PERFORMANCE MANAGEMENTRESEARCH UNIT

IS THERE AN EXPECTATION GAPOF MATHEMATICAL SKILLS

BETWEEN ACCOUNTING EDUCATIONAND PRACTICE?

GRAHAM FRANCIS, CLARE SPENCER AND JACKIE FRY1

98/6

1 The Authors would like to thank Roland Kaye, Matt Hinton and CIMA for their help withthis project. The opinions expressed are the authors’ own and should not be seen asrepresentative of CIMA.

2

3

ABSTRACT

Within the accountancy profession, there has been a steady move away from the detailed

technical side of the profession and towards the more strategic, business orientated approach.

This has been partly in response to the advent of new information technology making a

number of previously difficult calculations straightforward, but also due to a repositioning of

the accountant as a ‘business adviser’ rather than a purely technical accounting and finance

expert. This paper examines the dilemma faced by the professional accountancy bodies. Are

we training accountants in the use of outdated and redundant computational techniques?

Conversely, can accountants fully understand and interpret the results of calculations if they

have never studied the process from first principles? By removing them do we risk losing

potentially valuable differentiating skills in the drive to make accounting qualifications more

strategic and business orientated?

This working paper investigates the use of quantitative skills by accountants and addresses

two main questions:

1. What quantitative techniques are accountants using in their work?

2. Is current accountancy training providing adequate coverage of appropriate quantitative

techniques?

The paper reports the findings of two questionnaire surveys carried out in conjunction with

the Chartered Institute of Management Accountants (CIMA) as part of their ongoing syllabus

development work. The first questionnaire was distributed to over 7000 CIMA employers,

both in the UK and overseas. The questionnaire explores the techniques employed by the

CIMA members and their accounting staff and also their views on the importance of

quantitative techniques in the role of a modern accountant. Lecturers on professional

accountancy courses were asked to complete a second adapted version of the questionnaire to

4

allow comparison of the views of representatives from the training and practitioner

perspectives.

An analysis of the syllabus content of the main international accounting bodies was carried

out with respect to quantitative techniques. The analysis was not restricted to the syllabus, but

guidance notes, teaching materials and past examination papers were all used to determine

both the breadth and depth of coverage. The result of this analysis was compared with the

results of the questionnaires discussed above to identify inconsistencies between the work of

modern accountants and their current accountancy training programmes.

5

1. Introduction

Quantitative techniques underpin much of the day to day work of a modern accountant. But

how much actual knowledge and understanding of these various techniques does the

accountant need? Is an awareness of the techniques available sufficient or should accountants

demonstrate proficiency in applying them as a right of passage into their profession? With the

growth in the ease of use and sophistication of modern software are we coaching accountants

in obsolete and unnecessary skills? Are business skills more important? Is the time needed to

teach some of these techniques unjustified given the minimal use made of them by a large

number of accountants in practice? Conversely is the profession in danger of losing its one

vital differentiating factor from the hordes of MBA graduates flooding into business? As one

respondent put it ‘if the accountant does not have any mathematical skills, no-one else will’.

This paper reports on the actual scope and content of the quantitative technique elements of

accounting programmes world-wide, as well as the views of qualified accountants and

professional accountancy course lecturers on what that content should be. We look at whether

there is a difference between what is being taught and assessed and the skills used in practice.

Additionally, we will examine what skills employers expect from a qualified management

accountant and to what extent they are required in the role of a modern accountant compared

to being a professional expectation.

2. Literature review

There is a fairly wide body of research on the application of quantitative techniques by

managers (such as Juritz et al, 1988; Naudé et al, 1997) but much less specifically on their

use by accountants. An abridged summary of relevant survey findings is shown in Table 1,

(See Appendix A for unabridged version). Naudé et al (1997), showed quite a consistent

pattern of the usage of quantitative techniques by managers, between the UK, South Africa

and New Zealand.

There is evidence that the nature of quantitative methods used, is contingent upon

organisational characteristics. Drury et al (1993) found larger organisations making more use

of mathematical methods. Juritz et al (1985) found a similar trend in South Africa.

7

Table 1 – Percentage of respondents who use techniques (based on yes or no)This study Naudé et al 19971 Drury et

al 1993Østergaard

19932Wisniewsk

i 19903Coccari

1989Juritz etal 19884

Kathawala1988

Forrester19845

Wegner19836

Green etal 1977

Alpander 1976

n=296 n=36 n=639 n=408 n=172 n=288 n=900? N=65 n=226 n=164 n=78 n=75(total, breakdown between groups notgiven)

Employers UK

LecturersUK

UK SouthAfrica

NewZealand

UK Denmark EU USA SouthAfrica

USA UK SouthAfrica

USA Expatriatesin DCs(USA)

Expatriatesin DCs(Not USA)

Expatriatesin LDCs(USA)

Expatriatesin LDCs(Not USA)

Fractions, percentages and ratios 100 100Index numbers 20 22 15Powers and roots 47 94Annuities and perpetuities 71 97Formulation and solution of linearequations

57 94

Break-even analysis 91 50 60 35 65 20Inventory control/analysis 67 63 45 67.6 30 68 27 78Formulation and solution ofpolynominal equations

25 58

Learning curves 64Calculus 19 58Logarithms 14 42Probabilities and expected value 84 94 8 10 11 51 72Simulation techniques 65 38 29.3 20 84 16 32 68 50 40 40 15Bayesian statistics 36 26Game theory 31 23Markov chain 24 22Queuing theory 17.6 46 39 30 22 30 8Decision trees 70 94 77 9 3Linear regression 48 97Forecasting 29 31 20 60 96 32 54Moving averages 44 38Econometric models 15 10 15 30Multiple regression techniques 36Time series analysis 88Correlation coefficients 44 89 13 25 11 35 37 30 87 16 54 86Standard deviation 55 94Basic stats and graphs 75 65 80 25 52Analysis of variance 81 72Normal distribution 59 84Sampling 20 89 85Quality control 7 14 16 54 25 91.2 40 32Hypothesis testing 4 5 7Confidence intervals 7 13 9Chi square testing 15 78 48 48Contingency tables 12 12 11Nonparametric tests 3 4 2Linear programming 28 89 37 29 20 23.5 20 64 12 83 40 15Non-linear programming 45 37Note 1 Based on a 5 point scale of no-little-moderate-frequent-extensive use. Reflects percentage replying to frequent or extensive.

8

Note 2 Based on a 4 point scale of not available-never-occasional-frequent. Reflects percentage replying occasional or frequent.Quoted in Naudé et al 1997.Note 3 Percentage indicating high frequency of use. Quoted in Naudé et al 1997.Note 4 Percentage indicating routine usage.Note 5 Based on a 4 point scale of none-peripheral-much-extensive. Reflects percentage replying to much or essential. Quoted in Naudé et al 1997.Note 6 Based on a 5 point scale of no-little-moderate-frequent-extensive use. Reflects percentage replying to frequent or extensive.

9

Kathawala (1988) again found large firms in the USA made more use of quantitative

techniques and that there was a different pattern of techniques used for service and

manufacturing firms. In terms of functional areas, Coccari (1989) found that ‘production

managers’ made the greatest use of Operational Research techniques and ‘Accounting’ and

‘Finance’ made the greatest use of forecasting methods.

Coppinger and Epley (1972) examining the non-use of advanced mathematical techniques,

found, with the exception of discounted cash flow, little use of other techniques. Kathawala

(1988) considered lack of knowledge to be a significant barrier to the use of techniques.

Where as Stray et al (1994) cite both time to collect and process data as well as lack of

knowledge. Naudé et al (1997) sought to differentiate between an awareness of the techniques

and their usage.

Whilst this paper focuses on underlying quantitative skills as well as application, much of the

research has focused simply on the applications. The survey by Drury et al (1993) mainly

concentrated on management accounting practice but also included a section on ‘Other

Aspects of Management Accounting’ that included questions on quantitative techniques.

Their findings also revealed mistakes in the treatment of inflation.

One area, which has been extensively researched, is Capital Investment Appraisal, with

studies by Drury et al (1993) and Sangster (1993) amongst others. Pike’s studies (see Pike

and Wolfe, 1988; Pike and Neale, 1993 for summaries), have shown a changing pattern of

techniques, but this can not be put down to the training of accountants as Capital Budgeting

techniques and their relative merits have long been included in the syllabuses.

In recent years, particularly following Johnson and Kaplan (1987), there has been much

emphasis on the need for changes in management accounting practice (see Scapens, 1991;

Bromwich and Bhimani, 1989) This has inevitably led to discussion about the changing roles

of management accountants. CIMA’s 'Standards of Competence in Management Accounting'

(1994) also seeks to define the key roles of a professional management accountant.

Kaplan (1995) (cf Francis et al, 1998) argues that management accountants should:

10

• become part of their organisation’s value-added team,

• participate in the formulation and implementation of strategy,

• translate strategic intent and capabilities into operational and managerial measures,

• move away from being scorekeepers of the past to become the designers of the

organisation's critical management information systems.

