Transfer Prices: A Financial Perspective

Nilufer UsmenDepartment of Economics and Finance, Montclair State University, Montclair, NJ, 04043e-mail: [email protected]

Abstract

The arguments for and against transfer pricing schemes so far have focused on profit-seeking approaches based on tax differentials, or on evasion of government enforcedgoods and fund flow restrictions. This article shifts to a value-seeking framework wheretransfer prices act as strategic tools that may enhance value for the multinational witha foreign affiliate by exploiting financial and/or tax arbitrage that also lead to owner-ship arbitrage. The results show that there is an optimal level of transfer price depend-ing on the specific exchange rate distribution when the cost structure allows for apenalty for overcharging. Moreover, this article introduces a new form of tax arbitragebenefit of transfer prices that is based on present value of tax shields.

1. Introduction

Within a multinational firm, it is not uncommon to transfer goods,

services and loanable funds between the parent and an affiliate or

between any two of its alliances. The transfer prices1 attached to these

flows can be adjusted by the parent following certain methods that are

supervised by the tax jurisdictions and other government authorities

where the companies are incorporated. It is well documented that due

to tax differences, import duties, quotas imposed by host countries

and/or exchange restrictions or restrictions on ownership, it may be in

the best interest of profit maximization to assign a higher/lower price

to the transferred goods, services or funds than arm’s length.2 In prac-

tice, multinationals do have the schemes in place to charge prices that

are legitimate and that can be substantiated but also that may vary

from their true values. The degree of arbitrariness in setting transfer

prices depends on whether these products or services are traded in the

open market. Even with traded products and services, it is possible to

vary the transfer price by using different credit terms. Therefore, we

may assume that the MNCs have considerable leeway to adjust the

level of transfer prices charged to their affiliates.

The arguments for and against transfer price schemes thus far

have focused on profit maximization within regulations imposed by

government authorities. The analyses have shown how to regulate

Journal of International Financial Management & Accounting 23:1 2012

© 2012 Blackwell Publishing Ltd., 9600 Garsington Road, Oxford OX4 2DQ, UK and 350 Main Street, Malden, MA 02148, USA.

transfer prices to increase after-tax profits for the parent company

in the presence of differential taxes, import duties, partial ownership,

deferred repatriation of income and different dividend pay-out ratios.

In these past analyses, the uncertainty about exchange rates has

been often overlooked notwithstanding the fact that most transfer

pricing situations involve cross-border cash flows. Moreover, there

has been a decline in the interest for doing research in this area in

financial economics even though the role played by transfer prices

has become more significant as a result of globalization of busi-

nesses and corresponding increase in intra-firm trade and fund flows

across borders.3

This article will explore the role played by transfer prices in

multinational financial decision making within an intertemporal value-

seeking framework, in the sense that input decisions are made now

while the revenues occur in the future. In this framework, the future

uncertain revenues will further be impacted by exchange rate volatility.

To my best knowledge, this article will be the first in transfer pricing

literature to account for both cash flow and exchange rate uncertain-

ties and their interactions simultaneously. It will view transfer prices

as a scheme that can create or destroy value for the firm as it shifts

revenues within the network of alliances and the parent.

There are four features of the model developed in this study. One is

market segmentation that leads to financial arbitrage, the second is the

covariance between exchange rates and foreign currency cash flows

and the third is the tax differential that leads to tax arbitrage. The

fourth is the transfer price/cost structure that allows for transfer price

to differ from cost but also limits the deviation by a penalty brought

by government authorities. These four features, one by one or jointly

affect the incentives to set the transfer price that will enhance the value

of the multinational parent.

Specifically, in the present analysis, transfer prices will be presented

as a strategic tool that can be used to exploit the benefits of financial

and tax arbitrage which lead together to ownership arbitrage to

increase the value of a multinational. Financial arbitrage is prevalent

in a world where capital markets are effectively segmented due to

direct and indirect investment barriers, as evidenced in previous

research.4 It is documented that direct barriers, such as taxes or

restrictions on foreign ownership of domestic securities, as well as

indirect barriers, such as differences in information, accounting state-

ments, investor preferences or political risk, result in segmentation of

2 Nilufer Usmen

© 2012 Blackwell Publishing Ltd.

international capital markets. The asset-valuation implication of seg-

mented markets is that each market assigns a different premium to

the same risk leading to different valuations of the same cash flows

in two markets. If the markets were integrated, assets with equal risk

located in different countries would yield the same expected returns

in a common currency. This article will also note that although finan-

cial arbitrage, a product of market segmentation, is partially caused

by tax differences, tax differences are not the only reason to have dif-

ferent valuations in different countries. This article, hence, will pres-

ent a base case where taxes are assumed away but value differentials

and financial arbitrage opportunities are still possible due to other

barriers in international capital markets. The impact of tax differences

on value will be introduced later and termed as tax arbitrage.

Whether the value gain is due to financial or tax arbitrage or both,

there will be a resulting ownership arbitrage as to who should own

the subsidiary.

This article begins with a definition of financial arbitrage (owner-

ship arbitrage) in international capital markets in a state-preference

framework, and under risk neutrality. This hinges on the covariance

between foreign cash flows and exchange rates. The next section will

show that although the above definition of segmented capital markets

requires that different risk premiums be attached to the same risk; a

finer description of segmentation and financial arbitrage reveals that

the same cash flows can still have different valuations under risk neu-

trality due to the covariance term. Based on this definition, the differ-

ential value of a foreign affiliate to a parent financed by equity is

derived. This is the value difference of the foreign affiliate’s cash flows

between the foreign and domestic capital markets that are partially

segmented. In this value differential equation, transfer prices become a

decision variable that determines the value gain to the parent. Hence,

the multinational should set the total transfer prices charged to its

affiliate as to increase this value differential whenever positive. This

article proceeds to introduce differential taxes for the countries that

host the parent and the affiliate. The impact of the tax differences on

differential values and the interactions between the two sources of

arbitrage opportunities, namely financial and tax arbitrage are

explored.

