Investor Presentation | September 2017

2

Confidential: Not for distribution or publication

Disclaimer

Forward-Looking Statements

This presentation contains “forward-looking statements” within the meaning of the Federal Private Securities Litigation Reform Act of 1995. Forward-looking

statements may include, but are not limited to, statements relating to our 2017 Adjusted EBITDA outlook. Some of the forward-looking statements can be identified

by the use of terms such as “may,” “intend,” “might,” “will,” “should,” “could,” “would,” “expect,” “believe,” “estimate,” “anticipate,” “predict,” “project,” “potential,” or

the negative of these terms, and similar expressions. You should be aware that these forward-looking statements are subject to risks and uncertainties that are

beyond our control. Further, any forward-looking statement speaks only as of the date on which it is made, and we undertake no obligation to update any forward-

looking statement to reflect events or circumstances after the date on which it is made or to reflect the occurrence of anticipated or unanticipated events or

circumstances. New factors emerge from time to time that may cause our business not to develop as we expect, and it is not possible for us to predict all of them.

Factors that may cause actual results to differ materially from those expressed or implied by the forward-looking statements include, but are not limited to, the

following: cyclicality in residential and commercial construction markets; general economic and financial conditions; weather conditions, seasonality and availability

of water to end-users; laws and government regulations applicable to our business that could negatively impact demand for our products; public perceptions that

our products and services are not environmentally friendly; competitive industry pressures; product shortages and the loss of key suppliers; product price

fluctuations; inventory management risks; ability to implement our business strategies and achieve our growth objectives; acquisition and integration risks;

increased operating costs; and other risks, as described in Item 1A, “Risk Factors,” and elsewhere in our Annual Report on Form 10-K for the fiscal year ended

January 1, 2017.

Non-GAAP Financial Information

This release includes certain financial information, not prepared in accordance with U.S. GAAP. Because not all companies calculate non-GAAP financial

information identically (or at all), the presentations herein may not be comparable to other similarly titled measures used by other companies. Further, these

measures should not be considered substitutes for the information contained in the historical financial information of the Company prepared in accordance with

U.S. GAAP that is set forth herein.

We present Adjusted EBITDA in order to evaluate the operating performance and efficiency of our business. Adjusted EBITDA represents EBITDA as further

adjusted for items permitted under the covenants of our credit facilities. EBITDA represents our Net income (loss) plus the sum of Income tax (benefit),

Depreciation and amortization and interest expense, net of interest income. Adjusted EBITDA is also adjusted for stock-based compensation expense, related

party advisory fees, (gain) loss on sale of assets, other non-cash items and other non-recurring (income) loss. Adjusted EBITDA does not include pre-acquisition

acquired Adjusted EBITDA of any acquired company. Adjusted EBITDA is not a measure of our liquidity or financial performance under GAAP and should not be

considered as an alternative to net income, operating income or any other performance measures derived in accordance with GAAP, or as an alternative to cash

flow from operating activities as a measure of our liquidity. The use of Adjusted EBITDA instead of net income has limitations as an analytical tool. Because not all

companies use identical calculations, our presentation of Adjusted EBITDA may not be comparable to other similarly titled measures of other companies, limiting

its usefulness as a comparative measure. See the Appendix for a reconciliation of Adjusted EBITDA to net income. Net debt is defined as long-term debt (net of

issuance costs and discounts) plus capital leases, net of cash and cash-equivalents on our balance sheet. Leverage Ratio is defined as Net Debt to the trailing

twelve months Adjusted EBITDA. We define Organic Daily Sales as Organic Sales divided by the number of Selling Days in the relevant reporting period. We

define Organic Sales as Net sales, including Net sales from newly-opened greenfield stores, but excluding Net sales from acquired stores until they have been

under our ownership for at least four full fiscal quarters at the start of the fiscal year. Selling Days are the number of business days, excluding Saturdays, Sundays

and holidays, that SiteOne branches are open during the relevant reporting period.

3

Confidential: Not for distribution or publication

Today’s presenters

Doug Black

Chairman & CEO

▪ Joined SiteOne in April 2014

▪ Previously spent 18 years at CRH plc most recently as President and COO of Oldcastle Inc.

▪ Held a variety of roles including CEO and COO of Oldcastle Materials

▪ Previously a consultant with McKinsey

▪ M.B.A. from Duke and B.S. from the U.S. Military Academy at West Point

Pascal Convers

EVP of Strategy,

Development &

Investor Relations

▪ Joined SiteOne in July 2014

▪ 10 years at CRH plc, recently as SVP of Strategy and Development for Oldcastle Materials

▪ Previously CRH’s Managing Director for concrete and landscaping operations in France

▪ Spent 13 years at Eastman Chemical Company, held senior leadership roles in Europe, North America

and Asia-Pacific

▪ M.B.A. from Duke, M.S. from Ecole Des Mines de Paris and B.S. in Chemical Engineering from Rennes

