DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

01 September 2014

Asia Pacific/Singapore

Equity Research

Forest Products

Halcyon Agri Corporation Ltd

(HALC.SI / HACL SP) REINSTATEMENT

Capacity expansion to drive growth

■ Re-instate coverage with OUTPERFORM. We re-instate coverage of

Halcyon Agri with an OUTPERFORM rating (previously Neutral) and target

price of S$1.20 (previously S$0.80). We believe there is over 40% share

price upside driven by significant capacity growth and supported by

increasing demand in the global tyre market, which should lead to a five-fold

growth in net profit over 2013-16E.

■ Licensed capacity doubled with Anson acquisition. Following the

acquisition of Anson Company from Lee Rubber for a consideration of

S$450 mn, Halcyon's licensed capacity will increase by 408,000 mT to reach

748,000 mT, making it one of the largest producers of Technically Specified

Rubber (TSR) globally. Rising demand for natural rubber is likely to be

driven by an expanding tyre market, which we expect to grow at 3.8% per

annum in 2013-17E.

■ Potential synergies to further drive earnings growth. With the use of

Halcyon's sales and marketing to support Anson's operations, we see scope

for Anson's margin to increase from US$161/mT in 2013 to US$320/mT in

2016E, in line with Halcyon's margin. Overall, we expect the volume growth

and acquisition synergies to drive an increase in net profit from US$9 mn in

2013 to US$50 mn in 2016.

■ Valuation attractive. Halcyon currently trades at a 2015E P/E of 9.2x and 2016E P/E of 5.8x, a discount to global tyre manufacturers and commodity traders. Our S$1.20 target price is based on a 2016E P/E of 8.0x, in line with its peers. In our view, the successful execution of its planned capacity growth would drive re-rating. Key risks include high net gearing post acquisition of 2.5x, which would be closer to 2.0x after adjustment for working capital loans.

Share price performance

0

100

200

300

400

0

0.5

1

1.5

2

Feb-13 Jun-13 Oct-13 Feb-14 Jun-14

Price (LHS) Rebased Rel (RHS)

The price relative chart measures performance against the

FTSE STRAITS TIMES IDX which closed at 3327.09 on

29/08/14

On 29/08/14 the spot exchange rate was S$1.25/US$1

Performance over 1M 3M 12M Absolute (%) 2.4 10.4 26.9 — Relative (%) 3.2 9.4 17.4 —

Financial and valuation metrics

Year 12/13A 12/14E 12/15E 12/16E Revenue (US$ mn) 205.0 400.0 1,287.5 1,362.5 EBITDA (US$ mn) 13.1 18.4 78.5 101.1 EBIT (US$ mn) 12.1 17.0 67.1 89.8 Net profit (US$ mn) 9.1 6.7 31.2 49.6 EPS (CS adj.) (US$) 0.02 0.02 0.07 0.12 Change from previous EPS (%) n.a. -62.4 0.5 27.3 Consensus EPS (US$) n.a. 0.03 0.09 0.09 EPS growth (%) -7.9 -31.3 338.5 58.9 P/E (x) 27.7 40.3 9.2 5.8 Dividend yield (%) 1.2 1.2 1.2 1.2 EV/EBITDA (x) 18.1 30.4 7.6 5.6 P/B (x) 3.1 2.5 2.0 1.5 ROE (%) 17.1 6.8 23.8 29.5 Net debt/equity (%) net cash 163.8 158.7 114.0

Source: Company data, Thomson Reuters, Credit Suisse estimates.

Rating (from Neutral) OUTPERFORM* Price (29 Aug 14, S$) 0.85 Target price (S$) (from 0.80) 1.20¹ Upside/downside (%) 41.2 Mkt cap (S$ mn) 336.6 (US$ 269.6) Enterprise value (US$ mn) 559.67 Number of shares (mn) 396.00 Free float (%) 33.0 52-week price range 0.98 - 0.66 ADTO - 6M (US$ mn) 1.4

*Stock ratings are relative to the coverage universe in each

analyst's or each team's respective sector.

¹Target price is for 12 months.

Research Analysts

Gerald Wong, CFA

65 6212 3037

01 September 2014

Halcyon Agri Corporation Ltd (HALC.SI / HACL SP) 2

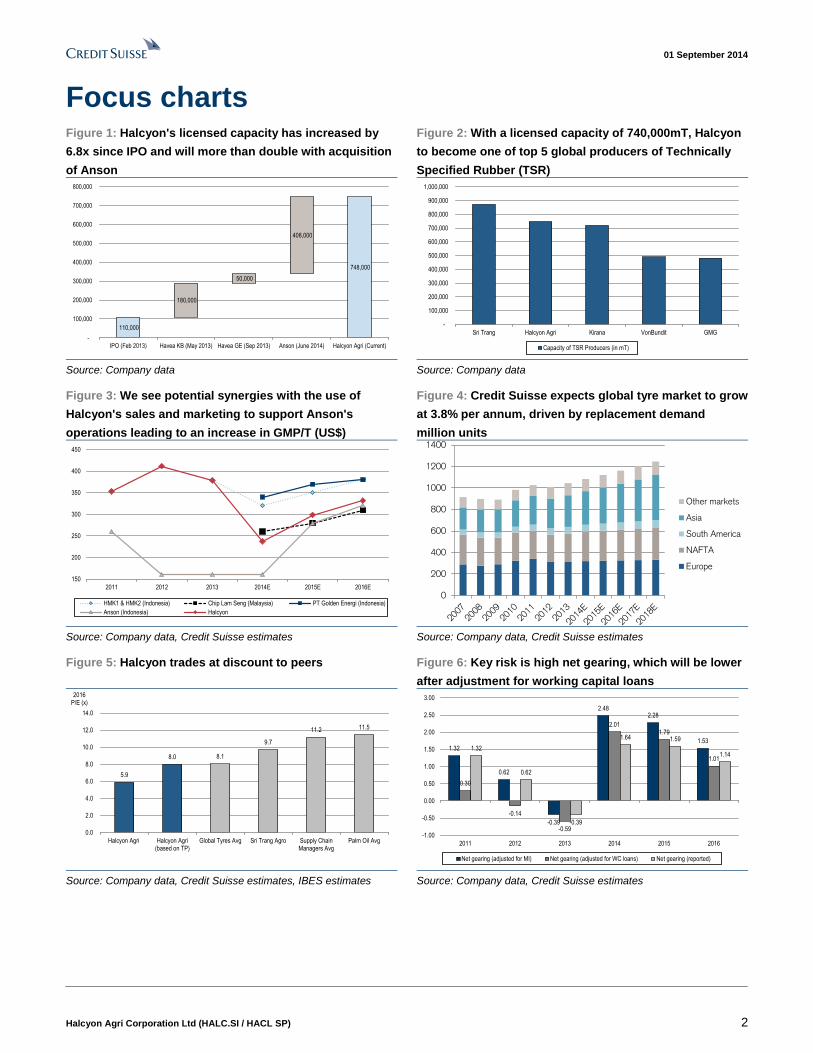

Focus charts Figure 1: Halcyon's licensed capacity has increased by

6.8x since IPO and will more than double with acquisition

of Anson

Figure 2: With a licensed capacity of 740,000mT, Halcyon

to become one of top 5 global producers of Technically

Specified Rubber (TSR)

110,000

748,000

180,000

50,000

408,000

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

IPO (Feb 2013) Havea KB (May 2013) Havea GE (Sep 2013) Anson (June 2014) Halcyon Agri (Current)

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1,000,000

Sri Trang Halcyon Agri Kirana VonBundit GMG

Capacity of TSR Producers (in mT)

Source: Company data Source: Company data

Figure 3: We see potential synergies with the use of

Halcyon's sales and marketing to support Anson's

operations leading to an increase in GMP/T (US$)

Figure 4: Credit Suisse expects global tyre market to grow

at 3.8% per annum, driven by replacement demand

million units

150

200

250

300

350

400

450

2011 2012 2013 2014E 2015E 2016E

HMK1 & HMK2 (Indonesia) Chip Lam Seng (Malaysia) PT Golden Energi (Indonesia)

Anson (Indonesia) Halcyon

0

200

400

600

800

1000

1200

1400

Other markets

Asia

South America

NAFTA

Europe

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 5: Halcyon trades at discount to peers Figure 6: Key risk is high net gearing, which will be lower

after adjustment for working capital loans

5.9

8.0 8.1

9.7

11.2 11.5

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Halcyon Agri Halcyon Agri(based on TP)

Global Tyres Avg Sri Trang Agro Supply ChainManagers Avg

Palm Oil Avg

2016 P/E (x)

1.32

0.62

-0.39

2.482.28

1.53

0.30

-0.14

-0.59

2.011.79

1.01

1.32

0.62

-0.39

1.64 1.59

1.14

-1.00

-0.50

0.00

0.50

1.00

1.50

2.00

2.50

3.00

2011 2012 2013 2014 2015 2016

Net gearing (adjusted for MI) Net gearing (adjusted for WC loans) Net gearing (reported)

Source: Company data, Credit Suisse estimates, IBES estimates Source: Company data, Credit Suisse estimates

01 September 2014

Halcyon Agri Corporation Ltd (HALC.SI / HACL SP) 3

Capacity expansion to drive growth Licensed capacity doubled with acquisition of Anson

In August 2014, Halcyon completed the acquisition of Anson company, which is part of the

Lee Rubber Group. Anson owns and operates nine crumb rubber factories in Indonesia

with a total licensed export capacity of 408,000 mT per annum. Halcyon Rubber Company

acquired Anson for a consideration of S$450mn, which will be funded by a combination of

issuance of preference shares and borrowing. With the acquisition of Anson, Halcyon's

licensed export capacity will increase from 340,000 mT per annum to 748,00 mT per

annum. In combination with Halcyon's two existing HMK factories in Palembang, Halcyon

will become the largest crumb rubber producer and exporter in Palembang with a market

share of 30%. Halcyon will also become one of the top five producers of Technically

Specified Rubber (TSR) globally.

Potential synergies from combination of Anson and

Halcyon Agri

In addition, we expect the combination of Anson and Halcyon Agri to lead to potential

synergies. In 2012 and 2013, Halcyon Agri's margin was on average US$235/mT higher

than Anson, driven by the full capture of sales and marketing margin in Halcyon Agri.

When fully integrated, this could lead to potential EBITDA contribution of US$29 mn. We

forecast Anson's margin to increase from US$161/mT in 2013 to US$320/mT in 2016E, in

line with Halcyon's margin in 2014 YTD. Halcyon's distribution capabilities have been

further strengthened through its proposed acquisition of New Continent Enterprises, a

leading global dealer and distributor of natural rubber. Overall, we expect the volume

growth and acquisition synergies to drive an increase in net profit from US$9 mn in 2013

to US$50 mn in 2016.

Beneficiary of rising natural rubber demand

Halcyon is a beneficiary of rising demand for natural rubber, which is expected to grow

53% from 10.9 mn tonnes in 2011 to 16.7 mn tonnes in 2021, representing a CAGR of

4.4%. This is driven mainly by an expanding tyre market, which is the largest consumer of

natural rubber, accounting for about 70% of total demand. The tyre market has defensive

growth characteristics as the replacement market makes up for 70% of the total tyre

demand. Credit Suisse automotive team expects medium-term average tyre demand

growth of 3.8% per annum. This is driven mainly by replacement of passenger tyres,

particularly in China where we expect to grow by 7.3% in 2013-17E.

Valuation attractive

Halcyon currently trades at a 2015E P/E of 9.2x and 2016E P/E of 5.8x, a significant

discount to global tyre manufacturers and commodity traders despite its greater earnings

visibility. Our target price of S$1.20 is based on a 2016E P/E of 8.0x, in line with its peers.

On our estimates, it is trading at a 2016E P/B of 1.5x against expected ROE of 29.5%. In

our view, successful execution of its planned capacity growth would drive re-rating.

Key risks would include high net gearing post acquisition of 2.5x, which would be closer to

2.0x after adjusting for working capital loans. Other risks include dependence on raw

materials from several large suppliers and a large number of small suppliers. Also,

Halcyon's top five customers accounted for close to 90% historically. We expect its

customer base to be more diversified with the acquisition of New Continent Enterprises

(NCE), which allows the company to sell to a wider network of smaller, non-tyre

consumers in markets such as the EU and the USA.

01 September 2014

Halcyon Agri Corporation Ltd (HALC.SI / HACL SP) 4

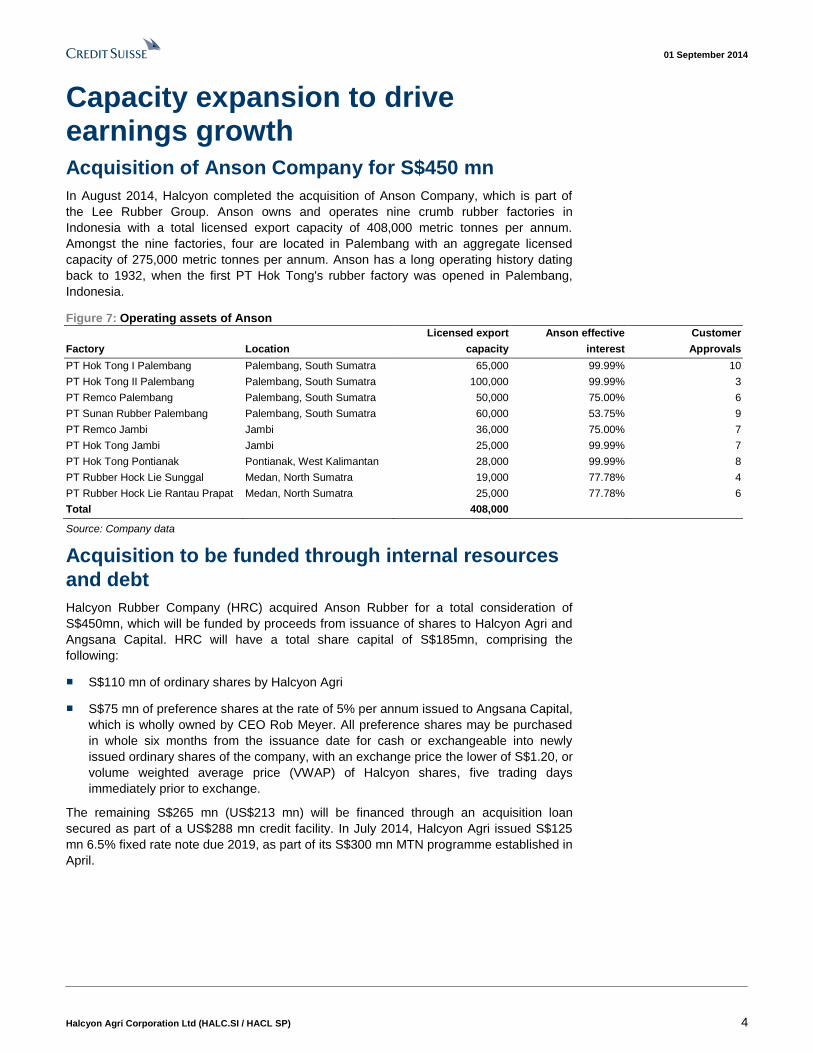

Capacity expansion to drive earnings growth Acquisition of Anson Company for S$450 mn

In August 2014, Halcyon completed the acquisition of Anson Company, which is part of

the Lee Rubber Group. Anson owns and operates nine crumb rubber factories in

Indonesia with a total licensed export capacity of 408,000 metric tonnes per annum.

