ipaa │2009 Private Capital Conference

Surviving and ProsperingIn Uncertain Times

January 14, 2009

Overview of ESS Funds Group

• Energy Special Situations Funds est. late 2005• Two institutional funds - $340+ million• Pursue middle-market, energy opportunities• 13 investments since inception• $150+ million uncommitted capital• Fund managers:

Jon Linker, Jeff Hewitt, Tim Sullivant

ESSF Strategy

• Invest in companies/projects - all energy sectors – Seek growth and value creation

• Sole manage small investments ($5 - $40 mm)• Partner large deals ($30 - $150 mm); 5 co’s.• Management track record and co-invest are key• Structure, incentives create common objectives• Equity-oriented - all financial structures possible

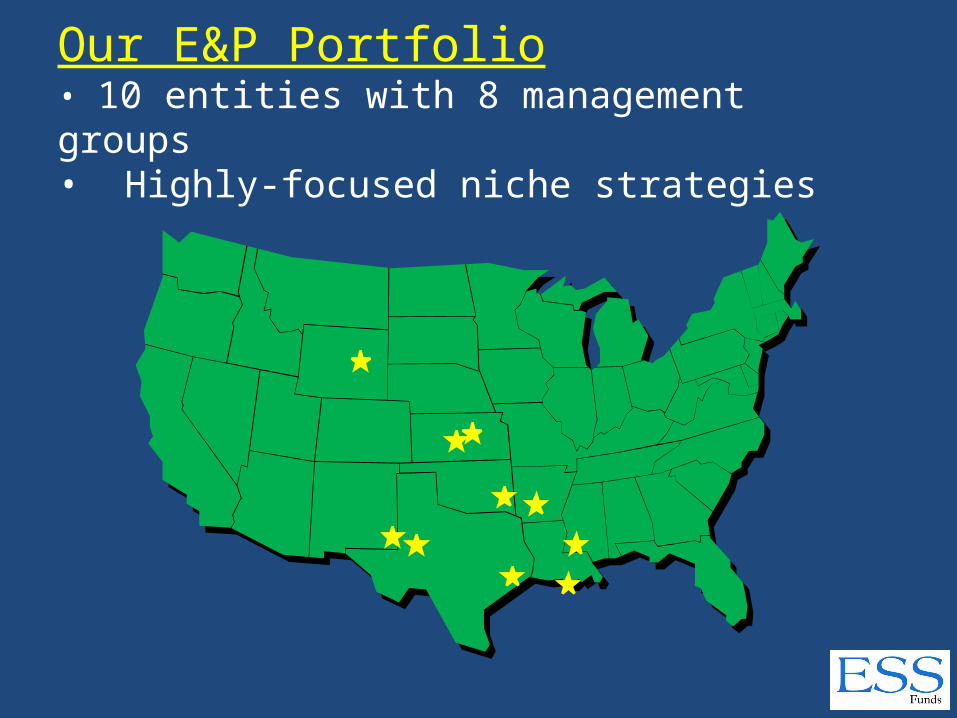

Our E&P Portfolio• 10 entities with 8 management groups• Highly-focused niche strategies

What Will 2009 Bring?

“Every new beginning starts from some other beginning’s end …”