Section 1Company overview

5

Confidential: Not for distribution or publication

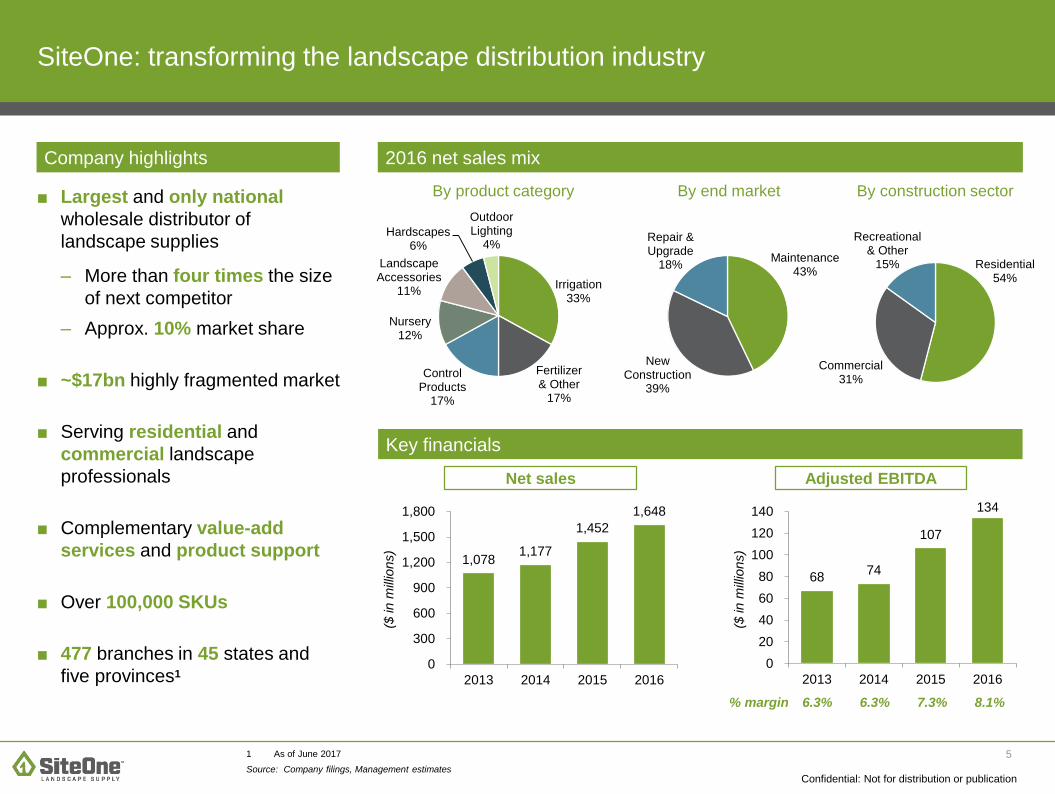

Adjusted EBITDANet sales

■ Largest and only national

wholesale distributor of

landscape supplies

– More than four times the size

of next competitor

– Approx. 10% market share

■ ~$17bn highly fragmented market

■ Serving residential and

commercial landscape

professionals

■ Complementary value-add

services and product support

■ Over 100,000 SKUs

■ 477 branches in 45 states and

five provinces1

2016 net sales mix

By product category By end market By construction sector

Company highlights

Key financials

SiteOne: transforming the landscape distribution industry

% margin 6.3% 6.3% 7.3% 8.1%

1 As of June 2017

Source: Company filings, Management estimates

Irrigation33%

Fertilizer& Other

17%

Control Products

17%

Nursery12%

Landscape Accessories

11%

Hardscapes6%

Outdoor Lighting

4%Maintenance

43%

New Construction

39%

Repair & Upgrade

18% Residential54%

Commercial31%

Recreational & Other

15%

1,078 1,177

1,452

1,648

0

300

600

900

1,200

1,500

1,800

2013 2014 2015 2016

($ in m

illio

ns)

68 74

107

134

0

20

40

60

80

100

120

140

2013 2014 2015 2016

($ in m

illio

ns)

6

Confidential: Not for distribution or publication

SiteOne plays a critical role in the professional landscape supply value chain

Thousands

of suppliers

Hundreds of thousands

of customers

Large: ~27% of 2016 net sales

■ >$200K in avg. annual

purchases

Medium: ~54% of 2016 net sales

■ $10K – 200K in avg. annual

purchases

Coast-to-coast

national network

Extensive

sales &

marketing

Rapid

product

launches

Fewer and larger

shipments

Broadest

product

offering

Superior

technical

expertise

Customer

loyalty

program

Trade credit,

sales leads

and training

SiteOne provides: SiteOne provides:

Critical business partner Small: ~18% of 2016 net sales

■ <$10K in avg. annual

purchases

One-stop shop

Source: Company data, Management estimates

7

Confidential: Not for distribution or publication

We are the Only National One-stop Shop Provider in the Industry

Source: Management estimates, Company data; Wholesale outlets only

Irrigation

Fertilizer

& Other

Control

Products Nursery

Landscape

Accessories Hardscapes

Outdoor

Lighting

% of 2016 Sales 33% 17% 17% 12% 11% 6% 4%

Key Products

Key Suppliers

Market Position #1 #1#1#1 #1 #1#1

8

Confidential: Not for distribution or publication

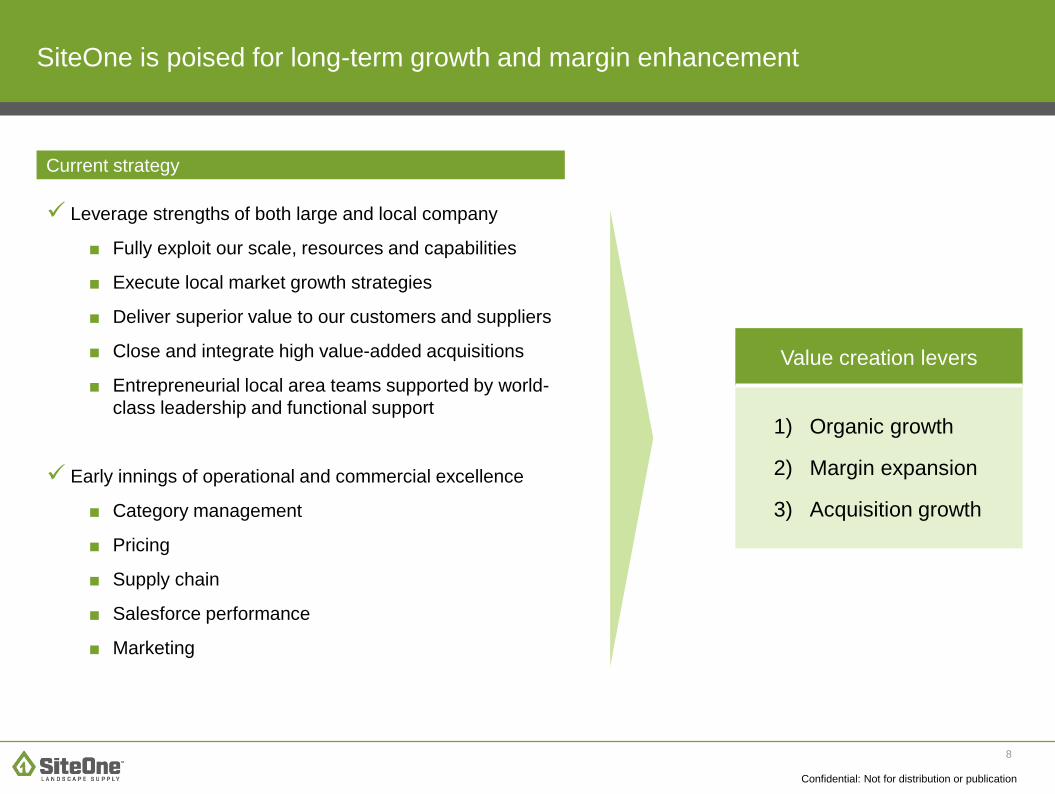

SiteOne is poised for long-term growth and margin enhancement

Current strategy

✓ Leverage strengths of both large and local company

■ Fully exploit our scale, resources and capabilities

■ Execute local market growth strategies

■ Deliver superior value to our customers and suppliers

■ Close and integrate high value-added acquisitions

■ Entrepreneurial local area teams supported by world-

class leadership and functional support

✓ Early innings of operational and commercial excellence

■ Category management

■ Pricing

■ Supply chain

■ Salesforce performance

■ Marketing

Value creation levers

1) Organic growth

2) Margin expansion

3) Acquisition growth

9

Confidential: Not for distribution or publication

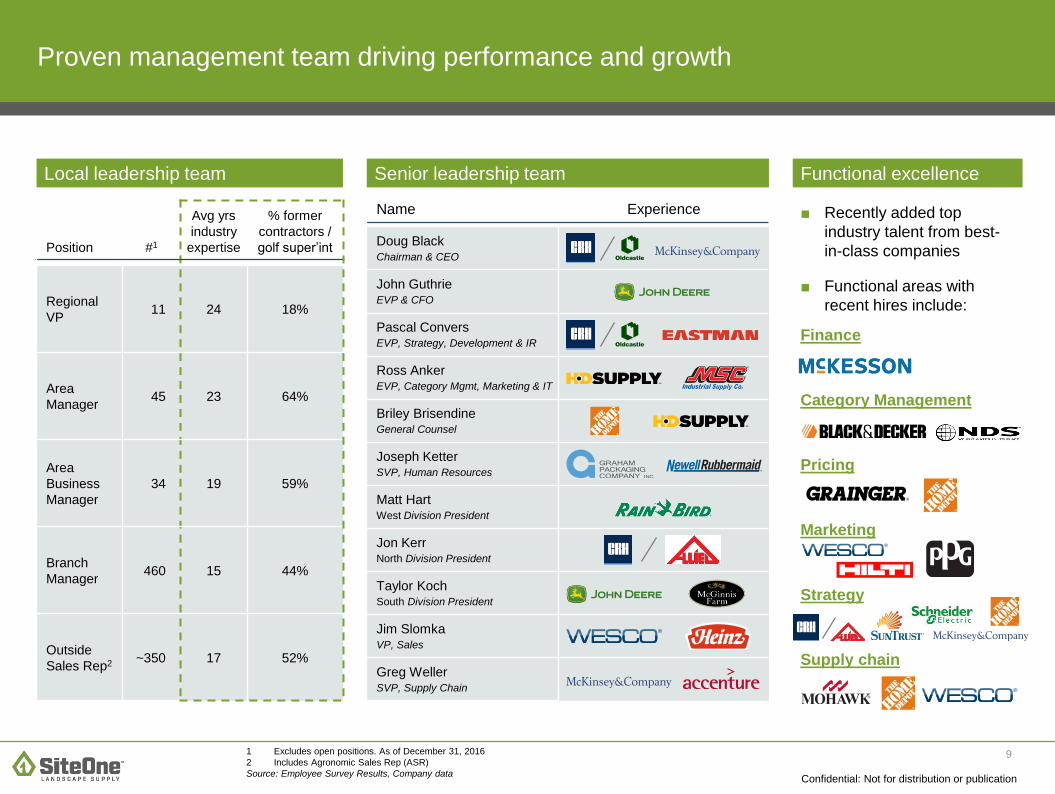

Position #1

Avg yrs

industry

expertise