Amongst the nine factories, four are located in Palembang with an aggregate licensed

capacity of 275,000 metric tonnes per annum. Anson has a long operating history dating

back to 1932, when the first PT Hok Tong's rubber factory was opened in Palembang,

Indonesia.

Figure 7: Operating assets of Anson

Licensed export Anson effective Customer

Factory Location capacity interest Approvals

PT Hok Tong I Palembang Palembang, South Sumatra 65,000 99.99% 10

PT Hok Tong II Palembang Palembang, South Sumatra 100,000 99.99% 3

PT Remco Palembang Palembang, South Sumatra 50,000 75.00% 6

PT Sunan Rubber Palembang Palembang, South Sumatra 60,000 53.75% 9

PT Remco Jambi Jambi 36,000 75.00% 7

PT Hok Tong Jambi Jambi 25,000 99.99% 7

PT Hok Tong Pontianak Pontianak, West Kalimantan 28,000 99.99% 8

PT Rubber Hock Lie Sunggal Medan, North Sumatra 19,000 77.78% 4

PT Rubber Hock Lie Rantau Prapat Medan, North Sumatra 25,000 77.78% 6

Total 408,000

Source: Company data

Acquisition to be funded through internal resources

and debt

Halcyon Rubber Company (HRC) acquired Anson Rubber for a total consideration of

S$450mn, which will be funded by proceeds from issuance of shares to Halcyon Agri and

Angsana Capital. HRC will have a total share capital of S$185mn, comprising the

following:

■ S$110 mn of ordinary shares by Halcyon Agri

■ S$75 mn of preference shares at the rate of 5% per annum issued to Angsana Capital,

which is wholly owned by CEO Rob Meyer. All preference shares may be purchased

in whole six months from the issuance date for cash or exchangeable into newly

issued ordinary shares of the company, with an exchange price the lower of S$1.20, or

volume weighted average price (VWAP) of Halcyon shares, five trading days

immediately prior to exchange.

The remaining S$265 mn (US$213 mn) will be financed through an acquisition loan

secured as part of a US$288 mn credit facility. In July 2014, Halcyon Agri issued S$125

mn 6.5% fixed rate note due 2019, as part of its S$300 mn MTN programme established in

April.

01 September 2014

Halcyon Agri Corporation Ltd (HALC.SI / HACL SP) 5

Figure 8: Co-investment structure

ANSON COMPANY (PTE) LTD SINGAPORE

Halcyon Rubber Company Pte Ltd

Halcyon Agri Coporation Limited

Angsana Capital Ltd

Keystone Pacific Pte Ltd

Mr Robert Meyer

100%

100%

100%

Preference shares40.5% S$75m

Ordinary shares59.5% S$110m

Source: Company data

Acquisition multiple of 15.5x P/E and 2.7x P/B

Anson generated net profit of S$29.1 mn in 2013, flat from 2012 net profit of S$29.9 mn.

Based on the consideration of S$450 mn, this would imply a P/E of 15.5x. Anson had cash

and cash equivalents of S$93.5 mn, borrowings of S$48.6 mn, and shareholdings equity of

S$165.2 mn. This would imply an acquisition multiple of 2.7x P/B, compared to a ROE of

17.6% generated.

Figure 9: Anson financial statement

S$ mn 2011 2012 2013

Revenue 1924.4 1239.3 963.2

Gross material profit 129.9 61.4 62.2

EBITDA 107.5 38.2 41.7

Net income after tax 74.0 29.9 29.1

Sales volume (tonnes) 328,888 301,769 303,472

Average revenue per tonne (S$) 5851 4107 3174

Average revenue per tonne (US$) 4647 3257 2496

GMP/tonne (S$) 395 204 205

GMP/tonne (US$) 314 161 161

EBITDA/tonne (S$) 327 127 137

Net income per tonne (S$) 225 99 96

Source: Company data

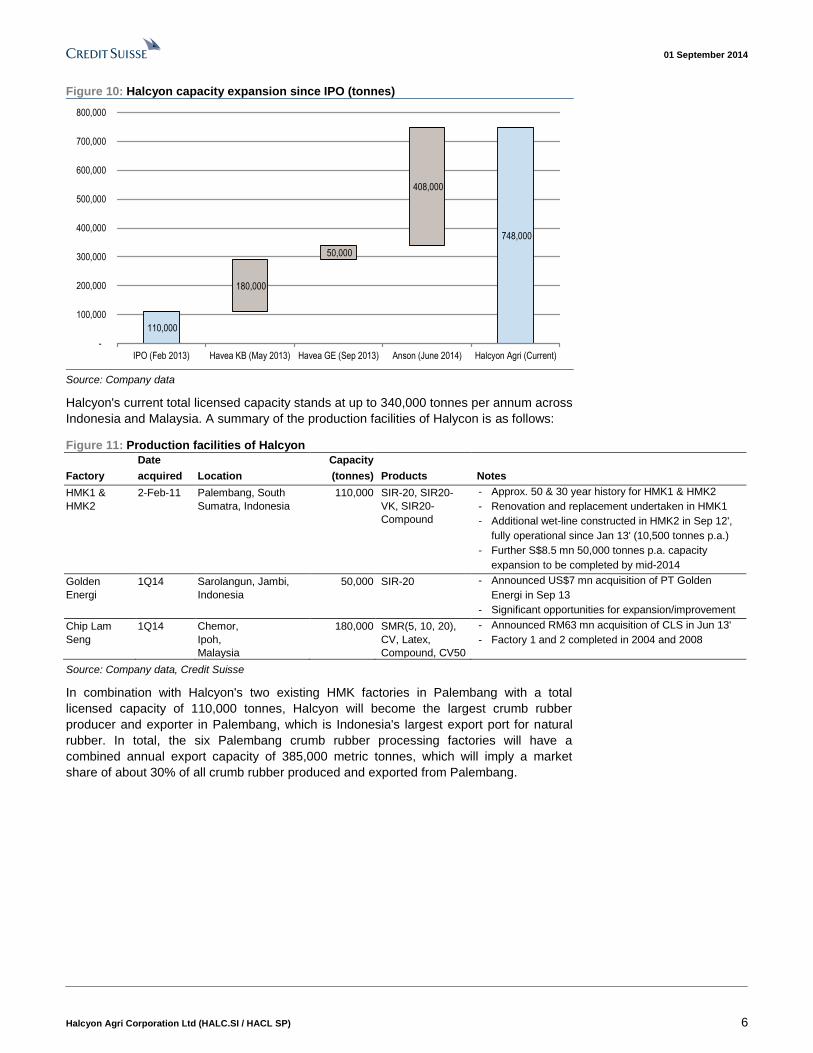

Licensed capacity expanded 6.8x since IPO

With the completion of the acquisition of Anson, Halcyon's consolidated licensed natural

rubber export capacity is expected to increase from 340,000 tonnes per annum to 748,000

tonnes per annum.

01 September 2014

Halcyon Agri Corporation Ltd (HALC.SI / HACL SP) 6

Figure 10: Halcyon capacity expansion since IPO (tonnes)

110,000

748,000

180,000

50,000

408,000

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

IPO (Feb 2013) Havea KB (May 2013) Havea GE (Sep 2013) Anson (June 2014) Halcyon Agri (Current)

Source: Company data

Halcyon's current total licensed capacity stands at up to 340,000 tonnes per annum across

Indonesia and Malaysia. A summary of the production facilities of Halycon is as follows:

Figure 11: Production facilities of Halcyon

Date Capacity

Factory acquired Location (tonnes) Products Notes

HMK1 &

HMK2

2-Feb-11 Palembang, South

Sumatra, Indonesia

110,000 SIR-20, SIR20-

VK, SIR20-

Compound

- Approx. 50 & 30 year history for HMK1 & HMK2

- Renovation and replacement undertaken in HMK1

- Additional wet-line constructed in HMK2 in Sep 12',

fully operational since Jan 13' (10,500 tonnes p.a.)

- Further S$8.5 mn 50,000 tonnes p.a. capacity

expansion to be completed by mid-2014

Golden

Energi

1Q14 Sarolangun, Jambi,

Indonesia

50,000 SIR-20 - Announced US$7 mn acquisition of PT Golden

Energi in Sep 13

- Significant opportunities for expansion/improvement

Chip Lam

Seng

1Q14 Chemor,

Ipoh,

Malaysia

180,000 SMR(5, 10, 20),

CV, Latex,

Compound, CV50

- Announced RM63 mn acquisition of CLS in Jun 13'

- Factory 1 and 2 completed in 2004 and 2008

Source: Company data, Credit Suisse

In combination with Halcyon's two existing HMK factories in Palembang with a total

licensed capacity of 110,000 tonnes, Halcyon will become the largest crumb rubber

producer and exporter in Palembang, which is Indonesia's largest export port for natural

rubber. In total, the six Palembang crumb rubber processing factories will have a

combined annual export capacity of 385,000 metric tonnes, which will imply a market

share of about 30% of all crumb rubber produced and exported from Palembang.

01 September 2014

Halcyon Agri Corporation Ltd (HALC.SI / HACL SP) 7

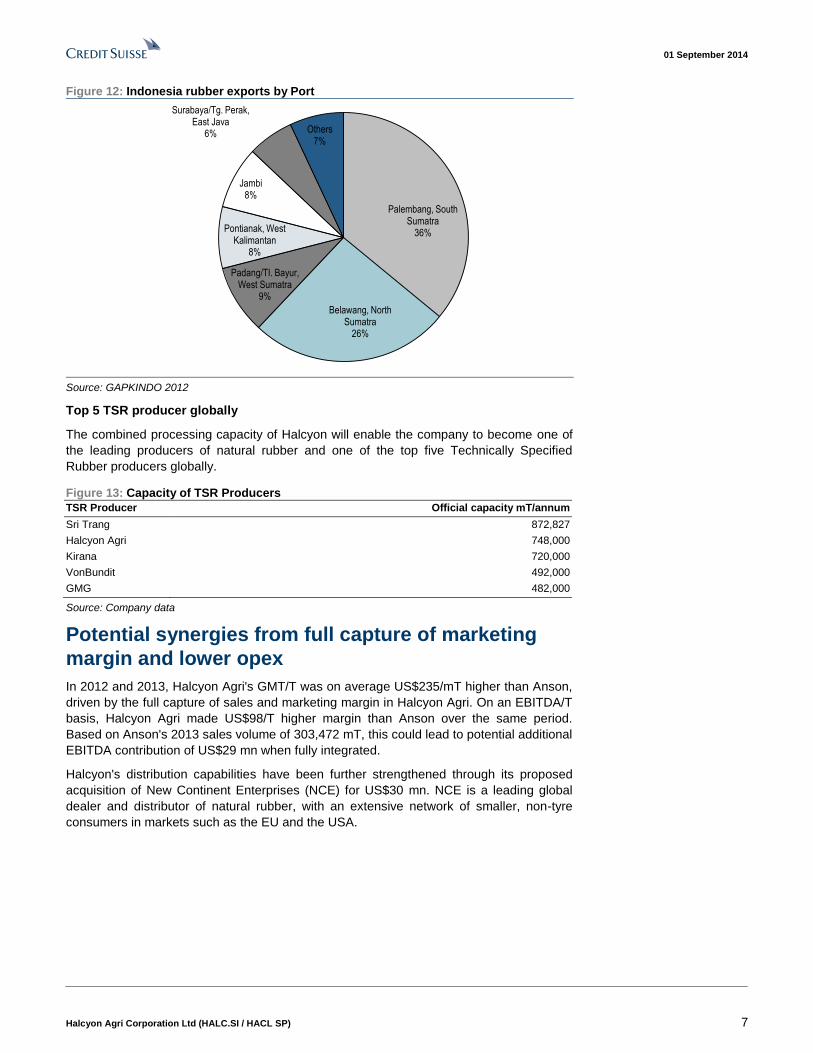

Figure 12: Indonesia rubber exports by Port

Palembang, South Sumatra

36%

Belawang, North Sumatra

26%

Padang/TI. Bayur, West Sumatra

9%

Pontianak, West Kalimantan

8%

Jambi8%

Surabaya/Tg. Perak, East Java

6% Others7%

Source: GAPKINDO 2012

Top 5 TSR producer globally

The combined processing capacity of Halcyon will enable the company to become one of

the leading producers of natural rubber and one of the top five Technically Specified

Rubber producers globally.

Figure 13: Capacity of TSR Producers

TSR Producer Official capacity mT/annum

Sri Trang 872,827

Halcyon Agri 748,000

Kirana 720,000

VonBundit 492,000

GMG 482,000

Source: Company data

Potential synergies from full capture of marketing

margin and lower opex

In 2012 and 2013, Halcyon Agri's GMT/T was on average US$235/mT higher than Anson,

driven by the full capture of sales and marketing margin in Halcyon Agri. On an EBITDA/T

basis, Halcyon Agri made US$98/T higher margin than Anson over the same period.

Based on Anson's 2013 sales volume of 303,472 mT, this could lead to potential additional

EBITDA contribution of US$29 mn when fully integrated.

Halcyon's distribution capabilities have been further strengthened through its proposed

acquisition of New Continent Enterprises (NCE) for US$30 mn. NCE is a leading global

dealer and distributor of natural rubber, with an extensive network of smaller, non-tyre

consumers in markets such as the EU and the USA.

