Fund Derivatives

David Wakeling

Allen & Overy LLP

5 September 2008

What I will be talking about today

Two presentations for the price of one

Hedge Funds (& Mutual Funds)

Vs

Exchange Traded Funds

Conceptual differences

Liquid

Price transparency

Equity-like characteristics

Secondary market

Uniformity of product (although differences emerging?)

Illiquid

Pricing issues (delays)

Fund Manager NAV

Transferability?

Highly bespoke (reliance key person/ manager etc)

ETFs Mutual Funds Hedge Funds

Different documentation

Hedge Funds (and Mutual Funds): 2006 ISDA Fund Derivatives Definitions

Exchange Traded Funds: The ETF Supplement?

Hedge funds

Characteristics of Hedge Funds

Key characteristics of hedge funds (and mutual funds)

Pricing & Liquidity

Transparency

Fund risk profile & structure A derivative on a hedge fund reflects these

characteristics

Pricing & Liquidity

When Hedge Funds Bar the Door – “If you thought getting into a hedge fund was tough, try getting out of one”

Richie Capital Management

Pardus Capital Management LP

Sandelman Partners Multi-Strategy Fund Ltd.

Drake Capital Management LLC

Russell Investments D.B. Zwirn & Co.

Transparency

Never have so many short sellers made so much money – Harbinger Capital; Paulson & Co.

Bear Sterns; HBOS; Fannie Mae and Freddie Mac

SEC moves to curb short selling FSA ruling lifts lid on hedge funds’ positions Australia takes aim at short selling Bets on HBOS rise in spite of short-sell rule

Fund Structure and Risk Profile

Lahde Capital flew high and called it a day

GLG and Greg Coffey

Peloton flew high, fell fast

As the markets throw knuckle balls, hedge-fund stars still hit home runs Paulson & Co. made money betting on the collapse of

subprime mortgages in 2007

Harbinger Capital reaps subprime profits

Characteristics of Hedge Funds

Key characteristics of hedge funds (and mutual funds)

Pricing & Liquidity

Transparency

Fund risk profile & structure

Characteristics of Hedge Funds

Key characteristics of hedge funds (and mutual funds)

“KYF” (“know your fund”) and the building block approach

Fund derivative reflects these difference- Equity Derivatives Definitions not up to the job…

2006 ISDA Fund Derivatives Definitions

2006 Fund Derivatives Definitions

Structural similarities between the Fund Definitions and the Equity Definitions

Key differences between the Fund Definitions and the Equity Definitions

Reflect key characteristics of hedge funds

2006 Fund Defs- Structural similarities to the Equity Definitions Modelled on the 2002 ISDA Equity Derivatives Definitions

Stand-alone booklet of definitions to be incorporated into short-form Confirmations for individual trades

Options, forwards and swaps covered

Single “Fund Interest” (analogous to Share) and basket trades contemplated

Knock-in and Knock-out trades contemplated

Mechanics of exercise for option transactions

Mechanics of prepayment for forward transactions

2006 Fund Defs- Structural similarities to the Equity Definitions Fund swap mechanics

Valuation provisions

Cash and physical settlement provisions

Dividends

Adjustments and modifications

Extraordinary Events

Miscellaneous representations, agreements and acknowledgement

Key differences between the Fund Definitions and the Equity Definitions Key characteristics of hedge funds (and mutual

funds)

Pricing & Liquidity

Transparency

Fund risk profile & structure A derivative on a hedge fund reflects these

characteristics

1/ PRICING & LIQUIDITY

1/ Differences- pricing & liquidity

KYF- how do you value an interest in the fund?

Many funds, especially hedge funds, set up, administered and valued in “off-shore” jurisdictions

Primarily concerned with funds not traded on a public exchange. No liquid secondary market

Less transparency in terms of regulatory disclosure requirements

Meaning of NAV

Fees, incentive fees, trail fees

Hold back/ claw back

1/ Differences- pricing & liquidity

KYF- how do you buy and sell interests in the fund?

Primarily concerned with funds not traded on a public exchange. No liquid secondary market

Transfer restrictions

Timing of subscription and redemption

Gating

Use of side letters

1/ Differences- pricing & liquidity

Valuation methodologies based on subscriptions and redemptions (not secondary market)

Reported Value Method and Deemed Payout Method

1/ Differences- pricing & liquidity: Deemed Payout Method of Valuation Deemed Payout Method, Observation Dates & subscription/ redemption

cycles measures redemption payments

Redemption Proceeds per Fund Interest Unit “that would be received by the Hypothetical Investor … in connection with a redemption of all Fund Interest Units that are subject to valuation during the period from, and including, the Initial Observation Date to, and including, the Final Observation Date” (Section 1.18 Relevant Price, Section 5.9 Final Price, Section 7.3 Settlement Price)

Redemption Proceeds (Section 1.43) - the redemption proceeds “that would be paid by the related Reference Fund to a Hypothetical Investor who, as of the relevant Redemption Valuation Date, redeems such amount of such Fund Interest”

Provided that proceeds that would or could be paid in property other than cash shall be valued or treated as payable in cash

