1|V

• The40-year-oldglobalwarehouseclubsectorisestimatedtogenerateapproximately$191billioninrevenuesin2017.

• Theclubs’businessmodelseekstolimitgrossprofitssoastoofferlowpricestomemberswhilegeneratingprofitsforshareholdersthroughreasonablemembershipfees.

• ThemajorityoftheclubsarelocatedintheUS,whichaccountedfornearlythree-quartersofsectorrevenuesin2016.Themarketisdominatedbythreecompanies:BJ’sWholesaleClub,CostcoWholesaleandSam’sClub(adivisionofWalmart).

• TheUSwarehouseclubsectorgrewata7.2%CAGRfrom2001through2016.ItsgrowthrateoutpacedthatofthetotalUSretailindustryby3.3percentagepointsovertheperiod.Theinternationalmarketgrewatanevenbrisker10.8%CAGR.

• Yetthesector’sgrowthrateslowedoverthesameperiod,actuallyhittingzeroin2015.AndresearchersareforecastingthattheUSsegmentwillgrowata2.4%CAGR,morethan1.5pointslowerthanoverallretail,from2016through2020.

• Thespoilerbehindthesector’sdeceleratinggrowthratehaslikelybeene-commerce,whichtheclubshavebeenslowtoembrace.Warehouseclubscurrentlygenerate4%orlessoftheirrevenuesfrome-commerce.

• Asisthecasewithmanyotherretailers,warehouseclubsneedtodevelopastrategytocompetewithe-commerceplayers,aswellasleveragetheiruniquestrengthstoadapttootherdemographicandtechnologicalchanges.

InPartTwoofthisDeepDive,weprovideanoverviewofthewarehouse-clubsector.

June 5, 2017

V

2

June5,2017

vV

V|DeepDive:WarehouseClubStores

V

ExecutiveSummary..............................................................................................................................3WarehouseClubCompaniesataGlance...............................................................................................5WarehouseClubAdvantages................................................................................................................6EconomiesofScaleMaximizeEfficiency...............................................................................................6ExpandedProductMixAttractsShoppers.............................................................................................7Value,TreasureHuntandOrganicsAppealtoConsumers.....................................................................8IntheSweetSpotoftheWeinswigRetailHourglass.............................................................................9WarehouseClubChallenges...............................................................................................................11GenerationalandDemographicChangesinShopperPreferences.......................................................11E-Commerce.......................................................................................................................................12AmazonEverywhere..........................................................................................................................13Conclusion………………………………………………………………………………………………………………………………………...13

Table of Contents

3|V

1

1

Warehouseclubstoreshavehadagreatruninthe40yearssince1976,whenSolPricefoundedthefirstPriceClub,whichultimatelybecametoday’sCostco.Theclubswereinitiallyopenonlytobusinesscustomers,butlaterallowedemployeesofnonprofitandgovernmentorganizationstojoin,andeventuallyopenedtothepublic.Theclubshadauniquebusinessmodel—limitingprofitabilitysoastopassthesavingsontocustomersandmakingthebulkoftheirprofitsfrommembershipfees.Customerslovetheclubs’lowprices,theabilitytobuyinenormousquantitiesandthedelightoffindingunexpectedbargainsintreasurehuntsthroughoutthestores.Therearenotmanystoresinwhichcustomerscanpurchasea20lb.packageofsteaks,aflat-panelTVandadiamondengagementringallinonetrip.

Thewarehouseclubshavesuccessfullyleveragedpostwardemographics,generallysituatingthemselvesinsuburbanareaswithhighmedianincomesandmanysmallbusinessestoserve,offeringconsumersinthoseareastheconveniencetheyneed.Whileshoppersinsuchareastendtobeaffluent,everybodylovesabargain,somanywell-offconsumersshopthewarehouseclubsalongwiththeirmoreprice-consciousneighbors.

Executive Summary

4

June5,2017

vV

V|DeepDive:WarehouseClubStores

V

22

Theclubs’popularityhasshownupintheirfinancials.From2001through2016,USwarehouseclubrevenuesgrewataCAGRof6.2%,outpacingthe3.0%annualgrowthrateoftheoverallretailindustrybymorethanthreepercentagepoints.Thesector’sgrowthoutsidetheUSwasevenmorebriskoverthesameperiod,averaging10.8%.Profitabilitydidnotsuffer,either.Despitetheclubs’vowtolimitgrossmarginsinordertoofferattractiveprices,thetopthreeUSwarehouseclubsgenerallyhaveseenoperatingmarginsofaround2%–4%.