01 September 2014

Halcyon Agri Corporation Ltd (HALC.SI / HACL SP) 8

Figure 14: Comparative GMP/T (US$) Figure 15: Comparative EBITDA/T (US$)

412

379

161 161

0

50

100

150

200

250

300

350

400

450

2012 2013

Halcyon Anson

225

180

101108

0

50

100

150

200

250

2012 2013

Halcyon Anson

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Due to economies of scale from its larger processing capacity, Anson's operating

expenses were on average US$136/mT lower than Halcyon Agri in 2012-13. Should

Halcyon Agri be able to lower operating cost to be in line with Anson, this could lead to an

additional EBITDA contribution of US$10 mn based on Halcyon's 2013 sales volume of

79,108 mT.

Figure 16: Comparative opex/MT

187199

6053

0

50

100

150

200

250

2012 2013

Halcyon Anson

Source: Company data, Credit Suisse

01 September 2014

Halcyon Agri Corporation Ltd (HALC.SI / HACL SP) 9

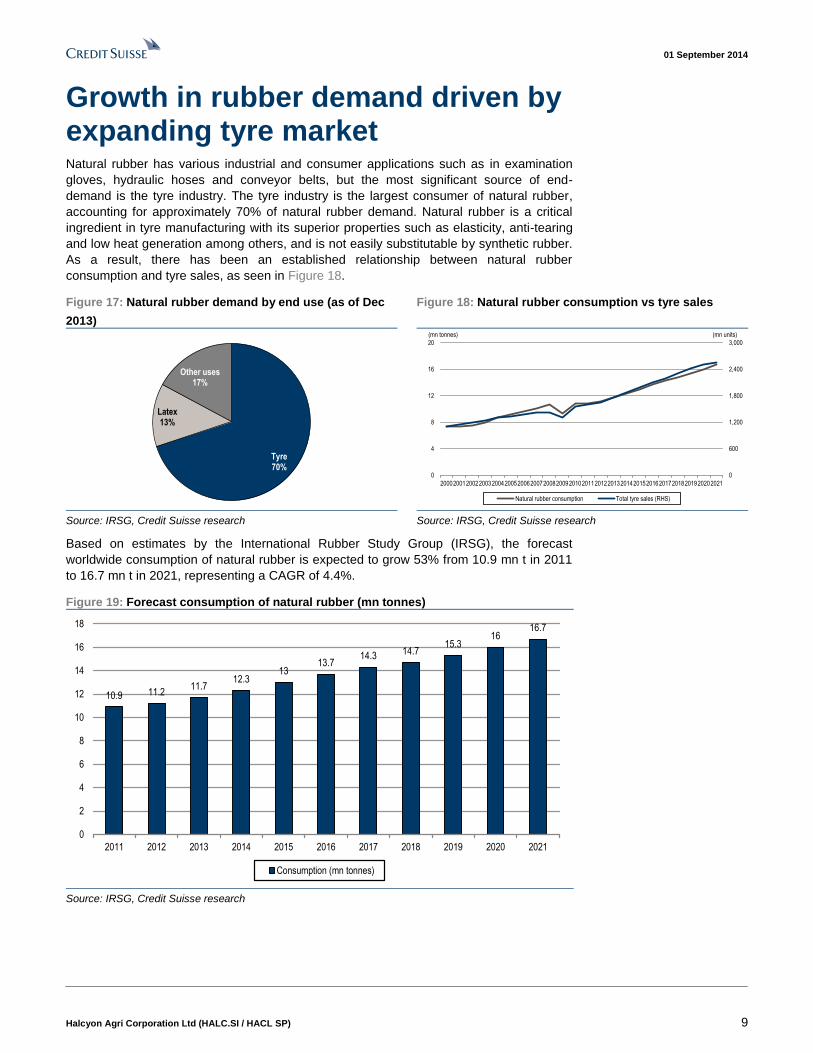

Growth in rubber demand driven by expanding tyre market Natural rubber has various industrial and consumer applications such as in examination

gloves, hydraulic hoses and conveyor belts, but the most significant source of end-

demand is the tyre industry. The tyre industry is the largest consumer of natural rubber,

accounting for approximately 70% of natural rubber demand. Natural rubber is a critical

ingredient in tyre manufacturing with its superior properties such as elasticity, anti-tearing

and low heat generation among others, and is not easily substitutable by synthetic rubber.

As a result, there has been an established relationship between natural rubber

consumption and tyre sales, as seen in Figure 18.

Figure 17: Natural rubber demand by end use (as of Dec

2013)

Figure 18: Natural rubber consumption vs tyre sales

Tyre70%

Latex13%

Other uses17%

0

600

1,200

1,800

2,400

3,000

0

4

8

12

16

20

2000200120022003200420052006200720082009201020112012201320142015201620172018201920202021

(mn units)(mn tonnes)

Natural rubber consumption Total tyre sales (RHS)

Source: IRSG, Credit Suisse research Source: IRSG, Credit Suisse research

Based on estimates by the International Rubber Study Group (IRSG), the forecast

worldwide consumption of natural rubber is expected to grow 53% from 10.9 mn t in 2011

to 16.7 mn t in 2021, representing a CAGR of 4.4%.

Figure 19: Forecast consumption of natural rubber (mn tonnes)

10.9 11.211.7

12.313

13.714.3 14.7

15.316

16.7

0

2

4

6

8

10

12

14

16

18

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Consumption (mn tonnes)

Source: IRSG, Credit Suisse research

01 September 2014

Halcyon Agri Corporation Ltd (HALC.SI / HACL SP) 10

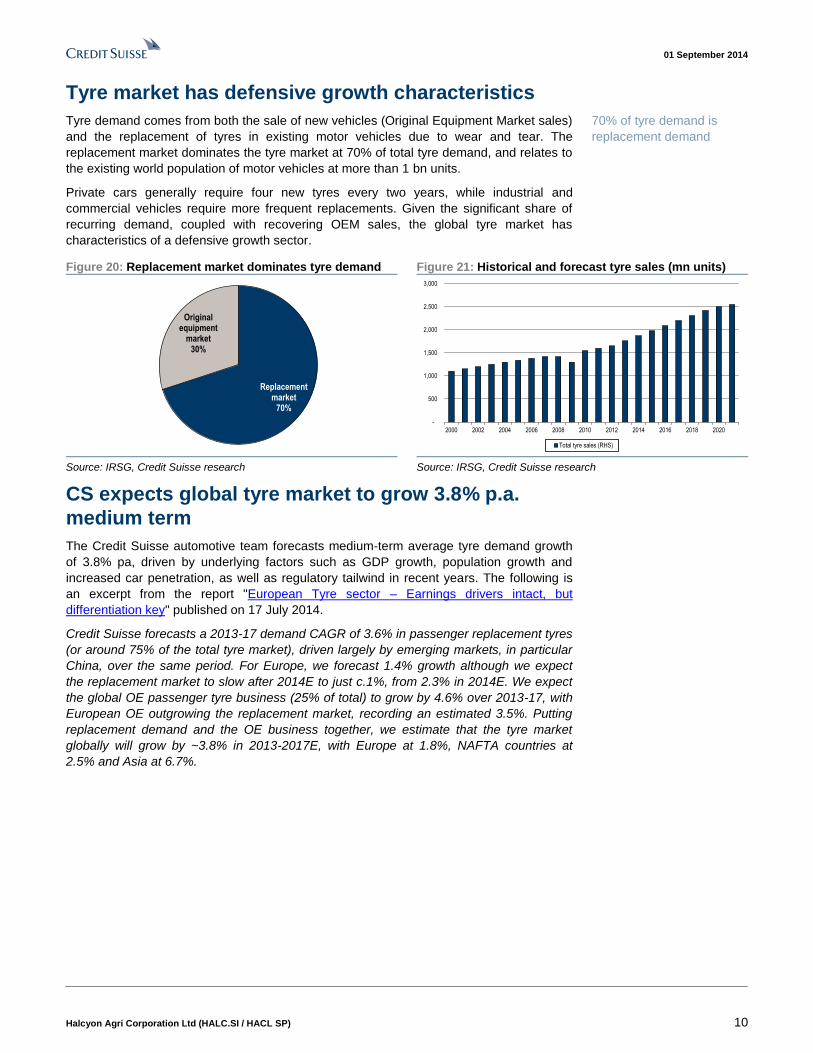

Tyre market has defensive growth characteristics

Tyre demand comes from both the sale of new vehicles (Original Equipment Market sales)

and the replacement of tyres in existing motor vehicles due to wear and tear. The

replacement market dominates the tyre market at 70% of total tyre demand, and relates to

the existing world population of motor vehicles at more than 1 bn units.

Private cars generally require four new tyres every two years, while industrial and

commercial vehicles require more frequent replacements. Given the significant share of

recurring demand, coupled with recovering OEM sales, the global tyre market has

characteristics of a defensive growth sector.

Figure 20: Replacement market dominates tyre demand Figure 21: Historical and forecast tyre sales (mn units)

Replacement market

70%

Original equipment

market30%

-

500

1,000

1,500

2,000

2,500

3,000

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Total tyre sales (RHS)

Source: IRSG, Credit Suisse research Source: IRSG, Credit Suisse research

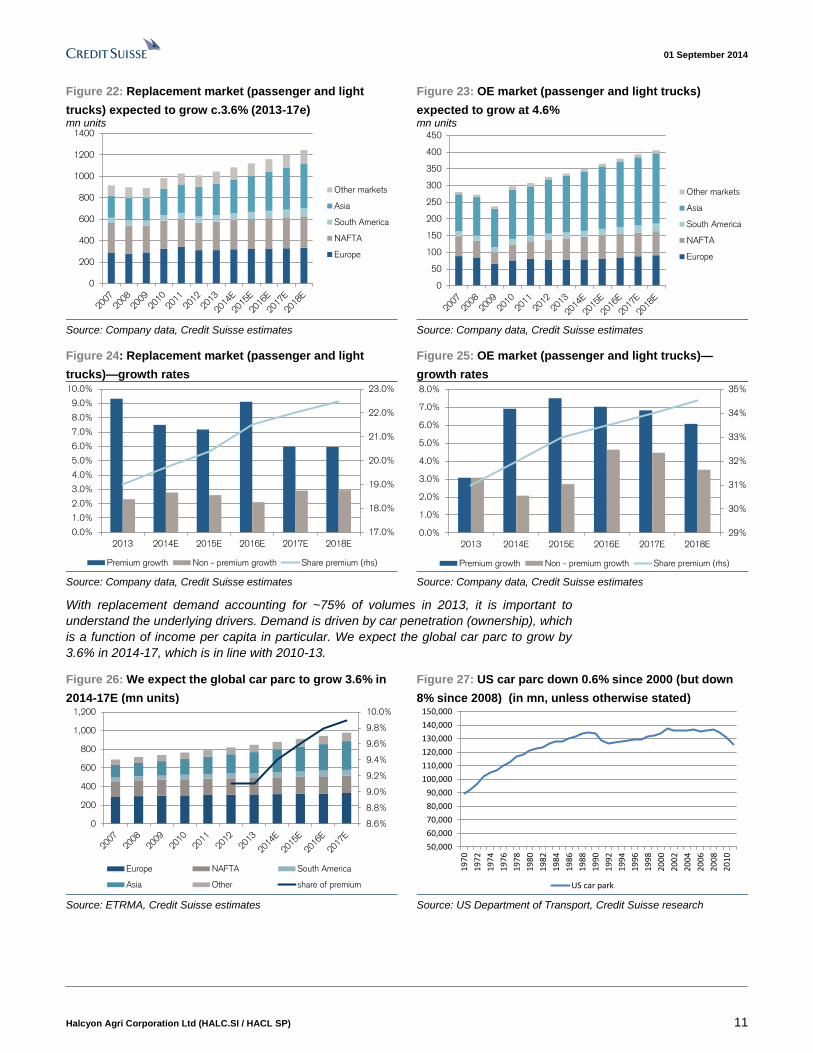

CS expects global tyre market to grow 3.8% p.a.

medium term

The Credit Suisse automotive team forecasts medium-term average tyre demand growth

of 3.8% pa, driven by underlying factors such as GDP growth, population growth and

increased car penetration, as well as regulatory tailwind in recent years. The following is

an excerpt from the report "European Tyre sector – Earnings drivers intact, but

differentiation key" published on 17 July 2014.

Credit Suisse forecasts a 2013-17 demand CAGR of 3.6% in passenger replacement tyres

(or around 75% of the total tyre market), driven largely by emerging markets, in particular

China, over the same period. For Europe, we forecast 1.4% growth although we expect

the replacement market to slow after 2014E to just c.1%, from 2.3% in 2014E. We expect

the global OE passenger tyre business (25% of total) to grow by 4.6% over 2013-17, with

European OE outgrowing the replacement market, recording an estimated 3.5%. Putting

replacement demand and the OE business together, we estimate that the tyre market

globally will grow by ~3.8% in 2013-2017E, with Europe at 1.8%, NAFTA countries at

2.5% and Asia at 6.7%.

70% of tyre demand is

replacement demand

01 September 2014

Halcyon Agri Corporation Ltd (HALC.SI / HACL SP) 11

Figure 22: Replacement market (passenger and light

trucks) expected to grow c.3.6% (2013-17e) mn units

Figure 23: OE market (passenger and light trucks)

expected to grow at 4.6% mn units

0

200

400

600

800

1000

1200

1400

Other markets

Asia

South America

NAFTA

Europe

0

50

100

150

200

250

300

350

400

450

Other markets

Asia

South America

NAFTA

Europe

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 24: Replacement market (passenger and light

trucks)—growth rates

Figure 25: OE market (passenger and light trucks)—

growth rates

17.0%

18.0%

19.0%

20.0%

21.0%

22.0%

23.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

2013 2014E 2015E 2016E 2017E 2018E

Premium growth Non - premium growth Share premium (rhs)

29%

30%

31%

32%

33%

34%

35%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

2013 2014E 2015E 2016E 2017E 2018E

Premium growth Non - premium growth Share premium (rhs)

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

With replacement demand accounting for ~75% of volumes in 2013, it is important to

understand the underlying drivers. Demand is driven by car penetration (ownership), which

is a function of income per capita in particular. We expect the global car parc to grow by

3.6% in 2014-17, which is in line with 2010-13.