The model uses a cost structure where profits from intra-firm trade

and fund flows resulting from setting transfer prices above production

cost are allowed, but there is also a penalty for unsubstantiated high

Value Enhancing Transfer Prices 3

© 2012 Blackwell Publishing Ltd.

transfer prices charged to the affiliate that would trigger scrutiny from

the government authorities. Hence, the profit potential of increasing

transfer prices are offset by this countervailing cost such that the par-

ent may seek an optimal level of transfer price that should be charged

to the affiliate to maximize the differential value whenever positive.

Note that this value gain is independent of tax differentials or financial

arbitrage. Hence, the overall value gain for the parent depends on the

combined impact of financial arbitrage, tax arbitrage and profits to be

made on intra-firm trade and fund flows. This article will trace each

component of value gain to its roots and look at their interactions as

well.

The model developed in this paper is an easy optimization problem

where the optimal levels of transfer prices to be charged to the affiliate

are jointly determined with who should own the affiliate which is

termed as ownership arbitrage. In short, the parent has to decide

whether it is worthwhile to maintain the ownership of the affiliate

along with what transfer price to charge to maximize its gains. As sta-

ted above, the source of value gains for the parent equity holders are

financial arbitrage, tax arbitrage, and profits to be made from charging

the affiliate for the goods, services and funds transferred above their

production cost. Furthermore, the framework of the model is con-

strained to the totally owned affiliates with 100 per cent repatriation of

dividends with no tax deferral but with allowance of full tax credit. As

noted in previous research, tax avoidance policies that prescribe shift

of income to low tax jurisdictions will not be applicable in this set-up.

Nevertheless, this article finds a new source of tax arbitrage when the

home and host countries have different taxes based on present value of

tax shields. This result favors increasing transfer prices for affiliates in

countries with higher tax rates.

The numerical simulations of the model reveal a number of results.

In a base case where taxes are assumed away, the covariance of cash

flows and exchange rates determines whether the parent should main-

tain the ownership of the affiliate. This covariance becomes sole deter-

mining factor for country of ownership in segmented markets where

financial arbitrage is possible for risky assets but not for risk-free ones.

Whenever this covariance is strongly positive, parent should own the

particular affiliate otherwise the affiliate should be carved off and sold

to host country investors. Hence, the decision to set the transfer prices

and ownership of the affiliate are determined simultaneously by the

affiliate cash flows and exchange rates. In this base case where only

4 Nilufer Usmen

© 2012 Blackwell Publishing Ltd.

financial arbitrage is possible, transfer prices play a role in increasing

value to the parent only if uncovered interest rate parity (UIRP) is vio-

lated for risk-free assets of the two countries and favors parent owner-

ship. Whenever the value differential is positive and parent ownership

is supported, the optimal transfer price is determined at a level that is

above the expected trigger price. This finding results from the cost

structure developed in this article.

When tax arbitrage is also considered, ownership decision may be

reversed in the case of strong negative covariance between affiliate cash

flows and exchange rates that would have otherwise indicated host

country ownership. Specifically, for high tax rates in host country that

allows for tax arbitrage gains of our model to be significant, parent

ownership becomes optimal. Once again, under the cost structure of

this article high transfer prices increase profits and hence value beyond

the impact of financial and tax arbitrage, but a penalty on transfer

prices set above a reasonable limit offsets this advantage. The optimal

transfer prices obtained when taxes are considered, however, are lower

for affiliates in higher tax rate countries but higher for lower tax rate

countries compared to the base case.

The numerical simulations demonstrate how a manager of a multi-

national can easily implement the model and obtain an optimal level

of transfer price by using cash flow and exchange rate distributions

and estimated values of parameters such as its profit margin.

2. Financial Arbitrage

Financial arbitrage will be modeled in a state-preference framework.5

Suppose there is an asset that generates state contingent cash flows, R

(s), in foreign currency, and there is also a domestic substitute with

cash flows, [R(s)e(s)], where e(s) are the state contingent exchange

rates. A domestic investor can sell the foreign asset and convert the

proceeds to domestic currency at e0, the spot exchange rate, to buy the

domestic perfect substitute. To avoid arbitrage the following must

hold:

e0½RsRðsÞbðsÞ� ¼ RsRðsÞeðsÞaðsÞ ð1Þ

In the above expression, a(s) and b(s) are the state contingent risk

adjustment factors (pricing vectors, state contingent discount rates) in

the domestic and foreign markets, respectively.

Value Enhancing Transfer Prices 5

© 2012 Blackwell Publishing Ltd.

Sufficient conditions for (1) to hold are

hðsÞ ¼ eðsÞaðsÞ � e0bðsÞ ¼ 0 for every s ð2Þ

However, in a fully integrated market where all securities should be

priced the same in the two markets the condition in (2) is necessary,

too. However, given that in reality capital markets around the world

are somewhat segmented, it is more likely that

hðsÞ 6¼ 0 for some s ð3Þ

Condition (3) furnishes a formal description of market segmentation

in a state-preference framework which is consistent with the standard

definition and empirical evidence. The validity of this condition rests

upon the fact that in an imperfect world capital market, arbitrage can-

not take place instantaneously and effectively, especially for longer

maturities and for arbitrage opportunities that demand high volume of

funds. Hence, h(s) represent the financial arbitrage opportunities pres-

ent in the market. If h(s) is positive, the same unit of income in foreign

currency will have a higher value in the domestic market in that state.

If the reverse is true and h(s) is negative, then the foreign market

places a higher value for the same unit of income in foreign currency

in state s.

It is also well-known that

1

RsaðsÞ ¼ ra and1

RsbðsÞ ¼ rb ð4Þ

where ra and rb are one plus the risk-free interest rates in the two

countries.

