Getting strategic –and tactical - about digital disruption1Q 2017 KPMG Global Insights Pulse

May 16, 2017

2© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Webcast participants

Stan Lepeak

Director, Global

Management Consulting

Research, KPMG LLP

(US)

Morris Treadway

Global Lead,

Financial Management and

Partner, KPMG LLP (US)

Dave Brown

Global Lead,

Shared Services &

Outsourcing Advisory and

Partner, KPMG LLP (US)

3© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. NDPPS 653829

To ask a question, use the ‘Ask a Question’

box on your media player

Technical issues: use the '?' button in the

upper right corner of your webcast player to

access our new online help portal

— If this does not resolve your issue, please

submit a question through the ‘Ask a

Question’ box, and you will receive a reply

from our technical staff shortly in the

‘Answered Questions’ box.

CPE regulations require that online

participants take part in online questions

1. Must respond to a minimum of three

questions per 50 minutes

2. Polling questions will appear on your

media player

3. Post webcast survey must be

completed

4. Results will be reviewed in the

aggregate; no responses will be tracked

back to any individual or organization

Administrative

1

2

3

4

4© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. NDPPS 653829

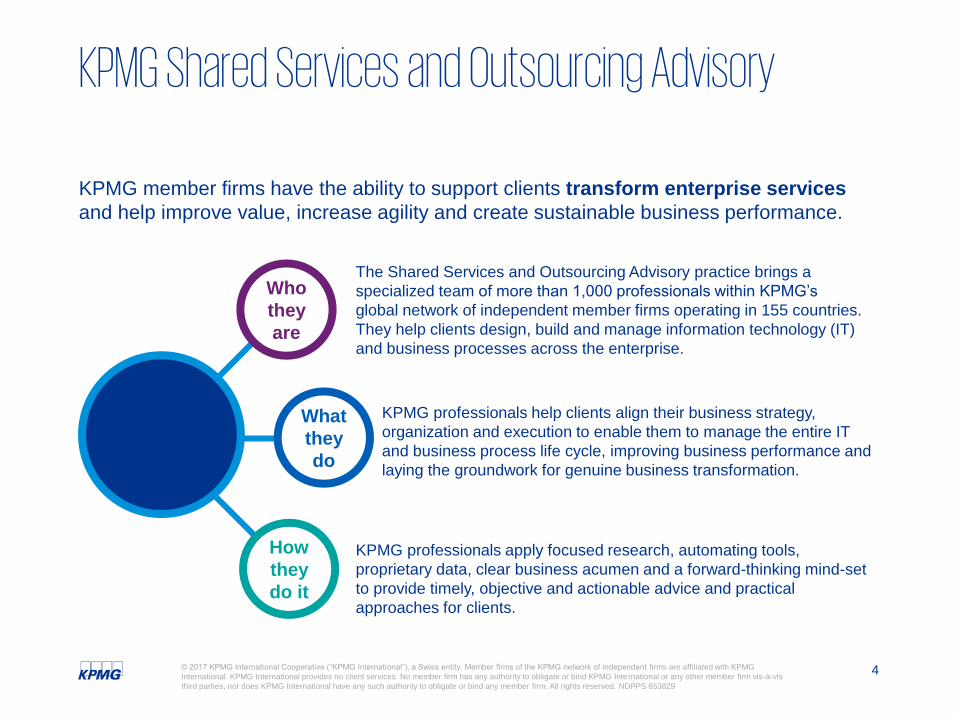

KPMG Shared Services and Outsourcing Advisory

KPMG member firms have the ability to support clients transform enterprise services

and help improve value, increase agility and create sustainable business performance.

Who

they

are

What

they

do

How

they

do it

The Shared Services and Outsourcing Advisory practice brings a

specialized team of more than 1,000 professionals within KPMG’s

global network of independent member firms operating in 155 countries.

They help clients design, build and manage information technology (IT)

and business processes across the enterprise.

KPMG professionals help clients align their business strategy,

organization and execution to enable them to manage the entire IT

and business process life cycle, improving business performance and

laying the groundwork for genuine business transformation.

KPMG professionals apply focused research, automating tools,

proprietary data, clear business acumen and a forward-thinking mind-set

to provide timely, objective and actionable advice and practical

approaches for clients.

5© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. NDPPS 653829

KPMG Enterprise Performance Management (EPM)KPMG's EPM Center of Excellence supports KPMG member firms as they assist clients

to holistically align their business strategies with plans and actions that help optimize

performance, drive growth and deliver sustainable value — resulting in a competitive

advantage.

Who

they

are

What

they

do

How

they

do it

KPMG firms in 152 countries bring clients a specialized team of more than

1,135+ EPM professionals. They help clients manage and execute

their business strategies to improve decision-making and help

optimize performance across all business domains and functions.

KPMG professionals help empower organizations with the ability to

dynamically manage, analyze and predict their business performance

so they can anticipate and adapt swiftly to market conditions.

Enabled by technology, EPM analyzes internal and external data to

improve performance by aligning strategies, plans, decisions and actions

through a tightly integrated capability across people, process and

technology that embeds leading practices to enable a continuous

improvement process and culture.

6© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. NDPPS 653829

Polling question 1In which of the following industry groups does your organization operate?

