Women Managing the Farm

Conference-KansasBreakout Session 2

TRUSTS (Advanced)

Tim J. Larson, J.D., P.A.

7570 W. 21st St. N.

Building 1026, Suite C

Wichita, KS 67205

316-729-0100

Estate Planning for Farm Families - Business Succession Estate Planning – The Basics Everyone

Should Know

What is Estate Planning?

How does property pass after a death?

Will you be incapacitated or need assistance or long term care?

Will estate tax or some form of income tax affect your family?

What are the most common mistakes, goals and concerns clients face in Estate Planning? What solutions are available?

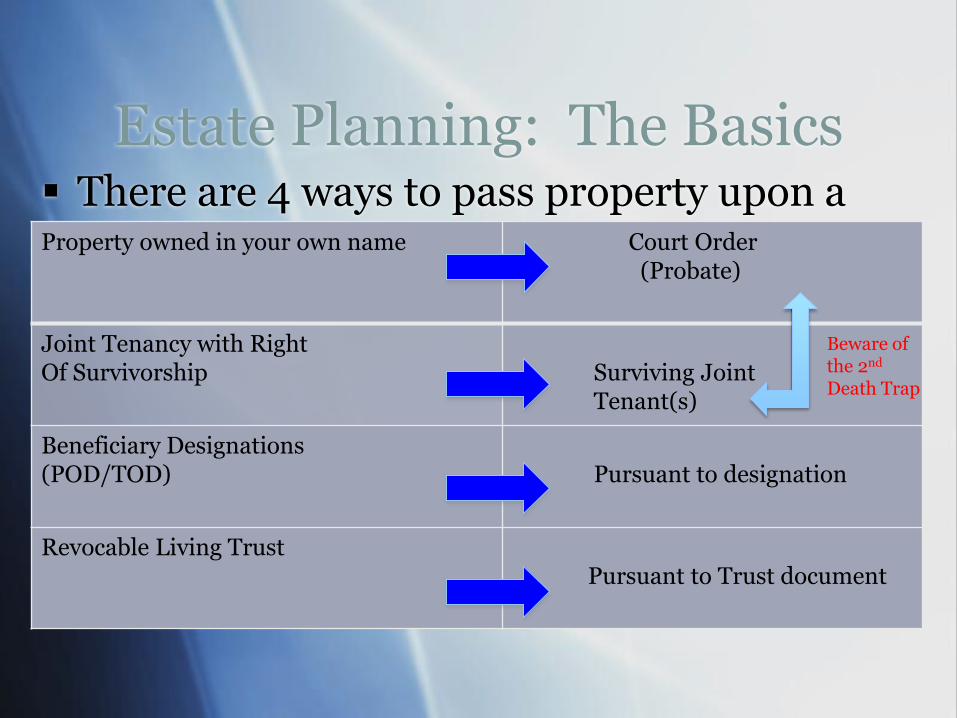

Estate Planning: The Basics There are 4 ways to pass property upon a

deathProperty owned in your own name Court Order (Probate)

Joint Tenancy with RightOf Survivorship Surviving Joint

Tenant(s)

Beneficiary Designations(POD/TOD) Pursuant to designation

Revocable Living TrustPursuant to Trust document

Beware of the 2nd

Death Trap

In order to understand the

present-

Let’s take a look at the past few years of

changing estate tax law, and the Tax Planning

Techniques and Strategies of the last 25

Years.

5

Federal Estate Tax Planning

Under The

Economic Growth and Tax Relief

Reconciliation Act of 2001

6

Sunset Provision (This would

become a big part of the “Fiscal

Cliff” in 2012SEC. 901. SUNSET OF

PROVISIONS OF ACT.

(a) IN GENERAL- All provisions of, and amendments made by, this Act shall not apply—

(1) to taxable, plan, or limitation years beginning after December 31, 2010, or

(2) in the case of title V, to estates of decedents dying, gifts made, or

generation skipping transfers, after December 31, 2010.

7

Federal Estate and Gift Tax

in 2002

A top tax.

An everything tax.

Estate tax exemption based on year of

death.

Annual gift tax exclusion of $11,000 (in

2002) per recipient per calendar year.

Rates range from 37% to 50% in 2002.

8

What Is Included in an Estate?

Real Estate

Personal Property

Stocks, Bonds, Mutual Funds

Bank Accounts

Retirement Accounts

Businesses

Life Insurance

Hint: Everything!

9

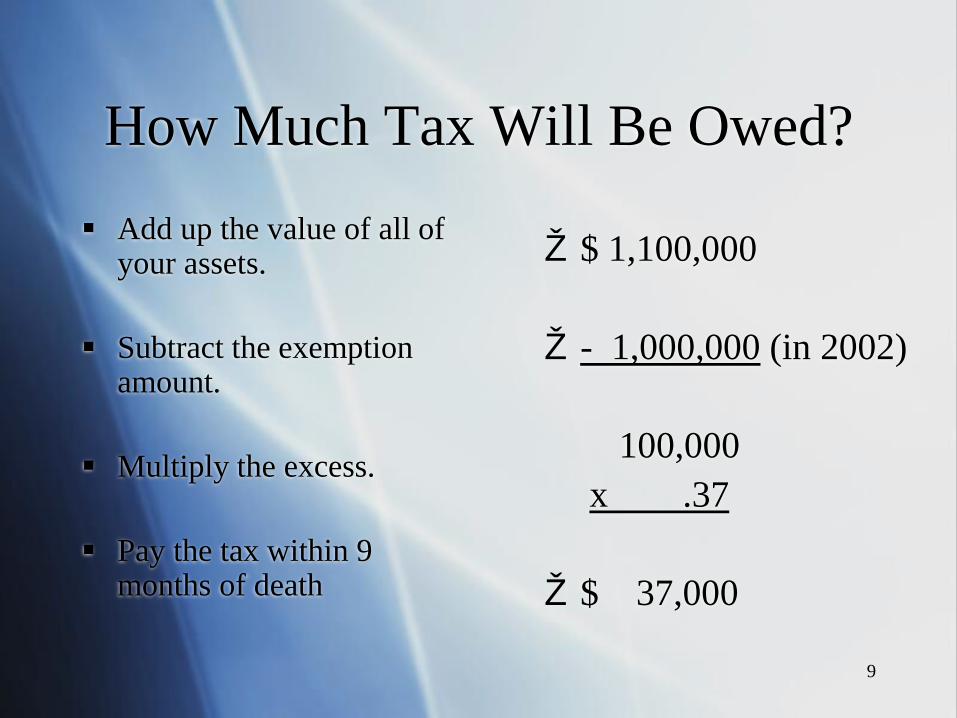

How Much Tax Will Be Owed?

Add up the value of all of your assets.

Subtract the exemption amount.

Multiply the excess.