Under risk neutrality, a(s) and b(s) become p(s)/ra and p(s)/rbrespectively where p(s) are state probabilities that are assumed to be

the same for both set of investors. In this case, to avoid arbitrage

RRðsÞ eðsÞra

� e0rb

� �pðsÞ ¼ 0 ð5Þ

The above can be simplified to

EðRÞEðhÞ þ CovðR; eÞ=ra ¼ 0 ð6Þ

6 Nilufer Usmen

© 2012 Blackwell Publishing Ltd.

where

EðhÞ ¼ EðeÞra

� e0rb

� �

Expressions in (5) and (6) are descriptions of the UIRP relationship

under risk neutrality. Note that for risky assets with cash flows R(s),

E(h) = 0 is not sufficient for arbitrage to disappear totally. For these

assets, Cov(R,e) will still lead to value discrepancies in segmented capi-

tal markets. The above expression implies that even if arbitrage is not

possible on the average and for risk-free assets whenever E(h) = 0,

deviations can still occur in specific h(s). These deviations are captured

by the covariance term. It should be noted that this covariance term

would not exist if the two capital markets were perfectly integrated

and financial arbitrage could take place in every state for every risky

asset. If it exists, it may also be interpreted as a nonlinear impact of

exchange rates on value.

3. The Valuation Model: Base Case

In this article, there is a parent with an affiliate in a foreign country.

The parent is all equity financed and the affiliate will also be financed

by equity alone. The affiliate will be wholly owned by the parent in the

sense that the parent will not share decision-making control with any

other shareholder in the host country as would have been the case with

a joint venture.6 However, the ownership of the affiliate by parent is

not automatic and will depend on market valuations. For strategic rea-

sons, the parent would like to retain the ownership whenever optimal.

The affiliate generates state contingent cash flows, R(s), in foreign

currency net of costs that are not associated with intra-company trans-

fers. The parent company charges to the affiliate a lump sum price C

in foreign currency for intra-company transfer of goods, services and

funds. The transfer price may be denominated in the foreign currency

for purposes of natural hedging or for other operational reason.7

Although in practice it may be wiser to show a detailed list of specific

items charged to the affiliate to make it easier to substantiate the prices

to the local government authorities, for the purposes of this article a

single price C will be used. This price may cover physical goods and

services transferred to the subsidiary, corporate overhead, royalties,

licensing fees and interest payments on inter-company loans. Once the

Value Enhancing Transfer Prices 7

© 2012 Blackwell Publishing Ltd.

total level of C is determined by the parent, the parent will have lati-

tude to assign individual prices to each item that is charged. C is a

contractual price that is determined by the parent today and that is to

be charged to the affiliate at a future date.

The real known cost of producing this portfolio of goods, services

and funds to parent will be fixed at C* in home currency of the parent.

Moreover, a countervailing cost will be introduced where there will be

a penalty to parent if C is increased to a level that will trigger authori-

ties to intervene in setting the transfer price. In particular, if C is

raised beyond a level that exceeds the standard profit margin of the

parent, the additional profits will be penalized by a that is >1. In other

words, if C* is the true cost and p is a mark-up that is slightly above

the profit margin that the parent earns on its similar business with

third parties, the parent will be penalized whenever Ce(s) > C*(1 + p),

the trigger price. The penalty will be the loss of abnormal profits, as

Ce(s) will be forced to a lower level within the reasonable range

[C* � C*(1 + p)], and some more as penalty and litigation costs; hence

a > 1. Basically, this countervailing cost structure is based on the

premise that government authorities have reasonable diligence and

penalize the firm when transfer prices are set significantly above arm’s

length price.

Initially, to rid the results of this article from potential gains of tax

arbitrage and import tariff/duty avoidance, we exclude taxes, tariffs

and duties to arrive at a base case.

If the affiliate was valued by host country investors, it would have a

value of

Vb ¼ ðEðRÞ � CÞ=rb ð7Þ

If instead, it was valued by the parent country investors, the value

of the affiliate would be

Va ¼Xs

½RðsÞ � C�eðsÞpðsÞ=ra þXs

ðCeðsÞ � C�ÞpðsÞ=ra� a

XD

ðCeðsÞ � C�ð1þ pÞÞpðsÞÞ=ra

where

D ¼ fs : Ce(s) > C�ð1þ pÞg ð8Þ

8 Nilufer Usmen

© 2012 Blackwell Publishing Ltd.

In (8), e(s) are the state contingent exchange rates, and p(s)/ra and

p(s)/rb are state contingent discount factors as noted before.

The condition under which the ownership of the affiliate should be

maintained by parent is

DV ¼ Va � e0Vb > 0 ð9Þ

where e0 is the spot exchange rate. If DV is negative, the affiliate

should be carved off and sold to investors in the host country.8

DV in (9) can be expressed as:

DV ¼ ðEðRÞ � CÞEðhÞ þ fCovðR; eÞ þ ðCEðeÞ � C�Þ� a

XD

ðCðeÞ � C�ð1þ pÞÞpðsÞg=ra ð10Þ

This result can be interpreted as ownership arbitrage and it partially

stems from the covariance term and states that the firm may want to

sell the foreign entity to foreign owners facing a different covariance

structure. However, it should also be noted that the covariance term

appears in the first place due to existence of risky financial arbitrage.

C is bounded by zero on the lower end, meaning only the cases

where the parent is charging the affiliate a positive C will be relevant.

Moreover, the model allows for C values to exceed R(s) values in some

states. This implies that the parent ex ante is willing to absorb losses

from the affiliate in some contingencies if that is going to increase

value today. As there are no outside claimants, this is a reasonable

assumption.

There is also an assumption in the model that exchange rate fluctua-

tions do not have an impact on the cash flows and value of domestic

operations. Otherwise, the multinational may want to sell the domestic

entity to foreigners. It will suffice to assume that exchange rate uncer-

tainty has a greater impact on the value of the foreign subsidiary than

on parent.

The goal of the parent is to set C such that DV has the largest posi-

tive value. If DV were negative, the optimal decision for the firm

would be to spin-off and sell the affiliate to foreign investors and col-

lect cash. In determining maximum positive DV, however, C remains

as a crucial decision variable to exploit the benefits of financial arbi-

trage (ownership arbitrage) embedded in market conditions, as well as

to boost profits from intra-firm trade and fund flows.

Value Enhancing Transfer Prices 9

© 2012 Blackwell Publishing Ltd.

