Interest Rate and Financing of Islamic Banks: Evidence from Pakistan

Maria Hashim

Lecturer,Institute of Business and Management Sciences (IBMS),

Muhammad Nouman

Lecturer,Institute of Business and Management Sciences (IBMS)

Zahoor Khan

Assistant Professor, Institute of Management Sciences

Abstract

Islamic banks are not allowed to charge interest; however, they use interest-based benchmarks as

a pricing reference, due in part to the absence of stable and dependable alternatives. Though,

benchmarking interest rate in Islamic banking does not violate the Shariah rulings. However, it is

usually argued that benchmarking interest rate violates the basic philosophy of Islamic banking

and finance. Moreover, it exposes Islamic banks to the problems of conventional banks,

particularly the interest rate risk. The present study investigates the long term and short

association among interest rate and financing of the overall Islamic banking industry of Pakistan

via different modes. Findings of the study reveal invariably strong links between the Islamic and

the conventional banking systems in Pakistan. These findings suggest that paradoxical as it may

seem, the financing of Islamic banks operating within a dual banking system are vulnerable to

interest rate risk.

Keywords: Islamic banking, benchmarking interest, Interest rate risk, Pakistan

1. Introduction

Islamic banking is a growing rapidly in the Muslim countries and the primary world financial

hubs (Nouman, Ullah, & Gul, 2018). There are more than 300 institutions carrying out interest

free banking in 80 countries. These institutions provide interest free financial services to their

clients, including not only Muslims but also non-Muslims who are having an extreme interest in

the financial products of Islamic banks (Awan, 2009).

Despite the impressive growth of Islamic banking throughout the world, a comprehensive

Islamic financial system is still in its nascence (Nouman et al., 2018). Many issues and

challenges related to the Islamic financial system and its various aspects need to be addressed

yet. Among these is the issue of using interest rate as a benchmark by Islamic banks. Although

Islamic banks do not charge interest, however, they use interest-based benchmarks as a pricing

reference, due in part to the absence of stable and dependable alternatives (Ayub, 2007; El-

Gamal, 2006; Reuters, 2016; Usmani, 2002b).

Many advocates of Islamic banking favor benchmarking interest rate (See for example El-

Gamal, 2006; Hamoud, 1994; Jaman, 2011; Usmani, 2002a). They justify Interest as a

benchmark on the grounds that Islamic banking being a niche market has to co-exist with the

conventional banking (See for example, Hamoud, 1994, Usmani, 2002a). Islamic banks have to

use interest rate as a benchmark to remain competitive and be able to attract deposits from

customers (Jaman, 2011). Moreover, it helps in avoiding arbitrage in the dual banking

environment (Bacha, 2004; Jaman, 2011). Aznan Hasan who is a Shariah advisor to Malaysia's

stock exchange Bursa Malaysia opined in an interview that the presence of two separate

benchmarks for the Islamic and conventional banks will result into a severe turbulence in the

country. In fact, it would open ways to arbitrage i.e., if people see conventional financing

suitable in a given situation, they will switch to conventional financing and vice versa.

On the contrary, many Islamic scholars criticize benchmarking interest as not being adequately

based on real economic activity, which is a core requisite in Islamic finance (Reuters, 2016).

Moreover, it violates the basic philosophy of Islamic banking and finance (Usmani, 2002b) and

makes the transactions of Islamic banks indistinguishable from those of conventional banks

(Ayub, 2007). Therefore, though benchmarking interest rate in Islamic banking does not violate

the Shariah rulings1, it is heavily criticized and has become a subject of debate (Jaman, 2011).

Furthermore, Benchmarking interest rate is not without implications. Though Islamic banking is

interest free, benchmarking interest rate exposes Islamic banks to the problems of conventional

banks, particularly the interest rate risk2 (Bacha, 2004; Rosly, 1999). According to Bacha (2004)

1 Benchmarking interest for estimating the profit or loss of a permitted transaction does not make the transaction

Haram or invalid. Rather the validity of a transaction is determined by its mechanism/nature. (Ayub, 2007).

2In the context of banking system, interest rate risk refers to the effect of changes in interest rate on the net worth,

profits, and/or cash flows of a bank (Bacha, 2004).

Benchmarking interest rate leads to invariably strong links between the Islamic and the

conventional banking systems. This leads to several implications particularly when a large non-

Muslim customer base exists. First, due to strong association between the two banking systems,

there is a possibility of arbitrage between the systems, particularly by the non-Muslims who are

indifferent towards both banking systems. This in turn implies that deposit rates within the

Islamic banking system must change with adjustments in the prevailing interest rate in the

conventional system. Otherwise, rate differentials will prevail leading to arbitrage opportunities.

Third, due to opportunities of such risk free arbitrage through fund flows, Islamic banks become

vulnerable to the repercussions of interest rate volatility that normally pertain to the conventional

banking system. For example, the costs of funds of Islamic banks will change with changes in

the cost of funds of the conventional banking system. Thus, though the effect of interest rate

variation on the Islamic banking industry may be indirect, the repercussions would be the same.

