INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

© OECD/IEA 2008

Liberalised electricity market

experience in OECD countries

Francois Nguyen

Senior Policy Advisor - Electricity

Office of Long Term Co-operation and Policy Analysis

Regulatory Reform Review

Working Group Seminar

Beijing - 28 March 2008

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

© OECD/IEA 2008

Outline

Introduction

Global energy challenges

Evolving electricity market structure

Security of supply and market delivery of

investments

Marginal pricing and competitive market

regulation

Empowering consumers for demand

participation

Conclusions

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

© OECD/IEA 2008

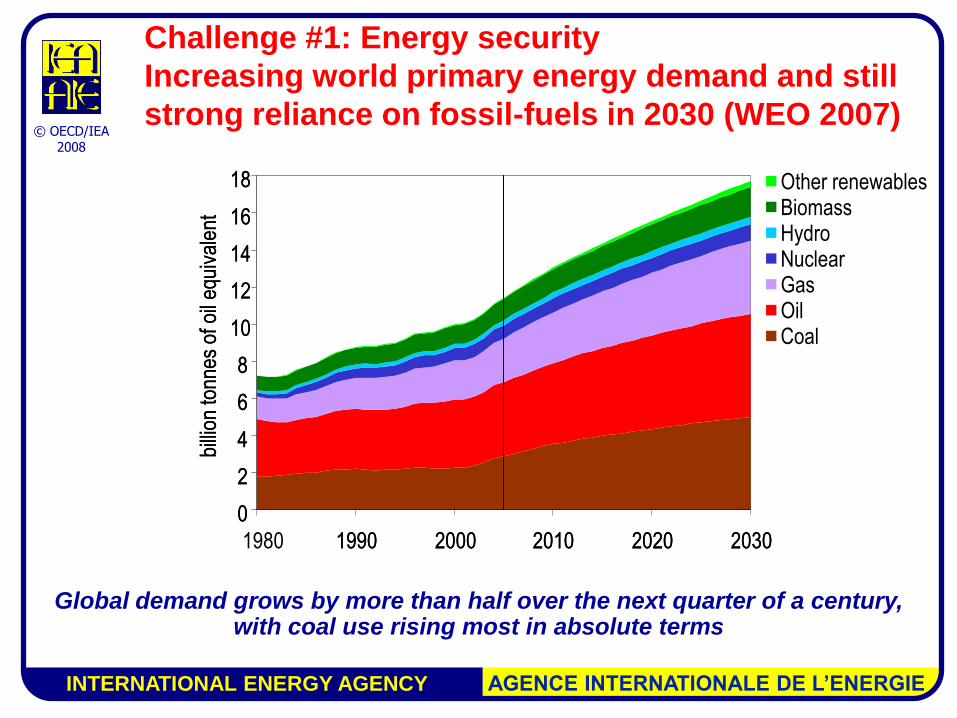

Challenge #1: Energy security

Increasing world primary energy demand and still

strong reliance on fossil-fuels in 2030 (WEO 2007)

Global demand grows by more than half over the next quarter of a century, with coal use rising most in absolute terms

0

2

4

6

8

10

12

14

16

18

1980 1990 2000 2010 2020 2030

billi

on to

nnes

of o

il eq

uiva

lent

0

2

4

6

8

10

12

14

16

18

1990 2000 2010 2020 2030

billi

on to

nnes

of o

il eq

uiva

lent

Other renewablesBiomassHydroNuclearGasOilCoal

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

© OECD/IEA 2008

Challenge #2: Energy investments

Huge investments will be required over the period

to 2030

0 1 000 2 000 3 000 4 000 5 000

OECD North America

China

OECD Europe

Transition economies

Middle East

Latin America

Africa

Rest of developing Asia

India

OECD Pacific

Inter regional transport

billion dollars (2006)

CoalOilGasElectricity

0 1 000 2 000 3 000 4 000 5 000

-

billion dollars (2006)

CoalOilGasElectricity

China and India account for 22 % of global energy investments

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

© OECD/IEA 2008

Challenge # 3: Climate change

CO2 emissions are on an unsustainable path

Stabilising greenhouse-gas concentration at 450 ppm would require

emissions to be reduced to 23 Gt in 2030

10

15

20

25

30

35

40

45

2005 2010 2015 2020 2025 2030

Gt o

f CO

2

CCS in industry - 3%CCS in power generation - 9%Nuclear - 13%

Renewables - 20%

Switching from coal to gas - 8%End Use electricity efficiency - 17%

End Use fuel efficiency - 30%

Reference Scenario

42 Gt

450 Stabilisation Case

23 Gt

27 Gt

Energy-Related CO2 Emissions

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

© OECD/IEA 2008

Evolving market structure:

