“MAKING A LAUNCH STRATEGY FOR A NEW BRAND OF AN EMERGING

COMPANY IN THE INTERNATIONAL AND DOMESTIC MARKET” by Diptarup Biswas

Dissertation submitted to the Rajiv Gandhi University Of Health Science, Karnataka, Bangalore In partial fulfillment of the requirements for the degree of MASTER OF PHARMACY IN PHARMACEUTICAL MARKETING AND MANAGEMENT Under the guidance of Dr.V Kusum Devi (H.O.D) Department of Pharmaceutical Marketing and Management Al – Ameen College of Pharmacy Bangalore – 560027 March 2010

COPYRIGHT

Declaration by the Candidate

I here by declare that the Rajiv Gandhi University of Health Sciences,

Karnataka shall have the rights to preserve, use and disseminate this

dissertation / thesis in print or electronic format for academic / research

purpose.

Date: March 2010

Place: Bangalore

DIPTARUP BISWAS

© Rajiv Gandhi University of Health Sciences, Karnataka

ii

Declaration by the Candidate

I hereby declare that this dissertation/ thesis entitled “Making a launch

strategy for a new brand of an emerging company in the international

and domestic market” is a bonafide work carried out by me under the kind

guidance of Dr. V Kusum Devi, (H.O.D) Department of Pharmaceutical

Marketing and Management, Al-Ameen College of Pharmacy, Bangalore

Date: March 2010

Place: Bangalore

DIPTARUP BISWAS

iii

CERTIFICATE BY THE GUIDE This is to certify that the dissertation entitled

“MAKING A LAUNCH STRATEGY FOR A NEW BRAND OF AN EMERGING COMPANY IN THE INTERNATIONAL AND DOMESTIC MARKET” is a bonafide research work done by

DIPTARUP BISWAS

In partial fulfillment of the requirement for the degree of

Master of Pharmacy in Pharmaceutical Marketing and Management

Date : March 2010 Place: Bangalore

Signature of the Guide

Dr. V Kusum Devi HOD

Dept. of Pharmaceutical Marketing and Management

iv

CERTIFICATE OF CO-GUIDE

This is to certify that the dissertation entitled “Making a launch strategy for a

new brand of an emerging company in the international and domestic

market” is a bonafide research work carried out by Diptarup Biswas under the

co-guidance of Dr. Anjan Roy.

Dr. Anjan Roy

Managing Director

R L FINE CHEM

v

ENDORSEMENT BY THE HOD, PRINCIPAL/HEAD OF THE INSTITUTION

This is to certify that the dissertation entitled Making a launch strategy for a

new brand of an emerging company in the international and domestic

market” is a bonafide research work carried out by Diptarup Biswas under the

guidance of Dr.V Kusum Devi (HOD)

Department of Pharmaceutical marketing and management, Al-Ameen College of Pharmacy, Bangalore Dr. V Kusum Devi HOD Dept. Pharmaceutical Marketing and Management Al-Ameen College of Pharmacy Bangalore 560027

Prof. B.G Shivananda Principal Al-Ameen College of Pharmacy Bangalore 560027

Date : March 2010 Place : Bangalore

Date : March 2010 Place : Bangalore

vi

ACKNOWLEDGEMENT

As I begin to reflect on to the magnitude of this project, I am reminded of the

kindness, support and affection rendered to me by selfless people to whom I am grateful.

I am indebted to my esteemed guide Dr. V Kusum Devi, HOD, Department of

Pharmaceutical marketing and management, for her valuable guidance, her advice and

constant encouragement, which saw me through the course of my research work.

I extended my sincere gratitude to Mr. Ashoke Bhattacharya (Vice President, R

L Fine Che)., Mr. Pawan K. Ghai (Marketing Head, RL Fine Chemicals), Mr Anjan

Ray (Managing Director, R L Fine Chem), Mr. P V Prasad (General manager, Centum

Pvt. Ltd), Dr. Asha N, Mr. Indu Sankar (Asst. Manager, International Procurement,

Manipal) for providing me valuable help and guidance through out my academic period

here.

I am thankful to “Almighty” and my “Guru-dev” for showering their grace and

blessing on me and helping me to overcome every obstacle I faced till now in my life.

I am blessed indeed to have such supportive, caring, and loving Parents, and it is

to them that I dedicate this thesis.

vii

I also want to thank my late Grand father, Choto pisi and Pisay-mosai, Mejo pisi

and Pisay mosai, Chanu pisi, Mala kakimuni, Jethu and Jemma for their support and

blessings.

I would be failing in my duty, if I do not express my heartfelt thanks to my

dearest friends, Gayatri, Siddharth, Rohit, Pasa, Chinmaya, Pankaj, Amitava, Trishna,

Snigdha, Sourab, Deena, Priyanka, Shruti, Suman, my juniors Pradipta, Saptarshi,

Soumoditta, Jaydeep, Chandana, Shubojit and seniors Aditya bhai, Viswas bhai, Sardul

bhai for their immense love, help, encouragement and support and without which I may

not have completed this work successfully.

I am also indebted to all the Cardiologists, MD Internal medicine, General

practitioners and Pharmacists/Chemists across Bangalore and Kolkata, who

participated in the primary market research and provided their comments and views that

laid the foundation of this work.

And lastly I would like to thank all those who have directly or indirectly helped

me getting through this project successfully.

Date: March 2010

Place: Bangalore Diptarup Biswas

viii

TABLE OF CONTENTS

ix

Sl. No.

CONTENTS PAGE NUMBER

1 Introduction 1

2 Need for study 4

3 Objectives 7

4 Review of Literature 8

5 Methodology 35

6 Results 45

7 Discussion 212

8 Conclusions 217

9 Summary 222

10 Bibliography 226

11 Annexure 230

LIST OF ABBREVEATIONS

x

ABBREVEATIONS

FULL FORMS

US United States

IMS Intercontinental Marketing Services

HCT Hydrochlorothiazide

BP Blood Pressure

CC Candesartan cilexetil

WHO World Health Organization

CO Cardiac Output

PVR Peripheral vascular resistance

ACTH Adrenocorticotropic hormone

IUPAC International Union of Pure and Applied Chemists

AUC Area Under Curve

RAAS Renin–Angiotensin–Aldosterone System

ARBs Angiotensin Receptor Blockers

ACEi Angiotensin-Converting Enzyme Inhibitor

CEO Chief Executive Officer

GDP Gross Domestic Product

USD United States Doller

CA Current Account

FDI Foreign Direct Investment

PT Partido dos Trabalhadores (portugese)

PAC Programade Aceleraçãodo Crescimento (portugese)

TRIPS Trade Related Intellectual Property Rights

ANVISA National Sanitary Vigilance Agency

IPR Intellectual Property Rights

HIV Human Immuno Virus

PTO Patent and Trademark Office

CMED Chamber for the Regulation of the Market of Medicines

xi

GNI Gross National Income

OECD Organization for Economic Cooperation and Development

RBI Reserve Bank of India

CNS Central Nervous System

CAGR Compounded Annual Growth Rate

CVS Cardio Vascular Disease

OPPI Organization of Pharmaceutical Producers of India

ORG Operational Research Group

R&D Research and Development

KPMG Klynveld Peat Marwick Goerdeler (accounting firm)

USFDA United States Food and Drug Administration

CRAMS Contract Research and Manufacturing services

JHW Jaipur Heart Watch

DOHA Declaration-Concession to developing nations

DCs Developed Countries

LDCs Less Developed Countries

WTO World Trade Organization

API Active Pharmaceutical Industry

BRIC Brazil, Russia, India and China

NCE New Chemical Entity

UKMCA United Kingdom Module Constructors Association

NDDS Novel Drug Delivery System

ANDA Abbreviated New Drug Application

TB Tuberculosis

AT Angiotensin Receptor

CCA Calcium Channel Antagonist

DPCO Drug Price Control Order

POD points of difference

POP points of parity

IBOPE Instituto Brasileiro de Opinião Pública e Estatística (portugese)

LIST OF TABLES

Table No.

Tables Page No.

4.1 Different brands of Candesartan available in Indian market 30

4.2 Different brands of Candesartan available in Brazilian market 31

6.1.1 Fact File Brazil 46

6.1.2 Economic Indicators 48

6.1.3 Major markets-2007 51

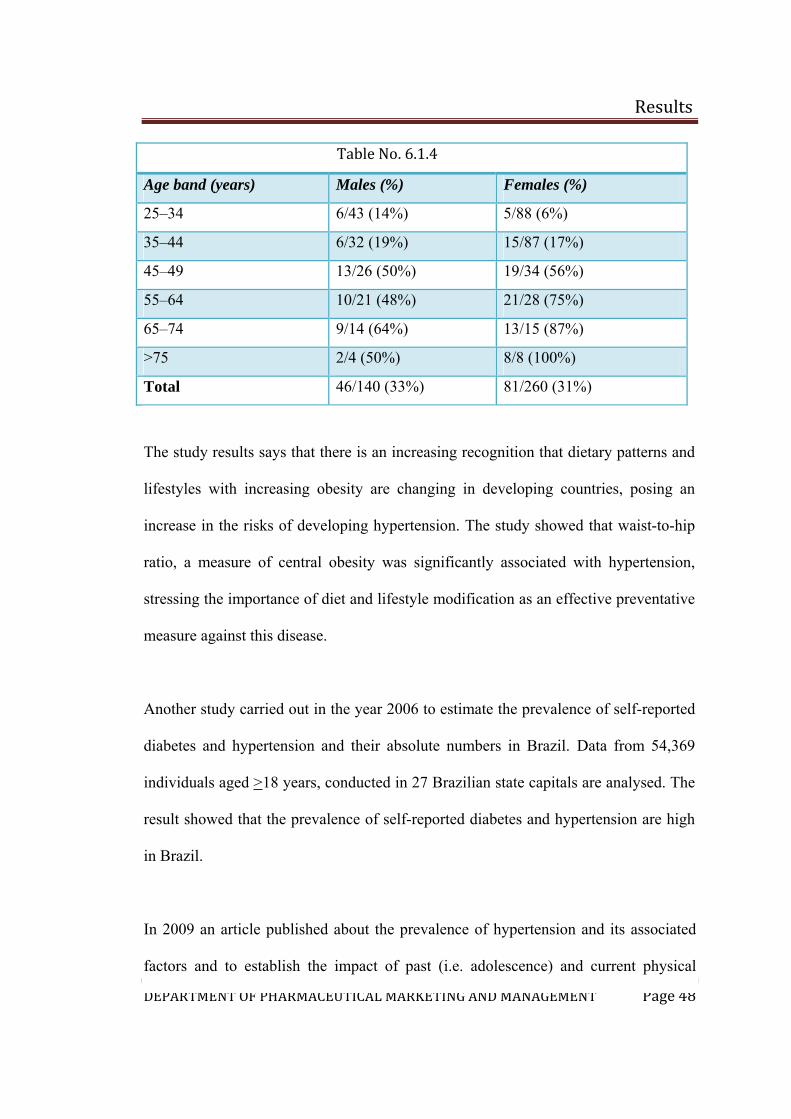

6.1.4 Prevalence of hypertension by age and sex in Brazil 53

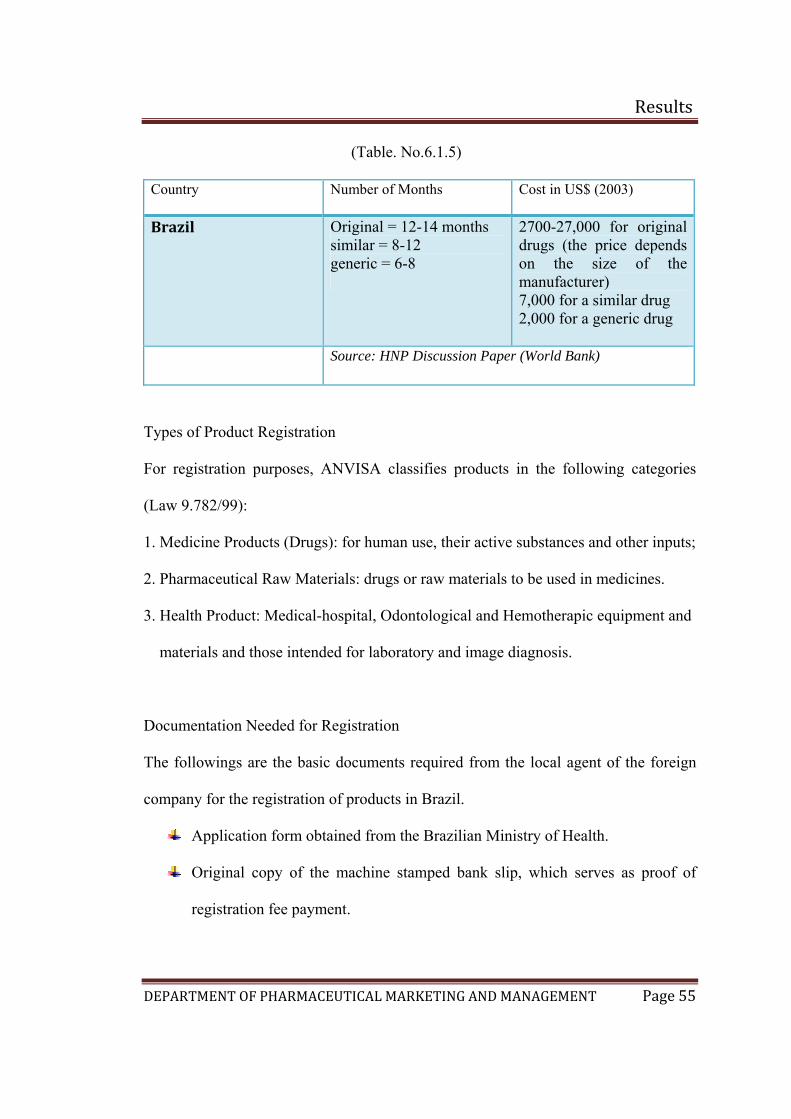

6.1.5 Time and fees for registration of drug in Brazil 60

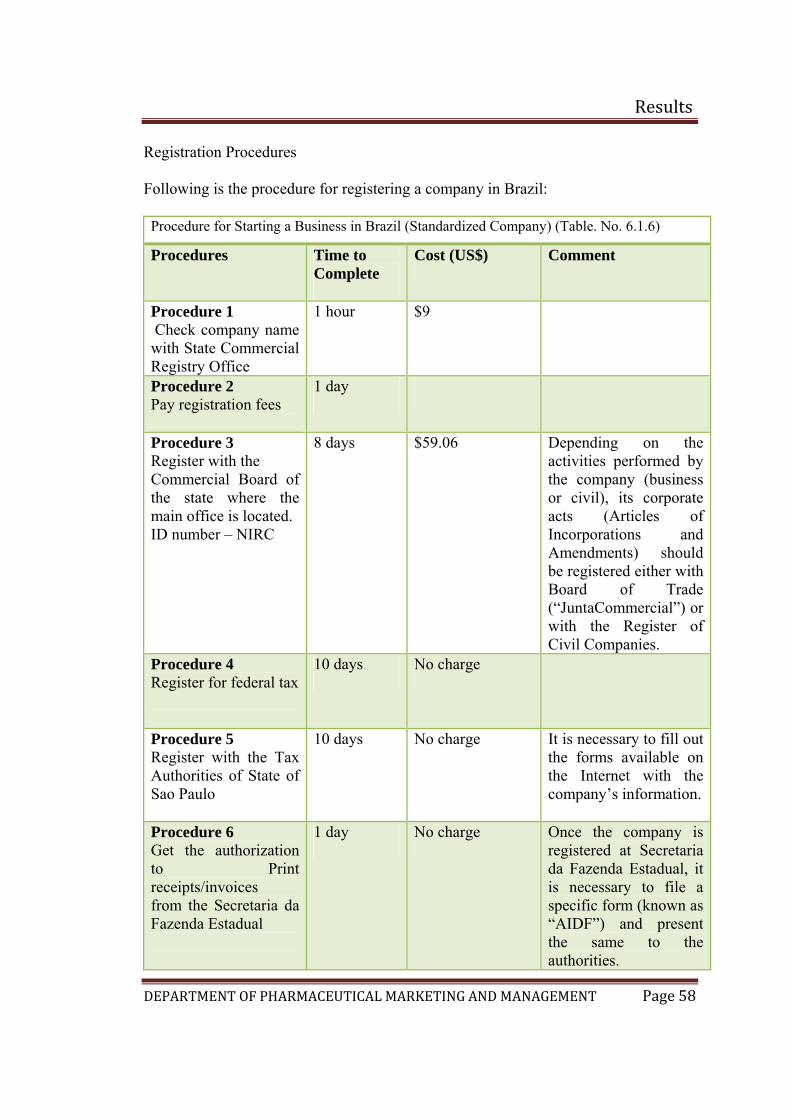

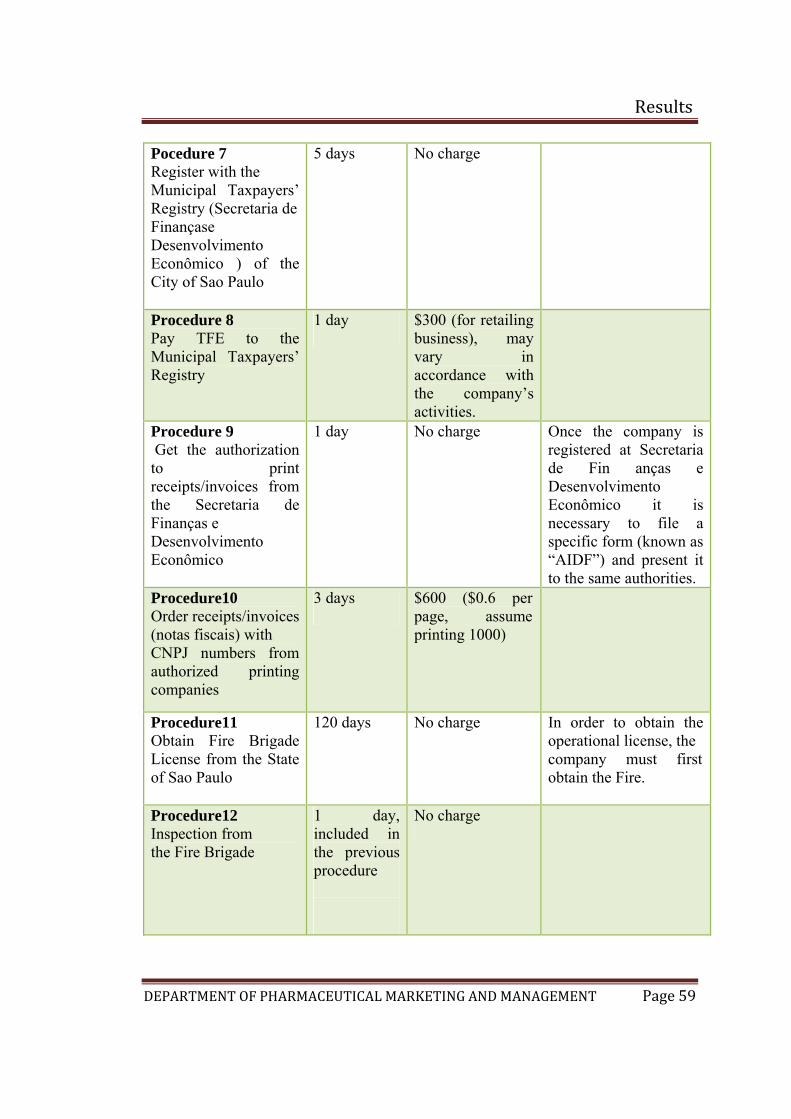

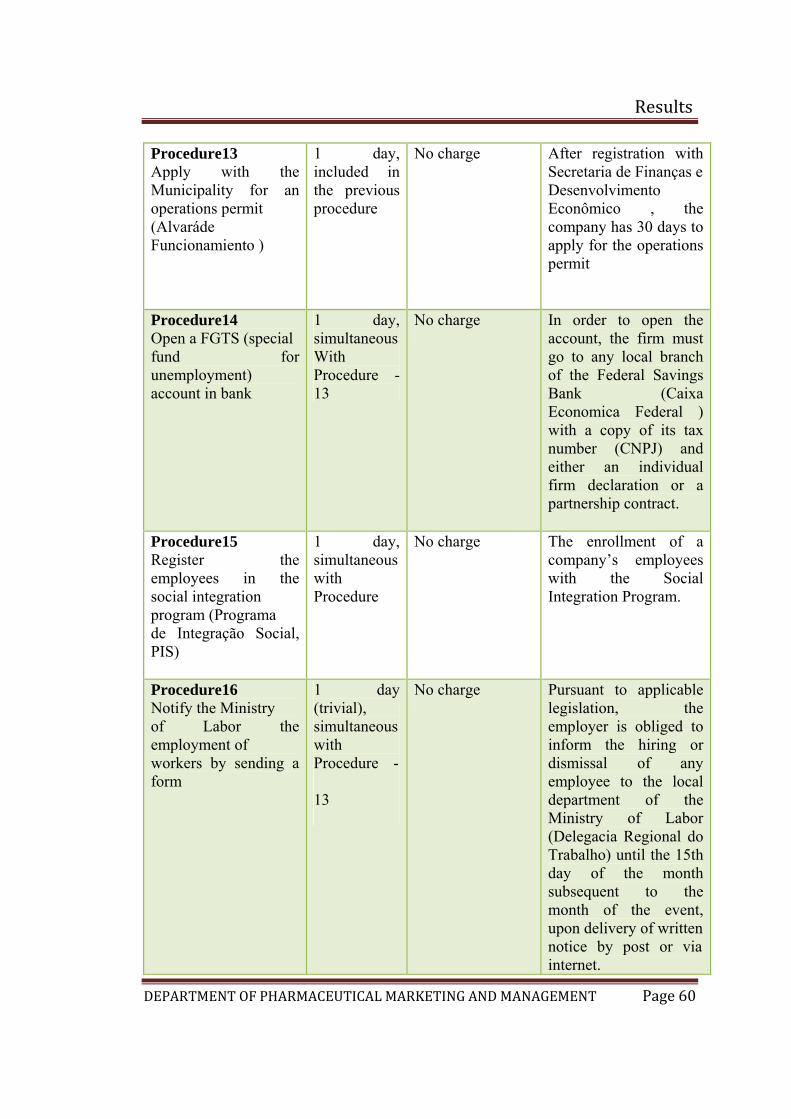

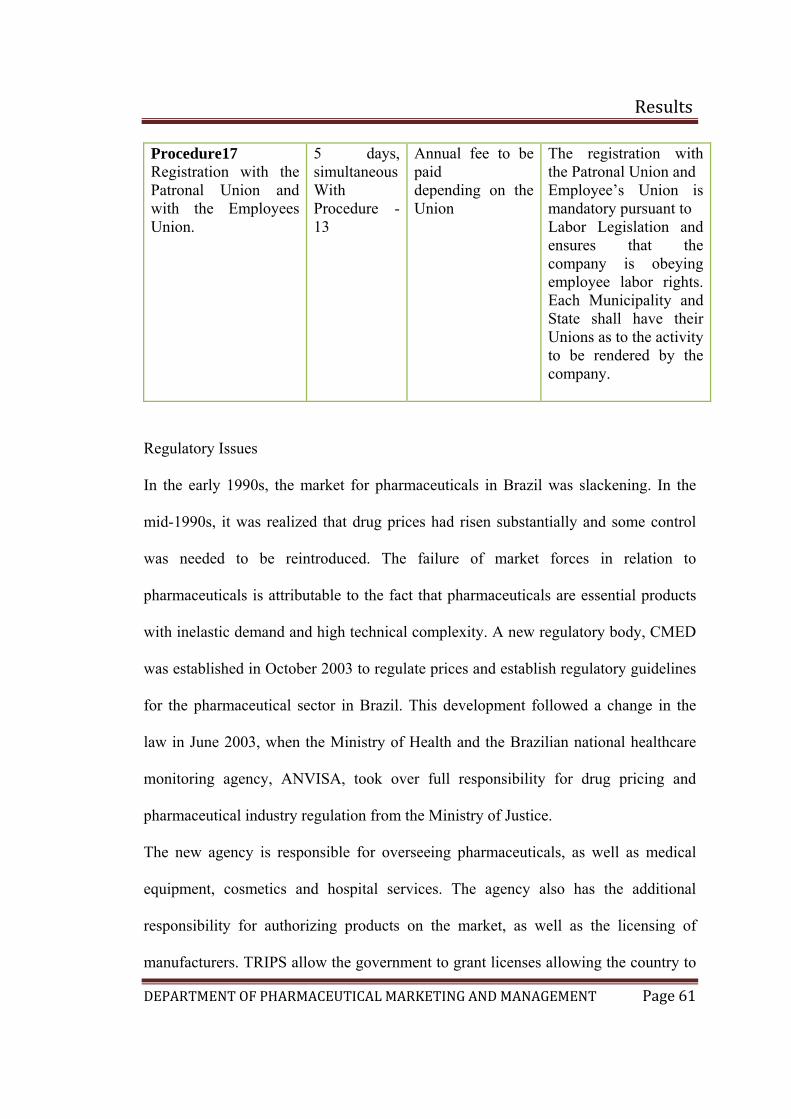

6.1.6 Procedure for Starting a Business in Brazil (Standardized Company)

63

6.1.7 Growth in Main Industry sectors ( in percentage) 69

6.1.8 Fact file India 69

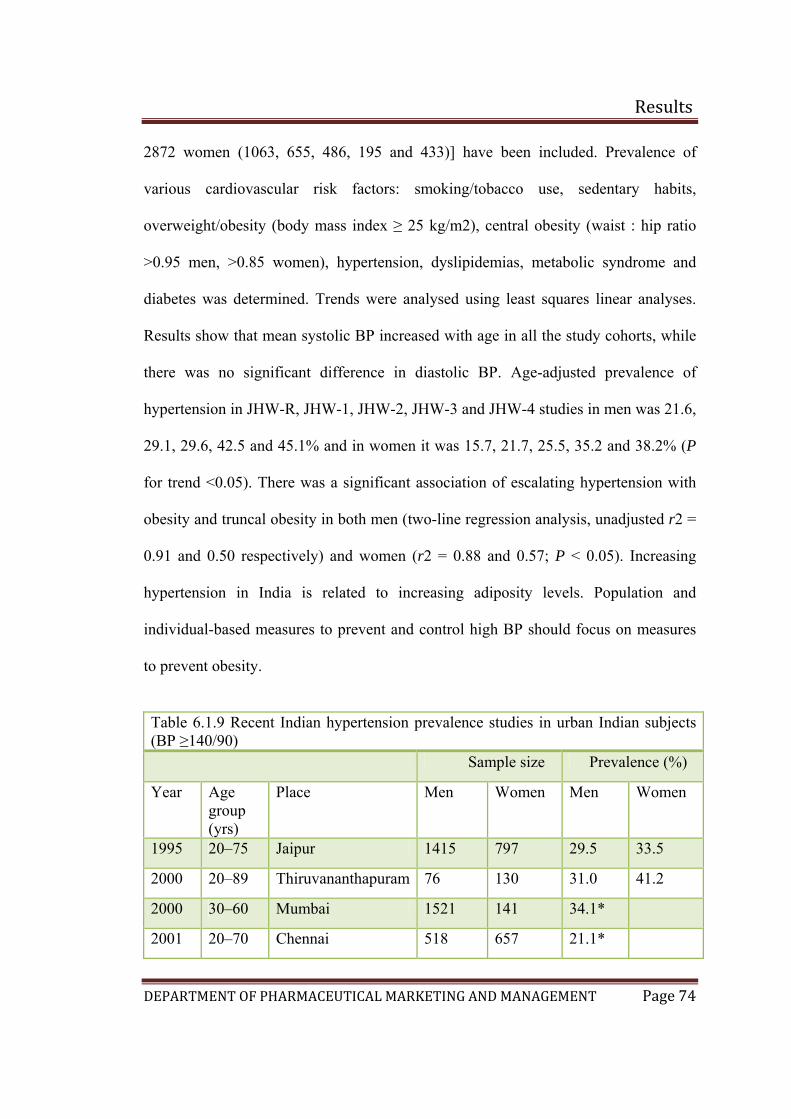

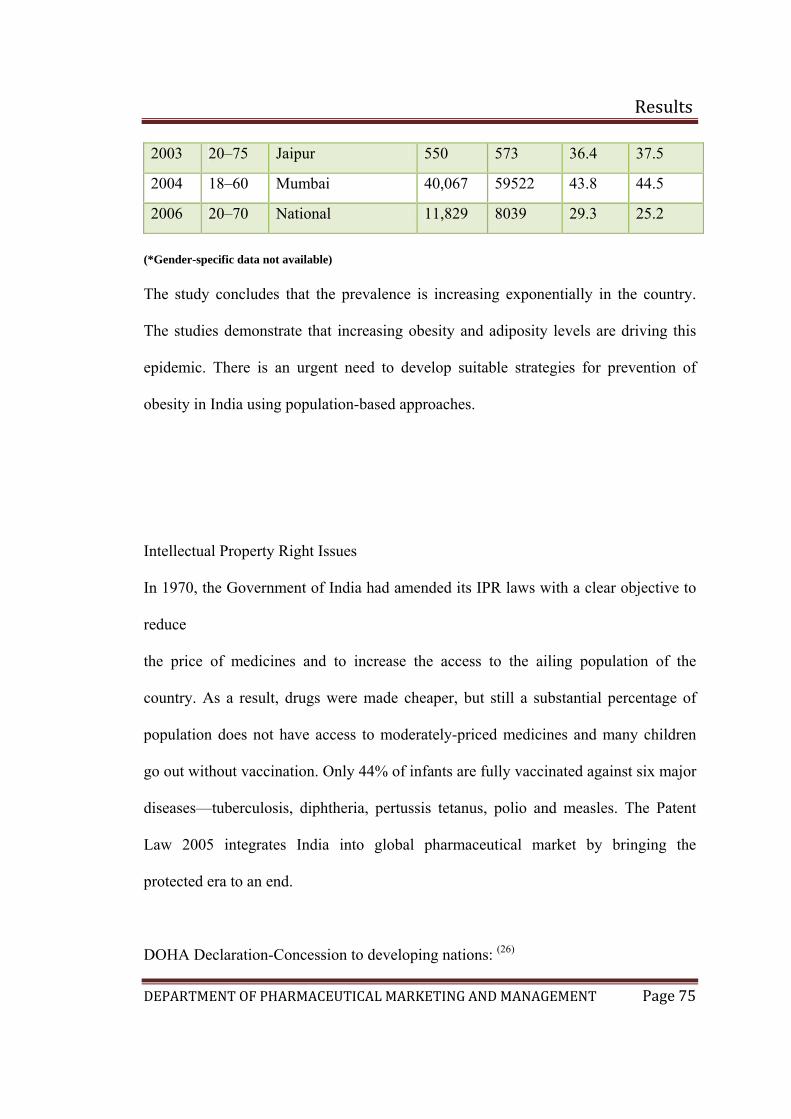

6.1.9 Recent Indian hypertension prevalence studies in urban Indian subjects

78

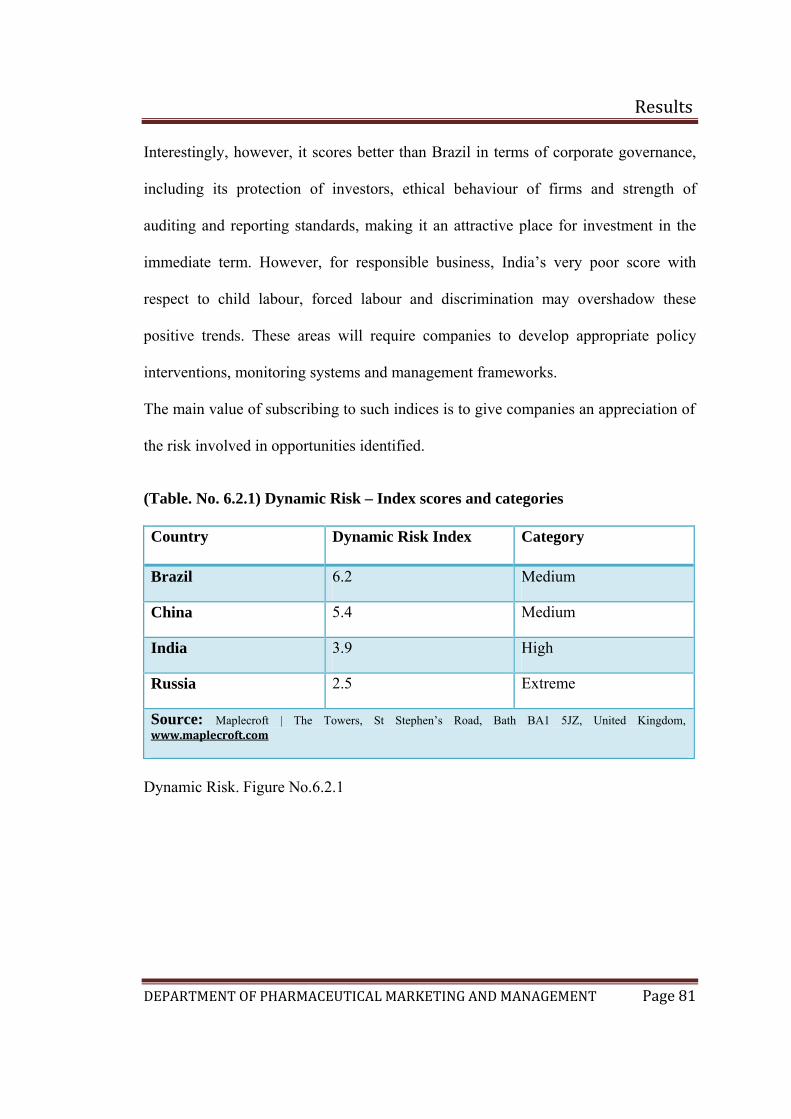

6.2.1 Dynamic Risk – Index scores and categories 86

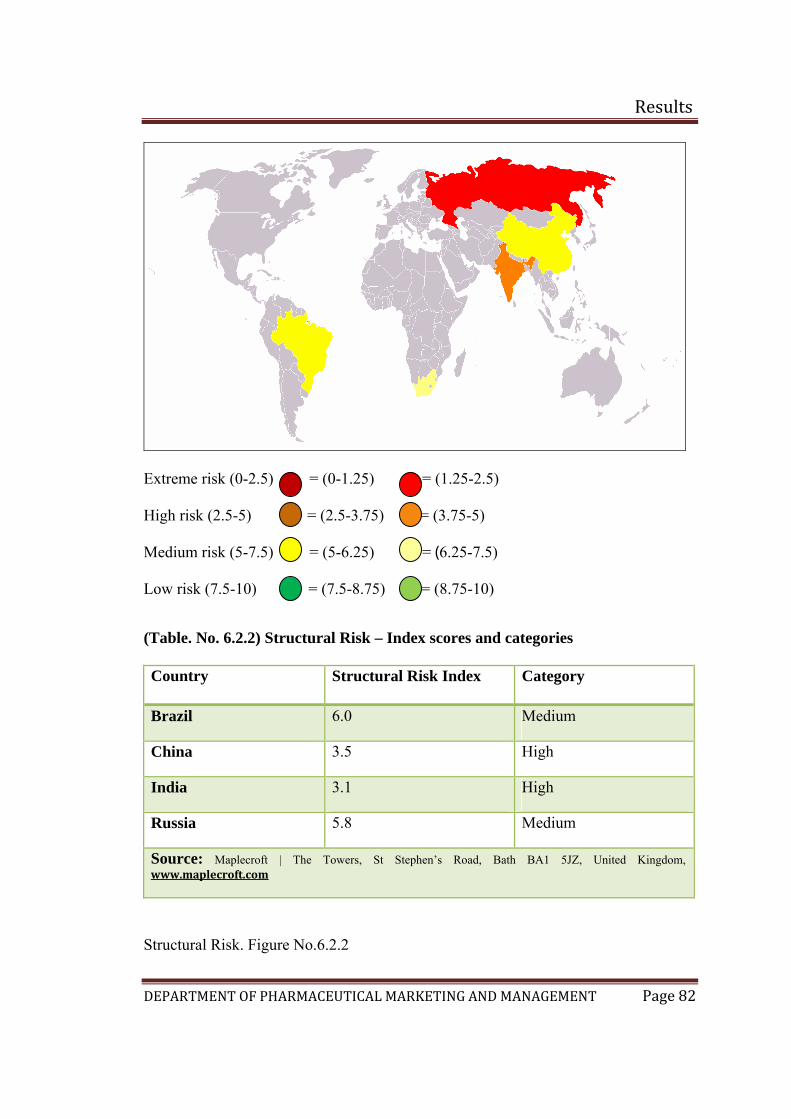

6.2.2 Structural Risk – Index scores and categories 87

6.2.3 Seven risk families 88

xii

LIST OF FIGURES

xiii

Figure No.

Figures Page No.

