ConfidentialInvestor UpdateFY – 2018

February 2019

1

Cautionary statement

This presentation has been prepared by PT Saka Energi Indonesia (“PGN Saka” of the “Company”) and is only for informational purposes and does not constitute a recommendation regarding the

securities or debt of PGN Saka or any of its subsidiaries, or an investment in the Company. The information in this presentation is confidential and none of the information appearing in this presentation

may be distributed to the press or other media or reproduced or redistributed in whole or in part in any form at any time without the prior written consent from the Company. This document remains the

property of PGN Saka and on request must be returned and any copies destroyed.

Neither PGN Saka nor any of its respective affiliates, shareholders, directors, employees, agents, advisors or representatives makes any representation or warranty, either expressed or implied, in relation

to the accuracy, completeness or reliability of the information contained in this presentation, nor is this presentation intended to be a complete statement or summary of the state and condition of the

Company. The information set out herein may be subject to updating, completion, revision, verification and amendment without notice and such information may change materially. The information in this

presentation should not be regarded by recipients as a substitute for the exercise of their own judgement.

This presentation is not intended as, and does not form part of, any offer to sell or subscription of or solicitation or invitation to buy or subscribe for any securities. Neither this presentation nor anything

contained herein shall form the basis of, or be relied on in connection with, any contract or commitment whatsoever.

This presentation contains forward-looking statements relating to PGN Saka operations that are based on management’s current expectations, estimates and projections about the petroleum. Words or

phrases such as “expects,” “forecast,” “projects,” “estimates,” “may,” “could,” “outlook,” “on schedule,” “on track,” and similar expressions are intended to identify such forward-looking statements. These

statements are not guarantees of future performance and are subject to certain risks uncertainties and other factors, many of which are beyond the company’s control and are difficult to predict.

Therefore, actual outcomes and results may differ materially from what is expressed or forecasted in such forward-looking statements. The reader should not place undue reliance on these forward-

looking statements, which speak only as of the date of this presentation. Unless legally required, PGN Saka undertakes no obligation to update publicly any forward-looking statements, whether as a

result of new information, future events or otherwise.

Among the important factors that could cause actual results to differ materially from those in the forward-looking statements are: changing crude oil and natural gas prices; changing refining, marketing

and chemicals margins; the company’s ability to realize anticipated cost savings and expenditure reductions; actions of competitors or regulators; timing of exploration expenses; timing of crude oil lifting's;

the competitiveness of alternate-energy sources or product substitutes; technological developments; the business, results of operations and financial condition of the company’s suppliers, vendors,

partners, and equity affiliates, particularly during extended periods of low prices for crude oil and natural gas; the inability or failure of the company’s joint-venture partners to fund their share of operations

and development activities; the potential failure to achieve expected net production from existing and future crude oil and natural gas development projects; potential delays in the development,

construction or start-up of planned projects; changing economic, regulatory and political environments in the various countries in which the company operates; the potential liability for remedial actions or

assessments under existing or future environmental regulations and litigation; significant business, operational, investment or product changes required by existing or future environmental statutes and

regulations, the company’s future acquisition or disposition of assets and gains and losses from asset dispositions or impairments; government-mandated sales, divestitures, recapitalizations, industry-

specific taxes, changes in fiscal terms or restrictions on scope of company operations; foreign currency movements compared with the U.S. dollar; the effects of changed accounting rules under generally

accepted accounting principles promulgated by rule-setting bodies. Other unpredictable or unknown factors not discussed in this presentation could also have material adverse effects on forward-looking

statements. No assurance can be given that further events will occur, that projections will be achieved, or that the Company’s assumptions are correct. Actual results may differ materially from those

projected.

Any opinions expressed in this presentation are subject to change without notice and may differ or be contrary to opinions expressed by other businesses areas or groups of the Company as a result of

using different assumptions and criterion or otherwise.

2

Table of contents

Section 1 Corporate overview 3

Section 2 Operational and Financial highlights 8

Appendix A EBITDA Reconciliation 13

Appendix B Regulation and Upstream fiscal regime 15

Corporate Overview

Section 1

4

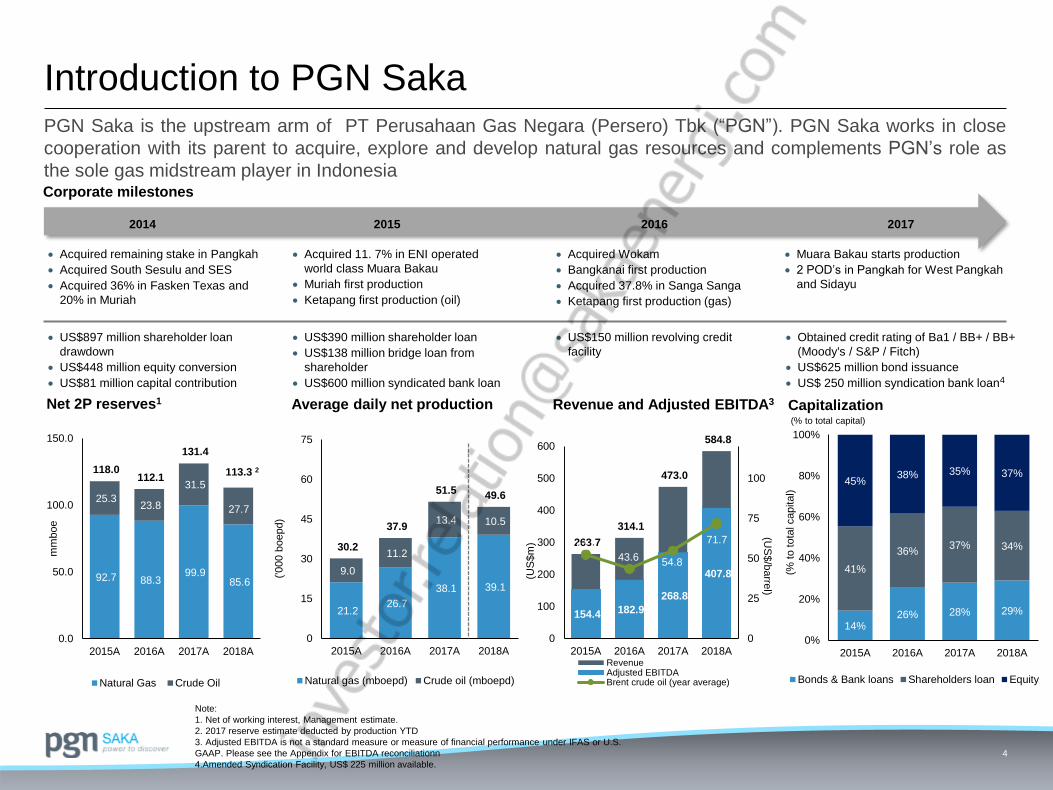

Introduction to PGN SakaPGN Saka is the upstream arm of PT Perusahaan Gas Negara (Persero) Tbk (“PGN”). PGN Saka works in close

cooperation with its parent to acquire, explore and develop natural gas resources and complements PGN’s role as

the sole gas midstream player in IndonesiaCorporate milestones

Net 2P reserves1 Revenue and Adjusted EBITDA3 Capitalization

Note:

1. Net of working interest, Management estimate.

2. 2017 reserve estimate deducted by production YTD

3. Adjusted EBITDA is not a standard measure or measure of financial performance under IFAS or U.S.

GAAP. Please see the Appendix for EBITDA reconciliationn

4.Amended Syndication Facility, US$ 225 million available.