A vast literature has stemmed from this debate. Several studies have empirically investigated the

impact of interest on different aspects of Islamic banks (See for example Haron & Ahmad, 2000;

Kolapo & Fapetu, 2015; Relasari & Soediro, 2017; Shamsuddin, 2014; Zainol & Kassim, 2010).

However, an important concentration apparent within the extant literature is the over-whelming

attention given to the effect of interest rate on the deposits, profitability, risk, and stock prices of

Islamic banks; whereas the financing side of Islamic banks remains relatively unexplored. To

bridge this gap the present study empirically investigates the effect of interest rate on the

financing of Islamic banks operating in Pakistan. Using quarterly data for the time period March-

2003 to September-2018, this paper argues that paradoxical as it may seem, the financing of

Islamic banks operating within a dual banking system may also be vulnerable to the interest rate

risk.

The reset of the paper is structured as follows: section 2 elaborates an integrated review of the

literature, followed by research methodology in section 3. Empirical results and findings are

presented and contextually discussed in section 4, while section 5 concludes the paper.

2. Literature Review

Islamic banking, being based on Islamic principles, discourages interest (Riba) and endorses the

concept of profit sharing (Nouman & Ullah, 2014; Warde, 2000). Therefore, it is characterized

by an array of unique Shariah compliant financial services (Hearn, Piesse, & Strange, 2012).

However, due to the absence of a stable benchmark, Islamic banks are using interest-based

benchmarks as pricing reference for all products throughout the world (Ayub, 2007; Reuters,

2016; Usmani, 2002b).

Benchmarking interest has become a subject of debate in the Islamic banking and finance

literature (Jaman, 2011). Moreover, it has opened several avenues for research. Several studies

have investigated the effect of interest rate on different aspects of Islamic banking industry. For

example; various studies have considered the impact of interest rate on the profitability of

Islamic banks (See for example Gul, Irshad, & Zaman, 2011; Haron, 1996; Khan & Sattar, 2014;

Malik, Khan, Khan, & Khan, 2014). Similarly, many researchers have investigated the effect of

interest rate on deposits of Islamic banks (See for example Akhtar, Akhter, & Shahbaz, 2017;

Hakan & Gülümser, 2011; Haron & Ahmad, 2000; Haron & Azmi, 2005; Kolapo & Fapetu,

2015; Relasari & Soediro, 2017; Yap & Kader, 2008; Zainol & Kassim, 2010). Whereas, the

impact of interest rate on the stock prices of the Islamic banks was considered by Ayub and

Masih (2013), Hussin, Muhammad, Abu, and Awang (2012) and Shamsuddin (2014).

On the contrary, literature on the link between interest rate and the financing of Islamic banks is

relatively limited. Few studies have investigated the effect of interest rate on the financing of

Islamic banks in the Malaysian context. For example, Yusoff, Rahman, and Alias (2001)

attempted to investigate the effect of interest rate on the supply of Islamic financing in Malaysia.

They found that the growth of the growth of financing in Islamic banking is significantly

influenced by changes in interest rate. While, Yap and Kader (2008) and Kader and Leong

(2009) empirically investigated how interest rate fluctuations in a dual banking system effects

the demand for the financing Islamic banks. Using monthly data of Malaysian Islamic banks for

the time period 1999 to 2007, they found that any rise in the base offering rate would motivate

profit oriented clients to gain funding from Islamic banks and vice versa. The study concluded

that Islamic banks, though operating on interest free ideologies, are prone to interest rate risk due

to the fact that most of the customers are profit seekers. Similarly, Khalidin and Masbar (2017)

investigated the effect of interest rate on Islamic banks’ financing in the Indonesian context.

However, by far, the link between interest rate and financing of Islamic banks remains

unexplored in the context of other countries. Hence, the current study contributes to the extent

literature by investigating the link between interest rate and the financing portfolio of Islamic

banking industry in the Pakistan.

3. Research Methodology

3.1 Data and variables

In this research secondary data has been used. Quarterly data on the financing mix of Islamic

banking industry for the time period December-2003 to September-2018 was obtained from

Islamic banking bulletins issued by the Islamic banking department (IDB) of State Bank of

Pakistan (SBP). The financing mix of the Islamic banking industry includes the financing of all

scheduled Islamic banks operating in Pakistan via different modes. Among different modes of

financing, the most dominant modes including Murabahah, Diminishing Musharakah, Ijarah,

Salam, Istisna, Musharakah, and Mudarabah were considered for the present study. On the other

hand the time series quarterly data of interest rate was collected from the SBP official website.

Since, in Pakistan Islamic banks use Karachi Inter Bank Offer Rate (KIBOR) as a benchmark for

determining the cost of financing. Therefore, KIBOR was used as proxy for interest rate.