4.1 Anatomic sites of blood pressure control 8

4.2 Baro-reflexes arc 10

4.3 Amino terminal of human Angiotensinogen 11

4.4 Management of hypertension 18

4.5 Chemical Structure of Candesartan cilexetil 20

4.6 Chemical Structure of Hydrochlorothiazide 25

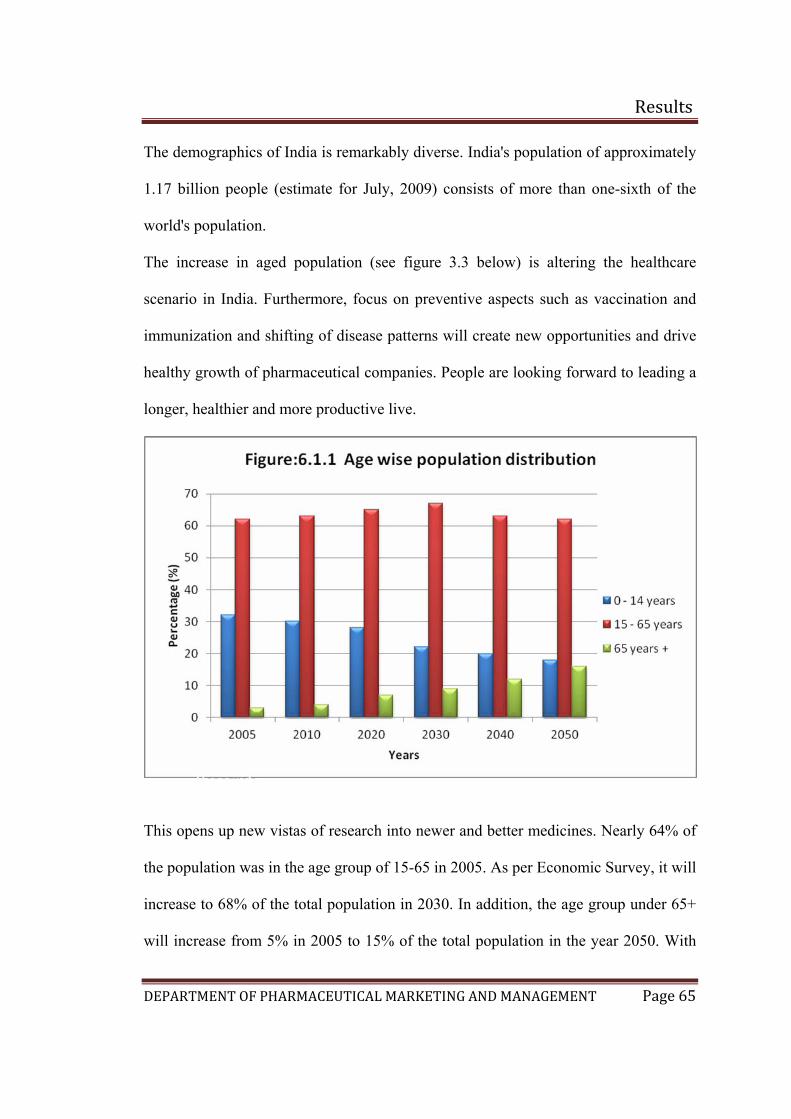

6.1.1 Age wise population distribution 70

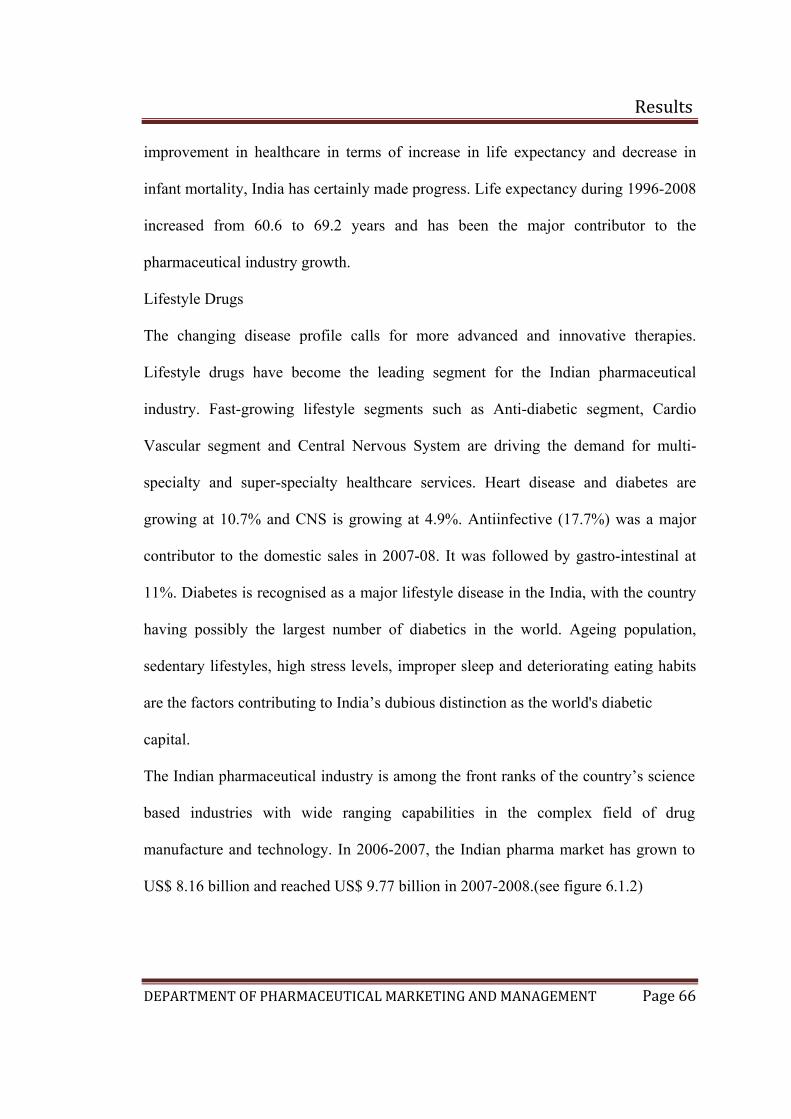

6.1.2 Indian pharmaceutical market 71

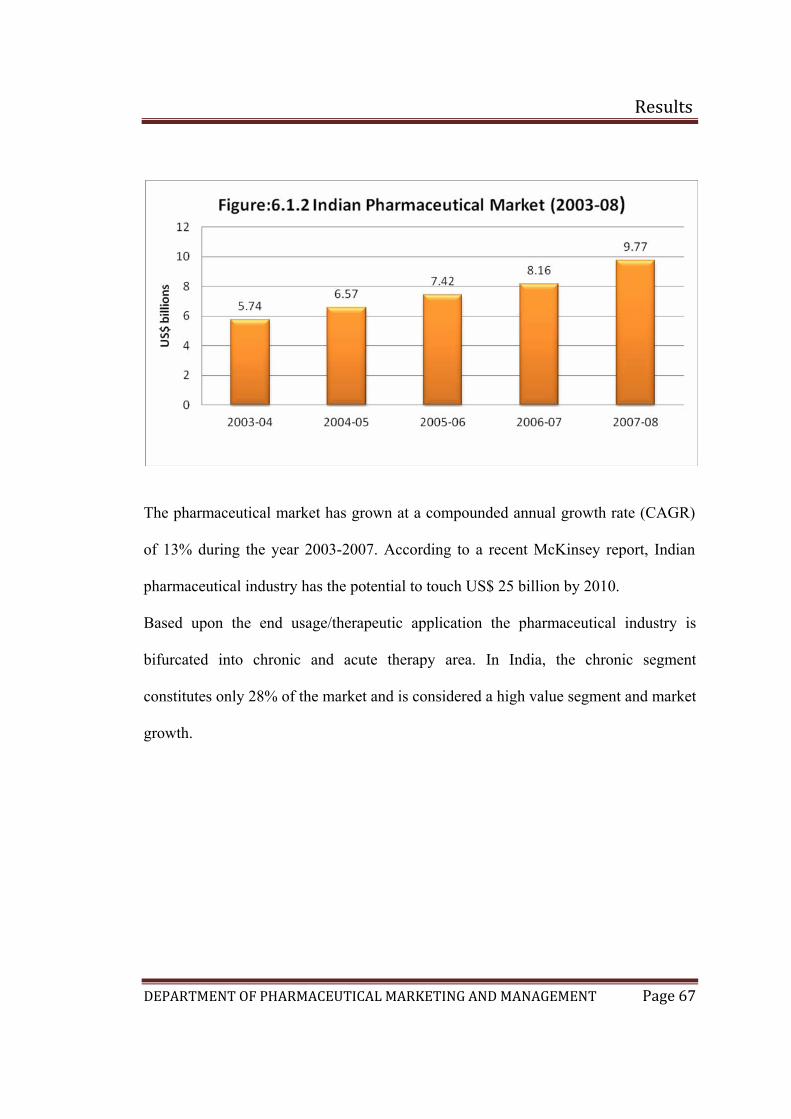

6.1.3 Chronic segments 72

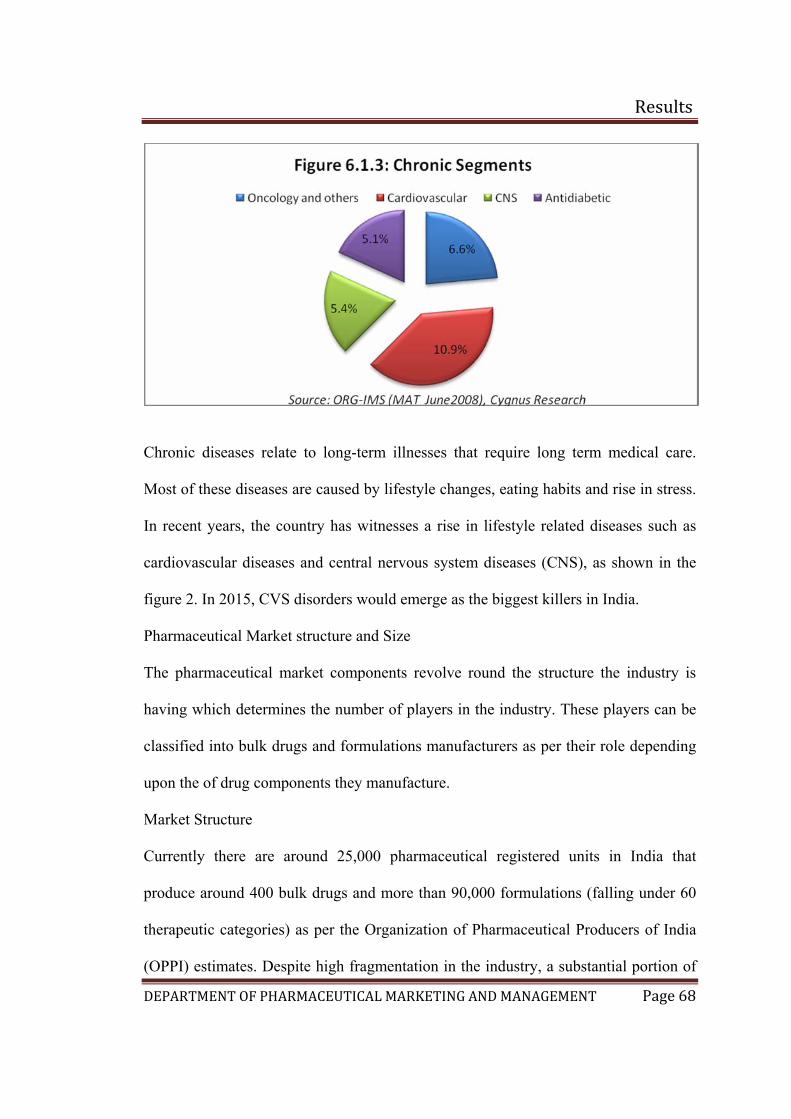

6.1.4 Retail sales of major companies 73

6.2.1 Dynamic Risk 86

6.2.2 Structural Risk 87

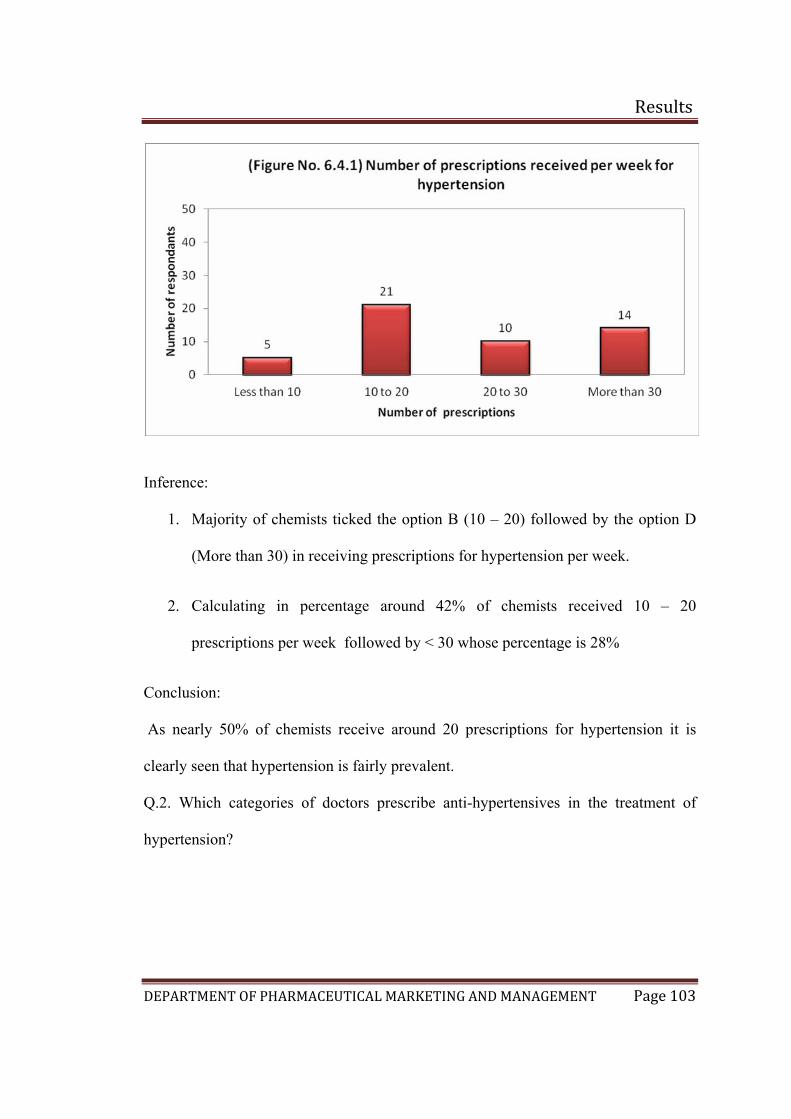

6.4.1 Number of prescriptions received per week for hypertension in Bangalore 104

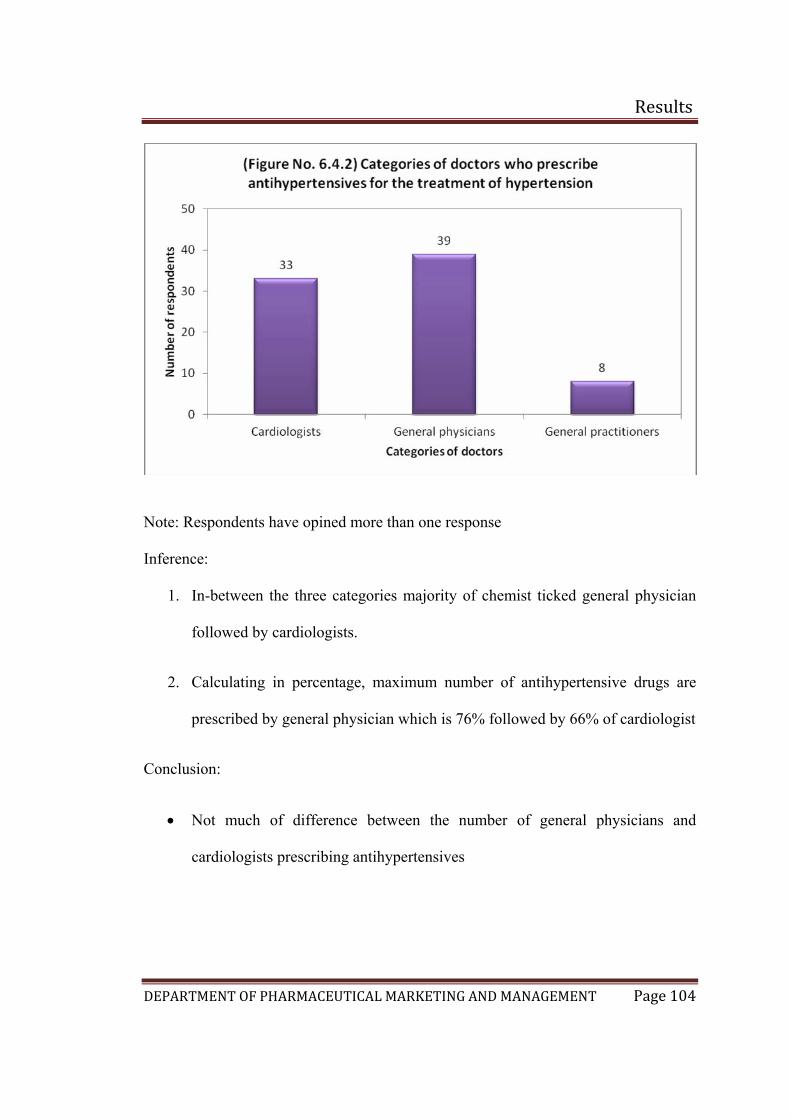

6.4.2 Categories of doctors who prescribe anti-hypertensives for the treatment of hypertension 105

6.4.3 Trend of movement of the following brands of ACE inhibitors 107

6.4.4 Trend of movement of the following brands of ARBs 109

6.4.5 Comparison between top 5 brands of ACE inhibitor and ARB 111

6.4.6 Trend of movement of the following brands of ACE inhibitors + Diuretic 112

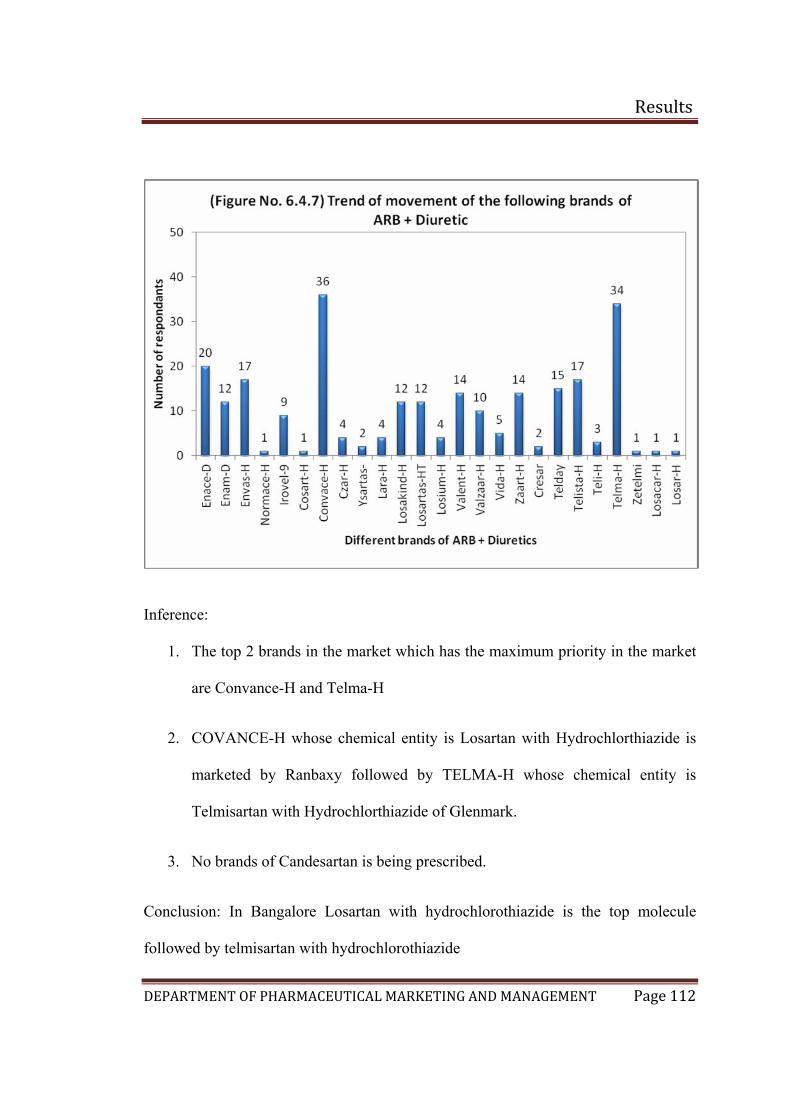

6.4.7 Trend of movement of the following brands of ARB + Diuretic 113

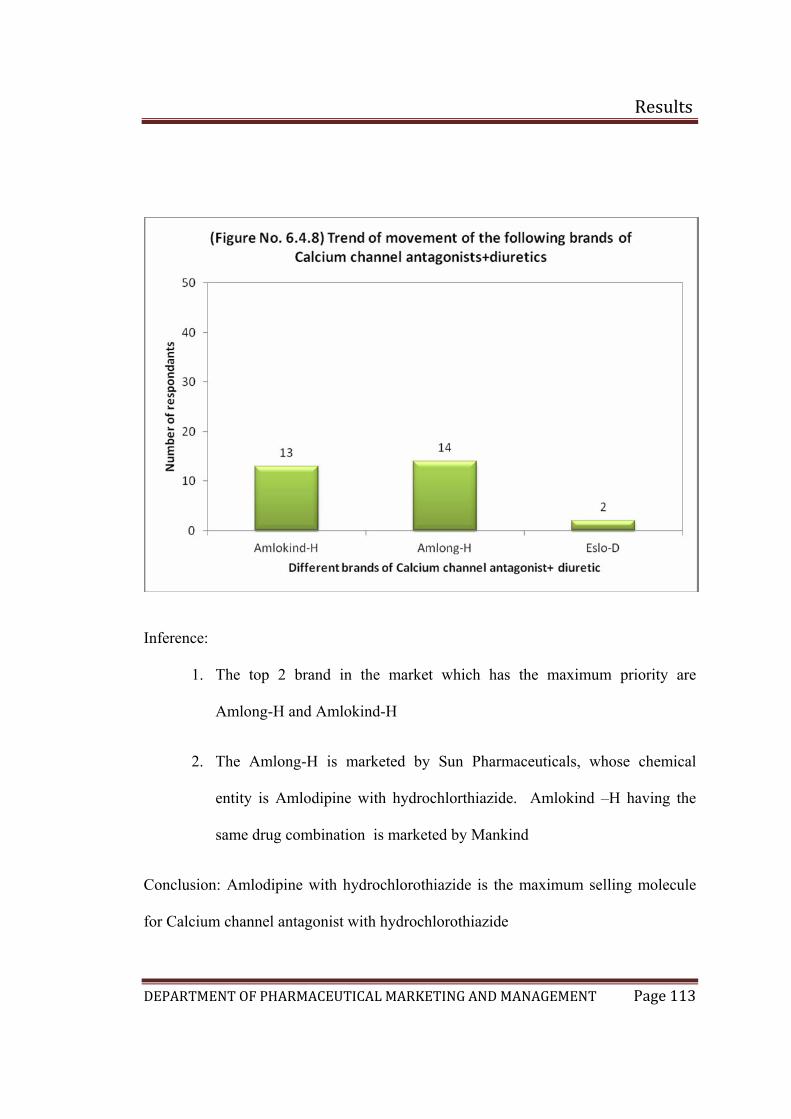

6.4.8 Trend of movement of the following brands of Calcium channel antagonist + Diuretic 114

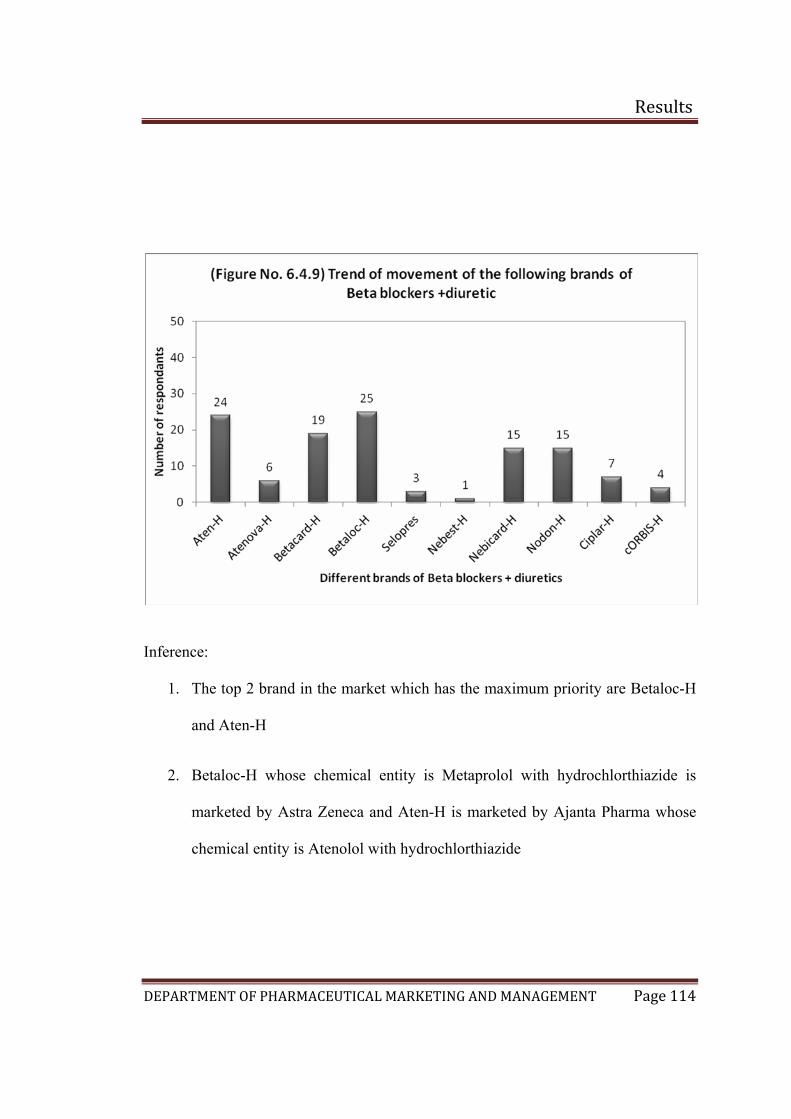

6.4.9 Trend of movement of the following brands of Beta blocker + Diuretic 115

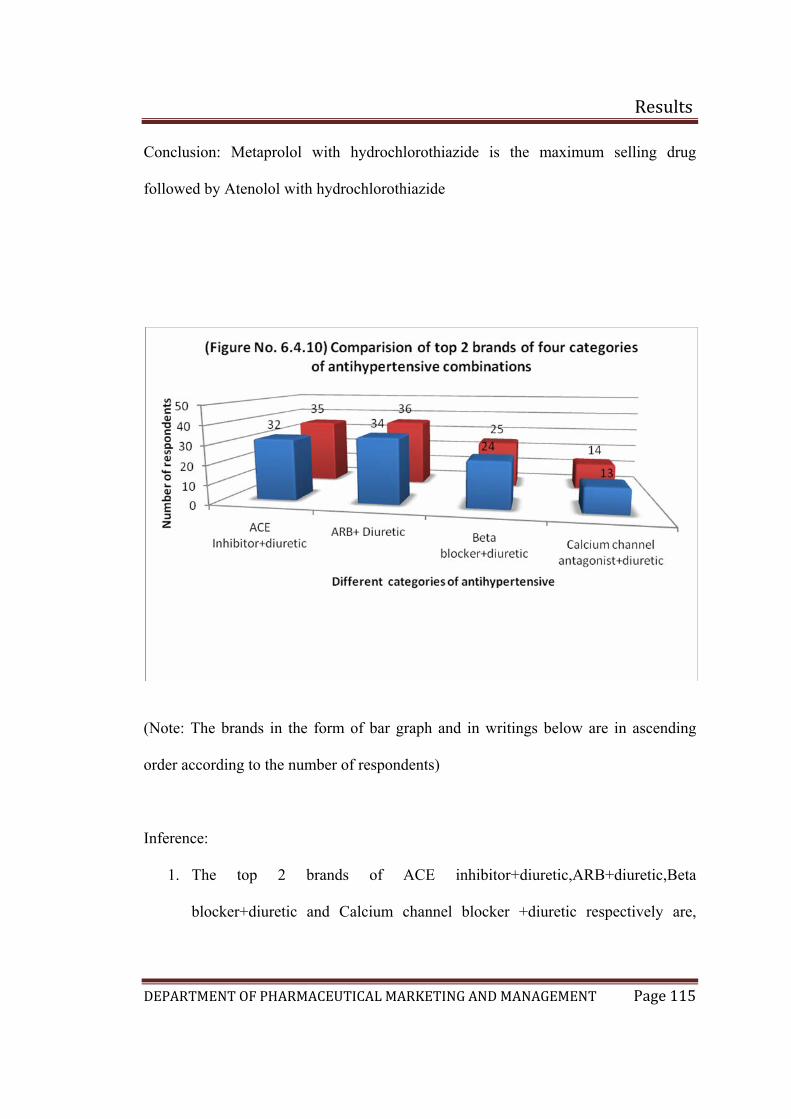

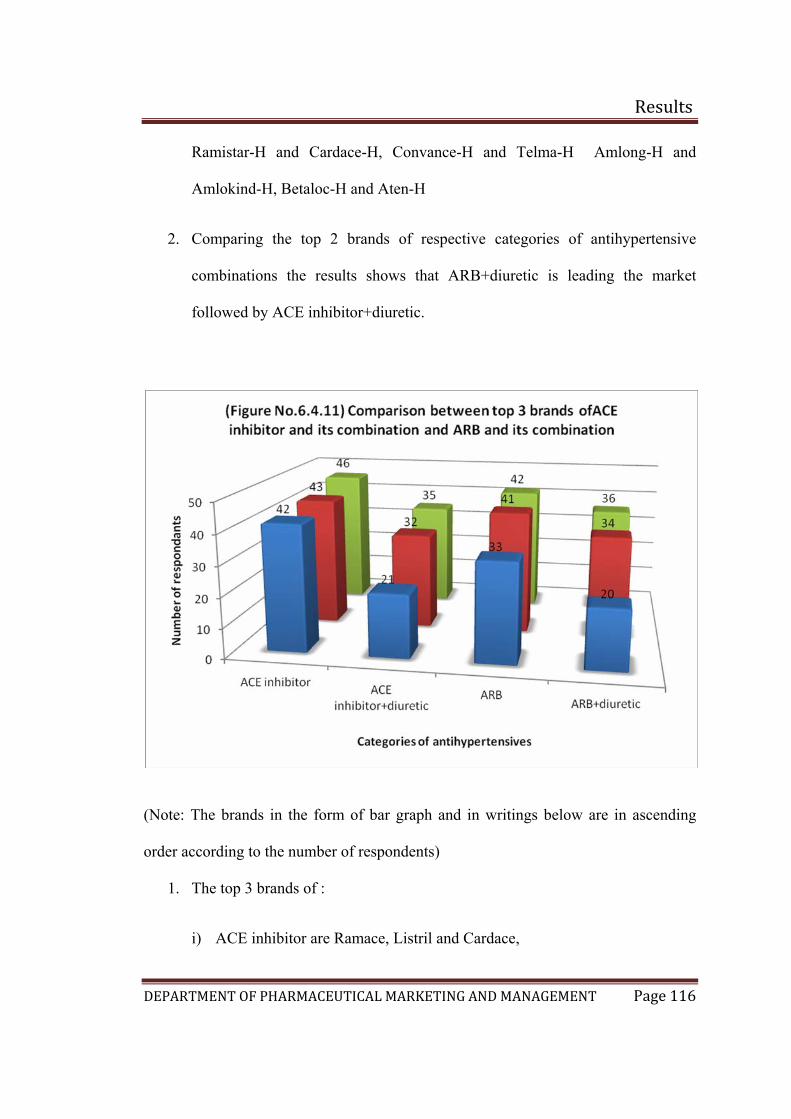

6.4.10 Comparison of 2 brands of four categories of antihypertensive combinations 116

xiv

