1

IMPORTANT NOTICE Investing in mutual fund schemes involves certain risks and considerations associated generally with making investments in securities. The value of the Scheme’s investments may be affected generally by factors affecting financial markets, such as price and volume, volatility in interest rates, currency exchange rates, changes in regulatory and administrative policies of the Government or any other appropriate authority (including tax laws) or other political and economic developments. Consequently, there can be no assurance that the Scheme offered in this Offer Document would achieve the stated objectives. The NAV of the Units of the Scheme may fluctuate and can go up or down. Past performance of the schemes managed by the Sponsors or their affiliates or the Asset Management Company is not indicative of the future performance of the Scheme nor will the performance of the Scheme, following the commencement of the operations, be indicative of the Scheme’s future performance. Prospective investors are advised to review this Offer Document carefully and in its entirety and consult their legal, tax and financial advisors to determine possible legal, tax and financial or any other consequences of subscribing to, purchasing or holding Units under the Scheme, before making an application to subscribe or purchase the Units. ICICI Prudential Mutual Fund (the Fund) and ICICI Prudential Asset Management Company Limited (the AMC), have not authorized any person to give any information or make any representations, either oral or written, not stated in this Offer Document in connection with issue of Units under the Scheme. Prospective investors are accordingly advised not to rely upon any information or representations not incorporated in this Offer Document. Any subscription, purchase or sale made by any person on the basis of statements or representations which are not contained in this Offer Document or which are inconsistent with the information contained herein shall be solely at the risk of the investor. Unitholders / investors are requested to read and understand the Offer Document, Key Information Memorandum and risk factors furnished with the scheme in which they seek to make investments or in which they have invested. Unitholders / Investors are urged not to rely upon or be mislead by any oral promises or statements made by the distributors / intermediaries of the Mutual Fund and it is brought to the special attention of investors that the AMC / Mutual Fund will not be liable for mis-statement or communication by agents / distributors which are not previously expressly authorized / approved by the AMC / Mutual Fund. AMC, Trust and the Fund shall not be responsible for any claims made by the Unitholders / Investors based on such oral promises made by the distributors / intermediaries. The current Regulations impose certain restrictions and conditions on the AMC for entering into transactions with the Sponsors and their associates on behalf of the Fund. These restrictions include: a) Purchase or sale of securities through any broker associated with the Sponsors or through a firm which is an

associate of the Sponsor(s) shall not exceed an average of 5% of the aggregate purchases and sale of securities made by the Fund in all its Schemes in a block of any three months.

b) Utilization of the services of the Sponsors or any of their associates, for the purpose of any securities transactions and distribution and sale of securities shall be made only if a disclosure to this effect is made in the Offer Document and the brokerage or commission paid is also disclosed in the half yearly annual accounts of the mutual fund.

c) The Mutual Fund Scheme shall not make any investment in: 1. any unlisted security of an associate or group company of the Sponsor; or 2. any security issued by way of private placement by an associate or group company of the Sponsor; or 3. the listed securities of group companies of the Sponsor which is in excess of 25% of its net assets.

In this Offer Document, all references to “$” are to United States of America Dollars, “£” to Pound Sterling of United Kingdom and “Rs.” to Indian Rupees. The Reference Exchange Rate between the United States Dollar and the Indian Rupee has been taken at $1 = Rs.45.76 and UK£ and Indian Rupee at 1£=Rs.84.82. This Offer Document is dated June 11, 2007.

2

TABLE OF CONTENTS 1. Highlights ....................................................................................................................................................................... 6 2. Risk Factors .................................................................................................................................................................... 8 3. Due Diligence Certificate ............................................................................................................................................. 16 4. Definitions .................................................................................................................................................................... 17 5. Summary – ICICI Prudential Interval Fund Quarterly Interval Plan-II ....................................................................... 19 6. Constitution of the Mutual Fund................................................................................................................................... 21 a) The Sponsors ......................................................................................................................................................... 21 b) The Trustee Company ........................................................................................................................................... 22 i. Directors ......................................................................................................................................................... 23 ii. Rights and Obligations of the Trustee............................................................................................................ 24 iii. Trusteeship Fees............................................................................................................................................. 27 c) Management of Asset Management Company (AMC)......................................................................................... 27 i. Board of Directors of the AMC...................................................................................................................... 28 ii. Powers, Duties & Responsibilities of the AMC............................................................................................. 32 iii. Key Employees of AMC & relevant experience............................................................................................ 32 iv. Fund Manager ……………………………………………………………………………………………… 39 v. Compliance Officer ........................................................................................................................................ 39 vi. Investor Relations Officer .............................................................................................................................. 39 d) Auditors ................................................................................................................................................................. 39 e) Registrar................................................................................................................................................................. 39 f) Custodian ............................................................................................................................................................... 39 7. Investment Objectives & Policies .............................................................................................................................. 41 Fundamental Attributes of the Scheme......................................................................................................................... 41 a) Type of the Scheme ............................................................................................................................................... 41 b) Investment Objective............................................................................................................................................. 41 c) Investment Pattern & Investment Policies ............................................................................................................ 41 d) Asset Allocation Pattern ………………………………………………………………………………………... 41 e) Change in Investment Pattern................................................................................................................................ 42

f) Terms of the Scheme ............................................................................................................................................. 42 g) Change in Fundamental Attributes........................................................................................................................ 44

h) Investment Strategy .............................................................................................................................................. 44 i) Position of debt market in India ……………………………………………………………………………….. 44

j) Portfolio Turnover ................................................................................................................................................. 45 k) Procedure followed for investment decisions………………………………………………………………….. 45 l) Exposure to Derivatives ........................................................................................................................................ 46 m) Investment Restrictions for the Scheme................................................................................................................ 47 n) Underwriting by the Fund ..................................................................................................................................... 48 o) Computation of Net Asset Value........................................................................................................................... 48 p) Accounting Policies & Standards.......................................................................................................................... 51 8. Units & The New Fund Offer .................................................................................................................................... 53 General Information...................................................................................................................................................... 53 a) Minimum Subscription Amount............................................................................................................................ 53 b) Offer Price ……………………………………………………………………………………………………….53 c) New fund offer period ........................................................................................................................................... 53 d) New Fund Offer Expenses..................................................................................................................................... 53 e) Options and Investment plans offered under the Scheme ..................................................................................... 53 f) Pledge of Units for Loans ...................................................................................................................................... 53 g) How to Switch ....................................................................................................................................................... 53

3

h) Who can Invest? .................................................................................................................................................... 54 i) How to Apply?....................................................................................................................................................... 54 i. New Fund Offer ............................................................................................................................................. 54 ii. Resident Investors - Mode of Payment .......................................................................................................... 55 iii. NRIs & FIIs .................................................................................................................................................... 55 iv. Mode of Payment on Repatriation Basis........................................................................................................ 56

v. Mode of Payment on Non-Repatriation Basis................................................................................................ 56 vi. Investments of the minor Investor on attaining Majority ………………………………………………….. 56

vii. Application under Power of Attorney/Body Corporate/Registered Society/Partnership............................... 56 viii. Joint Applicants.............................................................................................................................................. 57 ix. Nomination Facility........................................................................................................................................ 57 j) Issuance of Units/Refund ...................................................................................................................................... 57 k) Account Statements ............................................................................................................................................... 57 l) Refunds.................................................................................................................................................................. 57 m) Redemption of Units.............................................................................................................................................. 58 i. Redemption Price ........................................................................................................................................... 58

ii. Applicable NAV............................................................................................................................................. 59 iii. Cooling off period for web based transactions …………………………………………………………….. 59

iv. How to Redeem? ............................................................................................................................................ 59 v. Payment of Proceeds ...................................................................................................................................... 60 vi. Non receipt of email communication by investor …………………………………………………………..60

vii. Redemption by NRIs/ FIIs ............................................................................................................................. 60 viii Effect of Redemptions.................................................................................................................................... 61

ix Fractional Units .............................................................................................................................................. 61 x Signature mismatch cases ………………………………………………………………………………….. 61

xi Right to Limit Redemptions........................................................................................................................... 61 xii. Suspension of Sale and Redemption of Units ................................................................................................ 61 xiii. Permanent Account No. …………………………………………………………………………………... 62 xiv. Dormant Account Locking ………………………………………………………………………………… 62 xv. Unique Identification Number …………………………………………………………………………….. 62

o) Purchase of Units after the New fund offer period................................................................................................ 62 i. Purchase Price ................................................................................................................................................ 62 ii. How to Purchase?........................................................................................................................................... 63 iii. Purchase by NRIs ........................................................................................................................................... 63

iv. Applicable NAV............................................................................................................................................. 63 p) Prevention of Money Laundering ………………………………………………………………………………. 63 q) Pan Based KYC Process ………………………………………………………………………………………. 64

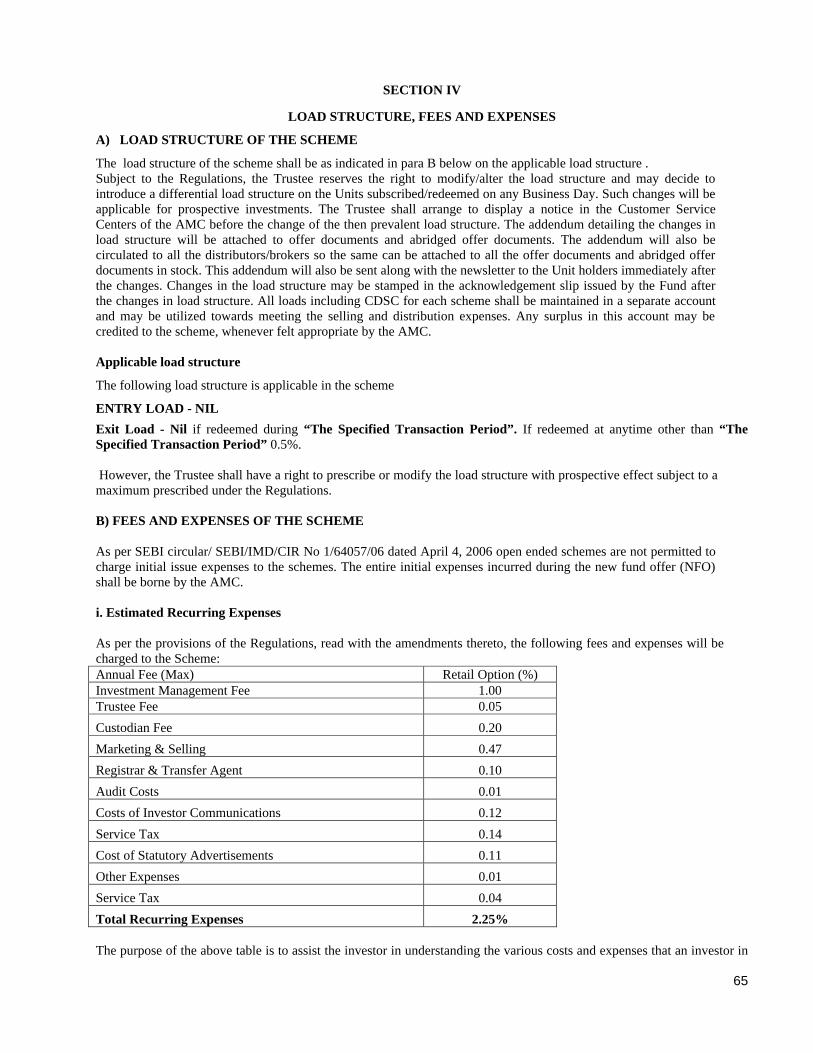

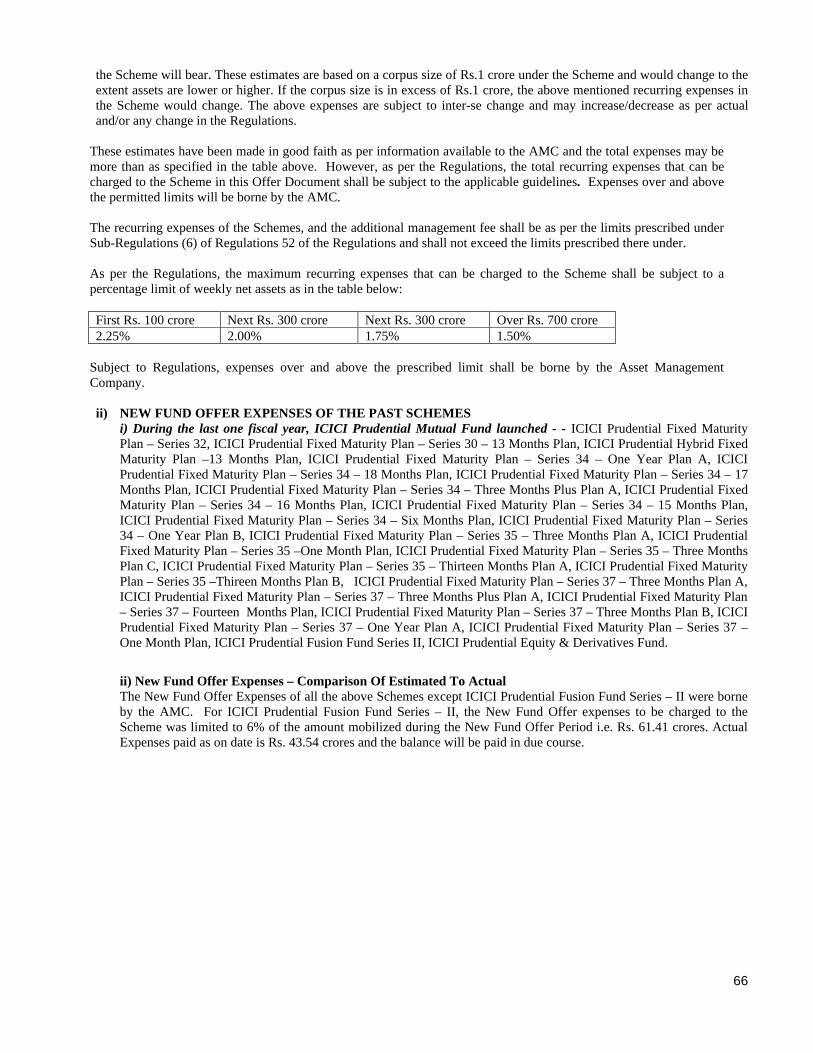

9. Load Structure, Fees and Expenses .......................................................................................................................... 66 a) Load Structure of the Scheme …………………………………………………………………………………...66