3.2 Statistical Tests and Model

Different statistical tools were used for the analyses of the data. The Phillips Perron (PP) and

Augmented Dickey-Fuller (ADF) tests were used for testing the unit root problem at level and 1st

difference of each series. Moreover, the multivariate Johansen and Jusiles (JJ) Co-integration test

has been used for testing long run association among interest rate and the financing of Islamic

banking industry via different modes. Finally, Vector Error Correction Model (VECM) has been

used for testing the short run relationship between the interest rate and the financing of Islamic

banking industry.

3.2.1 Unit Root

Economic and financial time series are usually influenced by the changing environment (Zivot &

Wang, 2006), particularly the dynamic state of economy and natural disasters. Therefore, the

time series variables usually follow random walk ( i.e., they do not exhibit constant mean or

variance, or both across time), referred to as the unit root (or non-stationary) problem (Gujarati,

2009). The unit root induces problems in statistical inference involving time series models.

Therefore, the non-stationary time series cannot be predicted precisely.

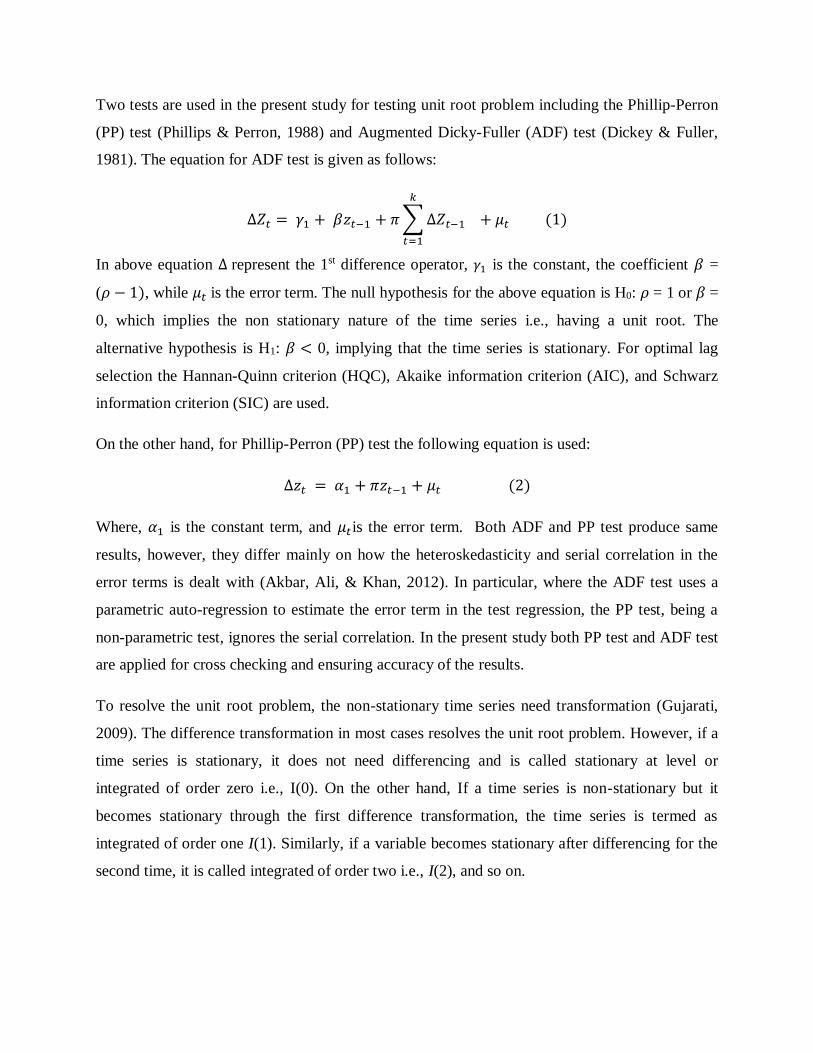

Two tests are used in the present study for testing unit root problem including the Phillip-Perron

(PP) test (Phillips & Perron, 1988) and Augmented Dicky-Fuller (ADF) test (Dickey & Fuller,

1981). The equation for ADF test is given as follows:

∆𝑍𝑡 = 𝛾1 + 𝛽𝑧𝑡−1 + 𝜋 ∑ ∆𝑍𝑡−1

𝑘

𝑡=1

+ 𝜇𝑡 (1)

In above equation ∆ represent the 1st difference operator, 𝛾1 is the constant, the coefficient 𝛽 =

(𝜌 − 1), while 𝜇𝑡 is the error term. The null hypothesis for the above equation is H0: 𝜌 = 1 or 𝛽 =

0, which implies the non stationary nature of the time series i.e., having a unit root. The

alternative hypothesis is H1: 𝛽 < 0, implying that the time series is stationary. For optimal lag

selection the Hannan-Quinn criterion (HQC), Akaike information criterion (AIC), and Schwarz

information criterion (SIC) are used.