Despitethisprosperity,growthhasslowedoverthepast15years,andglobalgrowthgroundtonearzeroin2015,makingitaninflectionpoint.Now,theUSsegmentisforecasttogrowannuallyatabout2.4%,lessthanhalfapointhigherthanthetotalretailindustry.Theslowdowncanbeattributedtochangesindemographicsandthewayspeopleshopand,ofcourse,tothesteadygrowthandencroachmentofe-commerce.In2016,e-commerceaccountedfor8.1%ofUSretailandgrewby15.1%yearoveryear.

Whatshouldthewarehouseclubsdotorecapturetheirpreviousappealtoconsumersandreignitethegrowthratesofyearspast?Clearly,e-commerceispartoftheanswer.Amongthemajorwarehouseclubs,e-commerce’sshareofsalesislikelyhighestatCostco,wherethechannelaccountsfor4%ofrevenues.Oneshort-livedbutinterestingplayerinthee-commercefieldwasJet.com,whichWalmartacquiredin2016.Jetattemptedtocombinethelowpricesofwarehouseclubswiththeconvenienceandeaseofe-commerceandm-commerce.Thecompanyalsoimplementedsomeinnovativewaystoreduceshippingcosts.

Thewarehouseclubsneedtoleveragetheiruniquestrengths,whichincludeprovidinghigh-qualitygoodsatlowpricesandprovidingcustomerswithatreasurehuntexperience,aswellasofferingstrongprivate-labelbrands.Costco’sKirklandSignatureprivatelabelaccountsforaboutone-quarterofthecompany’ssales,makingita$30billionbrand.KirklandSignatureproductsareavailableonAmazon.comandJet.com,andthelabelisarguablyamajorinternationalbrandinitsownright.

WarehouseclubsalsoneedtoadapttothechangingdemographicpatternsofAmericansuburbanlife.Membersofyoungergenerationsareincreasinglylivingincitiesratherthaninsuburbs.Inurbanareas,livingspaceandstorageareatapremium,andmanyurbandwellersdonotownavehiclethattheycandrivetoawarehouseclubandfillwithlarge,bulkypurchases.Tomeettheseconsumers’needs,warehouseclubsshouldexploreofferingmoreoftheirgoodsinsmallerquantitiesonlineandalsoexploredeliverymethodsthate-commercecompaniesareusing,suchasclick-and-collectandexpeditedshipping.

Inthisdeep-divereport,weofferanoverviewofthewarehouseclubsector,analyzethekeyfactorsthatareinfluencingthesectorandprofilethemajorplayers,aswellasprovidesuggestionsonwhatwarehouseclubscandotorecapturethestronggrowththeysawinpreviousperiods.

