TRENDS IN GLOBAL CLEAN ENERGY FINANCE

Michael Liebreich

Chairman of the Advisory Board

Twitter: @mliebreich

Our Common Future under Climate

Change, Paris, 9 July 2015

1 Michael Liebreich Our Common Future under Climate Change, Paris, 9 July 2015 @MLiebreich

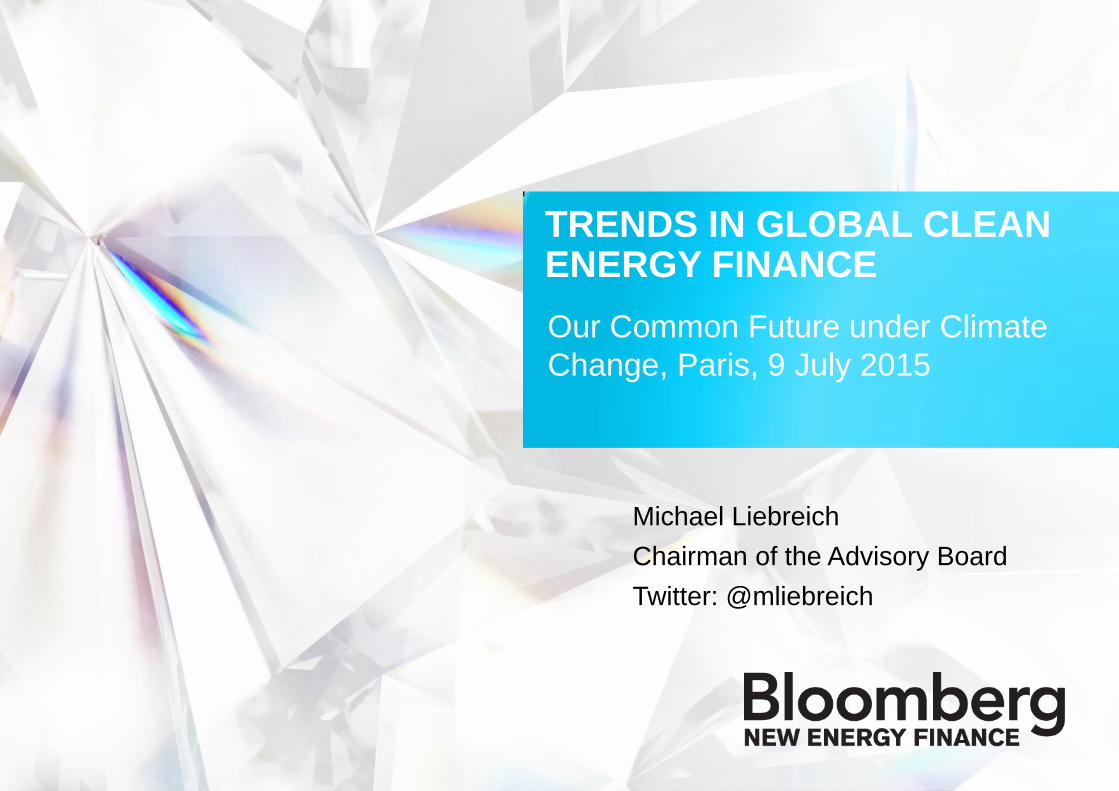

Note: Total values include estimates for undisclosed deals. Includes corporate and government R&D, and spending for

digital energy and energy storage projects (not reported in quarterly statistics), as well as a BNEF estimate for large hydro

investment. Source: Bloomberg New Energy Finance

NEW INVESTMENT IN CLEAN ENERGY 2004–14 ($BN)

0

50

100

150

200

250

300

350

400

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

30%

50%

27%

12% -9%

35%

7% -7%

-8%12%

0

100

200

300

400

500

600

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 20142015 Q1

Expected

Large hydro

Other

Solar

Wind

2 Michael Liebreich Our Common Future under Climate Change, Paris, 9 July 2015 @MLiebreich

TOTAL INVESTMENTS PER TECHNOLOGY, 2015-40 (US$ REAL)

Source: Bloomberg New Energy Finance

RENEWABLES TAKE

65% OF THE $12.2

TRILLION POWER

INVESTMENT TO 2040

3 Michael Liebreich Our Common Future under Climate Change, Paris, 9 July 2015 @MLiebreich

Emissions must be cut 40-70% by mid-century

and phased out entirely by 2100

G7 JUNE 2015 – SCHLOSS ELMAU

Picture: Wikimedia

4 Michael Liebreich Our Common Future under Climate Change, Paris, 9 July 2015 @MLiebreich

There is an urgent need to

develop sources of

renewable energy.