There may be two interpretations of the case where deviations from

UIRP are observed. One is when nominal interest rate differential does

not predict the nominal exchange rate changes. This may be exploited

by means of traditional financial arbitrage whereby country-a investors

move funds but continue to value at country-a discount rate. Second

is real interest rate differentials do not predict real exchange rate

changes which can only be exploited by means of arbitrage of real

assets. The firm can move production between the domestic and the

foreign entity in response to real deviations. This may be called pro-

duction arbitrage. As we do not observe much ownership arbitrage

such a response may be more realistic and tells us that the multina-

tional has other ways of achieving the same. The model accounts for

both interpretations.9

In particular, if risk-free arbitrage is possible and E(h) < 0, increas-

ing C would increase value to the parent and guarantee parent own-

ership as well. Otherwise, parent should set C low to increase this

differential value to make it conducive to parent ownership. Another

term that results from segmented markets paradigm of this article is

the covariance term between affiliate cash flows and exchange rates.

This term is independent of the level of C. Hence, for financial arbi-

trage gains C is a decision factor only for cases where UIRP for risk-

free assets is violated under risk neutrality. When risk-free arbitrage

is not possible but risky arbitrage is still prevalent, the covariance

structure of cash flows and exchange rates lead to ownership arbi-

trage.

Hence, if we further assume E(h) = 0, and that arbitrage is only

possible for risky assets but not for risk-free ones, we obtain

DV ¼ fCovðR; eÞ þ ðCEðeÞ � C�Þ � aEDðCeðsÞ � C�ð1þ pÞÞg=ra ð11Þ

The first term is what is left of the impact of market segmentation

on dividends repatriated which is independent of C, and hence parent

can no longer use C to exploit risk-free financial arbitrage. However,

risky financial arbitrage is still a significant factor in determining the

ownership of the affiliate due to the covariance term. The other two

terms appear as a result of the cost structure of the model. The second

term shows the increase in value to parent by raising C to the highest

possible level; the third term is the penalty if C is increased beyond a

reasonable level to government authorities. In those states where Ce(s)

exceeds the trigger price there will be a loss of a per cent of value.

10 Nilufer Usmen

© 2012 Blackwell Publishing Ltd.

Hence,

@DVR@C

¼ EðeðsÞÞra

� aEDeðsÞra

ð12Þ

and an optimal C is reached when

EðeðsÞÞ ¼ aEDeðsÞ ð13Þ

Note that the distribution of e(s) over states and its nonlinearity on

value is crucial to this result. The right hand term is the expected

exchange rate restricted to the states where the set transfer price

exceeds the trigger price. The optimal C is reached when this condi-

tional expected value in D equals the unconditional expected value of

the exchange rate distribution.

4. Numerical Example and Results: Base Case

This section will investigate the relationships characterized by the

model between C that is determined by the parent, the cash flows of

the affiliate and the exchange rates.

Table 1 below presents the hypothetical data created to fit the

model descriptions.

The data represents an example of values these variables can take

given the desired relationships in the mathematical model. They neither

are empirical data nor are they random (ad hoc) selections, but plausi-

ble representations of the behavior of these variables in real life. For

example, exchange rate values were based on a normalization of an

exchange rate distribution where today’s spot rate is one and the “b”

currency can appreciate or depreciate within a 35–40 per cent band.

This is a reasonable representation of exchange rate behavior for many

currencies. Cash flows of the example can be scaled up or down with

no loss of generality as long as they correlate to exchange rates in the

prescribed manner. Variations of the example in Table 1 were also

tried but did not change the results in any substantial way. The numer-

ical exercises illustrate the mathematical relationships of the model and

the results seem to be robust to variations in inputs.

Based on the values in Table 1 and assuming uniform probabilities,

p(s) = 1/N, we find that Cov(R,e1) = �15.1389 and Cov(R,e2) =+17.00. The data in fact shows strong correlations for cash flows and

Value Enhancing Transfer Prices 11

© 2012 Blackwell Publishing Ltd.

exchange rates as would be the case with import-based and export-

oriented affiliates. Also E(e1) = E(e2) = 0.99. The two exchange rate

variables have same means, although their variations over states are

different. As e0 = 1, both e(s) variables do not show any significant

expected change in exchange rates over time. These exchange rate dis-

tributions were chosen as such to free the results of the numerical

example from a bias in expected exchange rate depreciation or appreci-

ation. The parameter values chosen are ra = 1.045, p = .25 and

a = 1.05. These p and a values may vary for different firms. Obviously,

as p increase the negative impact of the penalty term will be lessened

and as a increases the same impact will strengthen. Also, without loss

of generality, we assume that ra = rb such that E(h) = 0.

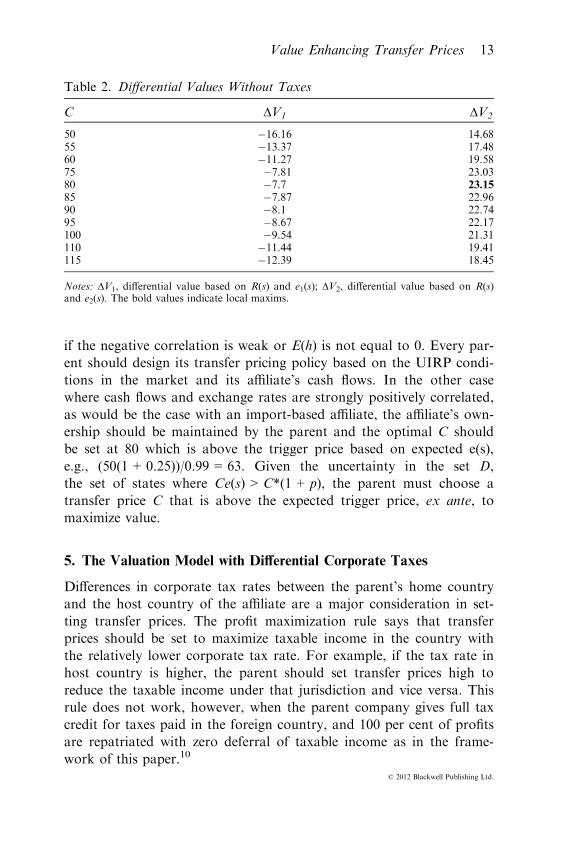

Table 2 tabulates the differential values computed by varying C and

using the data in Table 1. Note that CE(s) > C*, meaning sensible

corporate policy is to set the expected income to the parent from

transferring goods and services at the minimum to equal to the cost of

producing the goods and services and funds charged to the affiliate.

