HUD’s Rental Assistance

Demonstration (“RAD”) Program

Panelists Carol Oster, Development Manager, Rochester’s Cornerstone Group LTD. Rochester, NY based affordable housing development firm, consulting/partnering with public housing agencies for real estate redevelopment/new construction and asset management.

Greg Bryne, Senior Project Manager, Rental Assistance Demonstration Program, Office of Public and

Indian Housing. HUD Washington, DC coordinating implementation of HUD’s Rental Assistance Demonstration

(RAD) Program.

Michael Tonovitz, Vice President, CVR Associates, Inc. Tampa, Florida based affordable housing consulting firm focusing on organizational efficiencies by providing technical assistance and program management to Public Housing and Housing Choice Voucher Programs.

Michael Reardon, Partner Nixon Peabody LLC Washington, DC office representing public agencies on affordable housing issues and affordable real estate transactions. Prior to joining Nixon Peabody LLP, Mr. Reardon was Assistant General Counsel for Assisted Housing at HUD.

Robin Rubado, Asset Manager, Rochester’s Cornerstone Group

Rochester, NY based affordable housing development firm, consulting/partnering with public housing agencies for real estate redevelopment/new construction and asset management.

RAD Track Overview Five panelists present (Q & A following each section):

1) RAD Program Overview 2) PHA considerations for RAD transactions 3) Financing for RAD conversions, rehabilitation

and/or new construction 4) Legal considerations for RAD transactions 5) Asset Management 6) RAD application and timeline 7) RAD Inventory Assessment Tool Demo & Final

Q & A

– Build on the proven Section 8 platform

– Leverage private capital to preserve assets

– Offer residents greater choice and mobility

Key RAD Goals

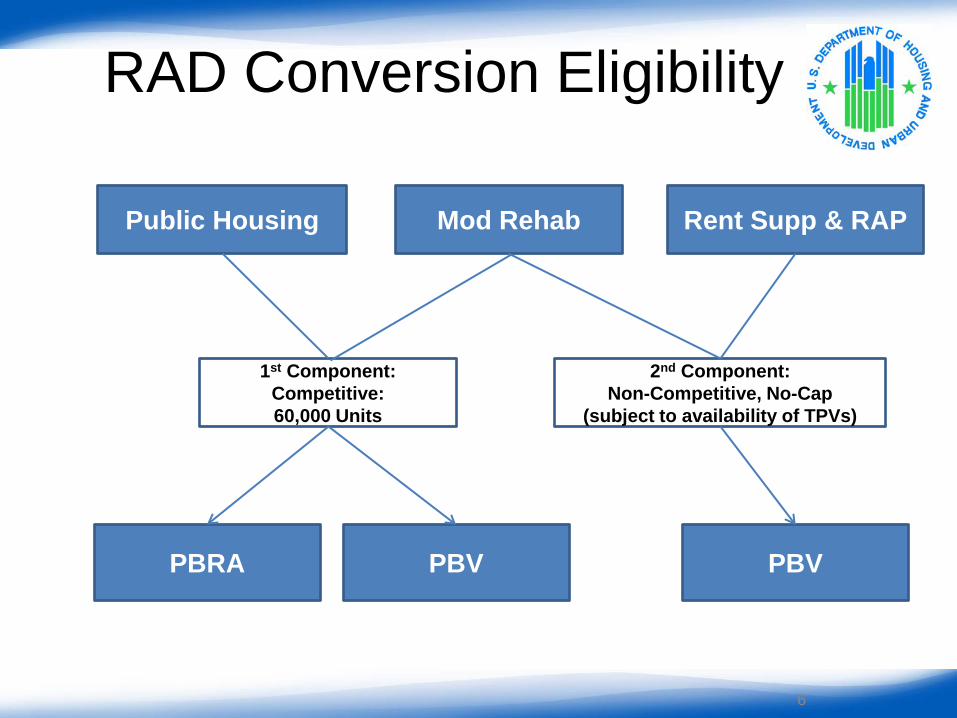

RAD Conversion Eligibility

Public Housing Mod Rehab Rent Supp & RAP

1st Component: Competitive: 60,000 Units

PBRA PBV

2nd Component: Non-Competitive, No-Cap

(subject to availability of TPVs)

PBV

6

Public Housing Conversion Rent Levels

ACC Section 8 7

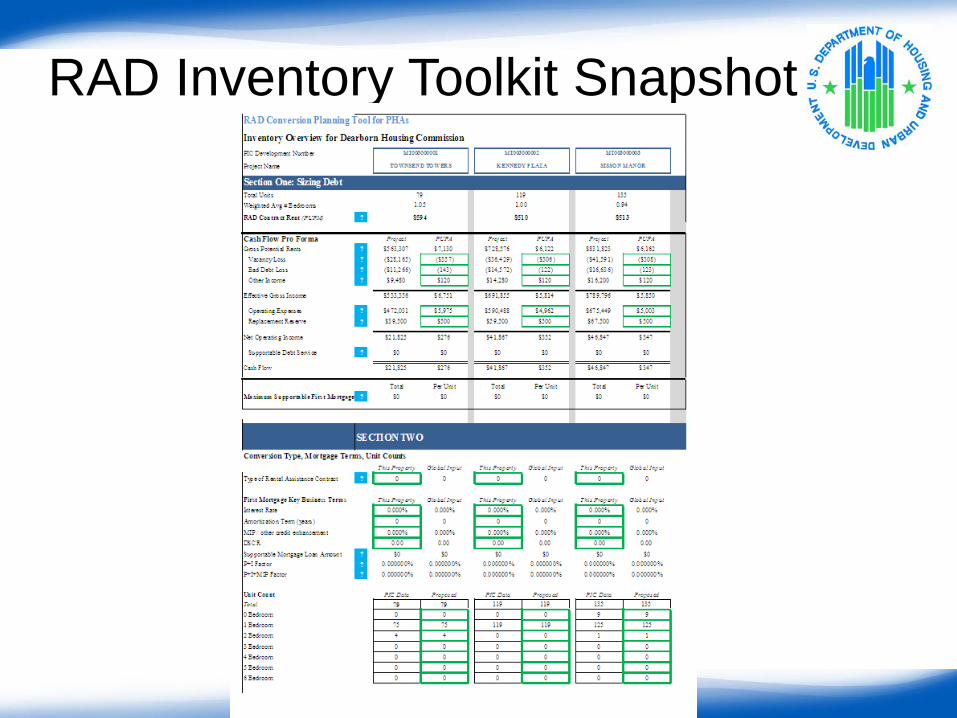

RAD Inventory Toolkit Snapshot

8

Newark Housing Authority

RAD Inventory Toolkit Demo

RAD Inventory Toolkit Demo

RAD Notice, application materials, and

additional resources can be found at

www.hud.gov/rad

Email questions to [email protected]