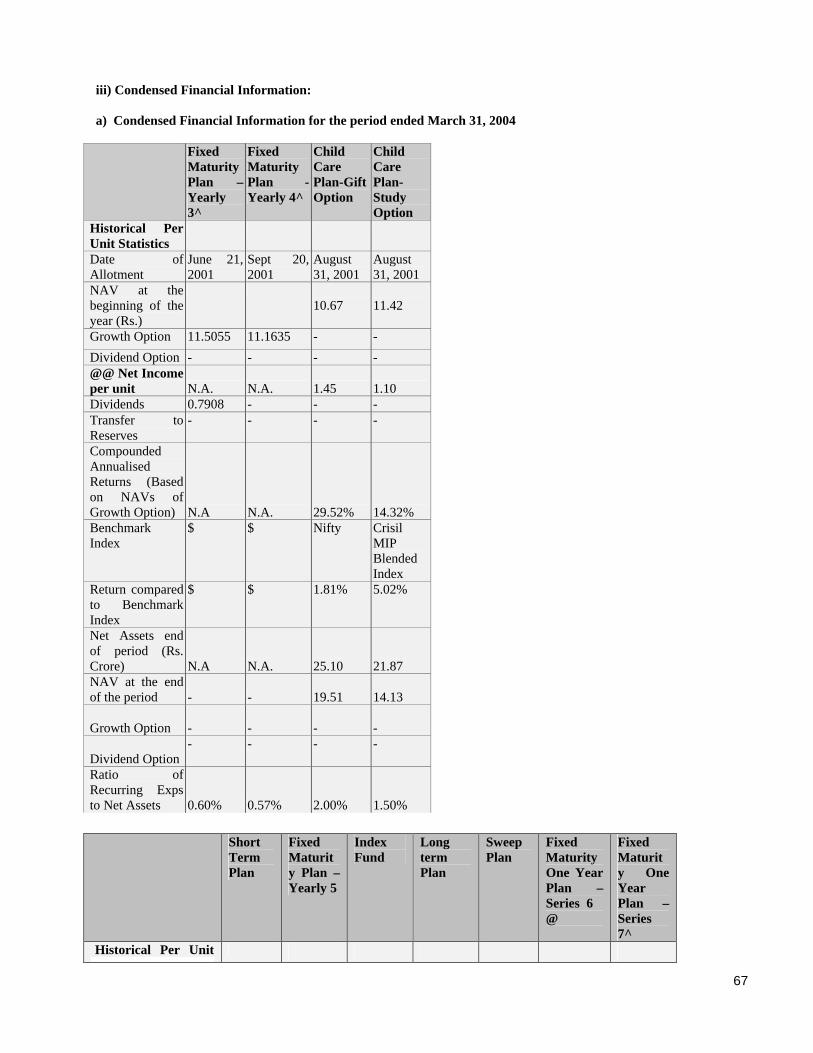

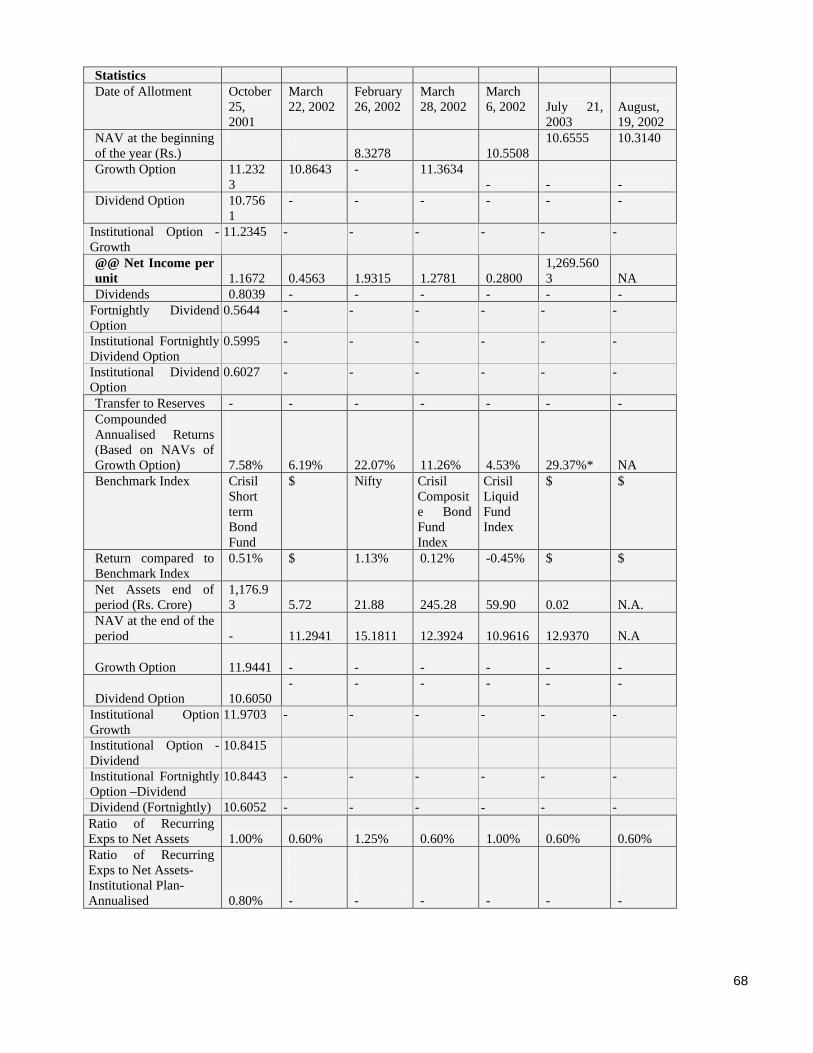

b) Fees and Expenses of the Scheme......................................................................................................................... 66 i. Estimated Recurring Expenses....................................................................................................................... 66 ii) Fees and Expenses of the Existing Scheme........................................................................................................... 67 i. New Fund Offer Expenses of the past scheme............................................................................................... 67 ii. Condensed Financial Information .................................................................................................................. 68 10. Unitholders Rights and Services................................................................................................................................ 91 a) Investors Services.................................................................................................................................................. 91 b) Ease of Transactions.............................................................................................................................................. 91 i. Customer Service Centers in major metros.................................................................................................... 91 ii. Process transactions in a timely manner ........................................................................................................ 91 c) Problem Resolution ............................................................................................................................................... 91

4

d) NAV Information .................................................................................................................................................. 92 e) Disclosure of information under the Regulations.................................................................................................. 92 f) Rights of Unitholders of the Scheme..................................................................................................................... 92 g) Duration of the Scheme/Winding up..................................................................................................................... 93 h) Procedure and manner of Winding up................................................................................................................... 93 i) Tax Benefits........................................................................................................................................................... 93

1) To the Mutual Fund……………………………………………………………………………………….. 94 2) To the Unitholders.......................................................................................................................................... 94

2.1 Income received from mutual fund ……………………………………………………… ............................. 94 2.2 Long term capital gains on transfer of units……………………………………………………………………94

i. For Individuals and HUFs………………………………………………………………………….……94 ii. For Partnership Firms, Non-Residents, Indian Companies/Foreign Companies …………………. …...94 iii. For Non-resident Indians ………………………………………………………………………….. …..95 iv. For Overseas Financial Organisations and Foreign Institutional Investors fulfilling conditions laid down

under section 115AB (Offshore Fund).................................................................................................... 95 2.3 Short term capital gains on trasfer of units …………………………………………………………………95 2.4 Capital Losses ……………………………………………………………………………………………….96

