INTERNATIONAL EXPERIENCE OF LONG TERM LIFE INSURANCE:

A MODEL PROPOSAL FOR EMERGING MARKETS

Dr. Ahmet Naim OKTAYYeditepe University

INTRODUCTION

Introduction•The Caucasia is a geopolitical region at the border of

Europe and Asia and situated between the Black and Caspian Sea. Politically, the Caucasus region is separated between northern and southern parts.

Introduction

IntroductionNorth Caucasia comprises of the following states:• Russian Federation (partially) → nominal GDP/Capita $12.993

▫ Chechnya Pop: 1.268.989▫ Dagestan Pop: 2.910.249▫ Ingushetia Pop: 412.529▫ Adyghe Pop: 439.996▫ Kabardino-Balkaria Pop: 859.939▫ Karachay-Cherkessia Pop: 477.899▫ North Ossetia Pop: 712.980▫ Krasnador Krai Pop: 5.226.647▫ Stavropol Krai Pop: 2.786.281

• Total Population 15.095.469

IntroductionSouth Caucasia consists of the countries below:• Azerbaijan (Pop: 9.165.000, nominal GDP/capita: $6.872• Georgia (Pop:4.469.000, nominal GDP/capita: $3.210• Armenia (Pop:3.262.200, nominal GDP capita : $3.032 Total Population : 16.896.200 As a result when we talk about Caucasia Region we talk about a population of 32.000.000. Of course this 32.000.000 belongs to different cultures and has different languages. But life insurance has a universal language which we will have a look in this study.

Introduction

2010Low income Countries 1005 – belowMiddle Income Countries 1006 – 12.275 Lower-Middle Income 1006 – 3.975 Higher-Middle Income 3.976 – 12.275High Income Countries 12.276 - above

The World Bank classifies countries according to their GDP per capita.

TABLE I: Classifications of World countries according to GDP/CapitaSource: Halil Seyidoğlu, International Economics p.12 & World Bank Report, p.75

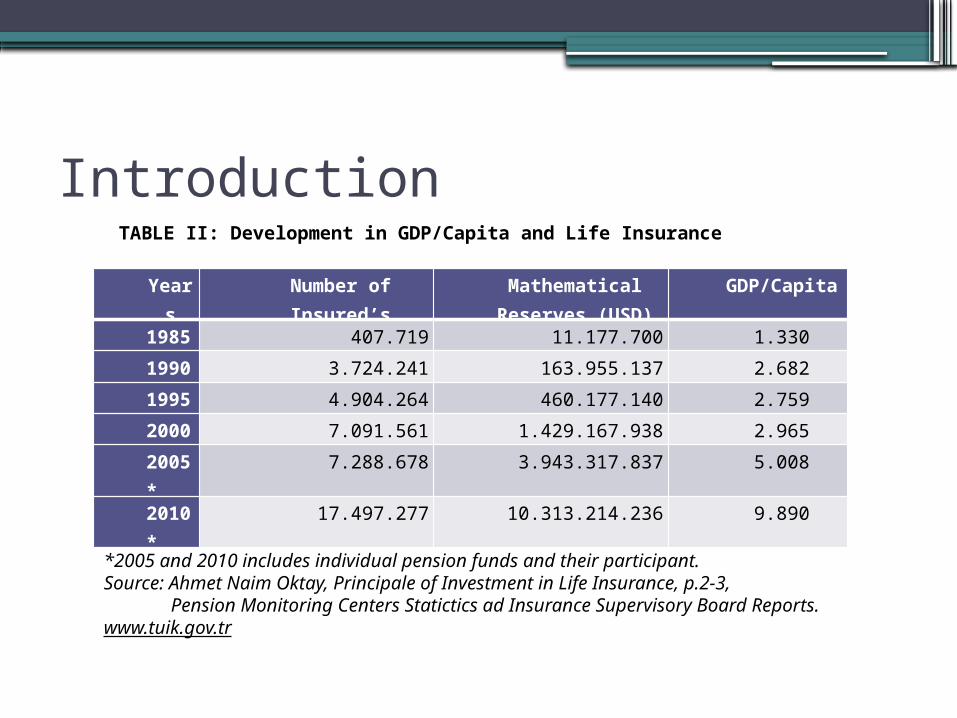

IntroductionTABLE II: Development in GDP/Capita and Life Insurance

*2005 and 2010 includes individual pension funds and their participant.Source: Ahmet Naim Oktay, Principale of Investment in Life Insurance, p.2-3, Pension Monitoring Centers Statictics ad Insurance Supervisory Board Reports.www.tuik.gov.tr