5|V

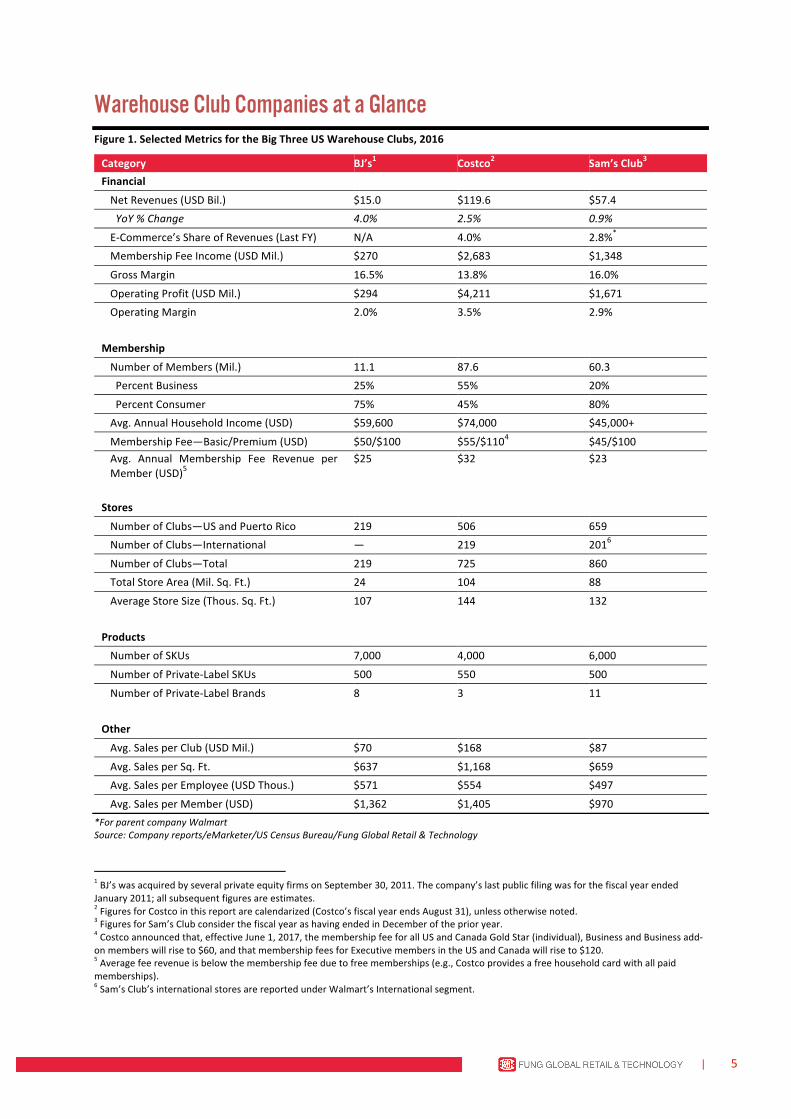

Warehouse Club Companies at a Glance

Figure1.SelectedMetricsfortheBigThreeUSWarehouseClubs,2016

Category BJ’s1 Costco2 Sam’sClub3Financial NetRevenues(USDBil.) $15.0 $119.6 $57.4YoY%Change 4.0% 2.5% 0.9%

E-Commerce’sShareofRevenues(LastFY) N/A 4.0% 2.8%*MembershipFeeIncome(USDMil.) $270 $2,683 $1,348

GrossMargin 16.5% 13.8% 16.0%

OperatingProfit(USDMil.) $294 $4,211 $1,671OperatingMargin 2.0% 3.5% 2.9%

Membership NumberofMembers(Mil.) 11.1 87.6 60.3PercentBusiness 25% 55% 20%

PercentConsumer 75% 45% 80%Avg.AnnualHouseholdIncome(USD) $59,600 $74,000 $45,000+

MembershipFee—Basic/Premium(USD) $50/$100 $55/$1104 $45/$100Avg. Annual Membership Fee Revenue perMember(USD)5

$25 $32 $23

Stores NumberofClubs—USandPuertoRico 219 506 659NumberofClubs—International — 219 2016

NumberofClubs—Total 219 725 860TotalStoreArea(Mil.Sq.Ft.) 24 104 88

AverageStoreSize(Thous.Sq.Ft.) 107 144 132

Products NumberofSKUs 7,000 4,000 6,000

NumberofPrivate-LabelSKUs 500 550 500

NumberofPrivate-LabelBrands 8 3 11

Other Avg.SalesperClub(USDMil.) $70 $168 $87

Avg.SalesperSq.Ft. $637 $1,168 $659Avg.SalesperEmployee(USDThous.) $571 $554 $497

Avg.SalesperMember(USD) $1,362 $1,405 $970*ForparentcompanyWalmartSource:Companyreports/eMarketer/USCensusBureau/FungGlobalRetail&Technology

1BJ’swasacquiredbyseveralprivateequityfirmsonSeptember30,2011.Thecompany’slastpublicfilingwasforthefiscalyearendedJanuary2011;allsubsequentfiguresareestimates.2FiguresforCostcointhisreportarecalendarized(Costco’sfiscalyearendsAugust31),unlessotherwisenoted.3FiguresforSam’sClubconsiderthefiscalyearashavingendedinDecemberoftheprioryear.4Costcoannouncedthat,effectiveJune1,2017,themembershipfeeforallUSandCanadaGoldStar(individual),BusinessandBusinessadd-onmemberswillriseto$60,andthatmembershipfeesforExecutivemembersintheUSandCanadawillriseto$120.5Averagefeerevenueisbelowthemembershipfeeduetofreememberships(e.g.,Costcoprovidesafreehouseholdcardwithallpaidmemberships).6Sam’sClub’sinternationalstoresarereportedunderWalmart’sInternationalsegment.