Hence, letting C* = 50 in home currency, C = 50/0.99 = 50.5 is chosen

to be the minimum transfer price that may be set by the parent.

Simulation results in Table 2 show that when cash flows and

exchange rates are strongly negatively correlated as would be the case

for an export-oriented affiliate, there is not much room for the parent

to maintain the ownership of the affiliate by manipulating transfer

prices in the absence of tax arbitrage. Note that this result may change

Table 1. Data on Model Specifications: An example

States R(s) e1(s) e2(s)

1 200 0.80 1.202 220 0.70 1.403 80 1.00 0.804 75 1.20 0.705 50 1.40 0.656 150 1.30 0.907 190 0.85 1.108 250 0.65 1.309 85 1.10 0.8510 175 0.90 1.00

e0 = 1.0 ra = 0.045

Notes: R(s) is state contingent cash flows of the affiliate; e1(s) is an example of state contin-gent exchange rates that are negatively correlated to R(s); e2(s) is an example of state contin-gent exchange rates that are positively correlated to R(s); e0 is the spot exchange rate and rais the risk-free interest rates in the home market.

12 Nilufer Usmen

© 2012 Blackwell Publishing Ltd.

if the negative correlation is weak or E(h) is not equal to 0. Every par-

ent should design its transfer pricing policy based on the UIRP condi-

tions in the market and its affiliate’s cash flows. In the other case

where cash flows and exchange rates are strongly positively correlated,

as would be the case with an import-based affiliate, the affiliate’s own-

ership should be maintained by the parent and the optimal C should

be set at 80 which is above the trigger price based on expected e(s),

e.g., (50(1 + 0.25))/0.99 = 63. Given the uncertainty in the set D,

the set of states where Ce(s) > C*(1 + p), the parent must choose a

transfer price C that is above the expected trigger price, ex ante, to

maximize value.

5. The Valuation Model with Differential Corporate Taxes

Differences in corporate tax rates between the parent’s home country

and the host country of the affiliate are a major consideration in set-

ting transfer prices. The profit maximization rule says that transfer

prices should be set to maximize taxable income in the country with

the relatively lower corporate tax rate. For example, if the tax rate in

host country is higher, the parent should set transfer prices high to

reduce the taxable income under that jurisdiction and vice versa. This

rule does not work, however, when the parent company gives full tax

credit for taxes paid in the foreign country, and 100 per cent of profits

are repatriated with zero deferral of taxable income as in the frame-

work of this paper.10

Table 2. Differential Values Without Taxes

C ΔV1 ΔV2

50 �16.16 14.6855 �13.37 17.4860 �11.27 19.5875 �7.81 23.0380 �7.7 23.15

85 �7.87 22.9690 �8.1 22.7495 �8.67 22.17100 �9.54 21.31110 �11.44 19.41115 �12.39 18.45

Notes: ΔV1, differential value based on R(s) and e1(s); ΔV2, differential value based on R(s)and e2(s). The bold values indicate local maxims.

Value Enhancing Transfer Prices 13

© 2012 Blackwell Publishing Ltd.

In this section, the differential value model developed in (10) will be

extended to include differential corporate taxes. As in the base case,

100 per cent ownership by the parent and 100 per cent payout of divi-

dends are targeted. Foreign dividend withholding tax is zero. There

are no tariffs/duties and the parent country allows for full foreign tax

credit for taxes paid in the host country and tax deferral is not

allowed. The parent has enough income from other sources to use the

tax credits in full.

Let ta equal the corporate tax rate in the home (parent) country,

and tb equal the corporate tax rate in the host country of the affiliate.

Then, the after-tax value of the affiliate is

VTb ¼Xs

ðRðsÞ � CÞð1� tbÞpðsÞ=rb ð14Þ

whereas the affiliate has an after-tax value, VTa, in the home country

represented by,

VTa ¼Xs

ðRðsÞ � CÞð1� taÞeðsÞpðsÞ=ra

þXs

ðCeðsÞ � C�Þð1� taÞpðsÞ=ra

� aXD

ðCeðsÞ � C�ð1þ pÞÞð1� taÞpðsÞ=ra

ð15Þ

Note that with full foreign tax credit, the effective tax rate at home

is equal to the home corporate tax rate ta and it seems as if there is no

tax advantage to maximize taxable income in the home/host country

even if tb 6¼ ta.

The differential value of the affiliate after taxes is

DVT ¼ VTa � e0VTb;

which can be represented by,

DVT ¼ ð1� taÞDV� fðta � tbÞðEðRÞ � CÞEðeðsÞÞg=ra ð16Þ

It is surprising that, in spite of the assumptions of full tax credit

and 100 per cent repatriation of dividends, there is still tax arbitrage

gains possible as is captured by the second term in (16). As noted

14 Nilufer Usmen

© 2012 Blackwell Publishing Ltd.

before, under these conditions, the previous research had shown that

there would be no tax arbitrage opportunity.11

When corporate taxes are considered the differential value in (16)