1/ Differences- pricing & liquidity: Deemed Payout Method of Valuation

“Final Observation Date” (Section 1.50) – with respect to a Valuation Date, specified date, failing which the Valuation Date itself, subject to Sections 6.6 and 6.7 (Disruption), 11.1 (Adjustments) and 11.2 (Correction)

Section 11.2(ii) - where Redemption Proceeds that would have been paid to Hypothetical Investor adjusted to reflect additional payment or claim for repayment (clawback), and adjustment made by end of Cut-off Period starting on Final Observation Date, Calculation Agent to adjust to account for correction

“Cut-off Period” (Section 1.51) - unless specified, one year (or up to earlier specified Final Cut-off Date)

1/ Differences- pricing & liquidity: Deemed Payout Method of Valuation

“Fund Disruption Event” where “Fund Settlement Disruption” on the relevant Valuation Date (Section 6.3)

“Fund Settlement Disruption” where failure by the Reference Fund to pay the full amount of the Redemption Proceeds by the scheduled payment date

Consequence is to postpone the relevant Valuation Date (and therefore the Final Observation Date) to next undisrupted day or last day of Cut-off Period (Section 6.6)

1/ Differences- pricing & liquidity: Reported Value Method of Valuation

Reported Value Method Reported Fund Interest Value … as of the Valuation Date … subject to the

applicable Reported Value Convention” (Section 1.18 Relevant Price, Section 5.9 Final Price, Section 7.3 Settlement Price)

If Confirmation specifies Calculation Agent Adjustment, Calculation Agent to adjust to reflect: fees that would be charged Redemption Proceeds that would have been received by the Hypothetical Investor

If Calculation Agent determines no adjustment will produce a commercially reasonable result, Deemed Payout Method shall apply

Calculation Agent Adjustment makes outcome similar to Deemed Payout Method, but involves more discretion

1/ Differences- pricing & liquidity: Reported Value Method of Valuation

“Reported Value Convention (Section1.42) – the method to be used for determining Reported Fund Interest Value where Valuation Date is not a Scheduled Fund Valuation Date:

“Prior Redemption Valuation Date” – immediately preceding Scheduled Redemption Valuation Date value (this is the fallback if no Convention is specified)

“Following Redemption Valuation Date” – next following Scheduled Redemption Valuation Date value

“Prior Fund Valuation Date” – immediately preceding Scheduled Fund Valuation Date value

“Last Reported Value Date” – most recently available Reported Fund Interest Value

“Following Fund Valuation Date” – next following Scheduled Fund Valuation Date value

1/ Differences- pricing & liquidity: Reported Value Method of Valuation

“Fund Disruption Event” where “Fund Valuation Disruption” on the relevant Valuation Date (Section 6.3)

“Fund Valuation Disruption” occurs where Reported Value Convention is Prior Redemption Valuation Date or

Following Redemption Valuation Date, if Reference Fund fails to determine redemption value on scheduled redemption valuation date

where any other Reported Value Convention applies, if Reference Fund fails to determine the fund value on scheduled fund valuation date

Consequence is to postpone the relevant Valuation Date to next undisrupted day or last day of Cut-off Period (Section 6.6)

2/ TRANSPARENCY

2/ Differences- Transparency

KYF- how do you know what is going on with the fund?

Many funds, especially hedge funds, set up have less transparency in terms of regulatory disclosure requirements

Personalised investment (fees, subscription and redemption date etc)

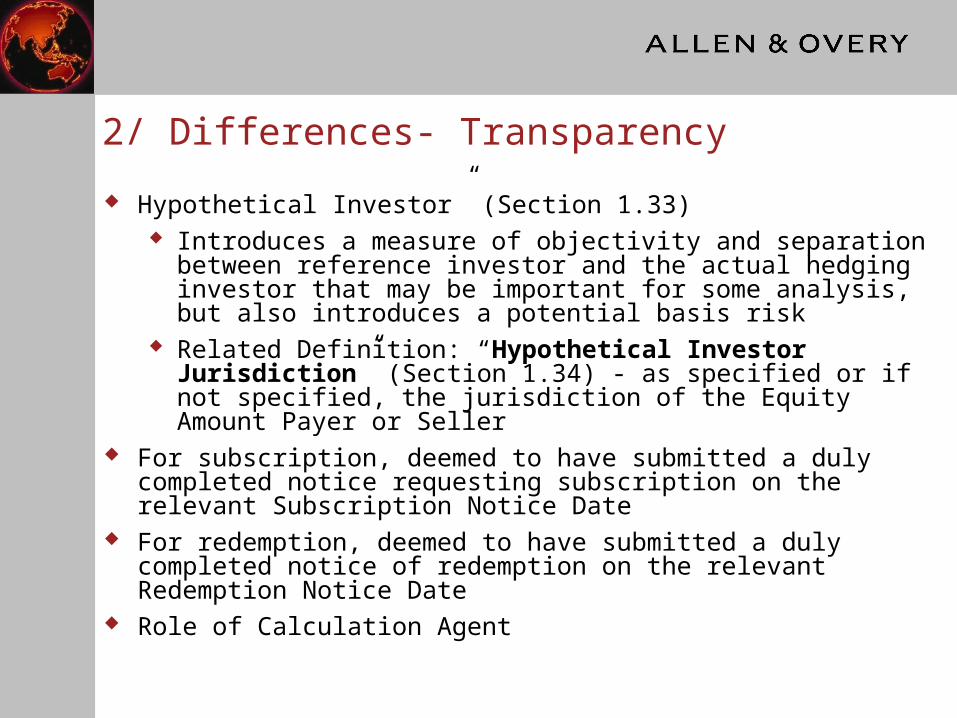

2/ Differences- Transparency

Hypothetical Investor” (Section 1.33) Introduces a measure of objectivity and separation between

reference investor and the actual hedging investor that may be important for some analysis, but also introduces a potential basis risk

