Region 4)

Source: LADWP 2012 Financial Statements, LADWP Water Executive Office, AWWA 2012 Water Utilities Benchmarking Survey (including LADWP’s survey responses), Strategy& analysis

LADWP

1Q

2Q

3Q

4Q

558 2,049

2,160

1,651

1,052

563

422

269

O&M Cost Per Customer

($MM/Cust)

O&M Cost Per Million Gallons

Distributed

($MM/MG) (Large Utility

Companies)

(Western

Region)

(Large Utility

Companies)

(Western

Region)

3,983

2,554

1,858

2,049

717

542

416

558

63.54

48.23

30.10

Customer Service Cost per

Account

($/Account) (Large Utility

Companies)

(Western

Region)

66.35

53.43

43.25

71.53 71.53

© PA Knowledge Limited 2013 11

Major Recent LADWP Initiatives Benchmarking – Power System

The Power System’s performance is strong overall; however, individual areas for

further cost and operational improvements were identified for further evaluation.

Considerations:

• 2nd Quartile performance on a

per customer basis is a strong

indicator of cost effectiveness

• Low distribution capital

expenditures may indicate

underspending

Source: LADWP 2012/2013 Financial Statements, FERC Form 1 Data, SNL Data, Strategy& analysis

1Q

2Q

3Q

4Q

LADWP

(Large Utility Companies)

n=29

745

630

469

625

(Western Region)

n=22

805

642

506

625

(Western Region)

n=15

2.15

1.73

1.35

1.48

1Q

2Q

3Q

4Q

LADWP

(Large Utility Companies)

n=31

2.07

1.70

1.44

1.48

= LADWP position

Total O&M per Customer

($/Customer)

Distribution CapEx per Distribution

Depreciation Expense

($/$)

© PA Knowledge Limited 2013 12

Major Recent LADWP Initiatives Benchmarking – Power System

= LADWP position

(Large Utility

Companies)

n=32

132

118

93

80

LADWP

1Q

2Q

3Q

4Q

Distr O&M per Customer

($/Customer)

(Western

Region)

n=15

93

84

63

132 65

Customer Service O&M per

Customer

($/Customer)

(Large Utility

Companies)

n=32

(Western

Region)

n=15

65

134

94

66

126

109

86

The Distribution area appears to offer an opportunity for future improvement.

Considerations:

• Infrastructure age; upgrades should reduce maintenance costs over long term

• Allocation process between water and power for Customer service costs

• Recent IOU increased customer service focus

• Higher relative cost of living in California

Source: LADWP 2012/2013 Financial Statements, FERC Form 1 Data, SNL Data, Strategy& analysis

© PA Knowledge Limited 2013 13

Major Recent LADWP Initiatives Benchmarking – Power System (continued)

LADWP’s Power System operational performance is generally strong.

SAIFI - System Average Interruption Frequency Index: the average annual number of times each customer sees an interruption

SAIDI - System Average Interruption Duration Index: the average annual number of minutes each customer sees during an interruption

CAIDI - Customer Average Interruption Duration Index): the average annual number of minutes each customer sees during an interruption

for those customers that have an interruption

Considerations:

• Weather contributes to higher

reliability in Southern California

• Aging infrastructure could impact

future results

LADWP

1Q

2Q

3Q

4Q

115.66

88.23

61.65

SAIDI

National Panel

63.69

1.25

0.84

0.72

SAIFI

National Panel

0.45

115.66

88.23

61.65

CAIDI

National Panel

63.69

= LADWP position

© PA Knowledge Limited 2013 14

© PA Knowledge Limited 2013

CURRENT INDUSTRY TRENDS

© PA Knowledge Limited 2013 15

Current Water Utility Industry Trends

LADWP is facing many of the same opportunities and challenges being addressed by

other water utilities in California (and elsewhere).

Response to historic drought in California

Aging infrastructure (EPA forecasts $384.2 billion

required investment in water infrastructure

nationwide over 20 years)

Regulatory mandates (e.g., Long-Term 2 Enhanced Surface Water

Treatment and Stage 2 Disinfectants and Disinfection Byproducts Rule –

EPA/Safe Drinking Water Act )

Bay Delta Conservation Plan

Balancing investment needs with

maintaining reasonable customer rates

Proposition 218

requirements and recent

legal challenges

© PA Knowledge Limited 2013 16

Current Power Utility Industry Trends

Similarly the Power System is facing many of the same opportunities and challenges

being addressed by other power utilities in California (and elsewhere).

Meeting renewable energy

resource targets

Aging infrastructure (195,000

(61%) of poles are more than 50

years old)

Regulatory mandates (e.g., elimination of once-through-cooling –

EPA/Clean Water Act; SWRCB)

Energy efficiency goals

Balancing investment needs with maintaining

reasonable customer rates

Proposition 26 requirements and recent legal

challenges

Net energy metering

© PA Knowledge Limited 2013 17

© PA Knowledge Limited 2013

REVENUE REQUIREMENT ANALYSIS WATER SYSTEM

© PA Knowledge Limited 2013 18

Water System Revenue Requirement Analysis How Funds are Used?