LAUDATO SI – DEMAND SIDE

Pope Francis

Picture: Wikimedia

5 Michael Liebreich Our Common Future under Climate Change, Paris, 9 July 2015 @MLiebreich

Source: The Economist

THE ECONOMIST COVER, “SHEIKHS VERSUS SHALE” DECEMBER 2014

6 Michael Liebreich Our Common Future under Climate Change, Paris, 9 July 2015 @MLiebreich

Note: Prices are in real (2014) USD Source: Bloomberg New Energy Finance, Maycock

SOLAR PV EXPERIENCE CURVE (US$/W)

1988

1976

1998

2004

2014

2008

0,1

1

10

100

1 10 100 1 000 10 000 100 000 1 000 000 10 000 000

Cumulative production (MW)

SOLAR PV MODULE

COSTS HAVE FALLEN

99% SINCE 1976

80% SINCE 2008

7 Michael Liebreich Our Common Future under Climate Change, Paris, 9 July 2015 @MLiebreich

Source: Bloomberg New Energy Finance

6-CENT SOLAR – THE NEW NORMAL?

Name:

Team:

Event:

Date:

Record:

Usain Bolt

Jamaica

100m

August 2008

9.58 seconds

Name:

Team:

Event:

Date:

Record:

Paddy Padmanathan

ACWA Power

Solar PV

January 2015

US$5.84c

8 Michael Liebreich Our Common Future under Climate Change, Paris, 9 July 2015 @MLiebreich

NEW INVESTMENT IN CLEAN ENERGY 2004-2014 ($BN)

