Quarterly Real Estate Analysis for DELHI NCRInsite

Price TrendsGrowth Drivers

Supply Analysis

October-December 2014

32

INTRODUCTION

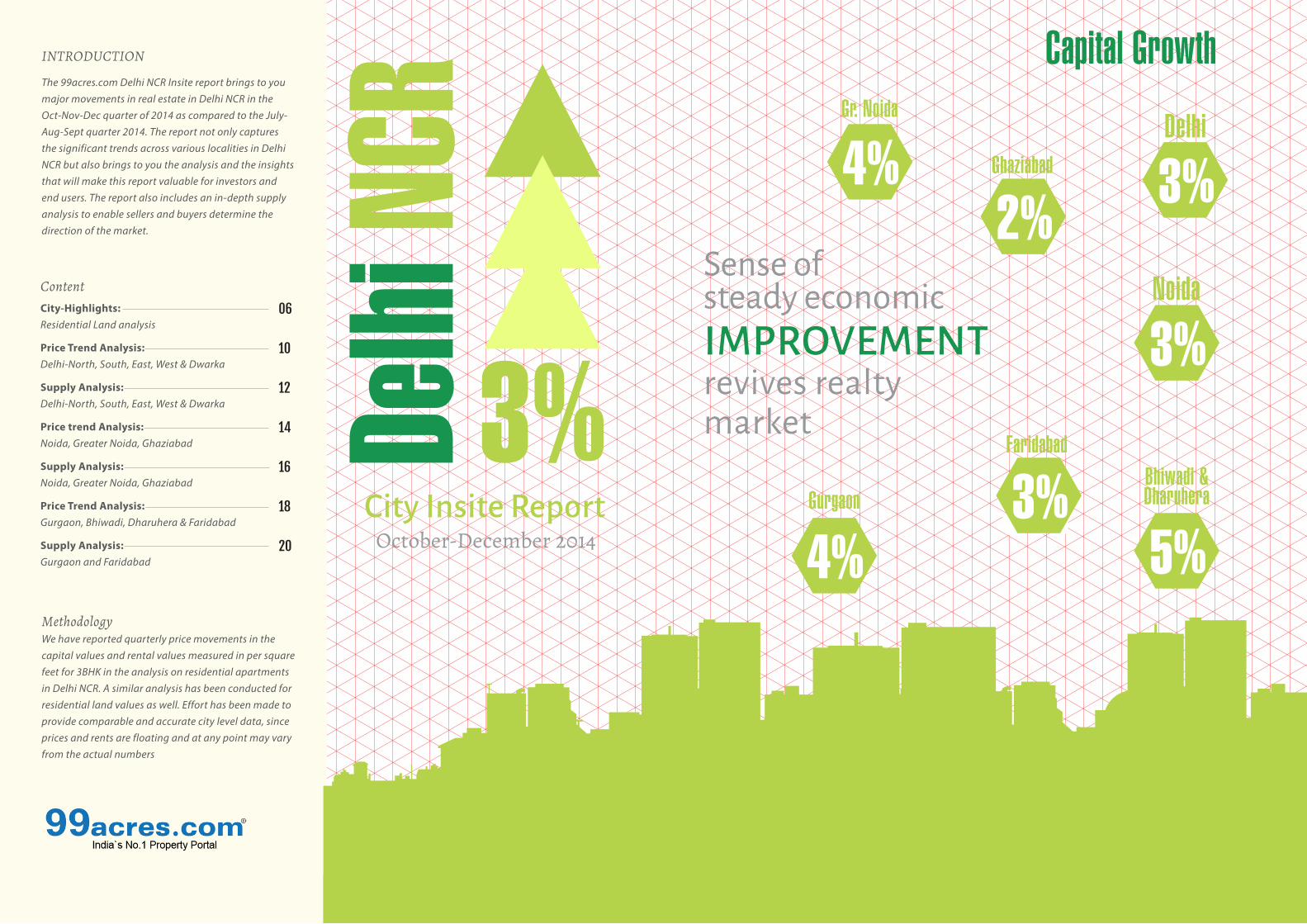

The 99acres.com Delhi NCR Insite report brings to you major movements in real estate in Delhi NCR in the Oct-Nov-Dec quarter of 2014 as compared to the July-Aug-Sept quarter 2014. The report not only captures the significant trends across various localities in Delhi NCR but also brings to you the analysis and the insights that will make this report valuable for investors and end users. The report also includes an in-depth supply analysis to enable sellers and buyers determine the direction of the market.

MethodologyWe have reported quarterly price movements in the capital values and rental values measured in per square feet for 3BHK in the analysis on residential apartments in Delhi NCR. A similar analysis has been conducted for residential land values as well. Effort has been made to provide comparable and accurate city level data, since prices and rents are floating and at any point may vary from the actual numbers

