Structured Financing – Global HospitalsSeptember 2010

Private & Confidential

Structured Financing – Global HospitalsSeptember 2010

Table of Contents

Introduction

Healthcare Industry

Company Overview

Financials

Terms of the Issue

Annexures

Private & Confidential

Introduction

Healthcare Industry

Company Overview

Financials

Terms of the Issue

Annexures

Introduction

Global Hospitals (“Global” or “the Company”) is a group of super-specialty hospitals in India withover 10 years of operations and over 2,000 beds under buildout

To fund the capital expenditure for Global’s new Mumbai hospital that is expected to becommissioned in mid-2011 and other expansion projects in the near term, Global is raising Rs. 100crores through issue of compulsorily convertible preference shares

This offer has been structured to offer investors in the issue a minimum return of 16% IRR

This is therefore an excellent investment opportunity for those looking at guaranteed returnopportunities

Private & Confidential

Global Hospitals (“Global” or “the Company”) is a group of super-specialty hospitals in India withover 10 years of operations and over 2,000 beds under buildout

To fund the capital expenditure for Global’s new Mumbai hospital that is expected to becommissioned in mid-2011 and other expansion projects in the near term, Global is raising Rs. 100crores through issue of compulsorily convertible preference shares

This offer has been structured to offer investors in the issue a minimum return of 16% IRR

This is therefore an excellent investment opportunity for those looking at guaranteed returnopportunities

HEALTHCARE INDUSTRY

Private & Confidential

Strong Underlying Demand for Healthcare in India

Underlying supply – demand gap in healthcare facilities in India still low as compared to otheremerging economies

According to the WHO (World Heath Statistics 2009 report), the total expenditure on healthcare inIndia constituted 3.6% of the gross domestic product in 2006, which is much lower than healthcarespending in other developing countries such as Brazil (7.5%), China (4.6%) and Mexico (6.6%).

Beds available in India at 1.5 per thousand equals that of sub-Saharan Africa and are less than halfof world average at 3.3 per thousand, which presents significant growth potential for the sector asaffordability and availability increases

Private & Confidential

Underlying supply – demand gap in healthcare facilities in India still low as compared to otheremerging economies

According to the WHO (World Heath Statistics 2009 report), the total expenditure on healthcare inIndia constituted 3.6% of the gross domestic product in 2006, which is much lower than healthcarespending in other developing countries such as Brazil (7.5%), China (4.6%) and Mexico (6.6%).

Beds available in India at 1.5 per thousand equals that of sub-Saharan Africa and are less than halfof world average at 3.3 per thousand, which presents significant growth potential for the sector asaffordability and availability increases

Key Measures of Current Weak Infrastructure (# per Thousand)

Situation Particularly Poor in Case of Tertiary Beds,the Space where Global Operates

Tertiary beds, 2001*

Country Share in total no.of beds

Percent

Availability

Beds per ’00,000

7-14India 5 - 10

Specialist physicians, 2001*

Country Share in total no. ofregisteredphysicians

Percent

Availability

Beds per ’00,000

12-18India 10 - 15

Private & Confidential

13-25

65-85

China

Brazil

5 – 10**

20 – 25***

27-31

86-95

South Africa

Korea

35 – 40

50 – 55

* Latest data available used (1997-2001)** Medical colleges and cancer beds account for 5% of total beds*** Surgery beds and medicine beds in single/multi-specialty hospitals

Source: Espicom reports; Mckinsey analysis

According to CII-McKinsey, medical value travel in India is expected to grow to an approximately Rs100 bn (USD 2.4 bn) industry by 2012

n 2004, according to CRIS-INFAC, between 150,000 and 180,000 international patients receivedmedical treatment in India, up from approximately 10,000 in 1995. Patients from approximately 55countries were treated at Indian hospitals.

India has recently introduced a visa category for individuals seeking medical treatment in India

Medical Tourism adds upside to the sector and India provides best in class medical practices atdeveloping world prices

Significant Upside Potential from Medical Tourism forBest Quality Care Healthcare Providers

Private & Confidential

According to CII-McKinsey, medical value travel in India is expected to grow to an approximately Rs100 bn (USD 2.4 bn) industry by 2012

n 2004, according to CRIS-INFAC, between 150,000 and 180,000 international patients receivedmedical treatment in India, up from approximately 10,000 in 1995. Patients from approximately 55countries were treated at Indian hospitals.