Pay the tax within 9 months of death

Ž $ 1,100,000

Ž - 1,000,000 (in 2002)

100,000

x .37

Ž $ 37,000

10

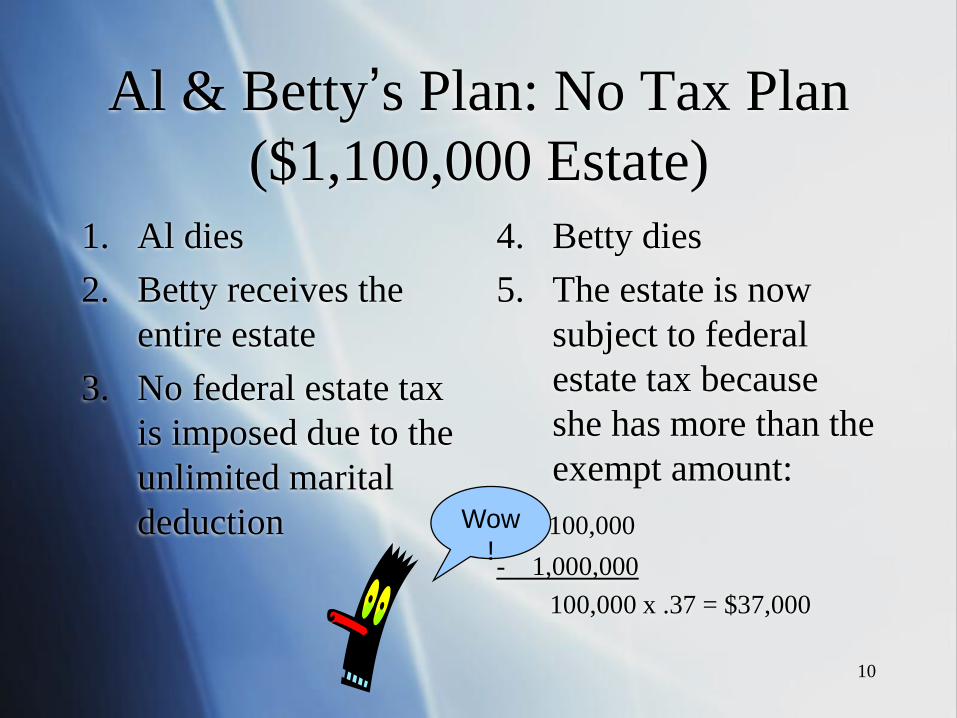

Al & Betty’s Plan: No Tax Plan

($1,100,000 Estate)

1. Al dies

2. Betty receives the

entire estate

3. No federal estate tax

is imposed due to the

unlimited marital

deduction

4. Betty dies

5. The estate is now

subject to federal

estate tax because

she has more than the

exempt amount:

$1,100,000

- 1,000,000

100,000 x .37 = $37,000

Wow

!

11

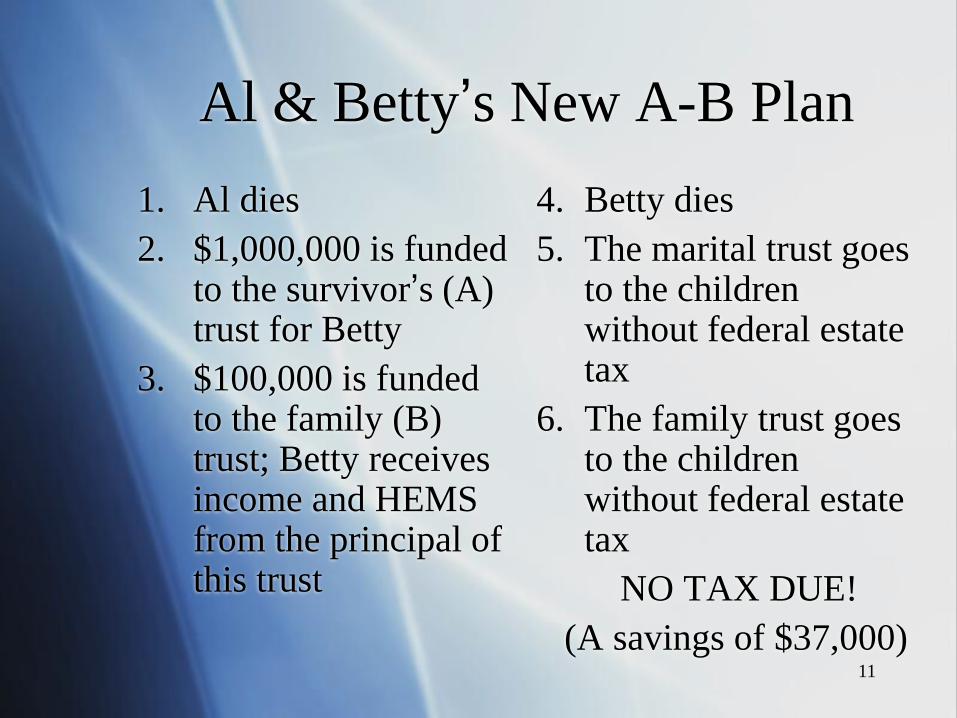

Al & Betty’s New A-B Plan

1. Al dies

2. $1,000,000 is funded to the survivor’s (A) trust for Betty

3. $100,000 is funded to the family (B) trust; Betty receives income and HEMS from the principal of this trust

4. Betty dies

5. The marital trust goes to the children without federal estate tax

6. The family trust goes to the children without federal estate tax

NO TAX DUE!

(A savings of $37,000)