6.4.11 Comparison between top 3 brands of ACE inhibitor and its combination and ARB and its combination 117

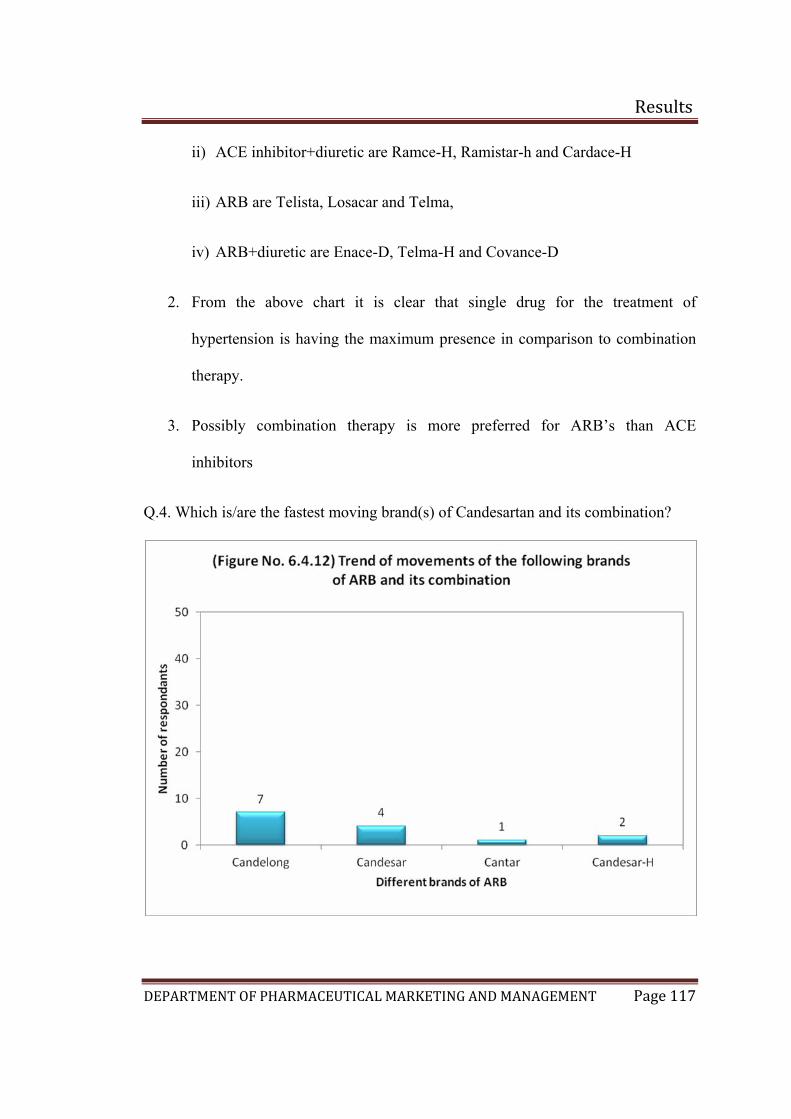

6.4.12 Trend of movement of the following brands of Candesartan and its combination 118

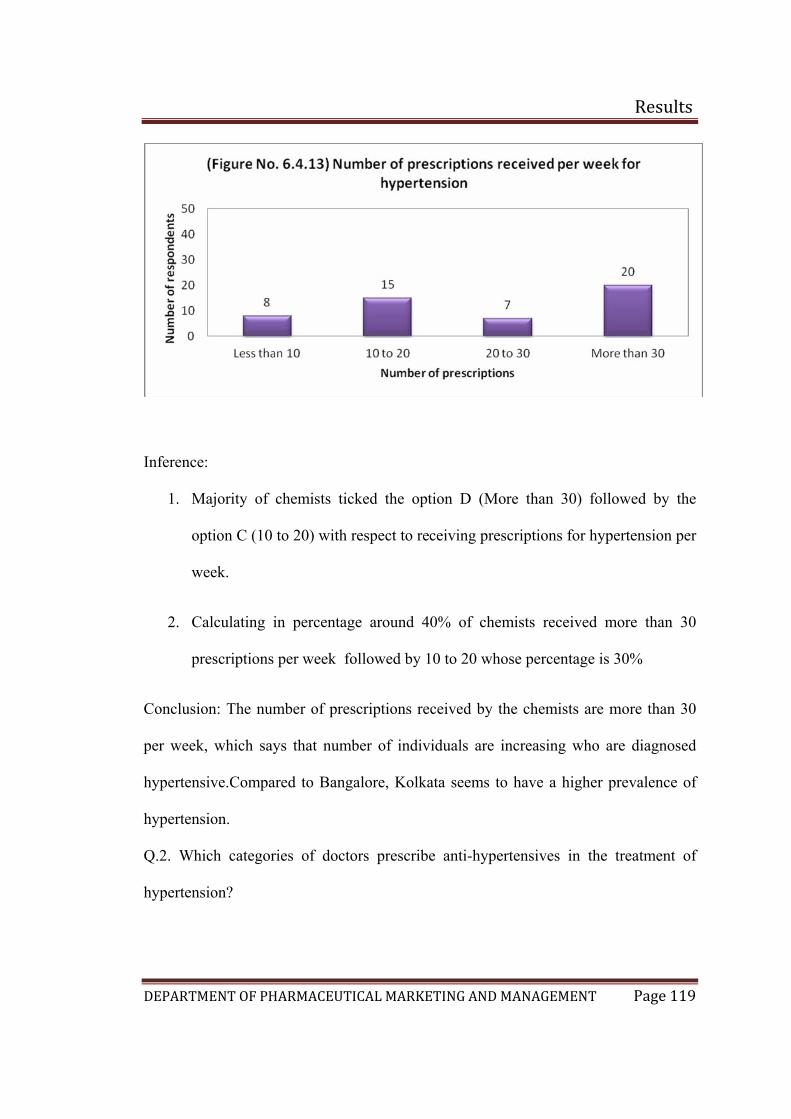

6.4.13 Number of prescriptions received per week for hypertension In Kolkata 119

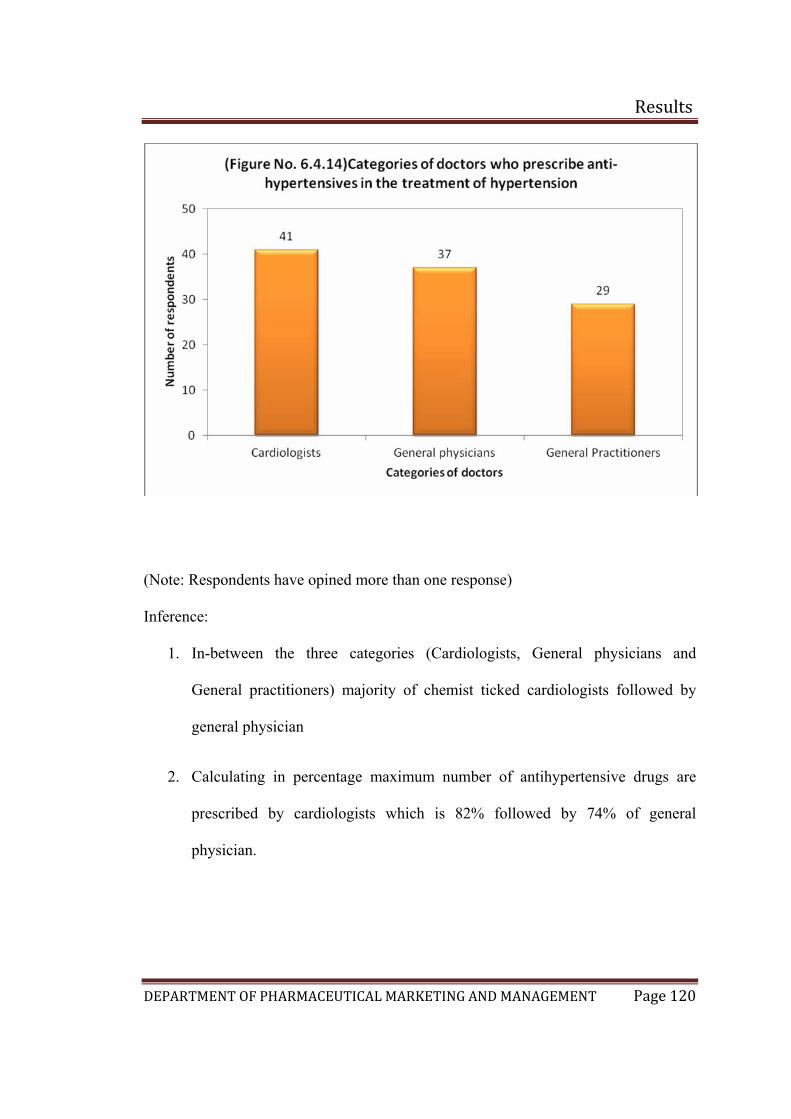

6.4.14 Categories of doctors who prescribe anti-hypertensives for the treatment of hypertension 120

6.4.15 Trend of movement of the following brands of ACE inhibitors 122

6.4.16 Trend of movement of the following brands of ARBs 124

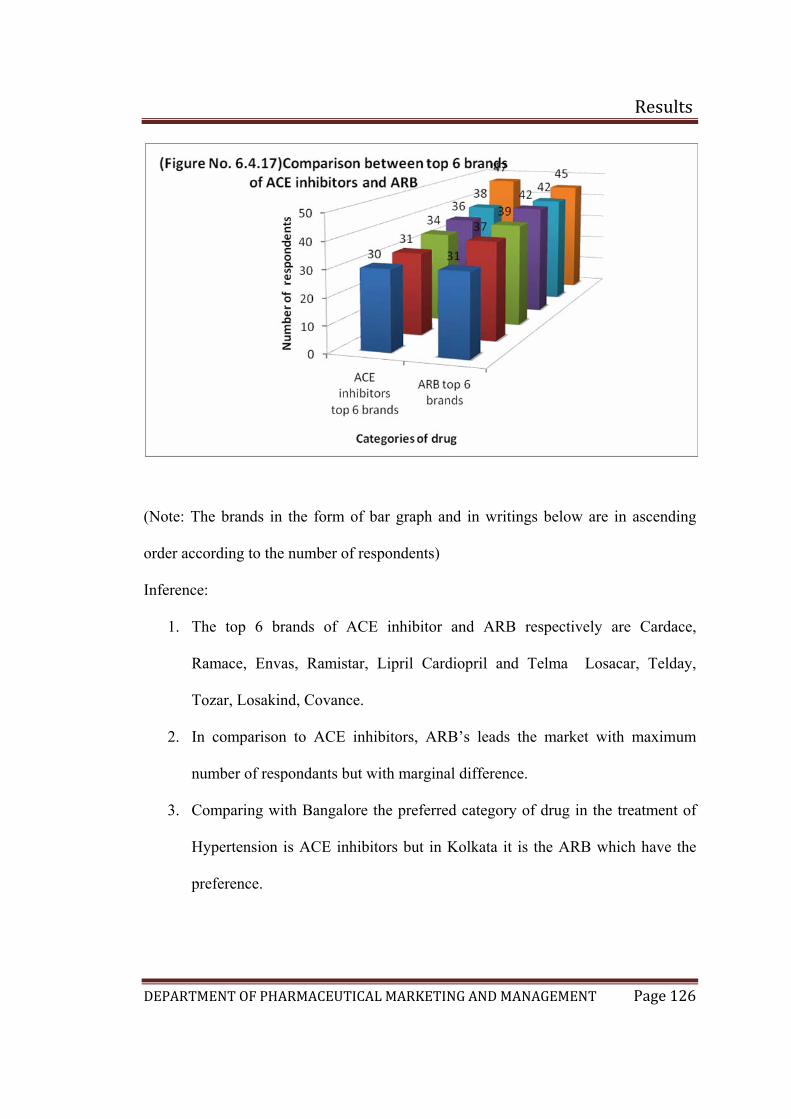

6.4.17 Comparison between top 6 brands of ACE inhibitor and ARB 126

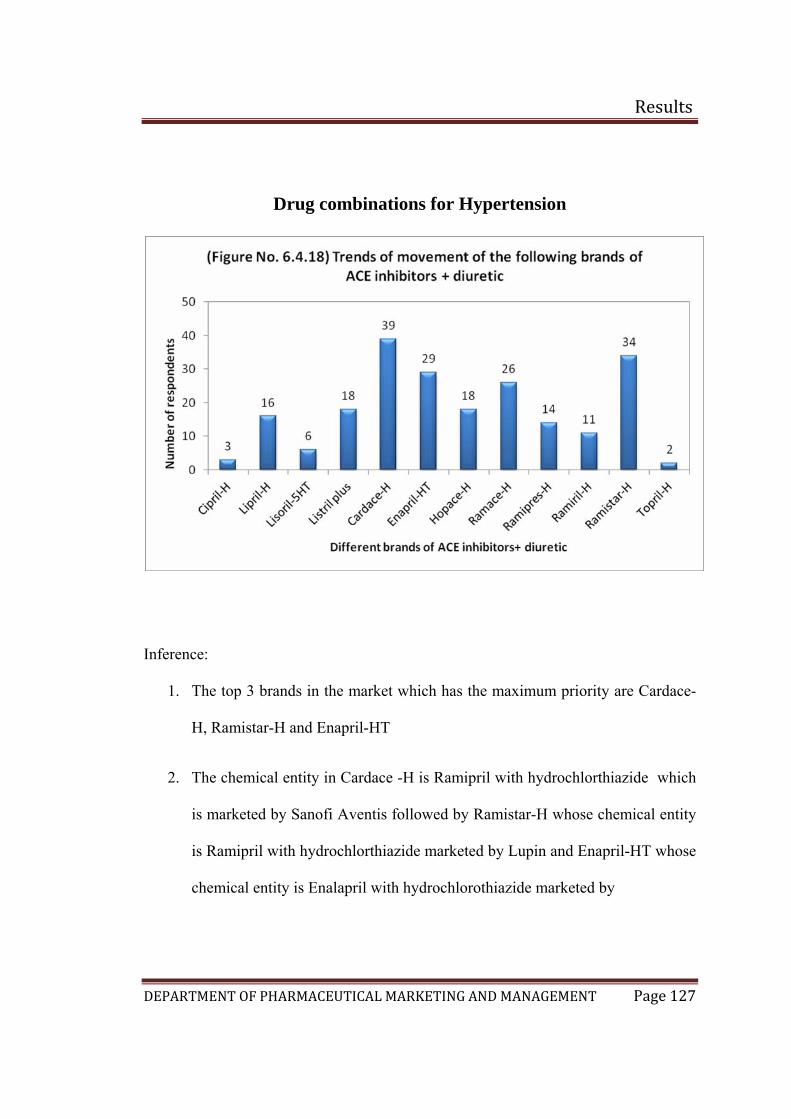

6.4.18 Trend of movement of the following brands of ACE inhibitors + Diuretic 127

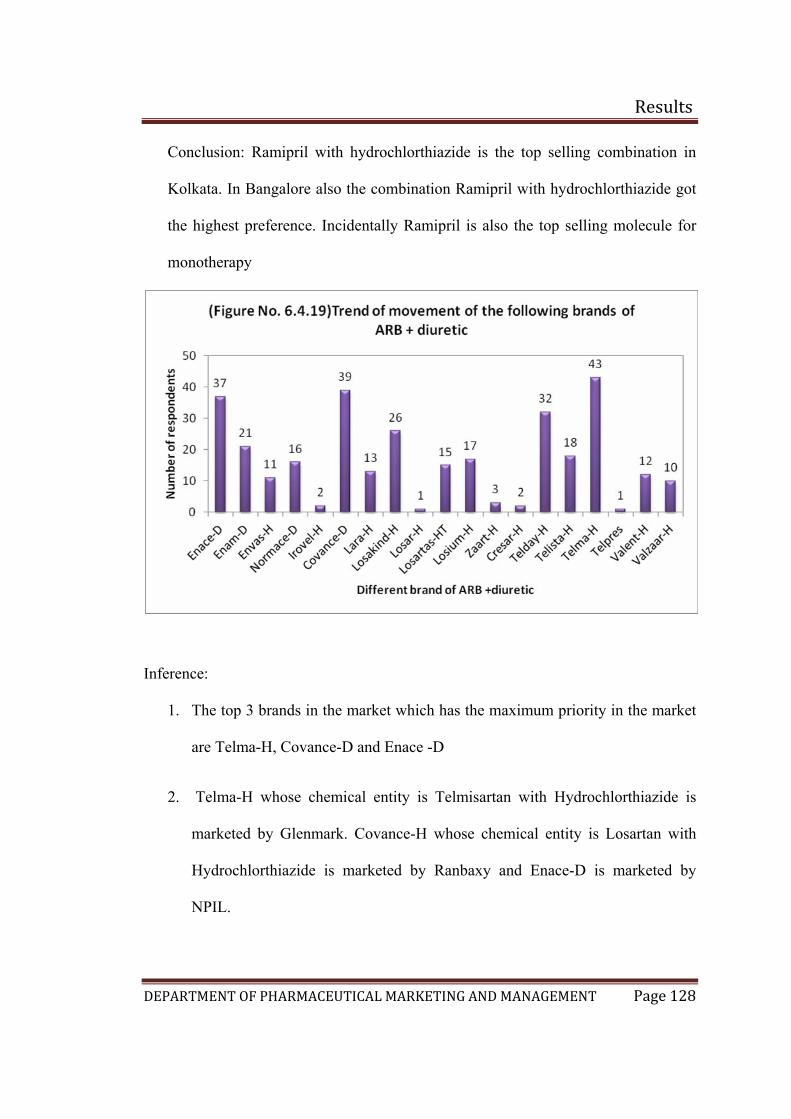

6.4.19 Trend of movement of the following brands of ARB + Diuretic 128

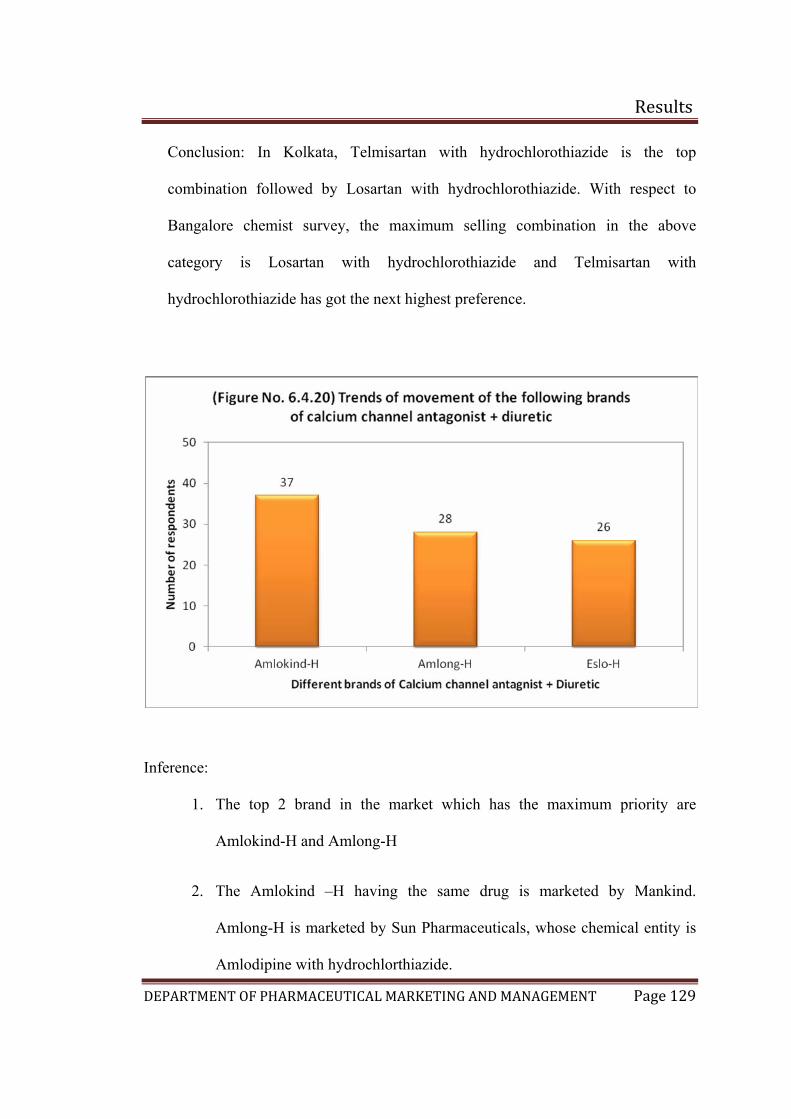

6.4.20 Trend of movement of the following brands of Calcium channel antagonist + Diuretic 129

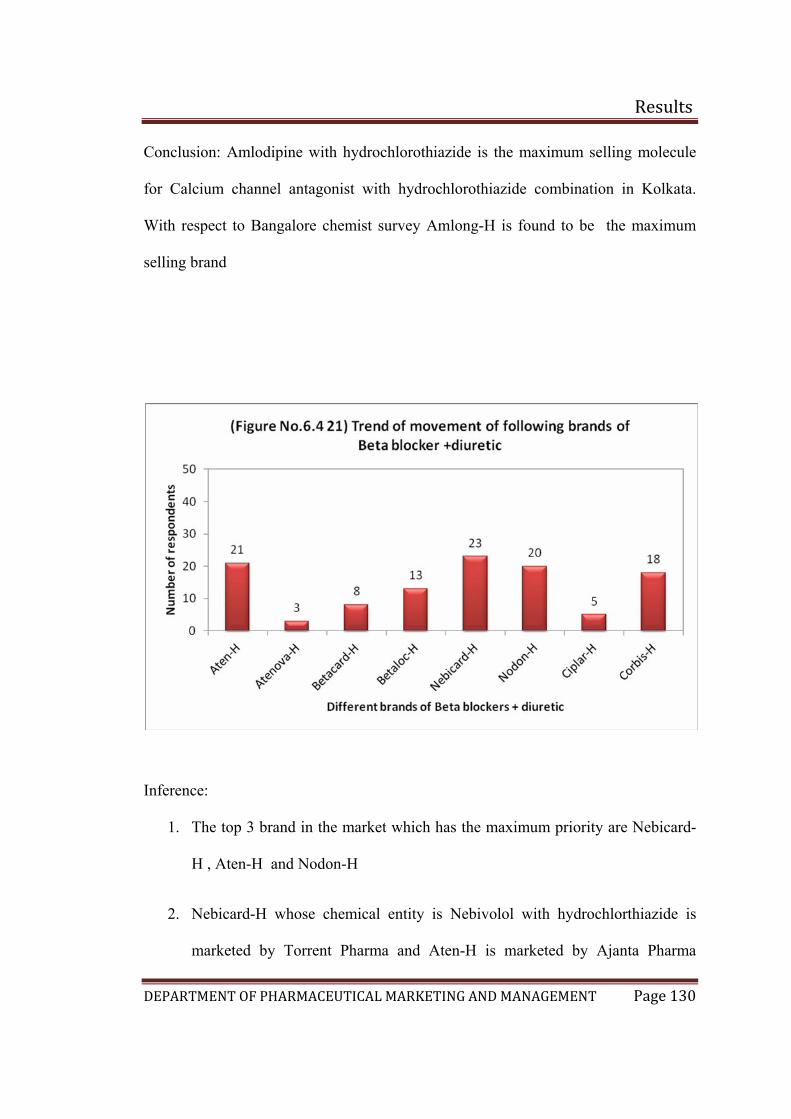

6.4.21 Trend of movement of the following brands of Beta blocker + Diuretic 130

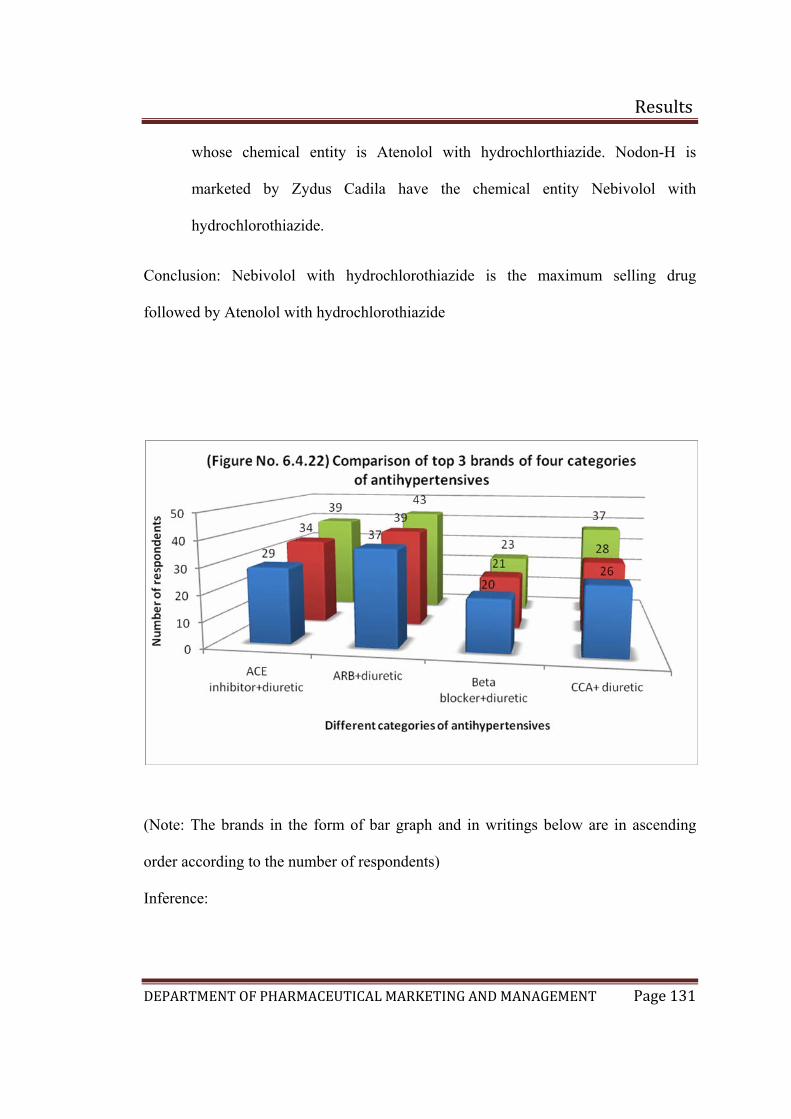

6.4.22 Comparison of 3 brands of four categories of antihypertensive combinations 131

6.4.23 Comparison between top 4 brands of ACE inhibitor and its combination and ARB and its combination 132

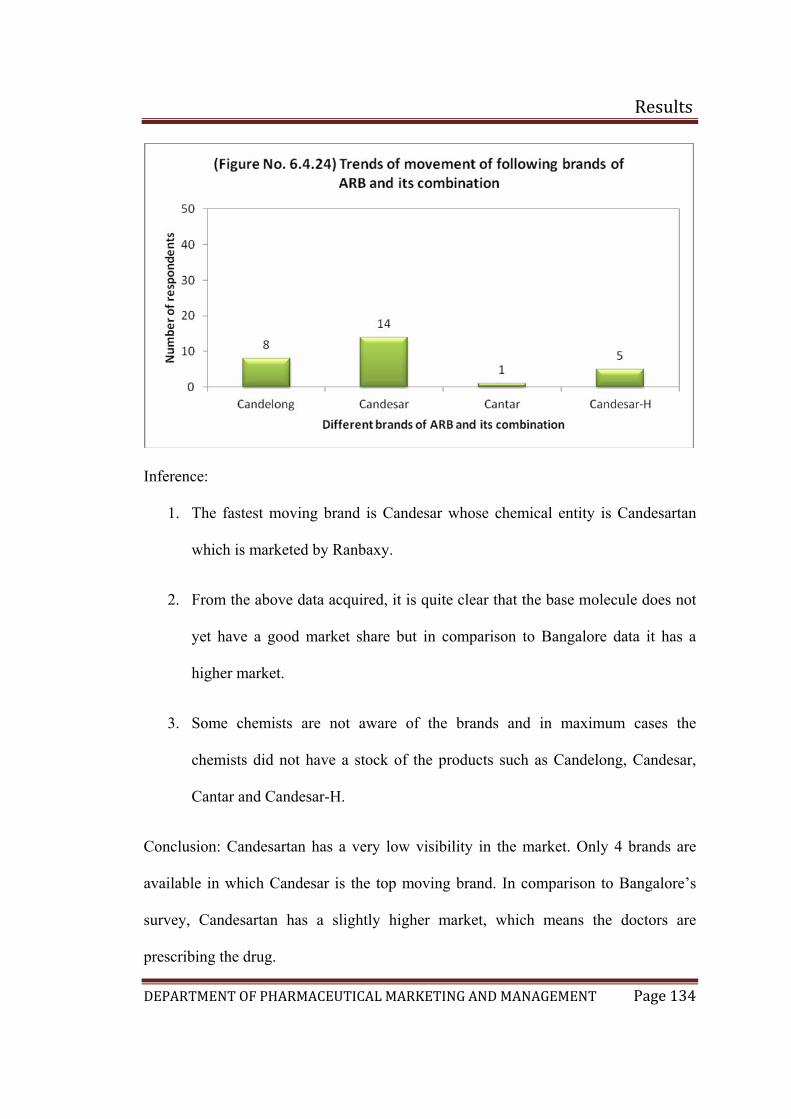

6.4.24 Trend of movement of the following brands of Candesartan and its combination 133

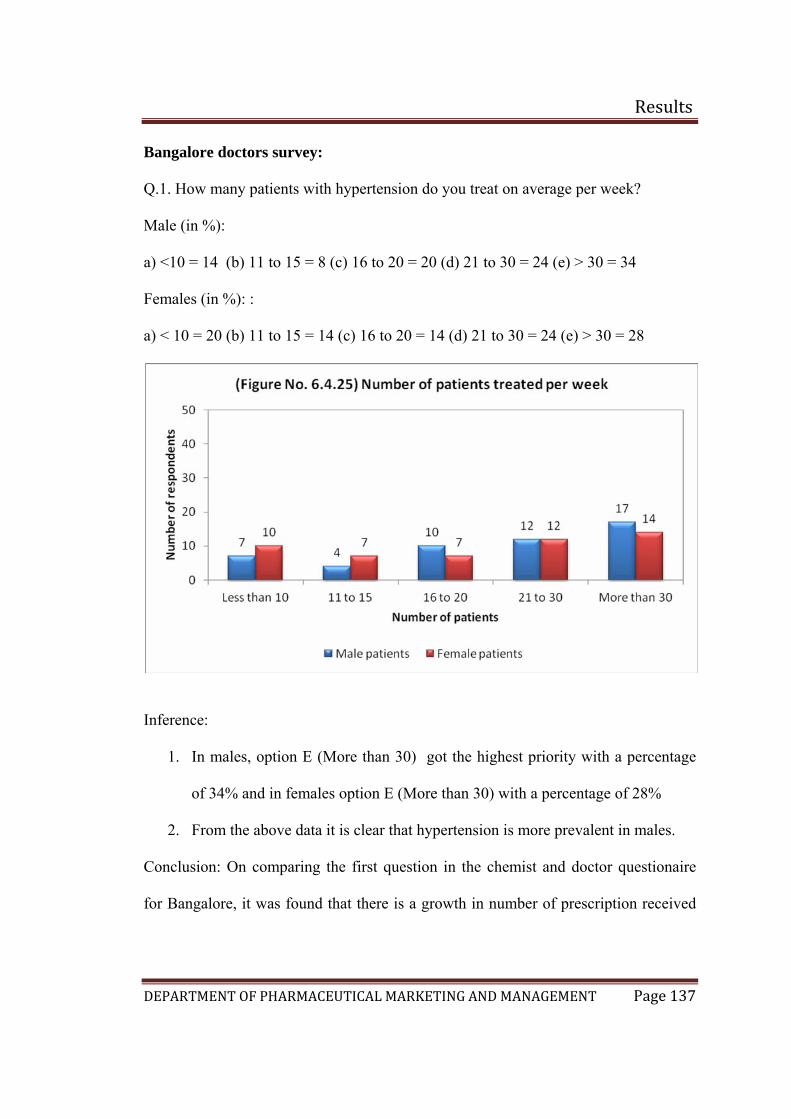

6.4.25 Number of patients treated per week in Bangalore 135