6

June5,2017

vV

V|DeepDive:WarehouseClubStores

V

EconomiesofScaleMaximizeEfficiencyWarehouseclubsoffermembersthelowestpossibleretailprices,sometimesreachingwholesalelevels.Alargemembershipbaseenablestheclubstopurchaselargevolumesatlowcost.Beyondthat,limitingthenumberofSKUstheypurchasetojust4,000–8,000enableswarehouseclubstopurchaseevenlargervolumesinfewercategories,whichhelpsthemmaintainacapongrossmarginsonbehalfoftheircustomers.Inthisway,thesectorachieveseconomiesofscalethatcompetitorsinotherretailformats—includingthemassmerchandise,discount,consumerelectronicsandsupermarketformats—cannoteasilyachieve,giventheirlargerofferingsof25,000–100,000SKUs.Inmanycategories,consumerscanfindsubstantialsavingsatwarehouseclubs.Comparedwithpricesatlocalgrocers,forexample,theaveragesavingscanbe65%ormore.

Alimitedmerchandiseselectionalsoenablestheclubstomaximizeefficiencyinproductdistribution,handling,stockingandmerchandising.FewerSKUsdrivesuperiorinventoryturns,too.Sincethenarrowchoiceleadstosalesofwhatisavailable,aslongastheitemsaredesirable,thosesalesdriveinventoryturns.Whiletheclubs’actualgrossmargindollarsmaybebelowthoseofmassmerchantsorsupermarkets,greaterturnsgeneratemoreingrossmargindollarsperSKU.

Warehouse Club Advantages

Warehouseclubsoffermembersthelowestpossibleretailprices,sometimesreachingwholesalelevels.Alargemembershipbaseenablestheclubstopurchaselargevolumesatlowcost.Beyondthat,limitingthenumberofSKUstheypurchasetojust4,000–8,000enableswarehouseclubstopurchaseevenlargervolumesinfewercategories,whichhelpsthemmaintainacapongrossmarginsonbehalfoftheircustomers.

7|V

ExpandedProductMixAttractsShoppersWhilesellingnationalbrands(inbothfoodandnonfoodcategories)atverylowpricesistheclubs’valueproposition,thechainsareincreasinglysellingprivate-labelproductsandaddingbusinesses,suchasgasfillingstations,pharmacies,automaintenanceservicesandopticalcenters.

ThefigurebelowshowsthatCostco’srevenuesharebycategoryhasremainedfairlyconstantduringthepastfiveyears,thoughfoods,freshfoodsandsoftlinegoodshaveexperiencedslightincreases.Together,foodsandfreshfoodsrepresentmorethanone-thirdofCostco’srevenues.

Figure2.CostcoRevenueBreakdown,byCategory

Source:Companyreports

21% 21% 22% 22% 22%

13% 13% 13% 14% 14%

22% 22% 21% 21% 21%

16% 16% 16% 16% 16%

10% 11% 11% 11% 12%

18% 17% 17% 16% 15%

FY12 FY13 FY14 FY15 FY16

Foods FreshFoods Sundries Hardlines Sonlines Other

Costco’srevenuesharebycategoryhasremainedfairlyconstantduringthepastfiveyears,thoughfoods,freshfoodsandsoftlinegoodshaveexperiencedslightincreases.Together,foodsandfreshfoodsrepresentmorethanone-thirdofCostco’srevenues.

8

June5,2017

vV

V|DeepDive:WarehouseClubStores

V

Value,TreasureHuntandOrganicsAppealtoConsumersWarehouseclubsappealtoconsumersonanumberoffrontsasidefromofferingvalue.Theyalsoofferashoppingexperiencethathasatreasurehuntaspect,ascertainitemsmaybeavailableonlyduringasinglevisit,ratherthaneverytimeashoppervisitsthestore.Inaddition,theclubsappealtotheirmembersbyofferingarangeoforganicitems,whichhavegrowninpopularityoverrecentyears.

Thebargain:Warehouseclubmembersenjoyknowingtheyaregettingthebestdealpossible.Theno-frillsshoppingenvironmentoftheclubs,alongwiththeirlackofadvertising,communicatesthevaluepropositiontomembers—nounnecessaryexpenditureswillthreatenthesavingspassedalongtomembers.(Multivendormailerspaidforbywarehouseclubsareusedformarketing,buttheseoftencontaincouponsthatmakethedealsevenbetter.)