depends not only on how the host tax rate tb differs from the home

tax rate ta, but also on how that difference weighs on the market valu-

ations of cash flows transferred to parent. The first term in DVT is a

tax reduced version of DV of the base case and stands for ownership

arbitrage. As discussed previously, the source of value discrepancy in

this term or ownership arbitrage are the financial arbitrage opportuni-

ties as represented by E(h) and Cov(R,e), as well as the cost structure

of the model. The second term in DVT is due to tax differences

between the two countries and therefore may be attributed to tax arbi-

trage. This second term tells us that DVT can be increased or

decreased beyond that of financial arbitrage and pricing gains/losses

and the impact comes about by the market value of the cash flows to

the domestic shareholders if ta does not equal to tb. Roughly speaking,

if tb > ta, every additional unit of C will result in a value loss to

domestic shareholders. However, if tb < ta, the domestic shareholders

may increase their differential value by the difference (ta � tb) by

increasing C. Here, tax arbitrage suggests that if the host tax rate is

higher (lower), maximize (minimize) taxable income in that country by

setting transfer prices lower (higher). The implications of this result are

contrary to conventional practice, and hence may seem counterintui-

tive. However, the finding is a complimentary source of tax arbitrage

benefit and may still exist where the standard tax minimization rule

does not apply as explained above. From standard corporate finance

theory dating back to Modigliani and Miller (MM) with taxes, we

know that a firm can increase its after-tax value beyond a base case by

increasing the present value of tax shields. In the classical MM propo-

sitions, tax shields were due to tax deductibility of debt whereas in this

article they are due to deductibility of transfer prices as cost. The sec-

ond term in (16) can be interpreted in terms of the present value of tax

shields to the parent due to deductibility of transfer prices. Specifically,

this term can be separated into two parts and one of those parts is

(ta � tb)CEe(s)/ra. This is the difference in the present value of tax

shields due to the deductibility of transfer prices C, in the host country

with a tax rate of tb versus the present value of that tax shield when ta,

home country tax rate is applied. In other words, the tax shields are

earned at the rate tb but are used at the rate ta, the effective tax rate

for the parent. It implies that when tb > ta, the parent should set C

Value Enhancing Transfer Prices 15

© 2012 Blackwell Publishing Ltd.

low to be taxed maximum at the higher rate to end up with the higher

present value of tax shields. As the tax credits earned in the host coun-

try can be used against tax deficits on other income of the parent, they

are valuable and increase the value to the parent. The underlying

assumption is that the parent can earn excess foreign tax credits in one

country and can use them against tax deficits from another country

when consolidating foreign income at home. This mechanism becomes

the source of tax arbitrage in this article. The size of tax arbitrage

apparently hinges on the tax codes that allow or restrict companies to

use tax credit earned on foreign income fully at home. If the tax codes

put limitations on usage of excess foreign tax credits, tax arbitrage

opportunities would be bounded.12

These implications will be discussed below with a numerical

example. Table 3 will also use the data presented in Table 1 along with

various tax rates in potential host countries.

Looking at ΔVT1 values, we can see that favorable tax advantage

can change the outcome of the base case. This type of an affiliate

whose cash flows are strongly negatively correlated with exchange rates

should have been carved off and sold to host country investors in the

absence of tax arbitrage as was shown in the base case. This result is

enhanced whenever tb < ta such that the impact on value of tax arbi-

trage is negative and there is no advantage from the lower tax rates in

the host country. However, when tb exceeds ta and tax advantage turns

to be favorable, it becomes feasible to maintain the ownership of the

affiliate. However, in this case, the optimal C is lower at 60 or 75. As

ta < tb for these cases the weight put on penalty (1 � ta) is greater

than the weight put on profits (1 � tb), the negative impact of penalty

dominates resulting in lower C values, (see footnote 2).

The ΔVT2 values are almost all positive and are pointing to the fact

that tax arbitrage, favorable or unfavorable, would not alter the out-

come that the affiliate should be totally owned by the parent if cash

flows and exchange rates are strongly positively correlated. It is not

surprising that in cases where tb > ta a lower C value than 80 is opti-

mal as explained above, whereas C needs to be raised above 80 to

maximize value gains when tb < ta and tax arbitrage is unfavorable.

This numerical example demonstrates that finding the optimal C is

an easy optimization problem for managers. The only inputs needed

are cash flow and exchange rate distributions and estimates of p and aand interest rates. Using these inputs covariances and expected values

can be readily estimated and differential values are computed. Hence,

16 Nilufer Usmen

© 2012 Blackwell Publishing Ltd.

the model is operational and can easily be put to practice by the man-

agers of the multinationals.

6. Conclusion

Multinationals have long used transfer pricing mechanisms to circum-

vent market imperfections brought about by government authorities

such as tariffs, duties, exchange controls and blocked funds. Another

well-known use of transfer price schemes is to exploit tax arbitrage

opportunities. The previous arguments on the benefits of moving

income from one jurisdiction to another using transfer prices were

based on profit-seeking incentives and implied that the taxable income

in a high tax rate country should be minimized to minimize global tax

Table 3. Differential Values with Corporate Taxes

tb 0.15 0.20 0.25 0.30 0.35 0.40 0.45C ΔVT1 ΔVT1 ΔVT1 ΔVT1 ΔVT1 ΔVT1 ΔVT1

50 �25.21 �20.58 �15.94 �11.31 �6.68 �2.05 2.5855 �22.54 �18.15 �13.75 �9.36 �4.96 �0.57 3.8360 �20.36 �16.20 �12.04 �7.89 �3.73 0.43 4.58

75 �15.80 �12.36 �8.91 �5.47 �2.02 1.42 4.8680 �15.01 �11.80 �8.59 �5.39 �2.20 1.03 4.2385 �14.42 �11.44 �8.48 �5.51 �2.54 0.43 3.4090 �13.86 �11.13 �8.40 �5.67 �2.94 �0.21 2.5395 �13.55 �11.10 �8.57 �6.10 �3.58 �1.10 1.41100 �13.45 �11.19 �8.93 �6.68 �4.42 �2.16 0.09110 �13.35 �11.57 �9.79 �8.01 �6.22 �4.44 �2.66115 �13.30 �11.76 �10.22 �8.67 �7.13 �5.58 �4.04

tb 0.15 0.20 0.25 0.30 0.35 0.40 0.45C ΔVT2 ΔVT2 ΔVT2 ΔVT2 ΔVT2 ΔVT2 ΔVT2

50 �3.62 1.01 5.65 10.28 14.91 19.54 24.1755 �0.95 3.44 7.84 12.23 16.63 21.02 25.4260 1.23 5.39 9.55 13.70 17.86 22.02 26.1775 5.79 9.23 12.68 16.12 19.57 23.01 26.46

80 6.58 9.79 12.99 16.20 19.41 22.62 25.8285 7.18 10.14 13.11 16.08 19.05 22.02 24.9990 7.73 10.46 13.19 15.92 18.65 21.38 24.1295 8.04 10.53 13.02 15.52 18.01 20.51 23.00100 8.14 10.40 12.66 14.91 17.17 19.43 21.68110 8.24 10.02 11.80 13.58 15.36 17.15 18.93115 8.29 9.83 11.37 12.92 14.46 16.00 17.55

Notes: ΔVT1, differential value with corporate taxes based on R(s) and e1(s); ΔVT2, differen-tial value with corporate taxes based on R(s) and e2(s); ta = 0.30 and tb is the corporate taxrate in host country. The bold values indicate local maxims.