Note: Does not include carbon capture and storage

0.6 0.8 1.2 2.5 2.6 1.7 4.5 3.2 10.9 9.513.6

04 05 06 07 08 09 10 11 12 13 14

Middle East & Africa

27.738.1

51.872.6

87.5 89.0

119.2129.1

98.3

66.0 66.5

04 05 06 07 08 09 10 11 12 13 14

Europe

18.425.330.940.9

52.365.0

78.798.3

113.2126.5

154.3

04 05 06 07 08 09 10 11 12 13 14

Asia & Oceania

11.819.037.345.546.839.5

55.372.6

59.055.460.8

04 05 06 07 08 09 10 11 12 13 14

North America & Caribbean

1.5 4.5 6.9 13.1 15.8 10.7 13.8 13.4 12.5 10.2 14.6

04 05 06 07 08 09 10 11 12 13 14

Central & South America

Source: Bloomberg New Energy Finance

9 Michael Liebreich Our Common Future under Climate Change, Paris, 9 July 2015 @MLiebreich

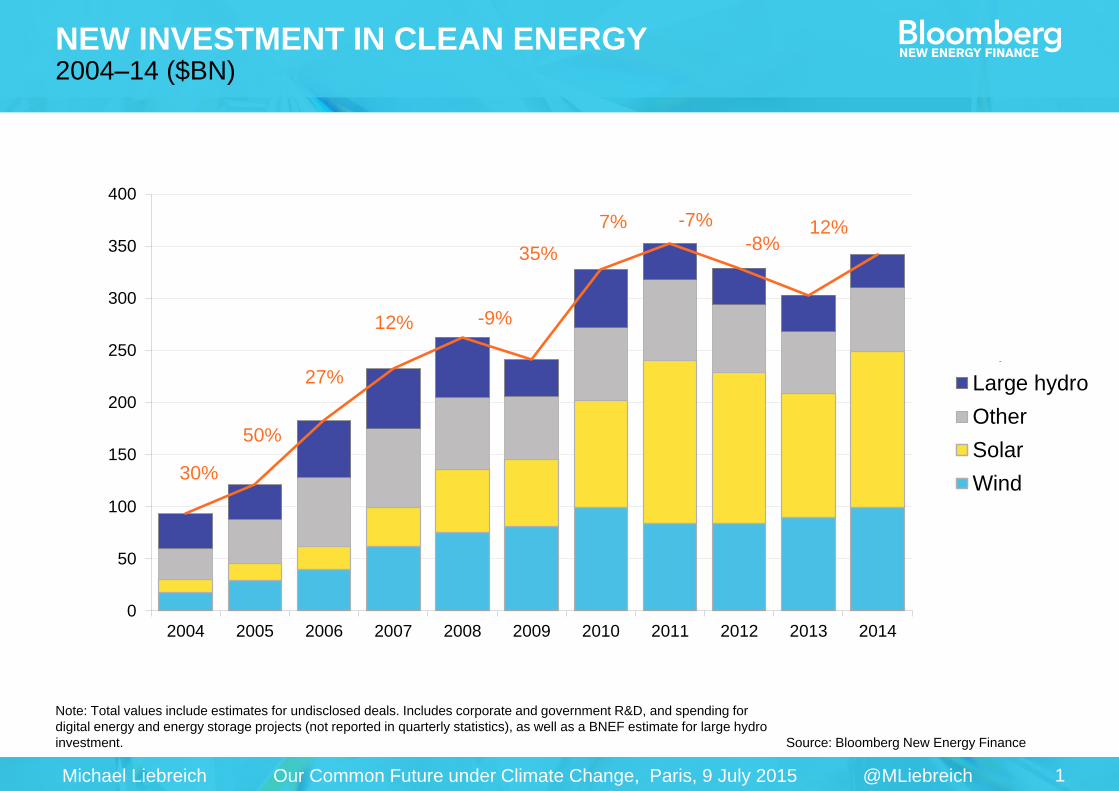

US & CHINA CAPACITY BUILD OUT (GW)

Source: Bloomberg New Energy Finance

US China

9201,163

442

442

996

1,362

2,601

2014 2030

Incrementallow-carbon

Low-carbon

Fossil fuels

792 810

302 302

2731,094

1,384

2014 2030

Incrementallow-carbon

Low-carbon

Fossil fuels

China’s low-carbon

additions 2015-2030

~ 90% of US 2015

capacity

10 Michael Liebreich Our Common Future under Climate Change, Paris, 9 July 2015 @MLiebreich

RENEWABLES IN INDIA, 2006–22 (GW)

0

50

100

150

200

250

Upto2006

2008 2010 2012 2014 2016 2018 2020 2022

Solar 0.6GW/year

Wind 2.0GW/year

11 Michael Liebreich Our Common Future under Climate Change, Paris, 9 July 2015 @MLiebreich

Source: Bloomberg New Energy Finance

RENEWABLES IN INDIA, 2006–22 (GW)

0

50

100

150

200

250

Upto2006

2008 2010 2012 2014 2016 2018 2020 2022

Solar 0.6GW/year

Wind 2.0GW/year

Solar 6 GW/year

Wind 3 GW/year

12 Michael Liebreich Our Common Future under Climate Change, Paris, 9 July 2015 @MLiebreich

Source: Bloomberg New Energy Finance

RENEWABLES IN INDIA, 2006–22 (GW)

0

50

100

150

200

250

Upto2006

2008 2010 2012 2014 2016 2018 2020 2022

Solar 0.6GW/year

Wind 2.0GW/year

Solar 6 GW/year

Wind 3 GW/year

X

Modi target:

Solar 12 GW/year

Wind 8 GW/year

13 Michael Liebreich Our Common Future under Climate Change, Paris, 9 July 2015 @MLiebreich

RENEWABLES GENERATION CUMULATIVE CAPACITY 2020 – 2040

0GW

1,000GW

2,000GW

3,000GW

4,000GW

5,000GW

6,000GW

7,000GW

8,000GW

2020 2030 2040

IEA 450

IEA Current Policies

IEA New Policies

World EnergyCouncil Symphony

World EnergyCouncil Jazz

BNEF

Source: Bloomberg New Energy Finance, World Energy Council, IEA

RENEWABLE CAPACITY

UNDER NEO WILL BE 50%

HIGHER IN 2040 THAN IEA

NEW POLICIES SCENARIO

14 Michael Liebreich Our Common Future under Climate Change, Paris, 9 July 2015 @MLiebreich

MAJOR GLOBAL SHALE FIELDS

Source: EIA Assessment of World Shale Gas Resources, April

2011 Note: Technically recoverable shale gas resources shown

Canada

Brazil

Poland Norway

China

Australia

South Africa 200 trillion

cubic feet

USA

Mexico

Libya

Algeria

Argentina

UK

15 Michael Liebreich Our Common Future under Climate Change, Paris, 9 July 2015 @MLiebreich

Note: For the underlying data to this chart, go to BI LNGGG<GO> Source: Bloomberg New Energy Finance