Figure 26: We expect the global car parc to grow 3.6% in

2014-17E (mn units)

Figure 27: US car parc down 0.6% since 2000 (but down

8% since 2008) (in mn, unless otherwise stated)

8.6%

8.8%

9.0%

9.2%

9.4%

9.6%

9.8%

10.0%

0

200

400

600

800

1,000

1,200

Europe NAFTA South America

Asia Other share of premium

50,000

60,000

70,000

80,000

90,000

100,000

110,000

120,000

130,000

140,000

150,000

19

70

19

72

19

74

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

US car park

Source: ETRMA, Credit Suisse estimates Source: US Department of Transport, Credit Suisse research

01 September 2014

Halcyon Agri Corporation Ltd (HALC.SI / HACL SP) 12

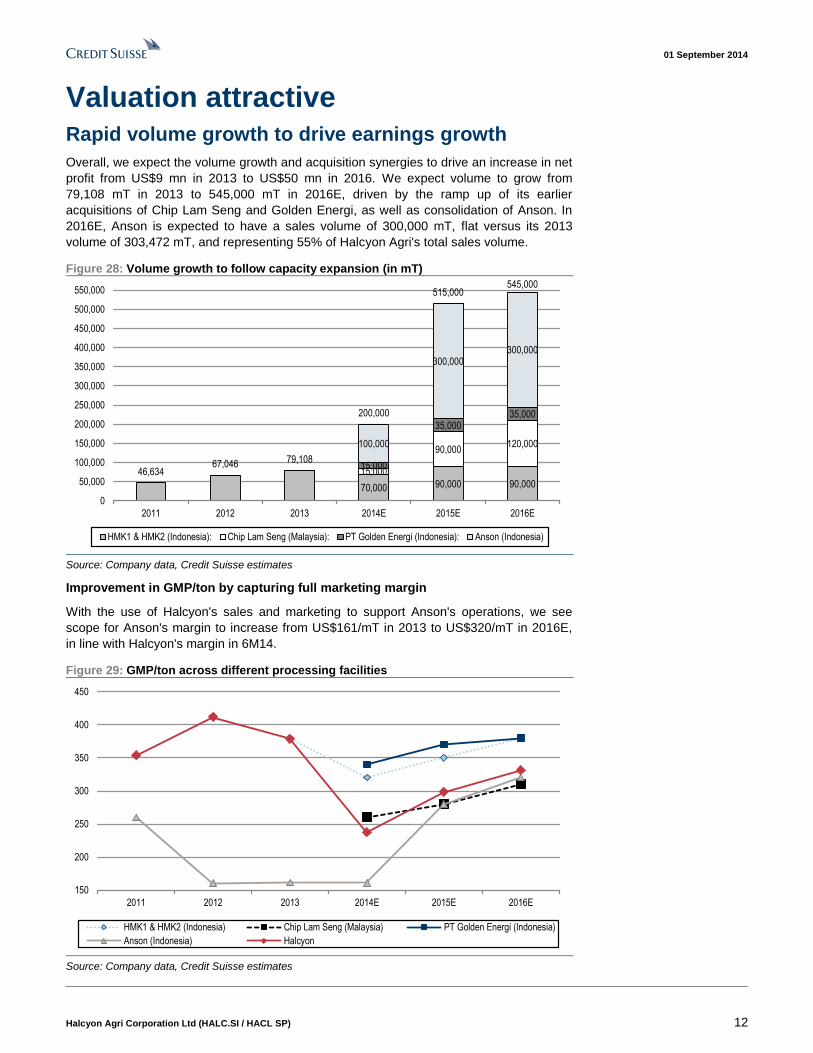

Valuation attractive Rapid volume growth to drive earnings growth

Overall, we expect the volume growth and acquisition synergies to drive an increase in net

profit from US$9 mn in 2013 to US$50 mn in 2016. We expect volume to grow from

79,108 mT in 2013 to 545,000 mT in 2016E, driven by the ramp up of its earlier

acquisitions of Chip Lam Seng and Golden Energi, as well as consolidation of Anson. In

2016E, Anson is expected to have a sales volume of 300,000 mT, flat versus its 2013

volume of 303,472 mT, and representing 55% of Halcyon Agri's total sales volume.

Figure 28: Volume growth to follow capacity expansion (in mT)

70,000 90,000 90,000

15,000

90,000120,000

15,000

35,00035,000

100,000

300,000300,000

46,63467,046 79,108

200,000

515,000545,000

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

550,000

2011 2012 2013 2014E 2015E 2016E

HMK1 & HMK2 (Indonesia): Chip Lam Seng (Malaysia): PT Golden Energi (Indonesia): Anson (Indonesia)

Source: Company data, Credit Suisse estimates

Improvement in GMP/ton by capturing full marketing margin

With the use of Halcyon's sales and marketing to support Anson's operations, we see

scope for Anson's margin to increase from US$161/mT in 2013 to US$320/mT in 2016E,

in line with Halcyon's margin in 6M14.

Figure 29: GMP/ton across different processing facilities

150

200

250

300

350

400

450

2011 2012 2013 2014E 2015E 2016E

HMK1 & HMK2 (Indonesia) Chip Lam Seng (Malaysia) PT Golden Energi (Indonesia)

Anson (Indonesia) Halcyon

Source: Company data, Credit Suisse estimates

01 September 2014

Halcyon Agri Corporation Ltd (HALC.SI / HACL SP) 13

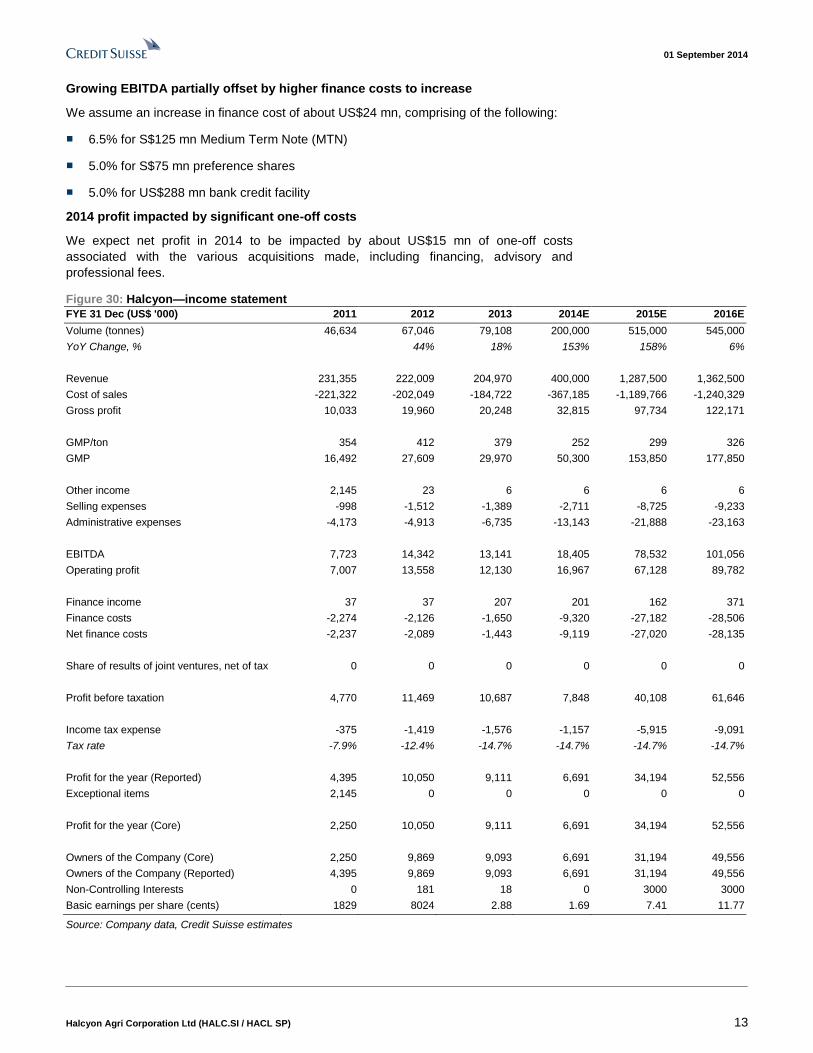

Growing EBITDA partially offset by higher finance costs to increase

We assume an increase in finance cost of about US$24 mn, comprising of the following:

■ 6.5% for S$125 mn Medium Term Note (MTN)

■ 5.0% for S$75 mn preference shares

■ 5.0% for US$288 mn bank credit facility

2014 profit impacted by significant one-off costs

We expect net profit in 2014 to be impacted by about US$15 mn of one-off costs

associated with the various acquisitions made, including financing, advisory and

professional fees.

Figure 30: Halcyon—income statement

FYE 31 Dec (US$ '000) 2011 2012 2013 2014E 2015E 2016E

Volume (tonnes) 46,634 67,046 79,108 200,000 515,000 545,000

YoY Change, % 44% 18% 153% 158% 6%

Revenue 231,355 222,009 204,970 400,000 1,287,500 1,362,500

Cost of sales -221,322 -202,049 -184,722 -367,185 -1,189,766 -1,240,329

Gross profit 10,033 19,960 20,248 32,815 97,734 122,171

GMP/ton 354 412 379 252 299 326

GMP 16,492 27,609 29,970 50,300 153,850 177,850

Other income 2,145 23 6 6 6 6

Selling expenses -998 -1,512 -1,389 -2,711 -8,725 -9,233

Administrative expenses -4,173 -4,913 -6,735 -13,143 -21,888 -23,163

EBITDA 7,723 14,342 13,141 18,405 78,532 101,056

Operating profit 7,007 13,558 12,130 16,967 67,128 89,782

Finance income 37 37 207 201 162 371

Finance costs -2,274 -2,126 -1,650 -9,320 -27,182 -28,506

Net finance costs -2,237 -2,089 -1,443 -9,119 -27,020 -28,135

Share of results of joint ventures, net of tax 0 0 0 0 0 0

Profit before taxation 4,770 11,469 10,687 7,848 40,108 61,646

Income tax expense -375 -1,419 -1,576 -1,157 -5,915 -9,091

Tax rate -7.9% -12.4% -14.7% -14.7% -14.7% -14.7%

Profit for the year (Reported) 4,395 10,050 9,111 6,691 34,194 52,556

Exceptional items 2,145 0 0 0 0 0

Profit for the year (Core) 2,250 10,050 9,111 6,691 34,194 52,556

Owners of the Company (Core) 2,250 9,869 9,093 6,691 31,194 49,556

Owners of the Company (Reported) 4,395 9,869 9,093 6,691 31,194 49,556

Non-Controlling Interests 0 181 18 0 3000 3000

Basic earnings per share (cents) 1829 8024 2.88 1.69 7.41 11.77

Source: Company data, Credit Suisse estimates

01 September 2014

Halcyon Agri Corporation Ltd (HALC.SI / HACL SP) 14

Figure 31: Halcyon—balance sheet

FYE 31 Dec (US$ '000) 2011 2012 2013 2014 2015 2016

Non-current assets 22,260 21,280 27,912 402,774 401,370 400,096

Other assets - - 2,054 64,294 64,294 64,294

Intangible assets 10,000 10,000 10,000 214,960 214,960 214,960

Property, plant and equipment 11,963 10,922 15,537 123,199 121,795 120,521

Investment in subsidiaries - - - 0 0 0

Deferred charges 251 202 124 124 124 124

Deferred tax assets 46 156 197 197 197 197

Current assets 34,826 40,829 79,896 228,333 289,401 368,523

Cash and bank balances 8,406 11,866 52,688 154,856 131,186 195,934

Trade receivables 10,611 6,816 7,347 19,726 63,493 67,192

Other receivables 1,512 1,131 2,549 2,549 2,549 2,549

Derivative financial instruments 3,067 718 903 903 903 903

Inventories 11,230 20,298 16,409 50,299 91,270 101,945

Total assets 57,086 62,109 107,808 631,107 690,771 768,619

Current liabilities 31,167 34,723 26,107 302,588 331,374 359,981

Derivative financial instruments 1,282 977 789 789 789 789

Trade payables 33 1,626 0 0 0 0

Other payables 7,318 3,028 2,823 5,570 18,047 18,814

Loan payables 22,329 28,110 21,143 294,878 311,186 339,026

Provision for taxation 205 982 1,352 1,352 1,352 1,352

Non-current liabilities 8,897 1,116 1,429 151,429 151,429 151,429

Loan payables 8,500 - - 150,000 150,000 150,000

Retirement benefit obligations 222 529 648 648 648 648

Deferred tax liabilities 175 587 781 781 781 781

Total liabilities 40,064 35,839 27,536 454,017 482,803 511,410

Equity attributable to owners of the Company 17,022 26,089 80,110 116,927 144,806 191,047

Share capital 12,500 12,500 63,713 96,958 96,958 96,958

Capital reserves 143 143 143 143 143 143

Accumulated profits (losses) 4,503 14,372 21,195 24,767 52,646 98,887

Foreign currency translation reserve -124 -926 -4,941 -4,941 -4,941 -4,941

Non-controlling interests - 181 162 60,162 63,162 66,162

Total equity 17,022 26,270 80,272 177,089 207,968 257,209

Source: Company data, Credit Suisse estimates

01 September 2014

Halcyon Agri Corporation Ltd (HALC.SI / HACL SP) 15

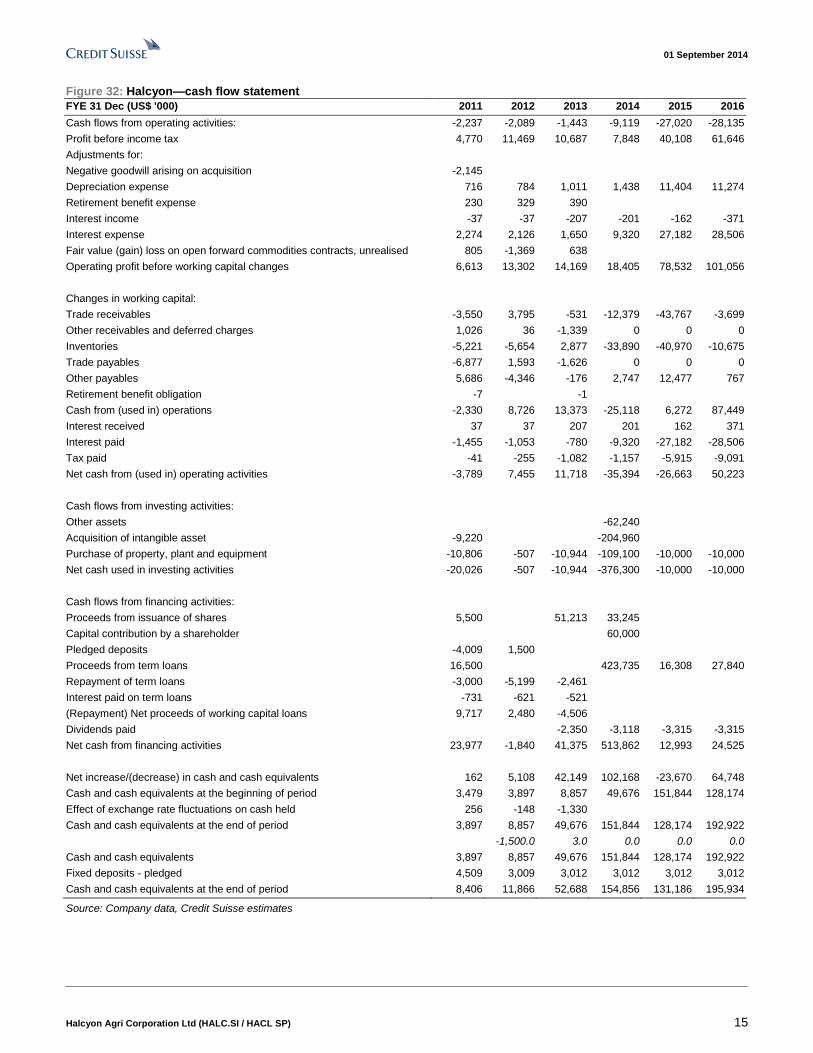

Figure 32: Halcyon—cash flow statement

FYE 31 Dec (US$ '000) 2011 2012 2013 2014 2015 2016

Cash flows from operating activities: -2,237 -2,089 -1,443 -9,119 -27,020 -28,135