India has recently introduced a visa category for individuals seeking medical treatment in India

Medical Tourism adds upside to the sector and India provides best in class medical practices atdeveloping world prices

Cost Comparison in US$ Indian Medical Travel Value

COMPANY OVERVIEW

Private & Confidential

Global Hospitals was founded in 1998 by Dr. K. Ravindranath, Chairman & Managing Director, whois also a reputed surgeon in India and overseas for his work in gastrointestinal surgery and minimalaccess surgery• He has spent considerable time in the UK, working in Memorial Hospital Darlington,

Hammersmith Hospital, London, St. Mark Hospital, London and Kings College Hospital, Londonand also trained more than 500 surgeons in the country and has performed over 20,000laparoscopic surgeries

The Company has achieved significant success in disciplines like Organ Transplant,Gastroenterology, Nephrology, Cardiology and many others specialized disciplines.

The Company has achieved scale to be amongst the Top 3 Healthcare providers in the country interms of bed capacity with a dominant presence in the southern India with expansions in West &East India under execution

The Company has over 300 professional doctors and 65 experienced management teammembers

Amongst the Top 3 Private Healthcare Providers inthe Country

Private & Confidential

Global Hospitals was founded in 1998 by Dr. K. Ravindranath, Chairman & Managing Director, whois also a reputed surgeon in India and overseas for his work in gastrointestinal surgery and minimalaccess surgery• He has spent considerable time in the UK, working in Memorial Hospital Darlington,

Hammersmith Hospital, London, St. Mark Hospital, London and Kings College Hospital, Londonand also trained more than 500 surgeons in the country and has performed over 20,000laparoscopic surgeries

The Company has achieved significant success in disciplines like Organ Transplant,Gastroenterology, Nephrology, Cardiology and many others specialized disciplines.

The Company has achieved scale to be amongst the Top 3 Healthcare providers in the country interms of bed capacity with a dominant presence in the southern India with expansions in West &East India under execution

The Company has over 300 professional doctors and 65 experienced management teammembers

According to CRIS-INFAC, there are six major providers of private healthcare in India, namely theApollo Group, CARE Hospitals, Fortis Healthcare, Manipal Group, Max Healthcare, and WockhardtHospitals

The table below summarizes certain key statistics regarding these healthcare providers, and issourced from CRIS-INFAC and hospital published data, except as indicate

Major Player in a Fragmented Market with Few ScaledModels

Private & Confidential

Number of Beds* Year Location (s) in India Type of Facility**

Apollo*** 5,556 FY10 Pan India P,T,Q

Fortis Healthcare (Incl. Wockhardt) 5,044# FY10 Pan India S,T,Q

Global Hospitals 1,623 FY10 South, West S,T,Q

Manipal Group 1,519 FY10 South P,S,T

Max Healthcare 1,206 FY10 NCR P,S,T,Q

Notes:* Providers may not use the same criteria for counting the number of beds** P: Primary; S: Secondary; T: Tertiary; Q: Quaternary*** Number of beds does not include beds operated by subsidiaries, joint ventures, associates or those in managed hospitals# 3,142 without Wockhardt

Source: Company Filings, company Websites and Broker Research

Global Hospitals: Profile Amongst Best in Class

Global was founded in 1998 and currentlyoperates 4 tertiary-care hospitals, supported by 3regional primary / secondary-care hospitals in ahub and spoke model

Global has entered into associations forknowledge transfer with leading institutes

– Affiliations – King’s College Hospital,London, UK, and with Prof Tanaka, Kyoto,Japan for Liver Transplantation

– Associations – Medical University of SouthCarolina, USA

– Technology Development Board, Dept. ofScience & Technology Govt. of India

– MOU with Bio-Genex Laboratories,California and ICFAI University

India’s first ever dedicated center for multi-organtransplantation

Many First’s in the Country

First Split Liver Transplant.

