HAHN & HESSEN LLP 488 Madison Avenue New York, New York 10022 Telephone: (212) 478-7200 Facsimile: (212) 478-7400 Mark T. Power, Esq. Janine M. Figueiredo, Esq. Counsel for Debtors and Debtors in Possession UNITED STATES BANKRUPTCY COURT EASTERN DISTRICT OF NEW YORK ---------------------------------------------------------------------- X In re: Décor Holdings, Inc., et al.,1 Debtors.

: : : : : : : : : :

Chapter 11 Case No. 19-71020 (REG) Case No. 19-71022 (REG) Case No. 19-71023 (REG) Case No. 19-71024 (REG) Case No. 19-71025 (REG) Substantively Consolidated

---------------------------------------------------------------------- X

DEBTORS’ MEMORANDUM OF LAW (I) IN SUPPORT OF ENTRY OF AN ORDER (A) CONFIRMING THE THIRD AMENDED JOINT CHAPTER 11 PLAN

OF LIQUIDATION PROPOSED BY THE DEBTORS, AND (B) APPROVING THE SALE OF SUBSTANTIALLY ALL OF THE DEBTORS’ ASSETS

The above-captioned debtors and debtors-in-possession (collectively, the “Debtors”),

submit this memorandum of law (the “Memorandum of Law”) in support of an order (a)

confirming the Third Amended Joint Chapter 11 Plan of Liquidation Proposed by the Debtors (the

1 The Debtors in these chapter 11 cases, along with the last four digits of each Debtor’s federal tax identification number, are: Décor Holdings, Inc. (4174); Décor Intermediate Holdings LLC (5414); The Robert Allen Duralee Group, Inc. (8435); The Robert Allen Duralee Group, LLC (1798); and The Robert Allen Duralee Group Furniture, LLC (2835). The corporate headquarters and the mailing address for the Debtors listed above is 49 Wireless Boulevard, Suite 150, Hauppauge, NY 11788. The Debtors also maintain a separate corporate office at 2 Hampshire Street, Suite 300, Foxboro, MA 02035.

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

2

“Plan”),2 and (b) approving the sale of substantially all of the Debtors’ assets. For the

reasons stated herein, the Debtors believe that the Plan satisfies the requirements for

confirmation set forth in section 1129 of title 11 of the United States Code (the “Bankruptcy

Code”), and is otherwise in the best interest of the Debtors’ creditors and all parties in

interest in these chapter 11 cases. In support of this Memorandum of Law, the Debtors rely

on the (i) Declaration of Paul H. Deutch Regarding the Methodology for the Tabulation of Votes On

and Results of Voting with Respect to the Second Amended Joint Chapter 11 Plan of Liquidation

Proposed by the Debtors [D.I. 279] (the “Certification of Ballots”), and (ii) the proffered

testimony of Timothy Boates, Chief Restructuring Officer, in support of (i) confirmation of

the Plan and (ii) the Sale (the “Boates Testimony”), and the proffered testimony of J. Scott

Victor, Managing Director of SSG Advisors, LLC, investment bankers to the Debtors, in

support of the Sale (the “Victor Testimony”). In support of confirmation of the Plan, the

Debtors respectfully represent as follows:

I. PRELIMINARY STATEMENT

1. The Debtors’ proposed Plan, which includes and incorporates the sale of

substantially all of the Debtors’ assets as described herein (the “Sale”), should be confirmed.

The Plan provides a clear path for the successful conclusion of these chapter 11 cases, and is

overwhelmingly supported by, among others, the Debtors’ General Unsecured Creditors,

and DIP Lenders.

2. Prior to and after the commencement of these chapter 11 cases, the Debtors

and their professionals explored various strategies for resolving the Debtors’ significant

financial difficulties, including possible reorganization or liquidation. After extensive

2 Capitalized terms used but not otherwise defined herein shall have the meanings ascribed to them in the Plan.

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

3

analysis and consideration, however, the Debtors determined that a marketing and sale of

substantially all of their assets as a going concern would be the best method for preserving

the value of their assets and would be in the best interests of their creditors. As such, the

Debtors’ ultimate goal throughout this chapter 11 process has been to consummate a going

concern sale of substantially all of their assets through the confirmation of a Plan.

3. The Plan is largely premised upon the Court’s approval of the Sale. Approval

of the Sale and confirmation of the Plan are so inextricably linked such that failure to

approve the Sale will ultimately render the Plan infeasible, leading to a liquidation of the

Debtors’ assets under chapter 7 of the Bankruptcy Code. As such, in support of both the

Plan and the Sale and as described in detail herein, the Debtors submit that (i) the Plan

complies with confirmation provisions of the Bankruptcy Code, (ii) the terms and

conditions of the Sale and its corresponding asset purchase agreement (the “APA”) are fair

and reasonable, (iii) the sale and purchase of the Purchased Assets (as defined herein)

pursuant to the Plan and APA, is non-collusive, fair and reasonable and was conducted

openly and in good faith, (iv) the transfer of the Purchased Assets represents an arm’s-length

transaction and was negotiated in good faith between the parties, (v) the Purchaser (as

defined herein), as transferee of the Purchased Assets, is a good faith purchaser under

Bankruptcy Code § 363(m) and, as such, should be entitled to the full protection of

Bankruptcy Code § 363(m), (vi) the Purchased Assets should be sold free and clear of all

claims, interests, and encumbrances pursuant to Bankruptcy Code § 1141(c) to maximize

the value of the Debtors’ assets, (vii) the Sale was not controlled by an agreement among

potential purchasers, (viii) no cause of action exists against the Purchaser or with respect to

the Sale of the Purchased Assets to the Purchaser under § 363(n), and (ix) any claims under

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

4

§ 363(n) or any other claims as against the Purchaser should be released, waived and

discharged.

4. Confirmation of the Plan, and the related approval of the Sale, will achieve

the best possible result for the Debtors, their creditors, and all other parties-in-interest in

these chapter 11 cases. Accordingly, the Debtors respectfully request that the Court confirm

the Plan and approve the Sale.

II. BACKGROUND

A. General Background Regarding These Chapter 11 Cases

5. On February 12, 2019 (the “Petition Date”), each of the Debtors filed a

voluntary petition for relief under chapter 11 of the Bankruptcy Code.

6. The Debtors continue to operate their business as debtors in possession

pursuant to sections 1107(a) and 1108 of the Bankruptcy Code.

7. No trustee or examiner has been appointed in these Chapter 11 Cases.

8. On February 15, 2019, Omni Management Group, Inc. (“Omni”) was

appointed as Claims and Noticing Agent for the Debtors. See Order Appointing Omni

Management Group, Inc. as Claims and Noticing Agent for the Debtors Pursuant to 28 U.S.C. §

156(C), 11 U.S.C. § 105(a), and Administrative Order No. 658 Nunc Pro Tunc to the Petition Date

[D.I. 46].

9. On March 19, 2019, pursuant to Bankruptcy Code Section 1102(a)(1), the

Office of the United States Trustee for the Eastern District of New York (the “U.S.

Trustee”) appointed three unsecured creditors to an Official Committee of Unsecured

Creditors. On March 22, 2019, the U.S. Trustee amended its notice, reducing the members

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

5

of the Committee to two of those creditors. The Committee has selected Perkins Coie LLP

to act as its proposed counsel in these chapter 11 cases.

10. Prior to the Petition Date, the Debtors retained Timothy Boates of RAS

Management Advisors, LLC to perform the functions and hold the title of Chief

Restructuring Officer (the “CRO”). The CRO has taken over as the daily manager of the

Debtors, is responsible for managing the Debtors as debtors-in-possession in these chapter

11 cases, and has been intimately involved in the formulation, preparation, and

consummation of the Plan.

11. On April 5, 2019, the Debtors submitted their Motion for an Order Approving the

Substantive Consolidation of the Debtors for Purposes of Balloting, Solicitation of Votes and

Distributions under the Debtors’ Chapter 11 Plan [D.I. 213] (the “Substantive Consolidation

Motion”), which Motion was granted by the Court on April 11, 2019. See Order, Pursuant to

Bankruptcy Code Sections 105(a) and 302, Approving the Substantive Consolidation of the Debtors for

Purposes of Balloting, Solicitation of Votes and Distributions under the Debtors’ Chapter 11 Plan (the

“Substantive Consolidation Order”) [D.I. 230]. Pursuant to the Substantive Consolidation

Order, all of the Debtors’ chapter 11 cases were consolidated for both substantive and

administrative purposes into the Lead Case, docket number 19-71020. Further, as a result of

the Debtors’ substantive consolidation, all intercompany liabilities that existed between the

respective Debtor entities (the “Intercompany Claims”) were expunged.