Business or IT service provider

KPMG employee

Financial services

Diversified industrials/manufacturing

Energy and natural resources

Healthcare and pharmaceuticals

Retail consumer goods/Food and beverage

Technology

Government/Education

Other

Select one:

7© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. NDPPS 653829

KPMG Global Insights Pulse The surveys are a quarterly review of global business services (GBS), related

service delivery market trends and individual observations from the ‘front lines’

— KPMG’s global network of

advisors focused on:

— Sourcing advisory

— Financial management

— CIO advisory

— People and change

— Business operations

— Tax, deal advisory,

and audit

— KPMG market research

— Digital disruption

and digitalization

— The role of the finance

organization in

enabling digitalization

— The role of the GBS

organization in

enabling digitalization

— Digitalization as an enabler

for organization agility,

collaboration and partnering

— Call center/customer care

— Finance and accounting

— Human resources

— Information technology

— Procurement

— Real estate and facilities

management

— Vertical industry BPO

— Emerging BPO/KPO functions

Focus on performance,

trends, and future state

— Global Insights Pulse launched in 2004 by EquaTerra*

— Part of a growing family of KPMG Pulse market research studies

* KPMG LLP (US), KPMG Holdings Limited (UK) and KPMG International acquired the business and subsidiaries of advisory firm EquaTerra, Inc. in February 2011.

Input sources: Topics evaluated: Primary functional focus:

Digital disruption and digitization

9© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. NDPPS 653829

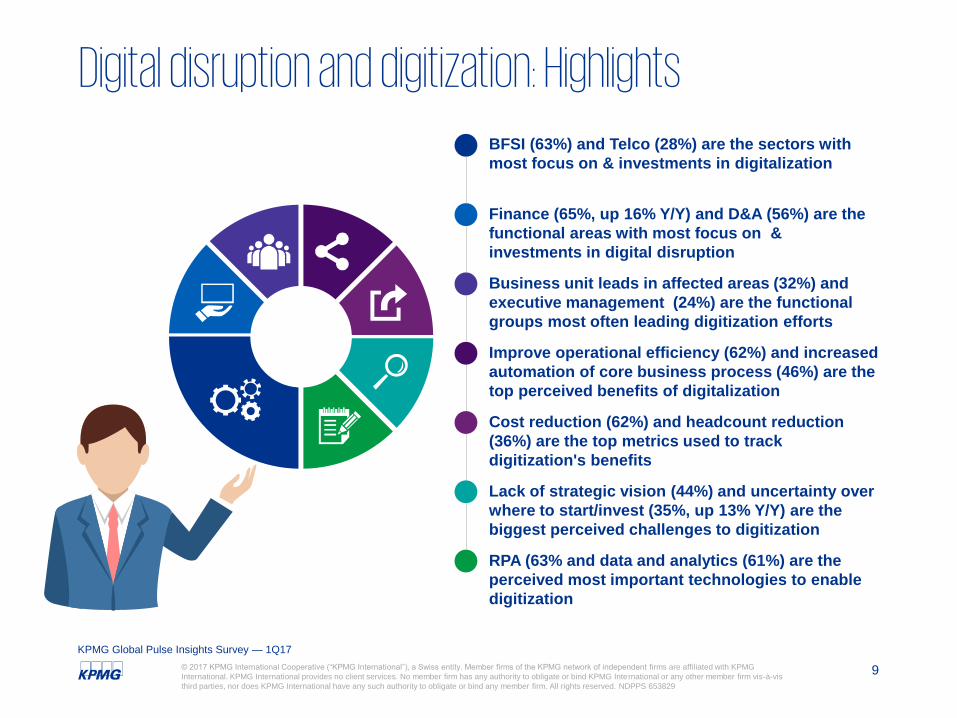

Digital disruption and digitization: HighlightsBFSI (63%) and Telco (28%) are the sectors with

