1

Grupo Energía de Bogotá

First Quarter 2013 Results

and Key Developments

Special Report on ConTugas

Investor Conference Call

May 2013

I. Grupo Energía de Bogotá overview and strategy

II. Key developments for Grupo Energía de Bogotá

III. Consolidated financial results and indicators

IV. Special report on ConTugas

V. Questions and answers

VI. Disclaimer

VII. Annex

Agenda

2

Overview and Stragegy of GEB

3

Strategy

Transportation and distribution of energy.

Regional scope.

68.1%

25%

15.6%

Electricity

Transmission

40% 40%

1.8%

98.4%

Generation

51.5% *

2.5%

Distribution

51.5% *

16.2%

51%

82%

Distribution Transportation

Natural Gas

75%

60%

100%

99.94%

*EEB is not the controlling shareholder.

Shareholder Agreements ensure the

maximum distribution of dividends and

provide veto rights for major decisions.

40%

25%

Grupo EEB overview

Regional leader in the energy sector: electricity and natural gas – except E&P;

operations in Colombia, Peru, and Guatemala.

Founded in 1896

District of Bogota is the controlling shareholder: 76.2%.

Shares listed on the Colombian stock exchange; international standards of corporate

governance.

One of Colombia’s largest issuers of debt and equity.

USD Million F 12

Operating revenue 896

Operating income 316

Consolidated EBITDA LTM 724

Net Income 391

Focus on

natural

monopolies

Ample access

to capital

markets

Ambitious

projects in

execution

Growth in

controlled

subsidiaries

Sound

regulatory

framework

Experienced

management

and partners

I. Grupo Energía de Bogotá overview and strategy

II. Key developments for Grupo Energía de Bogotá

III. Consolidated financial results and indicators

IV. Special report on ConTugas

V. Questions and answers

VI. Disclaimer

VII. Annex

Agenda

4

5

Key Developments

On March 31, 2013, the EEB Shareholders’ Meeting approved payment of dividends of COP

403,604 million (COP 43.96 per share). The dividend was the equivalent to 96% of the total

that could legally be distributed. Minority investors will be paid their dividend in a single

installment on May 22, 2013. The Capital District will be paid in two equal installments on June

20, 2013 and November 27, 2013

EEB was included in the COLCAP stock index effective February 1, 2013, reflecting the

increase in trading volumes. This is a tradable index that includes the most representative and

liquid shares in Colombia.

On April 16, 2013, EEB was awarded the Chivor II electricity transmission project through a

bidding process, with an estimated value of USD 101 million.

The Board of Directors approved presenting an offer in the bidding process in Chile to

construct and operate electricity transmission lines. The total estimated value of the projects is

USD 165 million. The results of the bidding process will be announced in June 2013

The Board of Directors authorized the creation of an engineering services company in Peru.

This new subsidiary will seek to develop business in the natural gas and electricity

transportation and distribution sectors.

The CEO of EEB confirmed EEB’s interest in participating in the Panama interconnection

project, and noted the importance of having an open, competitive process.

The February 2013 Shareholders’ Meeting of TGI approved not distributing earnings and constituting

the appropriate legal reserves. A reserve of COP 157,805 million was established to protect future

earnings from exchange fluctuations.

On May 7, 2013, Standard & Poor´s raised TGI’s foreign currency credit rating from “BB” to “BBB-”,

Regulated revenues are expected to increase approximately 10% as a result of the increase in tariffs

authorized by the regulatory agency in December 2012. The new rates will be in effect until 2017.

On April 1, 2013, Cálidda issued USD 320 million in bonds in the international capital markets (2023/

4.375%) under Rule 144A/Reg. S. The resources obtained will enable the company to finance its

2013-14 expansion plan and improve the debt maturity profile.

EEB was awarded projects with a value of approximately USD 73 million, to connect cogeneration

plants to the national grid. TRECSA, an EEB subsidiary, is expected to carry out the works.

Key Developments

The Board of Directors of EEB authorized providing guarantees or making intercompany loans to its

Guatemalan subsidiary for up to USD 230 million (2013-14). These resources complement and are

in addition to the equity contributions already made, and will enable the company to advance with

the negotiation of credits.