Dan Wilson, Semisonic

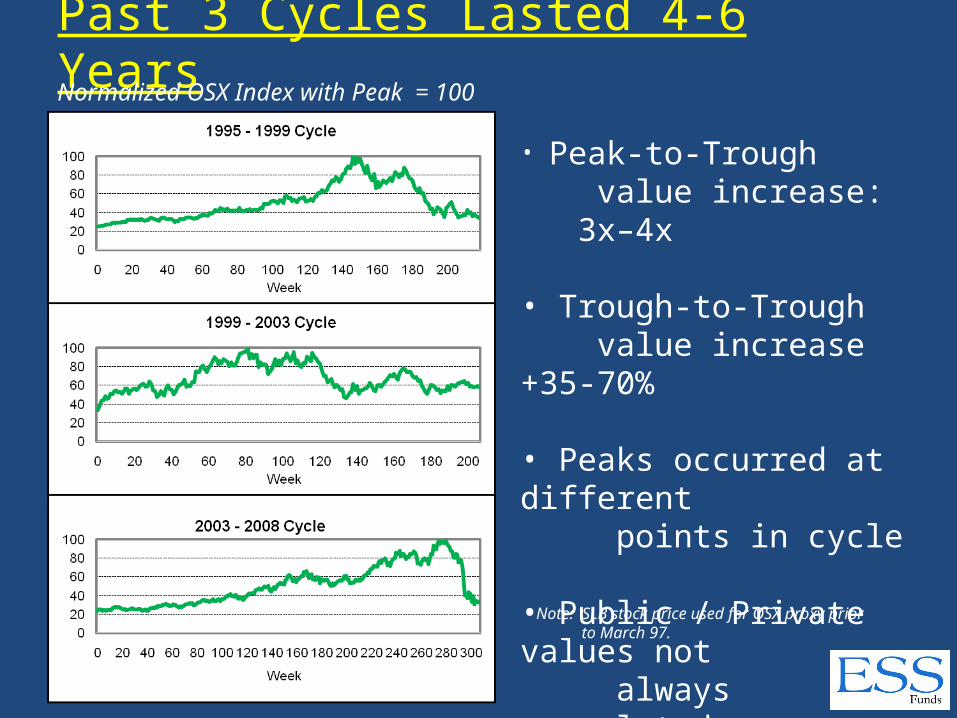

Past 3 Cycles Lasted 4-6 YearsNormalized OSX Index with Peak = 100

• Peak-to-Trough value increase: 3x–4x

• Trough-to-Trough value increase +35-70%

• Peaks occurred at different points in cycle

• Public / Private values not always correlated

Note: SLB stock price used for OSX proxy prior to March 97.

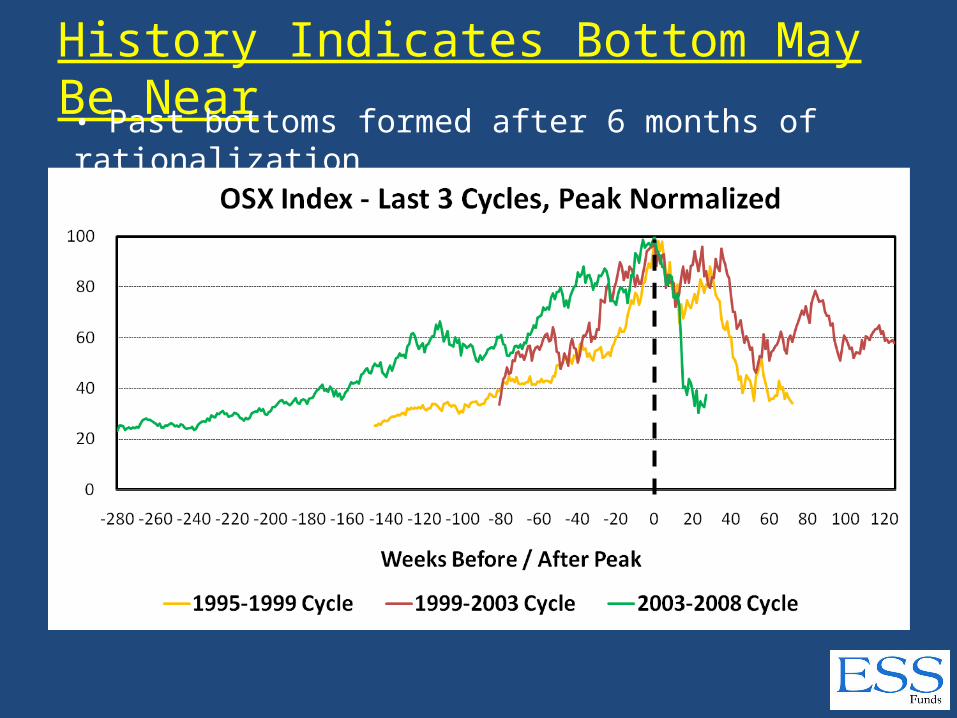

History Indicates Bottom May Be Near• Past bottoms formed after 6 months of rationalization

