IIA Meeting – Measuring IA value and performance

February 12, 2016

Jen Carlson, EY Advisory Services Senior

Manager

Page 1 Measuring IA value and performance

Contents

► Introduction

► Defining the value of Internal Audit (IA)

► Measuring value and performance-metrics matter

► Communicating effectively

► Appendix

Page 2 Measuring IA value and performance

Polling question #1

► What is your current role?

A. Internal Audit leadership/(S)VP/director

B. Internal Audit manager/leader

C. Internal Audit staff

D. Internal Audit co-source provider

Page 3 Measuring IA value and performance

Introduction

Page 4 Measuring IA value and performance

What is value?

► How IA value is perceived by an organization can be

influenced by a number of factors:

► Corporate culture

► Scale, complexity and nature of the business

► Organizational structure

► Regulatory requirements

► Competitive pressures

Value is in the eye of the beholder!

Page 5 Measuring IA value and performance

The IA value proposition

Internal Audit:

► Provides assurance on the

organization’s governance, risk

management and control processes

to support the achievement of

enterprise goals

► Analyzes and assesses data and

business processes to offer insights

and recommendations for improved

efficiency and effectiveness

► Commits to honesty and integrity and

serves as an objective source of

independent advice

IIA Internal Audit value

proposition

Source: The IIA’s Internal Audit Value

Proposition graphic

Page 6 Measuring IA value and performance

What if Internal Audit was a valued business advisor?

Audit committee and executive

management expectations

Strategic and business

line goals

Mandate for Internal Audit

Strategic and valued advisor

Internal Audit function serves as a subject matter

specialist to business management around strategic

initiatives, challenges and changes in the organization.

The function has the people, knowledge and experiences

to effectively provide this level of service.

Business insight

In addition to covering the “basics,” the Internal Audit

function is designed to provide high-quality, relevant

business insight as an integral part of its activities.

Business insight is not a by-product, but an explicit

outcome from the function’s activities.

Non-negotiable

Control and compliance monitoring structure

Internal Audit function focused on evaluating the design

and the effectiveness of internal controls in those areas

outlined in their charter or mandate. Also includes focusing

on compliance with key regulations and policies.

Page 7 Measuring IA value and performance

Polling question #2

► How would you describe your IA department’s

focus today?