Largest Cadaver Liver TransplantProgramme

First Auxiliary Liver Transplant

Foremost Hospital to do stem celltransplantation inSpine/Cardiac/Neuro

First Hospital to do small boweltransplantation

Largest Minimal AccessSurgery/Bariatric SurgeryProgramme

First Hospital to do NucleusTransplantation in Spine

Private & Confidential

Global was founded in 1998 and currentlyoperates 4 tertiary-care hospitals, supported by 3regional primary / secondary-care hospitals in ahub and spoke model

Global has entered into associations forknowledge transfer with leading institutes

– Affiliations – King’s College Hospital,London, UK, and with Prof Tanaka, Kyoto,Japan for Liver Transplantation

– Associations – Medical University of SouthCarolina, USA

– Technology Development Board, Dept. ofScience & Technology Govt. of India

– MOU with Bio-Genex Laboratories,California and ICFAI University

India’s first ever dedicated center for multi-organtransplantation

Many First’s in the Country

First Split Liver Transplant.

Largest Cadaver Liver TransplantProgramme

First Auxiliary Liver Transplant

Foremost Hospital to do stem celltransplantation inSpine/Cardiac/Neuro

First Hospital to do small boweltransplantation

Largest Minimal AccessSurgery/Bariatric SurgeryProgramme

First Hospital to do NucleusTransplantation in Spine

Building a pan-India Chain of Super Tertiary Hospitals

Total potential capacity of 2,023 beds. Most of the infrastructure spend on 1,623 beds alreadycomplete.

Current bed count of ~800 beds fully operational with another 775 beds can be “switched” on ascapacity ramps up with minimal capital spend.

Additional 450 beds in Mumbai to come on stream by June 2011. Creating a significant presence in ‘Tertiary Care’ and ‘Transplantation’ markets.

Sl. Location City Area FY10Operational

Beds

PotentialBed Capacity

(1)

CommencementDate

Ownership

Hubs

Private & Confidential

Hubs

1 Lakdi-ka-Pul Hyderabad 67,000 Sft 150 150 1998 Long Term Lease (20 Yr)

2 Aware Hyderabad 130,000 Sft 110 300 Oct-08 Long Term Lease (25 Yr)

3 BGS Global Bangalore 360,000 Sft 200 500 Mar-08 Long Term Lease (30 Yr)

4 ChennaiHealth City

Chennai 21 Acres ofplot

215 500 (2) Mar-09 Owned

5 Lower Parel Mumbai 267,000 Sft - 450 2011E Long Term Lease (99 Yr)

Spokes

6 Vijaynagar Bangalore 5,400 Sft 56 56 2008 Long Term Lease (25 Yr)

7 Divakar Bangalore 8,600 Sft 17 17 2008 Long Term Lease (25 Yr)

8 Ramnagar Bangalore 5,000 Sft 50 50 2008 Long Term Lease

Total Beds 798 2,023(1) All the common infrastructure under operation and additional beds to be “switched on” as capacity ramps up(2) Chennai has surplus 9 acre land which can be potentially used for additional 500 beds using the common infrastructure

Company Holding Structure

Ravindranath GE MedicalAssociates Private Limited

(Holding company)

Center for Digestive & KidneyDiseases Private Limited

(Mumbai)- 65% subsidiary

- Balance with leading partnerdoctors

Global Sunrise MedicalAssociates Private Limited

(Kolkata)- 65% subsidiary

- Balance with Sureka Group (JVpartners)

Global Clinical ResearchServices Private Limited- Clinical research initiative

- To be 100% subsidiary

Private & Confidential

Center for Digestive & KidneyDiseases Private Limited

(Mumbai)- 65% subsidiary

- Balance with leading partnerdoctors

Global Sunrise MedicalAssociates Private Limited

(Kolkata)- 65% subsidiary

- Balance with Sureka Group (JVpartners)

Global Clinical ResearchServices Private Limited- Clinical research initiative

- To be 100% subsidiary

Indivision India Partners (“Indivision”) investedin the company in 2007. Indivision is a$425million private equity fund managed byEverstone Capital

The Company has issued further CCPs toPromoters & Indivision and is undertaking partconversion of CCPS

Current Stake(%)

Stake Post NewInvestor (%)

Promoters &Friends

56.30 50.67

Indivision* 43.70 39.33

New Investors 10.00

Total 100.00 100.00* Indivision currently holding CCPS which is getting partly converted to equitystake subject to RBI approval

FINANCIALS

Private & Confidential

Financial Summary : Profitability on track after initialramp up of facilities

Private & Confidential

FY10 profitability reflected the first year of operations for 2 new hospitals (Chennai and Aware) andsecond year of operations for Bangalore.