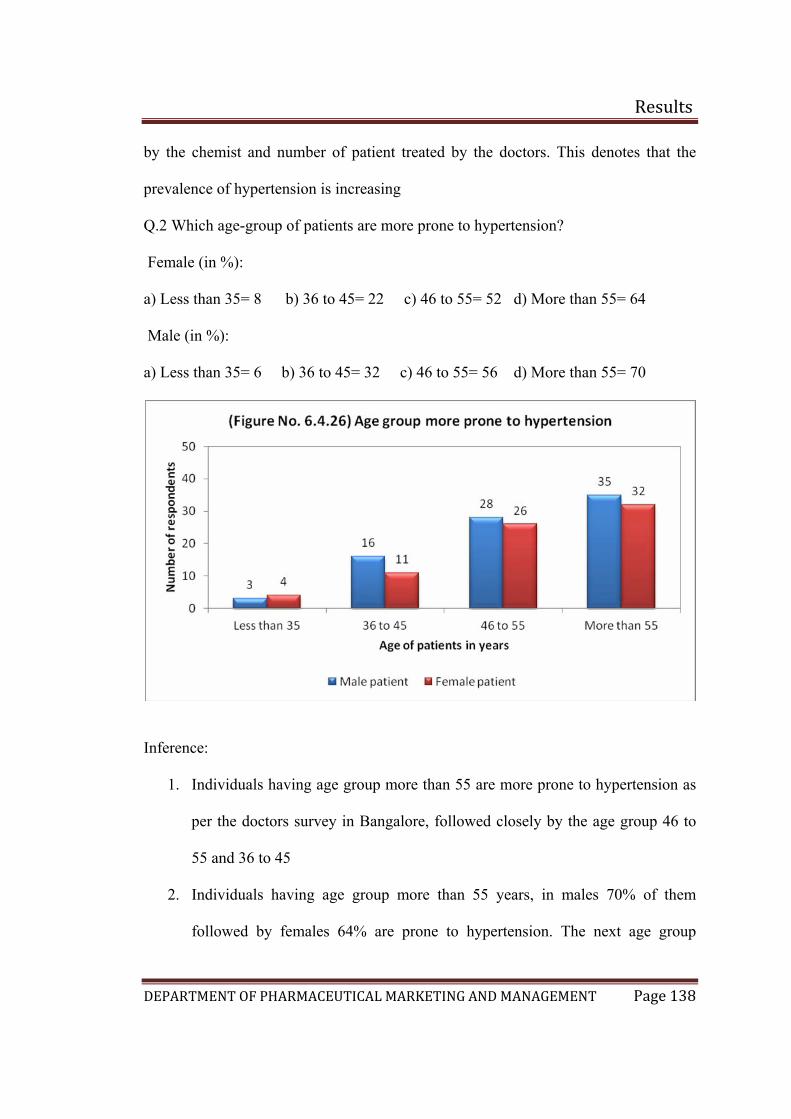

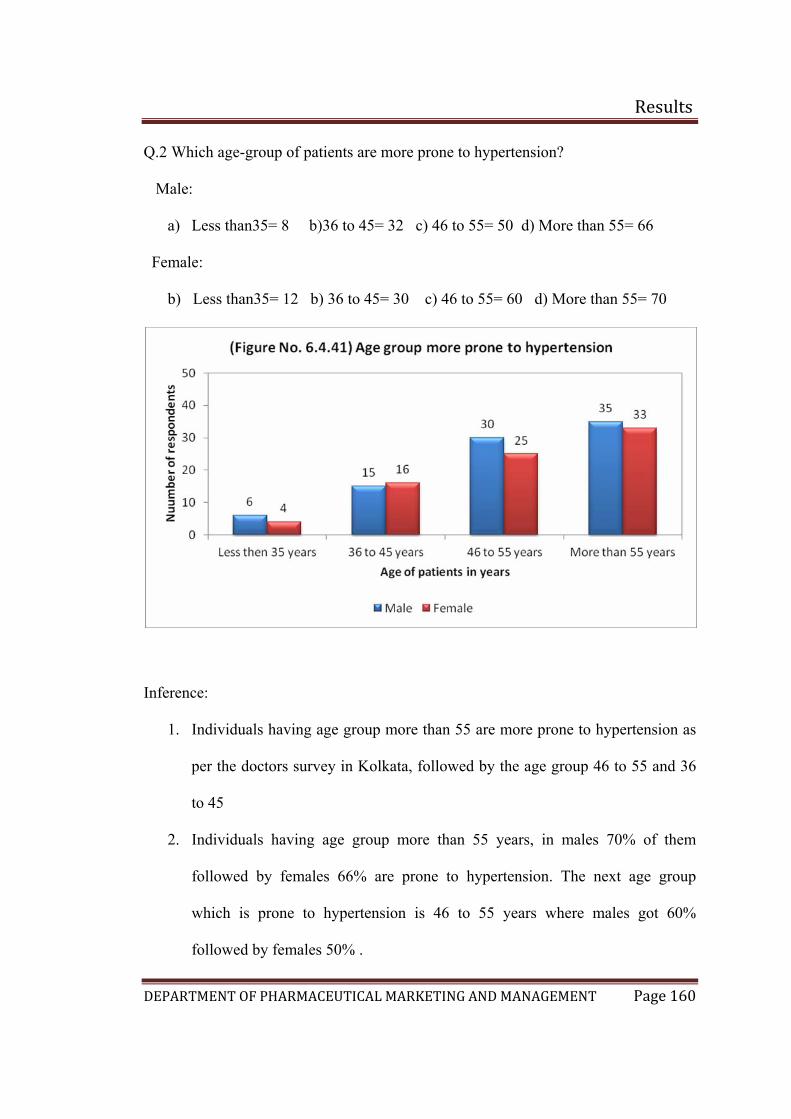

6.4.26 Age-group more prone to hypertension 136

6.4.27 Choice of drugs preferred by doctors to corresponding age group 138

6.4.28 Trend of movement of the following brands of ACE inhibitors 141

6.4.29 Trend of movement of the following brands of ARBs 143

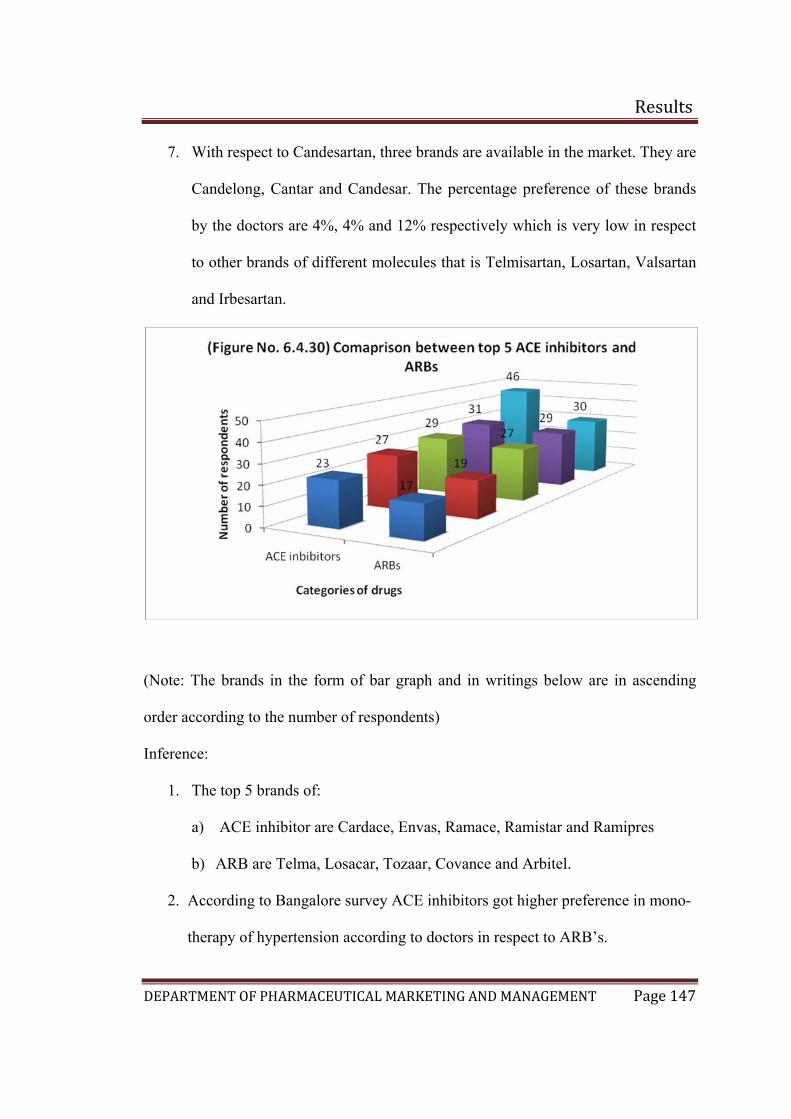

6.4.30 Comparison between top 5 brands of ACE inhibitor and ARB 145

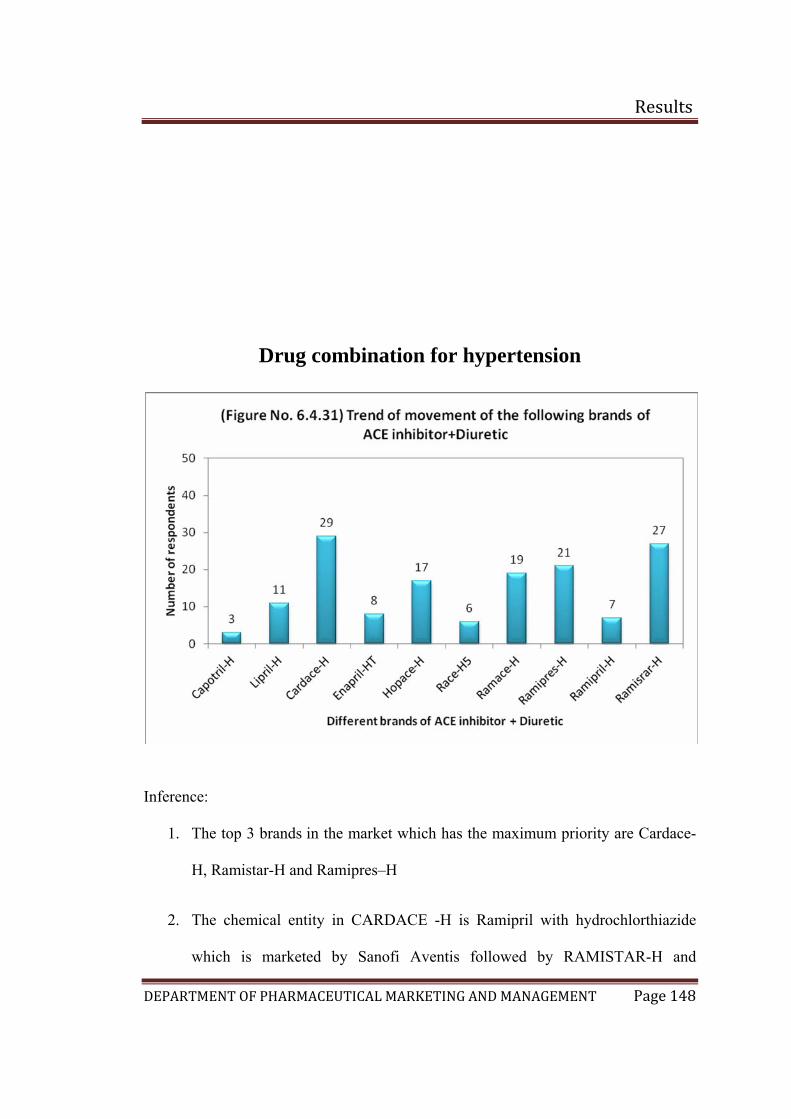

6.4.31 Trend of movement of the following brands of ACE inhibitors + Diuretic 146

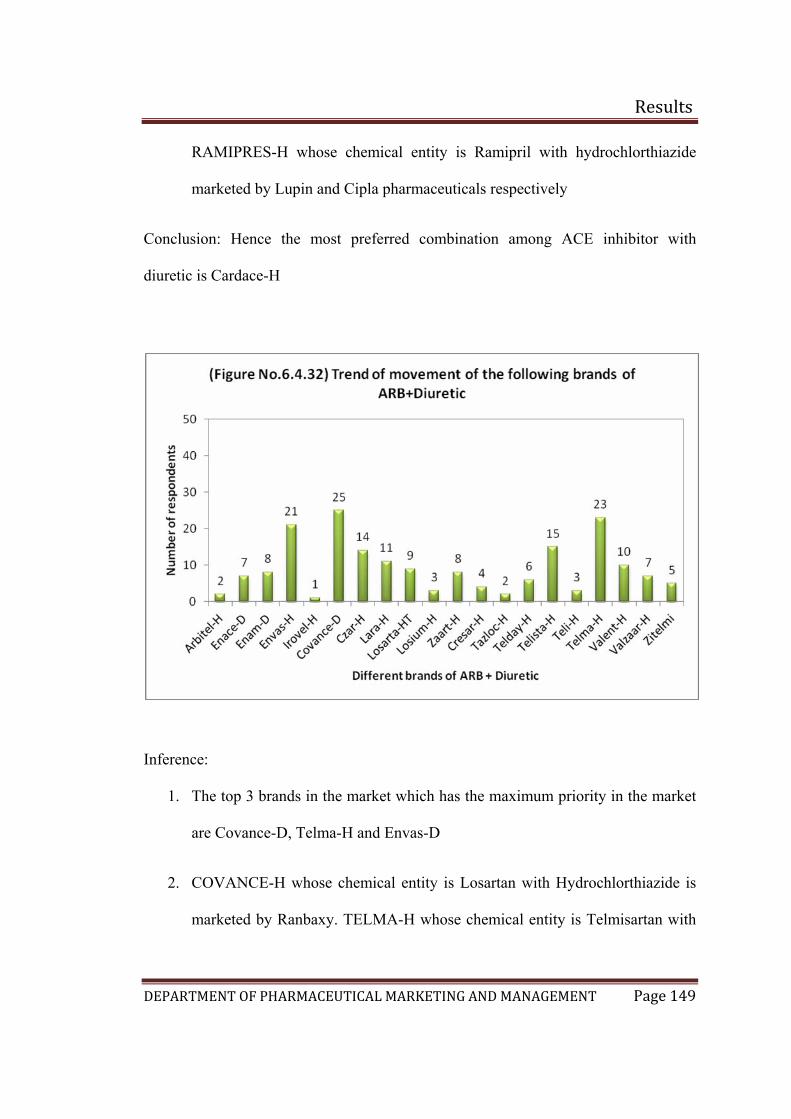

6.4.32 Trend of movement of the following brands of ARB + Diuretic 147

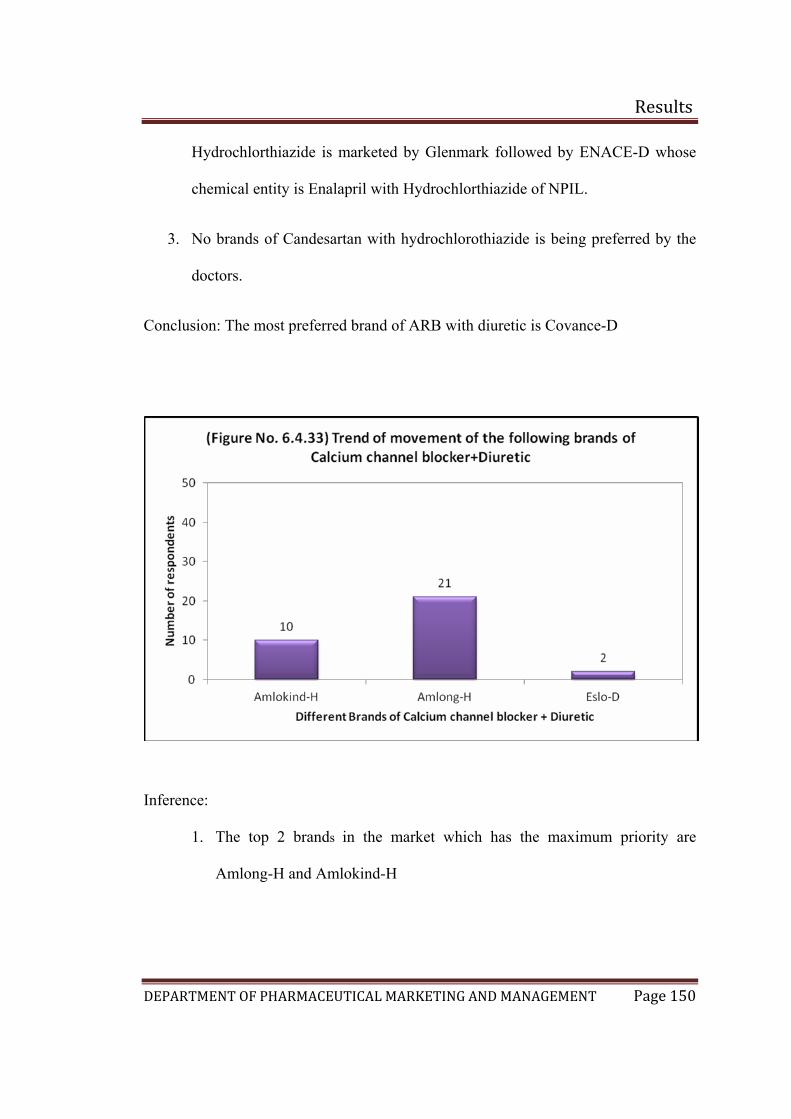

6.4.33 Trend of movement of the following brands of Calcium channel antagonist + Diuretic 148

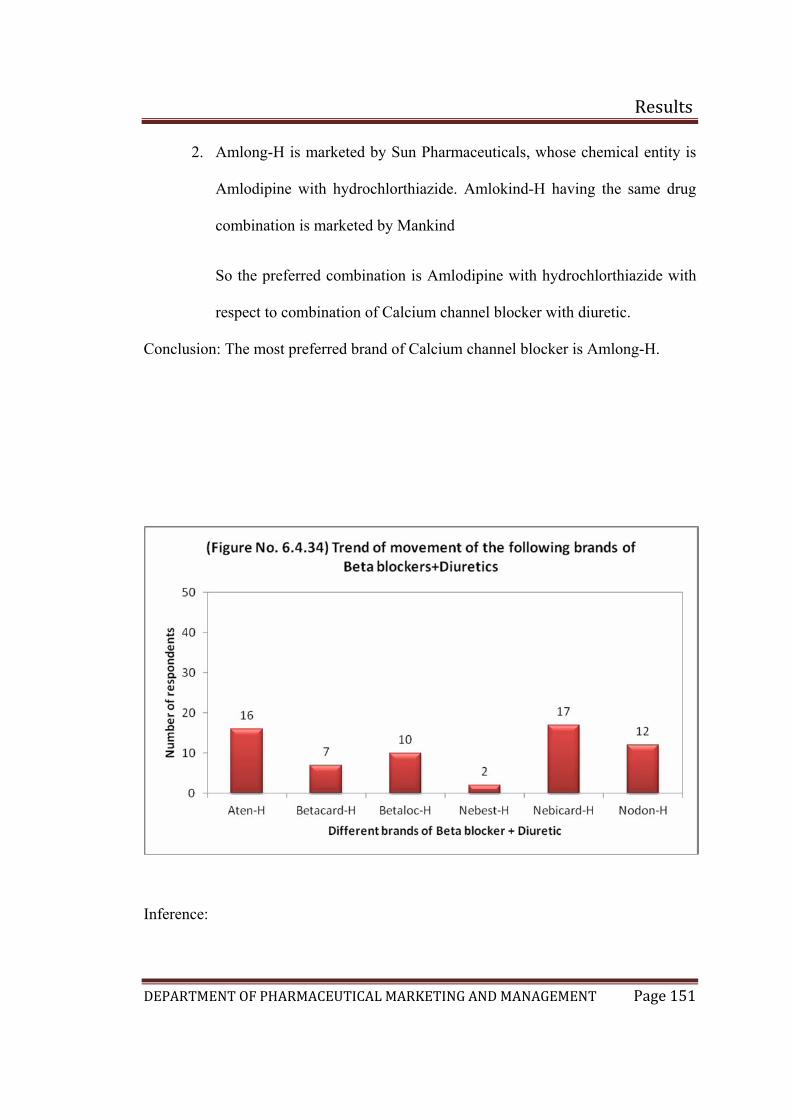

6.4.34 Trend of movement of the following brands of Beta blocker + Diuretic 149

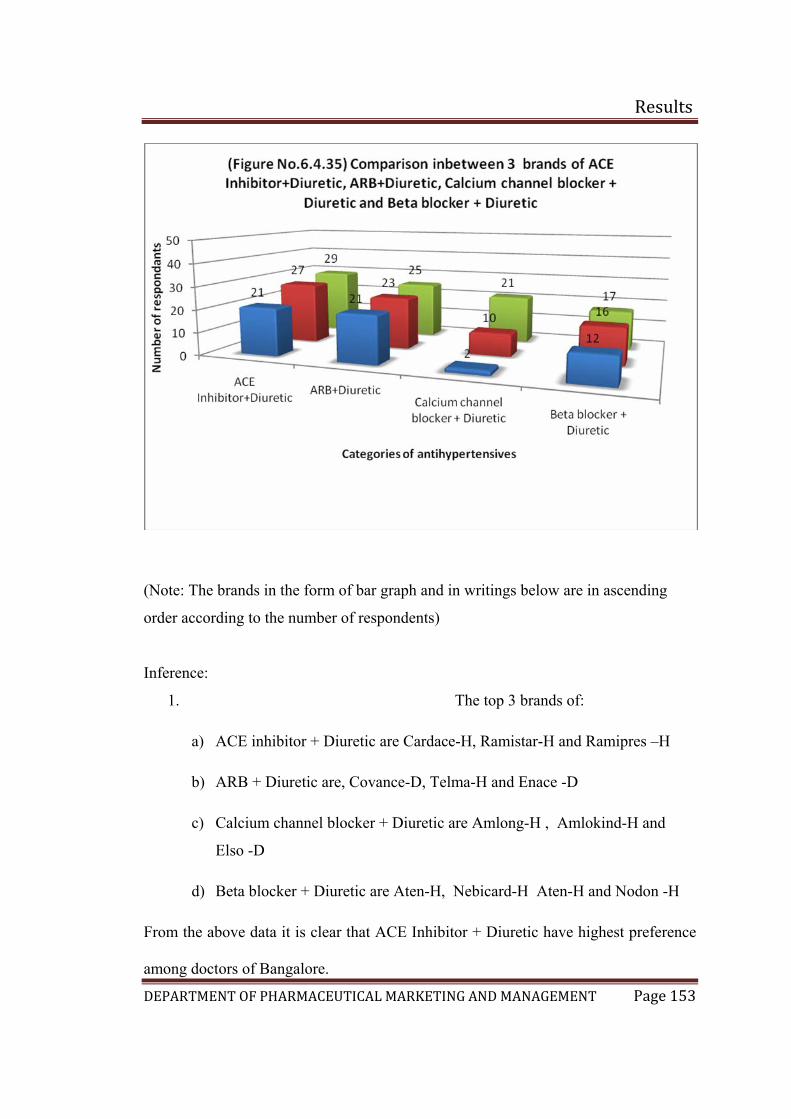

6.4.35

Comparison between top 3 brands of ACE inhibitors + Diuretic ARB + Diuretic, Calcium channel antagonist + Diuretic and Beta blocker + Diuretic

150

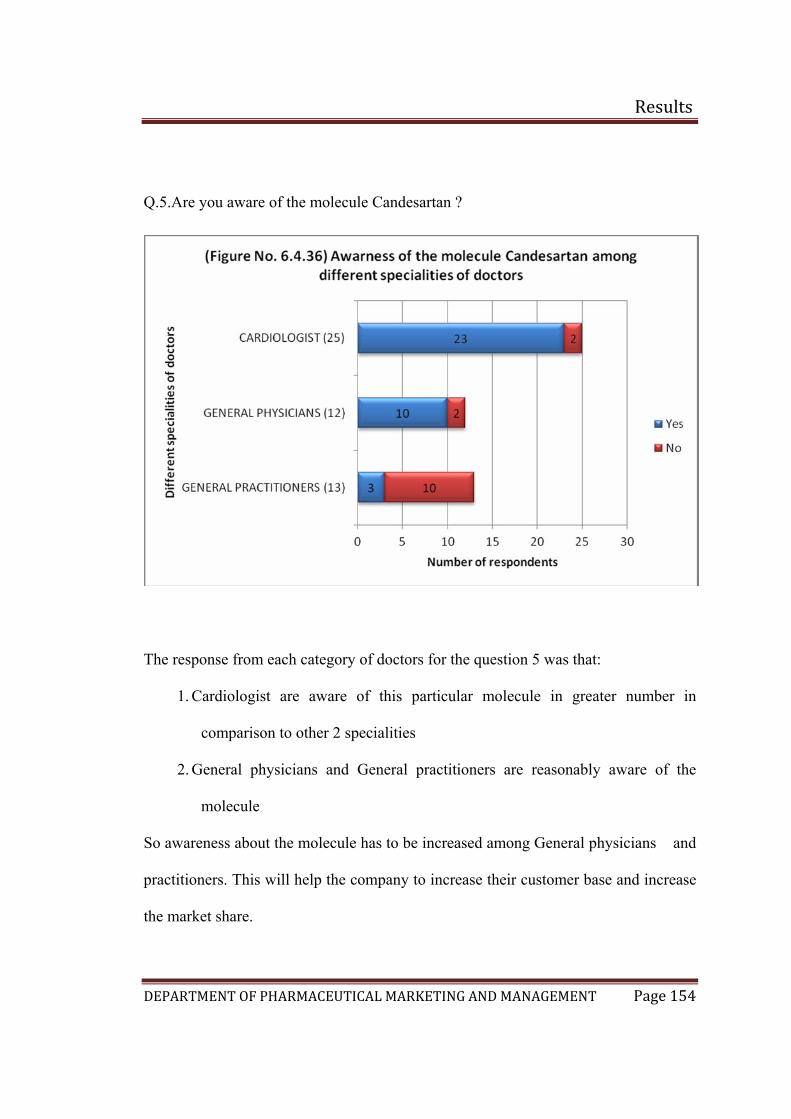

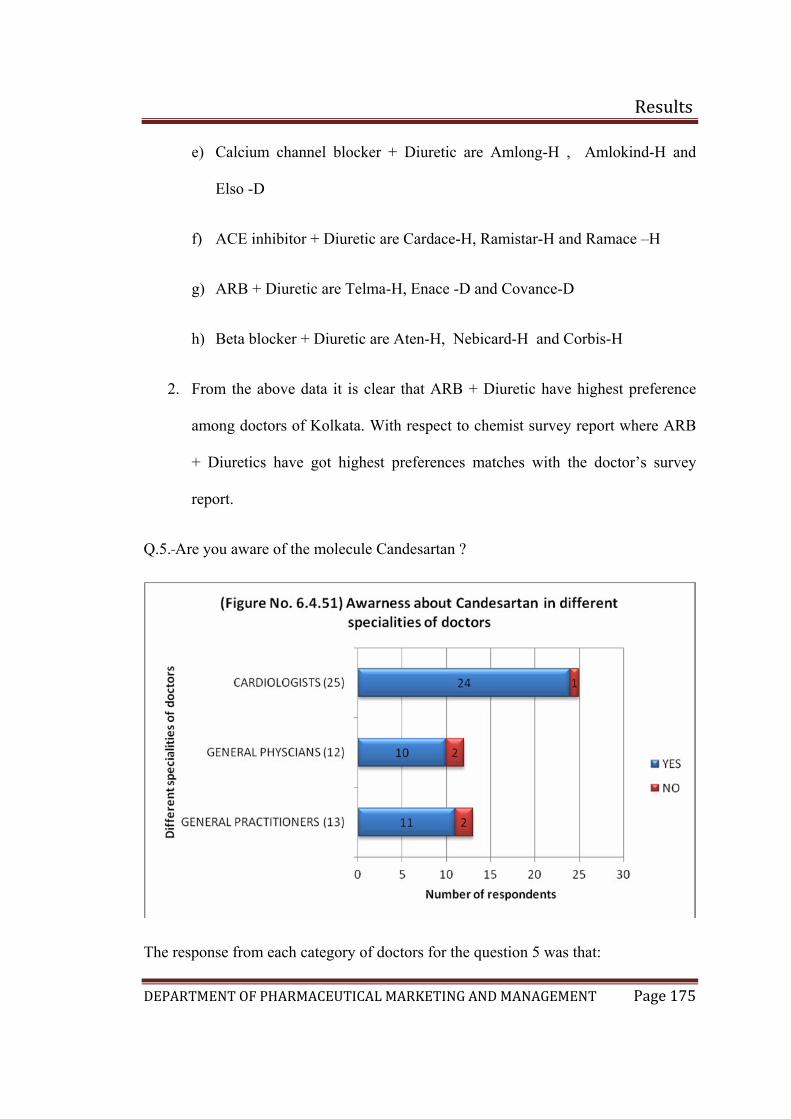

6.4.36 Awareness of the molecule Candesartan among different specialities of doctors 151

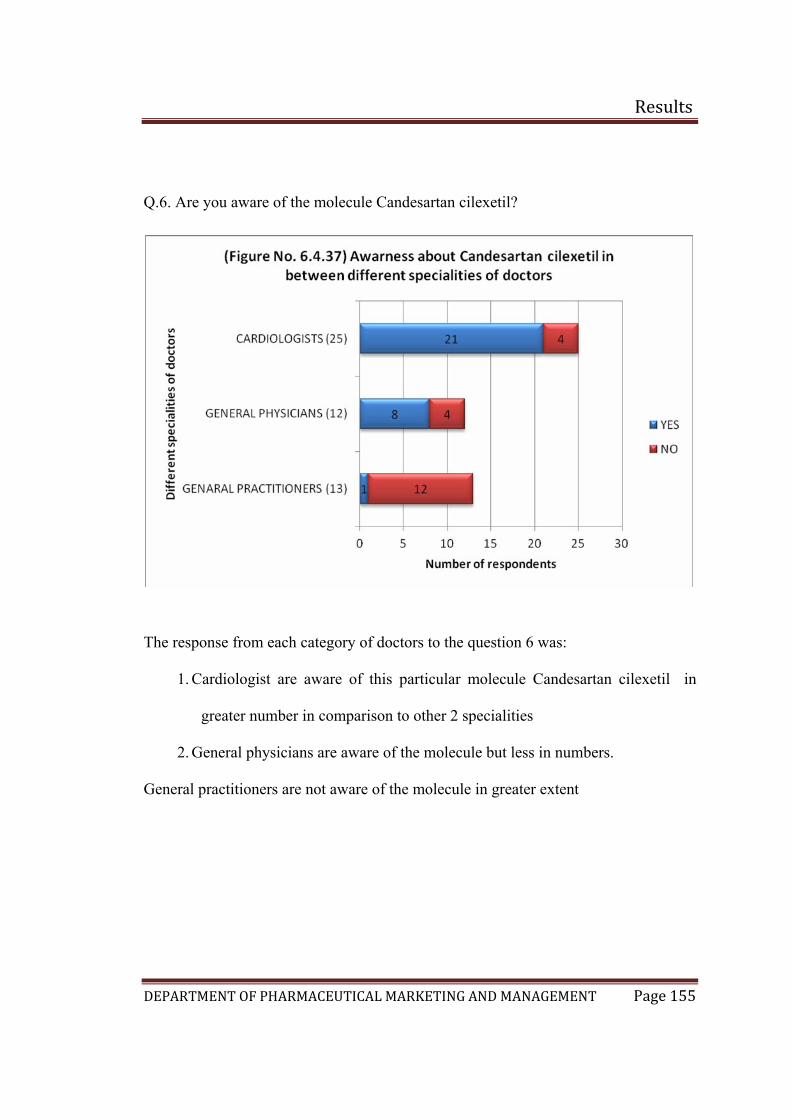

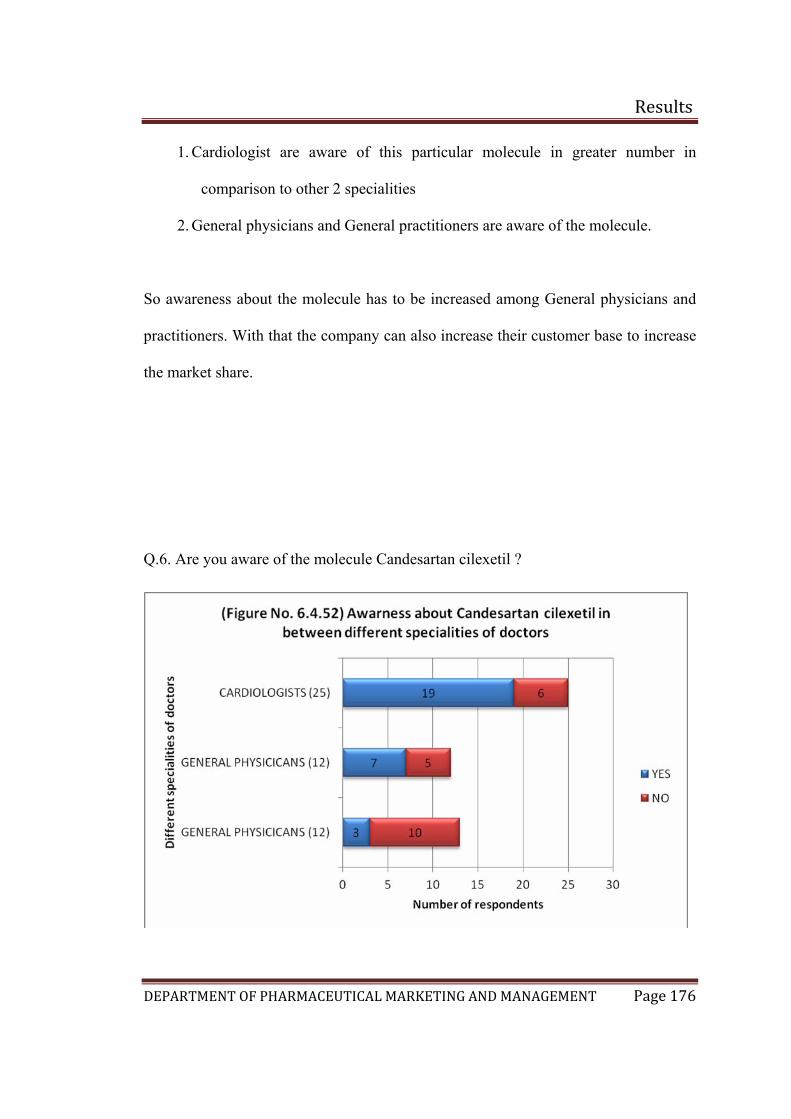

6.4.37 Awareness of the molecule Candesartan cilexetil among different specialities of doctors 152

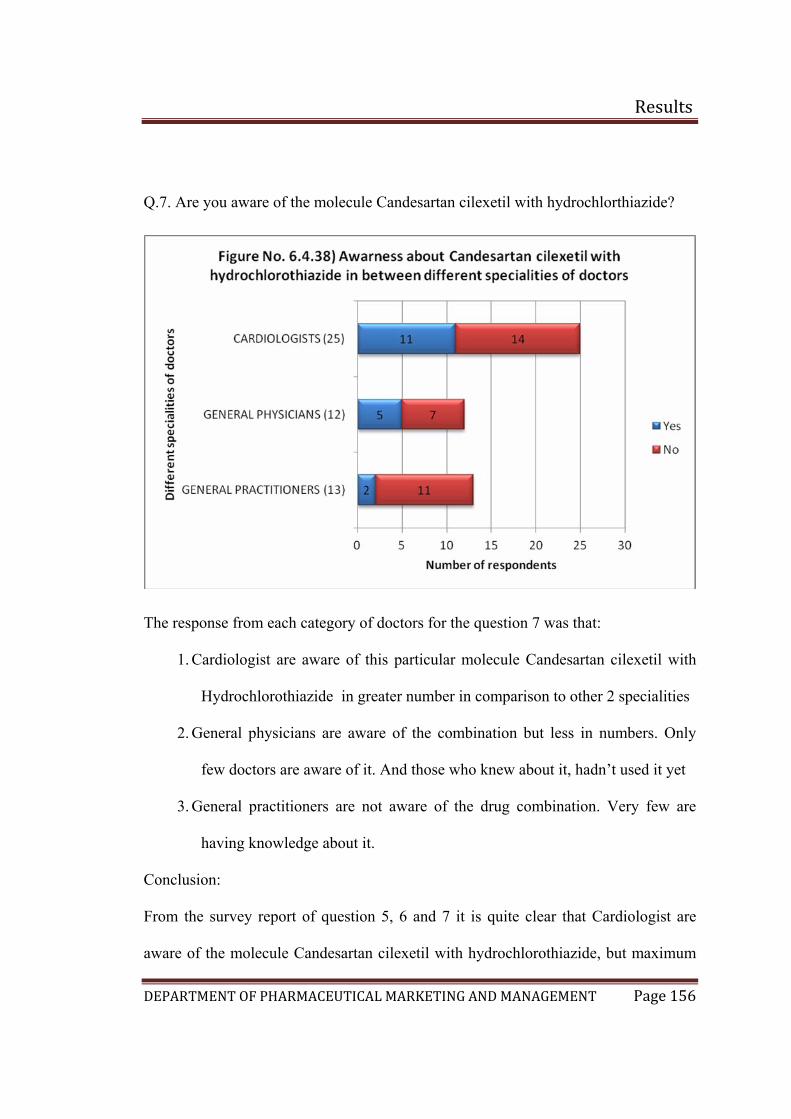

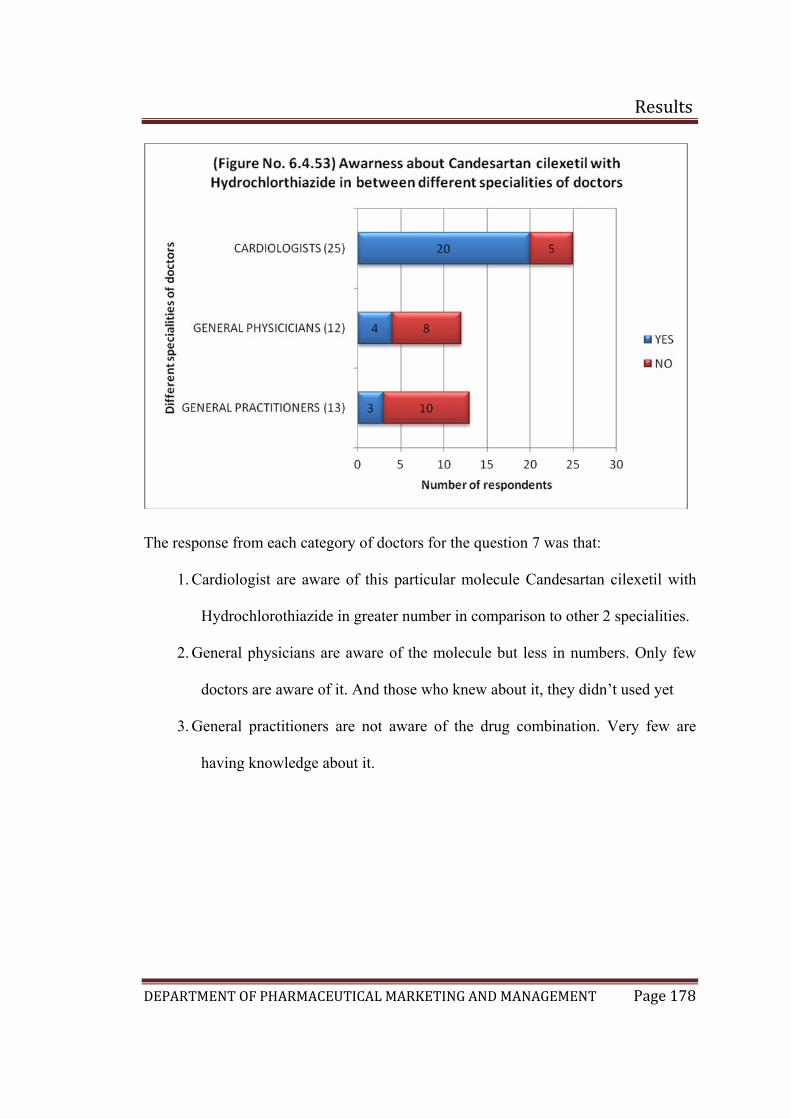

6.4.38 Awareness of the molecule Candesartan cilexetil with hydrochlorothiazide among different specialities of doctors 153