I. Grupo Energía de Bogotá overview and strategy

II. Key developments for Grupo Energía de Bogotá

III. Consolidated financial results and indicators

IV. Special report on ConTugas

V. Questions and answers

VI. Disclaimer

VII. Annex

Agenda

7

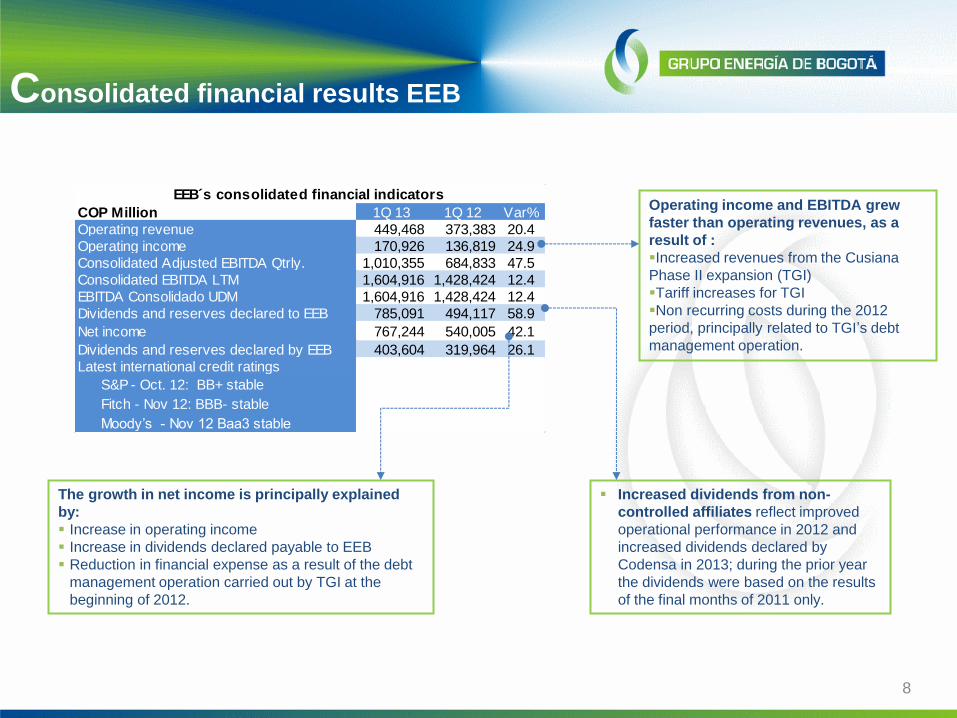

Consolidated financial results EEB

8

The growth in net income is principally explained

by:

Increase in operating income

Increase in dividends declared payable to EEB

Reduction in financial expense as a result of the debt

management operation carried out by TGI at the

beginning of 2012.

Operating income and EBITDA grew

faster than operating revenues, as a

result of :

Increased revenues from the Cusiana

Phase II expansion (TGI)

Tariff increases for TGI

Non recurring costs during the 2012

period, principally related to TGI’s debt

management operation.

Increased dividends from non-

controlled affiliates reflect improved

operational performance in 2012 and

increased dividends declared by

Codensa in 2013; during the prior year

the dividends were based on the results

of the final months of 2011 only.

COP Million 1Q 13 1Q 12 Var%

Operating revenue 449,468 373,383 20.4

Operating income 170,926 136,819 24.9

Consolidated Adjusted EBITDA Qtrly. 1,010,355 684,833 47.5

Consolidated EBITDA LTM 1,604,916 1,428,424 12.4

EBITDA Consolidado UDM 1,604,916 1,428,424 12.4

Dividends and reserves declared to EEB 785,091 494,117 58.9

Net income 767,244 540,005 42.1

Dividends and reserves declared by EEB 403,604 319,964 26.1

Latest international credit ratings

S&P - Oct. 12: BB+ stable

Fitch - Nov 12: BBB- stable

Moody’s - Nov 12 Baa3 stable

EEB´s consolidated financial indicators

Debt indicators

9

The reduction in net leverage is the

result of:

Increase in consolidated EBITDA.

Reduction in net debt ( -1.6%) as a

result of the payment of EEB short term

debt.

The interest coverage ratio improved

as a result of:

Increase in consolidated EBITDA.

Lower financial expenses, as a result of

the debt management operations

carried out by EEB and TGI.

Agenda

10

I. Grupo Energía de Bogotá overview and strategy

II. Key developments for Grupo Energía de Bogotá

III. Consolidated financial results and indicators

IV. Special report on ConTugas

V. Questions and answers

VI. Disclaimer

VII. Annex

Overview ConTugas

Departamento de Ica

Poblacun Population: 763,558

GDP Growth: 5.9% - 2012

Pisco and Marcona designated as petrochemical

industry hub.

Strong agroindustry, fishing, and steel industries

Geography: Desert and plains.

Ica Department

Natural gas market in Peru

Official studies show that there is a

high potential for reserves from other

fields to meet internal demand.

One of the principal government

policies – continued from the previous

administration – is “Mass Distribution of

Natural Gas” to broaden access to this

energy source to the different regions

of the country.

Currently, the gas

transportation company

(TGP) is expanding its

capacity

Fuente: Ministerio de Energía y Minas

Provinces served: Ica, Pisco, Nazca (including

Marcona District) and Chincha

Concession term: 30 years

Length:

Aprox. 251 km (Trunk pipeline)

Aprox. 54 km (Branches)

Rights of way: 87.3 % of the rights of way are on

properties owned by the Peruvian government.

Principal contractual obligations:

-Begin Commercial Operations (“POC”) 24

months after the Closing Date

-Connect 31,625 residential clients 12 months

after POC, and 50,000 clients 6 years after POC.

Project Characteristics

Concession authorized by PROINVERSION for

the distribution of natural gas in the Ica

Department of Peru

ConTugas project

Strengths Characteristics

Natural monopoly with a

stable regulatory framework

Exclusive rights to distribute natural gas over the life of the concession (30 years)

in the Ica Department

Capital intensive.

