Weave Services Limited

0

What is

innovation in

the apparel industry

?

Consulting-Outsourcing-Capability Building

Weave Services Limited

1

Innovation can be translated into 4 major segments

Science based innovation

• R&D driven

• Example: Biogenedeveloped treatments to cancer and other diseases

Engineering based

• Large scale transformation

• Example: High Speed Rail, China owning ~40% of the global railroad equipment

Customer focused

• Explore niche in the market

• Example: Xiaomi developed cheaper mobile phone to penetrate the large untapped Chinese mass market

Efficiency based innovations

• Ecosystem based/ Industry 4.0

• Example: Everstar launched automated manufacturing connected to online design and customer customization solutions

Source: McKinsey Quarterly- gauging the strength of Chine innovation. Oct 2015

Weave Services Limited

2

Service level

>90%

In store availabilityIn-store availability through VMI models

Warehousing cost

$0.30 USD

Direct to store model with cross-docking

Manufacturing cost

-10%FOB

Lean model factories with high automation

Competitive advantage

Speed of supply

Vertically integrated supply chain

Lead time reduction

72 hrs

design to marketOrder to ship, online customizable services

Why does Efficiency Innovation matter?

Top line

Warehousing cost

Bottom line

Manufacturing cost

Lead time reduction Service level Competitive advantage

Fabric colour compliance

Rejects %

Increase colour matching IQC compliance

Fabric colour compliance

Weave Services Limited

3

Efficiency Innovation solves the core problems faced by your business

Top line

Bottom line

Lead time reduction

72 hrs

design to marketOrder to ship, online customizable services

Service level

>90%

In store availabilityIn-store availability through VMI models

Warehousing cost

$0.30 USD

Direct to store model with cross-docking

Manufacturing cost

-10%FOB

Lean model factories with high automation

Competitive advantage

Speed of supply

Vertically integrated supply chain

Fabric colour compliance

Rejects %

Increase colour matching IQC compliance

Weave Services Limited

4

0%

5%

10%

15%

20%

25%

30%

35%

40%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Productivity change %

Real wage change %

US footwear productivity is 4 times higher than China

“(In China) the average is 0.5 pair per labor hour,

compared with more than 2 pairs in North

America. This difference is NOT primarily due to

automation, but to smart industrial engineering.”

Renaud AnjoranQualityInspection.org

0

100

200

300

400

500

600

700

Malaysia

Thailand

China

Philippines

Indonesia

Monthly Wages in China have risen dramaticallyAvg. Monthly Wages, 2010 prices $

Source: The Economist Intelligence Unit, https://qualityinspection.org/asian-countries-comparison/

Outside of the big players, the industry has invested very little in Efficiency Driven innovations

Labor productivity has not seen comparative growth over the past years % change of Manufacturing labor productivity and real wages from 2001 - 2012

Weave Services Limited

5

The manufacturers who don’t, are in danger of becoming low value-add factory landlord

of VF products are produced by VF, with the remainder sourced from third parties

24%Of VF products are produced by VF, with the remainder sourced from third parties

30K+ Associates supporting Supply Chain activities

VF owns production facilities in the Americas & EMEA

125 Inventory-to-cash days, one of the best for the industry

New Balance reduces lead time by 95%

NB Contra.

Productivity of its own factories is 4X that of contractors

FOB cost difference is only <10%

+400%

The productivity of NB’s own facilities is much higher

<10%

NB Contra.

"We've taken our process—from cutting raw materials to shipping finished shoes — from eight days down to three hours"