3. Tax deduction at source………………………………………………………………………………………. …96

4. Exemption from tax on capital gains arising on transfer of units held for more than 12 months……………… 97

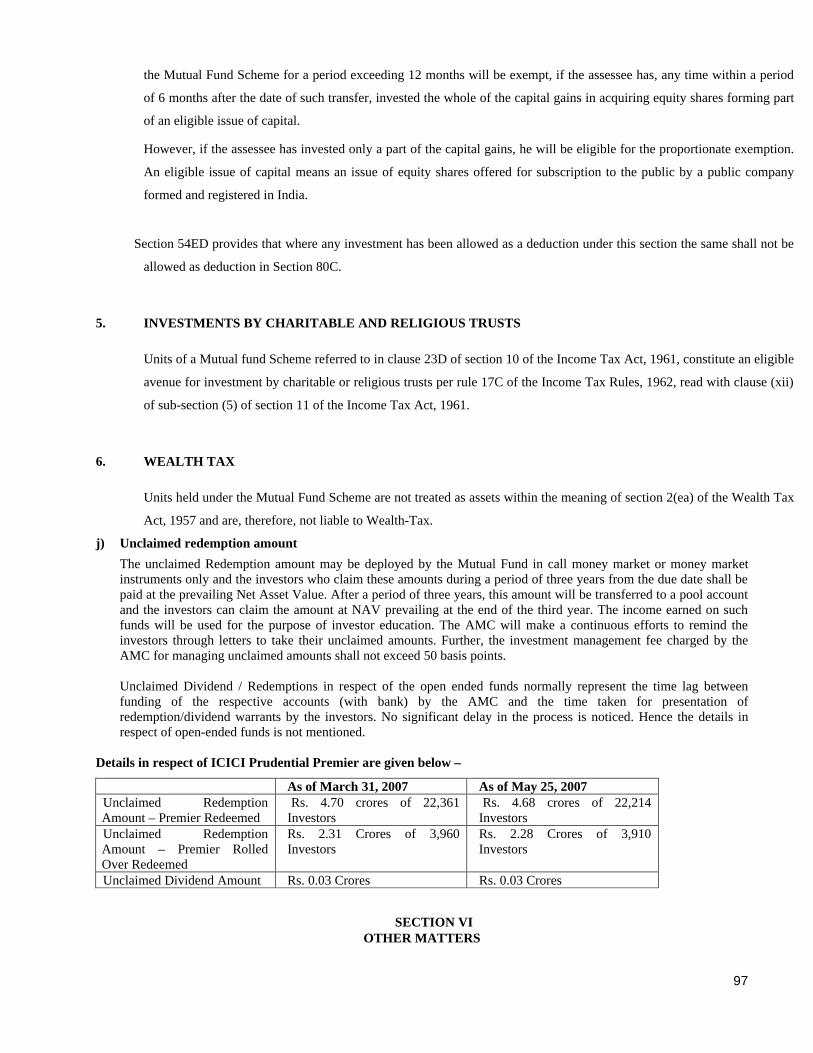

5. Investments by charitable and religious trusts in the plan………………………………………………………..98

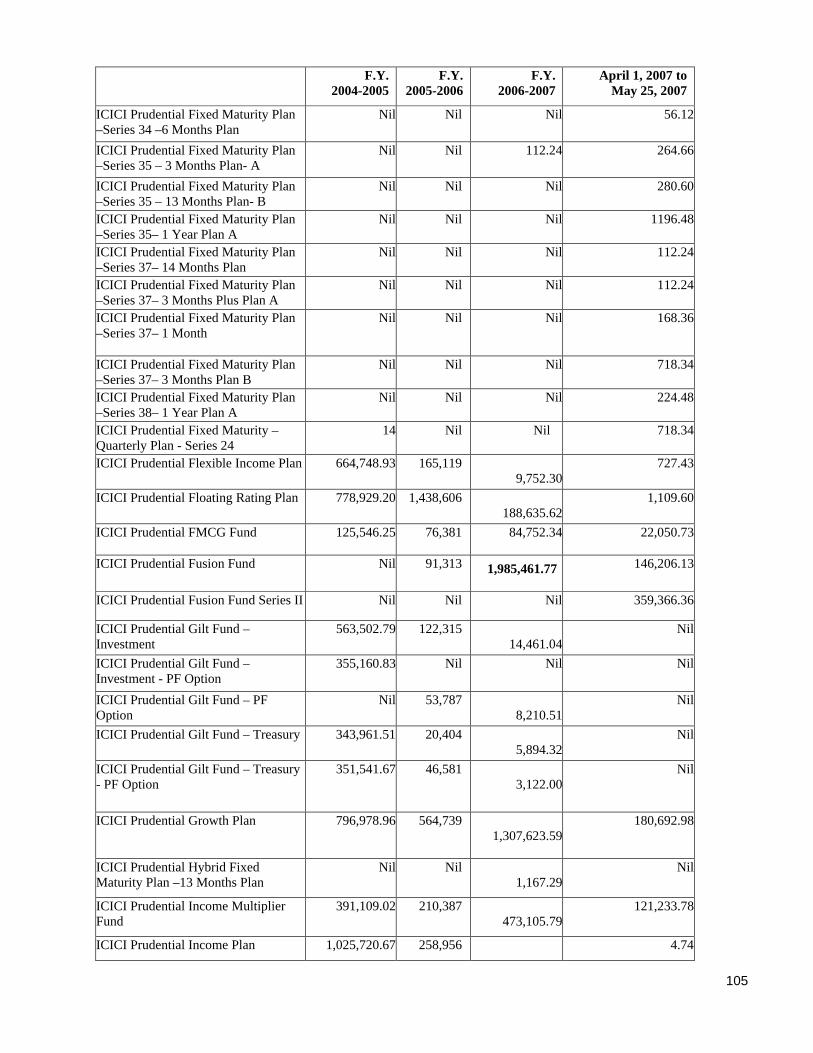

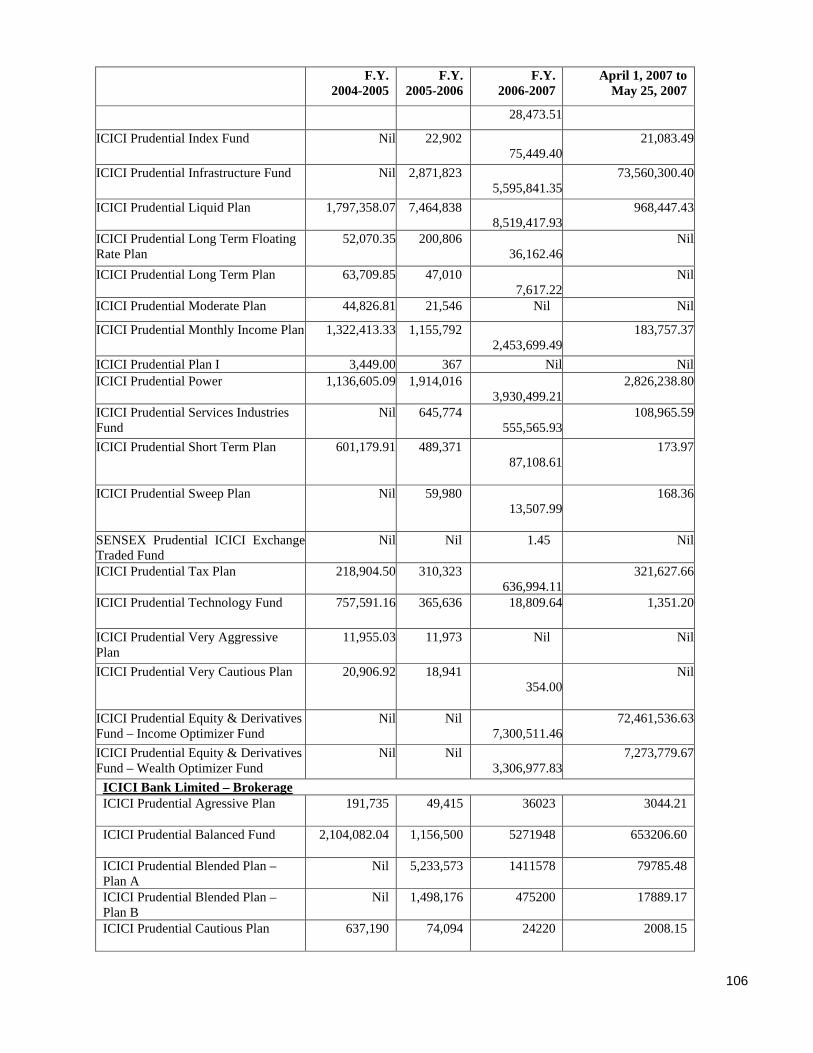

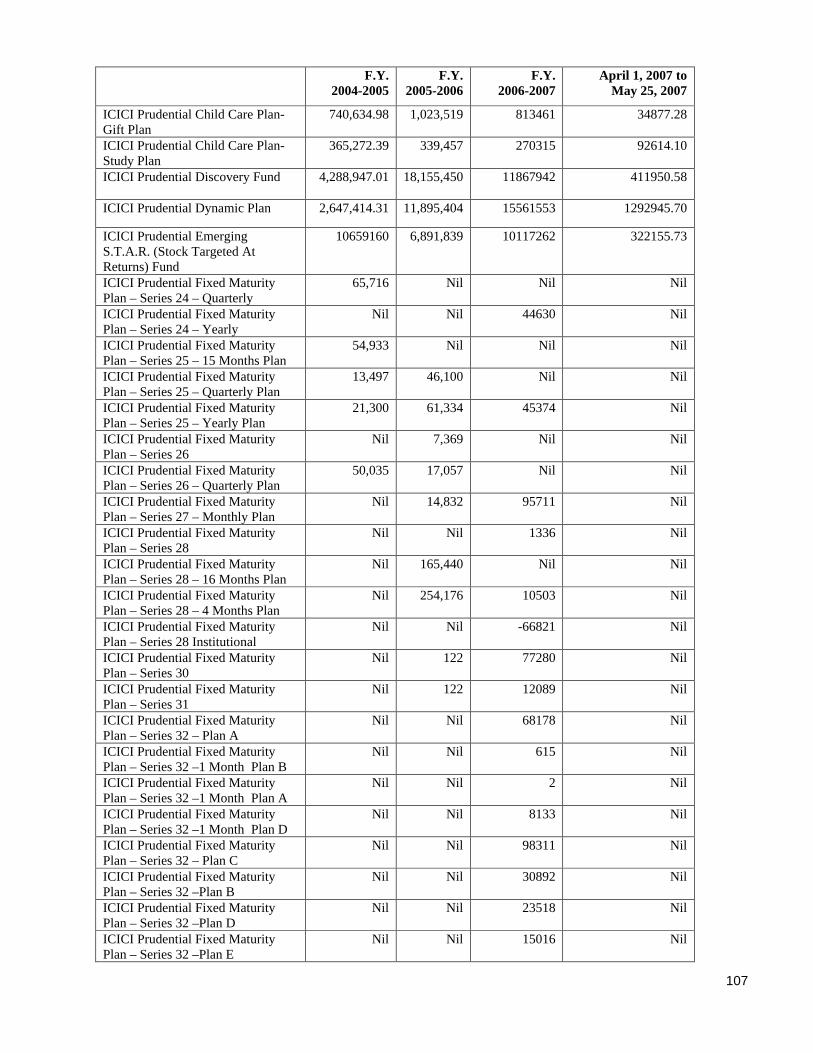

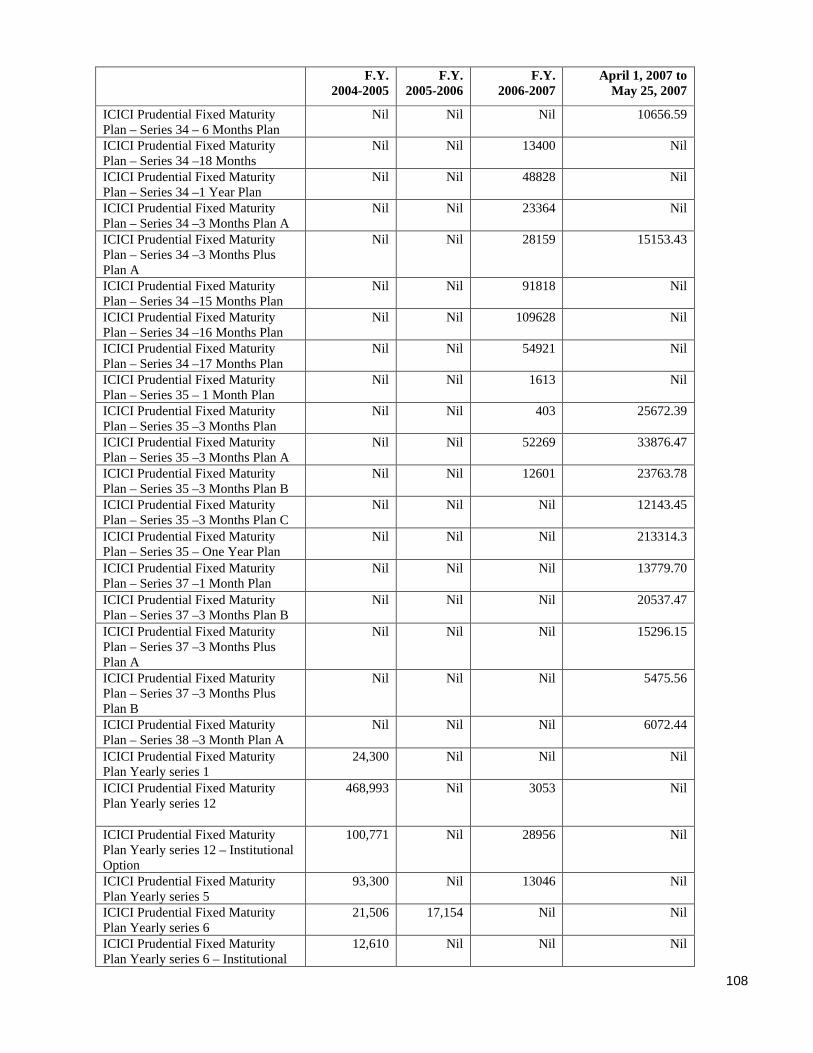

6. Wealth Tax Sec. 2 (ea)……………………………………………………………………………………………98 j) Unclaimed redemption amount……………………………………………………………………………………….98 11. Other Matters a) Unitholders Grievances Redressal Mechanism..................................................................................................... 99 b) Associate Transactions ........................................................................................................................................ 101 c) Details of Investment in Companies that hold more than 5% ……………………………………………… 117 of NAV of Schemes managed by the AMC d) Penalties and Pending Litigations ....................................................................................................................... 125 e) Borrowing by the Mutual Fund ........................................................................................................................... 134 f) Stock Lending by the Mutual Fund.................................................................................................................... 134 g) Inter-Scheme Transfers ....................................................................................................................................... 134 h) General Information ............................................................................................................................................ 134

• Power to make Rules ........................................................................................................................................... 134

• Power to remove Difficulties............................................................................................................................... 134

• Scheme to be binding on the Unitholders............................................................................................................ 134

• Documents available for Inspection .................................................................................................................... 134

5

Highlights

● The Sponsors of the Fund are Prudential plc of the United Kingdom (UK) and ICICI Bank Limited (erstwhile ICICI Limited). Prudential plc is a leading international financial services group providing retail financial products and services and fund management to many millions of customers worldwide. As a group Prudential plc has, as of December 31, 2005, over GBP234 billion of funds under management, more than 16 million customers and over 31,661 employees worldwide as of December 31, 2005. Securities and Exchange Board of India, vide its letter no. MFD/PM/567/02 dated June 4, 2002, has accorded its approval in recognizing ICICI Bank Ltd. as a co-sponsor consequent to the merger of ICICI Ltd. with ICICI Bank Ltd.

ICICI Bank is India's second-largest bank with total assets of about Rs. 251,389 crores as at March 31, 2006 and profit after tax of Rs. 2,540 crores for the year ended March 31, 2006 (Rs. 2005 crores for the year ended March 31, 2005). ICICI Bank has a network of about 614 branches and extension counters and over 2,200 ATMs. ICICI Bank offers a wide range of banking products and financial services to corporate and retail customers through a variety of delivery channels and through its specialised subsidiaries and affiliates in the areas of investment banking, life and non-life insurance, venture capital and asset management. ICICI Bank set up its international banking group in fiscal 2002 to cater to the cross border needs of clients and leverage on its domestic banking strengths to offer products internationally. ICICI Bank currently has subsidiaries in the United Kingdom, Russia and Canada, branches in Singapore, Bahrain, Hong Kong, Sri Lanka and Dubai International Finance Centre and representative offices in the United States, United Arab Emirates, China, South Africa and Bangladesh. UK subsidiary of ICICI Bank has established a branch in Belgium. ICICI Bank is the most valuable bank in India in terms of market capitalisation. (Source: Overview at www.icicibank.com).

ICICI Bank was originally promoted in 1994 by ICICI Limited, an Indian financial institution, and was its wholly

owned subsidiary. ICICI's shareholding in ICICI Bank was reduced to 46% through a public offering of shares in India in fiscal 1998, an equity offering in the form of ADRs listed on the NYSE in fiscal 2000, ICICI Bank's acquisition of Bank of Madura Limited in an all-stock amalgamation in fiscal 2001, and secondary market sales by ICICI to institutional investors in fiscal 2001 and fiscal 2002. ICICI was formed in 1955 at the initiative of the World Bank, the Government of India and representatives of Indian industry.

Pursuant to the Scheme of Amalgamation effective March 30, 2002, among ICICI, ICICI Personal Financial Services, ICICI Capital Services and ICICI Bank, sanctioned by the High Court of Gujarat and the High Court of Judicature at Bombay and approved by the Reserve Bank of India, ICICI, ICICI Personal Financial Services and ICICI Capital Services were merged with ICICI Bank in an all-stock merger. ICICI Bank is the surviving legal entity in the amalgamation.

ICICI Bank was formerly a wholly owned subsidiary of ICICI Ltd, an Indian financial institution.

� Fund Management expertise Prudential plc is a leading international financial services group providing retail financial products and services and fund management to many millions of customers worldwide. As a group Prudential plc has, as of December 31, 2005, over GBP234 billion of funds under management, more than 16 million customers and over 31,661 employees worldwide as of December 31, 2005.

ICICI Prudential Asset Management Company Limited, the Investment Manager to ICICI Prudential Mutual Fund, manages assets over Rs.42,660 crores as of April 13, 2007 through 34 schemes. It is one of the largest asset management companies in the country.

• Investment Objectives

The investment objective of the scheme is to generate optimal returns consistent with moderate levels of risk and liquidity by investing in debt securities and money market securities.