Years Number of Insured’s Mathematical Reserves (USD)

GDP/Capita

1985 407.719 11.177.700 1.330

1990 3.724.241 163.955.137 2.682

1995 4.904.264 460.177.140 2.759

2000 7.091.561 1.429.167.938 2.965

2005* 7.288.678 3.943.317.837 5.008

2010* 17.497.277 10.313.214.236 9.890

HISTORICAL DEVELOPMENT OF LIFE INSURANCE

Historical Development Of Life Insurance

The main motivation for life insurance is to provide financial assistance for people after the decease of the family’s breadwinner. • In ancient Greek • Rome•A rider to marine insurance policies

Historical Development Of Life Insurance

The first example of a life policy was issued in Great Britain in 1583.

▫ “Amicable Society for a Perpetual Assurance Office” 1757. ▫ Some mathematicians were working on mortality tables. ▫ Edmund Halley ▫ James Dudson (1755). ▫ Equitable Life Society established in 1762 ▫ Richard Dune and William Morgan to invent “whole life” policies.

• “insurable interest” in life contracts in 1774.• First products with profit sharing launched by Westminster Society

(1792) and Pelican Life Office (1797).

Historical Development Of Life Insurance

• After the industrial revolution, for both death and retirement benefit became a new trend.

• In parallel with increasing inflation and volatilities in 1970’s, Universal Life policies

• Several life insurance companies had to be liquidated

• Balwin United (1983). Executive Life (1991), First Capital Life (1991), Fidelity Bankers Life, Monarch Capital Corporation, Mutuel Benefit (1991).

Historical Development Of Life Insurance

• In order to protect insured’s from this kind of financial disasters, states brought new regulations ▫The solvability▫The transparency▫The audit and rating.

THE IMPORTANCE OF LIFE INSURANCE IN TERMS OF

ECONOMICS

Impact of Life Insurance on Macro-Economics

Some researches showing that insurance market has significant roles in promoting economic growth. The process of economic growth requires investment and increases in real savings.

Impact of Life Insurance on Macro-Economics

• There are a lot of instruments of which people can save ▫accounts in the banks, securities, bonds, etc.

• But life assurance provides protection from economic loss of an unexpected death, people can also save through their life

• We can say that, premium payment may be considered as a semi-compulsory saving.