Sense of steady economic IMPROVEMENT revives realty market

City Insite ReportOctober-December 2014

Delhi

NCR

3%

3%Delhi

ContentCity-Highlights: Residential Land analysis

Price Trend Analysis: Delhi-North, South, East, West & Dwarka

Supply Analysis: Delhi-North, South, East, West & Dwarka

Price trend Analysis: Noida, Greater Noida, Ghaziabad

Supply Analysis: Noida, Greater Noida, Ghaziabad

Price Trend Analysis: Gurgaon, Bhiwadi, Dharuhera & Faridabad

Supply Analysis: Gurgaon and Faridabad

06

10

12

14

16

18

203%Faridabad

3%

Ghaziabad

2%

Gr. Noida

4%

Noida

3%

Gurgaon

4%

Bhiwadi & Dharuhera

5%

Capital Growth

54

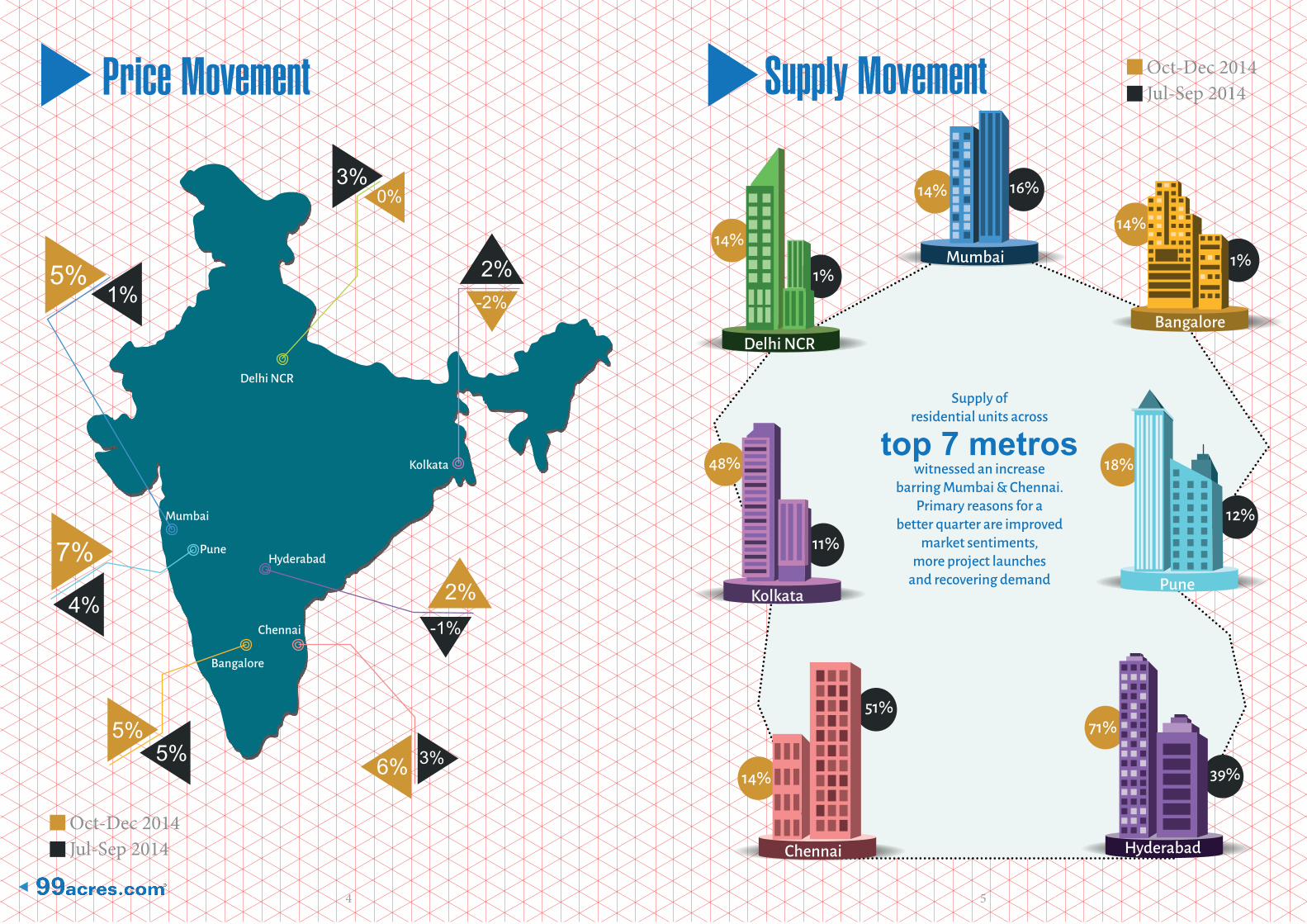

Price Movement Supply Movement

Supply of residential units across

top 7 metros witnessed an increase

barring Mumbai & Chennai. Primary reasons for a

better quarter are improved market sentiments,

more project launches and recovering demand

3%

3%

-1%

-2%

0%

6%

2%

2%

5%

4%

1%

5%

7%

5%

Delhi NCR

Mumbai

Bangalore

Hyderabad

Kolkata

Chennai

Pune

Kolkata

48%

11%

Mumbai

14% 16%

Delhi NCR

14%

1%

Pune

18%

12%

14%

1%

Bangalore

14%

51%

Chennai

71%

39%

Hyderabad

Oct-Dec 2014Jul-Sep 2014

Oct-Dec 2014Jul-Sep 2014

76

Delhi NCR

Ghaziabad

Noida

Faridabad

Gurgaon

Faridabad

Delhi North 2%Absence of new launches plague growth

Delhi West 5%Huge supply for ready to move inventory

Delhi East 3%

Subdued owing to depleting infrastructure

Delhi South 2%High-end inventory and limited buyer-baseGurgaon

4%High prices keep volumes low

Noida 3%Banking on Noida-Greater Noida Expressway

Faridabad 3%Sectors in Nehar Par on a growth spree

Ghaziabad 2%Trans-hindon localities recovering from last quarter's dip

Greater Noida 4%Metro link to Noida a major growth driver

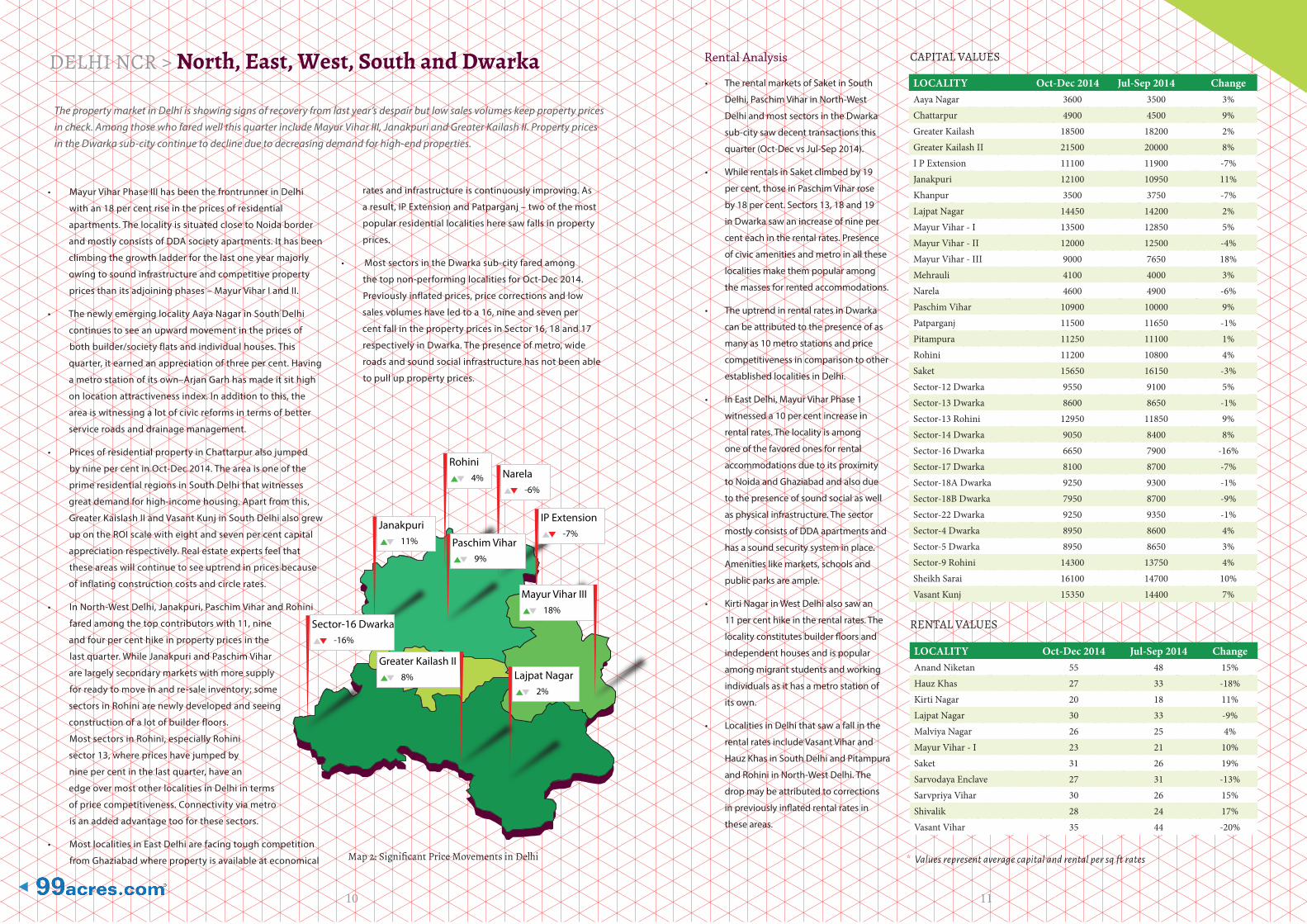

Map 1: Average Price

Movements for different

zones in Delhi NCR

DELHI NCRCity Highlights

With healthy appreciation in housing prices in most residential pockets, the realty atmosphere in Delhi NCR seems to be improving. Micro-markets of Greater Noida, Bhiwadi and Dharuhera have recovered from last quarter’s dip and so have most localities in Delhi. This growth is seen as a result of key policy announcements and stability of new governance at the Center.

• SurajpurinGreaterNoidatoppedtheROI

chartsforDelhiNCRinOct-Dec2014with

20percentincreaseinthecapitalvalue

ofresidentialapartments.Thiswas

followedbySector31inGurgaon

andMayurViharIIIinEastDelhi

withanappreciationof18per

centeach.Someotherlocalities

inGurgaonthatfaredhighon

theROIchartincludeSushantLok

Phase-I(16percent),Sector-68and

59thatroseby15percenteachand

Sohnathatroseby13percent.

• Interestingly,inDelhi,alotof

localitiesrecoveredfromlastquarter’s

dipandshowedgoodgrowth.Some

ofthemincludePaschimVihar,Chattarpur,

VasantKunj,UttamNagar,RohiniandGreaterKailash.

Despitebeingsecondarymarkets,theselocalitiesrevived

duetobetterinvestorsentimentinOct-Dec2014in

comparisontothelastquarter.

• ForGhaziabadwhereeventhepopulartrans-hindon

localitiessawafallinpropertypriceslastquarter,this

quarterwasrewarding.WhilebothKaushambiand

Vasundharawitnessedsevenpercentcapitalappreciation,

housingpricesinVaishaliandIndirapuramjumpedupby

fiveandfourpercentrespectively.Thepresenceofgrowth

driverssuchasmetroandproximitytoNH24and

AnandViharISBTcanbeattributedtothepopularity

oftheselocalitiesamongbothendusersaswellas

investors.

• ThetwonationalhighwayscrossingGhaziabad,NH-

24andNH-58witnessedajumpofalmostsevenand

Top Performers in Delhi NCR (Residential Apartments and Builder Floors)

Top Non -Performers in Delhi NCR (Residential Apartments and Builder Floors)

KEY INFLUENCERS

• Newmetrolinksinthepipeline–

Noida-GreaterNoida;DilshadGarden-

NewBusStand,Ghaziabad;Badarpur-

YMCAChowk,Faridabad

• Industrialandinfradevelopments

nearSohna,BhiwadiandDharuhera

• WideningofNH-24andlinking

NH-58withNH-24;FNGExpressway,

SouthernPeripheralRoadandKundli-

Manesar-PalwalExpresswayservingas

connectivitylinks

• RapidMetroinGurgaonbenefitting

sectorsfallingonitsrouteby

connectingNH-8toDelhiMetrovia

CyberCity,Gurgaon

• Slowpaceofinventoryofftakein

luxurysegmenthasincreasedthe

supplytheaffordablehousing

“Sense of steady economic improvement seemed to have helped Delhi NCR realty market recover from the 2-year long slump.”

ninepercentrespectivelyinthepricesofresidential

apartmentsmainlyduetokeypolicyannouncements

includingwideningofNH-24andaffordablehousing

optionsonNH-58.

• Sector131emergedasthefront-runnerinNoidawith12

percentgrowthincapitalvalues.Apartfromthis,most

sectorsfallingalongNoida-GreaterNoidaExpresswayalso

gainedthisquartermajorlyowingtotheirlocationandthe

infradevelopmentshappeningaround.