Profit before income tax 4,770 11,469 10,687 7,848 40,108 61,646

Adjustments for:

Negative goodwill arising on acquisition -2,145

Depreciation expense 716 784 1,011 1,438 11,404 11,274

Retirement benefit expense 230 329 390

Interest income -37 -37 -207 -201 -162 -371

Interest expense 2,274 2,126 1,650 9,320 27,182 28,506

Fair value (gain) loss on open forward commodities contracts, unrealised 805 -1,369 638

Operating profit before working capital changes 6,613 13,302 14,169 18,405 78,532 101,056

Changes in working capital:

Trade receivables -3,550 3,795 -531 -12,379 -43,767 -3,699

Other receivables and deferred charges 1,026 36 -1,339 0 0 0

Inventories -5,221 -5,654 2,877 -33,890 -40,970 -10,675

Trade payables -6,877 1,593 -1,626 0 0 0

Other payables 5,686 -4,346 -176 2,747 12,477 767

Retirement benefit obligation -7 -1

Cash from (used in) operations -2,330 8,726 13,373 -25,118 6,272 87,449

Interest received 37 37 207 201 162 371

Interest paid -1,455 -1,053 -780 -9,320 -27,182 -28,506

Tax paid -41 -255 -1,082 -1,157 -5,915 -9,091

Net cash from (used in) operating activities -3,789 7,455 11,718 -35,394 -26,663 50,223

Cash flows from investing activities:

Other assets -62,240

Acquisition of intangible asset -9,220 -204,960

Purchase of property, plant and equipment -10,806 -507 -10,944 -109,100 -10,000 -10,000

Net cash used in investing activities -20,026 -507 -10,944 -376,300 -10,000 -10,000

Cash flows from financing activities:

Proceeds from issuance of shares 5,500 51,213 33,245

Capital contribution by a shareholder 60,000

Pledged deposits -4,009 1,500

Proceeds from term loans 16,500 423,735 16,308 27,840

Repayment of term loans -3,000 -5,199 -2,461

Interest paid on term loans -731 -621 -521

(Repayment) Net proceeds of working capital loans 9,717 2,480 -4,506

Dividends paid -2,350 -3,118 -3,315 -3,315

Net cash from financing activities 23,977 -1,840 41,375 513,862 12,993 24,525

Net increase/(decrease) in cash and cash equivalents 162 5,108 42,149 102,168 -23,670 64,748

Cash and cash equivalents at the beginning of period 3,479 3,897 8,857 49,676 151,844 128,174

Effect of exchange rate fluctuations on cash held 256 -148 -1,330

Cash and cash equivalents at the end of period 3,897 8,857 49,676 151,844 128,174 192,922

-1,500.0 3.0 0.0 0.0 0.0

Cash and cash equivalents 3,897 8,857 49,676 151,844 128,174 192,922

Fixed deposits - pledged 4,509 3,009 3,012 3,012 3,012 3,012

Cash and cash equivalents at the end of period 8,406 11,866 52,688 154,856 131,186 195,934

Source: Company data, Credit Suisse estimates

01 September 2014

Halcyon Agri Corporation Ltd (HALC.SI / HACL SP) 16

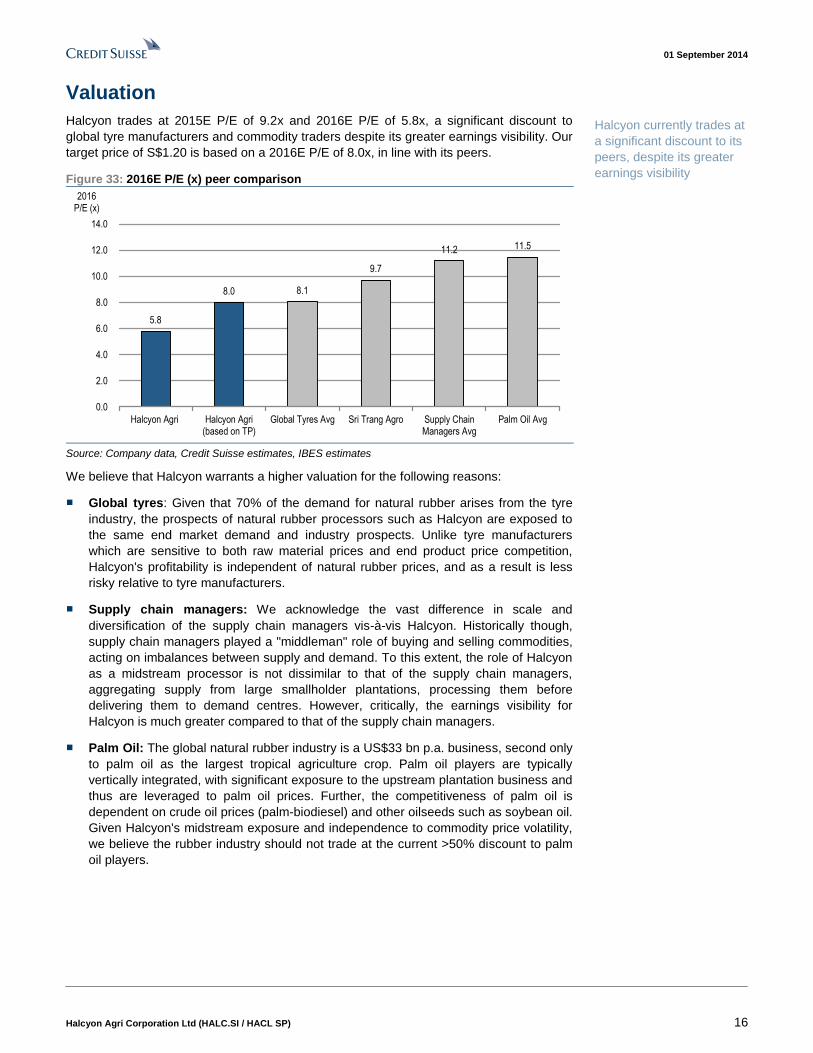

Valuation

Halcyon trades at 2015E P/E of 9.2x and 2016E P/E of 5.8x, a significant discount to

global tyre manufacturers and commodity traders despite its greater earnings visibility. Our

target price of S$1.20 is based on a 2016E P/E of 8.0x, in line with its peers.

Figure 33: 2016E P/E (x) peer comparison

5.8

8.0 8.1

9.7

11.2 11.5

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Halcyon Agri Halcyon Agri(based on TP)

Global Tyres Avg Sri Trang Agro Supply ChainManagers Avg

Palm Oil Avg

2016 P/E (x)

Source: Company data, Credit Suisse estimates, IBES estimates

We believe that Halcyon warrants a higher valuation for the following reasons:

■ Global tyres: Given that 70% of the demand for natural rubber arises from the tyre

industry, the prospects of natural rubber processors such as Halcyon are exposed to

the same end market demand and industry prospects. Unlike tyre manufacturers

which are sensitive to both raw material prices and end product price competition,

Halcyon's profitability is independent of natural rubber prices, and as a result is less

risky relative to tyre manufacturers.

■ Supply chain managers: We acknowledge the vast difference in scale and

diversification of the supply chain managers vis-à-vis Halcyon. Historically though,

supply chain managers played a "middleman" role of buying and selling commodities,

acting on imbalances between supply and demand. To this extent, the role of Halcyon

as a midstream processor is not dissimilar to that of the supply chain managers,

aggregating supply from large smallholder plantations, processing them before

delivering them to demand centres. However, critically, the earnings visibility for

Halcyon is much greater compared to that of the supply chain managers.

■ Palm Oil: The global natural rubber industry is a US$33 bn p.a. business, second only

to palm oil as the largest tropical agriculture crop. Palm oil players are typically

vertically integrated, with significant exposure to the upstream plantation business and

thus are leveraged to palm oil prices. Further, the competitiveness of palm oil is

dependent on crude oil prices (palm-biodiesel) and other oilseeds such as soybean oil.

Given Halcyon's midstream exposure and independence to commodity price volatility,

we believe the rubber industry should not trade at the current >50% discount to palm

oil players.

Halcyon currently trades at

a significant discount to its

peers, despite its greater

earnings visibility

01 September 2014

Halcyon Agri Corporation Ltd (HALC.SI / HACL SP) 17

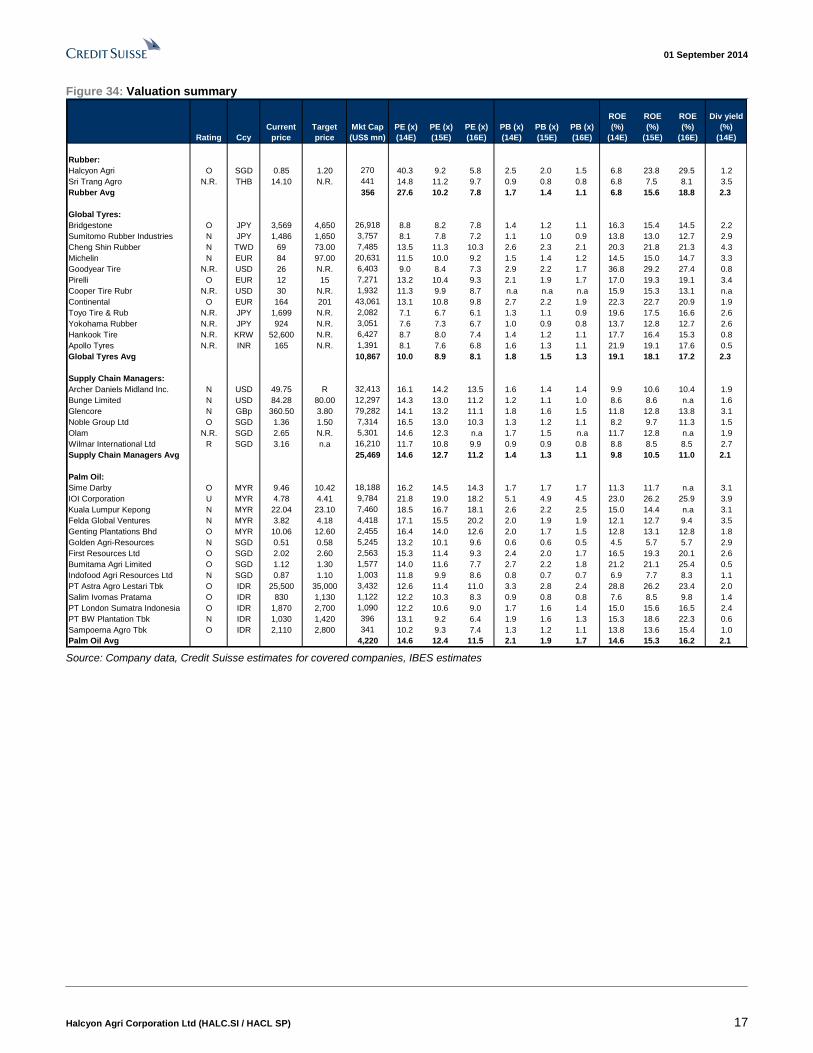

Figure 34: Valuation summary

Rating Ccy

Current

price

Target

price

Mkt Cap

(US$ mn)

PE (x)

(14E)

PE (x)

(15E)

PE (x)

(16E)

PB (x)

(14E)

PB (x)

(15E)

PB (x)

(16E)

ROE

(%)

(14E)

ROE

(%)

(15E)

ROE

(%)

(16E)

Div yield

(%)

(14E)

Rubber:

Halcyon Agri O SGD 0.85 1.20 270 40.3 9.2 5.8 2.5 2.0 1.5 6.8 23.8 29.5 1.2

Sri Trang Agro N.R. THB 14.10 N.R. 441 14.8 11.2 9.7 0.9 0.8 0.8 6.8 7.5 8.1 3.5

Rubber Avg 356 27.6 10.2 7.8 1.7 1.4 1.1 6.8 15.6 18.8 2.3

Global Tyres:

Bridgestone O JPY 3,569 4,650 26,918 8.8 8.2 7.8 1.4 1.2 1.1 16.3 15.4 14.5 2.2

Sumitomo Rubber Industries N JPY 1,486 1,650 3,757 8.1 7.8 7.2 1.1 1.0 0.9 13.8 13.0 12.7 2.9

Cheng Shin Rubber N TWD 69 73.00 7,485 13.5 11.3 10.3 2.6 2.3 2.1 20.3 21.8 21.3 4.3

Michelin N EUR 84 97.00 20,631 11.5 10.0 9.2 1.5 1.4 1.2 14.5 15.0 14.7 3.3

Goodyear Tire N.R. USD 26 N.R. 6,403 9.0 8.4 7.3 2.9 2.2 1.7 36.8 29.2 27.4 0.8

Pirelli O EUR 12 15 7,271 13.2 10.4 9.3 2.1 1.9 1.7 17.0 19.3 19.1 3.4

Cooper Tire Rubr N.R. USD 30 N.R. 1,932 11.3 9.9 8.7 n.a n.a n.a 15.9 15.3 13.1 n.a