(% to total capital)

2014 2015 2016 2017

Acquired remaining stake in Pangkah

Acquired South Sesulu and SES

Acquired 36% in Fasken Texas and

20% in Muriah

Muara Bakau starts production

2 POD’s in Pangkah for West Pangkah

and Sidayu

Acquired Wokam

Bangkanai first production

Acquired 37.8% in Sanga Sanga

Ketapang first production (gas)

Acquired 11. 7% in ENI operated

world class Muara Bakau

Muriah first production

Ketapang first production (oil)

US$897 million shareholder loan

drawdown

US$448 million equity conversion

US$81 million capital contribution

US$390 million shareholder loan

US$138 million bridge loan from

shareholder

US$600 million syndicated bank loan

US$150 million revolving credit

facility

Obtained credit rating of Ba1 / BB+ / BB+

(Moody's / S&P / Fitch)

US$625 million bond issuance

US$ 250 million syndication bank loan4

154.4 182.9

268.8

407.8

263.7

314.1

473.0

584.8

52.5 43.6 54.8

71.7

0

25

50

75

100

0

100

200

300

400

500

600

2015A 2016A 2017A 2018A

(US

$/b

arre

l)

(US

$m

)

RevenueAdjusted EBITDABrent crude oil (year average)

14%26% 28% 29%

41%

36%37% 34%

45%38% 35% 37%

0%

20%

40%

60%

80%

100%

2015A 2016A 2017A 2018A

(% to tota

l capital)

Bonds & Bank loans Shareholders loan Equity

Average daily net production

21.2 26.7

38.1 39.1

9.0

11.2

13.4 10.5

30.2

37.9

51.5 49.6

0

15

30

45

60

75

2015A 2016A 2017A 2018A

('000 b

oepd)

Natural gas (mboepd) Crude oil (mboepd)

92.7 88.3 99.9

85.6

25.3 23.8

31.5

27.7

118.0 112.1

131.4

113.3 2

0.0

50.0

100.0

150.0

2015A 2016A 2017A 2018A

mm

boe

Natural Gas Crude Oil

5

PT Saka Energi Investasi

(SEInv)

Muriah PSC

(20%)

0.003%

43.04%56.96%

99.997%

PT Saka Energi Investasi

(SEInv)

SES PSC1

(8.9%)

PT Saka Energi

Internasional (SEInt)

Fasken

(36%)

Saka Energi Overseas

Holding BV (SEOH)

100%

Saka Indonesia

Pangkah BV (SIPBV)

100%99.9%

99.9%

0.1%

0.1%

Ketapang PSC

(20%)

South Sesulu PSC

(100%)

Bangkanai PSC

(30%)

West Bangkanai PSC

(30%)

Wokam II PSC

(100%)

Muara Bakau PSC

(11.7%)

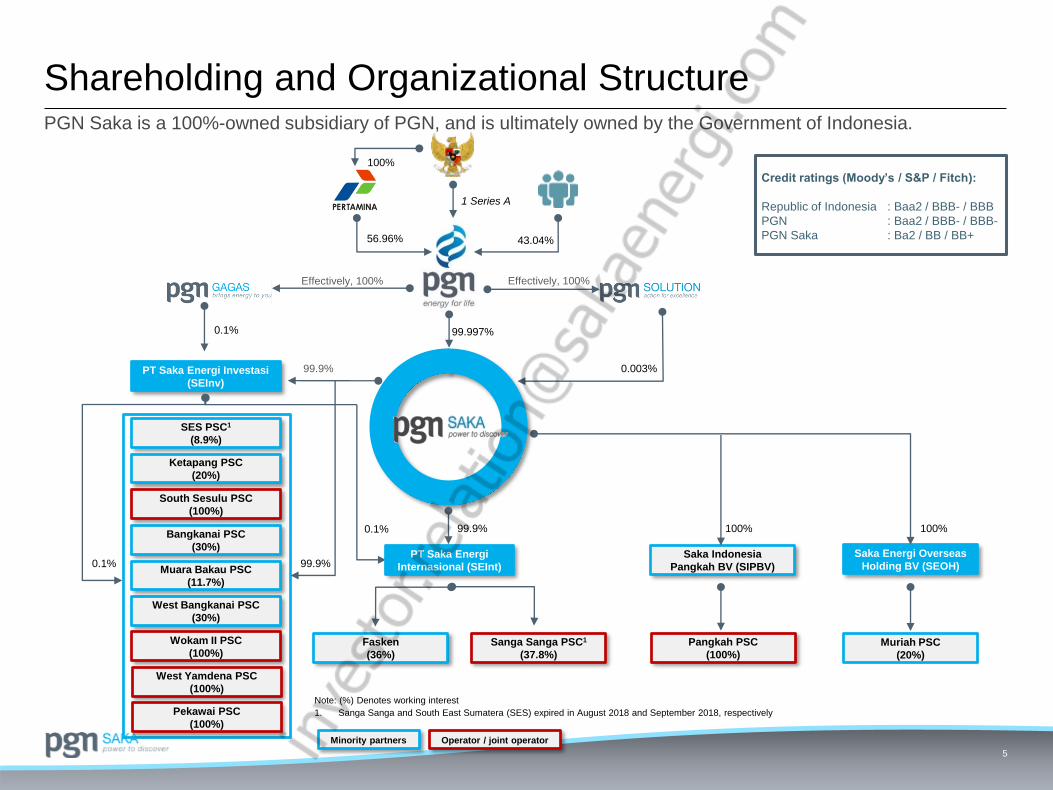

Note: (%) Denotes working interest

1. Sanga Sanga and South East Sumatera (SES) expired in August 2018 and September 2018, respectively

Pangkah PSC

(100%)

Sanga Sanga PSC1

(37.8%)

Minority partners Operator / joint operator

West Yamdena PSC

(100%)

Pekawai PSC

(100%)

100%

1 Series A

Effectively, 100% Effectively, 100%

0.1% 99.9%

Credit ratings (Moody’s / S&P / Fitch):

Republic of Indonesia : Baa2 / BBB- / BBB

PGN : Baa2 / BBB- / BBB-

PGN Saka : Ba2 / BB / BB+

PGN Saka is a 100%-owned subsidiary of PGN, and is ultimately owned by the Government of Indonesia.