• ForGreaterNoida,therealtymarkethasstartedmoving

nowwithmostlocalitiesgivinghealthyreturns.Apartfrom

Surajpur,whichperformedthebestintheentireDelhiNCR

region,Sector16,SectorOmicron,ZETA,ChiandChi-Pi

alsosawgoodhikesinthepricesofresidentialapartments.

Costefficiency,affordabilityandimprovingconnectivity

areseenasthegrowthstimulatorshere.

• BhiwadiwhichsufferedduetotheoverallslumpinDelhi

NCRlastquarter,grewby5percentinOct-Dec2014.The

sub-cityalongwithDharuheraaregrowingaseconomical

investmentzones.

• ThesupplyequationinDelhiremainedunchangedwith

builderfloorsbeingthemostsuppliedpropertytype

followedbysocietyapartmentsinOct-Dec2014.Within

builderfloors,readytomovein3BHKemergedasthe

mostsuppliedunit.ForallotherpocketsinDelhiNCR,the

numberofunder-constructionsocietyapartmentswere

higherthanallotherpropertytypes.

98

Top Performers in Delhi NCR (Residential Land)

Top Non-Performers in Delhi NCR (Residential Land)

“Availability of land parcels at economical rates and new policy on freehold plots has benefited Tronica City and Govind Puram in Ghaziabad.”

Residential Land Analysis

• ScantylandparcelsinDelhihaveopeneddoorsfor

micro-marketsinNCRthatarebecomingfavored

choicesforinvestinginresidentialland.Asaresult,

whileTronicaCityandGovindPuraminGhaziabad

areamongthetopgainers;otherwisepopularareas

ofSouthDelhi–ChattarpurandVasantKunjsaw

dropsinthepricesofresidentiallandinOct-Dec2014

asagainstthelastquarter.Probablereasonsforthis

shiftofinvestorinterestfromDelhitoneighboring

regionscouldbeaffordability,improvingconnectivity

andinfrastructuraldevelopmentsplannedinthese

newlyemergingareas.Moreover,inflatingpricesinthe

primeregionsofDelhiarekeepingsalesvolumeslow

impactingthepricesadversely.

• TronicaCityinGhaziabad,locatedjust2kmfromDelhi

border,hasatotalof12residentialandeightindustrial

sectors.TheUPgovernmenthasallotted2400acres

landforplotteddevelopmentandisgoingtoallot1200

acresofadditionallandinthenearfuturehere.The

policyonfreeholdconversionoftheseplotsandeasy

sale,purchaseandtransferoflandherebytheState

governmenthasmadeitearnaprofitof35percentthis

quarter.Connectivityintheareawillfurtherimprove

aftertheconstructionoftheproposedSignatureBridge.

Thisisalsoexpectedtoboosttherealtymarketinthe

area.Residentialplotsinthebeltarecurrentlypricedin

therangeofRs18,550-22,950persqyd.

• GovindPuraminGhaziabadalsorankedasoneofthe

topgainersinresidentiallandcategoryinOct-Dec

2014witha15percentcapitalappreciation.Located

onHapurRoad,thelocalityenjoysgoodconnectivity

withNoida,EastDelhiandGhaziabadthroughNH-24

andNH-58.Itcaterstothehousingneedsofthosewith

limitedbudgetsandoffersamixofsocietyflats,builder

floors,independenthousesandplots.Demandfrom

mid-incomehousingcategoryandthoseworkinginthe

industrialzonesnearbyincludingKaviNagar,Buland

ShaherandMeerutroadkeeptherealtymarketbuzzing.

Residentialplotsinthelocalityarepricedintherange

ofRs13,050-22,050persqyd.

• SohnaRoadinGurgaoncontinuedtoclimbupinthe

popularitychartandperformedwellinbothresidential

landandresidentialapartmentcategoryinOct-Dec

2014.Whileapartmentpricesappreciatedby11per

cent,pricesofresidentiallandwitnessedagrowthof20

percent.Theareabenefitsfromgoodconnectivitywith

theprimelocationsofGurgaon,DelhiandFaridabad

andisgoingtowitnessalotofsocialand

physicalinfradevelopmentsasperSohna

MasterPlan-2031.

• Otherlocalitiesthatwitnessedprice

appreciationincludeSector41-Noida,

Sector31-GurgaonandSector50-Gurgaon.

Priceappreciationintheselocalitiesis

attributabletoincreasein‘ask’pricesby

sellers,aswellasgoodconnectivityto

adjoininglocalities.

• LandpricesinYamunaExpressway(also

knownasTajExpressway)howeverfell

downby18percentmajorlyowingto

thenewLandAcquisitionActbyYamuna

ExpresswayIndustrialDevelopment

Authority’s(YEIDA)announcedinJuly

2014.Theauthorityhadannouncedthe

residentialplots’schemein2009-10but

failedtohandoverpossessionofthese

plotstoallotteesduetomassfarmer

protest.AsperthenewAct,ifafarmer

deniestoacceptcompensationforhisland,

governmentwillhavetore-acquirethe

samelandimplementing2013Act.This

hasmarredlandratesintheareadespite

thepresenceofgrowthdriverssuchas

Formula-1track.Theaverageratesfell

downfromRs22,950persqydtoRs18,900

persqydinthelastonequarter.

• Weakinvestorsentimentsincaseof

residentiallandcanbeattributedtoprice

depreciationinmostlocalitiesincluding

NajafgarhandBadarpur.WhileNajafgarh

witnessedapricedepreciationofover

16percent,pricesofresidentialplotsin

Badarpurfelldownby50percent.Incase

ofNajafgarh,thedipincapitalpricesof

plotscouldbeattributedtodepletingcivic

amenitiesandslowpaceofinfrastructural

developments.

• InBadarpur,whichliesontheoutskirts

ofDelhi,residentialplotpriceshad

risensignificantlyfollowingthe

announcementoflandpoolingpolicyby

DelhiDevelopmentAuthority(DDA)in

January2014.Theregionisnowinaprice

correctionmodeandhencehasaccounted

forsuchahugedepreciation.

LOCALITY Oct-Dec 2014 Jul-Sep 2014 ChangeAnsals Golf Link 31050-45,000 41400-49950 -8%Ansals Golf Links I 43650-45900 45450-49950 -7%Badarpur 4950-9900 4950-13050 -50%Badarpur Border 3600-4500 3150-6300 -11%Burari 27450-47250 44800-55800 -16%Chattarpur 76500-112500 77400-125100 -22%Dadri 9900-19350 8550-10350 9%Dasna 10350-11250 8100-10800 9%Delta -I Gr Noida 49500-58950 48150-50400 8%G T Road 8550-9900 10350-12150 -16%Gamma II Gr Noida 43200-49050 45450-60300 -10%Golf Course Ext. Road 104400-125100 94050-121050 6%Golf Course Road 136800-154350 125100-149850 6%Govind Puram 13050-22050 13950-20700 15%Indirapuram 31050-31050 31050-112500 -33%Najafgarh 35550-46350 44100-58500 -16%NH-8 72450-105750 72450-107550 -7%Nirvana Country 149850-159750 135000-152550 12%Noida Extension 13050-18900 13950-18900 -6%NRI City 58950-67500 54450-62550 9%Pari Chowk 3600-4500 3600-5400 -20%Rosewood 99450-112050 93600-106200 8%Sector 21 Faridabad 63000-84150 63000-77400 12%Sector-102 Gurgaon 59,850-63900 62550-72000 -7%Sector-108 Noida 104400-114750 108900-120150 -7%Sector-116 Noida 68850-73350 66600-72450 7%Sector-122 Noida 18900-99450 17550-75600 20%Sector-128 Noida 102150-250200 96750-278100 -25%Sector-150 Noida 10800-20700 9000-20700 14%Sector-162 Noida 22500-22500 17550-25200 14%Sector-166 Noida 23850-25200 21600-23400 12%Sector-3 Gr Noida 32400-40950 39600-46800 -10%Sector-31 Gurgaon 137250-149850 112500-125550 20%Sector-36 Noida 136800-157050 136800-182250 -12%Sector-41 Noida 116100-167400 106200-147150 26%Sector-51 Noida 131400-165600 130950-152100 12%Sector-54 Gurgaon 137700-154350 119250-146700 7%Sector-96 Noida 168300-175950 175500-189450 -8%Sohna Road 19350-99000 18900-93150 20%South City 122400-145800 112500-137700 7%Sun City 137250-150750 124650-140400 9%Tronica City 18450-22950 13050-22050 35%Uttam Nagar 73800-118800 102600-156150 -27%Vasant Kunj 102150-271350 124650-187650 -19%Yamuna Expressway 11700-24300 12600-26100 -18%

* Values represent average capital range per square yard

CAPITAL VALUES- Residential Land

1110

CAPITAL VALUES

RENTAL VALUES

* Values represent average capital and rental per sq ft rates

• TherentalmarketsofSaketinSouth

Delhi,PaschimViharinNorth-West

DelhiandmostsectorsintheDwarka

sub-citysawdecenttransactionsthis

quarter(Oct-DecvsJul-Sep2014).