Littleluxuriesandbigluxuries:Frugalwarehouseclubshoppersstillwantluxuries,andtheclubformatoffersthoseatverycompetitiveprices.Thecombinationofhigh-endandlow-endproductsmakeswarehouseclubsevenmoreofadestinationforshopping.AstheWeinswigRetailHourglassmodelbelowillustrates,high-andlow-endretailersareenjoyingsuccess,whilethoseinthemidmarketarenotfaringaswell.Warehouseclubmemberscanaffordtosplurgeonafewluxuryitemsbytradingdownonotheritemsintheirshoppingcart.

Thetreasurehunt:Asteadyflowofhigh-end,uniquemerchandiseisaconstantatwarehouseclubs,creatingatreasure-huntexperienceforshoppers.Thismerchandisingstrategyincludesa“buyitnow”factor,asaproductmaynotbeinstockonthemember’snextvisit.Moreover,savingmoneybyshoppinginawarehousecluballowsconsumerstojustifytherewardofavalue-pricedtreasure.TreasuresatCostcoincludeachangingassortmentoffinejewelryandthePolishStonewarecollectioninhousewares.AtSam’sClub,aKitchenAidgrillwasrecentlyofferedata30%discounttoitsoriginal,$1,299.99pricetag.About25%ofCostco’srevenuesderivefromtreasure-huntitems,accordingtoarecentForbesarticle.

Organics:Warehouseclubspridethemselvesondiscoveringnewitemsthatwillinteresttheiraffluentmembershipandgeneratesales.“Organic”isthenewbuzzwordinfoodandhealthandbeautyaidsand,forwarehousecluboperators,organicsrepresenttheircoresectortenets,combiningqualityandthefunofatreasurehuntwithexclusiveandhard-to-findproducts.Costcomorethandoubleditsnumberoforganicofferingsfrom50afewyearsagotomorethan130in2016.Thecompanyrecentlyexceeded$4billioninannualorganicssales,bypassingWholeFoodsMarkettotakethenumber-onespotintermsoforganicssales.Generally,organicshaveahigherpricepointandhigherprofitmarginthandononorganics,drivinguptheaveragetransactionvalue.

Warehouseclubsappealtoconsumersonanumberoffrontsasidefromofferingvalue.Theyalsoofferashoppingexperiencethathasatreasurehuntaspect,ascertainitemsmaybeavailableonlyduringasinglevisit,ratherthaneverytimeashoppervisitsthestore.