EBITDA turning positive effective FY11 as Bangalore & Chennai ramps up in current year. Chennai isexpected to be key driver of EBITDA by FY14 (37% contribution) with Bangalore, Mumbai andHyderabad with 15-16% each being the next key contributors.

PAT margins projected to be double digit FY13 onwards under steady state operations.

YTD July tracking broadly in line with plan (93% revenue achieved with EBITDA slightly better thanbudgets)

Raising capital to strengthen the balance sheet

Private & Confidential

Minority interests are on account of partner doctors collectively owning 35% equity partnerships forMumbai with Equity contribution of Rs400Mn to be funded proportionately

Equity Funding infusion taken for Rs750Mn in FY11

Cash Flows and Use of Proceeds

Private & Confidential

Increase in Equity from Current Shareholdersrepresents additional funding of Rs300Mncompleted by July 2010

Current Fund Raising of Rs750 million primarily tofund the Capital Expenditure of the Mumbai otherhospitals

Capex (Rs Mn)FY11E FY12E FY13E FY14E

Hyderabad 29 10 10 20Bangalore 135 10 10 20Chennai 75 89 10 20Mumbai 750 255 20Aware 109 10 10 20Total 1,099 374 40 100

Comparable Company Analysis

Rs Mn,

unless specified otherwise FY10 FY11 FY12 FY10 FY11 FY12 FY10 FY11 FY12 FY13 FY14

Bed Capacity 5,556 6,756 7,156 3,142 5,044 6,000 1,573 2,023 2,023 2,023 2,023

Operational Beds 3,889 4,729 5,283 3,142 5,044 6,000 798 930 1,323 1,723 2,023

Revenue 20,540 24,081 28,413 9,125 15,535 18,609 1,671 3,036 4,308 5,810 7,098

Revenue/Bed/annum 5.3 5.1 5.4 2.9 3.1 3.1 2.1 3.3 3.3 3.4 3.5

EBITDA 3,196 4,094 4,449 1,502 3,004 3,865 (87) 351 929 1,305 1,654

% margin 15.6% 17.0% 15.7% 16.5% 19.3% 20.8% -5.2% 11.6% 21.6% 22.5% 23.3%

PAT 1,376 1,570 1,859 642 1,282 2,088 (600) (201) 400 770 906

% margin 6.7% 6.5% 6.5% 7.0% 8.3% 11.2% -35.9% -6.6% 9.3% 13.2% 12.8%

Debt 8,300 10,000 11,300 8,250 9,317 10,000 2,931 3,224 3,086 2,723 2,360

Equity 15,766 16,823 18,130 21,313 22,594 25,081 1,110 1,816 2,216 2,986 3,892

Debt:Equity 0.5 0.6 0.6 0.4 0.4 0.4 2.6 1.8 1.4 0.9 0.6

Price# 768 768 768 152 152 152

No. Of Shares 62 62 62 317 317 317

Market Cap 47,473 47,473 47,473 48,265 48,265 48,265

P/E 34.5 30.2 25.5 75.2 37.6 23.1

EV/EBITDA 17.5 13.6 12.9 37.6 18.8 14.9

EV/Bed 10.0 8.3 8.0 18.0 11.2 9.6

* Includes Wockhardt additions in FY11 #Price as of June 16, 2010

GlobalApollo Fortis*

Private & Confidential

Apollo Hospitals, the largest hospital chain in India, is trading at FY12 EV/EBITDA of 12.9x andFortis Healthcare, the second largest chain in India, is trading at 14.9x (better growth profile vsApollo)

Rs Mn,

unless specified otherwise FY10 FY11 FY12 FY10 FY11 FY12 FY10 FY11 FY12 FY13 FY14

