International tax research beyond APB 23

Kevin Markle, University of Iowa

ATA Doctoral Consortium, Washington, D.C. February 25, 2015

Mark

le –

Inte

rnati

onal beyond A

PB

23

2

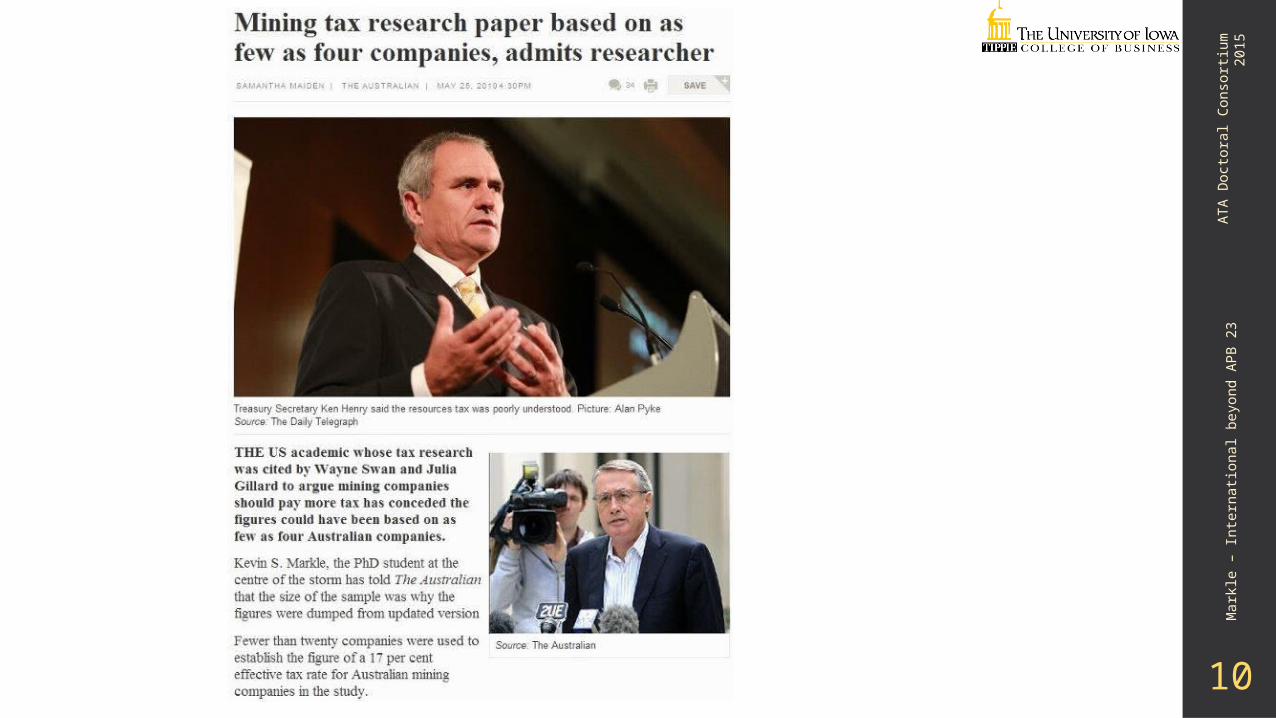

Main points1. The international tax research landscape

2. Our competitive advantage

3. With great power comes…

ATA

Doct

ora

l C

onso

rtiu

m

2015

Mark

le –

Inte

rnati

onal beyond A

PB

23

3

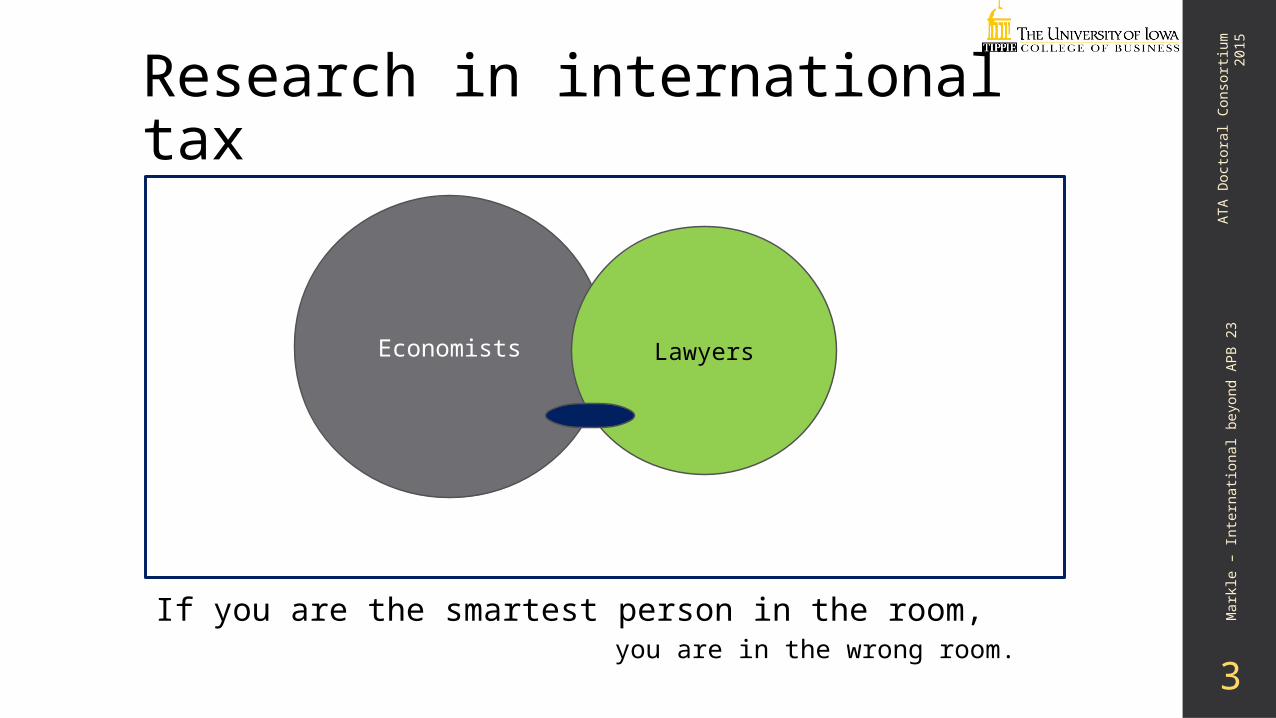

Research in international tax

If you are the smartest person in the room,

ATA

Doct

ora

l C

onso

rtiu

m

2015

you are in the wrong room.

Economists Lawyers

Accountants

Mark

le –

Inte

rnati

onal beyond A

PB

23

4

Our competitive advantageWe understand financial accounting

• Hanlon, Lester, and Verdi – The effect of repatriation tax costs on US multinational investment

• Edwards, Kravet, and Wilson – Trapped cash and the profitability of foreign cash acquisitions

• De Simone – Does a common set of accounting standards affect tax-motivated income shifting for multinational firms?

• Blouin, Huizinga, Laeven, and Nicodeme – Thin capitalization rules and multinational firm capital structure

• Dyreng and Markle – The effect of financial constraints on the tax-motivated income shifting of U.S. multinationals