Impact of Life Insurance on Macro-Economics

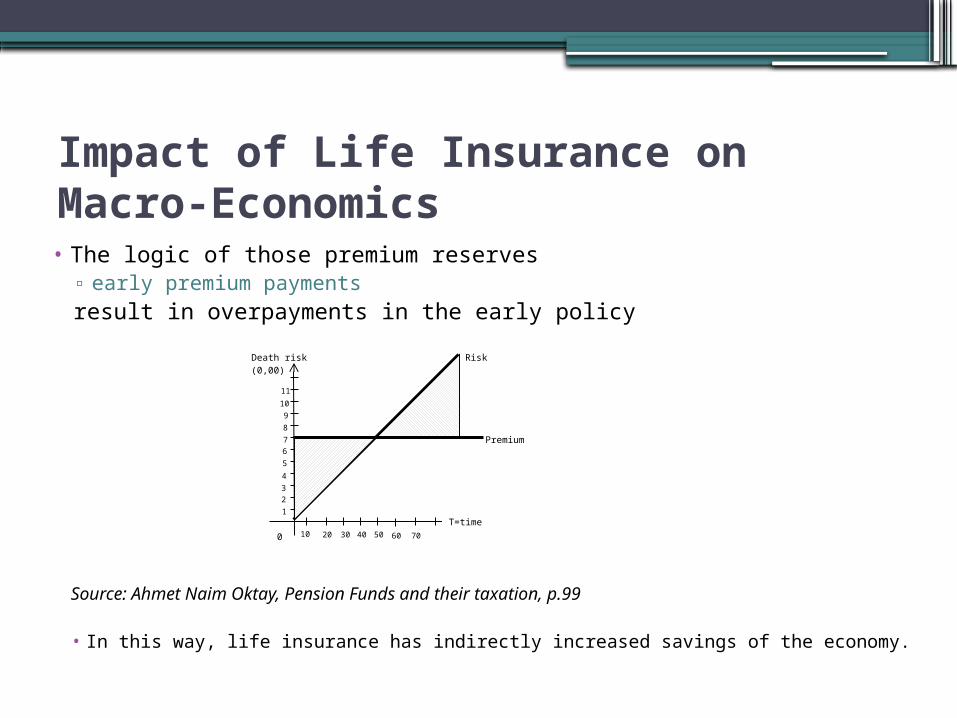

• The logic of those premium reserves ▫ early premium payments result in overpayments in the early policy

Death risk (0,00)

T=time

0 10 20 30 40 50 7060

1234

56789

10

11

Premium

Risk

Source: Ahmet Naim Oktay, Pension Funds and their taxation, p.99

• In this way, life insurance has indirectly increased savings of the economy.

Impact of Life Insurance on Macro-Economics

• TABLE III: Life premium volume in USD in 2010

• Source: Sigma, World Insurance in 2010, Statistical Appendix, p.10

• The life insurance premium composes 57,9% of the total premium volume which is USD 4.324.239 million.

Region Premium Volume(in millions of

USD)North America 557.007Latin America and Carrabin

54.458

Europe 955.553Asia 858.466Africa 42.796Oceania 39.436TOTAL 2.507.715

Impact of Life Insurance on Macro-Economics

An empirical and theoretical study done in Nebraska shows us

• that one percentage point increase in the growth of life insurance industry is associated with a 0,25 per cent increase in the growth rate

• the life insurance growth explains approximately 14% of the variance of economic growth

Impact of Life Insurance on Macro-Economics

• Insurance and pension sector normally induces a superior GDP growth then other sectors.

• Source: TSSRB, Shaping our future: 2023 vision for Turkish Insurance Sector, 2012, p.6

Impact of Life Insurance on Macro-Economics

Europe • produces 38% of life premiums, in the world

• life insurance reserves and in pension funds reserves was 1.442.643 million of euro in 2011

Impact of Life Insurance on Household’s Economics

• The family as a smallest unit of the society and economy

Impact of Life Insurance on Household’s Economics

Keep in mind some differences from general insurance: ▫ risk namely “death” is certain. ▫ life insurance is a long-term contract▫ It is difficult to determine the economic or the financial value

of life.▫ life insurance contract is not a contract of indemnity.▫ the premium is calculated according to mortality table.

Impact of Life Insurance on Household’s Economics

• Different economic uses life insurance offers:• Life insurance makes the family financially secure.• Life insurance is also a saving instrument.• Helps in meeting responsibilities of even after death like higher

education of children, • Helps in repaying the mortgage loans• Life insurance also provides old age benefits, • Creditors can also use it in case of non-repayment

Impact of Life Insurance on Household’s Economics

People are likely to change their saving behaviour if they have life insurance• they feel less necessary to accumulate funds• policy loans are utilized as an emergency fund• insurance helps reducing worry and fear

▫peace of mind, • increases the happiness of individuals.

Impact of Life Insurance on the Micro-Economics

• Partners of firm can get the lives of the partners insured

• A firm can get the life of its key man insured

• Group insurance policies can improved productivity.