12. On March 15, 2019, the Debtors filed a motion (the “Disclosure Statement

Motion”) for entry of an order, (i) approving the Disclosure Statement for Plan of

Liquidation Proposed by the Debtors (the “Initial Disclosure Statement”), (ii) establishing

solicitation and voting procedures for the Joint Chapter 11 Plan of Liquidation Proposed by

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

6

the Debtors (the “Initial Chapter 11 Plan”), (iii) scheduling a Confirmation Hearing (the

“Confirmation Hearing”), and (iv) establishing notice and objection procedures for

confirmation of the Plan [D.I. 148].

13. Following receipt of comments from various interested parties, on April 9,

2019, the Debtors filed their First Amended Joint Chapter 11 Plan of Liquidation Proposed by the

Debtors (the “First Amended Plan”) and related Disclosure Statement for First Amended Plan of

Liquidation proposed by the Debtors (the “First Amended Disclosure Statement”) [D.I. 219].

14. Following the hearing to consider the approval of the First Amended

Disclosure Statement, the Debtors filed the Plan and the related Disclosure Statement for

Second Amended Plan of Liquidation Proposed by the Debtors (the “Disclosure Statement”) [D.I.

241].

15. On April 15, 2015, the Court entered the Order (I) Approving the Disclosure

Statement, (II) Establishing Plan Solicitation and Voting Procedures, (III) Scheduling a Confirmation

Hearing, and (IV) Establishing Notice and Objection Procedures for Confirmation of the Debtors’

Chapter 11 Plan of Liquidation (the “Disclosure Statement Order”) [D.I. 238], concluding that

the Disclosure Statement contained adequate information sufficient for a reasonable

hypothetical investor to make an informed judgment on the Plan; approving the Debtors’

proposed solicitation and voting procedures for the Plan (the “Solicitation Procedures”);

and establishing notice and objection procedures for confirmation of the Plan. Pursuant to

the Disclosure Statement Order, the Court scheduled the Confirmation Order for May 2,

2019, and set the deadline to object to confirmation of the Debtors’ Plan for April 29, 2019

(the “Plan Objection Deadline”). As of the Confirmation Hearing, the Debtors believe that

all formal and informal objections to confirmation of the Plan will have been resolved on a

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

7

consensual basis, other than the vote by the holder of Class 2 Secured Claims to reject the

Plan, which will necessitate a finding by the Court to find that the Plan satisfies the

“cramdown” requirements of Section 1129(b) of the Bankruptcy Code since the Plan does

not discriminate unfairly and is fair and equitable as to Class 2.

B. The Plan

16. Among other things, the Plan facilitates the Sale, liquidates the Debtors’

estates following consummation of the Sale, and distributes the Debtors’ remaining assets –

principally cash – to the holders of Allowed Claims in accordance with the respective rights

and priorities. The Plan provides for the full satisfaction of all Administrative and Priority

Claims on the Plan’s effective date (the “Effective Date”), or as soon thereafter as

reasonably practicable. Proceeds of any Chapter 5 Claims (net any proceeds used to cover

shortfalls in any of the Reserve Funds) will be shared between the holders of Class 5

General Unsecured Claims and the holders of Class 1 Senior Secured Loan Claims under a

formula set forth in the Plan. The projected proceeds from the Sale will be insufficient to

satisfy the Class 1 Senior Secured Loan Claims.

17. The Plan provides for the classification of certain Classes of Claims as

Impaired or not Impaired, and provides for such classes’ voting rights. The Plan’s

classification scheme is set forth as follows:

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

8

Class Claim Status Voting Rights

1 Senior Secured Loan Claims Impaired Entitled to Vote

2 Junior Secured Loan Claims Impaired Entitled to Vote

3 Other Secured Claims Impaired Entitled to Vote

4 Other Priority Claims Unimpaired Deemed to Accept

5 General Unsecured Claims Impaired Entitled to Vote

6 Intercompany Claims Impaired and No Distribution Deemed to Reject

7 Equity Interests Impaired and No Distribution Deemed to Reject

Thus, other than claims that are not required to be satisfied under the Bankruptcy Code, the

Plan provides for seven (7) different classes of Claims.

18. Class 4 (Other Priority Claims) is not impaired under the Plan and is therefore

conclusively presumed to have accepted the Plan pursuant to section 1126(f) of the

Bankruptcy Code. Accordingly, the votes of holders of Class 4 Claims were not solicited.

See Certification of Ballots.

19. Holders of claims in Classes 6 and 7 (collectively, the “Deemed Rejecting

Classes”) are not entitled to receive or retain any property under the Plan. Section 1126(g)

of the Bankruptcy Code provides that “[n]otwithstanding any other provision of this section,

a class is deemed not to have accepted a plan if such plan provides that the claims or

interests of such class do not entitle holders of such claims or interests to receive or retain

any property under the plan on account of such claims and interests.” Under the Debtors’

Plan, holders of Intercompany Claims and Equity Interests in the Debtors will not receive

any distributions or retain any property on account of such Claims or Interests. As such,

these Deemed Rejecting Classes are conclusively presumed to have rejected the Plan and

votes of the Deemed Rejecting Classes were not solicited. See Certification of Ballots.

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

9

20. Classes 1, 2, 3, and 5 (the “Voting Classes”) are impaired under the Plan.

The votes of holders of Claims in the Voting Classes were solicited. See Certification of

Ballots.

C. Solicitation of Votes and Noticing of Non-Voting Procedures

21. In accordance with the Solicitation Procedures, on April 12, 2019, the

Debtors commenced their solicitation (the “Solicitation”) of votes on the Plan by mailing

certain packages of information (the “Solicitation Packages”) to all creditors and interest-

holders entitled to receive the Solicitation Packages. Each Solicitation Package contained:

(a) the Confirmation Hearing Notice; (b) to Classes entitled to vote on the Plan: (1) the

Disclosure Statement Order (without attachments); (2) the Disclosure Statement, together

with all attachments (including the Plan); (3) a cover letter from the Creditors’ Committee

setting forth the Creditors’ Committee’s support thereof; (4) the applicable Ballot; and (5) a

return envelope; and (c) to Classes not entitled to vote: a Notice of Non-Voting Status. See

Certification of Ballots.

22. As provided in the Disclosure Statement Order, the deadline to vote on the

Debtors’ Plan was set for April 26, 2016 and 4:00 p.m. (prevailing Eastern Time) (the

“Voting Deadline”).

23. The Debtors received 87 valid votes, totaling $33,100,989.91 in liabilities from

holders of Claims in the Voting Classes by the Voting Deadline. See Certification of Ballots.

As set forth below and in the Certification of Ballots, Classes 1 and 5 voted in favor of the

Plan by overwhelming percentages. Class 2 voted to reject the Plan (the “Rejecting Class”

and together with the Deemed Rejecting Classes, the “Rejecting Classes”). Id. No votes

were received from holders of claims in Class 3, and as such Class 3 neither accepted nor

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

10

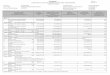

rejected the Plan. A breakdown of the Voting Classes’ votes on the Plan have been set forth

in the following table:

Class Total Accepted Rejected Outcome

1 $22, 245,679.48 $22, 245,679.48 (100%) $0 (0%) ACCEPTED

2 $5,871,903.37 $0 (0%) $5,871,903.37 (100%) REJECTED

3 $N/A $N/A $N/A N/A

5 $4,983,407.06 $4,401,188.43 (88.32%) $582,218.63 (11.68%) ACCEPTED

TOTAL $33,100,989.91 $26,646,867.91 $6,454,122.00

D. The Sale Process

24. On the Petition Date, the Debtors filed a Motion for Entry of (A) an Order (I)

Approving Bid Procedures (the “Bid Procedures”) in Connection with the Sale of

Substantially All of the Debtors’ Assets, (II) Authorizing the Debtors to Enter into Stalking

Horse Agreements and Approving Certain Bid Protections, (III) Scheduling an Auction

(the “Auction”) for and Hearing to Approve Sale of Assets, (IV) Approving Notice of Date,

Time and Place for Auction and for Hearing on Approval of Sale, (V) Approving

Procedures for the Assumption and Assignment of Certain Executory Contracts and

Unexpired Leases (the “Assignment Procedures”), (VI) Approving Form and Manner of

Notice Thereof, and (VII) Granting Related Relief; and (B) an Order Authorizing and

Approving (I) the Sale of Substantially All of the Debtors’ Assets Free and Clear of Liens,

Claims, Rights, Encumbrances, and Other Interests, (II) the Assumption and Assignment of

Certain Executory Contracts and Unexpired Leases and (III) Granting Related Relief [D.I.

21] (the “Sale Motion”).