6

• Transparency – AMC will calculate and disclose the first NAV not later than 30 days from the closure of the New Fund Offer Period. Subsequently, the NAV will be calculated and disclosed at the close of every Business Day. In addition, the AMC will disclose details of the portfolio at least on a half-yearly basis.

• Load

Entry Load -Nil

Exit Load - Nil if redeemed during “The Specified Transaction Period”.

If redeemed at anytime other than “The Specified Transaction Period” exit load will be 0.5%

However, the Trustee shall have a right to prescribe or modify the load structure with prospective effect subject to a maximum prescribed under the Regulations.

• Subscription – The scheme will be available for fresh purchases once a quarter only during “The Specified Transaction Period” i.e. 15th June, 15th September, 15th December, 15th March .If such day is a non business day, the next business day.

• High Liquidity - The scheme will offer for subscription / switch and redemption / switch out of units without any load on specified transaction period, once a quarter on an on going basis, under the plan. The scheme will also offer redemptions on all business days, other than the specified transaction period, subject to the applicable exit load. The AMC shall have the flexibility to change / alter the Transaction Period depending on the prevailing market conditions and in the interest of the unit holders.

• New Fund offer Expenses: The Scheme being an open-ended Scheme, no New Fund Offer expenses shall be

charged in accordance with SEBI Circular dated April 04, 2006.

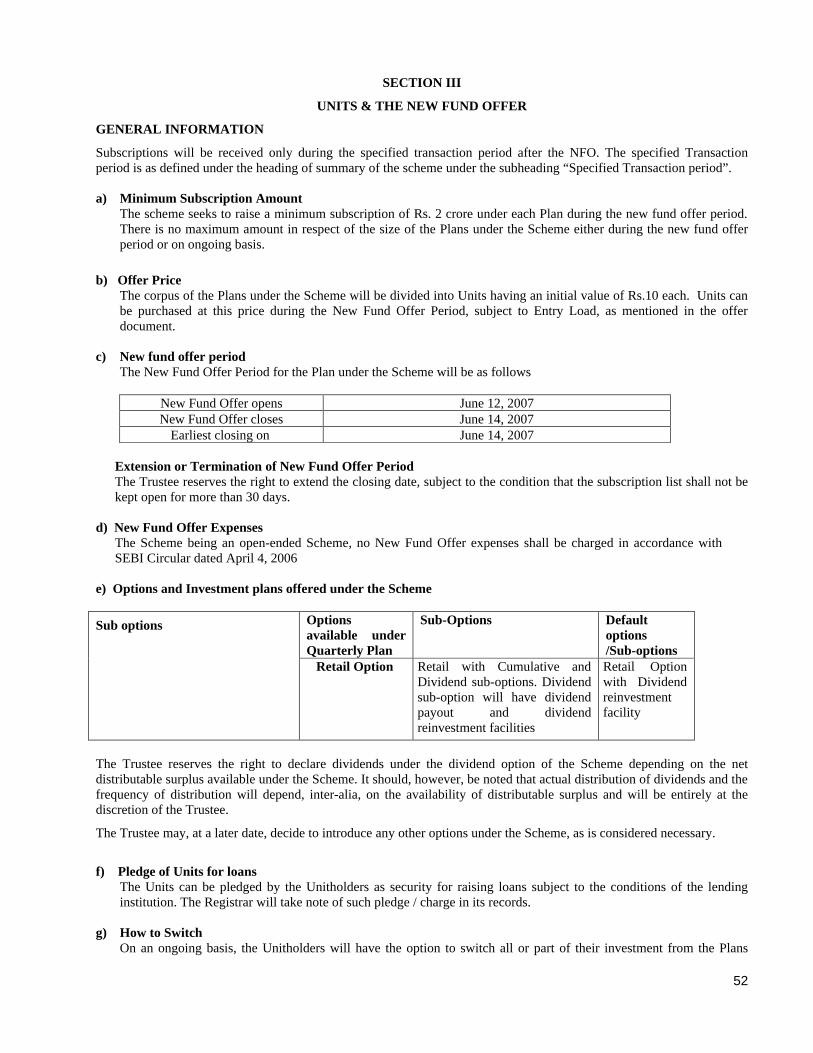

• Option – There is one option being launched under the Scheme viz. Retail option. Retail option will have Cumulative and Dividend sub-options. Dividend sub-option will have dividend payout and dividend reinvestment facility. The default sub-option for the plan is Dividend with reinvestment facility.

The Trustee reserves the right to declare dividends under the dividend option of the Scheme depending on the net distributable surplus available under the Scheme. It should, however, be noted that actual distribution of dividends and the frequency of distribution will depend, inter-alia, on the availability of distributable surplus and will be entirely at the discretion of the Trustee.

The Trustee may, at a later date, decide to introduce any other options under the Scheme, as is considered necessary.

• Investors who hold units in any of the open-ended debt schemes of the Fund may switch all or part of their holdings to the Plans under the Scheme, during the specified transaction period. Switch-ins can also be made from close-ended debt schemes maturing during the specified transaction period.

• Repatriation – Repatriation benefits would be available to NRIs/PIOs/FIIs, subject to applicable Regulations notified by Reserve Bank of India from time to time.

• For details on tax update, please refer page 100 of this document.

• Investors in the Scheme are not being offered any guaranteed returns.

• Investors are advised to consult their Legal /Tax and other Professional Advisors in regard to tax/legal implications relating to their investments in the Scheme and before making decision to invest in the Scheme or redeem the Units in the Scheme.

7

RISK FACTORS AND SPECIAL CONSIDERATIONS

• Mutual Funds and securities investments are subject to market risks and there is no assurance or guarantee that the objectives of the Scheme will be achieved.

• As with any securities investment, the NAV of the Units issued under the Scheme can go up or down depending on the factors and forces affecting the capital markets.

• Past performance of the Sponsors, AMC/Fund does not indicate the future performance of the Scheme of the Fund.

• The Sponsors are not responsible or liable for any loss resulting from the operation of the Scheme beyond the contribution of an amount of Rs. 22.2 lacs collectively made by them towards setting up the Fund and such other accretions and additions to the corpus set up by the Sponsors.

• ICICI Prudential Interval Fund is the name of the Scheme and does not in any manner indicate either the quality of the Scheme or its future prospects and returns.

• The NAVs of the Scheme may be affected by changes in the general market conditions, factors and forces affecting capital market, in particular, level of interest rates, various market related factors and trading volumes, settlement periods and transfer procedures.

• In the event of receipt of inordinately large number of redemption requests or of a restructuring of the Scheme’s portfolio, there may be delays in the redemption of Units. Please see page 68 for “Right to Limit Redemptions” in this Offer Document.

• The liquidity of the Scheme’s investments is inherently restricted by trading volumes in the securities in which it invests.

• Investors in the Scheme are not offered any guaranteed returns.

• Mutual Funds being vehicles of securities investments are subject to market and other risks and there can be no guarantee against loss resulting from investing in schemes. The various factors which impact the value of scheme investments include but are not limited to fluctuations in the bond markets, fluctuations in interest rates, prevailing political and economic environment, changes in government policy, factors specific to the issuer of securities, tax laws, liquidity of the underlying instruments, settlements periods, trading volumes etc. and securities investments are subject to market risks and there is no assurance or guarantee that the objectives of the Scheme will be achieved.

• As the liquidity of the Scheme’s investments could at times, be restricted by trading volumes and settlement periods, the time taken by the Fund for redemption of units may be significant in the event of an inordinately large number of redemption requests or of a restructuring of the Scheme’s portfolio. In view of this the Trustee has the right, in sole discretion to limit redemptions (including suspending redemption) under certain circumstances, as described under the section titled “Right to limit Repurchases”.

● From time to time and subject to the regulations, the sponsors, the mutual funds and investment Companies managed by them, their affiliates, their associate companies, subsidiaries of the sponsors and the AMC may invest in either directly or indirectly in the scheme. The funds managed by these affiliates, associates and/ or the AMC may acquire a substantial portion of the Scheme. Accordingly, redemption of units held by such funds, affiliates/associates and sponsors may have an adverse impact on the units of the Scheme because the timing of such redemption may impact the ability of other unitholders to redeem their units

The Scheme may invest in other schemes managed by the AMC or in the schemes of any other Mutual Funds, provided it is in conformity to the investment objectives of the Scheme and in terms of the prevailing Regulations. As per the Regulations, no investment management fees will be charged for such investments.

From time to time and subject to the regulations, the AMC may invest in this Scheme. The decision to invest in the Scheme by the AMC will be based on parameters specified by the Board of the AMC.

Further, as per the Regulation, in case the AMC invests in any of the schemes managed by it, it shall not be entitled to charge any fees on such investments. It may be noted that no prior intimation/indication would be given to investors when the composition/asset allocation pattern under the scheme undergo changes within the permitted band of upto 35% for debt. The investors/unitholders can ascertain details of asset allocation of the scheme as on the last date of each month on AMC’s website at www.icicipruamc.com that will display the asset allocation of the scheme as on the given day.

• In case the Scheme on the date of allotment of NFO does not have 20 investors and if at the time of allotment any one

8

of the investors holds more than 25% of net assets of the Scheme the Scheme will be wound up immediately in terms of SEBI Circular dated December 12, 2003 having reference no- SEBI/IMD/CIR No 10/22701/03. The condition will also be applied at each specified transaction period at the time of allotment of additional units

• Different types of securities in which the scheme would invest as given in the offer document carry different levels

and types of risk. Accordingly the scheme’s risk may increase or decrease depending upon its investment pattern. E.g. corporate bonds carry a higher amount of risk than Government securities. Further even among corporate bonds, bonds which are AAA rated are comparatively less risky than bonds which are AA rated.

Additional risk factors • The value of the Scheme’s investments, may be affected generally by factors affecting securities markets, such as

price and volume volatility in the markets, interest rates, currency exchange rates, changes in policies of the Government, taxation laws or any other appropriate authority policies and other political and economic developments which may have an adverse bearing on individual securities, including debt markets. Consequently, the NAV of the Units of the Scheme may fluctuate and can go up or down.

• Trading volumes, settlement periods and transfer procedures may restrict the liquidity of the investments made by the Scheme. Different segments of the Indian financial markets have different settlement periods and such periods may be extended significantly by unforeseen circumstances leading to delays in receipt of proceeds from sale of securities. The NAV of the Scheme can go up and down because of various factors that affect the capital markets in general.

• The NAV of the Scheme to the extent invested in Debt and Money market securities, are likely to be affected by changes in the prevailing rates of interest.

• Investment decisions made by the AMC may not always be profitable, as actual market movements may be at variance with anticipated trends.

Scheme Specific Risk Factors The investors in ICICI Prudential Interval Fund should be particularly aware of the risks generally associated with investment in fixed income and money market securities. Given below are some of the common risks associated with investment in fixed income and money market securities. These risks include but are not restricted to: Liquidity risk, Interest Rate Risk, Liquidity or Marketability Risk, Credit and Downgrading Risk, and Reinvestment Risk Liquidity risk In case of abnormal circumstances it will be difficult to complete the square off transaction due to liquidity being poor in stock futures/spot market. However fund will aim at taking exposure only into liquid stocks where there will be minimal risk to square off the transaction. Fixed Income Securities: • Interest Rate Risk: As with all debt securities, changes in interest rates may affect the Scheme’s Net Asset Value as

the prices of securities generally increase as interest rates decline and generally decrease as interest rates rise. Prices of long-term securities generally fluctuate more in response to interest rate changes than do short-term securities. Indian debt markets can be volatile leading to the possibility of price movements up or down in fixed income securities and thereby to possible movements in the NAV.

• Liquidity or Marketability Risk: This refers to the ease with which a security can be sold at or near to its valuation

yield-to-maturity (YTM). The primary measure of liquidity risk is the spread between the bid price and the offer price quoted by a dealer. Liquidity risk is today characteristic of the Indian fixed income market.

• Credit Risk : Credit risk or default risk refers to the risk that an issuer of a fixed income security may default (i.e. will

be unable to make timely principal and interest payments on the security). Because of this risk corporate debentures are sold at a yield above those offered on Government Securities, which are sovereign obligations and free of credit risk. Normally, the value of a fixed income security will fluctuate depending upon the changes in the perceived level of credit risk as well as any actual event of default. The greater the credit risk, the greater the yield required for someone to be compensated for the increased risk.

9

• Reinvestment Risk: This risk refers to the interest rate levels at which cash flows received from the securities in the Scheme are reinvested. The additional income from reinvestment is the “interest on interest” component. The risk is that the rate at which interim cash flows can be reinvested may be lower than that originally assumed.

• Money Market Securities are subject to the risk of an issuer’s inability to meet interest and principal payments on its

obligations and market perception of the creditworthiness of the issuer Risks attached with the use of derivatives: Derivative products are leveraged instruments and can provide disproportionate gains as well as disproportionate losses to the investor. Execution of such strategies depends upon the ability of the fund manager to identify such opportunities. Identification and execution of the strategies to be pursued by the fund manager involve uncertainty and decision of fund manager may not always be profitable. No assurance can be given that the fund manager will be able to identify or execute such strategies. As and when the Scheme trade in the derivatives market there are risk factors and issues concerning the use of derivatives that Investors should understand. Derivative products are specialized instruments that require investment techniques and risk analyses different from those associated with stocks and bonds. The use of a derivative requires an understanding not only of the underlying instrument but of the derivative itself. Derivatives require the maintenance of adequate controls to monitor the transactions entered into, the ability to assess the risk that a derivative adds to the portfolio and the ability to forecast price or interest rate movements correctly. There is the possibility that a loss may be sustained by the portfolio as a result of the failure of another party (usually referred to as the “counter party”) to comply with the terms of the derivatives contract. Other risks in using derivatives include the risk of mis pricing or improper valuation of derivatives and the inability of derivatives to correlate perfectly with underlying assets, rates and indices. Thus, derivatives are highly leveraged instruments. Even a small price movement in the underlying security could have a large impact on their value. Also, the market for derivative instruments is nascent in India. “The risks associated with the use of derivatives are different from or possibly greater than the risks associated with investing directly in securities and other traditional investments.”