• Industry offers regular full time employment to a large number of people

TYPES OF LONG TERM LIFE INSURANCE

Types of Long Term Life Insurance

• Term life insurance

• Whole life insurance

• Endowment insurance

• Pensions

Term Assurance Plans• protection for a limited number of years.• no maturity value.• The face amount of the policy is payable only if the insured’s

death occurs.• Nothing paid in case of survival• Can be issued for a short period but customarily provides

protection for at least a set number of years, • Since price of terms products of different companies can be

easily comparable, a wide variety product diversification was made

Term Assurance Plans• Level term assurance: The amount insured is at a fix level

within the term of the policy.• Renewable Term Assurance: The insured can renew his

policy at maturity date without any medical examination.• Convertible Term Assurance: The insured can convert his

policy into a whole life or endowment policy at any time he wants.

• Decreasing Term Assurance: These policies are commonly used to pay off a loan balance on the death of the debtor, insured e.g. mortgage protection plan.

Term Assurance Plans• Expanding Term Assurance: Fixed Death Benefit may cause a decrease

in real terms during the period of the policy. This policy gives the opportunity to increase death benefit at a fixed rate each year.

• Index-linked Term Assurance: This type of policies gives a rise to the amount insured according to the consumer price index.

• Unit linked Term Assurance: The premium paid by the insured are allocated to purchase “units”. If the value of the limits is higher than the amount defined at the inception of the policy, this surplus is paid to the insured.

• Money back Policies: In case of a death, the amount insured is paid to the beneficiary of the policy. If the insured survives at maturity date, the premium is refunded.

Whole Life (Straight Life) Policies•Whole life insurance provide protection over one’s

entire life time. •Payment of the face amount upon the insured’s death

regardless of when death occurs.•Terminal age in all mortality tables is 100 years. •Cash values are available by surrendering the policy.• Loan can be obtained.

Whole Life (Straight Life) Policies• For a $ 100.000, straight life policy issued at age 35, for example, the cash value

may be $5.000 after five years and $12.000 after ten years, $28.000 after twenty years and $100.000 after sixty-five years.

FİGURE: Joseph M Belth, Life Insurance a consumer’s handbook

Whole Life (Straight Life) Policies•Policies paying a set benefit ordinary whole life policies

are certainly sold, however investment linked benefits are more common. Policies with profits (also termed “participating”),

•Another variation is unit-linked cover. Once the number of units possessed known, the policyholder can quickly value the policy as the unit price is publicly quoted.

Whole Life (Straight Life) Policies

•Universal Life Policies launched in USD in 1970’s and still a good product for emerging market.

• It has two main characteristics: Transparency and Flexibility.

Whole Life (Straight Life) Policies

•Transparency is achieved by breaking down the contract into its three components:▫The protection component▫The saving’s component and▫The expense component

•The second main characteristic is the “flexibility” of charging the face amount, premium payments and cash value