Cooper (1996) argues that management accountants role must evolve:

“Look out, Management Accountants. To survive, you must develop skillsin systems design and implementation, change management, and strategyas well as cost management and management accounting.”

Developments in information technology have also had a profound effect on roles of

accountants and their required skills. However an over reliance on computers can be

problematic. Ward (1997) points out that there were mistakes in as many as 90% of

spreadsheets, highlighting the importance of having an understanding of what is going on

inside the computer. (cf Earl and Hopwood, 1981)

“Organisations…and business schools…are investing significantly incomputational hardware and software…On the other hand the sameinstitutions are increasingly turning their backs on ‘Bean Counters’.”

Dhebar (1993)

These pressures have led to a need for syllabuses to develop to reflect the needs of students.

As Hanno and Turner (1996) state:

“The accounting profession is clearly a dynamic and changing field. Thefuture will demand a more fluid and adaptive approach to deliveringaccounting education.”

Whilst the changing environment faced by management accountants has placed new skill

demands on them, their traditional need for quantitative skills remains. Spencer and Francis

(1998a & b) found there were expectations of what a qualified accountant should be able to

do. Yet whilst quantitative skills were necessary, they were not sufficient in themselves to

make a ‘good’ accountant. Communication and computing skills were two other important

11

facets. Simons and Higgins (1993) claim that both practitioner and academics see a need for

more attention on communication and problem solving skills.

In terms of syllabus development, there have been several studies on the quantitative method

content of MBA programmes; (see for example Borsting et al, 1988; Rose et al, 1988 and

Easton et al, 1988). Coccari (1989) concluded that Universities place too much emphasis on

teaching techniques, which are little used in practice. Carver and King (1986) found that most

practitioners want input into accounting syllabuses.

Siegel and Kulesza (1996) (cf Benke, 1996) also consider there to be a gap between theory

and practice in the US. Tyrrall and Wrighton (1997) suggest a lack of congruence between the

expectations of academics, practitioners and students. Bain (1992) argues for a more

integrative approach to teaching quantitative methods rather than compartmentalising into

distinct disciplines.

Tony Mock’s (1996) article, questioned how good accountants need to be at Maths and what

their background knowledge to meet expectations:

“Isn’t it time we look through the veil of mystery surroundingmathematics, admit what we do and don’t understand and seek todistinguish between what is of practical relevance and what isnot?”…Mock also requested… “Can management accounting academicsand practitioners get together to ensure that the areas of research beingfollowed and exam syllabuses set are of practical relevance. Can thoseresponsible for setting exam syllabuses and teaching them ensure studentsare given the tools necessary to do the job.”

3. Methodology

In order to collect data for this project two questionnaire surveys were undertaken. The first

was designed to determine the current practice of accountants in business and their views on

the role of quantitative techniques in the work of an accountant. This questionnaire was sent

to over 7000 CIMA employers, responsible for overseeing the training of the accountants

within their organisation training for the CIMA examinations. Replies were received from

296 employers who represent a comparatively large sample for this type of survey (see Table

1). These questionnaires were enclosed as part of CIMA’s employment group newsletter. This

12

method of distribution is likely to have contributed to the response rate. CIMA commissioned

the survey and chose this method of distribution to enable the employers to contribute to

CIMA’s Syllabus 2000 review.

The second smaller survey was of accountancy lecturers who attended a CIMA lecturer’s

conference. Although only 36 responses were received this does represent a high proportion

of those teaching in the areas of the syllabus which involve quantitative methods. The

purpose of the second questionnaire was to compare and contrast the views of these two

stakeholders in the accounting profession. The differences between the expectations of these

groups has been suggested by Siegel and Kulesza (1996), Benke (1996) and Tyrrall and

Wrighton (1997).

In order that comparison could be made between them, the questionnaires contained virtually

identical questions with only slight changes made to reflect the contexts of the two groups.

The questionnaires are included with results in Appendices B and C. The questions include 3

tables of Likert scales. These are suitable for attitude measurement (see Robson, 1993)

questions and also allowed other questions to reflect the frequency of use. Previous studies of

managers (rather than specifically accountants) have used a variety of scales. We have

reclassified these and our results are in Table 1 and Appendix A for purposes of comparison.

The 7 point Likert scales were labeled in order to help define the ranges. The use of such

scales in accounting education research is advocated by Hartman and Ruhl (1996) who

criticise the methodology used by some previous studies into syllabus requirements. The

questionnaires also asked an open question to provide scope for respondents to add their

comments and collected some data on the respondents’ backgrounds.

To gain a complete picture of what is currently required for professional qualification, the

quantitative method syllabus content of many of the main international accounting bodies was

analysed. A wider review of the whole of these syllabuses has also been carried out by the

Open University (Lewis and Kaye, 1997) The syllabuses examined included the main UK

bodies and countries such as Canada, Australia, South Africa and New Zealand. This analysis

was carried out using the BAAEC (Board of Accreditation of Accountancy Educational

Courses) assessment grids. The BAAEC supervises the process through which academic

courses in the United Kingdom and Eire are recognised by the Institute of Chartered

13

Accountants of England and Wales (ICAEW), the Institute of Chartered Accountants of

Scotland (ICAS), CIMA and The Chartered Institute of Public Finance and Accountancy

(CIPFA). These grids provide a comprehensive list of indicative content of Foundation and

Professional stage accountancy qualifications. The analysis was not restricted to the syllabus;

guidance notes, teaching materials and past examination papers were all used to determine

both the breadth and depth of coverage. The result of this analysis was compared with the

results of the questionnaires discussed above to identify inconsistencies between the needs of

modern accountants and their current accountancy training programmes.

4. Results

This section first considers the results from the Employers questionnaire. It then compares

these with the results of the similar questionnaire completed by the accountancy lecturers, to

draw conclusions as to both the similarities and differences between their views on the role of

quantitative skills for the modern management accountant.

4.1 Employers questionnaire

From the 7000 questionnaires sent to CIMA employers a total of 296 responses were

received. The majority of the respondents were in senior management positions within the

finance function of their organisation (see Table 2).

Table 2 – Position of Employer respondents within their organisations

% Chief Executive/ Director 7.8 Finance Director/Deputy/Controller 60.4 Accountant/Assistant Accountant 13.0 Manager 9.2 Other 9.6

The respondents came from across the full range of business sectors although, as one might

expect given that these organisations are training CIMA students, there was a bias towards the

manufacturing sector (see Table 3).

14

Table 3 – Business sectors of organisations covered by Employers

% Manufacturing 44.0 Public sector 18.1 Service 13.0 Financial 6.5Other 18.4

Respondents also came from the full size range of organisations, although the majority was

from medium sized organisations, as defined by the number of employees (see Table 4).

Table 4 – Number of employees within Employers’ organisations

% Small (less than 100 employees) 9.9 Medium (100-2500 employees) 57.0 Large (over 2500 employees) 33.1

We found some evidence that quantitative techniques were in greater use in large

organisations. This supports previous studies by Drury et al (1993), Juritz (1988) and

Kathawala (1988).

The Employers were asked a range of questions about the role of quantitative skills looking at

what quantitative techniques are used, what skills they expect of an accountant and how that

role has changed with the advent of new technology. A copy of the full results from the

questionnaire is include in Appendix B. They were also asked to comment freely on their

opinions of any of these areas. Of the 296 respondents 107 added written comments to their

questionnaire, a content analysis of which is included in Appendix D.

15

4.1.1 The importance of quantitative skills

Employers view technical skills as being crucial to the role of a modern management

accountant. 68% of participants agreed that management accountants need strong

mathematical skills and that the day to day role of an accountant requires something more

than basic numeracy skills (see Table 5). As one employer commented:

“A high level of numeracy is essential, irrespective of the use of complexmathematical techniques. If a qualified accountant is not able to drawconclusions from a set of numbers he is useless, and this ability dependson being highly numerate.”

This view of the importance of a high level of numeracy was expressed by 25% of the

respondents who made written comments.

Table 5 – Employers’ responses to the role and skills requirements of today’smanagement accountants

Disagree

1,2,3%

Neutral4%

Agree5,6,7

%In the modern role of a management accountant, concepts are moreimportant than detailed calculations 27 25 48

Management accountants need strong mathematical skills 12 20 68

The modern role of a management accountant requires businessskills more than technical skills 13 28 59

Today’s management accountants do not make full use of themathematical techniques available to them 13 22 65

The day to day role of the management accountant only requiresbasic numeracy skills 68 10 22

New technology has dramatically reduced the mathematical skillsneeded by a management accountant 34 13 53

Newly qualified management accountants have weak mathematicalskills 37 41 22

Mathematical ability in newly qualified management accountantshas fallen over the last 5 years 27 52 21

16

When employers were asked to comment on the importance for newly qualified management

accountants to be able to carry out specific quantitative applications, very few felt that any of

the techniques presented were unimportant. An extract of these results is shown in Table 6.