A. Offer strategic advice plus provide business insights and

cover control and compliance activities

B. Provide business insights plus cover control and

compliance activities

C. Evaluate control and compliance activities

Page 8 Measuring IA value and performance

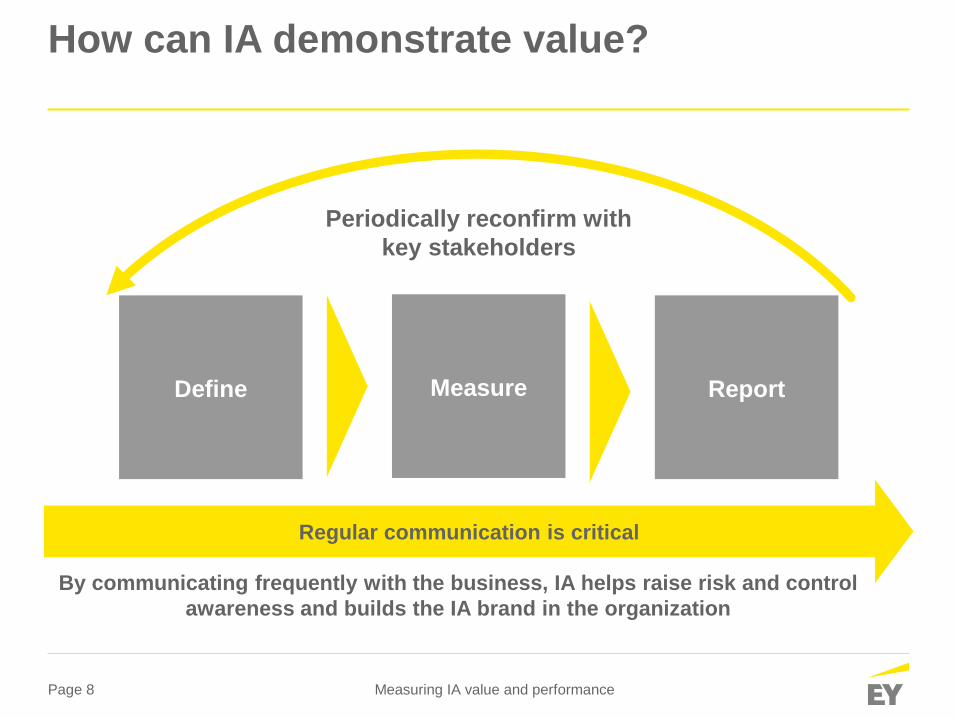

How can IA demonstrate value?

Regular communication is critical

Periodically reconfirm with

key stakeholders

Define Measure Report

By communicating frequently with the business, IA helps raise risk and control

awareness and builds the IA brand in the organization

Page 9 Measuring IA value and performance

Defining the value of IA

Page 10 Measuring IA value and performance

Defining value

► How can IA define its value?

► Understand who the stakeholders are, for example:

► Audit committee

► Executive management

► Business line management

► Other risk/insurance/compliance functions

► Regulators

► External auditors

► Conduct interviews to learn what they expect from IA:

► Not all stakeholders are created equal, but all perspectives are helpful

when defining value.

► Develop a list of value-adding activities based on input from

various stakeholders with special emphasis on key stakeholders

(e.g., audit committee and executive management)

Page 11 Measuring IA value and performance

Defining value

► How can IA define its value?

► Add proactive IA activities that go beyond core traditional IA

activities that will add value

► Validate the list with key stakeholders and agree on what

constitutes true value

► Agree on a mandate with the audit committee and

executive management

► Verify that the mandate is reflected in the IA Charter

Page 12 Measuring IA value and performance

A balancing act Meeting stakeholder expectations

► As stakeholders demand more, IA needs to align its focus to these expectations.

Focus will be balanced not just on the assurance activities historically incorporated in

audit plans, but also to continue to increase advisory activities that drive business

insights and serve as a source of independent advice.

► Finding that balance is unique to each organization and its strategic objectives.

► This balance does not become stagnant, but continually teeters between the two as

objectives change.

AdvisoryAssuranceInternal Audit

mandate

Internal Audit needs to be nimble and flexible in order to respond to the changing environment.

Page 13 Measuring IA value and performance

Value-add activities to consider

Case studyA global IA department includes time for a balanced set of activities in its

annual strategic plan. A sample of activities include:

► Factors strategic risks in its risk assessment and audit plan

► Proactively reviews control design during large system

development projects

► Conducts monthly lunch and learn events for the organization

► Offers internal online courses on risk and control

► Establishes regular meetings with stakeholders to keep abreast of

changing priorities and build relationships

Strategic transactions

Plan to participate, evaluate risks and/or

review the design of controls throughout

the project

Triggering events may include:

► Mergers, acquisitions or divestitures

► New product launch

► Patent expiry

► Litigation

Risk and control

awareness sessions

Provide periodic

sessions to the business

around risks and controls

of significance to the

organization

Strategic risks

There appears to be a

significant disconnect

between the risks that

can have the most

significant impact on

the organization and

the amount of time IA

spends on those risks. Source: Executive Guidance: Reducing Risk Management’s

Organizational Drag, CEB, Inc. 2014

% of strategic risk failure

leading to a significant

market decline

% of time IA

spends on

strategic risks

86% 6%

Page 14 Measuring IA value and performance

Value-add activities to consider

Case studyAn IA department in a large institution formally devotes a portion of its available hours to

identifying emerging risks and their implications to the business. IA then discusses the

issue, risk implications and opportunities with the business. A sample of the risk

categories include:

► Cyber threats and recent events in the marketplace

► Changes to the geopolitical and/or economic landscape that might

impact the organization

► Changes in emerging markets where the organization does business

► Competitor innovations and their implications to the organization

► Events that might impact the company’s reputation

Emerging risks

IA needs to become the

forward-looking “eyes” of

management and the

board, offering visibility not

only into the risks they

know and monitor today,

but also where risks may

emerge or evolve as the

business continues to

change, e.g., cyber, use of

third parties, social media

and business continuity.