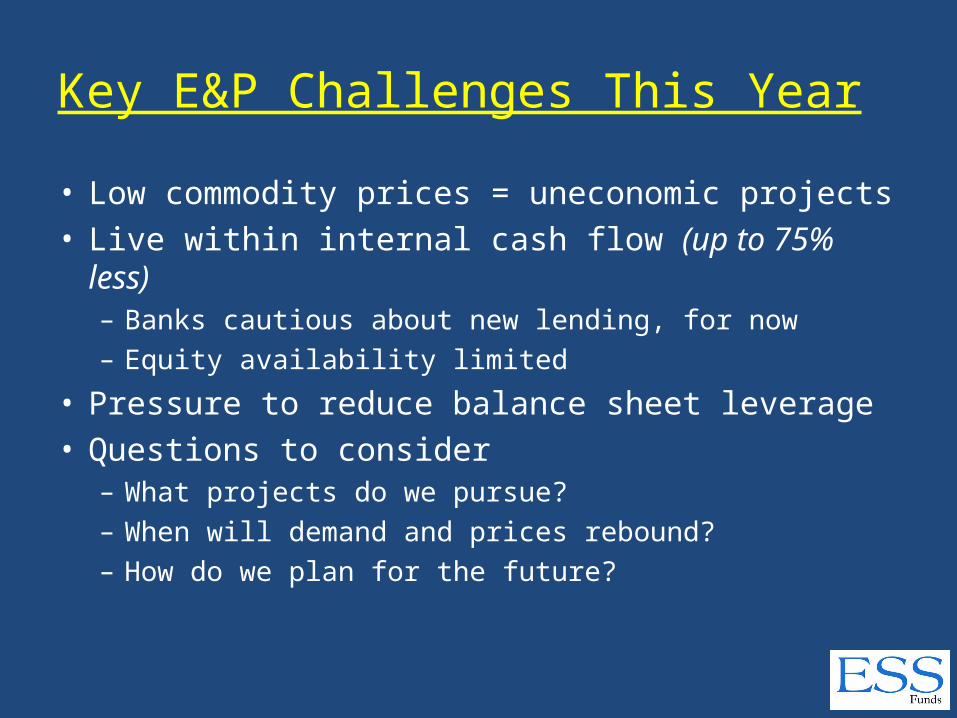

Key E&P Challenges This Year

• Low commodity prices = uneconomic projects• Live within internal cash flow (up to 75% less)

– Banks cautious about new lending, for now– Equity availability limited

• Pressure to reduce balance sheet leverage• Questions to consider

– What projects do we pursue?– When will demand and prices rebound?– How do we plan for the future?