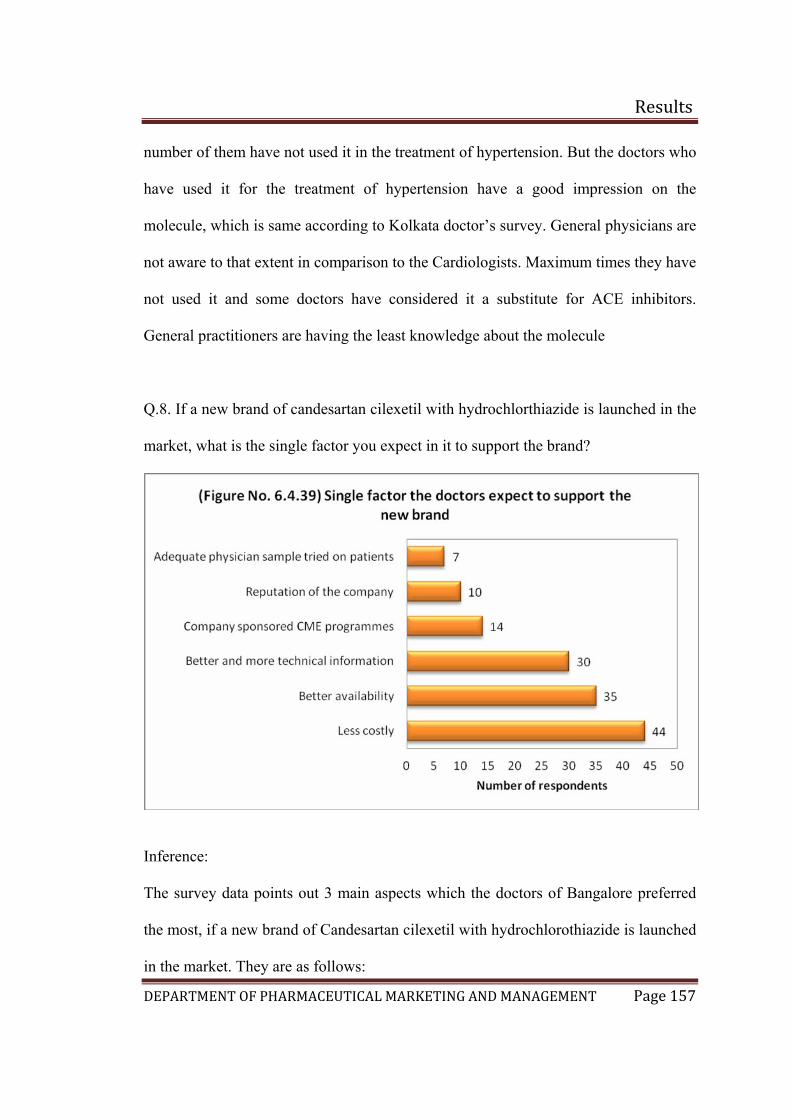

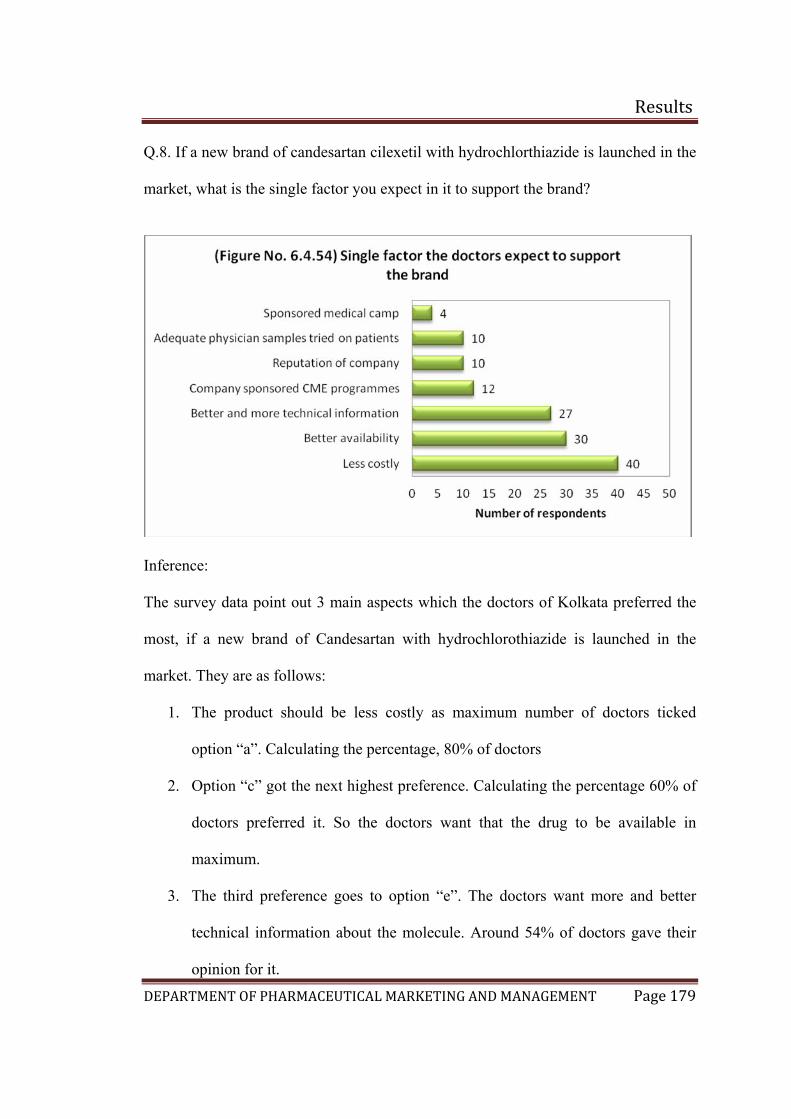

6.4.39 Single factor the doctors expect to support the brand 154

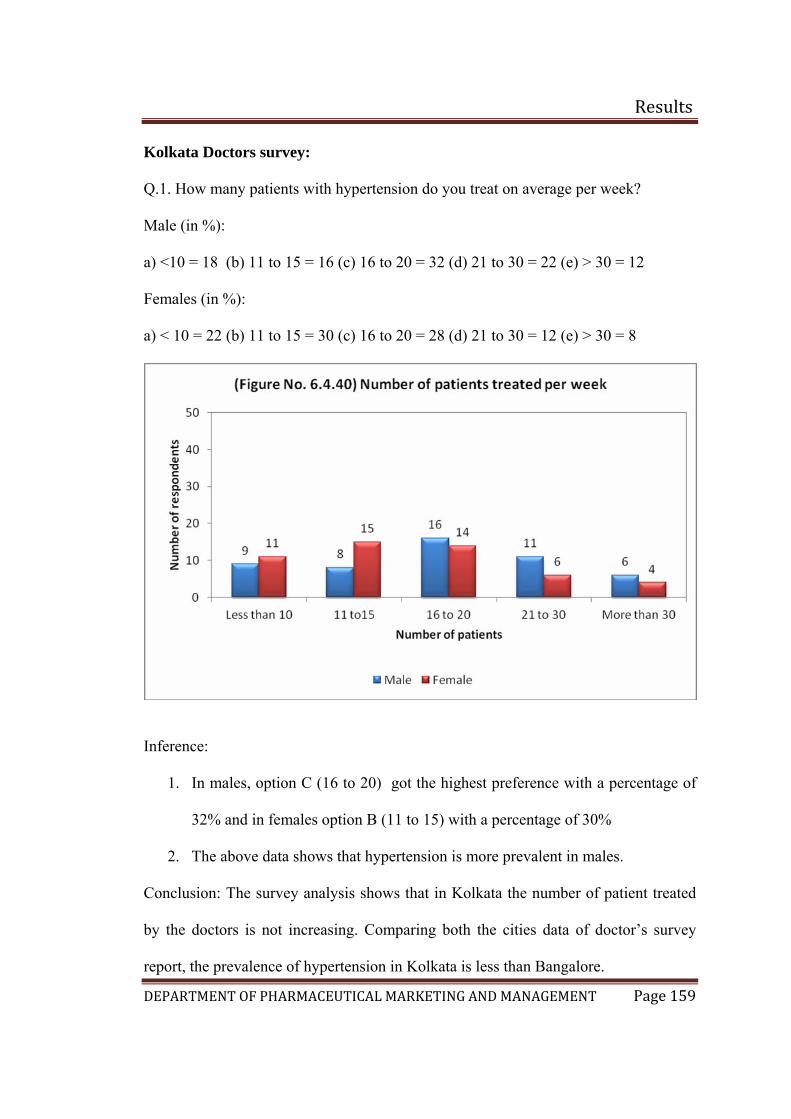

6.4.40 Number of patients treated per week in Kolkata 156

6.4.41 Age-group more prone to hypertension 157

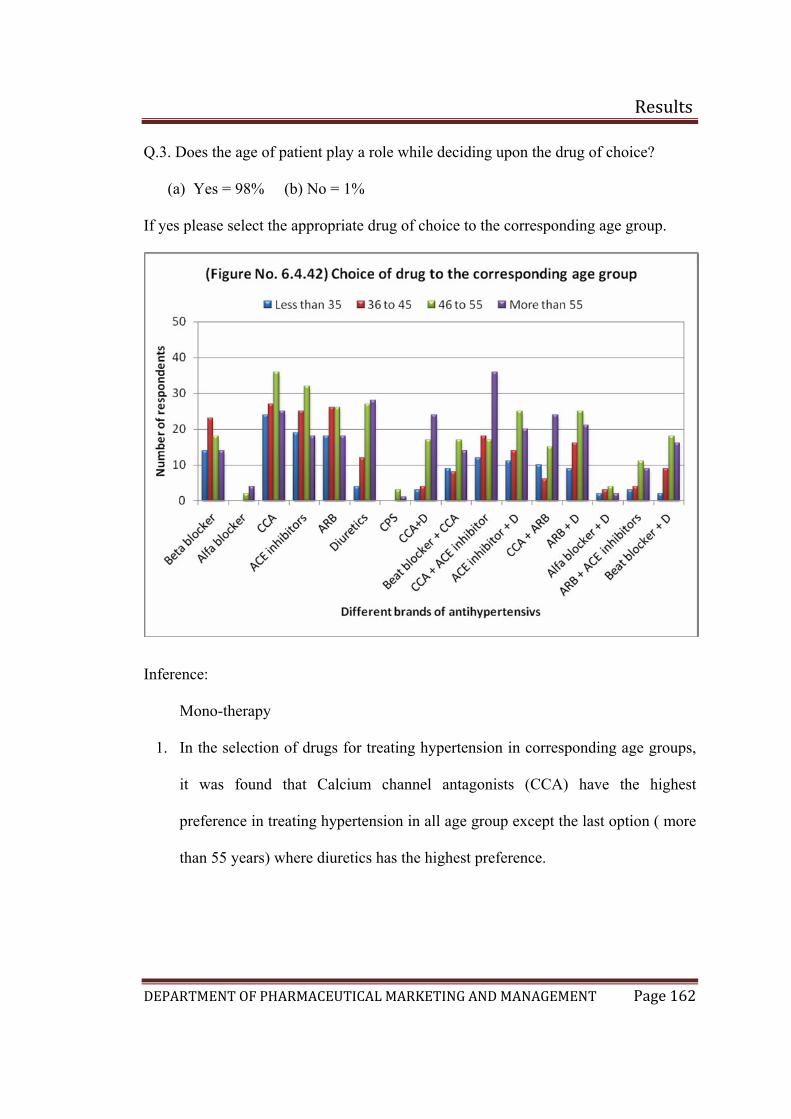

6.4.42 Choice of drugs preferred by doctors to corresponding age group 158

6.4.43 Trend of movement of the following brands of ACE inhibitors 161

6.4.44 Trend of movement of the following brands of ARBs 163

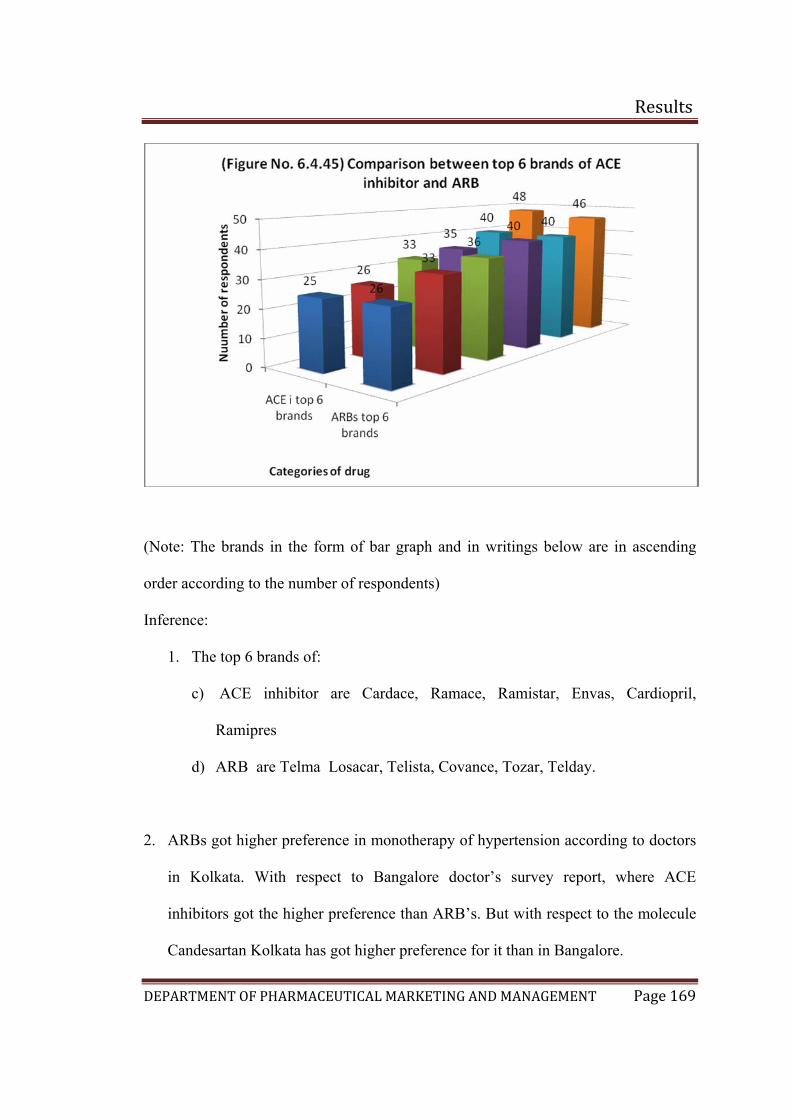

6.4.45 Comparison between top 6 brands of ACE inhibitor and ARB 165

6.4.46 Trend of movement of the following brands of ACE inhibitors + Diuretic 166

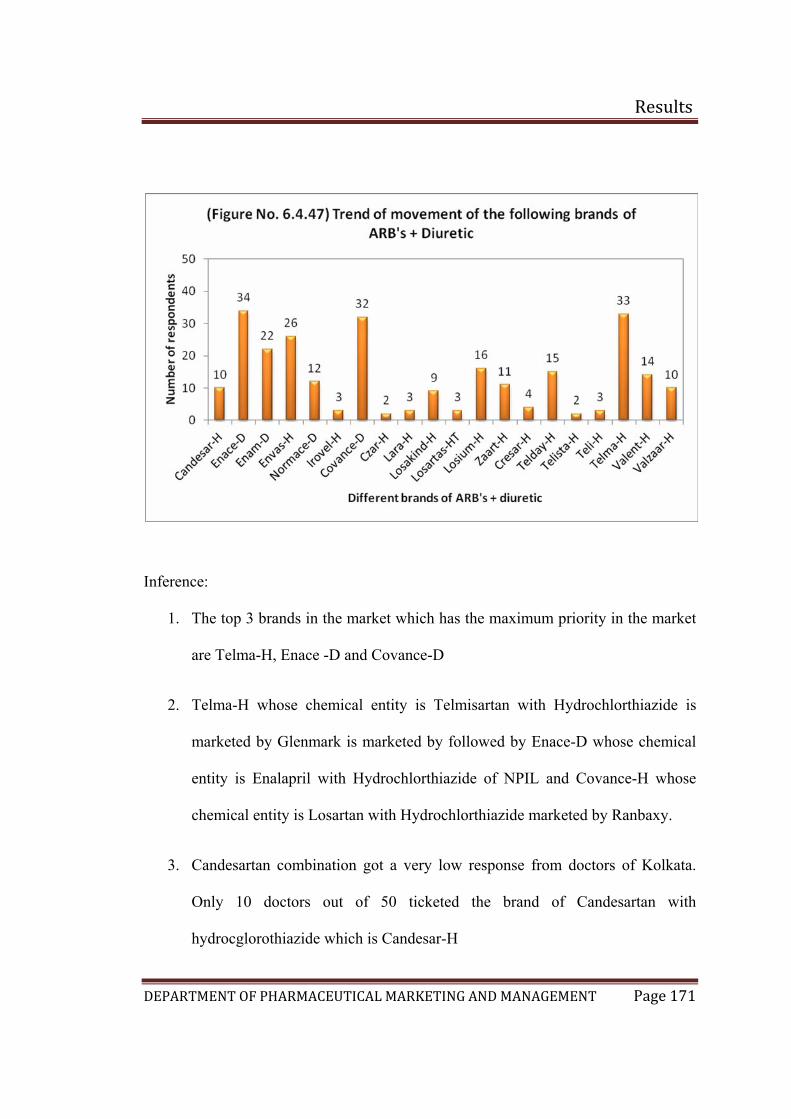

6.4.47 Trend of movement of the following brands of ARB + Diuretic 167

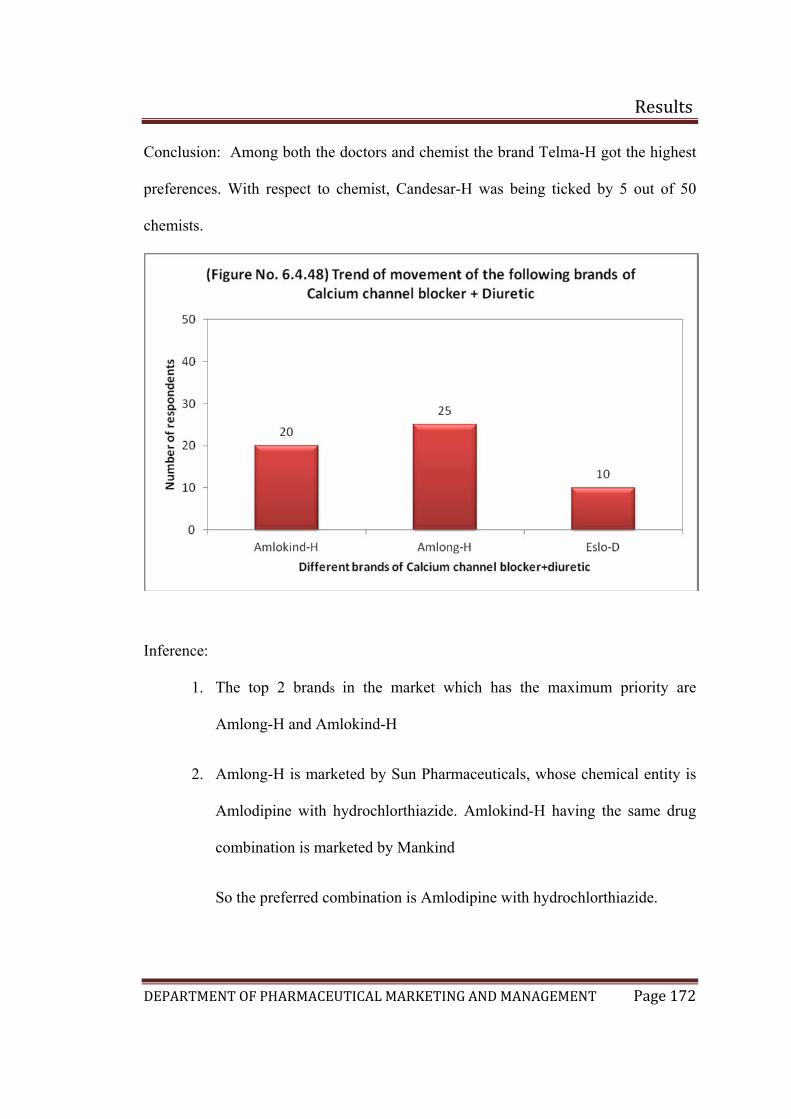

6.4.48 Trend of movement of the following brands of Calcium channel antagonist + Diuretic 168

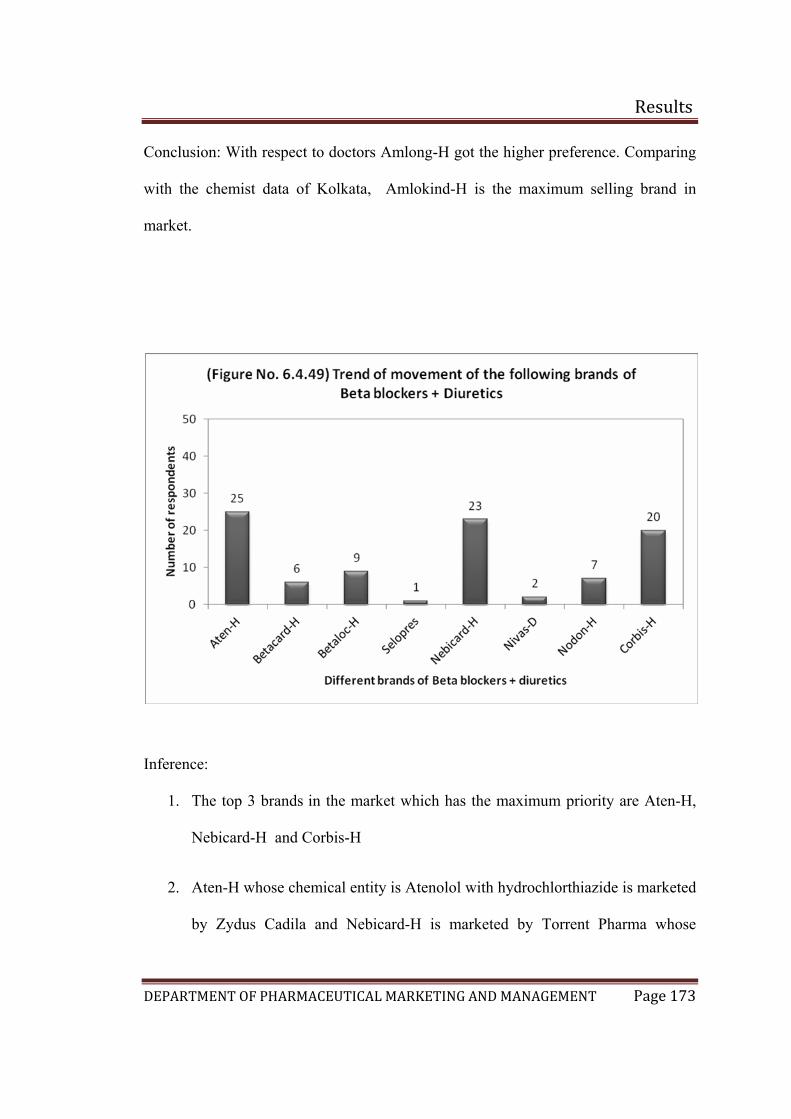

6.4.49 Trend of movement of the following brands of Beta blocker + Diuretic 169

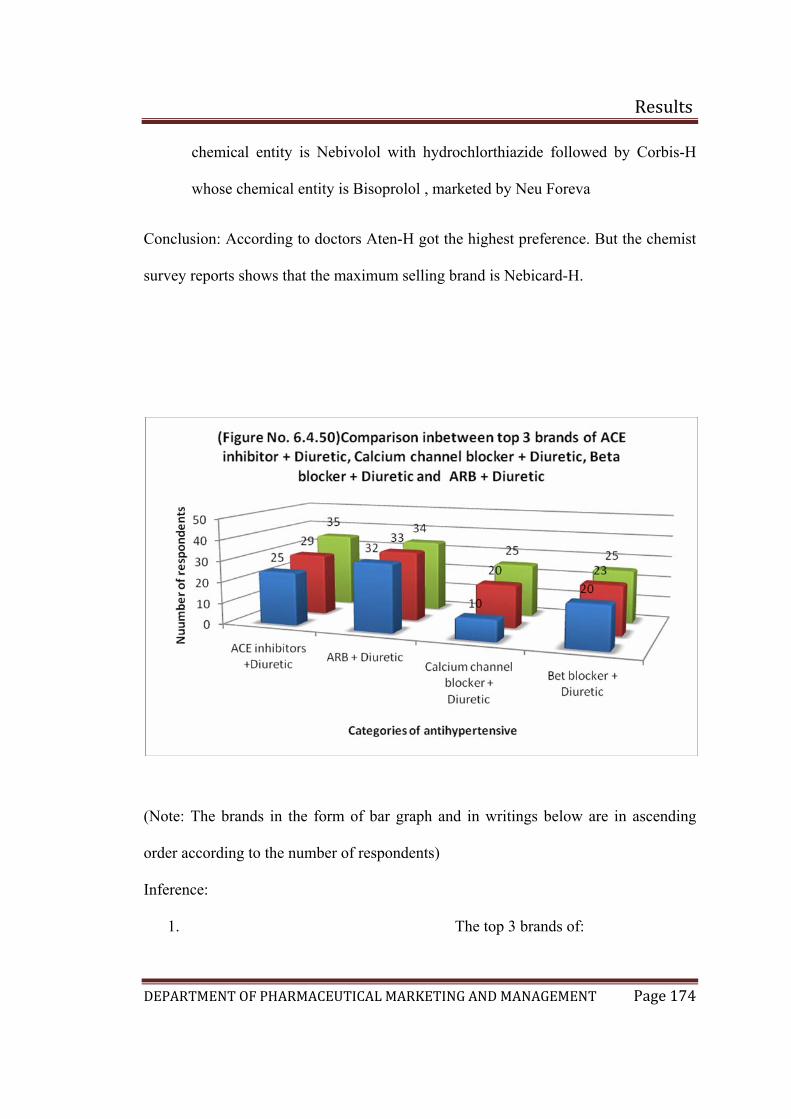

6.4.50 Comparison between top 3 brands of ACE inhibitors + Diuretic ARB + Diuretic, Calcium channel antagonist + Diuretic and Beta blocker + Diuretic

170

6.4.51 Awareness of the molecule Candesartan among different specialities of doctors 171

6.4.52 Awareness of the molecule Candesartan cilexetil among different specialities of doctors 172

6.4.53 Awareness of the molecule Candesartan cilexetil with hydrochlorothiazide among different specialities of doctors 173

6.4.54 Single factor the doctors expect to support the brand 174

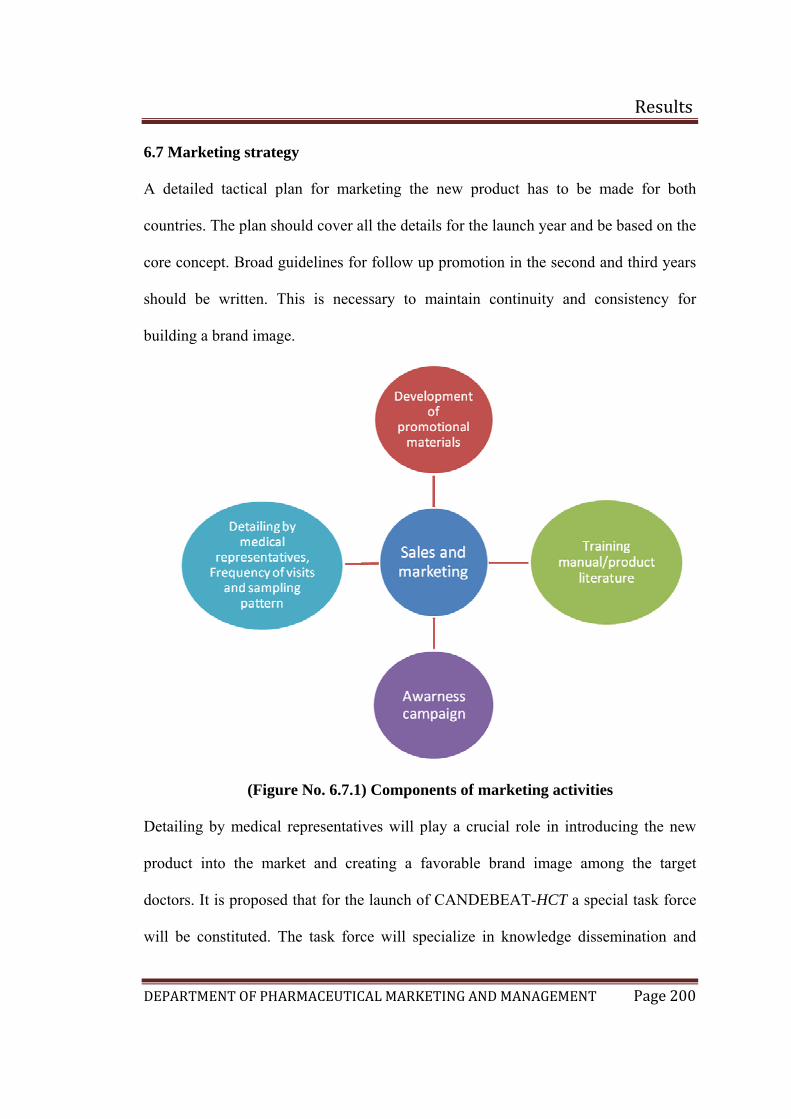

6.7.1 Components of marketing activities 190

xv

Introduction

DEPARTMENT OF PHARMAEUTICAL MARKETING AND MANAGEMENT Page 1

1. Introduction

Emerging from a highly protected economy and an insulated business environment,

many companies in India have come a long way in their quest to become global

players. Indian companies have started to venture into the global business arena by

acquisition, joint venturing and direct investment. Although the opportunities for

companies to enter and compete in foreign market are significant, the risks can also

be high.(1)

Among these companies, pharmaceutical organizations in India are also

competing in the global market. There are several factors which are responsible for

drawing more and more companies into the international arena:

• The company discovers that some foreign markets present higher profit

opportunities than the domestic market.

• The company needs a large customer base to achieve economies of scale

• The company wants to reduce its dependence on any one market

• Global firms offering better products can attack the company’s domestic

market.

• The company might want to counterattack these competitors in their home

markets.(1)

Introduction

DEPARTMENT OF PHARMAEUTICAL MARKETING AND MANAG

The Chartered Institute of Marketing Defines marketing as the “Management

process responsible for identifying, anticipating and satisfying customer

requirements profitably”. Thus marketing involves: n

Focusing on the needs and wants of customers

Identifying the best method of satisfying those needs a

Orienting the company towards the process of providin

Meeting organizational objectives(2)

Achieving product success is difficult. Projects like these

development for a number of reasons. Sometimes available

meet desired performance specifications or a desired price p

firm’s strategy changes, rendering the product on longer inte

beats the firm to the market or sometimes the development te

marketing or management in commercializing the product.

either strategic or development process factors or some com

most important aspects to manage effectively in the process

stages and the proficiencies of both the technological and ma

within them.( 3)

The key difference between domestic marketing and marke

scale is the multi-dimensionality and complexity of the many

a company may operate in.(4)

Introductio

EMENT Page 2

nd wants

g that satisfaction

are abandoned during

technology is unable to

oint. At other times, a

resting, or a competitor

am is unable to interest

Product can fail due to

bination of two. So the

are the predevelopment

rketing-related activities

ting on an international

foreign country markets

Introduction

DEPARTMENT OF PHARMAEUTICAL MARKETING AND MANAGEMENT Page 3

Developing a new product and launching in the market is time and resource

consuming, as great care must be taken to ensure the best decisions are made before

the product reaches channel members and final consumers.

Therefore to launch a new product in the domestic and international market, some

important aspects such as analysis of targeted country, risks, cultural aspects,

competitors, company financial status should be extensively analyzed. The proposed

study involves the consideration of all the relevant aspects for the launch of a new

brand of a combination product that is Candesartan cilexetil with Hydrochlorothiazide

in domestic and international markets. It involves the development of tactics, plans

and strategies which helps to introduce the proposed new brand successfully.

Candesartan cilexetil with hydrochlorothiazide belonging to the therapeutic category

antihypertensives will be introduced in the market by formulating an effective launch

strategy.

• This project proposes to assist the company to develop a preliminary strategy

plan for introducing the new product into the market. The plan consists of

three part, such as

• The first part describes the target market’s size, structure and behavior; the

planned product positioning; and the sales, market share and profit goals

sought in the first few years

• The second part outlines the planned price, distribution strategy, and

marketing budget for the first year

Introduction

DEPARTMENT OF PHARMAEUTICAL MARKETING AND MANAGEMENT Page 4

The third part of the marketing-strategy plan describes the long-run sales and profit

goals and marketing mix strategy over time.(1)

When launching new products in today’s competitive market, it is critical to develop

innovative launch strategies that differentiate a company’s new brand and position it

for maximum growth. Without aggressive tactics, a company risks in missing a

window of opportunity for achieving optimal results from the launch. The

development, evaluation and implementation of launch strategies are essential for a

successful product launch.

Thereby a launch strategy for a product includes the development of strategy that

is externally oriented, proactive, timely, implementable and appropriate for a long

time horizon.(5)

Introduction

DEPARTMENT OF PHARMAEUTICAL MARKETING AND MANAGEMENT Page 5

Objectives

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 8

3. OBJECTIVES

The study covers the following objectives:

1. To study the epidemiology of hypertension

2. Study of the anti-hypertensive drugs market with special reference to

Candesartan cilexetil with Hydrochlorthiazide

3. To find out the prescription trends for the treatment of Hypertension.

4. Preparation of the launch strategy for a new brand of Candesartan cilexetil

with Hydrochlorthiazide

Need for study

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 5

2. NEED FOR STUDY

The global pharmaceutical market was valued at US$ 712 billion in 2007. Major

markets can be broadly classified into mature markets and emerging markets

depending upon the nature of the market growth. The market growth accelerates in the

seven pharma emerging markets are China, Brazil, Mexico, South Korea, India,

Turkey and Russia. In these markets there is significantly greater access to both

generic and innovative medicines as primary care improves and becomes available in

rural areas. Ongoing economic growth in the developing world will continue to shift

the focus from infectious diseases to cardiovascular, diabetes and other chronic

illnesses.

From the source of IMS health audit 2007 world wide, Angiotensin-II antagonists

ranked 8th, amounting to a global sales of US$ 19.4 billion with a growth of 13.6%

within the top leading therapeutic segments.

The angiotensin II receptor blocker candesartan cilexetil and the diuretic

hydrochlorothiazide (HCT) is a combination introduced by Astrazeneca. It is used to

treat high blood pressure (hypertension) when one medicine (monotherapy) is not

sufficiently effective. The combination of two medicines that have different ways of

working (modes of action) and leads to a greater lowering of blood pressure in more

people than with either medicine used alone. The following studies supports the

greater efficacy and cost effectiveness of the product:

The clinical studies carried out by the company proved that the drug reduces

blood pressure and proportion of patients with normalized BP was greater with

Candesartan-HCT 16/12.5 mg than with Losartan-HCT 50/12.5 mg.(6)

Need for study

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 6

Another study which was carried out to compare the antihypertensive effect

and tolerability of a once-daily combination of candesartan cilexetil, and the

diuretic hydrochlorothiazide (HCT), with a combination of lisinopril and HCT

in patients with primary hypertension. The results proved that the

combinations of candesartan cilexetil/HCT once daily, and lisinopril/HCT,

once daily, had similar antihypertensive efficacy in patients, but candesartan

cilexetil/HCT was significantly better tolerated than lisinopril/HCT.(7)

The use of candesartan cilexetil as part of antihypertensive therapy in elderly

patients with elevated blood pressure was deemed to be cost effective in a

Swedish analysis, primarily resulting from a reduced risk of nonfatal stroke.(8)

The antihypertensive efficacy and tolerability of combination therapy with

candesartan cilexetil, 16 mg plus hydrochlorothiazide (CC/HCT), 12.5 mg was

compared with that of amlodipine , in a multicentre, double-blind, randomised,

parallel-group study in patients with mild-to-moderate essential hypertension

inadequately controlled by monotherapy.. In conclusion, CC/HCTZ and

amlodipine were equally effective in reducing BP in hypertensive patients not

controlled by monotherapy, but CC/HCT was much better tolerated.(9)

From the above mentioned data it is quite clear that the molecule Candesartan

cilexetil with Hydrochlorthiazide is a potent drug having superiority over other drug

in the same and different categories of antihypertensives and also economical and

safe.

Now developing a competitively advantaged product requires: input from customers

on unmet needs, input from marketing as to what the competition is doing to address

Need for study

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 7

the need, input from manufacturing about what the firm can currently build to satisfy

the need, input from R&D about new ways of potentially addressing the need and

input from finance about costs. Which finally leads to successful new product

development fulfilling the requirements of profit, market share and customer

satisfaction.(4)

Candesartan cilexetil with hydrochlorothiazide belongs to the therapeutic category of

antihypertensives will be introduced in the market by formulating an effective launch

strategy in the domestic and Brazilian market.

The apparent reasons for selecting Brazilian and Indian market is due to their market

growth of 13.4% and 13% respectively which is higher in comparison to other major

pharmaceutical markets, such as North America, Europe and Japan according to IMS

health report. The driving force behind the growth is the rising consumption levels in

both the countries.

This project proposes to assist the company to develop a preliminary strategy plan for

introducing the new product into the market.

Review of literature

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 9

4. REVIEW OF LITERATURE

The Concept of Hypertension (10)

According to WHO, Hypertension is the state of body in which systolic BP is 150

mmHg or more & diastolic BP is 95 mmHg or more.

Hypertension can be classified either essential (primary) or secondary.

Secondary hypertension indicates that the high blood pressure is a result of (i.e.,

secondary to) another condition, such as kidney disease or tumors

(pheochromocytoma and paraganglioma). Persistent hypertension is one of the risk

factors for strokes, heart attacks, heart failure and arterial aneurysm, and is a leading

cause of chronic renal failure.

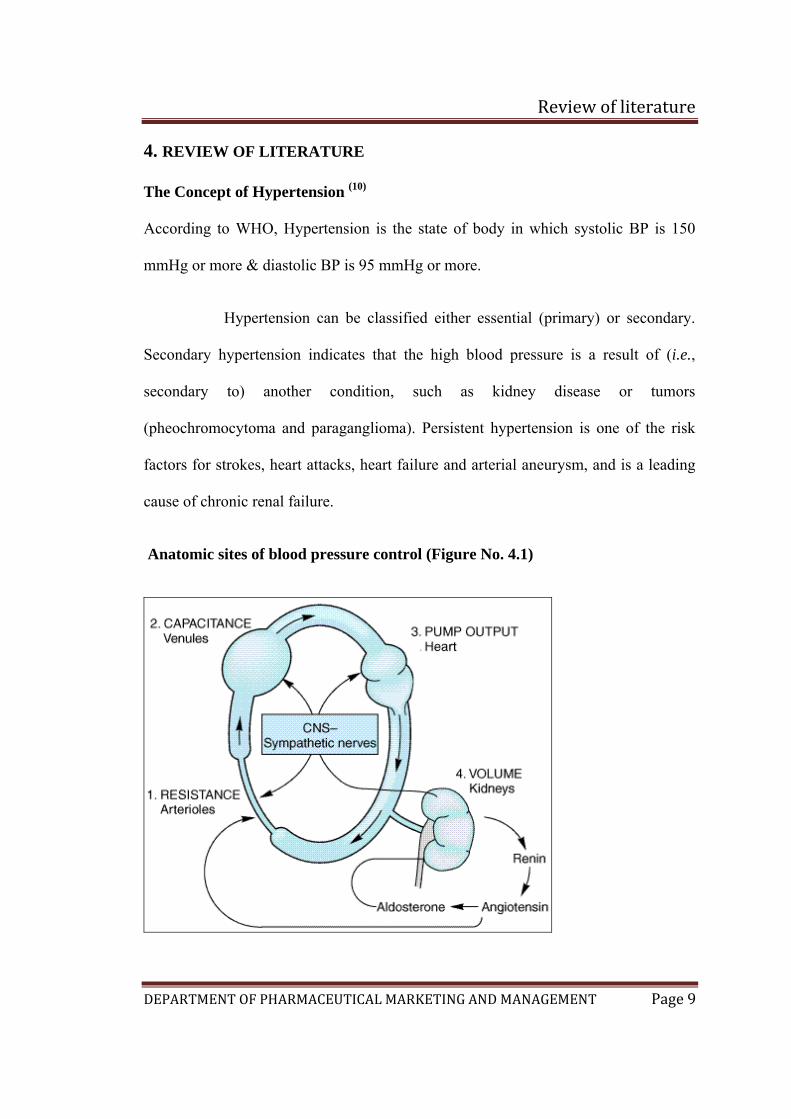

Anatomic sites of blood pressure control (Figure No. 4.1)

Review of literature

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 10

According to the hydraulic equation, arterial blood pressure (BP) is directly

proportionate to the product of the blood flow (cardiac output, CO) and the resistance

to passage of blood through precapillary arterioles (peripheral vascular resistance,

PVR): Physiologically, in both normal and hypertensive individuals, blood pressure is

maintained by moment-to-moment regulation of cardiac output and peripheral

vascular resistance, exerted at three anatomic sites (Figure 4.1): arterioles,

postcapillary venules (capacitance vessels), and heart. A fourth anatomic control site,

the kidney, contributes to maintenance of blood pressure by regulating the volume of

intravascular fluid. Baroreflexes, mediated by autonomic nerves, act in combination

with humoral mechanisms, including the renin-angiotensin-aldosterone system, to

coordinate function at these four control sites and to maintain normal blood pressure.

Finally, local release of hormones from vascular endothelium may also be involved in

the regulation of vascular resistance

Blood pressure in a hypertensive patient is controlled by the same mechanisms that

are operative in normotensive subjects. Regulation of blood pressure in hypertensive

patients differs from healthy patients in that the baroreceptors and the renal blood

volume-pressure control systems appear to be "set" at a higher level of blood

pressure. All antihypertensive drugs act by interfering with these normal mechanisms.

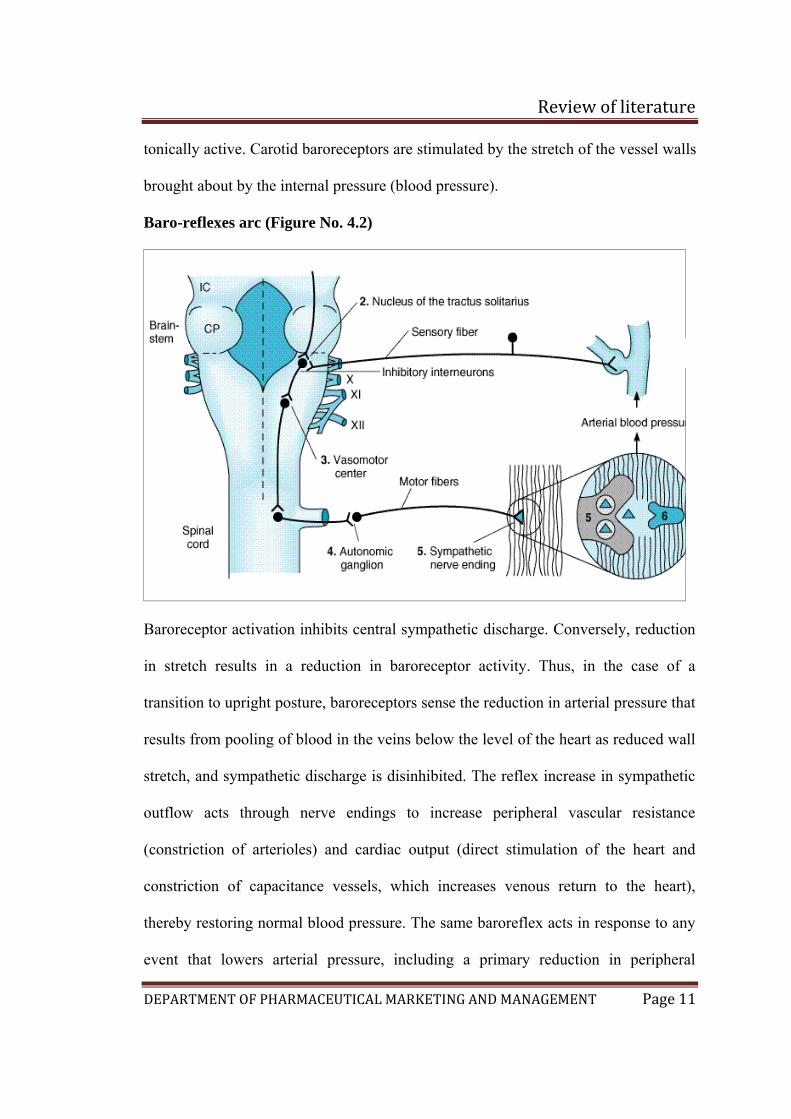

Postural Baroreflex

Baroreflexes are responsible for rapid, moment-to-moment adjustments in blood

pressure, such as in transition from a reclining to an upright posture (Figure 4.2).

Central sympathetic neurons arising from the vasomotor area of the medulla are

Review of literature

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 11

tonically active. Carotid baroreceptors are stimulated by the stretch of the vessel walls

brought about by the internal pressure (blood pressure).