• WhilerentalsinSaketclimbedby19

percent,thoseinPaschimViharrose

by18percent.Sectors13,18and19

inDwarkasawanincreaseofnineper

centeachintherentalrates.Presence

ofcivicamenitiesandmetroinallthese

localitiesmakethempopularamong

themassesforrentedaccommodations.

• TheuptrendinrentalratesinDwarka

canbeattributedtothepresenceofas

manyas10metrostationsandprice

competitivenessincomparisontoother

establishedlocalitiesinDelhi.

• InEastDelhi,MayurViharPhase1

witnesseda10percentincreasein

rentalrates.Thelocalityisamong

oneofthefavoredonesforrental

accommodationsduetoitsproximity

toNoidaandGhaziabadandalsodue

tothepresenceofsoundsocialaswell

asphysicalinfrastructure.Thesector

mostlyconsistsofDDAapartmentsand

hasasoundsecuritysysteminplace.

Amenitieslikemarkets,schoolsand

publicparksareample.

• KirtiNagarinWestDelhialsosawan

11percenthikeintherentalrates.The

localityconstitutesbuilderfloorsand

independenthousesandispopular

amongmigrantstudentsandworking

individualsasithasametrostationof

itsown.

• LocalitiesinDelhithatsawafallinthe

rentalratesincludeVasantViharand

HauzKhasinSouthDelhiandPitampura

andRohiniinNorth-WestDelhi.The

dropmaybeattributedtocorrections

inpreviouslyinflatedrentalratesin

theseareas.

Rental Analysis

LOCALITY Oct-Dec 2014 Jul-Sep 2014 ChangeAaya Nagar 3600 3500 3%Chattarpur 4900 4500 9%Greater Kailash 18500 18200 2%Greater Kailash II 21500 20000 8%I P Extension 11100 11900 -7%Janakpuri 12100 10950 11%Khanpur 3500 3750 -7%Lajpat Nagar 14450 14200 2%Mayur Vihar - I 13500 12850 5%Mayur Vihar - II 12000 12500 -4%Mayur Vihar - III 9000 7650 18%Mehrauli 4100 4000 3%Narela 4600 4900 -6%Paschim Vihar 10900 10000 9%Patparganj 11500 11650 -1%Pitampura 11250 11100 1%Rohini 11200 10800 4%Saket 15650 16150 -3%Sector-12 Dwarka 9550 9100 5%Sector-13 Dwarka 8600 8650 -1%Sector-13 Rohini 12950 11850 9%Sector-14 Dwarka 9050 8400 8%Sector-16 Dwarka 6650 7900 -16%Sector-17 Dwarka 8100 8700 -7%Sector-18A Dwarka 9250 9300 -1%Sector-18B Dwarka 7950 8700 -9%Sector-22 Dwarka 9250 9350 -1%Sector-4 Dwarka 8950 8600 4%Sector-5 Dwarka 8950 8650 3%Sector-9 Rohini 14300 13750 4%Sheikh Sarai 16100 14700 10%Vasant Kunj 15350 14400 7%

LOCALITY Oct-Dec 2014 Jul-Sep 2014 ChangeAnand Niketan 55 48 15%Hauz Khas 27 33 -18%Kirti Nagar 20 18 11%Lajpat Nagar 30 33 -9%Malviya Nagar 26 25 4%Mayur Vihar - I 23 21 10%Saket 31 26 19%Sarvodaya Enclave 27 31 -13%Sarvpriya Vihar 30 26 15%Shivalik 28 24 17%Vasant Vihar 35 44 -20%

Janakpuri 11%

Rohini 4% Narela

-6%

IP Extension -7%

Paschim Vihar 9%

Lajpat Nagar 2%

Greater Kailash II 8%

Mayur Vihar III 18%

Sector-16 Dwarka -16%

DELHI NCR > North, East, West, South and Dwarka

The property market in Delhi is showing signs of recovery from last year’s despair but low sales volumes keep property prices in check. Among those who fared well this quarter include Mayur Vihar III, Janakpuri and Greater Kailash II. Property prices in the Dwarka sub-city continue to decline due to decreasing demand for high-end properties.

• MayurViharPhaseIIIhasbeenthefrontrunnerinDelhi

withan18percentriseinthepricesofresidential

apartments.ThelocalityissituatedclosetoNoidaborder

andmostlyconsistsofDDAsocietyapartments.Ithasbeen

climbingthegrowthladderforthelastoneyearmajorly

owingtosoundinfrastructureandcompetitiveproperty

pricesthanitsadjoiningphases–MayurViharIandII.

• ThenewlyemerginglocalityAayaNagarinSouthDelhi

continuestoseeanupwardmovementinthepricesof

bothbuilder/societyflatsandindividualhouses.This

quarter,itearnedanappreciationofthreepercent.Having

ametrostationofitsown–ArjanGarhhasmadeitsithigh

onlocationattractivenessindex.Inadditiontothis,the

areaiswitnessingalotofcivicreformsintermsofbetter

serviceroadsanddrainagemanagement.

• PricesofresidentialpropertyinChattarpuralsojumped

byninepercentinOct-Dec2014.Theareaisoneofthe

primeresidentialregionsinSouthDelhithatwitnesses

greatdemandforhigh-incomehousing.Apartfromthis,

GreaterKaislashIIandVasantKunjinSouthDelhialsogrew

upontheROIscalewitheightandsevenpercentcapital

appreciationrespectively.Realestateexpertsfeelthat

theseareaswillcontinuetoseeuptrendinpricesbecause

ofinflatingconstructioncostsandcirclerates.

• InNorth-WestDelhi,Janakpuri,PaschimViharandRohini

faredamongthetopcontributorswith11,nine

andfourpercenthikeinpropertypricesinthe

lastquarter.WhileJanakpuriandPaschimVihar

arelargelysecondarymarketswithmoresupply

forreadytomoveinandre-saleinventory;some

sectorsinRohiniarenewlydevelopedandseeing

constructionofalotofbuilderfloors.

MostsectorsinRohini,especiallyRohini

sector13,wherepriceshavejumpedby

ninepercentinthelastquarter,havean

edgeovermostotherlocalitiesinDelhiinterms

ofpricecompetitiveness.Connectivityviametro

isanaddedadvantagetooforthesesectors.

• MostlocalitiesinEastDelhiarefacingtoughcompetition

fromGhaziabadwherepropertyisavailableateconomical

ratesandinfrastructureiscontinuouslyimproving.As

aresult,IPExtensionandPatparganj–twoofthemost

popularresidentiallocalitiesheresawfallsinproperty

prices.

• MostsectorsintheDwarkasub-cityfaredamong

thetopnon-performinglocalitiesforOct-Dec2014.

Previouslyinflatedprices,pricecorrectionsandlow

salesvolumeshaveledtoa16,nineandsevenper

centfallinthepropertypricesinSector16,18and17

respectivelyinDwarka.Thepresenceofmetro,wide

roadsandsoundsocialinfrastructurehasnotbeenable

topulluppropertyprices.

Map 2: Significant Price Movements in Delhi

1312

DELHI NCR > North, East, West, South and DwarkaSupply analysis

• BuilderfloorshavedominatedpropertysupplyinDelhi

withthecurrentquarterreflectinga50percentshare.

Builderfloorswerefollowedbysocietyapartments(47per

cent)andindependenthousesorvillas(just3percent).

Interestingly,theabundantsupplyofbuilderfloorsis

owingtothefloorbasedsystemthatisprevalentinDelhi.

Alowrisebyanindependentbuilder/ownercancomprise

ofmultiplefloorsthatcanhavemultipleowners.

• Therehavebeeninsignificantchangesinthesupplyof

builderfloorsinthelastquartercomparedtotheprevious

one.However,annualnumbersrevealthetotalsupplyof

builderfloorsinDelhihasrisenbyalmost5percent.

• Duetoabsenceofnewlaunchesintheregion,number

ofsocietyapartmentsarefarlesserinnumberthanbuilder

floorsandindependenthouses.Developersfocusmoreon

peripheralareaslikeGreaterNoida,Ghaziabad,Bhiwadi

andDharuherawherelandcostiseconomicalanddemand

forsocietyapartmentsishigher.

• Highconstructioncostsandinflatedcirclerateshaveled

tohighincomesegmentbeingthemostsuppliedinDelhi.

Majorityofresidentialunitsavailablefallinthepricerange

ofRs60lakh-1crore,reflectinglittlechangefromthe

previousquarters.Anannualcomparisonrevealsthattotal

supplyforhigh-incomehousingsegmentinDelhihasgone

upbyalmost65percent.

• Interestingly,thesupplyforaffordablecategoryinDelhi

(propertypricedwithinRs40lakh)hasgoneupby120per

centinthelastoneyear.

