1

Renata Navikaitė

Head of Regulatory Services Division

Klaipėda LNG Terminal: Gateway to the Baltic Sea Gas Market

Photo A. Kubaitis

February 18, 2016, Klaipėda

2

Overview of Klaipėdos nafta and Klaipėda LNG terminal

KN as a diversified oil product and LNG terminal operator

40+ years of oil product terminal

operations

Successful fast track LNG

terminal project implementation

LNG reloading and bunkering

station project LNG bunkering vessel project

State fuel reserves

LNG terminal consulting projects

3

Overview of the Klaipėda LNG terminal

Successful operations after commissioning in autumn

FSRU Independence

Arrived on the 27th of October

2014

Commissioning cargo

Delivered 28th of October

2014

Commercial operations

First commercial send-out from 1st

of January 2015

First commercial cargo

Delivered 23rd of December

2014

4

5 Deck of FSRU Independence

Regasification unit

6

Naujausios nuotraukos iš statybų aikštelės

Construction of the jetty

High pressure gas platform Service platform

7

Naujausios nuotraukos iš statybų aikštelės Gas transmission

system Gas metering station

and control center

8

Overview of Klaipėdos nafta and Klaipėda LNG terminal

Key achievements

LNG terminal

launched

on time

Minimal

impact on the

environment

Security of

energy supply

Savings of

30 mln.

EUR

Professional

project team

Positive

public opinion

Prompt implementation

Financing by

EIB, NIB

Business

model

approved by

EU

Managed

international

public

tenders

Lithuania fulfills

N-1 standard

Positive

evaluation of 12 audits

European

Commission support

9

Commercial Operations of the Klaipėda LNG Terminal

Services of the Terminal

LNG reloading LNG regasification

Services

Start from the 1st of January, 2015.

New opportunities in 2016-2017

LNG bunkering and truck

reloading

LNG reloading station

• Minimal send out ensures constant operational availability

• All services are on a transparent third party access basis

• LNG cargo break-bulking

possibilities

LNG regasification tariff – 0,10

EUR/MWh

LNG reloading tariff – 1,14

EUR/MWh

• Capacities allocated before and during the Gas Year (October – October)

10

Commercial Operations of the Klaipėda LNG Terminal

Terminal Business Model

Unused

capacity

Third Party Access

infrastructure

Terminal User

Unused

capacity

-

2.000.000

4.000.000

6.000.000

8.000.000

10.000.000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Terminal User

Terminal User

Terminal User

Terminal capacities are available via open booking procedure

(nm3/day)

• Currently 3 Terminal users

• Reserved capacities for Gas Year 2016 – 1.1 bln. nm3

• Terminal utilisation rate – 29%

Capacity available for traders

Average daily send-out

New gas year

11

LNG regasification/ pipe markets

Baltic-connector

GIPL

LNG ship reloading markets LNG trucking markets

Markets accessible starting the 1st of January, 2015

Markets accessible after regional interconnections are finished

Markets accessible after on-shore LNG reloading station is finished

Small & Mid-scale LNG terminals

(5.000-50.000m3; operational and under development)

Access to new Baltic Sea markets

12

Access to natural gas markets in the Baltic sea region

• Klaipeda LNGT provides access to well interconnected natural gas

market of the Baltic States, including the Incukalns underground gas

storage facility

• Finish market is accessible after the completion of Baltic Connector

pipeline

• Polish market is accessible after the completion of GIPL pipeline

• Access to Ukrainian market is available once the transit is agreed

UKRAINE

GIPL

15

BCM/yr

LATVIA

POLAND

BELARUS

2.3

BCM/yr

FINLAND

Klaipeda LNG

terminal

LITHUANIA

Incukalns gas

storage

1.3

BCM/yr

0.6

BCM/yr

ESTONIA

Baltic-connector

to Finland

42.5

BCM/yr

3.7

BCM/yr

Third Party Access infrastructure

GIPL (Gas interconnection Poland Lithuania) and BalticConnector pipeline

Possible gas flows from Klaipeda LNG terminal

Natural Gas Consumption

13

Gävle project

Expected start-up: 2018

Nynäshamn project

Operational from: 2011

Gothenburg project

Expected start-up: 2017

Tallinn-Muuga project

Expected start-up: 2017

Tallinn-Muuga project

Expected start-up: 2017

Haminan project

Expected start-up: 2017-

2018

Rauma project

Expected start-up: 2017-

2018

Pori project

Expected start-up: 2016

Manga project

Expected start-up: 2017-

2018

Regional hub in Klaipėda

Reload hub for the Baltic Sea region

14

LNG reloading station in the port of Klaipėda

KN oil terminal

LNG supply route FSRU

LNG Reloading station

LNG Supply Route

LNG unloading

FSRU Independence

LNG LNG

LNG LNG

LNG reloading service LNG transportation

LNG reloading into LNG trailers

Integrated service LNG Reloading station

Flexible hose LNG dispenser

LNG trailer C-type containers

15

Thank you for your attention.

16

0

5

10

15

20

25

30

35

40

45

50

1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7

2013 2014 2015

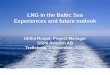

Klaipeda LNGT in the Regional Gas Market

Security of Gas Supply- Price

FI

(28.67)

LT

(36.73) 18.25

Prices EUR, MWh (2014)

No data

< 21.00

21.00 – 25.00

25.01 – 29.00

> 29.00

TOP 5 end 2014

Price level

1. Lithuania

2. Estonia

3. Latvia

4. Greece

5. Slovenia

Comparison of EU wholesale gas prices (2014 Q4) vs July 2015

Source: DG Energy, GetBaltic, Latvijas Gaze, Elering

LV

(30.31) 21.21

EE

(33.29) 21.81

GR

(29.80)

SL

(29.25)

PL

(26.20)

Historical gas prices, 2013-2015

• World trend – gas prices are going down due to:

• Oil price crisis;

• Mild winters in the recent years;

• New sources of LNG – shale gas;

• Decreased demand in Asia as a result of

energy balance diversification.

• Regardless, dependency on a single gas supplier

translated to the highest price in the EU until the

end of 2014.

Lithuania RU-DE boarder

HH (USA)

Japan

EU avg import price

Eur/ MWh

17

20

22

24

26

28

30

32

34

36

38

2012 2013 2014 2015 H1

EU average RU-DE boarder Regional average Lithuania NBP+3.5

Average annual natural gas import price EUR/ MWh

Klaipėda LNG

Terminal is in

Operation

(LT, LV, EE, FI)

LNG price sets

natural gas price cap

2. Global Natural Gas Prices

A Cap for Natural Gas Prices in the Region

Sources: NCC,GetBaltic, Latvijas Gaze, Elering, Energiavirasto, The ICE, Indexmundi, ycharts, x-rates.com

Monthly prices are averaged to get the annual average price; Respective month exchange rates are used for currency conversions where needed; Reference for the last 3 months of 2015 H1 price in Lithuania is the GetBaltic fulfilled transaction

weighted average price for transactions carried out within a month; 3.5 EUR/MWh are added to the NBP price to represent LNG shipping, supplier margin and any other additional costs; 10.4 MWh/1000 nm3 natural gas for conversions where

needed.

Recommended