most focus on & investments in digitalization

Business unit leads in affected areas (32%) and

executive management (24%) are the functional

groups most often leading digitization efforts

Finance (65%, up 16% Y/Y) and D&A (56%) are the

functional areas with most focus on &

investments in digital disruption

Improve operational efficiency (62%) and increased

automation of core business process (46%) are the

top perceived benefits of digitalization

Cost reduction (62%) and headcount reduction

(36%) are the top metrics used to track

digitization's benefits

Lack of strategic vision (44%) and uncertainty over

where to start/invest (35%, up 13% Y/Y) are the

biggest perceived challenges to digitization

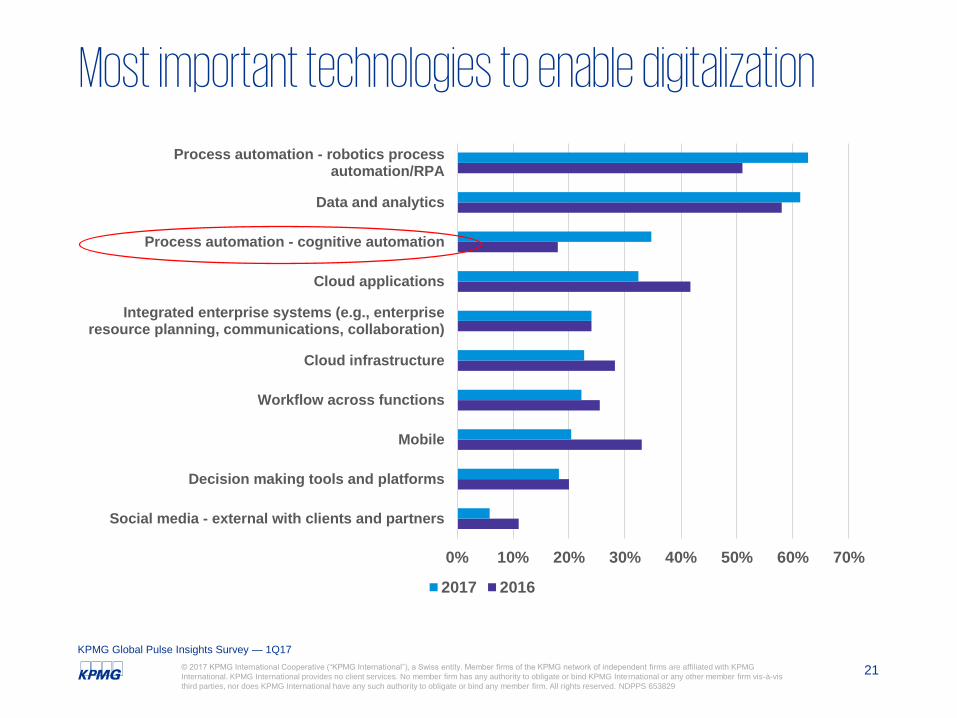

RPA (63% and data and analytics (61%) are the

perceived most important technologies to enable

digitization

KPMG Global Pulse Insights Survey — 1Q17

10© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. NDPPS 653829

Sectors with most focus on and investments in digitalization: Top 10

0% 10% 20% 30% 40% 50% 60% 70%

High Tech Products/Svcs

Automotive

Manufacturing

Pharma/Biotech

Energy/Utilities, Oil & Gas

Entertainment/Media, Hospitality/Travel,

Healthcare

CPG, Food & Beverage, Retail, Wholesale

Telco

Banking, Financial Services, Insurance

2017 2016

KPMG Global Pulse Insights Survey — 1Q17

11© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. NDPPS 653829

Functional areas with most focus on and investments in digital disruption

0% 10% 20% 30% 40% 50% 60% 70%

Transportation/logistics

All business functions

Human resources

Procurement

Sales & marketing

Supply chain

Customer care

Information technology

Data and analytics

Finance & accounting

2017 2016

KPMG Global Pulse Insights Survey — 1Q17

12© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. NDPPS 653829

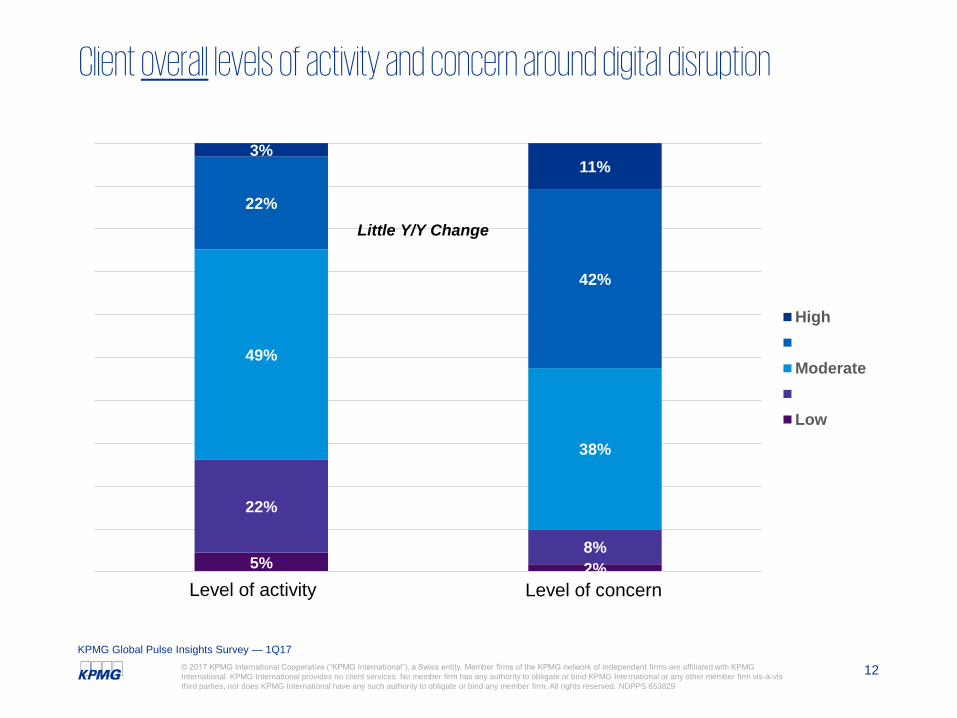

Client overall levels of activity and concern around digital disruption

5% 2%

22%

8%

49%

38%

22%

42%

3%11%

Level of Activity Leve of Concern

High

Moderate

Low

Little Y/Y Change

Level of activity Level of concern

KPMG Global Pulse Insights Survey — 1Q17

13© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. NDPPS 653829

Polling question 2:How concerned is your organization about digital disruption?

Very concerned

Somewhat concerned

Not at all concerned

Select one:

14© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. NDPPS 653829

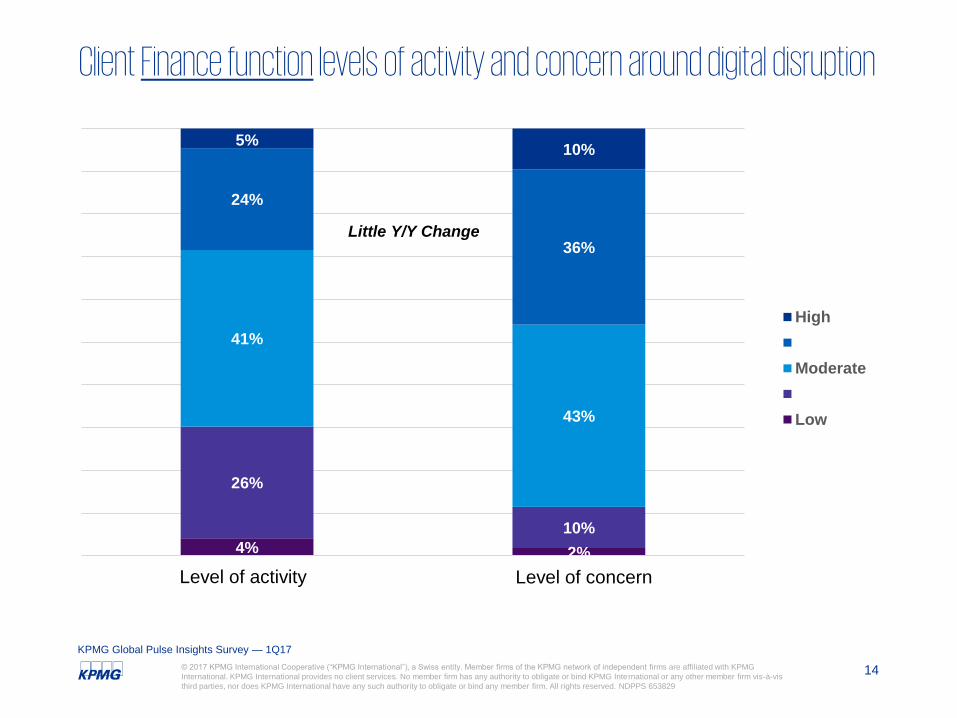

Client Finance function levels of activity and concern around digital disruption

4% 2%

26%

10%

41%

43%

24%

36%

5%10%

Level of Activity Leve of Concern

High

Moderate

Low

Little Y/Y Change

KPMG Global Pulse Insights Survey — 1Q17

Level of activity Level of concern

15© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. NDPPS 653829

Very active

Somewhat active

Not at all active

Polling question 3:How active is your organization in addressing and responding to digital disruption?

(Please select one)

Select one:

16© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. NDPPS 653829

Functional group most often leading digitization efforts

0% 5% 10% 15% 20% 25% 30% 35%

Everyone

No one

Dedicated digitization team

IT group

Executive management

Business unit leaders in affected areas

2017 2016

KPMG Global Pulse Insights Survey — 1Q17

17© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. NDPPS 653829

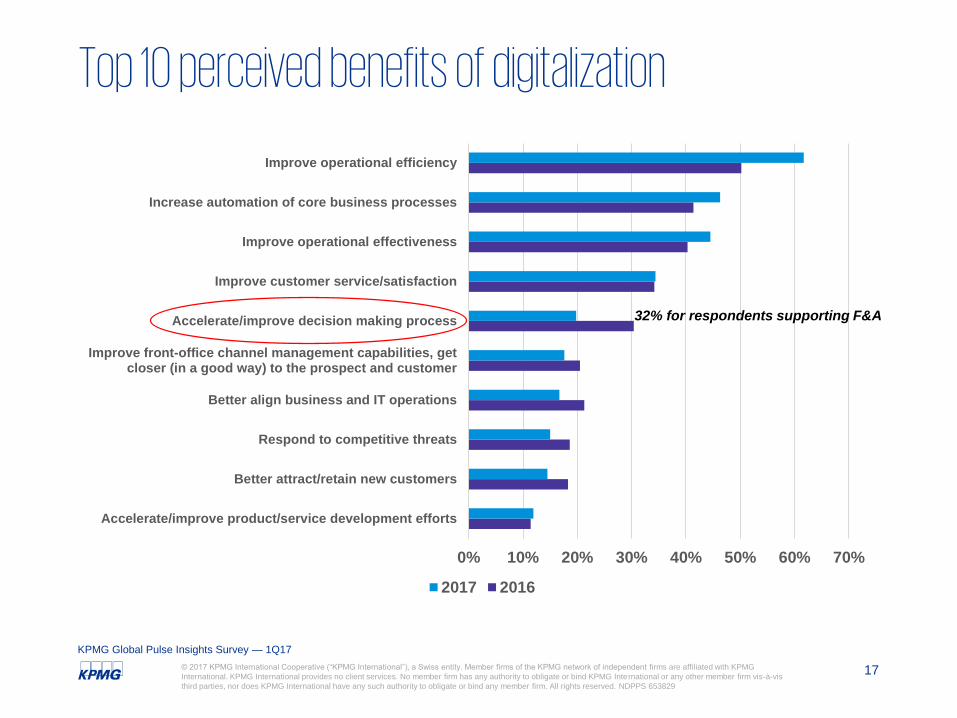

Top 10 perceived benefits of digitalization

0% 10% 20% 30% 40% 50% 60% 70%

Accelerate/improve product/service development efforts

Better attract/retain new customers

Respond to competitive threats

Better align business and IT operations

Improve front-office channel management capabilities, getcloser (in a good way) to the prospect and customer

Accelerate/improve decision making process

Improve customer service/satisfaction

Improve operational effectiveness

Increase automation of core business processes

Improve operational efficiency

2017 2016

32% for respondents supporting F&A

KPMG Global Pulse Insights Survey — 1Q17

18© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. NDPPS 653829

Metrics used to track benefits of digitization

0% 10% 20% 30% 40% 50% 60% 70%

No specific metrics/many metrics

Not meaningfully measuring

Revenue growth

Level/degree of process automation

Case by case metrics per project/initiative

Function/process operational efficiency

Function/process operational effectiveness

Reduced cycle times (i.e., for product/servicedevelopment/roll-out, general projects, etc.)

Headcount reduction

Cost reduction

2017 2016

Just 38% for respondents

supporting F&A

KPMG Global Pulse Insights Survey — 1Q17

19© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. NDPPS 653829

Top 10 biggest challenges to digitization

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

No sense of urgency

Inability to develop compelling business case

Limitations of IT systems

Lack of funding

Poor understanding of impact

Cultural resistance to new ways of doingbusiness

Limited/conflicting understating of what it is

Lack of critical skills internally

Uncertainty as to where to start/invest mostheavily

Lack of strategic vision

2017 2016

KPMG Global Pulse Insights Survey — 1Q17

20© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. NDPPS 653829

Polling question 4:What do you see as the biggest challenge in enabling digitalization?