• Therehasbeena15percentincreaseinthesupplyof

residentialunitspricedoverRs1croreinthelastone

year(Oct-Dec2013vsOct-Dec2014).

Availability of Different Types of Property

Availability of Property in Different Budgets

Supply of affordable housing options in Delhi has gone up by 120 per cent in the last one year owing to huge demand for this category. Interestingly, the total supply for high-income housing segment has also gone up by almost 65 per cent due to inflating construction costs in some regions.

AvailabilityofReadytoMoveandUnderConstructionpropertyindifferentbudgets

AvailabilityofReadytoMoveandUnderConstructionpropertybyBHK

“With a few fresh launches and limited under construction inventory, Delhi is majorly a re-sale market with builder floors as the most supplied property type.”

• IfonelooksatthepropertypricedwithinRs40lakhin

Delhi,mostofthesupply(over80percent)isunder

construction.Thiscouldbeowingtonewprojects

launchedinaffordablelocalitiesofDelhi.

• Thescene,however,isquitedifferentforallotherbudget

categorieswhereinmostofthepropertysupplyis

readytooccupyandasmallshareofinventoryisunder

construction.ForpropertyrangingaboveRs40lakh,over

80percentisreadytooccupywithmostofitbeingre-sale

propertyandonly15-20percentisunderconstruction

property.ThisindicatesthatDelhihaslimitedoptionsfor

underconstructionornewpropertyformid,highand

luxuryhousingsegments.

• Thiscouldbethereasonforinvestorinterestshifting

towardsadjoiningareaslikeGhaziabad,GreaterNoida,

BhiwadiandDharuherathatareemergingasnew

growthcorridorsduetoalotofbuilderactionandunder

constructioninventorythatleavesscopeforearningprofits

oninvestments.

• Quarter-on-quarternumbersforunderconstructionversus

readytomoveinventoryhardlyshowsanychangesasthe

equationhashadalwaysremainedsameinDelhi’scase.

Ready to Move vs. Under-construction

• ForthequarterendingDecember2014,3BHKemerged

asthemostsuppliedunitforbuilderfloorsandsociety

apartmentsinDelhifollowedby2BHK,4BHKand1

BHK.ThetrendhasremainedsameinDelhiforyears

owingtothepreferencegiventomorespacious

apartments.Anaverage3BHKinDelhimeasuresaround

1300-1600sqftanda2BHKaround900-1200sqft.

• Delhiisprimarilyaresalemarketbecauseofhardly

anynewprojectlaunches.Withinthe3BHKcategory,

morethanthreequartersisreadytooccupyandthe

remainingisunderconstruction.Interestingly,eventhe

leastsupplieduniti.e.1BHKhas90percentasreadyto

moveandjust10percentunderconstructioninventory.

• Quarter-on-quartercomparisonrevealsthatthesupply

ofreadytomovein1BHKunitshavegoneupbyfour

percentandthenumberofreadytomove4BHKunits

havegoneupmarginallybytwopercent.Subsequently,

supplyofunderconstruction1BHKunitshasgonedown

byfourpercentwhilethatfor4BHKunitshasdropped

bytwopercent.For2BHKand3BHKunits,theequation

didnotalterinthisquarter.

BHK-wise Distribution of Property

1514

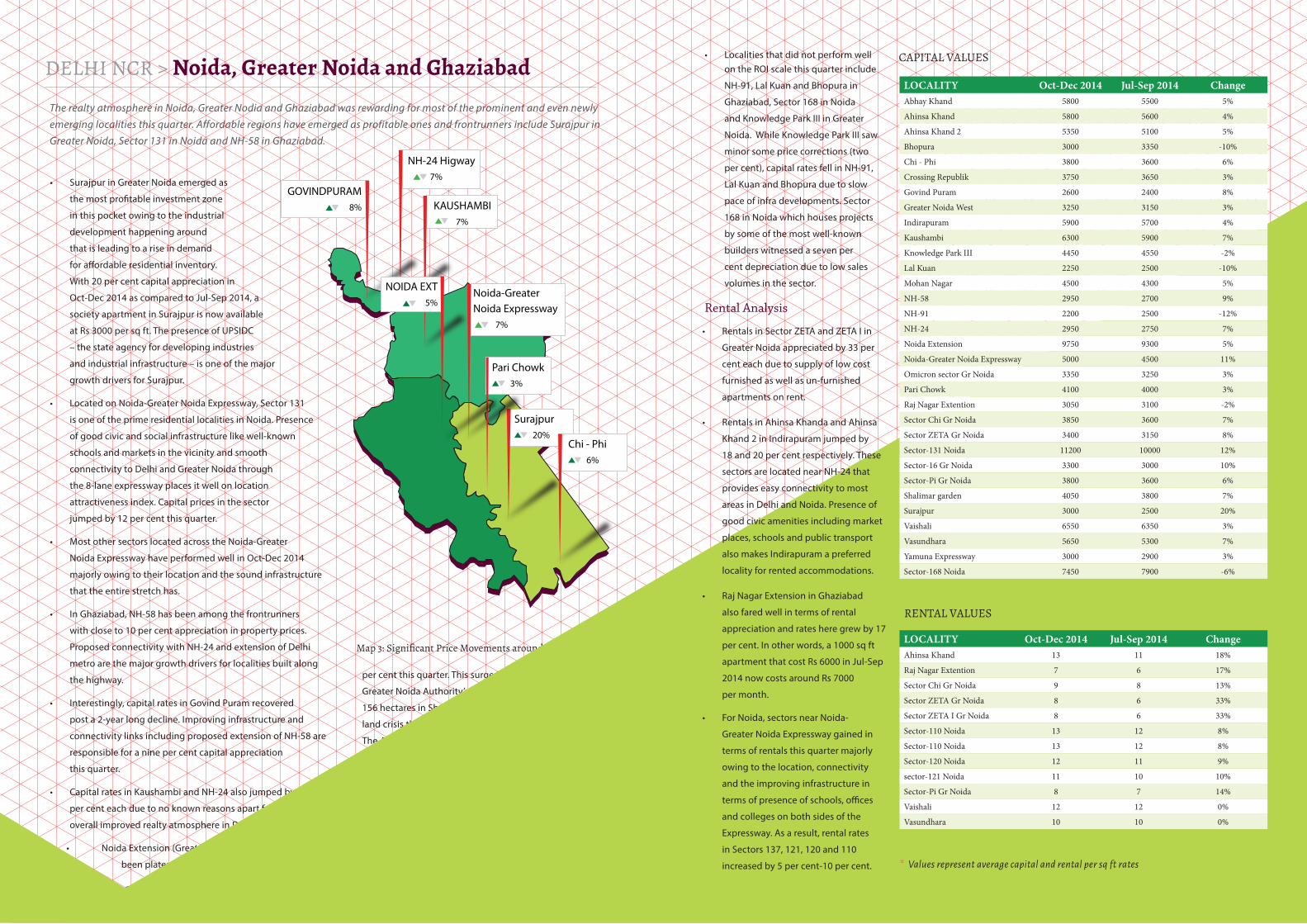

Greater Noida

Noida

Ghaziabad

Surajpur 20%

Chi - Phi 6%

NH-24 Higway 7%

Noida-Greater Noida Expressway 7%

Pari Chowk 3%

KAUSHAMBI 7%

GOVINDPURAM 8%

NOIDA EXT 5%

DELHI NCR > Noida, Greater Noida and Ghaziabad

• SurajpurinGreaterNoidaemergedas

themostprofitableinvestmentzone

inthispocketowingtotheindustrial

developmenthappeningaround

thatisleadingtoariseindemand

foraffordableresidentialinventory.

With20percentcapitalappreciationin

Oct-Dec2014ascomparedtoJul-Sep2014,a

societyapartmentinSurajpurisnowavailable

atRs3000persqft.ThepresenceofUPSIDC

–thestateagencyfordevelopingindustries

andindustrialinfrastructure–isoneofthemajor

growthdriversforSurajpur.

• LocatedonNoida-GreaterNoidaExpressway,Sector131

isoneoftheprimeresidentiallocalitiesinNoida.Presence

ofgoodcivicandsocialinfrastructurelikewell-known

schoolsandmarketsinthevicinityandsmooth

connectivitytoDelhiandGreaterNoidathrough

the8-laneexpresswayplacesitwellonlocation

attractivenessindex.Capitalpricesinthesector

jumpedby12percentthisquarter.

• MostothersectorslocatedacrosstheNoida-Greater

NoidaExpresswayhaveperformedwellinOct-Dec2014

majorlyowingtotheirlocationandthesoundinfrastructure

thattheentirestretchhas.

• InGhaziabad,NH-58hasbeenamongthefrontrunners

withcloseto10percentappreciationinpropertyprices.

ProposedconnectivitywithNH-24andextensionofDelhi

metroarethemajorgrowthdriversforlocalitiesbuiltalong

thehighway.

• Interestingly,capitalratesinGovindPuramrecovered

posta2-yearlongdecline.Improvinginfrastructureand

connectivitylinksincludingproposedextensionofNH-58are

responsibleforaninepercentcapitalappreciation

thisquarter.