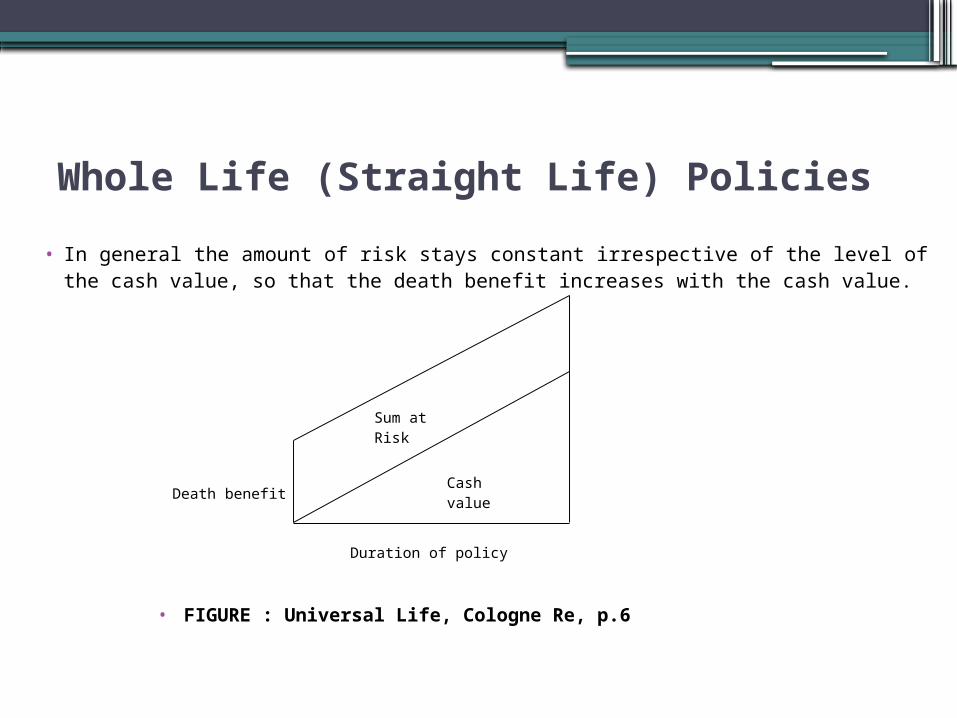

Whole Life (Straight Life) Policies• In general the amount of risk stays constant irrespective of the level of the cash

value, so that the death benefit increases with the cash value.

• FIGURE : Universal Life, Cologne Re, p.6

Death benefit

Sum at Risk

Cash value

Duration of policy

Endowment Insurance• Endowment policies promise

▫ the policy face amount on the death of the insured during ▫ to pay the full-face amount at the end of the term of the insured services the term

FIGURE: Diagram of Hypothetical Twenty-Year Endowment• Source: Joseph M.Belth, p.43

Endowment Insurance

Endowment policies may be diversified as follows:• Single premium endowment policies.• Retirement income policy: the amount payable at death is the

face amount or cash value, whichever is greater.• A semi endowment policy-pay upon survival.• Modified endowment policy-provides for payment periodically.• Deposit term- First year premium were not to be higher than

renewed premiums.• Juvenile endowment policies – designed to cover child’s

education, marriage, and independence

Endowment Insurance

Those policies can be with profit or without profit. Cash value of the policy that is to say the mathematical reserves of the company is allocated for investment on financial instruments and real estates.

The periodical (usually yearly) return of those investments is shared between the company and the insured at a defined percentage.

Endowment Insurance

• In unit linked policies, an investment fund is established and divided into “units”. Each unit has a daily value. The number of unit obtained by the policy owner and the value of each unit gives us total cash value.

•The policyholder has the option of investing across various schemes, i.e. diversified equity funds, balanced funds, debt funds etc.

Endowment Insurance

Pension (Retirement) PoliciesThere are two main types of Pension products.

▫ Defined – benefit▫ Defined contribution

• In defined benefit, ▫ the capital or the annuity to be paid at the maturity date is known. ▫ The actuarial formula being used is the same as “defined capital”

or “deferred annuity” formulas. ▫ The increasing longevity of life and fluctuation of interest in the

market may cause problem• Defined contribution product is an investment plan• The investment principle is almost the same with unit-linked

policies.

GOVERNMENTAL SUPPORT

Governmental Support

•The governments support life insurance due to the reason stated in chapter 3.

•Additionally, life insurance serves as a complementary benefit to social security.

Governmental Support• Turkish social security has an annual institution deficit > TL 25b...• Total revenue and expenditure of Social Security Institution• Billion TL

2000 01 02 03 04 05 06 07 08 09 2010

• Source: TSSRB; Shaping our future: 2023 vision for Turkish Insurance Sector, 2012, p.9