Select one:

Uncertainty as to where to start/invest most heavily

Poor understanding of impact

Financial services

Inability to develop compelling business case

No sense of urgency

Lack of critical skills internally

Lack of funding

Lack of strategic vision

Limited/conflicting understanding of what it is

Limitations of IT systems

21© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. NDPPS 653829

Most important technologies to enable digitalization

0% 10% 20% 30% 40% 50% 60% 70%

Social media - external with clients and partners

Decision making tools and platforms

Mobile

Workflow across functions

Cloud infrastructure

Integrated enterprise systems (e.g., enterpriseresource planning, communications, collaboration)

Cloud applications

Process automation - cognitive automation

Data and analytics

Process automation - robotics processautomation/RPA

2017 2016

KPMG Global Pulse Insights Survey — 1Q17

The role of the finance function in enabling digitization

23© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. NDPPS 653829

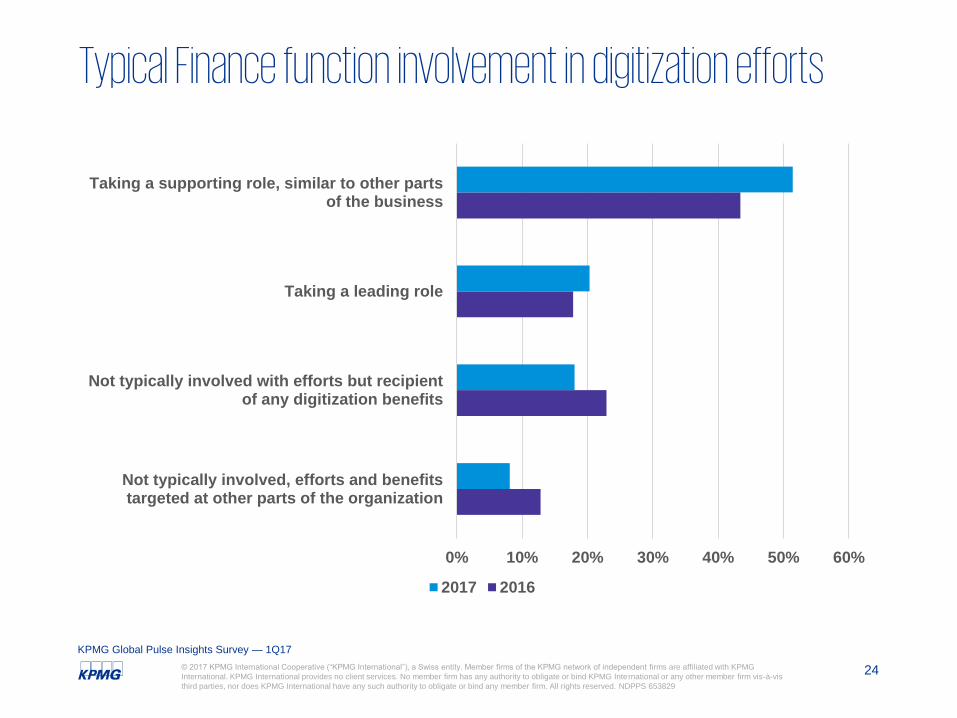

Role of the Finance function in enabling digitization: Highlights

Finance function is mostly likely to

play a supporting role, similar to

other parts of the business (51%),

in digitization efforts

Ability to apply financial & data

analytics to identify opportunities for

profitable growth (47%) and can

develop business cases/plans,

manage implementation efforts

(42%) are the most valuable skills

the finance function can bring to

digitization efforts

47%51%

$

KPMG Global Pulse Insights Survey — 1Q17

24© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. NDPPS 653829

Typical Finance function involvement in digitization efforts

0% 10% 20% 30% 40% 50% 60%

Not typically involved, efforts and benefitstargeted at other parts of the organization

Not typically involved with efforts but recipientof any digitization benefits

Taking a leading role

Taking a supporting role, similar to other partsof the business

2017 2016

KPMG Global Pulse Insights Survey — 1Q17

25© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. NDPPS 653829

Most valuable skills the Finance function can bring to digitization efforts

0% 10% 20% 30% 40% 50% 60%

Can manage risks in digitization implementationefforts

Already experienced with digitalization tools, issuesand needs

Can best leverage and utilize new insights gainedfrom digitization

Understands regulatory risks, issues andrequirements

Understands the business

Can bring C-level support and direction toe efforts

Possesses cross-functional view of the organization

Can develop business cases and plans and manageimplementation efforts for various investments

Ability to apply financial and data analytics toidentify new opportunities for profitable growth