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

11

25. In order to properly and effectively market the Debtors’ assets and to create a

robust and active Auction for the Sale, the Debtors retained SSG Capital Advisors (“SSG”)

as its investment banker. SSG has solicited various potentially interested buyers for the

Debtors’ assets and has actively marketed the Debtors’ assets throughout these chapter 11

cases.

26. On March 15, 2019, the Court entered an order (a) approving the Debtors’

proposed Bid Procedures in connection with the Sale, (b) authorizing the Debtors to enter

into Stalking Hose Asset Purchase Agreements and approving certain bid protections, (c)

scheduling the Auction, and (d) approving the Notice of date, time, and place for the

Auction [D.I. 145] (the “Bid Procedures Order”).

27. On April 12, 2019, the Debtors entered into a stalking horse asset purchase

agreement (the “Stalking Horse APA” or “APA”) with RADG Holdings, LLC, a Delaware

limited liability company (the “Stalking Horse Bidder”). The Debtors concurrently filed a

Notice of Designation of RADG Holdings LLC as Stalking Horse Bidder [D.I. 232] (the “Stalking

Horse Bid Notice”), together with the Stalking Horse APA, as required by the Bid

Procedures and Bid Procedures Order.

28. Shortly thereafter, pursuant to the Bid Procedures, the Stalking Horse Bidder

provided the Debtors with certain future performance information (the “Adequate

Assurance Information”) including, among other things, information regarding the Stalking

Horse Bidder’s current financial condition and ability to consummate the Sale.

29. Pursuant to the Bid Procedures and Bid Procedures Order, all other potential

bidders who desired to make a bid for the Debtors’ assets were required to submit such bids

by April 25, 2019, at 5:00 p.m. (prevailing Eastern Time) (the “Bid Deadline”).

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

12

E. Cancellation of Auction and Designation of the Stalking Horse Bidder as Successful Bidder

30. The Debtors did not receive any Qualified Bids (as defined in the Bid

Procedures) by the Bid Deadline. Shortly thereafter, the Debtors cancelled the Auction and

declared the Stalking Horse Bidder as the successful bidder (the “Successful Bidder” or

“Purchaser”).

31. On April 26, 2019, the Debtors filed a Notice of (I) Cancellation of Auction and

Designation of Stalking Horse Bidder as the Successful Bidder and (II) Proposed Assumption and

Assignment of Certain Executory Contracts and Unexpired Real Property Leases (the “Notice of

Successful Bidder”) [D.I. 276], which identified certain executory contracts and unexpired

leases proposed to be assumed by the Successful Bidder. The Notice of Successful Bidder

was immediately served on all parties in interest and on the applicable Non-Debtor

Counterparties (defined below) to the Debtors’ executory contracts and unexpired leases.

F. The APA and Transition Services Agreement

32. Pursuant to the terms of the APA, the Purchaser has agreed to purchase

substantially all of the Debtors’ business-related assets for an estimated purchase price of

$19,000,000, which amount is comprised of (i) a cash payment of $8,000,000 at the time of

the closing of the Sale (the “Closing”), plus (ii) a post-Closing cash payment in an amount

of not less than $10,000,000 and not more than $11,000,000, payable out of the first $11

million in pre-Closing receivables collected after the Closing, less any out-of-pocket costs

collection, and (iii) the assumption of certain assumed liabilities (the “Purchase Price”). See

APA § 2.2. The Purchase Price is subject to, among other things, a working capital

adjustment if the level of inventory and receivables fall below certain thresholds at the time

of the Closing. See APA § 2.4.

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

13

33. “Purchased Assets” include, among other things, the Debtors’ (i) inventory

(except where specifically excluded) and receivables, (ii) tangible personal property, (iii)

ownership interest in Robert Allen Fabrics (Canada), Ltd., (iv) unfulfilled customer orders,

and (v) intellectual property. See APA § 2.1.

34. “Assumed Liabilities” include, among other things, (i) liabilities arising after

the Closing in connection with the operation and use of all Purchased Assets, (ii) liabilities

under all assigned contracts and leases, (iii) cure costs relating to all assigned contracts and

leases (iv) certain PTO obligations owed to employees of the Debtors who are retained by

the Purchaser after the Closing, and (v) the Debtors’ outstanding liabilities related to the

Debtors’ customer programs, including customer credits. See APA § 2.3.

35. The Horse APA also provides for Excluded Assets to be retained by the

Debtors, including certain (i) cash, cash equivalents, and marketable securities, (ii) equity

interests and capital stock, (iii) pre-Closing tax refunds and tax attributes, (iv) assets of the

Plan maintained by the Debtors, (v) insurance policies, (vi) contract rights, (vii) security

deposits and utility deposits relating to an Excluded Asset, and (vii) Avoidance Actions,

including Chapter 5 Claims. See APA § 1.1 (defining “Excluded Assets”).

36. The Stalking Horse APA provides for the Closing to occur no later than three

business days after the entry of the order confirming the Debtors’ Plan, subject to the

occurrence of certain conditions precedent to closing having been satisfied or waived by

either the Debtors or the Purchaser. APA § 9.1. The Closing of the Sale is expressly

conditioned upon the Court’s confirmation of the Plan. See APA §§ 8.3, 9.1.

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

14

37. The APA also envisions the parties entering into a post-closing Transition

Services Agreement, which is currently being finalized with the Buyer and will be filed with

the Court.

G. The Assumption and Assignment Process

38. On April 15, 2019, the Court entered the Order Approving the Assignment

Procedures [D.I. 239] (the “Assignment Procedures Order”). On the same day, the Debtors

served the Assignment Procedures Order, as well as the Notice of Assignment Procedures and

Possible Assumption and Assignment of Certain Executory Contracts and Unexpired Leases in

Connection with Sale (the “Potential Assumption and Assignment Notice”) on all

counterparties to the Debtors’ executory contracts (the “Non-Debtor Counterparties”).3 See

Omni Affidavit of Service [D.I. 254]. The Debtors attached a schedule (the “Cure

Schedule”) to the Potential Assumption and Assignment Notice which described all of the

Debtors’ executory contracts and unexpired leases, along with their respective cure amounts

(the “Cure Costs”), to provide the Non-Debtor Counterparties with sufficient cure

information.

39. On April 26, 2019, following the declaration of the Stalking Horse Bidder as

the Successful Bidder, the Debtors served the Notice of Successful Bidder on all Non-Debtor

Counterparties whose contracts the Purchaser proposed to assumed pursuant to the terms of

the APA (the “Proposed Assigned Contracts”). All other executory contracts and

unexpired leases which were not listed on the Notice of Successful Bidder were to be

rejected upon confirmation of the Plan.

3 The Debtors also filed the Assumption and Assignment Notice on the Debtors’ docket for purposes of additional notice and for executory contract counterparties’ convenience. See D.I. 240.

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

15

40. Pursuant to the Assignment Procedures, Non-Debtor Counterparties were

given until April 24, 2019, at 4:00 p.m. (Eastern Time) (the “Cure Cost/Assignment

Objection Deadline”) to object to (i) the Debtors’ proposed cure cost for assuming and

assigning a Non-Debtor Counterparty’s contract, (ii) the proposed assumption, assignment

and/or transfer of such Non-Debtor Counterparty’s Contract, and (iii) the identity of, or

adequate assurance of future performance provided by, the Stalking Horse (each respective

objection, a “Cure Cost/Assignment Objection”).

41. Six Non-Debtor Counterparties filed Cure Cost/Assignment Objections prior

to the Cure Cost Assignment Objection Deadline, and a small number of Non-Debtor

Counterparties submitted informal objections (collectively, the “Objecting Non-Debtor

Counterparties”). The Debtors have been working together with the Objecting Non-Debtor

Counterparties in good faith to resolve all outstanding Objections. Many have been resolved

by mutual agreement, or have been deemed irrelevant based on the Purchaser’s

determination to reject such executory contract or unexpired lease. To the extent the

Debtors and the Objecting Non-Debtor Counterparties cannot resolve their outstanding

Objections, however, the Debtors intend to resolve such Objections at or after the

Confirmation Hearing. Furthermore, if any Cure Cost/Assignment Objections remain

unresolved after the Confirmation Hearing, the Assignment Procedures and Plan provide

for the adjournment of such outstanding Objections to a subsequent hearing, along with the

establishment of a Cure Claim Reserve Fund to reserve for any disputed amounts relating to

the Cure Costs of such executory contracts or unexpired leases.

III. THE PLAN SHOULD BE CONFIRMED

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

16

42. To obtain confirmation of the Plan, the Debtors must demonstrate that the

Plan satisfies the applicable provisions of section 1129 of the Bankruptcy Code by a

preponderance of the evidence. As set forth by the United States Court of Appeals for the

Fifth Circuit in Heartland Savings & Loan Association v. Briscoe Enterprises., Ltd. II (In re Briscoe

Enterprises., Ltd. II):

The combination of legislative silence, Supreme Court holdings, and the structure of the [Bankruptcy] Code leads this Court to conclude that preponderance of the evidence is the debtor’s appropriate standard of proof under both § 1129(a) and in a cramdown.