Before reform

Centralised

investment decisions

Investment driven by

economies of scale

All risks and costs

passed-through

Regulated return on

investments

Vertically Integrated Utility

•Generation

•Transmission

•Distribution

Customers

Few incentives for efficiency, innovation or least-cost risk management

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

© OECD/IEA 2008

Evolving market structure:

After reform

Competitive generation

Generation investments

driven by risk/return

equation

T&D remain regulated

Unbundling limits pass -

through

Strong incentives for least-

cost risk management

Generators

Customers

T& D and related network services

LDC/ Retailers

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

© OECD/IEA 2008

Transmission in liberalised markets

Before Connect large scale generation

sources to load centers

Means to achieve economies of scale

Often a complement to generation

Planning is centralised and well coordinated

Reliability investments

After Connect diversified generation

sources to load centers

Means to achieve energy diversification and competitive markets – open and non discriminatory access

Can be a substitute to generation

Planning is more complex

Reliability and economic investments

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

© OECD/IEA 2008

“Unbundling” security of supply

Reliability of electricity supply

Energy security

Coal, natural gas, uranium...

Adequacy System security

Generation capacity,

transmission and

distribution networks

Operation, control,

contingency management...

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

© OECD/IEA 2008

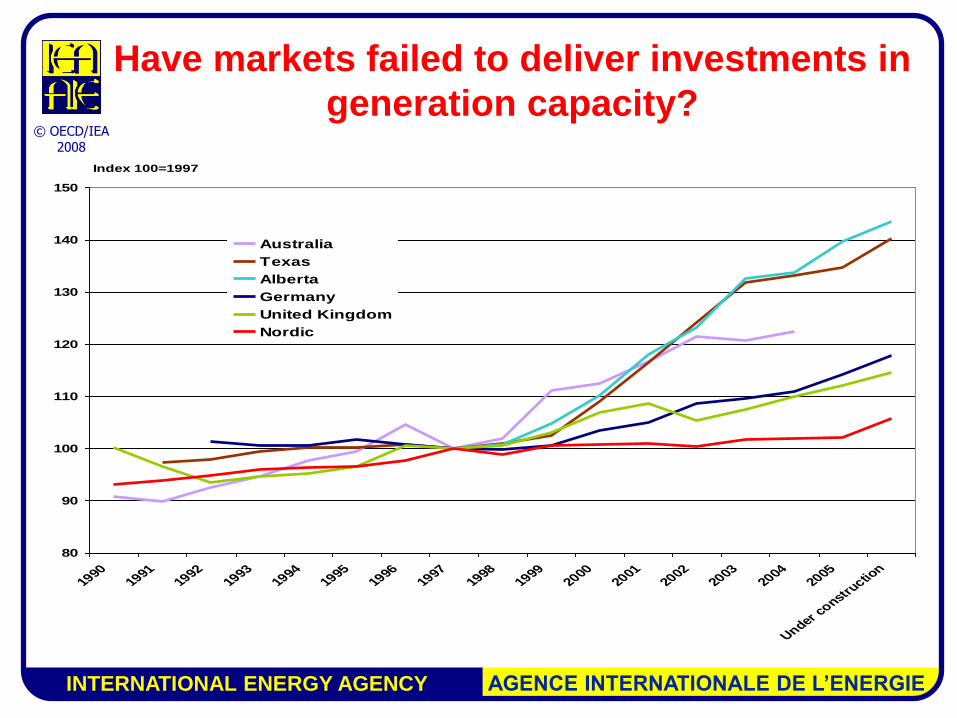

Have markets failed to deliver investments in

generation capacity?