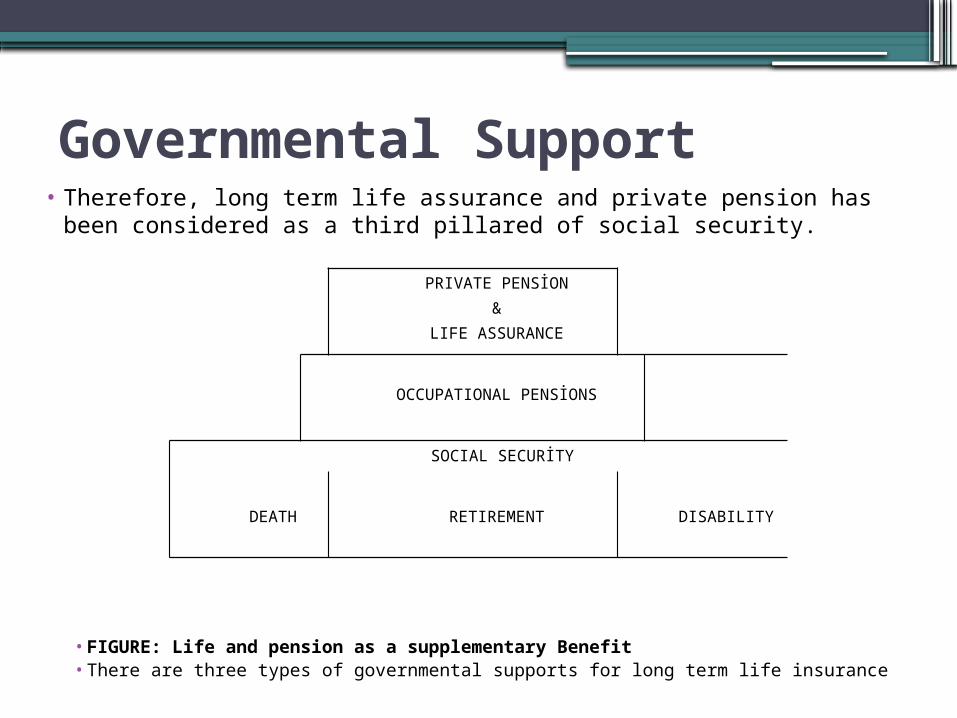

Governmental Support• Therefore, long term life assurance and private pension has been

considered as a third pillared of social security.

• FIGURE: Life and pension as a supplementary Benefit• There are three types of governmental supports for long term life insurance

PRIVATE PENSİON&

LIFE ASSURANCE

OCCUPATIONAL PENSİONS

SOCIAL SECURİTY

DEATH

RETIREMENT

DISABILITY

Regulations as to Transparency of Life Insurance

• Each year the global economy adds an estimated 150 million new customer of financial services.

• Even in well-developed markets, weak consumer protection and a lack of financial literacy can render households vulnerable to unfair and abusive practices by financial institutions as well as financial frauds and scams operated by intermediaries.

• At its heart, the need for consumer’s protection arises from an imbalance of power, information and resources between consumers and financial service providers

Regulations as to Transparency of Life Insurance

•A financial sector should provide consumers with:•Transparency by providing full, plain, adequate and

comparable information•Choice by ensuring fair, non-coercive and reasonable

practices• inexpensive and speedy mechanism to address

complaints and resolve disputes.

Financial Transparency

• Insurance companies have a great importance

▫by alleviating the financial hardship if a covered risk takes

▫by giving a considerable amount of saving, providing financial security

Financial Transparency• That is why the supervisory authorities impose rules to

facilitate customer’s periodic control on their on-going contracts as

For this reason;▫ The customer should receive periodic statements ▫ Customers should have a means to dispute the accuracy of

the statement within a stipulated period.▫ Insurers should be required to disclose the cash value within

a reasonable time. ▫ a table showing projected cash values should be provided at

the time of delivery of the initial contract

Financial Transparency• As a general rule;

▫Every insurance undertaking is required to establish an available solvency margin

▫The solvency margin shall correspond to the assets free of any foreseeable liabilities less any intangible item.

▫Detailed rules of assets that can be included in the available solvency margin.

• Solvency I rather crude “one size fits all” sets of rules. • It only considers underwriting risk. The rules are not

designed to take into account credit, market or liquidity risk.

Financial Transparency•European Commission announced that they were going

to “take a global lead in insurance regulation” …. by 2013.

•The Solvency II exercise envisages a principals Basel II approach. The insurers assess their capital needs, degree of volatility, availability of reinsurance other risk factors such as credit, market and liquidity risks.