12

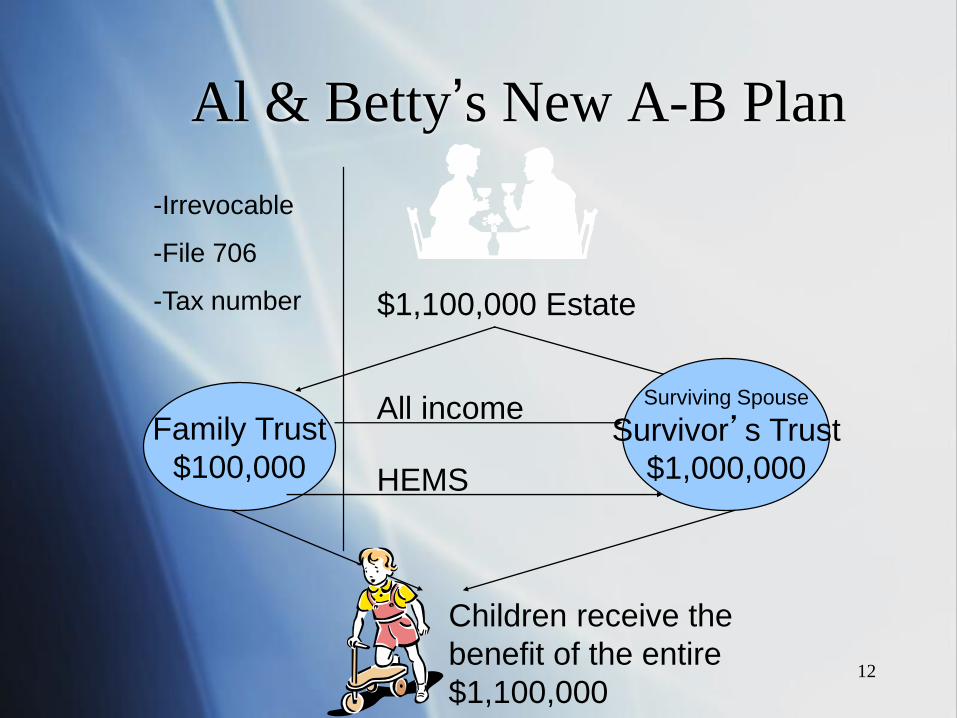

Al & Betty’s New A-B Plan

$1,100,000 Estate

Family Trust

$100,000

Surviving Spouse

Survivor’s Trust

$1,000,000

All income

HEMS

-Irrevocable

-File 706

-Tax number

Children receive the

benefit of the entire

$1,100,000

13

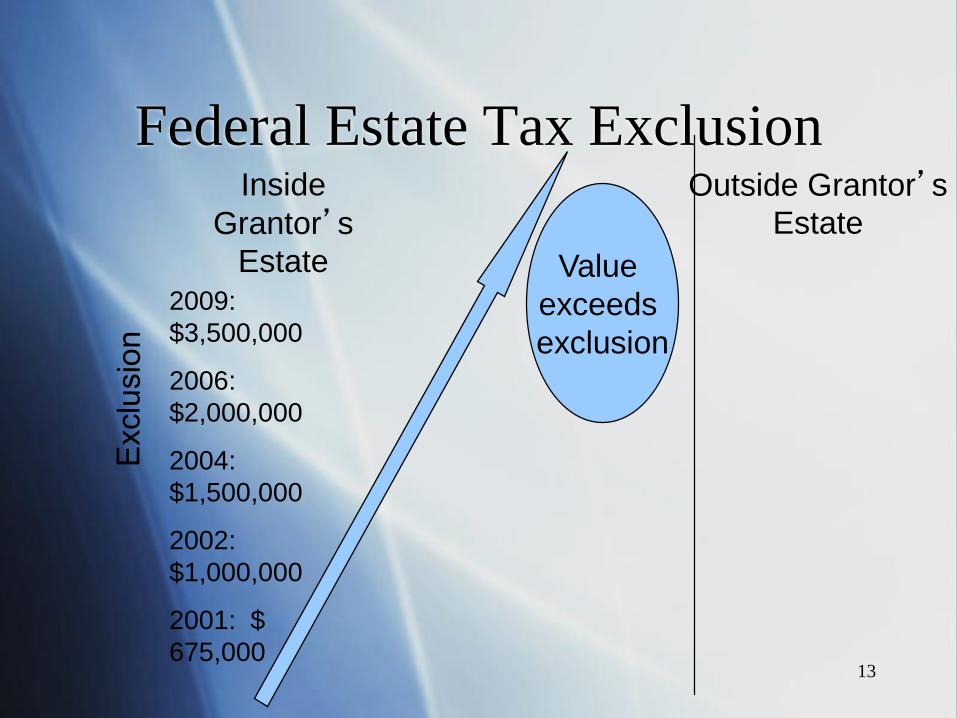

Federal Estate Tax ExclusionOutside Grantor’s

Estate

Inside

Grantor’s

Estate

2009:

$3,500,000

2006:

$2,000,000

2004:

$1,500,000

2002:

$1,000,000

2001: $

675,000

Value

exceeds

exclusion

14

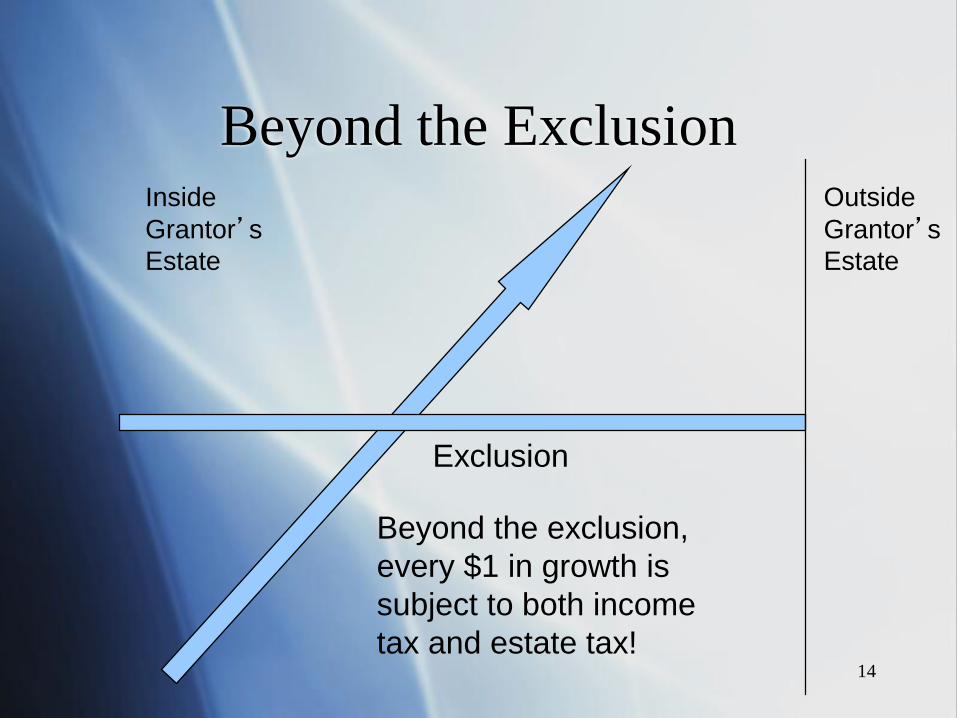

Beyond the Exclusion

Exclusion

Outside

Grantor’s

Estate

Inside

Grantor’s

Estate

Beyond the exclusion,

every $1 in growth is

subject to both income

tax and estate tax!