Leading practice – IA

helps management seize

the upside potential

associated with

emerging risks by

working with them to

identify, assess and

determine risk

tolerances.

Source: “There’s no reward without risk: EY’s global governance, risk and compliance survey 2015”

of respondents evaluate their

organization’s risk profile on an annual

basis, limiting their ability to adjust their

business strategy based on changes to

their risk landscape.

77%

of respondents only prepare

management dashboards annually or

quarterly, indicating further opportunity

exists to provide decision-makers with

vital risk insights.

78%

of respondents do not

produce a report, or only

prepare an integrated risk

management

report annually.

65%

Page 15 Measuring IA value and performance

Value-add activities to consider

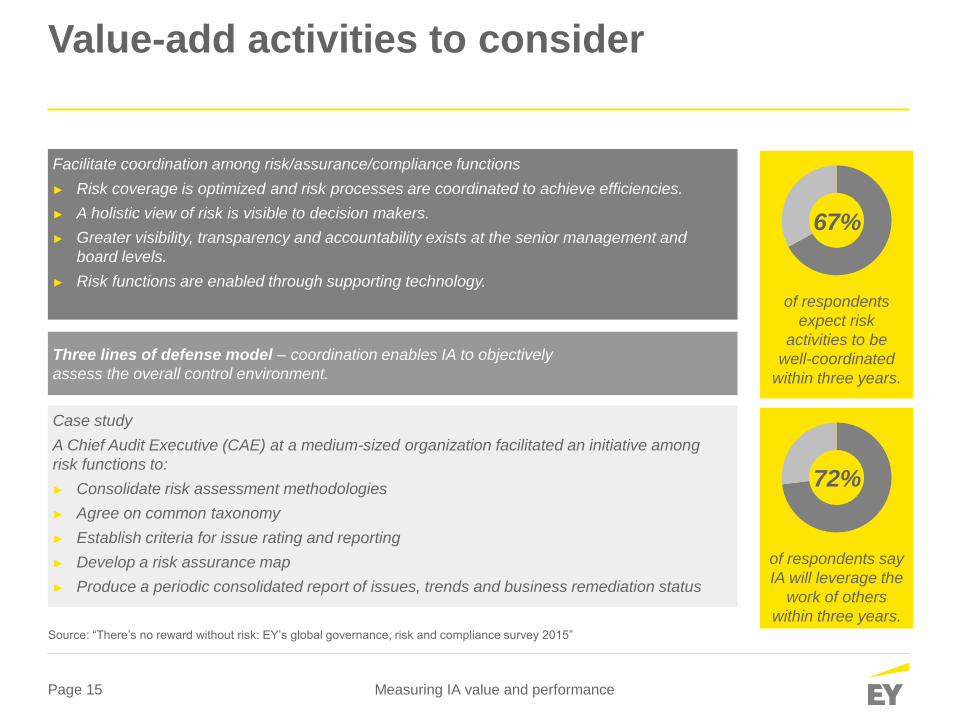

Case study

A Chief Audit Executive (CAE) at a medium-sized organization facilitated an initiative among

risk functions to:

► Consolidate risk assessment methodologies

► Agree on common taxonomy

► Establish criteria for issue rating and reporting

► Develop a risk assurance map

► Produce a periodic consolidated report of issues, trends and business remediation status

Facilitate coordination among risk/assurance/compliance functions

► Risk coverage is optimized and risk processes are coordinated to achieve efficiencies.

► A holistic view of risk is visible to decision makers.

► Greater visibility, transparency and accountability exists at the senior management and

board levels.

► Risk functions are enabled through supporting technology.

Three lines of defense model – coordination enables IA to objectively

assess the overall control environment.

of respondents say

IA will leverage the

work of others

within three years.

of respondents

expect risk

activities to be

well-coordinated

within three years.