Baro-reflexes arc (Figure No. 4.2)

Baroreceptor activation inhibits central sympathetic discharge. Conversely, reduction

in stretch results in a reduction in baroreceptor activity. Thus, in the case of a

transition to upright posture, baroreceptors sense the reduction in arterial pressure that

results from pooling of blood in the veins below the level of the heart as reduced wall

stretch, and sympathetic discharge is disinhibited. The reflex increase in sympathetic

outflow acts through nerve endings to increase peripheral vascular resistance

(constriction of arterioles) and cardiac output (direct stimulation of the heart and

constriction of capacitance vessels, which increases venous return to the heart),

thereby restoring normal blood pressure. The same baroreflex acts in response to any

event that lowers arterial pressure, including a primary reduction in peripheral

Review of literature

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 12

vascular resistance (eg, caused by a vasodilating agent) or a reduction in intravascular

volume (e.g, due to hemorrhage or to loss of salt and water via the kidney).

Renal Response to Decreased Blood Pressure

By controlling blood volume, the kidney is primarily responsible for long-term blood

pressure control. A reduction in renal perfusion pressure causes intrarenal

redistribution of blood flow and increased reabsorption of salt and water. In addition,

decreased pressure in renal arterioles as well as sympathetic neural activity (via -

adrenoceptors) stimulates production of renin, which increases production of

angiotensin II (see Figure 11–1). Angiotensin II causes (1) direct constriction of

resistance vessels and (2) stimulation of aldosterone synthesis in the adrenal cortex,

which increases renal sodium absorption and intravascular blood volume. Vasopressin

released from the posterior pituitary gland also plays a role in maintenance of blood

pressure through its ability to regulate water reabsorption by the kidney.

Review of literature

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 13

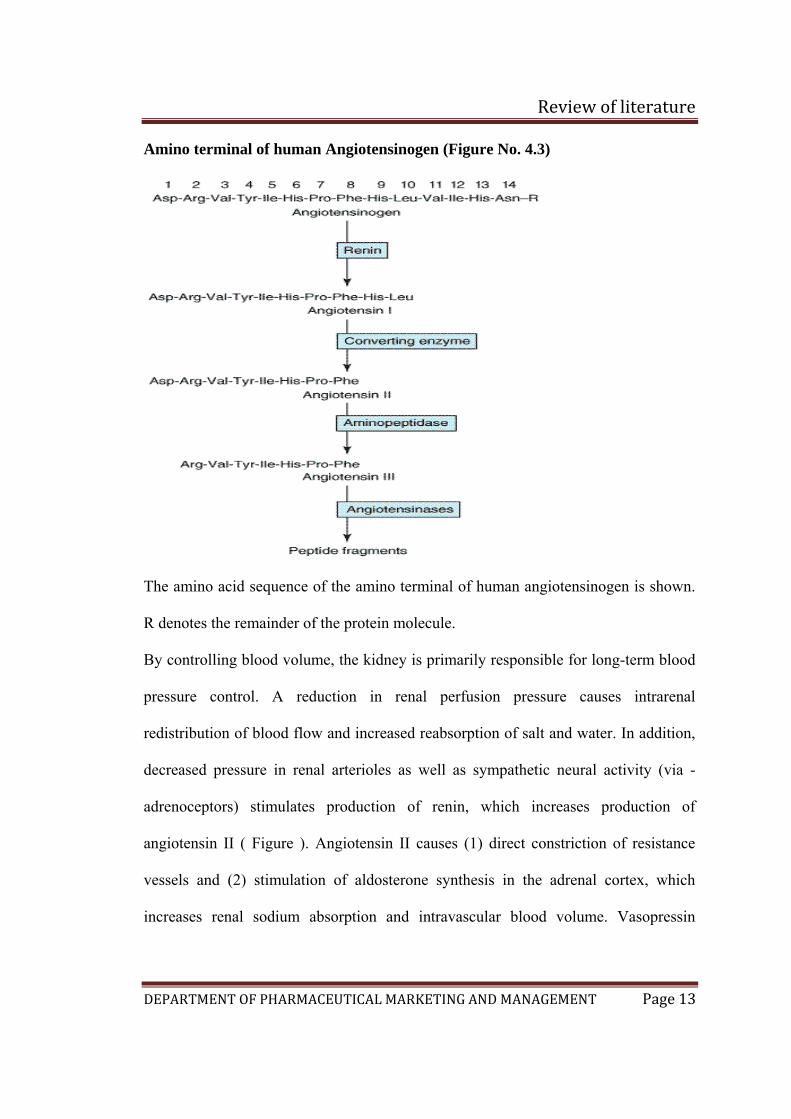

Amino terminal of human Angiotensinogen (Figure No. 4.3)

The amino acid sequence of the amino terminal of human angiotensinogen is shown.

R denotes the remainder of the protein molecule.

By controlling blood volume, the kidney is primarily responsible for long-term blood

pressure control. A reduction in renal perfusion pressure causes intrarenal

redistribution of blood flow and increased reabsorption of salt and water. In addition,

decreased pressure in renal arterioles as well as sympathetic neural activity (via -

adrenoceptors) stimulates production of renin, which increases production of

angiotensin II ( Figure ). Angiotensin II causes (1) direct constriction of resistance

vessels and (2) stimulation of aldosterone synthesis in the adrenal cortex, which

increases renal sodium absorption and intravascular blood volume. Vasopressin

Review of literature

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 14

released from the posterior pituitary gland also plays a role in maintenance of blood

pressure through its ability to regulate water reabsorption by the kidney

Angiotensin

Angiotensin II inhibits renin secretion. The inhibition, which results from a direct

action of the peptide on the juxtaglomerular cells, forms the basis of a short-loop

negative feedback mechanism controlling renin secretion. Interruption of this

feedback with inhibitors of the renin-angiotensin system (see below) results in

stimulation of renin secretion.

Pharmacologic Alteration of Renin Release

The release of renin is altered by a wide variety of pharmacologic agents. Renin

release is stimulated by vasodilators (hydralazine, minoxidil, nitroprusside), β-

adrenoceptor agonists (isoproterenol), -adrenoceptor antagonists, phosphodiesterase

inhibitors (theophylline, milrinone,rolipram), and most diuretics and anesthetics. This

stimulation can be accounted for by the control mechanisms just described. Drugs that

inhibit renin release are discussed below in the section on inhibition of the renin-

angiotensin system.

Angiotensinogen

Angiotensinogen is the circulating protein substrate from which renin cleaves

angiotensin I. It is synthesized in the liver. Human angiotensinogen is a glycoprotein

with a molecular weight of approximately 57,000. The 14 amino acids at the amino

terminal of the molecule are shown in (Figure 4.3). In humans, the concentration of

angiotensinogen in the circulation is less than the Km of the renin-angiotensinogen

reaction and is therefore an important determinant of the rate of formation of

Review of literature

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 15

angiotensin. The production of angiotensinogen is increased by corticosteroids,

estrogens, thyroid hormones, and angiotensin II. It is also elevated during pregnancy

and in women taking estrogen-containing oral contraceptives. The increased plasma

angiotensinogen concentration is thought to contribute to the hypertension that may

occur in these situations. There is also evidence for a genetic linkage between the

angiotensinogen gene and essential hypertension..

Angiotensin I

Although angiotensin I contains the peptide sequences necessary for all of the actions

of the reninangiotensin system, it has little or no biologic activity. Instead, it must be

converted to angiotensin II by converting enzyme. Angiotensin I may also be acted on

by plasma or tissue aminopeptidases to form [des-Asp1]angiotensin I; this in turn is

converted to [des-Asp1]angiotensin II (commonly known as angiotensin III) by

converting enzyme.

Converting Enzyme (Peptidyl Dipeptidase , Kininase II)

Converting enzyme is a dipeptidyl carboxypeptidase that catalyzes the cleavage of

dipeptides from the carboxyl terminal of certain peptides. Its most important

substrates are angiotensin I, which it converts to angiotensin II, and bradykinin, which

it inactivates. It also cleaves enkephalins and substance P, but the physiologic

significance of these effects has not been established. The action of converting

enzyme is prevented by a penultimate prolyl residue, and angiotensin II is therefore

not hydrolyzed by converting enzyme. Converting enzyme is distributed widely in the

body. In most tissues, converting enzyme is located on the luminal surface of vascular

endothelial cells and is thus in close contact with the circulation.

Review of literature

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 16

Angiotensinase

Angiotensin II, which has a plasma half-life of 15–60 seconds, is removed rapidly

from the

circulation by a variety of peptidases collectively referred to as angiotensinase. It is

metabolized during passage through most vascular beds (a notable exception being

the lung). Most metabolites

of angiotensin II are biologically inactive, but the initial product of aminopeptidase

action—[des- Asp1]angiotensin II—retains considerable biologic activity.

Actions of Angiotensin II

Angiotensin II exerts important actions at several sites in the body, including vascular

smoothmuscle, adrenal cortex, kidney, and brain. Through these actions, the renin-

angiotensin system plays a key role in the regulation of fluid and electrolyte balance

and arterial blood pressure. Excessive activity of the renin-angiotensin system can

result in hypertension and disorders of fluid and electrolyte homeostasis.

Blood Pressure

Angiotensin II is a very potent pressor agent—on a molar basis, approximately 40

times more potent than norepinephrine. The pressor response to intravenous

angiotensin II is rapid in onset (10– 15 seconds) and sustained during long-term

infusions of the peptide. A large component of the pressor response to intravenous

angiotensin II is due to direct contraction

Review of literature

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 17

of vascular—especially arteriolar—smooth muscle. In addition, however, angiotensin

II can also increase blood pressure through actions on the brain and autonomic

nervous system. The pressor response to angiotensin is usually accompanied by little

or no reflex bradycardia because the peptide acts on the brain to reset the baroreceptor

reflex control of heart rate to a higher pressure. Angiotensin II also interacts with the

autonomic nervous system. It stimulates autonomic ganglia, increases the release of

epinephrine and norepinephrine from the adrenal medulla, and—what is most

important—facilitates sympathetic transmission by an action at adrenergic nerve

terminals. The latter effect involves both increased release and reduced reuptake of

norepinephrine. Angiotensin II also has a less important direct positive inotropic

action on the heart.

Adrenal Cortex

Angiotensin II acts directly on the zona glomerulosa of the adrenal cortex to stimulate

aldosterone biosynthesis. At higher concentrations, angiotensin II also stimulates

glucocorticoid biosynthesis.

Kidney

Angiotensin II acts on the kidney to cause renal vasoconstriction, increase proximal

tubular sodium reabsorption, and inhibit the secretion of renin.

Central Nervous System

In addition to its central effects on blood pressure, angiotensin II acts on the central

nervous system to stimulate drinking (dipsogenic effect) and increase the secretion of

vasopressin and adrenocorticotropic hormone (ACTH). The physiologic significance

Review of literature

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 18

of the effects of angiotensin II on drinking and pituitary hormone secretion is not

known

Primary hypertension(11)

The cause of essential hypertension is unknown but a number of factors are related to

its development. These are as under:

Genetic factors: The evidences in support are the familial aggregation,

occurrence of hypertension in twins, epidemiologic data, experimental animal

studies and identification of hypertension susceptibility gene (angiotensinogen

gene)

Racial and environmental factors: A number of environmental factor have

been implicated in the development of hypertension including salt intake,

obesity, skilled occupation, higher living standards and patients in high stress.

Risk factors modifying the course of essential hypertension : These are, age,

sex, atherosclerosis and others (smoking, excess alcohol intake, diabetes

mellitus etc).

The pathogenetic mechanism in essential hypertension is explained by many

theories…..

1. High plasma level of catecholamines

2. Increase in blood volume

3. Increased cardiac output

Review of literature

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 19

4. Low renin essential hypertension due to altered responsiveness to renin release

5. High renin essential hypertension due to decresed adrenal responsiveness to

angiotensin ll

Secondary hypertension(11)

Renal hypertension: Hypertension produced by renal diseases is called renal

hypertension, which can again be subdivided into 2 groups:

a) Renal vascular hypertension

b) Renal parenchymal hypertension can be due to activation of renin-

angiotensin system, sodium and water retension, or release of

vasodepressor materials

Endocrine hypertension: A number of hormonal secretions may produce

secondary hypertension. These are due to diseased condition in adrenal gland,

parathyroid gland and oral contraceptives

Coarctation of aorta can cause hypertension

Neurogenic: psychogenic, polyneuritis, increased intracranial pressure etc are

uncommon causes of secondary hypertension

Another way of classifying hypertension is as follows….

Normal – (Systolic 90-120, diastolic 60-80)

Pre-hypertension – (Systolic 120-139, diastolic 80-99)

Review of literature

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 20

Hypertension Mild, Stage 1 - (Systolic 140-159 or diastolic 90-99)

Hypertension Moderate, Stage 2 - (Systolic 160 - 179 diastolic 100 – 109)

Hypertension Severe, Stage 3 - (Systolic 180 - 209 or diastolic 110 – 119)

Hypertension Very Severe, Stage 4 - (Systolic > or = 210 or diastolic > or =

120)

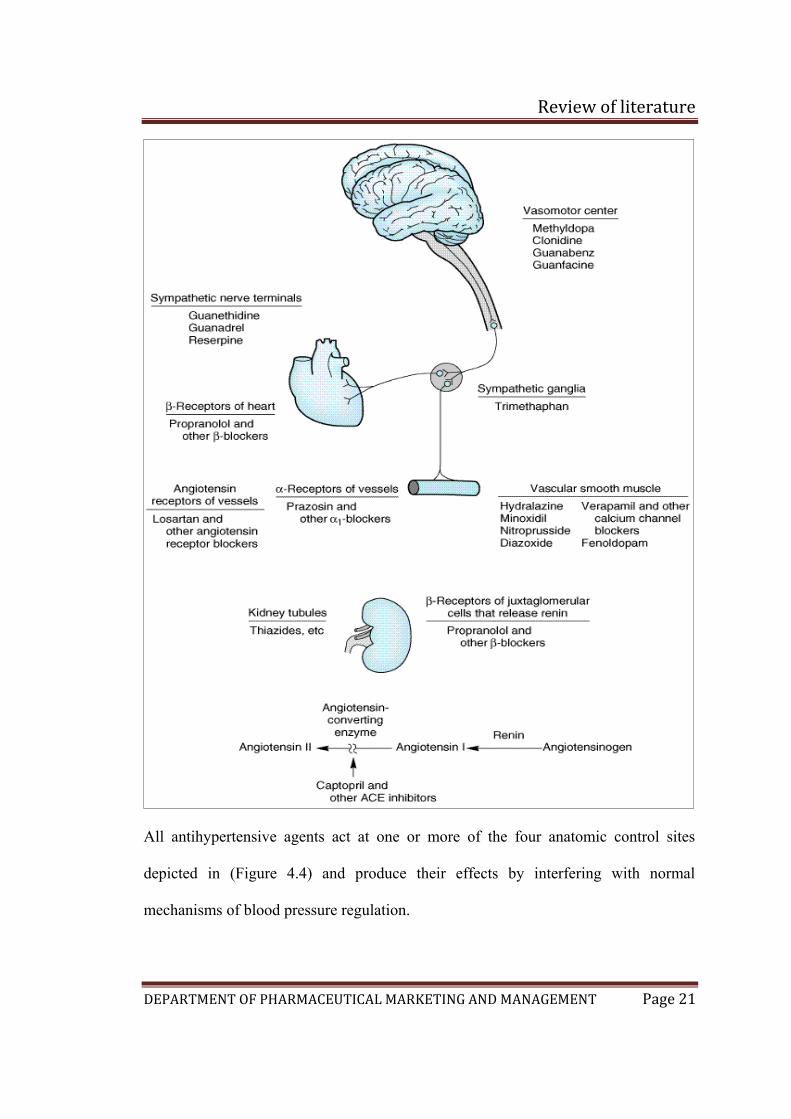

Management Of Hypertension (10) (Figure No. 4.4)

Review of literature

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 21

All antihypertensive agents act at one or more of the four anatomic control sites

depicted in (Figure 4.4) and produce their effects by interfering with normal

mechanisms of blood pressure regulation.

Review of literature

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 22

A useful classification of these agents categorizes them according to the principal

regulatory site or mechanism on which they act (Figure4.4). Because of their common

mechanisms of action, drugs within each category tend to produce a similar spectrum

of toxicities. The categories include the following:

(1) Diuretics, which lower blood pressure by depleting the body of sodium and

reducing blood volume and perhaps by other mechanisms.

(2) Sympathoplegic agents, which lower blood pressure by reducing peripheral

vascular

resistance, inhibiting cardiac function, and increasing venous pooling in capacitance

vessels.

(The latter two effects reduce cardiac output.) These agents are further subdivided

according to their putative sites of action in the sympathetic reflex arc.

(3) Direct vasodilators, which reduce pressure by relaxing vascular smooth muscle,

thus

dilating resistance vessels and—to varying degrees—increasing capacitance as well.

(4) Agents that block production or action of angiotensin and thereby reduce

peripheral

vascular resistance and (potentially) blood volume.

Review of literature

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 23

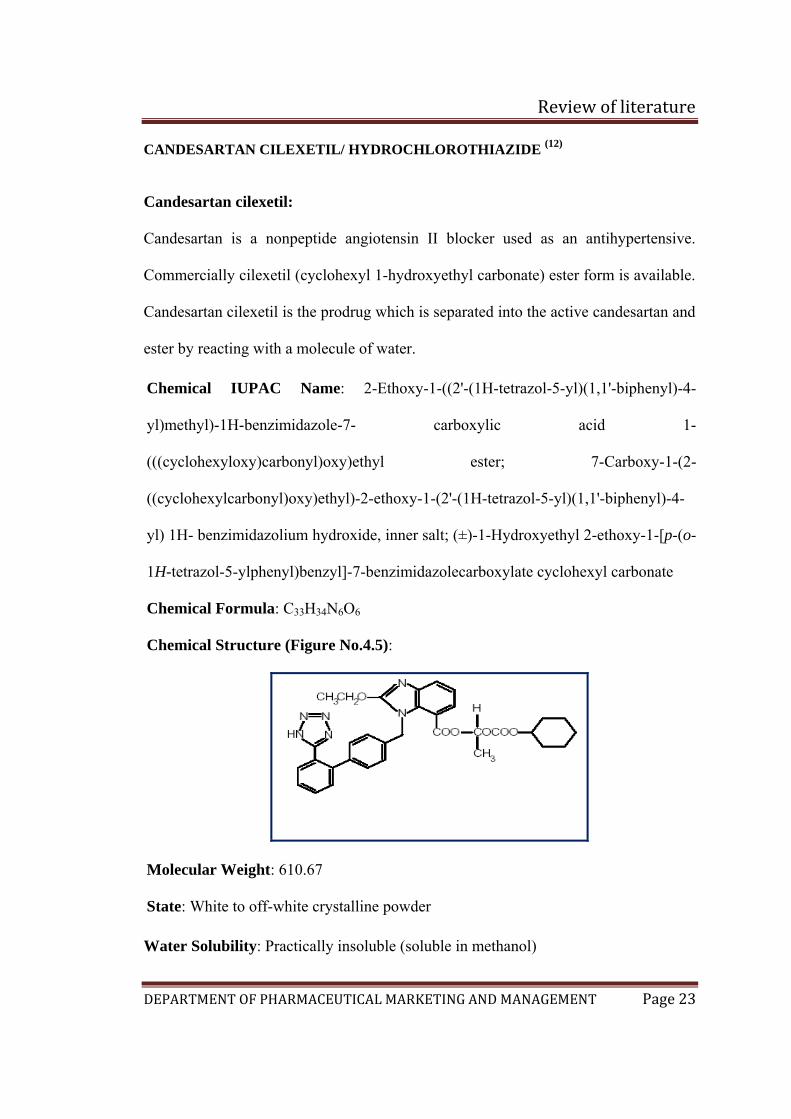

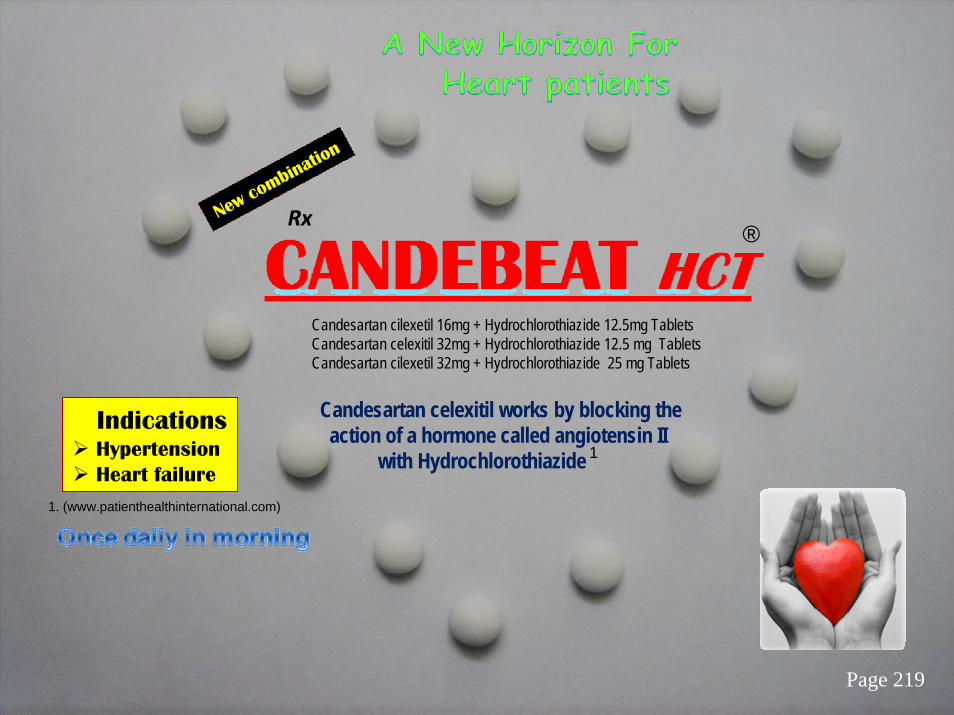

CANDESARTAN CILEXETIL/ HYDROCHLOROTHIAZIDE (12)

Candesartan cilexetil:

Candesartan is a nonpeptide angiotensin II blocker used as an antihypertensive.

Commercially cilexetil (cyclohexyl 1-hydroxyethyl carbonate) ester form is available.

Candesartan cilexetil is the prodrug which is separated into the active candesartan and

ester by reacting with a molecule of water.

Chemical IUPAC Name: 2-Ethoxy-1-((2'-(1H-tetrazol-5-yl)(1,1'-biphenyl)-4-

yl)methyl)-1H-benzimidazole-7- carboxylic acid 1-

(((cyclohexyloxy)carbonyl)oxy)ethyl ester; 7-Carboxy-1-(2-

((cyclohexylcarbonyl)oxy)ethyl)-2-ethoxy-1-(2'-(1H-tetrazol-5-yl)(1,1'-biphenyl)-4-

yl) 1H- benzimidazolium hydroxide, inner salt; (±)-1-Hydroxyethyl 2-ethoxy-1-[p-(o-

1H-tetrazol-5-ylphenyl)benzyl]-7-benzimidazolecarboxylate cyclohexyl carbonate

Chemical Formula: C33H34N6O6

Chemical Structure (Figure No.4.5):

Molecular Weight: 610.67

State: White to off-white crystalline powder

Water Solubility: Practically insoluble (soluble in methanol)

Review of literature

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 24

Half Life: Approximately 9 hours.

Melting point: 157 - 160 C

• Candesartan works by blocking the action of a hormone (a natural chemical

carried in the blood) called angiotensin II:

• It stops angiotensin II attaching itself (binding) to sites (called receptors)

found on cells in the body.

• In the body Angiotensin II causes blood vessels to become narrowed

(constricted) and in the kidney, it causes less urine to be produced so salt and

water are retained in the body. These actions may be part of the cause of high

blood pressure.

• If angiotensin II can’t bind to the receptors because of the action of

candesartan, the blood vessels relax and widen and blood pressure decreases.

Dose: The usual recommended starting dose of candesartan 16 mg once daily when it

is used as monotherapy in patients who are not volume depleted. Patients requiring

further reduction in blood pressure should be titrated to candesartan 32 mg. ( )

Pharmacokinetics: General

Candesartan cilexetil is rapidly and completely bioactivated by ester hydrolysis

during absorption from the gastrointestinal tract to candesartan, a selective AT1

subtype angiotensin II receptor antagonist. Candesartan is mainly excreted unchanged

in urine and feces (via bile). It undergoes minor hepatic metabolism by O-

demethylation to an inactive metabolite. The elimation half-life of candesartan is

Review of literature

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 25

approximately 9hours. After single and repeated administration, the pharmacokinetics

of candesartan are linier for oral doses upto 32 mg of candesartan cilexetil.

Candesartan and its inactive metabolite do not accumulate in serum upon repeated

once-daily dosing. Following administration of candesartan cilexetil, the absolute

bioavailability of candesartan was estimated to be 15%. After tablet ingestion, the

peak serum concentration (Cmax) is reached after 3 to 4 hours. Food with a high fat

content does not affect the bioavailability of candesartan after candesartan cilexetil

administration.

Metabolism and excretion:

Total plasma clearance of candesartan is 0.37 ml/min/kg, with a renal clearance of

0.19 ml/min/kg. when candesartan is administered orally, about 26% of the dose is

excreted unchanged in urine.

Distribution:

The volume of distribution of candesartan is 0.13L/kg. candesartan is highly bound to

plasma proteins (>99%) and does not penetrate red blood cells. The protein binding is

constant at candesartan plasma concentrations well above the range achieved with

recommended doses.

Special populations:

The pharmacokinetics of Candesartan have been studied in the elderly (≥65years).

The plasma concentration of Candesartan was higher in the elderly (Cmax was

approximately 50% higher, and AUC was approximately 80% higher) compared to

younger subjects administered the same dose. The pharmacokinetics of Candesartan

were linear in the elderly, and Candesartan and its inactive metabolite did not

Review of literature

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 26

accumulate in the serum of these subjects upon repeated, once-daily administration.

No initial dosage adjustment is necessary.

Gender:

There is no difference in the pharmacokinetics of Candesartan between male and

female subjects.

Pharmacodynamics:

Candesartan Cilexetil inhibits the pressor effects of angiotensin II infusion in a dose-

dependent manner. After 1 week of once-daily dosing with 8mg Candesartan cilexetil,

the pressor effect was inhibited by approximately 90% at peak with approximately

50% inhibition persisting for 24 hours.

Warnings:

Drug that act directly on the rennin-angiotensin system can cause fetal and neonatal

morbidity and death when administered to pregnant women. Post-marketing

experience has identified reports of fetal and neonatal toxicity in babies born to

women treated with Candesartan cilexetil during pregnancy. The use of drugs that act

directly on the rennin-angiotensisn system during the second and third trimesters of

pregnancy has been associated with fetal and neonatal injury, including hypotension,

neonatal skull hypoplasia, anuria, reversible or irreversible renal failure and death.

Oligohydramnios has been reported, presumably resulting from decreased fetal renal

functions.

Hypotension in volume and salt depleted patients:

Review of literature

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 27

Based on adverse events reported from all clinical trials, excessive reduction of blood

pressure was rarely seen in patients with uncomplicated hypertension treated with

candesartan cilexetil and hydrochlorothiazide. Initiation of antihypertensive therapy

amy cause symptomatic hypotension in patients with intravascular volume or sodium

depletion. These conditions should be corrected prior to administration of the drug.

Adverse reactions:

These include hypotension, hyperkalemia, and reduced renal function, including that

associated with bilateral renal artery stenosis and stenosis in the artery of a solitary

kidney. Hypotension is most likely to occur in patients in whom the blood pressure is

highly dependent on angiotensin II, including those with volume depletion (e.g., with

diuretics), renovascular hypertension, cardiac failure, and cirrhosis; in such patients

initiation of treatment with low doses and attention to blood volume is essential.

Hyperkalemia may occur in conjunction with other factors that alter K+ homeostasis,

such as renal insufficiency, ingestion of excess K+, and the use of drugs that promote

K+ retention.

Review of literature

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 28

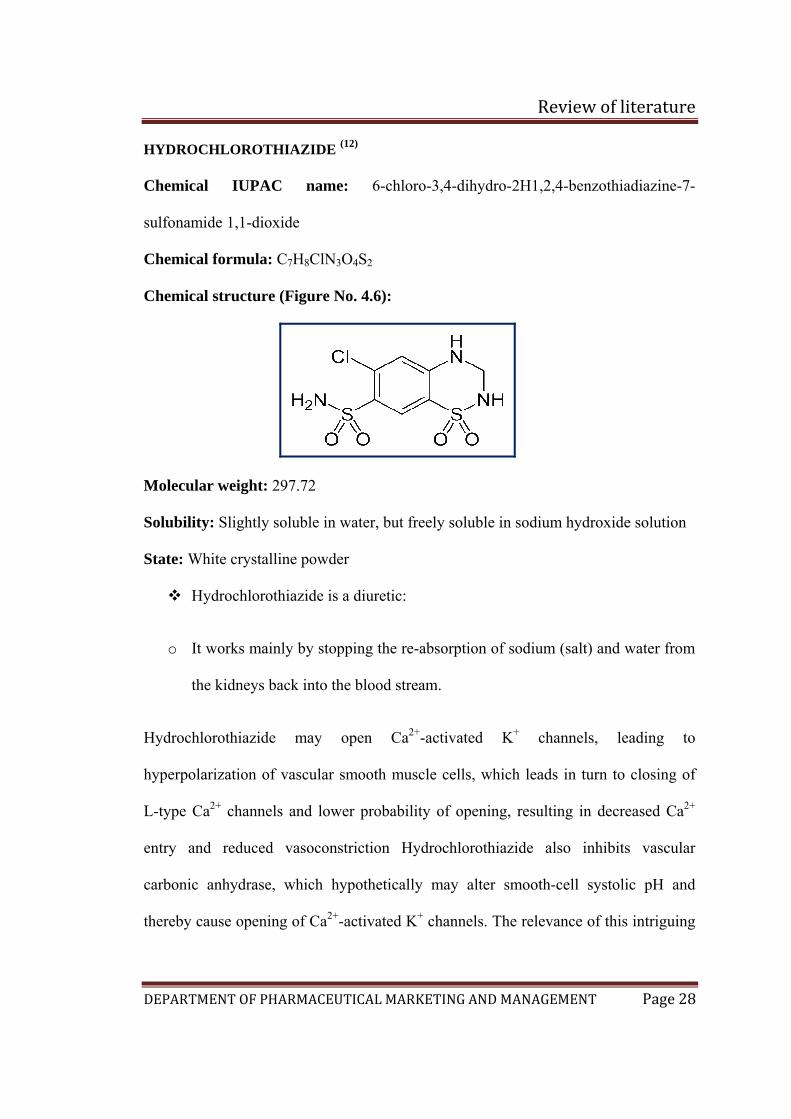

HYDROCHLOROTHIAZIDE (12)

Chemical IUPAC name: 6-chloro-3,4-dihydro-2H1,2,4-benzothiadiazine-7-

sulfonamide 1,1-dioxide

Chemical formula: C7H8ClN3O4S2

Chemical structure (Figure No. 4.6):

Molecular weight: 297.72

Solubility: Slightly soluble in water, but freely soluble in sodium hydroxide solution

State: White crystalline powder

Hydrochlorothiazide is a diuretic:

o It works mainly by stopping the re-absorption of sodium (salt) and water from

the kidneys back into the blood stream.

Hydrochlorothiazide may open Ca2+-activated K+ channels, leading to

hyperpolarization of vascular smooth muscle cells, which leads in turn to closing of

L-type Ca2+ channels and lower probability of opening, resulting in decreased Ca2+

entry and reduced vasoconstriction Hydrochlorothiazide also inhibits vascular

carbonic anhydrase, which hypothetically may alter smooth-cell systolic pH and

thereby cause opening of Ca2+-activated K+ channels. The relevance of this intriguing

Review of literature

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 29

finding to the observed antihypertensive effects of thiazides is speculative. These

effects lower the blood pressure

Dose: It is effective in doses of 12.5 to 50 mg once daily.

Pharmacokinetics: General

When plasma levels have been followed for at least 24 hours, the plasma half-life has

been observed to vary between 5.6 and 14.8 hours

Metabolism and Excretion:

Hydrochlorothiazide is not metabolized but is eliminated rapidly by kidney. At least

61% of the oral dose is eliminated within 24 hours.

Distribution:

It crosses the placental barrier but not the blood brain barrier and is excreted in breast

milk.

Pharmacodynamics:

After oral administration of hydrochlorothiazide, dieresis begins within 2 hours, peak

in about 4 hours and last about 6 to 12 hours.

Warnings:

Thiazide diuretics should be used with caution in patients with impaired hepatic

function or progressive liver disease, since minor alterations of fluid and electrolyte

balance may precipitate hepatic coma. Hypersensitivity reactions to

hydrochlorthiazide may occur in patients with or without a history of allergy or

bronchial asthma, but are more likely in patients with such a history. Thiazide

Review of literature

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 30

diuretics have been reported to cause exacerbation or activation of systemic lupus

erythematous.

Adverse reactions:

Erectile dysfunction is a troublesome adverse effect of the thiazide-class diuretics,

and physicians should inquire specifically regarding its occurrence in conjunction

with treatment with these drugs. Gout may be a consequence of the hyperuricemia

induced by these diuretics. The occurrence of either of these adverse effects is a

reason for considering alternative approaches to therapy. However, precipitation of

acute gout is relatively uncommon with low doses of diuretics. Hydrochlorothiazide

may cause rapidly developing, severe hyponatremia in some patients. Thiazides

inhibit renal Ca2+ excretion, occasionally leading to hypercalcemia; although

generally mild, this can be more severe in patients subject to hypercalcemia, such as

those with primary hyperparathyroidism. The thiazide-induced decreased Ca2+

excretion may be used therapeutically in patients with osteoporosis or hypercalciuria.

Clinical trials (12)

Of 12 controlled clinical trials involving 4588 patients, 5 were double-blinded,

placebo controlled and evaluated the hypertensive effects of single entities vs the

combination. these 5 trials, of 8 to 12 weeks duration, randomized 3037 hypertensive

patients. does ranged from 2 to 32 mg Candesartan cilexetil and from 6.25 to 25 mg

Hydrochlorthiazide administered once daily in various combinations. the combination

of Candesartan cilexetil with Hydrochlorthiazide resulted in placebo-adjusted

decreases in sitting systolic and diastolic blood pressure of 14 – 18/8 – 11 mm Hg at

doses of 16 – 12.5 mg and 32 – 12.5 mg. The combination of Candesartan cilextil and

Review of literature

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 31

Hydrochlorthiazide 32 – 25 mg resulted in placebo adjusted decreases in sitting

systolic and diastolic blood pressure of 16- 19 /9 – 11 mm Hg. The placebo corrected

trough to peak ratio was evaluated in a study of Candesartan cilexetil

Hydrochlorthiazide 32 - 12.5 mg and was 88%.

Most of the antihypertensive effect of the combination was seen in 1 to 2 weeks with

the full effect observed within 4 weeks.in long term studies of upto 1 year, the blood

pressure lowering effect of the combination was maintained. the antihypertensive

effect was similar regardless of age or gender, and overall response to the

combination was similar in black and non-black patients.