15

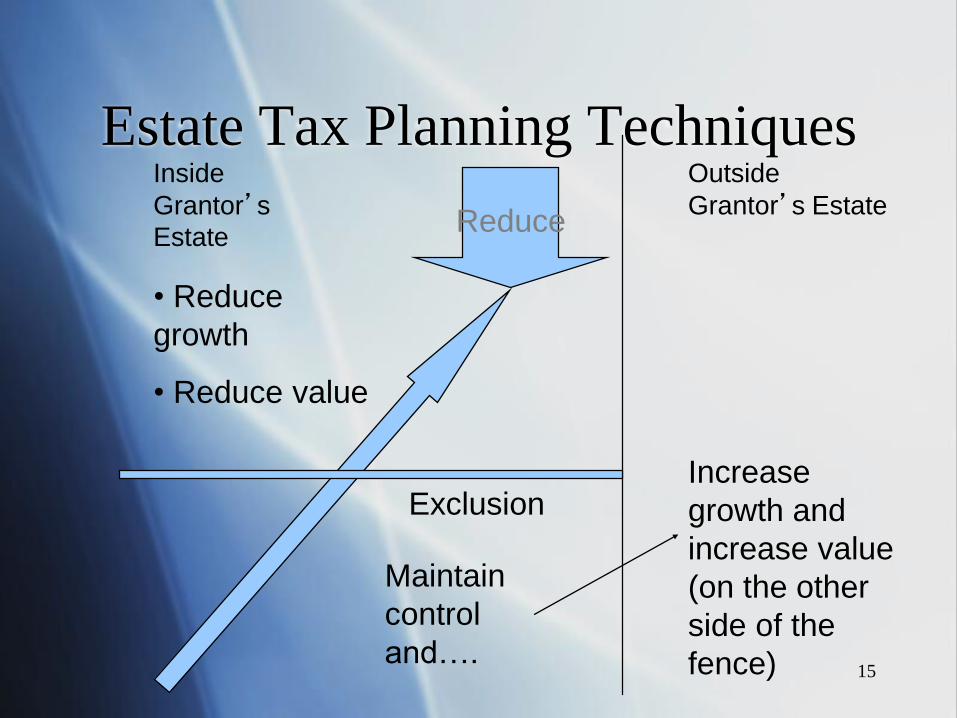

Estate Tax Planning TechniquesInside

Grantor’s

Estate

Outside

Grantor’s EstateReduce

• Reduce

growth

• Reduce value

Maintain

control

and….

Increase

growth and

increase value

(on the other

side of the

fence)

Exclusion

16

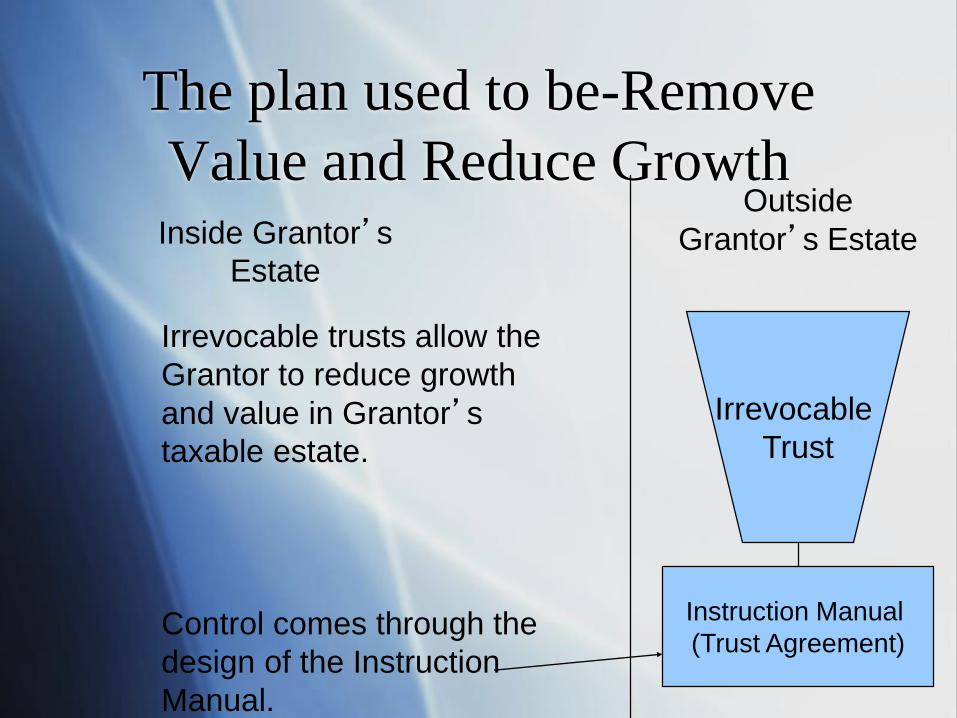

The plan used to be-Remove

Value and Reduce GrowthInside Grantor’s

Estate

Outside

Grantor’s Estate

Irrevocable

Trust

Irrevocable trusts allow the

Grantor to reduce growth

and value in Grantor’s

taxable estate.

Control comes through the

design of the Instruction

Manual.

Instruction Manual

(Trust Agreement)

The planning focus is no longer

on estate taxes for estates that are

less than $5,430,000 for an

individual

or

$10,680,000 for a married couple

This is because only 1% of the population is

affected by such a threshold.

What happened to all of the

estate TAX planning?

What happened at the top and the

bottom of the fiscal cliff at the end

of 2012? Was there a big “splat!”

What is the “rest of the

story?”

OR

As the end of 2012 approached, the fear was that

the Federal Gift and Estate tax exemption threshold

of $5,120,000 was going to go back (sunset) to a

$1,000,000 threshold at midnight, December 31st, 2012

as a result of the sunset provision in the federal law.

This was perceived by many as a one-time “use it or

lose it” opportunity to make gifts. People pondered

whether or not there would even be a “claw back” from

the estate tax at death if a person attempted to use the

gift tax exemption in 2012.

There was much discussion and in the end there was

much gifting.

Fiscal Cliff

The Estate Planning World Has Changed

Where are we now as a result of changes in

both Kansas and Federal law?

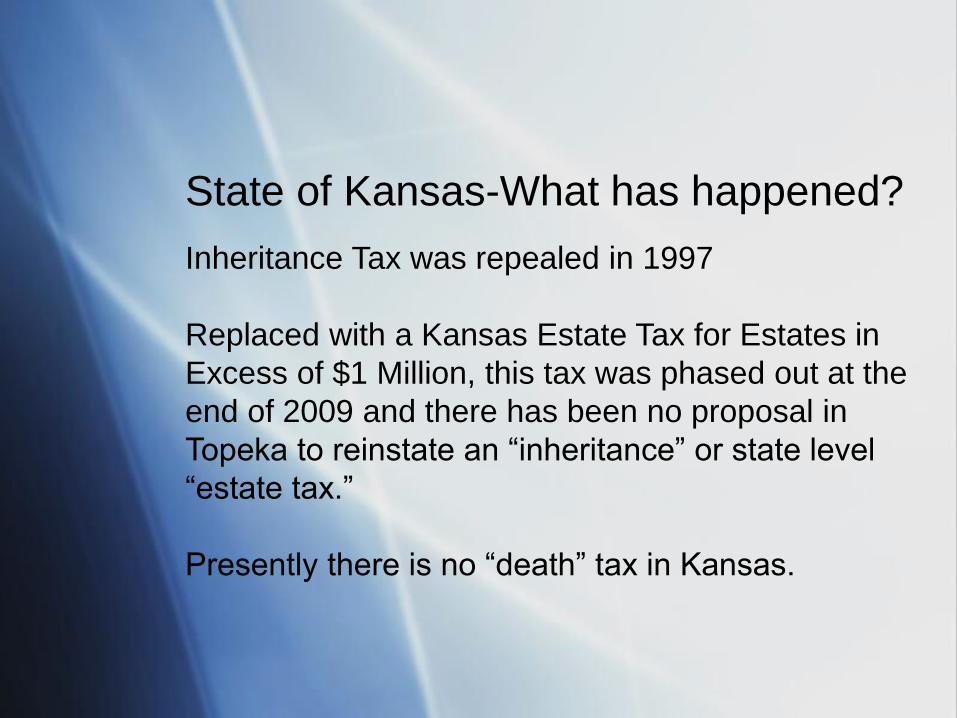

State of Kansas-What has happened?