2017 2016KPMG Global Pulse Insights Survey — 1Q17

The role of the GBS organization in enabling digitization

27© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. NDPPS 653829

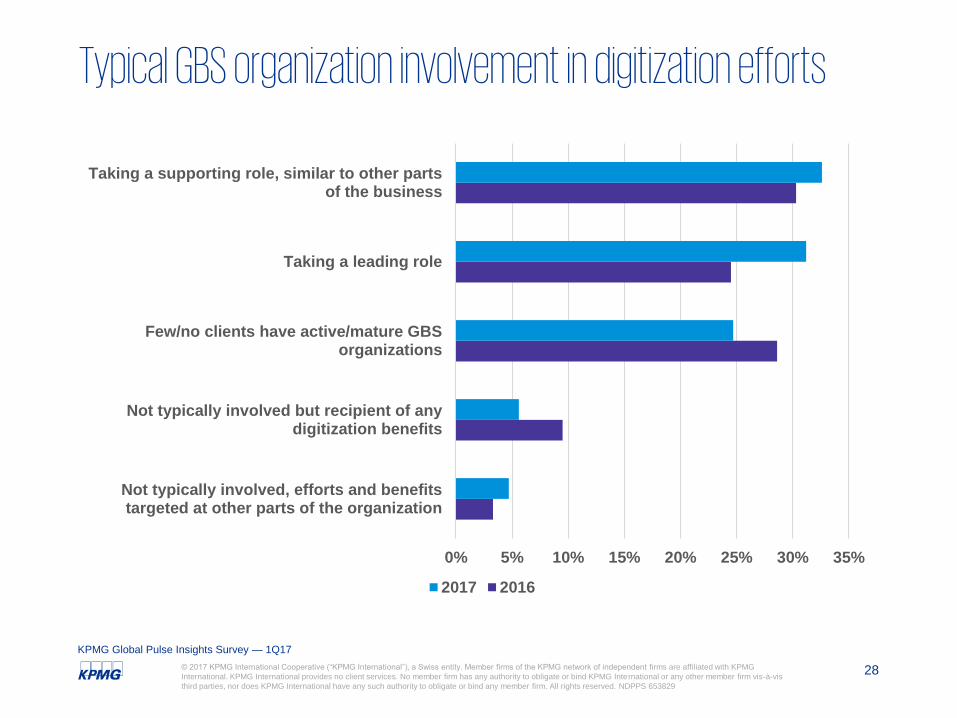

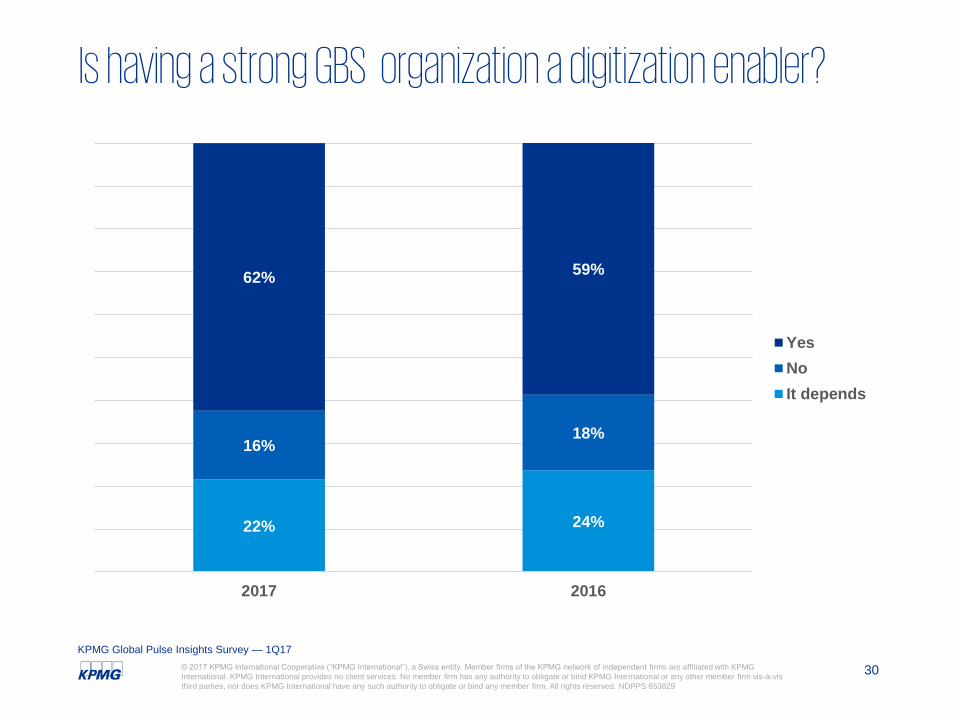

Role of the GBS organization in enabling digitization: Highlights

Sixty-two percent of respondents indicated

that having a strong GBS organization a

digitization enabler

The GBS organization is mostly likely to

play a supporting role, similar to other parts

of the business (33%), in digitization efforts

62%

33%

KPMG Global Pulse Insights Survey — 1Q17

28© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. NDPPS 653829

Typical GBS organization involvement in digitization efforts

0% 5% 10% 15% 20% 25% 30% 35%

Not typically involved, efforts and benefitstargeted at other parts of the organization

Not typically involved but recipient of anydigitization benefits

Few/no clients have active/mature GBSorganizations

Taking a leading role

Taking a supporting role, similar to other partsof the business

2017 2016

KPMG Global Pulse Insights Survey — 1Q17

29© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. NDPPS 653829

Polling question 5:How important do you think a strong global business services organization is

to enabling digitalization efforts?

Select one:

Very important

Somewhat important

Not at all important

30© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. NDPPS 653829

Is having a strong GBS organization a digitization enabler?

22% 24%

16%18%

62%59%

2017 2016

Yes

No

It depends

KPMG Global Pulse Insights Survey — 1Q17

Digitization as an enabler of organization agility, collaboration, and partnering

32© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. NDPPS 653829

Digitization as an enabler to organization agility, collaboration & partnering: Highlights

Sixty-four percent of

respondents indicated

that increased digitization

enables greater

organizational

collaboration and agility

The top means through

which digitization enables

greater collaboration and

partnering are reduce time

spend on transactional &

operational tasks to free

up time for collaboration

(67%) and better enable

cross-functional

ownership/accountability

for bus. Initiatives/better

enable planning/ execution

across functions (40%)