The specific risk factors arising out of a derivative strategy used by the Fund Manager may be as below: � The risk of mispricing or improper valuation and the inability of derivatives to correlate perfectly with

underlying assets, rates and indices. • Also please refer to Page 52 for example on Derivatives. Risk Analysis on underlying asset classes in Securitisation Generally available Asset Classes for securitisation in India Commercial Vehicles Auto and Two wheeler pools Mortgage pools (residential housing loans) Personal Loan, credit card and other retail loans Corporate loans/receivables In terms of specific risks attached to securitisation, each asset class would have different underlying risks, however, residential mortgages are supposed to be having lower default rates as an asset class. On the other hand, repossession and subsequent recovery of commercial vehicles and other auto assets is fairly easier and better compared to mortgages. Some of the asset classes such as personal loans, credit card receivables etc., being unsecured credits in nature, may witness higher default rates. As regards corporate loans/receivables, depending upon the nature of the underlying security for the loan or the nature of the receivable the risks would correspondingly fluctuate. However, the credit enhancement stipulated by rating agencies for such asset class pools is typically much higher and hence their overall risks are comparable to other AAA rated asset classes. The rating agencies have an elaborate system of stipulating margins, over collateralisation and guarantees to bring risk limits in line with the other AAA rated securities.

10

It is relevant to note here that predominantly the scheme intends to invest in only AAA rated securitised debt. This compares favourably with a portfolio which is constructed on the basis of AA rated securitised debt.

Some of the factors, which are typically analyzed for any pool are as follows:

Size of the loan: generally indicates the kind of assets financed with loans. Also indicates whether there is excessive reliance on very small ticket size, which may result in difficult and costly recoveries. To illustrate, the ticket size of housing loans is generally higher than that of personal loans. Hence in the construction of a housing loan asset pool for say Rs.1,00,00,000/- it may be easier to construct a pool with just 10 housing loans of Rs.10,00,000 each rather than to construct a pool of personal loans as the ticket size of personal loans may rarely exceed Rs.5,00,000/- per individual. Also to amplify this illustration further, if one were to construct a pool of Rs.1,00,00,000/- consisting of personal loans of Rs.1,00,000/- each, the larger number of contracts(100 as against one of 10 housing loans of Rs.10 lakh each) automatically diversifies the risk profile of the pool as compared to a housing loan based asset pool. Average original maturity of the pool: indicates the original repayment period and whether the loan tenors are in line with industry averages and borrower’s repayment capacity. To illustrate, in a car pool consisting of 60-month contracts, the original maturity and the residual maturity of the pool viz. number of remaining installments to be paid gives a better idea of the risk of default of the pool itself. If in a pool of 100 car loans having original maturity of 60 months, if more than 70% of the contracts have paid more than 50% of the installments and if no default has been observed in such contracts, this is a far superior portfolio than a similar car loan pool where 80% of the contracts have not even crossed 5 installments. Loan to Value Ratio: Indicates how much % value of the asset is financed by borrower’s own equity. The lower LTV, the better it is. This Ratio stems from the principle that where the borrowers own contribution of the asset cost is high, the chances of default are lower. To illustrate for a Truck costing Rs.20 lakhs, if the borrower has himself contributed Rs.10 lakh and has taken only Rs.10 lakh as a loan, he is going to have lesser propensity to default as he would lose an asset worth Rs.20 lakhs if he defaults in repaying an installment. This is as against a borrower who may meet only Rs.2 lakh out of his own equity for a truck costing Rs.20 lakh. Between the two scenarios given above, the latter would have higher risk of default than the former. Average seasoning of the pool: indicates whether borrowers have already displayed repayment discipline. To illustrate, in the case of a personal loan, if a pool of assets consist of those who have already repaid 80% of the installments without default, this certainly is a superior asset pool than one where only 10% of installments have been paid. In the former case, the portfolio has already demonstrated that the repayment discipline is far higher. Default rate distribution: Indicates how much % of the pool and overall portfolio of the originator is current, how much is in 0-30 DPD (days past due), 30-60 DPD, 60-90 DPD and so on. The rationale here is very obvious, as against 0-30 DPD, the 60-90 DPD is certainly a higher risk category. Unlike in plain vanilla instruments, in securitisation transactions it is possible to work towards a target credit rating, which could be much higher than the originator’s own credit rating. This is possible through a mechanism called ‘Credit enhancement’. The purpose of credit enhancement is to ensure timely payment to the investors, if the actual collection from the pool of receivables for a given period are short of the contractual payouts on securitisation. Securitisation are normally non-recourse instruments and therefore, the repayment on securitisation would have to come from the underlying assets and the credit enhancement. Therefore, the rating criteria centrally focus on the quality of the underlying assets. World over, the quality of credit ratings is measured by default rates and stability. An analysis of rating transition and default rates, witnessed in both international and domestic arena, clearly reveals that structured finance ratings have been characterized by far lower default and transition rates than that of plain vanilla debt ratings. Further, internationally, in case of structured finance ratings, not only are the default rates low but post default recovery is also high.

In the Indian scenario, also, more than 95% of issuances have been AAA rated issuances indicating the strength of the underlying assets as well as adequacy of credit enhancement. Investment exposure of the Fund with reference to Securitised Debt

11

The Fund will predominantly invest only in those securitisation issuances which have AAA rating indicating the highest level of safety from credit risk point of view at the time of making an investment. The Fund will not invest in foreign securitised debt. The fund may invest in various type of securitisation issuances, including but not limited to Asset Backed Securitisation, Mortgage Backed Securitisation, Personal Loan Backed Securitisation, Collateralized Loan Obligation / Collateralized Bond Obligation and so on.

The fund does not propose to limit its exposure to only one asset class or to have asset class based sub-limits as it will primarily look towards the AAA rating of the offering. The fund will conduct an independent due diligence on the cash margins, collateralisation, guarantees and other credit enhancements and the portfolio characteristic of the securitisation to ensure that the issuance fits in to the overall objective of the investment in high investment grade offerings irrespective of underlying asset class. Risk Factors specific to investments in Securitised Papers: Types of Securitised Debt vary and carry different levels and types of risks. Credit Risk on Securitised Bonds depends upon the Originator and varies depending on whether they are issued with Recourse to Originator or otherwise.

Even within securitised debt, AAA rated securitised debt offers lesser risk of default than AA rated securitised debt. A structure with Recourse will have a lower Credit Risk than a structure without Recourse. Underlying assets in Securitised Debt may assume different forms and the general types of receivables include Auto Finance, Credit Cards, Home Loans or any such receipts, Credit risks relating to these types of receivables depend upon various factors including macro economic factors of these industries and economies. Specific factors like nature and adequacy of property mortgaged against these borrowings, nature of loan agreement/ mortgage deed in case of Home Loan, adequacy of documentation in case of Auto Finance and Home Loans, capacity of borrower to meet its obligation on borrowings in case of Credit Cards and intentions of the borrower influence the risks relating to the asset borrowings underlying the securitised debt.

Holders of the securitised assets may have low credit risk with diversified retail base on underlying assets especially when securitised assets are created by high credit rated tranches, risk profiles of Planned Amortisation Class tranches (PAC), Principal Only Class Tranches (PO) and Interest Only class tranches (IO) will differ depending upon the interest rate movement and speed of prepayment. Unlike in plain vanilla instruments, in securitisation transactions, it is possible to work towards a target credit rating, which could be much higher than the originator’s own credit rating. This is possible through a mechanism called ‘Credit enhancement’. The process of ‘Credit enhancement’ is fulfilled by filtering the underlying asset classes and applying selection criteria, which further diminishes the risks inherent for a particular asset class. The purpose of credit enhancement is to ensure timely payment to the investors, if the actual collection from the pool of receivables for a given period is short of the contractual payout on securitisation. Securitisation is normally non-recourse instruments and therefore, the repayment on securitisation would have to come from the underlying assets and the credit enhancement. Therefore the rating criteria centrally focus on the quality of the underlying assets.

The change in market interest rates – prepayments may not change the absolute amount of receivables for the investors, but may have an impact on the re-investment of the periodic cash flows that the investor receives in the securitised paper.

Limited Liquidity & Price risk Presently, secondary market for securitised papers is not very liquid. There is no assurance that a deep secondary market will develop for such securities. This could limit the ability of the investor to resell them. Even if a secondary market develops and sales were to take place, these secondary transactions may be at a discount to the New Fund Price due to changes in the interest rate structure. Limited Recourse, Delinquency and Credit Risk

12

Securitised transactions are normally backed by pool of receivables and credit enhancement as stipulated by the rating agency, which differ from issue to issue. The Credit Enhancement stipulated represents a limited loss cover to the Investors. These Certificates represent an undivided beneficial interest in the underlying receivables and there is no obligation of either the Issuer or the Seller or the originator, or the parent or any affiliate of the Seller, Issuer and Originator. No financial recourse is available to the Certificate Holders against the Investors’ Representative. Delinquencies and credit losses may cause depletion of the amount available under the Credit Enhancement and thereby the Investor Payouts may get affected if the amount available in the Credit Enhancement facility is not enough to cover the shortfall. On persistent default of a Obligor to repay his obligation, the Servicer may repossess and sell the underlying Asset. However many factors may affect, delay or prevent the repossession of such Asset or the length of time required to realize the sale proceeds on such sales. In addition, the price at which such Asset may be sold may be lower than the amount due from that Obligor. Risks due to possible prepayments: Weighted Tenor / Yield Asset securitisation is a process whereby commercial or consumer credits are packaged and sold in the form of financial instruments Full prepayment of underlying loan contract may arise under any of the following circumstances; � Obligor pays the Receivable due from him at any time prior to the scheduled maturity date of that Receivable; or � Receivable is required to be repurchased by the Seller consequent to its inability to rectify a material

misrepresentation with respect to that Receivable; or � The Servicer recognizing a contract as a defaulted contract and hence repossessing the underlying Asset and selling

the same In the event of prepayments, investors may be exposed to changes in tenor and yield.

Bankruptcy of the Originator or Seller If originator becomes subject to bankruptcy proceedings and the court in the bankruptcy proceedings concludes that the sale from originator to Trust was not a sale then an Investor could experience losses or delays in the payments due. All possible care is generally taken in structuring the transaction so as to minimize the risk of the sale to Trust not being construed as a “True Sale”. Legal opinion is normally obtained to the effect that the assignment of Receivables to Trust in trust for and for the benefit of the Investors, as envisaged herein, would constitute a true sale. Bankruptcy of the Investor’s Agent If Investor’s agent, becomes subject to bankruptcy proceedings and the court in the bankruptcy proceedings concludes that the recourse of Investor’s Agent to the assets/receivables is not in its capacity as agent/Trustee but in its personal capacity, then an Investor could experience losses or delays in the payments due under the swap agreement. All possible care is normally taken in structuring the transaction and drafting the underlying documents so as to provide that the assets/receivables if and when held by Investor’s Agent is held as agent and in Trust for the Investors and shall not form part of the personal assets of Investor’s Agent. Legal opinion is normally obtained to the effect that the Investors Agent’s recourse to assets/receivables is restricted in its capacity as agent and trustee and not in its personal capacity. Credit Rating of the Transaction / Certificate The credit rating is not a recommendation to purchase, hold or sell the Certificate in as much as the ratings do not comment on the market price of the Certificate or its suitability to a particular investor. There is no assurance by the rating agency either that the rating will remain at the same level for any given period of time or that the rating will not be lowered or withdrawn entirely by the rating agency. Risk of Co-mingling The Servicers normally deposit all payments received from the Obligors into the Collection Account. However, there could be a time gap between collection by a Servicer and depositing the same into the Collection account especially considering that some of the collections may be in the form of cash. In this interim period, collections from the Loan Agreements may not be segregated from other funds of the Servicer. If the Servicer fails to remit such funds due to Investors, the Investors may be exposed to a potential loss.

13

Due care is normally taken to ensure that the Servicer enjoys highest credit rating on stand alone basis to minimize Co-mingling risk. Investors are urged to study the terms of the Offer Document carefully before investing in this Scheme, and to retain this Offer Document for future reference.

• Investors in the Scheme are not being offered any guaranteed returns.

• Investors are advised to consult their Legal /Tax and other Professional Advisors in regard to tax/legal implications relating to their investments in the Scheme and before making decision to invest in the Scheme or redeem the Units in the Scheme.