RAD Web Page

10

Other RAD

Considerations

RAD is revenue neutral in Year 1 – No new Funds from HUD! – Provisions for operating cost adjustments (“OCAF”) – Rents will never decrease – Protections from effects of Sequestration – PHA subsidies and Capital Fund appropriations are

decreasing

FUNDING

Tenants assisted with PBV can move after one year with a voucher

For PBRA units, tenants can move with a voucher after 24 months

PHA can limit PBRA turnover with a voucher to 1/3 of turnover in voucher program

Can limit moves to 15% of project Good cause exemptions in limited circumstances

Key Components

CHOICE MOBILITY

Pros – PHA administers assistance – Administrative fees earned – Management fees from both site and HCV program for COCC – No REAC Inspections

Cons

– Lower cap on maximum rents and thus less potential debt service (110% of FMR)

– Only 50% of units can receive assistance unless exceptions met – Need Capacity to administer PBV assistance (must have existing HCV

Program to self administer PBV)

PBV

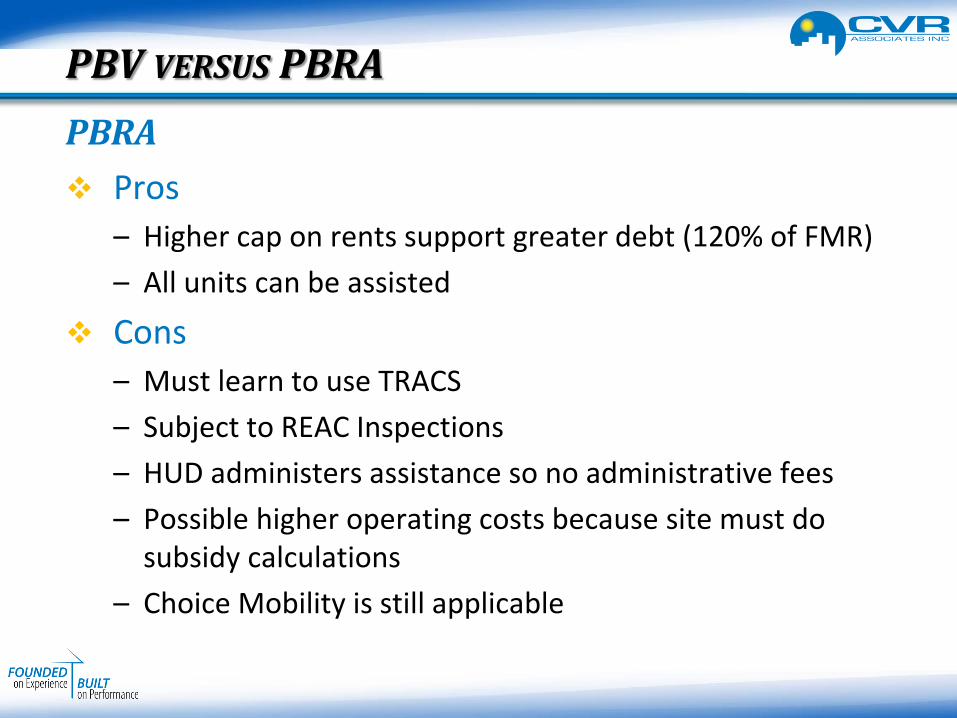

PBV VERSUS PBRA

Pros – Higher cap on rents support greater debt (120% of FMR) – All units can be assisted

Cons – Must learn to use TRACS – Subject to REAC Inspections – HUD administers assistance so no administrative fees – Possible higher operating costs because site must do

subsidy calculations – Choice Mobility is still applicable

PBRA

PBV VERSUS PBRA

Applies at turnover, not for existing residents Can be FSS participation or any other supportive

services program as defined by HCV Administrative Plan.

Key components – Intake and Assessment – Case Management – Individual Action Plan with Goals – Tracking and Reporting

HUD Requirements for Exemption

SUPPORTIVE SERVICES

Self-Sufficiency Upward Mobility Economic Independence Educational Achievement Quality of Life

Typical Program Goals

SUPPORTIVE SERVICES

Existing FSS Program Priority points for new HCV FSS coordinator

positions in an upcoming FSS competitions Site’s Operating Budgets (if allowed by funding

sources) HCV Admin Fees Partnership Agencies 501 (c) 3 affiliates Grants

Sources of Funding

SUPPORTIVE SERVICES

Current Capital Fund fungibility is lost Leveraging of Capital Funds for Debt lost Reserves become site specific Residual receipts might not be fungible depending

upon ownership structure If PHA eliminates all ACC units, Agency Plan might

not be required Could “De-Federalize” some PHA funds ACC units can not have Debt

ACC UNIT/FAIRCLOTH LIMIT REDUCTION

Agency Plan Amendment Required Resident Participation Required Choice Mobility Physical Needs Assessment

OTHER CONSIDERATIONS

A detailed physical inspection of a property to determine critical repair needs, short- and long-term rehabilitation needs, market comparable improvements, and environmental concerns