Contractual TransparencyConsumer products can be broken into three categories: • search goods (can be assessed in advance of purchase-

e.g. a piece of art), •experience goods (can be assessed relatively quickly

with use- e.g. soap powder), • credence good (attributes only discovered after a long

delay or upon occurrence of contingent event or never- e.g. a mutual fund). Insurance clearly fits into the credence good category and the sector thus relies heavily on the public’s trust

Contractual Transparency

• the aim of policy holder protection should surely be to:

a) Protect policyholders against losses arising from fraudb) Ensure that policyholders are not misledc) Prevent insurers from unfairly avoiding claims.d) Provide compensation for policyholders

Contractual Transparency• An insurance contract -likewise other legal contract- is

supposed to be concluded with good faith. • Good faith “bona fide” might require the parties to;

a) keep every promise which is made,b) negotiate in such a way as to avoid taking advantage of anotherc) do one’s best to complete the negotiations,d) act fairly an honestly,e) co-operate,f) inform the other party of all the needs to know,g) avoid lies and misleading conduct,h) abstain from fraud

Contractual Transparency• recent development in consumer rights and protection

obliges insurers to bear their responsibility arising out of the duty of “disclosure” as a matter of good faith.

•The information would cover:▫the status of insurer▫the value and type of assets in the fund;▫the rates of return generated on the assets;▫the fees or commissions charged

Contractual Transparency• As to the transparency in life assurance, according to the Art.36

and annex 111 of Directive 2002/83/EC, a written information to policyholders must be submitted relating to the definition of benefits, term of the contract, means of payment of premiums, surrender value and paid-up value (if any) and a cancellation period. Art 35 states that the policyholder has to have the opportunity to cancel the contract within a period of between 14 and 30 days from the time the policy holder was informed that the contract was incepted (cooling of period). Since the life insurance contract is a long-term contract, individual may be persuaded by high pressure salesmanship to enter into contracts which may not be entirely appropriate for them.

Contractual Transparency

•What remedies are available to the victim of bad faith?

▫Avoidance (rescission)▫Termination of the insurance contract▫Compensation

Tax Incentives• In many countries long-term life and pension premiums

contribution payment are encouraged through tax exemptions.• One way of this tax relief is called tax deduction.• The other way is tax credit method. It is a direct, dollar-for-

dollar reduction in tax liability, as distinguished from a tax deduction, which reduces taxes only by the percentage of a taxpayer’s Tax Bracket (A taxpayer in the 31% tax bracket would get a 31 cent benefit from each $1,00 deduction, for example). In the case of a tax credit, a taxpayer owing $10.000 would owe $ 9.000 of the took advantage of a $1,000 tax credit.

Tax Incentives•Also accumulated funds and mathematical reserves

return are encouraged by means of tax exemptions to some extent.

•Also, the capital and annuities payment can be exempted from taxes.

•We must confess that, in emerging markets where tax payment behaviour is not very strong,

Governmental Sponsorship• One of the method which is very efficient is the participation of

a government or a company into the premiums payment of the policies.

• In this method, let’s say a percentage of 25% is added by sponsor to the premium paid by insured. If the insured wait till his contract’s maturity date, he can obtain this additional fund consisting of the sponsor’s payments and its return. In case of surrender his policy within 10 years only 50% of the sponsored fund is paid to him. Additional fund may not be paid to the insured if the policy is surrendered within the first five years.

HOW TO SELL LONG-TERM LIFE INSURANCE

How to Sell Long-Term Life Insurance•At the first stage, some distribution channels like wise

internet, call center, banks even agencies have difficulty even in understanding various aspects of the long term life insurance policies.

•For this reason, a direct seller of an insurance produced must act as a financial advisor as well. ▫a special training, ▫some conditions of academic background ▫presentability is necessary.

How to Sell Long-Term Life Insurance• As to the advertising, a sufficient budget should be allocated.

• A list of potential customer is a useful instrument to reach the client.• The customer should be provided for a file and demonstration explaining the

product. Also, an explanatory note presenting the produces must be read and signed by the customer.