Value Enhancing Transfer Prices 17

© 2012 Blackwell Publishing Ltd.

liability. Minimization of global tax liability would be achieved by

charging high transfer prices in the countries with high tax rates. How-

ever, this type of tax arbitrage benefit disappears whenever dividends

are fully repatriated, there is no tax deferral and full tax credit is

allowed by home tax authorities.

This article presents a value-seeking framework under risk neutrality

where transfer prices are used to exploit tax arbitrage as well as finan-

cial arbitrage opportunities that are present in segmented international

capital markets. By shifting the focus from profit seeking to value-

seeking approach, the paper offers a new framework for setting trans-

fer prices based on the impact on value of financial and tax arbitrage.

However, for a parent to use transfer pricing schemes as a strategic

tool, it has to have a market valuation that would support its owner-

ship of the affiliate. In other words, financial and/or tax arbitrage may

lead to ownership arbitrage for the firm.

This article also develops a cost structure for transfer pricing

schemes where profits on intra-firm trade and fund flows are allowed

along with a penalty for transfer prices charged above a trigger level.

This value gain is treated independently of any financial or tax arbi-

trage effects. This value gain will exist even if there is no tax arbitrage

opportunity and capital markets are totally integrated. Subsequently,

an optimization framework is obtained where a value-maximizing level

of transfer price can be determined that takes into account favorable

and unfavorable impacts of financial and tax arbitrage along with

profit opportunities from transfer of any products, services or funds.

First, in a base case where taxes are assumed away, it argues that in

the presence of financial arbitrage alone, and in a case where cash

flows of the subsidiary are positively correlated to exchange rates as in

import-based affiliates, the parent should own the affiliate and set

transfer prices at a level higher than its expected trigger price to maxi-

mize value. This is not true for export-based affiliates where cash flows

and exchange rates are strongly negatively correlated. It is best to

carve off these affiliates and sell them to host country investors after

charging them C for the funds and services already transferred.

Exploring the extended model with tax differentials between the par-

ent and the host country reveals some surprising reversals to the impli-

cations of the profit-seeking rule and to the conventional practice. The

maxim that whenever the tax rate in the host country is lower/higher

than that of the parent transfer prices should be set low/high is no

longer valid because the framework of this article allows for full tax

18 Nilufer Usmen

© 2012 Blackwell Publishing Ltd.

credit and total repatriation of dividends with no deferral. However,

another form of tax arbitrage emerges where the level of transfer prices

determine the present value of tax shields based on transfer prices in

each country. The tax advantage of transfer prices depend on the size

of tax differences and how they interact with financial arbitrage oppor-

tunities in the market. When tax differences are large enough and tax

arbitrage effect is dominant, higher taxes in the host country becomes

a factor that increases the present value of tax shields. This gain is due

to tax code allowances that allow excess tax credits earned from one

affiliate to be applied against tax deficits from another affiliate. This

impact may interact with that of financial arbitrage and make it possi-

ble for the parent to own the affiliate in cases where financial arbitrage

alone would have prohibited it to happen. The optimal levels of trans-

fer prices differ from that of the base case and are lower/higher for

unfavorable/favorable tax arbitrage.

A set of testable propositions emerge from the findings of this

study. First, with segmented capital markets where UIRP holds for

risk-free assets, parent ownership tends to be more prevalent for affili-

ates whose cash flows are strongly positively correlated by exchange

rates and/or when host country tax rates are significantly higher than

home. Second, multinationals that set their transfer price higher than

the expected trigger price should have higher values compared to their

peers that do not. Accordingly, transfer prices should be set higher for

industries that have higher profit margins and lower penalties. The

third proposition of this article is that transfer prices should be higher/

lower than the expected trigger price for affiliates in countries with

higher/lower tax rates. This proposition stands in sharp contrast to

predictions of conventional profit maximization dictum that says the

parent has an incentive to charge high transfer prices in high tax envi-

ronments to shift profits to low tax locations.

A couple of caveats are in order while testing the above hypothesis.

The predictions of this article are valid for affiliates that are wholly

owned and that operate in environments where import duties are

insignificant. Moreover, the parent transfers 100 per cent of dividends

and full tax credit is allowed for foreign tax liability with no deferral.

This kind of environment may not exactly describe the institutional

practices at present but recent tax proposals by the U.S. administra-

tion is a step in that direction.13 Even if tax differences matter in the

conventional sense, this article shows that there is a mitigating factor

that should be balanced against the predictions of the well-known tax

Value Enhancing Transfer Prices 19

© 2012 Blackwell Publishing Ltd.

minimization rule. Also, the empirical investigation should show evi-

dence of the effect on firm value of the choice of transfer pricing pol-

icy. Empirical results that show correlations between the level of

transfer prices and tax rates will not be conclusive. Those correlations

would simply show evidence of the practices followed by the decision

makers in firms but would fail to show if those practices are value

enhancing. Another restriction in testing the propositions of this arti-

cle is that the model overlooks agency costs.14 While the direct effect

of choosing low/high transfer prices is to increase the after-tax value

of the parent, these effects may be potentially offset in poorly gov-

erned firms by increased opportunities for managers to manipulate

income. Therefore, the results should be tested for firms with high-

quality governance.

In summary, this article develops a value-seeking framework to ana-

lyze the benefits of transfer price schemes in the presence of financial

arbitrage and tax arbitrage in segmented international capital markets

that lead to ownership arbitrage. The model is flexible enough and can

easily be expanded to include the effects of import duties, partial own-

ership, variable dividend payout ratios, deferral of income repatriation,

and agency costs that may also affect the value of a multinational.

Furthermore, more complex financing structures like borrowing at

home or in the foreign country or hedging can also be handled by the

model. However, it is important to note that any of these new ele-

ments that may be included in the model should be viewed in terms of

their effects on value. The optimization model to be used by any par-

ticular company to set their optimal transfer price should modify the

present model to fit their business practices to allow them to draw

their own conclusions.