Table 6 – Importance of ability in quantitative areas for newly qualified managementaccountants

Unimportant%

Useful%

Essential%

Analysing data looking for trends and patterns

0 12 88

Formulating and solving problems as simple equations; forexample Price variance =Actual Qty ( Std price - Actual price)

2 30 68

Solution of problems with constraints; for example an optimalproduction plan given scarcity of labour and materials

2 54 44

Estimating straight line relationships between variables; forexample the relationship between variable costs and volume

2 42 56

Compounding and discounting ; for example in discountingcash flows or to find a monthly interest rate

4 53 43

Formulating and solving problems as more complex equations;for example y=axb for the learning curve effect

26 65 9

However in today’s environment employers saw these quantitative skills as lying along side

business and communication skills. 59% of employers agreed that the normal work of a

management accountant requires business skills more than technical skills. This is consistent

with the findings of Simons and Higgins (1993). As one employer noted in their written

comments:

“A good basic knowledge of mathematical skills is needed, but moreimportantly management accountants need to be able to understand thebusiness needs of their organisation, and have an all-round businessknowledge.”

4.1.2 Use of quantitative skills

In contrast to some of the findings above, the survey revealed a low level of actual use of

quantitative skills. Employers were asked how often they saw certain mathematical and

quantitative techniques being used. Table 7 summarises the results; techniques have been

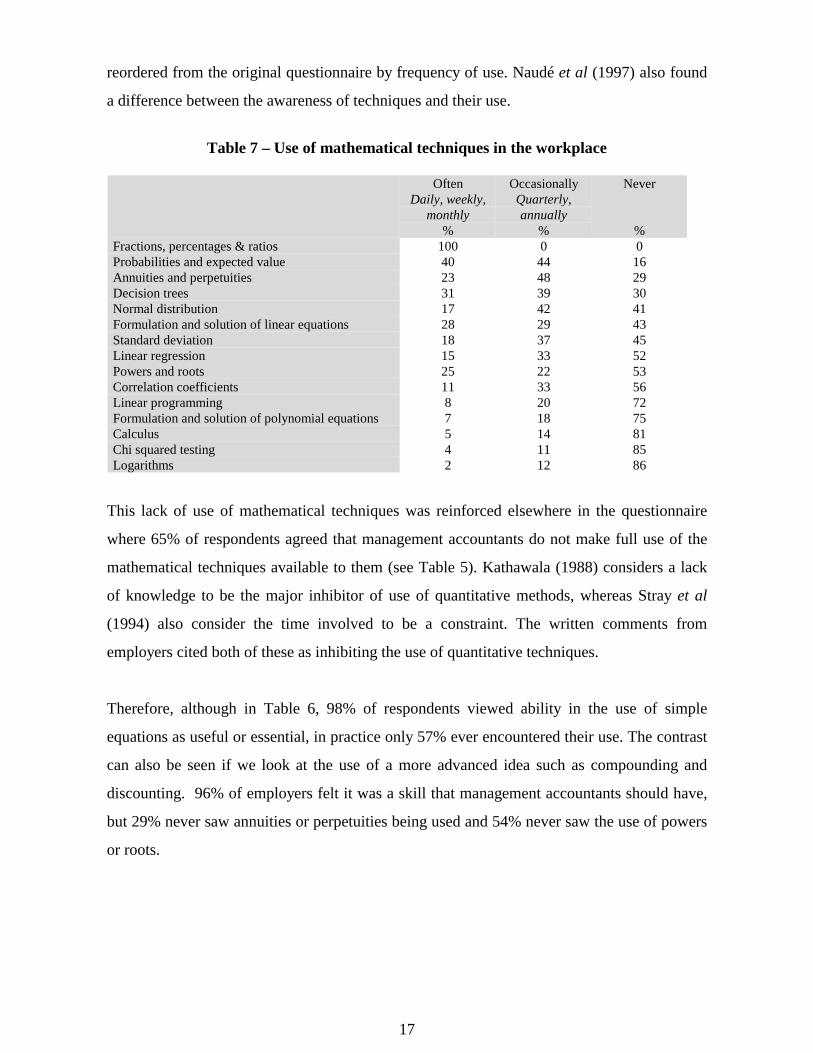

17

reordered from the original questionnaire by frequency of use. Naudé et al (1997) also found

a difference between the awareness of techniques and their use.

Table 7 – Use of mathematical techniques in the workplace

OftenDaily, weekly,

monthly%

OccasionallyQuarterly,annually

%

Never

%Fractions, percentages & ratios 100 0 0Probabilities and expected value 40 44 16Annuities and perpetuities 23 48 29Decision trees 31 39 30Normal distribution 17 42 41Formulation and solution of linear equations 28 29 43Standard deviation 18 37 45Linear regression 15 33 52Powers and roots 25 22 53Correlation coefficients 11 33 56Linear programming 8 20 72Formulation and solution of polynomial equations 7 18 75Calculus 5 14 81Chi squared testing 4 11 85Logarithms 2 12 86

This lack of use of mathematical techniques was reinforced elsewhere in the questionnaire

where 65% of respondents agreed that management accountants do not make full use of the

mathematical techniques available to them (see Table 5). Kathawala (1988) considers a lack

of knowledge to be the major inhibitor of use of quantitative methods, whereas Stray et al

(1994) also consider the time involved to be a constraint. The written comments from

employers cited both of these as inhibiting the use of quantitative techniques.

Therefore, although in Table 6, 98% of respondents viewed ability in the use of simple

equations as useful or essential, in practice only 57% ever encountered their use. The contrast

can also be seen if we look at the use of a more advanced idea such as compounding and

discounting. 96% of employers felt it was a skill that management accountants should have,

but 29% never saw annuities or perpetuities being used and 54% never saw the use of powers

or roots.

18

4.1.3 Specialist skills

At first sight the findings of the survey appear to indicate that accountants rarely use

quantitative skills but expect students to acquire them as a ‘right of passage’. However as a

number of respondents stressed, knowledge of and ability in applying quantitative techniques

is a crucial and differentiating skill for accountants. This skill helps to maintain the

accountant’s expert and positional power and provides them with an important underpinning

for wherever their accountancy career takes them. As Hoecht and Willet (1998) suggest

competence and knowledge can be assessed, certified and credentialled. It is at this point that

a professional group can score in both economic and social order, if it manages to determine

the nature of the knowledge to be examined, and gains the offered recognition from this state.

This was emphasized in the comments from one employer, who was not a qualified

accountant:

“We are a small company and our knowledge of management accountantsis very little. Our trainee is the only one in our organisation to try for thisqualification. However, we are impressed by CIMA and although we donot use quantitative techniques, we fully expect our trainee to qualify andbe able to use mathematical skills to improve our organisation’seffectiveness.”

There is the expectation that accountants, as specialists, are able to do more than their day to

day tasks in the organisation when necessary. A thorough grounding in the range of

quantitative techniques available ensures that they have the expertise to identify what

techniques to use in a given situation. As one employer put it:

“On a day to day basis, the role of the management accountant does notrequire a high level of mathematical skill. However, I have found thatperiodically, a problem will arise where an awareness and ability tosupply a particular mathematical tool has proved essential. We shouldcontinue to educate CIMA students to a high standard in maths to ensurethey are equipped to do the job.”

So, although many mathematical skills are not required on a day to day basis, the knowledge

of the range of quantitative techniques available to help a business is still seen by the

Employers as being a crucial part of the role of a management accountant. It can also be

19

viewed as a way of convincing the public that claims for professional privilege are based on

technical expertise, (Neu, 1991).

4.1.4 New technology

New technology also appears to have played its part in reducing the day to day use of

mathematical techniques. Often the necessary calculations are being carried out by software

packages and the accountant is being presented with the analysed data. This view was

reinforced by the fact that 53% of respondents agreed that new technology had dramatically

reduced the mathematical skills needed by management accountants. But as a number of

respondents stressed in their written comments, the ability to interpret and question results

can only really come from a fundamental understanding of how those results have been

generated. As one employer commented:

“Technology does away with much of the detailed knowledge of how to docalculations, but it is essential to understand what you are doing, why andhow to interpret the results.”

Within the accountancy profession, there has been a steady move away from the detailed

technical side of the profession and towards the more strategic, business orientated approach.

This has been partly in response to the advent of new information technology making a

number of previously difficult calculations straightforward, but also due to a repositioning of

the accountant as a ‘business adviser’ rather than a purely technical accounting and finance

expert, (see Cooper, 1996; Francis et al, 1998 and Kaplan, 1995).

In the view of the majority of the Employers, the modern management accountant need to be

multi-skilled with a good knowledge of the range of quantitative techniques available, but

also with strong business and communication skills to support the technical skills.

4.2 Lecturers’ questionnaire

From the Lecturers attending the CIMA Lecturers conference a total of 36 completed

responses were received. The majority of the respondents were involved in teaching the

quantitative papers for the CIMA examinations, which are Cost Accounting and Quantitative

20

Methods (CQM) at Stage 1, Operational Cost Accounting (OCA) and Management Science

Applications (MSA) at Stage 2, Management Accounting Applications (MAA) at Stage 3 and

Strategic Financial Management (SFM) and Management Accounting Control Systems

(MCS) at Stage 4.