On the other hand, for Phillip-Perron (PP) test the following equation is used:

∆𝑧𝑡 = 𝛼1 + 𝜋𝑧𝑡−1 + 𝜇𝑡 (2)

Where, 𝛼1 is the constant term, and 𝜇𝑡is the error term. Both ADF and PP test produce same

results, however, they differ mainly on how the heteroskedasticity and serial correlation in the

error terms is dealt with (Akbar, Ali, & Khan, 2012). In particular, where the ADF test uses a

parametric auto-regression to estimate the error term in the test regression, the PP test, being a

non-parametric test, ignores the serial correlation. In the present study both PP test and ADF test

are applied for cross checking and ensuring accuracy of the results.

To resolve the unit root problem, the non-stationary time series need transformation (Gujarati,

2009). The difference transformation in most cases resolves the unit root problem. However, if a

time series is stationary, it does not need differencing and is called stationary at level or

integrated of order zero i.e., I(0). On the other hand, If a time series is non-stationary but it

becomes stationary through the first difference transformation, the time series is termed as

integrated of order one I(1). Similarly, if a variable becomes stationary after differencing for the

second time, it is called integrated of order two i.e., I(2), and so on.

3.2.2 Cointegration

Two time series are said to be cointegrated when they follow a common equilibrium path.

Statistically speaking, in certain conditions the linear combination of two or more non-stationary

series (i.e., I(1)) may result into a stationary time series (i.e., I(0)). In such a case the variables

are said to be cointegrated (Gujarati, 2009). In other words, an array of time series are termed as

cointegrated if all of them are integrated at the same order and their linear combination is

stationary. Such linear combination imply the presence of a long-term relationship among the

variables (Johansen & Juselius, 1990). Based upon this notion, cointegration is used to test the

long run relationship among two or more time series.

Two approaches are widely used to investigate Cointegration in time series including: (i) Engle

and Granger (1987) unit root test of the regression residuals known as the Engle-Granger (EG)

cointegration test, and (ii) the Johansen and Juselius (1990) maximum-likelihood based test

known as the Johansen and Juselius (JJ) cointegration. Among these, the JJ Cointegration is

generally more powerful since it covers the short comings of EG Cointegration test. Therefore,

the present study applies JJ cointegration to investigate the long-term relationship between

interest rate and financing portfolio of Islamic banking industry. The general form of JJ model is

given as follows:

∆𝑥𝑡 = 𝜙𝑥𝑡−1 + ∑ 𝜗𝑖∆𝑥𝑡−𝑖

𝑘−1

𝑡=1

+ 𝜆𝑦𝑡 + 𝜀𝑡 (3)

Where, 𝑥𝑡 is (nx1) vector of I(1) time series variables, 𝜆𝑦𝑡 is a vector of constants, 𝜙 is the (n ×

n) matrix of long term parameters of the error correction, while 𝜗𝑖 represents the (n × n) matrices

of short term parameters of lagged difference factor.

The JJ Cointegration involves a three step procedure: In the first step the order of integration is

determined for each variable. In the second step the optimal lag length is selection using some

basic criterion e.g., Akaike information criterion (AIC), Schwarz information criterion (SIC), and

Hannan-Quinn criterion (HQC). Whereas, in the last step the cointegrating vectors are

determined using two tests namely Trace test, and Maximum Eigen value test, which eventually

indicate the presence or absence of cointegration. The formulas for Trace test, and Maximum

Eigen value test respectively are given as follows:

𝜆𝑡𝑟𝑎𝑐𝑒(𝑟) = −𝑇 ∑ In

𝑘

𝑖=𝑟+1

(1 − �̂�𝑖) (4)

𝜆𝑚𝑎𝑥(𝑟,𝑟+1) = −𝑇In(1 − �̂�𝑟+1) (5)

Where, r represents the number of cointegrating vectors under the null hypothesis while �̂�𝑖 are

the estimated Eigen values from the estimated matrix 𝜙. The trace and maximum Eigen values

tests help determine the number of cointegrating vectors. The presence of one or more

cointegrating vectors ultimately indicate that the variables are cointegrated, which implies that

the variables cannot move independently of each other. Put differently, the coitegration helps in

identifying the variables that would not drift too far from each other in the longer term, and

would tend to revert to the equilibrium (i.e., the mean distance between them).

3.3.3 Vector Error Correction Model (VECM)

After determining the cointegration, Vector Error Correction Model (VECM) is used to examine

speed of the adjustment process towards the long-term equilibrium i.e., how time series reconcile

errors while it pursues the long-run equilibrium. The mathematical presentation of VECM is as

follows:

∆y𝑡 = 𝑘 + ∑ 𝛽1𝑖∆𝑋1𝑡−𝑖

𝑘

𝑖=0

+ ∑ 𝛽2𝑖∆𝑋2𝑡−𝑖

𝑘

𝑖=0

… + ∑ 𝛽𝑛𝑖

𝑘

𝑖=0

𝛥𝑋𝑛𝑡−𝑖 + 𝑍1𝐸𝐶1𝑖−1 + 𝜀1𝑡 (6)

Where K is constant, Yt is the dependent variable, and ∆ is the 1st difference operator.