9|V

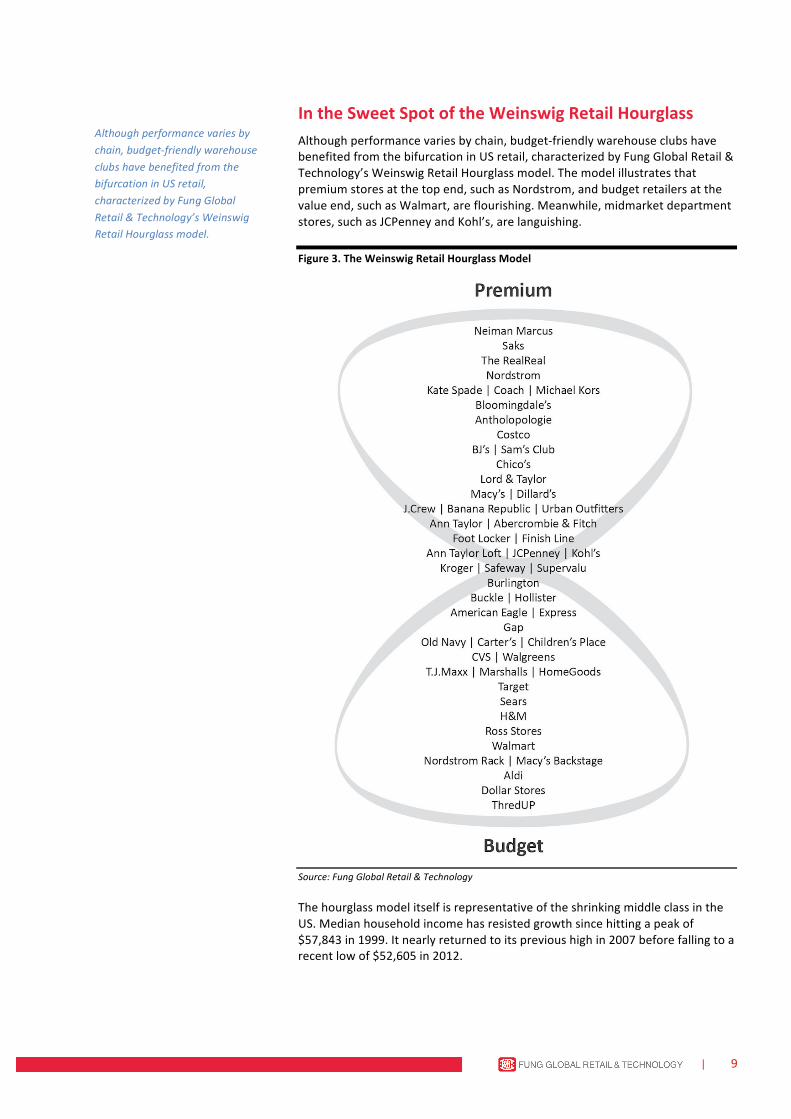

IntheSweetSpotoftheWeinswigRetailHourglassAlthoughperformancevariesbychain,budget-friendlywarehouseclubshavebenefitedfromthebifurcationinUSretail,characterizedbyFungGlobalRetail&Technology’sWeinswigRetailHourglassmodel.Themodelillustratesthatpremiumstoresatthetopend,suchasNordstrom,andbudgetretailersatthevalueend,suchasWalmart,areflourishing.Meanwhile,midmarketdepartmentstores,suchasJCPenneyandKohl’s,arelanguishing.

Figure3.TheWeinswigRetailHourglassModel

Source:FungGlobalRetail&Technology

ThehourglassmodelitselfisrepresentativeoftheshrinkingmiddleclassintheUS.Medianhouseholdincomehasresistedgrowthsincehittingapeakof$57,843in1999.Itnearlyreturnedtoitsprevioushighin2007beforefallingtoarecentlowof$52,605in2012.

Althoughperformancevariesbychain,budget-friendlywarehouseclubshavebenefitedfromthebifurcationinUSretail,characterizedbyFungGlobalRetail&Technology’sWeinswigRetailHourglassmodel.

10

June5,2017

vV

V|DeepDive:WarehouseClubStores

V

Figure4.US:MedianHouseholdIncome(USD)

Source:USCensusBureau

AccordingtothePewResearchCenter,theUSwealth(netassets)gapbetweenupper-incomeandmiddle-incomefamiliesisnowthewidestonrecordsince1983,at6.6times,reflectingnowealthgrowthformiddle-andlower-incomefamilies.Datafrom2012underlinethethree-decadesagaofmiddle-classstagnation.Againstthismacroeconomicbackdrop,itisnosurprisethatthemiddlegroundinUSretailisunderpressure.

Fortunatelyforwarehouseclubs,frugalityhasbecomethenewnormalinthepostrecessionrecovery.Whilethatfrugalitycertainlyplaystothecompetitiveadvantagesofwarehouseclubs,theclubsalsobenefitbytouchingupontheluxuryendoftheWeinswigRetailHourglass,astheyoffersomeluxuryitemsatverycompetitivepricestoindulgecustomers.Theclubs’abilitytoplayatboththehighandlowendsoftheretailmarketispowerful.

$46,000

$48,000

$50,000

$52,000

$54,000

$56,000

$58,000

$60,000

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

MedianIncome 1999Peak

Fortunatelyforwarehouseclubs,frugalityhasbecomethenewnormalinthepostrecessionrecovery.Whilethatfrugalitycertainlyplaystothecompetitiveadvantagesofwarehouseclubs,theclubsalsobenefitbytouchingupontheluxuryendoftheWeinswigRetailHourglass,astheyoffersomeluxuryitemsatverycompetitivepricestoindulgecustomers.

11|V

GenerationalandDemographicChangesinShopperPreferencesMuchhaschangedinretailinthe60-plusyearssinceentrepreneurSolPriceopenedhisveryfirststore,aFedMart,inanairplanehangarinSanDiego,California.Intheinterveningdecades,wehaveseenWalmartrisetoprominence,theadventandexpansionoftheInternetande-commerce,andsignificantchangesindemographicandsocialtrends.TheriseofwarehouseclubstoresseemspredicatedonthesuburbanizationintheUSthatpickedupafterWorldWarII,whichdroveanincreaseinconsumptionandtheconsumereconomy.