A detailed breakdown of the papers taught is shown in Table 8 below. Quantitative papers are

highlighted in bold

Table 8 – Subject specialisms of Lecturers (quantitative subjects shown in bold)% % % %

FAF 22 CQM 36 ECN 11 BSN 22 FNA 8 OCA 39 MSA 36 LAW 6 FRP 8 MAA 42 OMD 17 TAX 3 SFM 33 SMM 25 IFM 6 MCS 25

The Lecturers came from a mixture of public and private sector colleges (Table 9) and were

predominantly of Senior Lecturers or Director status (Table 10).

Table 9 – Type of organisation for which Lecturers teach

%

Public sector 51Private sector 37Freelance 12

Table 10 – Position of Lecturers within their organisations

% Director 40 Principal/Senior Lecturer 31 Lecturer 26 Professor 3

The lecturers were asked a similar range of questions to the Employers about the role of

quantitative techniques, looking at what skills they expect of an accountant and how they

believe the role has changed with the advent of new technology. A copy of the full results

from the questionnaire is included in Appendix C. They were also asked to add written

comments relating to any of these areas. Of the 36 lecturers who responded, 19 added written

comments to their questionnaire, a content analysis of which is included in Appendix D.

21

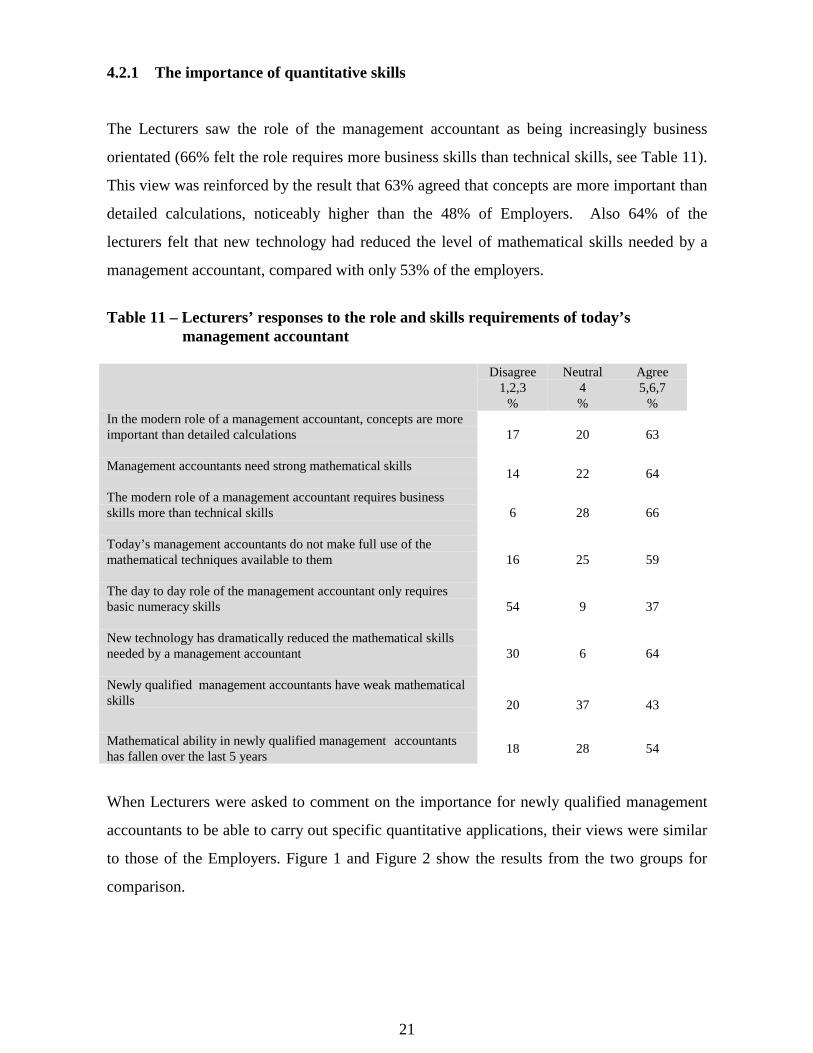

4.2.1 The importance of quantitative skills

The Lecturers saw the role of the management accountant as being increasingly business

orientated (66% felt the role requires more business skills than technical skills, see Table 11).

This view was reinforced by the result that 63% agreed that concepts are more important than

detailed calculations, noticeably higher than the 48% of Employers. Also 64% of the

lecturers felt that new technology had reduced the level of mathematical skills needed by a

management accountant, compared with only 53% of the employers.

Table 11 – Lecturers’ responses to the role and skills requirements of today’smanagement accountant

Disagree1,2,3

%

Neutral4%

Agree5,6,7

%In the modern role of a management accountant, concepts are moreimportant than detailed calculations 17 20 63

Management accountants need strong mathematical skills 14 22 64

The modern role of a management accountant requires businessskills more than technical skills 6 28 66

Today’s management accountants do not make full use of themathematical techniques available to them 16 25 59

The day to day role of the management accountant only requiresbasic numeracy skills 54 9 37

New technology has dramatically reduced the mathematical skillsneeded by a management accountant 30 6 64

Newly qualified management accountants have weak mathematicalskills 20 37 43

Mathematical ability in newly qualified management accountantshas fallen over the last 5 years 18 28 54

When Lecturers were asked to comment on the importance for newly qualified management

accountants to be able to carry out specific quantitative applications, their views were similar

to those of the Employers. Figure 1 and Figure 2 show the results from the two groups for

comparison.

22

Figure 1: Employers responses to the importance of ability in quantitative areas for newly qualified managment accountants

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Analysing data looking for trends and patterns

Compounding and discounting

Selection of appropriate sample size

Solution of problems with constraints

Formulating and solving problems as simple equations

Calculating the possible range of, and expected oraverage results from projects

Evaluating the reliability of results forecast by a modelcompared to actual results

Estimating straight line relationships between variables

Determining maximum and minimum points of functions

Formulating and solving problems as more complexequations

Percentage of respondents

EssentialUsefulUnimportant

Figure 2: Lecturers responses to the importance of ability in quantitative areas for newly qualified managment accountants

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Analysing data looking for trends and patterns

Compounding and discounting

Selection of appropriate sample size

Solution of problems with constraints

Formulating and solving problems as simple equations

Calculating the possible range of, and expected oraverage results from projects

Evaluating the reliability of results forecast by a modelcompared to actual results

Estimating straight line relationships between variables

Determining maximum and minimum points of functions

Formulating and solving problems as more complexequations

Percentage of respondents

EssentialUsefulUnimportant

23

4.2.2 Use of quantitative techniques

The Lecturers were asked to indicate what level of ability a management accountant shouldpossess in applying the mathematical techniques as shown in Table 12.

Table 12 – Lecturers’ opinion of the level of ability a management accountant should

possess Minimal ability

1 & 2%

Moderateability 3,4 & 5

%

High ability6 & 7

%Fractions, percentages & ratios 0 3 97Powers and roots 6 50 44Annuities and perpetuities 3 37 60Formulation and solution of linear equations 6 64 30Formulation and solution of polynomial equations 42 44 14Calculus 42 46 12Logarithms 58 36 6Probabilities and expected value 6 51 43Decision trees 6 56 38Linear regression 3 58 39Correlation coefficients 11 54 35Standard deviation 6 58 36Normal distribution 6 64 30Chi squared testing 22 52 26Linear programming 11 56 33

Figures 3 and 4 show the comparison of these results against the actual use of these

techniques in practice as indicated by the Employers. Here there can be seen to be

considerable mis-match between the techniques that Lecturers view as requiring a high level

of ability in, and the frequency of use of these techniques in practice. For example, Chi-

square testing is never used by 85% of Employers, whereas 78% of Lecturers felt that a

moderate or high ability in ability in applying the technique was necessary. However these

views are not incompatible as the Employers indicated that ability in quantitative skills is

important, even if these skills are rarely, if ever, called upon in practice.

4.2.3 Specialist skills

The Lecturers’ views appeared to be much more polarized than those of the Employers’ on

what mathematical skills are necessary for accountants. A number of Lecturers believed that

the mathematical content was much too high and only the skills used regularly on the job

should be taught, whereas others felt that the students should be trained to a very high level of

technical competence. The Employers generally agreed that knowledge of all available

24

Figure 3: Within your organisation how often do you see the following mathematical techniques being employed?

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Fractions, percentages andratios

Probabilities and expectedvalue

Annuities and perpetuities

Decision trees

Normal distribution

Formulation and solution oflinear equations

Standard deviation

Linear regression

Powers and roots

Correlation coefficients

Linear programming

Formulation and solution ofpolynomial equations

Calculus

Chi square testing

Logarithms

Percentage of respondents

OftenOccasionallyNever

Figure 4: Lecturers responses to what level of ability should a management accountant possess?