Shareholding and Organizational Structure

6

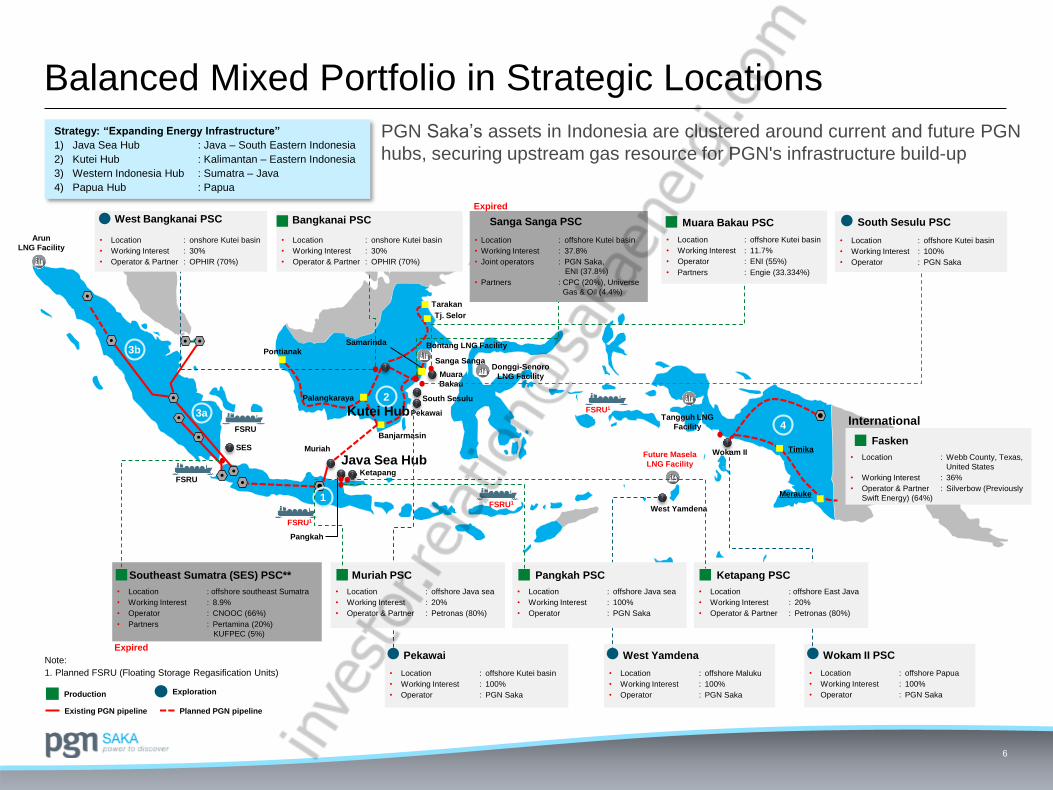

PGN Saka’s assets in Indonesia are clustered around current and future PGN

hubs, securing upstream gas resource for PGN's infrastructure build-up

Balanced Mixed Portfolio in Strategic Locations

Note:

1. Planned FSRU (Floating Storage Regasification Units)

• Location : offshore southeast Sumatra

• Working Interest : 8.9%

• Operator : CNOOC (66%)

• Partners : Pertamina (20%)

KUFPEC (5%)

Tangguh

LNG

Facility 4SES

FSRU

Muara

Bakau

KetapangFSRU

Pontianak

West YamdenaFSRU1

FSRU1

Future Masela

LNG Facility

FSRU1

Sanga Sanga

South Sesulu

Pekawai

Pangkah

Muriah

Palangkaraya

Banjarmasin

Wokam II

• Location : offshore Papua

• Working Interest : 100%

• Operator : PGN Saka

Wokam II PSC

• Location : onshore Kutei basin

• Working Interest : 30%

• Operator & Partner : OPHIR (70%)

Bangkanai PSC

• Location : onshore Kutei basin

• Working Interest : 30%

• Operator & Partner : OPHIR (70%)

West Bangkanai PSC

Southeast Sumatra (SES) PSC**

Java Sea Hub

• Location : offshore Kutei basin

• Working Interest : 100%

• Operator : PGN Saka

South Sesulu PSC

• Location : offshore Kutei basin

• Working Interest : 11.7%

• Operator : ENI (55%)

• Partners : Engie (33.334%)

Muara Bakau PSC

Strategy: “Expanding Energy Infrastructure”

1) Java Sea Hub : Java – South Eastern Indonesia

2) Kutei Hub : Kalimantan – Eastern Indonesia

3) Western Indonesia Hub : Sumatra – Java

4) Papua Hub : Papua

3b

3a

1

2

4

Kutei Hub

Timika

Merauke

Tangguh LNG

Facility

• Location : offshore Kutei basin

• Working Interest : 37.8%

• Joint operators : PGN Saka,

ENI (37.8%)

• Partners : CPC (20%), Universe

Gas & Oil (4.4%)

Sanga Sanga PSC

Arun

LNG Facility

Bontang LNG Facility

Donggi-Senoro

LNG Facility

Tarakan

Tj. Selor

Samarinda

Production Exploration

Existing PGN pipeline Planned PGN pipeline

• Location : offshore Maluku

• Working Interest : 100%

• Operator : PGN Saka

West Yamdena

• Location : offshore Kutei basin

• Working Interest : 100%

• Operator : PGN Saka

PekawaiExpired

Expired

• Location : offshore Java sea

• Working Interest : 20%

• Operator & Partner : Petronas (80%)

Muriah PSC

• Location : offshore Java sea

• Working Interest : 100%

• Operator : PGN Saka

Pangkah PSC

• Location : Webb County, Texas,

United States

• Working Interest : 36%

• Operator & Partner : Silverbow (Previously

Swift Energy) (64%)

Fasken

International

• Location : offshore East Java

• Working Interest : 20%

• Operator & Partner : Petronas (80%)