% former

contractors /

golf super’int

Regional

VP11 24 18%

Area

Manager45 23 64%

Area

Business

Manager

34 19 59%

Branch

Manager460 15 44%

Outside

Sales Rep2 ~350 17 52%

Functional excellenceLocal leadership team Senior leadership team

■ Recently added top

industry talent from best-

in-class companies

■ Functional areas with

recent hires include:

Finance

Category Management

Pricing

Marketing

Strategy

Supply chain

Name Experience

Doug BlackChairman & CEO

John GuthrieEVP & CFO

Pascal ConversEVP, Strategy, Development & IR

Ross AnkerEVP, Category Mgmt, Marketing & IT

Briley BrisendineGeneral Counsel

Joseph Ketter SVP, Human Resources

Matt HartWest Division President

Jon KerrNorth Division President

Taylor Koch South Division President

Jim Slomka VP, Sales

Greg Weller SVP, Supply Chain

1 Excludes open positions. As of December 31, 2016

2 Includes Agronomic Sales Rep (ASR)

Source: Employee Survey Results, Company data

Proven management team driving performance and growth

10

Confidential: Not for distribution or publication

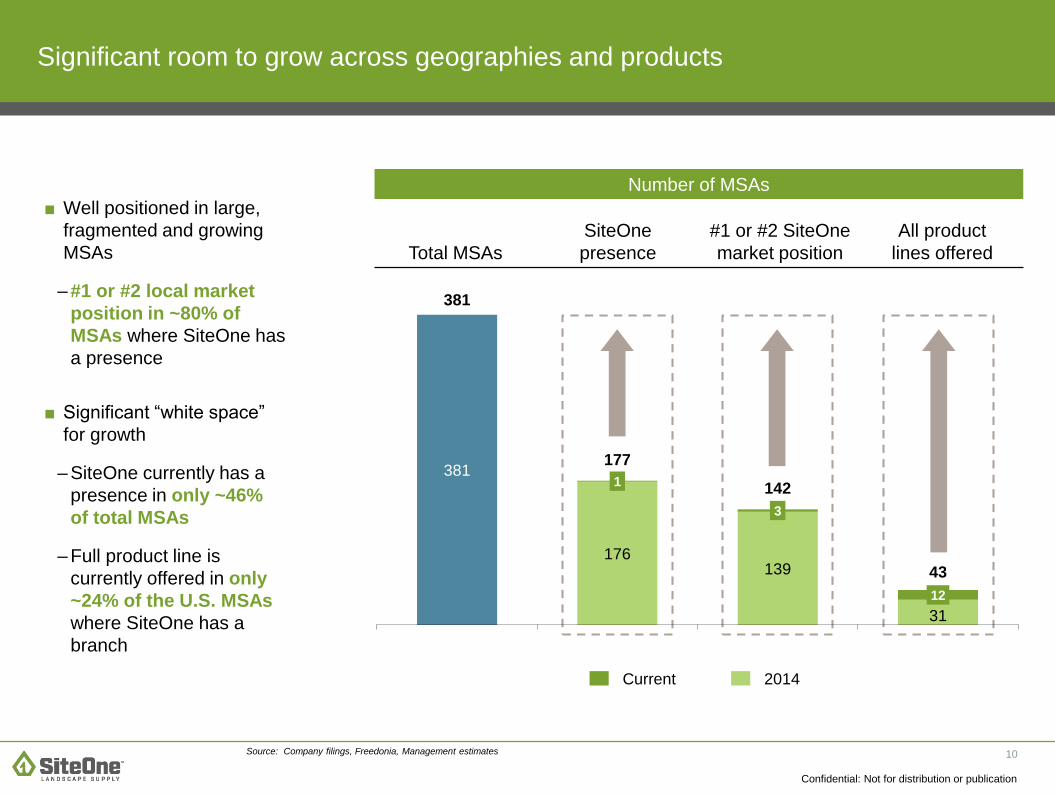

Number of MSAs

Total MSAs

SiteOne

presence

#1 or #2 SiteOne

market position

All product

lines offered

Significant room to grow across geographies and products

■ Well positioned in large,

fragmented and growing

MSAs

– #1 or #2 local market

position in ~80% of

MSAs where SiteOne has

a presence

■ Significant “white space”