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Fractions, percentages andratios

Probabilities and expectedvalue

Annuities and perpetuities

Decision trees

Normal distribution

Formulation and solution oflinear equations

Standard deviation

Linear regression

Powers and roots

Correlation coefficients

Linear programming

Formulation and solution ofpolynomial equations

Calculus

Chi square testing

Logarithms

Percentage of respondents

High ability

Moderate ability

Minimal ability

25

techniques was an important differentiator for the profession and therefore supported a high

content of quantitative techniques within CIMA’s examination syllabus. Tyrrall and Wrighton

(1997), Benke (1996) and Siegel and Kulesza (1996) have all noted the differences in

expectations between academics and practitioners.

As one Lecturer commented:

“Students simply need to have the skills required to meet the needs ofwork.”

Whereas another summarised the opposite view that:

“Mathematical skills are generic skills which provide a framework for competentprofessional practice.”

4.2.4 New Technology

Lecturers appeared to view new technology as having a greater impact on the role of

management accountants than did the Employers. Of the 19 Lecturers who commented, 5

cited the need for more training of software skills within the student-training period.

Interestingly this compares with only 9 out of the 107 employers who noted the same need.

5. Coverage of quantitative techniques in accountancy programmes

The syllabus content for the Chartered Institutes of England and Wales, Scotland, Australia,

New Zealand, Canada, South Africa and Ireland were reviewed alongside the Chartered

Institute of Management Accountants (CIMA) and the Association of Charted Certified

Accountants (ACCA).

The inclusion of basic statistical and mathematical techniques, such as linear regression and

decision trees varied depending on the entry route into the profession. Bodies such as CIMA

and ACCA, which admit a large number of non-graduates directly into student membership,

had comprehensive coverage of these areas. Those bodies where the majority of students must

have taken a specific university programme before entering for the professional examinations,

such as Canada, Australia and New Zealand did not cover a number of these basic techniques

explicitly.

26

With more advanced quantitative techniques CIMA had the most comprehensive coverage,

reflecting its specialism within the field of management accounting. Apart from these

differences at the two extremes of the spectrum of techniques, the core of quantitative

techniques considered within our questionnaire were included by all the bodies.

None of the bodies appeared to formally examine the hands-on use of IT, although this would

be expected to form part of the professional experience requirements necessary to gain

membership.

6. Conclusions

The findings of this survey indicate that accountants rarely use the more advanced

quantitative techniques, but expect students to study them as a ‘right of passage’. We have

found that there is an expectation that management accountants have a knowledge of and

ability in applying quantitative techniques. This was seen as a crucial and differentiating skill

for accountants. This skill is critical in maintaining the accountant’s expert and positional

power and provides them with an important underpinning for wherever their accountancy

career takes them.

There is the expectation that accountants, as specialists, are able, when necessary, to do more

than their day to day tasks in the organisation. A thorough grounding in the range of

quantitative techniques available ensures that they have the expertise to identify what

techniques to use in a given situation. Quantitative skills in themselves are often not required

on a day to day basis, because the calculations are being carried out by software packages and

the accountant is being presented with the analysed data. But, as a number of respondents

stressed in their written comments, the ability to interpret and question results can only really

come from a fundamental understanding of how those results have been generated. As one

employer commented:

27

“Technology does away with much of the detailed knowledge of how to docalculations, but it is essential to understand what you are doing, why andhow to interpret the results.”

Within the accountancy profession, there has been a steady move away from the detailed

technical side of the profession and towards the more strategic, business orientated approach.

However a review of the syllabus content of some of the major international accounting

bodies showed that there remains a large body of core quantitative techniques within them.

This paper has examined the dilemma faced by the professional accountancy bodies. Are we

training accountants in the use of outdated and redundant computational techniques?

Conversely, can accountants fully understand and interpret the results of calculations if they

have never studied the process from first principles? By removing them do we risk losing

potentially valuable differentiating skills in the drive to make accounting qualifications more

strategic and business orientated?

It is our view that accountants can not interpret the results of calculations if they have not

been trained at some point in the underlying principles. We also believe that a knowledge and

understanding of the range of quantitative techniques available to organisations is a powerful

differentiator for the accounting profession even if the occasions upon which accountants are

required to draw upon that knowledge are few and far between.

This ongoing research project has already directly fed into CIMA’s Syllabus development. A

second questionnaire is planned to those who expressed a willingness to participate further, to

explore in more depth the way that quantitative techniques are applied and also to identify

areas where they could be applied. Additional research could further explore the differing

expectations of academics, accountants and student accountants, in terms of what

professional qualification should represent with respect to quantitative skills.

28

7. References

7.1 Articles, reports and monographs

Alpander, G.G., (1976) ‘Use of Quantitative Methods in International Operations by U.S.

Overseas Executives’, Management International Review, Vol. 16, pp. 71-77

Bain, S.G., (1992) ‘The Future of Management Education’, Journal of the Operational

Research Society, Vol. 43 No. 6, pp. 557-561.

Benke, R.L., Jr., (1996) ‘150-Hour Programs and the Preparation of Management

Accountants’, Journal of Accounting Education, Vol. 14 No. 2, pp. 187-192.

Bromwich, M., & Bhimani, A., (1989) Management Accounting: Evolution Not Revolution,

CIMA, London.

Borsting, J.R., Cook, T.M., King, W.R., Rardin, R.L., & Tuggle, F.D., (1988) ‘A Model for a

first MBA Course in Management Science / Operations Research’, Interfaces, Vol. 18 No. 5,

pp. 72-80.

Carver, M.R., and King, T.E., (1986) ‘Attitudes of Accounting Practitioners Towards

Accounting Faculty and Accounting Education’, Journal of Accounting Education, Spring,

pp. 31-43.

CIMA, (1994) Standards of Competence in Management Accounting, Version 2.

Coccari, R.L., (1989) ‘How Quantitative Business Techniques are Being Used’, Business

Horizons, July/August, pp. 70-74.

Cooper, R., (1996) ‘Lookout, Management Accountants’, Management Accounting, June, pp.

35-41

29

Coppinger, R.J., & Epley, E.S., (1972) ‘The Non-Use of Advanced Mathematical

Techniques’, Managerial Planning, Vol. 20 May/June, pp. 12-15.

Dhebar, A., (1993) ‘Managing the Quality of Quantitative Analysis’, Sloan Management

Review, Winter, pp. 69-75.

Drury, C., Braund, S., Osbourne, P., & Tayles, M., (1993) A Survey of Management

Accounting Practices in UK Manufacturing Companies, ACCA Research Report.

Earl, M.J., and Hopwood, A.G., (1981) ‘From Management Information to Information

Management’, In Lucus, M.C., et al. (eds.) The Information Systems Environment, North

Holland, Amsterdam.

Easton, G., Roberts, H.V., & Tiao, G.C., (1988) ‘Making Statistics More Effective in Schools

and Business’, Journal of Business & Economic Statistics, Vol. 6 No. 2, pp. 247-260.

Francis, G.A.J., Hinton, C.M., Holloway, J., & Mayle, D., (1998) ‘A Role for Management

Accountants in Best Practice Benchmarking?’ Open University Business School Working

Paper, 98/2.

Green, T.B., Newson, W.B., & Jones, S.R., (1977) ‘A Survey of the Application of

Quantitative Techniques to Production/Operations Management in Large Corporations’,

Academy of Management Journal, Vol. 20 No. 4, pp. 669-676.

Hanno, D.M., & Turner, R.M., (1996) ‘The Changing Face of Accounting Education’,

Massachusetts CPA Review, Vol. 70 No. 1, pp. 8-12.

Hartman, B.R., & Ruhl, J.M., (1996) ‘What Corporate America Wants in Entry-Level

Accountants: Some Methodological Concerns’, Journal of Accounting Education, Vol. 14

No. 1, pp. 1-16.

30

Hoecht, A., & Willett, C., (1998) ‘The Price of Entry: Social Closure and Rites of Passage in

the UK Auditing Profession’ British Accounting Association Annual Conference, Manchester

April 1998.

Johnson, H.T., & Kaplan, R.S., (1987) Relevance Lost: The Rise and Fall of Management

accounting, Harvard Business School Press, Boston.

Juritz, J.M., Money, A.H., & Affleck-Graves, J., (1988) ‘A Survey of the Statistical Methods

Used in Business and Industry in South Africa’, South African Journal of Higher Education,

Vol. 2 No. 1, pp. 57-64.

Kaplan, R.S., (1995) 'New Roles for Management Accountants', Journal of Cost

Management, Fall, pp. 6-16.

Kathawala, Y., (1988) ‘Applications of Quantitative Techniques in Large and Small

Organizations in the United States: An empirical Analysis’, Journal of the Operational

Research Society, Vol. 39, No. 11, pp. 981-989.

Lewis, R., & Kaye, G.R., (with Dunn, J., Francis, G.A.J., Gadella, J., Lucas, U., &

Richardson, D.O.,) (1997) ‘Proposal for the Development of a Common Syllabus’, Report to

the Chartered Accounting Group Executive (CAGE).

Mock, A., (1996) ‘How Good do we Need to be at Sums?’, Management Accounting,

January, pp. 30-31.

Naudé, P., Band, D., Stray, S., & Wegner, T., (1997) ‘An International Comparison of

Management’s Use of Quantitative Techniques, and the Implications for MBA Teaching’,

Management Learning, Vol. 28 No. 2, pp. 217-233.