Bed Capacity 5,556 6,756 7,156 3,142 5,044 6,000 1,573 2,023 2,023 2,023 2,023

Operational Beds 3,889 4,729 5,283 3,142 5,044 6,000 798 930 1,323 1,723 2,023

Revenue 20,540 24,081 28,413 9,125 15,535 18,609 1,671 3,036 4,308 5,810 7,098

Revenue/Bed/annum 5.3 5.1 5.4 2.9 3.1 3.1 2.1 3.3 3.3 3.4 3.5

EBITDA 3,196 4,094 4,449 1,502 3,004 3,865 (87) 351 929 1,305 1,654

% margin 15.6% 17.0% 15.7% 16.5% 19.3% 20.8% -5.2% 11.6% 21.6% 22.5% 23.3%

PAT 1,376 1,570 1,859 642 1,282 2,088 (600) (201) 400 770 906

% margin 6.7% 6.5% 6.5% 7.0% 8.3% 11.2% -35.9% -6.6% 9.3% 13.2% 12.8%

Debt 8,300 10,000 11,300 8,250 9,317 10,000 2,931 3,224 3,086 2,723 2,360

Equity 15,766 16,823 18,130 21,313 22,594 25,081 1,110 1,816 2,216 2,986 3,892

Debt:Equity 0.5 0.6 0.6 0.4 0.4 0.4 2.6 1.8 1.4 0.9 0.6

Price# 768 768 768 152 152 152

No. Of Shares 62 62 62 317 317 317

Market Cap 47,473 47,473 47,473 48,265 48,265 48,265

P/E 34.5 30.2 25.5 75.2 37.6 23.1

EV/EBITDA 17.5 13.6 12.9 37.6 18.8 14.9

EV/Bed 10.0 8.3 8.0 18.0 11.2 9.6

* Includes Wockhardt additions in FY11 #Price as of June 16, 2010

GlobalApollo Fortis*

TERMS OF THE ISSUE

Private & Confidential

Amount of Financing Upto Rs.100 Crores

Instrument Compulsory Convertible Preferential Shares (“CCPS”)

Transaction Date September 30th, 2010

Conversion Date September 30th, 2013 or the Exit Event

Pre-Money Valuation 750 Crores

At an IPO event prior to the Conversion Date, holders of the CCPS can convert their shares intocommon shares if they receive at least a 16% IRR based on the post-money IPO per sharevaluation of the common share as compared to the pre-money valuation of the CCPS.

At an IPO event prior to the Conversion Date, if upon conversion the holders of the CCPS do notreceive at least an 16% IRR based on the post-money IPO per share valuation of the commonshare of the company as compared to the pre-money valuation of the CCPS, the number ofcommon shares received upon conversion will be increased such that the IRR is 16%.

If there is no IPO event by the Conversion Date, the Conversion Date of the CCPS will beextended by one year during which the Company will attempt exit through a third party / strategicsale with conversion terms as described in the above two paragraphs.

If there is no exit through third party / strategic sale within one year after the Conversion Date, thepromoters of the Company will buy back the CCPS at a purchase price such that each holderreceives a 20% IRR based on the purchase price as compared to the pre-money valuation of theCCPS.

Private & Confidential

Conversion

At an IPO event prior to the Conversion Date, holders of the CCPS can convert their shares intocommon shares if they receive at least a 16% IRR based on the post-money IPO per sharevaluation of the common share as compared to the pre-money valuation of the CCPS.

At an IPO event prior to the Conversion Date, if upon conversion the holders of the CCPS do notreceive at least an 16% IRR based on the post-money IPO per share valuation of the commonshare of the company as compared to the pre-money valuation of the CCPS, the number ofcommon shares received upon conversion will be increased such that the IRR is 16%.

If there is no IPO event by the Conversion Date, the Conversion Date of the CCPS will beextended by one year during which the Company will attempt exit through a third party / strategicsale with conversion terms as described in the above two paragraphs.

If there is no exit through third party / strategic sale within one year after the Conversion Date, thepromoters of the Company will buy back the CCPS at a purchase price such that each holderreceives a 20% IRR based on the purchase price as compared to the pre-money valuation of theCCPS.