Similalry, X represents the independent I(1) variables 1…n, 𝛽1 to 𝛽𝑛 represent the coefficient of

independent variables X1…. Xn respectively, Z1 is the coefficient of error correction term, EC1t -

1 is the error correction term , and 𝜀1𝑡 is the residual or error term.

4. Results and Discussion

Table 1 presents results of Philips and Perron (PP) test and Augmented Dickey and Fuller (ADF)

test. Results of both tests indicate that all variables have unit root problem at level. However,

these variable become stationary at the first difference indicating that all variables are integrated

at order 1 I(1). Hence, the Johansen and Juselius (JJ) co-integration test can be used to check the

long run association among the variables under consideration.

Table 1: Results of Unit Root test

Variables

Augmented Dicky Fuller (ADF) test Phillips—Perron (PP) test

At level At first difference At level At first difference

Pro.

Pro.

Pro.

Pro.

Murabahah -3.038443 0.1353 -5.957237 0.0001 -3.04617 0.1333 -25.4406 0.0000

Ijarah -1.379737 0.8500 -3.768033 0.0314 -0.72603 0.9638 -6.59459 0.0000

Musharakah -1.010998 0.9307 -6.595182 0.0000 -3.91156 0.9102 -6.60906 0.0000

Dimin. Musharakah 0.855359 0.9997 -6.154707 0.0000 0.716264 0.9995 -6.20161 0.0000

Salam -2.126865 0.5120 -8.159308 0.0000 -1.83400 0.6671 -10.4342 0.0000

Istisna -2.723863 0.2332 -13.13378 0.0000 -5.21445 0.2332 -12.198 0.0000

Mudarabah -2.975746 0.1523 -6.123009 0.0001 -2.55418 0.3022 -6.17788 0.0000

Total investment -0.966195 0.9360 -5.118414 0.0011 -1.17317 0.9007 -5.08033 0.0012

Interest Rate -2.147901 0.5051 -4.29417 0.0077 -1.63501 0.7622 -3.96501 0.0177

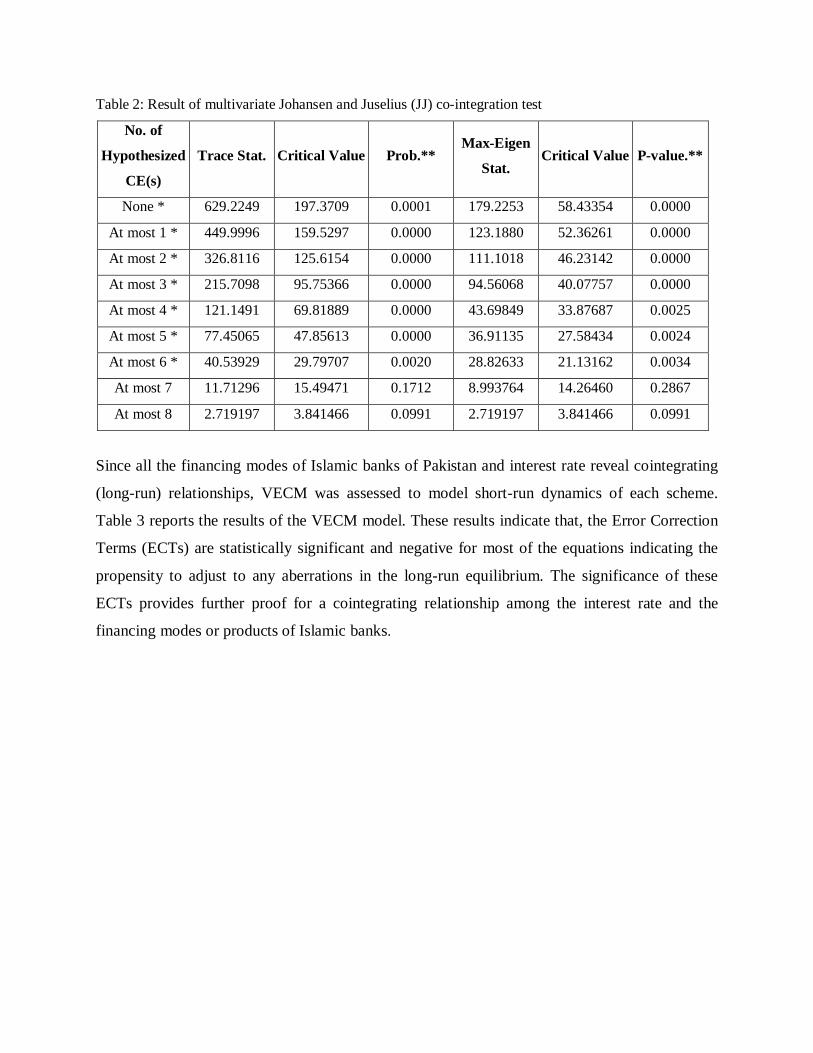

Table 2 presents results of Johansen and Juselius (JJ) co-integration test. The JJ co-integration is

applied to evaluate the Long run relationship among interest rate and modes of financing. The

Trace statistics and the Maximum-Eigen values indicate that there are at most seven (07) co-

integrating equation, indicating that the variables are co-integrated. Consequently, based on the

results it is concluded that long-run relationship exists between interest rate and different modes

of Islamic financing. These results are consistent with the findings of Kader and Leong (2009),

Khalidin and Masbar (2017), Yap and Kader (2008), and Yusoff et al. (2001).