80

90

100

110

120

130

140

150

19901991

19921993

19941995

19961997

19981999

20002001

20022003

20042005

Under constru

ction

Australia

Texas

Alberta

Germany

United Kingdom

Nordic

Index 100=1997

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

© OECD/IEA 2008

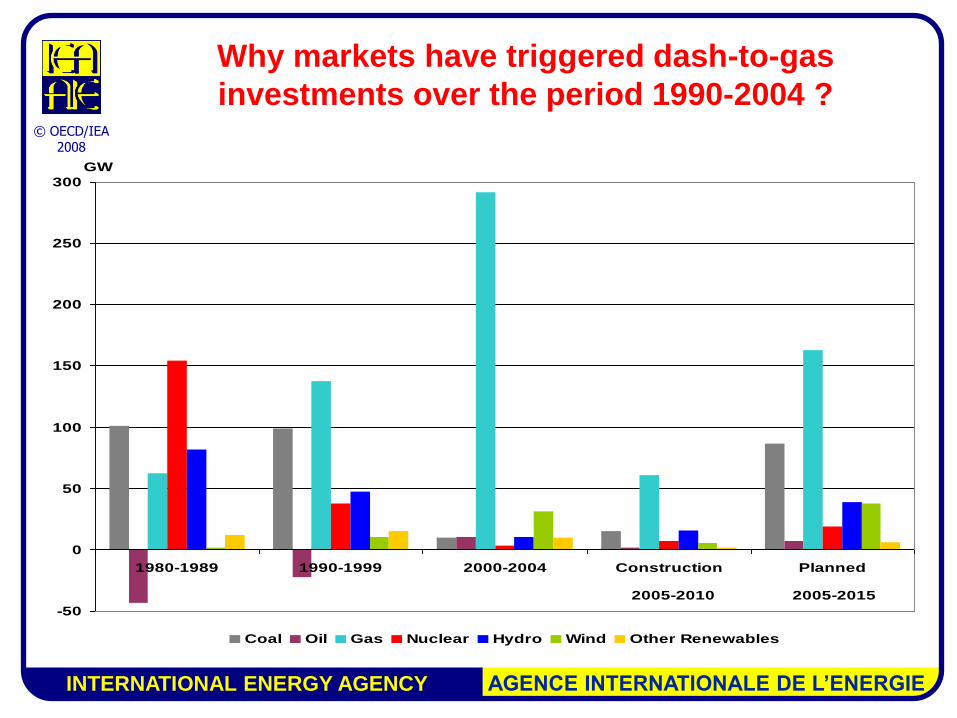

Why markets have triggered dash-to-gas

investments over the period 1990-2004 ?

-50

0

50

100

150

200

250

300

1980-1989 1990-1999 2000-2004 Construction Planned

Coal Oil Gas Nuclear Hydro Wind Other Renewables

GW

2005-2010 2005-2015

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

© OECD/IEA 2008

Risk and return assessment tends to favour

investments in gas-fired power plants

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

© OECD/IEA 2008

Market reform and grid reliability

Market reform is not to blame for the 2003

blackout in North America

Liberalised markets have contributed to:

increased cross-border and regional trade

longer distance use of transmission

infrastructure

greater, more volatile and less predictable

grid usage

Creating new real-time challenges for system

operators

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

© OECD/IEA 2008

Marginal pricing ensures optimal dispatch

in competitive generation markets

Decentralised decision making in competitive markets is a strong instrument to ensure optimal dispatch

Lack of price elasticity on the demand side may be the critical market failure for a robust price settlement at all times

Must run (e.g. wind)

Nuclear

Coal

Gas

Oil & old plants

USD/MWh

MW

0

to

- ?

15

to

5

40

to

20

55

to

40

100

to

60

Demand

- off peak

Demand

- peak

Demand

- extreme

Supply

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

© OECD/IEA 2008

Example of price responsiveness in

the Nordic markets

Nordic drought

-30%

-20%

-10%

0%

10%

20%

30%

1 8 15 22 29 36 43 50 5 12 19 26 33 40 47 2 9 16 23 30 37 44 51

-900

-600

-300

0

300

600

900

Norway hydro - Deviation from median, %

2002 2003 2004 WeekSource: adapted from ECON Energy, 2003

-30%

1

-900

-600

-300

0

300

600

900

Sweden hydro - Deviation from median, %

-30%

1

-900

-600

-300

0

300

600

900

Nord Pool System price, NOK/MWh

Price: NOK/MWh

-30%

1

-900

Net trade Norway to Sweden, GWh

Trade: GWh

1 EURO = 8 NOK

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

© OECD/IEA 2008

Flexibility is critical for market clearing in

tight situations

Cost reflective pricing creates incentives for flexible resources to meet peak-load particularly in situations of scarcity