14

Sponsors

ICICI Bank Limited Landmark, Race Course Circle, Vadodara 390 007, India

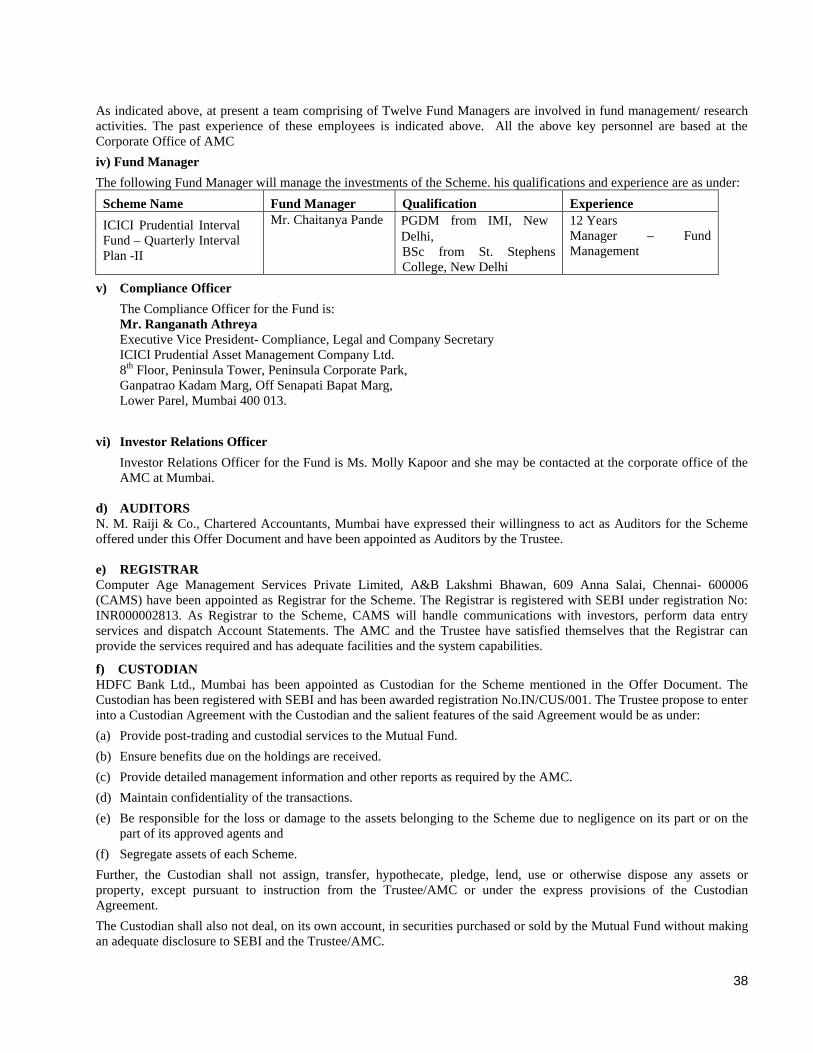

Prudential plc Laurence Pountney Hill, London EC4R DHH, United Kingdom Asset Management Company ICICI Prudential Asset Management Company Limited Registered Office 12th Floor, Narain Manzil, 23 Barakhamba Road, New Delhi – 110 001 Telephone: 011 - 23752515-18 Fax: 011-23358582 Corporate Office 8th Floor, Peninsula Tower, Peninsula Corporate Park, Ganpatrao Kadam Marg, Off Senapati Bapat Marg, Lower Parel, Mumbai 400 013. Telephone: 022 – 24997000 Fax : 022 - 24997029 Trustee ICICI Prudential Trust Limited 12th Floor, Narain Manzil, 23 Barakhamba Road, New Delhi – 110 001 Registrar Computer Age Management Services Private Limited Unit : ICICI Prudential Mutual Fund A& B Lakshmi Bhawan, 609, Anna Salai, Chennai- 600006. Auditors to the Scheme N. M. Raiji & Company Universal Insurance Building Sir Phiroze Shah Mehta Road Mumbai 400 001 Custodian HDFC Bank Ltd, HDFC Bank House Senapati Bapat Marg, Lower Parel, Mumbai- 400013 Legal Advisors A.R.A. LAW Advocates & Solicitors 3/F, Mahatma Gandhi Memorial Building, 7, Netaji Subhash Road, Charni Road (West), Mumbai – 400 004

15

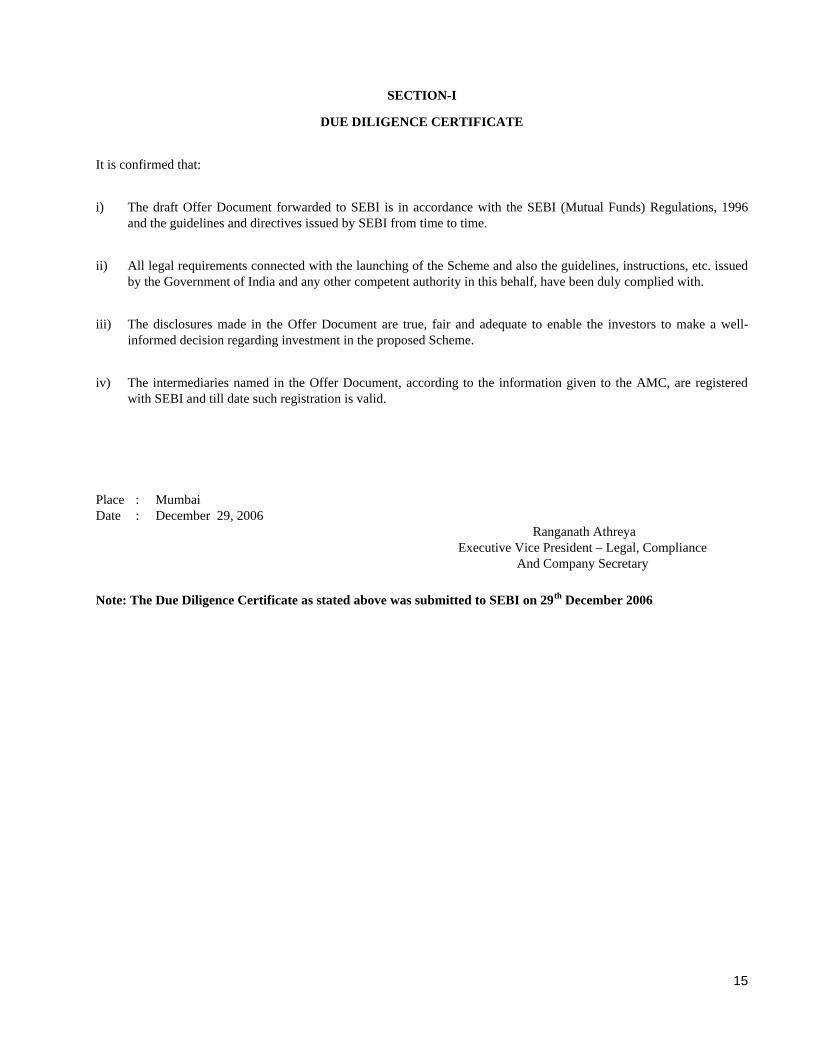

SECTION-I

DUE DILIGENCE CERTIFICATE

It is confirmed that:

i) The draft Offer Document forwarded to SEBI is in accordance with the SEBI (Mutual Funds) Regulations, 1996 and the guidelines and directives issued by SEBI from time to time.

ii) All legal requirements connected with the launching of the Scheme and also the guidelines, instructions, etc. issued by the Government of India and any other competent authority in this behalf, have been duly complied with.

iii) The disclosures made in the Offer Document are true, fair and adequate to enable the investors to make a well-informed decision regarding investment in the proposed Scheme.

iv) The intermediaries named in the Offer Document, according to the information given to the AMC, are registered with SEBI and till date such registration is valid.

Place : Mumbai Date : December 29, 2006 Ranganath Athreya Executive Vice President – Legal, Compliance And Company Secretary

Note: The Due Diligence Certificate as stated above was submitted to SEBI on 29th December 2006

16

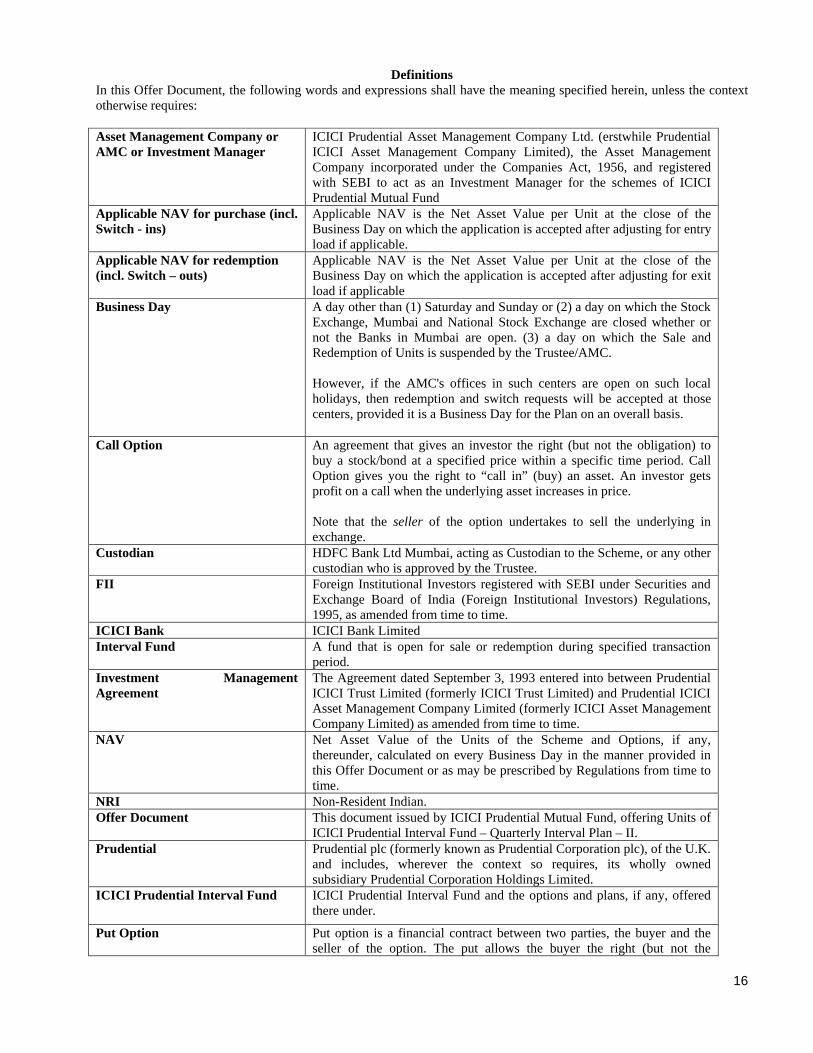

Definitions In this Offer Document, the following words and expressions shall have the meaning specified herein, unless the context otherwise requires: Asset Management Company or AMC or Investment Manager

ICICI Prudential Asset Management Company Ltd. (erstwhile Prudential ICICI Asset Management Company Limited), the Asset Management Company incorporated under the Companies Act, 1956, and registered with SEBI to act as an Investment Manager for the schemes of ICICI Prudential Mutual Fund

Applicable NAV for purchase (incl. Switch - ins)

Applicable NAV is the Net Asset Value per Unit at the close of the Business Day on which the application is accepted after adjusting for entry load if applicable.

Applicable NAV for redemption (incl. Switch – outs)

Applicable NAV is the Net Asset Value per Unit at the close of the Business Day on which the application is accepted after adjusting for exit load if applicable

Business Day A day other than (1) Saturday and Sunday or (2) a day on which the Stock Exchange, Mumbai and National Stock Exchange are closed whether or not the Banks in Mumbai are open. (3) a day on which the Sale and Redemption of Units is suspended by the Trustee/AMC. However, if the AMC's offices in such centers are open on such local holidays, then redemption and switch requests will be accepted at those centers, provided it is a Business Day for the Plan on an overall basis.

Call Option An agreement that gives an investor the right (but not the obligation) to buy a stock/bond at a specified price within a specific time period. Call Option gives you the right to “call in” (buy) an asset. An investor gets profit on a call when the underlying asset increases in price. Note that the seller of the option undertakes to sell the underlying in exchange.

Custodian HDFC Bank Ltd Mumbai, acting as Custodian to the Scheme, or any other custodian who is approved by the Trustee.

FII Foreign Institutional Investors registered with SEBI under Securities and Exchange Board of India (Foreign Institutional Investors) Regulations, 1995, as amended from time to time.

ICICI Bank ICICI Bank Limited Interval Fund A fund that is open for sale or redemption during specified transaction

period. Investment Management Agreement

The Agreement dated September 3, 1993 entered into between Prudential ICICI Trust Limited (formerly ICICI Trust Limited) and Prudential ICICI Asset Management Company Limited (formerly ICICI Asset Management Company Limited) as amended from time to time.

NAV Net Asset Value of the Units of the Scheme and Options, if any, thereunder, calculated on every Business Day in the manner provided in this Offer Document or as may be prescribed by Regulations from time to time.

NRI Non-Resident Indian. Offer Document This document issued by ICICI Prudential Mutual Fund, offering Units of

ICICI Prudential Interval Fund – Quarterly Interval Plan – II. Prudential Prudential plc (formerly known as Prudential Corporation plc), of the U.K.

and includes, wherever the context so requires, its wholly owned subsidiary Prudential Corporation Holdings Limited.

ICICI Prudential Interval Fund ICICI Prudential Interval Fund and the options and plans, if any, offered there under.

Put Option Put option is a financial contract between two parties, the buyer and the seller of the option. The put allows the buyer the right (but not the

17

obligation) to sell a financial instrument (the underlying instrument) to the seller of the option at a certain time for a certain price (the strike price). The seller assumes the corresponding obligations. Note that the seller of the option undertakes to buy the underlying in exchange

RBI Reserve Bank of India, established under the Reserve Bank of India Act, 1934, as amended from time to time.

SEBI Securities and Exchange Board of India established under Securities and Exchange Board of India Act, 1992, as amended from time to time.

The Fund or The Mutual Fund

ICICI Prudential Mutual Fund (formerly Prudential ICICI Mutual Fund), a trust set up under the provisions of the Indian Trusts Act, 1882. The Fund was initially registered with SEBI as ICICI Mutual Fund vide Registration No.MF/003/93/6 dated October 13, 1993and subsequently renamed as Prudential ICICI Mutual Fund. The Fund has obtained approval from SEBI for change in name to ICICI Prudential Mutual Fund vide SEBI’s letter dated IMD/PM/90168/07 dated April 02, 2007.