Notes

1. In this article, transfer prices are used synonymously with internal prices usedwithin a corporation that differs from arm’s length.2. Horst (1971), Arpan (1972), Fowler (1978), Collins and Frankel (1985), and Kant

(1988), for example.3. A recent article by Curtis (2008) argues that transfer pricing has been often

framed as a tax issue but it has repercussions much beyond that for a multinationaltreasurer. As noted by Curtis, transfer pricing is closely knitted with the efficiency ofmany financial management functions in the multinational. This article is a step intothat kind of inquiry.4. Stulz (1981), Eun and Janakiramanan (1986), Hietala (1989), Bonser-Neal et al.

(1990), and Nishiotis (2004).

20 Nilufer Usmen

© 2012 Blackwell Publishing Ltd.

5. This framework was developed in Thomadakis and Usmen (1991) and Usmen(1994).6. Desai et al. (2004) show empirical evidence from the past twenty years that there

is a trend away from joint ventures to majority and whole ownership of the affiliates byU.S. MNCs. They argue that this trend can be explained by the increased burden ofjoint ventures for the MNC who would like to make decisions freely about selling andfinancing to minimize worldwide costs. Especially, when the local partners have a stakein local profits alone, the MNC cannot set transfer prices in a way that would minimizeglobal tax liability.7. The cost of the resources transferred to the subsidiary could also be charged in

domestic currency units. In that case, cash flows of the foreign subsidiary would have acost of C/e(s) and the impact of exchange rate uncertainty still be captured in themodel. However, the present model charges C in foreign currency for reasons of natu-ral hedging.8. This type of modeling is also used in Thomadakis and Usmen (1991) and Usmen

(1994). The hypothetical valuation of the cash flows in the host country are relevantbecause the parent should remain the owner if it can create a value beyond the alterna-tive of selling the affiliate upfront to host country investors after charging them C forthe products, services and funds already transferred. One should not be confused bythinking that there are no foreign owners to value the cash flows that differs from theparent and therefore this value differential is contradictory.9. We thank an anonymous referee for pointing this to us.10. See for example, Clausing (2003).11. Based on (16), the optimal C is obtained where ð1� tbÞEðeðsÞÞ ¼ ð1� taÞaEDeðsÞ.

Again, the covariance between tax shields and exchange rates come into play. It is thenonlinearity with respect to exchange rates on value that explains why the tax differen-tial matters.12. For example, the U.S. tax code allows foreign tax credits derived from one

source against foreign tax liabilities from another source provided they are based onsame type of income. This practice is known as tax averaging. However, total tax cred-itable in any 1 year is limited by a formula based on foreign versus total taxableincome of the multinational.13. Financial Times, Wednesday, May 6, 2009 issue reported that Obama Adminis-

tration is cracking down on tax avoidance loopholes that allow U.S. multinationals toreport disproportionately high profits in low tax countries and to delay paying U.S.taxes by deferring repatriation of these profits.14. Value-maximization runs into obstacles in the presence of agency costs. See, for

example, Jensen (2001).

References

Arpan, J.S., International Intracorporate Pricing (New York: Praeger, 1972).Bonser-Neal, G., G. Brauer, R. Neal and S. Wheatley, “International InvestmentRestriction and Closed-End Country Fund Prices,” Journal of Finance 45 (1990),pp. 523–548.

Clausing, K.A., “Tax-Motivated Transfer Pricing and US Intrafirm Trade Prices,”Journal of Public Economics 87 (2003), pp. 2007–2223.

Collins, J.M. and A. Frankel, “International Cash Management Practices of LargeU.S. Firms,” Journal of Cash Management 5 (1985), pp. 42–48.

Value Enhancing Transfer Prices 21

© 2012 Blackwell Publishing Ltd.

Curtis, S.L., “Transfer Pricing for Corporate Treasury in the Multinational Enterprise,”Journal of Applied Corporate Finance 20 (2008), pp. 97–112.

Desai, M.A., C.F. Foley and J.R. Hines Jr., “The Costs of Shared Ownership: Evidencefrom International Joint Ventures,” Journal of Financial Economics 73 (2004), pp. 323–374.

Eun, C.S. and S. Janakiramanan, “A Model of International Asset Pricing with a Con-straint on the Foreign Equity Ownership,” Journal of Finance 41 (1986), pp. 897–914.

Financial Times, Wednesday, May 6, (2009), pgs 3, 8 and 9.Fowler, D.J., “Transfer Prices and Profit Maximization in Multinational EnterpriseOrganizations,” Journal of International Business Studies 9 (1978), pp. 9–26.

Hietala, P., “Asset Pricing in Partially Segmented Markets: Evidence from the FinishMarket,” Journal of Finance 41 (1989), pp. 603–613.

Horst, T., “The Theory of the Multinational Firm: Optimal Behavior Under DifferentTariff and Tax Rates,” Journal of Political Economy 79 (1971), pp. 1059–1072.

Jensen, M.C., “Value Maximization, Stakeholder Theory, and the Corporate ObjectiveFunction,” European Financial Management 7 (2001), pp. 297–317.

Kant, C., “Foreign Subsidiary, Transfer Pricing and Tariffs,” Southern Economic Jour-nal 55 (1988), pp. 162–170.

Nishiotis, G.P., “Do Indirect Investment Barriers Contribute to Capital Market Seg-mentation?,” Journal of Financial and Quantitative Analysis 39 (2004), pp. 613–630.

Stulz, R.M., “On the Effects of Barriers to International Investment,” Journal ofFinance 36 (1981), pp. 923–934.

Thomadakis, S.B. and N. Usmen, “Foreign Project Financing in Segmented CapitalMarkets: Equity Versus Debt,” Financial Management 20 (1991), pp. 42–53.

Usmen, N., “Currency Swaps, Financial Arbitrage, and Default Risk,” Financial Man-agement 23 (1994), pp. 43–57.

22 Nilufer Usmen

© 2012 Blackwell Publishing Ltd.

Recommended