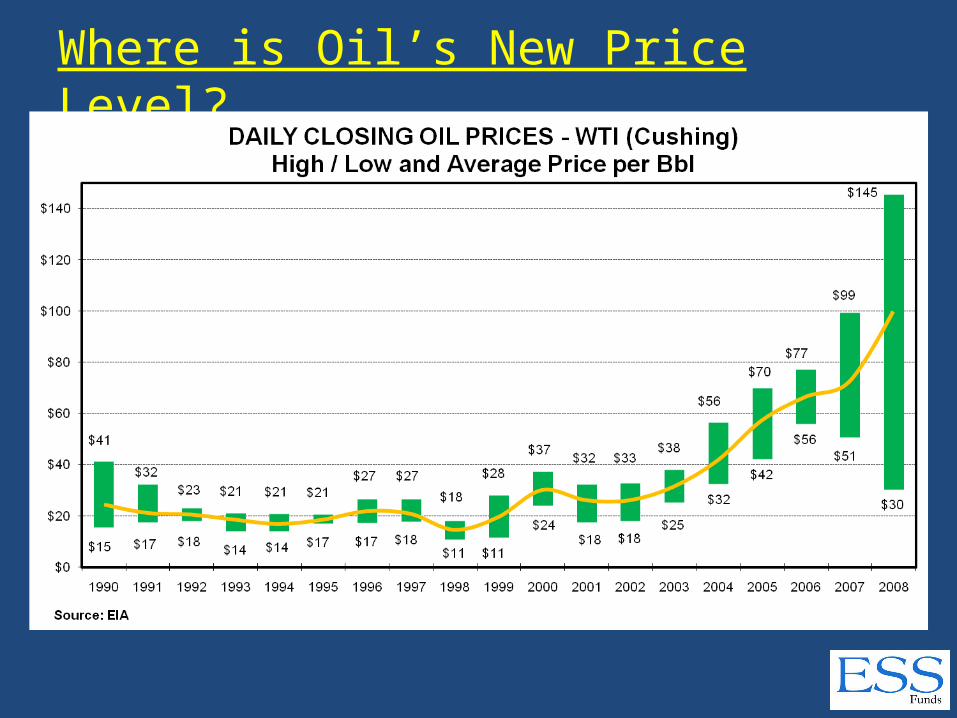

Where is Oil’s New Price Level?

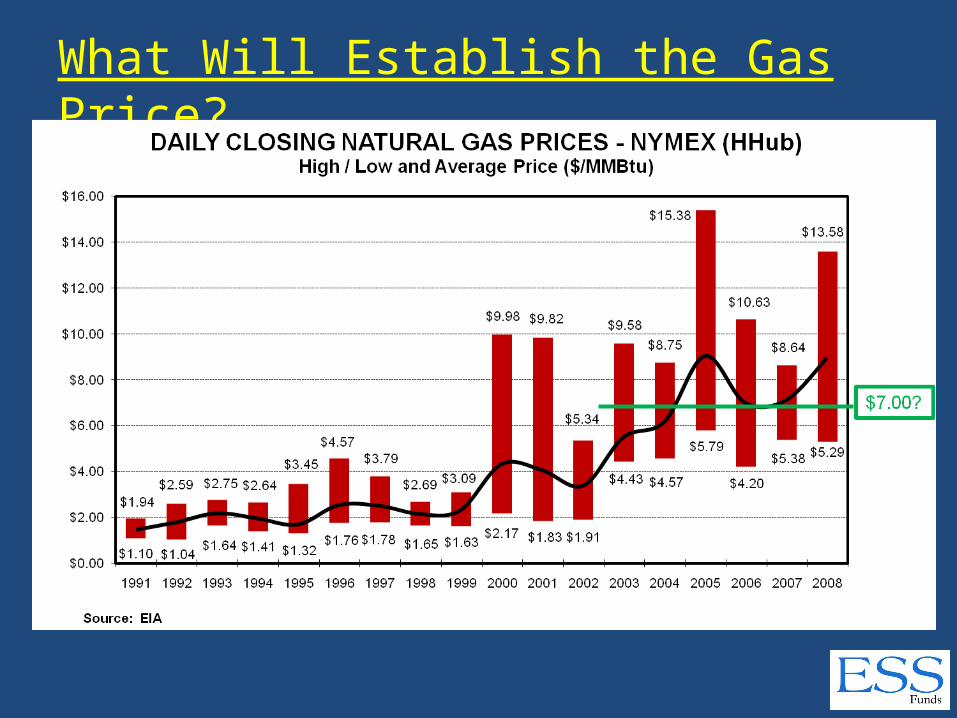

What Will Establish the Gas Price?