Neu, D., (1991) ‘Trust, Impression Management and the Public Accounting Profession’,

Critical Perspectives on Accounting, Vol 2, pp. 295-313.

31

Pike, R.H., and Neale, W., (1993) Corporate Finance and Investment: Decisions and

Strategies, Prentice Hall.

Pike, R.H., and Wolfe, M.B., (1988) Capital Budgeting in the 1990’s, CIMA, London.

Robson, C., (1993) Real World Research: A Resource for Social Scientists and Practitioner-

Researchers, Blackwell, Oxford.

Rose, E.L., Machak, J.A. & Spivey, W.A., (1988) ‘A Survey of the Teaching of Statistics in

M.B.A. Programs’, Journal of Business & Economic Statistics, Vol. 6 No. 2, pp. 273-282.

Sangster, A., (1993) ‘Capital Investment Appraisal Techniques: A Survey of Current Usage’,

Journal of Business Finance and Accounting, April.

Scapens, R.W., (1991) Management Accounting: A Review of Recent Developments,

MacMillan, London.

Seigel, G., & Kulesza, B., (1996) ‘The Coming Changes in Management Accounting

Education’, Management Accounting (USA), January, pp. 43-47.

Simons, K. & Higgins, M., (1993) ‘An Examination of Practitioners’ and Academicians’

Views on the Content of the Accounting Curriculum’, Accounting Educators’ Journal, Vol. 5

No. 2, pp. 24-34.

Spencer, C., & Francis, G.A.J., (1998a) ‘Quantitative Techniques: Do we practice what we

preach?’, Qualification News, 1998(1).

Spencer, C., & Francis, G.A.J. (1998b) ‘The Use of Quantitative Techniques By Accountants

in Practice and Training: An Empirical Study’ British Accounting Association National

Conference, Manchester April 98.

Stray, S., Naudé, P., Wegner, T., (1994) ‘Statistics in Management education’ British Journal

of Management, Vol. 5, pp. 73-82.

32

Tyrrall D.E., & Wrighton S., (1997) ‘Whither Accounting Education?’, Management

Accounting, November, p. 67.

Ward, M., (1997) ‘Fatal Addition’, New Scientist, 16 August, pp. 13.

Wegner, T., (1983) ‘A Survey of Quantitative Methods in South African Management’, South

African Journal of Business Management, Vol. 14 No. 3, pp. 120-124.

7.2 Syllabuses

Institute of Chartered Accountants in Australia. Education handbook 1996: professional year

programme.

Institute of Chartered Accountants in Ireland. Syllabus: professional examination two and

three, for examination 1996.

Institute of Chartered Accountants in Ireland. Syllabus: final admitting examination, for

examination 1996.

Institute of Chartered Accountants in New Zealand. Admission to the College of Chartered

Accountants: information update, ICANZ.

Institute of Chartered Accountants of England and Wales. Examinations conduct and

syllabuses: intermediate, until May 1996; final, until July 1997.

Institute of Chartered Accountants of Scotland. Syllabus 1996/97.

New Zealand Society of Chartered Accountants. Admissions policy. NZCA Education

Committee, 1994.

New Zealand Society of Chartered Accountants. The body of knowledge, NZCA Education

Committee, January 1992.

33

New Zealand Society of Chartered Accountants. Log book.

The Provincial Institutes of Chartered Accountants in Canada and Bermuda Syllabus for entry

to the chartered accountancy profession, issued 1995 effective for the 1996 Uniform Final

Examination.

Public Accountants and Auditors Board (South Africa). Manual of information for the

guidance of registered accountants and auditors, 1996.

Public Accountants and Auditors Board (South Africa). The education requirements of the

Public Accountants and Auditors Board, Johannesburg 1993.

34

Appendix A:

This study 1998 Alpander 1976 Green etal 1977

Kathawala 1988

Coccari1989

Drury etal 1993

Wegner1983 1

Forrester1984 2

Juritz etal 1988 3

Wisniewski 1990 4

Østergaard1993 5

Naudé et al 1997 6

n=296 n=36 n=75 (total, breakdown between groups notgiven)

n=78 n=226 n=900? N=288 n=164 n=65 n=639 n=408 n=172

Technique

Employers UK

LecturersUK

Expatriates in DCs(USA)

Expatriates in DCs(Not USA)

Expatriates in LDCs(USA)

Expatriates in LDCs(Not USA)

USA USA USA UK SouthAfrica

UK SouthAfrica

EU Denmark UK SouthAfrica

NewZealand

Fractions, percentages andratios

100 100

Index numbers 20 22 15Powers and roots 47 94Annuities and perpetuities 71 97Formulation and solution oflinear equations

57 94

Break-even analysis 60 35 65 20 91 50Inventory control/analysis 78 68 67.6 67 27 30 45 63Formulation and solution ofpolynominal equations

25 58

Learning curves 64Calculus 19 58Logarithms 14 42Probabilities and expected value 84 94 72 51 8 10 11Simulation techniques 50 40 40 15 68 84 29.3 32 16 20 38 65Bayesian statistics 26 36Game theory 23 31Markov chain 22 24Queuing theory 30 22 30 8 39 46 17.6Decision trees 70 94 9 3 77Linear regression 48 97Forecasting 96 54 32 60 29 31 20Moving averages 38 44Econometric models 15 10 15 30Multiple regression techniques 36Time series analysis 88Correlation coefficients 44 89 86 87 54 16 30 37 35 13 25 11Standard deviation 55 94Basic statistics and graphs 52 25 80 65 75Analysis of variance 72 81Normal distribution 59 84Sampling 85 89 20Quality control 91.2 32 40 25 54 7 14 16Hypothesis testing 4 5 7Confidence intervals 7 13 9

35

Chi square testing 15 78 48 48Contingency tables 12 12 11Nonparametric tests 3 4 2

36

Appendix A continued

This study 1998 Alpander 1976 Green etal 1977

Kathawala 1988

Coccari1989

Drury etal 1993

Wegner1983 1

Forrester1984 2

Juritz etal 1988 3

Wisniewski 1990 4

Østergaard1993 5

Naudé et al 1997 6

n=296 n=36 n=75 (total, breakdown between groups notgiven)

n=78 n=226 n=900? N=288 n=164 n=65 n=639 n=408 n=172

Technique

Employers UK

LecturersUK

Expatriates in DCs(USA)

Expatriates in DCs(Not USA)

Expatriates in LDCs(USA)

Expatriates in LDCs(Not USA)

USA USA USA UK SouthAfrica

UK SouthAfrica

EU Denmark UK SouthAfrica

NewZealand

Linear programming 28 89 40 15 83 64 23.5 37 12 20 20 29Non-linear programming 37 45Venture analysis 35 24 32 20Dynamic programming 26 10 24 8 39Marginal analysis 20 15 20 5Inferential methods 33 28 70 17Network models/analysis 83 51 8.7 76 28 20 18 29Production and schedulingmodels

70.6

Maintenance and repair models 20.5Goal programming 29 34Factor analysis 28 51Discriminant analysis 27 34Canonical analysis 11 18Experimental design 60 0 40 44 1 1 2Cluster analysis 36Exponential smoothing 64Integer programming 29Multi-dimensional scaling 33PERT/CPM 79Transportation model 39Data collection and presentation 73 73 58Sample survey design 13 13 14Multivariate models 9 4 3

Note 1 Based on a 5 point scale of no-little-moderate-frequent-extensive use. Reflects percentage replying to frequent or extensive.Note 2 Based on a 4 point scale of none-peripheral-much-extensive. Reflects percentage replying to much or essential. Quoted in Naudé et al 1997.Note 3 Percentage indicating routine usage.Note 4 Percentage indicating high frequency of use. Quoted in Naudé et al. 1997.Note 5 Based on a 4 point scale of not available-never-occasional-frequent. Reflects percentage replying occasional or frequent. Quoted in Naudé et al 1997.Note 6 Based on a 5 point scale of no-little-moderate-frequent-extensive use. Reflects percentage replying to frequent or extensive.