Table 2: Result of multivariate Johansen and Juselius (JJ) co-integration test

No. of

Hypothesized

CE(s)

Trace Stat. Critical Value Prob.** Max-Eigen

Stat. Critical Value P-value.**

None * 629.2249 197.3709 0.0001 179.2253 58.43354 0.0000

At most 1 * 449.9996 159.5297 0.0000 123.1880 52.36261 0.0000

At most 2 * 326.8116 125.6154 0.0000 111.1018 46.23142 0.0000

At most 3 * 215.7098 95.75366 0.0000 94.56068 40.07757 0.0000

At most 4 * 121.1491 69.81889 0.0000 43.69849 33.87687 0.0025

At most 5 * 77.45065 47.85613 0.0000 36.91135 27.58434 0.0024

At most 6 * 40.53929 29.79707 0.0020 28.82633 21.13162 0.0034

At most 7 11.71296 15.49471 0.1712 8.993764 14.26460 0.2867

At most 8 2.719197 3.841466 0.0991 2.719197 3.841466 0.0991

Since all the financing modes of Islamic banks of Pakistan and interest rate reveal cointegrating

(long-run) relationships, VECM was assessed to model short-run dynamics of each scheme.

Table 3 reports the results of the VECM model. These results indicate that, the Error Correction

Terms (ECTs) are statistically significant and negative for most of the equations indicating the

propensity to adjust to any aberrations in the long-run equilibrium. The significance of these

ECTs provides further proof for a cointegrating relationship among the interest rate and the

financing modes or products of Islamic banks.

Table 3: Results of Vector Error Correction Model

Error

Correction: D(Interest) D(D-MUSH) D(IJ) D(IST) D(MUD) D(MUR) D(MUSH) D(SA)

CointEq1 -0.672253 -3.382036 -0.581539 0.430316 -24.46044 -2.560423 2.655683 -1.745189

(0.11804) (2.11383) (0.77197) (1.14907) (35.6962) (8.24812) (2.38265) (1.52503)

[-5.69530] [-1.59995] [-0.75332] [ 0.37449] [-0.68524] [-0.31043] [ 1.11459] [-1.14437]

CointEq2 -0.037377 0.043735 0.031475 0.493875 2.432885 0.506982 0.237529 0.127325

(0.01292) (0.23134) (0.08449) (0.12576) (3.90666) (0.90269) (0.26076) (0.16690)

[-2.89339] [ 0.18905] [ 0.37255] [ 3.92726] [ 0.62275] [ 0.56164] [ 0.91091] [ 0.76287]

CointEq3 0.318315 -2.442175 -0.420135 -0.206332 -26.88263 -1.974563 2.458692 0.171841

(0.08369) (1.49868) (0.54731) (0.81467) (25.3082) (5.84782) (1.68927) (1.08123)

[ 3.80367] [-1.62955] [-0.76763] [-0.25327] [-1.06221] [-0.33766] [ 1.45548] [ 0.15893]

CointEq4 0.050100 0.001641 -0.012469 -2.227717 -3.342971 -0.953983 -0.975892 -0.246477

(0.05626) (1.00753) (0.36795) (0.54769) (17.0141) (3.93136) (1.13566) (0.72688)

[ 0.89049] [ 0.00163] [-0.03389] [-4.06750] [-0.19648] [-0.24266] [-0.85932] [-0.33909]

CointEq5 -0.010013 -0.011126 0.009922 -0.027594 -0.513296 -0.067951 -0.017963 -0.017378

(0.00151) (0.02704) (0.00988) (0.01470) (0.45668) (0.10552) (0.03048) (0.01951)

[-6.63032] [-0.41143] [ 1.00460] [-1.87703] [-1.12396] [-0.64394] [-0.58928] [-0.89069]

CointEq6 0.027583 -0.072926 -0.017174 -0.423708 -3.977291 -0.905436 0.017069 0.027022

(0.01477) (0.26456) (0.09662) (0.14381) (4.46758) (1.03230) (0.29820) (0.19087)

[ 1.86715] [-0.27565] [-0.17776] [-2.94626] [-0.89026] [-0.87711] [ 0.05724] [ 0.14158]

CointEq7 -0.069444 0.708680 0.073959 0.316387 5.691700 -0.099243 -0.629024 -0.003684

(0.02495) (0.44684) (0.16318) (0.24290) (7.54577) (1.74356) (0.50366) (0.32237)

[-2.78316] [ 1.58598] [ 0.45323] [ 1.30254] [ 0.75429] [-0.05692] [-1.24890] [-0.01143]

The p-values for each co-integrating equation are presented in Table 4 to determine whether

short run relationship exists among variables. To calculate p-values the system equations have

been used. The estimated coefficients of the ECT indicate the speed of adjustment towards the

equilibrium point. The co-efficient of co-integrating equation 1 indicate that 67.22% deviance in

the interest rate from its equilibrium point recuperate every quarter (since the current study uses

quarterly data). The probability value of the error correction coefficient for interest rate is

significant (less than 0.05) and negative in sign, categorically proposing that short run causality

exist, which moves from the interest rate to financing modes of Islamic banking industry.