Sales & Marketing

Department

ZONE I ZONE II ZONE III

CONCLUSION : A MODEL PROPOSAL FOR

EMERGING MARKET

States Sponsorship

• in Turkey 65% of the insured cannot benefit from tax deduction.

•Thus a governmental sponsorship is very important to motivate people in purchasing long term life insurance policies.

Regulation for Transparency•The customer must be aware of

▫all loadings on the policy ▫an easily readable, understandable and comprehensive

text should be prepared.

•The public authority must announce the principles,▫check the actuarial aspect of the product ▫control advertisement against unfair competition.

Distribution Channels

• Long term life and pension product are allowed to be sold only through approved salesmen.

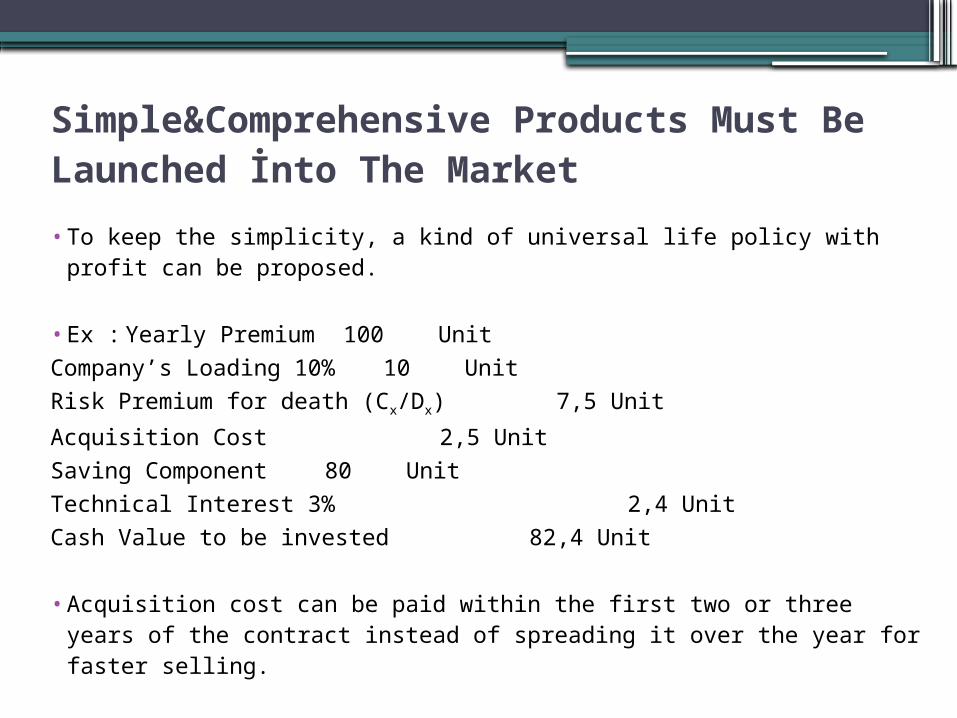

Simple&Comprehensive Products Must Be Launched İnto The Market• To keep the simplicity, a kind of universal life policy with profit can be

proposed.

• Ex : Yearly Premium 100 UnitCompany’s Loading 10% 10 UnitRisk Premium for death (Cx/Dx) 7,5 UnitAcquisition Cost 2,5 UnitSaving Component 80 Unit Technical Interest 3% 2,4 UnitCash Value to be invested 82,4 Unit

• Acquisition cost can be paid within the first two or three years of the

contract instead of spreading it over the year for faster selling.

Assistance Benefit

•Since long-term life assurance is a long term commitment, it is strongly advised to give a cheap fringe benefit to the policyholder to fortify his confidence. This assistance may be a medical call center service or “concierge” only.

Dispute Settlement

•Direct information and notification with the policyholder will be highly recommended through normal post and call canter to decreases cancellation and lapses of contracts.

THANKS

Dr. Ahmet Naim OKTAY

Recommended