• CapitalratesinKaushambiandNH-24alsojumpedbyseven

percenteachduetonoknownreasonsapartfromthe

overallimprovedrealtyatmosphereinDelhiNCR.

• NoidaExtension(GreaterNoidaWest)thathad

beenplateauingforoverayearjumpedbyfive

The realty atmosphere in Noida, Greater Nodia and Ghaziabad was rewarding for most of the prominent and even newly emerging localities this quarter. Affordable regions have emerged as profitable ones and frontrunners include Surajpur in Greater Noida, Sector 131 in Noida and NH-58 in Ghaziabad.

percentthisquarter.Thissurgeisseenastheresultof

GreaterNoidaAuthority’sannouncementofacquiring

156hectaresinShahberi-thevillageattheheartofthe

landcrisisthatgrippedNoidaExtensionthreeyearsago.

TheAuthorityislikelytocompletethere-acquisition

withintwomonths.

Map 3: Significant Price Movements around Noida

“Major highways including NH-24 and NH-58 in Ghaziabad and the Noida-Greater Noida Expressway are emerging as growth corridors. ”

CAPITAL VALUES• LocalitiesthatdidnotperformwellontheROIscalethisquarterinclude

NH-91,LalKuanandBhopurain

Ghaziabad,Sector168inNoida

andKnowledgeParkIIIinGreater

Noida.WhileKnowledgeParkIIIsaw

minorsomepricecorrections(two

percent),capitalratesfellinNH-91,

LalKuanandBhopuraduetoslow

paceofinfradevelopments.Sector

168inNoidawhichhousesprojects

bysomeofthemostwell-known

builderswitnessedasevenper

centdepreciationduetolowsales

volumesinthesector.

• RentalsinSectorZETAandZETAIin

GreaterNoidaappreciatedby33per

centeachduetosupplyoflowcost

furnishedaswellasun-furnished

apartmentsonrent.

• RentalsinAhinsaKhandaandAhinsa

Khand2inIndirapuramjumpedby

18and20percentrespectively.These

sectorsarelocatednearNH-24that

provideseasyconnectivitytomost

areasinDelhiandNoida.Presenceof

goodcivicamenitiesincludingmarket

places,schoolsandpublictransport

alsomakesIndirapuramapreferred

localityforrentedaccommodations.

• RajNagarExtensioninGhaziabad

alsofaredwellintermsofrental

appreciationandratesheregrewby17

percent.Inotherwords,a1000sqft

apartmentthatcostRs6000inJul-Sep

2014nowcostsaroundRs7000

permonth.

• ForNoida,sectorsnearNoida-

GreaterNoidaExpresswaygainedin

termsofrentalsthisquartermajorly

owingtothelocation,connectivity

andtheimprovinginfrastructurein

termsofpresenceofschools,offices

andcollegesonbothsidesofthe

Expressway.Asaresult,rentalrates

inSectors137,121,120and110

increasedby5percent-10percent.

Rental Analysis

RENTAL VALUES

LOCALITY Oct-Dec 2014 Jul-Sep 2014 ChangeAbhay Khand 5800 5500 5%

Ahinsa Khand 5800 5600 4%

Ahinsa Khand 2 5350 5100 5%

Bhopura 3000 3350 -10%

Chi - Phi 3800 3600 6%

Crossing Republik 3750 3650 3%

Govind Puram 2600 2400 8%

Greater Noida West 3250 3150 3%

Indirapuram 5900 5700 4%

Kaushambi 6300 5900 7%

Knowledge Park III 4450 4550 -2%

Lal Kuan 2250 2500 -10%

Mohan Nagar 4500 4300 5%

NH-58 2950 2700 9%

NH-91 2200 2500 -12%

NH-24 2950 2750 7%

Noida Extension 9750 9300 5%

Noida-Greater Noida Expressway 5000 4500 11%

Omicron sector Gr Noida 3350 3250 3%

Pari Chowk 4100 4000 3%

Raj Nagar Extention 3050 3100 -2%

Sector Chi Gr Noida 3850 3600 7%

Sector ZETA Gr Noida 3400 3150 8%

Sector-131 Noida 11200 10000 12%

Sector-16 Gr Noida 3300 3000 10%

Sector-Pi Gr Noida 3800 3600 6%

Shalimar garden 4050 3800 7%

Surajpur 3000 2500 20%

Vaishali 6550 6350 3%

Vasundhara 5650 5300 7%

Yamuna Expressway 3000 2900 3%

Sector-168 Noida 7450 7900 -6%

LOCALITY Oct-Dec 2014 Jul-Sep 2014 ChangeAhinsa Khand 13 11 18%

Raj Nagar Extention 7 6 17%

Sector Chi Gr Noida 9 8 13%

Sector ZETA Gr Noida 8 6 33%

Sector ZETA I Gr Noida 8 6 33%

Sector-110 Noida 13 12 8%

Sector-110 Noida 13 12 8%

Sector-120 Noida 12 11 9%

sector-121 Noida 11 10 10%

Sector-Pi Gr Noida 8 7 14%

Vaishali 12 12 0%

Vasundhara 10 10 0%

* Values represent average capital and rental per sq ft rates

1716

• Societyapartmentscontinuetobethemostsupplied

propertytypeinallthreepockets–Noida,GreaterNoida

andGhaziabadincomparisontobuilderfloorsand

independenthouses/villas.Quarter-on-quartercomparison

revealsthatthenumberofresidentialapartmentsinthese

threepocketshavegoneupby10percent.

• Annualcomparisonrevealsthatthesupplyofapartments

hasgoneby15percentowingtoanumberofnewproject

launchesinthelastoneyearwithGreaterNoidaWest.

Aslightdecreaseinthesupplyofreadytomovein

residentialapartmentsreflectthatfewerprojectshave

beendeliveredthisquarterversusthepreviousone.

• Thoughthereareinsignificantchangeswithrespectto

percentagesinthesupplyofbuilderfloorsduringthis

quarterversusthepreviousone,thenumberhasdoubled

inthelastoneyear.Thiscouldbeduetotherisingdemand

ofaffordablepropertyintheseareas.

• Independenthousesorvillashoweveraretheleast

suppliedpropertytypeastheycatertotheluxurysegment

needsandthesepocketswitnessmoredemandfrom

low-incomeandmid-incomehousingsegments.

• Noida,GreaterNoidaandGhaziabadcatertotheaffordable

segmentcategorythemostwith35percentofitssupply

withinRs40lakh.Outofthesethree,GreaterNoidahasthe

maximumsupplyofapartmentsinthisrange(43percent),

followedbyNoida(29percent)andfinallyGhaziabad

(28percent).

• Morethanaquarterofthesupplyofresidentialapartments

inthesethreepocketsfallinthemid-incomehousing(Rs

40-60lakh)category.Ofthesethree,Noidahasalmosthalf

ofthesupplyandtheremainingtwoareas-GreaterNoida

andGhaziabadhave25percentsupplyeachforthis

budgetrange.

Availablity of Different Types of Property

Availability of Property in Different Budgets

DELHI NCR > Ghaziabad, Noida and Greater NoidaSupply Analysis

With the supply of residential apartments increasing by 10 per cent in Oct-Dec 2014, under-construction inventory in Noida, Greater Noida and Ghaziabad is on a rise. Notably, 35 per cent of the total property supply in these pockets falls in the affordable housing segment. AvailabilityofReadytoMoveand

UnderConstructionpropertyindifferentbudgets

• Itisnotablethat70percentofthesupplyofresidential

apartmentsinNoidaiscurrentlyunderconstruction

andonly30percentisreadytomovein.Thisindicates

thatalotofinventoryisgoingtobeavailablein3-4

yearsfromnow.

• ThepictureissimilarforGreaterNoidawithitsshareof75

percentofunderconstructionandonly25percentready

tomoveininventory.

• ForGhaziabad,however,theready-to-moveversusunder

constructioninventoryequationisdifferentfromtheother

tworegions.SincemostoftheTransHindonlocalitiesare

well-developed,60percentofthepropertysupplyisready

tooccupyandtherest40percentisunderconstruction.

• Quarter-on-quarteranalysisshowsthemaximumsupplyfor

bothreadytomoveinandunderconstructioninventory

forapartments,builderfloorsandindependenthousesfall

intheaffordablehousingsegment(<Rs40lakh).From

Jul-Sep2014toOct-Dec2014quartertherehasbeen

a2percentincreaseinsupplyofthereadytooccupy

inventoryandasubsequent2percentdecreaseinthe

supplyofunderconstructioninventory.Thisismajorlydue

tomoreprojectcompletionsandfewerprojectlaunchesin

thelastquarter.

Ready to Move vs. Under-construction

• 2BHKand3BHKcontinuetobethemostsuppliedunitsin

Noida,GreaterNoidaandGhaziabadinOct-Dec2014.Thisis

becauseofmoredemandforaffordableproperty

• Afewdevelopersintheseareasarelaunchingluxuryand

ultra-luxuryprojects,hence4BHKand5BHKarenotamong

thefavoredunitsandthushavelimitedsupply.