Inheritance Tax was repealed in 1997

Replaced with a Kansas Estate Tax for Estates in

Excess of $1 Million, this tax was phased out at the

end of 2009 and there has been no proposal in

Topeka to reinstate an “inheritance” or state level

“estate tax.”

Presently there is no “death” tax in Kansas.

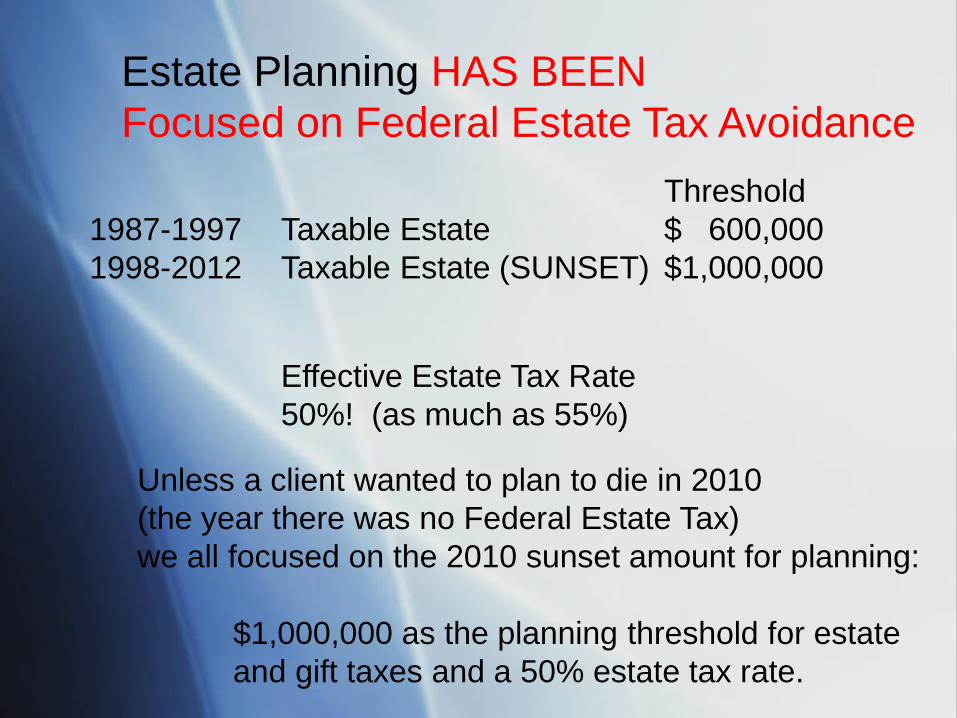

Threshold

1987-1997 Taxable Estate $ 600,000

1998-2012 Taxable Estate (SUNSET) $1,000,000

Effective Estate Tax Rate

50%! (as much as 55%)

Unless a client wanted to plan to die in 2010

(the year there was no Federal Estate Tax)

we all focused on the 2010 sunset amount for planning:

$1,000,000 as the planning threshold for estate

and gift taxes and a 50% estate tax rate.

Estate Planning HAS BEEN

Focused on Federal Estate Tax Avoidance

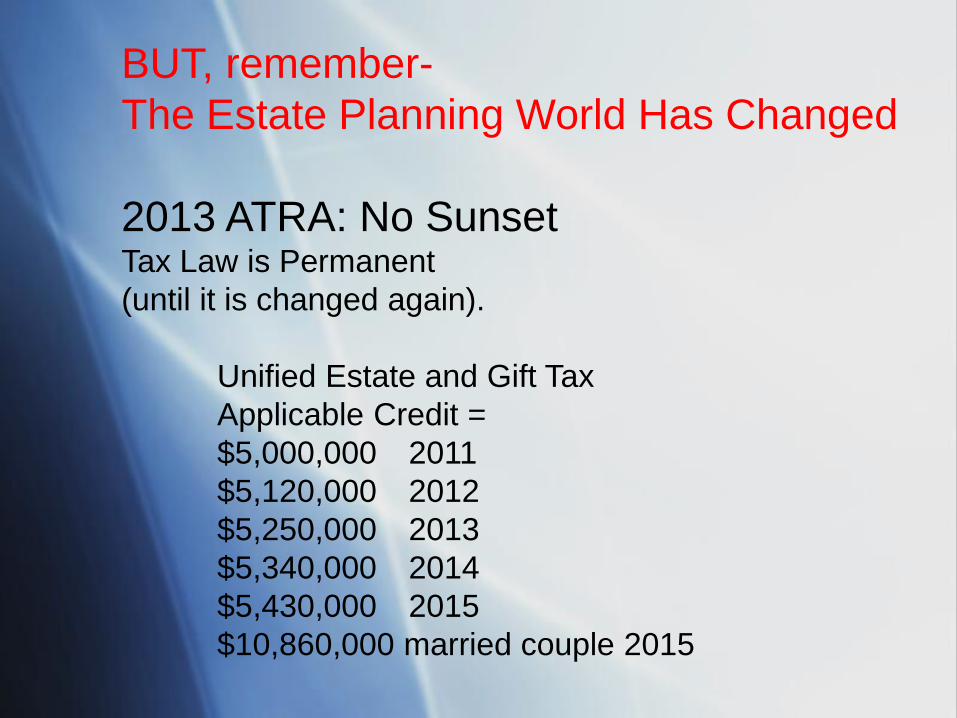

BUT, remember-

The Estate Planning World Has Changed

2013 ATRA: No SunsetTax Law is Permanent

(until it is changed again).