LNG EXPORT CAPACITY BY COUNTRY/REGION (MMTPA)

0

100

200

300

400

500

600

700

800

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8

201

9

202

0

Other

North America

Russia

East Africa

West Africa

Australia

Other

North America

Russia

West Africa

North Africa

Indonesia

Malaysia

Australia

Qatar

Demand

Pre

-FID

O

pe

rati

on

al,

un

de

r c

on

str

uc

tio

no

r p

os

t-F

ID

16 Michael Liebreich Our Common Future under Climate Change, Paris, 9 July 2015 @MLiebreich

0

2

4

6

8

10

12

14

16

18

20

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Note: Japan-Korea Marker is based on broker assessments of the spot price of un-contracted LNG cargoes delivered into

the Northeast Asia market.

Source: Bloomberg New Energy Finance,

ICAP, Platts

OIL AND GAS PRICES: HENRY HUB, NBP, BAFA, AND NE LNG, 2004–15 (US$/MMBTU)

0

2

4

6

8

10

12

14

16

18

20

NBP (UK)

Henry Hub (US)

BAFA (Germanyborder price forRussian gas)

North East Asia LNG

~ $5 spread to

Henry Hub?

17 Michael Liebreich Our Common Future under Climate Change, Paris, 9 July 2015 @MLiebreich

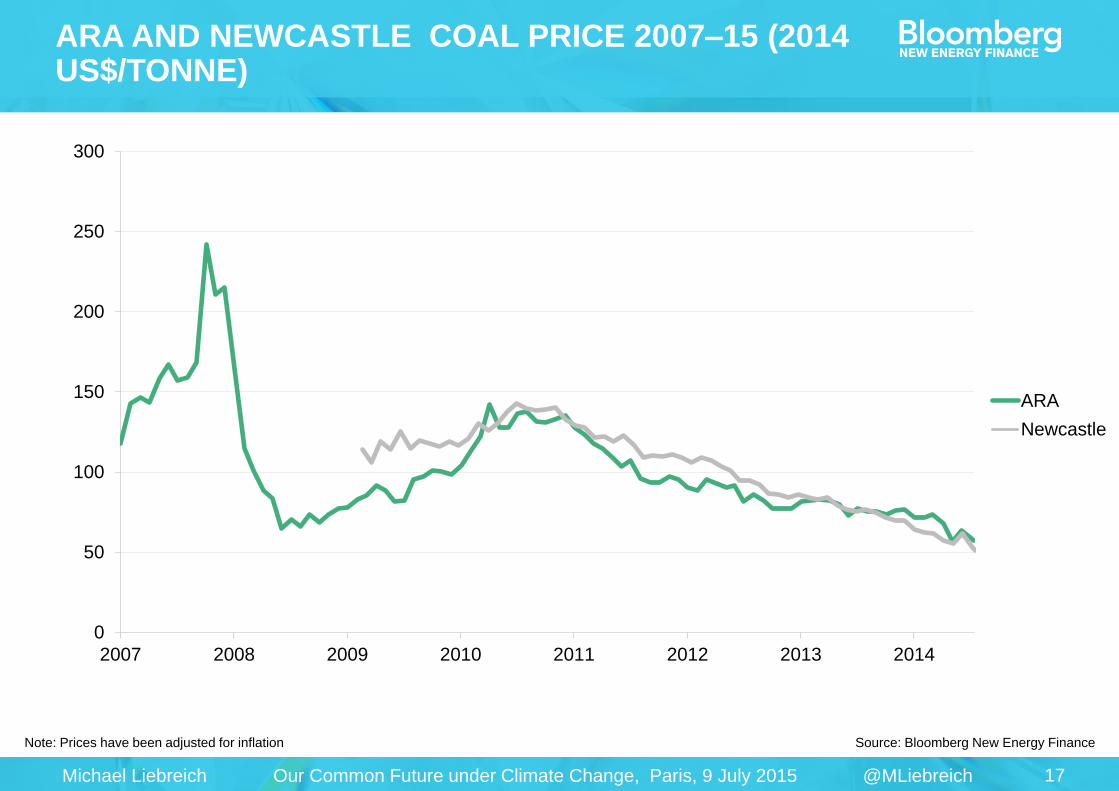

Note: Prices have been adjusted for inflation Source: Bloomberg New Energy Finance

