For private circulation onlySeptember 2013www.deloitte.com/in

Foreign Universities in India Untapped opportunities for foreign varsities in the Indian higher education sector

2

The Indian Government is in the process of notifying rules which will pave the way for foreign universities to set up a campus in India –world’s third largest higher education system with about 50% population below 25 yearsEntry of Foreign Universities in India A recent press release has indicated that the Government is in the process of notifying rules which will pave the way for entry and operation of foreign universities in India. Under the proposed rules, a foreign university needs to fulfill certain eligibility criterion which includes the following:• Shouldberankedamongstthetop400universitiesoftheworldaspertherankingspublishedbyTimesHigherEducation,QuacquarelliSymonds(QS)ortheAcademicRankingofWorldUniversities(ARWU);

• Shouldformanot-for-profitlegalentityinIndia,registered under section 25 of the Companies Act 1956,forsettingupthecampus;

• Toberegisteredasanot-for-profitlegalentity,in existence for at least twenty years, in the host country;

• Tobeaccreditedbyanaccreditingagencyofthehostcountry. In absence of its accreditation in that country, it should be accredited by an internationally accepted systemofaccreditation;

• Toofferprogrammesofstudyorcoursestobeofquality comparable to those offered to students in its maincampusoverseas;

• Tomaintainacorpusofnotlessthan`250millionbeforebeingnotified;

Theaboveconditionsarecontainedinthepressrelease, the final list of requirements will emerge as and when the proposed rules get notified. Based on our discussions with the Government, we understand that the proposed rules will be notified shortly.

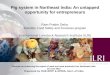

Indian Higher Education - Market AttractivenessAs per estimates, the higher education sector is expectedtowitnessaCAGRof20%inafiveyearperiodstarting2010therebybecominga$57bnmarketby2015.Asignificantportionofthismarketiscontributedby dollar expenditure of Indian students pursuing higher education overseas.

713

41

1314

16

20

27

57

Others

Germany

Australia

UK

USA

Higher Education Market ($ bn)

Foreign

Domestic

2010

Source: Analyst Reports, Deloitte Analysis

2008 2010E 2015E

Break up of countries students ‘Go To’

54%

18%

14%3%

10%

TheIndianhighereducationsectorhasbeentraditionally dominated by Government sponsored universities and colleges. Given the massive demand supply gap, the sector has witnessed a sudden increase of private institutions whose share in higher education enrollmentshastouched59%.

Number of Private Higher Education Institutions

Share of private sector institutions in total higher sector enrolment

Higher Education Enrolments (mn people)

Professional Courses 21%

5% CAGR

General Courses 6%

18,145

2007 2012

20072001 2012

29,662

33%

54% 59%

1/3rd of these institutions were set up in last 5 years

10.9

14.3

2.8

7.1

0

5

10

15

20

25

Professional courses charge up to 10x higher fees vs. general courses; now account for 1/3rd of the enrolments

Source:MHRD,DeloitteAnalysis

Foreign Universities in India 3

Huge untapped opportunity for foreign educatorsIndia has the third largest higher education system in theworldafterChinaandtheUS,withatotalenrolmentofover27.5mnstudents.Inspiteofthis,theGERispresentlylaggingat19.4%(2011)whichisfarlowerthantheworldaverage.Thissignifiesatremendousgrowth potential, especially given the Government’s targetofachievingGERof30%by2020.Giventhelimited financial commitment of the Government and massivedemand-supplygap,theforeigneducationproviders can play a major role in the Indian higher education sector. In addition, only 15 Programmes cover 82%ofthetotalstudentsenrolledinhighereducation,revealing opportunities for provision of niche and specializedofferings.Theproposedruleswillallowtheforeign universities to introduce global best practices in India and offer quality education to millions aspiring to study in a world class university.

Key opportunities for foreign universities in India•Establishing an Indian campus, subject to notification

of rules•Establishing formal educational institutes in

collaboration with Indian private sector•Twinningarrangements/academicandfinancial

collaborations with Indian institutions•SetupanIndiansubsidiaryforcoursecontent

development, executive training and other unregulated offerings

Deloitte Value Proposition and Service Offerings

MarketFeasibilityStudy Post entry advisory

Tax&Regulatoryadvisory

Marketingandmanagement advisory

Implementation assistance

Partnering for Success

Foreign University India Campus

Market Feasibility and Entry Strategy

Tax & Regulatory advisory

Implementation assistance

Marketing and management advisory

Post entry advisory

• “GoNo-Go”Decisionbased on feasibility study

• “GoNo-Go”Decisionbased on feasibility study

• Estimatingmarketsize,faculty availability and competitor profiling

• Assessingdemandofcourses and programs

• LocationAssessment• Developingoptimum

business model• Brandrecognitionand

building• Exploringcollaboration

options with Indian institutions

• Analyzingimpactofmeeting regulatory requirements

• Developingroadmaptoobtain approvals

• Taxefficient®ulatory compliant structuring

• Reviewofbusinessplanfor tax optimisation

• Seekingclarificationfromregulators/revenue authorities

• Adviceandassistancein obtaining regulatory approvals

• Effectivefollow-uptorespond to any queries

• RegistrationofSection25 company

• Taxregistrations/approvals

• Assistanceinnegotiations with StateGovernmentsforincentives

• Dealadvisoryincludingacademic collaborations

• Developingthe“rightvalueproposition”forstudents

• Marketingandpositioning strategy

• HumanCapitalAdvisoryfor hiring faculty and administrative staff

• Taxandregulatorycompliance

• FinancialReporting• Internalcontrol

processes• TechnologyServices

– Datasecurity,miningandMIS

– Content management and archiving system

• ERPservices

Deloitte in India• OneofthelargestprofessionalservicesorganizationsinIndia—over20,000

professionals • Strongnationalpresenceandwidereachwith13regionalcenters• Weserve243andaudit93ofthetopBT500companies• Weofferourservicesto42ofthetop50BTcompanies

Foranyqueries,pleasecontact:

Rohin Kapoor (India)+91(0124)[email protected]

DeloittereferstooneormoreofDeloitteToucheTohmatsuLimited,aUKprivatecompanylimitedbyguarantee,anditsnetworkofmemberfirms,eachofwhichisalegallyseparateandindependententity.Pleaseseewww.deloitte.com/aboutforadetaileddescriptionofthelegalstructureofDeloitteToucheTohmatsuLimitedanditsmember firms.

‘DeloitteinIndia’hereinreferstoDTTLmemberfirmsinIndia

ThismaterialandtheinformationcontainedhereinpreparedbyDeloitteToucheTohmatsuIndiaPrivateLimited(DTTIPL)isintendedtoprovidegeneralinformationonaparticularsubjectorsubjectsandisnotanexhaustivetreatmentofsuchsubject(s).NoneofDTTIPL,DeloitteToucheTohmatsuLimited,itsmemberfirms,ortheirrelatedentities(collectively,the“DeloitteNetwork”)is,bymeansofthismaterial,renderingprofessionaladviceorservices.Theinformationisnotintendedtoberelieduponasthesolebasisforanydecisionwhichmayaffectyouoryourbusiness.Beforemakinganydecisionortakinganyactionthatmightaffectyourpersonalfinancesorbusiness, you should consult a qualified professional adviser.

NoentityintheDeloitteNetworkshallberesponsibleforanylosswhatsoeversustainedbyanypersonwhoreliesonthismaterial.

©2013DeloitteToucheTohmatsuIndiaPrivateLimited.MemberofDeloitteToucheTohmatsuLimited

Recommended