Unified Estate and Gift Tax

Applicable Credit =

$5,000,000 2011

$5,120,000 2012

$5,250,000 2013

$5,340,000 2014

$5,430,000 2015

$10,860,000 married couple 2015

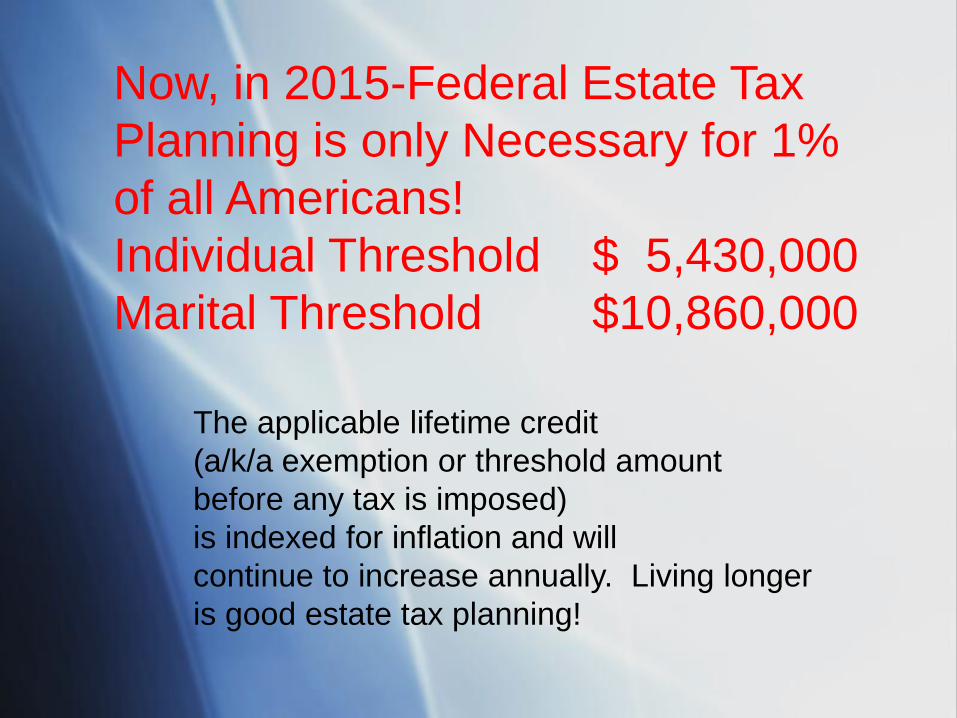

The applicable lifetime credit

(a/k/a exemption or threshold amount

before any tax is imposed)

is indexed for inflation and will

continue to increase annually. Living longer

is good estate tax planning!

Now, in 2015-Federal Estate Tax

Planning is only Necessary for 1%

of all Americans!

Individual Threshold $ 5,430,000

Marital Threshold $10,860,000

It is fair to say that the focus of those with

taxable estates from 1986 until the end of 2012

was on estate and gift taxes and avoiding those

taxes.

Where should we focus now, after ATRA?

After ATRA there will need to be more focus

on income tax issues in the planning because

of the fact that the primary concern for most

people will no longer be the estate tax.

Where has the focus been?

Estate Planning Focus on Estate Tax

What are the issues facing those that do not have estates

that will be subject to federal estate tax?

The non-tax issues have not changed.

• People are still going to focus on planning for retirement.

• People are still going to be faced with the possibility of

becoming incapacitated and/or having diminished

capacity.

• People will be concerned how to leave property for

spouses and descendants.

• People are still going to be faced with the inevitability

of death and what to do with their $’s and other stuff.

After ATRA-Estate Planning Focus on Income Tax

Again, what hasn’t changed on the estate planning side?

The need to plan for the possibility of aging, retirement,

incapacity, need for assistance, long-term care - both with

finances and documents, powers of attorney, living wills, and

other written plans and directions.

People will continue to have a need for growth of assets and

income.

People will continue to want to plan for children and

grandchildren no matter what the size of their estate is.

Clients want to Leave a Legacy. This has not changed.

They want to say “I love you.” Yet, they often want to assert some

Control. Incentive Planning can be negative or positive.

One option:

Negative Incentives for Beneficiaries who are not doing

what they should be doing:

•Refusing to work when they are able to do so

•Substance Abuse or other addictions

Reduce or stop distributions for certain situations on an attempt to

provide an incentive that is negative:

“I may not be able to make you do what I want you

to do, but I can make you wish you had.”

W.E. (Wally) Larson

Clients want to leave a Legacy. This has not changed.

Positive incentives for Beneficiaries

Increase distributions provide for bonus in certain events:

• Provide funds for education, maybe require being full

time student, maintain a certain grade point average,

to pursue a specific type of training or degree.

• Distribution of lump sum upon graduation or at age 30

(incentive to get education)

• Dollar for dollar earned income match up to a certain

income level.

(incentive to be a productive person)

• Family Bank concept (make loans for various

purposes to beneficiaries and increase availability

of funds for successes)

• Incentives for Charitable Giving by matching charitable

giving up to a certain level.

• Provide for opportunities. Incentive-Trustee directed to take into

consideration how previous distributions have been dealt with by

beneficiary.

Step-Up in Basis to fair market value at death

did not change!

General Rule:

Basis of property in the hands of person acquiring

property from decedent … is the fair market value at

the date of decedent’s death.

(Although referred to as the “step-up” rule, there

can also be a step-down in basis.)

What income tax matters did not change with ATRA?

Results of ATRA:

Prior to ATRA most planners would have agreed that

it made sense to obtain valuation adjustments and make

lifetime gifts for those with potentially

taxable estates, because passing basis and having imbedded

capital gain in property transferred during life without a

step-up in basis was considered better than paying estate tax

but getting a step-up in basis.

Now, with the greater exemption (applicable credit) amount

locked in and indexed to inflation, and with the threshold for

an estate tax liability Increasing significantly before the

possibility of tax being owed at 40% continues to grow

annually, holding assets until death to get a step-up in basis

may be the better tax avoidance plan.

Now, there is an even greater need to look at the

nature of the assets in a client’s estate to determine

income tax issues, such as those relating to basis.

Assets that have a low basis and that are likely

to be sold by the next generation are the most

significant for which to contemplate ways to

get a step-up in basis.

Prior to ATRA it was considered good planning to move

assets to a younger generation and have growth occur

in the estate of the younger generation.

Now, if capital gains tax rates go up and an individual is

faced with a significant state income tax, these types of

gifts come with a lot of risk.

One option may be to transfer assets to a trust that

includes provisions allowing the Trustee to force estate

tax inclusion (thus obtaining a step-up in basis) but at the

same time protecting assets from creditors and predators.

Irrevocable Life Insurance Trusts are still attractive to

provide an offset for possible taxes (income tax or estate

tax) particularly with the use of the annual exclusion for

funding.

Traditional Planning prior to ATRA

For a married couple:

A/B Trust Planning was primarily done by creating a

Separate trust for each spouse. (Although it can be

done with a joint trust.)

There are many variations, but the significant intent

of planning in the manner was to make sure that

exemption (applicable credit) for estate taxes was not

wasted at the death of the first spouse to die.

Typically, the result was to create a trust to hold assets

outside of the estate of the surviving spouse but for the

benefit of the surviving spouse.

Common names:

Credit Shelter Trust, Bypass Trust, Family Trust, A/B

Traditional Planning prior to ATRA

Example-Farm Family with Land

It was not unusual to have half the value of the farm

ground in the Credit Shelter or Family Trust.

What has happened in the last ten years with land

values in Kansas? Values have increased significantly.

Result:

We now have Credit Shelter or Family Trusts that have

land with low basis compared to fair market value that

will not step-up in basis at the death of the second

spouse to die.

Deceased Spouse Unused

Exemption otherwise known as

DSUENo longer a primary planning

objective to make sure that estate tax

exemption is fully used at the first

death for a married couple!