95% of the change between LADWP’s Water Revenue Fund actual spending in FY

2013-14 to proposed spending in FY 2019-20 (O&M and capex) is projected to be

non-labor. • Non-labor spending is projected to

increase from $382M in FY 2013-14 to

$1.15B in FY 2019-20.

• The average annual Water System

spending of $1.5 billion per year over the

five-year rate action will support an annual

18,000 jobs and induce an annual $4

billion in additional economic activity and

output.*

Non-labor expenditures include outside services and materials

*Source: Derived from Exhibit 3-2, page 14. “Los Angeles Department of Water and Power: Supplying Power, Water and Jobs for Los Angeles,” September 2012. Economic and Policy

Analysis Group; Los Angeles County Economic Development Corporation

© PA Knowledge Limited 2013 19

Water System Revenue Requirement Analysis Current Revenue Situation

Based on an analysis of the financial plan, underlying budget and required major

programs, LADWP’s current Water System revenues will not cover the revenue

requirement.

• Capital spending for

infrastructure and mandated

programs is a large driver.

• The gap slowly increases over

time as investments are made.

*Purchased water is based on the current assumption of normal hydrology for the next five-years, which is subject to change.

*

© PA Knowledge Limited 2013 20

Water System Revenue Requirement Analysis Incremental Required Revenues

To meet its obligations, LADWP will require $90 million

in additional revenue requirement on average over the

next five years (not including the impact of purchased water).

Five-Year Revenue Requirement

Source Five Years ($M)

Infrastructure $300

Conservation* ($30)

Water Quality $108

Water recycling $22

Stormwater $8

Groundwater $24

Owens Valley $19

Purchased water** ($220)

Total $230

Revenue Requirement

Rate Driver Average Annual Increase ($M)

Infrastructure $59

Conservation (Securitization)* ($6)

Water Quality $22

Groundwater (Securitization) $5

Stormwater $2

Recycled Water $4

Owens Valley $4

Total before Purchased Water $90

Purchased Water** ($44)

Total $46

*Many conservation investments are eligible for lower financing through

securitization, resulting in a reduction in revenue requirement.

**Purchased water is negative due to the current assumption of normal hydrology for

the next five-years.

Infrastructure and water quality are the major

drivers of revenue requirement.

© PA Knowledge Limited 2013 21

Water System Revenue Requirement Analysis Meeting Regulatory Obligations and Increasing Infrastructure Investment

LADWP’s revenue requirement should allow the Department to meet water quality

mandates, increase local supply and increase infrastructure reliability investments in

a measured manner.

New revenues will help reduce the mainline

replacement cycle from 250 to 182 years, which

is a good movement towards a more reliable and

sustainable infrastructure

The revenue requirement reflects an increase in

conservation and a gradual shift to a more local water

supply (assuming a return to normal hydrology).

© PA Knowledge Limited 2013 22

© PA Knowledge Limited 2013

REVENUE REQUIREMENT ANALYSIS POWER SYSTEM

© PA Knowledge Limited 2013 23

Power System Revenue Requirement Analysis How Funds are Used?

80% of the change between LADWP’s Power Revenue Fund actual spending in FY

2013-14 to proposed spending in FY 2019-20 (O&M and capex) is projected to be

non-labor.

Non-labor expenditures include outside services and materials

*Source: Derived from Exhibit 3-2, page 14. “Los Angeles Department of Water and Power: Supplying Power, Water and Jobs for Los Angeles,” September 2012. Economic and Policy

Analysis Group; Los Angeles County Economic Development Corporation

• Non-labor spending is projected to

increase from $827M in FY 2013-14 to

$1.41B FY 2019-20.

• The average annual Power System

spending of $2.65 billion per year over the

five-year rate action will support an annual

33,321 jobs and induce an annual $8.39

billion in additional economic activity and

output.*

© PA Knowledge Limited 2013 24

Power System Revenue Requirement Analysis Current Revenue Situation

Based on an analysis of the financial plan, underlying budget and required major

programs, LADWP’s current Power System revenues will not cover the revenue

requirement.

• Capital spending for

infrastructure and mandated

supply programs is a large

driver.

• The gap slowly increases over

time as investments are made.