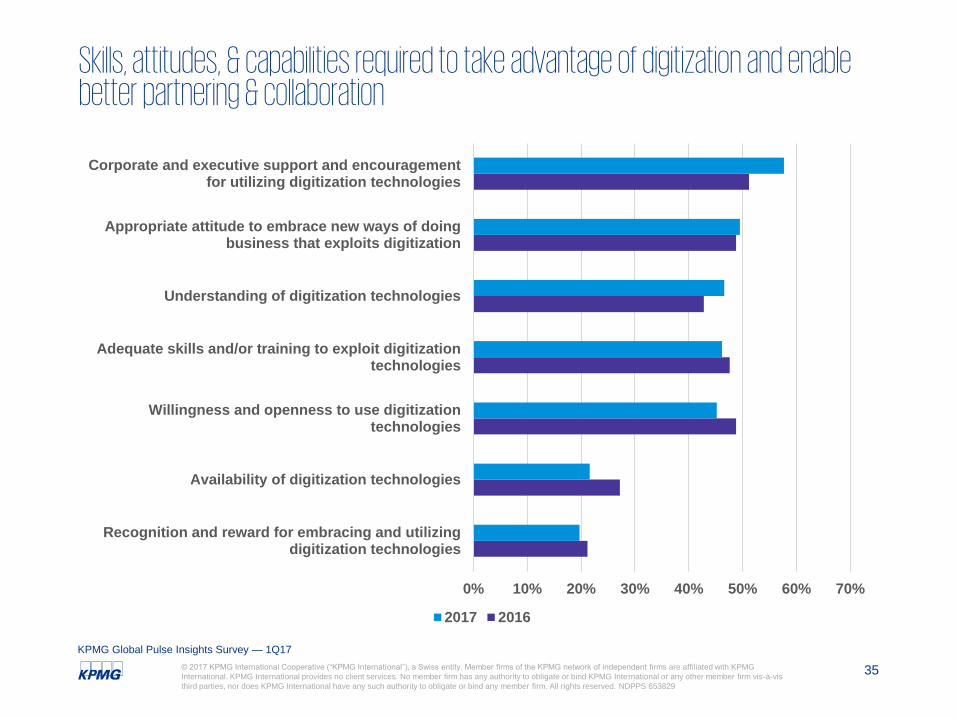

The top skills/attitudes/

capabilities required to

take advantage of

digitization to enable

better partnering and

collaboration are

corporate/executive

support/encouragement

for utilizing digitization

technologies (58%) and a

willingness & openness

to use digitization

technologies (50%)

KPMG Global Pulse Insights Survey — 1Q17

33© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. NDPPS 653829

Does increased digitization enable greater organizational collaboration and agility?

18% 20%

17% 13%

64% 67%

2017 2016

Yes

No

It depends

KPMG Global Pulse Insights Survey — 1Q17

34© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. NDPPS 653829

How does digitization enable greater collaboration & partnering?

0% 10% 20% 30% 40% 50% 60% 70%

Better involve clients and partners to participate in ideageneration, problem solving, etc. (i.e., enable external

crowd sourcing)

Create greater awareness of cross-functional needs andissues

Involve more resources across the organization toparticipate in idea generation, problem solving, etc.

(i.e., enable corporate crowd sourcing)

Improve cross-function communications

Better identify how functions can and shouldcollaborate to address key issues, needs, etc.

Provide greater visibility into redundancy of efforts,investments, etc. across functions

Better enable cross-functional ownership andaccountability for business initiatives and better enable

the ability to plan and execute across functions

Reduce time spend on transactional and operationaltasks to free up time for collaboration

2017 2016

KPMG Global Pulse Insights Survey — 1Q17

35© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. NDPPS 653829

Skills, attitudes, & capabilities required to take advantage of digitization and enable better partnering & collaboration

0% 10% 20% 30% 40% 50% 60% 70%

Recognition and reward for embracing and utilizingdigitization technologies

Availability of digitization technologies

Willingness and openness to use digitizationtechnologies

Adequate skills and/or training to exploit digitizationtechnologies

Understanding of digitization technologies

Appropriate attitude to embrace new ways of doingbusiness that exploits digitization

Corporate and executive support and encouragementfor utilizing digitization technologies

2017 2016

KPMG Global Pulse Insights Survey — 1Q17

36© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. NDPPS 653829

To what extent does the typical organization possess, embody & leverage the required partnering & collaboration skills, attitudes & capabilities?

3% 5%

33%37%

57% 45%

7%13%

0.5% 0%

Overall organizational digitizationskills

Finance function digitization skills

5=To a great extent

3=Somewhat

1=Not at all

KPMG Global Pulse Insights Survey — 1Q17

Learn more

38© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. NDPPS 653829

Learn more — Shared Services & Outsourcing AdvisoryKPMG Shared Services and Outsourcing Institute:

https://institutes.kpmg.us/institutes/shared-services-outsourcing-institute.html

Global Insights Pulse Surveys:

https://institutes.kpmg.us/institutes/shared-services-outsourcing-institute/articles/campaigns/ssoa-pulse-surveys.html

GBS Maturity Research Program:

https://institutes.kpmg.us/institutes/shared-services-outsourcing-institute/articles/campaigns/global-business-services-maturity.html

KPMG Anticipate:

https://home.kpmg.com/xx/en/home/insights/2016/05/kpmg-anticipate.html

KPMG Institutes Home:

http://www.kpmginstitutes.com/

Blog: Reality Check:

https://advisory.kpmg.us/blog.html

Podcasts: Advice Worth Keeping:

https://institutes.kpmg.us/institutes/shared-services-outsourcing-institute/events/podcast-series/advice-worth-keeping-podcast-series.html

39© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. NDPPS 653829

Learn more — EPM and FinanceCFO/Real Insights:https://advisory.kpmg.us/managementconsulting/cfo-real-insights.html

KPMG Advisory Institute:http://www.kpmg-institutes.com/institutes/advisory-institute.html

Recent thought leadership and publications:

KPMG Anticipate:https://home.kpmg.com/xx/en/home/insights/2016/05/kpmg-anticipate.html

"The view from the top" | KPMG and Forbeshttps://home.kpmg.com/xx/en/home/insights/2015/10/view-from-top.html

“Profitability and Cost Analysis: An Eye on Value” | KPMG and ACCAhttps://home.kpmg.com/uk/en/home/insights/2016/04/profitability-and-cost-analysis-an-eye-on-value-kpmg-and-acca-re.html

“CEOs of financial institutions expect more from their finance function” | Frontiers in Financehttps://home.kpmg.com/xx/en/home/insights/2016/03/ceos-of-financial-institutions-fs.html

"Digital Disruption and Transformation" | KPMG and Financier Worldwide / Risk & Compliancehttp://www.kpmg-institutes.com/institutes/advisory-institute/articles/2017/04/digital-disruption-riskandcompliancemagazine.html.

http://www.kpmg-institutes.com/institutes/advisory-institute/articles/2017/04/digital-transformation-riskandcompliancemagazine.html

40© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. NDPPS 653829

Join the KPMG Institutes for the latest on GBS

www.kpmg.com/us/joinssoi

Q & A

Speaker bios

43© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. NDPPS 653829

David J. Brown

David Brown

Global Lead,

Shared Services & Outsourcing

Advisory and

Partner, KPMG LLP (US)

KPMG LLP (US)

Orlando, FL

+1 314 803 5369

Background

Dave is the global lead for KPMG LLP’s (KPMG) Shared Services and Outsourcing Advisory practice. In this role, Dave

provides shared service and outsourcing advice to many of the larger, complex deal structures. Dave has more than two

decades of experience in IT and business process outsourcing; shared services design/build/implement and sourcing

management; contract renegotiations; and finance budgeting, planning and analysis. Dave also delivers hands-on

services as a client executive and has led many multinational deals and provided leadership support on several large

and complex deals for both IT and business processes.

Professional and industry experience

In addition to advising clients, Dave engages senior members of outsourcing service providers’ financial and IT delivery

teams to establish and implement industry-accepted processes and structures related to outsourcing transactions.

Before joining KPMG through the acquisition of EquaTerra — where he held various senior leadership positions

including one through which he established the Financial Architect and Benchmarking practices, and was a client

executive leading large multinational, multifunctional shared service and outsourcing engagements — Dave was a

senior advisor at TPI. In that role, he assisted clients with the evaluation, negotiation, implementation and management

of IT and business process sourcing initiatives.

Earlier in his career, Dave held various financial and IT positions in the telecom industry, at organizations including

Southwestern Bell Information Services, Southwestern Bell Directory Operations, Ameritech Advertising Services and

Bell Canada.

Sample client experience

— Led a large pharmaceutical company through a global IT outsourcing transition involving transitions with total contract value in excess of US$1 billion

— Led a global finance and accounting outsourcing transaction and global shared service design/build and implementation for a global pharmaceutical company

— Provided financial and negotiation support for Unilever’s finance and accounting outsourcing deal (Europe and North America)

— Led an assessment of Oil’s (Brazilian Telecom) IT operations, outsourcing and joint venture options. Led negotiations with third-party provider

— Led a large US Oil and Gas company through a finance and accounting outsourcing transaction, providing overall leadership and financial support

— Led a large transportation company through procure-to-pay sourcing opportunity, providing leadership and financial support

— Assisted several clients with leadership and financial support that were pursuing IT and finance and accounting sourcing opportunities through market assessments of their current finance and accounting environment, or financial support during the transaction or negotiation

44© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. NDPPS 653829

Morris (‘Mo’) TreadwayBackground

With more than 25 years as a business transformation specialist, Mo has helped companies define

and deploy innovative global transformation programs for large clients to improve global integration

and enterprise performance, and realize business outcomes that deliver value. This value is realized

through delivering improved business insight, a forward-looking finance function and ultimately

improving the company’s organizational competency to dynamically manage execution of its

business strategies and enterprise performance.

Mo has worked across a multitude of industries and brings to bear decades of consulting experience

primarily focused on financial management and performance management solutions, business

analytics and business intelligence to design and implement leading solutions, assets and

capabilities that address today’s most complex business challenges and issues.

Areas of expertise

Advisory, Management Consulting, Business Transformation, Financial Management, Enterprise

Performance Management, Business Intelligence, Business Analytics, Global Account Leadership

Morris Treadway

Global Lead,

Financial Management and

Partner, KPMG LLP (US)

KPMG LLP (US)

Houston, Texas

+1 832 880 8006

45© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved. NDPPS 653829

Stan Lepeak Background

Leads market research and thought leadership efforts for KPMG International, focused on trends,

issues and futures in enterprise services transformation and optimization, the threats and

opportunities from market and technology disruptions and industry best practices in responding to

and capitalizing on these market trends

Industry expertise

— The tactical and strategic organizational opportunities, challenges and ramifications from:

— technology disrupters and enablers such as cloud, big data and analytics, mobile, Internet of

Things, social media, consumerization of IT and robotics process automation

— business disrupters such as globalization, increased regulatory and compliance complexity,

talent and skills shortages, shifting global economic and competitive dynamics and

geopolitical risks

— Global business services usage and models including shared services, process outsourcing and

automation, and cloud, and their leading practices and maturity models across major back- (F&A,

HR, IT, procurement, supply chain), middle- and front-office functions

— Use of data and analytics, process automation and related technologies to create and exploit

'intelligent' business functions to enable organizational innovation and transformation

— Vertical industry and geographic trends and variations relative to disruptive market trends and

technologies and their impact on enterprise transformation and innovation efforts

Professional experience

— 25 years' experience in the business and IT services markets. Led global research for leading

boutique sourcing advisory firm EquaTerra (acquired by KPMG in 2011) for seven years.

Previous to that, worked for the META Group (acquired by Gartner in 2004) as VP and Research

Director. He has had executive roles on the vendor and provider side in the software and services

industries as well as positions in finance, accounting and operations across several industries.

— Noted commentator and frequent speaker on global business services and globalization, and

business and IT enablers and disrupters

Stan Lepeak

Director, Global Management

Consulting Research, KPMG

LLP (US)

KPMG LLP (US)

+1 203 444 1268

© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG

network of independent firms are affiliated with KPMG International. KPMG International provides no client

services. No member firm has any authority to obligate or bind KPMG International or any other member firm

vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member

firm. All rights reserved. NDPPS 653829

The information contained herein is of a general nature and is not intended to address the circumstances of any

particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no

guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in

the future. No one should act on such information without appropriate professional advice after a thorough

examination of the particular situation.

The KPMG and logo are registered trademarks or trademarks of KPMG International.

kpmg.com/socialmedia kpmg.com/app

Recommended