Tool is at www.hud.gov/RAD Must be completed by a qualified, independent

third-party inspector Due to HUD within 90 days of CHAP issuance

Requirements

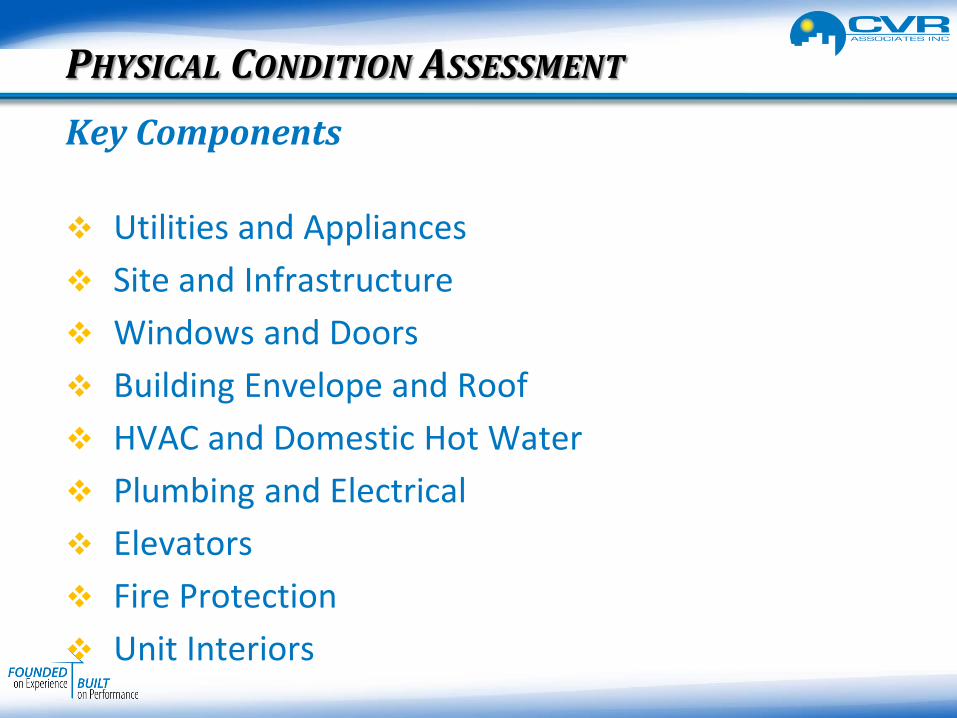

PHYSICAL CONDITION ASSESSMENT

Utilities and Appliances Site and Infrastructure Windows and Doors Building Envelope and Roof HVAC and Domestic Hot Water Plumbing and Electrical Elevators Fire Protection Unit Interiors

Key Components

PHYSICAL CONDITION ASSESSMENT

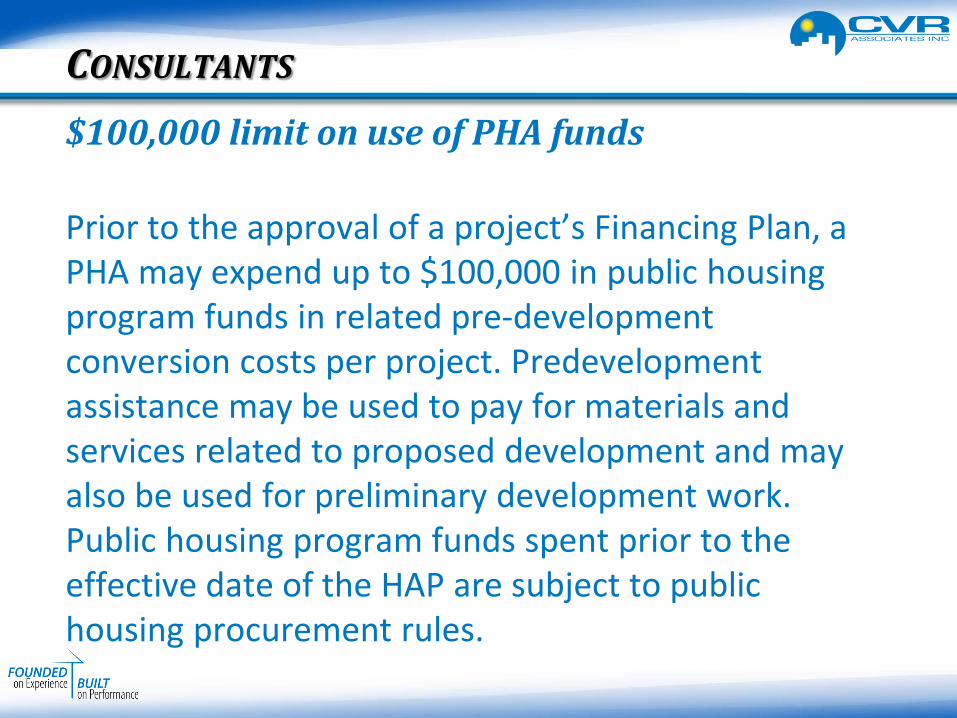

Prior to the approval of a project’s Financing Plan, a PHA may expend up to $100,000 in public housing program funds in related pre-development conversion costs per project. Predevelopment assistance may be used to pay for materials and services related to proposed development and may also be used for preliminary development work. Public housing program funds spent prior to the effective date of the HAP are subject to public housing procurement rules.