Table 4: Probability values for System Equations

Coefficients Standard Errors t-Stat P-value

C (1) - 0.672253 0.118036 - 5.695301 0.0001

C (2) - 0.037377 0.012918 - 2.893386 0.0126

C (3) 0.318315 0.083687 3.803666 0.0022

C (4) 0.050100 0.056261 0.890491 0.3894

C (5) - 0.010013 0.001510 - 6.630320 0.0000

C (6) 0.027583 0.014773 1.867147 0.0846

C (7) - 0.069444 0.024952 - 2.783157 0.0155

C (8) 0.036347 0.125650 0.289269 0.7769

C (9) - 0.062175 0.091319 - 0.680851 0.5079

C (10) 0.017809 0.012012 1.482567 0.1620

C (11) - 0.013637 0.013204 - 1.032798 0.3205

C (12) - 0.152602 0.086830 - 1.757486 0.1023

C (13) - 0.043072 0.038353 - 1.123042 0.2817

C (14) 0.020206 0.032544 0.620872 0.5454

C (15) 0.013767 0.013713 1.003936 0.3337

C (16) 0.008078 0.001757 4.597213 0.0005

C (17) 0.003570 0.001527 2.338428 0.0360

C (18) - 0.026675 0.015059 - 1.771422 0.0999

C (19) - 0.009682 0.009788 - 0.989160 0.3406

C (20) - 0.019166 0.019070 - 1.005032 0.3332

C (21) 0.007437 0.015362 0.484134 0.6363

C (22) - 0.000193 0.021206 - 0.009104 0.9929

C (23) - 0.014031 0.009731 - 1.441956 0.1730

C (24) 0.423356 0.325637 1.300085 0.2162

The results of VECM reveal that there are seven equations which are negative in sign and

significant, indicating that the short run association exist between the time series and are capable

to adjust their errors from long run equilibrium in sufficient way.

5. Conclusion

The findings of this study suggest that a significant long-term and short-term relationship exists

between the interest rate and the financing of Islamic banking industry via different modes. Thus

any rise in the base offering rate would motivate profit oriented clients to gain funding from

Islamic banks and vice versa. The study therefore concludes that invariably strong links exist

between the Islamic and the conventional banking systems due to benchmarking interest rate.

Therefore, Islamic banks, though operating on interest free ideologies, are prone to interest rate

risk due to the fact that most of the customers are profit seekers. Our findings are consistent with

the view of Bacha (2004) and Rosly (1999) who suggest that benchmarking interest based rate

exposes Islamic banks to the interest rate risk. Based on the findings it is strongly recommended

that Islamic banks should have their own benchmark.

6. References

Akbar, M., Ali, S., & Khan, M. F. (2012). The relationship of stock prices and macroeconomic

variables revisited: Evidence from Karachi stock exchange. African Journal of Business

Management, 6(4), 1315-1322.

Akhtar, B., Akhter, W., & Shahbaz, M. (2017). Determinants of deposits in conventional and

Islamic banking: a case of an emerging economy. International Journal of Emerging

Markets, 12(2), 296-309.

Awan, A. G. (2009). Comparison of Islamic and conventional banking in Pakistan. Proceedings

2nd CBRC, Lahore, Pakistan, 1-36.

Ayub, A., & Masih, M. (2013). Interest rate, exchange rate, and stock prices of Islamic banks: A

panel data analysis. MPRA Paper No. 58871.

Ayub, M. (2007). Understanding Islamic Finance. England: John Wiley & Sons Ltd,.

Bacha, O. I. (2004). Dual banking systems and interest rate risk for Islamic banks. Retrieved

from MPRA website: Online at http://mpra.ub.uni-muenchen.de/12763/

Dickey, D. A., & Fuller, W. A. (1981). Likelihood ratio statistics for autoregressive time series

with a unit root. Econometrica: journal of the Econometric Society, 1057-1072.

El-Gamal, M. A. (2006). Islamic finance: Law, economics, and practice: Cambridge University

Press.

Engle, R. F., & Granger, C. W. (1987). Co-integration and error correction: representation,

estimation, and testing. Econometrica: journal of the Econometric Society, 251-276.

Gujarati, D. N. (2009). Basic econometrics: Tata McGraw-Hill Education.

Gul, S., Irshad, F., & Zaman, K. (2011). Factors Affecting Bank Profitability in Pakistan.

Romanian Economic Journal, 14(39), 61-87.