Price caps and other market intervention mute incentives

Imports,open cycle gas,

back up generation,demand response

USD/MWh

MW

10000to

100

Imports

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

© OECD/IEA 2008

Increasing cross-border trade improves supply

flexibility

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

© OECD/IEA 2008

Demand participation makes markets

work better

Price

Quantitiy

Supply

Inelastic

Demand

Inelastic Clearing Price

Elastic

Demand

Elastic Clearing Price

Less demand

- improved

reliability

- less investment

Lower prices

- improved efficiency

- reduced market power

Consumption is not homogenous

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

© OECD/IEA 2008

Empowering consumers:

the third pillar

Retail competition protects and brings the benefits

to the consumer through competitive prices,

customer choice and innovation

Demand response to price adds real resources to

the system

Transparent prices improve framework for energy

efficiency

Balancing supply & demand investment

Mitigate possible abuse of market power

Large potential benefits still remain to be realised

De

ma

nd

Tra

ns

mis

sio

n

Ge

ne

rati

on

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

© OECD/IEA 2008

Real competition is a prerequisite

Unbundling

Truly independent system operation

Market rules giving fair and easy access to all

market players

Regulation of natural monopolies

Regulation of competition

Liberalisation is a process that requires political

commitment and strong government involvement

Competitive market framework provides signals to

market participants

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

© OECD/IEA 2008

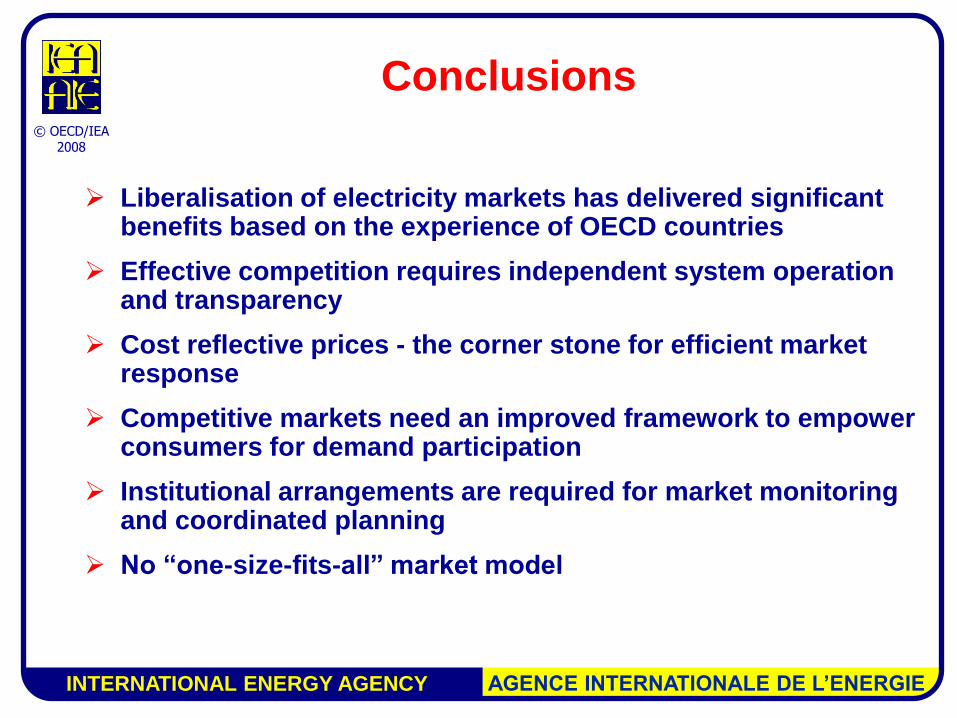

Conclusions

Liberalisation of electricity markets has delivered significant benefits based on the experience of OECD countries

Effective competition requires independent system operation and transparency

Cost reflective prices - the corner stone for efficient market response

Competitive markets need an improved framework to empower consumers for demand participation

Institutional arrangements are required for market monitoring and coordinated planning

No “one-size-fits-all” market model

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

© OECD/IEA 2008

Thank you!

Some references:

OECD/IEA, 2007: World Energy Outlook 2007 - China and India insights

OECD/IEA, 2007: Tackling investment challenges in power generation in IEA countries

OECD/IEA, 2006: China’s power sector reforms – Where to next?

OECD/IEA, 2005: Lessons from liberalised electricity markets

Planned publications (2008)

Electricity transmission investments in liberalised markets: trends, issues and best practices

Customer choice in electricity markets: Retail switching and demand response in competitive markets

Recommended