$100,000 limit on use of PHA funds

CONSULTANTS

RAD conversion provides access to debt & equity markets PHA retains 3rd party consultant to determine the

project’s capital needs and other project costs: • Repairs (Davis Bacon wage rates apply) • Soft cost including financing fees, architectural,

LIHC allocation fees, etc • 10% development fee (LIHC transaction 10%

acquisition/15% improvements) • Capitalized reserves

Financing RAD conversions, rehabilitation and/or new construction

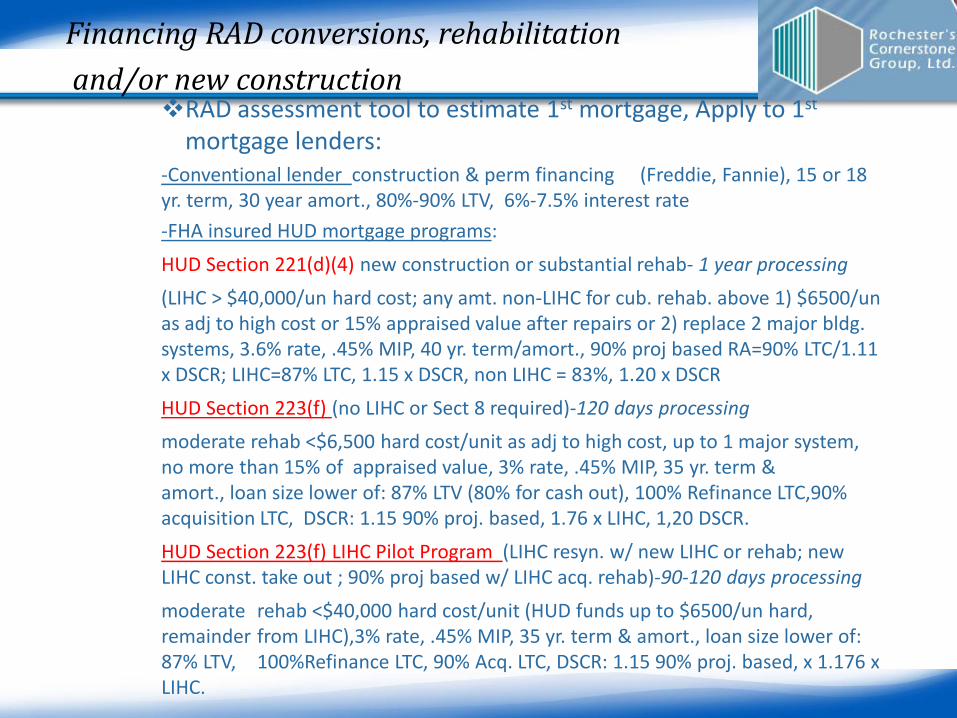

RAD assessment tool to estimate 1st mortgage, Apply to 1st mortgage lenders:

-Conventional lender construction & perm financing (Freddie, Fannie), 15 or 18 yr. term, 30 year amort., 80%-90% LTV, 6%-7.5% interest rate -FHA insured HUD mortgage programs:

HUD Section 221(d)(4) new construction or substantial rehab- 1 year processing (LIHC > $40,000/un hard cost; any amt. non-LIHC for cub. rehab. above 1) $6500/un as adj to high cost or 15% appraised value after repairs or 2) replace 2 major bldg. systems, 3.6% rate, .45% MIP, 40 yr. term/amort., 90% proj based RA=90% LTC/1.11 x DSCR; LIHC=87% LTC, 1.15 x DSCR, non LIHC = 83%, 1.20 x DSCR HUD Section 223(f) (no LIHC or Sect 8 required)-120 days processing moderate rehab <$6,500 hard cost/unit as adj to high cost, up to 1 major system, no more than 15% of appraised value, 3% rate, .45% MIP, 35 yr. term & amort., loan size lower of: 87% LTV (80% for cash out), 100% Refinance LTC,90% acquisition LTC, DSCR: 1.15 90% proj. based, 1.76 x LIHC, 1,20 DSCR. HUD Section 223(f) LIHC Pilot Program (LIHC resyn. w/ new LIHC or rehab; new

LIHC const. take out ; 90% proj based w/ LIHC acq. rehab)-90-120 days processing moderate rehab <$40,000 hard cost/unit (HUD funds up to $6500/un hard,

remainder from LIHC),3% rate, .45% MIP, 35 yr. term & amort., loan size lower of: 87% LTV, 100%Refinance LTC, 90% Acq. LTC, DSCR: 1.15 90% proj. based, x 1.176 x LIHC.

Financing RAD conversions, rehabilitation and/or new construction

If additional “Gap” financing needed, identify sources, apply for grants:

-PHAs available public housing funding, including Operating Reserves, Capital Funds, and Replacement Housing Factor (RHF), whether for rehabilitation or new construction.

-CDBG local municipality -County HOME -Federal Home Loan Bank of New York Federal & State 9% Low Income Tax Credits 4% as-of-right credits coupled with tax exempt bond