Related Definition: “Hypothetical Investor Jurisdiction” (Section 1.34) - as specified or if not specified, the jurisdiction of the Equity Amount Payer or Seller

For subscription, deemed to have submitted a duly completed notice requesting subscription on the relevant Subscription Notice Date

For redemption, deemed to have submitted a duly completed notice of redemption on the relevant Redemption Notice Date

Role of Calculation Agent

3/ RISK PROFILE & Structure

3/ Differences- Risk profile & Structure

KYF- What is the fund about?

Fund focuses on particular investment strategy or strategies in contrast to general business of the issuer of an equity share

Investment restrictions

Service providers

Legal nature and status of fund (often not in corporate form - for example trust, partnership), domicile

3/ Differences- Risk profile & Structure

Extraordinary Fund Events: Fund Modification & Strategy Breach

Extraordinary Fund Events: Adviser Resignation Event

Fund Service Provider concept

3/ Differences- Risk profile & Structure

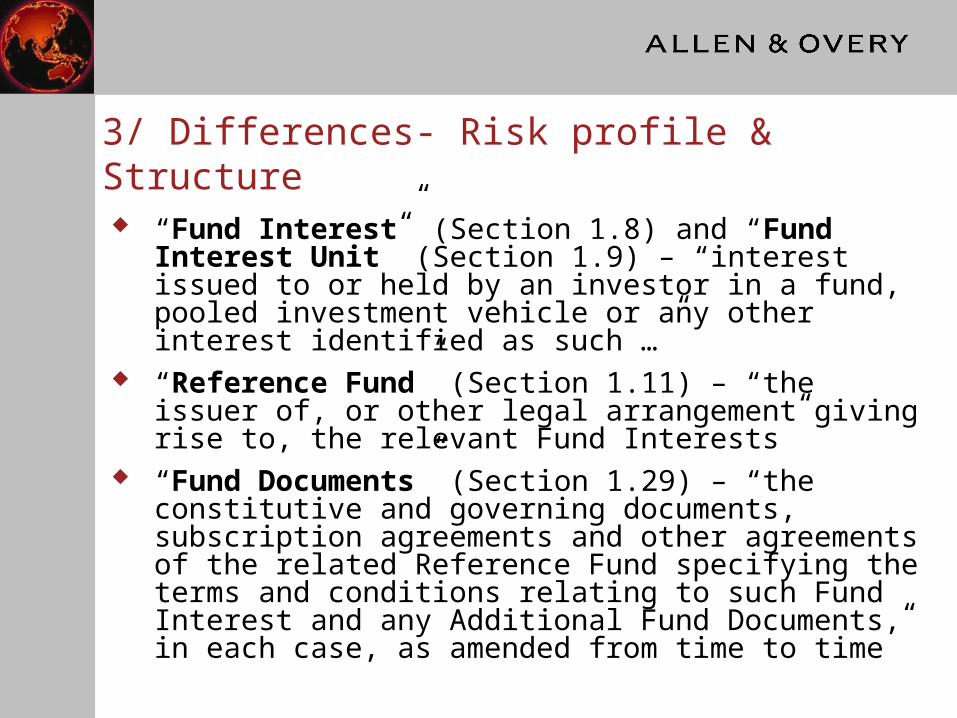

“Fund Interest” (Section 1.8) and “Fund Interest Unit” (Section 1.9) – “interest issued to or held by an investor in a fund, pooled investment vehicle or any other interest identified as such …”

“Reference Fund” (Section 1.11) – “the issuer of, or other legal arrangement giving rise to, the relevant Fund Interests”

“Fund Documents” (Section 1.29) – “the constitutive and governing documents, subscription agreements and other agreements of the related Reference Fund specifying the terms and conditions relating to such Fund Interest and any Additional Fund Documents, in each case, as amended from time to time”

Exchange traded funds

Exchange traded funds

Two presentations for the price of one

Hedge Funds (& Mutual Funds)

Vs

Exchange Traded Funds

Exchange Traded Funds- key characteristics What is an ETF?

Strategy

Exchange traded

Creation Units

Pricing & liquidity, transparency and risk profile

Key players

Developments in the market

ETF Supplement

Ignores Creation Units (probably) Index equity ETFs only Share trade Share and index trade

Valuation disruption (level of index) Index Disruption Events Underlying exchanges

Share and index and fund trade Extraordinary Fund Events

Fund Derivatives

David Wakeling

5th September, 2008

Recommended