for growth

– SiteOne currently has a

presence in only ~46%

of total MSAs

– Full product line is

currently offered in only

~24% of the U.S. MSAs

where SiteOne has a

branch

Source: Company filings, Freedonia, Management estimates

Current 2014

381

176 139

31

1

3

12

381

177

142

43

11

Confidential: Not for distribution or publication

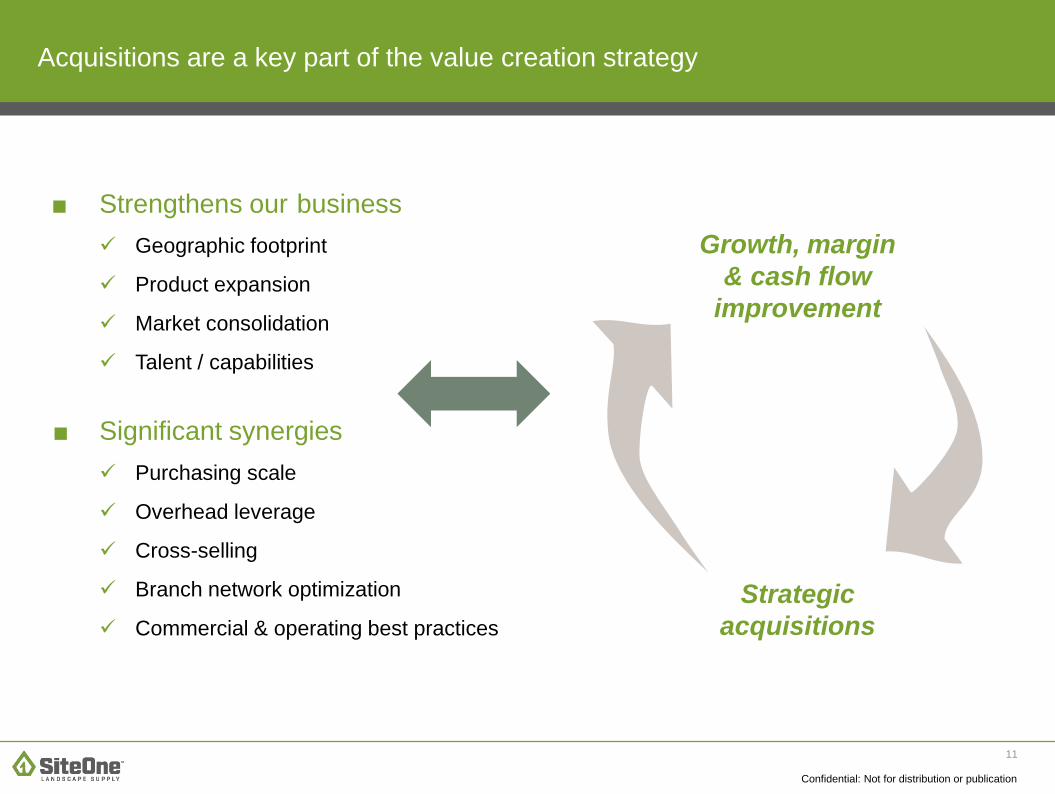

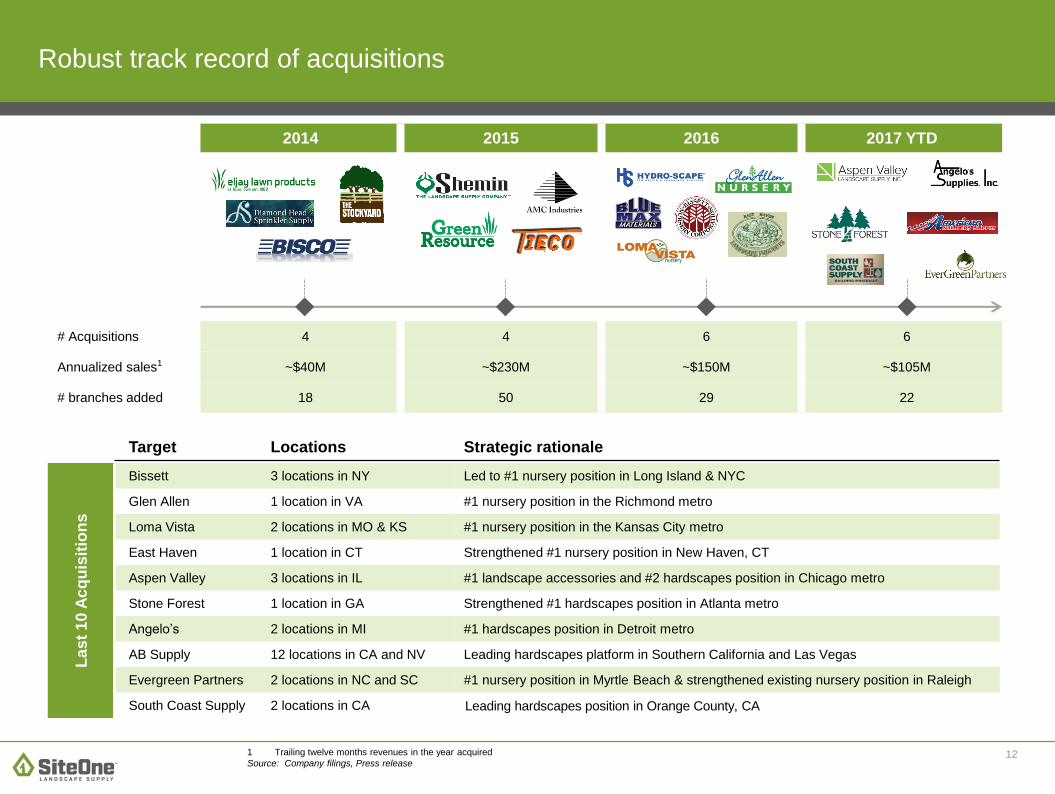

Acquisitions are a key part of the value creation strategy

■ Strengthens our business

✓ Geographic footprint

✓ Product expansion

✓ Market consolidation

✓ Talent / capabilities

■ Significant synergies

✓ Purchasing scale

✓ Overhead leverage

✓ Cross-selling

✓ Branch network optimization

✓ Commercial & operating best practices

Growth, margin

& cash flow

improvement

Strategic

acquisitions

12

2014 2015 2016 2017 YTD

# Acquisitions 4 4 6 6

Annualized sales1 ~$40M ~$230M ~$150M ~$105M

# branches added 18 50 29 22

Robust track record of acquisitions

Target Locations Strategic rationale

La

st

10

Ac

qu

isit

ion

s

Bissett 3 locations in NY Led to #1 nursery position in Long Island & NYC

Glen Allen 1 location in VA #1 nursery position in the Richmond metro

Loma Vista 2 locations in MO & KS #1 nursery position in the Kansas City metro

East Haven 1 location in CT Strengthened #1 nursery position in New Haven, CT

Aspen Valley 3 locations in IL #1 landscape accessories and #2 hardscapes position in Chicago metro

Stone Forest 1 location in GA Strengthened #1 hardscapes position in Atlanta metro

Angelo’s 2 locations in MI #1 hardscapes position in Detroit metro

AB Supply 12 locations in CA and NV Leading hardscapes platform in Southern California and Las Vegas

Evergreen Partners 2 locations in NC and SC #1 nursery position in Myrtle Beach & strengthened existing nursery position in Raleigh

South Coast Supply 2 locations in CA Leading hardscapes position in Orange County, CA