Liquidation Preference First pay 100% of the Amount of Financing to the holders of the CCPS in preference to othershareholders; the remaining assets shall be distributed pro-rata amongst all shareholders

Fees Profit share of 20% over 16% IRR

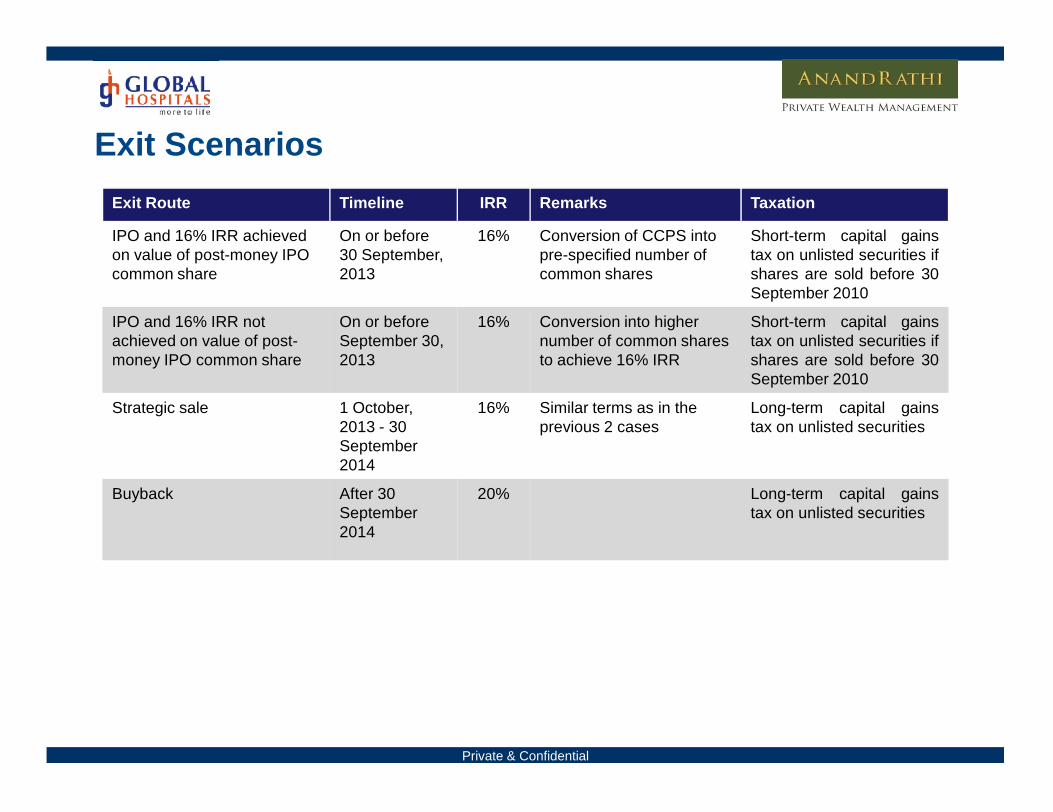

Exit Scenarios

Exit Route Timeline IRR Remarks Taxation

IPO and 16% IRR achievedon value of post-money IPOcommon share

On or before30 September,2013

16% Conversion of CCPS intopre-specified number ofcommon shares

Short-term capital gainstax on unlisted securities ifshares are sold before 30September 2010

IPO and 16% IRR notachieved on value of post-money IPO common share

On or beforeSeptember 30,2013

16% Conversion into highernumber of common sharesto achieve 16% IRR

Short-term capital gainstax on unlisted securities ifshares are sold before 30September 2010

Strategic sale 1 October,2013 - 30September2014

16% Similar terms as in theprevious 2 cases

Long-term capital gainstax on unlisted securities

Private & Confidential

Strategic sale 1 October,2013 - 30September2014

16% Similar terms as in theprevious 2 cases

Long-term capital gainstax on unlisted securities

Buyback After 30September2014

20% Long-term capital gainstax on unlisted securities

Risk Disclosure

This is an investment in a company that is not publicly listed on an exchange. The acquisition valueof the shares should not be taken to be indicative of the value of the shares at the time of exit viaeither a private placement to a buyer or through selling in the market if the Equity Shares are laterlisted on a public exchange.