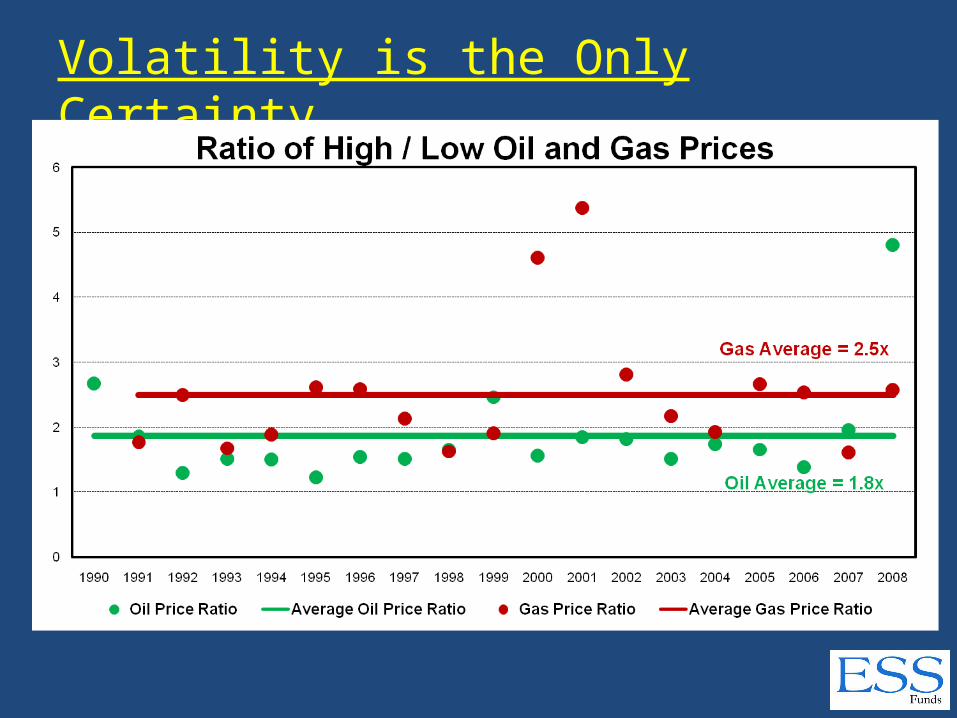

Volatility is the Only Certainty

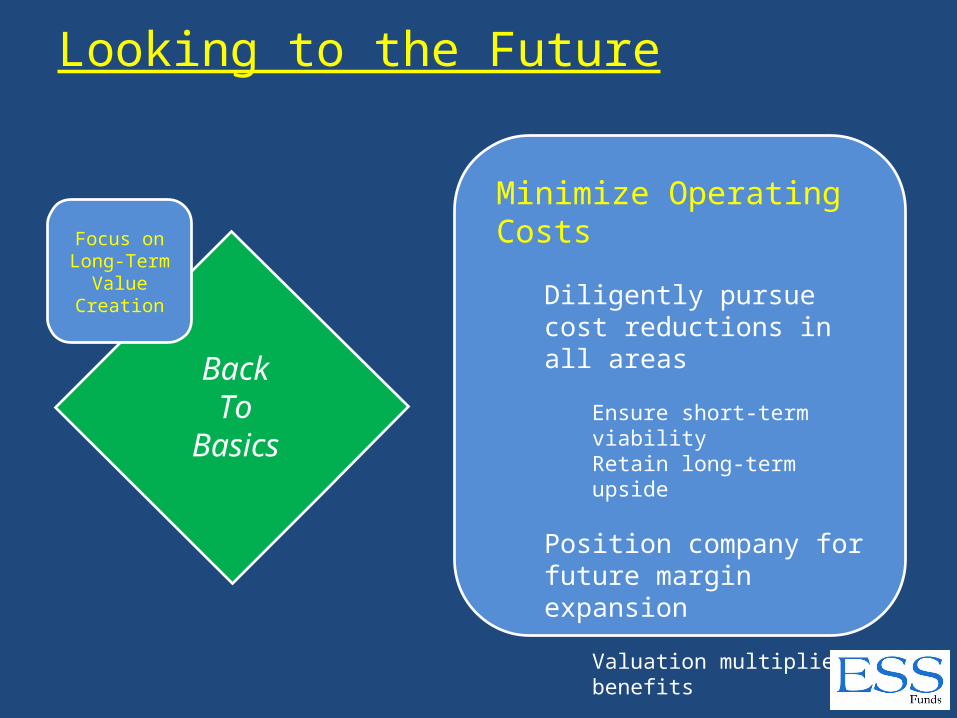

Looking to the Future

Focus on Long-Term Value Creation

Accumulate low-risk producing assets

Build portfolio of future growth opportunities

Prudently use leverage (leverage kills)