financing Historic tax credits

Financing RAD conversions, rehabilitation and/or new construction

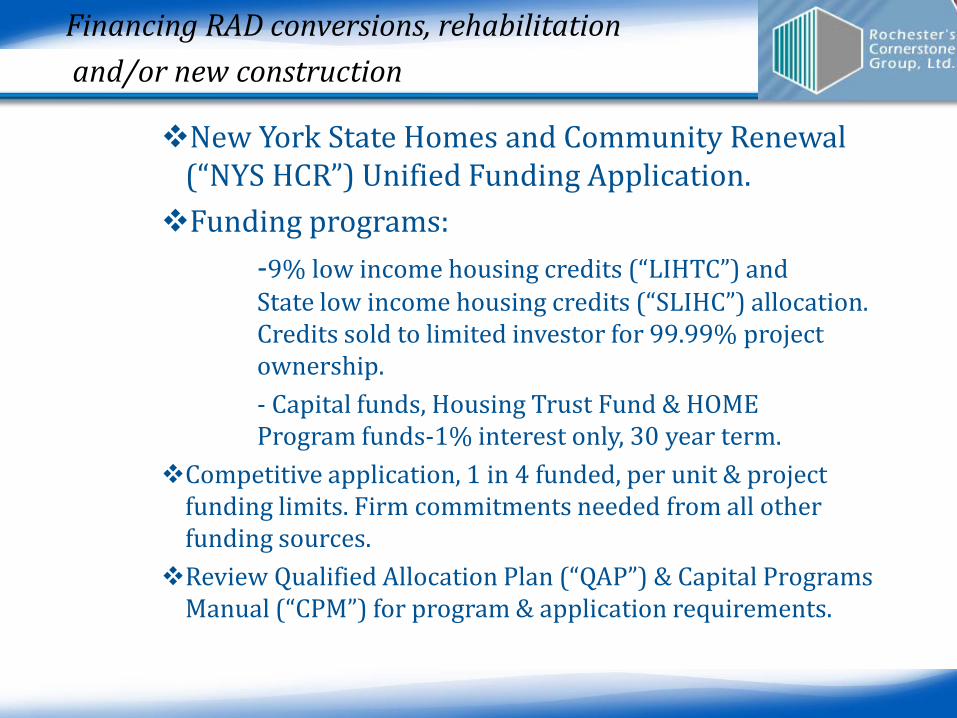

New York State Homes and Community Renewal (“NYS HCR”) Unified Funding Application. Funding programs: -9% low income housing credits (“LIHTC”) and State low income housing credits (“SLIHC”) allocation. Credits sold to limited investor for 99.99% project ownership. - Capital funds, Housing Trust Fund & HOME Program funds-1% interest only, 30 year term. Competitive application, 1 in 4 funded, per unit & project

funding limits. Firm commitments needed from all other funding sources.

Review Qualified Allocation Plan (“QAP”) & Capital Programs Manual (“CPM”) for program & application requirements.

Financing RAD conversions, rehabilitation and/or new construction

New York State Housing Finance Agency Funding

Application (“NYS HFA”) Funding programs: -4% as-of rights credits (“LIHTC”) coupled with tax exempt bonds -State low income housing credits (“SLIHC”) allocation . Credits sold to limited investor for 99.99% project ownership - Homes for Working Families (“HWF”) Loan-1% interest only, 30 year term Open round, however limited resources Review Qualified Allocation Plan (“QAP”) & HWF regulations

for program & application requirements

Financing RAD conversions, rehabilitation and/or new construction

LIHC transactions - consider partnering with an experienced LIHC developer

Why •Expertise •Leverage Capacity •Raise Equity or Resources •Share the Risk

How to Select •Developer and Management Skills •Technical Skills •Compatibility: Experience working with

partners, especially PHA & nonprofits •Trustworthiness

LIHC & SLIHC transaction financial guarantees to construction lender & equity: • Construction completion • Environmental • Operating deficit • Tax credit compliance • Developer fee

Financing RAD conversions, rehabilitation and/or new construction

Financing RAD conversions, rehabilitation and/or new construction Financial transaction examples-FHA insured, 185 unit project – replacement value $ 20 million Sources FHA 223(f) Loan $4,000,000 21,622 total $4,000,000 21,622

Uses Capitalized reserve $449,000 $2,427 Repairs $2,775,000 15,000 Development fee 400,000 2,162 Cash to owner 100,000 541 Transaction Costs/Financing Fees 276,000 1,492 total $4,000,000 21,622

Financing RAD conversions, rehabilitation and/or new construction

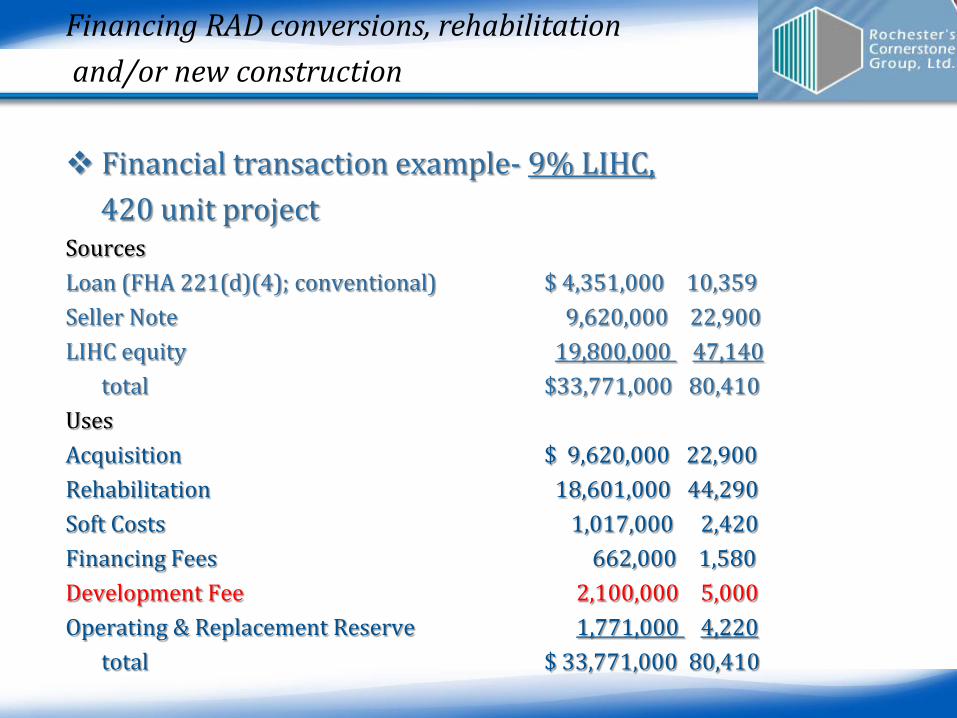

Financial transaction example- 9% LIHC, 420 unit project Sources Loan (FHA 221(d)(4); conventional) $ 4,351,000 10,359 Seller Note 9,620,000 22,900 LIHC equity 19,800,000 47,140 total $33,771,000 80,410 Uses Acquisition $ 9,620,000 22,900 Rehabilitation 18,601,000 44,290 Soft Costs 1,017,000 2,420 Financing Fees 662,000 1,580 Development Fee 2,100,000 5,000 Operating & Replacement Reserve 1,771,000 4,220 total $ 33,771,000 80,410