994 F.2d 1160, 1165 (5th Cir. 1993); see also In re 20 Bayard Views, LLC 445 B.R. 83, 93

(Bankr. E.D.N.Y. 2011); In re Young Broad, Inc., 430 B.R. 99, 128 (Bankr. S.D.N.Y. 2010);

In re Armstrong World Indus., Inc., 348 B.R. 111, 120 (D. Del. 2006). Applicable case law

holds that when considering confirmation of a chapter 11 plan, creditor democracy – an

integral element in a chapter 11 case – should be afforded substantial deference in the

absence of a clear impediment to plan confirmation. See, e.g., Williams v. Hibernia Nat’l Bank

(In re Williams), 850 F.2d 250, 253 (5th Cir. 1988). The Supreme Court has emphasized that

the creditors should be permitted to decide whether a proposed plan is in their best interests.

See Norwest Bank Worthington v. Ahlers, 485 U.S. 197, 207 (1988); see also Coltex Loop Cent.

Three Partners, L.P. v. BT/SAP Pool C Assocs., L.P. (In re Coltex Loop Central Three Partners,

L.P.), 138 F.3d 39, 44 (2d Cir. 1998) (“The Code thus strikes a considered balance between

creditor and debtor interests, which… courts must scrupulously respect.”).

43. As further described herein, and as evidenced in the Boates Testimony and

Certification of Ballots, the Debtors submit that the proposed Plan satisfies all applicable

subsections of section 1129 of the Bankruptcy Code other than section 1129(a)(8). As

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

17

described more fully below, however, the Plan may be confirmed notwithstanding the fact

that not all Classes of Claims or Equity Interests have voted in favor of the Debtors’ Plan.

Accordingly, the Debtors request that the Plan be confirmed.

A. Section 1129(a)(1): Compliance with Applicable Provisions of the Bankruptcy Code

44. Section 1129(a)(1) of the Bankruptcy Code provides that a plan may be

confirmed only if “[t]he plan complies with the applicable provisions of this title.” 11 U.S.C.

§ 1129(a)(1).

45. The legislative history of section 1129(a)(1) explains that this provision

embodies the requirements of, among others, sections 1122 and 1123 of the Bankruptcy

Code governing, respectively, the classification of claims and the contents of the plan. H.R.

Rep. No. 595, 95th Cong., 1st Sess. 412 (1977); S. Rep. No. 989, 95th Cong., 2d Sess. 126

(1978); see also Kane v. Johns-Manville Corp. (In re Johns-Manville Corp.), 843 F.2d 636, 648-49

(2d Cir. 1988) (“[T]he legislative history of subsection 1129(a)(1) suggests that Congress

intended the phrase ‘applicable provisions’ in this subsection to mean provisions of Chapter

11 that concern the form and content of reorganization plans.”); In re Drexel Burnham

Lambert Group Inc., 138 B.R. 723, 757 (Bankr. S.D.N.Y. 1992); In re Sabine Oil & Gas Corp.,

555 B.R. 180, 310 (Bankr. S.D.N.Y. 2016) (“In order to determine whether a plan complies

with section 1129(a)(1) of the Code, a court must ensure that the requirements of sections

1122 and 1123 are met.”); In re Texaco Inc., 84 B.R. 893, 905 (Bankr. S.D.N.Y. 1988) (“In

determining whether a plan complies with section 1129(a)(1), reference must be made to

Code §§ 1122 and 1123 with respect to the classification of claims and the contents of a plan

of reorganization”). As described herein, the Plan complies with the requirements of

sections 1122 and 1123 and all other applicable provisions of the Bankruptcy Code.

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

18

i. Section 1122: Classification

46. Section 1122 of the Bankruptcy Code provides:

1. Except as provided in subsection (b) of this section, a plan may place a claim or an interest in a particular class only if such claim or interest is substantially similar to the other claims or interests of such class.

2. A plan may designate a separate class of claims consisting only of every unsecured claim that is less than or reduced to an amount that the court approves as reasonable and necessary for administrative convenience.4

11 U.S.C. § 1122.

47. For a plan to comply with Section 1122, it is not necessary that all

substantially similar claims or interests be designated in the same class, but only that all

claims in a particular class be substantially similar to each other, and have substantially

similar rights to the Debtors’ assets. In re One Times Square Assocs. Ltd. P’Ship, 159 B.R. 695,

703 (Bankr. S.D.N.Y. 2007). Thus, courts generally afford a plan proponent significant

flexibility in classifying claims under section 1122, as long as a reasonable legal and/or

factual basis exists for the proposed classifications, and all claims within a particular class

are substantially similar. See, e.g., In re Jersey City Med. Ctr., 817 F.2d 1055, 1060–61 (3d Cir.

1987) (“Congress intended to afford bankruptcy judges broad discretion [pursuant to section

1122] to decide the propriety of plans in light of the facts”); Olympia & York Fla. Equity Corp.

v. Bank of N.Y. (In re Holywell Corp.), 913 F.2d 873, 880 (11th Cir. 1990) (proponent of plan

has considerable discretion in classifying claims and interests according to relevant facts and

circumstance of case); Teamster’s Nat’l Freight Indus. Negotiating Comm. v. U.S. Truck Co., Inc.

(In re U.S. Truck Co., Inc.), 800 F.2d 581, 586 (6th Cir. 1986) (noting court’s “broad

4 Section 1122(b) of the Bankruptcy Code is inapplicable here because the Plan does not include a convenience class.

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

19

discretion” to determine proper classifications); Windels Marx Lane & Mittendorf, LLP v.

Source Enters., Inc. (In re Source Enters., Inc.), 392 B.R. 541, 556 (S.D.N.Y. 2008) (“Moreover,

‘[a] plan proponent is afforded significant flexibility in classifying claims under § 1122(a) if

there is a reasonable basis for the classification scheme and if all claims within a particular

class are substantially similar.”) (quoting In re Drexel Burnham Lambert Grp., Inc., 138 B.R.

723, 757 (Bankr. S.D.N.Y. 1992)).

48. With the exception of Administrative Claims, Professional Fee Claims, the

DIP Loan Claim, and Priority Tax Claims, which need not be classified pursuant to section

1123(a)(1) of the Bankruptcy Code, Articles 3 and 4 of the Plan provide for separate

classification of Claims against and Equity Interests in the Debtors based upon the legal

nature and priority of such Claims and Interests. See generally Plan, Articles 3 and 4. This

classification scheme complies with section 1122(a) of the Bankruptcy Code because the

Claims or Interests within each particular Class are substantially similar to each other.

Similar Claims have not been placed into different Classes in order to dictate the outcome of

the vote on the Plan. Further, valid business, legal, and factual reasons exist for separately

classifying the various Classes. Accordingly, the Debtors submit that the classification

scheme in the Plan satisfies section 1122 of the Bankruptcy Code.

ii. Section 1123(a)

49. Section 1123(a) of the Bankruptcy Code sets forth seven applicable

requirements with which all chapter 11 plans must comply. See 11 U.S.C. § 1123(a). The

Debtors submit that the Plan fully complies with each enumerated requirement.

a. Section 1123(a)(1): Designation of Classes of Claims and Interests

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

20

50. Section 1123(a)(1) provides that a plan must designate, subject to section 1122

of the Bankruptcy Code, classes of claims and equity interests. See 11 U.S.C. § 1123(a)(1).

The Plan designates seven (7) Classes of Claims against and Equity Interests in the Debtors,

subject to section 1122. See generally Plan, Articles 3 and 4. Accordingly, the Plan satisfies

the requirements of Section 1123(a)(1) of the Bankruptcy Code.

b. Section 1123(a)(2): Specification of Classes that are Not Impaired by the Plan

51. Section 1123(a)(2) of the Bankruptcy Code requires that a plan specify which

classes of claims or interests are unimpaired by the plan. See 11 U.S.C. § 1123(a)(2). Article

3 of the Plan specifies that Class 4 is Unimpaired. See Plan, Article 3. Accordingly, the Plan

satisfies the requirements of section 1123(a)(2) of the Bankruptcy Code.

c. Section 1123(a)(3): Specification of Treatment of Classes that are Impaired by the Plan

52. Section 1123(a)(3) of the Bankruptcy Code requires that a plan specify how it

will treat impaired classes of claims or interests. See 11 U.S.C. § 1123(a)(3). Articles 3 and 4

of the Plan specify that the Voting Classes and Deemed Rejecting Classes are Impaired and

clearly specify the treatment of the Claims and Interests in those Classes. See Plan, Articles 3

and 4. Accordingly, the Plan satisfies the requirements of section 1123(a)(3) of the

Bankruptcy Code.

d. Section 1123(a)(4): Equal Treatment of Claims Within Each Class

53. Section 1123(a)(4) requires that a plan provide the same treatment for each

claim or interest within a particular class unless any claim or interest holder agrees to

receive less favorable treatment than other class members. See 11 U.S.C. 1123(a)(4).