The Trustee ICICI Prudential Trust Limited (formerly ICICI Trust Limited), a company set up under the Companies Act, 1956, and approved by SEBI to act as the Trustee for the schemes of ICICI Prudential Mutual Fund

The Regulations Securities and Exchange Board of India (Mutual Funds) Regulations, 1996, as amended from time to time.

Trust Deed The Trust Deed dated August 25, 1993 establishing ICICI Mutual Fund, (subsequently renamed ICICI Prudential Mutual Fund) as amended from time to time.

Trust Fund Amounts settled/contributed by the Sponsors towards the corpus of the ICICI Prudential Mutual Fund and additions/accretions thereto.

Unit The interest of an investor, which consists of one undivided share in the Net Assets of the Scheme.

Unit holder A holder of Unit(s) in the scheme of ICICI Prudential Interval Fund as contained in this Offer Document.

18

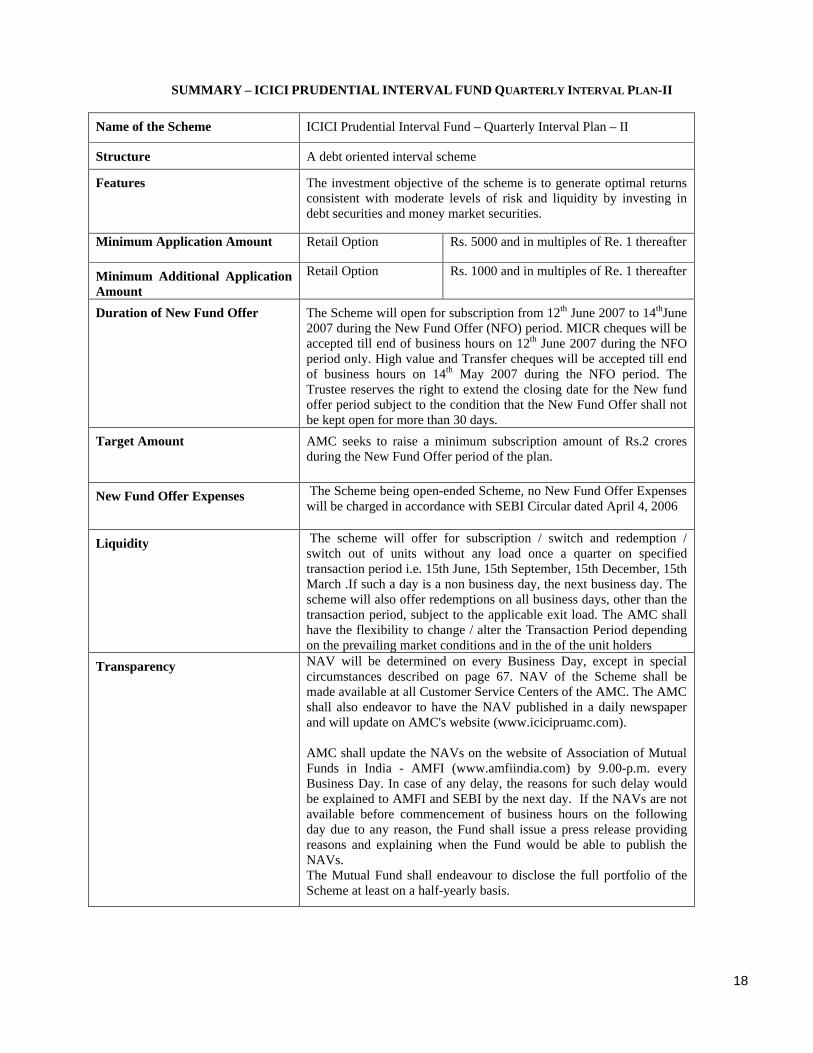

SUMMARY – ICICI PRUDENTIAL INTERVAL FUND QUARTERLY INTERVAL PLAN -II

Name of the Scheme ICICI Prudential Interval Fund – Quarterly Interval Plan – II

Structure A debt oriented interval scheme

Features The investment objective of the scheme is to generate optimal returns consistent with moderate levels of risk and liquidity by investing in debt securities and money market securities.

Minimum Application Amount Retail Option Rs. 5000 and in multiples of Re. 1 thereafter

Minimum Additional Application Amount

Retail Option Rs. 1000 and in multiples of Re. 1 thereafter

Duration of New Fund Offer The Scheme will open for subscription from 12th June 2007 to 14thJune 2007 during the New Fund Offer (NFO) period. MICR cheques will be accepted till end of business hours on 12th June 2007 during the NFO period only. High value and Transfer cheques will be accepted till end of business hours on 14th May 2007 during the NFO period. The Trustee reserves the right to extend the closing date for the New fund offer period subject to the condition that the New Fund Offer shall not be kept open for more than 30 days.

Target Amount AMC seeks to raise a minimum subscription amount of Rs.2 crores during the New Fund Offer period of the plan.

New Fund Offer Expenses The Scheme being open-ended Scheme, no New Fund Offer Expenses will be charged in accordance with SEBI Circular dated April 4, 2006

Liquidity The scheme will offer for subscription / switch and redemption / switch out of units without any load once a quarter on specified transaction period i.e. 15th June, 15th September, 15th December, 15th March .If such a day is a non business day, the next business day. The scheme will also offer redemptions on all business days, other than the transaction period, subject to the applicable exit load. The AMC shall have the flexibility to change / alter the Transaction Period depending on the prevailing market conditions and in the of the unit holders

Transparency NAV will be determined on every Business Day, except in special circumstances described on page 67. NAV of the Scheme shall be made available at all Customer Service Centers of the AMC. The AMC shall also endeavor to have the NAV published in a daily newspaper and will update on AMC's website (www.icicipruamc.com). AMC shall update the NAVs on the website of Association of Mutual Funds in India - AMFI (www.amfiindia.com) by 9.00-p.m. every Business Day. In case of any delay, the reasons for such delay would be explained to AMFI and SEBI by the next day. If the NAVs are not available before commencement of business hours on the following day due to any reason, the Fund shall issue a press release providing reasons and explaining when the Fund would be able to publish the NAVs. The Mutual Fund shall endeavour to disclose the full portfolio of the Scheme at least on a half-yearly basis.

19

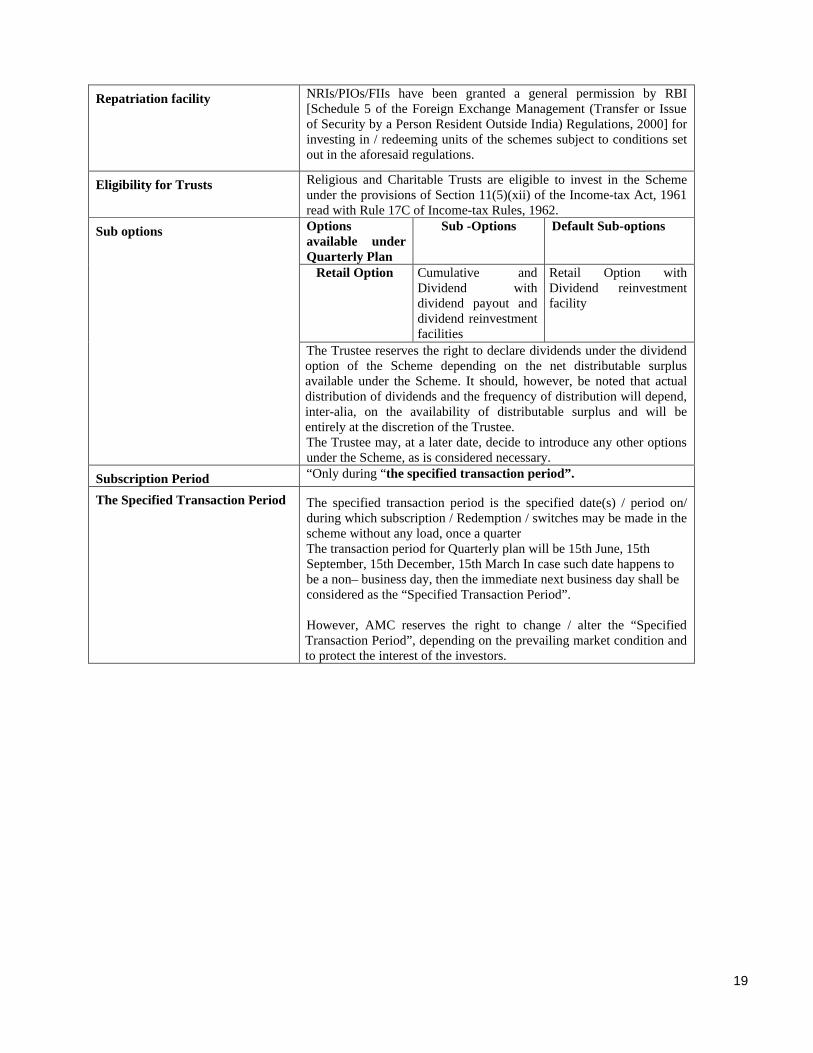

Repatriation facility NRIs/PIOs/FIIs have been granted a general permission by RBI [Schedule 5 of the Foreign Exchange Management (Transfer or Issue of Security by a Person Resident Outside India) Regulations, 2000] for investing in / redeeming units of the schemes subject to conditions set out in the aforesaid regulations.

Eligibility for Trusts Religious and Charitable Trusts are eligible to invest in the Scheme under the provisions of Section 11(5)(xii) of the Income-tax Act, 1961 read with Rule 17C of Income-tax Rules, 1962. Options available under Quarterly Plan

Sub -Options Default Sub-options

Retail Option

Cumulative and Dividend with dividend payout and dividend reinvestment facilities

Retail Option with Dividend reinvestment facility

Sub options

The Trustee reserves the right to declare dividends under the dividend option of the Scheme depending on the net distributable surplus available under the Scheme. It should, however, be noted that actual distribution of dividends and the frequency of distribution will depend, inter-alia, on the availability of distributable surplus and will be entirely at the discretion of the Trustee. The Trustee may, at a later date, decide to introduce any other options under the Scheme, as is considered necessary.

Subscription Period “Only during “the specified transaction period”.

The Specified Transaction Period The specified transaction period is the specified date(s) / period on/ during which subscription / Redemption / switches may be made in the scheme without any load, once a quarter The transaction period for Quarterly plan will be 15th June, 15th September, 15th December, 15th March In case such date happens to be a non– business day, then the immediate next business day shall be considered as the “Specified Transaction Period”. However, AMC reserves the right to change / alter the “Specified Transaction Period”, depending on the prevailing market condition and to protect the interest of the investors.

20

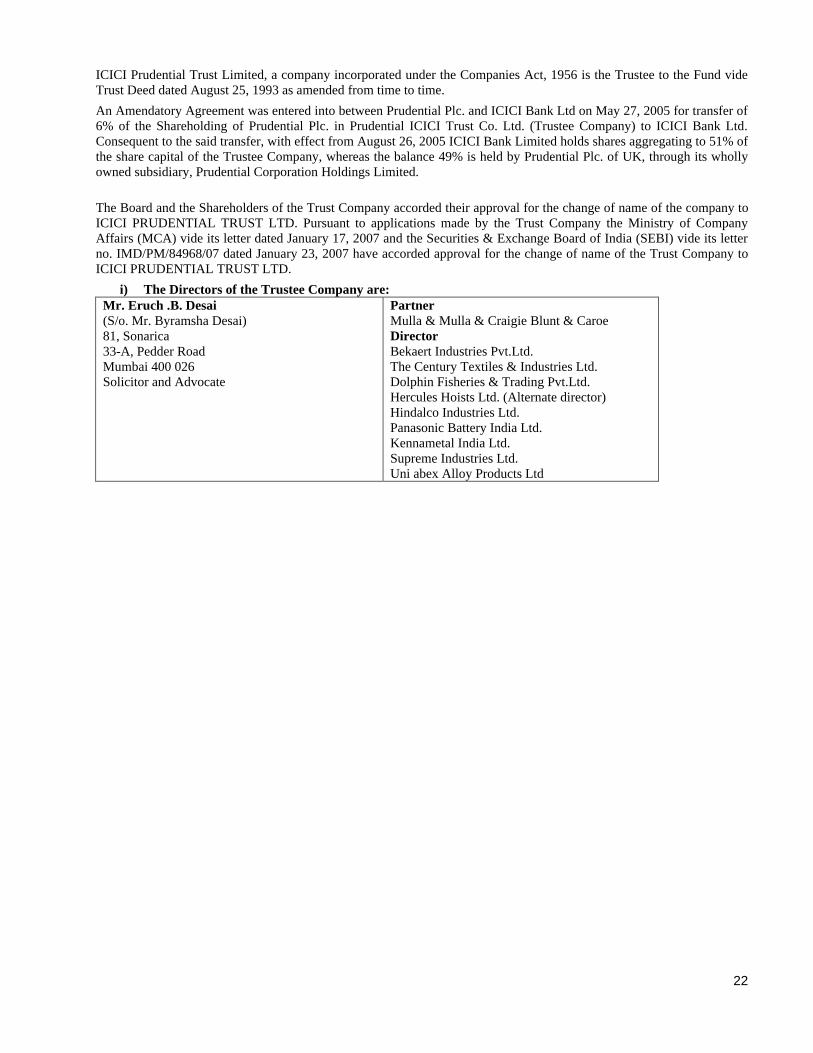

CONSTITUTION OF THE MUTUAL FUND ICICI Mutual Fund, which has been renamed as ICICI Prudential Mutual Fund (“the Mutual Fund” or “the Fund”) has been constituted as a Trust in accordance with the provisions of the Indian Trusts Act, 1882 (2 of 1882). The Mutual Fund was registered with SEBI on October 13, 1993. ICICI Mutual Fund was established by erstwhile ICICI Ltd. (Since merged with ICICI Bank Ltd), by execution of a Trust Deed dated August 25, 1993. Prudential plc, through its wholly owned subsidiary, Prudential Corporation Holdings Limited, has contributed an amount of Rs.12.2 lacs to the corpus of the Fund and has received permission for such contribution from the RBI vide letter No: CO.FID (I) 4940/10/I.07.02.200 (221) 97-98 dated April 25, 1998. SEBI has approved the change in name of the Fund to Prudential ICICI Mutual Fund vide its letter IIMARP / 88 / 98 dated April 16, 1998. A deed of amendment to the Trust Deed dated August 25, 1993 was executed and registered.