Create sustainable corporate entity

BackTo

Basics

Looking to the Future

Minimize Operating Costs

Diligently pursue cost reductions in all areas

Ensure short-term viability Retain long-term upside

Position company for future margin expansion

Valuation multiplier benefits

BackTo

Basics

Focus on Long-Term

Value Creation

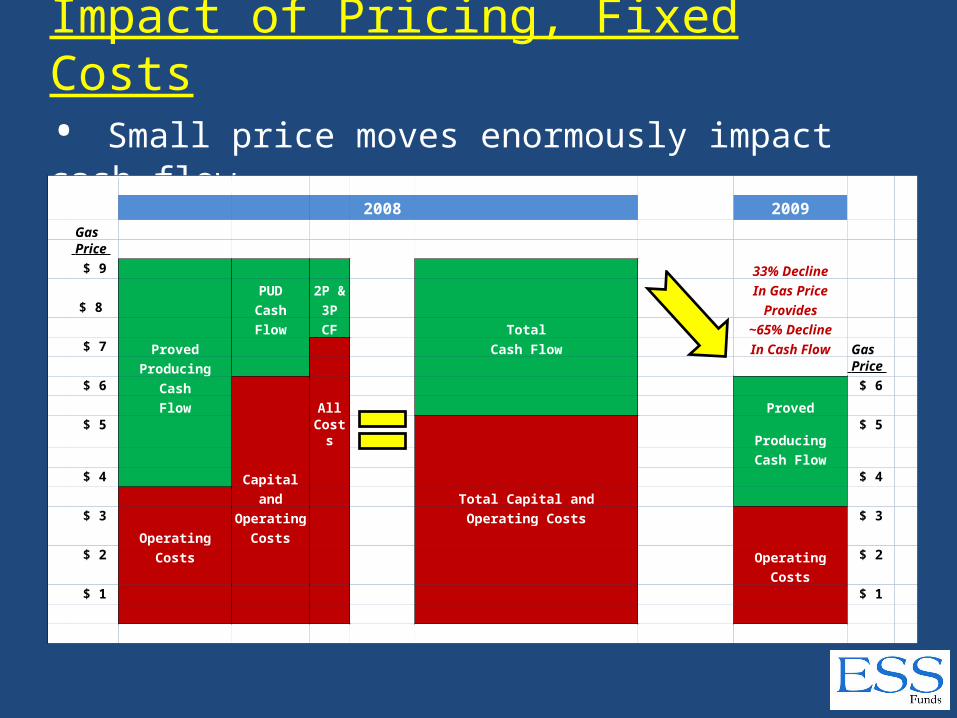

Impact of Pricing, Fixed Costs• Small price moves enormously impact cash flow

2008 2009

Gas

Price

$ 9 33% Decline

PUD 2P & In Gas Price

$ 8 Cash 3P Provides

Flow CF Total ~65% Decline

$ 7 Proved Cash Flow In Cash Flow Gas