Pursuant to the Plan, the treatment of each Claim against or Equity Interest in the Debtors

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

21

in each respective Class is the same as the treatment of every other Claim or Interest in such

Class, unless the holder of a particular Claim or Interest has agreed to less favorable

treatment for such Claim or Interest. See Plan, Article 4. Accordingly, the Plan satisfies the

requirements of section 1123(a)(4) of the Bankruptcy Code.

e. Section 1123(a)(5): Adequate Means for Implementation

54. Section 1123(a)(5) of the Bankruptcy Code requires that a plan provide

“adequate means” for its implementation. 11 U.S.C. § 1123(a)(5). Adequate means for

implementation of a plan may include, inter alia, retention by the debtor of all or part of its

property and the transfer of property of the estate to one or more entities. See In re MF Global

Inc., 478 B.R. 611, 618 (Bankr. S.D.N.Y. 2012) (“Section 1123(a)(5) provides a means for

the estate to transfer property as part of a confirmed plan, requiring that a plan of

reorganization provide means for implementation . . . .”).

55. Article 5 of the Plan provides adequate and proper means for the

implementation of the Plan. As described in section 5.1 of the Plan, by virtue of the Court

entering the Substantive Consolidation Order, the Debtors have eliminated all

Intercompany Claims, have consolidated all obligations and guarantees of each respective

Debtor, have consolidated all Claims filed or to be filed against the Debtors in these chapter

11 cases, and have consolidated all joint and several liabilities. As a result of the substantive

consolidation of assets and liabilities, upon the Effective Date of the Plan, all claims based

upon guarantees of collection, payment, or performance by one Debtor as to the obligations

of another Debtor will be released and discharged.

56. Section 5.2 of the Plan provides that the Debtors shall consummate the Sale

of the Debtors’ assets to the Purchaser selected pursuant to the Bid Procedures and Bid

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

22

Procedures Order. Pursuant to Section 9.1 of the Plan, all Estate Assets will vest in the

Post-Confirmation Debtors free and clear of all liens, encumbrances, charges and other

interests, except as provided for in the Plan. Concurrently, the proceeds of the Sale will be

distributed to Creditors by the Plan Administrator in accordance with the terms of the Plan.

57. Sections 5.4 through 5.6 of the Plan provide for the appointment of a Plan

Administrator in order to, among other things: (a) consummate the Sale, (b) make

distributions to certain Classes of Creditors, (c) prosecute objections to Claims and

compromise or settle any Claims, and (d) wind-down the Debtors’ affairs.

58. Section 5.7 of the Plan provides for the appointment of a Litigation

Administrator for the purposes of pursuing Chapter 5 Claims and Other Claims for the

benefit of Class 1 Senior Secured Loan Claims and Class 5 Class 5 General Unsecured

Claims. The proceeds of any Chapter 5 Claims (less amounts used to cover any shortfall in

any Reserve Funds) will be shared between the Holders of Class 5 General Unsecured

Claims and the Holders of Senior Secured Claims in a priority order and percentage set

forth in the Plan, which has been agreed-to between the Committee and the Holders of

Senior Secured Loan Claims. The Plan provides for the establishment of a Plan Expense

Reserve Fund, which will be used to satisfy any costs and obligations in connection with the

administration of the Plan after the Effective Date.

59. The Debtors submit that the forgoing provisions in the Plan, together with the

documents and agreements contemplated therein, provide adequate means for

implementing the Plan as required by section 1123(a)(5) of the Bankruptcy Code.

f. Section 1123(a)(6): NOT APPLICABLE

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

23

60. Section 1123(a)(6) of the Bankruptcy Code requires that a debtor’s corporate

documents prohibit the issuance of non-voting equity securities and requires an amendment

of a debtor’s charter to so provide. See 11 U.S.C. § 1123(a)(6). The Plan provides for the

liquidation of the Debtors and the cancellation of all Equity Interests in the Debtors. Neither

the Debtors nor the Post-Confirmation Debtor will issue any equity securities. Therefore,

section 1123(a)(6) of the Bankruptcy Code is not applicable to the Plan.

g. Section 1123(a)(7): Directors and Officers

61. Section 1123(a)(7) of the Bankruptcy Code requires that a plan “contain only

provisions that are consistent with the interests of creditors and equity security holders and

with public policy with respect to the manner of selection of any officer, director, or trustee

under the plan and any successor to such officer, director, or trustee.” 11 U.S.C. §

1123(a)(7).

62. The Plan provides that on the Effective Date, the Plan Administrator will be

deemed the sole shareholder, officer and director of the Post-Confirmation Debtors in order

to effectively administer the Plan. See Plan § 5.4. Timothy Boates, the Debtors’ current

CRO, has been designated in the Plan as the proposed Plan Administrator based upon his

familiarity with the Debtors’ operations as well as his understanding of the Plan and these

chapter 11 cases. The Plan provides for the CRO’s removal by the Bankruptcy Court upon

a showing of good cause. See Plan § 5.5. The Debtors submit that the appointment

contemplated by the Plan, as well as the corresponding oversight, removal, and replacement

procedures provided therein, are consistent with the interests the Debtors’ creditors and

consistent with public policy.

iii. Section 1123(b)

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

24

63. Section 1123(b) of the Bankruptcy Code sets forth certain permissive

provisions that may be incorporated into a chapter 11 plan. The contents of the Plan are

consistent with these provisions.

a. Section 1123(b)(1): Impairment and Non-Impairment of Claims

64. Section 1123(b)(1) provides that a plan “may impair or leave unimpaired any

class of claims, secured or unsecured, or of interests.” 11 U.S.C. § 1123(b)(1). As described

above, the Plan deems the Voting Classes and Deemed Rejecting Classes Impaired and

Class 4 (Other Priority Claims) Unimpaired. Therefore, the Plan is consistent with section

1123(b)(1) of the Bankruptcy Code.

b. Section 1123(b)(2): Executory Contracts and Unexpired Leases

65. Section 1123(b)(2) allows a plan to provide for assumption, assumption and

assignment, or rejection of executory contracts and unexpired leases pursuant to section 365

of the Bankruptcy Code.

66. Subject to the occurrence of the Effective Date, the confirmation of the Plan

will constitute approval of the assumption of the leases and executory contracts listed on

Exhibit 1 (the “Schedule of Assumed Contracts”) annexed to the proposed order confirming

the Debtors’ Plan. Confirmation of the Plan will also act as an approval of the assignment

of the leases and executory contracts to the Purchaser. See Plan § 7.1.

67. The Plan provides for the creation of a Cure Claim Reserve Fund in the event

there are outstanding Cure Cost/Assignment Objections at the time the Plan is confirmed

and to the extent the APA does not require the Purchaser of the Debtors’ assets to pay all

cure amounts of assumed contracts. While the Debtors are working diligently to resolve all

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

25

of the Cure Cost/Assignment Objection prior to confirmation of the Plan, the Plan has

safeguarded against the possibility that certain Objection may not promptly be resolved.

68. The Plan also constitutes a motion under section 365(a) of the Bankruptcy

Code for authorization to reject certain executory contracts and unexpired leases not

previously assumed, assigned or rejected. Except as otherwise set forth in the Plan, the

Debtors intend to reject the executory contracts and unexpired leases identified on Exhibit 2

(the “Schedule of Rejected Executory Contracts and Unexpired Leases”) annexed to the

proposed order confirming the Plan as of the effective dates set forth therein.5 Any

executory contract or unexpired lease that is not assumed by the Purchaser or identified on

the Schedule of Rejected Executory Contracts and Unexpired Leases will be deemed

rejected by the Debtors upon confirmation of the Plan.