Men and women, aged 20–80 years, during treatment with any kind of

antihypertensive monotherapy for at least 4 weeks were randomised to treatment with

Candesartan cilexetil (Candes)-Hydrochlorthiazide (HCT) or Los-HCT once daily for

12 weeks. Efficacy analysis was performed according to intention to treat. The

reduction in BP was independent of previous antihypertensive agent, gender and age

of the patient. It was concluded conclude that the combination Candes-HCT reduced

blood pressure effectively and was well tolerated. BP was normalised in 61% of these

patients who had insufficient response to previous monotherapy. The reduction in

blood pressure and proportion of patients with normalized BP was greater with

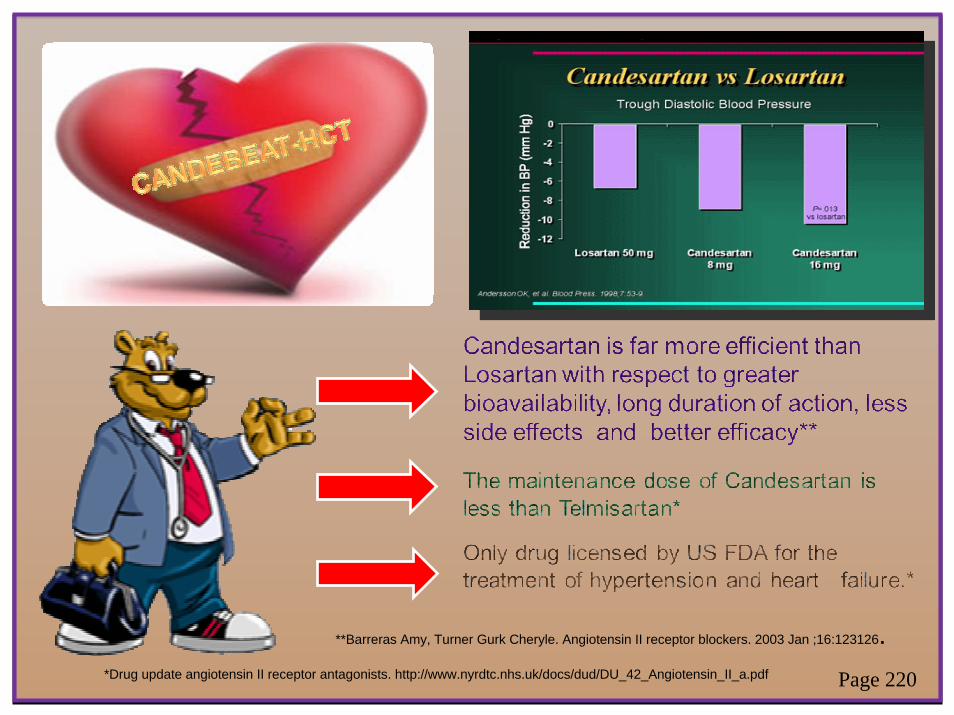

Candes-HCT 16/12.5 mg than with Los-HCT 50/12.5 mg.(13)

Monotherapy with an antihypertensive agent is likely to achieve a desirable lowering

of blood pressure in about 50% of patients. The aim of this study was to compare the

Review of literature

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 32

antihypertensive effect and tolerability of a once-daily combination of the angiotensin

II type 1 (AT1) receptor blocker candesartan cilexetil, and the diuretic

hydrochlorothiazide (HCT), with a combination of the angiotensin-converting

enzyme inhibitor, lisinopril and HCT in patients with primary hypertension. The

study included men and women, 20-80 years of age, with sitting diastolic blood

pressure of 95-114 mm Hg. After a run-in period of 2 weeks on any antihypertensive

monotherapy, 355 patients were randomized to double-blind treatment with either a

combination of candesartan cilexetil/HCT or a combination of lisinopril/HCT The

combinations of candesartan cilexetil/HCT once daily, and lisinopril/HCT, once daily,

had similar antihypertensive efficacy in patients with mild to moderate hypertension

during the 26-week treatment period, candesartan cilexetil/HCT was significantly

better tolerated than lisinopril/HCT.(6)

The primary objective of the study was to assess the bioequivalence of one

candesartan cilexetil/hydrochlorothiazide (HCT) 32/25 mg tablet and two candesartan

cilexetil/HCT 16/12.5 mg tablets after single dose administration. The secondary

objective of the study was to assess the pharmacokinetics of candesartan cilexetil 32

mg and HCT 25 mg after single dose administration of the fixed combination tablet

and after each monocomponent (ie one candesartan cilexetil tablet 32 mg tablet and

two HCT 12.5 mg tablets). According to the group-sequential design, 53 healthy male

and female subjects, aged between18 and 59 years, with female subjects comprising

at least 20% per treatment group, were enrolled in the first step, to ensure completion

by at least 48 subjects. A total of 48 subjects completed the study. Single dose

administration of candesartan cilexetil and hydrochlorothiazide was well tolerated,

Review of literature

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 33

and no new safety issues were identified during the study regardless of the

administration schedule. Headache and dizziness were the most frequently observed

adverse events (AE). No deaths, serious adverse events, or adverse events classified

as "other significant AEs" occurred during the study. No subject discontinued study

treatments due to an AE. There were no clinically relevant changes in laboratory

safety variables or physical examinations. An expected blood pressure lowering effect

was observed reaching mean minimum SBP and DBP values at around 8 hours after

dosing of 32 mg candesartan cilexetil, ie, after one candesartan cilexetil/HCT 32/25

mg tablet, after two candesartan cilexetil/HCT16/12.5 mg tablets or after one

candesartan cilexetil 32mg tablet. This blood pressure lowering effect was less

evident after treatment with two HCT 12.5 mg tablets.(10)

The angiotensin II receptor blocker candesartan cilexetil and the diuretic

hydrochlorothiazide is a combination introduced by Astrazeneca. It is used to treat

high blood pressure (hypertension) when one medicine (monotherapy) is not

sufficiently effective. The combination of two medicines that have different ways of

working (modes of action) and leads to a greater lowering of blood pressure in more

people than with either medicine used alone.(7)

Hypertension treatment and control is largely unsatisfactory when guideline-defined

blood pressure goal achievement and maintenance are considered. Patient- and

physician-related factors leading to non-adherence interfere in this respect with the

efficacy, tolerability, and convenient use of pharmacological treatment options.

Review of literature

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 34

Blockers of the renin–angiotensin system (RAS) are an important component of

antihypertensive combination therapy. Thiazide-type diuretics are usually added to

increase the blood pressure lowering efficacy. Fixed drug–drug combinations of both

principles like candesartan/hydrochlorothiazide (HCT) are highly effective in

lowering blood pressure while providing improved compliance, a good tolerability,

and largely neutral metabolic profile. Comparative studies with losartan/HCT have

consistently shown a higher clinical efficacy with the candesartan/HCT combination.

Data on the reduction of cardiovascular endpoints with fixed dose combinations of

antihypertensive drugs are however scarce, as are the data for candesartan/HCT. But

many trials have tested candesartan versus a non-RAS blocking comparator based on

a standard therapy including thiazide diuretics. The indications tested were heart

failure and stroke and particular emphasis was put on elderly patients or those with

diabetes. In patients with heart failure, for example, the fixed dose combination might

be applied in patients in whom individual titration resulted in a dose of 32 mg

candesartan and 25 mg HCT which can then be combined into one tablet to increase

compliance with treatment. Also in patients with stroke the fixed dose combination

might be used in patients in whom maintenance therapy with both components is

considered. Taken together candesartan/HCT assist both physicians and patients in

achieving long-term blood pressure goal achievement and maintenance. (13)

Therapeutic interventions that block the renin–angiotensin–aldosterone system

(RAAS) have an important role in slowing the progression of cardiovascular risk

factors to established cardiovascular diseases. In recent years, angiotensin receptor

Review of literature

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 35

blockers (ARBs) have emerged as effective and well-tolerated alternatives to an

angiotensin-converting enzyme inhibitor (ACEi) for RAAS blockade. The ARB

candesartan was initially established as an effective once-daily antihypertensive

treatment, providing 24 h blood pressure (BP) control with a trough:peak ratio close

to 100%.

Compared with other ARBs, candesartan demonstrates the strongest binding affinity

to the angiotensin II type 1 receptor. Clinical trials have demonstrated that

candesartan is well tolerated in combination with diuretics or calcium channel

blockers (CCBs), making it a suitable treatment option for patients whose

hypertension is not adequately controlled by monotherapy. Subsequently, candesartan

became the only ARB licensed in the UK to treat patients with CHF and left

ventricular ejection fraction ≤ 40% as add-on therapy to an ACEi or when an ACEi is

not tolerated. Studies in patients with symptomatic HF have indicated that candesartan

treatment was associated with significant relative risk reductions in cardiovascular

mortality and hospitalisation due to CHF. (14 )

Review of literature

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 36

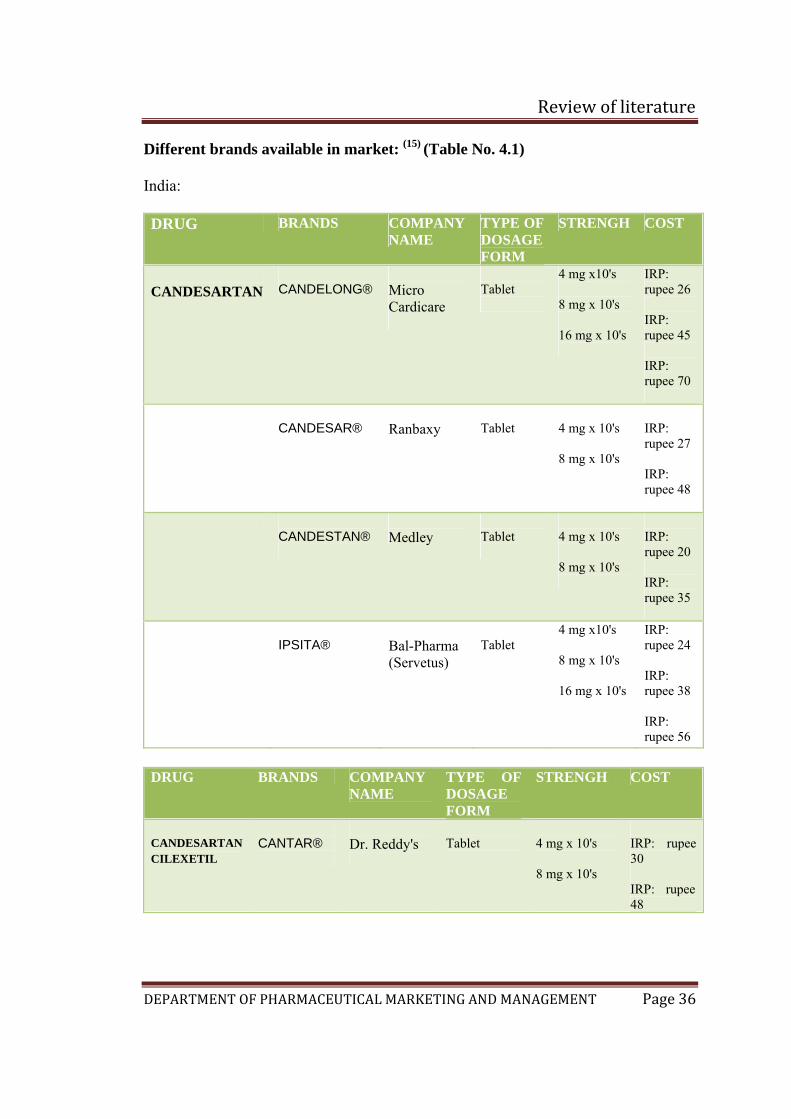

Different brands available in market: (15) (Table No. 4.1)

India:

DRUG BRANDS COMPANY NAME

TYPE OF DOSAGE FORM

STRENGH COST

CANDESARTAN

CANDELONG®

Micro Cardicare

Tablet

4 mg x10's 8 mg x 10's 16 mg x 10's

IRP: rupee 26 IRP: rupee 45 IRP: rupee 70

CANDESAR®

Ranbaxy

Tablet

4 mg x 10's 8 mg x 10's

IRP: rupee 27 IRP: rupee 48

CANDESTAN®

Medley

Tablet

4 mg x 10's 8 mg x 10's

IRP: rupee 20 IRP: rupee 35

IPSITA®

Bal-Pharma (Servetus)

Tablet

4 mg x10's 8 mg x 10's 16 mg x 10's

IRP: rupee 24 IRP: rupee 38 IRP: rupee 56

DRUG BRANDS COMPANY

NAME TYPE OF DOSAGE FORM

STRENGH COST

CANDESARTAN CILEXETIL

CANTAR®

Dr. Reddy's

Tablet

4 mg x 10's 8 mg x 10's

IRP: rupee 30 IRP: rupee 48

Review of literature

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 37

DRUG BRANDS COMPANY NAME

TYPE OF DOSAGE FORM

STRENGH COST

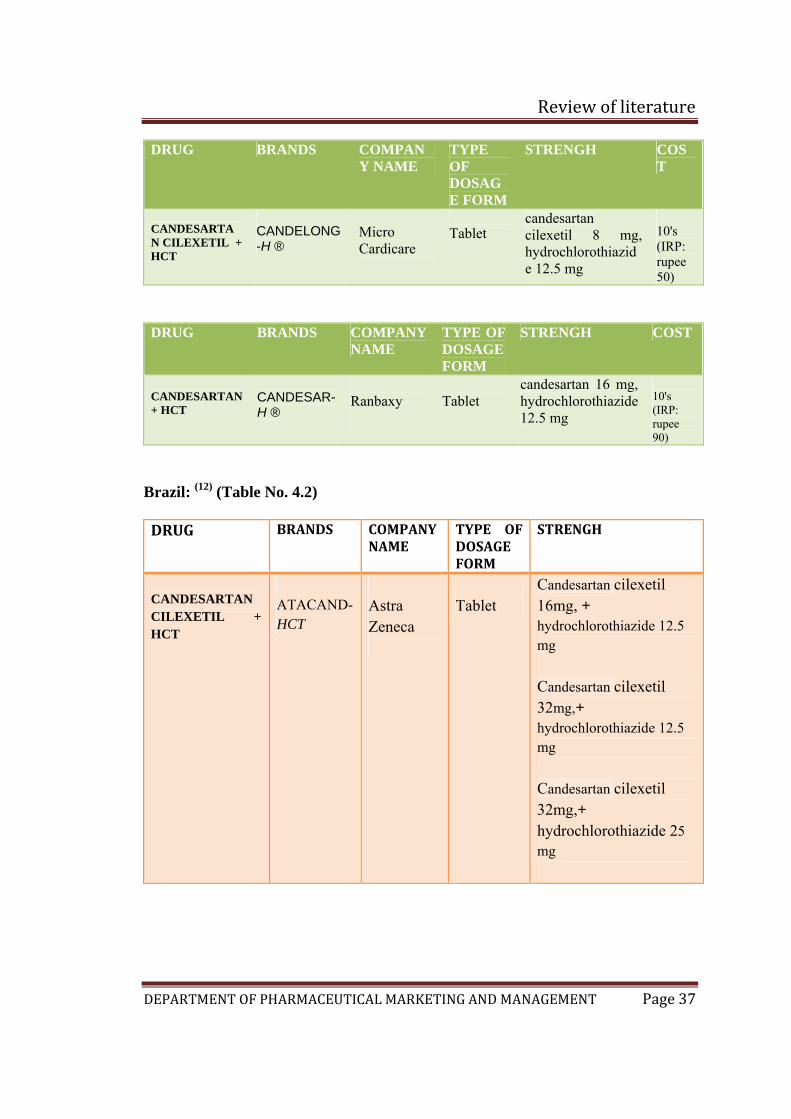

CANDESARTAN CILEXETIL + HCT

CANDELONG-H ®

Micro Cardicare

Tablet

candesartan cilexetil 8 mg, hydrochlorothiazide 12.5 mg

10's (IRP: rupee 50)

DRUG BRANDS COMPANY NAME

TYPE OF DOSAGE FORM

STRENGH COST

CANDESARTAN + HCT

CANDESAR-H ®

Ranbaxy

Tablet

candesartan 16 mg, hydrochlorothiazide 12.5 mg

10's (IRP: rupee 90)

Brazil: (12) (Table No. 4.2)

DRUG BRANDS COMPANY NAME

TYPE OF DOSAGE FORM

STRENGH

CANDESARTAN CILEXETIL + HCT

ATACAND- HCT

Astra Zeneca

Tablet

Candesartan cilexetil 16mg, + hydrochlorothiazide 12.5 mg Candesartan cilexetil 32mg,+ hydrochlorothiazide 12.5 mg Candesartan cilexetil 32mg,+ hydrochlorothiazide 25 mg

Review of literature

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 38

Market potential:

According to World Health Organisation (WHO) the mortality from cardiovascular

disease by the year 2020 in low to middle income countries will exceed deaths from

infectious and parasitic disease in all regions except sub-Saharan Africa, where

hypertension is a major risk factor. (16) Where in India also high blood pressure is a

major risk factor and better control can lead to prevention of 300,000 of 1.5 million

annual deaths from cardiovascular disease. (17)

Thus the market potential (in terms of prevalence) is huge. Recently, the JNC 7 (the

Seventh report of the Joint National Committee on Prevention, detection, evaluation,

and treatment of High Blood pressure) has defined blood pressure 120/80 mmHg to

139/89 mmHg as "Pre-hypertension.“ Pre-hypertension is not a disease category;

rather, it is a designation chosen to identify individuals at high risk of developing

hypertension. Hence, strategies devised to increase awareness can help in gaining

footholds in the latent potential market also.

Methodology

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 38

5. METHODOLOGY

Source of Data:

The source for market research will include:

• Primary source: Primary data will be obtained from the identified respondents

by the administration of questionnaire following informed consent

Inclusion criteria:

a) Doctors who are cardiologist, general physician and general practitioners.

b) Registered pharmacists who are at retail outlets and hospitals

Exclusion criteria:

a) Doctors who do not belong to the specialties mentioned above and who

practice in Ayurvedic , Homeopathy, Unani etc are not included in the study

b) Pharmacist who are not registered and trainees are not included in the study

• Secondary source:

a) Journals

b) Trade and business journals

c) Internationals magazine

d) Textbook of pharmaceutical marketing and international marketing

Methodology

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 39

e) Internet

f) Pharma pulse

g) Pharma biz

Method of collection of data:

Preliminary communication with doctors and pharmacists through personal

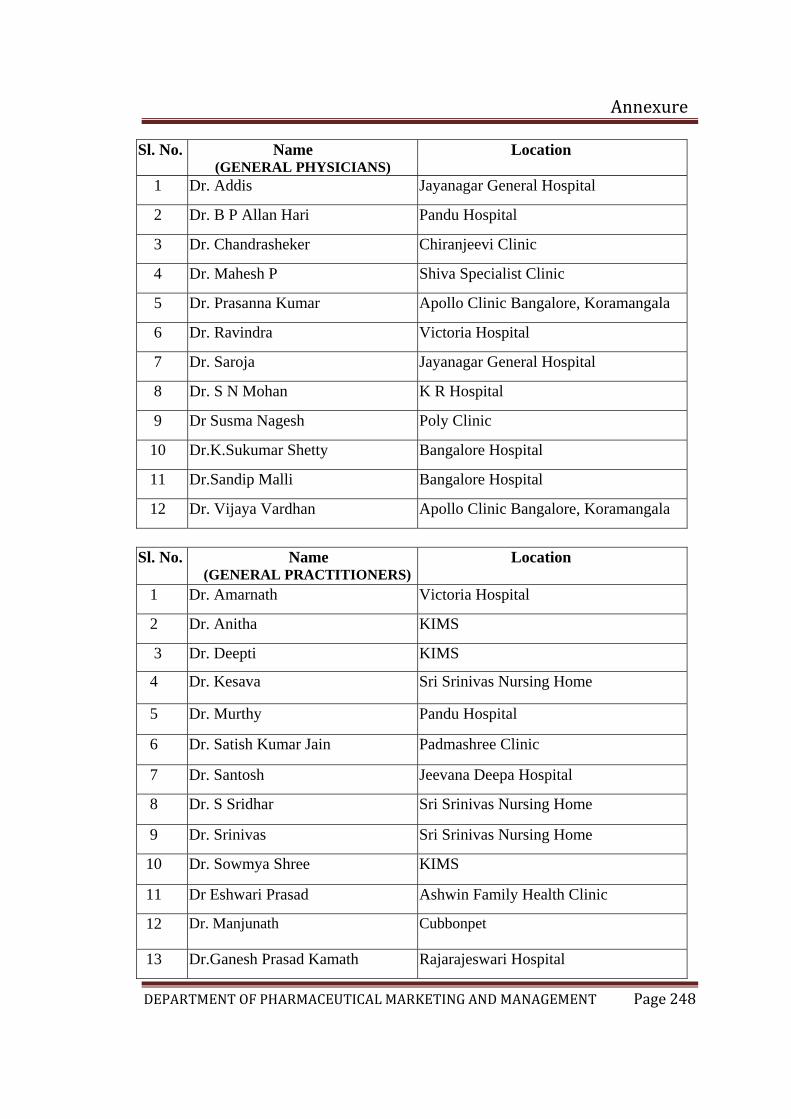

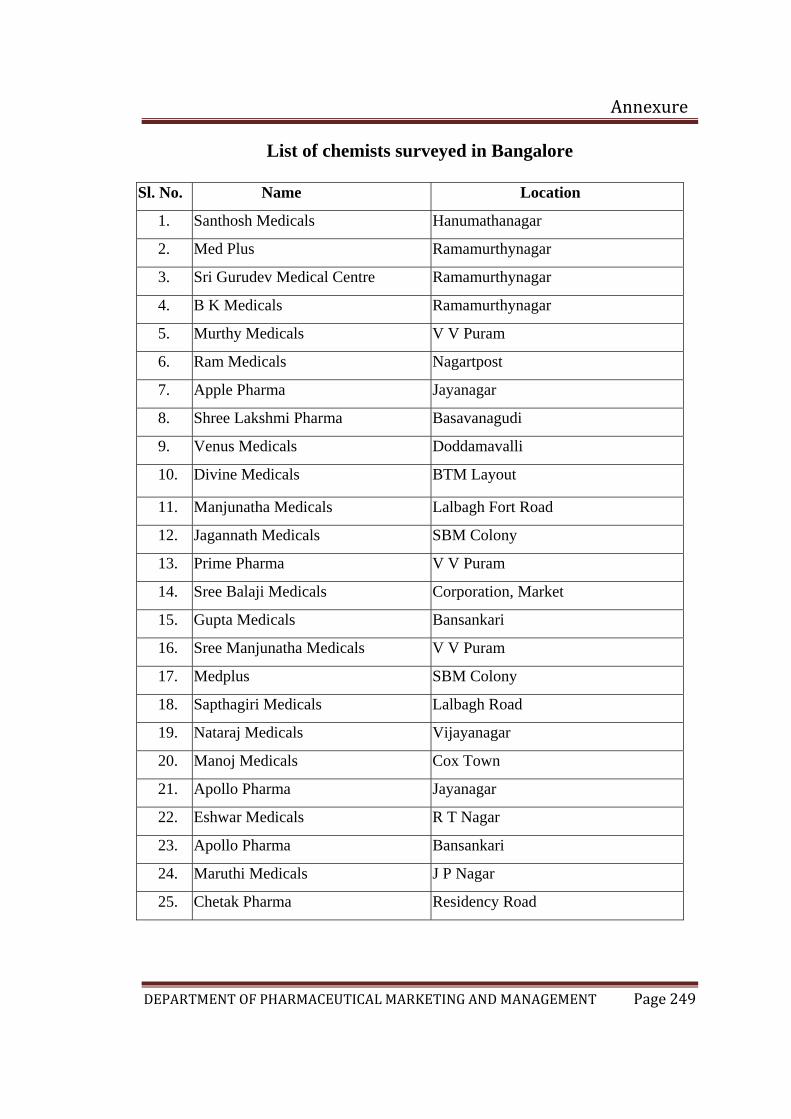

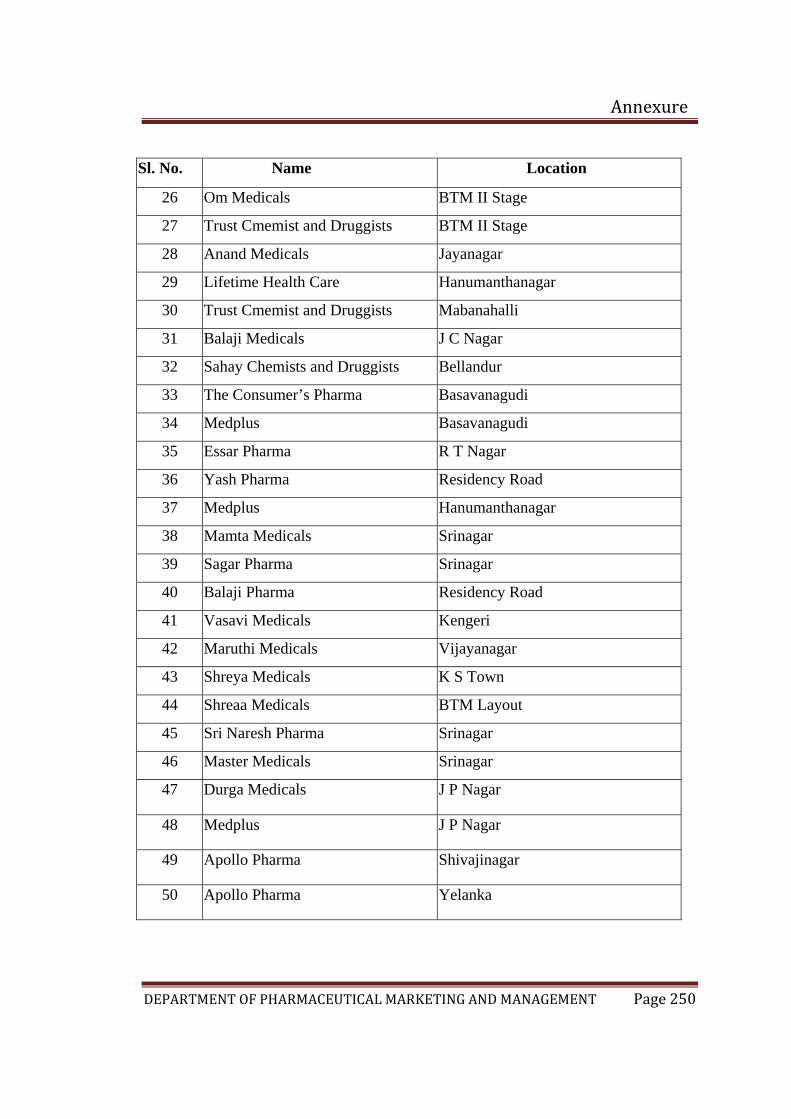

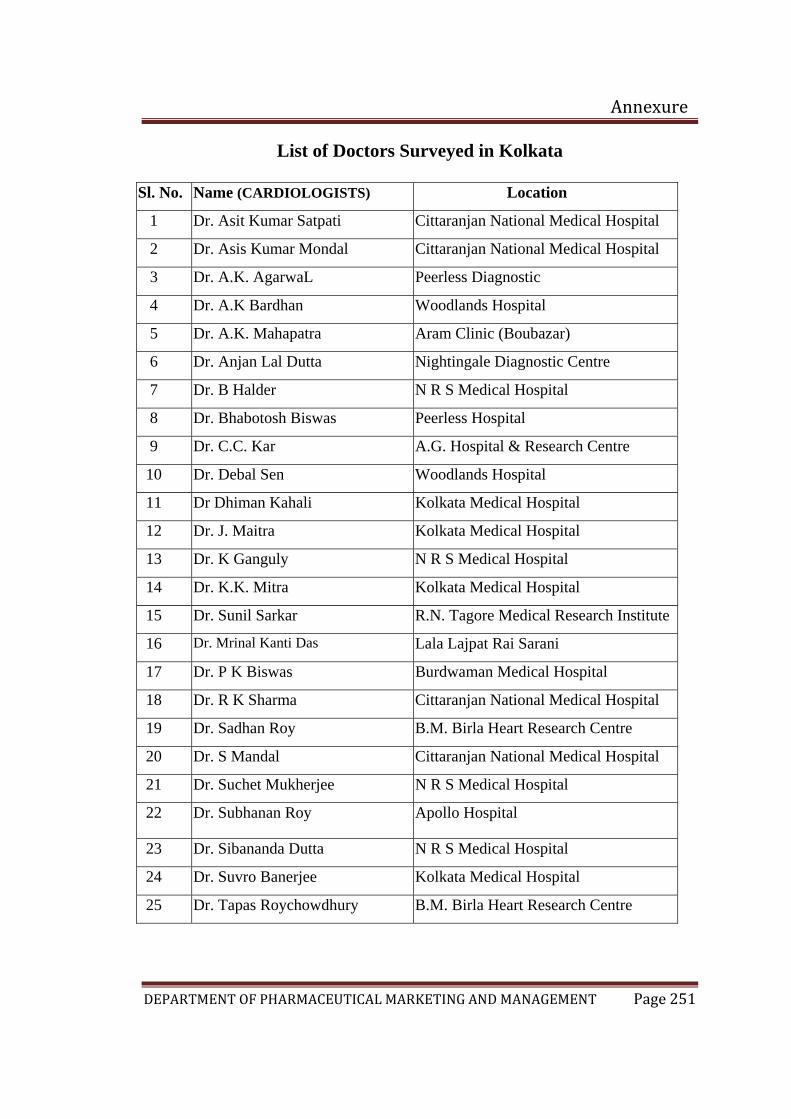

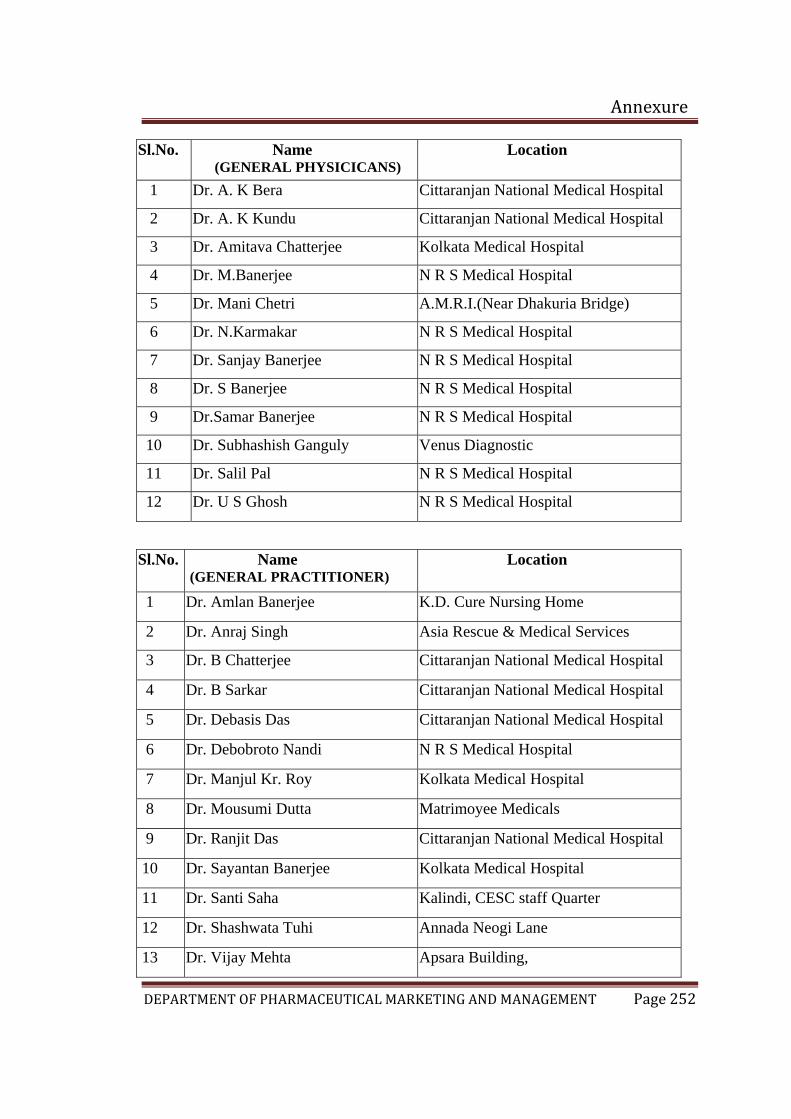

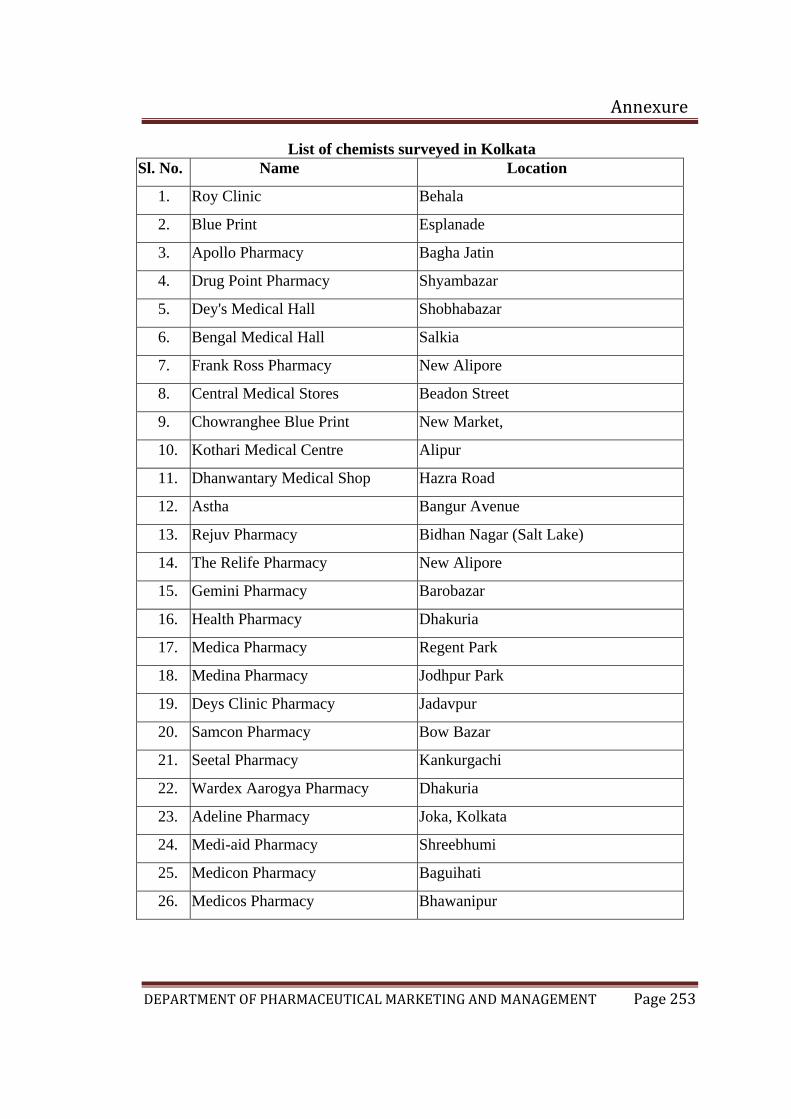

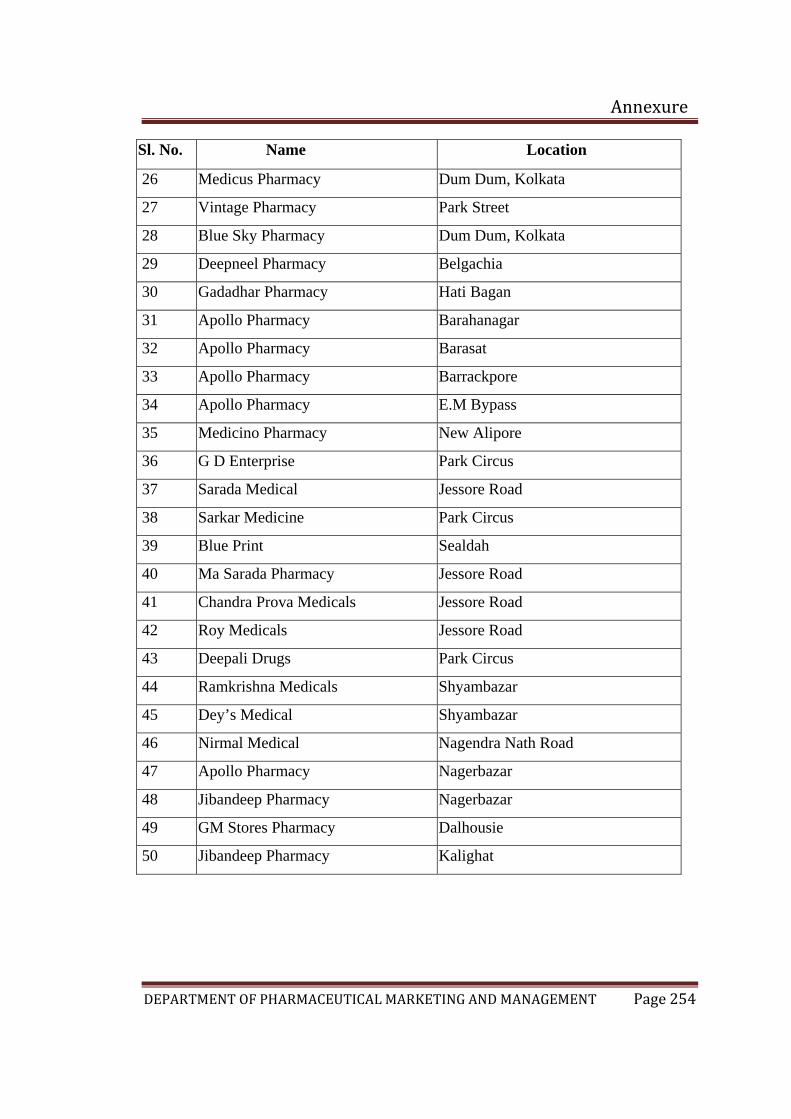

interview to get consent to participate in the survey

Sample size:

1. Doctors:

a) 50 Cardiologists

b) 25 General physicians

c) 25 General practitioners

2. Pharmacist:

a) 100 registered pharmacists

Methodology

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 40

AL -AMEEN COLLEGE OF PHARMACY, BANGALORE-27

DEPARTMENT OF PHARMA MARKETING AND MANAGEMENT

QUESTIONNAIRE FOR DOCTOR

Q.1. How many patients with hypertension do you treat on average per week?

A. MALES:

a) Less than 10 (b) 11 to 15 (c) 16 to 20 (d) 21 to 30 (e) more than 30

B. FEMALES:

a) Less than 10 (b) 11 to 15 (c) 16 to 20 (d) 21 to 30 (e) more than 30

Q.2. Which age-group of patients are more prone to hypertension?