Inrecentyears,ithasbecomefashionable,particularlyamongtwentysomethings,tomovebacktourbancenters,whicharecharacterizedbysmallapartmentsratherthanbythelargehousescommoninsuburbs.Theseyoungerconsumersaremorelikelytoshareassets,suchascars,andtousepublictransportation—whichmakestransportingbulkquantitiesofgoodsfromawarehousestoreimpracticalandunwieldy.Moreover,thelowpricesandconvenienceofferedthroughe-commerce,mobilecommerce,andsubscriptionandotherservicesmakeitpossibleforshopperstohavegoodseasilyshippedtotheirhomesnow,eliminatingtheneedtodriveandloadavehicleatawarehousestore.Theseareonlysomeofthechallengesthatwarehouseclubsfaceintermsoffuturegrowth.

Warehouse Club Challenges

Youngerconsumersaremorelikelytoshareassets,suchascars,andtousepublictransportation—whichmakestransportingbulkquantitiesofgoodsfromawarehousestoreimpracticalandunwieldy.

12

June5,2017

vV

V|DeepDive:WarehouseClubStores

V

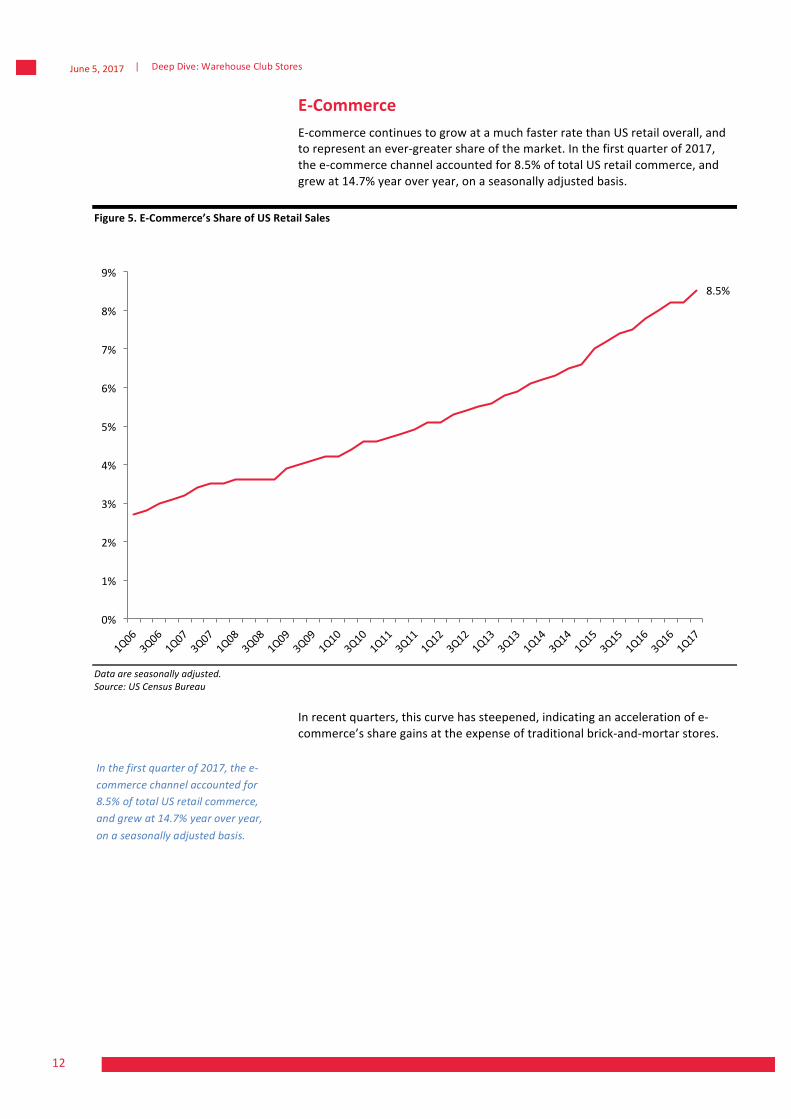

E-CommerceE-commercecontinuestogrowatamuchfasterratethanUSretailoverall,andtorepresentanever-greatershareofthemarket.Inthefirstquarterof2017,thee-commercechannelaccountedfor8.5%oftotalUSretailcommerce,andgrewat14.7%yearoveryear,onaseasonallyadjustedbasis.