Source: “There’s no reward without risk: EY’s global governance, risk and compliance survey 2015”

67%

72%

Page 16 Measuring IA value and performance

Measuring value – metrics matter

Page 17 Measuring IA value and performance

Metrics matter

“What gets measured gets done, what gets

measured and fed back gets done well, what

gets repeated gets rewarded.”John E. Jones, noted author and leadership trainer

Page 18 Measuring IA value and performance

Metrics matter

► Metrics do more than set goals:

► They effectively communicate priorities.

► They help drive behavior.

► Metrics that do not align with the organization’s goals can

make those goals harder to reach.

► Metrics should be aligned with IA’s mandate to facilitate

delivering value.

► Effective metrics increase employee motivation

and satisfaction.

Page 19 Measuring IA value and performance

Is there a measurement gap?

of CAEs surveyed say

informing and advising the

audit committee bring the

most value.

of CAEs surveyed say

they have no formal

measures of value.

1. Assuring the adequacy and

effectiveness of the internal

control system (86%)

2. Recommending business

improvement (55%)

3. Assuring the organization’s

risk management

processes (53%)

4. Assuring regulatory

compliance (50%)

5. Informing and advising

management (40%)

1. Percentage of audit plan

complete (66%)

2. Timely closure of

audit issues (42%)

3. Completion of mandated

coverage (41%)

4. Client satisfaction

goals (38%)

5. The fulfillment of specific

expectations set and agreed

to with key stakeholders

(32%)

Top five IA activities that bring

the most value*

Top five IA

performance measures*

* Chief audit executive responses

Source: Delivering on the promise: Measuring Internal Audit Value and Performance, IIA CBOK 2015

15%

28%

Page 20 Measuring IA value and performance

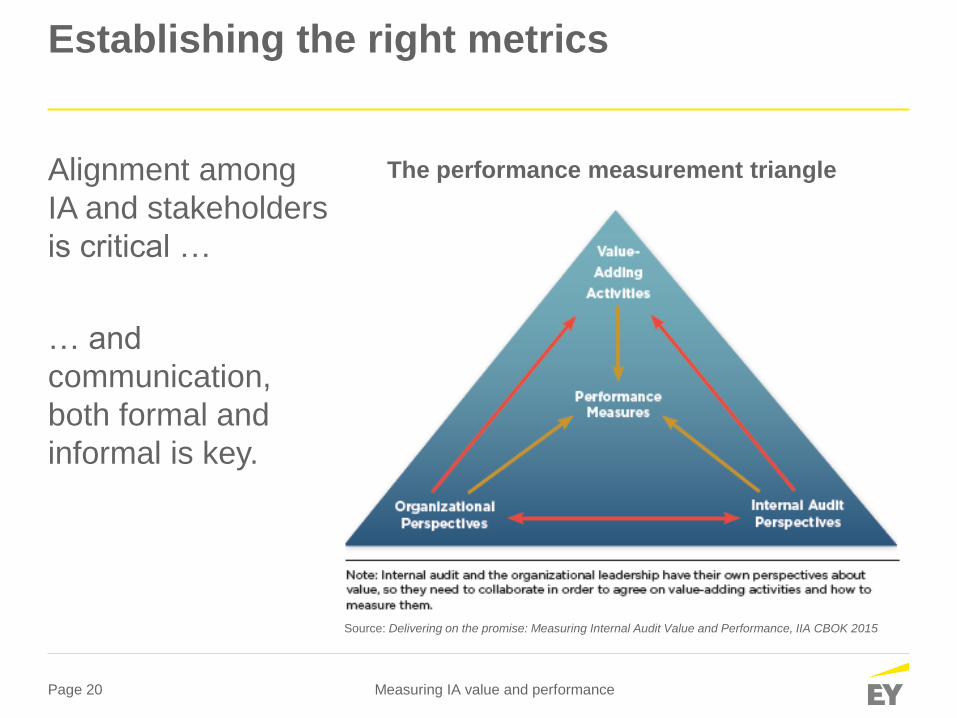

Establishing the right metrics

Alignment among

IA and stakeholders

is critical …

… and

communication,

both formal and

informal is key.