© PA Knowledge Limited 2013 25

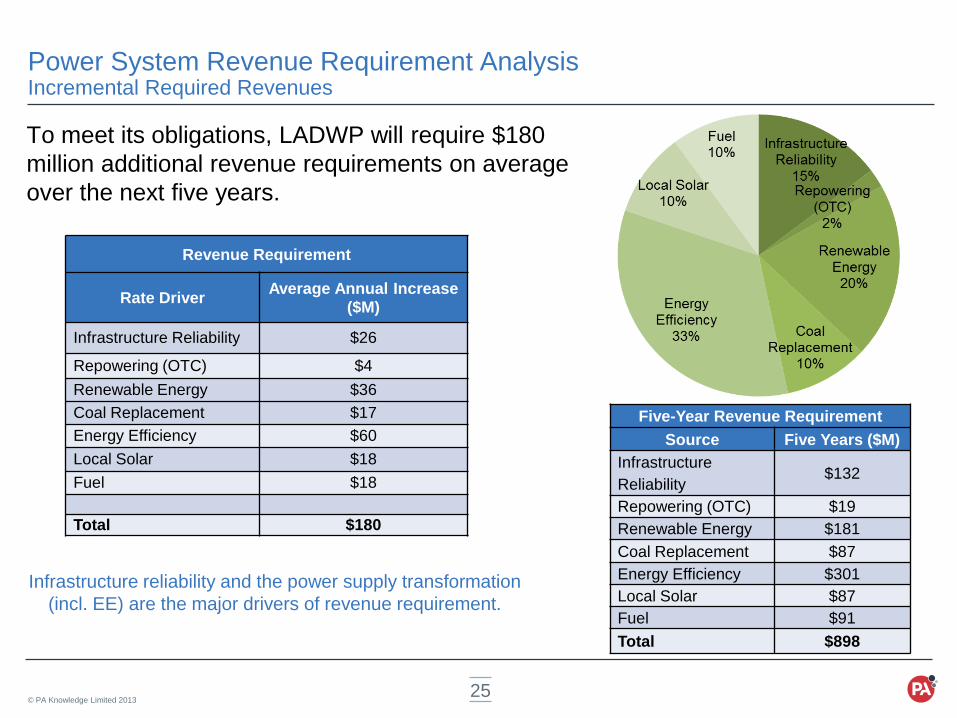

Power System Revenue Requirement Analysis Incremental Required Revenues

To meet its obligations, LADWP will require $180

million additional revenue requirements on average

over the next five years.

Five-Year Revenue Requirement

Source Five Years ($M)

Infrastructure

Reliability $132

Repowering (OTC) $19

Renewable Energy $181

Coal Replacement $87

Energy Efficiency $301

Local Solar $87

Fuel $91

Total $898

Revenue Requirement

Rate Driver Average Annual Increase

($M)

Infrastructure Reliability $26

Repowering (OTC) $4

Renewable Energy $36

Coal Replacement $17

Energy Efficiency $60

Local Solar $18

Fuel $18

Total $180

Infrastructure reliability and the power supply transformation

(incl. EE) are the major drivers of revenue requirement.

© PA Knowledge Limited 2013 26

Power System Revenue Requirement Analysis Increasing Infrastructure Reliability and Meeting Regulatory Obligations

LADWP’s revenue requirement should allow the Department to meet renewable

energy mandates and increase infrastructure reliability investments in a measured

manner.

The number of poles over fifty years old will

decrease over five years, but the average

age will still be over fifty years.

Elimination of Once-Through Cooling continues to be a major

LADWP program as LADWP meets EPA mandates.

© PA Knowledge Limited 2013 27

© PA Knowledge Limited 2013

INDUSTRY RATE TRENDS

© PA Knowledge Limited 2013 28

Industry Rate Trends Water Utilities

LADWP has not had a base water rate change in over five years; however, other

major California cities have been increasing rates to address the challenges facing

the industry.

• Water utility rate increases are

expected to continue as more

drought management programs

are implemented and aging

infrastructure replacement

accelerates.

• LADWP’s typical single- family

residential customer bill is

currently very competitive, a

situation expected to continue as

other water utilities increase rates.

Anticipated increases are either proposed or approved.

Bill comparisons for utilities with water budgets were based on medium temperature zone, low season, lot size < 7,500 sqft,

three people per household, January month, 1,500 sqft irrigable land and lowest pumping zone charge where applicable.

© PA Knowledge Limited 2013 29

Industry Rate Trends Power Utilities

LADWP has not had a base power rate increase for three of the last five years;

however, other major California cities have been steadily increasing rates to address

the challenges facing the industry.

• Power utility rate increases are

expected to continue to allow utilities

to increase infrastructure

replacement and meet additional

regulatory requirements.

• LADWP’s typical customer bill is

currently less than most other major

California cities on average.

Anticipated increases are either proposed or approved.

Bill comparisons based on 500kWh usage in summer

© PA Knowledge Limited 2013 30

© PA Knowledge Limited 2013

SUMMARY

© PA Knowledge Limited 2013 31

Summary

LADWP’s proposed five-year revenue requirement has been developed based on a

comprehensive budget and financial plan that was developed to balance program

needs and customer rate implications.

• Incremental revenue will be invested largely in

infrastructure and regulatory mandated programs.

• Competitive bidding will help ensure efficient use of

financial resources.

• Increased use of contract resources will help control

costs and increase business development in the Los

Angeles Region.

• The revenue requirement should allow LADWP to

maintain Board approved financial metrics.

Given the trend toward increasing water and power

rates in California (and elsewhere in the United States)

LADWP customer rates should remain competitive.

Major Water Rate Drivers

Infrastructure

Water Quality

Sustainable Local Water Supply

Owens Valley Regulatory Compliance

Purchased Water*

*Purchased water can increase or decrease the revenue requirement depending on hydrology conditions.

Major Power Rate Drivers

Infrastructure

Power Supply Transformation

Renewable Energy Resources

Customer Opportunity Programs (EE, local

solar)

Fuel

Recommended