Continental O EUR 164 201 43,061 13.1 10.8 9.8 2.7 2.2 1.9 22.3 22.7 20.9 1.9

Toyo Tire & Rub N.R. JPY 1,699 N.R. 2,082 7.1 6.7 6.1 1.3 1.1 0.9 19.6 17.5 16.6 2.6

Yokohama Rubber N.R. JPY 924 N.R. 3,051 7.6 7.3 6.7 1.0 0.9 0.8 13.7 12.8 12.7 2.6

Hankook Tire N.R. KRW 52,600 N.R. 6,427 8.7 8.0 7.4 1.4 1.2 1.1 17.7 16.4 15.3 0.8

Apollo Tyres N.R. INR 165 N.R. 1,391 8.1 7.6 6.8 1.6 1.3 1.1 21.9 19.1 17.6 0.5

Global Tyres Avg 10,867 10.0 8.9 8.1 1.8 1.5 1.3 19.1 18.1 17.2 2.3

Supply Chain Managers:

Archer Daniels Midland Inc. N USD 49.75 R 32,413 16.1 14.2 13.5 1.6 1.4 1.4 9.9 10.6 10.4 1.9

Bunge Limited N USD 84.28 80.00 12,297 14.3 13.0 11.2 1.2 1.1 1.0 8.6 8.6 n.a 1.6

Glencore N GBp 360.50 3.80 79,282 14.1 13.2 11.1 1.8 1.6 1.5 11.8 12.8 13.8 3.1

Noble Group Ltd O SGD 1.36 1.50 7,314 16.5 13.0 10.3 1.3 1.2 1.1 8.2 9.7 11.3 1.5

Olam N.R. SGD 2.65 N.R. 5,301 14.6 12.3 n.a 1.7 1.5 n.a 11.7 12.8 n.a 1.9

Wilmar International Ltd R SGD 3.16 n.a 16,210 11.7 10.8 9.9 0.9 0.9 0.8 8.8 8.5 8.5 2.7

Supply Chain Managers Avg 25,469 14.6 12.7 11.2 1.4 1.3 1.1 9.8 10.5 11.0 2.1

Palm Oil:

Sime Darby O MYR 9.46 10.42 18,188 16.2 14.5 14.3 1.7 1.7 1.7 11.3 11.7 n.a 3.1

IOI Corporation U MYR 4.78 4.41 9,784 21.8 19.0 18.2 5.1 4.9 4.5 23.0 26.2 25.9 3.9

Kuala Lumpur Kepong N MYR 22.04 23.10 7,460 18.5 16.7 18.1 2.6 2.2 2.5 15.0 14.4 n.a 3.1

Felda Global Ventures N MYR 3.82 4.18 4,418 17.1 15.5 20.2 2.0 1.9 1.9 12.1 12.7 9.4 3.5

Genting Plantations Bhd O MYR 10.06 12.60 2,455 16.4 14.0 12.6 2.0 1.7 1.5 12.8 13.1 12.8 1.8

Golden Agri-Resources N SGD 0.51 0.58 5,245 13.2 10.1 9.6 0.6 0.6 0.5 4.5 5.7 5.7 2.9

First Resources Ltd O SGD 2.02 2.60 2,563 15.3 11.4 9.3 2.4 2.0 1.7 16.5 19.3 20.1 2.6

Bumitama Agri Limited O SGD 1.12 1.30 1,577 14.0 11.6 7.7 2.7 2.2 1.8 21.2 21.1 25.4 0.5

Indofood Agri Resources Ltd N SGD 0.87 1.10 1,003 11.8 9.9 8.6 0.8 0.7 0.7 6.9 7.7 8.3 1.1

PT Astra Agro Lestari Tbk O IDR 25,500 35,000 3,432 12.6 11.4 11.0 3.3 2.8 2.4 28.8 26.2 23.4 2.0

Salim Ivomas Pratama O IDR 830 1,130 1,122 12.2 10.3 8.3 0.9 0.8 0.8 7.6 8.5 9.8 1.4

PT London Sumatra Indonesia O IDR 1,870 2,700 1,090 12.2 10.6 9.0 1.7 1.6 1.4 15.0 15.6 16.5 2.4

PT BW Plantation Tbk N IDR 1,030 1,420 396 13.1 9.2 6.4 1.9 1.6 1.3 15.3 18.6 22.3 0.6

Sampoerna Agro Tbk O IDR 2,110 2,800 341 10.2 9.3 7.4 1.3 1.2 1.1 13.8 13.6 15.4 1.0

Palm Oil Avg 4,220 14.6 12.4 11.5 2.1 1.9 1.7 14.6 15.3 16.2 2.1 Source: Company data, Credit Suisse estimates for covered companies, IBES estimates

01 September 2014

Halcyon Agri Corporation Ltd (HALC.SI / HACL SP) 18

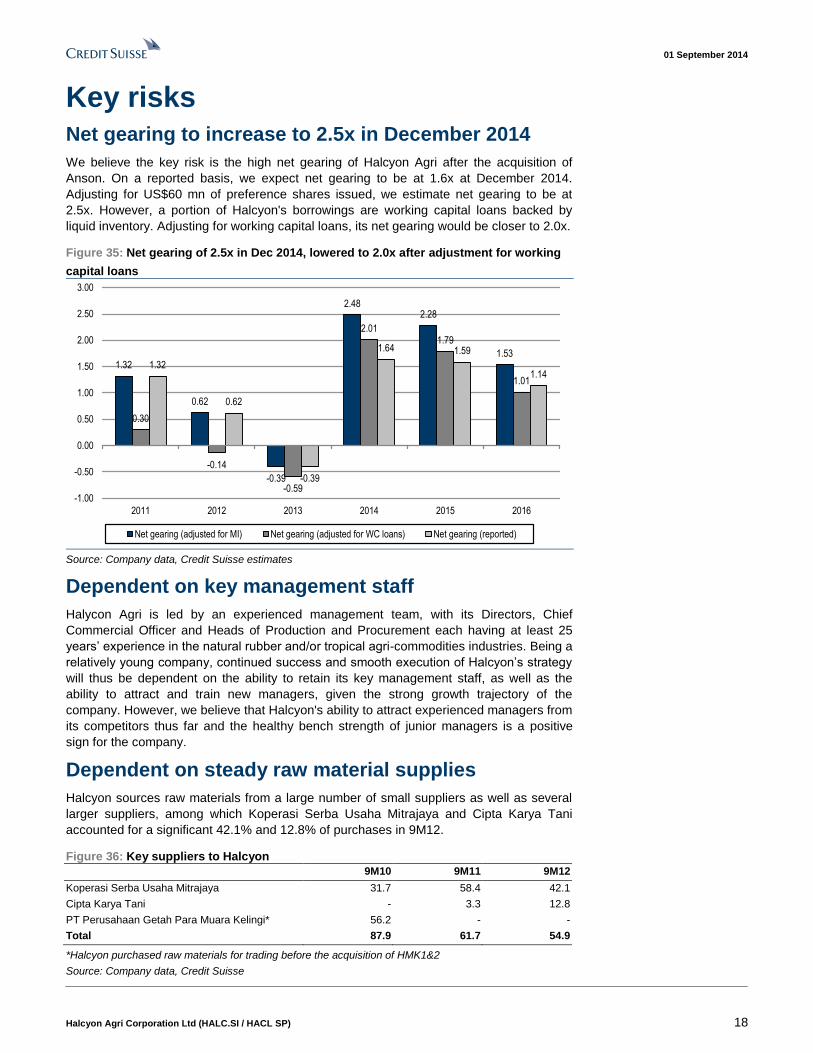

Key risks Net gearing to increase to 2.5x in December 2014

We believe the key risk is the high net gearing of Halcyon Agri after the acquisition of

Anson. On a reported basis, we expect net gearing to be at 1.6x at December 2014.

Adjusting for US$60 mn of preference shares issued, we estimate net gearing to be at

2.5x. However, a portion of Halcyon's borrowings are working capital loans backed by

liquid inventory. Adjusting for working capital loans, its net gearing would be closer to 2.0x.

Figure 35: Net gearing of 2.5x in Dec 2014, lowered to 2.0x after adjustment for working

capital loans

1.32

0.62

-0.39

2.482.28

1.53

0.30

-0.14

-0.59

2.011.79

1.01

1.32

0.62

-0.39

1.64 1.59

1.14

-1.00

-0.50

0.00

0.50

1.00

1.50

2.00

2.50

3.00

2011 2012 2013 2014 2015 2016

Net gearing (adjusted for MI) Net gearing (adjusted for WC loans) Net gearing (reported)

Source: Company data, Credit Suisse estimates

Dependent on key management staff

Halycon Agri is led by an experienced management team, with its Directors, Chief

Commercial Officer and Heads of Production and Procurement each having at least 25

years’ experience in the natural rubber and/or tropical agri-commodities industries. Being a

relatively young company, continued success and smooth execution of Halcyon’s strategy

will thus be dependent on the ability to retain its key management staff, as well as the

ability to attract and train new managers, given the strong growth trajectory of the

company. However, we believe that Halcyon's ability to attract experienced managers from

its competitors thus far and the healthy bench strength of junior managers is a positive

sign for the company.

Dependent on steady raw material supplies

Halcyon sources raw materials from a large number of small suppliers as well as several

larger suppliers, among which Koperasi Serba Usaha Mitrajaya and Cipta Karya Tani

accounted for a significant 42.1% and 12.8% of purchases in 9M12.

Figure 36: Key suppliers to Halcyon

9M10 9M11 9M12

Koperasi Serba Usaha Mitrajaya 31.7 58.4 42.1

Cipta Karya Tani - 3.3 12.8

PT Perusahaan Getah Para Muara Kelingi* 56.2 - -

Total 87.9 61.7 54.9

*Halcyon purchased raw materials for trading before the acquisition of HMK1&2

Source: Company data, Credit Suisse

01 September 2014

Halcyon Agri Corporation Ltd (HALC.SI / HACL SP) 19

Given that Halcyon does not have long-term supply contracts with any of its suppliers, and

transacts largely on a cash-on-delivery basis with all its suppliers in line with industry

practices, it is dependent on the steady supply of raw materials at fair prices to fulfil its

obligations to customers. Unfavourable weather conditions and other supply side

constraints may thus affect the availability of raw materials from suppliers, and restrict

Halcyon’s ability to grow its processing volumes. Through geographical expansion to

Malaysia, we believe Halcyon's dependence on its key suppliers will progressively come

down over the coming periods.

Major customers account for significant revenues

Sales to Halcyon’s major customers account for a substantial portion of total revenues:

Figure 37: Customers accounting for more than 5% of total revenue

(%) 9M10 9M11 9M12

Cooper Tire 72.8 48.7 38.8

Bridgestone - 7.5 13.7

Sri Trang International - 16 13.1

New Continent Enterprise - 9.5 12.9

Marubeni 7.6 14.9 9.3

Continental 17.2 - -

Total 97.6 96.6 87.8

Source: Company data, Credit Suisse

Top five customers of Halcyon in 9M12 are the established international tyre

manufacturers and trading houses, and they contributed 88% of total revenue for 9M12.

Material cancellations or reduction in orders from these key customers would thus have a

significant impact on Halcyon. We expect its customer base to be more diversified with the

acquisition of Chip Lam Seng, which has approvals to sell processed rubber to new

customers such as Hankook and Nexen.

Significant exposure to tyre industry

Given that the tyre industry represents the largest end market for natural rubber, and that

virtually all of Halcyon’s products are sold directly or indirectly to the tyre manufacturers,

Halcyon is substantially exposed to the end market demand in the tyre industry.

A sizeable number of Halcyon’s direct customers include the leading tyre manufacturers,

who require their suppliers to undertake a rigorous qualification programme to ensure that

their output meets the standards required. These customers also enforce strict quality

control standards on their natural rubber suppliers, and as a result any suspension of

approval status and product claims may adversely affect the long term sales relationship

of Halcyon and its key customers. However, despite the short operating history of Halcyon,

the company is already an approved supplier to nine of the major tyre manufacturers, with

steady progress being made on approvals with the other major manufacturers. As such,

we believe that the right systems and processes are in place to ensure continued

compliance with the rigorous qualification programmes of Halcyon's customers.

Funding risk

Halcyon transacts on a cash-on-delivery basis with all its suppliers, while payment periods

for its customers generally range from 2 to 15 days upon delivery. In addition, natural

rubber yields are lowest during the wintering period, which typically spans from August to

October. As a result, inventory holdings of raw materials typically increase during the

wintering period to manage exposure to seasonality. Given the significant amount of cash

involved in its operations, Halcyon relies on working capital facilities provided by the banks

to fund its purchases, and in times of higher market prices for natural rubber, working

capital requirements will increase. Halcyon will thus be affected should it be unable to

continue to access sufficient working capital at reasonable rates. However, we understand

01 September 2014

Halcyon Agri Corporation Ltd (HALC.SI / HACL SP) 20

that significant undrawn capacity exists for the working capital facilities provided by the

banks. Further, such loans are collateralised by the inventories purchased, thus providing

greater security to the lending banks and correspondingly, lower funding risks to Halcyon.

Foreign currency risk

At present, all of Halcyon's purchases are denominated in IDR, given that raw materials

are purchased from the local suppliers on a daily basis, while all of Halcyon's revenues are

denominated in USD. In 9M12, approximately 47.7%, 31.8% and 20.5% of the group’s

expenses were denominated in SGD, USD and IDR, respectively. Foreign currency

exposure thus arises from timing differences between invoicing and collection and

payment and may affect the financial position of Halcyon as it does not currently have a

formal foreign currency hedging policy in place. On an operational basis, foreign currency

risk for Halcyon is mitigated through the daily purchasing of raw materials, with the

exchange rate fixed on a daily basis. Halcyon thus does not seek to take a position on

foreign currencies, and is thus less susceptible to the volatilities in the foreign exchange

market.