The performance measurement triangle

Source: Delivering on the promise: Measuring Internal Audit Value and Performance, IIA CBOK 2015

Page 21 Measuring IA value and performance

Closing the measurement gap

► Develop specific, measurable (quantitative and/or qualitative) metrics

that address stakeholder expectations and operational aspects of the

department (operate like a business)

Moving to a more balanced approach

► Traditional metrics:

► Audit plan completion

► Risk areas covered

► Utilization rate

► Training hours

► Audit cycle time

► Additional metrics:

► Leading practices shared

► Substantive conversations

► Design of

controls evaluation

► Leadership development

► Trends and issues identified

Page 22 Measuring IA value and performance

IA value scorecard Track and evaluate value delivered through KPIs

Utilization

Leading practices

implemented

Cost savings

realized

Training

Audit plan

completion

Tra

dit

ion

al IA

KP

IsE

me

rgin

g IA

KP

Is

Risk areas covered

At or above targetUnderutilized

100% complianceNo training

Compliance only Leading practices

above target

No quantified cost

savings

Cost savings above

target

Significantly delayed

program

100% audit completion

Compromised risk

coverage

100% risk coverage

Is our team fully utilized at all levels within the

IA function?

How many IA recommendations on leading

practices were implemented by business?

What cost savings has IA identified through

control efficiencies or operational

recommendations?

Has the IA team completed training, CPE

credits and appropriate certifications?

What percent of the audit plan been

completed?

Have all significant risks been monitored by IA

through the audit plan?

Benchmarking and

business insight

What type of external business insight and

industry benchmarking is brought to the

business by IA?

No external

insightsBenchmarking on all

targeted areas

Assessment of key performance indicator (KPI)

Subject-matter

resources

What percent of the audit plan makes use of

subject-matter resources to increase audit

depth/value?

General IA

team onlySMRs brought into all

targeted audits

Illustrative

Page 23 Measuring IA value and performance

Consider a self-assessment model

How is your IA function positioned to deliver and demonstrate value?

Focus area Basic Evolving Established Advanced Leading

Stakeholder

expectations

Expectations of IA stakeholders

may not be fully understood.

IA purpose and mandate is directly

aligned with stakeholder expectations.

Mandate IA strategy and objectives are

narrowly defined with little or no

input from executive management

or the audit committee.

IA strategy, objectives and value

contribution to the business are co-

developed with executive management

and the audit committee and are fully

aligned with organizational strategies

and business objectives.

Communication

with key

stakeholders

Communication may be limited,

infrequent and/or focused only on

IA results.

IA communication with the audit

committee, executive management and

the business occurs on a regular basis

and includes discussions of emerging

risks, trends and leading control

practices.

Leadership

development

Job rotation assignments between

internal audit and the business are

ad hoc.

IA plays a key role in the organization’s

leadership development program as

critical step of a formal job rotation

program.

Illustrative

Page 24 Measuring IA value and performance

Consider a self-assessment model

Focus area Basic Evolving Established Advanced Leading

IA enabled

business

performance

IA activities are primarily focused

on controls and compliance.

IA focuses on risks that would inhibit

achievement of business objectives,

enable value creation and support cost

reduction.

People IA does not utilize a people model

to identify and align skills with key

risk areas and internal/external

stakeholder expectations.

The IA function utilizes a formalized

people model to document skills by

level and align skills with key risk areas

and internal/external stakeholder

expectations.

Methods Audit needs assessment does not

reflect the business strategy and

risk profile.

Integration of risk assessment/audit

planning and IA activities including

periodic updates to the audit needs

assessment.

Technology

enablement

IA utilizes basic tools and

technology providing limited

efficiency and leverage.

IA utilizes leading edge tools and

technologies which enable

effective/efficient work streams,

collaborative efforts and efficient

knowledge exchange.

How is your IA function positioned to deliver and demonstrate value?