Financing RAD conversions, rehabilitation and/or new construction Financial transaction example- 4% LIHTC, 420 unit project Sources Loan (FHA 221(d)(4); Bond) $ 7,650,000 18,210 Seller Note 9,620,000 22,900 Deferred Developer Fee 1,050,000 2,500 LIHC equity 9,932,000 23,650 Other Capital 6,149,000 14,640 total $34,401,000 81,900 Uses Acquisition $ 9,620,000 22,900 Rehabilitation 18,601,000 44,290 Soft Costs 1,017,000 2,420 Financing Fees 1,292,000 3,080 Development Fee 2,100,000 5,000 Oper. & RR Reserve/ Working Cap 1,771,000 4,220 total $ 34,401,000 81,900

Legal Structure and Ownership Considerations

Ownership means legal title

• Could be through contract, partnership or voting right of entity • 51% or more interest in of the general partner of limited partnership

Control means ability to direct the financial, legal, beneficial,

or other interests of the owner

• Long term ground lease • Subordinate seller (PHA) financing • Right of fires refusal in sale of project Other forms of control

• Capable public entity • Capable non-public entity as determined by Secretary • For-Profit entity to facilitate use of low-income housing tax credits

RAD Notice provides for the following priority in ownership

RAD Statute provides Ownership or Control by Public or Nonprofit Entity

• PHA or other public entity could be Owner with FNA or conventional financing

• Single Asset Borrower Requirement for FHA Financing • Must be eligible mortgagor under FHA guidance • Creation of PHA affiliate or Instrumentality • No competitive requirements for contractor

selection

No New Financing or Debt Only Financing

May Be Dependent on Financing Plan

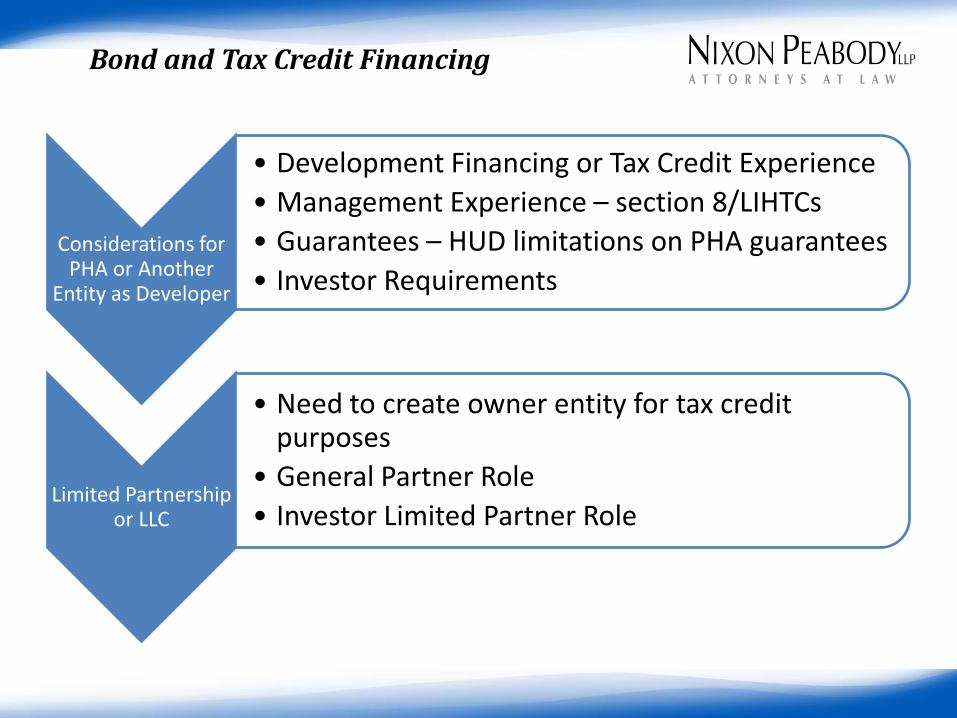

Considerations for PHA or Another

Entity as Developer

• Development Financing or Tax Credit Experience • Management Experience – section 8/LIHTCs • Guarantees – HUD limitations on PHA guarantees • Investor Requirements

Limited Partnership or LLC

• Need to create owner entity for tax credit purposes

• General Partner Role • Investor Limited Partner Role

Bond and Tax Credit Financing

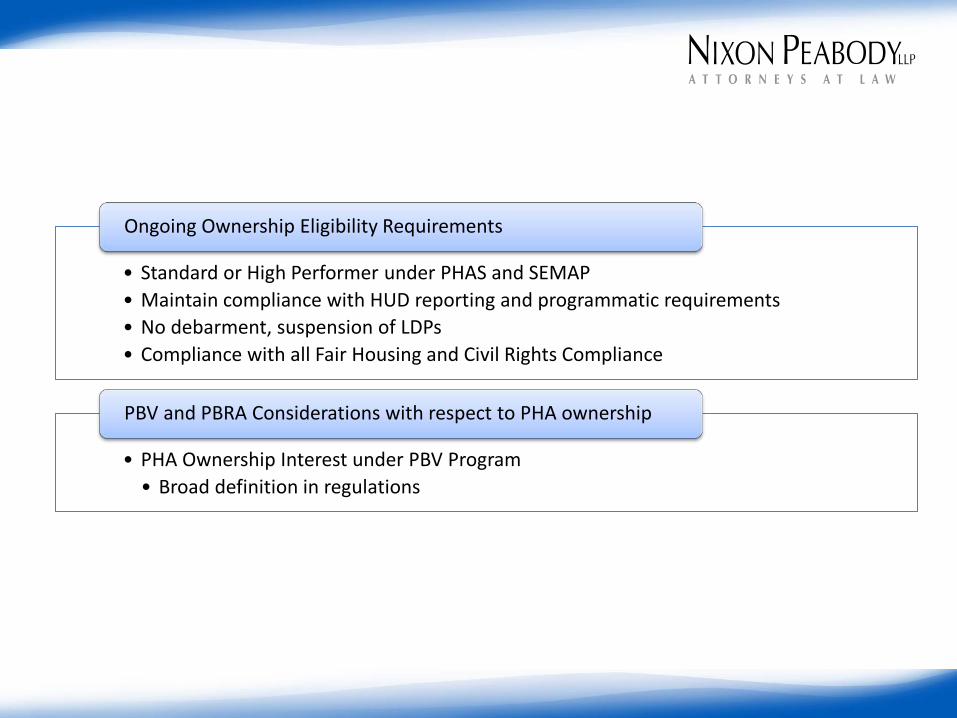

• Standard or High Performer under PHAS and SEMAP • Maintain compliance with HUD reporting and programmatic requirements • No debarment, suspension of LDPs • Compliance with all Fair Housing and Civil Rights Compliance