Ketapang PSC

7

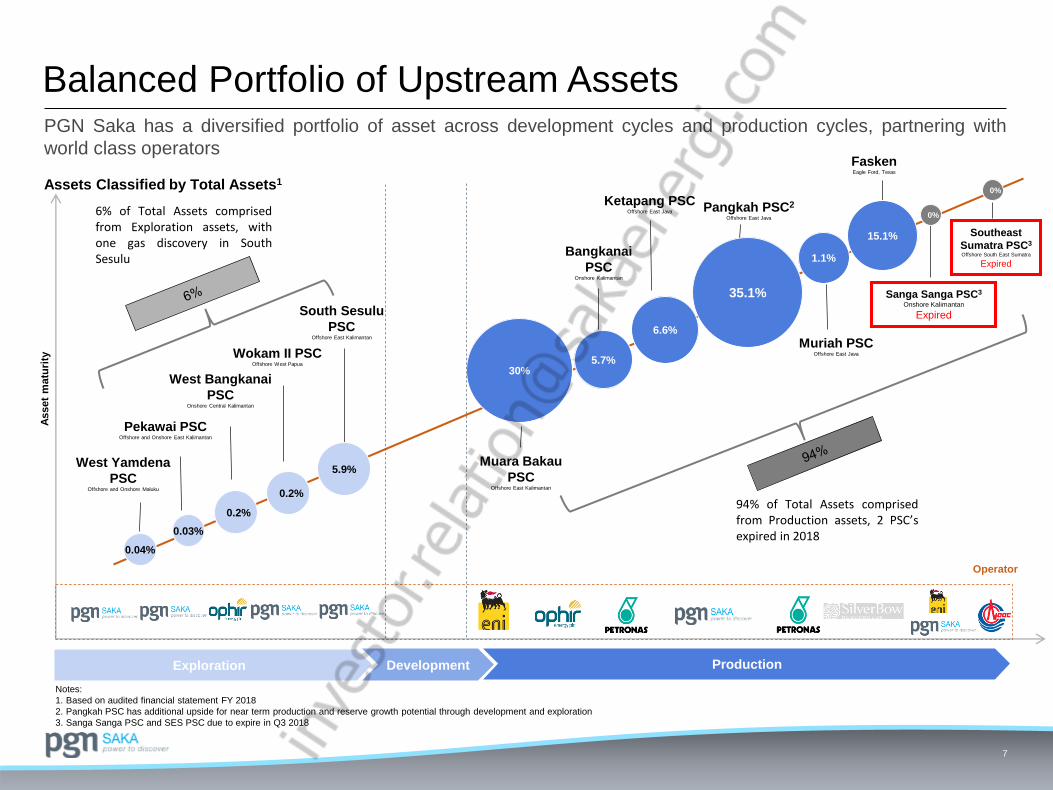

Balanced Portfolio of Upstream AssetsA

sset

matu

rity

FaskenEagle Ford, Texas

Southeast

Sumatra PSC3

Offshore South East Sumatra

Expired

Muara Bakau

PSCOffshore East Kalimantan

South Sesulu

PSCOffshore East Kalimantan

Operator

Sanga Sanga PSC3

Onshore Kalimantan

Expired

Exploration Development Production

Assets Classified by Total Assets1

Wokam II PSCOffshore West Papua

West Bangkanai

PSCOnshore Central Kalimantan

PGN Saka has a diversified portfolio of asset across development cycles and production cycles, partnering with

world class operators

Notes:

1. Based on audited financial statement FY 2018

2. Pangkah PSC has additional upside for near term production and reserve growth potential through development and exploration

3. Sanga Sanga PSC and SES PSC due to expire in Q3 2018

5.9%

Pangkah PSC2

Offshore East Java

Muriah PSCOffshore East Java

Ketapang PSCOffshore East Java

Bangkanai

PSCOnshore Kalimantan

30%5.7%

6.6%

35.1%

1.1%

15.1%

6% of Total Assets comprisedfrom Exploration assets, withone gas discovery in SouthSesulu

94% of Total Assets comprisedfrom Production assets, 2 PSC’sexpired in 20180.03%

0.04%

Pekawai PSCOffshore and Onshore East Kalimantan

West Yamdena

PSCOffshore and Onshore Maluku

0%

0.2%

0.2%

0%

Operational & Financial Highlights

Section 2

9

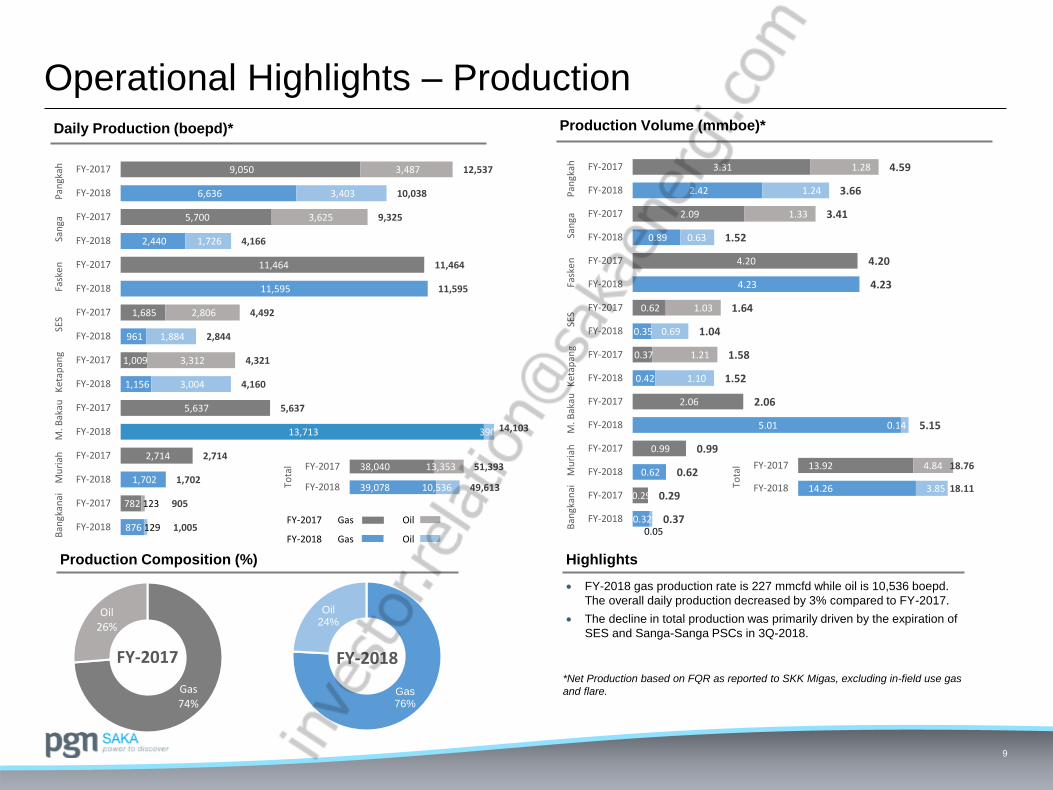

Operational Highlights – ProductionDaily Production (boepd)*

Production Composition (%)