Brendan MellyDirector of U.S. operations

Red Wing demonstrates a vertically integrated company

Tanneries

ProcesseingRaw Materials

Producing parts of shoes

Final Assembly

Weave Services Limited

6

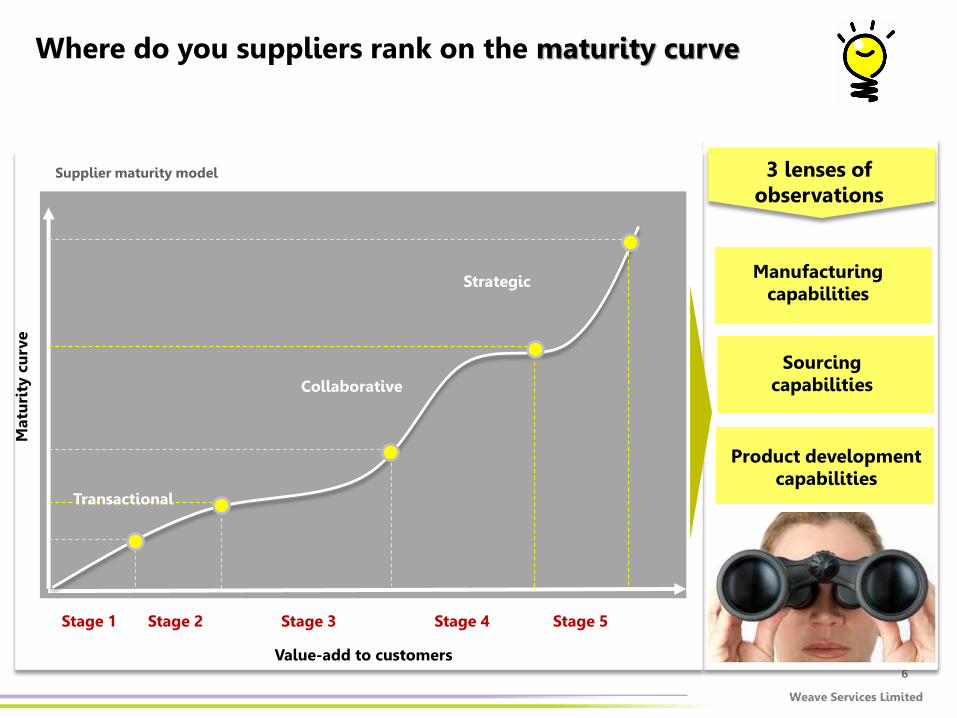

Where do you suppliers rank on the maturity curveM

atu

rity

cu

rve

Value-add to customers

Manufacturing capabilities

Sourcing capabilities

Product development capabilities

Stage 1 Stage 2 Stage 3 Stage 4 Stage 5

Transactional

Collaborative

Strategic

Supplier maturity model 3 lenses of observations

Weave Services Limited

7

Efficiency innovations enable manufacturers to grow along the maturity curve

Maturity matrix- core competencies

Low value add High value add

Stage 1 Stage 2 Stage 3 Stage 4 Stage 5

Manufacturing

Sourcing

Product development/design

- +

Planning capabilities Basic schedulingTimely pulling of forward orders

Integration to Master planning

Joint-forecast with customers

Replenishment to customer sales

Integrated systems EDI PO’s ASN capable Integrated production plans

Integrated forecast and order plans

Joint Analytics

Fabric library Driven by customer

Fabric library on core styles

Fabric library on new colors/yarn

Extensive and avant-garde range

Joint-development

Quality controls Non-systematic QC-AQL by customer Machine based QA- Priority based TQM

Innovation management Customer led/market led

Sales led Dedicated team Innovation targets and budget allocated

Integrated to customers

Customer collaboration Transactional Sales team based Planning team based

Joint project team Joint investments

Market intelligence No source available Product based on market release

Competitors SWOT

Customer/ demand analysis

Advanced trend projections

MTO MTF VMIReplenishment models

Lean controls Warehouse inventory control

WIP targets Set TAKT time JIT inventory MRP consolidation

Procurement practicesLarge vendor base/relationship based

Structured negotiation practices

Based on supplier performance

Integrated network with customers

Based on market fact sheet

Weave Services Limited

8

Focus the maturity curve on 3 major areas

Replenishment methodologies

Lean practices Customer intelligence

Speed replenishment End-2-End integrated lean operations

Insight driven collaboration

Weave Services Limited

9

Fashion retailers are hungry for speed, but at what cost?

Fast fashion brand and retailers are faced with a conundrum

Client example

Weave Services Limited

10

Brands leverage calculated risk models…

• Risk 1: lost sales

• Risk 2: end of season stock + material commitment

Speed programs…it “takes 2 to tango”