Portability

for

Present Estate Tax Law For deaths in 2014 the Estate Tax Exemption was

$5,340,000

For 2015, the current estate tax exemption is $5,430,000.

Presently the exemption amount is indexed for inflation.

Top tax rate is 40% on the excess.

It is estimated that in 2013 when the law was made

permanent in its present form, only 3800 estates would

need to file returns at present levels, or less than 1% of all

decedent’s estates in the United States.

Estate and Gift Taxes no longer a

Common Problem

99 % of all Americans will not

have an estate or gift tax concern

after ATRA’s enactment!

Deceased Spouse Unused

Exemption

TRA ’12 permanently enacted from TRA ’10 the

provisions that provide a surviving spouse will be

able to use the unused exemption of a

predeceased spouse who died after December 31,

2010 for both gift and estate tax purposes. This is

commonly referred to as “portability.”

Using Portability to obtain

“Step-Up” in Basis “The use of a predeceased spouse’s unused exemption is

not a planning technique. It would normally only be

employed by a surviving spouse due to desirable planning

not being utilized in the predeceased spouse’s estate. This

would include funding a Family Trust for the benefit of the

surviving spouse with the predeceased spouse’s unused

exemption amount.”

This statement was published and presented a little over

one year ago in a program outlining the current status of

the law. It is typical of the belief all planners have had for

over 25 years that a primary goal of good planning was to

make sure that exemption (applicable credit) was not

wasted at the death of the first spouse to die.

Times have changed.

Using Portability to obtain

“Step-Up” in Basis

It has been hard to accept that planning to utilize DSUE

does affect planning and should be a part of many new

plans because it is an option to make sure the ability to

obtain a step-up in basis is not lost!

It has very much become an “estate planning technique!”

Portability and the DSUE

The “All-American Estate Plan for decades has

been the following: “Leave it all to the surviving

spouse.”

With a lower estate tax threshold, the “leave it all

to the surviving spouse” plan was seen as a

“waste” of exemption that was undesirable for any

couple with a marital estate in excess of $600,000

or $1,000,000.

The tax bill would be due within nine months of

the second death!

Portability and the DSUE

Under this type of plan, the unlimited marital deduction

was perceived as a trap for the unwary individual and it

resulted in a trap for imposing estate tax when the

surviving spouse died and the “wasting” of the exemption

could not be undone.

(Remember a tax of 50% was imposed on the first dollar in

excess of $1,000,000!)

Portability and DSUE

Congress, as often seems to be the case, took action to

protect those who found themselves the victim of this tax

trap about 15 years too late because under current law far

fewer estates feel the estate tax impact.

Congress’ Solution: the 2010 Tax Act. (2-year patch)

Provided for Portability of Unused Exemption beginning

in 2011.

Portability and DSUE What are the Requirement for the DSUE

Married Couples or widowed

Singles are not impacted

Mechanics of DSUE

Must be married at time of death

Both spouses are US citizens

Death after Jan 1, 2011

DSUE allocation is made to surviving Spouse

Timely filed election is made on the estate tax return

Portability and DSUE

Proceed with caution if there are multiple deceased

spouses – the last deceased spouse’s DSUE eliminates any

DSUE from a prior deceased spouse.

However, for fun, contemplate the “black widow” estate

plan through the use of gifting by the wealthy “black

widow”: Spouse “dies” and “black widow” obtains

DSUE, uses gift exemption to the fullest, then surviving

spouse remarries next non-propertied spouse down the hall

at the nursing home, repeat as many times as possible.

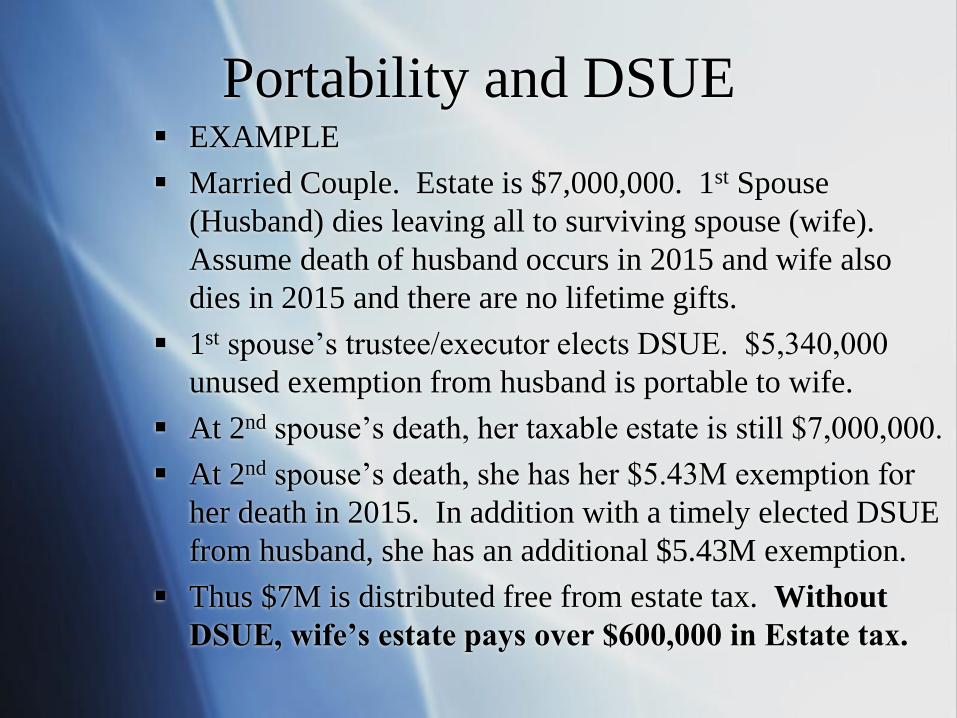

Portability and DSUE EXAMPLE

Married Couple. Estate is $7,000,000. 1st Spouse

(Husband) dies leaving all to surviving spouse (wife).

Assume death of husband occurs in 2015 and wife also

dies in 2015 and there are no lifetime gifts.

1st spouse’s trustee/executor elects DSUE. $5,340,000

unused exemption from husband is portable to wife.

At 2nd spouse’s death, her taxable estate is still $7,000,000.

At 2nd spouse’s death, she has her $5.43M exemption for

her death in 2015. In addition with a timely elected DSUE

from husband, she has an additional $5.43M exemption.

Thus $7M is distributed free from estate tax. Without

DSUE, wife’s estate pays over $600,000 in Estate tax.

Portability and DSUE• Filing the 706 timely to Elect DSUE

• For Non-taxable Estates:• Property qualified for marital deduction of charitable deduction

is subject to special valuation rules – For a good laugh, See Next Slide for language from Form 706 for special valuation rules.

• Property should still be listed on appropriate schedules.

• Only in limited types of items is a valuation needed

• For the vast majority of assets, a good faith estimate is made.

• Essentially value is made by good faith estimate and then rounded to the nearest $250,000 to determine DSUE.