Production Volume (mmboe)*

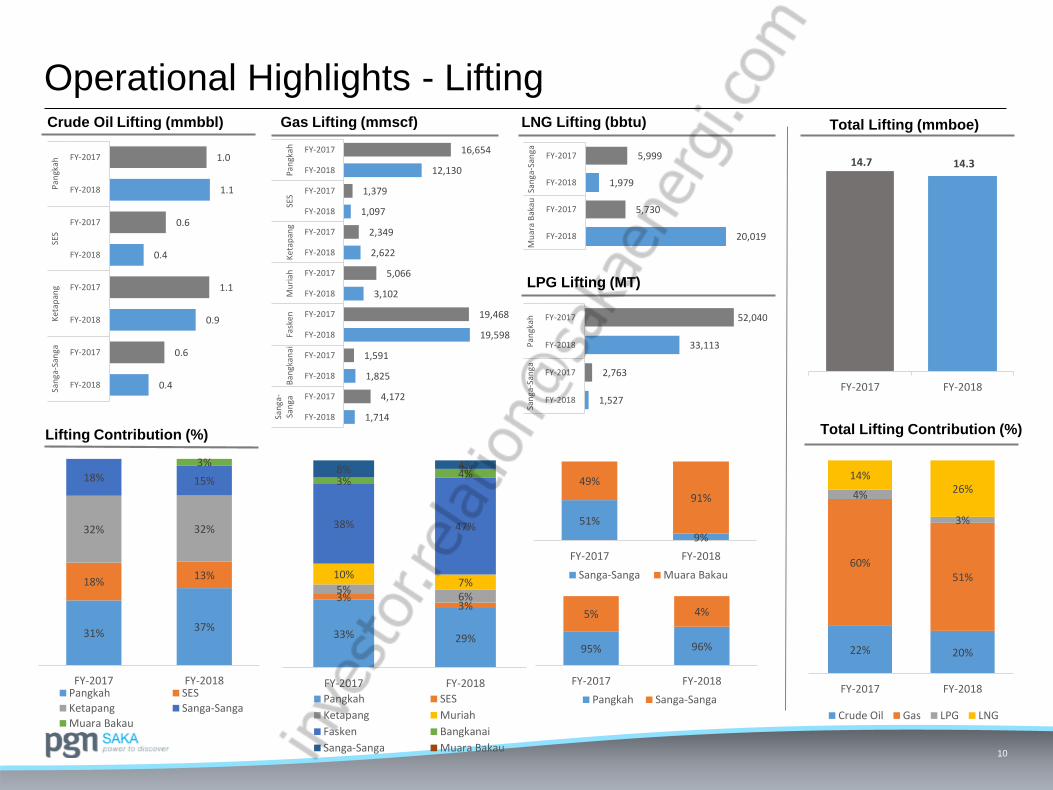

Highlights

FY-2018 gas production rate is 227 mmcfd while oil is 10,536 boepd.

The overall daily production decreased by 3% compared to FY-2017.

The decline in total production was primarily driven by the expiration of

SES and Sanga-Sanga PSCs in 3Q-2018.

*Net Production based on FQR as reported to SKK Migas, excluding in-field use gas

and flare.

FY-2017 Gas Oil

FY-2018 Gas Oil 876

782

1,702

2,714

13,713

5,637

1,156

1,009

961

1,685

11,595

11,464

2,440

5,700

6,636

9,050

129

123

390

3,004

3,312

1,884

2,806

1,726

3,625

3,403

3,487

1,005

905

1,702

2,714

14,103

5,637

4,160

4,321

2,844

4,492

11,595

11,464

4,166

9,325

10,038

12,537

FY-2018

FY-2017

FY-2018

FY-2017

FY-2018

FY-2017

FY-2018

FY-2017

FY-2018

FY-2017

FY-2018

FY-2017

FY-2018

FY-2017

FY-2018

FY-2017

Ban

gkan

aiM

uri

ahM

. Bak

auK

etap

ang

SES

Fask

enSa

nga

Pan

gkah

39,078

38,040

10,536

13,353

49,613

51,393

FY-2018

FY-2017

Tota

l

0.32

0.29

0.62

0.99

5.01

2.06

0.42

0.37

0.35

0.62

4.23

4.20

0.89

2.09

2.42

3.31

0.05

0.14

1.10

1.21

0.69

1.03

0.63

1.33

1.24

1.28

0.37

0.29

0.62

0.99

5.15

2.06

1.52

1.58

1.04

1.64

4.23

4.20

1.52

3.41

3.66

4.59

FY-2018

FY-2017

FY-2018

FY-2017

FY-2018

FY-2017

FY-2018

FY-2017

FY-2018

FY-2017

FY-2018

FY-2017

FY-2018

FY-2017

FY-2018

FY-2017

Ban

gkan

aiM

uri

ahM

. Bak

auK

etap

ang

SES

Fask

enSa

nga

Pan

gkah

Gas74%

Oil26%

FY-2017

Gas76%

Oil24%

FY-2018

14.26

13.92

3.85

4.84

18.11

18.76

FY-2018

FY-2017

Tota

l

10

LPG Lifting (MT)

LNG Lifting (bbtu)Crude Oil Lifting (mmbbl)

Operational Highlights - LiftingGas Lifting (mmscf) Total Lifting (mmboe)

Lifting Contribution (%) Total Lifting Contribution (%)