Producing Price

$ 6 Cash $ 6

Flow All Proved

$ 5 Costs Producing $ 5

Cash Flow

$ 4 Capital $ 4

and Total Capital and

$ 3 Operating Operating Costs $ 3

Operating Costs

$ 2 Costs Operating $ 2

Costs

$ 1 $ 1

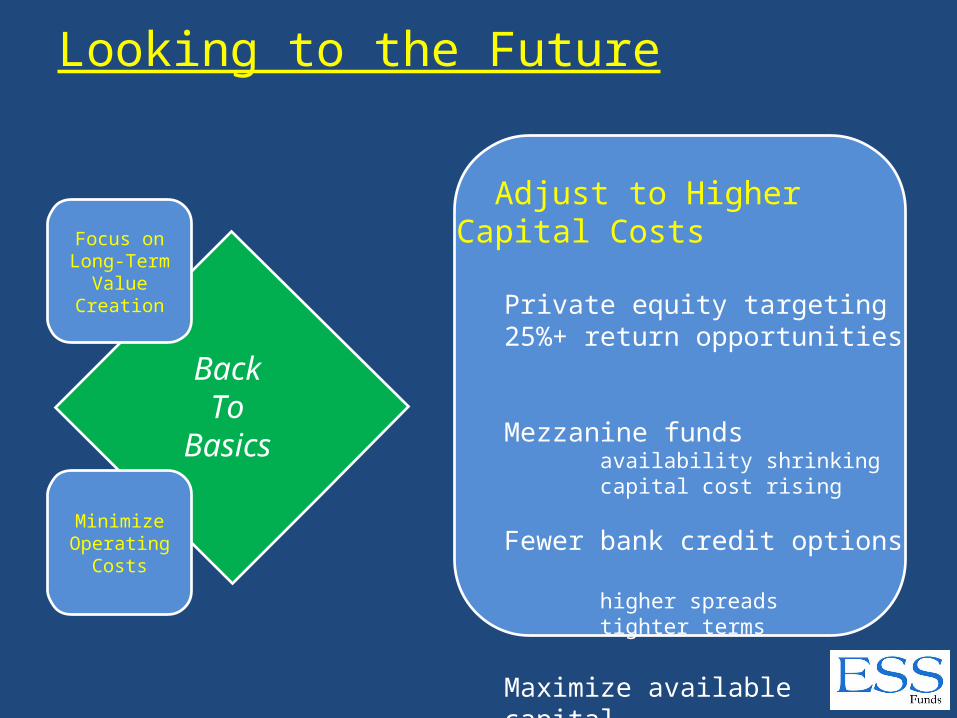

Looking to the Future

Adjust to Higher Capital Costs

Private equity targeting 25%+ return opportunities

Mezzanine funds availability shrinkingcapital cost rising

Fewer bank credit options higher spreadstighter terms

Maximize available capital

BackTo

Basics

Focus on Long-Term

Value Creation

MinimizeOperating

Costs

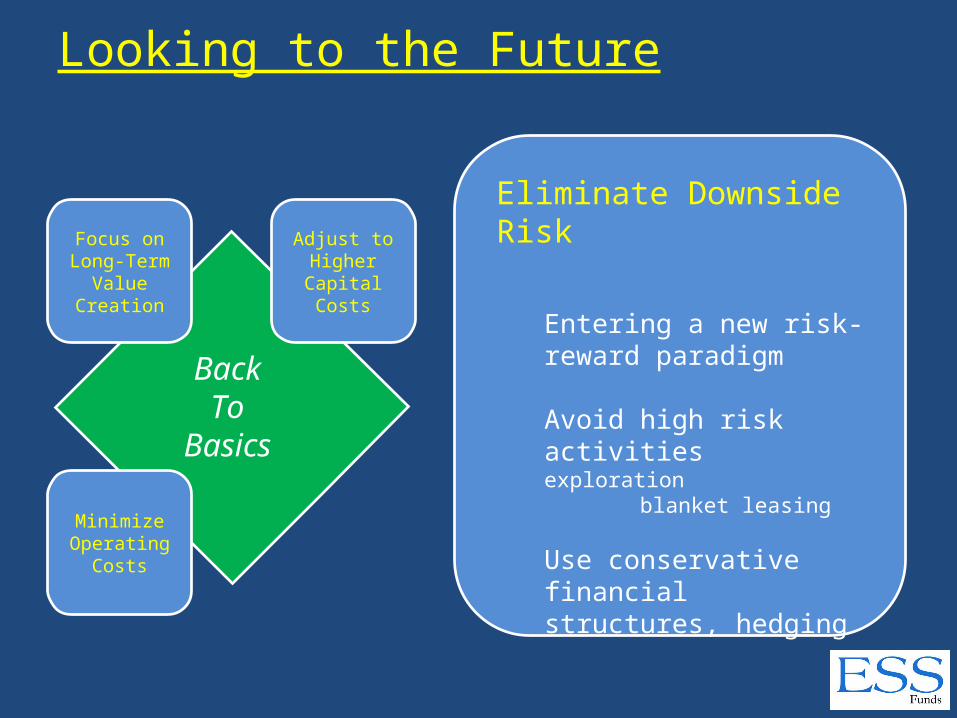