Ongoing Ownership Eligibility Requirements

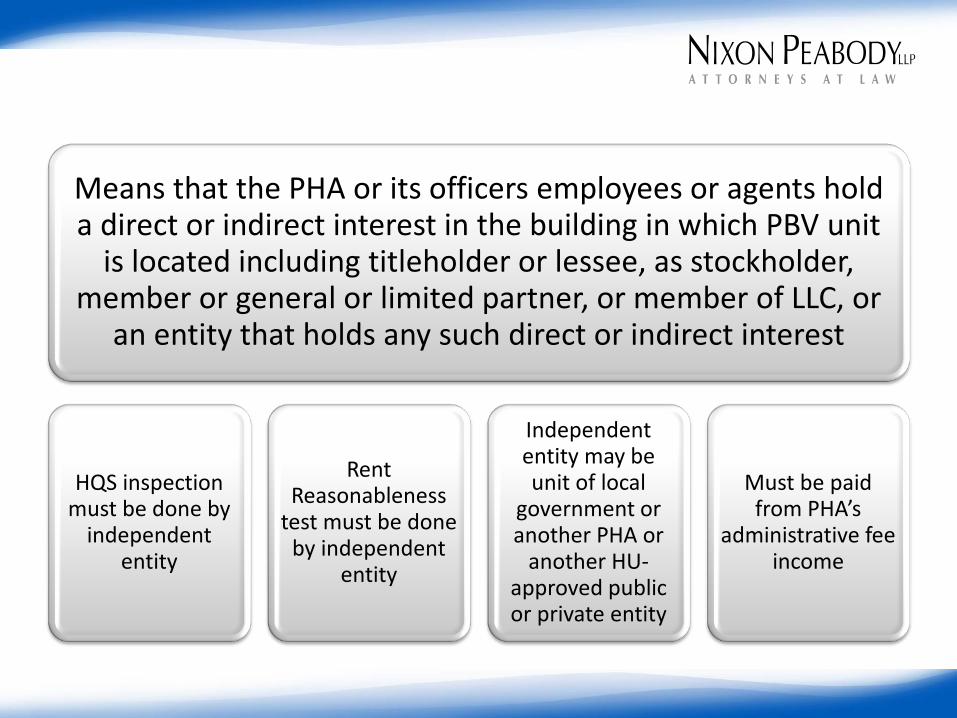

• PHA Ownership Interest under PBV Program • Broad definition in regulations

PBV and PBRA Considerations with respect to PHA ownership

Means that the PHA or its officers employees or agents hold a direct or indirect interest in the building in which PBV unit

is located including titleholder or lessee, as stockholder, member or general or limited partner, or member of LLC, or

an entity that holds any such direct or indirect interest

HQS inspection must be done by

independent entity

Rent Reasonableness

test must be done by independent

entity

Independent entity may be unit of local

government or another PHA or

another HU-approved public or private entity

Must be paid from PHA’s

administrative fee income

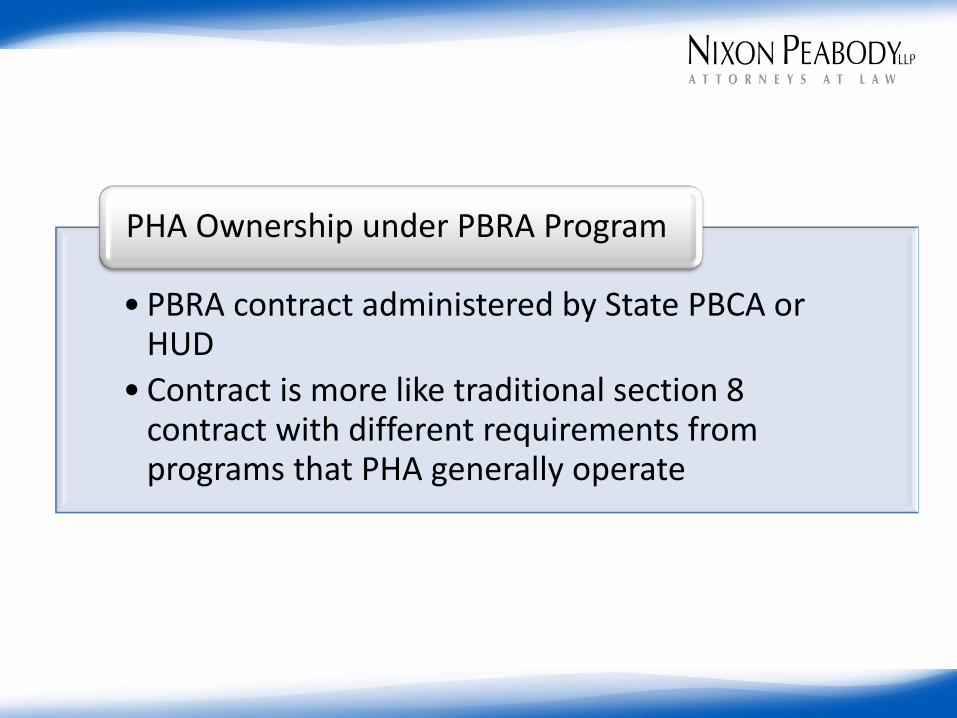

• PBRA contract administered by State PBCA or HUD

• Contract is more like traditional section 8 contract with different requirements from programs that PHA generally operate