0.4

0.6

0.9

1.1

0.4

0.6

1.1

1.0

FY-2018

FY-2017

FY-2018

FY-2017

FY-2018

FY-2017

FY-2018

FY-2017

San

ga-S

anga

Ket

apan

gSE

SP

angk

ah

1,714

4,172

1,825

1,591

19,598

19,468

3,102

5,066

2,622

2,349

1,097

1,379

12,130

16,654

FY-2018

FY-2017

FY-2018

FY-2017

FY-2018

FY-2017

FY-2018

FY-2017

FY-2018

FY-2017

FY-2018

FY-2017

FY-2018

FY-2017

San

ga-

San

gaB

angk

anai

Fask

enM

uri

ahK

etap

ang

SES

Pan

gkah

1,527

2,763

33,113

52,040

FY-2018

FY-2017

FY-2018

FY-2017

San

ga-S

anga

Pan

gkah

20,019

5,730

1,979

5,999

FY-2018

FY-2017

FY-2018

FY-2017

Mu

ara

Bak

auSa

nga

-San

ga

14.7 14.3

FY-2017 FY-2018

31%37%

18%13%

32% 32%

18% 15%

3%

FY-2017 FY-2018Pangkah SES

Ketapang Sanga-Sanga

Muara Bakau

33% 29%

3%3%

5%6%

10%7%

38% 47%

3%4%8% 4%

FY-2017 FY-2018

Pangkah SES

Ketapang Muriah

Fasken Bangkanai

Sanga-Sanga Muara Bakau

95% 96%

5% 4%

FY-2017 FY-2018

Pangkah Sanga-Sanga

51%

9%

49%

91%

FY-2017 FY-2018

Sanga-Sanga Muara Bakau

22% 20%

60%51%

4%

3%

14%26%

FY-2017 FY-2018

Crude Oil Gas LPG LNG

11

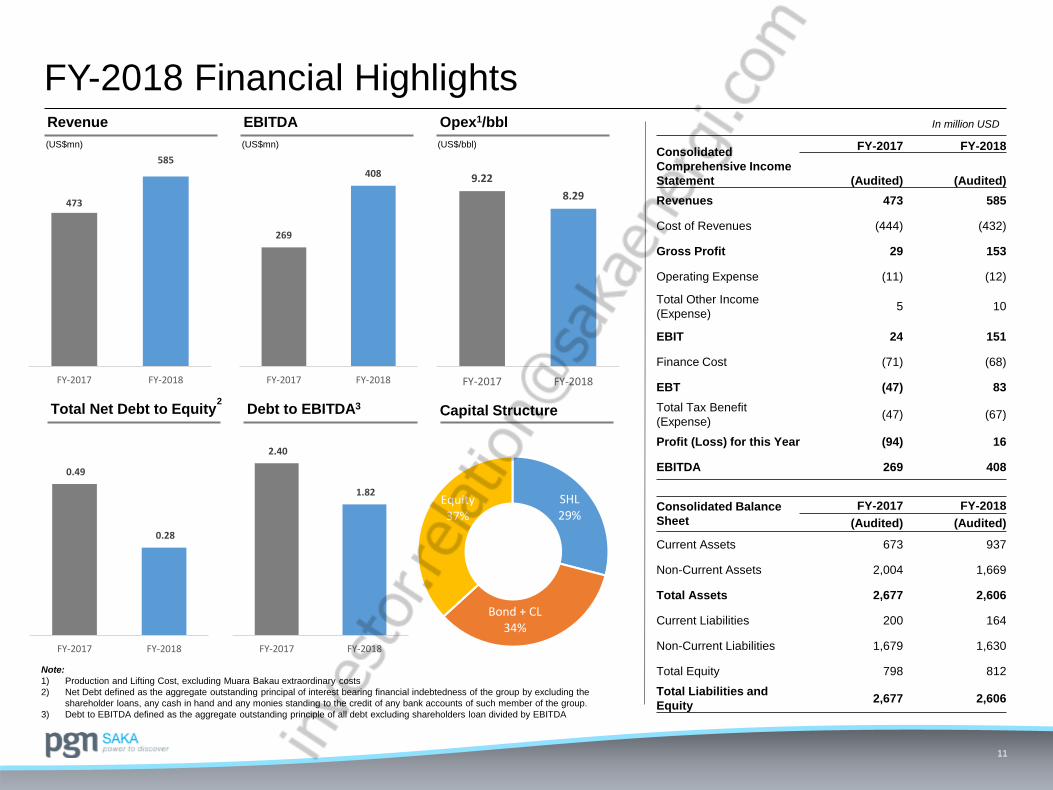

FY-2018 Financial HighlightsRevenue EBITDA Opex1/bbl

Capital StructureTotal Net Debt to Equity Debt to EBITDA3

Note:

1) Production and Lifting Cost, excluding Muara Bakau extraordinary costs

2) Net Debt defined as the aggregate outstanding principal of interest bearing financial indebtedness of the group by excluding the

shareholder loans, any cash in hand and any monies standing to the credit of any bank accounts of such member of the group.

3) Debt to EBITDA defined as the aggregate outstanding principle of all debt excluding shareholders loan divided by EBITDA

(US$mn) (US$mn) (US$/bbl)

2

In million USD

473

585

FY-2017 FY-2018

269

408

FY-2017 FY-2018

9.22

8.29

FY-2017 FY-2018

0.49

0.28

FY-2017 FY-2018

2.40

1.82

FY-2017 FY-2018

SHL29%

Bond + CL34%

Equity37%

Consolidated

Comprehensive Income

Statement

FY-2017 FY-2018

(Audited) (Audited)

Revenues 473 585

Cost of Revenues (444) (432)

Gross Profit 29 153

Operating Expense (11) (12)

Total Other Income

(Expense)5 10

EBIT 24 151

Finance Cost (71) (68)

EBT (47) 83

Total Tax Benefit

(Expense)(47) (67)

Profit (Loss) for this Year (94) 16

EBITDA 269 408

Consolidated Balance

Sheet

FY-2017 FY-2018

(Audited) (Audited)