• Identification of quick replenishment programs

• Joint end-2-end planning through T&A

• Increased liability level on trims and fabric

• Effective tracking and decision making processes

…and develop tight collabo-ration with manufacturers

Weave Services Limited

11

Focus the maturity curve on 3 major areas

Replenishment methodologies

Lean practices Customer intelligence

Speed replenishment End-2-End integrated lean operations

Insight driven collaboration

Weave Services Limited

12

Fashion brands are hungry for speed

We expect first output

production coming within the

1st day of production

55-65

5

25-30

15-20

10

Lead time in days

Leading manufacturers leverage Lead Time as a competitive weapon or USP

Receiving Cutting Sewing Packing

Weave Services Limited

13

End-2-end line

flow is now

talked about in

hoursSewing WIP and production time

30-50%

Packing Accuracy and processing time

10-20%

CuttingDefects and change over time

n/a

ReceivingIn-full, On Time performance, Quality

20-30%

InefficienciesManufacturing stages Opportunities

End-2-end TAKT time

20-50%Idle time between production stages

Leaning out operations requires Efficiency based innovations

Weave Services Limited

14

Focus the maturity curve on 3 major areas

Replenishment methodologies

Lean practices Customer intelligence

Speed replenishment End-2-End integrated lean operations

Insight driven collaboration

Weave Services Limited

15

Data management and market intelligence

• Historically the apparel industry

has lagged behind in market-

research-led innovations

Weave Services Limited

16

Data management and market intelligence

• Historically the apparel industry has lagged

behind in market research led innovations

• Large brands are by-and-large

leading the fabric innovation

through advanced R&D

Weave Services Limited

17

Data management and market intelligence

• Historically the apparel industry has lagged

behind in market research led innovations

• Large brands are by-an-large leading the

fabric innovation through advanced R&D

• This is the opposite end of the

spectrum to the FMCG industry

Weave Services Limited

18

Data management and market intelligence

• Historically the apparel industry has lagged

behind in market research led innovations

• Large brands are by-an-large leading the

fabric innovation through advanced R&D

• This is the opposite end of the spectrum to

the FMCG industry

• Leading organization split

merchandising functions to demand

and sales management team

Weave Services Limited

19

Manufacturers are revisiting their organization structure to provide stronger market led information

Leading firms invest in sales and marketing Traditional merchandising remains but it is evolving

Traditional merchandising

New operating model

• Sales/ market data driven

• Product development, PLM and product costing

• Product

development

• Fabric sourcing

• Product costing

McKinsey- Sales and Marketing

Weave Services Limited

20

What does it take to make it

happen?

Weave Services Limited

21

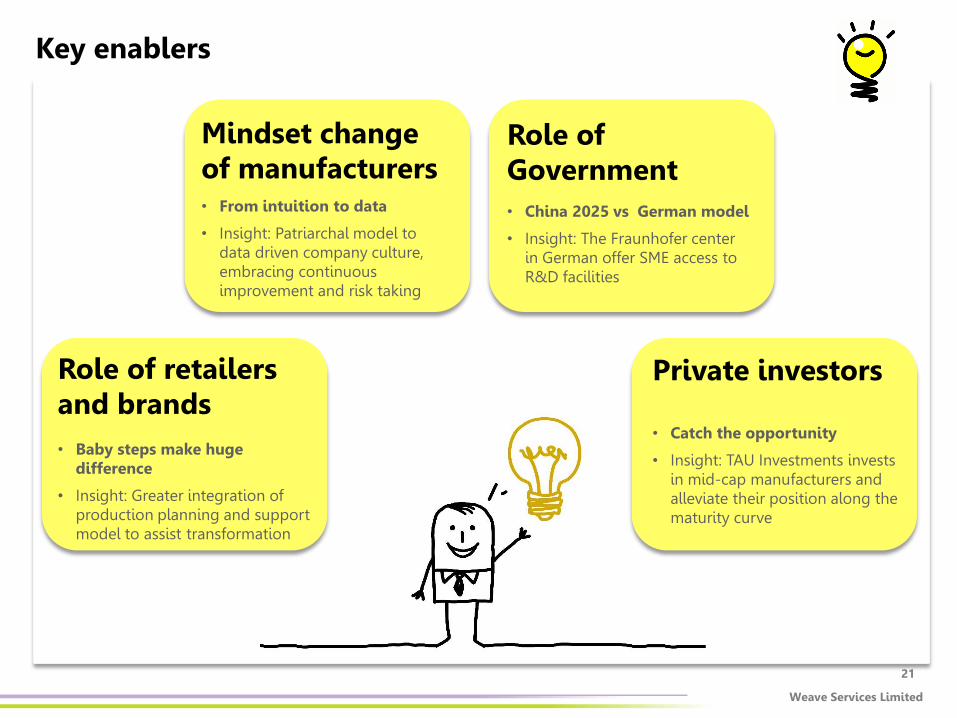

• Baby steps make huge difference

• Insight: Greater integration of production planning and support model to assist transformation

Key enablers

Role of retailers and brands

Manufacturers mindset

Private investors

• Catch the opportunity

• Insight: TAU Investments invests in mid-cap manufacturers and alleviate their position along the maturity curve

Mindset change of manufacturers

Role of Government

• From intuition to data

• Insight: Patriarchal model to data driven company culture, embracing continuous improvement and risk taking

• China 2025 vs German model

• Insight: The Fraunhofer centerin German offer SME access to R&D facilities

Weave Services Limited

22

In turbulent times,

Efficiency based

innovation

should be considered as a

core part of retailers and

manufacturers’ strategies…

…it will require more

collaboration, joint-efforts

and mutual understanding

from retailers and

manufacturers to unleash

the next level of efficiency!

Last words

Weave Services Limited

23

Weave Services LimitedTAL Building, 5th Floor, 49 Austin RoadKowloon, Hong KongPhone: +852 27386211Email: [email protected]

Consulting-Outsourcing-Capability Building

Recommended