ARA AND NEWCASTLE COAL PRICE 2007–15 (2014 US$/TONNE)

0

50

100

150

200

250

300

2007 2008 2009 2010 2011 2012 2013 2014

0

50

100

150

200

250

300

2007 2008 2009 2010 2011 2012 2013 2014

ARA

Newcastle

18 Michael Liebreich Our Common Future under Climate Change, Paris, 9 July 2015 @MLiebreich

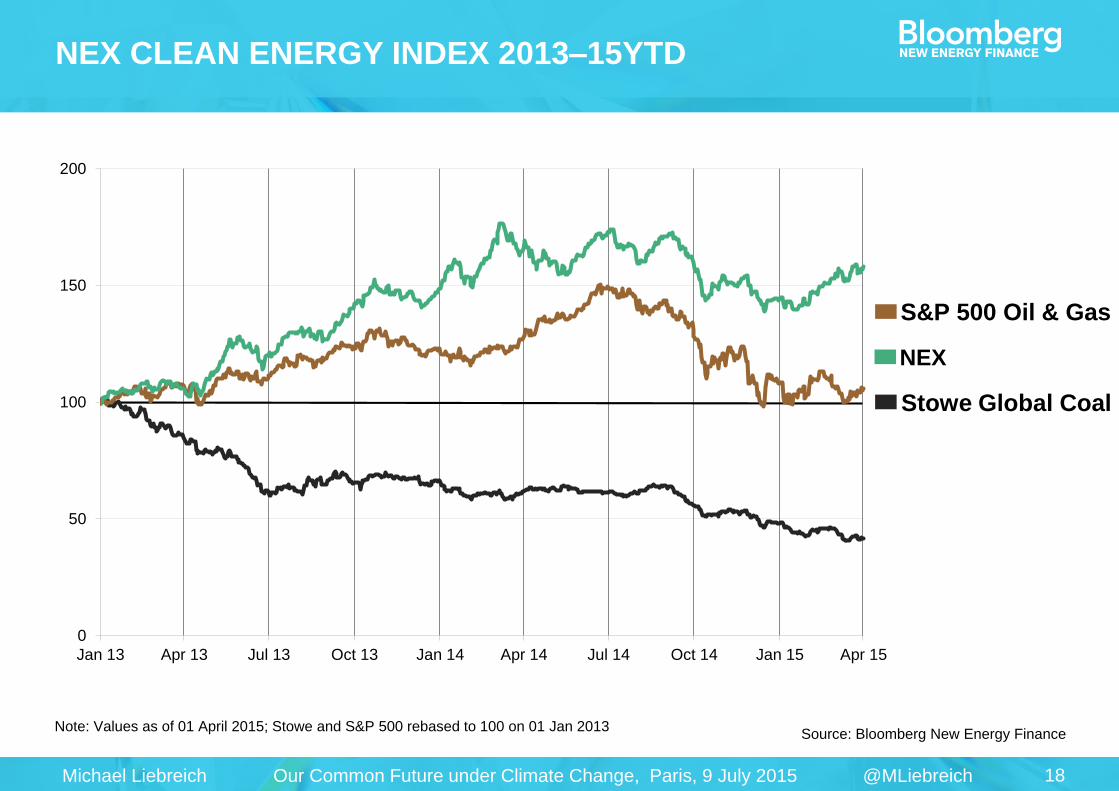

Note: Values as of 01 April 2015; Stowe and S&P 500 rebased to 100 on 01 Jan 2013 Source: Bloomberg New Energy Finance