01 September 2014

Halcyon Agri Corporation Ltd (HALC.SI / HACL SP) 21

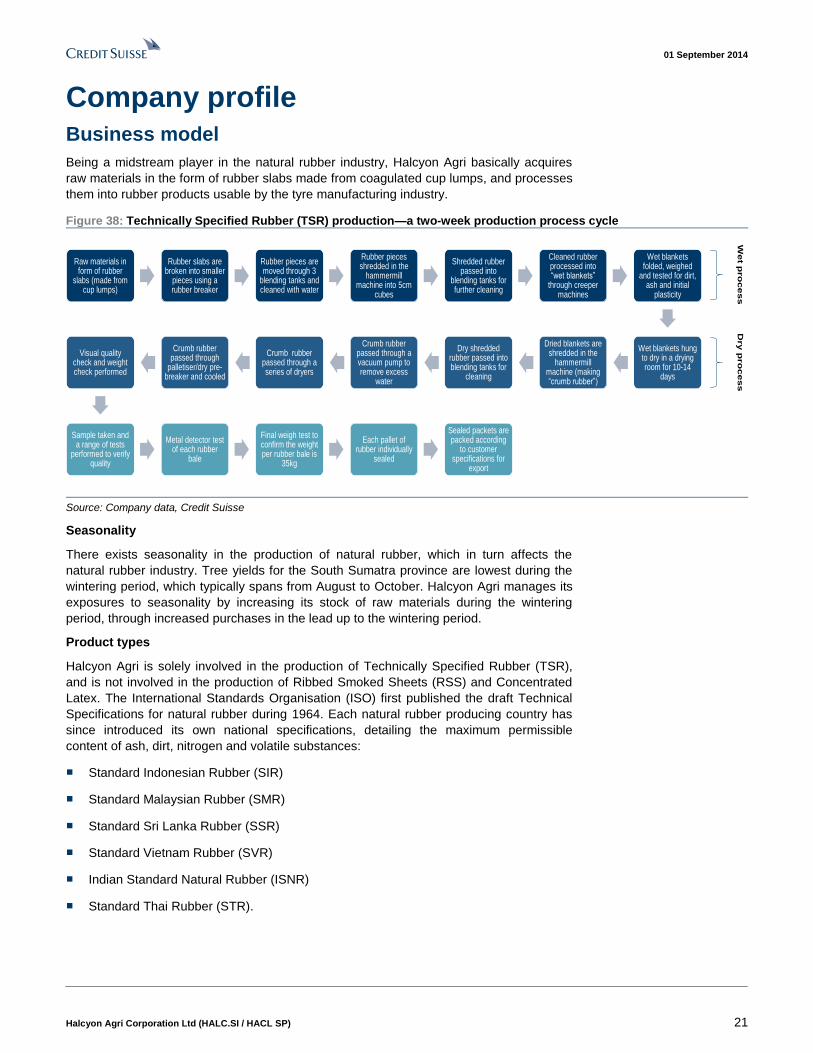

Company profile Business model

Being a midstream player in the natural rubber industry, Halcyon Agri basically acquires

raw materials in the form of rubber slabs made from coagulated cup lumps, and processes

them into rubber products usable by the tyre manufacturing industry.

Figure 38: Technically Specified Rubber (TSR) production—a two-week production process cycle

Raw materials in form of rubber

slabs (made from cup lumps)

Rubber slabs are broken into smaller

pieces using a rubber breaker

Rubber pieces are moved through 3

blending tanks and cleaned with water

Rubber pieces shredded in the

hammermillmachine into 5cm

cubes

Shredded rubber passed into

blending tanks for further cleaning

Cleaned rubber processed into “wet blankets”

through creeper machines

Wet blankets folded, weighed

and tested for dirt, ash and initial

plasticity

Wet blankets hung to dry in a drying room for 10-14

days

Dried blankets are shredded in the

hammermillmachine (making “crumb rubber”)

Dry shredded rubber passed into blending tanks for

cleaning

Crumb rubber passed through a vacuum pump to remove excess

water

Crumb rubber passed through a series of dryers

Crumb rubber passed through

palletiser/dry pre-breaker and cooled

Visual quality check and weight check performed

Sample taken and a range of tests

performed to verify quality

Metal detector test of each rubber

bale

Final weigh test to confirm the weight per rubber bale is

35kg

Each pallet of rubber individually

sealed

Sealed packets are packed according

to customer specifications for

export

We

t pro

ce

ss

Dry p

ro

ce

ss

Source: Company data, Credit Suisse

Seasonality

There exists seasonality in the production of natural rubber, which in turn affects the

natural rubber industry. Tree yields for the South Sumatra province are lowest during the

wintering period, which typically spans from August to October. Halcyon Agri manages its

exposures to seasonality by increasing its stock of raw materials during the wintering

period, through increased purchases in the lead up to the wintering period.

Product types

Halcyon Agri is solely involved in the production of Technically Specified Rubber (TSR),

and is not involved in the production of Ribbed Smoked Sheets (RSS) and Concentrated

Latex. The International Standards Organisation (ISO) first published the draft Technical

Specifications for natural rubber during 1964. Each natural rubber producing country has

since introduced its own national specifications, detailing the maximum permissible

content of ash, dirt, nitrogen and volatile substances:

■ Standard Indonesian Rubber (SIR)

■ Standard Malaysian Rubber (SMR)

■ Standard Sri Lanka Rubber (SSR)

■ Standard Vietnam Rubber (SVR)

■ Indian Standard Natural Rubber (ISNR)

■ Standard Thai Rubber (STR).

01 September 2014

Halcyon Agri Corporation Ltd (HALC.SI / HACL SP) 22

Figure 39: Standard Indonesian Rubber (SIR)

TSR CV TSR L TSR 5 TSR 10 TSR 20

Parameter Unit SIR 3CV50 SIR 3CV60 SIR 3L SIR 3WF SIR 5 SIR 10 SIR 10VK SIR 20 SIR 20VK

Dirt (max) % wt 0.03 0.03 0.03 0.03 0.05 0.1 0.1 0.2 0.2

Ash (max) % wt 0.5 0.5 0.5 0.5 0.5 0.75 0.75 1 1

Nitrogen (max) % wt 0.6 0.6 0.6 0.6 0.6 0.6 0.6 0.6 0.6

Volatile Matter (max) % wt 0.6 0.6 0.8 0.8 0.8 0.8 0.8 0.8 0.8

Initial Plasticity (min) 30 30 30 30 30 30 30 30 30

PRI index (min) 60 60 75 75 70 60 60 50 50

Colour Lovibond Scale (individual

value, max)

NA NA 6 NA NA NA NA NA NA

Mooney Viscosity (ML, 1+4, 100°C) 50 +/- 5 60 +/- 5 NA NA NA NA 60 +/- 5* NA 60 +/- 5*

Source: Inpol, Credit Suisse; *Not specification status, but are controlled at the producer end.

Being of Indonesian origin, Halcyon Agri produces TSR of varying specifications, all of

which are mainly used as key inputs in the manufacture of vehicle tyres:

■ SIR20: Standard medium grade rubber

■ SIR20-VK: Highly sought by customers due to technical properties, allowing tyre

manufacturers to lower their energy costs and increase manufacturing throughput.

Priced at a premium over SIR20.

■ SIR20-Compound: Suited in particular to the China market

■ Other products: SIR10, SIR10-VK

Revenues

Revenues are derived through the sale of natural rubber products, with minimal revenue

recognition due to the associated physical rubber hedging revenues and revenues from

the unrealised fair value gain/(loss) in open forward commodity contracts. Revenues are

thus largely driven by sales volume of rubber products sold.

Sales are conducted on a spot basis for delivery within three months, or conducted based

on long-term contracts. A majority of Halcyon Agri's volumes are sold through long-term

sales contracts ranging from 3 to 12 months, with a specified volume, delivery schedule

and pricing basis. Given the better visibility on demand and its corresponding effect on

procurement and production planning, Halcyon Agri seeks to have the majority of sales on

the basis of long-term contracts, with 74% of sales volume and 77% of revenue derived

from long-term contracts in 9M12.

Given the pricing premium of SIR20-VK and the strong demand-supply fundamentals,

Halycon Agri also seeks to maximise the production of SIR20-VK given its attractiveness

to tyre manufacturers.

Revenue breakdown by geography

The breakdown of revenue /sale and trading of processed rubber is based on the origin of

its customers’ ultimate parent company. Given that Cooper Tire accounts for a majority of

Halcyon Agri's revenues, sales to the US similarly accounts for a majority of its revenues.

01 September 2014

Halcyon Agri Corporation Ltd (HALC.SI / HACL SP) 23

Figure 40: Halcyon Agri revenue breakdown by geography

9M10 2011 2012

US$ mn % share US$ mn % share US$ mn % share

USA 7.2 72.7 110.7 48.7 89.2 40.4

Asia (ex SG & China) 0.8 8.1 87.3 38.4 80.1 36.3

Singapore 0.2 2.0 28.5 12.5 41.8 19.0

Europe 1.7 17.2 0.8 0.3 8.4 3.8

China - - - - 1.1 0.5

Total 9.9 100.0 227.2 100.0 220.6 100.0

Source: Company data, Credit Suisse research

Cost of sales breakdown

Raw material costs represent a significant majority of Halcyon Agri's cost of sales,

between 95% and 100% of total costs. Raw material costs are directly related to the

market price for natural rubber as gauged by the SICOM TSR20 prices, procurement

effectiveness and the availability of raw materials supply.

Figure 41: Halcyon Agri cost of sales breakdown

9M10 9M11 9M12

US$ mn % share US$ mn % share US$ mn % share

Raw materials 9.7 100 156.8 95 155.7 96.1

Employee benefit expense — — 1.2 0.7 2.2 1.4

Service fee — — 4.4 2.7 — —

Depreciation — — 0.5 0.3 0.5 0.3

Other processing costs — — 2.2 1.3 3.5 2.2

Total cost of sales 9.7 100 165.1 100 161.9 100

Source: Company data, Credit Suisse research

Brief history

Halcyon Agri was incorporated in Singapore in 2005, but remained a dormant company up

until 2010, when the company started its natural rubber trading business through investing

in Hevea Global in May 2010. Thereafter, Halcyon Agri acquired all outstanding shares of

Hevea Global in July 2010.

In September 2010, Halcyon Agri exercised in September 2010 an option (acquired in

August 2010) to acquire the HMK1 and HMK2 rubber processing facilities and the related

operating assets, as well as the know-how of the technology and processes relating to

SIR20-VK rubber, for a total consideration of US$20 mn from PT Perusahaan Getah Para

Muara Kelingi. The acquisition was completed in February 2011.

Although the company only began operations in recent years, the HMK1 and HMK2

processing facilities have been in operation since the 1960s and 1980s, respectively, and

enjoy a well-established reputation for high quality production in the natural rubber

industry. TSR produced by HMK1 and HMK2 have regularly outperformed the minimum

technical specifications required.

Halcyon Agri has since put in place its own risk management and merchandising

operations and professional systems, secured new funding and built up its own customer

base and customer contracts to be aligned to its business model.

Existing production facilities in Indonesia

The existing production facilities, HMK1 and HMK2, were acquired from PT Perusahaan

Getah Para Muara Kelingi, one of the group's suppliers of processed rubber, in 2010 while

the group was still primarily involved in the rubber trading business. Both production

facilities are ISO 9001 certified and fully mechanised, with in-house laboratories to monitor

product quality, as well as environmental performance metrics daily.

01 September 2014

Halcyon Agri Corporation Ltd (HALC.SI / HACL SP) 24

Both facilities are located on the banks of the Musi River in Palembang, Indonesia, which

provides direct access to the Boom Baru port for ease of export. Being located in the

South Sumatra Province, Indonesia, also allows for easy access to rubber trees from

which raw materials are sourced.

Total production capacity of the existing facilities is dependent on the number of Wet-Lines

and Dry-Lines installed, the number of shifts worked each day, and downtime for routine

repairs and maintenance. The facilities are currently operating based on three eight-hour

shifts per day, six days a week.

Figure 42: Historical capacity and utilisation of HMK1 and HMK2

Maximum capacity (tonnes) Production volume (tonnes) Utilisation rate (%)

2011 82,460 45,286 55%

2012 92,380 67,317 73%

Source: Company data, Credit Suisse

Utilisation rates have improved from 55% in 2011 to 73% in 2012 as a result of increased

rubber demand and process optimisation initiatives to reduce critical equipment downtime.

Halycon Agri also announced various acquisitions to expand its production capacity in

Indonesia, as well as to extend its foothold in Malaysia.

■ June 2013: Acquisition of Chip Lam Seng for RM63 mn (natural rubber processing in

Malaysia with 180,000 tonnes annual production capacity); conditions precedent

relating to the acquisition satisfied in full on 30 December 2013.

■ September 2013: Acquisition of JFL Agro Pte Ltd for RM143 mn (24,327 acres of land

in Malaysia to develop natural rubber plantations)

■ September 2013: Acquisition of 95% of PT; Golden Energi for US$7 mn (rubber

processing facility in Indonesia)

Chip Lam Seng

The addition of two rubber processing factories of CLS, with a combined 180,000 tonnes

per annum capacity will allow Halycon Agri to rapidly expand its production scale and

capabilities, thus reaping significant economies of scale.

Through the acquisition, Halcyon is able to immediately gain a foothold in the Malaysian

rubber industry through two modern factories completed in 2004 and 2008, with an

eventual aim of becoming the largest natural rubber business in Malaysia over five years.

In addition, diversification benefits will accrue through producing both Malaysian- and

Indonesian-origin rubber. SMR typically attracts a premium to SIR, and the acquisition will

allow Halycon Agri to produce various higher grades of rubber at attractive price premiums.

JFL Agro – Entry into the upstream segment

9,728 hectares of sultanate land in Malaysia (97 year lease remaining) will be acquired

and developed into a natural rubber plantation, through the acquisition of JFL Agro. This

enables Halcyon to move up the value chain, earning the upstream segment, which

typically earns a higher margin.

Figure 43: Valuation of JFL Agro

Valuation

Hectares per Hectare (MYR) Total (MYR m)

Plantable area 7,144 17,300 123.6

Unplantable area 2,584 5,683 14.7

Planted palm area 197 46,200 9.1

Total land size 9,728 145

Acquisition price 143.2

Source: Company data, Credit Suisse

01 September 2014

Halcyon Agri Corporation Ltd (HALC.SI / HACL SP) 25

The acquisition is complementary to Halcyon's rubber processing facilities in Malaysia,

potentially providing up to 10% of the required raw materials when the plantations are fully

matured. Though representing only a minority of CLS's needs, the rubber plantations will

enhance Halcyon's ability to procure raw materials and provide useful feedback on the

state of rubber plantations in Malaysia.

Given the long gestation period of the investment, with rubber plantations typically

requiring six to seven years to reach maturity, we have not factored in any contributions

from JFL Agro in our projections. Further, through the sale of palm oil products from the

197 acres of planted oil palm, any operational expenses associated with the development

of the rubber plantations are likely to be offset.