Looking to the Future

Eliminate Downside Risk

Entering a new risk-reward paradigm

Avoid high risk activities exploration blanket leasing

Use conservative financial structures, hedging

BackTo

Basics

Focus on Long-Term

Value Creation

MinimizeOperating

Costs

Adjust toHigherCapital Costs

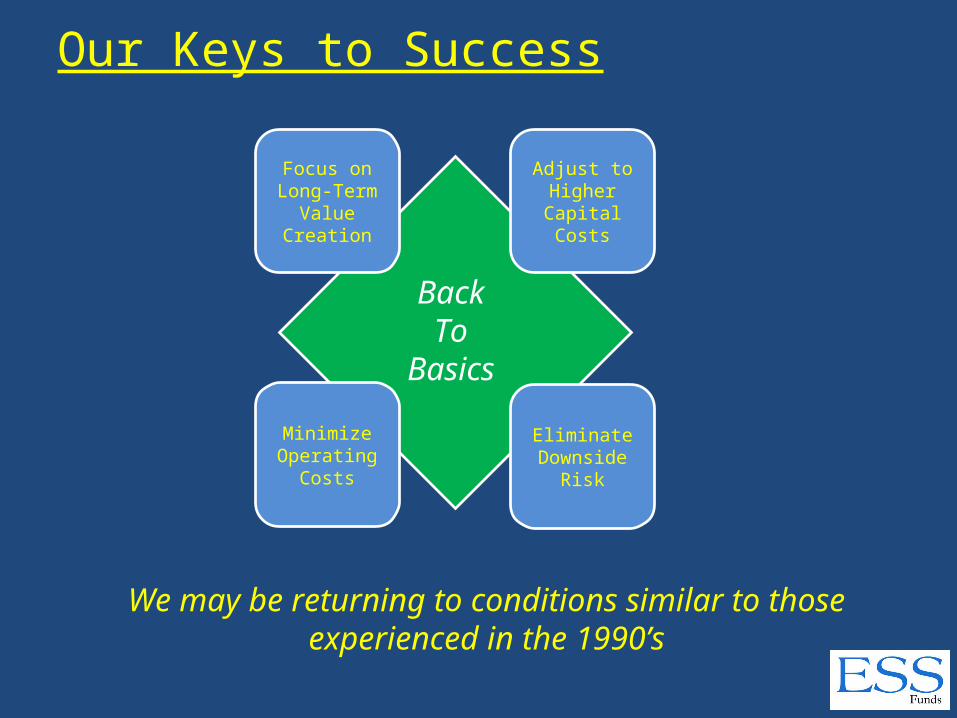

Our Keys to Success

BackTo

Basics

Focus on Long-Term

Value Creation

MinimizeOperating

Costs

Adjust to HigherCapital Costs

EliminateDownside

Risk

We may be returning to conditions similar to those experienced in the 1990’s

www.essfunds.com

Recommended