• ForOct-Dec2014,2BHKisthemostsuppliedunit(48per

cent)inGhaziabadfollowedby3BHK(34percent),1BHK

(12percent)and4BHK(6percent).

BHK-wise Distribution of Property

• Withmorethan45percentshareinthesupplyof

apartments,2BHKisalsothemostpopularunitin

GreaterNoidafollowedcloselyby3BHK(36percent).

• InNoidahowever,3BHKismorepopularthan2BHK

withcloseto45percentsupplyshare.2BHKfollows

closelywitha40percentshare.

• Onlyaquarterofthetotalsupplyofresidentialapartments

intheseareasfallsinthehigh-incomehousing(Rs60lakh-

1crore)category.ItisnotablethatNoidahasthemaximum

shareofsupplyforthisbudgetcategorywith60percent

ofitsresidentialapartmentsintherangeofRs60lakh-1

crore.ThisisfollowedbyGhaziabadwitha30percentand

GreaterNoidawithjust10percentsupplyshare.

• UnlikeGurgaon,Noida,GreaterNoidaandGhaziabadcater

moretothebudgethousingneedsandthushaslimited

supply(14percentofthetotalapartmentsupply)forthe

luxuryhousingsegment,whichrangesaboveRs1crore.

AvailabilityofReadytoMoveandUnderConstructionpropertybyBHK

1918

Faridabad

GurgaonGurgaon

Sector-31 Gurgaon 18%

Dwarka Expressway Gurgaon 3%

IMT Manesar -4%

Dharuheda 9%

Sushant Lok Phase - I 16%

Nehar Par 5%

Bhiwadi 5%

Sec 85 10%

Sohna 13%

Manesar 0%

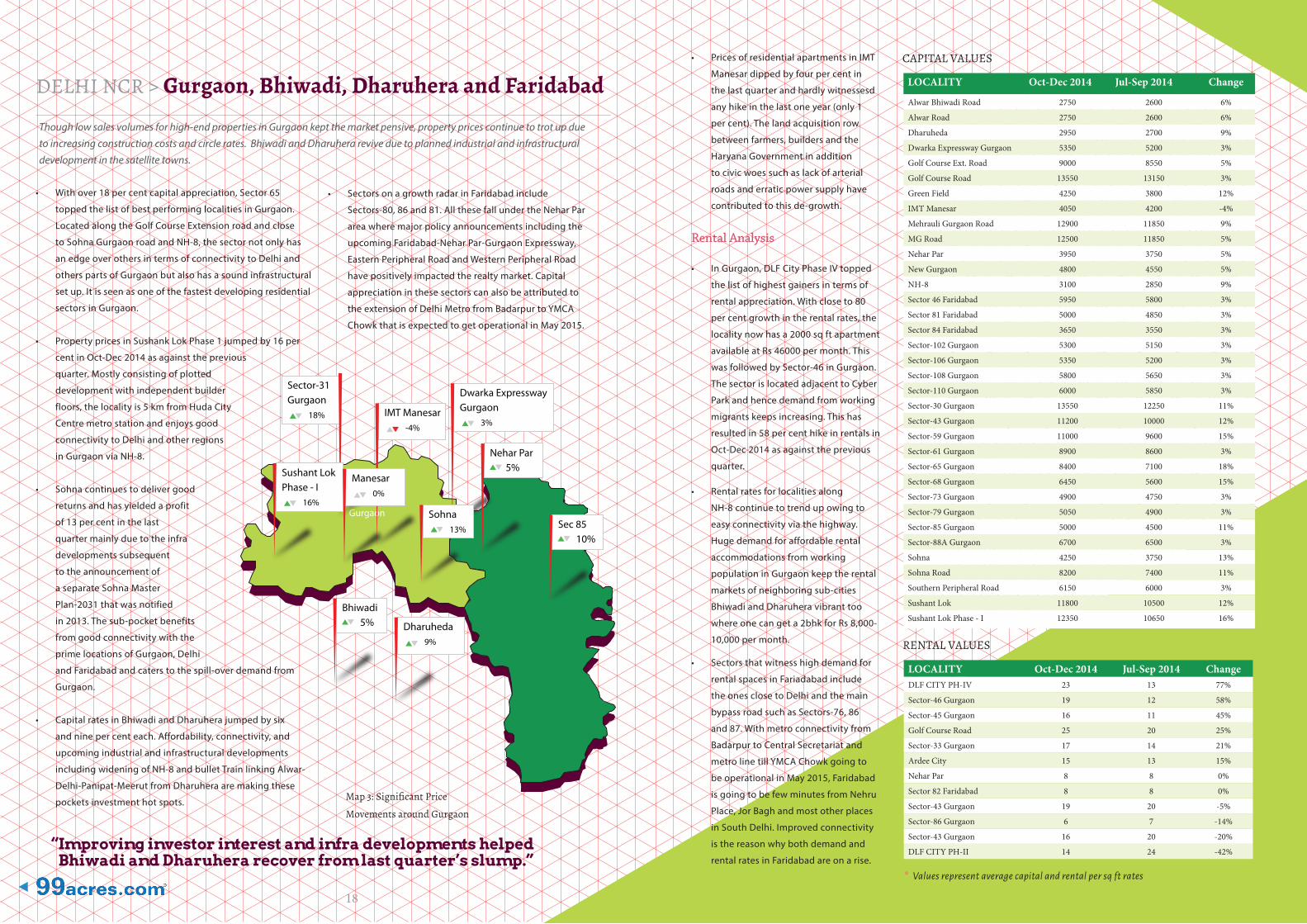

DELHI NCR > Gurgaon, Bhiwadi, Dharuhera and Faridabad

Though low sales volumes for high-end properties in Gurgaon kept the market pensive, property prices continue to trot up due to increasing construction costs and circle rates. Bhiwadi and Dharuhera revive due to planned industrial and infrastructural development in the satellite towns.

• Withover18percentcapitalappreciation,Sector65

toppedthelistofbestperforminglocalitiesinGurgaon.

LocatedalongtheGolfCourseExtensionroadandclose

toSohnaGurgaonroadandNH-8,thesectornotonlyhas

anedgeoverothersintermsofconnectivitytoDelhiand

otherspartsofGurgaonbutalsohasasoundinfrastructural

setup.Itisseenasoneofthefastestdevelopingresidential

sectorsinGurgaon.

• PropertypricesinSushankLokPhase1jumpedby16per

centinOct-Dec2014asagainsttheprevious

quarter.Mostlyconsistingofplotted

developmentwithindependentbuilder

floors,thelocalityis5kmfromHudaCity

Centremetrostationandenjoysgood

connectivitytoDelhiandotherregions

inGurgaonviaNH-8.

• Sohnacontinuestodelivergood

returnsandhasyieldedaprofit

of13percentinthelast

quartermainlyduetotheinfra

developmentssubsequent

totheannouncementof

aseparateSohnaMaster

Plan-2031thatwasnotified

in2013.Thesub-pocketbenefits

fromgoodconnectivitywiththe

primelocationsofGurgaon,Delhi

andFaridabadandcaterstothespill-overdemandfrom

Gurgaon.

• CapitalratesinBhiwadiandDharuherajumpedbysix

andninepercenteach.Affordability,connectivity,and

upcomingindustrialandinfrastructuraldevelopments

includingwideningofNH-8andbulletTrainlinkingAlwar-

Delhi-Panipat-MeerutfromDharuheraaremakingthese

pocketsinvestmenthotspots.

• SectorsonagrowthradarinFaridabadinclude

Sectors-80,86and81.AllthesefallundertheNeharPar

areawheremajorpolicyannouncementsincludingthe

upcomingFaridabad-NeharPar-GurgaonExpressway,

EasternPeripheralRoadandWesternPeripheralRoad

havepositivelyimpactedtherealtymarket.Capital

appreciationinthesesectorscanalsobeattributedto

theextensionofDelhiMetrofromBadarpurtoYMCA

ChowkthatisexpectedtogetoperationalinMay2015.

“Improving investor interest and infra developments helped Bhiwadi and Dharuhera recover from last quarter’s slump.”

Map 3: Significant Price

Movements around Gurgaon

• PricesofresidentialapartmentsinIMT

Manesardippedbyfourpercentin

thelastquarterandhardlywitnessesd

anyhikeinthelastoneyear(only1

percent).Thelandacquisitionrow

betweenfarmers,buildersandthe

HaryanaGovernmentinaddition

tocivicwoessuchaslackofarterial

roadsanderraticpowersupplyhave

contributedtothisde-growth.

• InGurgaon,DLFCityPhaseIVtopped

thelistofhighestgainersintermsof

rentalappreciation.Withcloseto80

percentgrowthintherentalrates,the

localitynowhasa2000sqftapartment

availableatRs46000permonth.This

wasfollowedbySector-46inGurgaon.