1 Trailing twelve months revenues in the year acquired

Source: Company filings, Press release

13

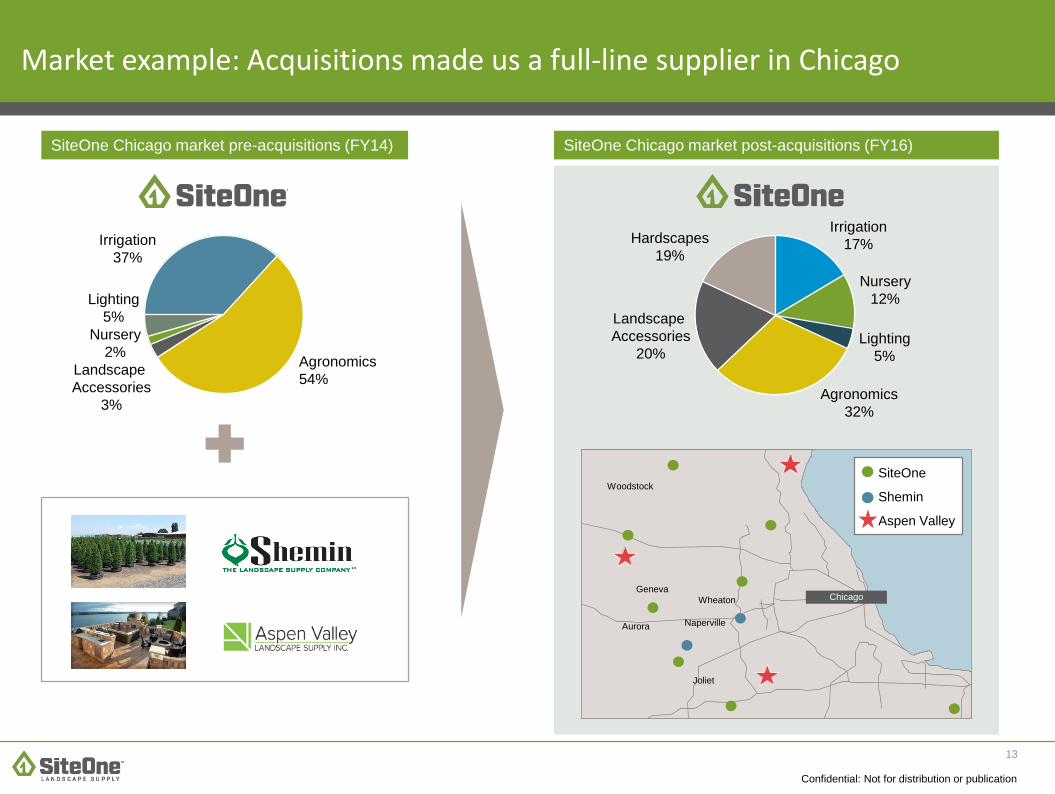

Confidential: Not for distribution or publication

Chicago

Woodstock

Geneva

Wheaton

NapervilleAurora

Joliet

SiteOne

Shemin

Aspen Valley

Market example: Acquisitions made us a full-line supplier in Chicago

Lighting

5%

Nursery

12%

Irrigation

17%Hardscapes

19%

Landscape

Accessories

20%

Agronomics

32%

Irrigation

37%

Lighting

5%

Nursery

2%Agronomics

54%Landscape

Accessories

3%

SiteOne Chicago market pre-acquisitions (FY14) SiteOne Chicago market post-acquisitions (FY16)

14

Confidential: Not for distribution or publication

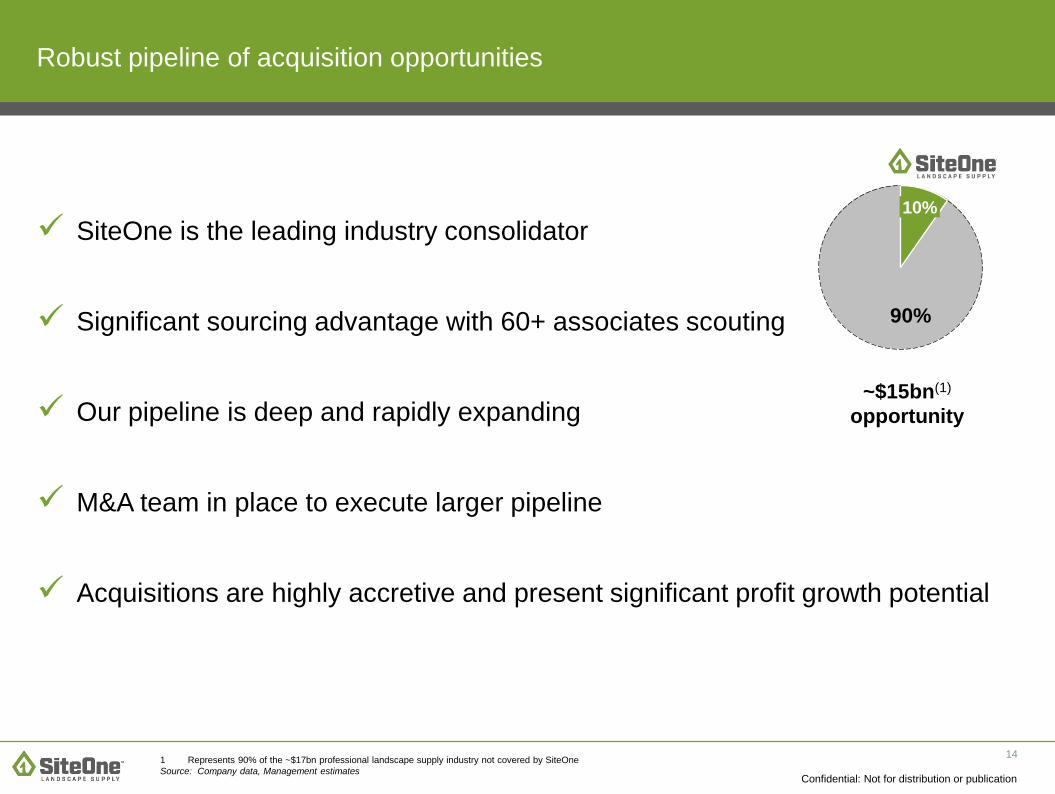

✓ SiteOne is the leading industry consolidator

✓ Significant sourcing advantage with 60+ associates scouting

✓ Our pipeline is deep and rapidly expanding

✓ M&A team in place to execute larger pipeline

✓ Acquisitions are highly accretive and present significant profit growth potential