PHA Ownership under PBRA Program

Tax Credit and Other Guarantees - PHA or an affiliate of PHA as owner or general partner in limited partnership or

managing member in LLC would be required to provide guarantees to investors and lenders

• Completion Guaranty • Must provide for lien free completion of the project by

date certain • LIHTC guarantees – assure placed in service date is met

and investor receives all of its tax creditors • Environmental Indemnifications or Guarantees

2. Guaranty Obligations and Indemnifications. (A) Except as provided in subparagraph (B) of this paragraph, the Limited Partners of the Owner acknowledge and agree that the neither the Authority not the General Partner of the Owner (the “General Partner”), or any entity with a controlling interest in the General Partner (the “Controlling Entity”), has authority to provide the Limited Partners with guarantees or indemnifications involving the assets of the Project (as the term “Project” is defined in paragraph 1 [4] herein, and as further defined in the ACC) or the assets of the Authority. Accordingly, the Limited Partner(s) acknowledge that public housing operating subsidies, or other receipts generated by the Project, may not be used to make cash flow distributions to the Limited Partner(s) and, furthermore, that they have no legal right of recourse under this Agreement against:

i. any public housing project of the Authority, including the Project that is the subject of this Limited Partnership

Agreement;

ii. any operating receipts of the Authority (as the term “operating receipts” is defined in the ACC); or

iii. any public housing operating reserve of the Authority reflected in the Authority’s annual operating budget and required under the ACC;

B. The Authority may, with HUD’s prior written approval in accordance with section 30 of the Act and the ACC, pledge

and grant to Owner an interest in its Authority Reserve solely to permit the use of such funds for eligible and necessary costs of the Project, as provided in the Regulatory and Operating Agreement and the Applicable Public Housing Requirements. In addition, any excess fees contained in the Authority’s Section 8 administrative fee reserve under 24 CFR § 982.155 shall not be subject to the restrictions in subparagraph (A) herein, nor are any other assets of the Authority arising under any program not administered by HUD subject to this restriction.

HUD Model Language on Limitation on PHA sources of guarantees

Michael H. Reardon, Esq.

401 9th Street, NW, Suite 900

Washington, DC 20004

(202) 585-8304

Contact us

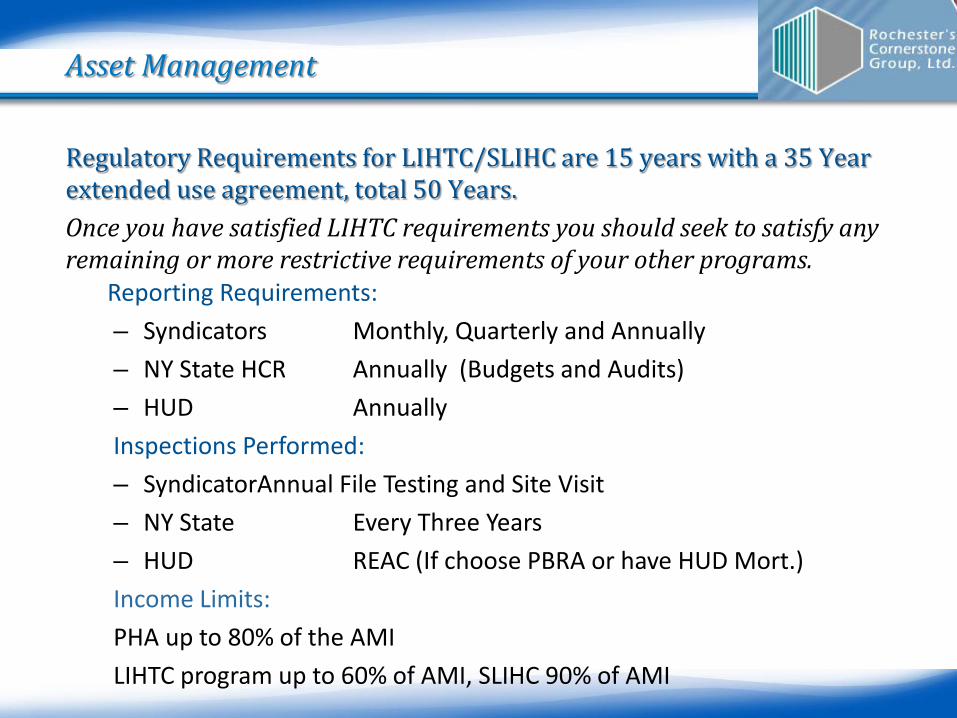

Asset Management

Reporting Requirements:

– Syndicators Monthly, Quarterly and Annually – NY State HCR Annually (Budgets and Audits) – HUD Annually Inspections Performed: – SyndicatorAnnual File Testing and Site Visit – NY State Every Three Years – HUD REAC (If choose PBRA or have HUD Mort.) Income Limits: PHA up to 80% of the AMI LIHTC program up to 60% of AMI, SLIHC 90% of AMI

Regulatory Requirements for LIHTC/SLIHC are 15 years with a 35 Year extended use agreement, total 50 Years. Once you have satisfied LIHTC requirements you should seek to satisfy any remaining or more restrictive requirements of your other programs.

Asset Management

RAD application and timeline

Conversion Steps – Public Housing

52

HUD Publishes Final Notice

PHAs submits Excel-based

Application to HQ

HQ reviews application and requests Field Office

input on Eligibility

HQ issues awards/Commitments

to Enter Housing Assistance Payments

Contract (CHAPs)

Project converts Remove from ACC Release DOT Execute HAP Execute RAD Use Agreement Close Financing

PBV

PBRA

PHA •Asset Management •Subsidy Administration

Multifamily Housing • Asset Management •Subsidy Administration

HUD issues RAD Conversion

Commitment

PIH • Voucher Oversight

PHAs have 6 months to submit Financing

Plan to HQ for review

Application Snapshot

53

RAD Inventory Assessment Tool Demo

Volunteers?

Final Q & A

Thank you for joining us!

RAD Inventory Assessment Tool Demo & Final Q & A

Recommended