Illustrative

Page 25 Measuring IA value and performance

Communicating effectively

Page 26 Measuring IA value and performance

Communicating effectively

► Align with the IIA’s International Professional Practices Framework

(IPPF) Core Principles that call for IA to:

► Communicate effectively

► Be insightful, proactive and future-focused

► Align with the strategies, objectives and risks of the organization

► Consider these attributes of effective communication:

► Demonstrates and communicates that IA is bringing value to the table

► Is not an annual exercise – should be in the “rhythm of the business”

► Must be formal and informal – oral and “in writing”

► Must be at the level and depth of interest to the “audience”

► Establishes communication protocols that foster open discussions with

management and other key stakeholders

► Revisits expectations and discuss IA’s progress towards meeting them

Page 27 Measuring IA value and performance

Communicating effectively

Communication with the business and

other risk/compliance functions Communication with the IA staff

Benefits:

► Provides the opportunity to move

beyond IA’s traditional role

► Builds relationships and trust

► Encourages coordination

► Helps change the culture

Benefits:

► Explains the value of metrics

► Gains buy-in on performance metrics

► Builds relationships and trust among

the staff

► Encourages coordination with others

Consider:

► Planning regular meetings to discuss

the business

► Periodic written reports concerning

audit activities

Consider:

► Regular staff meetings to discuss the

“state of internal audit activities”

► Encouraging staff to participate in

Corporate activities (e.g., charitable

events to build relationships with

colleagues beyond IA)

Page 28 Measuring IA value and performance

Communicating effectively

Communication with the audit committee and executive management

Develop a communication plan to meet regularly with members of executive management

and the audit committee chair

Sample topics to be discussed:

► Discussion of major risk trends and their implications (e.g., external events, major

system development implementations, significant management changes)

► IA issue trends, remediation status and implications

► Business insights and improvement opportunities noted

► Notable IA accomplishments/changes

► Upcoming IA projects

► Changes to the business and their impact on the IA plan

Page 29 Measuring IA value and performance

Audit committee reporting considerations

► Consider corporate culture and reporting norms

► Address stakeholder expectations and call out as appropriate

► Include qualitative and quantitative information and metrics

► Reflect key issues, trends noted, emerging risks and areas of focus

► Keep report at a relatively high level and provide details in an appendix

► Consider using a balanced scorecard or dashboard

Tips for presentation and display

► Use graphics, e.g., pie charts, bar

charts, wherever possible to

concisely deliver the message

► Establish a calendar of information

to be reported, to whom and when

► Develop a template for consistency

and comparison

Page 30 Measuring IA value and performance

Appendix

Page 31 Measuring IA value and performance

Potential key performance indicators

Objective Category Measurement

Lead

ers

hip

/bu

sin

ess

ad

vis

or

Leader development ► # IA staff promoted within IA

► IA is active participant in a leadership rotation program

► # IA alumni promoted within company

► # IA alumni at XX rank or XX salary grade

► # company staff seconded to IA

► IA viewed as the steward and first rotation of college recruitment program

for finance

Strategic alignment ► # audits that are aligned with key strategic initiatives

Audit committee/executive management

satisfaction survey

► Average overall ratings from each group

► Improvement from prior year

Benchmarking and business insight ► What external business insights and industry benchmarking is brought to

the business by IA

Management requests ► # of ad hoc management requests added to audit plan

Leading practices implemented ► How many IA recommendations on leading practices were implemented by

business

Executive interaction ► # interactions of IA leaders (CAE, directors, managers) with key executives

(as defined)

► #/% AC meetings attended by IA

Items marked in bold indicate emerging KPIs

Page 32 Measuring IA value and performance

Potential key performance indicators

Objective Category Measurement

Au

dit

eff

ecti

ven

ess

Risk areas covered ► % significant risks (as defined) addressed by IA plan

► New key business risks identified by IA

► Percentage of high, medium and low risk areas covered

Risk assessment ► Risk assessment coordinated with other risk/control compliance functions

► Risk assessment refresh performed as defined

Involvement of subject matter

resources (SMR)

internal or external to the company

► # audits that include SMRs

► % of audits with SMRs

► SMR participation across audit life cycle (hrs/%)

Quality Assurance and Improvement

Program (QAIP)

Internal

► #/% audits reviewed

► #/% audits with findings

► #/% findings that remain unresolved

► #/% recurring findings

► Annual review of IA Charter

QAIP

External

► Conformance opinion

► External assessment conducted within five years

Customer satisfaction ► Results of interviews conducted by objective third party – internal or

external to the company

► Average satisfaction survey rating from customers

► Improvement over prior year

► Customer response rate

Items marked in bold indicate emerging KPIs

Page 33 Measuring IA value and performance

Potential key performance indicators

Objective Category Measurement

Au

dit

eff

icie

ncy

Audit plan completion ► # audits budgeted

► #/% of audit plan completed

► #/% of audits completed on time (as defined)