69. All Non-Debtor Counterparties have received adequate notice of any and all

Cure Costs existing under their executory contracts and unexpired leases, as well as the

proposed assumption of their contracts or leases by the Purchaser. Accordingly, the

provisions of Article 7 of the Plan are permitted by section 1123(b)(2) of the Bankruptcy

Code.

c. Section 1123(b)(3): Settlements and Retention of Claims

70. Section 1123(b)(3) of the Bankruptcy Code provides that a plan may “provide

for (a) the settlement or adjustment of any claim or interest belonging to the debtor or to the

5 See DIESEL USA, Inc., Case No. 19-10432 (MFW), Docket No. 116, Confirmation Order ¶ 8 (April 12, 2019) (On April 12, 2019, United States Bankruptcy Judge for the District of Delaware, Mary F. Walrath, entered the Findings of Facts, Conclusions of Law and Order (I) Approving the Disclosure Statement and (II) Confirming the First Amended Chapter 11 Plan of Reorganization of Diesel USA, Inc. (the “Confirmation Order”), which, among other things, provided for an effective date of rejection for certain unexpired leases as of “[t]he later of the Plan Effective Date and the date of surrender of the premises”); see also DIESEL USA, Inc., Case No. 19-10432 (MFW), Docket No. 89, First Amended Plan Supplement, Exhibit A, Amended Rejection Schedule (April 5, 2019) (Identifying those unexpired leases to be rejected as of “[t]he later of the Plan Effective Date and the date of surrender of the premises”).

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

26

estate; or (b) the retention and enforcement by the debtor, by the trustee, or by a

representative of the estate appointed for such purpose, of any such claim or interest.” 11

U.S.C. § 1123(b)(3).

71. On the Effective Date, any right, claim or cause of action, belonging to the

Debtors or their estates against any Person or Entity, including without limitation, any

Chapter 5 Claims, that was not previously released by the Debtors or released in the Plan

will be retained by the Post-Confirmation Debtors, to the extent not previously adjudicated,

assigned and/or released. The Plan contemplates the appointment of a Litigation

Administrator who will be responsible for pursuing, settling, or releasing all Chapter 5

Claims and Other Claims for the benefit of the Debtors’ Class 1 Senior Secured Claimants

and Class 5 General Unsecured Claimants. Further, the Plan Administrator will be

responsible for pursuing Other Claims under the APA, if any, belonging to the Debtors or

their estates. The Debtors submit that these provisions of the Plan comply with section

1123(b)(3) of the Bankruptcy Code.

d. Section 1123(b)(4): Sale of Property and Distribution of Proceeds

72. Section 1123(b)(4) of the Bankruptcy Code permits a plan to provide for the

sale of all or substantially all of the property of the estate, and the distribution of the

proceeds of the sale among holders of claims or interests. See 11 U.S.C. 1123(b)(4).

73. As discussed in detail in the Disclosure Statement, this Memorandum of Law,

and various other documents filed in these chapter 11 cases, the Plan provides for the sale of

substantially all of the Debtors’ assets to the Purchaser and subsequent distribution of the

proceeds from such Sale to the Debtors’ Creditors. Liquidating plans such as the Plan

proposed by the Debtors which contemplate a sale of substantially all of a debtor’s assets

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

27

and subsequent distribution of assets have consistently been found to be permissible under

the Bankruptcy Code. See, e.g., Solow v. PPI Enters. (U.S.), Inc. (In re PPI Enters. (U.S.), Inc.,

324 F.3d 197, 211 (3d Cir. 2003) (“the Code clearly contemplates liquidating plans under 11

U.S.C. § 1123(b)(4)”); Coolwater LLC v. Camp Arrowhead (In re Camp Arrowhead), 2010 U.S.

Dist. LEXIS 4970, at *16 (W.D. Tex. Jan. 22, 2010) (“While it is true that a Chapter 11

debtor must demonstrate an ability to effectuate a viable plan of reorganization, the Debtor

may propose a liquidating plan, which is permitted under Section 1123(b)(4).”).

Accordingly, the Debtors’ Plan is permitted by and complies with section 1123(b)(4) of the

Bankruptcy Code.

e. Section 1123(b)(5): Modification of Rights of Holders of Claims

74. Section 1123(b)(5) provides that a plan may “modify the rights of holders of

secured claims, other than a claim secured only by a security interest in real property that is

the debtor’s principal residence, or of holders of unsecured claims, or leave unaffected the

rights of holders of any class of claims.” 11 U.S.C. § 1123(b)(5).

75. As permitted by section 1123(b)(5) of the Bankruptcy Code, the Plan modifies

the rights of Holders of Claims and Interests in the Voting Classes and Deemed Rejecting

Classes. The Plan leaves unaffected the rights of holders of Class 4 Claims.

f. Section 1123(b)(6): Other Provisions

76. Section 1123(b)(6) of the Bankruptcy Code provides that a Plan may “include

any other appropriate provision not inconsistent with the applicable provisions of this title.”

11 U.S.C. § 1123(b)(6). The Debtors’ Plan includes additional provisions which are not

inconsistent with applicable sections of the Bankruptcy Code, including, but not limited to:

(i) Plan § 5.4 (appointment of Plan Administrator); (ii) Plan § 5.8 (appointment of Litigation

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

28

Administrator); (iii) Plan § 5.10 (establishment of Plan Expense Reserve Fund); Plan § 6.4

(establishment of Disputed Claims Reserve); Plan § 6.8 (no distributions of less than twenty

($20) dollars); Plan § 7.4 (establishment of Cure Claim Reserve Fund); Plan § 11.6

(exculpation in favor of the Released Parties); Plan § 11.7 (releases by the Debtors and their

estates of the Released Parties); Plan § 11.8 (injunction against actions outside of the Plan).

The Debtors submit that all provisions of Plan, including those described herein, are

consistent with the Bankruptcy Code, and thus, the Plan complies with section 1123(b)(6) of

the Bankruptcy Code.

iv. Section 1123(d): Cure of Defaults INAPPLICABLE

77. Section 1123(d) of the Bankruptcy Code provides that, “if it is proposed in a

plan to cure a default the amount necessary to cure the default shall be determined in

accordance with the underlying agreement and applicable nonbankruptcy law.” 11 U.S.C. §

1123(d).

78. The Debtors do not believe that any such default exists and, therefore, the

Debtors submit that the Plan complies with the applicable provisions sections 1122 and

1123 of the Bankruptcy Code and meets the requirements of section 1129(a)(1) of the

Bankruptcy Code.

B. Section 1129(a)(2): Compliance with Sections 1125 and 1126 of the Bankruptcy Code

79. Section 1129(a)(2) of the Bankruptcy Code requires that the proponent of a

plan comply with the applicable provisions of the Bankruptcy Code. 11 U.S.C. § 1129(a)(2).

The legislative history of section 1129(a)(2) reflects that this provision is intended to

encompass the disclosure and solicitation requirements under sections 1125 and 1126 of the

Bankruptcy Code. See H.R. Rep. No. 95-595, at 412 (1977); S. Rep. No. 95-989, at 126

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

29

(1978) (“Paragraph (2) [of § 1129(a)] requires that the proponent of the plan comply with the

applicable provisions of chapter 11, such as section 1125 regarding disclosure.”); see also In re

PWS Holding Corp., 228 F.3d 224, 248 (3d Cir. 2000).

80. As previously noted, this Court has already approved the Debtors’ Disclosure

Statement pursuant to section 1125 as containing “adequate information” of a kind and in

sufficient detail to enable hypothetical reasonable investors typical of the Debtors’ creditors

to make an informed judgment whether to accept or reject the Plan. See Disclosure

Statement Order.

81. Section 1126 of the Bankruptcy Code specifies the requirements for

acceptance of a plan. In addition to approving the Debtors’ Disclosure Statement, the Court

also approved the Debtors’ Solicitation Procedures with respect to voting on the Plan.

Under section 1126, only holders of allowed claims and allowed equity interests in impaired

classes of claims or equity interests that will receive or retain property under a plan on

account of such claims or equity interests may vote to accept or reject such plan. See 11

U.S.C. § 1126. As set forth in the Certification of Ballots, the Debtors only solicited votes

on the Plan from holders of Claims in the Voting Classes, and have otherwise have fully

complied with the Solicitation Procedures and Disclosure Statement Order regarding

solicitation and tabulation of votes on the Plan. Moreover, the Debtors gave proper notice

to all Creditors of the Confirmation Objection Deadline, as well as the time and date of the

Confirmation Hearing by promptly serving the Confirmation Hearing Notice as part of each

respective Creditor’s Solicitation Package.

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

30

82. Based on the foregoing, the Debtors submit that the requirements of section

1125 and 1126 of the Bankruptcy Code have been satisfied and as such the Debtors have

complied with section 1129(a)(2) of the Bankruptcy Code.

C. Section 1129(a)(3): Plan Proposed in Good Faith

83. Section 1129(a)(3) of the Bankruptcy Code requires that a chapter 11 plan be

“proposed in good faith and not by any means forbidden by law.” 11 U.S.C. § 1129(a)(3). In

particular, “[g]ood faith should be evaluated ‘in light of the totality of the circumstances

surrounding establishment of [the] plan,’ mindful of the purposes underlying the Bankruptcy

Code. In re Chemtura Corp., 439 B.R. 561, 608 (Bankr. S.D.N.Y. 2010) (quoting In re Madison

Hotel Assocs., 749 F.2d 410, 425 (7th Cir. 1984)). “Whether a reorganization plan has been

proposed in good faith must be viewed in the totality of the circumstances, and the

requirement of Section 1129(a)(3) ‘speaks more to the process of plan development than to

the content of the plan.’” Id. (quoting In re Bush Indus., Inc., 315 B.R. 292, 304 (Bankr.