37

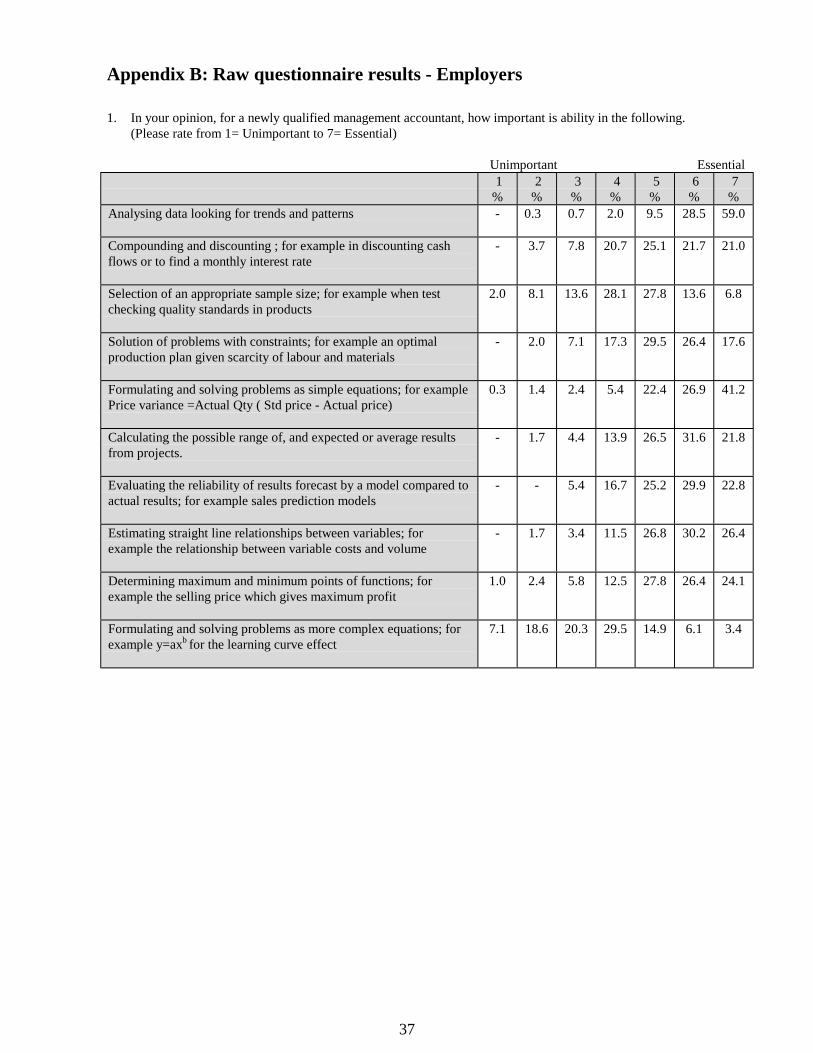

Appendix B: Raw questionnaire results - Employers

1. In your opinion, for a newly qualified management accountant, how important is ability in the following.(Please rate from 1= Unimportant to 7= Essential)

Unimportant Essential

1 %

2 %

3 %

4 %

5 %

6 %

7 %

Analysing data looking for trends and patterns

- 0.3 0.7 2.0 9.5 28.5 59.0

Compounding and discounting ; for example in discounting cashflows or to find a monthly interest rate

- 3.7 7.8 20.7 25.1 21.7 21.0

Selection of an appropriate sample size; for example when testchecking quality standards in products

2.0 8.1 13.6 28.1 27.8 13.6 6.8

Solution of problems with constraints; for example an optimalproduction plan given scarcity of labour and materials

- 2.0 7.1 17.3 29.5 26.4 17.6

Formulating and solving problems as simple equations; for examplePrice variance =Actual Qty ( Std price - Actual price)

0.3 1.4 2.4 5.4 22.4 26.9 41.2

Calculating the possible range of, and expected or average resultsfrom projects.

- 1.7 4.4 13.9 26.5 31.6 21.8

Evaluating the reliability of results forecast by a model compared toactual results; for example sales prediction models

- - 5.4 16.7 25.2 29.9 22.8

Estimating straight line relationships between variables; forexample the relationship between variable costs and volume

- 1.7 3.4 11.5 26.8 30.2 26.4

Determining maximum and minimum points of functions; forexample the selling price which gives maximum profit

1.0 2.4 5.8 12.5 27.8 26.4 24.1

Formulating and solving problems as more complex equations; forexample y=axb for the learning curve effect

7.1 18.6 20.3 29.5 14.9 6.1 3.4

38

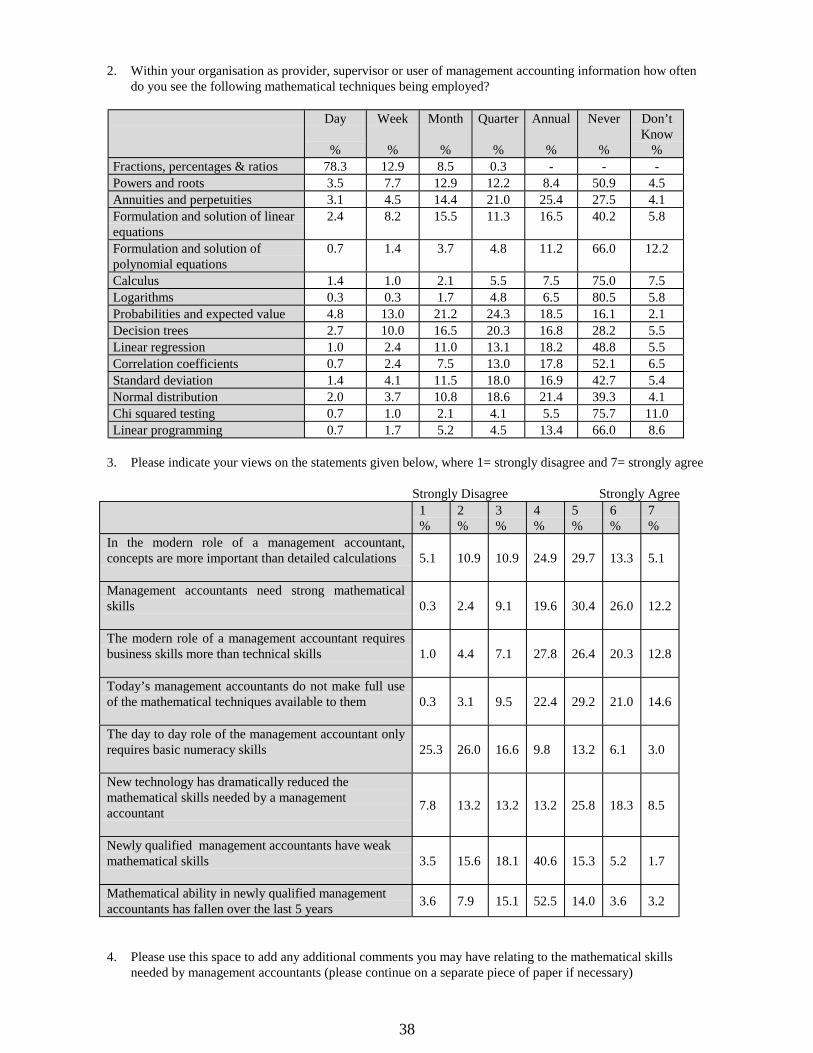

2. Within your organisation as provider, supervisor or user of management accounting information how oftendo you see the following mathematical techniques being employed?

Day

%

Week

%

Month

%

Quarter

%

Annual

%

Never

%

Don’tKnow

%Fractions, percentages & ratios 78.3 12.9 8.5 0.3 - - -Powers and roots 3.5 7.7 12.9 12.2 8.4 50.9 4.5Annuities and perpetuities 3.1 4.5 14.4 21.0 25.4 27.5 4.1Formulation and solution of linearequations

2.4 8.2 15.5 11.3 16.5 40.2 5.8

Formulation and solution ofpolynomial equations

0.7 1.4 3.7 4.8 11.2 66.0 12.2

Calculus 1.4 1.0 2.1 5.5 7.5 75.0 7.5Logarithms 0.3 0.3 1.7 4.8 6.5 80.5 5.8Probabilities and expected value 4.8 13.0 21.2 24.3 18.5 16.1 2.1Decision trees 2.7 10.0 16.5 20.3 16.8 28.2 5.5Linear regression 1.0 2.4 11.0 13.1 18.2 48.8 5.5Correlation coefficients 0.7 2.4 7.5 13.0 17.8 52.1 6.5Standard deviation 1.4 4.1 11.5 18.0 16.9 42.7 5.4Normal distribution 2.0 3.7 10.8 18.6 21.4 39.3 4.1Chi squared testing 0.7 1.0 2.1 4.1 5.5 75.7 11.0Linear programming 0.7 1.7 5.2 4.5 13.4 66.0 8.6

3. Please indicate your views on the statements given below, where 1= strongly disagree and 7= strongly agree

Strongly Disagree Strongly Agree1%

2%

3%

4%

5%

6%

7%

In the modern role of a management accountant,concepts are more important than detailed calculations 5.1 10.9 10.9 24.9 29.7 13.3 5.1

Management accountants need strong mathematicalskills 0.3 2.4 9.1 19.6 30.4 26.0 12.2

The modern role of a management accountant requiresbusiness skills more than technical skills 1.0 4.4 7.1 27.8 26.4 20.3 12.8

Today’s management accountants do not make full useof the mathematical techniques available to them 0.3 3.1 9.5 22.4 29.2 21.0 14.6

The day to day role of the management accountant onlyrequires basic numeracy skills 25.3 26.0 16.6 9.8 13.2 6.1 3.0

New technology has dramatically reduced themathematical skills needed by a managementaccountant 7.8 13.2 13.2 13.2 25.8 18.3 8.5

Newly qualified management accountants have weakmathematical skills 3.5 15.6 18.1 40.6 15.3 5.2 1.7

Mathematical ability in newly qualified managementaccountants has fallen over the last 5 years 3.6 7.9 15.1 52.5 14.0 3.6 3.2

4. Please use this space to add any additional comments you may have relating to the mathematical skills

needed by management accountants (please continue on a separate piece of paper if necessary)

39

See Appendix D for content analysis of written comments.