ThesectorislocatedadjacenttoCyber

Parkandhencedemandfromworking

migrantskeepsincreasing.Thishas

resultedin58percenthikeinrentalsin

Oct-Dec2014asagainsttheprevious

quarter.

• Rentalratesforlocalitiesalong

NH-8continuetotrendupowingto

easyconnectivityviathehighway.

Hugedemandforaffordablerental

accommodationsfromworking

populationinGurgaonkeeptherental

marketsofneighboringsub-cities

BhiwadiandDharuheravibranttoo

whereonecangeta2bhkforRs8,000-

10,000permonth.

• Sectorsthatwitnesshighdemandfor

rentalspacesinFariadabadinclude

theonesclosetoDelhiandthemain

bypassroadsuchasSectors-76,86

and87.Withmetroconnectivityfrom

BadarpurtoCentralSecretariatand

metrolinetillYMCAChowkgoingto

beoperationalinMay2015,Faridabad

isgoingtobefewminutesfromNehru

Place,JorBaghandmostotherplaces

inSouthDelhi.Improvedconnectivity

isthereasonwhybothdemandand

rentalratesinFaridabadareonarise.

Rental Analysis

CAPITAL VALUES

* Values represent average capital and rental per sq ft rates

RENTAL VALUES

LOCALITY Oct-Dec 2014 Jul-Sep 2014 Change

Alwar Bhiwadi Road 2750 2600 6%

Alwar Road 2750 2600 6%

Dharuheda 2950 2700 9%

Dwarka Expressway Gurgaon 5350 5200 3%

Golf Course Ext. Road 9000 8550 5%

Golf Course Road 13550 13150 3%

Green Field 4250 3800 12%

IMT Manesar 4050 4200 -4%

Mehrauli Gurgaon Road 12900 11850 9%

MG Road 12500 11850 5%

Nehar Par 3950 3750 5%

New Gurgaon 4800 4550 5%

NH-8 3100 2850 9%

Sector 46 Faridabad 5950 5800 3%

Sector 81 Faridabad 5000 4850 3%

Sector 84 Faridabad 3650 3550 3%

Sector-102 Gurgaon 5300 5150 3%

Sector-106 Gurgaon 5350 5200 3%

Sector-108 Gurgaon 5800 5650 3%

Sector-110 Gurgaon 6000 5850 3%

Sector-30 Gurgaon 13550 12250 11%

Sector-43 Gurgaon 11200 10000 12%

Sector-59 Gurgaon 11000 9600 15%

Sector-61 Gurgaon 8900 8600 3%

Sector-65 Gurgaon 8400 7100 18%

Sector-68 Gurgaon 6450 5600 15%

Sector-73 Gurgaon 4900 4750 3%

Sector-79 Gurgaon 5050 4900 3%

Sector-85 Gurgaon 5000 4500 11%

Sector-88A Gurgaon 6700 6500 3%

Sohna 4250 3750 13%

Sohna Road 8200 7400 11%

Southern Peripheral Road 6150 6000 3%

Sushant Lok 11800 10500 12%

Sushant Lok Phase - I 12350 10650 16%

LOCALITY Oct-Dec 2014 Jul-Sep 2014 ChangeDLF CITY PH-IV 23 13 77%

Sector-46 Gurgaon 19 12 58%

Sector-45 Gurgaon 16 11 45%

Golf Course Road 25 20 25%

Sector-33 Gurgaon 17 14 21%

Ardee City 15 13 15%

Nehar Par 8 8 0%

Sector 82 Faridabad 8 8 0%

Sector-43 Gurgaon 19 20 -5%

Sector-86 Gurgaon 6 7 -14%

Sector-43 Gurgaon 16 20 -20%

DLF CITY PH-II 14 24 -42%

2120

• Societyapartmentsarethemostsuppliedpropertytype

inGurgaonandFaridabadfollowedbybuilderfloors

andindependenthouses/villas.InFaridabad,residential

apartmentshavemorethanhalfoftheshareinthetotal

propertysupply.Independenthouses/villasareveryfewin

numbersandbuilderfloorshavelessthanhalfofthe

totalsupply.

• ForOct-Dec2014,societyapartmentshavehadthe

maximumshareofsupplyinGurgaon,followedbya

verylowpercentageofbuilderfloorsupplyandaneven

negligibleshareofindependenthouses/villas.

• Therehavebeeninsignificantchangesinthesupplyof

differenttypeofpropertiesinGurgaonandFaridabadin

Oct-Dec2014quarterasagainstthepreviousone.

• Duetohighconstructioncostsandinflatedpropertyrates,

mostpropertiesinGurgaonfallintheluxuryhousing

segment.Inotherwords,almost60percentofthe

propertiesinGurgaonarepricedasRs1croreandabove.

Onlyaquarteroftotalsupplyofpropertyinthepocket

fallsinthehigh-endhousingsegmentwhichispriced

betweenRs60lakhandRs1crore.

• Asisevidentfromthenumbers,averyinsignificantportion

ofthetotalsupplyofpropertyinGurgaonfallsinthe

affordableandmid-incomehousingcategory.

• InFaridabad,however,thepropertysegregationonthe

basisofbudgetisquitedifferentfromGurgaon.Mid-

incomehousing(Rs40-60lakh)andhigh-incomehousing

(Rs60lakh-1crore)haveequalsharesinthetotalproperty

supply.Evenaffordablehousingsupply,i.e.theproperty

pricedwithinRs40lakhhasa20percentshareandluxury

housingsupply,i.e.propertypricedaboveRs1croreisthe

least(only10percent)supplied.

Availability of Different Types of Property

Availability of Property in Different Budgets

DELHI NCR > Gurgaon and FaridabadSupply Analysis

Society apartments continue to have the most supplied property type in both Faridabad and Gurgaon. While the supply of affordable properties in Gurgaon saw a surge this quarter, the numbers remained same for Faridabad that continue to supply mid-income housing options the most.

Ready to Move vs. Under-construction

• 3BHKisthemostsuppliedcategoryinFaridabadand

Gurgaon,followedby2BHK,4BHKand1BHK.Within3

BHKs,readytomoveininventoryisslightlymorethan

underconstructionapartments.

• 1BHKunitsarealmostnominalinnumbersinboth

GurgaonandFaridabad.Thiscouldbeduetolowdemand

fortheseunitsforbothsaleandrentalpurposes.

• Morethanhalfofthe2BHKunitsinGurgaonandFaridabad

areunderconstructionindicatingthatthesupplyforthese

unitswillincreaseconsiderablyinthecoming2-4years

whentheseprojectswouldgetdelivered.

• 4BHKunitsontheotherhandhavelesserunder

constructioninventoriesthanreadytomoveinonesdueto

fraildemandaswellassupplyfortheseunits.

BHK-wise Distribution of Property

“2BHKs continue to be the most supplied apartment units in both Faridabad and Gurgaon with almost half the share in the total property supply.”

• Therehavebeennomajorchangesinthesupplyfigures

forbothunderconstructionandreadytooccupyproperty

forGurgaonandFaridabad.Thiscouldbebecauseoffewer

deliveriesaswellasfewerproductlaunchesthisquarter.

• Affordableandmid-incomehousingcategories(property

fallingwithinRs60lakh)havethemaximumsupplyof

underconstructioncategory.Thiscouldbeduetothe

launchofsomeaffordableprojectsinGurgaoninthelast

oneyear.Andsincealltheseprojectsarenew,supplyfor

readytomoveininventoryinthesecategoriesis

below20percent.

• Gurgaonhaswholesomesupplyofreadytomove

ininventoryinthehighincomeandluxuryhousing

categories.

• InFaridabad,propertiespricedwithinRs40lakhhavean

equalsupplyofreadytomoveinandunderconstruction

inventory.However,almostthreequartersofthetotal

supplyofpropertiespricedintherangeofRs40and60

lakharereadytooccupy.Thehigh-incomehousingand

luxuryhousingsegmentalsomajorlyconsistsofreadyto

moveinapartmentsandbuilderfloors.

• Quarter-on-quartercomparisonshowsthattherehave

beeninsignificantchangesinthesupplyofreadyto

moveinandunderconstructioninventoryinGurgaon

andFaridabadforallunitsintheOct-Dec2014as

comparedtothepreviousquarter.Theequationsin

boththeseregionsremainconstantduetotheinherent

natureoftheserealtymarkets.

AvailabilityoftoMoveandUnderConstructionpropertyindifferentbudgets

AvailabilityofReadytoMoveandUnderConstructionpropertybyBHK

Our Heritage

First Internet Company to be Listed

Info Edge (India) Ltd is India’s premier on-line classifieds company in recruitment, real estate, matrimony and education

a USD 1.84 Billion listed Indian Internet Conglomerate

Credentials of www.99acres.com

5 Million9 Million6 lac2.5 lac15,000+20% 2.5 million

Unique Visitors a month

Visitors a month

Residential and Commercial Properties

Searches everyday

New Projects

NRI Visitors

Registered Database

OFFICES

CITIES

India’s No.1 Property Portal

Recommended