An Amendatory Agreement was entered into between Prudential Plc. and ICICI Bank Ltd on May 27, 2005 for transfer of 6% of the Shareholding of Prudential Plc. in Prudential ICICI Asset Management Co. Ltd (AMC) and Prudential ICICI Trust Co. Ltd. (Trustee Company) to ICICI Bank Ltd. Consequent to the said transfer, with effect from August 26, 2005 ICICI Bank Limited holds shares aggregating to 51% of the share capital of AMC and Trustee Company, whereas the balance 49% is held by Prudential Plc. of UK, through its wholly owned subsidiary, Prudential Corporation Holdings Limited. AMC has informed SEBI of the said transfer. SEBI has vide its letter IMD/RK/42692/05 dated June 15, 2005 taken note of the proposed transfer. Consequent to the said transfer the name of the Mutual Fund has been changed to ICICI Prudential Mutual Fund. The approval for the said change has been accorded from SEBI vide its letter no. IMD/PM/90168/07 dated April 02, 2007. Accordingly the names of all the schemes/plans/options of ICICI PRUDENTIAL MUTUAL FUND which are commencing with PRUDENTIAL ICICI now stand changed to ICICI PRUDENTIAL followed by postscript of scheme name as approved by SEBI vide their Letter No- IMD/PM/90170/07 dated April 2, 2007.

a) Sponsors ICICI Bank Limited Securities and Exchange Board of India, vide its letter no. MFD/PM/567/02 dated June 4, 2002, has accorded its approval in recognizing ICICI Bank Ltd. As a co-sponsor consequent to the merger of ICICI Ltd. With ICICI Bank Ltd.

ICICI Bank is India's second-largest bank with total assets of about Rs. 251,389 crores as at March 31, 2006 and profit after tax of Rs. 2540 crores for the year ended March 31, 2006 (Rs. 2005 crores for the year ended March 31, 2005). ICICI Bank has a network of about 614 branches and extension counters and over 2,200 ATMs. ICICI Bank offers a wide range of banking products and financial services to corporate and retail customers through a variety of delivery channels and through its specialised subsidiaries and affiliates in the areas of investment banking, life and non-life insurance, venture capital and asset management. ICICI Bank set up its international banking group in fiscal 2002 to cater to the cross border needs of clients and leverage on its domestic banking strengths to offer products internationally. ICICI Bank currently has subsidiaries in the United Kingdom, Russia and Canada, branches in Singapore, Bahrain, Hong Kong, Sri Lanka and Dubai International Finance Centre and representative offices in the United States, United Arab Emirates, China, South Africa and Bangladesh. UK subsidiary of ICICI Bank has established a branch in Belgium. ICICI Bank is the most valuable bank in India in terms of market capitalisation. (Source: Overview at www.icicibank.com).

ICICI Bank was originally promoted in 1994 by ICICI Limited, an Indian financial institution, and was its wholly-owned subsidiary. ICICI's shareholding in ICICI Bank was reduced to 46% through a public offering of shares in India in fiscal 1998, an equity offering in the form of ADRs listed on the NYSE in fiscal 2000, ICICI Bank's acquisition of Bank of Madura Limited in an all-stock amalgamation in fiscal 2001, and secondary market sales by ICICI to institutional investors in fiscal 2001 and fiscal 2002. ICICI was formed in 1955 at the initiative of the World Bank, the Government of India and representatives of Indian industry.

Pursuant to the Scheme of Amalgamation effective March 30, 2002, among ICICI, ICICI Personal Financial Services, ICICI Capital Services and ICICI Bank, sanctioned by the High Court of Gujarat and the High Court of Judicature at Bombay and approved by the Reserve Bank of India, ICICI, ICICI Personal Financial Services and ICICI Capital Services

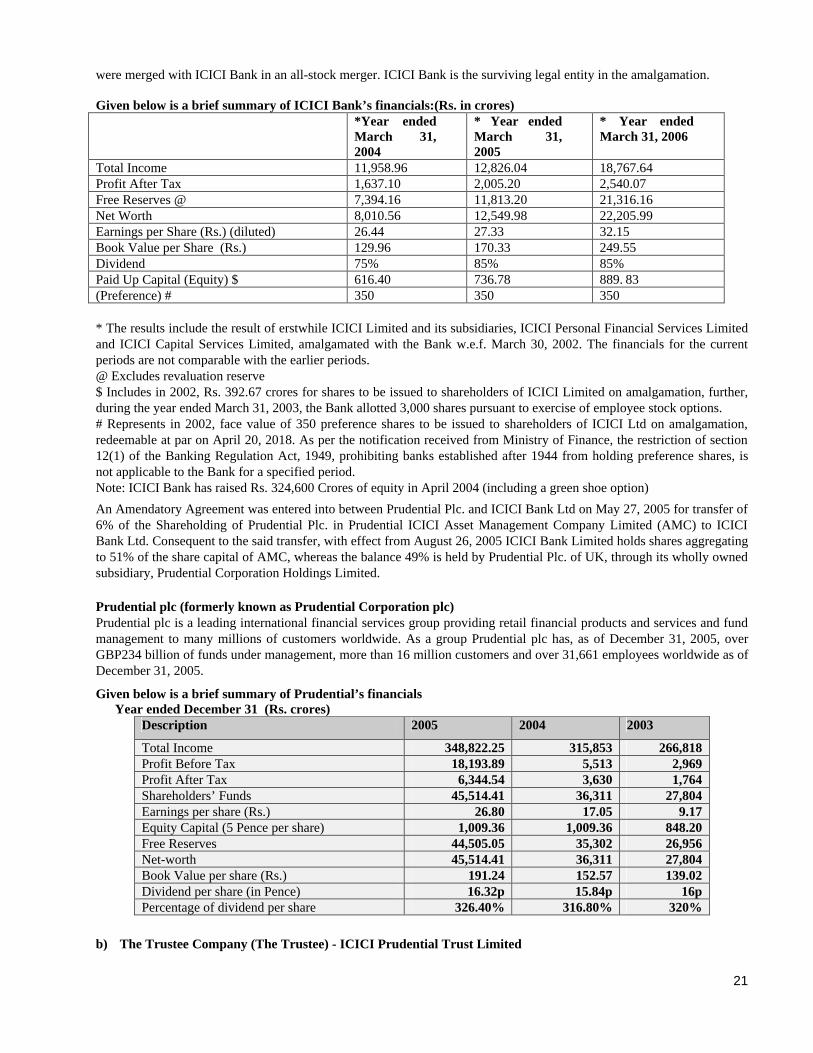

21

were merged with ICICI Bank in an all-stock merger. ICICI Bank is the surviving legal entity in the amalgamation. Given below is a brief summary of ICICI Bank’s financials:(Rs. in crores) *Year ended

March 31, 2004

* Year ended March 31, 2005

* Year ended March 31, 2006

Total Income 11,958.96 12,826.04 18,767.64 Profit After Tax 1,637.10 2,005.20 2,540.07 Free Reserves @ 7,394.16 11,813.20 21,316.16 Net Worth 8,010.56 12,549.98 22,205.99 Earnings per Share (Rs.) (diluted) 26.44 27.33 32.15 Book Value per Share (Rs.) 129.96 170.33 249.55 Dividend 75% 85% 85% Paid Up Capital (Equity) $ 616.40 736.78 889. 83 (Preference) # 350 350 350 * The results include the result of erstwhile ICICI Limited and its subsidiaries, ICICI Personal Financial Services Limited and ICICI Capital Services Limited, amalgamated with the Bank w.e.f. March 30, 2002. The financials for the current periods are not comparable with the earlier periods. @ Excludes revaluation reserve $ Includes in 2002, Rs. 392.67 crores for shares to be issued to shareholders of ICICI Limited on amalgamation, further, during the year ended March 31, 2003, the Bank allotted 3,000 shares pursuant to exercise of employee stock options. # Represents in 2002, face value of 350 preference shares to be issued to shareholders of ICICI Ltd on amalgamation, redeemable at par on April 20, 2018. As per the notification received from Ministry of Finance, the restriction of section 12(1) of the Banking Regulation Act, 1949, prohibiting banks established after 1944 from holding preference shares, is not applicable to the Bank for a specified period. Note: ICICI Bank has raised Rs. 324,600 Crores of equity in April 2004 (including a green shoe option)

An Amendatory Agreement was entered into between Prudential Plc. and ICICI Bank Ltd on May 27, 2005 for transfer of 6% of the Shareholding of Prudential Plc. in Prudential ICICI Asset Management Company Limited (AMC) to ICICI Bank Ltd. Consequent to the said transfer, with effect from August 26, 2005 ICICI Bank Limited holds shares aggregating to 51% of the share capital of AMC, whereas the balance 49% is held by Prudential Plc. of UK, through its wholly owned subsidiary, Prudential Corporation Holdings Limited.

Prudential plc (formerly known as Prudential Corporation plc) Prudential plc is a leading international financial services group providing retail financial products and services and fund management to many millions of customers worldwide. As a group Prudential plc has, as of December 31, 2005, over GBP234 billion of funds under management, more than 16 million customers and over 31,661 employees worldwide as of December 31, 2005.

Given below is a brief summary of Prudential’s financials Year ended December 31 (Rs. crores)

Description 2005 2004 2003

Total Income 348,822.25 315,853 266,818 Profit Before Tax 18,193.89 5,513 2,969 Profit After Tax 6,344.54 3,630 1,764 Shareholders’ Funds 45,514.41 36,311 27,804 Earnings per share (Rs.) 26.80 17.05 9.17 Equity Capital (5 Pence per share) 1,009.36 1,009.36 848.20 Free Reserves 44,505.05 35,302 26,956 Net-worth 45,514.41 36,311 27,804 Book Value per share (Rs.) 191.24 152.57 139.02 Dividend per share (in Pence) 16.32p 15.84p 16p Percentage of dividend per share 326.40% 316.80% 320%

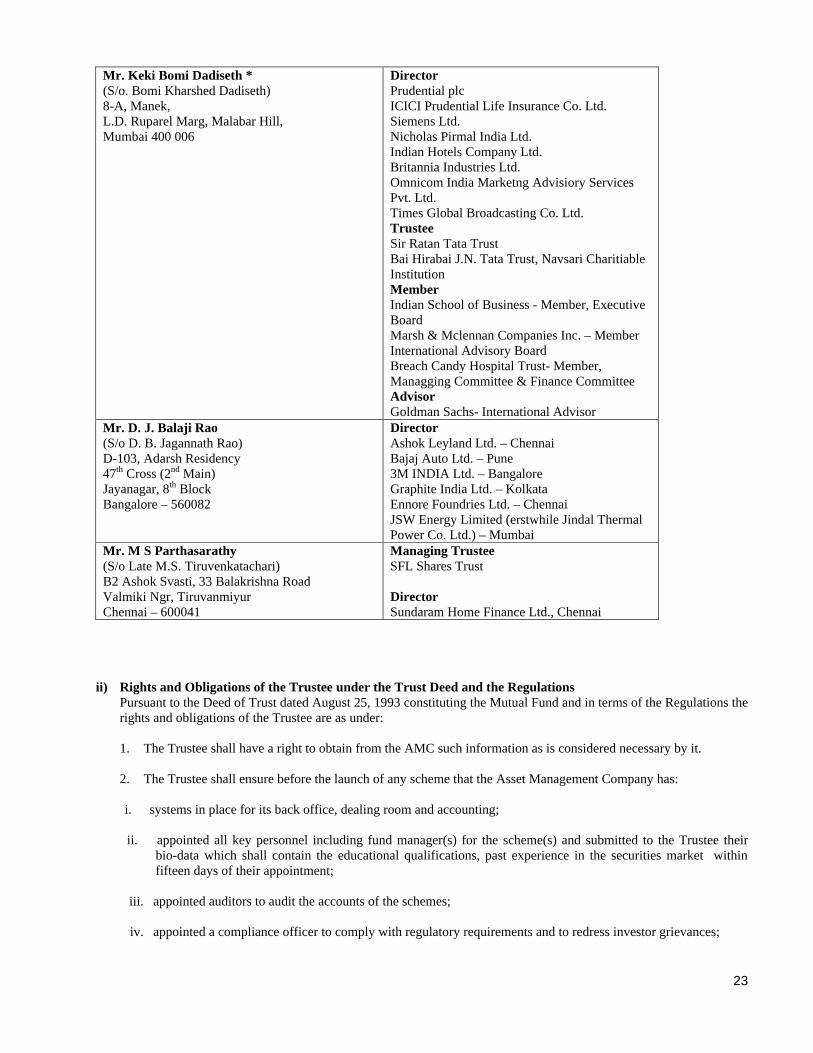

b) The Trustee Company (The Trustee) - ICICI Prudential Trust Limited

22