5. Within which business sector do you work? % %

Public sector 18.1 Financial 6.5 Manufacturing 44.0 Service 13.0 Other....................................... 18.4 (please

specify) 6. Which best describes your position within your organisation?

% % Chief executive 1.7 Management accountant 9.6 Director 6.1 Financial analyst 1.4 Finance Director/Deputy 36.5 Assistant Financial accountant 0.7 Financial controller 23.9 Assistant management accountant 0.3 Manager 9.2 Consultant/Member in practice 1.4 Financial accountant 2.4 Academic 1.4 Other .......................................... 5.5

(please specify) 7. What is the size of the organisation that you work for? % Small (less than 100 employees) 9.9 Medium (100-2500 employees) 57.0 Large (over 2500 employees) 33.1

40

Appendix C: Raw questionnaire results - Lecturers

1. In your opinion, for a newly qualified management accountant, how important is ability in the following.(Please rate from 1= Unimportant to 7= Essential) Unimportant Essential

1%

2%

3%

4%

5%

6%

7%

Analysing data looking for trends and patterns 0 0 0 0 14 17 69

Compounding and discounting; for example in discounting cashflows or to find a monthly interest rate

0 6 0 6 14 22 52

Selection of an appropriate sample size; for example when testchecking quality standards in products

0 8 11 28 22 20 11

Solution of problems with constraints; for example an optimalproduction plan given scarcity of labour and materials

0 3 8 8 36 28 17

Formulating and solving problems as simple equations; for examplePrice variance =Actual Qty ( Std price – Actual price)

3 0 11 6 8 25 47

Calculating the possible range of, and expected or average resultsfrom projects

0 0 0 14 17 28 41

Evaluating the reliability of results forecast by a model compared toactual results; for example sales prediction models

0 3 3 6 37 28 23

Estimating straight line relationships between variables; for examplethe relationship between variable costs and volume

0 0 6 11 23 31 29

Determining maximum and minimum points of functions; forexample the selling price which gives maximum profit

5 11 17 17 11 25 14

Formulating and solving problems as more complex equations; forexample y=axb for the learning curve effect

17 17 14 11 16 19 6

41

2. In your opinion, what level of ability should a management accountant possess in applying the followingmathematical techniques. (Please rate from 1= None: no need to even be aware of the technique to 7=Expert: Complete understanding and ability to apply in a range of circumstances)

None Expert1%

2%

3%

4%

5%

6%

7%

Fractions, percentages & ratios 0 0 0 0 3 19 78Powers and roots 0 6 3 15 32 15 29Annuities and perpetuities 3 0 0 3 34 31 29Formulation and solution of linearequations

0 6 11 25 28 16 14

Formulation and solution ofpolynomial equations

17 25 19 17 8 8 6

Calculus 25 17 19 16 11 6 6Logarithms 33 25 22 6 8 0 6Probabilities and expected value 6 0 8 3 40 20 23Decision trees 6 0 6 6 44 33 5Linear regression 0 3 8 22 28 33 6Correlation coefficients 0 11 0 29 25 29 6Standard deviation 0 6 14 19 25 17 19Normal distribution 0 6 22 14 28 11 19Chi squared testing 8 14 33 8 11 20 6Linear programming 3 8 14 23 19 14 19

3. Please indicate your views on the statements given below ( Please rate from 1= strongly disagree and 7=

strongly agree)

Strongly StronglyDisagree Agree

1%

2%

3%

4%

5%

6%

7%

In the modern role of a management accountant, concepts are moreimportant than detailed calculations

0 6 11 20 23 11 29

Management accountants need strong mathematical skills 0 3 11 22 22 22 20

The modern role of a management accountant requires businessskills more than technical skills

0 3 3 28 26 20 20

Today’s management accountants do not make full use of themathematical techniques available to them

0 8 8 25 20 22 17

The day to day role of the management accountant only requiresbasic numeracy skills

23 25 6 9 20 11 6

New technology has dramatically reduced the mathematical skillsneeded by a management accountant

11 8 11 6 22 25 17

Newly qualified management accountants have weak mathematicalskills

6 11 3 37 23 11 9

Mathematical ability in newly qualified management accountantshas fallen over the last 5 years

6 9 3 28 26 14 14

42

4. Please use this space to add any additional comments you may have relating to the mathematical skillsneeded by management accountants (please continue on a separate piece of paper if necessary)

See Appendix D for content analysis of written comments.

5. Within which education sector do you work?

% % Public sector 51 Freelance 12

Private sector 37 Other....................................... 0(Please specify)

6. Which best describes your position within your organisation? % % Professor 3 Director 31 Principal/Senior lecturer 40 Consultant/Member in practice 0 Lecturer 26 Other .......................................... 0

(Please specify) 7. Which papers do you teach?

% % 5 % FAF 22 CQM 36 ECN 11 BSN 22

FNA 8 OCA 39 MSA 36 LAW 6

FRP 8 MAA 42 OMD 17 TAX 3

SFM 33 SMM 25 IFM 6 MCS 25

43

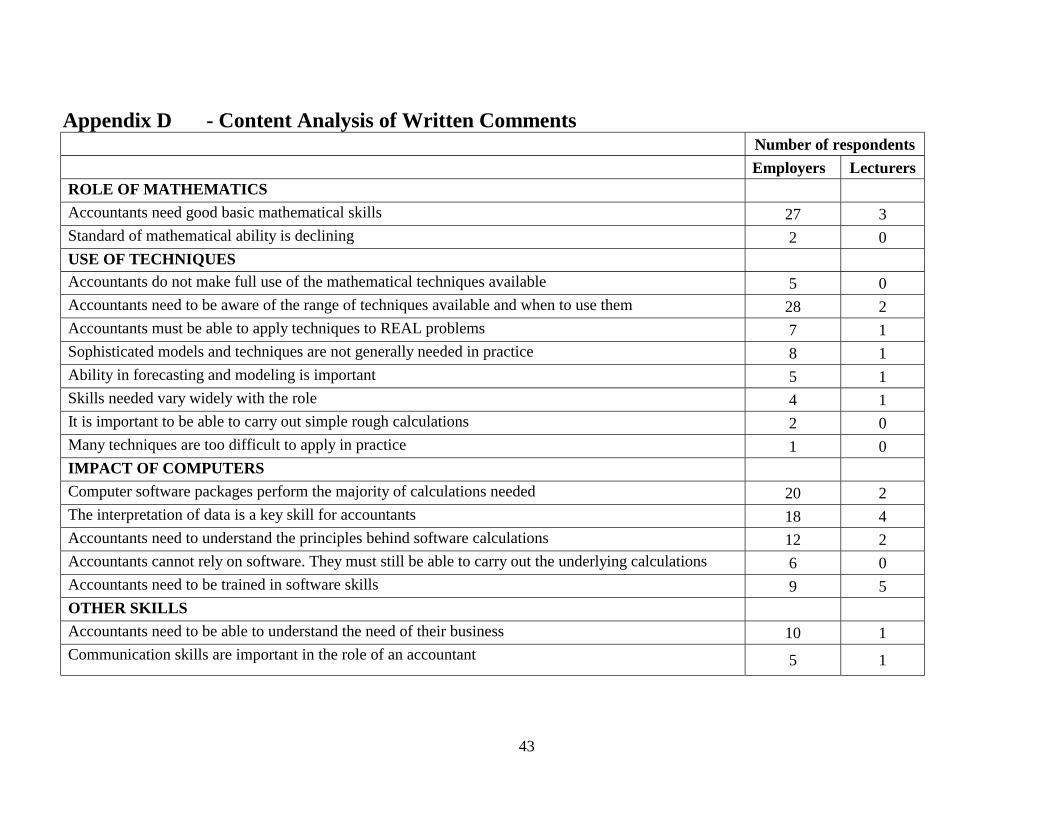

Appendix D - Content Analysis of Written CommentsNumber of respondentsEmployers Lecturers

ROLE OF MATHEMATICSAccountants need good basic mathematical skills 27 3Standard of mathematical ability is declining 2 0USE OF TECHNIQUESAccountants do not make full use of the mathematical techniques available 5 0Accountants need to be aware of the range of techniques available and when to use them 28 2Accountants must be able to apply techniques to REAL problems 7 1Sophisticated models and techniques are not generally needed in practice 8 1Ability in forecasting and modeling is important 5 1Skills needed vary widely with the role 4 1It is important to be able to carry out simple rough calculations 2 0Many techniques are too difficult to apply in practice 1 0IMPACT OF COMPUTERSComputer software packages perform the majority of calculations needed 20 2The interpretation of data is a key skill for accountants 18 4Accountants need to understand the principles behind software calculations 12 2Accountants cannot rely on software. They must still be able to carry out the underlying calculations 6 0Accountants need to be trained in software skills 9 5OTHER SKILLSAccountants need to be able to understand the need of their business 10 1Communication skills are important in the role of an accountant 5 1

Recommended