NEX CLEAN ENERGY INDEX 2013–15YTD

0

50

100

150

200

Jan 13 Apr 13 Jul 13 Oct 13 Jan 14 Apr 14 Jul 14 Oct 14 Jan 15 Apr 15

S&P 500 Oil & Gas

Stowe Global Coal

NEX

19 Michael Liebreich Our Common Future under Climate Change, Paris, 9 July 2015 @MLiebreich

NUCLEAR POWER PLANTS – HISTORIC CONSTRUCTION

0

1

2

3

4

5

6

1

Chart Title

0-10

11-19

20-39

40-59

60+

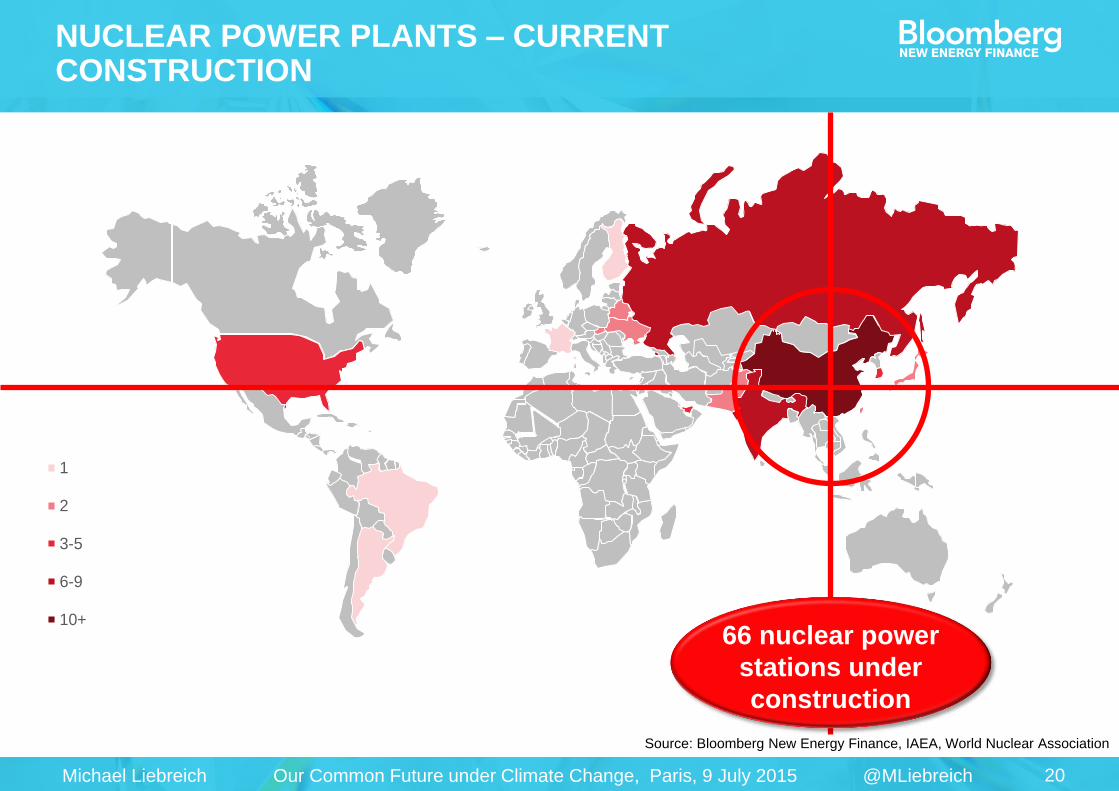

Source: Bloomberg New Energy Finance; IAEA, World Nuclear Association

566 nuclear

power stations

ever built

20 Michael Liebreich Our Common Future under Climate Change, Paris, 9 July 2015 @MLiebreich

Chart Title

1

2

3-5

6-9

10+

Source: Bloomberg New Energy Finance, IAEA, World Nuclear Association

66 nuclear power

stations under

construction

NUCLEAR POWER PLANTS – CURRENT CONSTRUCTION

21 Michael Liebreich Our Common Future under Climate Change, Paris, 9 July 2015 @MLiebreich

There is still a need to

develop adequate storage

technologies.

LAUDATO SI – INTEGRATION

Pope Francis Picture: Wikimedia

22 Michael Liebreich Our Common Future under Climate Change, Paris, 9 July 2015 @MLiebreich

ENERGY RETAIL BATTLEFIELD

HIVE home

heating

controls

Smart

thermostats to

reduce churn

Virtual mobile

operator – 80k

customers

Smart home

partnerships/investment

IHD and smart

thermostat

program

BEMS for DR

and energy

efficiency

Smart thermostats

and load

disaggregation

Integrated smart

homes

Smart

lighting /

home

automation

Smart

thermostats and

‘behavioural’ DR

Residential

energy

storage

HEM tools

and DR

Home energy

management

Behavioural

engagement

Smart thermostats,

home automation

Load disaggregation

Solar PV and

energy monitoring

HEM tools

Smart

thermostats

Smart

thermostats Connected

home / IoT

Load

disaggregation

Heating controls

Home

automation

HomeKit

1m connected

home

customers

Digital Life

connected

home service

Smart home

platform

(AT&T)

Nest

acquisition

Smart home

hubs

HEMS

platform

DR and retail

services

Energy supply

and services

Registered

energy supplier

Home

automation

Home automation

???