► # adjustments to the audit plan (add, cancel, defer, combine)

Audit cycle ► Total audit cycle time (days)

► Average # days for audit fieldwork (as defined)

► Average days to issue final report

► #/% audit results ratings (green, yellow, red)

Leverage ► # of findings that repeat across segments/business units

► # audits coordinated with other risk functions

► # repeat CAATs used by other audit teams

► # audits coordinated with external auditor

Audit costs ► Average costs per audit

► Average costs per auditor

► Travel as % of total department costs

► % of audits completed on budget (hrs and $)

► Actual hours as % of budgeted hours

► Actual $ as % of budgeted $

Technology enablement ► % of audits using data analytics

► % of audits using CAATs

Items marked in bold indicate emerging KPIs

Page 34 Measuring IA value and performance

Potential key performance indicators

Objective Category Measurement

Bu

sin

ess p

rocess im

pro

vem

en

t

Business process improvements

implemented

► %/# of process improvements recommended

► %/# of process improvements adopted by BU

► % of recommendations completed within agreed timing

► % of recommendations completed before original planned date

► # issues still open by audit plan year

► Average # days to close recommendations

► # of findings that repeat across segments/Bus

Cost savings realized ► Estimated $ cost savings identified through control efficiencies or

operational recommendations

► # recommendations that would result in cost reductions, stop revenue

leakage, improve working capital, control CAPEX, etc.

► Removal of redundant or ineffective controls

► # of audit procedures leveraging work of other risk/assurance/

compliance functions

Items marked in bold indicate emerging KPIs

Page 35 Measuring IA value and performance

Potential key performance indicators

Objective Category Measurement

Peo

ple

Utilization ► % of available hours on audits (by level)

► % of hours chargeable to audit project

► % of nights in hotel per five-day week

Certification ► % of staff certified

► Certifications held (by level)

Staff experience ► Years of experience in IA (by level)

► Years of industry experience (by level)

► % employees with industry experience

Turnover ► # staff transferred to roles in business

► # staff transferred from the business

► # staff leaving company

► # new hires

► Turnover rate (internal and external)

Staff development ► # hours training/CPE credits

► % feedback completed and delivered on time

► # “learning experiences” per auditor (e.g., participating in audit of particular BU

or around particular issue)

► # of business related courses attended

Employee satisfaction survey ► % satisfaction (by level)

► % improvement over prior year

Items marked in bold indicate emerging KPIs

Page 36 Measuring IA value and performance

Questions?

EY | Assurance | Tax | Transactions | Advisory

About EY

EY is a global leader in assurance, tax, transaction and advisory

services. The insights and quality services we deliver help build trust

and confidence in the capital markets and in economies the world

over. We develop outstanding leaders who team to deliver on our

promises to all of our stakeholders. In so doing, we play a critical role

in building a better working world for our people, for our clients and

for our communities.

EY refers to the global organization, and may refer to one

or more, of the member firms of Ernst & Young Global Limited,

each of which is a separate legal entity. Ernst & Young

Global Limited, a UK company limited by guarantee, does not

provide services to clients. For more information about our

organization, please visit ey.com.

Ernst & Young LLP is a client-serving member firm of

Ernst & Young Global Limited operating in the US.

© 2016 Ernst & Young LLP.

All Rights Reserved.

1602-1820683

ED None

This material has been prepared for general informational purposes

only and is not intended to be relied upon as accounting, tax or other

professional advice. Please refer to your advisors for specific advice.

ey.com

Recommended

![10. S · 10. s is - 2s - 1 (ia) _____ _____ 2 (iia) [ ] ns1 _____ _____ [ ] ns2+1 _____ _____ + 2](https://img.pdfslide.us/doc/110x75/5be5233109d3f2f9648d879f/10-s-10-s-is-2s-1-ia-2-iia-ns1-ns21.jpg)