Hakan, E. E., & Gülümser, A. B. (2011). Impact of interest rates on Islamic and conventional

Banks: The case of Turkey. MPRA Paper no. 29848.

Hamoud, S. H. (1994). Progress of Islamic banking: The aspirations and the realities. Islamic

Economic Studies, 2(1), 71-80.

Haron, S. (1996). Competition and other external determinants of the profitability of Islamic

banks. Islamic Economic Studies, 4(1), 49-64.

Haron, S., & Ahmad, N. (2000). The effects of conventional interest rates and rate of profit on

funds deposited with Islamic banking system in Malaysia. International Journal of

Islamic Financial Services, 1(4), 1-7.

Haron, S., & Azmi, W. W. (2005). Marketing strategy of Islamic banks: A lesson from Malaysia.

Paper presented at the International Seminar on Enhancing Competitive Advantage on

Islamic Financial Institutions, Jakarta.

Hearn, B., Piesse, J., & Strange, R. (2012). Islamic finance and market segmentation:

Implications for the cost of capital. International Business Review, 21, 102-113.

Hussin, M. Y. M., Muhammad, F., Abu, M. F., & Awang, S. A. (2012). Macroeconomic

variables and Malaysian Islamic stock market: a time series analysis. Journal of Business

Studies Quarterly, 3(4), 1.

Jaman, B. U. (2011). Benchmarking in Islamic Finance. UAE Laws and Islamic Finance.

Retrieved from UAE Laws and Islamic Finance website:

https://uaelaws.files.wordpress.com/2011/09/benchmarking-in-islamic-finance-and-

banking.pdf.

Johansen, S., & Juselius, K. (1990). Maximum likelihood estimation and inference on

cointegration—with applications to the demand for money. Oxford Bulletin of Economics

and statistics, 52(2), 169-210.

Kader, R. A., & Leong, Y. K. (2009). The impact of interest rate changes on Islamic bank

financing International Review of Business Research Papers, 5(3), 189-201.

Khalidin, B., & Masbar, R. (2017). Interest Rate and Financing of Islamic Banks in Indonesia (A

Vector Auto Regression Approach). International Journal of Economics and Finance,

9(7), 154.

Khan, W. A., & Sattar, A. (2014). Impact of interest rate changes on the profitability of four

major commercial banks in Pakistan. International Journal of Accounting and Financial

Reporting, 4(1), 142-154.

Kolapo, F., & Fapetu, D. (2015). The influence of interest rate risk on the performance of deposit

money banks in Nigeria. International Journal of Economics, Commerce and

Management, 3(5), 1218-1227.

Malik, M. F., Khan, S., Khan, M. I., & Khan, F. (2014). Interest rate and its effect on Bank’s

profitability. Journal of Applied Environmental and Biological Sciences, 4(8S), 225-229.

Nouman, M., & Ullah, K. (2014). Constraints in the application of partnerships in Islamic banks:

The present contributions and future directions. Business & Economic Reivew, 6(2).

Nouman, M., Ullah, K., & Gul, S. (2018). Why Islamic banks tend to avoid participatory

financing? A demand, regulation, and uncertainty framework Business & Economic

Review, 10(1), 1-32.

Phillips, P. C., & Perron, P. (1988). Testing for a unit root in time series regression. Biometrika,

75(2), 335-346.

Relasari, I. M., & Soediro, A. (2017). Empirical Research on Rate of Return, Interest Rate and

Mudharabah Deposit. Paper presented at the SHS Web of Conferences.

Reuters. (2016, September 12, 2016). State Bank widens Islamic banks' benchmark

requirements, Dawn.

Rosly, S. A. (1999). Al-Bay' Bithaman Ajil financing: Impacts on Islamic banking performance.

Thunderbird International Business Review, 41(4), 46-481.

Shamsuddin, A. (2014). Are Dow Jones Islamic equity indices exposed to interest rate risk?

Economic Modelling, 39, 273-281.

Usmani, M. I. A. (2002a). Meezan Bank’s Guide to Islamic Banking (First ed.). Karachi,

Pakistan: Darul-Ishaat.

Usmani, M. T. (2002b). An introduction to Islamic finance. The Hague: Kluwer Law

International.

Warde, I. (2000). Islamic Finance in the Global Economy. Edinburgh: Edinburgh University

Press.

Yap, K. L., & Kader, R. A. (2008). Impact of interest rate changes on performance of Islamic

and conventional banks. Malaysian Journal of Economic Studies, 45(2), 113.

Yusoff, L. M. M., Rahman, A. A., & Alias, N. (2001). Interest rate and loan supply: Islamic

versus conventional banking system. Jurnal kollomi Malaysia, 35, 61-68.

Zainol, Z., & Kassim, S. (2010). An analysis of Islamic banks' exposure to rate of return risk.

Journal of Economic Cooperation and Development, 31(1), 59-84.

Zivot, E., & Wang, J. (2006). Modeling Financial Time Series with S-PLUS®. New York, NY:

Springer New York.

Recommended