Essential infrastructure

asset for Peru

Major social and economic impact in the service area.

Potential demand: service area is expected to have major growth in demand for

natural gas in the coming years as a result of potential projects steel, agro

industrial, power plant generation and petrochemical sectors that are being

developed in the region.

Predictable, stable long

term revenues after signing

contracts

Regulation allows stability in the revenues from the distribution system:

- Tariffs are denominated in USD and adjusted by the combination of inflation

indexes.

- Tariffs for the initial period (8 years) are established in the concession agreement

and consider three scenarios for the growth in demand.

- Future tariff revisions (every 4 years) are determined based on recognition of

CAPEX and OPEX and a regulated return equal to the Actualization Rate defined

in the Regulations for the Distribution of Natural Gas (12% real per year) (D.S.

N° 040-2008-EM).

Long-term take or pay contracts (minimum 10 years).

Competitive natural gas

prices

Prices of natural gas are competitive compared to alternative fuels, ensuring

sustainability of the business (average savings of 43% to 75% depending on the

type of consumer) .

Experienced sponsor GEB is a leader in the natural gas transportation and distribution sectors in

Colombia and Peru.

ConTugas project

14

Tariff

1 • Stamp tariff

2

•Distribution tariff based on demand. Three scenarios for tariffs based on demand growth in the concession area.

3

• Initial tariffs set for 8 years, from the start of commercial operations.

4

• Cross subsidy of USD 150 per client to help pay for installation.

Natural Gas Demand

ConTugas project

Equivalent numbers for Ica

Residential 0%

Commercial and SME´s

0% NGV 5%

Industry 44%

Electric Generators

51%

Demand by Sector

Project Status

The project as a whole has a 75% advance as of

March 2013

- More than 100 km of high pressure pipeline

welded.

- More than 148 km of low pressure networks

(polyethylene) constructed.

- More than 10,000 sales to residential clients

and 7,500 internal installations built. Currently

services are only available in Pisco; during

2013, services are expected to begin in the

other cities.

- Approximately 90% of the rights of way have

been negotiated or have been resolved.

Environmental and social action:

- CONTUGAS presented the Environmental

Impact Studies (“EIA”) to MINEM, carried

out the workshops and required public

hearings, and addressed the observations

made to the EIA compiled by MINEM.

- The ConTugas EIA was approved on

December 15, 2010 through Resolution Nº

435-2010-MEM/AAE.

- To date, the company has complied with

the EIA, without any social conflict.

Project Status

Trunk Network and Branches

Advance as of March 2013

Financial Aspects

Gasoducto Regional de Ica

Dpto. Ica

Punto

Entrega TGP 0.5km

40km

220km

TOTAL: USD 345 MM

USD 98MM capital from shareholders

USD 23MM disbursements IGV

USD 133MM in construction loans

(syndicated credit for up to USD 215MM).

Funding sources through March 2013

I. Grupo Energía de Bogotá overview and strategy

II. Key developments for Grupo Energía de Bogotá

III. Consolidated financial results and indicators

IV. Special report on ConTugas

V. Questions and answers

VI. Disclaimer

VII. Annex

Agenda

18

Thank you

Additional information

Grupo Energía de Bogotá – Investor Relations webpage:

─ http://www.grupoenergiadebogota.com/inversionistas

─ http://www.grupoenergiadebogota.com/en/investors

+ 57 1 326 8000 Ext. 1546 / 1675

19

Agenda

20

I. Grupo Energía de Bogotá overview and strategy

II. Key developments for Grupo Energía de Bogotá

III. Consolidated financial results and indicators

IV. Special report on ConTugas

V. Questions and answers

VI. Disclaimer

VII. Annex

Disclaimer

The information presented herein is for informational and illustrative purposes

only. It is not, and does not seek to, provide legal or financial advice on any

subject. This information does not constitute an offer of any sort, and is subject

to change without notice.

EEB expressly states that it does not accept responsibility for any acts or

decisions taken or not taken based on this information. EEB does not accept

any responsibility for losses that might result from the execution of proposals or

recommendations presented. EEB is not responsible for any content that

originated with third parties. EEB may have provided, and might provide in the

future, information that is inconsistent with the information herein presented.

21

I. Grupo Energía de Bogotá overview and strategy

II. Key developments for Grupo Energía de Bogotá

III. Consolidated financial results and indicators

IV. Special report on ConTugas

V. Questions and answers

VI. Disclaimer

VII. Annex

Agenda

22

Annex – Indicators EEB

23

1Q 13 Share 1Q 12 Part. 1Q 13 1Q 12COP Million % COP Million % USD Million USD Million

Financial debt in COP 1,340 0.0 161,353 4.6 0.7 90Financial debt in USD 3,230,256 93.0 3,103,854 89.3 1,763.0 1,732Derivatives position 242,120 7.0 211,896 6.1 132.1 118Total f inancial debt 3,473,716 100.0 3,477,104 100.0 1,895.9 1,940

EEB Consolidated debt structure

Recommended

![TGI 08 Introduction[1]](https://img.pdfslide.us/doc/110x75/577d390f1a28ab3a6b990158/tgi-08-introduction1.jpg)