PT Golden Energi – Bolt on acquisition

Located in Jambi Province, Indonesia, PT Golden Energi represents an incremental ‘bolt

on’ acquisition, which enables Halcyon to leverage on its established Indonesian

operations and know-how. With a license to export 50,000 tonnes of natural rubber per

year, the factory, which was built in 2010, is capable of producing SIR-20 rubber.

Management team

Executive chairman and CEO – Robert Meyer

Mr Robert Meyer is the Executive Chairman and CEO of Halcyon Agri and is in charge of

formulating and executing the strategic business development of the Group.

Between 1999 and 2004, Mr Robert Meyer was a director in Kingfisher Automotive Pte. Ltd.

and its affiliated companies and was in charge of business development. His responsibilities

centred on finding new agencies for the company, as well as expanding its distribution

network in Asia. During that period, he travelled extensively throughout Asia and negotiated

sales and distribution contracts with automotive and industrial stockists in the region.

Mr Robert Meyer left Kingfisher Automotive Pte. Ltd. in December 2004 and founded the

Halcyon Group. He has contributed significantly to the Halcyon Group’s development and

charted its corporate direction together with his co-founders and management team. He is

in charge of formulating and executing the strategic business development of the Group,

and his responsibilities include overseeing the core aspects of the business such as

Halcyon Agri's rubber processing operations and sales and marketing operations.

Chief Commercial Officer – Andrew Trevatt

Mr Andrew Trevatt is responsible for merchandising, risk management and business

development.

Mr Andrew Trevatt started work in 1982 as a junior auditor/assistant to the senior

accountant at Aarons Grew & Woodcroft, Certified Accountants, London. In 1986, he

commenced working as a trader for Lewis & Peat (Rubber) Ltd, London, and stayed with

the company for 14 years till 2000. His last position held at Lewis & Peat (Rubber) Ltd,

London, was trading director. In 2002, he went on to work in Sri Trang International Pte.

Ltd. as its chief executive officer. In 2007, he joined Louis Dreyfus Commodities Asian Pte.

Ltd. as a trading manager.

Mr Andrew Trevatt joined Halcyon Agri in 2010. After 26 years of experience in the natural

rubber industry, he has a thorough understanding of its operations, including customer and

supplier relationships, natural rubber processing knowledge and customer requirement

knowledge. He is also responsible for growing the client and supplier base of the business.

Technical Director – James Ronald Bugansky

Mr James Ronald Bugansky is responsible for analysing, maintaining and ultimately

improving the company's technical resources in both existing factories, as well as in

potential mid and upstream acquisitions. Prior to his appointment, he had worked as an

exclusive consultant for Halcyon Agri since May 2013.

01 September 2014

Halcyon Agri Corporation Ltd (HALC.SI / HACL SP) 26

Mr James Bugansky has more than 34 years of experience in natural rubber processing and

plantations. Following his graduation from the Ohio State University in 1976, he started work

in the rubber industry as the Plantation Management Trainee of PT Goodyear Sumatra

Plantation before moving up to be the Assistant Managing Director of Goodyear Guatemala

Plantation, and subsequently Goodyear Brazil Plantation. From 1984 to 2001, he held a

senior management position at The Goodyear Tire & Rubber company's headquarters

covering different areas from Research and Development (Senior Research Fellow -

Research / Corporate), Administrative Management (Manager Plantation Operations),

Purchasing to Inventory and Material Management (Global Materials Manager).

In 2001, he returned to plantation work at PT Goodyear Sumatra Plantation Company in

Indonesia as General Manager and Director. Thereafter he worked as the Factories

Operations Manager at Firestone Liberia from 2007 to 2009 taking responsibility for three

natural rubber processing factories and one rubber wood factory. Following this, and prior

to his service with the Group, he was an independent consultant and worked for GMG

Global as the General Manager Industrial Performance/EHS.

Chief Financial Officer – Ng Eng Kiat

Mr Ng Eng Kiat, was appointed as Halcyon Agri's CFO on 1 January 2013. He joined the

Halcyon Group as its Financial Controller in December 2011 and has been responsible for

overseeing the accounting and financial matters of the Group since he joined the Halcyon

Group.

Prior to joining Halcyon, he worked as an Assurance Supervisor in KPMG LLP in Kuala

Lumpur, Malaysia from 2002 to 2005. In 2005, he went on to join Ernst & Young LLP in

Leeds, England as an Assurance Manager, and thereafter worked at the same firm in

Singapore as an Assurance Senior Manager from 2010 to 2011.

He has been a fellow member of the Association of Chartered Certified Accountants since

2005 and is also a member of the Institute of Certified Public Accountants of Singapore.

Director of Operations, Palembang – Leonard Beschizza

Mr Leonard Beschizza is responsible for industrial and human resource matters in

Palembang, including the daily procurement and monitoring of raw materials.

Mr Leonard Beschizza started working as a trader with Pacol Ltd, London, a member of

the Gill & Duffus Group in 1971. He went on to become a director of Pacol Sdn Bhd and

Pacol Singapore in 1976, and his duties included the procurement of natural rubber and

cocoa on behalf of Pacol’s UK and North American trading offices. In 1978, he returned to

Pacol Ltd, London, to head the natural rubber trading desk and was appointed as a main

board director in 1985. In 1987, he went on to become the director of Centrotrade

Singapore and headed the natural rubber trading team at Centrotrade Singapore. In 1995,

he headed the sales and marketing department in PT PP London Sumatra Indonesia and

dealt with the price risk management of agricultural products. In addition, he was a

moderator at the Indonesian Palm Oil Association or GAPKI (Gabungan Pengusaha

Kelapa Sawit Indonesia) conferences in 2008, 2009 and 2010.

Mr Leonard Beschizza joined Halcyon Agri in 2010. After working for about 40 years in the

natural rubber and agricultural industry, he is experienced in most aspects of the natural

rubber business, including the processing and trading of physical rubber and futures. He

also has an in-depth knowledge of the palm oil and cocoa industry.

Head of Production, Palembang – Alex Kurniawan Edy

Mr Alex Kurniawan Edy, Halcyon Agri's Head of Production, joined the Group in 2011 as

part of the acquisition of the HMK1 and HMK2 facilities. Since he joined the Group, he has

been responsible for overseeing the rubber processing operations, administrative and

human resource matters of PT Hevea. He has been involved in the natural rubber industry

for 20 years and, during this period, has been exclusively employed in relation to HMK1

and HMK2.

01 September 2014

Halcyon Agri Corporation Ltd (HALC.SI / HACL SP) 27

Mr Alex Kurniawan Edy started work at PT Perusahaan Getah Para Muara Kelingi in 1992

as its factory manager and remained with PT Perusahaan Getah Para Muara Kelingi until

Halcyon Agri's acquisition of HMK1 and HMK2 in 2011.

Mr Alex Kurniawan Edy has been the Chairman of the South Sumatra office of

GAPKINDO since 1996 and is also the Vice Chairman of GAPKINDO’s central office in

Jakarta.

Head of Procurement, Palembang – Rachman Rachmadi

Mr Rachman Rachmadi, Halcyon Agri's Head of Procurement, joined the Group in 2011 as

part of the acquisition of the HMK1 and HMK2 facilities. Since he joined the Group, he has

been responsible for overseeing the financial matters of PT Hevea and manages PT

Hevea’s raw material procurement and payment process. He has been involved in the

natural rubber industry for over 40 years and, in particular, has been closely involved with

the operations of HMK1 and HMK2 for 25 years.

Mr Rachman Rachmadi started work in 1968 as a director of PT Garuntang, a company

engaged in the rubber business in the Lampung Province in Indonesia. In 1987, he joined

PT Perusahaan Getah Para Muara Kelingi, from whom the HMK1 and HMK2 facilities

were acquired, as its finance manager. In 1990, he was made a director of PT Perusahaan

Getah Para Muara Kelingi and he remained with it until Halcyon Agri's acquisition of HMK1

and HMK2 in 2011.

01 September 2014

Halcyon Agri Corporation Ltd (HALC.SI / HACL SP) 28

Companies Mentioned (Price as of 28-Aug-2014)

Apollo Tyres (APLO.NS, Rs165.3) Archer Daniels Midland Inc. (ADM.N, $49.75) Bridgestone (5108.T, ¥3,608) Bumitama Agri Limited (BUMI.SI, S$1.11) Bunge Limited (BG.N, $84.28) Cheng Shin Rubber (2105.TW, NT$69.9) Continental (CONG.DE, €163.55) Cooper Tire Rubr (CTB.N, $30.37) Felda Global Ventures (FGVH.KL, RM3.93) First Resources Ltd (FRLD.SI, S$2.05) GMG (GMGG.SI, S$0.08) Genting Plantations Bhd (GENP.KL, RM10.16) Glencore (GLEN.L, 360.5p) Golden Agri-Resources (GAGR.SI, S$0.52) Goodyear Tire (GT.OQ, $25.77) Halcyon Agri Corporation Ltd (HALC.SI, S$0.86, OUTPERFORM, TP S$1.2) Hankook Tire (161390.KS, W53,500) IOI Corporation (IOIB.KL, RM4.82) Indofood Agri Resources Ltd (IFAR.SI, S$0.87) Kuala Lumpur Kepong (KLKK.KL, RM22.14) Kumho Tire (073240.KS, W10,600) Marubeni Corp (8002.T, ¥754) Michelin (MICP.PA, €84.04) Nexen Tire (002350.KS, W14,650) Noble Group Ltd (NOBG.SI, S$1.36) Olam (OLAM.SI, S$2.55) PT Astra Agro Lestari Tbk (AALI.JK, Rp26,000) PT BW Plantation Tbk (BWPT.JK, Rp1,025) PT London Sumatra Indonesia (LSIP.JK, Rp1,905) Pirelli (PECI.MI, €11.61) S Giti Tire (600182.SS, Rmb18.02) Salim Ivomas Pratama (SIMP.JK, Rp850) Sampoerna Agro Tbk (SGRO.JK, Rp2,080) Sime Darby (SIME.KL, RM9.47) Sri Trang Agro (STA.BK, Bt14.2) Sumitomo Rubber Industries (5110.T, ¥1,477) Toyo Tire & Rub (5105.T, ¥1,719) Wilmar International Ltd (WLIL.SI, S$3.15) Yokohama Rubber (5101.T, ¥923)

Disclosure Appendix

Important Global Disclosures

I, Gerald Wong, CFA, certify that (1) the views expressed in this report accurately reflect my personal views about all of the subject companies and securities and (2) no part of my compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this report.

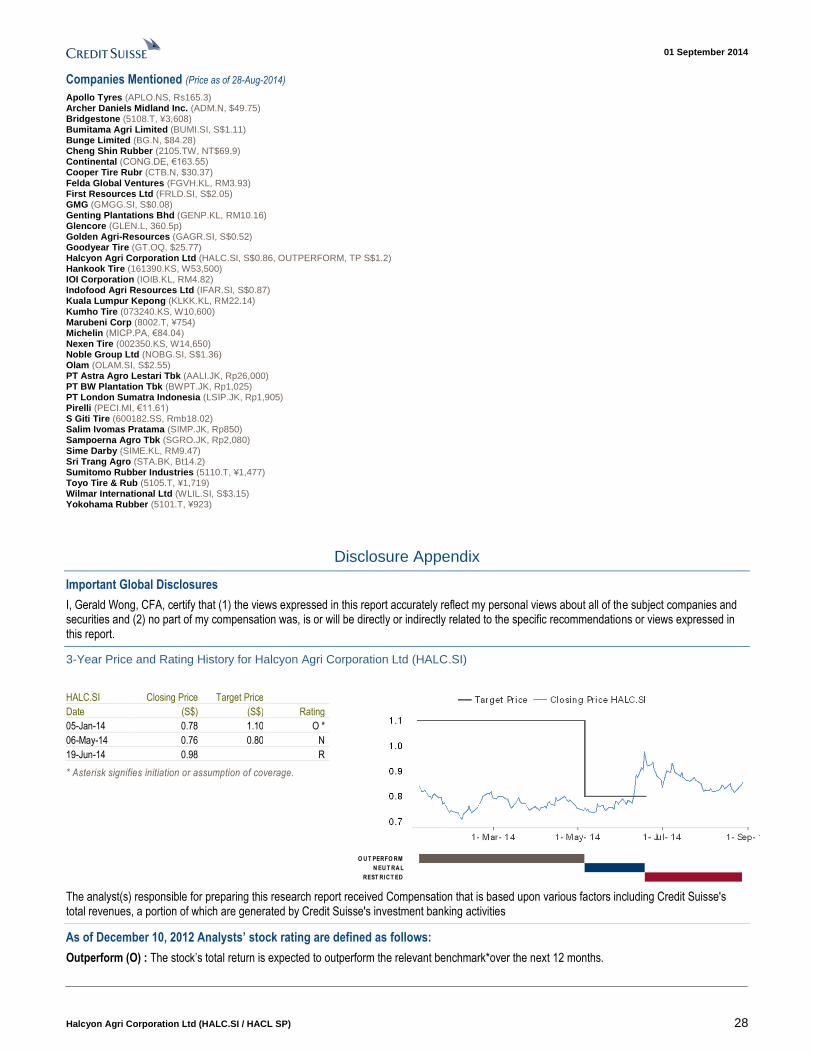

3-Year Price and Rating History for Halcyon Agri Corporation Ltd (HALC.SI)

HALC.SI Closing Price Target Price

Date (S$) (S$) Rating

05-Jan-14 0.78 1.10 O *

06-May-14 0.76 0.80 N

19-Jun-14 0.98 R

* Asterisk signifies initiation or assumption of coverage.

O U T PERFO RM

N EU T RA L

REST RICT ED

The analyst(s) responsible for preparing this research report received Compensation that is based upon various factors including Credit Suisse's total revenues, a portion of which are generated by Credit Suisse's investment banking activities

As of December 10, 2012 Analysts’ stock rating are defined as follows:

Outperform (O) : The stock’s total return is expected to outperform the relevant benchmark*over the next 12 months.

01 September 2014

Halcyon Agri Corporation Ltd (HALC.SI / HACL SP) 29

Neutral (N) : The stock’s total return is expected to be in line with the relevant benchmark* over the next 12 months.

Underperform (U) : The stock’s total return is expected to underperform the relevant benchmark* over the next 12 months.