Current Assets 673 937

Non-Current Assets 2,004 1,669

Total Assets 2,677 2,606

Current Liabilities 200 164

Non-Current Liabilities 1,679 1,630

Total Equity 798 812

Total Liabilities and

Equity2,677 2,606

12

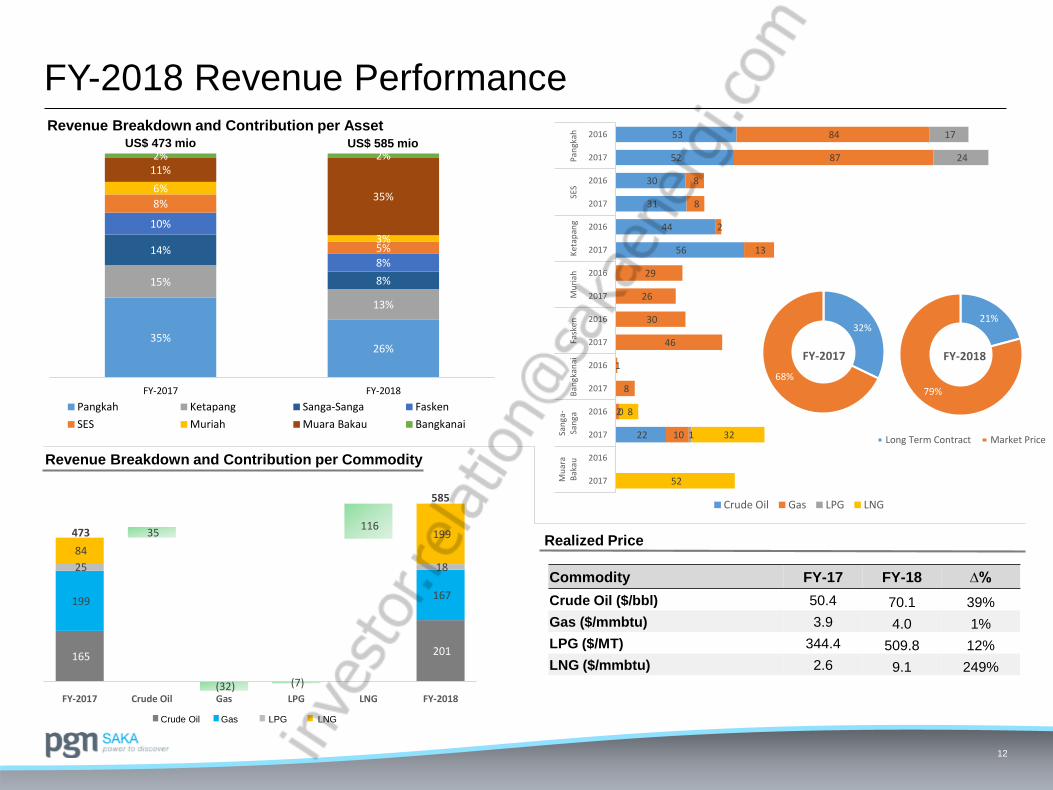

FY-2018 Revenue PerformanceRevenue Breakdown and Contribution per Asset

Revenue Breakdown and Contribution per Commodity

Realized Price

Crude Oil Gas LPG LNG

Commodity FY-17 FY-18 ∆%

Crude Oil ($/bbl) 50.4 70.1 39%

Gas ($/mmbtu) 3.9 4.0 1%

LPG ($/MT) 344.4 509.8 12%

LNG ($/mmbtu) 2.6 9.1 249%

35%26%

15%

13%

14%

8%

10%

8%

8%

5%

6%

3%

11%

35%

2% 2%

FY-2017 FY-2018

Axis TitlePangkah Ketapang Sanga-Sanga Fasken

SES Muriah Muara Bakau Bangkanai

US$ 473 mio US$ 585 mio

22

56

44

31

30

52

53

10

2

8

1

46

30

26

29

13

2

8

8

87

84

1

0

24

17

52

32

8

2017

2016

2017

2016

2017

2016

2017

2016

2017

2016

2017

2016

2017

2016

2017

2016

Mu

ara

Bak

auSa

nga

-Sa

nga

Ban

gkan

aiFa

sken

Mu

riah

Ket

apan

gSE

SP

angk

ah

Crude Oil Gas LPG LNG

32%

68%

FY-2017

21%

79%

FY-2018

Long Term Contract Market Price

165 201

199

35

(32) (7)

116

167

25 18

84

199 473

585

FY-2017 Crude Oil Gas LPG LNG FY-2018

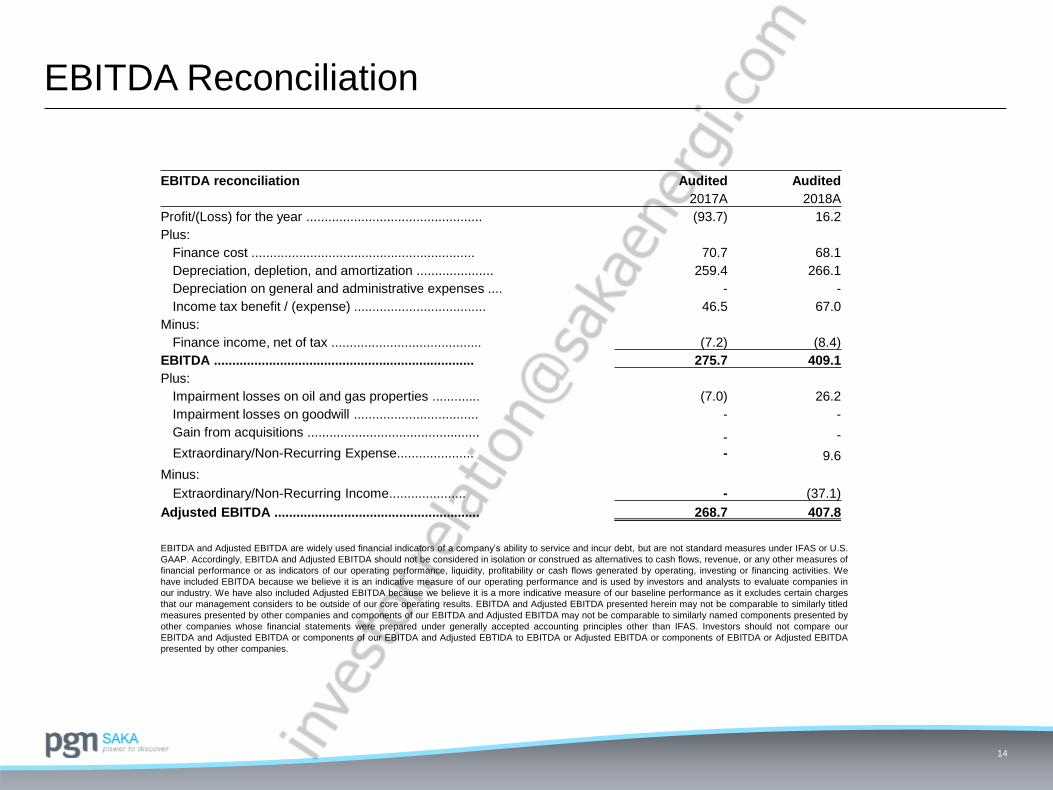

EBITDA reconciliation

Appendix A

14

EBITDA Reconciliation

EBITDA and Adjusted EBITDA are widely used financial indicators of a company’s ability to service and incur debt, but are not standard measures under IFAS or U.S.

GAAP. Accordingly, EBITDA and Adjusted EBITDA should not be considered in isolation or construed as alternatives to cash flows, revenue, or any other measures of

financial performance or as indicators of our operating performance, liquidity, profitability or cash flows generated by operating, investing or financing activities. We

have included EBITDA because we believe it is an indicative measure of our operating performance and is used by investors and analysts to evaluate companies in

our industry. We have also included Adjusted EBITDA because we believe it is a more indicative measure of our baseline performance as it excludes certain charges

that our management considers to be outside of our core operating results. EBITDA and Adjusted EBITDA presented herein may not be comparable to similarly titled

measures presented by other companies and components of our EBITDA and Adjusted EBITDA may not be comparable to similarly named components presented by

other companies whose financial statements were prepared under generally accepted accounting principles other than IFAS. Investors should not compare our

EBITDA and Adjusted EBITDA or components of our EBITDA and Adjusted EBTIDA to EBITDA or Adjusted EBITDA or components of EBITDA or Adjusted EBITDA

presented by other companies.