Sex of patient

Age group of patients in years

Female

Less than 35

36 to 45

46 to 55

More than 55

Methodology

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 41

Male

Less than 35

36 to 45

46 to 55

More than 55

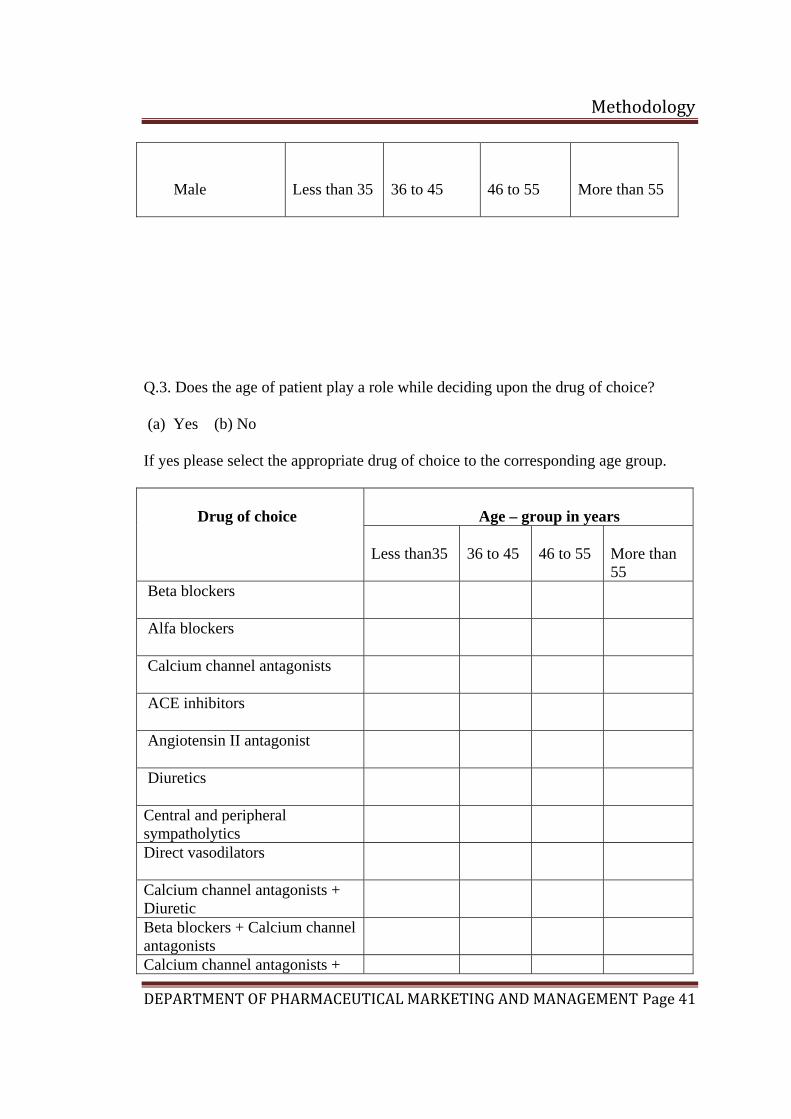

Q.3. Does the age of patient play a role while deciding upon the drug of choice?

(a) Yes (b) No

If yes please select the appropriate drug of choice to the corresponding age group.

Age – group in years

Drug of choice

Less than35

36 to 45

46 to 55

More than 55

Beta blockers

Alfa blockers

Calcium channel antagonists

ACE inhibitors

Angiotensin II antagonist

Diuretics

Central and peripheral sympatholytics

Direct vasodilators

Calcium channel antagonists + Diuretic

Beta blockers + Calcium channel antagonists

Calcium channel antagonists +

Methodology

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 42

ACE inhibitors Diuretic + ACE inhibitors

Calcium channel antagonists + Angiotensin II antagonist

Angiotensin II antagonist + Diuretic

Alfa blockers + Diuretic

Angiotensin II antagonist + ACE inhibitors

Beta blockers + Diuretic

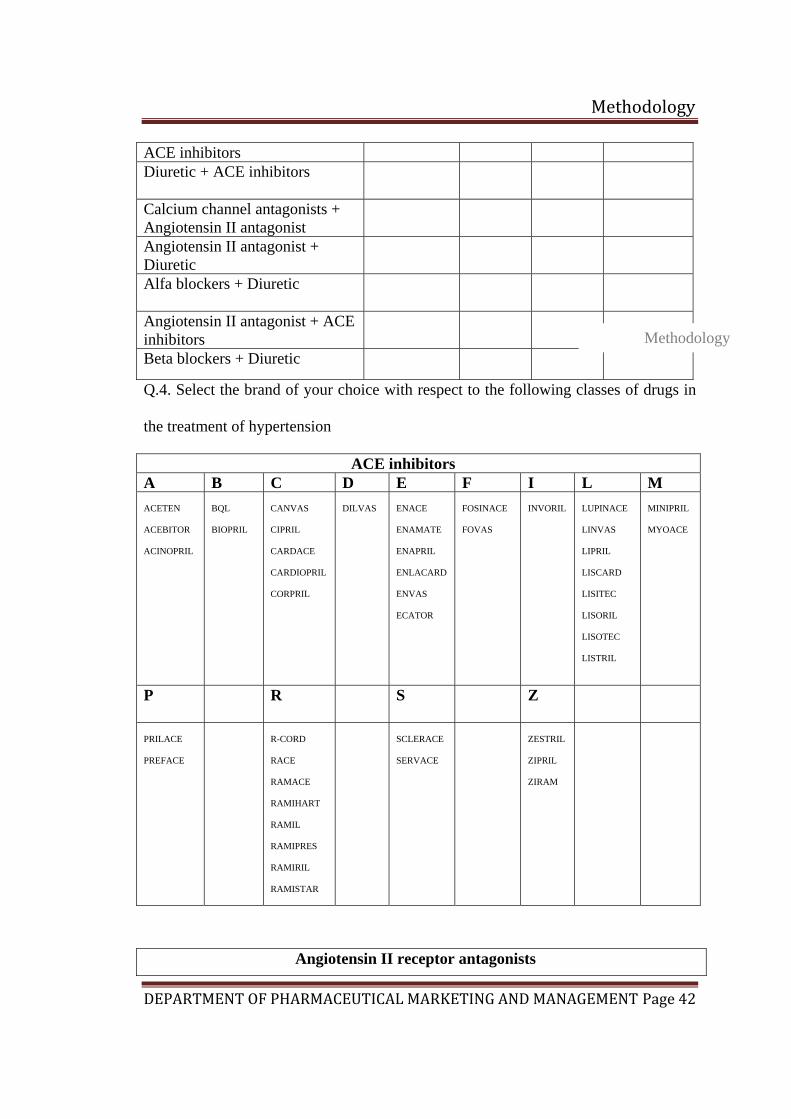

Q.4. Select the brand of your choice with respect to the following classes of drugs in

the treatment of hypertension

ACE inhibitors A B C D E F I L M ACETEN ACEBITOR ACINOPRIL

BQL BIOPRIL

CANVAS CIPRIL CARDACE CARDIOPRIL CORPRIL

DILVAS

ENACE ENAMATE ENAPRIL ENLACARD ENVAS ECATOR

FOSINACE FOVAS

INVORIL

LUPINACE LINVAS LIPRIL LISCARD LISITEC LISORIL LISOTEC LISTRIL

MINIPRIL MYOACE

P R S Z

PRILACE PREFACE

R-CORD RACE RAMACE RAMIHART RAMIL RAMIPRES RAMIRIL RAMISTAR

SCLERACE SERVACE

ZESTRIL ZIPRIL ZIRAM

Angiotensin II receptor antagonists

Methodology

Methodology

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 43

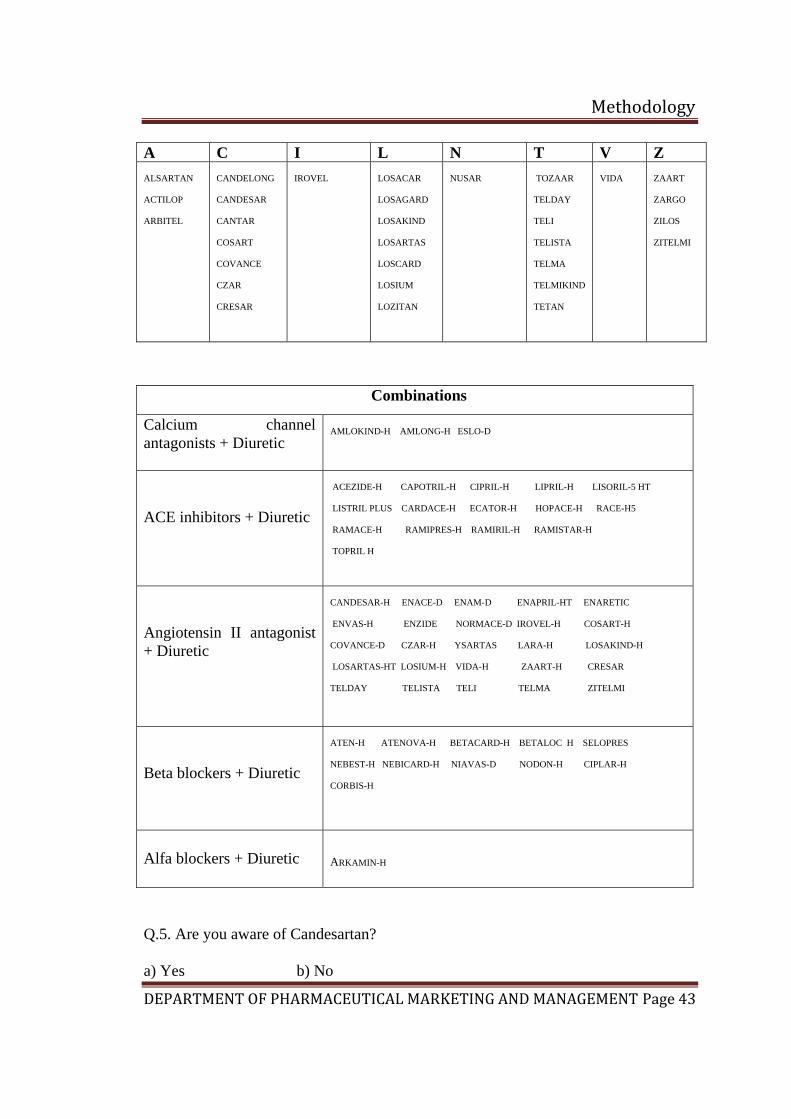

A C I L N T V Z ALSARTAN ACTILOP ARBITEL

CANDELONG CANDESAR CANTAR COSART COVANCE CZAR CRESAR

IROVEL

LOSACAR LOSAGARD LOSAKIND LOSARTAS LOSCARD LOSIUM LOZITAN

NUSAR

TOZAAR TELDAY TELI TELISTA TELMA TELMIKIND TETAN

VIDA

ZAART ZARGO ZILOS ZITELMI

Combinations

Calcium channel antagonists + Diuretic

AMLOKIND-H AMLONG-H ESLO-D

ACE inhibitors + Diuretic

ACEZIDE-H CAPOTRIL-H CIPRIL-H LIPRIL-H LISORIL-5 HT LISTRIL PLUS CARDACE-H ECATOR-H HOPACE-H RACE-H5 RAMACE-H RAMIPRES-H RAMIRIL-H RAMISTAR-H TOPRIL H

Angiotensin II antagonist + Diuretic

CANDESAR-H ENACE-D ENAM-D ENAPRIL-HT ENARETIC ENVAS-H ENZIDE NORMACE-D IROVEL-H COSART-H COVANCE-D CZAR-H YSARTAS LARA-H LOSAKIND-H LOSARTAS-HT LOSIUM-H VIDA-H ZAART-H CRESAR TELDAY TELISTA TELI TELMA ZITELMI

Beta blockers + Diuretic

ATEN-H ATENOVA-H BETACARD-H BETALOC H SELOPRES NEBEST-H NEBICARD-H NIAVAS-D NODON-H CIPLAR-H CORBIS-H

Alfa blockers + Diuretic

ARKAMIN-H

Q.5. Are you aware of Candesartan?

a) Yes b) No

Methodology

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 44

Please give opinion

………………………………………………………………………………………

Q.6. Are you aware of Candesartan Cilexetil?

a) Yes b) No

Please mention what you know about the molecule

………………………………………………………………………………………..

Q.7. Are you aware of Candesartan cilexetil with Hydrochlorthiazide?

a) Yes b) No

Please give your opinion

…………………………………………………………………………………………

Q.8. If a new brand of candesartan cilexetil with hydrochlorthiazide is launched in the

market, what is the single factor you expect in it to support the brand

a) Less costly

b) Reputation of the company

c) Better availability

d) Frequent visits by marketing people

e) Better and more technical information

f) Adequate physician samples to be tried on patients

g) Company sponsored CME programmes

Methodology

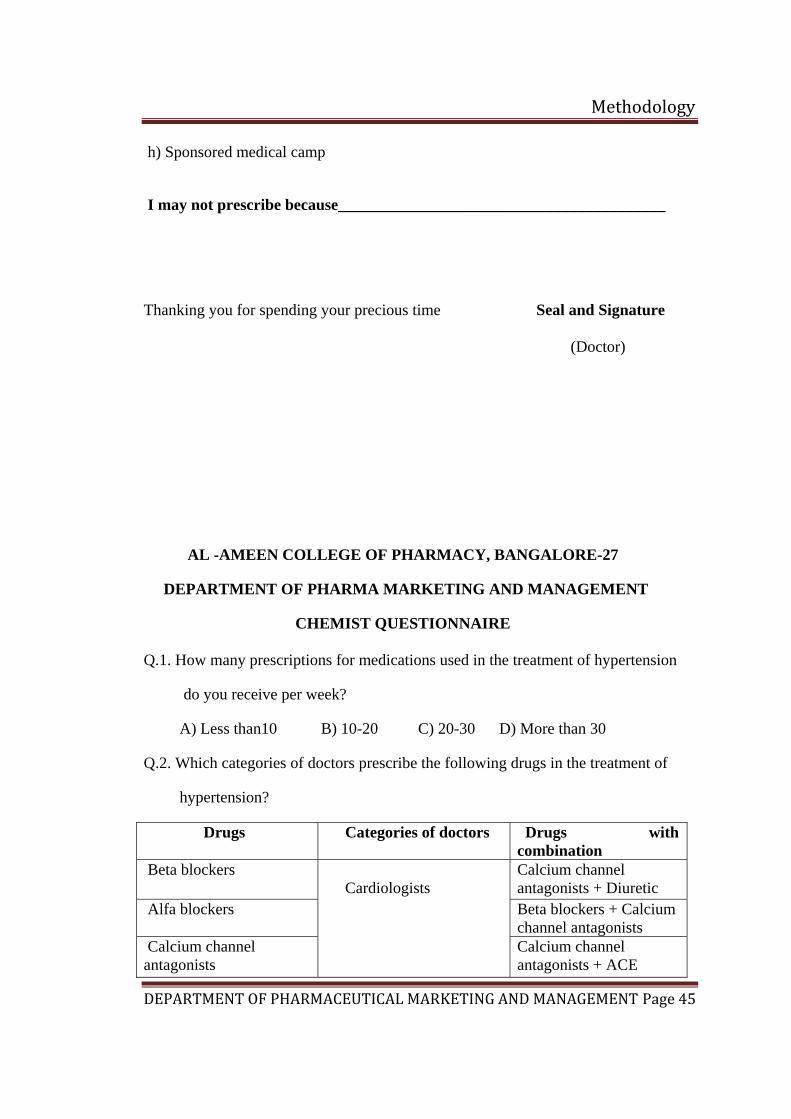

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 45

h) Sponsored medical camp

I may not prescribe because_________________________________________

Thanking you for spending your precious time Seal and Signature

(Doctor)

AL -AMEEN COLLEGE OF PHARMACY, BANGALORE-27

DEPARTMENT OF PHARMA MARKETING AND MANAGEMENT

CHEMIST QUESTIONNAIRE

Q.1. How many prescriptions for medications used in the treatment of hypertension

do you receive per week?

A) Less than10 B) 10-20 C) 20-30 D) More than 30

Q.2. Which categories of doctors prescribe the following drugs in the treatment of

hypertension?

Drugs Categories of doctors Drugs with combination

Beta blockers Calcium channel antagonists + Diuretic

Alfa blockers Beta blockers + Calcium channel antagonists

Calcium channel antagonists

Cardiologists

Calcium channel antagonists + ACE

Methodology

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 46

inhibitors

ACE inhibitors Diuretic + ACE inhibitors

Angiotensin II antagonis Calcium channel antagonists + Angiotensin II antagonist

Diuretics

General physicians

Angiotensin II antagonist + Diuretic

Central and peripheral sympatholytics

Alfa blockers + Diuretic

Angiotensin II antagonist + ACE inhibitors

Direct vasodilators

General practitioners

Beta blockers + Diuretic

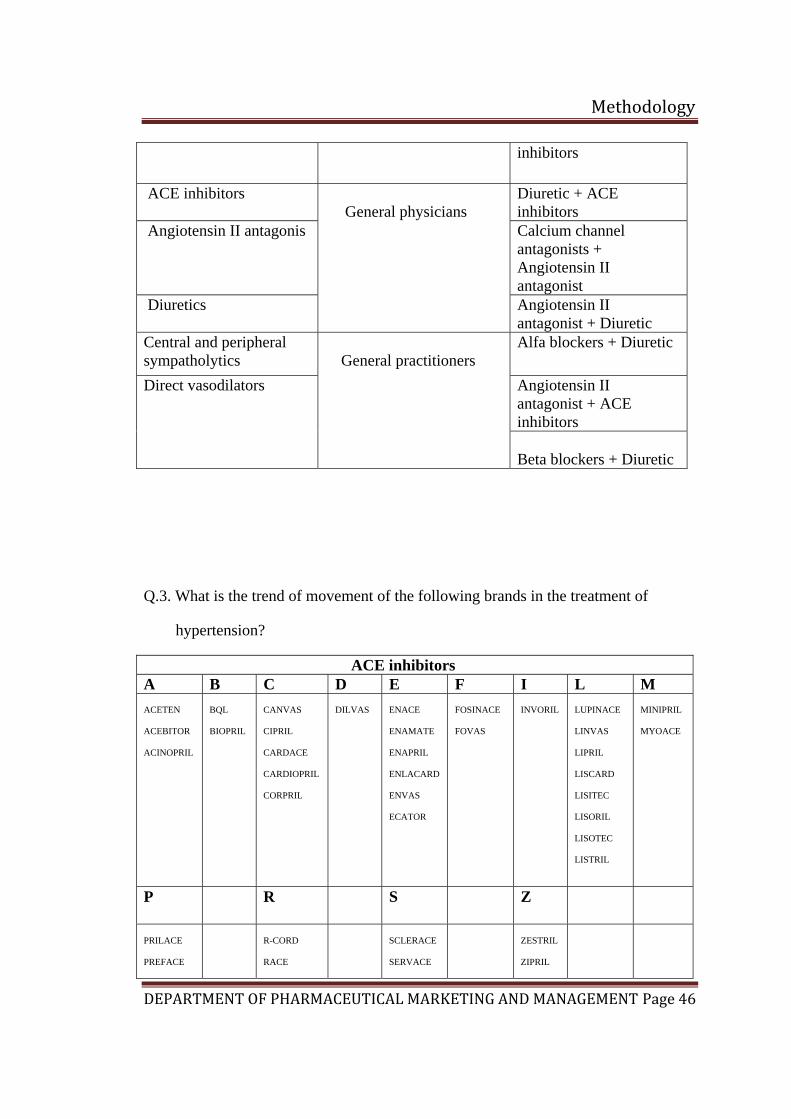

Q.3. What is the trend of movement of the following brands in the treatment of

hypertension?

ACE inhibitors A B C D E F I L M ACETEN ACEBITOR ACINOPRIL

BQL BIOPRIL

CANVAS CIPRIL CARDACE CARDIOPRIL CORPRIL

DILVAS

ENACE ENAMATE ENAPRIL ENLACARD ENVAS ECATOR

FOSINACE FOVAS

INVORIL

LUPINACE LINVAS LIPRIL LISCARD LISITEC LISORIL LISOTEC LISTRIL

MINIPRIL MYOACE

P R S Z

PRILACE PREFACE

R-CORD RACE

SCLERACE SERVACE

ZESTRIL ZIPRIL

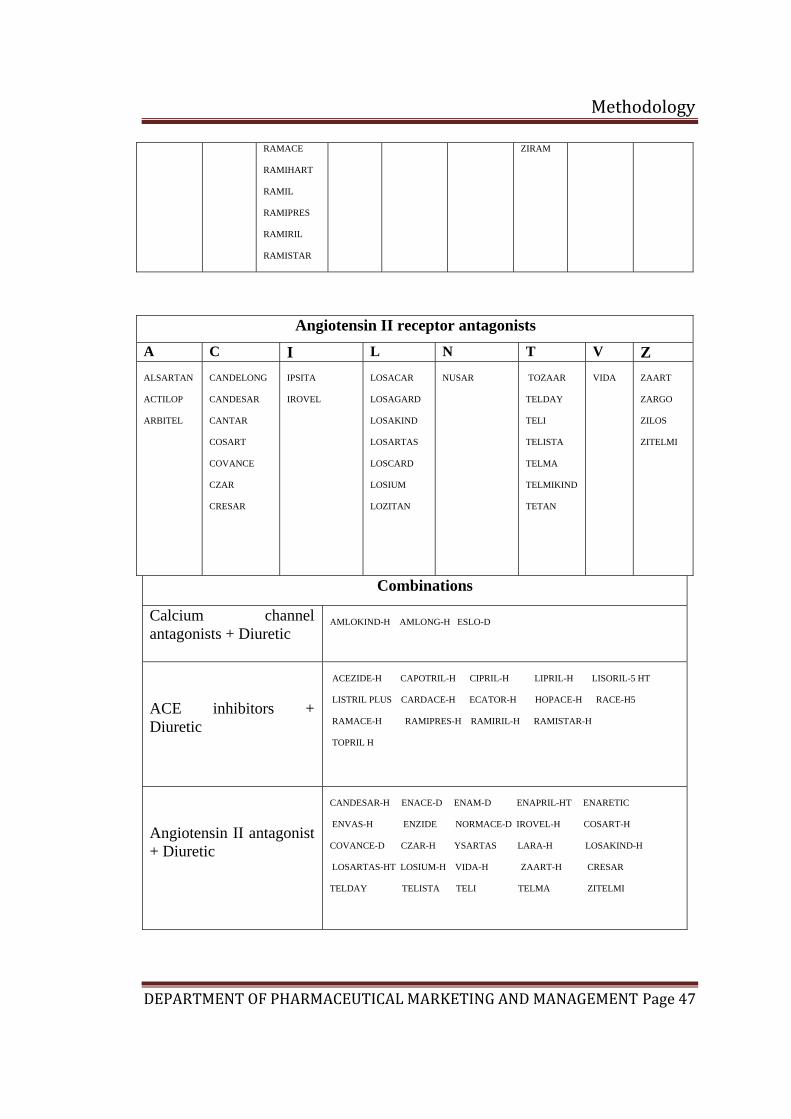

Methodology

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 47

RAMACE RAMIHART RAMIL RAMIPRES RAMIRIL RAMISTAR

ZIRAM

Angiotensin II receptor antagonists A C I L N T V Z ALSARTAN ACTILOP ARBITEL

CANDELONG CANDESAR CANTAR COSART COVANCE CZAR CRESAR

IPSITA IROVEL

LOSACAR LOSAGARD LOSAKIND LOSARTAS LOSCARD LOSIUM LOZITAN

NUSAR

TOZAAR TELDAY TELI TELISTA TELMA TELMIKIND TETAN

VIDA

ZAART ZARGO ZILOS ZITELMI

Combinations

Calcium channel antagonists + Diuretic

AMLOKIND-H AMLONG-H ESLO-D

ACE inhibitors + Diuretic

ACEZIDE-H CAPOTRIL-H CIPRIL-H LIPRIL-H LISORIL-5 HT LISTRIL PLUS CARDACE-H ECATOR-H HOPACE-H RACE-H5 RAMACE-H RAMIPRES-H RAMIRIL-H RAMISTAR-H TOPRIL H

Angiotensin II antagonist + Diuretic

CANDESAR-H ENACE-D ENAM-D ENAPRIL-HT ENARETIC ENVAS-H ENZIDE NORMACE-D IROVEL-H COSART-H COVANCE-D CZAR-H YSARTAS LARA-H LOSAKIND-H LOSARTAS-HT LOSIUM-H VIDA-H ZAART-H CRESAR TELDAY TELISTA TELI TELMA ZITELMI

Methodology

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 48

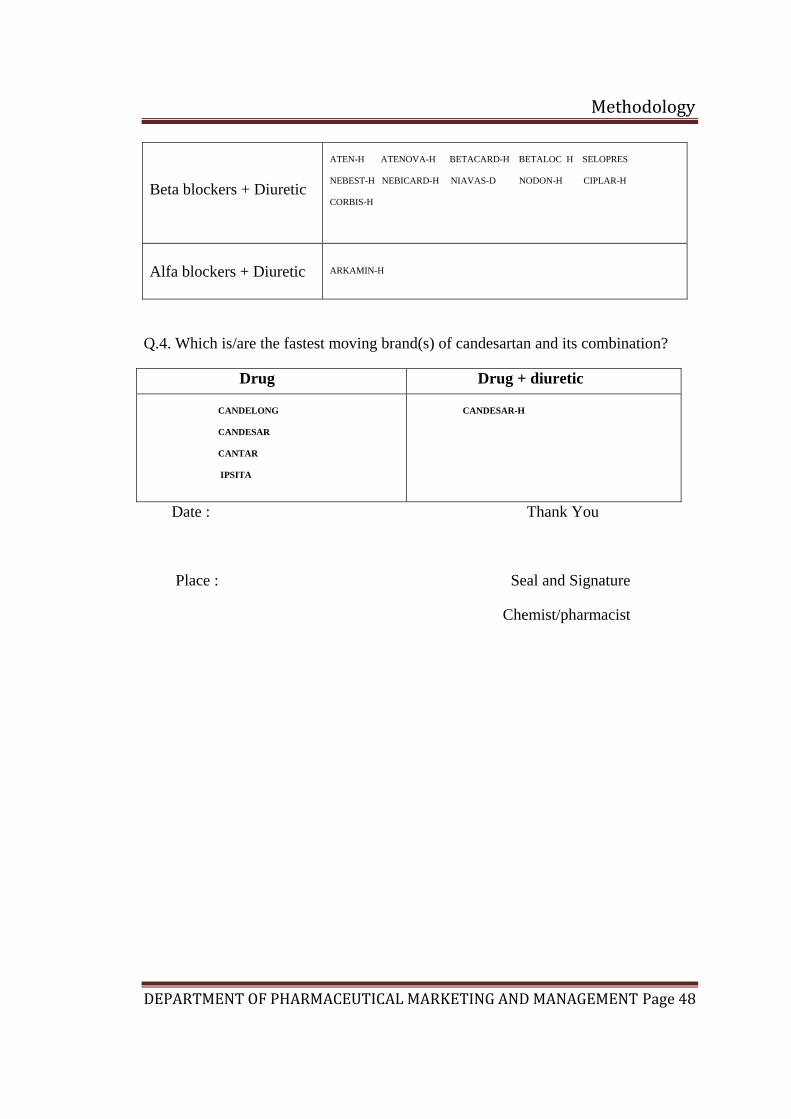

Beta blockers + Diuretic

ATEN-H ATENOVA-H BETACARD-H BETALOC H SELOPRES NEBEST-H NEBICARD-H NIAVAS-D NODON-H CIPLAR-H CORBIS-H

Alfa blockers + Diuretic

ARKAMIN-H

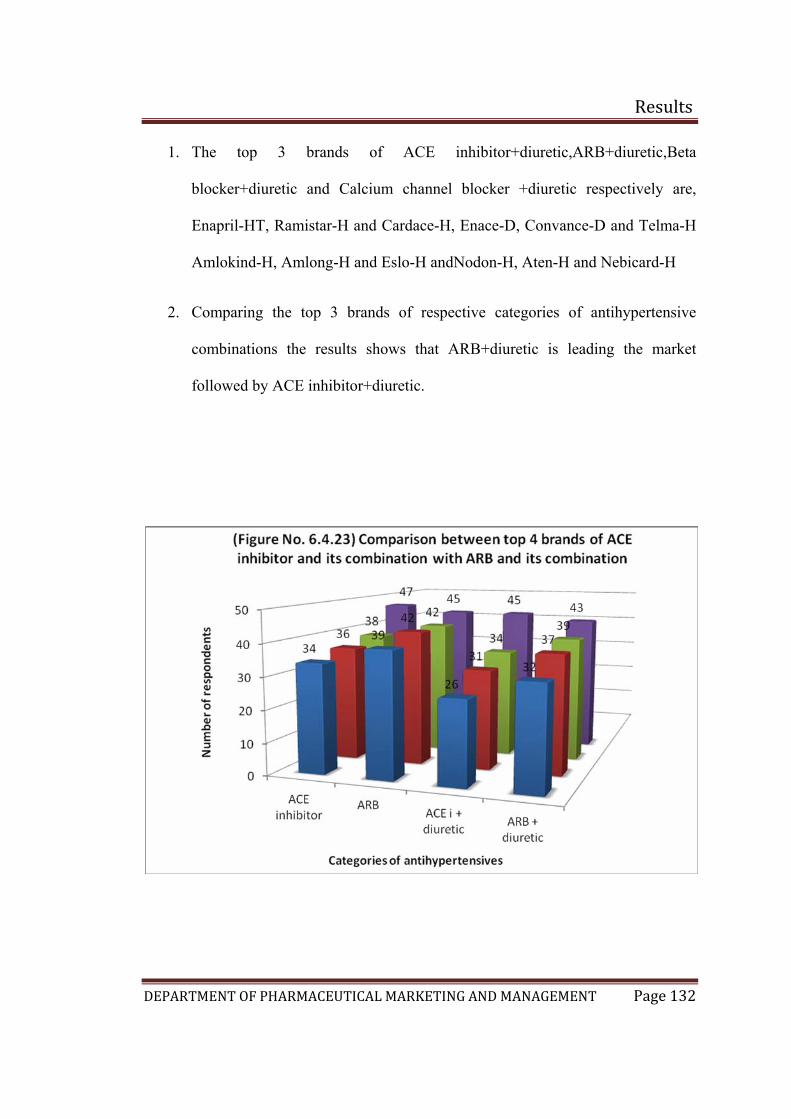

Q.4. Which is/are the fastest moving brand(s) of candesartan and its combination?

Drug Drug + diuretic CANDELONG CANDESAR CANTAR IPSITA

CANDESAR-H

Date : Thank You

Place : Seal and Signature

Chemist/pharmacist

Results

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 38

6. RESULTS

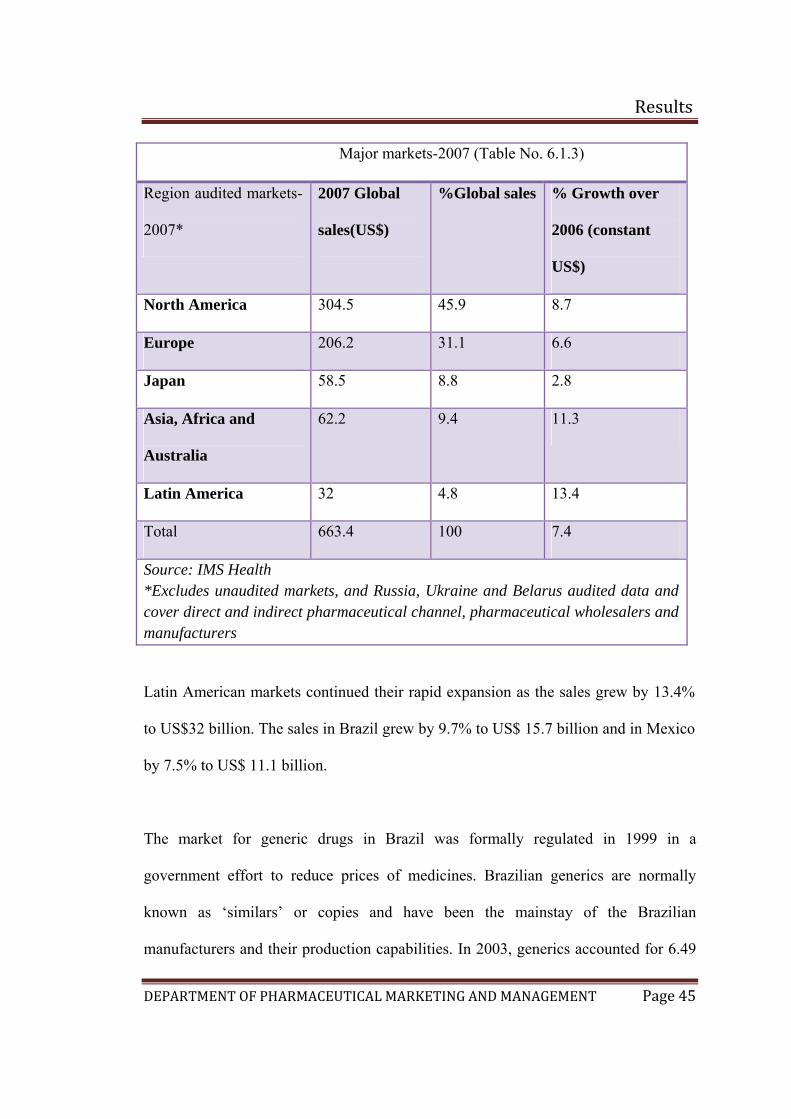

6.1 Country analysis: (Secondary data)

Brazil (18)(19)(20)(23)

Brazil became an independent nation in 1822 after three centuries under the rule of

Portugal. It has pursued industrial and agricultural growth and development exploiting

vast natural resources and a large labor pool. Today, it is South America's leading

economic power and a regional leader. Being the largest and most populous country

in South America, Brazil continues to feel the pressure from highly unequal income

distribution. Brazil is located in the eastern part of South America, bordering the

Atlantic Ocean, spreading across 8,511,965 sq km. It shares common borders with

every South American country except Chile and Ecuador. Brazilian climate can be

described as tropical, but temperate in southern part. It is rich with natural resources

like bauxite, gold, iron ore, manganese, nickel, phosphates, platinum, tin, uranium,

petroleum, hydropower and timber.

Results

DEPARTMENT OF PHARMACEUTICAL MARKETING AND MANAGEMENT Page 39

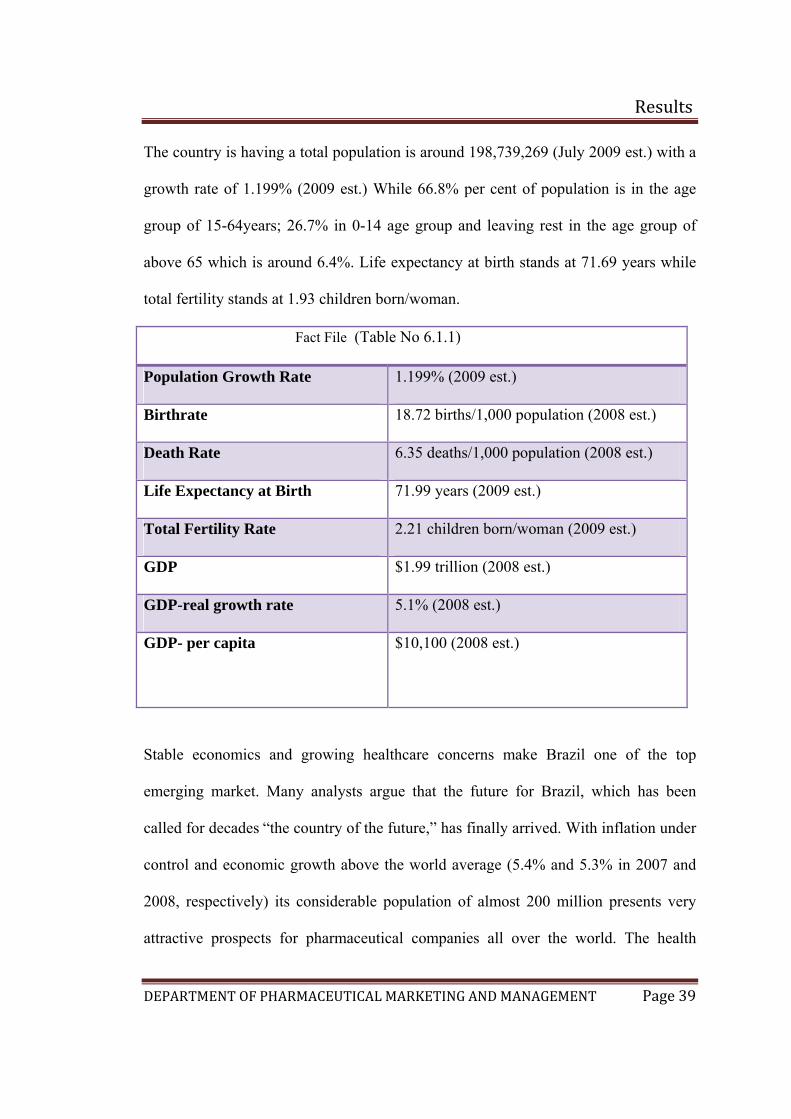

The country is having a total population is around 198,739,269 (July 2009 est.) with a

growth rate of 1.199% (2009 est.) While 66.8% per cent of population is in the age

group of 15-64years; 26.7% in 0-14 age group and leaving rest in the age group of

above 65 which is around 6.4%. Life expectancy at birth stands at 71.69 years while

total fertility stands at 1.93 children born/woman.

Fact File (Table No 6.1.1)

Population Growth Rate 1.199% (2009 est.)

Birthrate 18.72 births/1,000 population (2008 est.)

Death Rate 6.35 deaths/1,000 population (2008 est.)

Life Expectancy at Birth 71.99 years (2009 est.)

Total Fertility Rate 2.21 children born/woman (2009 est.)

GDP $1.99 trillion (2008 est.)

GDP-real growth rate 5.1% (2008 est.)

GDP- per capita $10,100 (2008 est.)

Stable economics and growing healthcare concerns make Brazil one of the top

emerging market. Many analysts argue that the future for Brazil, which has been

called for decades “the country of the future,” has finally arrived. With inflation under

control and economic growth above the world average (5.4% and 5.3% in 2007 and

2008, respectively) its considerable population of almost 200 million presents very