Bundled electricity

telecoms services

Bundled electricity,

entertainment and

home automation

Bundled telecoms

and energy

Bundled telecoms,

energy. Residential

energy storage.

Bundled telecoms,

electricity supply

beginning in 2016

Bundled insurance,

telecoms and energy

Bundled telecoms,

electricity and gas

23 Michael Liebreich Our Common Future under Climate Change, Paris, 9 July 2015 @MLiebreich

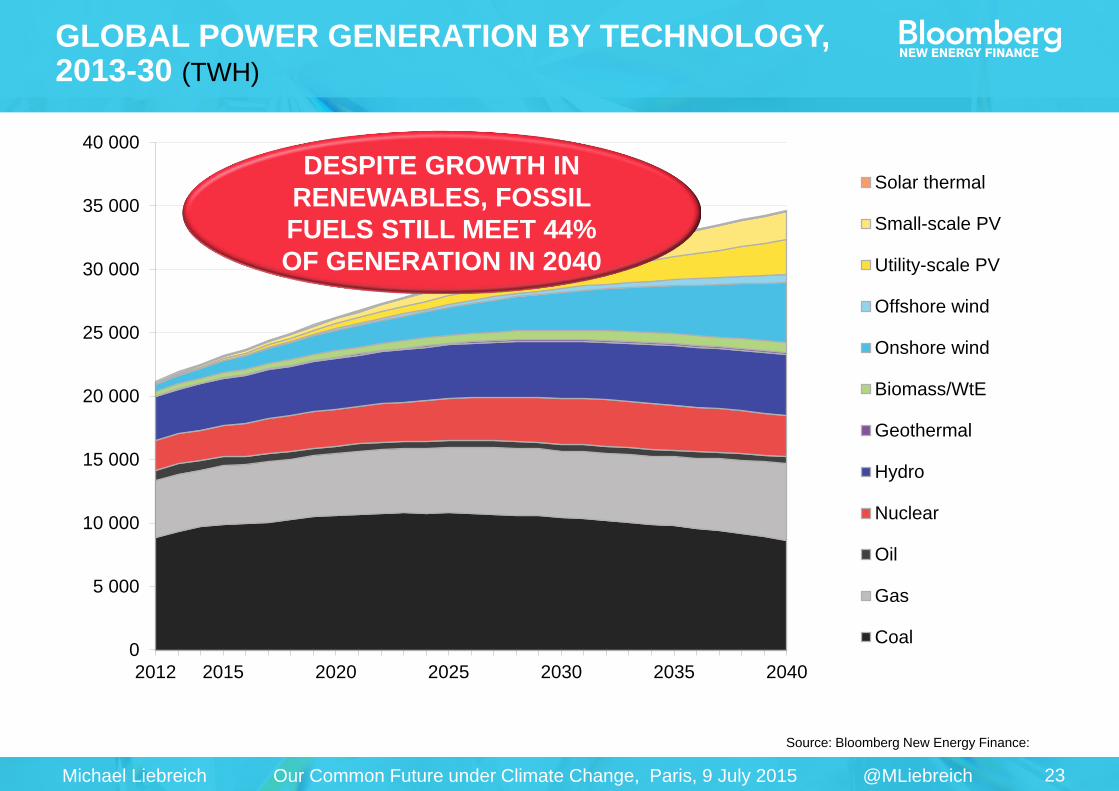

GLOBAL POWER GENERATION BY TECHNOLOGY, 2013-30 (TWH)

0

5 000

10 000

15 000

20 000

25 000

30 000

35 000

40 000

2012 2015 2020 2025 2030 2035 2040

Solar thermal

Small-scale PV

Utility-scale PV

Offshore wind

Onshore wind

Biomass/WtE

Geothermal

Hydro

Nuclear

Oil

Gas

Coal

Source: Bloomberg New Energy Finance:

DESPITE GROWTH IN

RENEWABLES, FOSSIL

FUELS STILL MEET 44%

OF GENERATION IN 2040

Unique analysis, tools and data for decision-makers

driving change in the energy system

MARKETS Renewable Energy

Energy Smart Technologies

Advanced Transport

Gas

Carbon and RECs

SERVICES Americas Service

Asia Pacific Service

EMEA Service

Applied Research

Events and Workshops

Michael Liebreich

Twitter: @mliebreich

Thanks!

Recommended