Figure5.E-Commerce’sShareofUSRetailSales

Dataareseasonallyadjusted.Source:USCensusBureau

Inrecentquarters,thiscurvehassteepened,indicatinganaccelerationofe-commerce’ssharegainsattheexpenseoftraditionalbrick-and-mortarstores.

8.5%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

Inthefirstquarterof2017,thee-commercechannelaccountedfor8.5%oftotalUSretailcommerce,andgrewat14.7%yearoveryear,onaseasonallyadjustedbasis.

13|V

AmazonEverywhereAmazonisbuildingonitsearlysuccessindisruptingthemarketsforbooksandmediabysteadilycontinuingtomoveintonewproductcategories,includinggroceryandapparel.ThecompanyisuniquelyabletoleveragebothitsITinfrastructure(throughAmazonWebServices)anditscontinuallydevelopingdeliveryinfrastructure,whichservestoreduceitsfulfillmentcostsbutcanalsobeemployedforgrocerydelivery.

Source:Shutterstock

Amazon’sPrimemembershipprogramworkssimilarlytoawarehouseclubmembership:memberspayanannualfeeforaccesstotheprogramanditsbenefits.Amongotherbenefits,AmazonPrimemembersreceivefreetwo-dayshipping,accesstoAmazon’saudioandvideoofferings,accesstofreebooks,andaccesstootherexclusiveservicessuchastheEchoconnectedintelligentdevice,Dashreorderingbuttons,andtheAmazonPrimeNowsmartphoneapp,whichenablesuserstoreceiveone-ortwo-hourdeliveryinselectedcities.

AmazonFreshisagrocerydeliveryservicethatisexclusivetoPrimemembers.Theservicecostsanadditional$14.99amonthontopofAmazonPrime,anddeliveriesarefreeforordersover$40.Memberscanorderfreshproduceandgroceries,includingspecialtiesfromlocalshopsandmarkets,forsame-dayornext-daydelivery,andcanselectatimefordelivery.

Conclusion—PartTwoPartTwoofthereportexaminedtheadvantagesandchallengeswarehouseclubsface.Advantagesincludetheeconomiesofscalewhileprovidingsignificantvaluepricingtocustomersandatreasurehuntshoppingexperiencethatoffersunexpectedsurprisesandbargains.Challengesthewarehouseclubsfaceincludeshiftingshopperpreferencesduetogenerationalanddemographicchanges,thesteadyencroachmentofe-commerce,andAmazon’sentryintomultipleareasofcommerce.

PartThreediscusses10topicsaffectingthewarehouseclubsectorandretailingeneral:thechanginggroceryshopper,e-commerce,mobilecommerce,roboticsinretail,privatelabels,thesourcingrevolution,ancillaryproductsandservices,USmarketsaturation,internationalexpansion,andthebriefindependenceofJet.com.ThereportconcludeswithprofilesofthetopthreeUSwarehouseclubsandananalysisoftheattractivenessofselectedglobalmarkets.

Amazon’sPrimemembershipprogramworkssimilarlytoawarehouseclubmembership:memberspayanannualfeeforaccesstotheprogramanditsbenefits

PartTwoofthereportexaminedtheadvantagesandchallengeswarehouseclubsface.PartThreediscusses10topicsaffectingthewarehouseclubsectorandretailingeneral.

14

June5,2017

vV

V|DeepDive:WarehouseClubStores

V

DeborahWeinswig,CPAManagingDirectorFungGlobalRetail&TechnologyNewYork:917.655.6790HongKong:852.6119.1779China:86.186.1420.3016deborahweinswig@fung1937.comJohnMercerSeniorAnalyst

JohnHarmon,CFASeniorAnalyst

AmyLinResearchAssistant

HongKong:8thFloor,LiFungTower888CheungShaWanRoad,KowloonHongKongTel:85223004406London:242-246MaryleboneRoadLondon,NW16JQUnitedKingdomTel:44(0)2076168988NewYork:1359Broadway,9thFloorNewYork,NY10018Tel:6468397017FungGlobalRetailTech.com

Recommended