Robust pipeline of acquisition opportunities

10%

~$15bn(1)

opportunity

90%

1 Represents 90% of the ~$17bn professional landscape supply industry not covered by SiteOne

Source: Company data, Management estimates

15

SiteOne’s 2017 outlook

✓ Underlying market trends remain positive

✓ Sales & marketing initiatives expected to accelerate market share gains

✓ Gross margin expansion expected to continue

✓ SG&A as % of net sales expected to decline slightly

✓ M&A activity continues to gain momentum from a robust pipeline

✓ 2017 Adjusted EBITDA expectation of $155 million to $165 million

Source: Company data

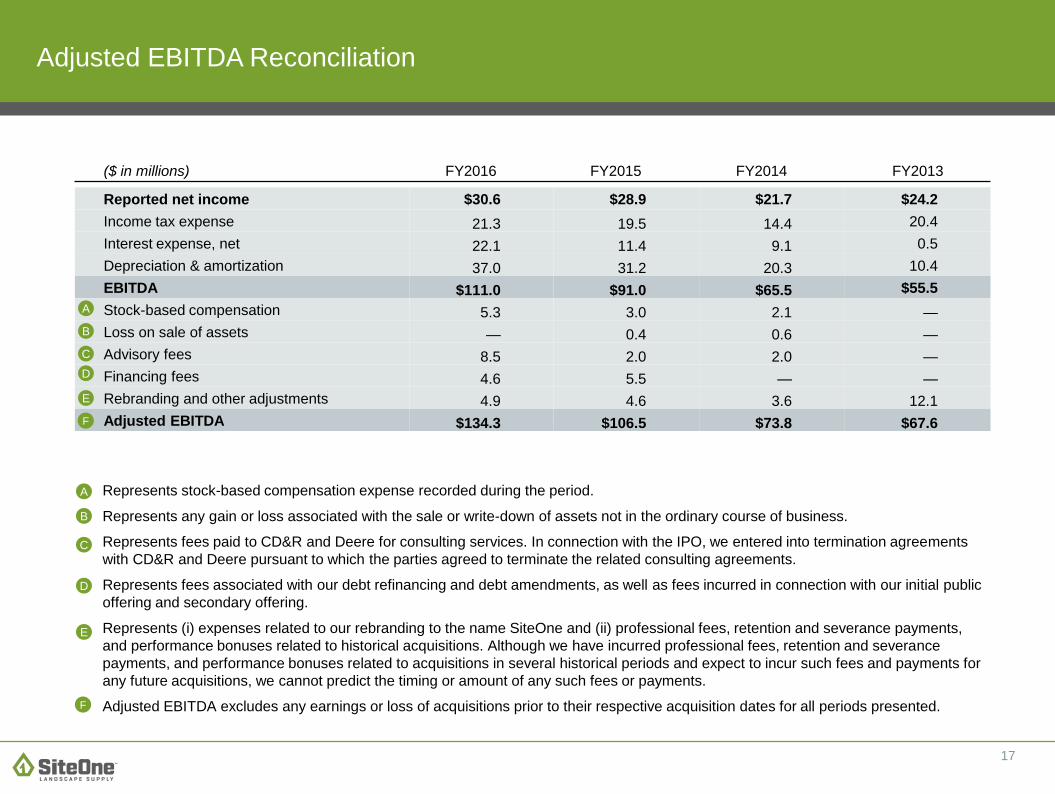

AppendixNon-GAAP Reconciliations

17

Adjusted EBITDA Reconciliation

($ in millions) FY2016 FY2015 FY2014 FY2013

Reported net income $30.6 $28.9 $21.7 $24.2

Income tax expense 21.3 19.5 14.4 20.4

Interest expense, net 22.1 11.4 9.1 0.5

Depreciation & amortization 37.0 31.2 20.3 10.4

EBITDA $111.0 $91.0 $65.5 $55.5

Stock-based compensation 5.3 3.0 2.1 —

Loss on sale of assets — 0.4 0.6 —

Advisory fees 8.5 2.0 2.0 —

Financing fees 4.6 5.5 — —

Rebranding and other adjustments 4.9 4.6 3.6 12.1

Adjusted EBITDA $134.3 $106.5 $73.8 $67.6

A

B

C

D

E

Represents stock-based compensation expense recorded during the period.

Represents any gain or loss associated with the sale or write-down of assets not in the ordinary course of business.

Represents fees paid to CD&R and Deere for consulting services. In connection with the IPO, we entered into termination agreements

with CD&R and Deere pursuant to which the parties agreed to terminate the related consulting agreements.

Represents fees associated with our debt refinancing and debt amendments, as well as fees incurred in connection with our initial public

offering and secondary offering.

Represents (i) expenses related to our rebranding to the name SiteOne and (ii) professional fees, retention and severance payments,

and performance bonuses related to historical acquisitions. Although we have incurred professional fees, retention and severance

payments, and performance bonuses related to acquisitions in several historical periods and expect to incur such fees and payments for

any future acquisitions, we cannot predict the timing or amount of any such fees or payments.

Adjusted EBITDA excludes any earnings or loss of acquisitions prior to their respective acquisition dates for all periods presented.

A

B

C

D

E

F

F

Recommended