W.D.N.Y. 2004)). Moreover, “The term ‘good faith’ . . . is generally interpreted to mean

that there exists a reasonable likelihood that the plan will achieve a result consistent with the

objectives and purposes of the Bankruptcy Code.” In re Chassix Holdings, Inc., 533 B.R. 64,

74 (Bankr. S.D.N.Y. 2015).

84. The Debtors submit that the Plan was proposed with the legitimate and

honest purpose of maximizing the value of the Debtors’ estates and to effectuate a

distribution of such value to the Debtors’ Creditors, and therefore was proposed in good

faith. The Plan provides for the approval of the APA, which was the product of arm’s

length bargaining among the Purchaser and key constituencies in these chapter 11 cases.

The Plan also provides for the distribution of proceeds following the Sale in a manner that is

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

31

consistent with the Bankruptcy Code. The good faith of the Plan is further evidenced by the

fact that the Debtors’ Class 1 Senior Secured Loan Voting Class and Class 5 General

Unsecured Claim Voting Class voted in its favor, which demonstrates the informed

judgment of such Creditors that the Plan is in their best interests. Accordingly, the Debtors

submit that the Plan complies with Section 1129(a)(3) of the Bankruptcy Code.

D. Section 1129(a)(4): Payment of Services and Expenses is Subject to Bankruptcy Court Approval

85. Section 1129(a)(4) of the Bankruptcy Code requires that any payments by a

debtor “for services or for costs and expenses in or in connection with the case, or in

connection with the plan and incident to the case,” either be approved by the Bankruptcy

Court as reasonable or subject to approval of the Bankruptcy Court as reasonable. 11 U.S.C.

§ 1129(a)(4). In essence, this subsection requires that any and all fees promised or received

from the estate in connection with or in contemplation of a chapter 11 case must be

disclosed and made subject to the court’s approval. Davis v. Elliot Mgmt. Corp. (In re Lehman

Bros. Holdings Inc.), 508 B.R. 283, 294 n. 9 (S.D.N.Y. 2014) (“Section 1129(a)(4) is partly

focused on ensuring disclosure of payments made in connection with the plan, but not

written into the plan.”); In re Journal Register Co., 407 B.R. 520, 537 (Bankr. S.D.N.Y. 2009);

see In re Johns-Manville Corp., 68 B.R. 618, 632 (Bankr. S.D.N.Y. 1986) (implying that court

must be permitted to review and approve reasonableness of professional fees made from

estate assets).

86. In these chapter 11 cases, only the Debtors’ retained professionals and the

Creditors Committee’s counsel are requesting payment which qualifies for disclosure under

section 1129(a)(4). Pursuant to section 2.3 of the Plan, each Professional requesting

compensation for services provided during these chapter 11 cases and incurred prior to the

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

32

Effective Date of the Plan is required to submit an application for allowance of final

compensation and reimbursement of expenses before the forty-fifth (45th) day after the

Effective Date. For fees incurred after the Effective Date, the Plan Administrator is granted

the authority to review and object to all requests for payment for post-Effective Date services

provided, which review is subject to further Bankruptcy Court review in the event of a

dispute regarding any post-Effective Date Professional Fee Claims. Given the procedures

provided in the Plan regarding Professional Fee Claims, the Debtors submit that the Plan

satisfies section 1129(a)(4) of the Bankruptcy Code.

E. Section 1129(a)(5): Disclosure Regarding Post-Confirmation Directors, Management, and Insiders

87. Section 1129(a)(5)(A)(i) of the Bankruptcy Code requires that the plan

proponent disclose the identity and affiliations of any individual proposed to serve, after

confirmation of a plan, as director, officer or voting trustee of the debtor, an affiliate of the

debtor participating in a joint plan with the debtor, or a successor to the debtor under the

plan. Further, section 1129(a)(5) requires that the appointment of such individual be

“consistent with the interests of creditors and equity security holders and with public policy .

. . .” 11 U.S.C. § 1129(a)(5)(A)(ii).

88. The Plan complies with section 1129(a)(5)(A)(i) of the Bankruptcy Code. The

Plan discloses the appointment of the Debtor’s current CRO as Plan Administrator to

consummate the Sale, complete the Debtor’s wind-down, and to make distributions to

certain Classes of Creditors entitled to receive distributions. See Plan §§ 1.52, 5.4 (“[o]n the

Effective Date and automatically and without further action, the Plan Administrator shall

be deemed the sole shareholder, officer and director of the Post-Confirmation Debtors…”).

The Plan also discloses the establishment of a Litigation Administrator designated by the

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

33

Creditors Committee to pursue Chapter 5 Claims and Other Claims on behalf of certain

Classes of Creditors. See Plan § 5.4, 5.8. The Plan relates solely to the Debtor and not to any

other person or entity. Thus, the Plan complies with section 1129(a)(5)(A)(i) of the

Bankruptcy Code to the extent applicable.

89. The Plan also complies with section 1129(a)(5)(A)(ii) of the Bankruptcy

Code. The appointment of the Debtors’ CRO is entirely consistent with the interests of the

holders of Claims against and Equity Interests in the Debtors and with public policy. The

Debtors’ CRO was selected after an extensive interview process, and has a complete

knowledge of the Debtors’ operations, bankruptcy cases, and Plan such that the Plan can be

implemented in an efficient and cost-effective manner. Further, the Senior Secured Loan

Creditors and the Creditors Committee have not expressed any concerns regarding the

Debtors’ CRO acting as Plan Administrator. Accordingly, the Debtors submit that the

requirements of section 1129(a)(5) are satisfied.

F. Section 1129(a)(6): NOT APPLICABLE

90. Section 1129(a)(6) of the Bankruptcy Code requires, with respect to a debtor

whose rates are subject to governmental regulation following confirmation, that appropriate

governmental approval has been obtained for any rate change provided for in the plan, or

that such rate change be expressly conditioned on such approval. 11 U.S.C. §1129(a)(6).

Section 1129(a)(6) of the Bankruptcy Code does not apply to the Plan as there is no

governmental regulatory commission that has jurisdiction over any rates of the Debtor.

G. Section 1129(a)(7): “Best Interests” Test

91. The Bankruptcy Code protects creditors and equity holders who are impaired

by a plan and who have not voted to accept a plan through the “Best Interests” test of

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

34

section 1129(a)(7). The Best Interests test requires that, with respect to each impaired class

of claims or interests, each holder of a claim in such classes has either accepted the plan, or

will receive property of a value not less than what such holder would receive if the debtor

were liquidated under chapter 7. See 11 U.S.C. § 1129(a)(7)(A)(ii); see also In re Jennifer

Convertibles, Inc., 447 B.R. 713, 724 (Bankr. S.D.N.Y. 2011).

92. The Debtors believe that the holders of Claims against and Equity Interests

in the Debtors will have an equal or greater recovery as a result of the Sale and under the

Plan than could be realized in a chapter 7 liquidation. The Plan provides for the

liquidation of the Post-Confirmation Debtors, and the Debtors are not seeking to require

Creditors to accept non-cash consideration so that the Debtors can pursue going-concern

value. Therefore, the only question remaining is whether non-accepting, Impaired

Creditors will have recovered more (or at least as much) under the Plan than they would

recover through an asset liquidation by a chapter 7 trustee.

93. Attached to the Debtors’ Disclosure Statement as Exhibit B is a liquidation

analysis (the “Liquidation Analysis”) which shows that Creditors are projected to realize

approximately $5.0 million less in a chapter 7 liquidation than the projected net recovery

from the Stalking Horse Bid in a going concern sale. If the Debtors’ assets are liquidated by

a chapter 7 trustee, the Debtors project that the maximum recovery for all Creditors would

be substantially less than what will be recovered if the Plan is confirmed and the Sale is

consummated. The Debtors intend to reduce virtually all of their assets to Cash through

selling substantially all of their assets to the Purchaser. In anticipation of the Sale, the

Debtors have already established systems and protocols for the efficient disposition of their

assets. The significantly increased costs and expenses of a chapter 7 liquidation, including

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

35

fees payable to a chapter 7 trustee, as well as the accompanying delay in the liquidation of

the Debtors’ assets, will only further decrease recoveries below that which will be recovered

through confirmation of the Plan and consummation of the Sale. Accordingly, the Debtors

submit that the Plan satisfies the Best Interests Test of section 1129(a)(7) with respect to all

Classes in the Plan.