No assurance can be given regarding an active and / or sustained trading in the Equity shares of thecompany or regarding the price at which the Equity Shares will be trading after listing. No assurancecan be given of finding a buyer for private placement or a public issuance / listing, in which case thesecurities acquired could become highly illiquid and unrealizable.

Private & Confidential

ANNEXURES

Private & Confidential

What are CCPS?

Compulsorily Convertible Preference Shares (CCPS) are preference shares that will be mandatorilyconverted into common shares on a particular date

Preference shares are similar to common shares but they do not usually have voting rights. They aresimilar to debt as they usually have a fixed dividend (similar to fixed interest payments on debt).

Preference shares are senior to equity but subordinate to debt in case of a liquidity event

CCPS are quite popular with PE Investors these days

They offer enhanced participatory role in the company by allowing certain covenants to be imposedon the company

• For instance, the number of shares into which each preference share can be converted isdecided before the investment is made

• On the conversion date, if the company has met its performance targets, the investor getsequity stake in the company by converting the preference shares into common shares

• However, if the company does not meet the performance targets as per the covenants, theinvestor can convert the preference shares into a higher number of common shares in thecompany. This increases the controlling power of the investor in the company.

Private & Confidential

Compulsorily Convertible Preference Shares (CCPS) are preference shares that will be mandatorilyconverted into common shares on a particular date

Preference shares are similar to common shares but they do not usually have voting rights. They aresimilar to debt as they usually have a fixed dividend (similar to fixed interest payments on debt).

Preference shares are senior to equity but subordinate to debt in case of a liquidity event

CCPS are quite popular with PE Investors these days

They offer enhanced participatory role in the company by allowing certain covenants to be imposedon the company

• For instance, the number of shares into which each preference share can be converted isdecided before the investment is made

• On the conversion date, if the company has met its performance targets, the investor getsequity stake in the company by converting the preference shares into common shares

• However, if the company does not meet the performance targets as per the covenants, theinvestor can convert the preference shares into a higher number of common shares in thecompany. This increases the controlling power of the investor in the company.

About Everstone Capital

Everstone Capital is an India focused investment manager with dedicated private equity and realestate funds

With offices in Mauritius, Singapore, Mumbai, Delhi and Bengaluru, the Everstone team comprisesover one hundred people with significant experience and a strong network of relationships

Indivision I is a $425 million private equity fund raised in 2006 which focuses on investing incompanies engaged in the provision of goods and services in domestic consumption and enablers ofinfrastructure segments

Some of the portfolio companies of Indivision I include:

• Global Hospitals

• Tikona Digital Networks

• VLCC Healthcare

• Future Media

• Lilliput Kidswear

• Blue Foods

• Percept

Private & Confidential

Everstone Capital is an India focused investment manager with dedicated private equity and realestate funds

With offices in Mauritius, Singapore, Mumbai, Delhi and Bengaluru, the Everstone team comprisesover one hundred people with significant experience and a strong network of relationships

Indivision I is a $425 million private equity fund raised in 2006 which focuses on investing incompanies engaged in the provision of goods and services in domestic consumption and enablers ofinfrastructure segments

Some of the portfolio companies of Indivision I include:

• Global Hospitals

• Tikona Digital Networks

• VLCC Healthcare

• Future Media

• Lilliput Kidswear

• Blue Foods

• Percept

THANK YOU

Private & Confidential

DisclaimersThis presentation has been issued by Anand Rathi Financial Services Limited (ARFSL), which is regulated by SEBI. The information herein wasobtained from various sources; we do not guarantee its accuracy or completeness. Neither the information nor any opinion expressed constitutes anoffer, or an invitation to make an offer, to buy or sell any securities or any options, futures or other derivatives related to such securities ("relatedinvestments"). ARFSL and its affiliates may trade for their own accounts as market maker / jobber and/or arbitrageur in any securities of this issuer(s) orin related investments, and may be on the opposite side of public orders. ARFSL, its affiliates, directors, officers, and employees may have a long orshort position in any securities of this issuer(s) or in related investments. ARFSL or its affiliates may from time to time perform investment banking orother services for, or solicit investment banking or other business from, any entity mentioned in this presentation.

Recommended