EBITDA reconciliation Audited Audited

2017A 2018A

Profit/(Loss) for the year ................................................ (93.7) 16.2

Plus:

Finance cost ............................................................. 70.7 68.1

Depreciation, depletion, and amortization ..................... 259.4 266.1

Depreciation on general and administrative expenses .... - -

Income tax benefit / (expense) .................................... 46.5 67.0

Minus:

Finance income, net of tax ......................................... (7.2) (8.4)

EBITDA ....................................................................... 275.7 409.1

Plus:

Impairment losses on oil and gas properties ............. (7.0) 26.2

Impairment losses on goodwill .................................. - -

Gain from acquisitions ............................................... -

-

-

Extraordinary/Non-Recurring Expense..................... 9.6

Minus:

Extraordinary/Non-Recurring Income..................... - (37.1)

Adjusted EBITDA ........................................................ 268.7 407.8

Regulation and upstream fiscal regime

Appendix B

16

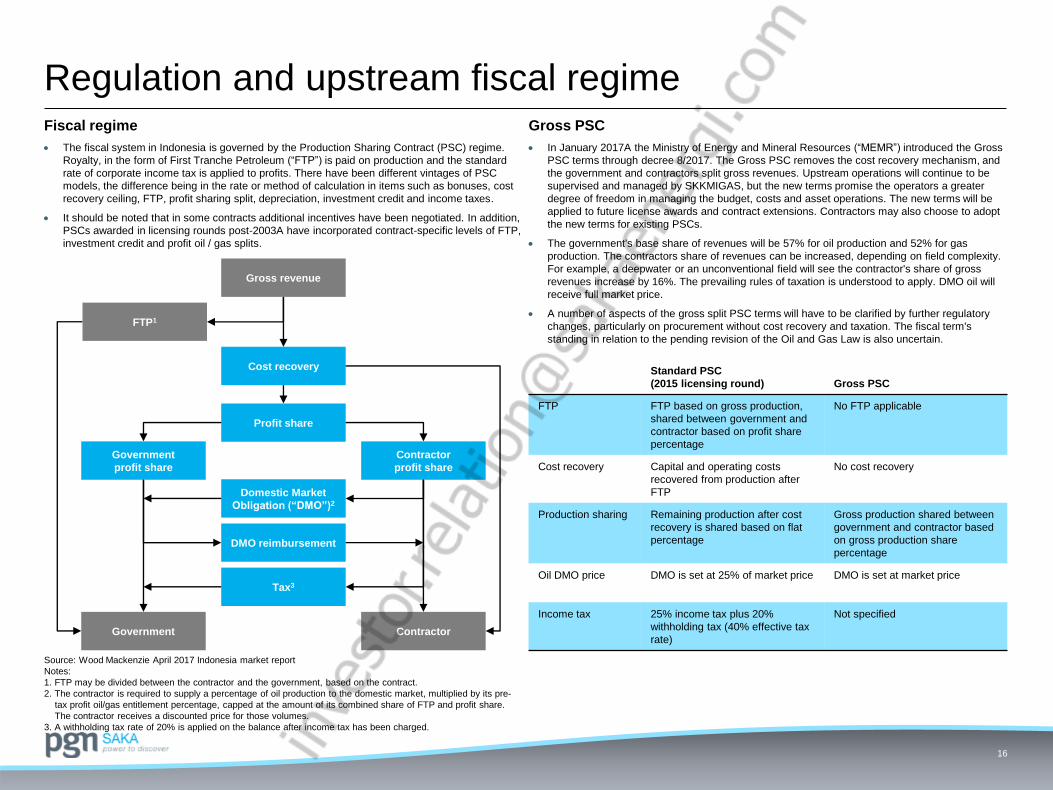

Regulation and upstream fiscal regime

The fiscal system in Indonesia is governed by the Production Sharing Contract (PSC) regime.

Royalty, in the form of First Tranche Petroleum (“FTP”) is paid on production and the standard

rate of corporate income tax is applied to profits. There have been different vintages of PSC

models, the difference being in the rate or method of calculation in items such as bonuses, cost

recovery ceiling, FTP, profit sharing split, depreciation, investment credit and income taxes.

It should be noted that in some contracts additional incentives have been negotiated. In addition,

PSCs awarded in licensing rounds post-2003A have incorporated contract-specific levels of FTP,

investment credit and profit oil / gas splits.

Fiscal regime

Cost recovery

Gross revenue

FTP1

Government

Profit share

Contractor

profit share

Government

profit share

Domestic Market

Obligation (“DMO”)2

Tax3

DMO reimbursement

Contractor

Source: Wood Mackenzie April 2017 Indonesia market report

Notes:

1. FTP may be divided between the contractor and the government, based on the contract.

2. The contractor is required to supply a percentage of oil production to the domestic market, multiplied by its pre-

tax profit oil/gas entitlement percentage, capped at the amount of its combined share of FTP and profit share.

The contractor receives a discounted price for those volumes.

3. A withholding tax rate of 20% is applied on the balance after income tax has been charged.

Gross PSC

In January 2017A the Ministry of Energy and Mineral Resources (“MEMR”) introduced the Gross

PSC terms through decree 8/2017. The Gross PSC removes the cost recovery mechanism, and

the government and contractors split gross revenues. Upstream operations will continue to be

supervised and managed by SKKMIGAS, but the new terms promise the operators a greater

degree of freedom in managing the budget, costs and asset operations. The new terms will be

applied to future license awards and contract extensions. Contractors may also choose to adopt

the new terms for existing PSCs.

The government's base share of revenues will be 57% for oil production and 52% for gas

production. The contractors share of revenues can be increased, depending on field complexity.

For example, a deepwater or an unconventional field will see the contractor's share of gross

revenues increase by 16%. The prevailing rules of taxation is understood to apply. DMO oil will

receive full market price.

A number of aspects of the gross split PSC terms will have to be clarified by further regulatory

changes, particularly on procurement without cost recovery and taxation. The fiscal term's

standing in relation to the pending revision of the Oil and Gas Law is also uncertain.

Standard PSC

(2015 licensing round) Gross PSC

FTP FTP based on gross production,

shared between government and

contractor based on profit share

percentage

No FTP applicable

Cost recovery Capital and operating costs

recovered from production after

FTP

No cost recovery

Production sharing Remaining production after cost

recovery is shared based on flat

percentage

Gross production shared between

government and contractor based

on gross production share

percentage

Oil DMO price DMO is set at 25% of market price DMO is set at market price

Income tax 25% income tax plus 20%

withholding tax (40% effective tax

rate)

Not specified

PT Saka Energi Indonesia

The Energy 11th – 12th Floor

Jl. Jenderal Sudirman Kav 52-53, SCBD

Jakarta 12190

Phone: +62(21) 29951000

Fax : +62(21) 29951001

Email: [email protected]

Recommended