Portability and DSUE

This is the language on each schedule of the

706 return. If the value of the gross estate, together with the amount of

adjusted taxable gifts, is less than the basic exclusion

amount and the Form 706 is being filed solely to elect

portability of the DSUE amount, consideration should be

given as to whether you are required to report the value of

assets eligible for the marital or charitable deduction on

this schedule. See the instructions and Reg. section

20.2010-2T (a)(7)(ii) for more information. If you are not

required to report the value of an asset, identify the

property but make no entries in the last four columns.

Portability and DSUE As a side note, when was the last time the IRS specifically

instructed a taxpayer to use their best judgment and that

there is no need to provide values for entries on the return?

And then the IRS makes a specific instruction to the

taxpayer that after they have used their best judgment and

skill in determining values that the IRS doesn’t need to

know about, the taxpayer is then to round those values to

the nearest $250,000 to determine remaining credit for a

return?!?

(see pages 16-17 of Instructions for Form 706 for more “best

guesstimate” language and the $250,000 rounding table)

Portability and DSUE

Back to a more serious note, when and

where should we utilize Portability and the

DSUE?

DSUE is not always a perfect solution.

Bypass Planning should still be used in many

cases

Creditor Protection

Predator Protection

Future appreciation of assets concerns

DSUE is not indexed and doesn’t apply to GST

exemption

Portability and DSUE

Considerations of when to elect portability?

What is the liability for failure to elect? Advisor/Executor may have exposure if tax occurs at

survivors death when it might not have otherwise done

so with timely election.

Cost considerations on non-taxable estates.

What if Congress reduces the exemption amount and

advisor/executor failed to timely elect?

Decision to use Bypass planning which results in no

step-up in basis at second death v. no Bypass planning

but 2nd death step-up.

Start with the end in mind-or-Where are you going?

What are your goals?

What are your concerns?

What do you want the picture to look like?

Who should be involved in the decision making?

Family Business Succession What is Estate Planning in the realm of

Family Business Succession?

Think of the family business (farm) as a team bus going down the road.

Where is the bus going?

What is the plan? You have to know where you are going in order to properly plan how to get there. What direction are you going and is it the right direction? Ultimately, there is more than one route that can be taken to get to the same destination. Who decides which route? What does the destination look like? Are there people on the bus that think the bus is going to a different destination?

Family Business Succession Who is driving the bus?

Should the current driver really be behind the wheel? Who decides where the bus is going? Who is at the helm making decisions? Why are we doing this plan? Who are those affected? Who is most affected? Does somebody else really want to be driving? Do you know when it is a good time to not drive and be a passenger?

Family Business Succession

Who is on the bus?

Why is this group together on the bus? Is there a sense of unity? Does anyone need to be included who has not been included? Is there anyone on the bus who doesn’t want to make the trip or would like a different destination? Are there people on the bus that don’t or won’t talk to each other?

Family Business Succession Client Goals and Concerns

Each family member is likely to have different Concerns and Goals.

Typically, it is good to have appropriate leadership in place prior to the passing of the Patriarch or Matriarch. One of the biggest mistakes in planning for business succession is simply waiting until there is a death to make a change.

Family Business Succession

Plan ahead for an orderly process and

transition, or stop when a key person dies

and attempt to reorganize.

Changing drivers while going down the

road is not a good plan.

It is your choice.

Family Business Succession

Think of having to change drivers on the bus while going down the road. There is likely to be a messy accident. People will be hurt and injuries suffered that may not heal. The bus may be wrecked so bad that we can’t get it back on the road, or the time and expense involved will drastically affect what it looks like when it does.

Mistakes Failing to plan for the possibilities

Illness

Incapacity

Long Term Care

(not just for the Patriarch or Matriarch that has driven the bus for many years, but for all of the players)

Mistakes Not communicating and transferring values.

Has the vision of one generation been shared with the next generation?

Has the older generation asked the younger generation what their vision is?

Getting the Priorities Right Start with the end in mind.

Get all the right people on the bus in the right seats.

Determine who should be involved in a discussion of where the destination should be.

Plan for the trip and plan for all aspects, including contingencies.

Know where you are headed and how you are going to get there.

Getting the Priorities Right

Know and consider the possible travel detours and problems that might prevent you from getting to your destination.

Don’t even turn the key and start the engine without having the plan in place and the GPS programmed.

Now Back to Basics Goal #1 – Probate Avoidance

Avoid, Minimize, or Reduce the loss of control and waste of time and expense associated with Probate. Ensure the largest amount of assets possible goes to the beneficiaries instead of other parties.

Solutions

Proper Titling of Assets

Coordination of Beneficiary Designations

Use of Trust planning to handle the administration

Utilizing the Will as a “spare-tire” or “back-up” plan for administration

Estate Planning: The Basics Goal # 2 – Capital Gains and other Income

Tax Issues (unless you are in the 1% that has a federally taxable estate)

What capital gains issues are there?

How are you operating and what entities are involved?

There are issues for succession if you have an LLC, Corporation, or Limited Partnership, for example.

Estate Planning: The Basics

Goal #3 - Family Harmony Concerns

How to prevent beneficiaries from fighting among themselves and having large attorney’s fees as a result.

Using Trust Planning typically provides a more difficult avenue to litigation

Selecting the correct Executor(s) or Trustee(s)

Openly discussing family concerns with estate planning attorney

No-contest clauses in planning documents-what can be prevented?

Beneficiaries need to receive good advice from their advisors

Estate Planning: The Basics

Goal #4 - Reduce Creditor Concerns for the Grantor

Solutions –

A revocable trust does not provide any additional creditor protection to the Grantor (s)

Use of Entity Planning (FLP, LLC, Irrevocable Trusts)

Farm Families can benefit greatly from asset protection strategies

Asset protection needs to be done at a time when everything is seemingly fine.

Estate Planning: The Basics Goal#5 – Protect Beneficiaries from

Creditors or Predators

Solutions

Open and frank discussion with estate planning attorney about your concerns regarding your beneficiaries issues with:

Troubled Marriages/Divorces

Bankruptcy

Lawsuits & Judgments

Special Needs

Poor Money Management/Substance Abuse Problems

Spendthrift Clauses in Trust Documents provide tremendous asset protect to beneficiaries

Estate Planning: The Basics

Goal #6 – Preserve or create a Family Legacy

Problem: Ensuring assets are managed in accordance with your wishes and that your success preserves a legacy for heirs.

Solutions

Incentive Clauses to prevent “Trust-Funders”

IRA Trusts with RMD requirements

For farming families, plans to keep land in family

Plan for succession of privately owned, family business

Plan for those who will be involved and those who will not be involved

Business Succession Planning We believe that the greatest mistake in

planning for those with family businesses is to do little but be the boss and then die. It is estimated that over 80% of the businesses

in the U.S. are private or family dominated

70% don’t make it to the 2nd generation

85% don’t make it to the 3rd generation

Average business lasts 24 years

The difference is in having a good plan, which involves including the key people necessary to make the transition from one generation to the next.

Recommended