H. Section 1129(a)(8): Acceptance by All Impaired Classes

94. Section 1129(a)(8) of the Bankruptcy Code requires that each class of claims

or interests under a plan has either accepted the plan or is not impaired under the plan. All

holders of Claims in Classes entitled to vote on the Plan received Solicitation Packages and

were given adequate opportunity to accept or reject the Plan. See Certification of Ballots.

With respect to holders of Claims in Class 4 whose claims are unimpaired, such claimants

have been “conclusively presumed” to have accepted the plan and need not be further

examined under section 1129(a)(8). See 11 U.S.C. 1126(f).

95. As set forth in the Certification of Ballots, Classes 1 and 5 have affirmatively

voted in favor of the Plan, which Classes are Impaired and eligible to vote on the Plan

(together with Class 4, the “Accepting Classes”). Therefore, section 1129(a)(8) is satisfied

with respect to the Accepting Classes.

96. The Plan does not satisfy section 1129(a)(8) of the Bankruptcy Code,

however, with respect to the Rejecting Classes. As described below, however,

notwithstanding the Rejecting Classes’ affirmative and automatic rejections of the Plan, the

Plan may still be confirmed pursuant to the “cramdown” provisions of section 1129(b) of

the Bankruptcy Code.

I. Section 1129(a)(9): Payment in Full of Allowed Priority Claimants

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

36

97. Section 1129(a)(9) of the Bankruptcy Code requires that certain priority

claims be paid in full on the effective date of a plan. The Debtors’ Plan satisfies each of the

requirements of section 1129(a)(9).

98. First, with respect to Allowed Administrative Claims (i.e., § 507(a)(2) and §

507(a)(3) claims), the Plan provides that such Claims will be paid: (i) the full amount thereof,

without interest, in Cash, as soon as practicable after the later of (a) the Effective Date, (b) the

date on which such Claim becomes an Allowed Claim, or (c) such other date as the holder

of an Allowed Administrative Claim and the Debtors might otherwise agree, or (ii) such

lesser amount as the holder of an Allowed Administrative Claim and the Debtors might

otherwise agree on such date as the holder of an Allowed Administrative Claim and the

Debtors might otherwise agree. See Plan § 2.2 (emphasis added).

99. Second, with respect to Other Priority Claims (all Priority Claims except

Priority Tax Claims) under section 507 of the Bankruptcy Code, the Plan provides that

“[o]n the Effective Date, or as soon thereafter as is reasonably practicable, each holder of an

Allowed Other Priority Claim will receive in full and final satisfaction of such Allowed

Other Priority Claim, except to the extent that such holder agrees to a less favorable

treatment, payment in full in Cash out of the Senior Claims Reserve Fund or other treatment

rendering such Claim Unimpaired.” Plan § 4.5 (emphasis added).

100. Third, with respect to Priority Tax Claims, the Plan provides that “[o]n the

Effective Date, or as soon thereafter as is reasonably practical, in full and final satisfaction

of such Allowed Priority Tax Claim, each holder of an Allowed Priority Tax Claim shall be

paid out of the Senior Claim Reserve Fund (a) an amount in Cash equal to the Allowed amount

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

37

of such Priority Tax Claim, or (b) such other treatment as to which the Debtors and the holder of such

Allowed Priority Tax Claim shall have agreed upon in writing.” Plan § 2.5 (emphasis added).

101. Based upon and Plan provisions set forth above, the Debtors submit that the

Plan satisfies section 1129(a)(9) of the Bankruptcy Code.

J. Section 1129(a)(10): Acceptance by at Least One Impaired Class

102. Section 1129(a)(10) of the Bankruptcy Code requires the affirmative

acceptance of a plan by at least one class of impaired claims, “determined without including

any acceptance of the plan by any insider.” 11 U.S.C § 1129(a)(10).

103. As previously described above and as evidenced by the Certification of

Ballots, holders of Claims in Classes 1 and 5 voted to accept the Plan, without including the

acceptance of the Plan by insiders within such Classes. See Certification of Ballots.

Therefore, the Debtors have satisfied section 1129(a)(10) of the Bankruptcy Code.

K. Section 1129(a)(11): Feasibility

104. Pursuant to section 1129(a)(11) of the Bankruptcy Code, a plan may be

confirmed only if “[c]onfirmation of the plan is not likely to be followed by the liquidation,

or the need for further financial reorganization, of the debtor or any successor to the debtor

under the plan, unless such liquidation or reorganization is proposed in the plan.” 11 U.S.C.

§ 1129(a)(11).

105. Since the Plan expressly provides for the liquidation of the Debtors’ assets,

section 1129(a)(11) of the Bankruptcy Code is satisfied. See In re Revco, 131 B.R. 615, 622

(Bankr. N.D. Ohio 1990) (holding that “[s]ection 1129(a)(11) is satisfied as the plan

provides that the property of [the] Debtors shall be liquidated”). The Debtors forecast that

the Cash payments to be made pursuant to the Plan will be funded through the amounts

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

38

obtained from the Sale and through the pursuit of Chapter 5 Claims. Further, the sale

proceeds and funding under the DIP Loan are projected to provide sufficient resources for

the Plan Administrator and the Litigation Administrator to timely meet all of the Post-

Confirmation Debtors’ obligations under the Plan. Accordingly, the Debtors submit that

the Plan meets the feasibility requirements of section 1129 of the Bankruptcy Code.

L. Section 1129(a)(12): Fees Payable Under 28 U.S.C. § 1930

106. Section 1129(a)(12) of the Bankruptcy Code requires the payment of “[a]ll

fees payable under section 1930 [of title 28 of the United States Code], as determined by the

court at the hearing on confirmation of the plan.” 11 U.S.C. § 1129(a)(12). Section 507 of

the Bankruptcy Code provides that “any fees and charges assessed against the estate under

[section 1930 of] chapter 123 of title 28” are afforded priority as administrative expenses. 11

U.S.C. § 507(a)(2). In accordance with these provisions, the Debtors submit that all fees

incurred and payable pursuant to section 1930 of title 28 of the United States Code shall be

paid in accordance with the section 2.2 of the Plan (payment of Allowed Administrative

Claims) on the Effective Date, or thereafter as and when they become due and owing until

entry of final decrees closing the Debtors’ chapter 11 cases. Thus, the Plan satisfies section

1129(a)(12) of the Bankruptcy Code.

M. Section 1129(a)(13): Retiree Benefits

107. Section 1129(a)(13) of the Bankruptcy Code requires that a plan provide for

the continuation, after the plan’s effective date, of all retiree benefits at the level established

by agreement or by court order pursuant to section 1114 of the Bankruptcy Code at any time

prior to confirmation of the plan, for the duration of the period that the debtor has obligated

itself to provide such benefits. 11 U.S.C. § 1129(a)(13).

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

39

108. While the Debtors do not believe that any retiree benefits (as defined by the

Bankruptcy Code) are owed at this time, the Debtors’ Plan provides for the payment of all

retiree benefits, if any, that are established or maintained by the Debtors prior to the

Effective Date. See Plan § 11.13. Accordingly, the Debtors submit that section 1129(a)(13)

of the Plan is satisfied.

N. Sections 1129(a)(14), (a)(15), and (a)(16): NOT APPLICABLE

109. Section 1129(a)(14) of the Bankruptcy Code relates to the payment of

domestic support obligations. The Debtors are not subject to any domestic support

obligations and, as such, section 1129(a)(14) does not apply. Section 1129(a)(15) of the

Bankruptcy Code applies only in cases in which the debtor is an “individual” (as that term is

defined in the Bankruptcy Code). None of the Debtors are “individuals” and, accordingly,

section 1129(a)(15) is inapplicable. Section 1129(a)(16) of the Bankruptcy Code applies to

transfers of property by a corporation or trust that is not a moneyed, business, or

commercial corporation or trust. All of the Debtors are businesses and accordingly, section

1129(a)(16) is inapplicable.

O. Section 1129(b): Cramdown

110. Section 1129(b) of the Bankruptcy Code provides a mechanism for

confirmation of a plan in circumstances where not all impaired classes of claims and equity

interests vote to accept a plan. This mechanism is known colloquially as “cram down.”

111. Section 1129(b) provides, in pertinent part:

[I]f all of the applicable requirements of [section 1229(a) of the Bankruptcy Code] other than [the requirement contained in section 1129(a)(8) that a plan must be accepted by all impaired classes] are met with respect to a plan, the court, on request of the proponent of the plan, shall confirm the plan notwithstanding the requirements of such paragraph if the plan

Case 8-19-71020-reg Doc 290 Filed 05/02/19 Entered 05/02/19 01:11:27

40

does not discriminate unfairly, and is fair and equitable, with respect to each class of claims or interests that is impaired under, and has not accepted, the plan.