ATA

Doct

ora

l C

onso

rtiu

m

2015

Mark

le –

Inte

rnati

onal beyond A

PB

23

5

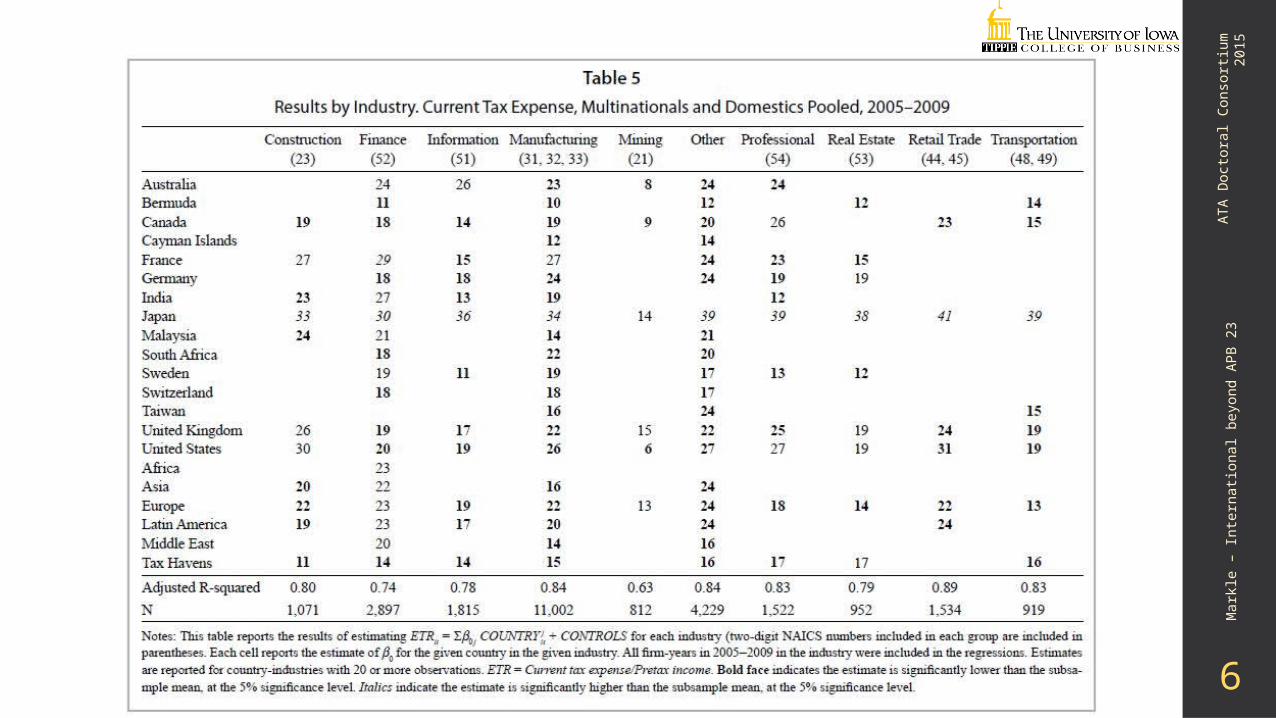

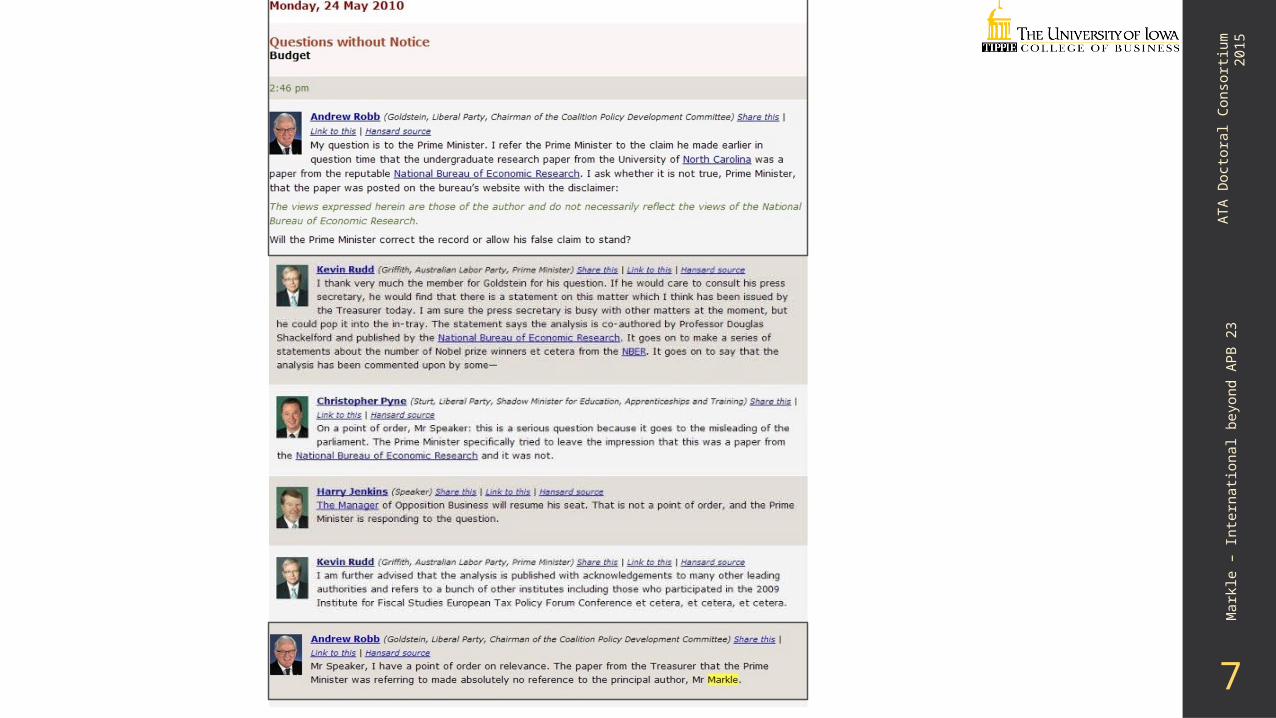

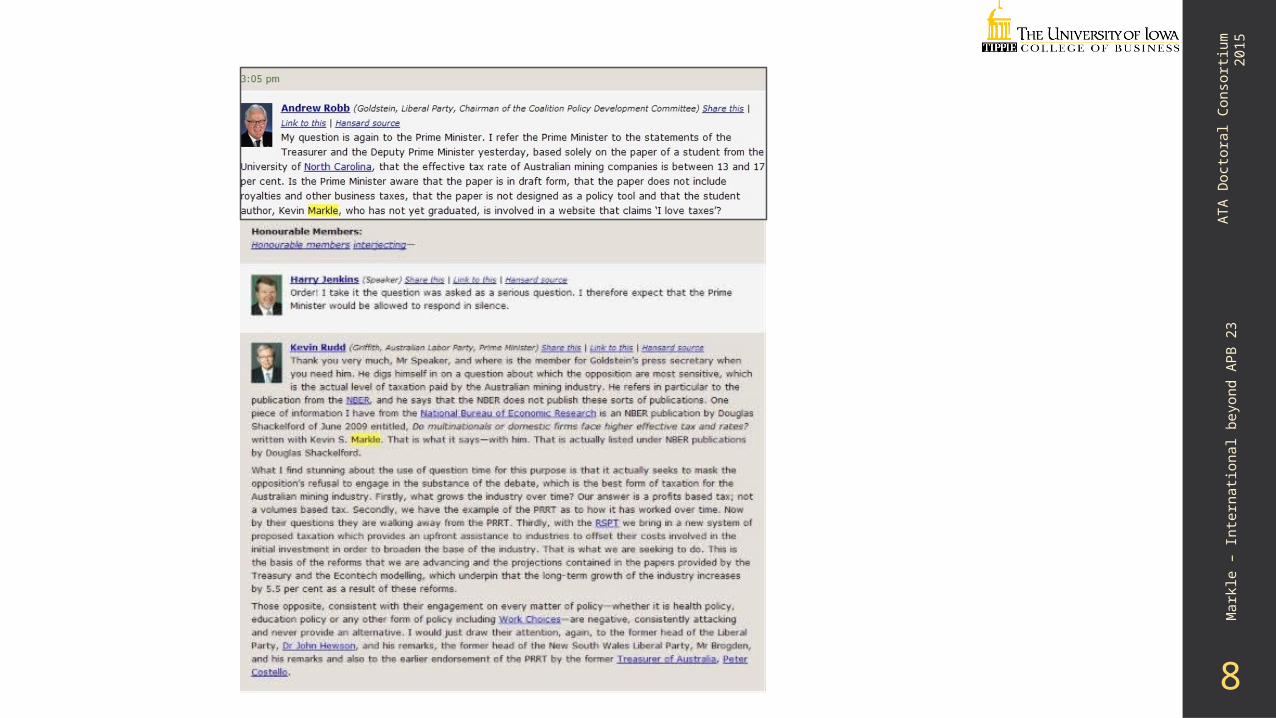

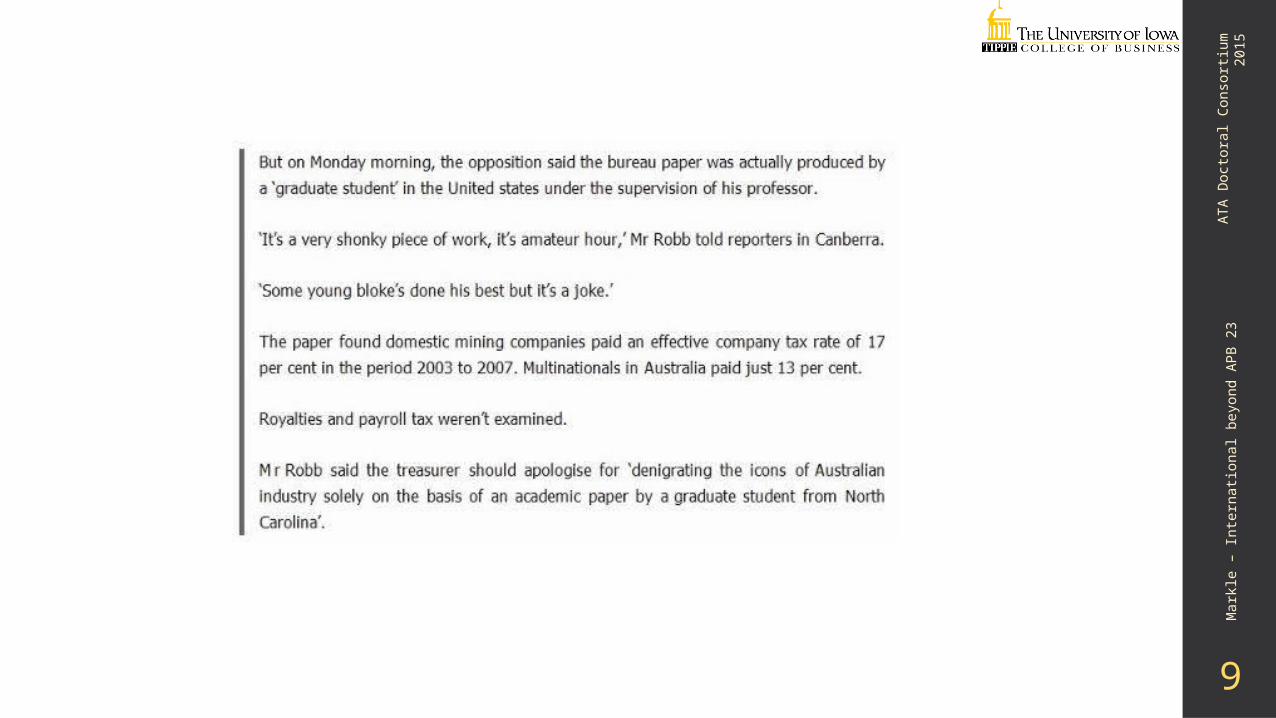

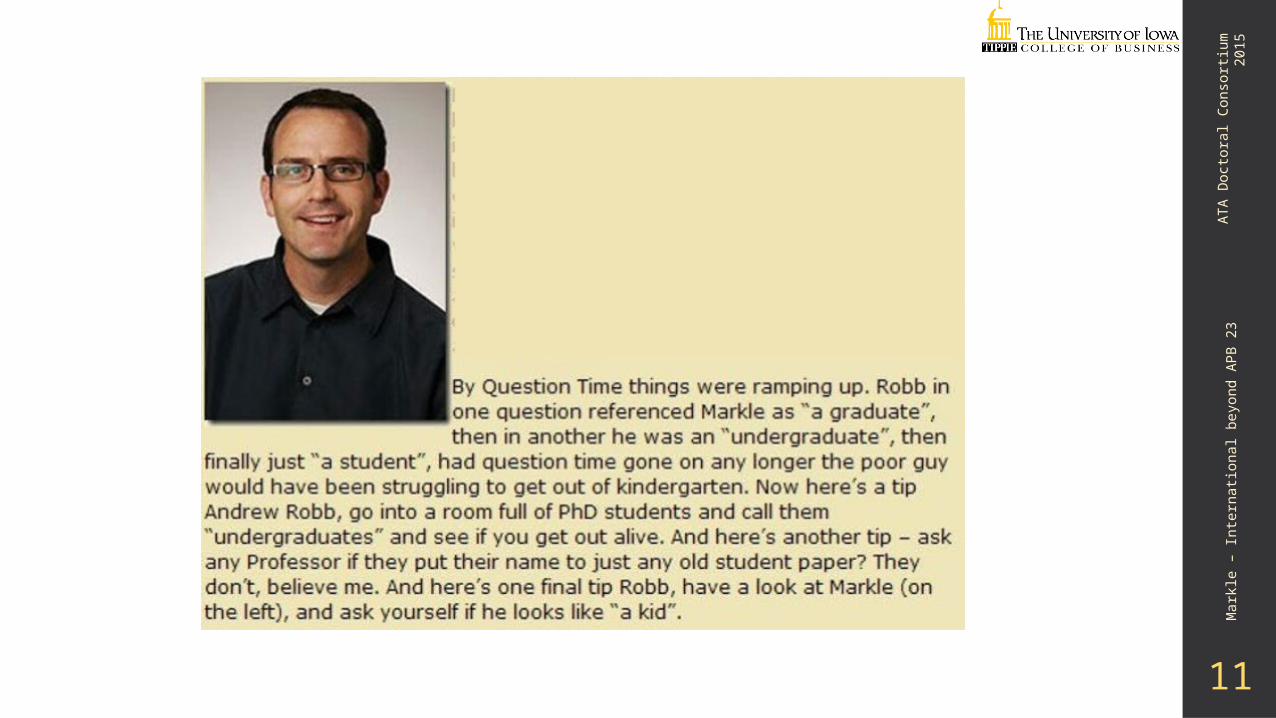

With great power comes…

ATA

Doct

ora

l C

onso

rtiu

m

2015

relevance

Mark

le –

Inte

rnati

onal beyond A

PB

23

6

ATA

Doct

ora

l C

onso

rtiu

m

2015

Mark

le –

Inte

rnati

onal beyond A

PB

23

7

ATA

Doct

ora

l C

onso

rtiu

m

2015

Mark

le –

Inte

rnati

onal beyond A

PB

23

8

ATA

Doct

ora

l C

onso

rtiu

m

2015

Mark

le –

Inte

rnati

onal beyond A

PB

23

9

ATA

Doct

ora

l C

onso

rtiu

m

2015

Mark

le –

Inte

rnati

onal beyond A

PB

23

10

ATA

Doct

ora

l C

onso

rtiu

m

2015

Mark

le –

Inte

rnati

onal beyond A

PB

23

11

ATA

Doct

ora

l C

onso

rtiu

m

2015

Mark

le –

Inte

rnati

onal beyond A

PB

23

12

We can contribute• OECD BEPS Project

Huge challenge is “measuring BEPS”

• Regime changes and tax reform We understand how existing data can be used in a quasi-experimental setting

ATA

Doct

ora

l C

onso

rtiu

m

2015

Recommended